spotlight the world in london

TRANSCRIPT

Savills World Research London Residential

Spotlight The World in London

Dynamics of a Global City Overseas investors help fund housing for the cosmopolitan city

Prime in the context of London

International developers deliver in London

What happens when governments intervene?savills.co.uk/research

2014

This publicationThis document was published in July 2014. The data used in the charts and tables is the latest available at the time of going to press. Sources are included for all the charts. We have used a standard set of notes and abbreviations throughout the document.

savills.co.uk/research 03

2014

London's prime residential markets are shaped by its position as a centre of global commerce

ForewordPLAYING IN THE PREMIER LEAGUE

P rime London house prices have grown, in real (inflation adjusted) terms, by an average of 4.9% per annum since

1979. Average UK house prices by the same measure, have grown by 2.9% per annum. A £100,000 UK property purchased in 1979 would today be worth £800,000. The same property in prime London would be worth £2 million. This out-performance of prime London can be put down to many factors, but it has left London house prices looking full by national standards at a time when housing is very high on the political agenda.

We believe the primary cause of London’s high prices is simple: strong demand for a scarce product. London has changed dramatically since the 1970s, and has been promoted from a national capital to the premier league of global cities. Along with New York, it is one of the most consistently successful cities in the world on a range of measures, economic, cultural and structural.

In common with other world cities, London has seen intense urbanisation. In 1984, the population of London started to grow again after five decades of decline. This population increase has resulted from inward migration as well as natural increase and this has been as much from other regions of the UK as from overseas.

Having said this, the 2011 census shows that 37% of all resident Londoners were born overseas. Projections show that, by 2021, London’s total population is set to rise by another million, the fastest growth rate ever.

During the 1936-84 population decline, London's stock of housing was reduced and since its population resurgence, housing has been undersupplied by at least 25,000 units

a year. The cumulative effect has been a supply shortage alongside sudden and, at the time, unexpected growth.

Intense competition for housing has been accompanied by economic growth and increasing prosperity in the city. With money the weapon of choice among those competing for space in the metropolis, it is hardly surprising house price growth has been so strong. This is especially the case in the prime market where affordability is not restricted by mortgage availability.

All this means inevitable price rises, which a London-centric national media broadcasts with alacrity. Coinciding as it has with restricted credit availability, recession, high deposit levels and a consequent lack of access to owner occupation for many, London’s housing crisis is widely reported and high on the political agenda.

London’s high and rising house prices, as well as the exclusion of many young people from owner occupation in the capital, has been blamed on an influx of overseas buyers. We think this is wrong.

Our measures have been for the purchase only of prime property where overseas involvement is higher than in Greater London as a whole. We also measure foreign nationalities but 85% of these overseas buyers live and work in London; they are Londoners. To caricature all overseas purchasers as absentee ‘buy-to-leave’ landlords is laughably wrong. London’s housing problems need solutions based on real evidence, not notions that are at best misguided and at worst that border on the xenophobic. We hope that the evidence we present here will help. n

ExECUTIvE SUMMARY

Only 7% of Greater London properties for sale were bought by purchasers from overseas in

2013-14. See pages 04/05

A global city, residential real estate is just one of London’s asset classes

that attracts foreign investment See pages 06/07

Some countries have introduced measures to dissuade foreign investment, while others

actively encourage it See pages 08/09

London is part of a global web of city-pairs where the wealthy hold property. We reveal their locations

