state strength, industry structure and industrial...

TRANSCRIPT

STATE STRENGTH, INDUSTRY STRUCTURE AND INDUSTRIAL POLICY: American and Japanese Experiences in Microelectronics

Glenn R. Fong Department of Political Science University of Illinois at Chicago

Appeared in Comparative Politics, v.22, n.3 (April 1990)

STATE STRENGTH, INDUSTRY STRUCTURE AND INDUSTRIAL POLICY: American and Japanese Experiences in Microelectronics

Increasing attention has been devoted to public and private sector capacities to maneuver in a global political economy of heightened industrial competition and persistent economic dislocation. In policy terms, debate has raged over the role and capabilities of governments in supporting industries, and over the need for private enterprises to undergo restructuring to gain or maintain competitiveness.1 Scholarly inquiries have investigated the differential capacities of national political economies. Comparative analysis points to certain countries whose public and private institutions enjoy relative advantages in competing in the world economy.2 This article offers case studies of two technology programs that provide revealing insight into public and private sector capabilities for government-industry collaboration, industrial policy-making3, and multifirm cooperation in Japan and the United States. One case study is the Very High Speed Integrated Circuit (VHSIC) program sponsored by the U.S. Department of Defense. This program was established in 1979 to infuse research and development funds into the electronics industry and advance the state-of-the-art in integrated circuitry. Some 25 companies ranging from major computer manufacturers to merchant semiconductor firms were on the receiving-end of VHSIC contracts. The program was budgeted at nearly $1 billion through 1988, and constituted the U.S. government's largest, most ambitious effort in microelectronics since the 1960s. The second case study is Japan's Very Large-Scale Integration (VLSI) project. Established by the Ministry of International Trade and Industry (MITI) in 1976, the VLSI project represents another government-industry effort to develop leading-edge semiconductor technology. Some $300 million was invested in this program through 1980, and five of Japan's leading electronics manufacturers participated in the effort. The project has been singled out as being centrally critical to Japan's current technology thrust and export drive in microelectronics. The two programs sought to promote industries and technologies of immense strategic political and economic value. Semiconductors are very thin squares of silicon material, usually smaller than a postage stamp, which contain miniature circuitry that can store and manipulate information in the form of electrical impulses.4 They have been described as the "industrial rice" of the 1990s and the "crude oil" of modern industry. Semiconductor devices are utilized as vital components in computers, telecommunications, industrial machinery, military equipment, and consumer electronics. The benefits of semiconductors are gained throughout manufacturing, agriculture, and the service sector. National economic wealth and, particularly in the case of America, national security increasingly rest upon advances in technology with microelectronics at the core. The VHSIC program and VLSI project provide penetrating windows on the relative capacities of the American and Japanese political economies. The programs placed rigorous demands upon government institutions and private enterprises by calling for concerted long-range planning, the pooling of public and private resources and expertise, and joint research among competing firms. The responses to such demands should reveal any cross-national differences in government-industry relations, industrial policy-making, and intra-industry relationships. In policy terms, we will be able to reflect upon popular conceptions that Japanese public and private sectors enjoy political

2 as well as economic advantages over their counterparts in America. At the level of theory, the two case studies reflect critically upon two major explanatory frameworks in international and comparative political economy: state capacity and industrial structure analyses. As reviewed in the second section of this article, the two frameworks trace national capacities for industrial policy, government-industry collaboration, and intra-industry cooperation, on the one hand, to the organization of government institutions, the structure of the private sector, and long-standing relations between state and industry, on the other. Because of trenchant structural contrasts along each of the latter dimensions, the analyses of state capacity and industrial structure posit contrasting and unambiguous implications for the American and Japanese political economies. With respect to Japan, all "indicators" point to pervasive state powers, a close working relationship between government and industry, and collusive relations among firms. Similarly stark yet empirically opposite expectations are made regarding America. The third section of the article provides brief overviews of the VHSIC and VLSI programs, and delineates the specific application and expectations of state capacity and industrial structure analyses for the two case studies. It is argued that the programs should serve as "crucial" cases for the two analytical frameworks. U.S.-Japanese structural differences are at their extreme in the political economies of their semiconductor industries. Broader generalizations of the American and Japanese political economies should, therefore, ring truest in the politics and production of microelectronics. Such expectations would seem to be confirmed by even the most sophisticated industry studies. Yet despite such favorable theory-confirming conditions, it will be shown in the fourth and fifth sections that the two analytical models fail to account for the experiences of VHSIC and the VLSI project. In particular, "maverick" American firms welcomed a government initiative that, in the past, they would have disdained. And Japanese firms proved unable to work together in the one area where cooperation is most expected -- collaborative research, while the "strong" Japanese state failed at attempts to orchestrate a heavily targeted, "dependent" industry. State Capacity and Industrial Structure Analyses Critical reservations are raised here for two major modes of analysis in international and comparative political economy. The first explanatory framework is industrial structure analysis which highlights characteristics of industries and their firms that affect their political behavior and impact upon government policy.5 Such industry characteristics would include: the size of the industry, concentration in industrial production, and unionization of labor.6 A series of conclusions emerge from the analysis of industrial structure regarding those characteristics that make industries most amenable to government-industry as well as intra-industry cooperation. Where industrial production is concentrated in the hands of a few large firms, the limited number of private actors facilitates both the formation of industry-wide consensus and public-private consultation. These circumstances would apply to the American steel and automobile industries as well as the Japanese steel industry.7 Conversely, obstacles are posed where production is fragmented and highly

