stat 274 theory of interest chapters 8 and 9: term

TRANSCRIPT

Stat 274

Theory of Interest

Chapters 8 and 9: Term Structure and

Interest Rate Sensitivity

Brian Hartman

Brigham Young University

Yield Curves

⌫(t) is the current market price for a t-year zero-coupon bond.

The t-year spot rate of interest, yt , is the yield per year on at-year zero-coupon bond.

⌫(t)(1 + yt)t = 1 ) ⌫(t) =

1

(1 + yt)t

The term structure of the interest rates is the relationshipbetween t and yt .

It is often presented as a plot of yt against t, known as theyield curve.

2

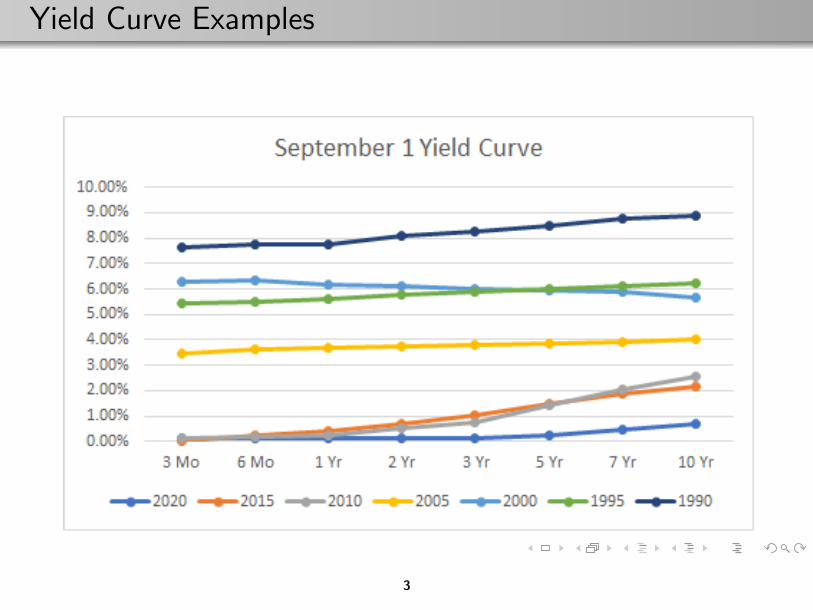

Yield Curve Examples

3

Forward Rates

Let f (t, t + k) be the forward rate of interest, the e↵ectiveannual rate of interest paid between time t and time t + k .

Forward rates use the following no-arbitrage argument.

[1 + f (t, t + k)]k =(1 + yt+k)t+k

(1 + yt)t=

⌫(t)

⌫(t + k)

4

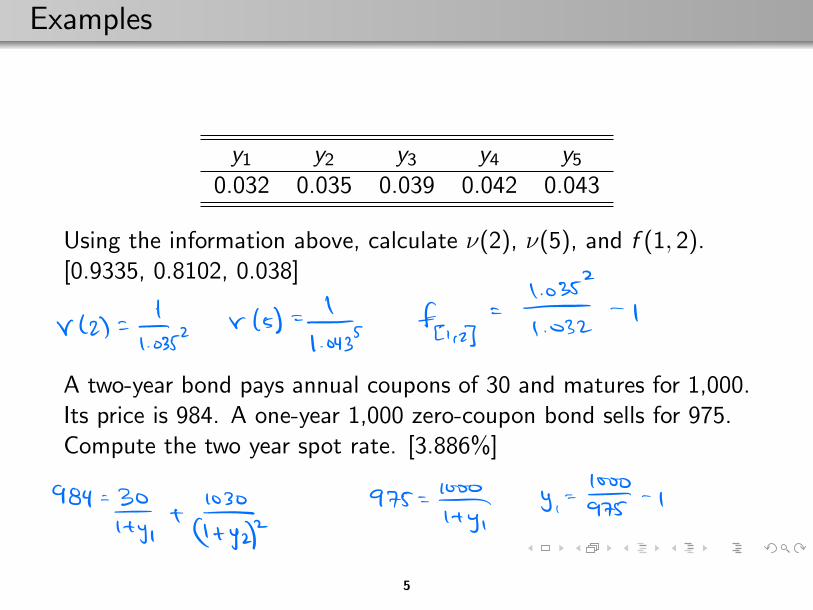

Examples

y1 y2 y3 y4 y50.032 0.035 0.039 0.042 0.043

Using the information above, calculate ⌫(2), ⌫(5), and f (1, 2).[0.9335, 0.8102, 0.038]

A two-year bond pays annual coupons of 30 and matures for 1,000.Its price is 984. A one-year 1,000 zero-coupon bond sells for 975.Compute the two year spot rate. [3.886%]

