state life insurance

DESCRIPTION

State Life InsuranceTRANSCRIPT

86

We shall guide who strive in our cause to

the path leading to us. Surely ALLAH is

with those who do well.

(AL-ANKABUT).

DEPARTMENT OF MANAGEMENT SCIENCES IUB 1

86

DEDICATION.

Dedicated to my beloved country and

to the people who devoted their lives for

the freedom of this country.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 2

86

PREFACE.The contribution of the service to the Pakistani

economy is increasing at an extra ordinary rate and the

present financial services revolution looks certain to

reinforce that trend considerably. The context does not

claim to exhaustive and the balance must inevitably be

open to criticism, but in attempting to give a general

insight to the casual inquirer, the needs of those seeking

in-depth knowledge within particular areas must

inevitably be sacrificed.

This report covers a detail and analytical view of the

State Life Insurance Corporation. As the title that this

report is the essence of the hard working which I have

done during my internship tenure. This report has been

written in the hope that it will help anybody, who read it

carefully to obtain a real understanding of the basic

structures, functions and techniques of the different

departments of State Life Insurance Corporation. The

report is long and wordy.

I hope that the report is relatively free of errors and

will appreciate if errors are brought to attention.

UBAID-UR-RAHMAN.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 3

86

ACKNOWLEDGMENT.I thank all mighty ALLAH, the beneficent and the

merciful, who gave me a chance and enough power to

write this report. I want to express my gratitude and

thanks to the Zonal Head Mr. Tufail Ahmad Ch. , Mr.

Ishfaq Abbasi Deputy Manager PHS and specially Mr.

Imtiaz Ali for enabling me to devote part their precious

time in the presentation of this report. I feel it my

bounded duty to acknowledge with deep gratitude and

invaluable help extended to me by my respected teachers

and friends. I am especially grateful to Mr. Nazik Hussian

for his encouragement and guidance to complete this

report.

All the additional typing was elegantly effected

by Mr. Shoib Akbar, who showed considerable

cruptographical expertise, not to mention immense

patience, in making some sense out my untidy and much

annotated scripts.

To all these I can only say - Thank You. I hope that

the end product is not totally unworthy of the time and

efforts they most generously gave.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 4

86

UBAID-UR-RAHMAN.

Table of Contents

1- Company and it's Introduction.

2- Mission and Objectives.

3- Organizational Structure.

4- Divisions.

5- Departments.

6- File Movements.

7- Customer and Products.

8- Bonuses.

9- Supplementary Contracts.

10- Basic Salary and Grading.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 5

86

11- Calculations.

12- Marketing Channel.

13- Selling Process.

14- Managment Stretagies.

15- SWOT Analysis.

16- Competitors.

17- Ratio Analysis.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 6

86

INTODUCTOIN

Insurance.

Insurance Companies.

Insurance Evaluation.

Life Insurance in Pakistan.

State Life in Pakistan.

State Life in Bahawalpur.

INTRODUCTION

Insurance

Insurance means that the Probable loss occurring

in future can be so shared that the overall

impacted of total loss to any individual or section

of the society is mitigated.

Insurance can be of l i fe for the compensation in

case of normal or accidental death or of property

l ike car, bus ship, airplane, etc. in case of loss

caused by fire, f loods, earthquakes etc. insurance

provides compensation for the loss to a maximum

extent.

History of Insurance:

The need of sharing losses caused particularly by

sea peri ls was left several hundred-year ago. The

DEPARTMENT OF MANAGEMENT SCIENCES IUB 7

86

merchant ships remaining away for months with

valuable cargo carried with them the hope of

marketing profits upon their safe return. The

peri ls of the sea however, infl icting extensive

damage to the ships and the goods loaded on

them resulting in sometimes the total disaster

ultimately caused great concern to those involved

in the business. They consequently jointed hand

to the way out and thus insurance was found to be

the only possible means to save individual from

total disaster. This idea originated from China

and then developed by England and other

European countries. In the beginning merchants

used to sit together and for certain define

amounts, members used to sign documents

accepting their share of risk in the ships or cargo

carried. This initial arrangement finally developed

to highly skil led and most scientif ic ways for

assessment of risk and underwriting and sti l l

countries. The persons signing in acceptance of

their shares are called underwriters.

Life INSURANCE:

Life insurance is a contract whereby the insure

promises to pay, in exchange of certain premium,

the sum insured, on the completion of a definite

period, or on the death of the insured person.

There is a difference between l ife insurance and

other forms of insurance l ike fire insurance,

marine insurance automobile insurance etc.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 8

86

covering immediate financial and economic losses.

In l ife insurance, it is not easy to ascertain with

exactness the total impact l ikely to occur due to

the death of the person. The values placed on the

l ife for possible assessment of the financial

repercussions anticipated as a result of death,

nevertheless, are related to a great extant and as

possible workable solution for maintaining source

of income to a maximum possible extant. In short

when a man dies, not only he but either the entire

source of income dies if he is only responsible for

producing the income for the family or important

part of source of income for the family, for the

family, in such case l ife insurance takes over the

l iabil ity and the responsibil ity of meeting family

needs.

BENEFITS OF LIFE

INSURANCE

Finacial Protection

Necessary Saving

Property Building

Loan Facility

Eduction and Marriage plan

Income Tax rebate

Retirement Fund

DEPARTMENT OF MANAGEMENT SCIENCES IUB 9

86

STATUE UNDER WHICH CREATED:-

Life insurance (Nationalization) order, 1972 (Presidential Order X of 1972)

Date of incorporation : November 01, 1972

Legal status: Autonomous coporation under the control of the ministry of Commerce, Govt. of

Pakistan.

Principal Office: State Life Building No.9Dr. Ziauddin Road Karachi, Pakistan.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 10

86

MISSION OF STATE LIFE INSURANCE

CORPORATION

“To ensure satisfaction of our valued policy

holders in processing new business providing

after sales services and optimizing returns of l i fe

fund through quality culture and to maintain our

position at the leading l ife insurer in Pakistan.”

OBJECTIVES OF SLIC

Following are the objectives:

To run l ife insurance business in sound l ines,

To provide more efficient services to

policyholder,

To maximize the return to policyholders by

economizing on expenses and increasing the

yield on investment,

To make l ife insurance a more effective means

of mobil izing national savings,

To widen the area of operation of l i fe insurance

and making it available to as large a section of

the population as possible, extending into from

the comparatively more efficient sections of

society to the common man in town and

vil lages,

To use th3e policyholders funds in the wider

interest of the community.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 11

86

History of Life insurance In Pakistan:

Before partition, there were only three major

insurance companies named Christian Mutual,

Muslim and eastern Federal Union transacting l ife

insurance through their Head Office in the ears,

which ultimately formed Pakistan. The need for

having a composite insurance company

particularly for Muslims was felt by some of the

eminent Muslim personalities. And Eastern

Federal Union Insurance Company was established

in 1932 by the struggle of those Muslim

personalities. The Muslim Insurance Company of

Pakistan was established in 1949.

Before the nationalization of companies in 1972,

there was a big competition between companies

involved in l ife insurance business in Pakistan as

there were more than thirty companies offering

the insurance facil ity. Upon nationalization of l i fe

insurance business in 1972, State Life Insurance

Corporation was formed to take entire l iabil it ies

and assets as they related to l ife insurance

business. Starting with three units A,B and C, it

was soon merger into a single corporation. Now

including Bahawalpur Zone, there are thirty zone

of Stat Life Insurance Corporation are working in

different parts of the country with Head Office at

Karachi.

In Pak , l i fe insurance business was nationalized

by Govt., Order in March 19, 1972 and in fact this

DEPARTMENT OF MANAGEMENT SCIENCES IUB 12

86

was an important step toward economic

development in the history of Pak.

The nationalized process was completed in two

phases. In f irst phase (March 19, 1972), the Govt.

has taken over the administration of 32

companies. After this, these were handed over to

trustee and sub-trustee in accordance to l ife

insurance nationalization order 1972.

In the second phase of nationalization (November

1, 1972) a single corporation, having three units,

came into existence by the name of State Life

Insurance Corporation (SLIC) of Pakistan.

These three units, constituted by merging of one

or more insurance companies, were named as A,B

and C units. For further improvement of the l ife

business in Pak, these units (A,B & C) were

merged together and converted into zones.

SLIC has enjoyed a complete monopoly the l ife

business ti l l 1990 when the Govt, had decided to

open it to local private sector insurers. At present

, besides SLIC, there are four other l ife insurers

operating in the country including two foreign

companies. The state Life Insurance Corporation

is reinsured by foreign insurance “Swiss RE”

(Switzerland).

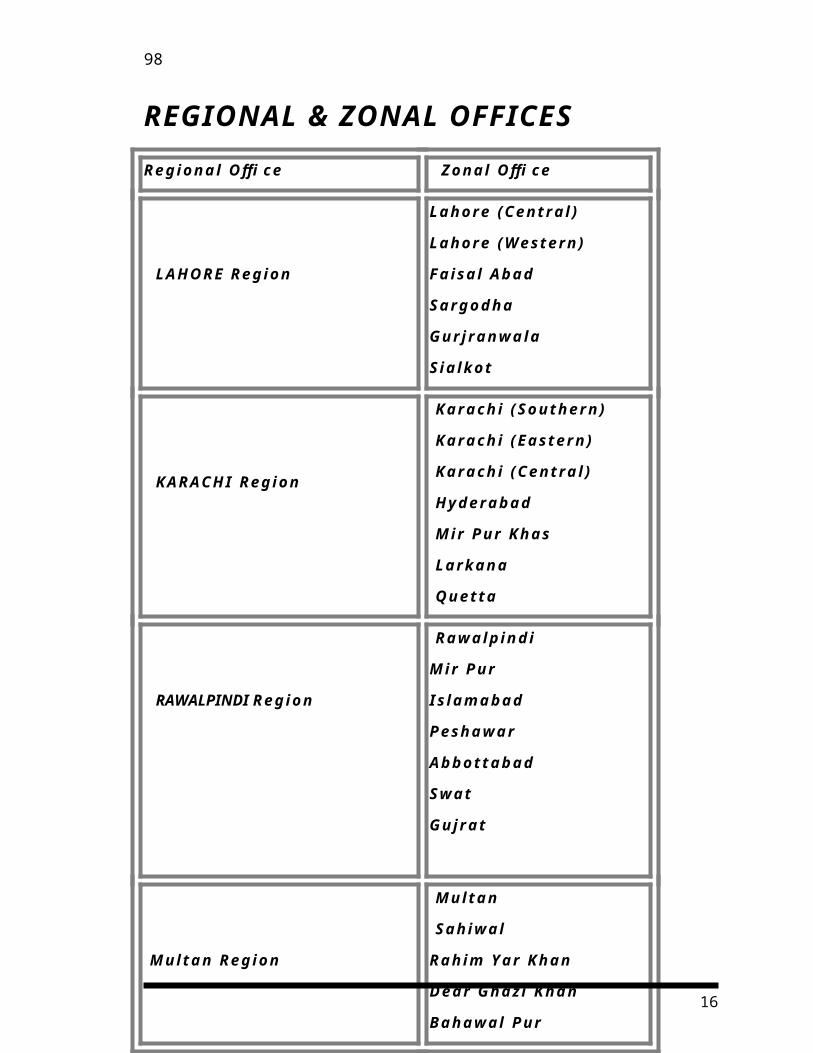

REGIONAL & ZONAL OFFICES

DEPARTMENT OF MANAGEMENT SCIENCES IUB 13

86

REGIONAL & ZONAL OFFICESDEPARMENTS:-

DEPARTMENT OF MANAGEMENT SCIENCES IUB

Regional Off ice Zonal Off ice

LAHORE Region

Lahore (Central)

Lahore (Western)

Faisal Abad

Sargodha

Gurjranwala

Sialkot

KARACHI Region

Karachi (Southern)

Karachi (Eastern)

Karachi (Central)

Hyderabad

Mir Pur Khas

Larkana

Quetta

RAWALPINDI Region

Rawalpindi

Mir Pur

Islamabad

Peshawar

Abbottabad

Swat

Gujrat

Multan Region

Multan

Sahiwal

Rahim Yar Khan

Dear Ghazi Khan

Bahawal Pur

14

86

1- Agency Adminstration Department.2- Human Resources Devolpment Department.3- New Buisness Department.4- Policy Holder Service Department.5- Budget and Accuonts Department.6- Personal and General Services Department.7- Marketing Department. 8- Audit Department.