See pages 10/11

International developers and investors are unlocking

new housing supply in London See pages 12/13

Yolande BarnesWorld Residential020 7409 [email protected]: @Yolande_Barnes

Spotlight | The World in London

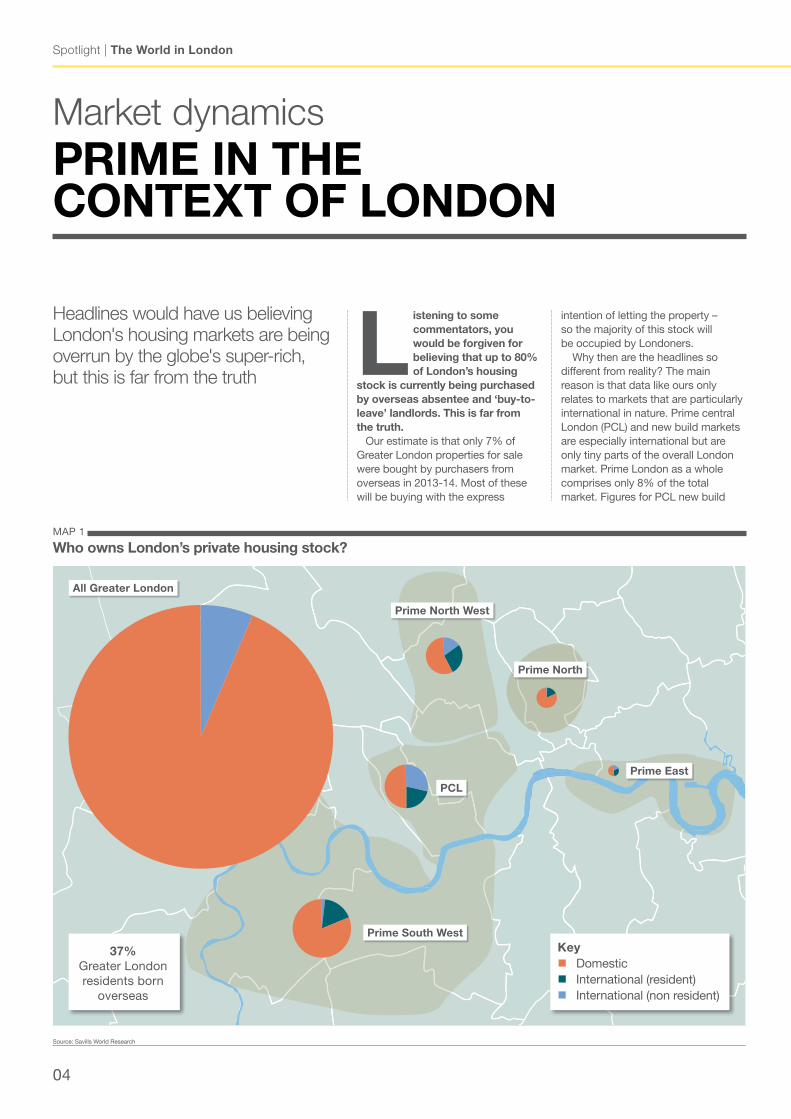

04

intention of letting the property – so the majority of this stock will be occupied by Londoners.

Why then are the headlines so different from reality? The main reason is that data like ours only relates to markets that are particularly international in nature. Prime central London (PCL) and new build markets are especially international but are only tiny parts of the overall London market. Prime London as a whole comprises only 8% of the total market. Figures for PCL new build

Market dynamicsPRIME IN THE CoNTExT of LoNDoN

L istening to some commentators, you would be forgiven for believing that up to 80% of London’s housing

stock is currently being purchased by overseas absentee and ‘buy-to-leave’ landlords. This is far from the truth. Our estimate is that only 7% of Greater London properties for sale were bought by purchasers from overseas in 2013-14. Most of these will be buying with the express

Headlines would have us believing London's housing markets are being overrun by the globe's super-rich, but this is far from the truth

MAP 1

Who owns London’s private housing stock?

Source: Savills World Research

Prime North

Prime North West

Prime East

PCL

Prime South WestKey Domestic International (resident) International (non resident)

Prime North

All Greater London

37%Greater London residents born

overseas

2014

savills.co.uk/research 05

“Prime London as a whole comprises only 8% the London market” Savills World Research

properties are simply not applicable to the market in general.

Also relevant is the fact that what is being measured is not foreign purchase but for the most part purchases by Londoners who happen to have overseas origins. Being such a cosmopolitan city, this is inevitably a high proportion of buyers but they are buying homes to live in; 88% of prime buyers are from the UK or are from overseas but buying their main residence.

A lot of the confusion around overseas purchase arises from the high levels of foreign buyer activity seen in specific, very small, sectors of the London market. Ultra prime new build developments comprising a few dozen units are no indicator of the broader London market in this regard.

Map 1 shows the prime markets that we measure in this publication set against all private stock in Greater London, account for just 8% of the total.

