state of the ethekwini economy - … learning exchange 2016...knowledge economy • new knowledge,...

TRANSCRIPT

STATE OF THE

ETHEKWINI ECONOMY KNOWLEDGE IN THE ECONOMY

KNOWLEDGE ECONOMY

• New knowledge, innovation and technological change have become the drivers of progress, growth and wealth in the world’s leading economies

• Reduced reliance on traditional resources such as labour and capital

• Innovation is identified as a driver for economic growth and productivity

• Indicators: – R&D expenditure

– patent data and bibliometric data; scientific publications and citations,

HIGH LEVEL ISSUES ON THE GLOBAL

ECONOMY

1. Period of low growth - Developing

markets are under pressure due to

• appreciation of US$,

• risk aversion and

• drop in commodity prices

• slowdown of China & BRICS (Look to

India for future opportunities)

2. Opportunities presented by deliberate

expansion of China into developing

economies; but caution advised.

3. Dramatic drop in oil price.

4. The 4th Industrial Revolution will impact

the way business and government is run

and bring challenges.

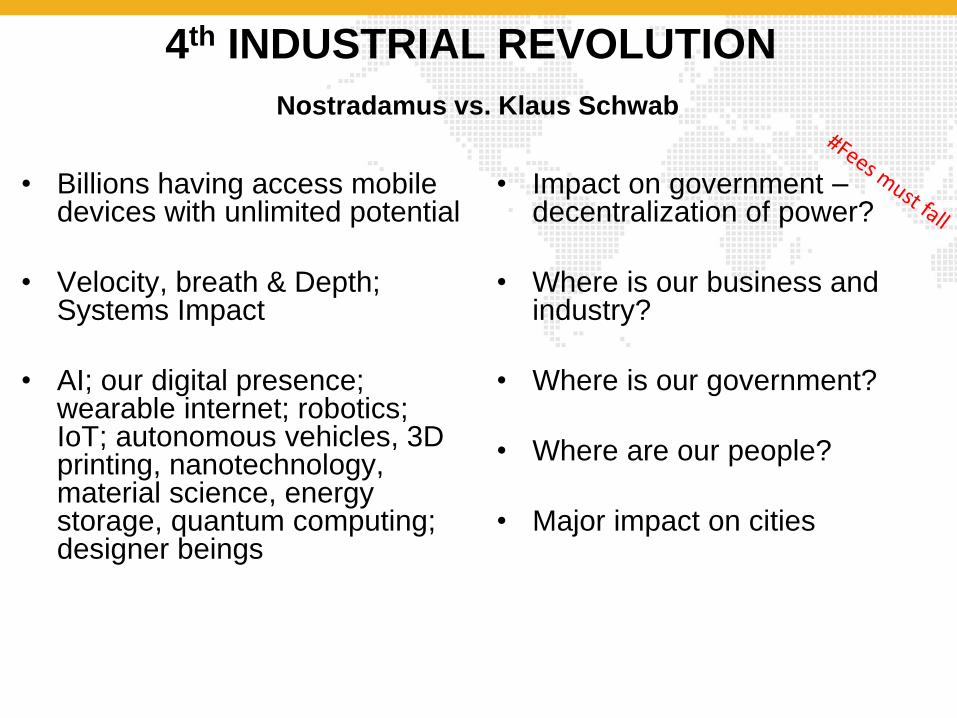

4th INDUSTRIAL REVOLUTION

Nostradamus vs. Klaus Schwab

• Billions having access mobile devices with unlimited potential

• Velocity, breath & Depth; Systems Impact

• AI; our digital presence; wearable internet; robotics; IoT; autonomous vehicles, 3D printing, nanotechnology, material science, energy storage, quantum computing; designer beings

• Impact on government – decentralization of power?

• Where is our business and industry?

• Where is our government?

• Where are our people?

