spi insurance company limited

TRANSCRIPT

www.saudipakinsurance.com.pk

Annual Report | for the year ended December 31, 2012

GROWING VALUES

SAUDI PAK INSURANCE COMPANY LIMITED

A commitment to

Growing ValuesSAUDI PAKINSURANCE

SAUDI PAK INSURANCE COMPANY LIMITED

Annual Report | for the year ended December 31, 2012

GROWING VALUES

“Saudi Pak insurance Company Limited” has always lived up to its name by

being one step ahead in the insurance industry, and finding new and affordable

insurance solutions. we have refocused our strategy to better use of expertise in

our business to secure our customers. we are trying to manage our business to

reduce volatility improve returns and accelerate growth through prudent

management and hard working. we will capture a profitable share of the many

opportunities we see around the country -helping customers achieve lifetime

financial security and creating long lasting values for shareholders. This is how

saudi pak is growing value.

Saudi Pak Insurance Company Limited.Major Share Holders of

United International Group

Silk Bank Limited

SAUDI PAK LEASING COMPANY LIMITED

In the Name of ALLAH, The Most Beneficent, The Most Merciful

”

”

Our strategy is based on key principles of execution, financial and underwriting discipline, and above all, focusing on our core business of insurance.

Contents

What is inside?

Overview

Business review& Governance

Financial Highlights

Financial Statements

Vision MissionAbout Us

At Saudi PakAt a GlanceFive Year At a Glance

Company InformationOur Core ManagementServices We OfferBoard of DirectorsSenior ManagementA Message from the ChairmanDirectors’ Report to the Members

Pattern of ShareholdingAuditor’s Report to the MembersBalance SheetProfit and Loss AccountStatement of Comprehensive IncomeStatement of Changes in EquityStatement of Cash FlowsStatement of PremiumsStatement of ClaimsStatement of ExpensesStatement of Investment IncomeNotes to the Financial StatementsOur Network

When we think about our future, the word that comes to mind is promise. Our promise to our people, our customers, our investors, our

communities and our suppliers is thatwe are going to build the best

insurance company in the Pakistan.

We believe we are well on our way.

1

Vision 6

Mission 7

About Us 8

6 Saudi Pak Insurance Company Limited

Our vision is to be the quality insurance service provider, recognized and appraised by performance and product development to cater the changing needs of customers and continuous growth of human resources.

Vision

We wish to become a dynamic insurance service provider, maintaining credibility and reputation while growing revenues over the coming years and improving insurance products by utilizing latest technologies. Saudi Pak Insurance Company Limited focusing to build up a team of professionals by imparting exhaustive training, education and career orientation for the benefit of the insurance industry. We shall endeavor our utmost to render the best possible services to our clients.

Mission

Annual Report | for the year ended December 31, 2012 7

8 Saudi Pak Insurance Company Limited

About Us

Ownership & Paid Up Capital

The company commenced its operations with a paid up capital of Rs. 200 million which has been raised to Rs. 325 million with an authorized capital of Rs. 500 million, thus providing a strong base for operations and substantial capacity for accommodating large industrial risks.

Professional Strength

The company is manned by duly qualified and experienced professionals of all discipline of insurance having substantial knowledge

of underwriting various products and claims management.

Claim Management

Claims are the end product of the insurance. At Saudi Pak Insurance, we believe in the philosophy that every claim is a service to the client and therefore must be handled in the most professional and judicious manner. We therefore give great emphasis to expeditious claim handling including assistance to the client in the risk management, loss mitigation, fast settlements

and early payments. For this purpose the Company’s claim department is led by a veteran who is assisted by a very efficient technical team of professionals. Believing in the quality of service the company employs the leading loss adjusters of the country who have foreign affiliation and years of experience to their credit.

Major Shareholders:

United International GroupSaudi Pak Industrial & Agricultural Investment Company Ltd.Silk Bank Ltd.Saudi Pak Leasing Co. Ltd.

Saudi Pak Insurance Company is a

general Insurance Company providing

insurance coverage to various

renowned companies and financial

institutions of Pakistan. Saudi Pak

Insurance started its operations from

April 14, 2005 and since then it has

managed to emerge as one of the

successful company of the insurance

industry. Fortunately to its credit, it is

jointly supported by the strong Saudi

Pak Group, UIG Group and Silk Bank

Limited.

Annual Report | for the year ended December 31, 2012 9

Branches

With 29 online branches across Pakistan, Saudi Pak Insurance enjoys unique position when it comes to client service. A suitable number of strategically located branches and desirable for an insurance company which plans to expand its operations nationwide in order to provide services to its clients who may situated at remote and far reaching places. With the above credentials we are Confident that our company has desired financial strength

and expertise to provide coverage to Clients various insurance requirements and hope that they will consider us to be the potential insurers of your valuables assets.

Technology is oneof the key

success factors in the business today. It serves as the backbone for all operational functions. The Company intends to establish itself as a technology oriented financial institution. The company has adopted top level

technologies like Oracle and IBM Servers and invested generously towards the infrastructure which is providing online real time branch connectivity which serves as means for data warehousing, catering of basic transaction and meeting the clients’ needs.

Over the course of 2012,we expect to see improvement

in our insurance operations,in terms of policy growth.

2

At Saudi Pak 12

At a Glance 13

Five Year At a Galance 15

12 Saudi Pak Insurance Company Limited

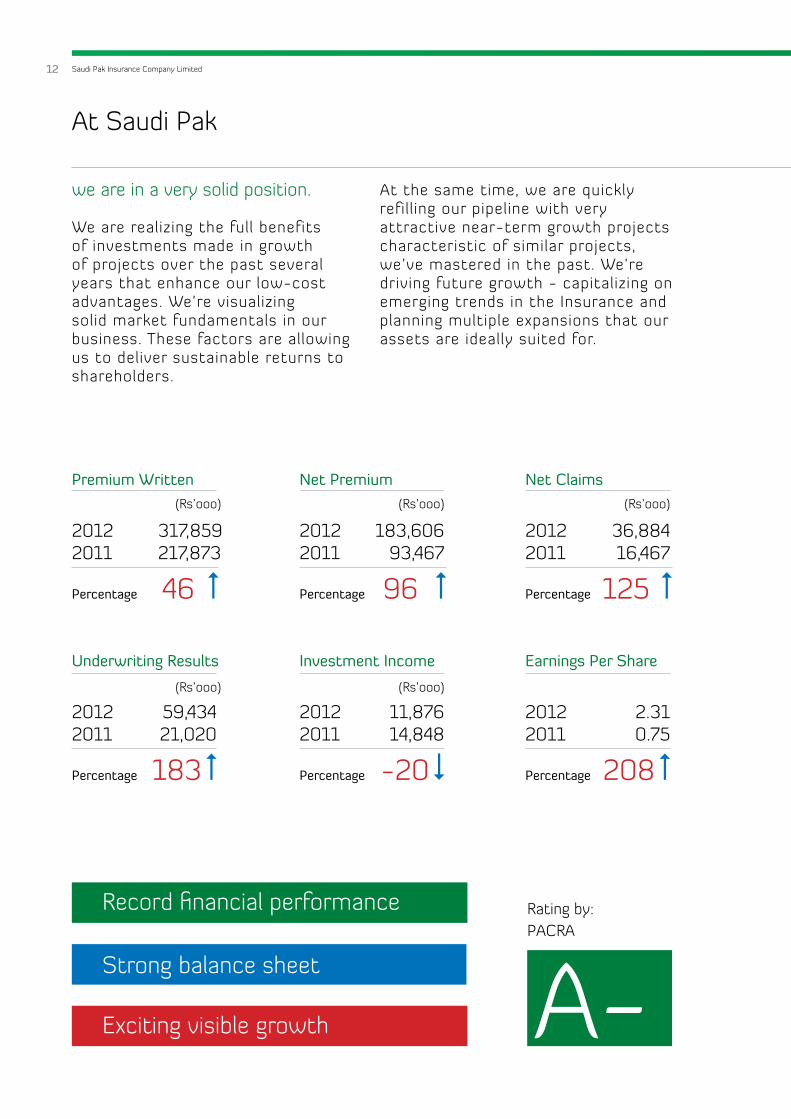

we are in a very solid position.

We are realizing the full benefits of investments made in growth of projects over the past several years that enhance our low-cost advantages. We’re visualizing solid market fundamentals in our business. These factors are allowing us to deliver sustainable returns to shareholders.

At the same time, we are quickly refilling our pipeline with very attractive near-term growth projects characteristic of similar projects, we’ve mastered in the past. We’re driving future growth - capitalizing on emerging trends in the Insurance and planning multiple expansions that our assets are ideally suited for.

