squeezing price elasticity into the pricing matrix

TRANSCRIPT

Proprietary Information of Fractal Analytics Inc.

This document contains proprietary and confidential information of Fractal Analytics and subsidiaries (Fractal) and shall not be reproduced or transferred to other

documents, disclosed to others or used for any purpose other than that for which it is furnished, without the prior written consent of Fractal. It shall be returned to

Fractal upon request.

Squeezing Price Elasticity into the

Pricing Matrix

By Deepak Ramanathan

Fractal Analytics Inc.

Presented at the SC CAS Fall meeting 2013

© Fractal 2013 | Confidential

Key points to be covered in the next 60 minutes

1. European insurers have realized substantial benefits by

using price elasticity in their pricing models

2. In the US, though European approach is prohibited, ‘intuition

led’ changes motivated by price elasticity occur

3. By being a bit more scientific while incorporating elasticity

we can improve performance o Without changing the rating structure

o Without introducing new variables in the ROC

o While maintaining ‘loss cost’ as the most important component of pricing

4. Using price elasticity, we can optimize prices while staying

within the allowable band of loss cost indicated relativities

2

© Fractal 2013 | Confidential

How do you determine the scope for improvement

in your pricing model?

3

Move to a multivariate

structure Add more interaction

Enhanced

methodology

Better capture rate of

risk in top deciles

Requires a combination of market knowledge and subjectivity

© Fractal 2013 | Confidential

Average Pricing

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

Population sorted by Predicted Risk Low Risk High Risk

Cu

mu

lati

ve

% o

f A

ctu

al

Lo

ss

es

How does Progressive view improvements to

price segmentations?

4

2.0–ca. 1994

Ideal Model

8.0 - 2009

“9.0”?

Source: From Progressive’s 2010 handbook ( investor presentation)

© Fractal 2013 | Confidential

We can enhance current segmentation in the

following 4 ways

5

3. New Data

2. Existing Data

1. Better Technique

• Non-parametric techniques (RF, GBM) are showing promise

• Leverage existing data better by creating complex interactions

• Innovative data sources (Telematics, Traffic density, Social data etc)

• Incorporate customer characteristics (elasticity and LTV) into pricing

4. Beyond Cost Plus

© Fractal 2013 | Confidential

Elasticity based pricing & optimization is a well

known concept in the insurance industry

6

It is about reaching the efficiency frontier

Loss cost based pricing

More profit /

same volume

More volume /

same profit

Vo

lum

e (

GW

P)

Profit (1 – loss ratio)

© Fractal 2013 | Confidential

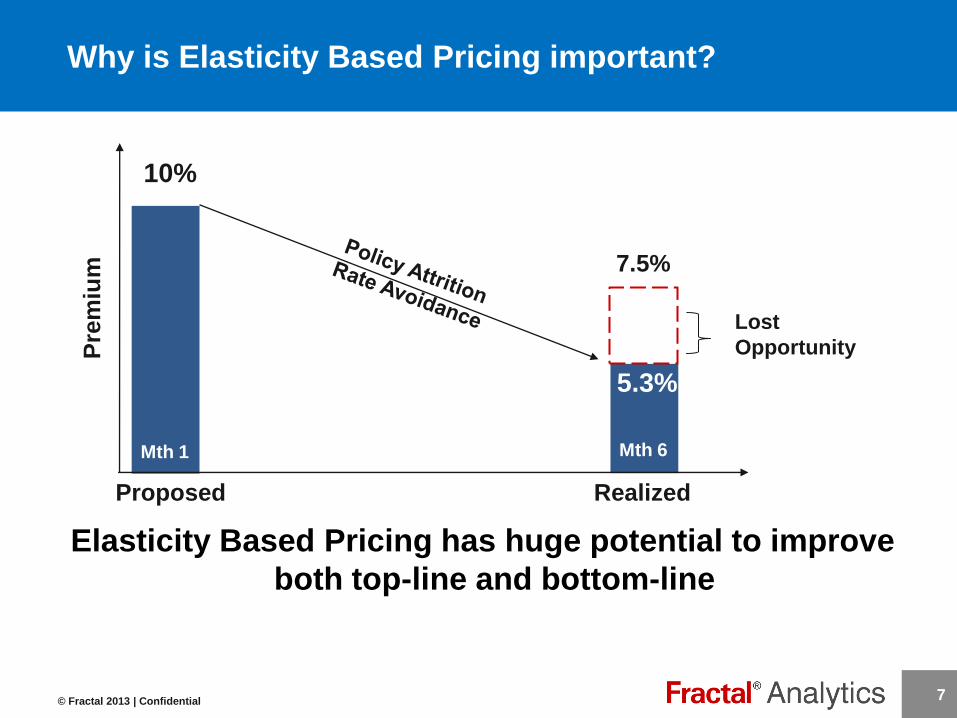

Why is Elasticity Based Pricing important?