• Major impact on cities

“We’re poised to experience more digital progress in the next 10

years than we have in the last 50” – Denis O’Brien Chairman of Digicel

2018 2021 2022 2023 2024 2025 2026 2027

Storage for all

Robot & services

- The internet of and for things

- Wearable internet

- 3D printing & manufacturing

- Implantable technologies

- Big data decisions

- Vision as new interface

- Our digital presence

- Governments & the blockchain

- A supercomputer in your pocket

- Ubiquitous computing

- 3D printing & human health

- The connected home

- 3D printing & consumer products

- AI & white collar jobs

- The sharing economy

- Driverless cars

- AI & decision making

- Smart cities

- Bitcoin & the blockchain

Average year each tipping point is expected to occur

ISSUES ON THE AFRICAN

ECONOMY 1. Africa is experiencing robust growth in particular markets and it is anticipated

that the growing young middle class will attract investment,

2. South Africa has an opportunity to expand further into African urban markets.

3. Egypt “now” Africa’s 2nd largest economy; but this is result of rebasing and

puts economy size in perspective

4. Cities to look out for: Lagos, Lusaka and Kinshasa (South African cities are

slipping in the rankings).

Internet and Patents

Ranking internet speed in Africa

1. Ghana

2. Zimbabwe

3. Kenya

4. Libya

5. Madagascar

6. South Africa (and 8th in

internet penetration in Africa)

World Intellectual Property Organisation

(WIPO) Patent Registrations 2013

• Africa: 500 of 205 000

• 351 international applications

from South Africa

• Morocco had 54 filings, Nigeria

and Kenya had seven each.

• Patent protection is still embryonic

on the fast-growing continent.

SOUTH AFRICAN ECONOMY AT A GLANCE

A diverse and resilient economy, that is under

severe pressure

SUMMARY: STATE OF SA ECONOMY

• South Africa remains a sound economy, not at all far from repair. IMF recommends the

following in order to reach 5% growth rate:

“…Improving electricity supply, enhanced competition in product markets, a more

inclusive labour market, and … an education system that provides SA’s youth with the

best education possible"