NEW BUSINESS DEPARTMENT

New Business (NB) is considered the soul of

Insurance companies. Profitabil ity and

survival of the business depends on the NB.

FUNCTION OF NEW BUSINESS

In this department, as the name shows, new

contracts start between proposes and

Insurance Company. Proposes is a person who

applies for the insurance protection.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 15

86

Main function of the NB is underwriting.

This department is responsible for processing

the new business introduced by the sales

force right from receiving a proposal on the

counter to mail ing the policy document to the

policyholder. It has various section to

perform the different task relating to the

acceptance or rejection of risks for l ife

insurance, the proposal are received and

initial ly is checked in al l respects i .e.

completion of al columns and then processed

by the underwriters depending upon whether

they have been introduced under the medical

or non-medical scheme. The risk is assessed

keeping in view the following factors:

Personal data, occupation, physical

and social features, health, family

history of the prospect.

Moral hazard, source of income,

nomination, relationship between the

nominee and the prospect.

Previous l ife insurance history of the

prospect if any.

Field officer’s or sale representatives

confidential report included in the

proposal form.

Financial underwriting i .e. source of

income, its legality and proof,

relationship between the prospect’s

income and sum assure.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 16

86

In case of non-medical scheme, the prospects

own statement and fi led officers or sales

representative’s reports have more importance.

After this assessment, the underwriting decision

is made which may be acceptance of a risk at

ordinary rated or with loading, call ing additional

evidences relating to health or f inancial status of

the prospecting for a define periods or straight

way declination. Premium rates, installments are

then checked and first premium receipts are

issued to the field force, and concerned

department l ike commission payments, agency

administration, computer division and marketing.

This is brief terms are the function on the new

business department. This is also a key function

as the underwriters are responsible for the

financial health of the l ife institution. By

accepting god risks they promote profitabil ity and

growth which help in meeting the financial

obligations of the l ife institution towards the

policyholders, its employees and the government.

WORKING OF NEW BUSINESS

The precise working of NB department is as

fol lows:

PROPOSAL NUMBER

In order to fulf i l l the recognition of the

insurance policy, NB department al locates a

number t each insurance policy for future

DEPARTMENT OF MANAGEMENT SCIENCES IUB 17

86

references. NB department verif ies whether

the cl ient is a new customer or a past

customer.

UNDERWRITING

Underwriting is the process through which the

underwriter assesses the risk associated with

the Insurance Proposal. Underwriter verif ies

the personal information provided in the

Proposal form (See annex. No.1). If he feels

that cl ient should have a medical checkup

then SLIC has its own penal of doctors to

provide medical assistance.

PREMIUM CALCULATION

After underwriting the premium of Sum

Assured is calculated in Policy Brief Sheet

(see annex No.2) in according with the rate

book provided by the SLIC. The policy fee is

charged of Rs. 100 or Rs 2.5 per thousands of

sum assured whichever is less. Further the

rates of supplementary contracts are added in

premium.

POLICY ISSUE SECTION

After premium calculation the insurance and

revenue stamps are embossed on the policy

bond and the policy d documents is sent to

cl ient (See annex No.3) one copy of policy

document is sent of (PHS) department of

record purpose.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 18

86

UNDERWRITING GUIDELINES

Taking of Authentic Age Proof

Verification on Nominee Relation with

Policyholder

Analyzing of health and financial status

of Prosper.

Verification of stated information on

Proposal Form.

Requirement of Medical Reports and

Tests.

Analyses of Medical Reports and Tests.

Analysis of health history and family

background.

Others requirements.

BUDGET & ACCOUNTS

DEPARTMENT

This department deals in:

Cash Collection

Cash Disbursement

Salary Preparation

Budget Preparation

Inter-Zone Transaction

Agents Commission

Imprest

DEPARTMENT OF MANAGEMENT SCIENCES IUB 19

86

CASH COLLECTION:

There are two mode of cash collection i.e., by Cash and by

Cheque. The collection is made for II Renewal Premium and I

.The premium is paid by cash in SLIC, and it is also paid by

cheque. These cheques are sent to the department. These

cheques are attached along with “ daily collection sheet”

(DCS) with full detail i.e. Banker’s name, location, date of

issue etc. and this sheet is sent to the SLIC’s authorized

bank (UBL) in Bahawalpur for collection.

CASH DISBURSEMENT:

For cash disbursement, f irst the voucher is

prepared, singed and prepared by authorized

officer, for the person to whom the payment is

made. This voucher is audited in case of having

the amount in excess of Rs.10000. these voucher

are punched (feeding) in computer. Voucher

l istings are maintained, cheques are prepared,

and these cheques are sent to concerned party.

Bank Statement is prepared by daily the

authorized bankers regarding total coactions and

payments of cheques i .e. realization of cheques.

These banks Statements are punched into the

computer. The data in f loppy regarding Cash Book

and Bank Statement is sent to Principle Office

(PO) Karachi. Different lodgers are prepared in

P.O and these are sent to SLIC Bahawalpur Zone

for further reconcil iation. Errors and commissions

are corrected.

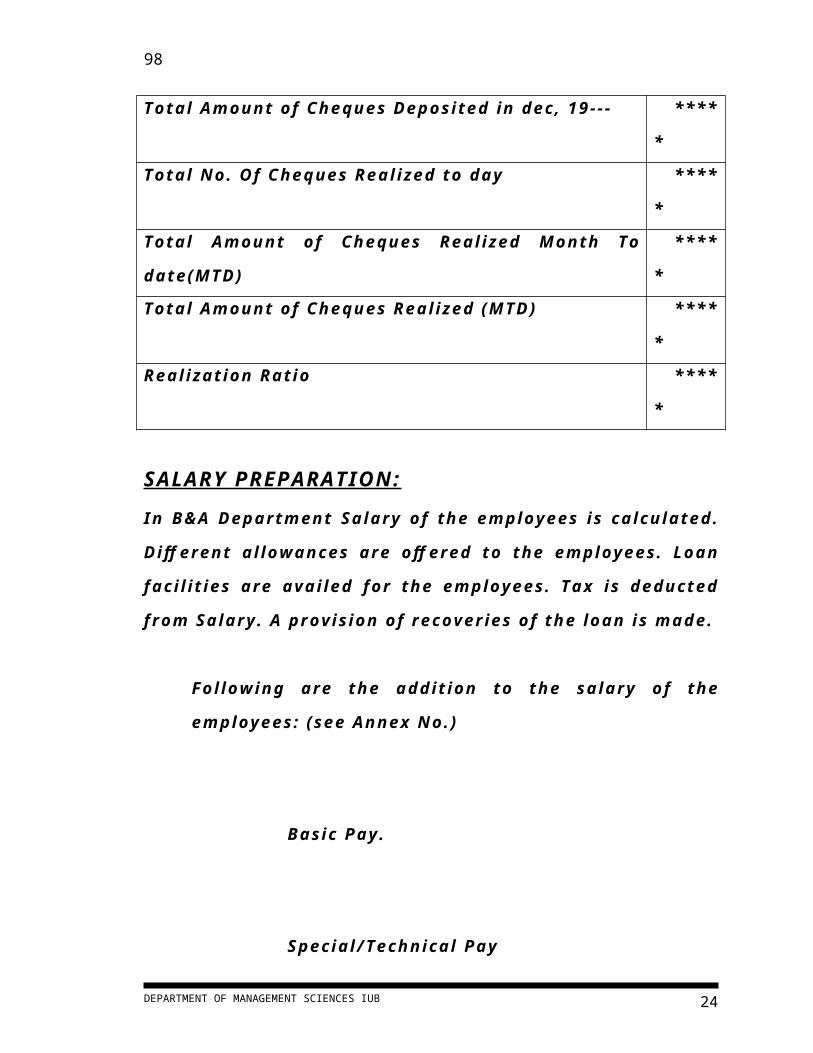

Following l ist are prepared by this section:

DEPARTMENT OF MANAGEMENT SCIENCES IUB 20

86

Data Wise Total List of Cheques

Encased.

List of Cheques Issued (Cash

Book)

List of Unmatched Cheques of

Bank & Cash Book Files.

Along with the above mentioned l ists, a “Daily

Cheques Realization Report” is prepared in the

following manner:

Total No. Of Cheques Deposited in Dec. 19

—

****

*

Total Amount of Cheques Deposited in dec,

19---

****

*

Total No. Of Cheques Realized to day ****

*

Total Amount of Cheques Realized Month

To date(MTD)

****

*

Total Amount of Cheques Realized (MTD) ****

*

Realization Ratio ****

*

DEPARTMENT OF MANAGEMENT SCIENCES IUB 21

86

SALARY PREPARATION:

In B&A Department Salary of the employees is

calculated. Different al lowances are offered to

the employees. Loan facil it ies are availed for the

employees. Tax is deducted from Salary. A

provision of recoveries of the loan is made.

Following are the addition to the salary of the

employees: (see Annex No.)

Basic Pay.

Special/Technical Pay

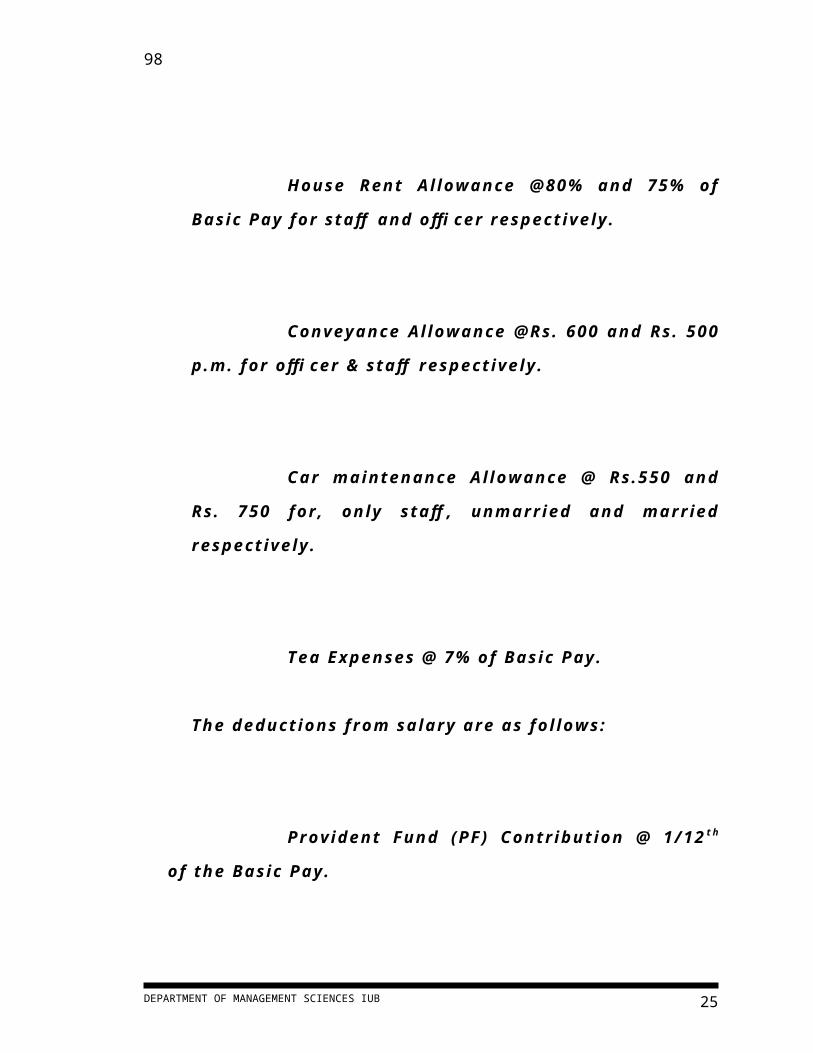

House Rent Allowance @80% and 75%

of Basic Pay for staff and officer respectively.

Conveyance Allowance @Rs. 600 and

Rs. 500 p.m. for officer & staff respectively.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 22

86

Car maintenance Allowance @ Rs.550

and Rs. 750 for, only staff, unmarried and

married respectively.

Tea Expenses @ 7% of Basic Pay.

The deductions from salary are as fol lows:

Provident Fund (PF) Contribution @

1/12 t h of the Basic Pay.

Union Subscription @ Rs. 50 and Rs.