3 dispersed across a large number of firms. Government intervention on behalf of the American textile industry has been limited to trade protection, and attempts at industrial adjustment in French textiles have been stymied because both sectors are composed of hundreds of small firms.8 Government initiatives find fertile ground in sectors with large work forces and strong labor organizations. Large employment rolls highlight the economic and strategic importance of an industry, and strong labor unions can act as potent political pressure groups.9 Moreover, the cases of the American steel, television and textile industries underscore the political advantages to be gained when management and labor work in concert.10 In contrast, government policies often prove ineffective and are resisted in industries characterized by intense intra-industry competition and technological dynamism. Such circumstances might apply to the U.S. chemical industry where highly competitive firms do not coalesce easily and are wary of the differential competitive impact of government policies. Competitive problems in technology-intensive sectors might be redressed by technological fixes rather than government policies, and those policies can be undermined by rapid technological change.11 Finally, industrial policies might fall victim to corporate diversity. The weak protectionist coalition among American footwear manufacturers has been attributed to the division within the industry between large and small firms. Political unity in the U.S. television industry has been hampered by that fact that some of the manufacturers are multinationals while others are only nationally based.12 The second explanatory framework for which reservations are raised is the analysis of state capacity or state structure.13 This framework highlights two structural features of political systems that help determine state capacities: centralization and policy networks. State centralization encompasses three forms of concentration of political authority. First, power within the central government may be concentrated. The executive dominates the legislature; within the executive, interagency relations are coordinated and their differences minimized. Second, overlapping authority among government agencies may be minimized. Agencies enjoy unchallenged jurisdiction over distinct policy arenas. Third, the central goverment may dominate local authorities limiting regional autonomy. Political power in decentralized states is fragmented within the central government as well as dispersed regionally and territorially. Policy networks refer to mechanisms of state penetration into society. These networks facilitate communication between government and industry, mobilize the support of societal groups, and serve to implement government policy. Policy networks may take the form of quasi-governmental organizations such as industry advisory councils, policy study groups, and think tanks; or less institutionalized but patterned linkages between government agencies, legislative bodies, political parties, banking institutions, trade associations, labor organizations, and other social groups. State centralization and policy networks influence the policy instruments at the disposal of the state. The array of policy instruments may be narrow or broad; those instruments may be macroeconomic or sectoral in scope, efficiently or ineffectively implemented, and systematically harmonized or uncoordinated. Policy networks penetrating deeply into the private sector can produce a vast array of policy levers over