Input costs

Demand and Output

• Inflation

• Electricity

• Municipal costs

• Labour

• Logistics

• Imported materials

• Red tape

• Fuel

• Water

• Infrastructure

• Drought

• Slower demand

• Productivity

• Commodity prices

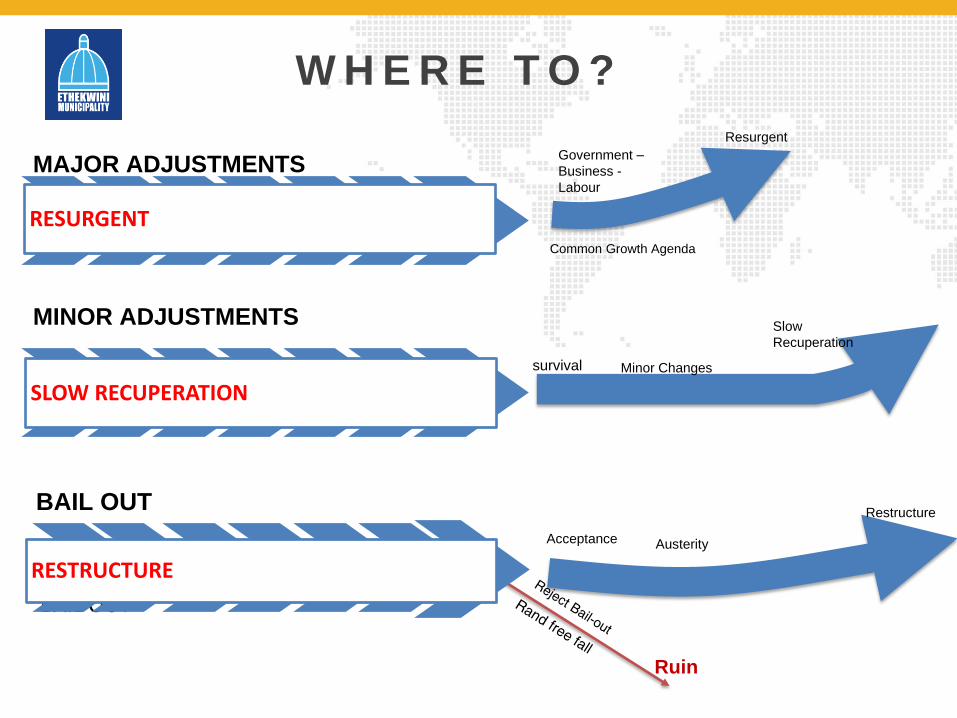

T H E B I G R I S K S A C R I S I S O F P O L I T I C A L E C O N O M Y

Social

Demands

Po

litica

l Ou

tloo

k

Austerity

Restructure

Ruin

survival Minor Changes

Resurgent

Government –

Business -

Labour

Common Growth Agenda

Slow

Recuperation

Acceptance

MAJOR ADJUSTMENTS

RESURGENT

MINOR ADJUSTMENTS

SLOW RECUPERATION

BAIL OUT

RESTRUCTURE

BAIL OUT

W H E R E T O ?

Moody’s did not downgrade SA, but the outlook is still negative. South Africa still at investment

grade because of Moody’s view that SA growth likely to gradually strengthen. Outlook on SA:

• Supply-side shocks from 2014 receded (Eskom reduced load shedding, the drought is

ending and the number of work days lost to strikes has shrunk significantly)

• Inflation outlook is more subdued

• Interest rates less likely to increase as inflation decreases. Households less under pressure.

• Country growth rate expected to increase to 1.5% in 2017.

• Efforts by government to engage business

• Reassessment of SOE operations

• Aggressive budget consolidation measures

• Gross govt debt expected to stabilize in the current fiscal year to 51% of GDP.

• Strength and independence of South Africa’s systems and institutions

BUT OUTLOOK STILL NEGATIVE BECAUSE:

• There are still risks associated with the growth, fiscal and political outlook

• Possibility of renewed volatility in global financial markets

SA STILL SEEN AS ECONOMICALLY SOUND BUT

MOODY’S TO KEEP AN EYE ON SA GVT PROGRESS AND REASSESS AGAIN

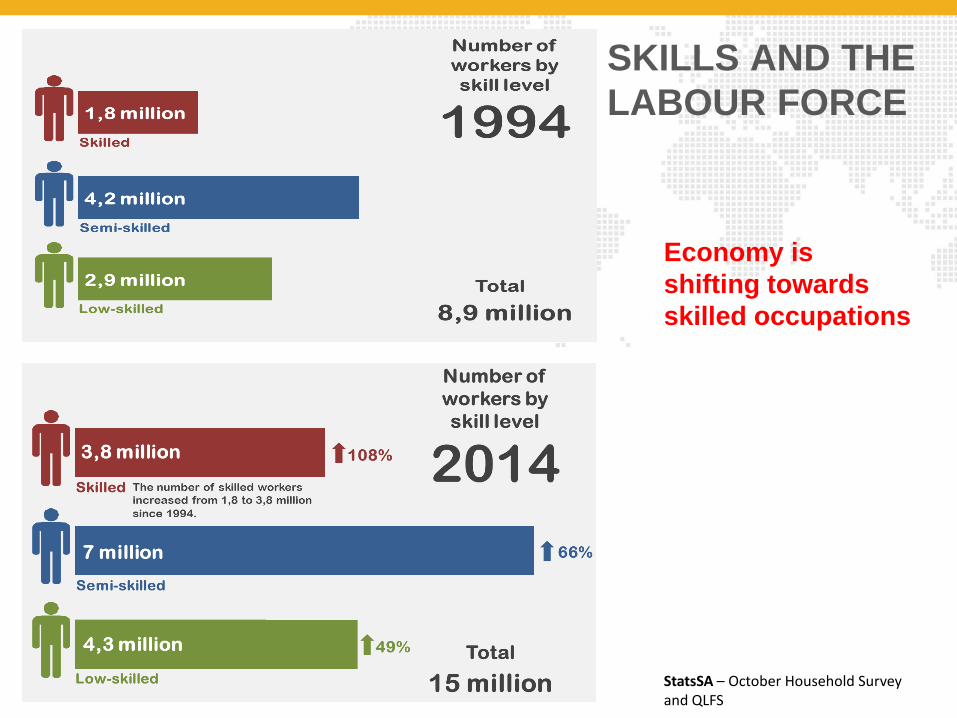

Economy is

shifting towards

skilled occupations

StatsSA – October Household Survey and QLFS

SKILLS AND THE

LABOUR FORCE

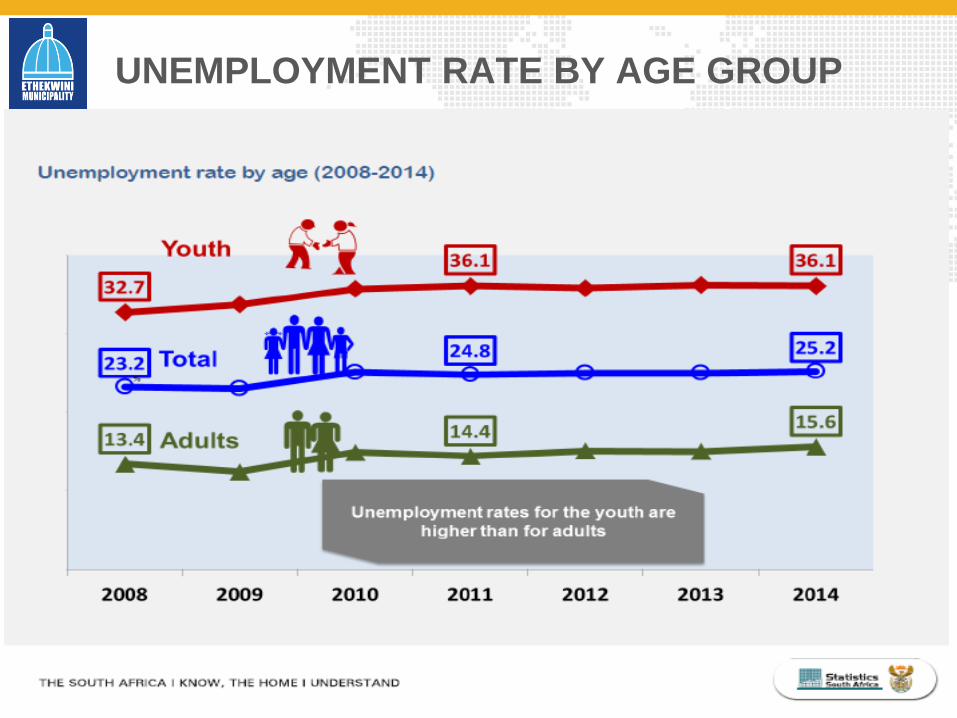

UNEMPLOYMENT RATE BY AGE GROUP

THE EDUCATION SYSTEM

National Development

Plan: CH9

SA faces a low growth, middle income trap, characterized by: • Weak competition • High

unemployment • Low savings • A poor skills profile

• The quality of education for most Black children is poor

• By the end of Grade 12, SA has lost half of every cohort entering the school system

………..”Which wastes human potential and harms life-chances of our youth”