Strong balance sheet

Exciting visible growth

Record financial performance Rating by: PACRA

A-

At Saudi Pak

Premium Written(Rs’ooo)

(Rs’ooo)

(Rs’ooo)

(Rs’ooo)

(Rs’ooo)

20122011

317,859217,873

46Percentage

Net Premium

20122011

183,60693,467

96Percentage

Net Claims

20122011

36,88416,467

125Percentage

Underwriting Results

20122011

59,43421,020

183Percentage

Investment Income

20122011

11,87614,848

-20 Percentage

Earnings Per Share

20122011

2.310.75

208 Percentage

Annual Report | for the year ended December 31, 2012 13

At a Glance“Excellence is not an act but a habit”

14 Saudi Pak Insurance Company Limited

Annual Report | for the year ended December 31, 2012 15

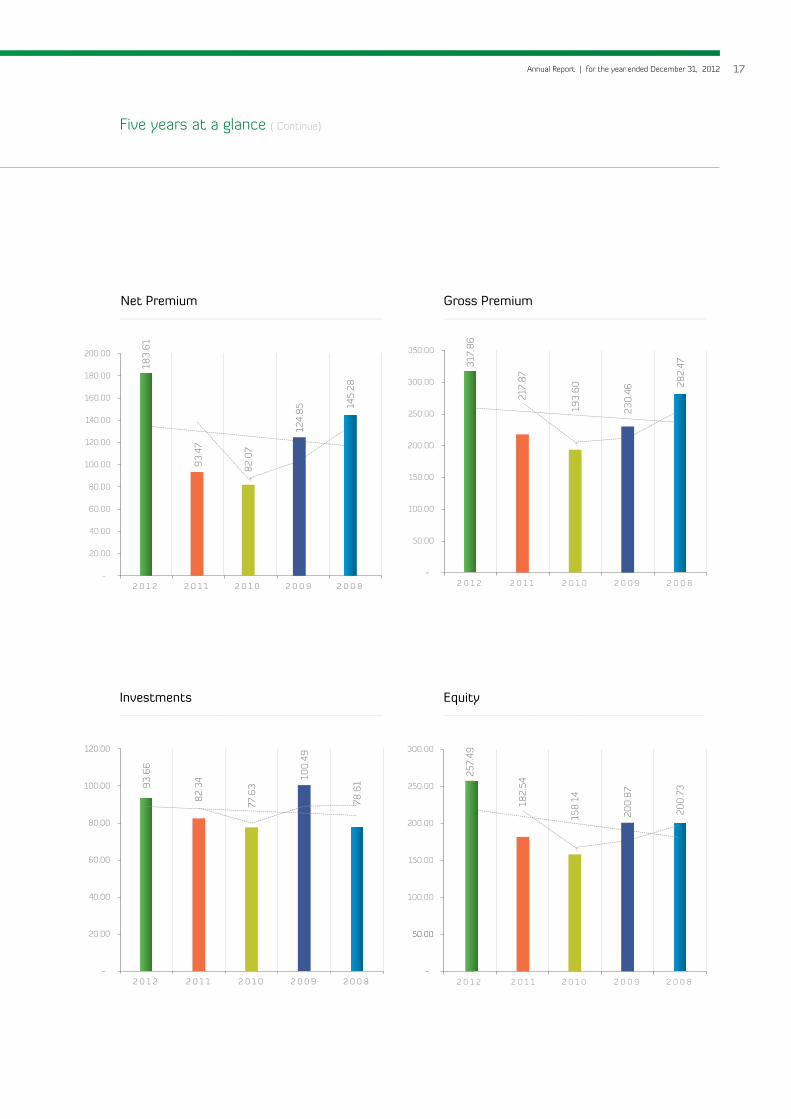

(RUPEES IN MILLIONS)

2012 2011 2010 2009 2008

Financial Data:

Paid up capital 325.00 325.00 325.00 325.00 325.00

Equity 257.49 182.54 158.14 200.87 200.73

Underwriting Provisions 245.78 228.72 228.63 299.82 401.26

Investment at cost 93.66 82.34 77.63 100.49 78.61

Total Assets (book value) 529.82 428.87 401.97 522.70 634.71

Fixed Assets (WDV) 56.61 32.79 25.98 31.28 38.27

Cash and bank deposits 70.41 62.99 50.67 32.39 99.82

Assets - Others 309.15 250.75 247.68 358.54 417.99

OPERATING DATA:

Gross Premium 317.86 217.87 193.60 230.46 282.47

Net Premium 183.61 93.47 82.07 124.85 145.28

Net Claims expenses 36.88 16.43 69.76 69.94 103.30

Management expenses 134.73 66.55 63.89 73.70 99.03

Underwriting Profit / (Loss) 59.43 21.02 (41.54) (8.22) (44.63)

Investment Income / (Loss) 10.21 7.45 3.26 10.79 (12.60)

Profit / (Loss) before Tax 23.86 25.34 (41.54) 1.47 (59.88)

Provision for Tax (51.08) 0.93 1.18 0.62 -

Profit / (Loss) after Tax 74.95 24.40 (42.73) 0.85 (59.88)

FINANCIAL RATIOS:

Profit before tax / Gross Premium (%) 7.5% 11.6% -21.5% 0.6% -21.2%

Profit before tax / Net Premium (%) 13.0% 27.1% -50.6% 1.2% -41.2%

Profit after tax / Gross Premium (%) 23.6% 11.2% -22.1% 0.4% -21.2%

Profit after tax / Net Premium (%) 40.8% 26.1% -52.1% 0.7% -41.2%

Management Expenses to Gross Premium (%) 42.4% 30.5% 33.0% 32.0% 35.1%

Management Expenses to Net Premium (%) 73.4% 71.2% 77.8% 59.0% 68.2%

Underwriting Profit / Net Premium (%) 32.4% 22.5% -50.6% -6.6% -30.7%

Net Claims / Net Premium (%) 20.1% 17.6% 85.0% 56.0% 71.1%

Return on Assets (%) 14.1% 5.7% -10.6% 0.2% -9.4%

LIQUIDITY / LEVERAGE RATIOS:

Current Ratio (Times) 1.20 1.27 1.22 1.21 1.19

Total Assets Turnover (Times) 1.67 1.97 2.08 2.27 2.25

Fixed Assets Turnover (Times) 0.18 0.15 0.13 0.14 0.14

Total Liability / Equity (Times) 1.06 1.35 1.54 1.60 2.16

Return on Capital Employed (%) 9.3% 13.9% -26.3% 0.7% -29.8%

Paid up Capital / Total Assets (%) 61.3% 75.8% 80.9% 62.2% 51.2%

Equity / Total Assets (%) 48.6% 42.6% 39.3% 38.4% 31.6%

RETURN TO MEMBERS:

Return on Equity -PBT (%) 9.3% 13.9% -26.3% 0.7% -29.8%

Return on Equity -PAT (%) 29.1% 13.4% -27.0% 0.4% -29.8%

Earnings per Share (Rs.) 2.31 0.75 (1.31) 0.03 (2.63)

Breakup Value per Share (Rs.) 7.92 5.62 4.87 6.18 6.18

Five years at a glance

16 Saudi Pak Insurance Company Limited

Five years at a glance ( Continue)

(59.43)

21.02 (41.54)

8.22

44.63

Underwriting Profit / (Loss)

2012

201020092008

2011 2012

201020092008

2011

Earnings per Share

44%

Deferred Tax

11% 18%

10%

18%

Investments

Receivables Other Assets

Assets 2012

Fixed Assets

5%

0%

46%

49%

Underwritin g Provisiions Deferred Liabilities

Creditors & Accruals Equity

Liabilities 2012

5%

0%

2.31

0.75

(1.31)

0.03

(2.63)

Annual Report | for the year ended December 31, 2012 17

Five years at a glance ( Continue)

93.4

7

82.0

7

124.

85 145.

28

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

2 0 1 2 2 0 1 1 2 0 1 0 2 0 0 9 2 0 0 8

Net Premium

183.

61

Gross Premium

317.

86

217.

87

193.

60

230.

46 28

2.47

-

50.00

100.00

150.00

200.00

250.00

300.00

350.00

2 0 1 2 2 0 1 1 2 0 1 0 2 0 0 9 2 0 0 8

93.6

6

82.3

4

77.6

3

100.

49

78.6

1

-

20.00

40.00

60.00

80.00

100.00

120.00

2 0 1 2 2 0 1 1 2 0 1 0 2 0 0 9 2 0 0 8

Investments

257.

49

182.

54

158.

14

200.

87

200.

73

-

50.00

100.00

150.00

200.00

250.00

300.00

2 0 1 2 2 0 1 02 0 1 1 2 0 0 9 2 0 0 8

Equity

Given the high cost of customeracquisition in the insurance sector,

insurers need to build customeradvocacy and minimise the value

leakage of existing customers.

3

Board of Directors 20

Company Information 22

Our Core Management 25

Services we offer 28

Senior Management 32

A Massage from the Chairman 34

Directors’ Report to the Members 35

20 Saudi Pak Insurance Company Limited

Mian M. A. ShahidChief Executive Officer

Syed Ammar Ali ZaidiDirector

Mr. Adnan AfridiChairman

Board of Directors

Annual Report | for the year ended December 31, 2012 21

Mr. Muhammad Saeed AkhterDirector

Mr. Abdul Majeed Director

Ms.Perveen Akhtar MalikDirector

Shiekh Aftab AhmedDirector

22 Saudi Pak Insurance Company Limited

Company Information

Audit CommitteeSyed Ammar Ali Zaidi (Chairman)

Mr. Muhammad Saeed Akhter (Member)

Mr. Abdul Majeed (Member)

Chief Internal AuditorMian Mohsin Aslam

AuditorsM/s Avais Hyder Liaquat Nauman

Chartered Accountants

M/s Sarwars

Chartered Accountants

Tax ConsultantM/s Muhammad Bilal & Company

Chartered Accountants

Registered OfficeSuite # 204-A, Second Floor,

Madina City Mall, Abdullah Haroon Road,

Karachi.

Phone # (021) 37010190, 35221805-6

Fax # (021) 37010191

Head Office1st Floor, UIG House,

6 - D, Upper Mall

Lahore.

