st quarter 2014 - ir.chartnexus.comir.chartnexus.com/thplantation/doc/presentation/thp - 1q14 -...

TRANSCRIPT

1 TH PLANTATIONS BERHAD

(Company No: 12696-M)

1st Quarter 2014 Analyst/Investor Briefing 21 May 2014 2.30pm

TH PLANTATIONS BERHAD

(Company No: 12696-M) Presented by: Radin Rosli Radin Suhadi Plantations Director

Aizzura Ab Rahim Investor Relations

2 TH PLANTATIONS BERHAD

(Company No: 12696-M)

1Q14 highlights

+18%

Mature Area

4.48 mt/ha

FFB Yield

+8%

FFB Production

+37%

FFB Processed

+214%

FFB Purchased

19.93%

OER

+34%

CPO Production

+23%

CPO ASP

4.43%

KER

+39%

Revenue

+49%

Gross Profit

+37%

Cost of Sales

+42%

EBITDA

+90%

Operating Profit

+33%

Profit After Tax

3 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Area Statement (including recently-acquired PT PKP)

Peninsular Sabah Sarawak Indonesia Total

Oil Palm

Mature 11,771 7,056 19,588 38,415

Immature 5,417 1,514 15,070 22,001

Total planted 17,188 8,570 34,659 60,416

Total planted (%) 28% 14% 58% 100%

In-course of planting 1,244 736 2,217 4,197

Greenfield 4,710 11,380 16,090

Rubber

Immature 2,982 2,982

In-course of planting 3,200 3,200

Greenfield 3,248 3,248

Teak 5,129 5,129

Infrastructure & Unplantable 1,567 1,779 10,605 - 13,951

Total land bank 19,998 25,644 52,191 11,380 109,213

Total land bank (%) 18% 24% 48% 10% 100%

4 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Area Statement (including recently-acquired PT PKP)

Mature Oil Palm 35%

Immature Oil Palm 20%

Immature Rubber 3%

Immature Teak 4%

In-course of planting

7%

Greenfield 18%

Infra & Others 13%

Total land bank: 109,213 Ha

>25 years (Old

Mature) 10%

20 - 25 (Old

Mature) 15%

10 - 19 (Prime

Mature) 24%

4 - 9 (Young

Mature) 51%

Average age: 13 years

5 TH PLANTATIONS BERHAD

(Company No: 12696-M)

A closer look at revenue

Avg Mature Area (ha) 3

2,5

40

38

,41

5

1Q13 1Q14

+18%

FFB Production (MT)

15

9,0

36

17

2,0

02

1Q13 1Q14

+8%

CPO Production (MT)

29

,55

8

39

,61

8

1Q13 1Q14

+34%

FFB Processed (MT)

14

5,3

62

19

8,7

42

1Q13 1Q14

+40%

CPO Sales (MT)

32

,94

0

39

,09

6

1Q13 1Q14

+19%

PK Production (MT)

7,3

83

8,8

03

1Q13 1Q14

+19%

6 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Bigger contribution of younger estates seen

FFB Yield (MT/ha) 4

.89

4.4

8

1Q13 1Q14

KER (%) 5

.08

4.4

3

1Q13 1Q14

-0.65 ppt

OER (%)

20

.33

19

.93

1Q13 1Q14

-0.40 ppt

-8% Estates FFB Cont Yields

Sg Arip 2% 3.02

Merbok 3% 3.48

Tg Lilin 3% 3.48

Raja Udang 5% 3.86

Enggang 5% 3.96

Estates FFB Cont Yields

Sg Tenegang 2% 6.02

Sg Merchong 2% 5.61

Sg Koyah 2% 5.35

Mamahat 6% 5.29

Gedong 5% 4.99

Prolonged dry spell in late 1Q – forced ripening

Industry-wide OER and KER downtrend

Note: 1st year harvesting: 7,484ha @ 20% of mature area

OER & KER seen improving in April onwards

Additional contributing factors:

7 TH PLANTATIONS BERHAD

(Company No: 12696-M)

4.51 4.66

5.76

7.22

4.89

5.41

6.92 6.61

4.48

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

-

50,000

100,000

150,000

200,000

250,000

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Lower yield due to bigger contribution of younger estates FF

B P

rod

uct

ion

(M

T)

Post major acquisitions

FFB Y

ield

/he

ctare (MT/H

a)

8 TH PLANTATIONS BERHAD

(Company No: 12696-M)