STATE OF ETHEKWINI ECONOMY

There are difficult economic times ahead which will be worsened by

the resource crisis and political outlook. Innovation and efficiency

are required for the economy to survive, and thrive

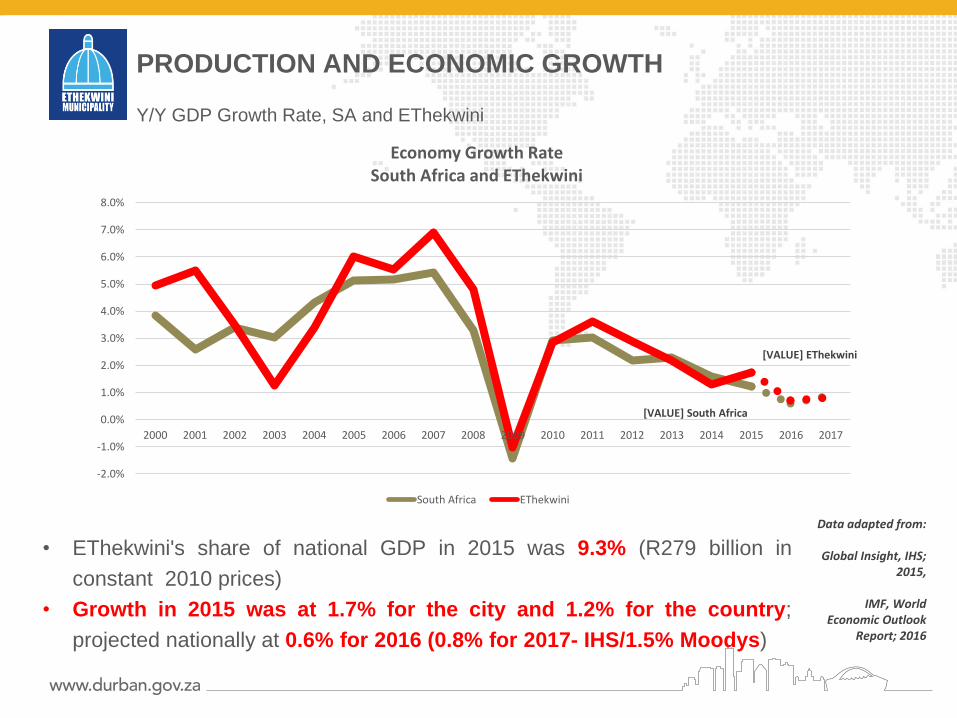

PRODUCTION AND ECONOMIC GROWTH

• EThekwini's share of national GDP in 2015 was 9.3% (R279 billion in

constant 2010 prices)

• Growth in 2015 was at 1.7% for the city and 1.2% for the country;

projected nationally at 0.6% for 2016 (0.8% for 2017- IHS/1.5% Moodys)

Data adapted from:

Global Insight, IHS; 2015,

IMF, World

Economic Outlook Report; 2016

Y/Y GDP Growth Rate, SA and EThekwini

[VALUE] South Africa

[VALUE] EThekwini

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Economy Growth Rate South Africa and EThekwini

South Africa EThekwini

• Total GDP in 2015 = R278,9 billion

(Constant 2010 Prices).

• Services now account for 75% of the

City’s economy.

• Main sectors in EThekwini’s economy–

community services, finance,

manufacturing and trade.

• EThekwini is two speed economy;

partially a mature, stagnant (in

secondary sector) economy,

dominated by rapid growth by the

tertiary sector.

Data from Global Insight, IHS; 2016

Primary Sector

Secondary Sector

Tertiary Sector

Agriculture 1%

Mining 0%

Manufacturing 17%

Electricity 2%

Construction 5%

Trade 16%

Transport 16%

Finance 22%

Community services

21%

GVA Composition of EThekwini in 2015

ETHEKWINI’S ECONOMIC COMPOSITION

• The significance of primary sector

has been reducing

• After the economic recession of 2008-

09, the secondary sector has

experienced very slow growth driven

mainly by construction, while

manufacturing has been relatively

stagnant

• McKinsey 2015 place emphasis on

advanced manufacturing

• Manufacturing’s best performers have

been food & beverage and the fuel

petroleum chemicals and rubber

products followed by transport

equipment

• The tertiary sector has experienced the

biggest growth

• The best performers have been wholesale

& retail trade, finance, community

services followed by land and water

transport.