30 for officer & staff respectively.

Salary Advance Repayment (24

monthly installments).

DEPARTMENT OF MANAGEMENT SCIENCES IUB 23

86

PF Loan Installement-2 (50 monthly

installments).

Pf Loan Installement-1 (26 monthly

installments).

Convince Loan Recovery (40 monthly

installments).

House Building Loan Installments.

House Rent Installment (18 monthly

installments).

Following are the different types of loans,

which can be availed by employees of SLIC

managed by salary section:

Two-Month Advance Salary.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 24

86

Loan-I against PF (3 Basic Pay).

Loan-2 against PF (12 Basic Pay or

90% of Pf employee own contribution,

whichever is less).

Conveyance Loan @ Rs. 55000 and Rs.

150000 for staff & officer respectively.

House Building Loan.

After preparation of salary payable (Additional &

Deduction) the data is purchased (feeding) into

the computer database. Different types of l ists

are prepared such as total loan payment,

al lowances etc.

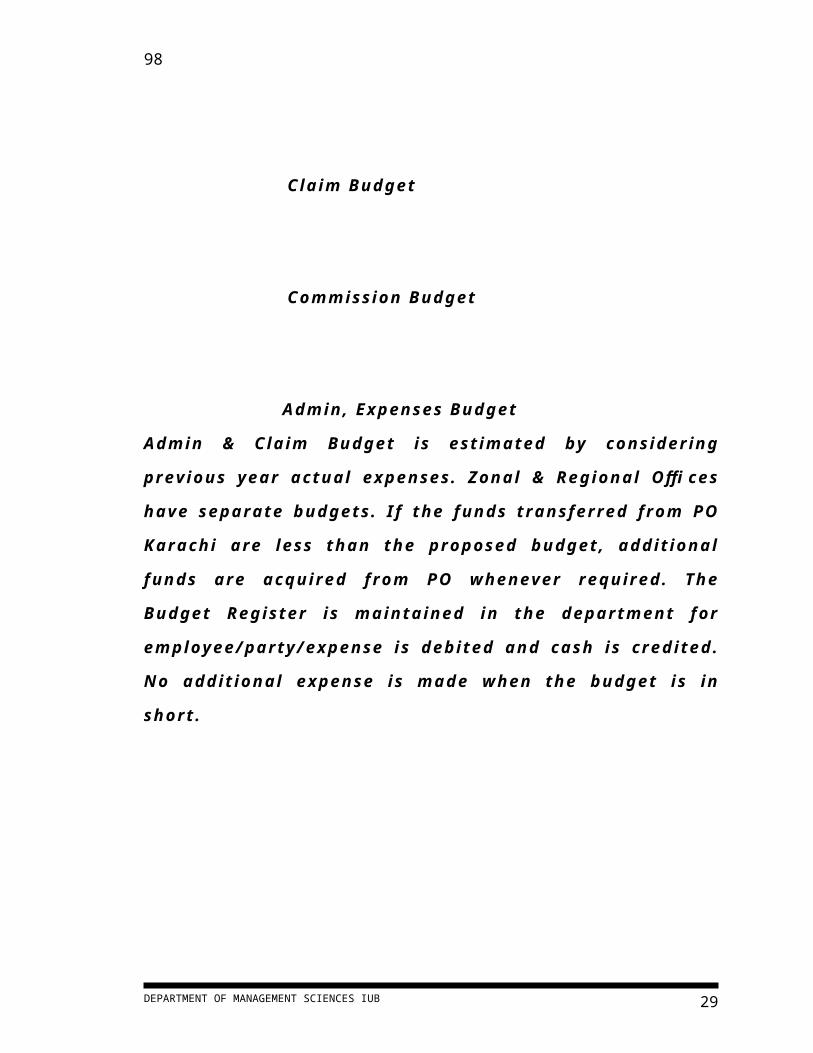

BUDGET PREPARATION:

DEPARTMENT OF MANAGEMENT SCIENCES IUB 25

86

Budget is prepared annually. Proposed Budget is

sent to PO. The funds of different heads of

proposed budget are transferred to Zonal Office

Bahawalpur wholly or partial ly. It is assumed that

each year First Year Premium (FYP) is increased

by 25%. According to this base the commission of

the agents are calculated and budgeted.

Following are the main types of budget:

Income Budget

Claim Budget

Commission Budget

Admin, Expenses Budget

Admin & Claim Budget is estimated by considering

previous year actual expenses. Zonal & Regional

Offices have separate budgets. If the funds

transferred from PO Karachi are less than the

proposed budget, additional funds are acquired

from PO whenever required. The Budget Register

DEPARTMENT OF MANAGEMENT SCIENCES IUB 26

86

is maintained in the department for

employee/party/expense is debited and cash is

credited. No additional expense is made when the

budget is in short.

INTER-ZONE TRANSACTION :

There is separate section for inter-zone

transaction in budget and accounts. Whenever any

expense is made on behalf of any other zone, the

debit note is issued to the concerned zone for

that expense. Similarly, other zone can issue

debit note to Bahawalpur Zone is they have

occurred the expenses on behalf of Bahawalpur

Zone.

The expense incurred on behalf of other zone can

be claimed, salary, TA/DA, claim investigation

expense, uti l ity, Meeting expense, entertainment,

repair & maintenance, rent, Medical expense etc.

COMMISSION SECTION:-

In B&A Department, the commission Section

calculates the commission. First Premium Receipt

(FPR) is prepared by the New Business

DEPARTMENT OF MANAGEMENT SCIENCES IUB

Employee

Grade

Loan % age Rate

(interest)

1,2,3 Rs. 150000 6

4 to 7 Rs. 200000 6

7 & onward Rs. 2155000 (or

30 Basic Pay

whichever is

high)

10

27

86

Department is sent to Commission Section to

calculate the commission of agent. It has four

copies, one for commission section and other

three for agents (SR,SO,SM).

The commission rates vary with the amount of FYP

and term of the policy. The Mode Bonus is given

to SR if the premium installment is annually,

@1.5% of FYP. All ied Bonus is given to SO,SR

@4.35% of FYP P.A., paid by monthly if they

have 72% of I I year persistency, 90% renewal

persistency, 10 SRS and last year FYP of

Rs.120000 and Rs.150000 respectively. Production

Bonus is given SR,SO & SM if they have last year

FYP of Rs.6000,Rs.15000, Rs.50000 respectively

and have minimum 70% of I I year persistency.

Further the tax is deducted @10% of commission

from the commission of agents. In commission

section different types of loans are given on

fulf i l lment of certain requirements and targets to

agent i .e. Emergency Advance, Eid Advance,

Conveyance Loan, House Building Loan.

COMMISSION RATES

DEPARTMENT OF MANAGEMENT SCIENCES IUB 28

86

DEPARTMENT OF MANAGEMENT SCIENCES IUB

F i r s t Y e a r R a t e

F o r S a l e s

R e p r e s e n t a t i v e

P r e m i u m T e r m ( Y e a r )

P r o d .

B o n u s

1 4 - O c t 1 5 - 1 9

2 0

A b o v e

R s . 1 - 3 9 9 9 2 5 % 3 0 % 3 5 % - -

4 0 0 0 - 5 9 9 9 2 5 % 3 0 % 3 5 % 2 . 0 0

6 0 0 0 - 7 9 9 9 2 5 % 3 0 % 3 5 % 2 . 5 0

8 0 0 0 - 9 9 9 9 2 5 % 3 0 % 3 5 % 3 . 0

1 0 0 0 0 a b o v e 2 5 % 3 0 % 3 5 % 3 . 5

F O R S A L E S O F F I C E R

P r e m i u m T e r m ( Y e a r )

1 0 T o 1 4 1 5 - 1 9

2 0

A b o v e

1 - 1 9 9 9 9 1 3 . 1 3 % 1 4 . 8 8 % 1 7 . 5 0 %

2 0 0 0 0 - 3 4 9 9 9 1 5 1 7 2 0

3 5 0 0 0 - 4 9 9 9 9 1 6 . 8 8 1 9 . 1 2 2 2 . 5

5 0 0 0 0 - 7 4 9 9 9 1 8 . 7 5 2 1 . 2 5 2 5

7 5 0 0 0 - a b o v e 1 9 . 5 2 2 . 1 2 6

F O R S A L E S M A N A G E R

P r e m i u m T e r m ( Y e a r )

1 0 T o 1 4 1 5 - 1 9

2 0

A b o v e

1 - 4 9 9 9 9 4 . 5 0 % 5 . 1 0 % 6 . 0 0 %

5 0 0 0 0 - 9 9 9 9 9 6 6 . 8 8

1 0 0 0 0 0 - 1 4 9 0 0 0 0 7 . 5 8 . 5 1 0

1 5 0 0 0 0 - 1 9 9 9 9 9 8 . 2 5 9 . 3 5 1 1

2 0 0 0 0 0 - a b o v e 9 1 0 . 2 1 2

S E C O N D & O N W A R D Y E A R S R A T E S

F O R S A L E S M A N A G E R

S R S O S M

I I Y e a r 1 0 . 0 0 % 2 . 0 0 % 1 . 0 0 %

O n w a r d 5 1 0 . 5 0 %

29

86

COMMISSION PAYMENT PROCEDURE :-

Following are three methods used by SLIC for

payment of commission to agents:

Payment by cheques

Authority Card.

Payment by Post.

In first method, the payment is directly made to

the agent by cheques. In the second method, the

payment is made to other person authorized by

agent by signing the “Authorized Card” (See

Annex NO0.5) in the third method the

commission is paid by post to his postal address

on his direction.

PRIZE AND AWARD:-

The prize and award are given to field force who

are achieved the highest FYP at any time

announced by SLIC.

EMERGENCY ADVANCE:-

It is given to SO,SM on the previous year

earning on the renewal premium. For SR

previous 2 year earning become entitlement of

loan.

EID ADVANCE:-

Previous year total earning of SR,SO and SM

becomes entitlement.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 30

86

CONVEYANCE LOAN:

It is given to SO,SM only on the condition of

having 5 year service association with SLIC and

two guarantors. The loan can be taken up

Rs.40000.

HOUSE BUILDING LOAN:

To obtain to this loan minimum association with

SLIC is 15 years and pervious year renewal

premium becomes entitlement.

IMPREST SECTION:

Imprest is the additional privileges given to the

employees (Area Managers). Annually, the

Imprest Entitlement is made for the AM by

considering the previous progress in the

business. Different Circulars arrive from PO to

Bahawalpur Zone mentioning the different type

of privileges on different FYP targets. These

privileges are free petrol, telephone, electricity,

clerk wage,

stationary and other facil it ies etc.

POLICY HOLDER SERVICE DEPARTMENT

PHS is the abbivation of "Policy Holder's Service" department. As the name indicating that all the services for policy holder are performed here. We can also call

DEPARTMENT OF MANAGEMENT SCIENCES IUB 31

86

these services, after sale sevices. It is the most busy department of SLIC in each zone. Every service process was taken very carefully in the last conference of SLIC. It was announced that every service would be completed within 15 days. Otherwise State Life pays restriction plenty to the policy holder. The head of PHS is also sitting in P.O, Karachi. His post is G.M, then each region contains D.G.M lastly the head of PHS deptt. in each zone is deputy manager.

Followings are the functions performed in PHS deptt.DEATH CLAIM

When a person dies, his relatives or heirs tell SLIC agent or directly to the zonal office. SLIC demands certain documents like1. Application for disease.2- NIC.3- Disease and nominators are attested.4- Death certificate from union council.5- Original documents (ORs).

Firstly deptt. manager or his colligue is appointed for the investigation of this case. He also checks FIR from the nearest Thana. If case is clear, then SLIC tries his best to give claim as soon as possible.

In case of accident, same process and way of investigation is performed. The place of investigation is also checked by the investigators seriously.SURRENDER

Another service of this deptt. is surrendering. If a policy holder wants to finish his policy due his cumpolsary need of money. Then he has two options. Firstly, he can take loan, from his own property. After requirement's completion he pays 13% interest and continues his policy. Secondly, if his need is not fulfilled with this amount then he can surrender his policy. But he can't gain all his amount because he is breaking the contract.

Followings are the required documents.1- Application.2- NIC & attestation.3- Original receipts.