5

Interest Rate Swaps - Introduction

Fixed and variable interest rates

LIBOR and prime interest rate

Interest rate swap: contract where one party pays a fixedinterest rate (swap rate, R) while the other pays a variablerate on a notional amount, Q

Period of the swap is known as the swap term or swap tenor

Net payments are made on the settlement dates

Time between settlement dates is the settlement period

For most swaps, the notional amount stays constant. If thenotional amount decreases, it is known as an amortizing swap.If the notional amount increases, it is an accreting swap

Most start at time zero, but if not, it is a deferred swap

To find the swap rate, we set the present value of the twopayment streams equal to each other

6

Swap Example 1

You borrow 500,000 at a variable interest rate for two years, withinterest payments at the end of each year. The current spot ratesare 5% for one year and 6% for two. To calculate the swap rate,set the two interest streams equal to each other.

500, 000(0.05)

1.05+

500, 000(0.07010)

1.062=

500, 000(R)

1.05+

500, 000(R)

1.062

R = 0.05971

7

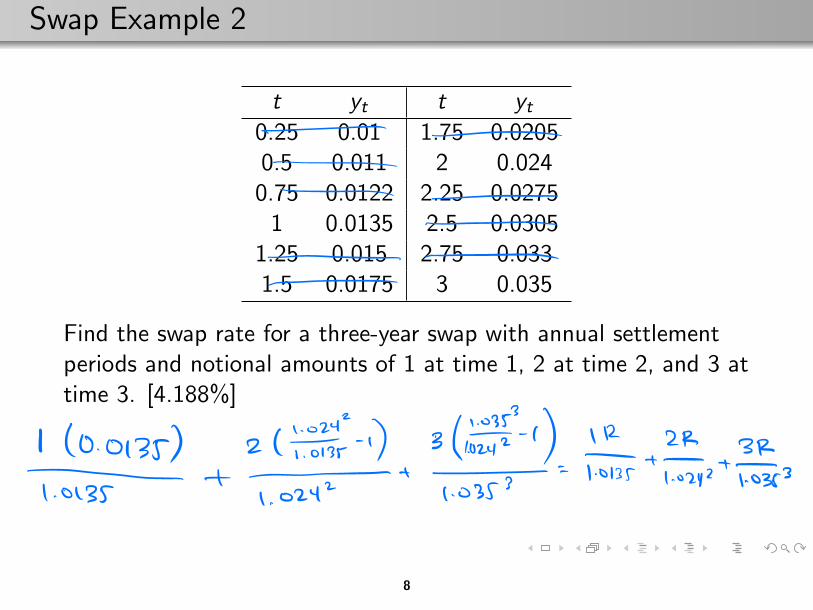

Swap Example 2

t yt t yt0.25 0.01 1.75 0.02050.5 0.011 2 0.0240.75 0.0122 2.25 0.02751 0.0135 2.5 0.0305

1.25 0.015 2.75 0.0331.5 0.0175 3 0.035

Find the swap rate for a three-year swap with annual settlementperiods and notional amounts of 1 at time 1, 2 at time 2, and 3 attime 3. [4.188%]

8

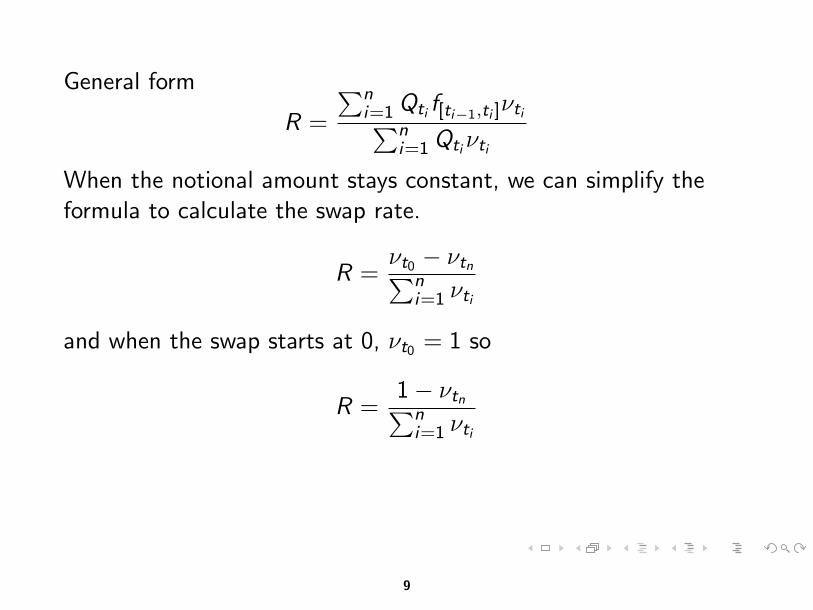

General form

R =

Pni=1Qti f[ti�1,ti ]⌫tiPn

i=1Qti⌫ti

When the notional amount stays constant, we can simplify theformula to calculate the swap rate.