Even in the more domestic prime markets of South West London and prime North, buyer profiles are more in line with the Greater London average. It is only prime North West, PCL and prime East where overseas buyer proportions are higher. Together these comprise 3.8% of Greater London private housing stock. n

GRAPH 1.3

Prime London buyer profiles by area

Source: Savills World Research

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%Prime South West Prime North Prime London Prime North West Prime East PCL

n Domestic n International - main residence n International - second home n International - investment n International - other

GRAPH 1.1

Greater London sales Q2 2013 to Q1 2014

GRAPH 1.2

Prime London buyer profiles

Source: Land Registry

Second Hand Over £500k, 23%

Second Hand Under £500k, 68%

New Build Under £500k, 7%

International - Main Residence, 20%

UK Buyers, 68%

International - Second Home, 6%

International - Investment, 5%

New build Over £500k, 2%

International - Other, 1%

8%Prime London

as a percentage of the total London market

88%of prime buyers

are purchasing their main residence

Source: Savills World Research

06

Spotlight | The World in London

“Global real estate investment is overwhelmingly a world city phenomenon” Savills World Research

Global economicsTHE DYNAMICS of A GLoBAL CITY

G lobal economic forces are shaping real estate markets across the world and few major cities

go untouched. The continued rebalancing of the financial system, the global concentration of wealth and the ongoing activities of central banks are among the recent trends that have all played a significant role in the behaviour of real estate markets. The global inflation of asset prices generally, and residential property in key cities in particular, has played out in many locations and London has been a key participant.

The appeal of London’s residential property to international buyers is echoed in the buyer profile of other real estate sectors in the capital.

The office sector is London’s biggest standard real estate investment class – with in excess of $20 billion in investment in 2013, of which $11.7 billion, or 57%, was cross-border according to RCA data. Over half of investment in London’s hotels was cross-border, while 43% of retail investment came from overseas.

London is not unique in attracting international capital. These trends are echoed in other major global cities. European and Australian cities benefit from the most international investment.

In the first six months of 2014 alone, cross-border capital accounted for more than 70% of all big ticket office deals in London, Tokyo and Sydney. Wealth generated in the ‘new world’ has flowed to safe haven, ‘old world’ markets.

The biggest office real estate deals of the past year were concentrated in a handful of cities (Graph 2.1). The majority of these deals occurred in North American cities, although in this case, the source of investment was overwhelmingly domestic.

Private wealthThe trends seen in big ticket commercial property investment are echoed by our analysis of private wealth. Just under half of all ultra high net worth real estate investment by value has been into the world’s top tier global urban centres. The 45 ‘Alpha Cities’ as defined by the Globalisation and World Cities Research Network. Five of these alone, namely Hong Kong, London, Moscow, Singapore and New York, account for 40% of holdings by value. Global real estate investment is overwhelmingly a world city phenomenon and the best addresses in the world are urban. London is one of the premier world cities which attracts real estate investment of all kinds, both cross-border and domestic.

London is one of the premier world cities, and, as such, it attracts significant investment of all kinds, both cross-border and domestic

TABLE 2.1

Investment into London’s major commercial asset classes, 2013

% cross-border All investment ($ billions)

Cross-border investment($ billions)

office 57% $20.5 $11.7

Retail 43% $3.1 $1.3

Hotel 54% $1.4 $0.8

Apartment 38% $1.4 $0.5

Industrial 17% $1.0 $0.2

Source: RCA (London metro area)

Non UK owners hold more than half of UK-listed equities

savills.co.uk/research 07

2014

overseas investorsOther asset classes are also characterised by high levels of foreign ownership. A 2010 study by the Office of Fair Trading found that 38% of UK infrastructure investment (including utilities) are held by foreigners. Overseas investors are growing in prominence and have been seen to bring new capital investment to the sector and increase competition, leading to efficiency improvements. These investors have interests around the world, of which the UK is only one of many markets in which they operate.

In the stock market, among UK listed companies, non-UK owners held more than half (53.2%) of all equities in 2012, £935.1 billion by value. This figure has grown rapidly, from 30.7% of the market in 1998, and 43.4% in 2010. The large increases partly reflect the growth in international mergers and acquisitions, and the ease with which overseas residents can invest in UK shares. n Source: RCA

Source: Savills World Research, RCA, ONS, OFT

GRAPH 2.1

Top cities for office investment, year to June 2014

$35

$30

$25

$20

$15

$20

$15

$10

$5

$-

Inve

stm

ent

volu

me

(bill

ion

s)