After all these completions surrender value is based on your cash value.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 32

86

ALTERATIONWhen policy holder wants some changing in his term,

sum assured then this changing is called Alteration of policy.

e.g. A policy holder has a policy of sum assured 2,00,000 and he is not satisfied to this. He wants to increase it. This is called Alteration.

TERM CHANGING – A policy contains 20 years to be matured, but policy

holder wants to decrease it. He thinks that after 15 years he would need this amount. This is another type of Alteration.

Followings are the requirements for Alteration.1- Original receipts.2- Alteration fee = 25 Rs.3- Alteration performa.4- Form.5- Application.6- I.D. card.NOMINATION CHANGE

3rd kind of alteration is nomination change. First a policy holder nominated his wife but after some time he gave divorce to her wife and now he wants another person for nomination. FILE TRANSFER

If your policy record is in Multan zone and now you are in Bahawalpur. Then you can tranfer here by application.MATURITY CLAIM

When a policy goes to its maturity, it means that its term is completed. SLIC sends a letter to its policy holder.If documents, original receipts, all premiums are right, then a healthy amount with bonuses goes to policy holder's account. Otherwise if you had taken loan and could not return 13% interest and having certain cash value in your policy, then this loan plus interest of that period would be deducted. All maturity claims goes to your account.LOANING

Other facility of SLIC is loaning. You can get loan from your account. Most of the people are allowed 70% loan from their own accounts. In case of serious need 80%

DEPARTMENT OF MANAGEMENT SCIENCES IUB 33

86

is allowed to be taken as loan. But with an emergency case and with the help of an authority you would be awarded 90%.

But it is beneficial for policy holders to take a minimum loan from their account. e.g - if you take 70% loan, then 30% will remain in your account and its cash value will remain take it inforce for more time. If you take 90% loan, then only 10% will remain in your account and it will cover less time to take policy inforced.

No deduction of Zakat from death claim. While Zakat is charged from both surrender and maturity claim.REVIVAL

Charging of late fee or extra fee is called Revival, if

the given premium date has been passed. Then till 30

days there is no extra fee, because these 30 days period

is called grace period. Then from 30 to 90 days when you

go to submit premium without late fee, then it may be

demande "DGH" (Declaration of Good Health) by the head

of this department. But from 90 days late fee will start. At

this time PS (Personal Statement) can also be demanded.

These all are the benefits of suspense accounts. But the

loss of suspense account is, party will never get the claim.

Because it is non-credit in account. Another term is

Special Revival, which means if you have forgotted your

policy after paying at least two premiums and then within

5 years it remains inforce, then policy holder has the

chance to renew it, e.g., he is unable to pay the remaining

premiums plus their late fee. Then he can renew it by the

starting of runnig year. In other words if you got your

policy in 97, then now it will skip to 2002.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 34

86

CONSTITUTION OF CLAIM COMMITTEE

The claims committee of principal office for taking

decisions on all the death & injured claims refers to the

principal office is reconstituted as follows.

1:- D.G.M (PHS) P.O. Conveyor.

2:- Manager (PHS) P.O Secretary.

3:- Manager (PHS) P.O Member.

4:- Manager (Oversees) Member.

5:- Manager (C&P) Division. Member.

PERSONAL & GENERAL SERVICE

DEPARTMENT (P&GS) The office & general matters are dealt in P&G

Department. This department has the sole

responsibil ity and authority of the disciplinary

action of the employees. Selection, recruitment,

termination of the employees is the main

functions of the P&G Department. This

department also deals in medical faci l ity to the

office employees, leaves and similar other general

services. The daily correspondence is dispatched

in this department. Following are the main section

of this department:

MEDICAL SECTION :

All this hospitalization expenses are beard by

SLIC provided that these are incurred in approved

DEPARTMENT OF MANAGEMENT SCIENCES IUB 35

86

hospital. The expenses of medicine are

reimbursed. The reimbursement of medicine is not

al lowed to staff (having grade 1 to18) but they

are given Rs.600 p.a. in shape of salary as

medical al lowance.

RENT SECTION:

When sale Manager (SM) is promoted to Area

Manager (AM),he is categorized as A,B,C and he

has entitle to have his own office at his choice at

the expense of SLIC. A good location is selected

by the A.M. after selection of place, Zonal Head is

informed about the location, by application

written by A.M. this application is transferred to

P&GS Department for the analysis of location of

the office. The Zonal Rent Committee (ZRC)

annualizes this location. A lease agreement is

made with the landlord after analyzing the

approved map for the location and property

registration form.

The office rent entitlement for the categories of

A,B,C of Am is Rs.2000, Rs.2000, & Rs.1000 P.M

respectively.

CAPITAL SECTION:

This section responsible for purchase, sale and

maintenance of furniture & fixture, equipment

etc. a Zonal Procurement Committee (ZPC) is

constituted for the purchase of assets. The assets

are purchased from the suitable supplier after

DEPARTMENT OF MANAGEMENT SCIENCES IUB 36

86

critically analyzing the quotation offered by

different venders.

Each year assets are depreciated @10% p.a. the

entry for the purchased assets is made in the

Register for Fixed Assets. Each ear the closing

balance is intimated to PO Karachi.

STATIONARY SECTION:

This section maintains the record of stationary

such as paper, pencil , envelops, printed letters,

form, calculators, dustbin, etc. whenever any

department requires the stationary, the

concerned department fi l ls a Requisition Slip. The

stationary is issued to the concerned department

and it is recorded in the register.

LEAVE SECTION:

Following are the main two types of leaves:

Casual Leave

Medical Leave

20 days casual leaves are allowed to al l

employees in a year. The medical leave or

application leave is al lowed for 48 days in a year.

Unused leaves are accumulated and after two

years these leaves in excess of 180 das can be

encased. In case of death all leaves, not uti l ized,

can be encased.

PERSONAL SECTION:

All the employee matter such as appointed,

promotion, demotion, transfer and allowances are

dealt by personal section. Annual Confidential

DEPARTMENT OF MANAGEMENT SCIENCES IUB 37

86

Report-ACR (see annex N. 10 for ACR) the

employees are prepared, under the supervision of

this section, by the departmental heads.

For the appointment of the staff, an

advertisement is initiated in the Newspaper.

Zonal Head is computer authority for this

appointment of officers is done by Principle office

(PO) Karachi or Regional Office. Selection

Committee constituted by Zonal Head conducts a

test and interview.

For promotion of the employees, there ACR’s are

necessary and minimum three years are required

to remain in one cadre. Each year he employees

are promoted by the criteria and instructions set

by PO Karachi. PO or Regional Office does

promotion of officers.

AGENCY DEPARTMENT Service provided by the SLIC is intangibles

and therefore are not acquired at the counter by

the people, who need it, so it must be sold them

through persuasive method. Field force of SLIC

plays an effective role in sell ing of tangibles

products (Insurance Plans). In order to maintain

the record of the field force agency department

was established. The main function of this

department includes recruitment, promotion, and

termination of the field force, al l ied and medical

faci l ity for f ield force. This department is also

DEPARTMENT OF MANAGEMENT SCIENCES IUB 38

86

responsible for insurance and renewal of l icense

to the field force.

RECRUITMENT:

The Sales Representative (SR) is appointed by

SO/SM. The requirement and conditions for the

appointment of SR is as fol lows:

Minimum qualif ication is required metric.

Age at entry must be than 18 years.

Annual quota for SR is Rs. 10000.

Application for the insurance of l icense is

necessary and it is renewed after each 3

years.

An application Form, along with l icense fee Rs.

50, attested photocopies of documents and

Nomination Form is submitted to the agency

department. A code number is al lotted at the

submission of application to SR and he can start

working as agent of the SLIC of Pakistan.

PROMOTION:

SR is promoted, upon fulfi l lment of certain term

and condition and on achievement of business

targets, to SO. Similarly SO is promoted to SM

and SM to A.M. fol lowing is the criteria:

FROM SR TO SM:

Two years working as SR:

Must have secured minimum Rs. 75000 FY

during immediate preceding two years,

but in any one calendar year, the FYP

should be less than Rs. 25000.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 39

86

Must have at least 20 policies in force on

different l ives.

Must have a achieved a minimum Second

Year Persistency of 70% in the immediate

preceding year.

Must have achieved a minimum Renewal

Persistency of 90% in the immediate

proceeding year.

FROM SO TO SM:

Must have working of minimum 2 years

as SO.

Mush have secured minimum Rs.250000

FYP in the immediate proceeding two

calendar years, but the FYP in any one

calendar year must not be less than

Rs.60000.

Must have at least 80 policies in force

in his/her organization;

Must have minimum Second Year

Persistency of 70% in the immediate

proceeding Year;

Must have minimum renewal

persistency of 90% in the immediate

proceeding year;

Must have minimum 4 productive SR.

FROM SM TO AM:

Must have working at least for 3 years

as SM;

DEPARTMENT OF MANAGEMENT SCIENCES IUB 40

86

Must have secured the following total

FYP for category A&B:

A= Rs.45,00,000

B= Rs.36,00,000

And last year FYP must not be than:

A= Rs. 20,00,000

B= Rs. 15,00,000

Number of policies in the last year must

not be less than:

A= Rs.200

B= Rs. 150

Must have minimum Second Year

Persistency of 70% in the immediate

proceeding year and minimum second

year persistency of 65% of the previous

year of the immediate preceding year;

Minimum 2 SO should be qualif ied to

sum;

Annual quota must have:

A= Rs. 30,00,000

B= Rs.18,00,000

TERMINATION & DEMOTION:

Any agent of SLIC, who behave negatively,

violates the rules & regulation or indulge fraud or

mal-practice, can be termination by the Zonal

Head. Any agent who fails to meet the annual

quota of FYP is demoted to immediate lower rank

of the field force.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 41

86

LICENSE:

The l icense to work as agent for SLIC is issued by

the Controller of Insurance Karachi. At specific of

t ime, a l ist of the field force is transferred to

controller of Insurance Karachi for new and

renewal of l icense. The l ist of l icense fee is given

below:

SR (New License for

Ist Year)

Rs. 59

SR (Renewal of

License)

Rs. 70

SR (Renewal with

late fee)

Rs.

125

SR/SM (Renewal of

License)

Rs.15

0

SO/SM (Renewal with

late fee)

Rs.20

0

List of Field Force in Bahawalpur Zone

Field Cadre No. Agent

SR 571

SO 189

SM 73

AM 11

DEPARTMENT OF MANAGEMENT SCIENCES IUB 42

86

HRD DEPARTMENTHRD is the abrevation of " Human Resource

Devolpment ". This dept. trained the field force to inhance

the people. It teaches throughout the Marketing channel

with their special courses.

Followings are the courses for field forces, because

this team is a front line of SLIC.

Courses Marketing

BTC ISR

BTC SO

ADP ISR

MOP SM , AM

MOSL SO , SM

MMS AM,SM

I have attended the BTC course. Following is the

detail.

Training and courses give the following benfits:-

1:- Professionality.

2:- Service Upgrading.

3:- Liklihood habits.

4:- Planning.

Target attaining:-

Time.

Income.

Place.

Following things are the key terms for a

marketor. Before going into a market.

ACTION

DEPARTMENT OF MANAGEMENT SCIENCES IUB 43

86

A = Active. C = Confidence. T =

Thankful.

I = Intelligent. O = Organized. N =

Noble.

KASH CASH

K = Knowledge.

A = Attitude.

S = Skill.

H = Habit.

You can get all wishes with the help of

these terms and then you can cash everything. If you are

unable to hold it then this English " Cash " will change

into Urdu " Kash ".

Your basic target is SALE.

S = Smile.

A = Attitude.

L = Love.

E = Evaluation.

BUDGETING (PRACTICAL PLANNIG)

Monthly Expenditures. Forecasting.

House rent 3000 Utility bills 1000

Food , Dressing 3000

Transportation 1000

Customer dealing 1200

Other expenses 800

Total. 10,000.00

DEPARTMENT OF MANAGEMENT SCIENCES IUB 44

86

To cover these expenses you have to income through

this forecasting.

MONTHLY INCOME FORECASTING

Income 10,000

Premium 25,000

Policies 10

Meeting 100

Name obtained 200

Working days 20

Meeting / day 5

The main purpose of the course is " To think in

advance " and this is the basic planning.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 45

86

INTERNAL AUDIT DEPARTMENT

This department plays a supervisory role

of al l of the all the other departments by checking

and verif ication of al l the working done by the

departments according to the rules and

regulations provided b PO Karachi t ime to time.