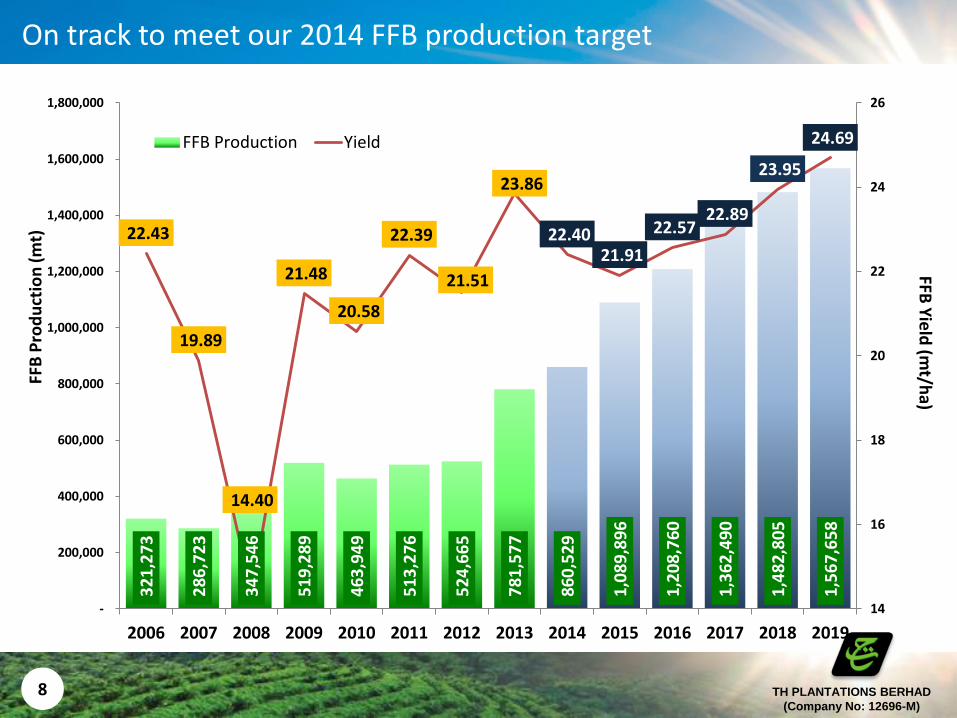

On track to meet our 2014 FFB production target

32

1,2

73

28

6,7

23

34

7,5

46

51

9,2

89

46

3,9

49

51

3,2

76

52

4,6

65

78

1,5

77

86

0,5

29

1,0

89

,89

6

1,2

08

,76

0

1,3

62

,49

0

1,4

82

,80

5

1,5

67

,65

8

22.43

19.89

14.40

21.48

20.58

22.39

21.51

23.86

22.40 21.91

22.57 22.89

23.95

24.69

14

16

18

20

22

24

26

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

FFB Production Yield

FFB

Pro

du

ctio

n (

mt)

FFB

Yie

ld (m

t/ha)

9 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Stronger CPO prices seen in 1Q of the year

Group 1Q14 1Q13

CPO RM2,507 RM2,035

PK RM1,918 RM1,115

FFB RM626 RM346

Sabah Sarawak

Sales Tax 7.5% 5%

Discount RM40-100

+23%

+72%

+81%

CPO Prices MPOB Reference

Price

Average Trading

Price

Average Selling Price

(before sales tax)

Average Selling Price

(after sales tax)

Sales Volume

(%)

Peninsular 2,658 2,642 2,621 - 30%

Sarawak 2,604 2,607 2,588 2,464 50%

Sabah 2,640 2,619 2,559 2,358 20%

10 TH PLANTATIONS BERHAD

(Company No: 12696-M)

1,1

29

1,4

92

1Q13 1Q14

CPO Production Cost (RM/MT)

Higher costs attributed to younger estates

Ave

rage

19

9 24

4

1Q13 1Q14

Estate Production Cost (RM/MT)

49

46

1Q13 1Q14

Mill Manufacturing Cost (RM/MT)

*excl depreciation *excl depreciation

*excl depreciation

+32%

+22%

-5%

11 TH PLANTATIONS BERHAD

(Company No: 12696-M)