LondonMetro

NYCMetro

Tokyo Paris LA Metro

SFMetro

Boston DC Metro

Sydney Chicago

n Domestic n Cross-border

TABLE 2.2

International ownership / cross-border investment by asset class

London prime residential

London mainstream residential

London office London retail London hotel UK quoted shares

UK infrastructure

& utilities

93%43% 57% 46% 54% 47% 53% 62% 38%43%57%

7%

2013-14 sales 2013-14 sales 2013 investment 2013 investment 2013 investment 2012 ownership 2010 ownership

n Domestic nCross-border

32%

68%

Spotlight | The World in London

08

“There is a fine line to tread between safeguarding homes without stifling the wider economic benefits of overseas investment” Savills World Research

Lessons for LondonGovERNMENT INTERvENTIoN

Some countries encourage overseas ownership, while others actively dissuade it. What lessons can London learn from this?

L ondon is by no means unique in attracting overseas money into its residential markets. Neither is it unique in

charging the weight of international money for pushing residential prices to new highs. In some countries, measures have been introduced to actively dissuade further foreign investment. Meanwhile, in other jurisdictions, policies have been actively initiated to encourage high-spending foreigners to buy property in a bid to revive depressed real estate markets and local economies.

There is a fine line to tread between safeguarding homes for the domestic market without stifling the wider economic benefits overseas buyers bring to the wider investment economy. We outline some of the policies implemented elsewhere and their lessons for London.

Incentives: Golden visasReal estate investor visa programmes, or ‘golden visas’, are now a key strategy in reviving residential markets and building broader economic recovery in countries including Spain, Greece and Portugal. These schemes work by investors making a minimum investment in residential real estate in return for being granted a visa providing residency rights or, in some cases, citizenship and consequently

valuable access to other European Schengen Area countries.

These countries are actively turning depressed real estate markets to their advantage. Many are also making a direct link, explicitly or implicitly, between the propensity for those investing in a country’s real estate to also invest in other areas of its economy.

Portugal has been among the most successful in the golden visa initiative, with its €500,000 minimum investment scheme enjoying strong traction with the Chinese, who accounted for 79% of the 734 visas issued since 2012. Russians, Angolans and Brazilians have been the next biggest recipients.

Spain, Cyprus and Greece have since followed suit with their own schemes, while a number of Caribbean islands offer particularly generous programmes. In both Grenada and St Kitts and Nevis, no visit to the country is even required.

LESSoNS foR LoNDoN?

London already offers visas to non-EU residents through its ‘Tier 1’ investor visa – although not via real estate investment. That some countries are actively encouraging more overseas ownership of residential property as a catalyst to broader economic growth is testament to the wider benefits these buyers are purported to bring.

Disincentives: foreign buyer duties and taxesAt the opposite end of the spectrum, some governments have introduced taxes to actively dissuade overseas purchasers of residential property.

Hong Kong and Singapore have been among the biggest international recipients of new wealth generated in mainland China. The weight of money pushing into these cities from here has helped push prime prices to new highs but both cities are seeing very high population growth within a physically constrained urban area. Both jurisdictions have countered these with additional stamp duties for foreign purchasers.

Non-resident buyers in Hong Kong pay an additional 15% stamp duty, on top of standard stamp duty (8.5% on property over HK$2 million) and duties of between 10% and 20% of purchase price if the property is sold within three years of purchase.

Together, this has made Hong Kong property a less enticing investment and the market has cooled considerably. At their peak in September 2011, foreign buyers accounted for 41.1% of the prime Hong Kong market (HK$12 million+). In March 2014 they made up just 18.5%.

In Singapore, a 15% duty on foreign buyers also applies, but all buyers have been hit with a number of new duties. These include duties ranging from 4% to 16% of the sale price if the property is sold within four years, and rules to ensure that a buyer’s monthly payments do not exceed 60% of their income. International buyer numbers have fallen, although as a proportion of the whole market they still account for around a quarter of the market, down marginally from a high of a third in 2011.

These ‘new world’ taxes are under constant scrutiny and can be changed quickly in response to market conditions. In the cities of the west, when introduced, they tend to be more permanent. Sydney has long placed some restrictions on overseas home ownership. New York effectively restricts a large amount of foreign property ownership through the co-op system of apartment tenure. This makes it extremely difficult for non US citizens to participate, limiting the full potential of that city's residential market.