These rules and regulation are provided to al l the

Zone through Pakistan in shape of circular. These

circulars are attached in the book, which is called

“Key to PO Circular Volume”. All working of the

departments are verif ication according to this

book. In this way, the frauds, errors, and

omission are detected.

TYPE OF AUDIT:

Pre-Audit

Post-Audit

When the audit is done before making payments,

it is called pre-audit. Audit conducted after

making payments is called post Audit. Pre audit is

conducted for al l the big payments such as

purchase of assets, payment at maturity of policy,

payment on death claim etc. Post audit is

DEPARTMENT OF MANAGEMENT SCIENCES IUB 46

86

conducted for al l-to-day expenses such as

traveling expenses, stationary etc .

CUSTOMERS OF STATE LIFE

1- EXTERNAL CUSTOMERS

External customers are those who have no link with

SLIC. They are the common people which are the main

target of sales force.

2- INTERNAL CUSTOMERS

Internal customers are infect those people who have

direct or indirect link with SLIC. These are employees of

the corporation and their relatives.

MARKETING PRODUCTS Table Name

01- Whole Life Assurance.

03- Endowment Assurance.

04- Progressive Premium.

05- Three Payment Plan.

06- Joint Life.

07- Child Protection.

09- Single Premium Endowment.

17- Optimal Maturity.

18- Rural Life.

19- Jeevan Sathi.

36- Shad Abad.

73- Sunehri Policy.

75- Child Education and Marriage(built in)

DEPARTMENT OF MANAGEMENT SCIENCES IUB 47

86

76- Child Education and Marriage(Non built in).

N.D.SCHEME

Policy fee is not charged on these plans.

18,71,72,73,77.

If policy sum assumed is 300,000 or more 50 paisa is

rebate on basic rate.

There is a 8% rebate for staff employees on planes.

01 to 07.

51 to 57.

These all plans are finished from July 2002.

02,21,51,52,53,54,55,56,58,59,62.

01:- Whole Life Assurance

Age limit = 10-65 years.

Minimum premium.

This is for low income people.

Bonus rate is Maximum 50 pasia is rebate on factor

which starts from three lack sum assured.

e.g.

Age = 34 years.

Maturity = 85 years.

Premium paid = 51 years.

= 500,000

23.49 - 0.50 = 22.99

22.99 + 4 ATB = 26.99

26.99*500 = 11495 *100

Premium. = 115

Maturity Claim:-

Regular Bonus 56*5*500 = 140,000.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 48

86

102*47*500 = 234,600.

Terminated 30*20*500 = 300,000.

= 32,86,000.

Death Claim

S.A. = 500,000.

Accedental claim = 500,000.

Age at Accident = 55 years.

Regular Bonus = 500*5*56 = 140,000.

500*16*102 = 8,16,000.

Terminted:-

500*11*30 = 1,65,000.

=21,21,000.

AIB added 2,85,495

Rs.

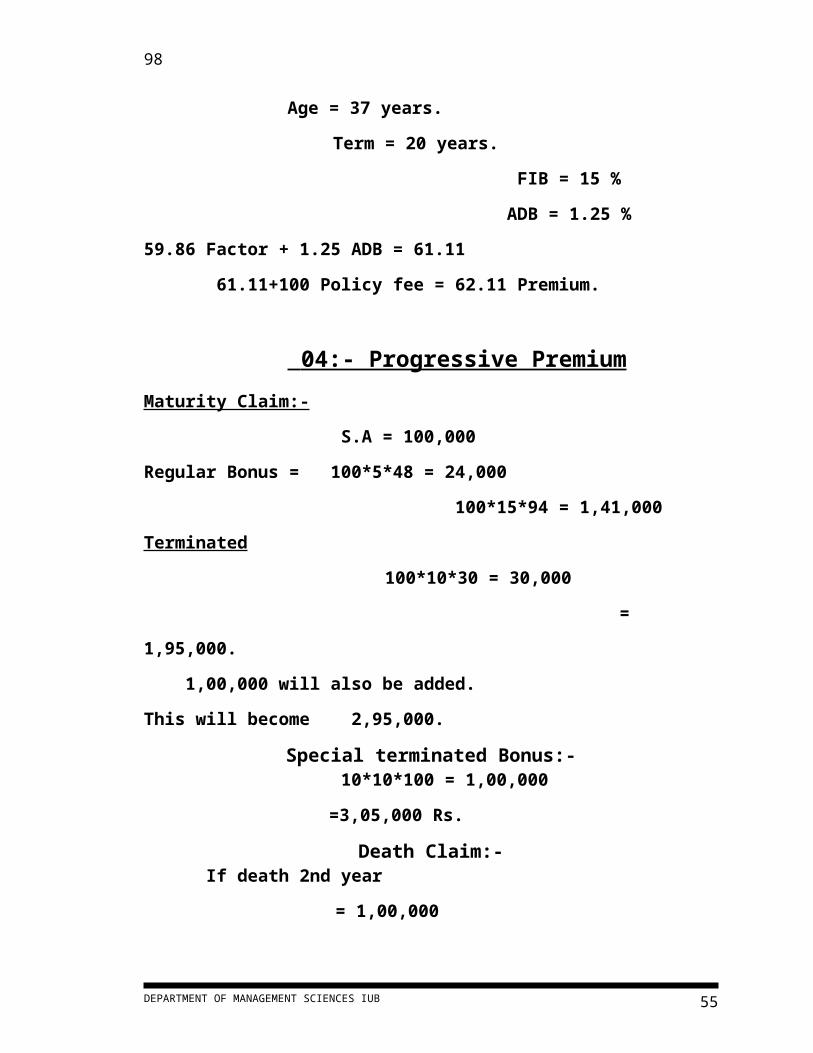

03:- Endowment Assurance

Age term = 20-65 years.

Maturity age = 75 years.

It's benefit is that time duration is on your wish.

This policy has a single nominee.

Age = 37 years.

Term = 20 years.

FIB = 15 %

ADB = 1.25 %

59.86 Factor + 1.25 ADB = 61.11

61.11+100 Policy fee = 62.11 Premium.

04:- Progressive Premium

DEPARTMENT OF MANAGEMENT SCIENCES IUB 49

86

Maturity Claim:-

S.A = 100,000

Regular Bonus = 100*5*48 = 24,000

100*15*94 = 1,41,000

Terminated

100*10*30 = 30,000

= 1,95,000.

1,00,000 will also be added.

This will become 2,95,000.

Special terminated Bonus:- 10*10*100 = 1,00,000

=3,05,000 Rs.

Death Claim:- If death 2nd year

= 1,00,000

Accedental Claim = 1,00,000

Regular Bonus = 48*1*100

= 2,04,800.

05:- Three Payment Plan

This is special for buisness man people.

Term = 18-30 years.

Terms:- 18,21,24,27,30 years.

Maturity will on every 6th year if term is 18 years.

e.g.

25% claim will be paid after 06 years.

25% claim will be paid after 12 years.

50% claim will be paid on maturity period.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 50

86

Best Use:- When you got 25% claim you can fix it in bank

scheme, after 10 years this amount will be 4 times.

Premium:- Age = 42 years

S.A = 50,000

Term = 21 years.

61.09*50 = 3054.5

3054.5 + 100 = 3154

` 07:- Child Protection

Child age = 6-15 years

Donar age = 20-50 years

Children have no alloted any suplimentary

contract before 5 years old. After 5 years age ADB can be

added.

If S.A is greater than 1,50,000 then under writer can

demand " Reject Medical Test ".

If Father Died .

Premium payment stops. Till maturity 10%

scholarship anuualy goes to

children. At maturity date claim plus bonuses will go to

children.

If Children Died .

If child died after 1st year of policy then 10% of S.A

+ 10% of Bonus will be. If after 2 years of policy then 20%

of S.A + 20% of bonus will go to father. After 10th

premium complete S.A + complete bonus will go in each

case.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 51

86

18:- Rural Life

Age = 20-55 years

Term = 15 or 20 years

In accidental case 3 times claim will paid.

In accidental case but with any claim will be paid.

The other facility for policy holder is that no late fee

will be charged within 8 months after premium paid

date.

This policy is free from policy fee.

Premium:- Term = 20 years

Age = 21 years

S.A = 1,00,000

59.12*100 = 5912

5912 + 100 = 6112

19:- Jeevan Sathi

Premium single

Protection double

If any one dies, the other partner gets claim. If

the other also dies, then the claim goes to the Hearis.

Isolated medical for both partners. Separated filling of

proposed forms. Each can take suplementory contract.

Table 19 = WP + TIR + 03

Equal age consideration.

Women age = 24 years - 2 = 22 years

Man's age = 34 years

DEPARTMENT OF MANAGEMENT SCIENCES IUB 52

86

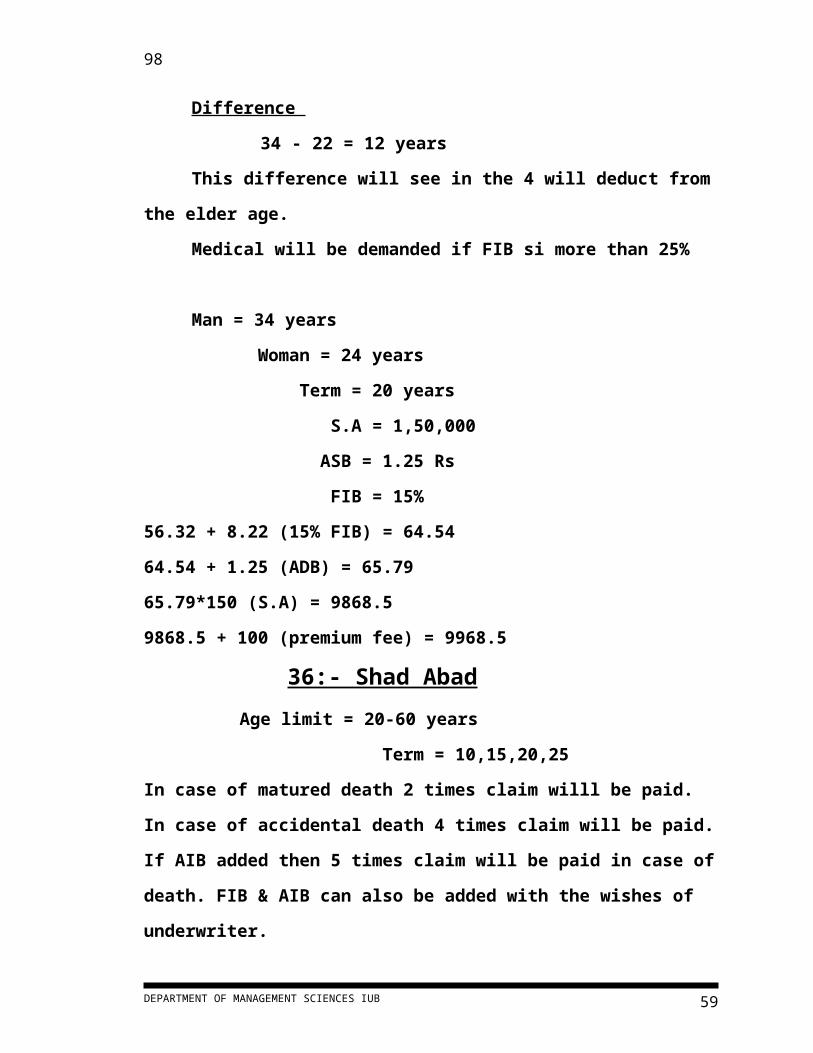

Difference

34 - 22 = 12 years

This difference will see in the 4 will deduct from the

elder age.

Medical will be demanded if FIB si more than 25%

Man = 34 years

Woman = 24 years

Term = 20 years

S.A = 1,50,000

ASB = 1.25 Rs

FIB = 15%

56.32 + 8.22 (15% FIB) = 64.54

64.54 + 1.25 (ADB) = 65.79

65.79*150 (S.A) = 9868.5

9868.5 + 100 (premium fee) = 9968.5

36:- Shad Abad

Age limit = 20-60 years

Term = 10,15,20,25

In case of matured death 2 times claim willl be paid. In

case of accidental death 4 times claim will be paid. If AIB

added then 5 times claim will be paid in case of death. FIB

& AIB can also be added with the wishes of underwriter.

T-36 = ADB + TIR + 03

Premium.