4 industry. Such levers may be industry-specific, offering the state targeted, "surgical" means of intervention including grants and subsidies, public investment banks, selective tax incentives, regional development assistance, R&D support policies, government procurement, industrial restructuring, and state enterprises. In the absence of such networks, governments are left with a limited array of less precise, economy-wide forms of intervention such as monetary and fiscal policy, infrastructural investments, and trade policy. State centralization can help ensure the effective implementation of policy as well as coordination with other policies. In contrast, policy in decentralized states may be duplicative, unfocused, contradictory, and less effectively employed. Ultimately, the "strength" of the state is shaped by its centralization, policy networks, and policy instruments. State strength or state capacity refers to the ability of government to extract resources from society, implement its policies even in face of societal opposition, and influence social groups. "Strong" states can resist societal pressures, change behavior of private actors, and transform the structure of its society and economy.14 Among advanced industrialized countries, state structures in the United States and Japan are taken as polar opposites. According to state capacity analysis, features of Japanese government are particularly well-suited for the promotion of industrial competitiveness and encouragement of industrial cooperation. With regard to state centralization, the Japanese political system is characterized by a unitary system of government where a powerful centralized state bureaucracy works closely with the country's dominant political party, the Liberal Democratic Party.15 Even skeptics of the strength of the Japanese state acknowledge "the more centralized nature of government authority in Japan than in the United States."16 Moreover in industrial affairs, the Ministry of International Trade and Industry (MITI) has been referred to as the "pilot agency" of Japan's developmental state "combin[ing] the functions of several U.S. agencies."17 Virtually all major manufacturing industries fall under the ministry's jurisdiction and it possesses a vast array of powerful, selective industrial policy instruments. The prestigious, cohesive MITI bureaucracy has been designated "the greatest concentration of brain power in Japan."18 In contrast, the American state is fragmented by separation of powers, federalism, bicameralism, the congressional committee system, judicial independence, autonomous bureaus, and undisciplined, nonprogrammatic political parties.19 Jurisdiction over industry matters "is spread willy-nilly throughout the government departments"20 including regulatory commissions, the Council of Economic Advisors, the Office of Management & Budget, the Office of the U.S. Trade Representative as well as the Departments of Commerce, Defense, Justice, Labor, and Treasury. The policies that emerge from such a decentralized setting are uncoordinated, can work at cross-purposes, and often have counterproductive effects on industrial competitiveness.21 Regarding state penetration into society, public and private sectors are relatively differentiated in the United States. State initiatives in industrial affairs are impeded by traditional adversarial relations between government and business. While American business leaders enjoy easy access in the political process, they remain hostile to government interference.22

5 In contrast, government-business relations in Japan are so symbiotic that differentiation between the two is virtually nonexistent. There is a high degree of public-private intercommunication, extensive career mobility between public and private sectors, and widespread informal mechanisms for public-private policy coordination and implementation.23 In industrial affairs, the organization of MITI into specialized vertical bureaus for specific industries is well-designed for close relations with the private sector. The MITI bureaus coordinate policy with counterparts in the legislature, LDP, industry associations, and major corporations. Crucial Cases The designation of Japan as an exemplar of state strength and government-business symbiosis is, of course, a matter of intense scholarly debate.24 Critics highlight fragmentation and conflict both within and between Japanese government and industry25 as well as discount the positive role of the state in the economy and even spotlight its negative and counterproductive impact.26 Yet the empirical setting for this study, the political economy of microelectronics, is an arena where Japan observers are much less divided. As elaborated below, even critics of the strong-state argument as it applies generally to Japan concede the prominent role of the Japanese government in the development of the semiconductor industry.27 Given this exceptional consensus, our Japanese case study should not be biased against the strong-state argument. If anything, the political economy of microelectronics in both America and Japan should be biased in favor of the analyses of state capacity as well as industrial structure. Politics and production in microelectronics are frequently taken as archetypes of the broader structural characteristics of the two national political economies. Japan's competitive success and America's problems in the industry, it is argued, are rooted in and exhibit the role played by conducive or debilitating features of their respective governmental and industrial structures. A major task of this section is to delineate how the analyses of state capacity and industrial structure should be and have been applied to the Japanese and American semiconductor industries. More importantly, because the industries should epitomize the impact of state and industrial structures, it is argued that the American Very High Speed Integrated Circuit program and the Japanese Very Large Scale Integration project should serve as "crucial case studies" for the two frameworks. As observed by Eckstein, crucial cases "simulate as closely as possible the specified conditions under which a law must hold."28 In the present study, the VHSIC program should resolutely demonstrate the explanatory power of industrial structure analysis, while the VLSI project should provide similar confirmation for both the industrial structure and state capacity frameworks. Because their features should so clearly play into the hands of specified theories, crucial cases serve as critical "do-or-die" tests for theoretical constructs. Crucial cases "must closely fit a theory if one is to have confidence in the theory's validity."29 VHSIC. The VHSIC program (1980-1988) sought to develop advanced integrated circuits that could be introduced into military systems in a timely and affordable manner. The most important features of VHSIC circuits are their state-of-the art minimum features sizes in the micron and submicron range30 and high-speed computational