2014

savills.co.uk/research 09

City/country Intention foreign buyer measure Impact

15% stamp duty on foreign buyers

Foreign buyers, the majority of them mainland Chinese, are down from 41% of the prime market in 2011, to just 18.5% in 2013. Their decline has been a factor in falling prime residential transaction volumes, down 41% in the year to Q1 2014. Prices now stand 8% below their 2012 peak.

Singapore

15% stamp duty on foreign buyers

Foreign buyer numbers have declined, but so have domestic volumes as other cooling measures take effect. The overseas share of the market has remained relatively constant. Singapore is demonstrating its resilience as a world city with diverse international demand base.

Australia Foreign investment in residential real estate is possible only where it increases Australia’s housing stock. Foreign buyers are restricted to new build stock or vacant land, and are subject to approval by the Foreign Investment Review Board.

The scheme is designed to channel foreign capital into new construction. Opponents argue it creates indirect competition for established dwellings as local buyers are displaced into the second hand market. The approval process creates an administrative hurdle to foreign investment.

Portugal

Portuguese visa for investors in property ≥ €500,000

Strong take up by the Chinese, accounting for 79% of those utilising the scheme to date. Lisbon is the favoured destination. Russians, Angolans, and Brazilians also present. The scheme helped stabilise prices in some prime markets, but the government anticipates broader economic benefits.

St Kitts and NevisCitizenship (and in turn visa free travel to in excess of 120 countries worldwide) for those buying property ≥ $400,000. No visit required. Established in 1984, the longest running scheme of its kind.

Supported by the scheme the island’s real estate market remained buoyant throughout the global financial crisis, with citizenship-investors accounting for around 60% of all residential transactions. In spite of foreign investor demand, property prices remain low by Caribbean standards, tempered by high stamp duties and sustained levels of new development.

TABLE 3.1

Regulating foreign buyers – the impact Selected country examples

Source: Savills World Research

Hong Kong

Singapore

Australia

Portugal

St Kitts & Nevis

LESSoNS foR LoNDoN?

Property taxation targeted at foreign buyers does have a suppressing effect on transactions – at least in the short term. It is only one of many factors that drive a foreign purchaser’s decision to buy abroad. On its own, the impact appears to be relatively temporary, cooling volumes notably, while suppressing values until adjustment for the new tax are being made. Limited past evidence would suggest that prices then resume their former trajectories post-adjustment.

In London, specific restrictions on foreign buyers would seem unlikely, particularly during a period when inward investment is being courted by the most senior politicians. The threat of a mansion tax would put the city further up the world cost rankings. Such a tax would mean that London then would rival the very high costs associated with purchasing residential real estate in Singapore and Hong Kong, if property is brought through a corporate vehicle. n

10

Spotlight | The World in London

MIAMI

NEW YoRK

T here are many reasons for overseas buyers to come to London. first and foremost are business reasons; over

85% of prime buyers live and work in London. other types of buyer, investors and second (third, fourth) home owners need a foothold in the city. over 95% have business interests the UK. The way that London operates on the world stage is revealed by our analysis of how money is held in real estate across the globe. London is part of a much wider network of city pairings where the world’s wealthy hold property. We have mapped out the top city pairs where ultra high net worth Individuals hold homes and divide the majority of their time. We have also indicated their main region of business where these ‘super

Source: Savills World Research, Wealth-XSource: Savills World Research

commuters’ host their operations.Our analysis found that while

London is at the nexus of these city hubs, it is just one of a dozen globally important locations. North American cities such as New York, Miami and Los Angeles are of prominence, with mainly domestic links, although LA boasts Pacific Rim pairings, and the New York / London axis is strong.

Pairs need not be geographically distant. In Asia, a Shenzhen / Hong Kong axis provides a foothold in both mainland China and trade-friendly Hong Kong. Monaco and London are a longstanding pair, the major world city complementing the low-tax, leisure destination in home ownership. Longer distance, historic and cultural ties are evident in the Sydney / London and London / Mumbai and Delhi doubles. n

Politically stable

English language Open for business

Secure & safe

Fair judicial system

Tax regime

Culture & heritage

Education

Security of tenure

Cosmopolitan

Advantageous timezone

Prestigious

Wealth cluster

Historic ties & relationships

Large & mature real estate market

Low interest rates Flexible labour market

Lack of bureaucracy

Financial centre

Creative centre

ICT centre

Innovative

Entertainment

Restaurants

Diverse neighbourhoods

Globally connected

Structural advantages Cultural advantages

GRAPH 4.1

Why London?