Phone # (042) 35776561-64

Fax # (042) 35776560

E-mail: [email protected]

Website: www.saudipakinsurance.com.pk

ChairmanMr. Adnan Afridi

Managing Director & Chief ExecutiveMian M. A. Shahid

DirectorsMs. Parveen Akhter Malik

Mr. Muhammad Saeed Akhter

Mr. Abdul Majeed

Syed Ammar Ali Zaidi

Sheikh Aftab Ahmed

Chief Financial OfficerMr. Naeem Tariq

Company SecretaryMr. Noshad Ahmed

Legal AdvisorsM/s Mandviwalla & Zafar

M/s Abdullah Associates

Human Resources CommitteeMs. Parveen Akhter Malik (Chairperson)

Mian M. A. Shahid (Member)

Syed Ammar Ali Zaidi (Member)

Risk Management CommitteeMr. Adnan Afridi (Chairman)

Mian M. A. Shahid (Member)

Ms. Parveen Akhter Malik (Member)

Annual Report | for the year ended December 31, 2012 23

Managing Director & Chief Executive Officer Mian M. A. Shahid

Deputy Managing Director Mr. Shaheryar Akbar Raja

Advisors Maj. Gen (R) Asif Duraiz Akhter

Mr. Naseer Ahmed(Former Member Revenue CBR)

(Former Additional Secretary Military Finance)

(Former Additional Secretary Finance)

Mr. Azizullah Memon(Former President Bolan Bank & UBL)

General Manager Admin Mr. Jamil Ahmed

Chief Manager Underwriting Mr. Imtiaz Ali

Chief Manager Health Mr. Muneer Khan

Manager Claims Motor Mr. Khalid Nazeer bajwa

Manager Claims Non Motor Mr. Naveed ul Haq Nomani

Chief Manager Accounts Mr. Faisal Akbar (FCA)

Manager I.T Mr. Munir Ahmed

Manager Re-Insurance Mr. Asif Azeem

Key Management Personnel

24 Saudi Pak Insurance Company Limited

Company Information

Apna Microfinance Bank

Bank Al-Falah Limited

Bank Al-Falah Islamic

Bank Al-Habib Limited

Habib Bank Limited

HSBC Bank Limited

KASB Bank Limited

National Bank of Pakistan

NIB Bank

SILKBANK Limited

Sindh Bank Limited

Soneri Bank Limited

Standard Chartered Bank Limited

State Bank of Pakistan

Tameer Microfinance Bank

The Bank Of Punjab

United Bank Limited

Allied Bank Limited

Askari Bank Limited

Faysal Bank Limited

Habib Metropolitan Bank Limited

Summit Bank Limited

MCB Bank Limited

SME Bank Limited

Dubai Islamic Bank Limited

Samba Bank Limited

Bankers

Annual Report | for the year ended December 31, 2012 25

We are well positioned to outperform in

an environment which remains challenging.

Our Core Management

26 Saudi Pak Insurance Company Limited

Our Core Management

Annual Report | for the year ended December 31, 2012 27

28 Saudi Pak Insurance Company Limited

Fire

Fire is not friendly with anyone, but our Fire policy is. The basic cover and the most essential for any business concern safeguards insurer’s interest against fire, which can be extended to include additional perils like Riot & Strike Damages, Malicious Damages, Earthquake Fire & Shock, Explosion, Impact Damage, Aircraft Damage, Atmospheric Disturbance and Burglary & House Breaking .

Annual Report | for the year ended December 31, 2012 29

Marine

This type of insurance relates to cargo handling while in transit in different modes of transportation. The Marine Cargo insurance is classified into three classes – Institute Cargo Clause A, B & C, offered to the client depending on their needs.

30 Saudi Pak Insurance Company Limited

Motor

A motor vehicle, being automobile, is exposed to several risks. We at Saudi Pak Insurance, offer comprehensive motor insurance for vehicles of all types i.e. private, commercial and motorcycle.

Annual Report | for the year ended December 31, 2012 31

Miscellaneous

This specialized insurance policy indemnifies an insured for any liability arising due to violation of duties out of negligence by the insured. Architects, Engineers, Consultants, Doctors, Surveyors etc can benefitfrom this cover.

32 Saudi Pak Insurance Company Limited

Mian M. A ShahidChief Executive Officer

Mr. Naseer AhmedAdvisor

Maj. Gen. (R) Asif Duraiz AkhterAdvisor

Mr. Shaheryar Akber RajaDeputy Managing Director

Mr.Azizulllah MemonAdvisor

Senior Management

Annual Report | for the year ended December 31, 2012 33

Mr, Naeem TariqChief Financial Officer

Mr. Khalid Nazeer Bajwa Manager Claims Motor

Mr. Munir AhmedManager I.T

Mr. Asif AzeemManager Re-Insurance

Mr. Muneer KhanChief Manager Health

Mr. Faisal AkbarChief Manager Accounts

Mr. Imtiaz AliChief Manager Underwriting

Mr. Noshad AhmedCompany Secretary

Mian Mohsin AslamChief Internal Auditor

34 Saudi Pak Insurance Company Limited

A Message from the

Chairman

SPICL achieved unprecedented record results for 2012. This performance success is the direct result of the remarkable efforts of our employees and our management to create a more robust, highly dynamic,continuously improving.

“We believe the

challenges we face

as a society present

us with an opportunity

to add value for

everyone, including

our shareholders.”

Despite economic conditions being impacted by deteriorating law and order conditions and political instability in the country, the year end results are reflective of the management’s continuing commitment in meeting the expectations of the shareholders who have invested and have trust in us. This has been made possible through attention to several core issues, including but not limited to, investing in the infrastructure and enhancing the geographical reach of the Company with a clear vision. I am confident that going forward, the Company will reap healthy returns from these investments.

During the year 2012, the Company continued to improve its performance and achieved outstanding results. Despite the challenges of the future in the form of increasing competition, difficult socio economic and political situation of the country, we remain committed to our vision, mission & core values. The Company is

geared up to meet the challenges of tomorrow and will continue to capitalize on new investments made in infrastructure, human resources and geographical outreach opportunities.

I would like to extend my appreciation to the management for their commitment, dedication and hard work in achieving these excellent results. I would also like to express my sincere appreciation to the Board members whose valuable guidance has always enlightened us in our decision making. Finally I express my gratitude to our stakeholders, regulators and our valued customers for their support and continued confidence in SPICL.

Adnan AfridiChairman

Karachi: March 28, 2013

Annual Report | for the year ended December 31, 2012 35

Directors‘ Report to the members

The Board of Directors is pleased to present the annual report of the Company together with the audited financial statements for the year ended December 31, 2012.

Economic Review

Pakistan’s economy witnessed a modest improvement in FY12 – real GDP grew by 3.7 percent during the year, compared with 3.0 percent in FY11. Although the economy underperformed compared with the growth target of 4.2 percent, this outcome was expected given the energy shortages; security concerns; and floods in two consecutive years. Nevertheless, growth was more broad-based compared to FY11, as it was evenly distributed across agriculture, industry and the services sector.

On the external front, remittances posted yet another year of strong growth, which not only helped narrow the current account deficit, but also contributed to economic activity. In overall terms, the external sector has been less worrying than anticipated at the beginning of the year; however, as financial inflows dried up, the burden of financing the current account deficit and external debt, has fallen on the country’s FX reserves.

The macro economic landscape was dominated by discount rate cuts by SBP from 12 percent to 9.5 percent on the back of easing inflation. However, the Rupee remained under pressure throughout the year due to external debt obligations.

Performance Analysis 2012

In 2012, despite a challenging economic environment, the total assets of the Company have recorded a growth of 23.5 percent to Rs. 529 million. The Company has shown an immense improvement across all segments of operations and business. Also, the Company has underwritten premium of Rs. 317.86 million (2011: Rs. 217.87 millions) posting an increase of Rs.100 million (46 percent) over the last year, with an increase of Rs. 90.14 million (96 percent) in the net premium income during the year.

The Company has invested into the infrastructure to increase our geographical reach forming a foundation for the future growth of our organization consequently resulting in an increase in expenses from Rs. 64 million to Rs. 115 million respectively. The Management is confident that this investment will provide a strong base to further increase revenues in the years to come.

Dear Shareholders,

December 31,2012

December 31,2011

Inc / (Dec)in %

(Rupees in thousands)

The Financial highlights are given hereunder:

Premium Written 317,859 217,873 46

Net Premium 183,606 93,467 96

Net Claims 36,884 16,427 125

Management & other expenses 115,266 64,690 78

Underwriting results 59,434 21,020 183

Investment and other Income 11,876 14,848 -20

Profit for the year before Tax 23,859 25,337 -6

Profit for the year after Tax 74,944 24,402 207

E.P.S. 2.31 0.75 208

Credit Rating

The Company is rated “A-“ by PACRA.

36 Saudi Pak Insurance Company Limited

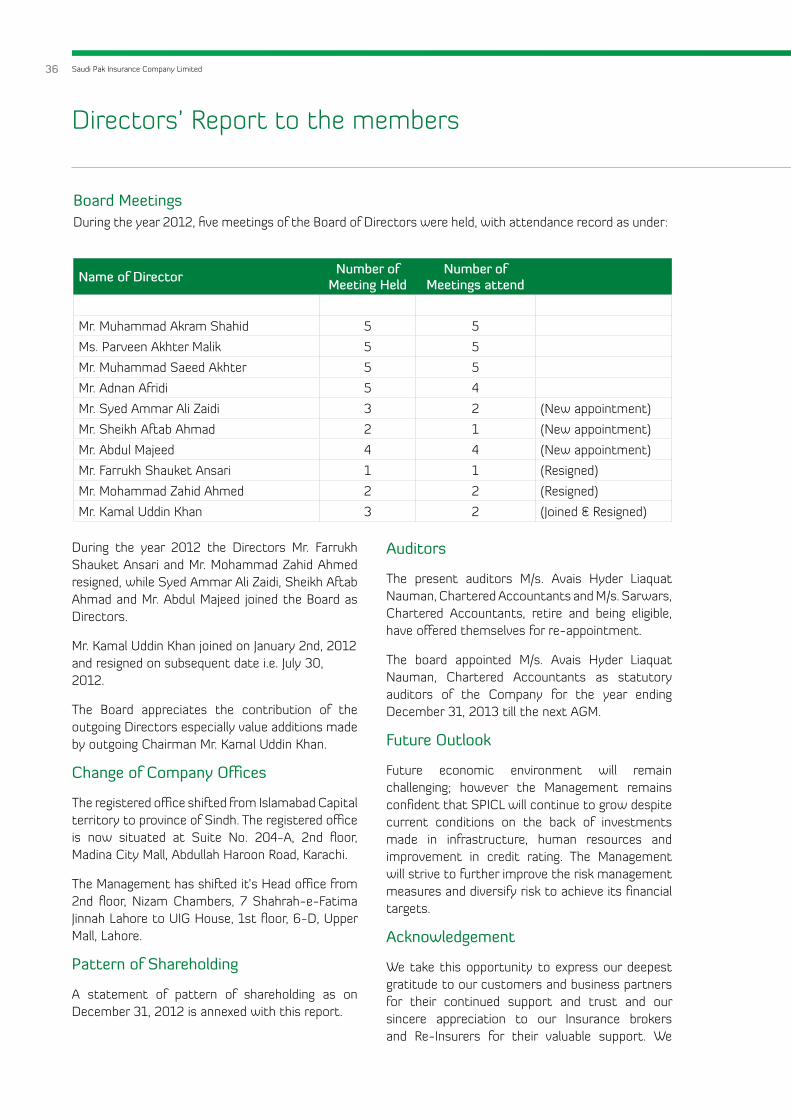

During the year 2012 the Directors Mr. Farrukh Shauket Ansari and Mr. Mohammad Zahid Ahmed resigned, while Syed Ammar Ali Zaidi, Sheikh Aftab Ahmad and Mr. Abdul Majeed joined the Board as Directors.