R =⌫t0 � ⌫tnPn

i=1 ⌫ti

and when the swap starts at 0, ⌫t0 = 1 so

R =1� ⌫tnPni=1 ⌫ti

9

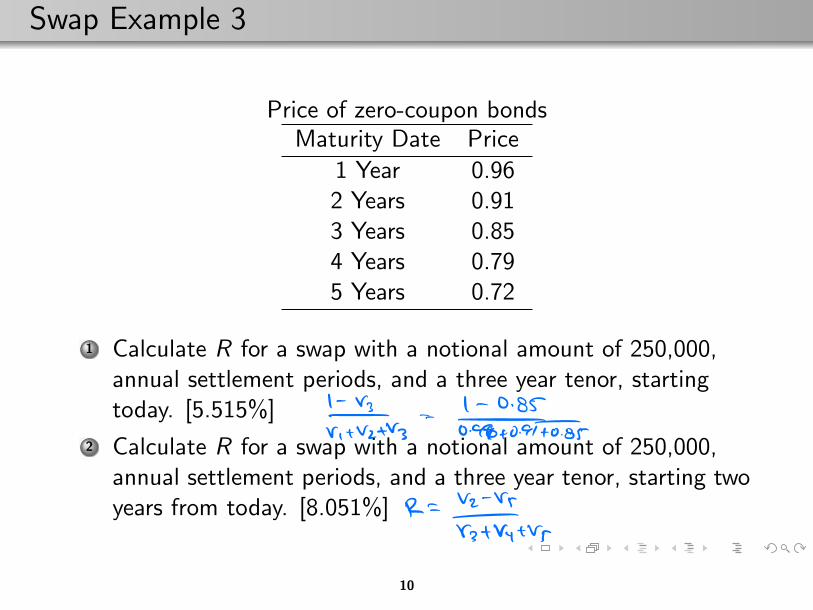

Swap Example 3

Price of zero-coupon bondsMaturity Date Price

1 Year 0.962 Years 0.913 Years 0.854 Years 0.795 Years 0.72

1 Calculate R for a swap with a notional amount of 250,000,annual settlement periods, and a three year tenor, startingtoday. [5.515%]

2 Calculate R for a swap with a notional amount of 250,000,annual settlement periods, and a three year tenor, starting twoyears from today. [8.051%]

10

Swap Example 3

Calculate R for a swap with a notional amount of 250,000, annualsettlement periods, and a three year tenor, starting today. [5.515%]

11

Swap Example 3

Calculate R for a swap with a notional amount of 250,000, annualsettlement periods, and a three year tenor, starting two years fromtoday. [8.051%]