• Mediocre performance of tourism sector

• Shifts away from unskilled and towards

semi-skilled and increasingly sectors

requiring higher skills.

SECTORAL TRENDS

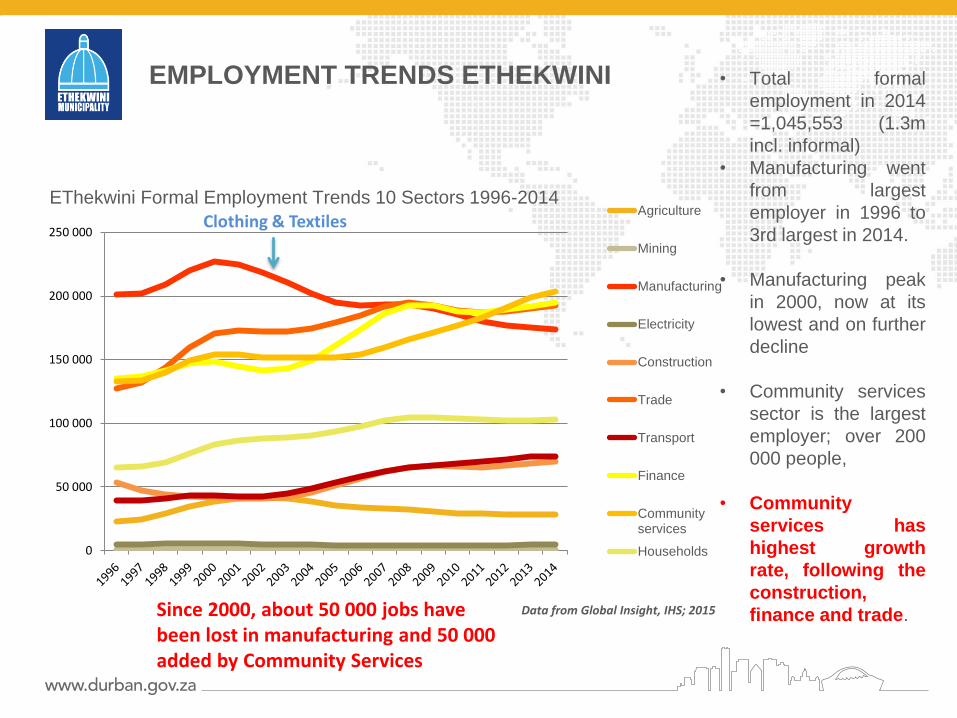

ETHEKWINI LABOUR MARKET

EMPLOYMENT TRENDS ETHEKWINI

0

50 000

100 000

150 000

200 000

250 000

EThekwini Formal Employment Trends 10 Sectors 1996-2014 Agriculture

Mining

Manufacturing

Electricity

Construction

Trade

Transport

Finance

Communityservices

Households

Data from Global Insight, IHS; 2015

• Total formal

employment in 2014

=1,045,553 (1.3m

incl. informal)

• Manufacturing went

from largest

employer in 1996 to

3rd largest in 2014.

• Manufacturing peak

in 2000, now at its

lowest and on further

decline

• Community services

sector is the largest

employer; over 200

000 people,

• Community

services has

highest growth

rate, following the

construction,

finance and trade.

Clothing & Textiles

Since 2000, about 50 000 jobs have been lost in manufacturing and 50 000 added by Community Services

EMPLOYMENT TRENDS ETHEKWINI

Data from Global Insight, IHS; 2015

0

20 000

40 000

60 000

80 000

100 000

120 000

199

6

199

7

199

8

199

9

200

0

200

1

2002

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

Informal Employment Trends 10 Sectors 1996-2014

Manufacturing

Construction

Trade

Transport

Finance

Communityservices

• Trade is by far

the highest

employer in

the informal

sector.