Elasticity Based Pricing has huge potential to improve

both top-line and bottom-line

7

5.3%

10%

7.5%

Lost

Opportunity

Mth 1 Mth 6

Proposed Realized

Pre

miu

m

© Fractal 2013 | Confidential

European insurers leverage elasticity in pricing

8

UK market regulations make it easy for insurers to leverage price elasticity

Discounts are offered at point of sale

purely based on elasticity

Selective Discounts

Prices are changed rapidly, some times

multiple times in a day

Frequent Rate Changes

Insurers experiment with prices in the

marketplace to create data for elasticity

Price Testing

© Fractal 2013 | Confidential

In the US, elasticity had not been widely used in

the past because of…

9

• No price testing

• Price parity

• Timeframe in which rates can be

taken

Regulatory requirement

The wait is over

We can capture part of the gain within the regulatory framework

People like us are already doing this

Lack of good data, inability to price

test

Data hurdles

© Fractal 2013 | Confidential 10

We often override pure loss cost in favor of more revenue

Aren’t factors frequently revised after meeting the sales

team?

Isn’t actuarially justified discount such as persistency

discount overridden?

Isn’t rate capping used frequently to avoid disruption?

What is the rationale for such "intuition led", "common

sense led” decisions?

What if we could make these decisions more data driven?

…But ‘intuition led’ Elasticity Based Pricing is

common

© Fractal 2013 | Confidential

Scientific Elasticity Based Pricing requires three

essential components

11

This helps insurers go beyond ‘cost plus’ pricing model and incorporate

key customer characteristics

Index for customer loyalty and

cross-sell potential

Measures customer risk

Helps in segmenting

customers based on risk

attributes

Measures customers’

reaction to price changes

Helps realize different profit

margin depending on price

sensitivity

Future revenue potential /

Lifetime value (LTV)

Loss Cost Modeling

Cost of doing business Price Elasticity

PRICING

© Fractal 2013 | Confidential

…And requires a lead time of up to a year

12

It takes ~6 months to build elasticity & LTV capabilities.

It takes an additional 6 months to run a pilot and validate results.

• Policy level elasticity data Estimated renewal/conversion

Estimated renewal premium

• Policy level LTV data Estimated survival

Estimated future cross-sell

• Elasticity & LTV measurement at

various price changes

© Fractal 2013 | Confidential

Traditional definition of price elasticity is what we read

in text books

13

% change in quantity demanded for

a 1% change in price

e Q / Q

P / P

Where, Q is quantity sold and P is price

Definition

Formula

Estimation Method

Examples

Price testing: Change prices to

monitor demand change

• Oil, rice, salt inelastic (0.4- 0.6)

• Pleasure travel elastic ~ 1.5

© Fractal 2013 | Confidential

…However, in the US insurance context, this concept

deviates widely

14 P is premium; EP is earned premium

New vs. renewal business

e EP / EP

P / P

…By book type

…in its definition

…in the

methodology

…and is not a point

estimate

No price testing and lack of

reliable competitive data

Elasticity is a function of current

premium the magnitude of change

© Fractal 2013 | Confidential

• Assume 3 year

data

• ~ 5 MM annual

policies

• Annual price

change & 80%

renewal

…however estimation is not all that complex

15

Our goal is fill this sparse matrix… Doable?

Dasher Dancer Cupid Comet Rudolph

-20%

0%

5%

+20%

Customers

Pre

miu

m c

ha

ng

e in

%a

ge

Back of envelop

math

Results in

• ~ 7.8 M customer

• 2 data points / policy

• 5% of cells populated

.

.

.

.

.

.

© Fractal 2013 | Confidential

An ensemble of models is built to predict the

probability and magnitude of each response

Understanding price elasticity

Who is going

to buy / renew At what price?