12

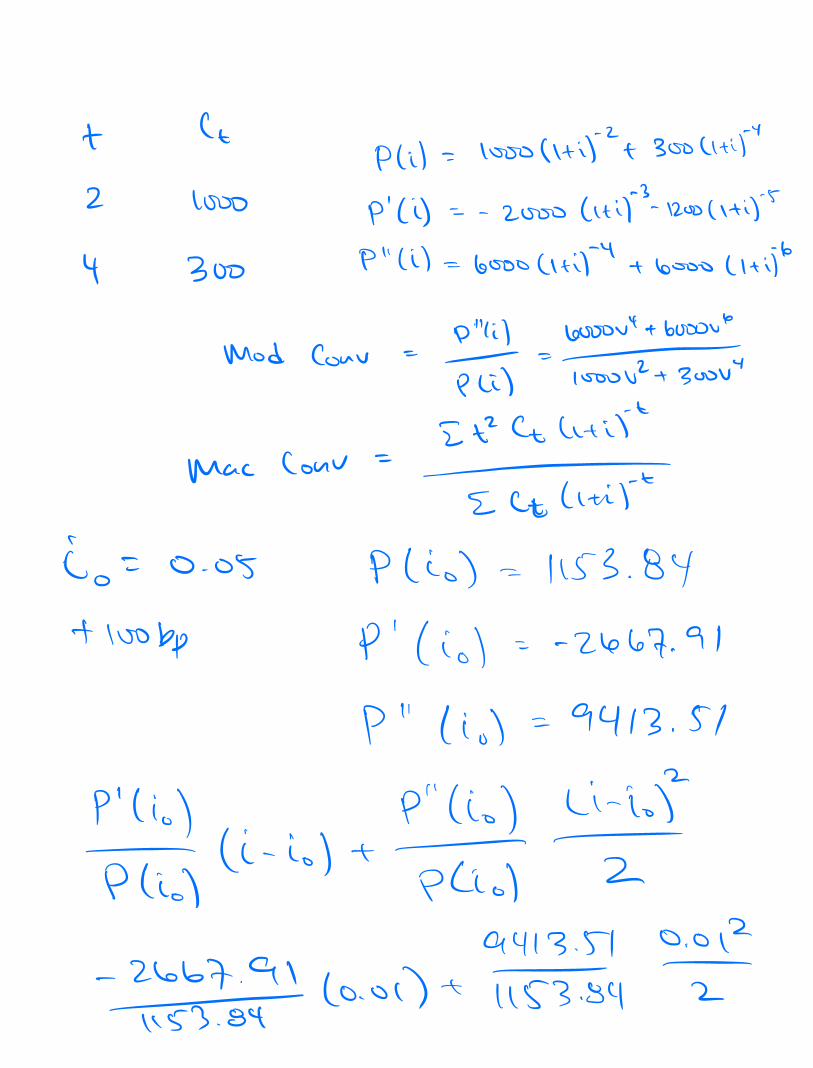

Sensitivity Approximations

Given an interest rate i , the present value of a set of cash flows is

P(i) =X

t�0

Ct(1 + i)�t

P 0(i) = �X

t�0

Ctt(1 + i)�t�1

P 00(i) =X

t�0

Ctt(t + 1)(1 + i)�t�2

The second-order Taylor approximation is

P(i) ⇡ P(i0) + P 0(i0)(i � i0) +P 00(i0)

2(i � i0)

2

13

Excel Sensitivity Example

Your company has the following future cash flows.

Assets

1M in one year

2M in two years

2M in six years

Liabilities

0.3M in one, two, and three years

3M in four years.

14

Sensitivity Results

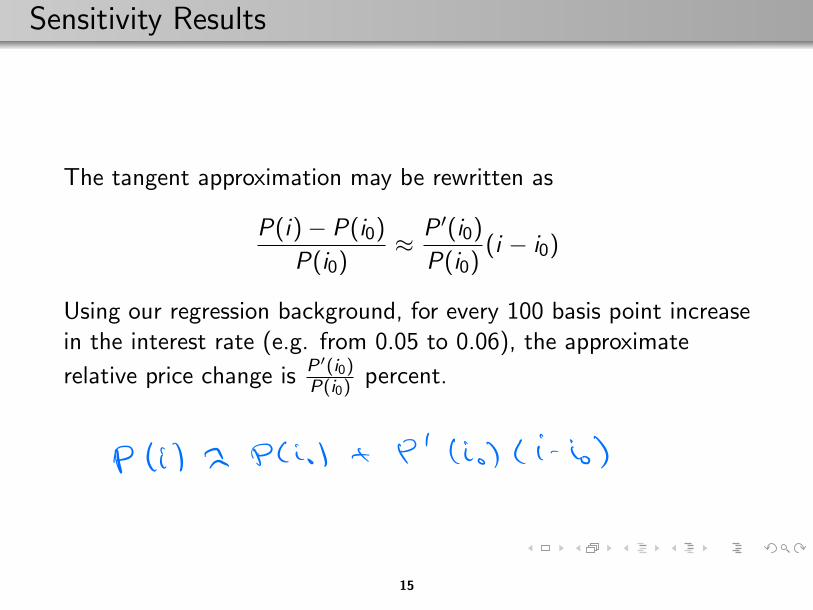

The tangent approximation may be rewritten as

P(i)� P(i0)

P(i0)⇡ P 0(i0)

P(i0)(i � i0)

Using our regression background, for every 100 basis point increasein the interest rate (e.g. from 0.05 to 0.06), the approximate

relative price change is P0(i0)P(i0)

percent.

15

Modified Duration

The modified duration is defined as

D(i , 1) = �P 0(i0)

P(i0)=

Pt�0 Ctt(1 + i)�t�1

Pt�0 Ct(1 + i)�t

The larger the modified duration, the more sensitive the price is tointerest rate changes. More generally, the modified duration is

D(i ,m) = �dP/di (m)

P(i)=

1 + i

1 + i (m)

m

!D(i , 1)

16

Macaulay Duration

Because i = e� � 1,

D(i ,1) = D(i , 1)(1 + i) =X

t�0

✓Ct(1 + i)�t

P(i)

◆t

Note that this is the weighted average of payment times, wherethe weights are the portion of the total price attributable to thatcash flow.