S.A = 2,00,000

Age = 25 years

Term = 20 years

DEPARTMENT OF MANAGEMENT SCIENCES IUB 53

86

53.45*200 = 10,690

10,690 + 100 = 10,790

73:- Sunehri Policy

Bonus rate = 115/1000

It is same of long life, plan,saving and protection.

Age limit = 20-60 years

Age = 34 years

S.A = 1,00,000

He wants no increase in 6% then this will proceed

like other policies.

If he wants to renew 6% then medical will be

demanded. No policy fee, no rebate. Suplementory

contracts.FIB, ADB, TIR.

Contracts and benefit of suplementory contract starts

from 3rd premium.

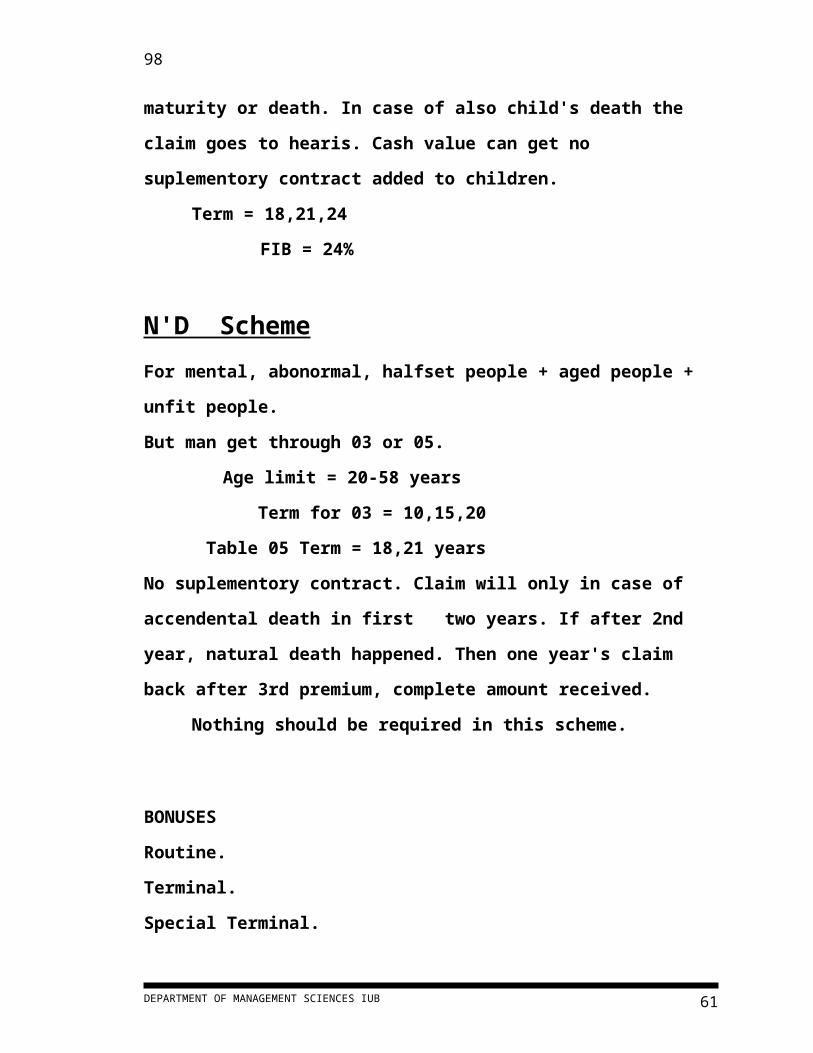

75:- Child Education and Marriage

Every person can get this for his nephew, son etc. In case

of policy holder's death 24% FIB scholarship goes to

children. But birth certificate will be demandedat maturity

or death. In case of also child's death the claim goes to

hearis. Cash value can get no suplementory contract

added to children.

Term = 18,21,24

FIB = 24%

N'D Scheme

DEPARTMENT OF MANAGEMENT SCIENCES IUB 54

86

For mental, abonormal, halfset people + aged people +

unfit people.

But man get through 03 or 05.

Age limit = 20-58 years

Term for 03 = 10,15,20

Table 05 Term = 18,21 years

No suplementory contract. Claim will only in case of

accendental death in first two years. If after 2nd year,

natural death happened. Then one year's claim back after

3rd premium, complete amount received. Nothing

should be required in this scheme.

BONUSES

Routine.

Terminal.

Special Terminal.

Interrum Bonus.

Regular ( Routine ) Bonuses:_

Time First Five Years After Five Years

<20 56 102

20> 48 94 01-Endowment.

15-19 35 81

10-14 20 60

20< 35 09

DEPARTMENT OF MANAGEMENT SCIENCES IUB 55

86

15-19 25 59 02-Payment

plan

10-14 19 53

TERMINAL BONUSES

At the maturity time or at the death time if the policy

inforced till after 4 years. After the 10th premium,

terminal bonus starts. This bonus is 30 Rs. / 1000 at the

premium, which is maximum at 600 Rs. per thousand.

e.g.

t-03

S.A = 100,000

Term = 25 years

Premium = 5000

100 (S.A)*15(Yrs. remaining)*30(Rate) = 45000

SPECIAL TERMINAL BONSUES

In case of FIB year in 2002 at policy maturity,

this bonus will be given to you. This will be given to you

at each last 10 years premium with the rate of 10 / 1000

which is maximum.

200 / 1000

e.g.

t-03

S.A = 100,000

Term = 30 years

FIB

100(S.A)*20(Yrs. remaining)*20(Rate) = 2000

DEPARTMENT OF MANAGEMENT SCIENCES IUB 56

86

INTERRUN BONUS

This is given as interrum bonus, which is given at

terminal bonus.

e.g.

Special bonus is given in 2002, but it does not goes

to policy holder and PH died. In this case the bonus which

is delievered in 2003, will also be given to policy holder.

e.g.

During 2002 a terminal bonus is given to Ubaid. But

the bonus certificate does not find to Ubaid, and such a

mistake happened. Then this will go to Ubaid's claim as

interrum bonus.

SPECIAL BONUS

Condition = Policy should be inforced when this

bonus is announced.

e.g.

premium of 94 will be paid in 95's premium date.

SUPPLEMENTARY CONTRACT

ADB.

AIB.

FIB.

TIR.

WP.

SWP.

SUPLEMENTORY CONTRACTS

DEPARTMENT OF MANAGEMENT SCIENCES IUB 57

86

ADB

Double claim paid from 5-55 years. ADB become 4 times in

ShadBad automatically. In table 18 this is 3 times, but in

case of injury or death with agricultural tool this will paid

5 times. Non external or intetrnal injury effect the

demand of ADB claim. Notice of claim is attached to the

documents when this contract starts. This contract is

checked within 90 days of death. has the right to

examine the body at any date. Termination in case of

death claim, or if goes to sixty years age. If you want to

include it in case of revival then this will happen

according to the rules of. Risks which are excluded in this

contract are in murder, heat stroke, in arresting, games,

pragrency, any effect from alcohol drug etc.

AIB

In case of death, double claim will go to party. In

accident, if two main organs, two arms, two legs, two

eyes or one arm, leg or eye died then complete claim will

be charged and all the premium life and on maturity.

Same Assured + Bonuses of Premium paid. But if one

main organ destroys

e.g.

One arm or one leg demage then half of the claim will

be paid but no rebate in premium. In case of one eye

1/3 of S.A will recieved. Finger of Shahadat or thumb

destroy, then 1/4 of S.A will recieved, no rebate in

DEPARTMENT OF MANAGEMENT SCIENCES IUB 58

86

premium. If there is any serious injury then 5/1000

recieved for 52 weeks. If injury is more than 15 days.

But after 52 weeks 100/1000 for 10 years will be

recieved.

Term = 20-55 years

FIB

It's limit starts from 10-50% and 10-25% . No medical

charge but after 25% FIB medically you will checked. In

case of death monthly scholarship paid.It's term is from

10-45 years. Age limit is from 20-50 years. Protection of

contract will remain at 65 years age. This contract

terminates on Expiry date, if the policy lapse, surrender

or on any policy anniversory at prior notice by the policy

holder. If your policy is on Revival then offcoursty it's

amount will be added.

TIR

Friend goes to Dubai, for two or three years and

gained a contract. That if your accident happened at any

place then it's equal amount goes to your account.

Term is from 10-25 years.

Age limit is from 20-60 years.

Maximum rate of TIR is 3 times. It's protection remains at

70 years age.

Because these contracts are of 2 or 3 years, so mostly

factory honours, driver people get this.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 59

86

SUPLEMENTORY CONTRACT RATES

Clerk, Professionals etc.

AIB = 4 Rs

ADB = 1.25 Rs

Buisness man

ADB = 1.5 Rs

AIB = 5 Rs

Former

ADB = 1.88 Rs

AIB = 6 Rs

Labour

ADB = 2.5 Rs

AIB = 6 + 2 = 8 Rs

FIB is on the wish of policy holder.

Followings are the plans which are off from July 2002.

02,21,51,52,53,54,55,56,58,59,62

SALARY AND GRADING

Grade Initial Pay Increment Max. Pay

1 1545 80 3456

2 1788 100 3868

3 1849 102 3991

4 2037 118 4515

5 2105 133 4898

6 2652 149 5781

7 3374 288 13454

8 4990 350 11990

DEPARTMENT OF MANAGEMENT SCIENCES IUB 60

86

9 7200 490 15530

10 8970 610 18120

11 12630 640 22230

12 13660 680 23860

13 15920 710 26620

14 18420 900 30120.

SWOT ANALYSIS

Strength.

Weakness.

Opportunities.

Threats.

SWOT ANALYSIS“There is an old Spain saying that to be a

bullfighter you must first Lear to be a

bull”.

SWOT stand for strength, Weakness,

Opportunities and Threats. The main aim of this

analysis is to identify the extent to which the

current strategy of the organization and its more

specific changing taking place in the business

environment. The idea of SWOT analysis is to

DEPARTMENT OF MANAGEMENT SCIENCES IUB 61

86

undertake a more structured analysis so as to

yield so as to yield f inding, which can contribute

the formulation of strategy.

STRENGTHS

SWOT Analysis of SLIC is as fol lows:

Field force Management

Good image

Excellent set up

Real estate division (investment

portfolio)

Training academies & training

centers

DEPARTMENT OF MANAGEMENT SCIENCES IUB 62

86

Marketing division

Advertising & Sales promotion

Computerization

Market leader

Return (bonus to policyholder)

Government security

FIELD FORCE MANAGEMENT :

SLIC has ful-f ledge HRDD in most ZONAL Offices

organized by qualif ied trainers and equipped by

modern equipment to mange and train f ield force.

GOOD IMAGE:

DEPARTMENT OF MANAGEMENT SCIENCES IUB 63

86

SLIC is an old insurance company operating in the

Pakistan and has created the good image and

good wil l in the eyes of general public. This is the

strength of SLIC.

EXCELLENT SETUP :

SLIC is a large Life Insurance Company in Pakistan

and have 27 Zonal Offices and 5 Regional Offices

throughout the country.

REAL ESTATE DIVISION (INVESTMENT

PROTFOLO ):

SLIC has well-equipped and computerized Real

Estate Division in principal office (PO) Karachi

supervised by highly qualif ied staff, engineers

and investment analysts.

TRAINING ACADEMIES & TRAINING

CENTERS :

SLIC has 3 training Academies at Karachi, Lahore

and Rawalpindi and 26 Training Centers in zonal

offices. In 1998, 1946 courses and seminars,

ranging from Basic Courses to advanced Programs

l ike ADP, MOP and MMS of LIMRA (USA) had

conducted.

MARKETING DIVISION:

This division is backbone of SLIC. During 1998,

25486 young and educated people were inducted

as SR in the sale force, this raising its strength to

256,814, inclusive of SO & SM.

ADVERTISING & SALES PROMOTION:

DEPARTMENT OF MANAGEMENT SCIENCES IUB 64

86

During 1998, a new penal of four advertising

agencies was selected. Outdoor advertising such

as installation of Unipole Hoarding display of

commercials in PTV is done and other publicity

materials such as Calendars, Stickers, Eid Cards,

and Posters are produced to boost business

activities.

COMPUTERIZATION:

About 2/3 working is computerized in SLIC. The

plan to computerized total working is under

review.