6 throughput. Technological advances were sought in lithography31, circuit design, wafer processing and fabrication, chip packaging and test, computer-aided design, and computer architecture and software. New radar, guidance, communications and other military systems are being designed to utilize VHSIC circuits. Three defense-related motives underlay the creation of the VHSIC program in 1979. First, advanced integrated circuit technology was sought as a force multiplier to offset the numerical military advantages of the Soviet Union. VHSIC represents the base technology for the "smart weapons" military strategy. A second motive behind VHSIC was the reassertion of Defense Department influence over the direction of developments in semiconductor technology. While semiconductor technology was driven by military requirements in the 1950s and early 1960s, the microelectronics industry had turned away from the defense sector and towards industrial and consumer markets in the 1970s. The immediate impetus for the establishment of VHSIC were reports of advances in Soviet integrated circuitry. VHSIC was designed, in part, to reextend the U.S. lead over the Soviets in military circuits. VHSIC was in the planning stages between October 1977 and June 1979 and, during this period, Defense Department officials consulted extensively with industry and academic specialists. Industry input was responsible for major organizational and technological features of the program. Most VHSIC contract work was carried out by companies that teamed up with each other to combine their research efforts (see Chart 1).

7

A central Pentagon office managed the diverse technical activities of some twenty different contractors. VHSIC was a tri-service (Army, Navy, Air Force) program in contrast to the usual practice of fragmenting military technology programs across the three services. With a price tag of nearly $1 billion over an eight-year period, VHSIC represented America's largest, most ambitious government initiative in microelectronics in decades.