17

Examples

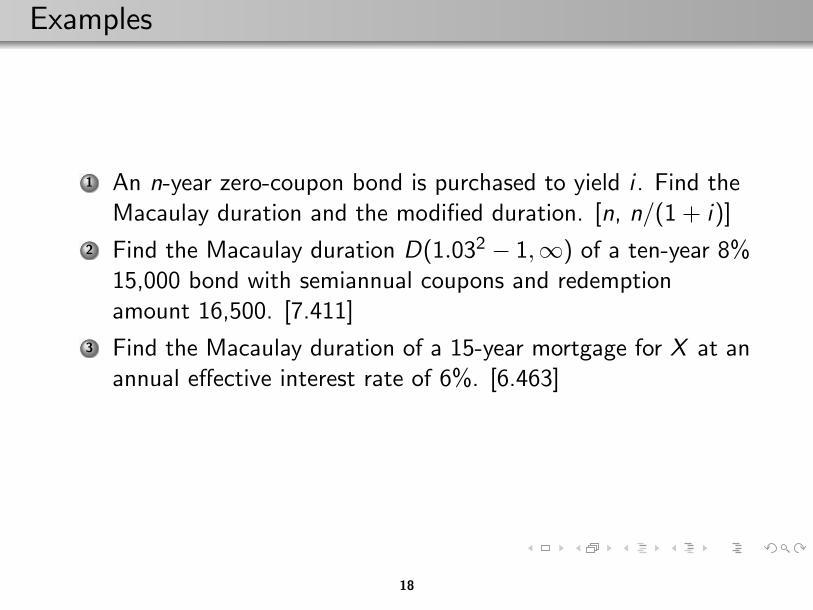

1 An n-year zero-coupon bond is purchased to yield i . Find theMacaulay duration and the modified duration. [n, n/(1 + i)]

2 Find the Macaulay duration D(1.032 � 1,1) of a ten-year 8%15,000 bond with semiannual coupons and redemptionamount 16,500. [7.411]

3 Find the Macaulay duration of a 15-year mortgage for X at anannual e↵ective interest rate of 6%. [6.463]

18

Examples

An n-year zero-coupon bond is purchased to yield i . Find theMacaulay duration and the modified duration. [n, n/(1 + i)]

19

Examples

Find the Macaulay duration D(1.032 � 1,1) of a ten-year 8%15,000 bond with semiannual coupons and redemption amount16,500. [7.411]

20

Examples

Find the Macaulay duration of a 15-year mortgage for X at anannual e↵ective interest rate of 6%. [6.463]

21

First-order Macaulay Approximation

Using the Macaulay duration, we can approximate the change inthe present value using the following formula

P(i) ⇡ P(i0)

✓1 + i01 + i

◆D(i0,1)

22

Convexity

We saw previously that the second-order approximation did abetter job than the tangent line. We will define the modifiedconvexity to be:

C (i , 1) =P 00(i)

P(i)

The quadratic approximation can then be rewritten as:

P(i)� P(i0)

P(i0)⇡ P 0(i0)

P(i0)(i � i0) +

P 00(i0)

2P(i0)(i � i0)

2

⇡ �D(i0, 1)(i � i0) + C (i0, 1)(i � i0)2

2

23

Example

A five-year zero-coupon bond redeemable at C is purchased toprovide an annual e↵ective yield of 6%. Find the modifiedconvexity C (i , 1). Use that, along with the modified duration, toestimate the relative price change if the interest rate goes up by100 basis points. [30/(1 + i)2, -0.04583]

24

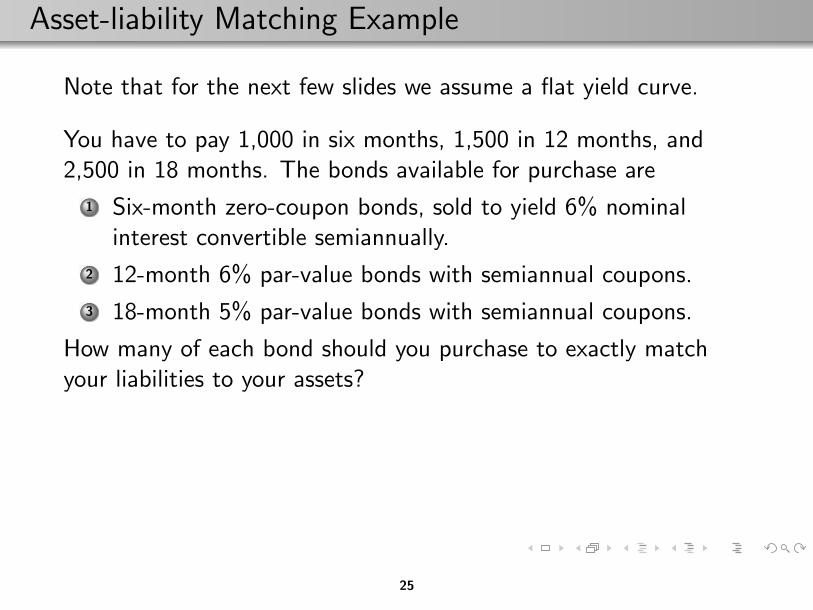

Asset-liability Matching Example

Note that for the next few slides we assume a flat yield curve.