RETURN (BONUS TO POLICYHOLDER):

SLIC provides different types of bonuses as

Reversionary, Terminal, Interim, One time, Golden

and Special Reversionary Bonus to the

policyholder.

GOVERNMENT SECURITY:

It is the main strength of SLIC. Due to this factor,

the image and good wil l for SLIC is further

enhanced:

OTHERS:

It is old and most experienced organization.

PO conducts marketing survey to analyze

environment and develop new plans.

Employees are fully devoted and highly paid

workers as compare to other organization.

It has highest paid up capital.

It is reinsured by Swiss Re (Insurance Company

Switzerland).

DEPARTMENT OF MANAGEMENT SCIENCES IUB 65

86

WEAKNESSES

Incompetent f ield force

Internal setting & culture

Centralized Decision Making

Internal department inefficiency

Selection & recruitment

Feed back

INCOMENTENT FIELD FORCE:

In term of quantity, it is strength but in term of

quality it is weakness. Most workers are not

DEPARTMENT OF MANAGEMENT SCIENCES IUB 66

86

highly educated. They are promoted by fulf i l l ing

targets.

INTERNAL SETTING & CULTURE :

Internal office setting and arrangement is not

satisfactory as compare to its competitors.

Dominant Culture needs further improvement but

sub culture (i .e HRDD, Group Insurance) of some

department is stationery. Yet there is need of

further improvement.

CENTRALIZED DECISION MARKETING:

Managerial decision-making is totally centralized

in the PO Karachi, Zonal Offices fol low the

instruction and rules & regulations provided by

PO. Sometimes decisions is taken by PO is not

strategic and adjustable in the local environment.

For prosperity & survival of the organization,

decentralization (to some extent) is necessary.

INTERNAL DEPARTMENT INEFFICIENCY :

Underwriting process (in NB Department) takes

longer time period, which irritates the

prospects.

Loan section takes 10 days to process.

Normally 1 to 2 months is required to surrender

the policy and take the Survival Benefit, which

is not justif ied.

SELECTION & RECRUITMENT :

SR are selected and recruited by SO & SM

irrespective of their education and unique

internal attributes.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 67

86

FEED BACK :

The Corporation does not have any effectives and

efficient feed back channel to disseminate sales

force suggestions to upper management. Further,

organization has no well organize system for feed

back between office employees and manager,

managers and Board of Directors.

OTHERS:

Frauds done by some deceives field workers

who deteriorate the good wil l & image of the

organization.

Ineffective downward and upward

communication channels.

OPPORTUNITIES

PER-CAPITA PREMIUM

In Pakistan per capita premium payment is 1.5

and $1.7 only for l ife & general insurance

respectively. There is an opportunity to enhance

this nominal rate. In Japan per capita premium for

l ife insurance is $3810.

POPULATION GROWTH RATE :

In Pakistan, population growth rate is

approximately 3%. It is a great opportunity for

insurance sector.

INSURED POPULATION:

DEPARTMENT OF MANAGEMENT SCIENCES IUB 68

86

In Pakistan 2% to 3% population is insured while

rest of the population provides opportunity to l ife

insurances to enhance their business.

GOVERNMENT REGULATION :

Section 10-B of Pakistan Commercial and

Industrial Standing Ordinance 1968 provides the

compulsory insurance of al l the employees of the

organization (whether private or Govt.). So it is a

great opportunity to SLIC.

ENTERY BARRIERS

To enter in the insurance business he investment

is required. Further 40% of premium is

compulsory for the private insurances, to cede to

Government of Pakistan security purpose

creating the entry barrier.

THREATS

COMPETITORS:

The existence of local and government insures

such as EFU, CU, Metropolitan. ALICO etc. is

threat to the survival of SLIC.

POLITCAL INSTABILITY :

Political instabil ity looses the confidence of the

policyholders. Further rules and regulations of

government are subject to change creating threat

to insurance business.

DEPARTMENT OF MANAGEMENT SCIENCES IUB 69

86

FEAR OF WAR

The relationships of Pakistan with India are not

satisfactory due to Kashmir dispute. There is

always a fear war creating the threat to

corporation and policyholders.

INVESTMENT CLIMATE:

Due to the polit ical instabil ity and government

changeover the investment cl imates are not

satisfactory in the country. So the return from

real estates and other activities is deteriorated.

Competors

ALICO

EFU

METRO POLETON

COMERCIAL LIFE

POSTAL LIFE

ADAM JEE

The main Competitors of SLIC are:

Eastern Federal Union (EFU)

Commercial Insurance Company

DEPARTMENT OF MANAGEMENT SCIENCES IUB 70

86

Metropolitan Insurance Company

American Life Insurance Company

(ALICO)

SLIC has enjoyed a complete monopoly ti l l 1990

when the Govt. has decided to al low the private

insurers to operate in the Pakistan. After 1990

the market share of SLIC is declining. But yet SLIC

has enjoyed the market share in l ife insurance

business of 91.4 on the basis of total premium

written off in 1997.

The year of establishment of the l ife insurance

companies are as fol lows:

DEPARTMENT OF MANAGEMENT SCIENCES IUB

EFU 1992

CU July

1996

ALICO May

1995

Metropoli

tan

Februa

ry 1993

SLIC 1972

71

86

EFU and CU have adopted the Unit Link System.

Whenever the policyholder takes the insurance

policy, he indirectly purchases the units of the

EFU and CU. The values if this unit is announced

daily in the newspaper.

The strategic analysis of SLIC is confined only 5 years starting from 1994 to 1998.The

main objective of this analysis to know the financial status and competitive position of

SLIC keeping in view different factors such as total business in force, life fund,

investment portfolio, total income, FYP etc. first, I start from premium Income of SLIC.

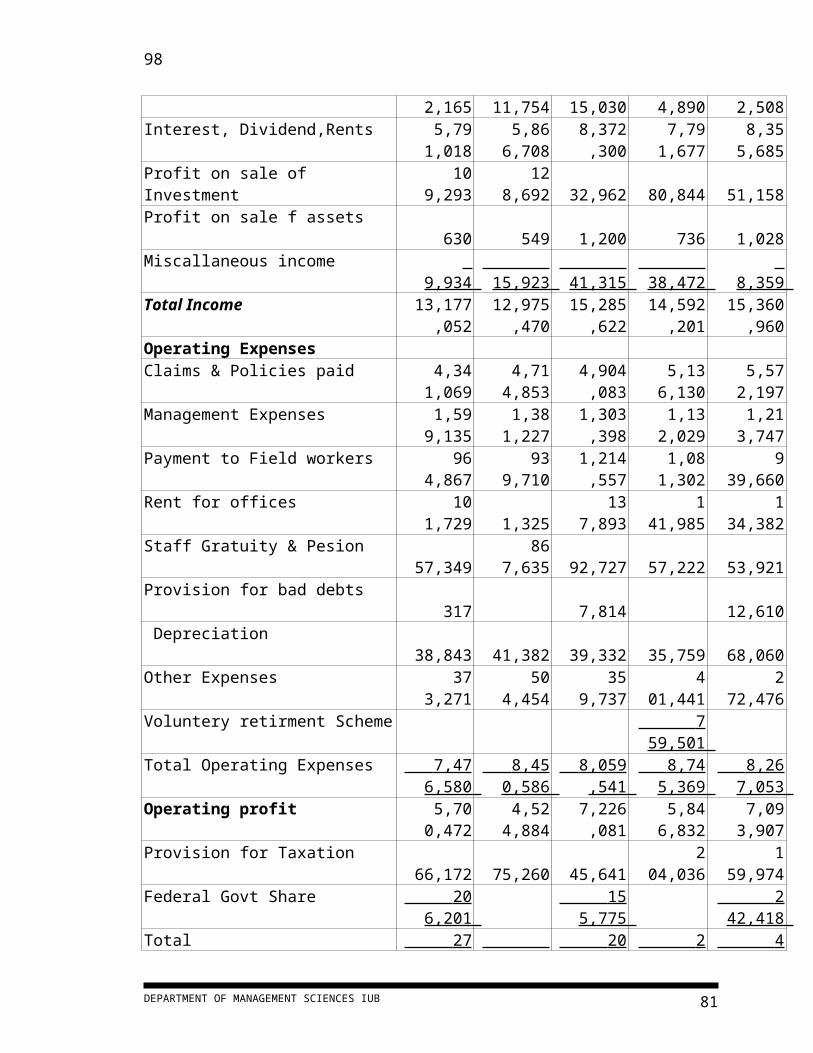

STATE LIFE INSURANCE CORPORATION OF PAKISTAN

SUMMARIZED INCOME STATEMENTFOR THE YEAR ENDED ON 31

DECEMBER-------------1997 1998 1999 2000 2001

Total IncomeFirst year premium 1,487,

409 1,293,

756 1,258,0

84 1,033,

522 1,121,

142 Renewal premium 4,363,

671 4,413,

159 4,311,4

67 4,537,

853 4,564,

562 Single premium

65 5

61 2,3

23 2,2

48

37 Group premium 1,412,

867 1,244,

368 1,250,9

41 1,101,

959 1,256,

481 Annunities 2,1

65 11,7

54 15,0

30 4,8

90 2,5

08 Interest, Dividend,Rents 5,791,

018 5,866,

708 8,372,3

00 7,791,

677 8,355,

685 Profit on sale of Investment 109,2

93 128,6

92 32,9

62 80,8

44 51,1

58 Profit on sale f assets 6

30 5

49 1,2

00 7

36 1,0

28 Miscallaneous income 9,9

34 15,9

23 41,3

15 38,4

72 8,3

59 Total Income 13,177,

052 12,975,

470 15,285,

622 14,592,

201 15,360,

960 Operating ExpensesClaims & Policies paid 4,341,

069 4,714,

853 4,904,0

83 5,136,

130 5,572,

197 Management Expenses 1,599,

135 1,381,

227 1,303,3

98 1,132,

029 1,213,

747

DEPARTMENT OF MANAGEMENT SCIENCES IUB 72

86

Payment to Field workers 964,867

939,710

1,214,557

1,081,302

939,660

Rent for offices 101,729

1,325

137,893

141,985

134,382

Staff Gratuity & Pesion 57,349

867,635

92,727

57,222

53,921

Provision for bad debts 317

7,814

12,610

Depreciation 38,843

41,382

39,332

35,759

68,060

Other Expenses 373,271

504,454

359,737

401,441

272,476

Voluntery retirment Scheme 759, 501

Total Operating Expenses 7,476, 580

8,450, 586

8,059,5 41

8,745, 369

8,267, 053

Operating profit 5,700,472

4,524,884

7,226,081

5,846,832

7,093,907

Provision for Taxation 66,172

75,260

45,641

204,036

159,974

Federal Govt Share 206,2 01

155,7 75

242, 418

Total 272,3 73

75,2 60

201,4 16

204, 036

402, 392

Net profit 5,428, 099

4,449, 624

7,024,6 65

5,642, 796

6,691, 515

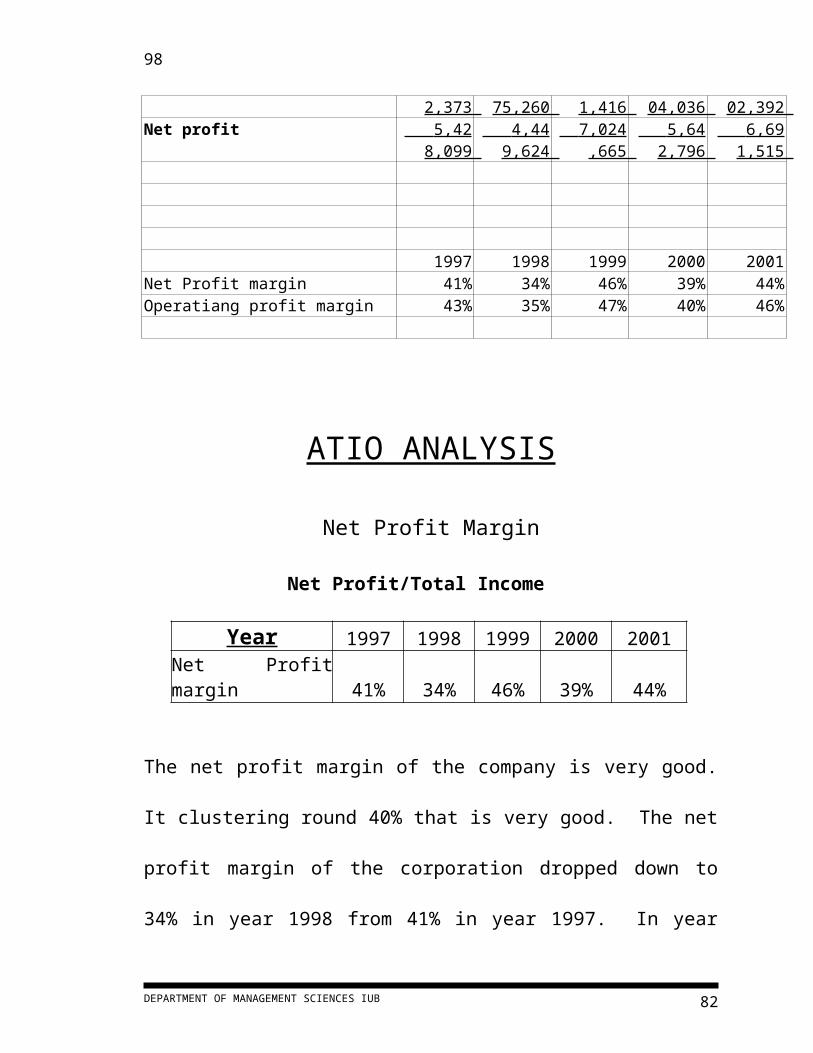

1997 1998 1999 2000 2001Net Profit margin 41% 34% 46% 39% 44%Operatiang profit margin 43% 35% 47% 40% 46%