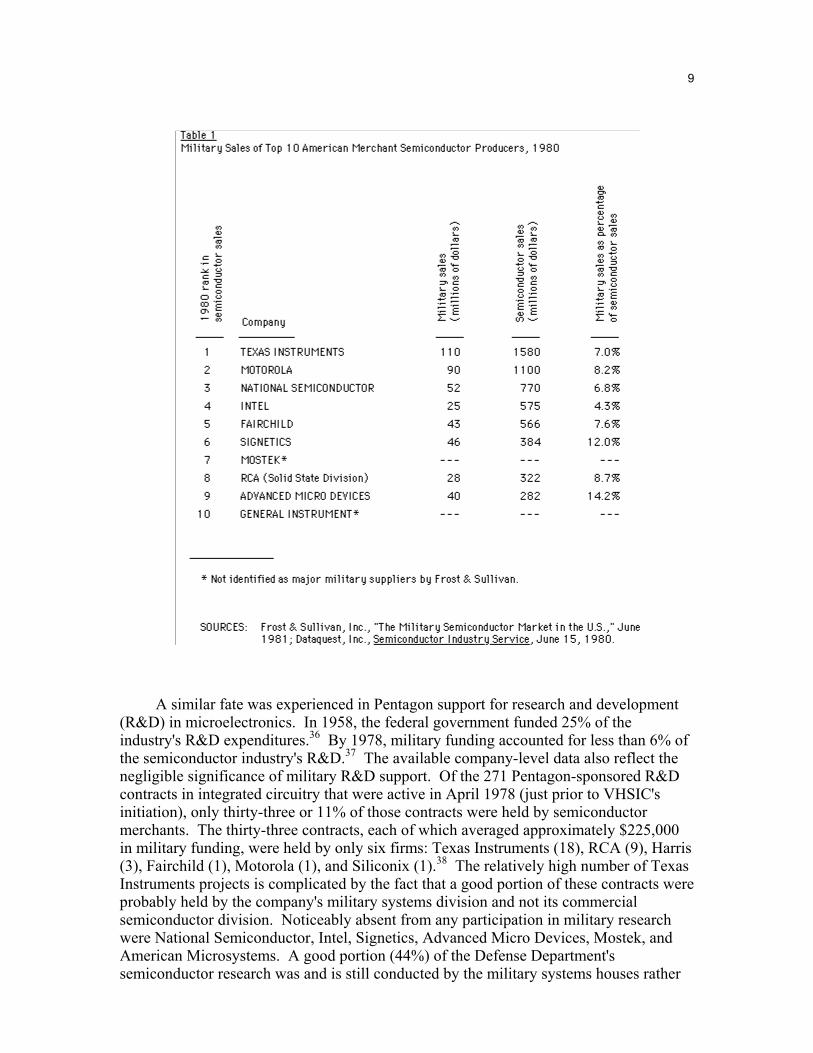

8 It should be emphasized that VHSIC was not designed as an industrial policy program aimed at promoting the international competitiveness of the American semiconductor industry. Still many of the program's features raise important issues relating to the objectives, planning, and management of industrial policies.32 This article considers one such issue: the reaction of industry to the VHSIC initiative. The problem of garnering private sector support is one of the most often cited obstacles to industrial policy in the United States. In 1979, thirty-two electronics firms submitted bids for VHSIC contracts diffusing fears that the program would not be supported by industry. For some of these firms, however, interest in VHSIC comes as no surprise. Foremost among such companies were the "military systems houses" such as General Electric, Hughes, Raytheon, Rockwell, TRW, and Westinghouse. These traditional defense contractors manufacture radar, electronic warfare, communications and guidance systems for the military, and are always on the lookout for Pentagon contracts. Among the industries whose technologies are utilized in VHSIC, the reaction of "merchant" semiconductor producers to the program carries the greatest ramifications for government-industry relations and industrial policy-making in the United States. Merchant producers, relatively small firms, sell semiconductors on the open market to other firms that use them as components in end products. In contrast, larger "captive" producers consume all or most of the semiconductors they manufacture for their own end products such as computers, industrial machinery, and consumer electronics. The U.S. microelectronics industry includes a handful of significant captives, IBM being the most prominent, and a large number of merchant producers. While semiconductor merchants were once heavily dependent upon the support of the military in the 1950s and early 1960s, such dependence has dramatically dissipated.33 In 1962, military procurement accounted for nearly 40% of total semiconductor production and 100% of integrated circuit production. By 1977, those figures had fallen to 12% and 7%, respectively.34 As indicated on Table 1, these aggregate industry characteristics also apply, on an individual basis, to the major semiconductor merchants. By 1978, computer applications alone accounted for four times the value of government purchases of semiconductors.35

9

A similar fate was experienced in Pentagon support for research and development (R&D) in microelectronics. In 1958, the federal government funded 25% of the industry's R&D expenditures.36 By 1978, military funding accounted for less than 6% of the semiconductor industry's R&D.37 The available company-level data also reflect the negligible significance of military R&D support. Of the 271 Pentagon-sponsored R&D contracts in integrated circuitry that were active in April 1978 (just prior to VHSIC's initiation), only thirty-three or 11% of those contracts were held by semiconductor merchants. The thirty-three contracts, each of which averaged approximately $225,000 in military funding, were held by only six firms: Texas Instruments (18), RCA (9), Harris (3), Fairchild (1), Motorola (1), and Siliconix (1).38 The relatively high number of Texas Instruments projects is complicated by the fact that a good portion of these contracts were probably held by the company's military systems division and not its commercial semiconductor division. Noticeably absent from any participation in military research were National Semiconductor, Intel, Signetics, Advanced Micro Devices, Mostek, and American Microsystems. A good portion (44%) of the Defense Department's semiconductor research was and is still conducted by the military systems houses rather

10 than the merchants.39 Overall, then, the merchant semiconductor industry cannot be considered to be closely tied to the military. This conclusion is reaffirmed by the fact that the VHSIC program was stimulated, in part, by the lack of attention given to military needs by the merchant producers.40 The VHSIC program would not have been necessary if the close ties between the military and the merchants of the 1950s and 1960s had been maintained. The relative autonomy of the merchant semiconductor industry from the defense sector helps to eliminate one important reason why these companies might flock to a military program such as VHSIC. Not only would military factors have minimal influence over the merchant producers, but there are a multitude of reasons -- informed by industrial structure analysis -- to expect this industry to oppose and scuttle VHSIC-like government initiatives. As reviewed in the second section, the analysis of industrial structure points to a series of characteristics that make industries most amenable to government initiatives. These would include sectors that are highly concentrated, technologically mature, unionized; and have large employment rolls, stable market shares, and homogeneity across firms. One could go on an enumerate the hypotheses that arise from industrial structure analysis, but it should be evident that across many if not all of the industrial variables the American merchant semiconductor sector is exactly the wrong kind of industry that one might expect to be hospitable to industrial policy-type government initiatives. Merchant semiconductor production (unlike captive production for internal use) is not concentrated in the hands of a few large companies, but is a highly fragmented sector composed of over a hundred small firms. The sector does not employ a large work force, and labor is not organized. Merchant producers are intensely competitive and highly innovative. Semiconductor market conditions have been characterized as "Schumpeterian competition" with aggressive price cutting to gain market share, traditionally low entry costs for new firms, and rapid turnover among industry leaders.41 The industry's technological dynamism is indicated by remarkable increases in labor productivity (20.5% annual increases from 1975 to 1979), dramatic price reductions per bit of computer memory, the doubling of circuit elements per chip per year (from less than 10 elements in the early 1960s to hundreds of thousands in the early 1980s), and the proliferation of new products brought to the marketplace.42 The industry also displays a high degree of diversity among its firms. With regard to differences in corporate origins and status, many merchants retain corporate independence (e.g., National Semiconductor and Intel); some have been acquired by larger corporations (e.g., Signetics by Phillips, Intersil by GE); others still are divisions of established, diversified companies (e.g., Harris, RCA). A number of producers are innovation leaders while others are technology followers or incremental innovators. Some have broad product lines while many more have limited, specialized product offerings. While many are devoted exclusively to semiconductor production, a number of firms have attempted vertical integration into the downstream manufacturing of computers and consumer electronics.43