You have to pay 1,000 in six months, 1,500 in 12 months, and2,500 in 18 months. The bonds available for purchase are

1 Six-month zero-coupon bonds, sold to yield 6% nominalinterest convertible semiannually.

2 12-month 6% par-value bonds with semiannual coupons.

3 18-month 5% par-value bonds with semiannual coupons.

How many of each bond should you purchase to exactly matchyour liabilities to your assets?

25

Immunization Example

You have to pay your brother 10,000 in exactly 5 years. He loansyou 7,835.26 (to yield him 5%). You can currently buy 5%zero-coupon bonds, but only for either 2, 3, or 7 years. How canyou be guaranteed to be able to pay him back?

If you put half (3,917.63) in each type of bond, sell the 7-yearbond in three years, and reinvest the entirety in a two-yearzero-coupon bond paying the prevailing interest rate, will you have10,000 in five years if the prevailing interest rate is

5%

20%

1%

26

Immunization Example

27

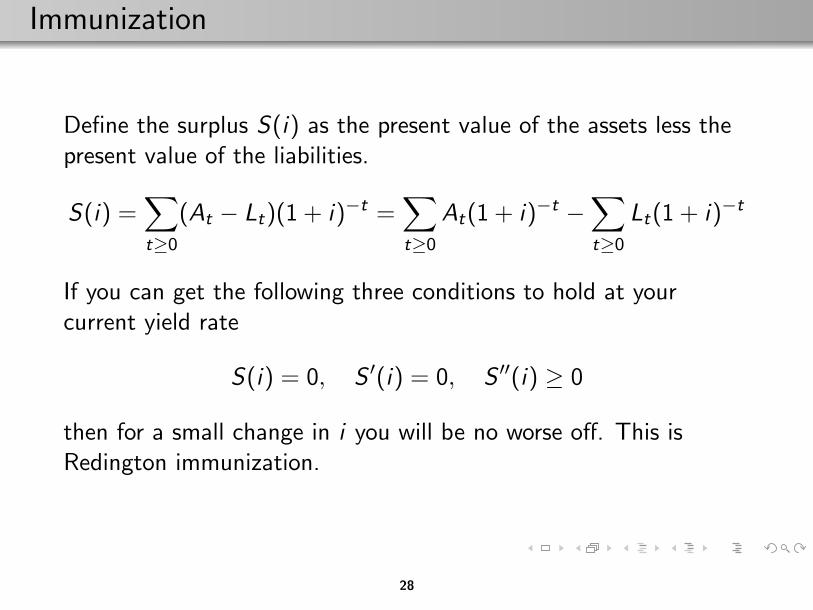

Immunization

Define the surplus S(i) as the present value of the assets less thepresent value of the liabilities.

S(i) =X

t�0

(At � Lt)(1 + i)�t =X

t�0

At(1 + i)�t �X

t�0

Lt(1 + i)�t

If you can get the following three conditions to hold at yourcurrent yield rate

S(i) = 0, S 0(i) = 0, S 00(i) � 0

then for a small change in i you will be no worse o↵. This isRedington immunization.

28

Full Immunization

While the Redington immunization prevents loss for small changesin the interest rate, under full immunization no change in theinterest rate will cause a decrease in price. If the following are true:

�0 is the current force of interest (i.e. no yield curve)

A single liability L is to be paid at time T

A pair of assets pay U and W at times T � u and T + w ,respectively (0 < u < T and w > 0).

The net present value S(�0) = 0 and the derivativeS 0(�0) = 0.

Then S(�) > 0 8 � 6= �0.