ATIO ANALYSIS

Net Profit Margin

Net Profit/Total Income

DEPARTMENT OF MANAGEMENT SCIENCES IUB 73

86

Year 1997 1998 1999 2000 2001Net Profit margin 41% 34% 46% 39% 44%

The net profit margin of the company is very good. It

clustering round 40% that is very good. The net profit

margin of the corporation dropped down to 34% in year

1998 from 41% in year 1997. In year 2001 that net profit

margin of the corporation is 44% that is 3% higher than the

profit ratio of 1997 i.e. 41%.

Operating Profit Margin

Operating Profit / Total Income

Year 1997 1998 1999 2000 2001Operating profit margin 43% 35% 47% 40% 46%

The operating profit margin has increased from 43% in year 1997 to 46% in year 2001. This thing shows that the management has taken some encouraging actions to reduce the operating expenses of the corporation.

Current RatioCurrent Assets / Current Liabilities

Year 1997 1998 1999 2000 2001Current Ratio 1224% 1066% 1160% 1399% 1300%

DEPARTMENT OF MANAGEMENT SCIENCES IUB 74

86

The company has kept the majority of its sources in the current assets. The ratio of the current assets is increasing over the year. The ratio of current assets to current l iabi l it ies has increased from 1224% in year 1997 to 1300% in year 2001.

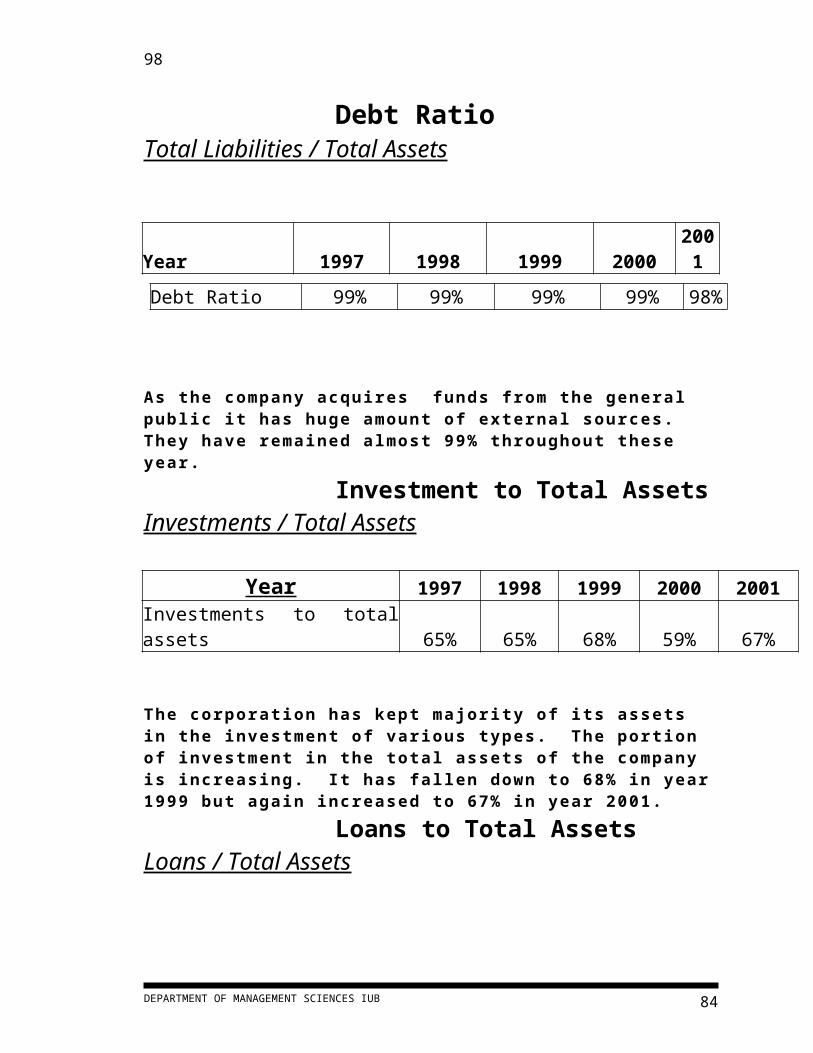

Debt RatioTotal Liabilities / Total Assets

Year 1997 1998 1999 2000200

1

As the company acquires funds from the general public it has huge amount of external sources. They have remained almost 99% throughout these year.

Investment to Total AssetsInvestments / Total Assets

Year 1997 1998 1999 2000 2001Investments to total assets 65% 65% 68% 59% 67%

The corporation has kept majority of its assets in the investment of various types. The portion of investment in the total assets of the company is increasing. It has fal len down to 68% in year 1999 but again increased to 67% in year 2001.

Loans to Total AssetsLoans / Total Assets

Year 1997 1998 1999 2000 2001Loans to Total Assets 7% 6% 6% 5% 5%

DEPARTMENT OF MANAGEMENT SCIENCES IUB

Debt Ratio 99% 99% 99% 99% 98%

75

86

The portion of the loan to total assets has remained constant from 5% to 7% in these f ive year. In year 1997 it was 7% that has fal len down to 5% in 2001.

Local Investments to Total Assets

Local Investment / Total Assets

Year 1997 1998 1999 2000 2001Local Investment to total assets 8% 8% 7% 6% 6%

The portion of the local investment in total

assets has been decreasing over the years.

It has fallen from 8% in year 1997 to 6% in

year 2001.

Investment to Government Securities

Investment in Govt. Securities / Total Assets

Years 1997 1998 1999 2000 2001Investment in govt securities to assets 65% 67% 68% 58% 67%

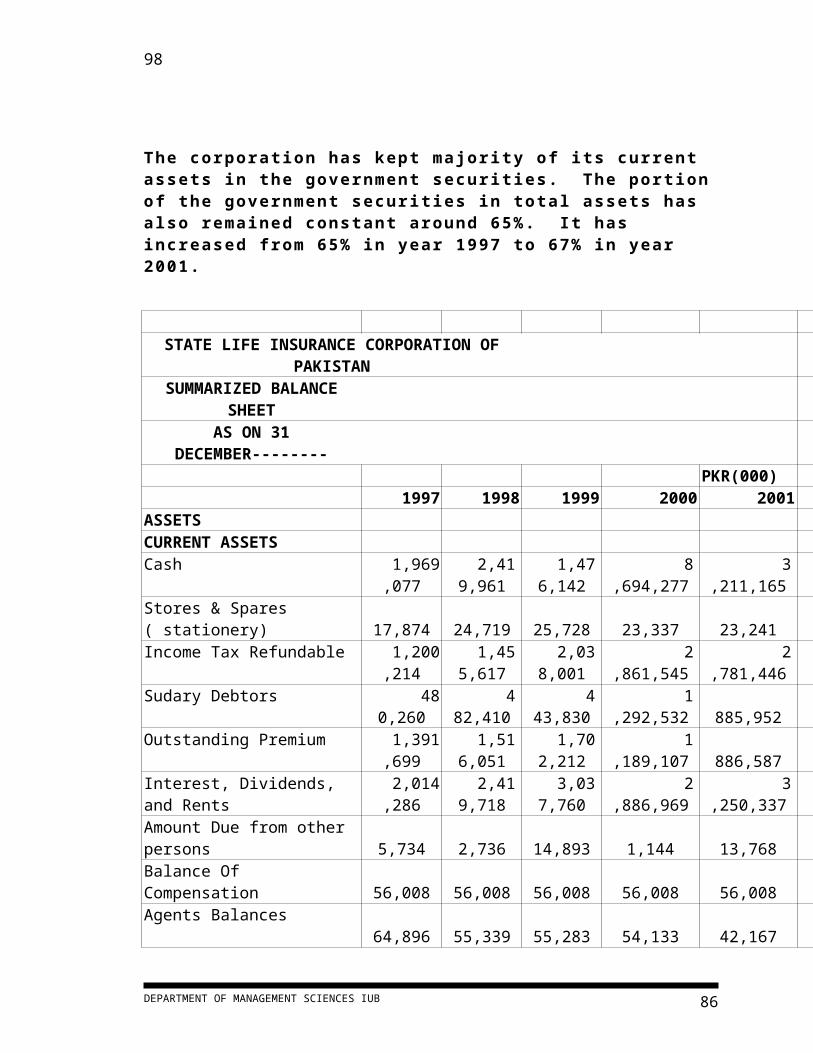

The corporation has kept majority of its current assets in the government securit ies. The portion of the government securit ies in total assets has also remained constant around 65%. It has increased from 65% in year 1997 to 67% in year 2001.

STATE LIFE INSURANCE CORPORATION OF PAKISTAN

DEPARTMENT OF MANAGEMENT SCIENCES IUB 76

86

SUMMARIZED BALANCE SHEET

AS ON 31 DECEMBER--------

PKR(000)1997 1998 1999 2000 2001

ASSETSCURRENT ASSETSCash 1,969,0

77 2,419,

961 1,476,

142 8,694,

277 3,211,

165 Stores & Spares ( stationery)

17,874

24,719

25,728

23,337

23,241

Income Tax Refundable 1,200,214

1,455,617

2,038,001

2,861,545

2,781,446

Sudary Debtors 480,260

482,410

443,830

1,292,532

885,952

Outstanding Premium 1,391,699

1,516,051

1,702,212

1,189,107

886,587

Interest, Dividends, and Rents

2,014,286

2,419,718

3,037,760

2,886,969

3,250,337

Amount Due from other persons

5,734

2,736

14,893

1,144

13,768

Balance Of Compensation 56,008

56,008

56,008

56,008

56,008

Agents Balances 64,896

55,339

55,283

54,133

42,167

InvestmentsGovt Securities 35,709,

618 40,477,

219 46,220,

194 42,526,

450 54,889,

017

TFCs 120,800

90,282

58,870

729,743

517,212

Certificate of Investments 1,000

1,000

1,000

1,000

Preferred Stocks 4,750

4,750

4,750

4,750

4,011

(-) Diminution in Value of Investments

47,2 96

929, 239

111, 648

177, 791

783, 083

Total Investments (net) 35,788, 872

39,644, 012

46,173, 166

43,084, 152

54,627, 157

Total Current Assets 42,988, 920

48,076, 571

55,023, 023

60,143, 204

65,777, 828

Non Current AssetsLoans 3,828,0

72 3,828,

072 3,828,

072 3,828,

072 3,828,

072

DEPARTMENT OF MANAGEMENT SCIENCES IUB 77

86

Wapda Bonds 600,000

600,000

600,000

600,000

600,000

U.K Govt Securities 243,684

243,684

243,684

243,684

243,684

Bonds, Debentures, Stocks 10,000

10,000

10,000

10,000

10,000

Ordinary Stock In Pakistan 4,614,223

4,614,223

4,614,223

4,614,223

4,614,223

Ordinary Stock Outside Pakistan

63,628

51,397

51,397

51,397