Mr. Kamal Uddin Khan joined on January 2nd, 2012 and resigned on subsequent date i.e. July 30, 2012.

The Board appreciates the contribution of the outgoing Directors especially value additions made by outgoing Chairman Mr. Kamal Uddin Khan.

Change of Company Offices

The registered office shifted from Islamabad Capital territory to province of Sindh. The registered office is now situated at Suite No. 204-A, 2nd floor, Madina City Mall, Abdullah Haroon Road, Karachi.

The Management has shifted it’s Head office from 2nd floor, Nizam Chambers, 7 Shahrah-e-Fatima Jinnah Lahore to UIG House, 1st floor, 6-D, Upper Mall, Lahore.

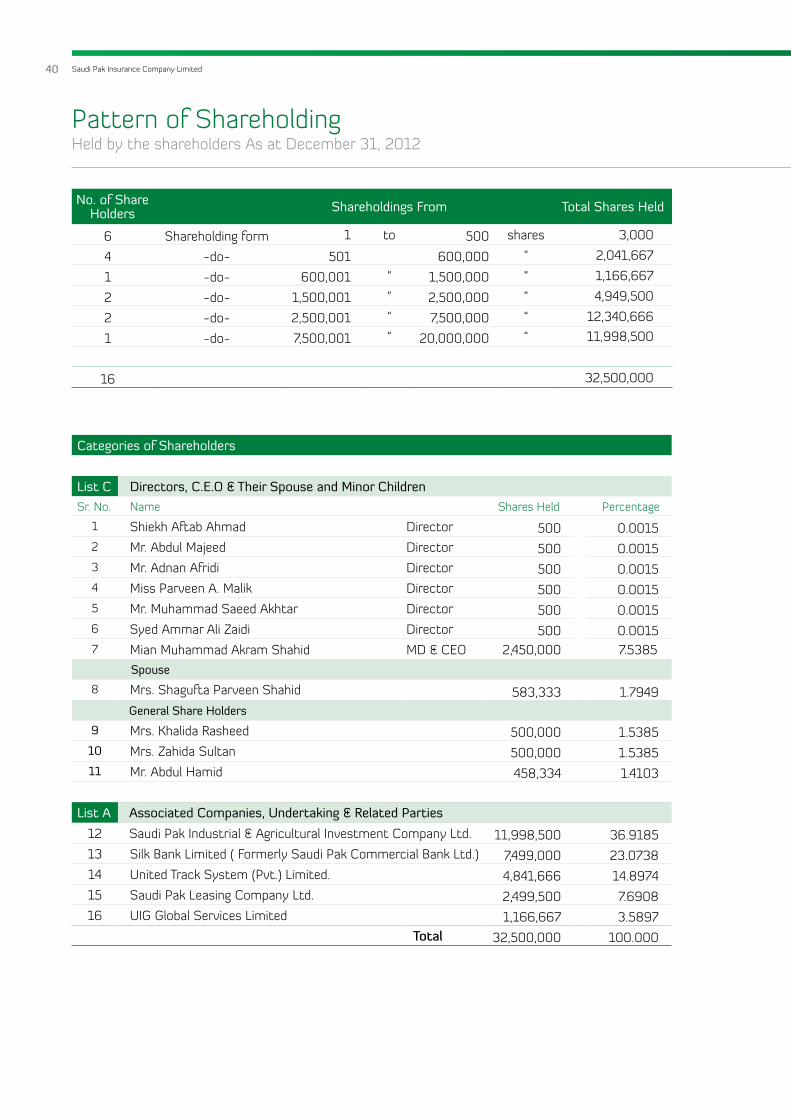

Pattern of Shareholding

A statement of pattern of shareholding as on December 31, 2012 is annexed with this report.

Auditors

The present auditors M/s. Avais Hyder Liaquat Nauman, Chartered Accountants and M/s. Sarwars, Chartered Accountants, retire and being eligible, have offered themselves for re-appointment.

The board appointed M/s. Avais Hyder Liaquat Nauman, Chartered Accountants as statutory auditors of the Company for the year ending December 31, 2013 till the next AGM.

Future Outlook

Future economic environment will remain challenging; however the Management remains confident that SPICL will continue to grow despite current conditions on the back of investments made in infrastructure, human resources and improvement in credit rating. The Management will strive to further improve the risk management measures and diversify risk to achieve its financial targets.

Acknowledgement

We take this opportunity to express our deepest gratitude to our customers and business partners for their continued support and trust and our sincere appreciation to our Insurance brokers and Re-Insurers for their valuable support. We

Board MeetingsDuring the year 2012, five meetings of the Board of Directors were held, with attendance record as under:

Name of Director Number ofMeeting Held

Number ofMeetings attend

Mr. Muhammad Akram Shahid 5 5

Ms. Parveen Akhter Malik 5 5

Mr. Muhammad Saeed Akhter 5 5

Mr. Adnan Afridi 5 4

Mr. Syed Ammar Ali Zaidi 3 2 (New appointment)

Mr. Sheikh Aftab Ahmad 2 1 (New appointment)

Mr. Abdul Majeed 4 4 (New appointment)

Mr. Farrukh Shauket Ansari 1 1 (Resigned)

Mr. Mohammad Zahid Ahmed 2 2 (Resigned)

Mr. Kamal Uddin Khan 3 2 (Joined & Resigned)

Directors’ Report to the members

Annual Report | for the year ended December 31, 2012 37

Directors’ Report to the members

would like to extend our appreciation to Securities Exchange Commission of Pakistan and State Bank of Pakistan for their guidance. We are also thankful to our clients for their patronage and Shareholders for their continue support. We are also equally thankful to our associates, staff and colleagues for their committed services to SPICL and look forward to their continued support.

For and on behalf of the Board of Directors

(Mian M. A. Shahid)Chief Executive Officer / Director

Karachi: March 28, 2013

In order to deliver and grow, your

Company depends greatly on

management at every level.

In 2012 we delivered a good result for our shareholders by executing on ourunderwriting strategies, improving

our customer orientation and protecting our strong capital position.

4

Pattern of Shareholding 40

Auditor’s Report to the Members 42

Balance Sheet 44

Profit and Loss Account 46

Statement of Comprehensive Income 47

Statement of Changes in Equity 48

Statement of Cash Flows 49

Statement of Premiums 51

Statement of Claims 52

Statement of Expenses 53

Statement of Investment Income 54

Notes to the Financial Statements 55

Our Network 93

40 Saudi Pak Insurance Company Limited

Categories of Shareholders

List C Directors, C.E.O & Their Spouse and Minor ChildrenSr. No. Name Shares Held Percentage

1 Shiekh Aftab Ahmad Director 500 0.0015 2 Mr. Abdul Majeed Director 500 0.0015 3 Mr. Adnan Afridi Director 500 0.0015 4 Miss Parveen A. Malik Director 500 0.0015 5 Mr. Muhammad Saeed Akhtar Director 500 0.0015 6 Syed Ammar Ali Zaidi Director 500 0.0015 7 Mian Muhammad Akram Shahid MD & CEO 2,450,000 7.5385

Spouse

8 Mrs. Shagufta Parveen Shahid 583,333 1.7949 General Share Holders

9 Mrs. Khalida Rasheed 500,000 1.5385 10 Mrs. Zahida Sultan 500,000 1.5385 11 Mr. Abdul Hamid 458,334 1.4103

List A Associated Companies, Undertaking & Related Parties

12 Saudi Pak Industrial & Agricultural Investment Company Ltd. 11,998,500 36.9185 13 Silk Bank Limited ( Formerly Saudi Pak Commercial Bank Ltd.) 7,499,000 23.0738 14 United Track System (Pvt.) Limited. 4,841,666 14.8974 15 Saudi Pak Leasing Company Ltd. 2,499,500 7.6908 16 UIG Global Services Limited 1,166,667 3.5897

Total 32,500,000 100.000

No. of Share Holders Shareholdings From Total Shares Held

6 Shareholding form 1 to 500 shares 3,000

4 -do- 501 600,000 “ 2,041,667

1 -do- 600,001 “ 1,500,000 “ 1,166,667

2 -do- 1,500,001 “ 2,500,000 “ 4,949,500

2 -do- 2,500,001 “ 7,500,000 “ 12,340,666

1 -do- 7,500,001 “ 20,000,000 “ 11,998,500

16 32,500,000

Pattern of ShareholdingHeld by the shareholders As at December 31, 2012

Financial StatementFor the year ended December 31, 2012

42 Saudi Pak Insurance Company Limited

Avais Hyder Liaquat Nauman Sarwars(Chartered Accountants) (Chartered Accountants)

Avais Chambers, Office # 12, II-Floor Lahore Centre, 1/C-5, Sikander Malhi Road 77-D Main Boulevard, Gulberg-III,Canal Park, Gulberg II, Lahore – Pakistan.Lahore - Pakistan Telephone: (92-42) 35782920-22Telephone: (92-42) 35872731/2/3 Telefax: (92-42) 35773825Telefax: (92-42) 35872734 E-mail: [email protected] E-mail: [email protected]

We have audited the annexed financial statements comprising of:

(i) Balance Sheet;(ii) Profit and Loss Account;(iii) Statement of Comprehensive Income;(iv) Statement of Changes in Equity;(v) Statement of Cash Flows;(vi) Statement of Premiums;(vii) Statement of Claims;(viii) Statement of Expenses; and(ix) Statement of Investment Income

of Saudi Pak Insurance Company Limited (“the Company”) as at 31 December, 2012 together with the notes forming part thereof, for the year then ended.