Super commutersLoNDoN AS PART of THE GLoBAL SCENE

New York Los Angeles

Domestic business pair

savills.co.uk/research 11

2014

MUMBAI

DELHI

SINGAPoRE

LoNDoN

MoNACoBEIJING

HoNG KoNG

LoS ANGELES

SHENzHEN

Source: Savills World Research, Wealth-X

SYDNEYMain business region—Asia—Europe —North America—Australasia

JAKARTA

London Monaco

City and leisure match

Hong Kong Singapore

Asian powerhouses

London Sydney

Historic and cultural ties

Spotlight | The World in London

12

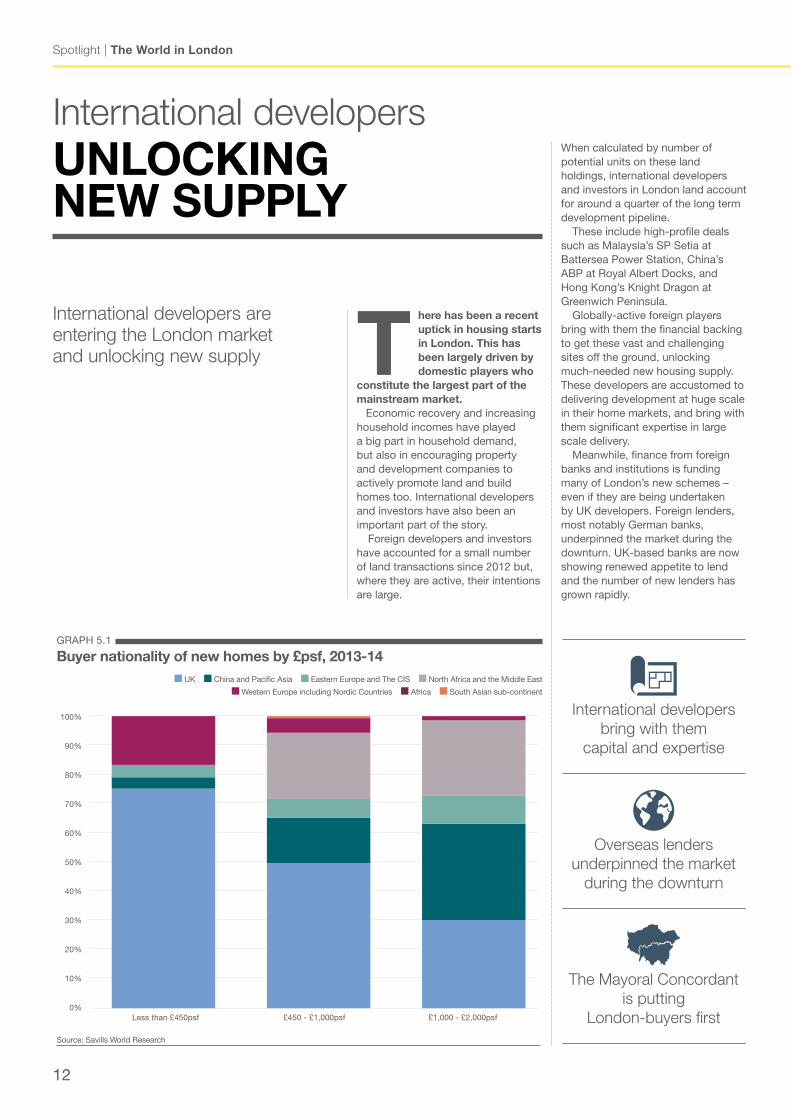

International developersUNLoCKING NEW SUPPLY

T here has been a recent uptick in housing starts in London. This has been largely driven by domestic players who

constitute the largest part of the mainstream market. Economic recovery and increasing household incomes have played a big part in household demand, but also in encouraging property and development companies to actively promote land and build homes too. International developers and investors have also been an important part of the story.

Foreign developers and investors have accounted for a small number of land transactions since 2012 but, where they are active, their intentions are large.

When calculated by number of potential units on these land holdings, international developers and investors in London land account for around a quarter of the long term development pipeline.