• The second

highest

employer is

construction,

and then

community

services.

• The informal

sector has

been growing

significantly.

UNEMPLOYMENT AND DISCOURAGED WORKERS

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

ET

hekw

ini M

etr

opolit

an

Mu

nic

ipalit

y

City o

f C

ape

Tow

n

Buffa

lo C

ity M

etr

op

olit

an

Mu

nic

ipalit

y

Tshw

an

e M

etr

op

olit

an

Mu

nic

ipalit

y

Ne

lson M

an

dela

Bay

Me

tropo

litan

Mun

icip

alit

y

Ma

nga

ung

City o

f Joh

ann

esburg

Eku

rhule

ni

StrictUnemploymentRate

DiscouragedWorkers

2016 Q1 Unemployment and Discouraged Workers in all Metros • EThekwini has lowest

strict unemployment

rate in the country; and

the third highest

proportion of

discouraged workers

• The growth in young

people entering the

working age bracket is

not yet being absorbed

by the labour force

• The labour force participation rate is dropping and the non-economically active

are increasing

• Note: According to Stats SA; Between Q4 2015 and Q1 2016, EThekwini spots an unusual

12% decrease in unemployment. Further queries are being made into these results.

Data from 2016 Q1 Quarterly Labour Force Survey, Statistics SA; 2015

BREAKDOWN OF THE WORKING AGE POPULATION IN

ETHEKWINI

0

200000

400000

600000

800000

1000000

1200000

1400000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Employed

Unemployed

Not econ.active

Weighted

CAGR

2008-2013

-0.1%

2.1%

-0.1%

Employed vs. Unemployed vs. Not Economically Active in EThekwini 2008 - 2013

• The not economically active of EThekwini are the main contributing factor to the drop in

the percentage of those unemployed. They are also growing at a positive rate of 2.1%,

compared to employed and unemployed which are growing at a rate of -0.1%.

Data from Quantec Standardised Regional Data, 2015

ETHEKWINI BUSINESS CLIMATE

DOING BUSINESS IN ETHEKWINI VS. OTHER SA METROS

Municipality

Municipal Seat

Starting a

business

Dealing with

construction

permits

Getting electricity Registering

property Enforcing contracts

Ranking

(1-9)

DTF

score

(100 =

best

result)

Ranking

(1-9)

DTF

score

(100 =

best

result)

Ranking

(1-9)

DTF

score

(100 =

best

result)

Ranking

(1-9)

DTF

score

(100 =

best

result)

Rankin

g (1-9)

DTF score

(100 = best

result)

Buffalo City, East

London 4 78.67 3 77.50 4 75.32 4 62.84 9 62.54

Cape Town 4 78.67 1 78.08 2 81.81 8 59.23 6 67.53

Ekurhuleni, Germiston

1 81.18 4 76.84 5 71.83 3 64.23 4 68.26

EThekwini, Durban 4 78.67 5 76.15 3 75.73 6 62.05 3 69.27

Johannesburg 1 81.18 8 68.52 8 55.74 1 65.82 8 66.14

Mangaung,

Bloemfontein 4 78.67 9 68.22 1 83.88 9 58.41 1 71.04

Msunduzi,

Pietermaritzburg 4 78.67 6 74.07 7 63.00 7 59.49 2 70.81

Nelson Mandela Bay,

Port Elizabeth 4 78.67 2 78.05 9 53.14 5 62.69 7 66.89

Tshwane, Pretoria 1 81.18 7 69.88 6 68.51 2 64.71 5 68.17

INVESTMENT IN ETHEKWINI

• Improvements required in registering a business, getting construction

permits and enforcing a contract.

• Is the public sector keeping pace with technological change? How

will this impact the economy?

• Investment in the secondary sector indicates strong mechanisation

trends which is good for competitiveness, but also an indication of the

need for more relevant, competitive labour

• Smart to Future cities – Smart cities to digital citizens

CITY INVESTMENT: MUNICIPAL BUDGET

• Good financial standing; credit rating; cash on hand and debt to own revenue.

• Data for 2013 – 2014 suggests a slight decline in income tax and company tax

payers. However revenue has increased.

• High spending on the Social programme is not sustainable or achievable

(50-year period)

• Spending towards knowledge and economic drivers

ETHEKWINI POVERTY AND SERVICE

DELIVERY

POVERTY

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%1

99

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

City of Cape Town

EThekwini

Ekurhuleni

City of Johannesburg

Nelson Mandela Bay

City of Tshwane

Mangaung

Buffalo City

People Living Below the Food Poverty Line per Metro, 1996- 2014: Percentage and Number

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

City of Cape Town

EThekwini

Ekurhuleni

City of Johannesburg

Nelson Mandela Bay

City of Tshwane

Mangaung

Buffalo City

OBSERVATIONS

OBSERVATIONS ON THE NATIONAL ECONOMY

1. The global economy is under pressure, and

impacting negatively on high risk

developing economies

2. Not withstanding the growth prospects for

Africa are good

3. Domestic factors: Gvt is trying hard and

making strides in aiming to address.

4. Social factors such as inequality and

joblessness are resulting in high social

demands.

5. Economic growth is fundamental and jobs

creation requires inclusive growth

6. How do we address the past and embrace

the future? CANT DO ONE

6. Declining private sector confidence is

constraining investment

7. Cities are centres of innovation. The

competitiveness of the cities are becoming

increasingly important to national economic

growth, but they need to be more efficient &

enabled

8. Developed economy is demanding skills

9. Many youth are being left behind

10. What is the future of jobs?

11. In 10 years 39% of South African jobs will be

disrupted (WEF)

12. Smsrt to future Cities - Cities must be citizen

centric (digital citizens!)

Government, Labour & Business need

to align to a national agenda

1. EThekwini's growth prospects are strongly

linked to the national picture. Biggest sectors are

global and vulnerable

.

2. Progress has been made on addressing

poverty, but education remains a challenge

3. City’s financial status remains strong, however

sustainability concerns.

4. The local economy has shifted

5. The main growth sectors are consumption related

and government

6. The official unemployment figures do not

reflect the real level of unemployment and

joblessness

7. Small number of employed and tax base

8. Technology and mega events - 2022

8. Labour – skills and productivity form part of the

unemployment problem – skills crises will deepen

9. There is a large youthful population – a big focus

on skills development could have a positive impact

10. Energy and water are placing a significant strain on

the economy (incl water pressure)

11. Local steel industry under pressure

12. Manufacturing survey: Skills mismatch is a major

problem

13. Red tape – WHERE IS THE SMART CITY?

14. Persistent; structural inequality poses a key risk to

the city’s future

15. The global business environment is changing,

are Durban firms ready – are we ready?

OBSERVATIONS ON THE LOCAL ECONOMY

1. The depreciation of the rand presents opportunities for local sourcing, beneficiation and

local production. However, this will take time and effort to achieve.

2. Despite the global and national challenges, a number of issues, such as red tape, are

within the control of the Municipality to address. Improve efficiency

3. Catalytic investments – investments in knowledge intensive industries

4. IRPTN and public transport orientated development – Room for Innovation

5. A good credit rating - enables city to better finance economic infrastructure

6. Localisation

7. Innovation and technology presents an opportunity to increase efficiency and solve

city problems

8. Durban has developed an innovation programme – how can we bridge the skills gap

9. Open data – open government

10. There is an emerging innovative cluster with crosspollination of technology &

creativity

11. Commonwealth Games - 2022

GREEN SHOOTS

Strong economic leadership that builds business confidence, drives

Implementation and improves internal efficiency will be key to rescue the

economy and lead us to the future