11 There is also considerable heterogeneity in the competitive strategies or overriding management orientations of the merchants. Some emphasize research and technological excellence, others low-cost production and manufacturing, and still others marketing and reliability. While virtually all manufacturers have overseas operations for semiconductor assembly, they differ in the extent to which research and design facilities are located abroad. The fragmentation, technological dynamism, interfirm rivalry, and diversity of the U.S. semiconductor industry pose unique challenges for the design of public policy. Semiconductor industry analysts have observed that government "policies impact various firms differently" and "firms react differently" to the same policy.44 The differential effects of policy are problematic because "policy makers often expect a policy to impact an industry and the firms in the industry in a relatively uniform way" and policy effects "on competitive behavior and performance may not be the originally anticipated effect."45 The challenges to industrial policy for microelectronics are accentuated where the Defense Department is involved. After the mid-1960s, merchant semiconductor producers developed a deep antagonism towards doing business the Pentagon. To begin with and as indicated in the above figures, military R&D funding favored larger, more established firms. Newer, smaller firms -- the lifeblood of the semiconductor industry -- could not compete against larger firms with better funded and more recognized research staffs.46 Moreover, after the mid-1960s the technical requirements of defense work increasingly deviated from mainstream commercial efforts. The Pentagon began requiring work on sophisticated, weapon-specific product applications calling, for instance, for radiation hardness and package strength specifications far in excess of civilian standards.47 In addition to representing a technological divergence from commercial endeavors, such military work clashed with standard industrial production methods. Commercial manufacturing seeks volume production to achieve economies of scale while defense work calls for small-batch, "one-of-a-kind" custom production. The small order sizes of the military call for different and often inferior quality control practices and less extensive process automation.48 The industry has also become deeply troubled over the Pentagon's tightening of technology transfer restrictions. Such restrictions have been especially applied to integrated circuit technology, and include controls on offshore production as well as exports. These restrictions threaten the worldwide production and marketing operations of American semiconductor firms. Finally, doing business with the military entails onerous bureaucratic requirements and complications. For each semiconductor product to qualify for military use, certification and qualification proceedings take as long as two years. Specifications that military circuits are to meet are stipulated in no less than 190 pages of requirements. A separate 500 page "encyclopedia" governs merely how the circuits are to be inspected and tested. Moreover, Pentagon requirements are subject to constant revision. In 1984, for instance, semiconductor makers were besieged with 883 updates in Pentagon specifications.49

12 Taken altogether, the above developments have "tended to discourage U.S. semiconductor companies from remaining in the military business."50 The industry is not just autonomous of but antagonistic toward the defense sector. Indeed, having emerged from "a developmental history that traditionally rewarded entrepreneurial independence,"51 American semiconductor firms developed hostile attitudes toward government in general. As a "shining example of ... competitive capitalism"52:

"the U.S. industry believed that commercial development of IC [integrated circuit] technology and markets had taken place optimally in the absence of significant government involvement. 53