It is the responsibility of the Company’s Board of Directors to establish and maintain a system of internal control, and prepare and present the financial statements in conformity with the approved Accounting Standards as applicable in Pakistan and the requirements of the Insurance Ordinance, 2000 (XXXIX of 2000) and the Companies Ordinance, 1984 (XLVII of 1984). Our responsibility is to express an opinion on these statements based on our audit.

We conducted our audit in accordance with the Auditing Standards as applicable in Pakistan. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting policies used and significant estimates made by management, as well as, evaluating the overall financial statements presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion:

(a) proper books of accounts have been kept by the Company as required by the Insurance Ordinance, 2000 and Companies Ordinance, 1984;

(b) the financial statements together with the notes thereon have been drawn up in conformity with the Insurance Ordinance, 2000 and the Companies Ordinance, 1984, and accurately reflect the books and records of the Company and are further in accordance with accounting policies consistently applied;

Auditors’ Report to the members

Annual Report | for the year ended December 31, 2012 43

(c) the financial statements together with the notes thereon present fairly, in all material respects, the state of the Company’s affairs as at 31 December 2012 and of the profits, its comprehensive income, its cashflows and changes in equity for the year then ended in accordance with approved accounting standards as applicable in Pakistan, and give the information required to be disclosed by the Insurance Ordinance, 2000 and the Companies Ordinance, 1984; and

(d) no Zakat was deductible at source under the Zakat and Usher Ordinance, 1980.

___________________________________ _______________________

AVAIS HYDER LIAQUAT NAUMAN SARWARS

Chartered Accountants Chartered Accountants

Audit Engagement Partner: Syed Ali Adnan Tirmizey Rashid Sarwar

Date: March 29, 2013

Place: Lahore

44 Saudi Pak Insurance Company Limited

Note2012 2011

Rupees Rupees

Share Capital And Reserves

Authorized Share Capital

50,000,000 (2011 : 50,000,000)

ordinary shares of Rs.10 each 500,000,000 500,000,000

Issued, subscribed and paid up share capital 5 325,000,000 325,000,000

Accumulated (loss) (67,510,963) (142,455,661)

257,489,037 182,544,339

Underwriting Provisions

Provision for outstanding claims (including IBNR) 80,911,792 112,663,524

Provision for unearned premium 145,874,535 105,136,280

Additional provision for unexpired risks 6,741,166 2,000,656

Commission income unearned 12,250,183 8,920,405

245,777,676 228,720,865

Deferred Liabilities

Staff retirement gratuity 6 2,294,644 944,644

Creditors And Accruals

Premium received in advance 1,660,784 -

Amount due to other insurers/re-insurers 7,576,658 3,555,785

Accrued expenses 7 6,790,489 4,346,136

Other creditors and accruals 8 8,235,495 8,761,420

24,263,426 16,663,341

Total Liabilities 272,335,746 246,328,850

Total Equity And Liabilities 529,824,783 428,873,189

Contingencies And Commitments 9 - -

Balance SheetAs at December 31, 2012

Mian M.A. Shahid Adnan Afridi Chief Executive Officer Chairman

Annual Report | for the year ended December 31, 2012 45

Balance SheetAs at December 31, 2012

Note2012 2011

Rupees Rupees

Cash And Bank Deposits 10

Cash and other equivalents 918,117 377,987

Current and other accounts 28,434,551 16,977,051

Deposits maturing within 12 months 40,966,000 45,431,000

Cash with State Bank of Pakistan 89,639 200,000

70,408,307 62,986,038

Loans To Employees 11 501,116 347,149

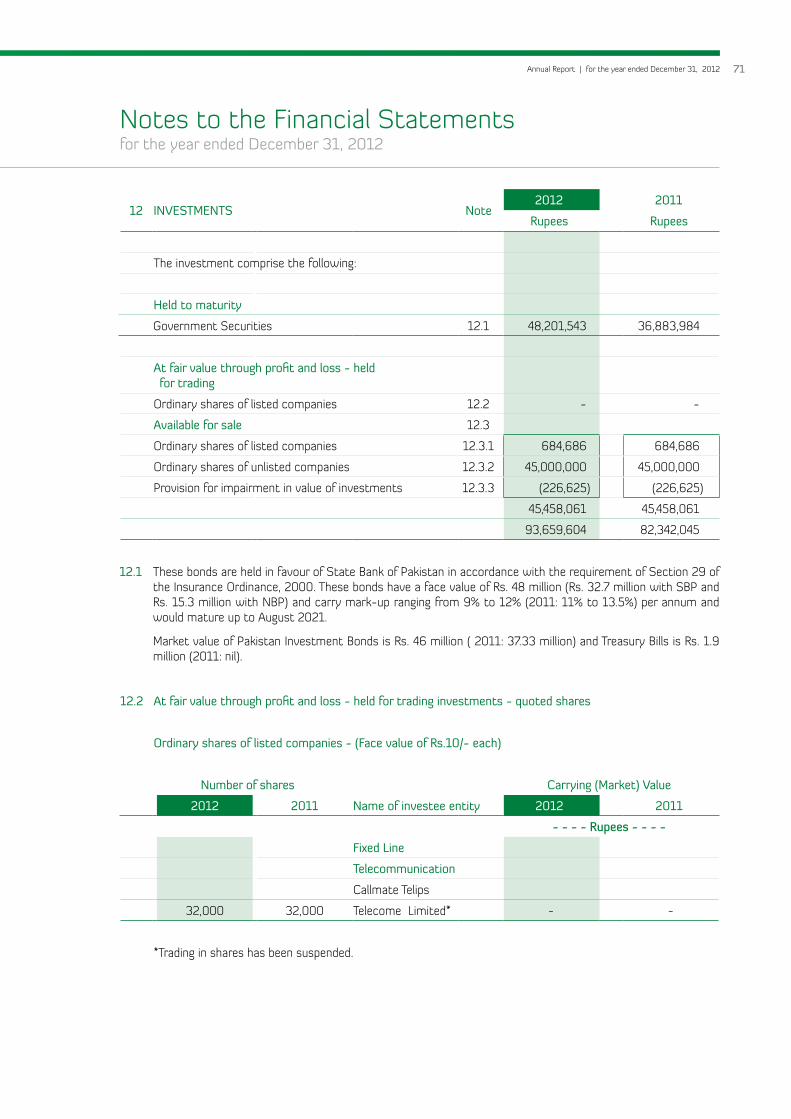

Investments 12 93,659,604 82,342,045

Deferred Tax Asset 13 52,003,623 -

Current Assets - Others

Premium due but unpaid 14 48,702,076 61,160,304

Amount due from other insurers/re-insurers 15 45,544,938 41,811,499

Prepaid reinsurance premium ceded 49,466,557 38,815,241

Accrued investment income 16 3,758,916 3,359,440

Reinsurance recoveries against outstanding claims 17 71,288,878 80,478,357

Taxation - payment less provision 4,541,771 3,874,189

Deferred commission expense 20,759,255 13,022,299

Prepayments 18 5,801,962 3,268,005

Sundry receivables 19 6,777,826 4,614,720

256,642,179 250,404,054

Fixed Assets 20

Tangible

Office improvements 10,330,878 8,368,591

Furniture and fixture 2,892,391 2,114,786

Office equipment 4,645,249 3,894,015

Computer equipment 2,124,800 2,066,562

Motor vehicles 36,361,369 16,030,865

56,354,687 32,474,819

Intangible

Computer software 255,267 319,084

TOTAL ASSETS 529,824,783 428,873,189

The annexed notes 1 to 32 form an integral part of these financial statements.

Sheikh Aftab Ahmed Syed Ammar ALi Zaidi Director Director

46 Saudi Pak Insurance Company Limited

Note

2012 2011

Fire and Property Damage

Marine Aviation And

TransportMotor Miscellneous Aggregate Aggregate

- - - - - - - - - - - - - - - - - R u p e e s - - - - - - - - - - - - - - - -

Revenue AccountNet premium revenue 34,047,317 16,094,142 82,970,819 50,494,457 183,606,735 93,467,937

Net claims (5,154,961) (2,272,662) (32,924,651) 3,468,563 (36,883,711) (16,426,926)

Premium deficiency reserve (6,741,166) - 1,025,018 975,638 (4,740,510) -

Management expenses 21 (30,199,156) (6,412,718) (23,306,687) (7,895,701) (67,814,262) (54,160,156)

Net commission (1,150,449) (1,878,567) (7,047,551) (4,657,071) (14,733,638) (1,860,655)

Underwriting Results (9,198,415) 5,530,195 20,716,948 42,385,886 59,434,614 21,020,200

Investment income 10,211,896 7,452,909

Other income 22 1,664,495 7,394,908

General and administration expenses 21 (47,451,896) (10,530,488)

Profit before tax 23,859,109 25,337,529

Less: Taxation

Current 23 (918,034) (934,679)

Deferred 13 52,003,623 -

51,085,589 (934,679)

Profit after tax 74,944,698 24,402,850

Profit And (Loss) Appropriation Account

Balance at commencement of year (142,455,661) (166,858,511)

Comprehensive income 74,944,698 24,402,850

Balance of accumulated (loss) at end of the year (67,510,963) (142,455,661)

Earnings Per Share

- basic and diluted 24 2.31 0.75

The annexed notes 1 to 32 form an integral part of these financial statements.

Profit and Loss Accountfor the year ended December 31, 2012

Mian M.A. Shahid Adnan Afridi Sheikh Aftab Ahmed Syed Ammer Ali Zaidi Chief Executive Officer Chairman Director Director

Annual Report | for the year ended December 31, 2012 47

Note2012 2011

Rupees Rupees

Profit / (loss) after tax 74,944,698 24,402,850

Other comprehensive income - -

74,944,698 24,402,850

The annexed notes 1 to 32 form an integral part of these financial statements.