29

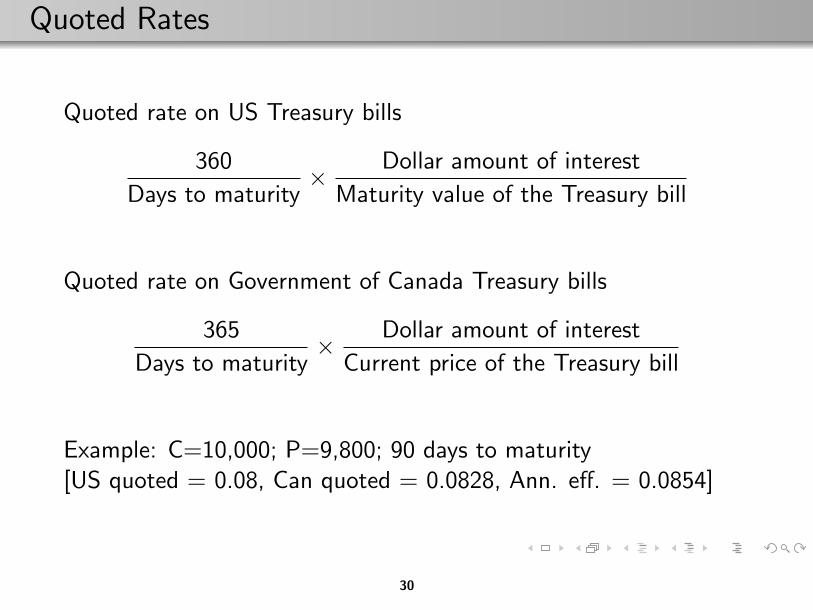

Quoted Rates

Quoted rate on US Treasury bills

360

Days to maturity⇥ Dollar amount of interest

Maturity value of the Treasury bill

Quoted rate on Government of Canada Treasury bills

365

Days to maturity⇥ Dollar amount of interest

Current price of the Treasury bill

Example: C=10,000; P=9,800; 90 days to maturity[US quoted = 0.08, Can quoted = 0.0828, Ann. e↵. = 0.0854]

30

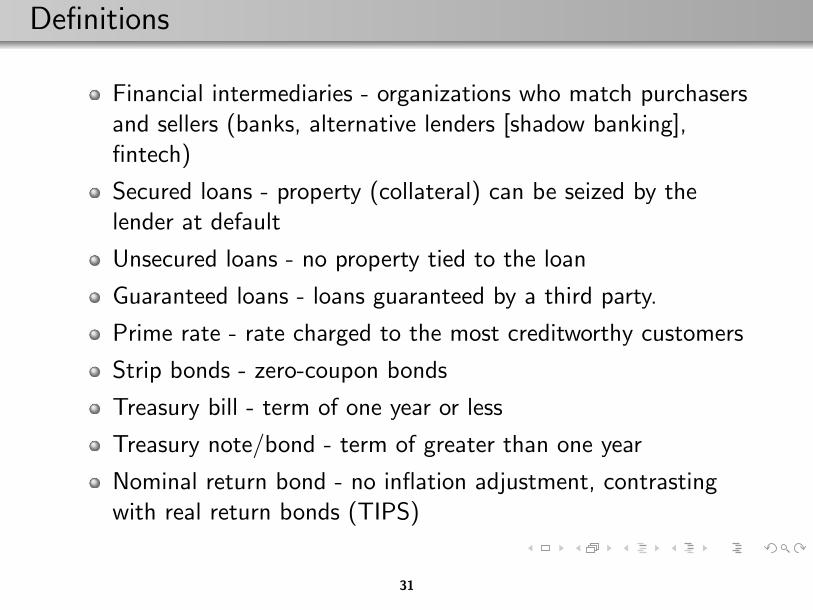

Definitions

Financial intermediaries - organizations who match purchasersand sellers (banks, alternative lenders [shadow banking],fintech)

Secured loans - property (collateral) can be seized by thelender at default

Unsecured loans - no property tied to the loan

Guaranteed loans - loans guaranteed by a third party.

Prime rate - rate charged to the most creditworthy customers

Strip bonds - zero-coupon bonds

Treasury bill - term of one year or less

Treasury note/bond - term of greater than one year

Nominal return bond - no inflation adjustment, contrastingwith real return bonds (TIPS)

31

Definitions continued

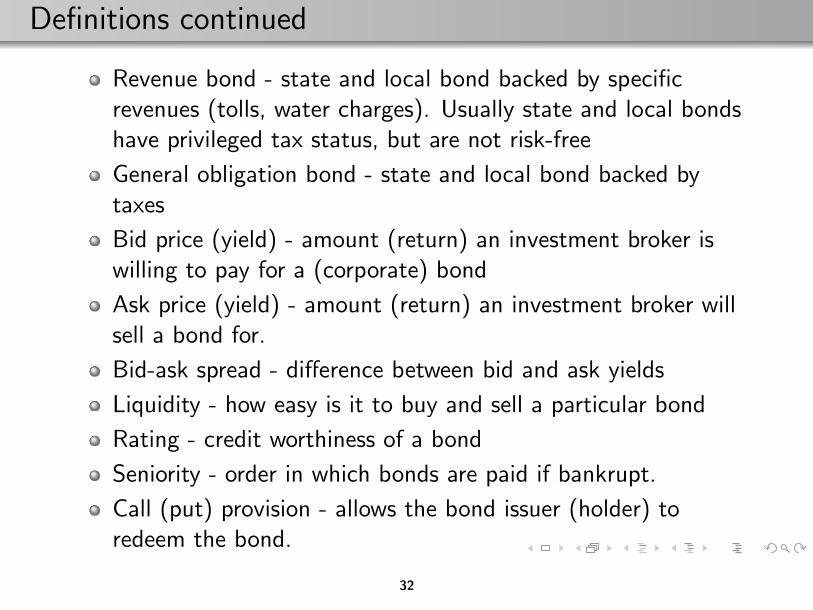

Revenue bond - state and local bond backed by specificrevenues (tolls, water charges). Usually state and local bondshave privileged tax status, but are not risk-free

General obligation bond - state and local bond backed bytaxes

Bid price (yield) - amount (return) an investment broker iswilling to pay for a (corporate) bond

Ask price (yield) - amount (return) an investment broker willsell a bond for.