In sum, one would be hard pressed to find more unfavorable conditions for industrial policy and government-industry collaboration than among merchant semiconductor producers. As one careful industry observer has pointed out, "one can argue that the state's role is inherently constrained by the special characteristics of the semiconductor industry."54 In this context, the industry should constitute an "easy" test for industrial structure analysis. With virtually all indicators pointing in directions adverse to government-industry collaboration and industrial policy-making, the plight of such policies should be patently predictable. At the same time and for the same reasons, the merchant semiconductor industry provides a "crucial" test for industrial structure analysis. If expectations are not fulfilled in this "must-fit" case, serious reservations are raised for the explanatory framework. VLSI. Japan's Very Large Scale Integration project serves as a crucial test for state capacity as well as industrial structure analyses. The VLSI project was established in 1976 through the efforts of the Ministry of International Trade and Industry (MITI) and Japan's leading manufacturers of computers and semiconductors. The program sought to enhance the capability of Japanese industry in developing VLSI devices for the next generation of computer systems.55 Not unlike the American program, the VLSI project sought advances in in fine-line lithography, circuit design, wafer processing and fabrication, chip packaging and test, and computer-aided design. The program was primarily motivated by MITI desires to strengthen the Japanese electronics industry through consolidation and restructuring. At the same time, Japan's computer industry, reeling from the 1974-75 recession, looked to their government for financial and technological support. The immediate stimulus to the program was speculation of a major product breakthrough by IBM that would undermine the competitiveness of the Japanese industry. From April 1975 to April 1976, MITI officials sought the support and advice of other government offices and industry in formulating the VLSI effort. Five of Japan's leading electronics manufacturers joined the project: Fujitsu, Hitachi, Mitsubishi, NEC, and Toshiba. These companies formed two sets of group labs, located at company facilities, to work on applied technology. Fujitsu, Hitachi and Mitsubishi teamed together in the Computer Development Laboratories (CDL), and NEC and Toshiba grouped together in the NEC-Toshiba Information Systems (NTIS) labs. In addition, all five companies as well as MITI sent researchers to a central research facility, the Cooperative Laboratory. The cooperative brought together nearly 100 engineers at a single site to work on longer-term basic and generic research in contrast to the more applied work of the two group labs (see Chart 1).

13 Forty percent of the VLSI project's $300 million budget was contributed by the government, with the remainder provided by the five companies. The project produced over 1000 semiconductor patents. The American Semiconductor Industry Association, among others, has pointed to the VLSI project as the decisive supporting element in Japan's export drive into the U.S. semiconductor market.56 Japan's VLSI project should provide a good test for industrial structure analysis. It has generally been concluded that the characteristics of the Japanese electronics sector make it amenable to and suitable for multifirm collaboration. A handful of companies -- NEC, Hitachi, Toshiba, Fujitsu, Mitsubishi, and Matsushita -- dominate electronics manufacturing in Japan.57 As reviewed earlier, industrial structure analysis would point to a greater potential for intra-industry cooperation and political unity in highly concentrated, oligopolistic industries. In addition, advanced technology arenas such as semiconductors would be the most likely to manifest multifirm collaboration. Where Japanese companies remain in a mode of catching up with the Americans -- as was the objective of the VLSI project -- the Japanese could be expected to coordinate their efforts. The intense competition between Japanese firms in manufacturing and marketing could be expected to recede where basic and generic research far-removed from the marketplace is involved. As claimed by two observers of Japanese industry:

A system has emerged in which there is cooperation in the funding of new technology projects . . ., but continued fierce competition in existing products and in the production and marketing of new products. 58

Even an analyst who largely discounts the contributions of MITI-sponsored research cooperatives argues that the projects serve to promote cooperation and communication among Japanese firms.59 Not only would industrial structure analysis expect multifirm collaboration in Japanese microelectronics, but the industrial characteristics of the Japanese manufacturers would seem to make them likely targets of government intervention. From the point of view of the Japanese government, the industrial structure of Japanese electronics provides secure "investment" risks around which to form public policy. Their large size, diversified product lines, and oligopolistic market positions reduce their exposure to competitive failure.60 More importantly, the industrial structure of Japanese electronics makes its firms very vulnerable to government influence. Reflecting structural differences in external corporate financing in Japan and the United States61, Japanese electronics firms rely much more heavily upon debt financing through bank loans rather than equity financing via stock issues. Approximately 67% of all corporate funding in Japan is financed by debt62 and the figure for Japanese semiconductor producers averages at 70%.63 In contrast, the corresponding figure for bank financing in the U.S. semiconductor industry is only 25%.64 While a select number of Japan's manufacturing firms are relatively free from dependence upon external loans, such exceptions do not apply to Japan's major semiconductor manufacturers -- including all five company participants in the VLSI project. As illustrated in Table 2, well under one-third of the corporate assets of the five

14 VLSI participants are accounted for by equity holdings.

Dependence upon external financing for the Japanese electronics industry translates into dependence upon the Japanese government.65 As observed by a prudent analyst:

Japanese corporations, when they want financing, mostly have to turn to the few large banks which dominate the Japanese financial system. These banks, in turn, are closely regulated by the Ministry of Finance. 66