Statement of Comprehensive Incomefor the year ended December 31, 2012

Mian M.A. Shahid Adnan Afridi Sheikh Aftab Ahmed Syed Ammer Ali Zaidi Chief Executive Officer Chairman Director Director

48 Saudi Pak Insurance Company Limited

Share capitalAccumulated (loss)/ profit

Total

- - - - - - - - - R u p e e s - -- - - -- - - -

Balance as at January 01, 2011 325,000,000 (166,858,511) 158,141,489

Comprehensive income/(loss) for the year - 24,402,850 24,402,850

Balance as at December 31, 2011 325,000,000 (142,455,661) 182,544,339

Balance as at January 01, 2012 325,000,000 (142,455,661) 182,544,339

Comprehensive income/(loss) for the year - 74,944,698 74,944,698

Balance as at December 31, 2012 325,000,000 (67,510,963) 257,489,037

The annexed notes 1 to 32 form an integral part of these financial statements.

Statement of Changes In Equityfor the year ended December 31, 2012

Mian M.A. Shahid Adnan Afridi Sheikh Aftab Ahmed Syed Ammer Ali Zaidi Chief Executive Officer Chairman Director Director

Annual Report | for the year ended December 31, 2012 49

Note2012 2011

Rupees Rupees

Operating Cash Flows

a) Underwriting activities

Premium received 331,978,178 188,933,588

Reinsurance premium paid (100,144,619) (87,552,285)

Claims paid (134,925,215) (74,138,498)

Reinsurance and other recoveries received 71,745,812 56,614,123

Commission paid (45,396,608) (27,867,185)

Commission received 26,255,792 20,437,270

Other underwriting payments (56,363,501) (42,894,728)

Net cash flow from underwriting activities 93,149,839 33,532,285

b) Other operating activities

Income tax paid (1,585,617) (789,365)

General and administrative expenses paid (47,451,896) (10,530,488)

Other operating payments (4,697,063) (2,443,229)

Other operating receipts 1,918,428 1,926,711

Loan (disbursed)/ refunded (153,967) 525,328

Net cash flow from other operating activities (51,970,115) (11,311,043)

Total cash flow from operating activities 41,179,724 22,221,242

Investment Activities

Profit/ return received 9,773,120 5,071,701

Dividend received 39,300 36,000

Payments for investments (11,317,559) (4,908,801)

Proceeds from disposal of investments - 200,000

Fixed capital expenditure (32,252,316) (12,544,118)

Proceeds from disposal of fixed assets - 2,234,017

Total cash flow from investing activities (33,757,455) (9,911,201)

Financing Activities

Total cash inflow from financing activities - -

Net cash inflow/(outflow) from all activities 7,422,269 12,310,041

Cash at the beginning of the year 62,986,038 50,675,997

Cash at the end of the year 70,408,307 62,986,038

The annexed notes 1 to 32 form an integral part of these financial statements.

Statement of Cash Flowsfor the year ended December 31, 2012

50 Saudi Pak Insurance Company Limited

Note2012 2011

Rupees Rupees

Reconciliation to Profit and Loss Account

Operating cash flows 41,179,724 22,221,242

Depreciation/ amortization expenses (8,436,265) (4,122,555)

(Loss)/ gain on disposal of fixed assets - 631,302

Provision for doubtful debts (6,256,996) (338,696)

Premium deficiency reserve (4,740,510) -

(Decrease) / Increase in assets other than cash 13,167,646 1,996,190

(Increase)/ Decrease in liabilities (21,266,386) (2,502,863)

Other income 10,172,596 7,416,909

Dividend income 39,300 36,000

Reversal/ (Provision) for taxation 51,085,589 (934,679)

Profit after taxation 74,944,698 24,402,850

Definition of cash

Cash comprises of cash in hand, policy stamps and bank balances which are readily convertible to cash in hand and which are used in the cash management function on a day-to-day basis.

Cash for the purpose of statement of cash flows consists of:

Cash and cash equivalents 10

Cash and other equivalents

Cash and other equivalents 918,117 377,987

918,117 377,987

Current and other accounts

Current accounts 26,104,724 13,423,411

PLS savings accounts 2,329,827 3,553,640

28,434,551 16,977,051

Deposits maturing within 12 months 40,966,000 45,431,000

Cash with State Bank of Pakistan 89,639 200,000

70,408,307 62,986,038

The annexed notes I to 32 from an integral part of these financial statements.

Statement of Cash Flowsfor the year ended December 31, 2012

Mian M.A. Shahid Adnan Afridi Sheikh Aftab Ahmed Syed Ammer Ali Zaidi Chief Executive Officer Chairman Director Director

Annual Report | for the year ended December 31, 2012 51

Busi

ness

Und

erw

ritte

n In

side

Pak

ista

n

Cla

ssPr

emiu

m

Writ

ten

Une

arne

d pr

emiu

mRe

serv

ePr

emiu

m

Earn

ed

Rein

sura

nce

Prem

ium

C

eded

Prep

aid

rein

sura

nce

prem

ium

ced

edRe

insu

ranc

e Ex

pens

e

Net

pre

miu

m r

even

ue

Ope

ning

Clo

sing

Ope

ning

Clo

sing

2012

2011

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- R

u p

e e

s -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

Dire

ct a

nd f

acul

tati

ve

Fire

and

pro

pert

y da

mag

e 1

41,5

49,5

54

32,

478

,68

7 7

3,8

38,9

60

10

0,1

89,

281

77,

916,

103

28

,870

,595

4

0,6

44,7

34

66,

141,

964

34,

047

,317

1

0,0

93,5

38

Mar

ine,

avi

atio

n an

d tr

ansp

ort

30

,057

,70

5 1

,295

,732

3

,544

,637

2

7,8

08

,80

0

12,

796,

058

4

27,6

10

1,5

09,

010

1

1,71

4,65

8

16,

094

,142

6

,70

3,58

3

Mot

or 1

09,

243,

160

2

4,53

9,43

1 4

7,67

0,3

98

86,

112,

193

2,0

26,8

68

1,9

98,9

70

88

4,46

4 3

,141

,374

8

2,97

0,8

19

40

,833

,963

Mis

cella

neou

s 3

7,0

08

,747

4

6,8

22,4

30

20

,820

,540

6

3,0

10,6

37

11,

426,

463

7,5

18,0

66

6,4

28,3

49

12,

516,

180

5

0,4

94,4

57

35,

836

,853

Tota

l 3

17,8

59,1

66

105,

136,

280

14

5,8

74,5

35

277

,120

,911

1

04,

165,

492

38

,815

,241

4

9,46

6,55

7 9

3,51

4,17

6 18

3,60

6,73

5 9

3,46

7,93

7

The

anne

xed

note

s 1

to 3

2 fo

rm a

n in

tegr

al p

art

of t

hese

fina

ncia

l sta

tem

ents

.

Sta

tem

ent

of P

rem

ium

sfo

r the

yea

r end

ed D

ecem

ber 3

1, 2

012

M

ian

M.A

. Sha

hid

Adn

an A

frid

i S

heik

h A

ftab

Ahm

ed

Sye

d A

mm

er A

li Za

idi

Chi

ef E

xecu

tive

Offi

cer

Cha

irman

D

irect

or

Dire

ctor

52 Saudi Pak Insurance Company Limited

Busi

ness

Und

erw

ritte

n In

side

Pak

ista

n

Cla

ss C

laim

s Pa

id

Out

stan

ding

cla

ims

Cla

im

Expe

nses

Rei

nsur

ance

an

d ot

her

Reco

verie

s Re

ceiv

ed

Rein

sura

nce

and

oth

er

Reco

verie

s in

res

pect

O

f ou

tsta

ndin

g c

laim

s

Rei

nsur

ance

A

nd o

ther

Re

cove

ries

Reve

nue

Net

cla

ims

expe

nses

Ope

ning

C

losi

ng

Ope

ning

C

losi

ng

2012

2011

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- R

u p

e e

s -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

Dire

ct a

nd f

acul

tati

ve

Fire

and

pro

pert

y da

mag

e 6

0,9

28,6

20

56,

680

,50

7 4

3,58

1,63

4 4

7,8

29,7

47

50

,78

6,97

1 4

9,51

5,59

8

41,

403,

413

42,

674,

786

5,1

54,9

61

765

,951

Mar

ine,

avi

atio

n an

d t

rans

port

10

,240

,054

5

,725

,30

7 4

,097

,521

8

,612

,268

6

,246

,459

1

,48

5,8

61

1,5

79,0

08

6

,339

,60

6 2

,272

,662

1

95,7

20

Mot

or 5

3,12

8,6

59

17,

88

0,4

68

11,

375,

686

46,

623,

877

1

1,8

56,6

07

4,9

95,3

81

6,8

38,0

00

1

3,69

9,22

6 3

2,92

4,65

1 1

0,5

83,

754

Mis

cella

neou

s 1

0,6

27,8

82

32,

377,

242

21,

856

,951

1

07,

591

6,5

89,

214

24,

481,

517

21,

468

,457

3

,576

,154

(3

,468

,563

) 4

,88

1,50

1

Tota

l 1

34,9

25,2

15

112

,663

,524

8

0,9

11,7

92

103,

173,

483

75,

479,

251

80

,478

,357

7

1,28

8,8

78

66,

289,

772

36,

88

3,71

1 1

6,42

6,92

6

The

anne

xed

note

s 1

to 3

2 fo

rm a

n in

tegr

al p

art

of t

hese

fina

ncia

l sta

tem

ents

.