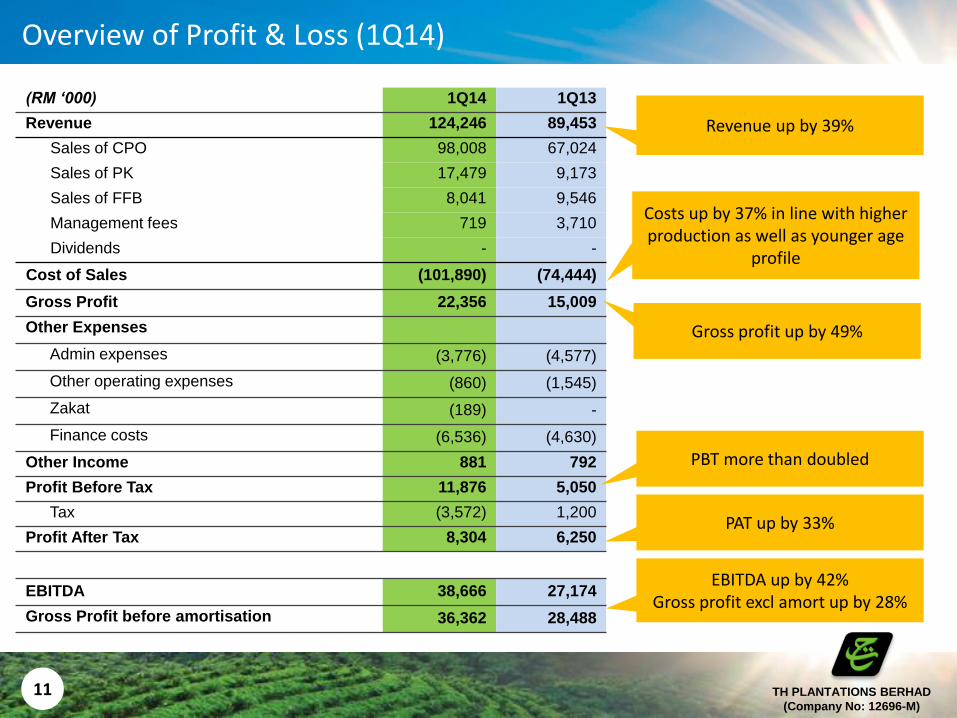

Overview of Profit & Loss (1Q14)

(RM ‘000) 1Q14 1Q13

Revenue 124,246 89,453

Sales of CPO 98,008 67,024

Sales of PK 17,479 9,173

Sales of FFB 8,041 9,546

Management fees 719 3,710

Dividends - -

Cost of Sales (101,890) (74,444)

Gross Profit 22,356 15,009

Other Expenses

Admin expenses (3,776) (4,577)

Other operating expenses (860) (1,545)

Zakat (189) -

Finance costs (6,536) (4,630)

Other Income 881 792

Profit Before Tax 11,876 5,050

Tax (3,572) 1,200

Profit After Tax 8,304 6,250

EBITDA 38,666 27,174

Gross Profit before amortisation 36,362 28,488

Revenue up by 39%

EBITDA up by 42% Gross profit excl amort up by 28%

Gross profit up by 49%

PBT more than doubled

PAT up by 33%

Costs up by 37% in line with higher production as well as younger age

profile

12 TH PLANTATIONS BERHAD

(Company No: 12696-M)

A closer look at costs

Cost of Sales 1Q14 1Q13 Variance (%) Remarks

Estate Production Cost 41,973 31,604 +33% Higher production and higher costs associated with younger palms

Overhead 6,641 5,349 +24% In line with acquisitions

FFB Purchases 21,774 6,051 +260% RUPOM commissioned in July 2013 as well as initiatives to increase utilisation at other mills

Mill Manufacturing Cost 12,581 8,832 +42% Higher production and new mill

Depreciation – Estates 2,136 1,594 +34% In line with major acquisitions

Depreciation – Mill 3,882 2,124 +83% In line with major acquisitions

Amortisation 14,007 13,478 +4% In line with guidance

Other Costs 1Q14 1Q13 Variance (%) Remarks

Admin Expenses 3,776 4,577 -17% Lower costs related to acquisitions

Other operating expenses 630 1,248 -50% Lower costs related to acquisitions

Depreciation 231 297 -22% -

Zakat 189 - +100% Net current assets > net current liabilities

Finance Cost 6,536 4,630 +41% Additional debt drawdown in April and Dec 2013

13 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Progress Update

14 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Sibu

Tawau

Kota Kinabalu

Sandakan

Kuching

Bintulu

Miri

Lahad

Datu

Seremban

Johor Bahru

Kuantan

Kuala Terengganu

Kota Baharu

Ladang Londah

Ladang Klagan 2

Ladang Klagan 4

Ladang Jatimas

Ladang Sungai Kerian

Ladang Sungai Rasau

Ladang Kepayang

Ladang Semalatong

Ladang Sungai Merchong

Ladang Bukit Lawiang

Ladang Gunung Sumalayang

Ladang Sungai Tenegang

Ladang Sungai Koyah

Ladang Sungai Arip

2014 development programme

Ladang Sungai Buan

OP new planting 2,217 ha

OP replanting 1,980 ha

Rubber new planting 3,200 ha

15 TH PLANTATIONS BERHAD

(Company No: 12696-M)