These include high-profile deals such as Malaysia’s SP Setia at Battersea Power Station, China’s ABP at Royal Albert Docks, and Hong Kong’s Knight Dragon at Greenwich Peninsula.

Globally-active foreign players bring with them the financial backing to get these vast and challenging sites off the ground, unlocking much-needed new housing supply. These developers are accustomed to delivering development at huge scale in their home markets, and bring with them significant expertise in large scale delivery.

Meanwhile, finance from foreign banks and institutions is funding many of London’s new schemes – even if they are being undertaken by UK developers. Foreign lenders, most notably German banks, underpinned the market during the downturn. UK-based banks are now showing renewed appetite to lend and the number of new lenders has grown rapidly.

International developers are entering the London market and unlocking new supply

GRAPH 5.1

Buyer nationality of new homes by £psf, 2013-14

Source: Savills World Research

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

n UK n China and Pacific Asia n Eastern Europe and The CIS n North Africa and the Middle East

n Western Europe including Nordic Countries n Africa n South Asian sub-continent

Less than £450psf £450 - £1,000psf £1,000 - £2,000psf

International developers bring with them

capital and expertise

Overseas lenders underpinned the market

during the downturn

The Mayoral Concordant is putting

London-buyers first

2014

savills.co.uk/research 13

LoNDoNERS fIRST: THe MAyORAL CONCORDATA commitment to launch to UK-based buyers first

In May 2014, Boris Johnson launched a Mayoral Concordat, a voluntary commitment by developers to market new homes in London to Londoners. 50 developers (accounting for the majority active in London) signed up at launch, committing them to selling new homes on every development to Londoners before, or at the same time as they are available to overseas buyers.

Developer business plans are based on an early return on capital employed. Many foreign buyers are willing to buy ‘off plan’ in a way that UK-based buyers generally haven’t been in the past. This means they put down deposits to buy a unit sometimes before construction has even commenced. This type of purchase has been critical in helping to forward fund the early stages of development

throughout the market downturn as it either provides finance and/or gives confidence to lenders that a scheme has sold and will sell in the marketplace. Selling abroad has therefore unlocked developments not only for the private sector but also for the much-needed affordable and intermediate housing on most London schemes. As most ‘off-plan’ buyers will seek to let their properties, overseas off-plan sales have also provided market-rented housing supply.

Today, London’s domestic market has recovered to a sufficient degree that developers are confident in launching to the home market. Such is the demand for new homes in the capital, an increasing number of local buyers (both domestic and foreign) are

increasingly willing to purchase off plan – again providing capital and security for forward-funding.

Foreign buyers bankrolled the industry during the credit crunch. Today, mortgage financed London-based buyers will drive the new build market. The greatest opportunity is in the lower mainstream markets (priced under £450psft), where Savills estimates a shortage of almost 6,500 homes a year. At the same time, the prime markets (priced in excess of £1,000psft) now look more fully supplied. As developers look beyond the prime markets of central London, London-based buyers will only grow in importance. The Mayoral Concordat ensures that London-based buyers have every possible opportunity to buy the new homes being built.

In London development finance, 63% of financiers fall into the ‘other lenders’ category.

Such is the strength of performance in the UK real estate sector (commercial property included) that there is a significant imbalance between opportunities for lending, which currently stand at £40 billion, compared to lender ambitions of £75 billion, according to Savills figures. This will encourage funders into secondary, non-core locations and possibly into more specialist and non-core types of property.

In the London residential sector, this means outer London locations, supported by domestic end-users. This should mean more supply where it is most needed, in the lower and mid mainstream markets. It should also start to lessen the perception that only prime central, international London is being built.

If housebuilding can be increased, this would do much to lessen the fear of overseas involvement. If home building is to be increased, overseas funders, developers, land owners and promoters – and even landlords and end-owners will be instrumental in enabling it to do so. We should expect nothing less in a global city. n

Spotlight | The World in London

14

OutlookWHo’S NExT?London will continue to attract overseas investment, but which nationalities will be making an impact in five years' time?

L ondon is shaped by global forces, and the economic performance of countries around the world will play out

in London’s real estate markets – though not always in an obvious way. Who will be making an impact on London in five years' time?