16

© Fractal 2013 | Confidential

Customers exhibit varying tolerance towards price

changes

17

New business customers are more elastic than existing ones because

they tend to shop with multiple carriers before making a decision

80

85

90

95

100

105

110

115

120

-10% 0% 10%

Ind

exe

d to

Pre

miu

m E

arn

ed

a

t 0

% p

rice

ch

an

ge

Uniform price change

Renewal business revenue change by segment

80

85

90

95

100

105

110

115

120

-10% 0% 10%

Ind

exe

d to

Pre

miu

m E

arn

ed

a

t 0

% p

rice

ch

an

ge

Uniform price change

New business revenue change by segment

Illustration only

Segment A- Least Sensitive Portfolio Average Segment B- Most Sensitive

>>>

© Fractal 2013 | Confidential

We can optimize prices by varying a limited

number of rating factors using elasticity & LTV

18

Elasticity & LTV provide new insights about the customer. This can

help us select “better” relativities.

Model Relativity

Upper Confidence

Level

Lower Confidence

Level

Age

35 – 40 years

Selected Relativity

Model Relativity

Upper Confidence

Level

Lower Confidence

Level

Limits

30/50

Selected Relativity

Upper Confidence

Level

Lower Confidence

Level

Territory

Pasadena

Selected Relativity=

Model Relativity

© Fractal 2013 | Confidential

Tests show that this approach works

19

Case Study: Simulation results from a large P & C insurer in the US

Parameter US Regulatory

Scenario

Average premium

change 0% (by design)

Number of policies +0.9%

Written premium +3.5%

Loss ratio -1.0%

Better retention & better top line growth, while remaining risk neutral

UK Market

Scenario (-10% to +10%)

0% (by design)

+3.7%

+9.7%

-2.3%

© Fractal 2013 | Confidential

Other benefits include better forecasting and

objective decision making

20

Rate capping

Forecasting

Framing the Distribution

- Product debate

© Fractal 2013 | Confidential

In Summary…

Optimization techniques have evolved to incorporate elasticity

Due to limited regulations and potential upside, European companies have been early adopters

US insurers are realizing the value of elasticity led optimization

While the accrued benefits may not be as high as in the European scenario, there is money to be made within regulatory constraints

It takes a year to build this capability and go to market with it

21

United States | United Kingdom | Singapore | Dubai | India

fractalanalytics.com

For further details contact:

®

Fractal Analytics helps Fortune 500 companies understand and engage consumers to inspire loyalty through

predictive analytics.

Fractal serves as a strategic partner to market-leading companies by institutionalizing data-driven decisions

across the enterprise.

Deepak Ramanathan Vice President Client Consulting

323-719-4165

Thank You

© Fractal 2013 | Confidential

Customers exhibit varying tolerance towards price

changes

23

91

100

108

93

100

105

95

100

103

80

85

90

95

100

105

110

115

120

-10% 0% 10%

Indexed t

o P

rem

ium

Earn

ed

at

0%

price c

hange

Uniform price change

Renewal business revenue change by segment

Illustration only

Segment A- Least Sensitive Portfolio Average Segment B- Most Sensitive

© Fractal 2013 | Confidential

Customers exhibit varying tolerance towards price

changes

24

94

100

107

97

100

105

110

100

85

80

85

90

95

100

105

110

115

120

-10% 0% 10%

Indexed t

o P

rem

ium

Earn

ed

at

0%

price c

hange

Uniform price change

New business revenue change by segment

Illustration only

Segment A- Least Sensitive Portfolio Average Segment B- Most Sensitive

<<<

© Fractal 2013 | Confidential

To estimate renewal elasticity, we need historical

data about policy renewals

25

Premium information

Old premium (before renewal)

New premium (billed renewal)

Customer reaction

Did the customer attrite?

Or renew at the billed premium?

Or at a different premium?

Policy characteristics

All rating factors

Demographics

Competitive data

Required

data

elements

© Fractal 2013 | Confidential

To estimate new business elasticity, we need

historical quote data

26

Quote conversion information

Did the quote convert?

At what price?

Rating information

Rating engine

Dates of rate change

Historical rating factor relativities

Quote characteristics

All rating factors

Demographics

Competitive data

Required

data

elements