Sta

tem

ent

of C

laim

sfo

r the

yea

r end

ed D

ecem

ber 3

1, 2

012

M

ian

M.A

. Sha

hid

Adn

an A

frid

i S

heik

h A

ftab

Ahm

ed

Sye

d A

mm

er A

li Za

idi

Chi

ef E

xecu

tive

Offi

cer

Cha

irman

D

irect

or

Dire

ctor

Annual Report | for the year ended December 31, 2012 53

Busi

ness

und

erw

ritte

n in

side

Pak

ista

n

Cla

ssC

omm

issi

on

Paid

or

Paya

ble

Def

erre

d co

mm

issi

onN

et

Com

mis

sion

ex

pens

e

Oth

er

Man

agem

ent

expe

nses

(n

ote

# 2

1)

Und

erw

ritin

g ex

pens

es

Com

mis

sion

re

ceiv

ed f

rom

re

-ins

urer

s

Une

arne

d co

mm

issi

onC

omm

issi

on

from

re

insu

rers

Net

und

erw

ritin

gex

pens

es

Ope

ning

Clo

sing

Ope

ning

Clo

sing

2012

2011

- -

- -

- -

- -

- -

- -

- -

- -

- -

- --

- -

- -

- -

- -

- -

- -

- R

u p

e e

s -

- -

- -

- -

- -

- -

- -

- -

- -

--

- -

- -

- -

- -

- -

- -

- -

- -

- -

- -

Dire

ct a

nd f

acul

tati

ve

Fire

and

pro

pert

y da

mag

e 2

5,50

2,72

3 5

,426

,892

13,

303,

430

17

,626

,18

5 3

0,1

99,1

56

47,

825

,341

19

,80

9,77

9 6

,999

,677

10

,333

,720

16

,475

,736

3

1,34

9,60

5 1

4,27

3,0

87

Mar

ine,

avi

atio

n an

d tr

ansp

ort

5,8

72,7

45

20

7,64

5 6

92,5

60

5,3

87,

831

6

,412

,718

11

,80

0,5

48

3,8

38,8

17

123

,150

4

52,7

03

3,5

09,

264

8,2

91,2

84

3,2

44,9

18

Mot

or 8

,911

,861

2

,122

,042

3,

88

8,8

66

7,1

45,0

37 2

3,30

6,68

7 3

0,4

51,7

24

23,

837

8

4,0

51

10

,40

2 9

7,48

6 3

0,3

54,2

38

15,

160

,935

Mis

cella

neou

s 5

,10

9,27

8

5,2

65,7

20

2,8

74,4

00

7

,50

0,5

99

7,8

95,7

01

15,

396,

299

2,5

83,

360

1

,713

,526

1

,453

,358

2

,843

,528

1

2,55

2,77

1 2

3,34

1,8

71

TOTA

L 4

5,39

6,60

7 1

3,0

22,2

99 2

0,7

59,2

55

37,6

59,6

52

67,

814

,261

10

5,47

3,91

2 2

6,25

5,79

3 8

,920

,40

4 1

2,25

0,1

83

22,

926,

014

8

2,54

7,8

98

56,

020

,811

The

anne

xed

note

s 1

to 3

2 fo

rm a

n in

tegr

al p

art

of t

hese

fina

ncia

l sta

tem

ents

.

Sta

tem

ent

of E

xpen

ses

for t

he y

ear e

nded

Dec

embe

r 31,

20

12

M

ian

M.A

. Sha

hid

Adn

an A

frid

i S

heik

h A

ftab

Ahm

ed

Sye

d A

mm

er A

li Za

idi

Chi

ef E

xecu

tive

Offi

cer

Cha

irman

D

irect

or

Dire

ctor

54 Saudi Pak Insurance Company Limited

Note2012 2011

Rupees Rupees

Income from trading investments

(Loss)/gain on trading - -

Dividend income - -

- -

Income from non-trading investments

Held to maturity

Return on government securities 5,228,398 4,276,287

Return on TDRs 4,953,564 3,153,873

Available-for-sale

Dividend income 39,300 36,000

10,221,262 7,466,160

(Loss)/gain on sale of non-trading investments

- Available-for-sale - -

Impairment (loss) on non-trading investments

- Available-for-sale - -

Provision for impairment in the value of

-Available-for-sale-investments - -

Investment related expenses 12.4 (9,366) (13,251)

Net investment income 10,211,896 7,452,909

The annexed notes 1 to 32 form an integral part of these financial statements.

Statement of Investment Incomefor the year ended December 31, 2012

Mian M.A. Shahid Adnan Afridi Sheikh Aftab Ahmed Syed Ammer Ali Zaidi Chief Executive Officer Chairman Director Director

Annual Report | for the year ended December 31, 2012 55

1 LEGAL STATUS AND NATURE OF BUSINESS

Saudi Pak Insurance Company Limited (the Company) is an unquoted public limited company incorporated in Islamabad, Pakistan on February 15, 2005 under the Companies Ordinance, 1984. The Company is engaged in non-life insurance business mainly comprising of fire, marine, motor and miscellaneous. The Company commenced its commercial operations on April 13, 2005. The registered office of the Company is situated at Suite # 204-A, Second Floor, Madina City Mall, Abdullah Haroon Road, Karachi and principal office of the Company is situated at UIG House 6-D, 1st Floor, Upper Mall, Lahore, Pakistan.

2 BASIS OF PREPARATION

These financial statements have been prepared in accordance with the format of financial statements issued by the Securities and Exchange Commission of Pakistan (SECP) through Securities and Exchange Commission (Insurance) Rules, 2002 [SEC (Insurance) Rules, 2002].

2.1 Statement of compliance

These financial statements have been prepared in accordance with approved accounting standards as applicable in Pakistan. Approved accounting standards comprises of such International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board as are notified under the Companies Ordinance, 1984, provisions of and directives issued under the Companies Ordinance, 1984, the Insurance Ordinance, 2000 and SEC (Insurance) Rules, 2002. In case requirements differ, the provisions or directives of the Companies Ordinance. 1984, Insurance Ordinance, 2000 and SEC (Insurance) Rules, 2002 shall prevail.

The SECP has allowed the insurance companies to defer the application of International Accounting Standard-39 (IAS-39) “Financial Instruments: Recognition and Measurement” in respect of valuation of ‘available-for-sale investments’. Accordingly, the requirements of IAS-39, to the extent required by SECP as aforesaid, have not been considered in the preparation of these Financial Statements.

2.2 Basis of measurement

These financial statements have been prepared under the historical cost convention except that certain financial instruments are carried at fair value and staff retirement benefits are stated at present value.

2.3 Functional and presentation currency

These financial statements are presented in Pakistan Rupees, which is also the Company’s functional and presentation currency. All financial information presented in Pakistan rupees are rounded off to nearest rupees unless otherwise stated.

2.4 Use of estimates and judgments

The preparation of financial statements in conformity with the requirements of approved accounting standards as applicable in Pakistan requires management to make certain judgments,accounting estimates and assumptions. It also requires the management to exercise its judgment in the process of applying the Company’s accounting policies. Actual results may differ from these estimates and associated assumptions are continually evaluated and are based on historical experience, statutory requirements and other factors considered reasonable in the circumstances. Revision to accounting estimates are recognized in the period in which the estimate is revised and in any future periods affected. The estimates and assumptions that are expected to have a significant effect on the assets and liabilities, income and expenses have been disclosed in note 4.24 to these financial statements.

Notes to the Financial Statementsfor the year ended December 31, 2012

56 Saudi Pak Insurance Company Limited

Notes to the Financial Statementsfor the year ended December 31, 2012

3 APPLICATON OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS

3.1 Standards, interpretations and amendments to published approved accounting standards that are not yet effective

The following revised standards, amendments and interpretations with respect to the approved accounting standards as applicable in Pakistan would be effective from the dates mentioned below against the respective standards:

Effective Date

Standard (accounting periods beginning on or after)

IFRS-7 Financial Instruments: Disclosures- (Amendments)

-Amendments enhancing disclosures about offsetting January 01, 2013

of financial assets and financial liabilities

Presentation of Financial Statements-Presentation of July 01, 2012

items of comprehensive income

IAS-27 Separate Financial Statements January 01, 2013

IAS-28 Investments in Associates and Joint Ventures January 01, 2013

IAS-32 Financial Instruments: Presentation (Amendment) January 01, 2014

IAS-19 Employee Benefits - (Amendments) January 01, 2013

The company expects that adoption of the above revisions and amendments of the standards will not materially effect the company’s financial statements in the period of initial application.

In addition to the above, the following new standards have been issued by IASB which are yet to be notified by the SECP for the purpose of applicability in Pakistan.

IASB Effective Date

Standard (annual periods beginning on or after)

IFRS-9 -Financial Instruments: Classification and Measurement January 01, 2015

IFRS-10 -Consolidated Financial Statements January 01, 2013

IFRS-11 -Joint Arrangements January 01, 2013

IFRS-12 -Disclosure of Interest in other Entities January 01, 2013

IFRS-13 -Fair Value Measurement January 01, 2013

Annual Report | for the year ended December 31, 2012 57

4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accounting policies adopted in the preparation of these financial statements are consistent with those of the previous financial year.

4.1 Adoption of new and amended international financial reporting standards (IFRSs)

The Company has adopted the following new and amended IFRS and IFRIC interpretations which become effective during the year:

Standard and Interpretation

Effective date

(accounting periodsbeginning on or after)

IFRS - 7 - Financial Instruments:

Disclosures - (Amendment) July 01, 2011

IAS - 12 - Income Taxes (Amendment) -

Recovery of underlying Assets January 01, 2012

The adoption of the above standard, amendments, interpretations and improvements did not have any material effect on the financial statements.

4.2 Insurance contracts

Insurance contracts are those contracts where the Company (the insurer) has accepted significant insurance risk from another party (the policyholders) by agreeing to compensate the policyholders if a specified uncertain future event (the insured event) adversely affects the policyholders.

Once a contract has been classified as an insurance contract it remains an insurance contract for the remainder of its lifetime, even if the insurance risk reduces significantly during this period, unless all rights and liabilities are extinguished or expired.

Insurance contracts are classified into following main categories, depending on the nature and duration of risk and whether or not the terms and conditions are fixed.

- Fire and property damages

- Marine, aviation and transport

- Motor

- Miscellaneous

Fire and property insurance contracts mainly compensate the Company’s customers for damage suffered to their properties or for the value of property lost.

Marine Insurance covers the loss or damage of vessels, cargo, terminals and any transport of property by which cargo is transferred, acquired or held between the points of origin and final destination.

Notes to the Financial Statementsfor the year ended December 31, 2012

58 Saudi Pak Insurance Company Limited

Motor insurance provides protection against losses incurred as a result of theft, traffic accidents and against third party liability that could be incurred in an accident.

Other various types of insurance are classified in miscellaneous category which includes mainly engineering, crop and livestock, personal accident, worker compensation, travel, products of financial institutions etc.

The Company does not issue any insurance contracts with discretionary participation features (DPF) or any investment contracts.