Before looking at which geographies might provide the biggest new sources of demand for London, it is worth noting that we detect a potential change in the nature of global investment in real estate generally. Where there has been a trend in recent years for new economies and emerging economies to produce investors eager for capital growth and/or the ‘storage’ of wealth in safe haven assets, we are detecting new motives at work.

Many of those motivated by ‘safe haven’ capital storage and growth have become landlords in ‘old world’ cities around the planet, including London. We anticipate there will continue to be an influx of landlords but they will increasingly be motivated by income returns rather than capital growth. This means they will be attracted to higher-yielding second tier cities and secondary locations in Greater London than they have been in the past.

Prime assets in heavily-invested world cities have become fully-valued – and are beginning to be perceived as such – so the prospects for capital growth have abated. Also, investors themselves have become fully invested in such assets and are now looking for alternatives.

These alternative assets may be prime properties in other world cities where further capital growth is anticipated. Other opportunities may be foreseen in second-tier UK cities and prime country property so that the emphasis comes off London.

With regard to newcomers in London, there will still be wealth generated around the globe that continues to seek a safe haven so this type of purchaser activity will not disappear entirely. Prime London will continue to remain a major recipient

of this type of investment even though cheap currency is ceasing to be such a motivator.

Major playersLooking at the economic performance of overseas economies can be a good indicator of potential outward investment because strong economies can mean more discretionary wealth for investment. However, strong-growth markets at home may mean prospective London buyers stay put to reap greater rewards from domestic housing. On the other hand, weak economies may result in more migrants to London in search of better opportunities, and in turn a place to live.

Overall, we expect continued demand for London housing in mainstream and prime family markets due to inward migration from both the UK and overseas. While remaining important, we expect slightly lower levels of prime and ultra-prime purchaser activity from overseas. There are already signs that prices in these sectors have reached a high

plateau where we anticipate they will remain for a while. Meanwhile, there is opportunity for yield-seeking investors in outer London.

Table 6.1 below shows which countries are forecast to generate the largest amounts of wealth in the next five years. Some, like Brazil, may also see an increasing propensity for overseas real estate investment (which is currently low and largely confined to the USA at present) which could benefit London. Others, like Hong Kong and Singapore, may show a decreasing appetite for London. Already, the mainland Chinese and Malaysians are becoming more active, while the Philippines, Nigeria and Indonesia remain on the radar but haven’t been major players yet. It should be noted that many of these nationalities, even private wealth, may continue to prefer investment in land and development companies rather than residences. In this case, we may see increased development funding and corporate backing for market and other rental buildings rather than prime home buying. n

TABLE 6.1

GDP growth forecasts, major markets

very high growth (≥ 5% in 2019

High growth(3% to 4.9% in 2019)

Moderate growth(2% to 2.9% in 2019)

Low growth(1% to 1.9% in 2019)

India Thailand Greece France

Nigeria Saudi Arabia Russia Portugal

China Hong Kong Ireland Switzerland

Philippines Singapore United Kingdom Austria

Indonesia Mexico Sweden Germany

Vietnam Turkey United States Spain

Malaysia Brazil Norway Japan

Pakistan Australia Canada Italy

Source: IMF

Change from 2013, forecast growth in 2019

savills.co.uk/research 015

Date

savills.co.uk/research 015

Research publicationsour latest reports

World Researchsavills.co.uk/research/uk/residential-research12 Cities Around the World in Dollars and Cents Spotlight | Prime Residential Retreats

For more publications, visit savills.co.uk/research Follow us on Twitter @SavillsUK

Yolande BarnesWorld Research+44 (0) 20 7409 [email protected] Twitter: @Yolande_Barnes

Paul TostevinWorld Research +44 (0) 20 7016 [email protected] Twitter: @Paul_Tostevin

Lucy GreenwoodWorld Research +44 (0) 20 7016 [email protected]

Please contact us for further informationSavills World Research London Residential

Savills plcSavills is a leading global real estate service provider listed on the London Stock Exchange. The company established in 1855, has a rich heritage with unrivalled growth. It is a company that leads rather than follows, and now has over 200 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

This report is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document without prior consent. Whilst every effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.

Jonathan HewlettHead of London Region+44 (0) 20 7824 [email protected]

Dominic GraceHead of London Residential Development+44 (0) 20 7409 [email protected]

savills.co.uk

33 Margaret StreetLondon W1G 0JD+44 (0) 20 7499 8644