2010 Age Profile – 19 Years

3,205 Ha 9%

8,050 Ha 21%

8,217 Ha 22%

3,069 Ha 8%

> 25 (Old Mature) 20-25 (Mature) 10 - 19 (Prime Mature) 4 - 9 (Young Mature)

1,113 Ha 2%

3,148 Ha 4%

25,118 Ha 34%

32,282 Ha 43%

2017 Age Profile – 10 Years

Average age to be optimised in 5 years

3,944 Ha 10%

5,846 Ha 15%

9,028 Ha 24%

19,597 Ha 51%

2014 Age Profile – 13 Years

Immature: 14,943 ha

Immature: 26,198 ha

Immature: 15,645 ha

16 TH PLANTATIONS BERHAD

(Company No: 12696-M)

PT PKP: Progress Update

• Acquisition completed on 11 January 2014 • Approx 11,380 hectares of land bank • About 30 ha have been cleared for nursery site – first batch of seeds

expected to arrive mid June • Planting expected to commence in 2Q15

17 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Progress photos taken recently

18 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Progress photos taken recently

19 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Outlook Production on track so far Weather may impact production Prices expected to be volatile

20 TH PLANTATIONS BERHAD

(Company No: 12696-M)

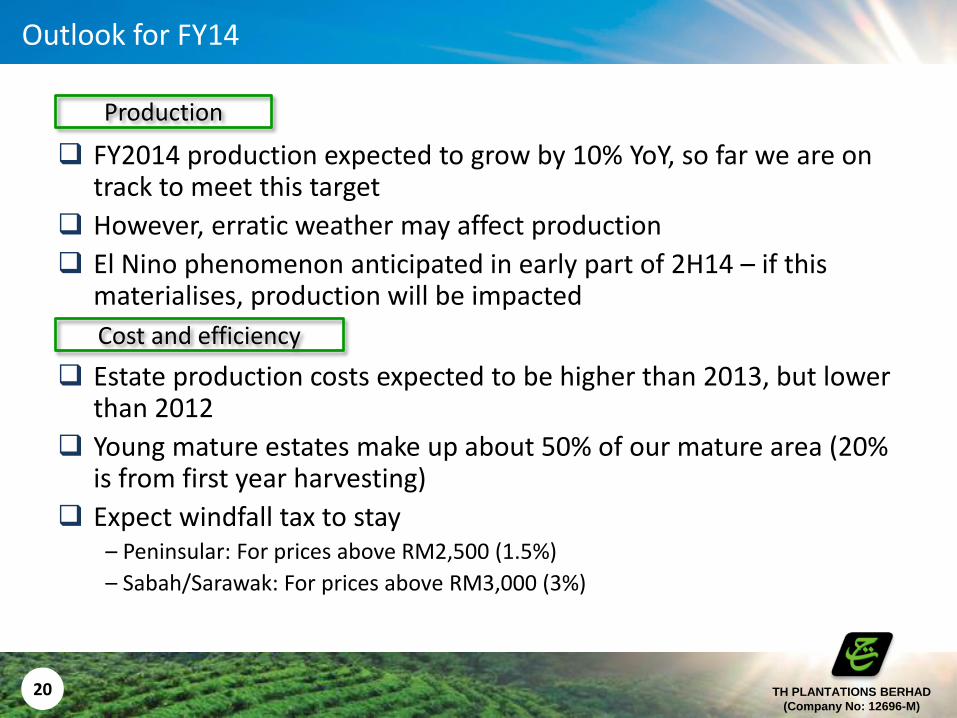

Outlook for FY14

FY2014 production expected to grow by 10% YoY, so far we are on track to meet this target

However, erratic weather may affect production

El Nino phenomenon anticipated in early part of 2H14 – if this materialises, production will be impacted

Estate production costs expected to be higher than 2013, but lower

than 2012

Young mature estates make up about 50% of our mature area (20% is from first year harvesting)

Expect windfall tax to stay – Peninsular: For prices above RM2,500 (1.5%)

– Sabah/Sarawak: For prices above RM3,000 (3%)

Production

Cost and efficiency

21 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Outlook for FY14

CPO prices are expected to be volatile for the rest of the year

Higher stockpiles

Increase in near-term production

Lower growth in China

Strengthening MYR

Increased demand of palm oil for biodiesel

Anticipation of El Nino

30% (long-term): 30% (forward) : 40% (spot) practised depending on prevailing prices

Marketing Strategy

CPO Price

22 TH PLANTATIONS BERHAD

(Company No: 12696-M)

Thank You

Our vision is to be an integrated and sustainable plantation player

with global recognition, promising premium quality products

For further information/queries, please email [email protected]

TH PLANTATIONS BERHAD

(Company No: 12696-M)