Bid-ask spread - di↵erence between bid and ask yields

Liquidity - how easy is it to buy and sell a particular bond

Rating - credit worthiness of a bond

Seniority - order in which bonds are paid if bankrupt.

Call (put) provision - allows the bond issuer (holder) toredeem the bond.

32

Definitions continued

Roles of a central bankOperation of the payment systemLender of last resort

US Federal Reserve Bank System (sets monetary policy)Board of Governors12 regional banks - buys and sells treasuries to move thefederal funds rateFederal Open Market Committee (FOMC) - sets the targetfederal funds rateGoals - maximum employment, stable prices, and moderatelong-term interest rates

Federal funds rate - interest rate at which banks with excessreserve funds at their District’s Federal Reserve Bank lendthese funds to other banks

Discount rate - rate at which banks can borrow moneydirectly from the Fed.

33

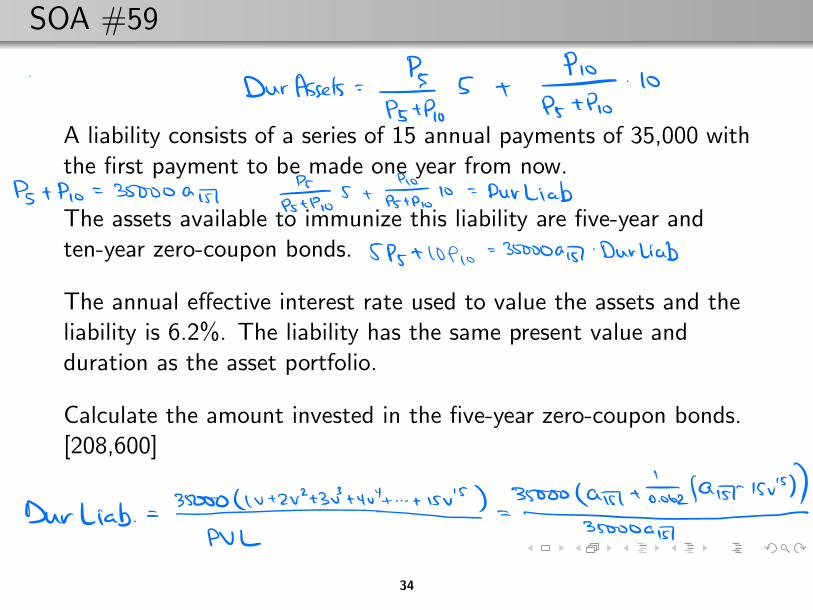

SOA #59

A liability consists of a series of 15 annual payments of 35,000 withthe first payment to be made one year from now.

The assets available to immunize this liability are five-year andten-year zero-coupon bonds.

The annual e↵ective interest rate used to value the assets and theliability is 6.2%. The liability has the same present value andduration as the asset portfolio.

Calculate the amount invested in the five-year zero-coupon bonds.[208,600]

34

SOA #69

An insurance company must pay liabilities of 99 at the end of oneyear, 102 at the end of two years and 100 at the end of three years.The only investments available to the company are the followingthree bonds. Bond A and Bond C are annual coupon bonds. BondB is a zero-coupon bond.

Maturity Yield-to-MaturityBond (in years) (Annualized) Coupon RateA 1 6% 7%B 2 7% 0%C 3 9% 5%

All three bonds have a par value of 100 and will be redeemed atpar. Calculate the number of units of Bond A that must bepurchased to match the liabilities exactly. [0.8807]

35

SOA #71

Aakash has a liability of 6000 due in four years. This liability willbe met with payments of A in two years and B in six years. Aakashis employing a full immunization strategy using an annual e↵ectiveinterest rate of 5%.

Calculate |A� B |. [586.41]

36

SOA #72

Jia Wen has a liability of 12,000 due in eight years. This liabilitywill be met with payments of 5000 in five years and B in 8 + byears. Jia Wen is employing a full immunization strategy using anannual e↵ective interest rate of 3%.

Calculate Bb . [2807.12]

37

SOA #73

Trevor has assets at time 2 of A and at time 9 of B. He has aliability of 95,000 at time 5. Trevor has achieved Redingtonimmunization in his portfolio using an annual e↵ective interest rateof 4%.

Calculate AB . [1.0132]

38