4.3 Premium

Premium written under a policy is recognized as income over the period of insurance from the date of issuance of the policy to which it relates to its expiry. Where the pattern of incidence of risk varies over the period of the policy, premium is recognized as revenue in accordance with the pattern of the incidence of risk. The portion of premium written relating to the unexpired period of coverage is recognized as unearned premium by the Company. This liability is calculated by applying 1/24 method as specified in the SEC (Insurance) Rules, 2002.

Premium income includes administrative surcharge that represents documentation and other charges recovered by the Company from policy holders in respect of policies issued, at the rate of 5% of the premium written restricted to a maximum of Rs. 2,000 per policy.

Receivables under insurance contracts are recognized when due, at the fair value of the consideration receivable less provision for doubtful debts, if any. If there is objective evidence that the receivable is impaired, the Company reduces the carrying amount of the receivable accordingly and recognizes that impairment loss in the profit and loss account.

Pakistan Reinsurance Company Limited (PRCL) retrocession business is booked on the basis of PRCL statements.

4.4 Reinsurance ceded

The Company enters into reinsurance contracts in the normal course of business in order to limit the potential for losses arising from certain exposures. Outward reinsurance premiums are accounted for in the same period as the related premiums for the direct or accepted reinsurance business being reinsured.

Reinsurance liabilities represent balances due to reinsurance companies. Amounts payable are estimated in a manner consistent with the related reinsurance contract. Reinsurance assets represent balances due from reinsurance companies. Amounts recoverable from reinsurers are estimated in a manner consistent with the provision for outstanding claims or settled claims associated with the reinsurance policies and are in accordance with the related reinsurance contract.

Reinsurance assets are not offset against related insurance liabilities. Income or expenses from reinsurance contract are not offset against expenses or income from related insurance assets.

Reinsurance assets or liabilities are derecognized when the contractual rights are extinguished or expired.

Notes to the Financial Statementsfor the year ended December 31, 2012

Annual Report | for the year ended December 31, 2012 59

The Company assesses its reinsurance assets for impairment on balance sheet date, if there is an objective evidence that the reinsurance asset is impaired, the Company reduces the carrying amount of the reinsurance asset to its recoverable amount and recognizes that impairment loss in the profit and loss account.

4.5 Claim expense

General insurance claims include all claims occurring during the year, whether reported or not, related internal and external claims handling costs that are directly related to the processing and settlement of claims, a reduction for the value of salvage and other recoveries and any adjustments to claims outstanding from previous years.

The Company recognizes liability in respect of all claims incurred up to the balance sheet date which is measured at the undiscounted value of the expected future payments. The claims are considered to be incurred at the time of the incident giving rise to the claim except as otherwise expressly indicated in an insurance contract. The liability for claims include amounts relating to unpaid reported claims, claims incurred but not reported (IBNR) and expected claims settlement costs.

Provision for liability in respect of unpaid reported claims is made on the basis of individual case estimates. Provision for IBNR is based on the management’s best estimate which takes into account the past trends, expected future patterns of reporting of claims and the claims actually reported subsequent to the balance sheet date.

4.6 Reinsurance recoveries against outstanding claims

Claims recoveries from the reinsurer are recognized as an asset at the same time as the claims which give rise to the right of recovery are recognized as a liability and are measured at the amount expected to be received. Claims expenses are reported net of reinsurance in the profit and loss accounts.

4.7 Commission expense and other acquisition costs

Commission expense and other acquisition costs are charged to the profit and loss account at the time the policies are accepted. Commission income from reinsurers is recognized at the time of issuance of the underlying insurance policy by the Company. This income is deferred and brought to account as revenue in accordance with the pattern of recognition of the reinsurance premium to which it relates. Profit commission, if any, which the Company may be entitled to under the terms of reinsurance is recognized on accrual basis.

4.8 Premium deficiency reserves

The Company is required as per SEC (Insurance) Rules, 2002, to maintain a provision in respect of premium deficiency for the class of business where the unearned premium liability is not adequate to meet the expected future liability, after reinsurance from claims and other supplementary expenses expected to be incurred after the balance sheet date in respect of the unexpired policies in that class of business at the balance sheet date. The movement in the premium deficiency reserve is recorded as an expense/ income in profit and loss account for the year.

Notes to the Financial Statementsfor the year ended December 31, 2012

60 Saudi Pak Insurance Company Limited

Percentage (%)

- Fire and property damage 90%

- Marine, aviation and transport 51%

- Motor 50%

- Miscellaneous 30%

The Company determines adequacy of liability of premium deficiency by carrying out analysis of its loss ratio of expired periods. For this purpose average loss ratio of last 3 years inclusive of claim settlement cost but excluding major exceptional claims are taken in to consideration to determine ultimate loss ratio to be applied on unearned premium.

4.9 Creditors, accruals and provisions

Liabilities for creditors and other amounts payable are carried at cost which is the fair value of the consideration to be paid in the future for the services received, whether or not billed to the Company.Provisions are recognized when the Company has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate of’ the amount can be made. Provisions are reviewed at each balance sheet date and adjusted to reflect the current best estimate.

4.10 Taxation

Income tax expense comprises current and deferred tax. Income tax expense is recognized in the profit and loss account, except to the extent that it relates to items recognized directly in other comprehensive income or below equity, in which case it is recognized in other com-prehensive income or below equity.

4.10.1 Current

Provision of current tax is based on the taxable income for the year determined in accordance with the prevailing law for taxation of income. The charge for current tax is calculated using prevailing tax rates or tax rates expected to apply to the profit for the year, if enacted. The charge for current tax also include adjustments, where considered necessary, relating to prior year arising from assessments made during the current year.

4.10.2Deferred

Deferred tax is accounted for using the balance sheet liability method in respect of all temporary differences at the balance sheet date between the tax bases and carrying amounts of assets and liabilities for financial reporting purposes. Deferred tax liabilities are generally recognized for all taxable temporary differences and deferred tax assets are recognized to the extent that it is

For this purpose, loss ratios for each class are estimated based on historical claim development. Judgment is used in assessing the extent to which past trends may not apply in future or the effetcts of one-off claims. If these ratios are adverse, premium deficiency is determined. The loss ratios estimated on these basis for the unexpired portion are as follows:

Notes to the Financial Statementsfor the year ended December 31, 2012

Annual Report | for the year ended December 31, 2012 61

probable that taxable profits will be available against which the deductible temporary differences, unused tax losses and tax credits can be utilized.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled, based on the tax rates (and tax laws) that have been enacted or substantively enacted at the balance sheet date. Deferred tax is charged or credited in the profit and loss account, except in the case of items credited or charged to equity in which case it is included in equity.

4.11 Staff retirement benefits (Defined benefit plan)

The Company operates an approved defined gratuity scheme for all its permanent employees who attain the minimum qualification period for entitlement to gratuity. Contributions to the fund are made based on actuarial recommendations and in line with the provisions of the Income Tax Ordinance, 2001. The most recent actuarial valuation was carried out for the year ended December 31, 2012 using the Projected Unit Credit Method. Actuarial gains/ losses are recognized over the average remaining service life of the employees. Detail of the scheme given in note 6 to the financial statements.

4.12 Cash and cash equivalents

Cash and cash equivalents include cash and balances with banks in current and deposit accounts and stamps in hand.

4.13 Investments

4.13.1 Recognition

All investments are initially recognized at cost, being the fair value of the consideration given and include transaction costs, except for held for trading in which case transaction costs are charged to the profit and loss account. These are recognized and classified as follows: -

- Investment at fair value through profit and loss (held for trading)

- Held to maturity

- Available for sale

4.13.2 Measurement

4.13.2.1 Investment at fair value through profit or loss -held for trading

Investments which are acquired principally for the purposes of generating profit from short term fluctuation in market price or are part of the portfolio in which there is recent actual pattern of short term profit taking are classified as held for trading.

Subsequent to initial recognition, these investments are remeasured at fair value. Gains or losses on investments on remeasurement of these investments are recognized in the profit and loss account.

Notes to the Financial Statementsfor the year ended December 31, 2012

62 Saudi Pak Insurance Company Limited

4.14 Amount due to other insurers/reinsurers

Liabilities for other insurers / reinsurers are carried at cost which is the fair value of consideration to be paid in the future for services.

4.15 Fixed assets

4.15.1 Tangible

These are stated at cost less accumulated depreciation and impairment losses, if any.

Depreciation on all fixed assets is charged to profit and loss account on the reducing balance method so as to write-off depreciable amount of an asset over its useful life

4.13.2.2 Held to maturity

Investments with fixed maturity, where management has both the intent and the ability to hold to maturity, are classified as held to maturity and are initially measured at cost.

At subsequent reporting date, these are measured at amortized cost less provision for impairment, if any. Any premium paid or discount availed on acquisition of held to maturity investment is deferred and amortized over the term of the investment using the effective yield method.

4.13.2.3 Available for sale

Available for sale investments are those non-derivative investments that are designated as available for sale or are not classified in any other category. These are primarily those investments that are intended to be held for an undefined period of time or may be sold in response to the need for liquidity are classified as available for sale. It also includes investments in associated undertakings where the Company does not have significant influence. The Company follows trade date accounting for ‘regular way purchase and sales’ of investments.

Subsequent to initial recognition at cost, these are stated at lower of cost or market value (market value being taken as lower if fall is other than temporary) in accordance with the requirements of the S.R.O. 938 issued by the Securities and Exchange Commission of Pakistan (SECP) in December 2002. The Company uses latest stock exchange quotation to determine the market value of its quoted investments whereas, impairment of unquoted investments is computed by reference to net assets of the investee on the basis of the latest available audited / unaudited financial statements.

Dividend income and entitlement of bonus shares are recognized when the Company’s right to receive such dividend and bonus shares is established.

Gain/ (loss) on remeasurment of available for sale investments are taken to non-owner changes in equity.

Notes to the Financial Statementsfor the year ended December 31, 2012

Annual Report | for the year ended December 31, 2012 63

4.16 Impairment

A financial asset is assessed at each balance sheet date to determine whether there is any objective evidence that it is impaired. A financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset.