state of illinois · illinois non-farm employment by industry1 fortune 500 companies headquartered...

TRANSCRIPT

State of Illinois General Obligation Bonds Rating Agency Presentation Information Summary October 2 and 3, 2017

1. Illinois’ Strong and Diverse Economy 3

2. FY 2018 Budget Update 9

3. Pensions 14

4. Debt Overview 18

5. Bill Backlog and Plan of Finance 23

Table of Contents

Kim Fowler

Chief Legal Counsel

Alexis Sturm

Chief of Staff

Kelly Hutchinson

Director of Capital Markets

Scott Harry

Director

Presentation Participants – Governor’s Office of Management and Budget

1

Charlie Weikel

Director – Governor's Office of

Policy & Operations

Passage of fiscal year 2018 Budget

Permanent increase in personal income tax and corporate income tax rates to 4.95% and 7.00% respectively

Passage of Tier 3 Pension Plan and funding changes

Passage of Senate Bill 1947 remedied education funding disparities

Reauthorization of Edge Tax Credits to allow the State to compete for major economic development projects

Reduced risk to swap counterparties by renegotiating rating triggers

Sovereign State with significant revenue flexibility

Illinois’ economy is the 5th largest in the United States and 18th largest worldwide

Statutory provisions gives priority to debt service over other State expenditures

GO Bond debt service has a continuing appropriation

Debt service is limited to no more than 7% of General Funds and Road Fund Appropriations, without a waiver from the Treasurer and Comptroller

Debt service requirements decline by over $978 million after FY 2019 due to pension bonds maturing, providing significant flexibility

Issuance of the General Obligation Bonds will pay off approximately $6.0 billion of outstanding bills and is

expected to result in the receipt of additional federal funds

By the end of fiscal year 2018, the bill backlog is expected to be approximately $7.5 billion, a nearly 50%

reduction

Recent Developments Inherent Credit Strengths

Note: Amounts related to the plan of finance and bill backlog are estimates

The State’s Credit Fundamentals Have Improved Significantly

2

1. Illinois’ Strong and Diverse Economy

Illinois is home to 36 Fortune 500 companies

– Only New York, California and Texas have more

The City of Chicago was named “top metro for corporate relocation(s)” for the 4th year in a row3

– Recent major relocations to Illinois include Mars and Conagra

Chicago’s diversified economy is a major attraction for workers and recent graduates across the nation, bringing educated and skilled workers into the State

Illinois has a strong economy with a diverse workforce

similar to the nation

Broad employment base with no industry accounting for

more than 20%

The State is well-positioned for long-term stability

through economic cycles

Fortune 500 Companies Headquartered in Illinois2 Illinois Non-Farm Employment by Industry1

1. U.S. Department of Labor, Bureau of Labor Statistics 2. Fortune.com 3. Site Selection Magazine.

2016

Rank

2015

Rank Company Industry Category

17 19 Walgreens Boots Alliance Food and Drug Stores

24 24 Boeing Aerrospace & Defense

33 35 State Farm Insurance Cos. Insurance: Property and Casualty (Mutual)

45 41 Archer Daniels Midland Food Production

74 59 Caterpillar Construction and Farm Machinery

83 80 United Continental Holdings Arlines

84 81 Allstate Insurance: Property and Casualty (Stock)

89 95 Exelon Utilities: Gas and Electric

105 97 Deere Construction and Farm Machinery

109 94 Mondelez International Food Consumer Products

111 123 AbbVie Health Care

112 109 McDonald's Food Services

124 122 US Foods Wholesalers: Food and Grocery

127 111 Sears Holdings General Merchandisers

135 138 Abbott Laboratories Medical Products and Equipment

197 173 Conagra Brands Food Consumer Products

199 220 CDW Information Technology Services

202 211 Illinois Tool Works Industrial Machinery

277 283 Discover Financial Services Commercial Banks

281 286 Baxter International Medical Products and Equipment

283 285 W.W. Grainger Wholesalers: Diversified

304 369 LKQ Wholesalers: Diversified

322 334 Tenneco Motor Vehicles & Parts

337 281 Navistar International Construction and Farm Machinery

338 315 Univar Wholesalers: Diversified

359 391 Anixter International Wholesalers: Electronics and Office Equipment

388 258 R.R. Donnelly & Sons Publishing, Printing

391 436 Jones Lang LaSalle Real Estate

392 377 Dover Industrial Machinery

427 767 TreeHouse Foods Food Consumer Products

433 451 Motorola Solutions Network and Other Communications Equipment

439 442 Old Republic International Insurance: Property and Casualty (Stock)

450 446 Packaging Corp. of America Packaging, Containers

456 456 Ingredion Food Production

462 471 Arthur J. Gallagher Diversified Financials

487 477 Essendant Wholesalers: Electronics and Office Equipment

Trade,

Transportation

and Utilities

20%

Professional and

Business

Services

16%

Education and

Health Services

15%

Government

14%

Leisure and

Hospitality

10%

Manufacturing

9%

Financial

Activities

6%

Mining, Logging,

Information and

Other Services

6%

Construction

3%

Illinois’ Strong and Diverse Economy

3 Illinois’ Strong and Diverse Economy

0.0

2.0

4.0

6.0

8.0

10.0

12.0

5,300

5,400

5,500

5,600

5,700

5,800

5,900

6,000

6,100

6,200

6,300

IL Employment IL Unemployment Rate National Unemployment Rate

$620,000

$630,000

$640,000

$650,000

$660,000

$670,000

$680,000

$690,000

$700,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 1Q17

Median Household Income

Illinois MHI has grown 4.5% annually on average since 2011, outpacing the

US (3.1%) and neighboring states (3.1%). Income as measured by both PCI and

MHI remains well above national averages.

Source: U.S. Department of Commerce, Bureau of Economic Analysis; Bureau of Labor Statistics 1. YTD averages 2. As of August 2017, not seasonally-adjusted and

preliminary and subject to change 3. Bureau of Economic Analysis 2017, data as of 7/2017.

Per Capita Personal Income1

Illinois’ Per Capita income is ranked 4th among the 10 largest states.

Upward Trend in IL Real GDP3

In Q1 of 2017 Illinois’ economy ranked 5th in the nation and 18th in the

world at $804 Billion (behind Florida and ahead of The Netherlands).

Average Non-farm Employment and Unemployment1,2

Employment increased with jobs exceeding 6.0 million in 2016.

Mil

lion

s of

Ch

ain

ed

2009 D

oll

ars

Un

em

plo

ym

en

t Rate

(%) E

mp

loym

en

t (T

hou

san

ds)

$48,000

$50,000

$52,000

$54,000

$56,000

$58,000

$60,000

$62,000

2012 2013 2014 2015 2016Illinois National

$36,000

$38,000

$40,000

$42,000

$44,000

$46,000

$48,000

$50,000

$52,000

$54,000

2011 2012 2013 2014 2015 2016 1H2017

Illinois United States Great Lakes

Illinois’ Robust Economic Indicators

4 Illinois’ Strong and Diverse Economy

Demographics by Age The State’s population mix by age mirrors the US but has a lower

percentage of people over 65.

Source: US Census, US Bureau of Labor Statistics.

Population Illinois is the 5th most populous state in the nation and has grown

each decade through 2010 with a modest YoY decline in 2016.

Highly Educated Population Illinois is home to top ranked universities bringing talented and educated individuals to the State. Illinois residents with college degrees is

32.3%, well above the US at 29.8% and the Great Lakes States at 26.2%.

0% 5% 10% 15% 20% 25% 30%

> 65 yrs

45 to 64

25 to 44

18 to 24

under 18

U.S. Illinois

10.0

10.5

11.0

11.5

12.0

12.5

13.0

1970 1980 1990 2000 2010 2016

mil

lio

ns

Demographic Analysis

5 Illinois’ Strong and Diverse Economy

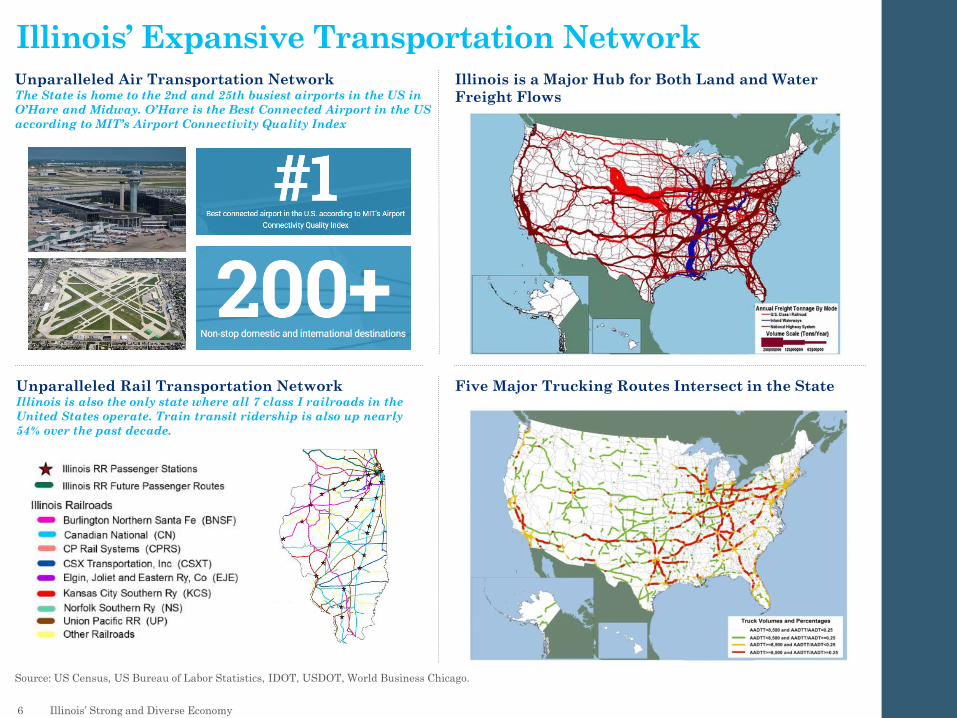

Illinois is a Major Hub for Both Land and Water

Freight Flows

Source: US Census, US Bureau of Labor Statistics, IDOT, USDOT, World Business Chicago.

Unparalleled Air Transportation Network The State is home to the 2nd and 25th busiest airports in the US in

O’Hare and Midway. O’Hare is the Best Connected Airport in the US

according to MIT’s Airport Connectivity Quality Index

Unparalleled Rail Transportation Network Illinois is also the only state where all 7 class I railroads in the

United States operate. Train transit ridership is also up nearly

54% over the past decade.

Five Major Trucking Routes Intersect in the State

Illinois’ Expansive Transportation Network

6 Illinois’ Strong and Diverse Economy

2. FY 2018 Budget Update

FY 2017 Budget Review

7 FY 2018 Budget Update

A full FY 2017 General Funds budget was not

enacted prior to the end of the fiscal year

All payments for General Obligation and Build

Illinois bond debt service were made

Final FY 2017 General Funds revenue totaled

$29.405 billion

For the General Funds budget, certain

appropriations were enacted and spending

occurred through statutory transfers, statutory

continuing appropriations, court orders and

consent decrees. Such spending is estimated to

total $34.0 billion in categories such as:

– Elementary and secondary education

– Medicaid and certain social service grant

programs covered by consent decree

– State employee payrolls by court order

– Pension contributions

– Transfers to other State funds, including for

debt service

– FY 2017 Appropriations in some cases were

used to pay FY 2016 obligations

Approximately $2.8 billion in State General

Funds operational liabilities were not

appropriated in FY 2017, but these may be paid

from future year appropriations

1. Cash basis. Does not include transfers in from Budget Stabilization Fund. 2. Estimated expenditures based on FY 2017 spending as of 10/4/17, does not reflect IOC

budgetary adjustments. Estimated expenditures are only those processed by Comptroller via appropriation, continuing appropriation or court order/consent decree during FY

2017 and FY 2017 lapse period. 3. GOMB estimate of FY 2017 General Funds liabilities not appropriated.

General Funds Estimated Results ($millions)

FY 2017

Estimated

Base Resources

State Sources $25,380

Transfers In1 $1,542

Total State Sources $26,922

Federal Sources $2,483

Total Resources $29,405

Estimated Budgetary Expenditures2 $29,400

Statutory Transfers Out $2,400

Debt Service $2,235

Total Transfers $4,635

Total Expenditures $34,035

Estimated General Funds Surplus (Deficit) (4,630)

Estimated FY 2017 Operational Liabilities Not Paid3 2,800

FY 2018 Budget Update

8 FY 2018 Budget Update

As of May 31, 2017, no appropriations bills for spending for Fiscal Year 2018 had passed both chambers of

the General Assembly. After this date, the Illinois Constitution requires that changes in law and

appropriations may be immediately effective only with the approval of 3/5ths of the members of each

chamber rather than a simple majority

In early July, the General Assembly passed a Fiscal Year 2018 budget package, including appropriations and

revenue increases

– The Governor vetoed the bills related to the budget package on July 4, 2017, citing imbalances in the

proposed Fiscal Year 2018 General Funds budget

– The Senate and the House of Representatives overrode the Governor’s veto of the budget package

Three budget-related Public Acts went into effect on July 6, 2017 – PA 100-21 (appropriations), PA 100-22

(revenues) and PA 100-23 (the budget implementation statutory changes)

Included in PA 100-22 were permanent increases in the individual income tax rate from 3.75 percent to

4.95 percent and in the corporate income tax rate from 5.25 percent to 7.0 percent, effective July 1, 2017

Other revenue changes included revisions to certain tax credits and corporate income tax deductions

FY 2018 Budget Update (continued)

9 FY 2018 Budget Update

PA 100-23, the statutory budget implementation bill, included several legislative changes:

The General Assembly enacted pension funding reforms with the expectation that the revisions would

reduce the amount of contributions the State is required to make during Fiscal Year 2018

For Fiscal Year 2018, there is a 10% reduction in State income and sales tax revenue sharing with local

governments and transit districts, and also a shifting of this revenue sharing from a legislative transfer from

the General Revenue Fund after income and sales taxes are deposited into the fund to a direct deposit

Authorization for the State to issue up to $6 billion in Section 7.6 Bonds (which includes the Bonds and the

Series of November 2017D Bonds) to be used to reduce the State’s accumulated unpaid bills by paying State

vouchers incurred prior to July 1, 2017

Authorization for the Comptroller to reallocate in Fiscal Year 2018 up to $292.8 million from specific funds

Authorization for the Comptroller to temporarily transfer balances in other State funds in State Treasury to

General Funds or the Health Insurance Reserve Fund prior to December 31, 2018

– Any such interfund borrowing amounts are required to be paid back within 24 months of the borrowing

under current statute

– Outstanding interfund borrowing cannot at any time exceed $1.2 billion

As of September 30, 2017, the Comptroller had processed fund reallocations totaling $126 million and

interfund borrowing of $150 million for deposit into the General Revenue Fund

FY 2018 Estimated General Funds Revenues

10 FY 2018 Budget Update

Under current law, General Funds revenues are estimated to total $35.899 billion for FY 2018, a $6.494

billion increase, or 22.1%, from FY 2017 actual revenues

– When compared to the same group of 7 funds in the revised definition, the FY 2018 revenue estimate is

$5.566 billion, or 18.4% higher than in FY 2017

– The FY 2018 numbers also reflect the impact of the direct deposit of income tax and sales tax revenue

sharing with local governments and transit districts, estimated to total $1.558 billion

– Does not include potential revenues from interfund borrowing or fund reallocations

Federal revenue receipts will depend on the amount of reimbursable Medicaid spending and the timing of

the payments by the State, but payments are expected to be more timely in FY 2018. If the Bonds are used

to pay Medicaid bills, additional federal revenues may be received

$millions

FY 2016 FY 2017 FY 2018

$ increase % increase Actual Actual Forecast

(Previous) (Previous) (Sept 2017)

State Sources: Revenues

Net Individual Income Taxes $12,890 $12,737 $17,250 $4,513 35.4%

Net Corporate Income Taxes 1,972 1,328 1,882 554 41.7%

Sales Taxes 8,063 8,043 7,970 (73) -0.9%

Total, Income and Sales Taxes 22,925 22,108 27,102 4,994 22.6%

Other State Revenues and Transfers 3,202 3,272 3,528 256 7.8%

Transfers In1 1,581 1,542 1,713 171 11.1%

Total State Sources 27,708 26,922 32,343 5,421 20.1%

Federal Sources 2,665 2,483 3,556 1,073 43.2%

Total Resources $30,373 $29,405 $35,899 $6,494 22.1%

1. Cash Basis. Does not include transfers from Budget Stabilization Fund or for FY 2018 interfund borrowing or fund reallocations. Note: General Funds in FY 2018 was

expanded to include 3 additional funds (the Commitment to Human Services Fund, Fund for the Advancement of Education, and the Budget Stabilization Fund) to a

total of 7 funds. FY 2017 and earlier reflects the original definition.

Estimated Spending for FY 2018 Budget Outlook

11 FY 2018 Budget Update

The estimated spending for the enacted FY 2018 General Funds budget is $37.4 billion

– Estimated spending from appropriations of $33.9 billion

– Debt service transfers to the GOBRI fund, including amounts needed for the Bonds, is estimated to total $2.9 billion

– Transfers to other State Funds is $573 million, significantly below previous year due to the direct deposit of local governments revenue sharing

The State’s base spending commitments are expected to exceed forecasted revenues by approximately

$1.5 billion

The FY 2018 General Funds budget will likely show a surplus reporting on a reporting basis due to:

– The transfer of a portion of the Bonds to the General Revenue Fund after issuance

– Potential additional federal revenues above the current federal revenue estimate if a portion of the Bonds are used to pay Medicaid bills

– Utilization of interfund borrowing and fund reallocations by the Comptroller in FY 2018

General Funds Expenditures1 ($billions)

FY 2018 Projected

Operating Budget (from Appropriations) $33.9

GO Bond Debt Service Transfers 2.9

Other Statutory Transfers 0.6

Estimated Total $37.4

1. Expenditures are GOMB estimates.

3. Pensions

Actuarial Assets as of June 30, 2016 were $81.5 billion and the Asset Market Value was $78.2

billion

The State Retirement Systems, in aggregate, were funded at 39.2% as of FY 2016 based on the

asset smoothing method and 37.6% using asset market value; individual percentages for each

fund vary

FY 2016 valuations show the impact of a reduction in funding levels due to actual returns

performing at lower than assumed rates of return in FY 2016 and the reduction in the assumed

investment rates of return by TRS and SERS and other SERS assumption changes

FY 2017 valuations and FY 2019 contributions will be available from the systems by November

1st. By statute, actuarial reports must be approved by each of the five systems’ boards before

then and forwarded to the State Actuary

SURS: October 19th

JRS and GARS: October 20th

TRS: October 26th

SERS: October 31st

End of Fiscal Year 2016 Pension Status

12 Pensions

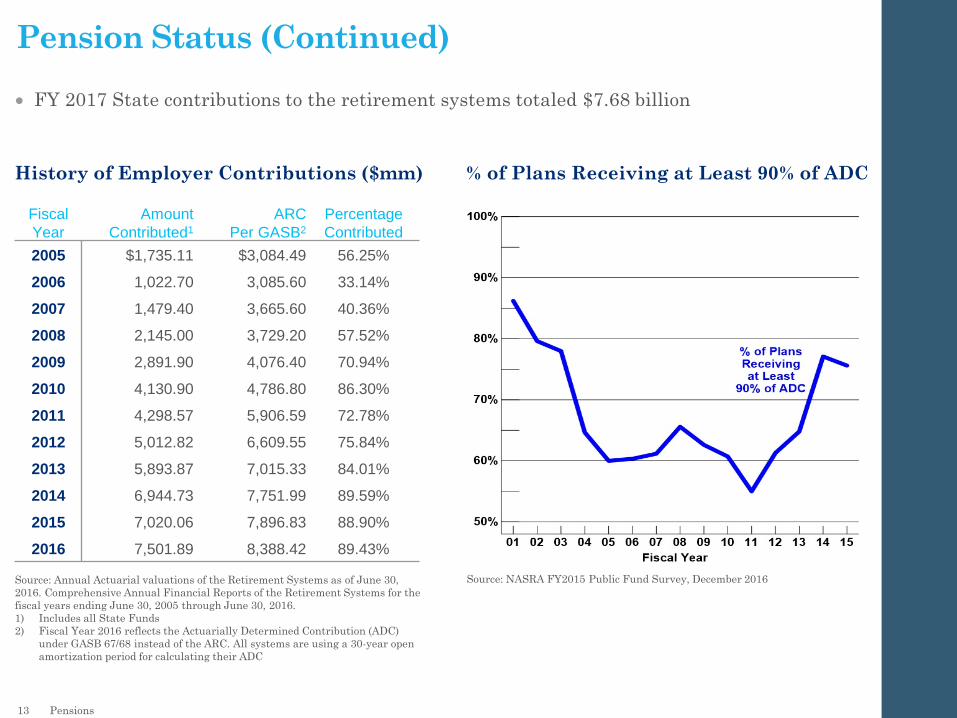

Pension Status (Continued)

History of Employer Contributions ($mm)

Source: Annual Actuarial valuations of the Retirement Systems as of June 30,

2016. Comprehensive Annual Financial Reports of the Retirement Systems for the

fiscal years ending June 30, 2005 through June 30, 2016.

1) Includes all State Funds

2) Fiscal Year 2016 reflects the Actuarially Determined Contribution (ADC)

under GASB 67/68 instead of the ARC. All systems are using a 30-year open

amortization period for calculating their ADC

Fiscal

Year

Amount

Contributed1

ARC

Per GASB2

Percentage

Contributed

2005 $1,735.11 $3,084.49 56.25%

2006 1,022.70 3,085.60 33.14%

2007 1,479.40 3,665.60 40.36%

2008 2,145.00 3,729.20 57.52%

2009 2,891.90 4,076.40 70.94%

2010 4,130.90 4,786.80 86.30%

2011 4,298.57 5,906.59 72.78%

2012 5,012.82 6,609.55 75.84%

2013 5,893.87 7,015.33 84.01%

2014 6,944.73 7,751.99 89.59%

2015 7,020.06 7,896.83 88.90%

2016 7,501.89 8,388.42 89.43%

% of Plans Receiving at Least 90% of ADC

Source: NASRA FY2015 Public Fund Survey, December 2016

FY 2017 State contributions to the retirement systems totaled $7.68 billion

13 Pensions

Pension Assumptions

Investment Rate of Return Assumptions Used by

the Retirement Systems

2009 2016

TRS 8.50% 7.00%

SURS 8.50% 7.25%

SERS 8.50% 7.00%

GARS 8.00% 6.75%

JRS 8.00% 6.75%

Source: Comprehensive Annual Financial Reports, Fiscal Year 2016; NASRA Issue Brief: Public Pension Plan Investment Return Assumptions, February 2017

Change in Distribution of Public Pension

Investment Return Assumptions, FY 2001-2015

14 Pensions

Senate Bill 42 (P.A. 100-0023) Includes Several Reforms to Illinois’ Pension Systems

Introduction of Tier 3 Optional Hybrid Plan - Tier 3 will offer a hybrid DB and DC plan

The small defined benefit has a multiplier of 1.25% of pensionable salary per years of service

In addition to the defined benefit, members of Tier 3 will get a defined contribution plan

Employees are to contribute a minimum of 4% of their salary and employers are to contribute no less than 2%, but no more than 6% of salary

The systems do not expect to implement the Tier 3 plan within FY 2018 and are not projecting an implementation date

Local Cost Shift - One key aspect of Tier 3 reforms is that school districts, universities and community colleges will assume the normal costs of benefits for their new hires upon implementation of a Tier 3 plan, regardless of whether the employee chooses a Tier 3 Optional Hybrid benefit or a more traditional Tier 2 defined benefit plan

To smooth the transition to Tier 3, the State will supplement the costs of local employers by paying 2% of employee payroll through fiscal year 2020 for all members of Tier 3

Additionally, starting July 1, 2017 local employers in SURS and TRS will also assume the normal cost of benefits for the portion of benefits attributable to all members’ salaries that exceed the Governor’s salary

5-Year Smoothing of Contributions - If systems change their actuarial assumptions, P.A. 100-0023 also contains reforms to how the State realizes those changes in its contributions

Beginning in FY 2018, the impact on the State's contributions from any changes each year in actuarial assumptions is smoothed over 5 years. Smoothing in FY 2018 reflects the impact of changes from FY 2014-FY 2017

The State’s FY 2018 original certified contributions in January 2017 totaled $8.843 billion of all funds, of which $7.813 billion was general funds

As required by SB42, the systems will recertify the State’s FY 2018 contributions taking into account the changes made in the new legislation

The recertified FY 2018 State contributions is expected to total $7.910 billion of all funds, of which $6.983 billion is general funds

Pension Update

15 Pensions

4. Debt Overview

General Obligation bonds are backed by the full faith and credit of the State

There is a continuing appropriation in place to ensure bond repayment without action by the General Assembly

Statutory provisions give priority to debt service over other State expenditures

GOBRI is a separate fund in the Treasury that can be applied to debt service payable on GO bonds and short-

term debt

Segregation of funds for debt service begins 12 months in advance for principal payments and 6 months in

advance for interest payments

Average life of all outstanding GO Bonds is approximately nine years

General Obligation Debt Service2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

$B

illi

on

s

Principal Interest

Current Par Outstanding

Capital Improvement Bonds $13.7 billion

Pension Bonds $11.0 billion

Total $24.7 billion

Fixed

Rate

98%

1. Waiver expected prior to posting POS. 2. As of 6/30/2017

Debt service declines

by $978 million once

pension bonds are

paid off in 2019

General Obligation Bond Overview

Hedged

Variable

Rate

2%

16 Debt Overview

Monies are transferred monthly to the GOBRI Fund and, by law, are used for the payment of GO Bonds issued under the Bond Act

and for the payment of Short-Term Debt

The Bond Act constitutes an irrevocable and continuing authority for and direction to the Treasurer and Comptroller to make the

necessary transfers to the GOBRI Fund

Approximately $2.816 billion in transfers from General Funds to GOBRI are estimated for FY 2018 with the balance expected to come

from other State funds

– In FY18, the State transfers will average approximately $250 million a month from General Funds to GOBRI after the issuance of the

Bonds and the capital projects bonds

– General Funds State Source Revenues available to make General Revenue Fund debt service total approximately $2.6 billion per

month on average and provide approximately 10.4x coverage on the amount required to be transferred into GOBRI each month for

General Funds share of debt service, after the issuance of the Bonds

As of September 30, 2017, $1.387 billion was available in GOBRI

Transfers to the GOBRI Fund ($Millions)2

Fiscal Year All Fund Cash Balances1

2013 2014 2015 2016 2017

General Revenue Fund

Capital Bonds $ 548.8 $ 602.9 $ 591.6 $ 556.5 $626.4

Pension Bonds 1,554.6 1,655.4 1,502.2 1,422.6 1,608.7

Road Fund 359.3 358.7 346.7 333.7 305.2

School Infra Fund 209.5 208.8 192.8 211.8 115.2

Capital Projects Fund 310.1 344.2 388.0 532.5 477.0

TOTAL $2,982.3 $3,170.0 $3,021.4 $3,057.1 $3,132.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2012 2013 2014 2015 2016 2017

$B

illi

on

s

1. Does not include Federal Trust Funds. Includes GOBRI. June 30, 2016 balances show an increase from FY 2015 due in part to the late enactment of FY 2016 appropriations for many State

funds.

2. Does not include debt service transfers on short-term debt as may have been from time to time outstanding

Strength of the State’s GO Pledge

17 Debt Overview

Interest Rate Swap Agreements

In 2003, the State executed five separate interest rate exchange agreements to hedge the variable rate of all $600 million of the Series 2003B Bonds at an effective fixed rate. The State pays a fixed interest rate of 3.89% and receives variable rates as shown below

In 2017, the State negotiated with the counterparties to change the agreements to have terms more favorable to the State, inc luding lowering the ratings triggers on all of its swaps

Interest Rate Exchange Agreements

Swap Counterparty Current Aggregate

Notional Amount

Fixed Rate

Paid Variable Rate Received

Additional Termination

Event Against Illinois

Mark-to-Market

as of 6/30/2017

Barclays Bank PLC1 $54,000,000 3.89% 82.7% of 1M LIBOR Below Ba1 or BB+ $(9,322,425)

Barclays Bank PLC2 54,000,000 3.89% 80.82% of 1M LIBOR Below Ba1 or BB+ (9,499,002)

Bank of America, N.A. 54,000,000 3.89% SIFMA3 Below Ba1 or BB+ (10,071,330)

JP Morgan Chase Bank, N.A. 54,000,000 3.89% SIFMA3 Below Ba1 or BB+ (10,071,330)

Deutsche Bank AG 384,000,000 3.89% SIFMA3 Below Ba1 or BB+ (71,618,343)

Total $600,000,000 $(110,582,430)

Variable Rate Bonds

The letters of credit expired in November 2016. To replace those letters of credit, the State entered into direct placements

The Series October 2003B Bonds were purchased on November 7, 2016 by four banks. The direct placements have a term of two years

and will expire on November 7, 2018. There is no acceleration risk as a result of a downgrade, only an increase in rates

Series 2003B Bonds

Owner Principal Amount Interest Rate Mode Sub-series

DNT Asset Trust4 $226,000,000 LIBOR 2003B-1

PNC Bank, National Association 224,000,000 LIBOR 2003B-2

State Street Public Lending Corporation5 75,000,000 LIBOR 2003B-3

RBC Municipal Products, LLC6 75,000,000 SIFMA 2003B-4

Total $600,000,000

1. Transaction was novated from AIG Financial Products to Barclays Bank on August 23, 2016. As part of the novation, the LIBOR barrier option was removed 2. Transaction was novated from Merrill Lynch Capital Services to Barclays Bank on

September 12, 2016. As part of the novation, the LIBOR barrier option was removed. 3. The variable rate received is 67% of 1 month LIBOR when 1 month LIBOR is ≥ 2.5%, or SIFMA, when 1 month LIBOR is < 2.5%. 4. An affiliate of JPMorgan Chase

Bank, National Association 5. An Affiliate of State Street Bank and Trust Company 6. An Affiliate of Royal Bank of Canada

The State Has Actively Managed Its Debt Obligations

18 Debt Overview

Debt Service - Illinois limits debt service expenditures to no more than 7 percent of General Funds and Road Fund appropriations, unless the transaction is specifically exempted by statute

Capital Expenditures - The State annually forecasts and analyzes revenues available for capital expenditures

The State conducts a formal capital planning process to rank projects based on specific criteria and evaluates the impact of new capital spending on the operating budget

The State performs facility management and condition assessments in order to provide information and recommendations for current and future capital expenditures

Strategic Fiscal Policies - the State has developed a series of fiscal priorities to help achieve a balanced budget. These include:

Reducing the State's pension liabilities

Maintaining debt affordability processes for capital programs

Funding key priorities

Implementing new revenue streams that reflect the State’s economic base

Investing in the economy and the State’s infrastructure

Containing costs and improving efficiency of State operations, IT efficiencies, and structural changes to grow the economy

Financial Management Policies

19 Debt Overview

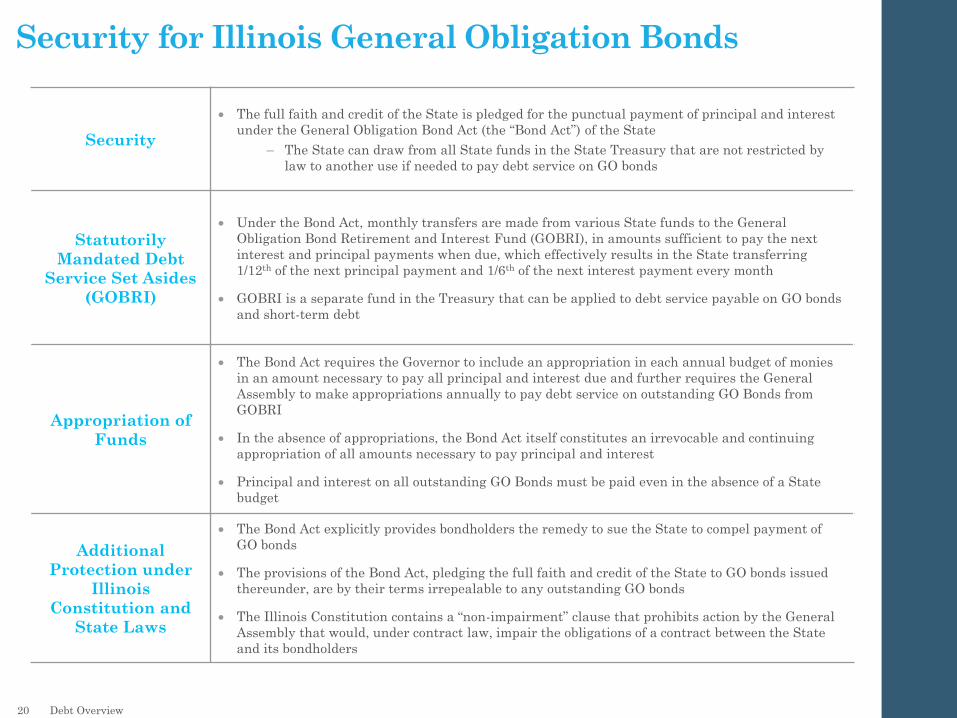

Security

The full faith and credit of the State is pledged for the punctual payment of principal and interest

under the General Obligation Bond Act (the “Bond Act”) of the State

– The State can draw from all State funds in the State Treasury that are not restricted by

law to another use if needed to pay debt service on GO bonds

Statutorily

Mandated Debt

Service Set Asides

(GOBRI)

Under the Bond Act, monthly transfers are made from various State funds to the General

Obligation Bond Retirement and Interest Fund (GOBRI), in amounts sufficient to pay the next

interest and principal payments when due, which effectively results in the State transferring

1/12th of the next principal payment and 1/6th of the next interest payment every month

GOBRI is a separate fund in the Treasury that can be applied to debt service payable on GO bonds

and short-term debt

Appropriation of

Funds

The Bond Act requires the Governor to include an appropriation in each annual budget of monies

in an amount necessary to pay all principal and interest due and further requires the General

Assembly to make appropriations annually to pay debt service on outstanding GO Bonds from

GOBRI

In the absence of appropriations, the Bond Act itself constitutes an irrevocable and continuing

appropriation of all amounts necessary to pay principal and interest

Principal and interest on all outstanding GO Bonds must be paid even in the absence of a State

budget

Additional

Protection under

Illinois

Constitution and

State Laws

The Bond Act explicitly provides bondholders the remedy to sue the State to compel payment of

GO bonds

The provisions of the Bond Act, pledging the full faith and credit of the State to GO bonds issued

thereunder, are by their terms irrepealable to any outstanding GO bonds

The Illinois Constitution contains a “non-impairment” clause that prohibits action by the General

Assembly that would, under contract law, impair the obligations of a contract between the State

and its bondholders

Security for Illinois General Obligation Bonds

20 Debt Overview

5. Bill Backlog and Plan of Finance

Medicaid

23.6%

State Employee

Health Insurance

35.1%

All Other

41.3%

0

2

4

6

8

10

12

14

16

Estimated Sept-17 Projected June-18

Estimated Bill Backlog ($billions)

Impact of the Financing on the Bill Backlog

21 Debt Overview and Plan of Finance

$15.1 billion1

$7.5 billion3

GOMB Estimate Composition of the Bill Backlog

(August 2017)

Source: State’s Office of the Comptroller and GOMB Estimates; 1. Comprised of $9.06 billion at the State Comptroller’s office and Comptroller estimate of $6.1 billion held at

State Agencies as of September 30, 2017. 2. Takes into account Comptroller estimates from December 31 and June 30 of each year when calculating the average. 3. GOMB

estimates.

The State is taking prudent and meaningful steps to reduce the amount of outstanding bills

The State’s bill backlog has increased from approximately $5 billion at the end of FY 2015 to approximately $15.1 billion as of September 30, 20171

– Estimated balance of the backlog at the end of FY 2018, as a result of the financing and application of federal funds, will be $7.5 billion, a nearly 50% reduction in the outstanding payables

December

2010-June

2015 Average2

= $7.1 billion

Competitive Transaction Overview

*Preliminary, subject to change.

The State is selling the $1.5 billion Series of November 2017ABC Bonds on a competitive basis

– The 2017ABC Bonds will be concurrently marketed with the $4.5 billion* 2017D Bonds to be sold on a negotiated

basis during the week of October 23rd

Future Financings

– The State plans to price one or more

series of General Obligation Bonds

for capital projects and information

technology projects, estimated at

$750 million, before December 31,

2017

22 Debt Overview and Plan of Finance

Preliminary Amortization ($000s)

Maturity

(November 1st)

November

2017ABC

(Competitive)

2018 $ 500,000

2019 500,000

2029 500,000

Total $1,500,000

General Obligation Bonds, Series of November 2017ABC*

Estimated Size

Series A (2018): 500,000,000

Series B (2019): 500,000,000

Series C (2029): 500,000,000

Total: $1,500,000,000

Method of Sale Competitive

Use of Proceeds To provide funds to pay vouchers previously incurred by the State and to pay costs of issuance

Tax Status Federally Tax-Exempt, State of Illinois Taxable

Coupon Fixed Rate

Amortization Serial bonds due on November 1, 2018-2019, and November 1, 2029

Interest Payment Dates May 1 and November 1, commencing May 1, 2018

Redemption Features 10-Year Par Call (Series C)

Security and

Repayment Source

Direct, full faith and credit general obligations of the State pursuant to the General Obligation Bond Act (the “Bond Act”). The provisions of the Bond Act are irrepealable until all bonds issued under the Bond Act, including the Bonds, are paid in full as to both principal and interest.

Ratings Receive ratings on October 6th & 10th

Sale Date October 17, 2017

Closing Date November 8, 2017

Financial Advisor PFM and PRAG

Preliminary Amortization ($000s)

Maturity

(November 1st)

November

2017D

(Negotiated)

2020 $ 500,000

2021 500,000

2022 500,000

2023 500,000

2024 500,000

2025 500,000

2026 500,000

2027 500,000

2028 500,000

Total $4,500,000

Negotiated Transaction Overview

*Preliminary, subject to change.

Future Financings

– The State plans to price one or more series of General Obligation Bonds for capital projects and information

technology projects, estimated at $750 million, before December 31, 2017

23 Debt Overview and Plan of Finance

General Obligation Bonds, Series of November 2017D*

Estimated Size $4,500,000,000

Method of Sale Negotiated

Use of Proceeds To provide funds to pay vouchers previously incurred by the State and to pay costs of issuance

Tax Status Federally Tax-Exempt, State of Illinois Taxable

Final Maturity November 1, 2028

Coupon Fixed Rate

Amortization Serial bonds due on November 1, 2020-28

Interest Payment Dates May 1 and November 1, commencing May 1, 2018

Redemption Features 10-Year Par Call

Security and

Repayment Source

Direct, full faith and credit general obligations of the State pursuant to the General Obligation Bond Act (the “Bond Act”). The provisions of the Bond Act are irrepealable until all bonds issued under the Bond Act, including the Bonds, are paid in full as to both principal and interest.

Ratings Receive ratings on October 6th & 10th

Sale Date Week of October 23, 2017

Closing Date November 8, 2017

Financial Advisor PFM and PRAG

The State is selling the $4.5 billion Series of November 2017D Bonds on a negotiated basis

– The 2017D Bonds will be concurrently marketed with the $1.5 billion 2017ABC Bonds to be sold on a competitive

basis on October 17th

Financing Overview

Use of

Proceeds

The Bonds are being issued to provide funds to finance capital projects under the State’s capital program, information technology and to pay costs of issuance of the Bonds.

Security

The Bonds are direct, general obligations of the State and, pursuant to Section 9(a) of Article IX of the Illinois Constitution and the General Obligation Bond Act of the State of Illinois, as amended (the “Bond Act”), the full faith and credit of the State is pledged for the punctual payment of interest on all bonds issued under the Bond Act, including the Bonds, as it comes due and for the punctual payment of the principal of all bonds issued under the Bond Act, including the Bonds, at maturity, or on any earlier redemption date, and redemption premium, if any. These provisions are irrepealable until all bonds issued under the Bond Act, including the Bonds, are paid in full as to both principal and interest.

Interest

Payment

Dates

June 1 and December 1, commencing June 1, 2018

Mode Fixed Rate Bonds

Ratings Receive ratings on October 6th & 10th

Pricing* Mid-November

Closing* Early December

*Preliminary, subject to change.

Capital Projects & IT Bonds - Issuance Terms and Schedule

Amortization*

Dec 1 Capital IT

2018 $26,000,000 $9,500,000

2019 26,000,000 9,500,000

2020 26,000,000 9,500,000

2021 26,000,000 9,500,000

2022 26,000,000 9,500,000

2023 26,000,000 9,500,000

2024 26,000,000 9,500,000

2025 26,000,000 9,500,000

2026 26,000,000 9,500,000

2027 26,000,000 9,500,000

2028 26,000,000 -

2029 26,000,000 -

2030 26,000,000 -

2031 26,000,000 -

2032 26,000,000 -

2033 26,000,000 -

2034 26,000,000 -

2035 26,000,000 -

2036 26,000,000 -

2037 26,000,000 -

2038 26,000,000 -

2039 26,000,000 -

2040 26,000,000 -

2041 26,000,000 -

2042 26,000,000 -

Total $655,000,000 $95,000,000

24 Bill Backlog and Plan of Finance

Date Event

October 2nd & 3rd Rating Meetings

October 6th & 10th Receive Ratings

October 6th Post Competitive Bill Backlog POS

October 10th Post Negotiated Backlog POS

October 17th Competitive Bill Backlog Sale

Week of October 23rd Negotiated Bill Backlog Sale

November 8th Bill Backlog Closing

Mid-November Capital Projects Bonds Sale

Early December Capital Projects Bonds Closing

September 2017 October 2017 November 2017

Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat

1 2 1 2 3 4 5 6 7 1 2 3 4

3 4 5 6 7 8 9 8 9 10 11 12 13 14 5 6 7 8 9 10 11

10 11 12 13 14 15 16 15 16 17 18 19 20 21 12 13 14 15 16 17 18

17 18 19 20 21 22 23 22 23 24 25 26 27 28 19 20 21 22 23 24 25

24 25 26 27 28 29 30 29 30 31 26 27 28 29 30

Transaction Timeline

25 Bill Backlog and Plan of Finance