High debt ratios can provide the Japanese government a formidable source of leverage over industries and firms. To take one of the less subtle cases, a major manufacturer of flexible manufacturing systems, Yamazaki, was forced to participate in a MITI research cooperative (much like the VLSI project) under pressure from its bank.67 Moreover, Japanese electronics firms are particularly sensitive to capital financing given their production-oriented corporate strategies. The domestic and international competitive success of these firms has rested upon high-volume, low-cost manufacturing with long-term time horizons for returns on investment. The success of these production-oriented strategies (as opposed to technology- or marketing-oriented strategies) that trade off short-term profit for market share relies heavily upon ready access to capital.68 The

15 Japanese companies can particularly benefit from -- if not depend upon -- government-backed financing. The industrial structure of Japanese electronics production and its political-economic implications represent, then, the mirror image of its American counterpart. If the fragmented, heterogeneous structure of the U.S. semiconductor industry was supposed to pose obstacles for multifirm collaboration and government industrial policy, then the large, oligopolistic, financially dependent and production-oriented Japanese firms should have the opposite tendencies. We should have then a second compelling case demonstrating the explanatory power of industrial structure analysis. Moreover, the Japanese electronics sector and the VLSI project in particular should provide an equally compelling case for a second mode of analysis investigating state-society relations: state capacity analysis. As reviewed in the second section, state structure analysis points to features of the Japanese state which are particularly well-suited for the promotion of industrial competitiveness and encouragement of multifirm collaboration. The strong, centralized Japanese state is contrasted to the decentralized, fragmented political system in the U.S. Likewise, symbiotic relations between Japanese government and business are distinguished from the more differentiated, if not antagonistic public-private sector relations in America. Japan's VLSI project would seem to be a perfect case to test and indeed confirm state structure analysis. Quite simply, the powerful influence of the strong Japanese state would seem to be especially applicable to high technology sectors such as computers and semiconductors. As is well known, the Japanese government has targeted the information electronics sector as key to its continued economic well-being. Computers and semiconductors lie at the core of the much-cited MITI "visions" of the future. Government assistance to these industries has taken the form of trade protection, research and development subsidies, tax benefits, leasing arrangements, and preferential procurement.69 While the impact of Japanese industrial policy varies greatly from sector to sector, electronics are among the select few sectors subject to extended and intensive government intervention. Indeed, the targeting of higher value-added, knowledge-intensive sectors continues as Japan's "developmental" system crumbles in most other arenas.70 In short, Japanese government has done its "utmost" to promote advanced electronics.71 And as one authority observes:

it is not likely that Japanese policy vis-a-vis its hi-tech industries will change in the near future. Instead, there is a distinct possibility of it becoming even more activist. 72

Most notably, even those analysts most skeptical about the role of government policy in Japan's economy acknowledge the formidable presence of the state in the Japanese electronics industry:

The most extensive government involvement in a particular industry involves computers. . . . The computer industry is often cited as an example of "Japan Incorporated," the close cooperation of government and business to promote Japanese industry at the expense of foreign firms. The computer industry,

16 however, is an exception . . . . 73 Where microelectronics research is concerned, MITI is firmly in command. 74 . . . there are a number of provisions in the Japanese tax code which do benefit particular high-technology sectors. The most generous of these provisions relate to the computer industry. . . . The one high-technology sector which has attracted the attention of the Japan Development Bank and the Small Business Finance Group is the computer industry. Since the early 1970s, this industry has received priority funding . . . . 75 Computers, though, have received heavier and more consistent assistance than any other high-technology industry. 76 Computers seem to be a prime example of an industry that may actually owe some its success to the existence of government policy. 77

Given its high-priority treatment, it is not surprising that analysts can conclude that the microelectronics industry "emerged from the drawing boards of Japan's economic planners."78 Beyond nurturing the growth of the microelectronics, government targeting has fostered the closest of ties and interaction between the government and industry.79 Even the Japan Economic Institute -- in a report designed to counter "unwarranted" assessments of the intimacy of government-business relations -- admits that while many "industries no longer need or want to cooperate with the government ..., there is likely to be a close relationship between the government and ... cutting-edge industries."80 Not only would the brunt of Japanese industrial policy be felt by high technology sectors, but MITI research programs like the VLSI project have been pinpointed as constituting the "main thrust" of current Japanese targeting efforts in semiconductors and computers.81 It has been argued that as traditional instruments of Japanese industrial policy have been dismantled (e.g., tariffs, foreign exchange controls, technology licensing), cooperative research and development programs have become a central targeting mechanism.82 And one of the foremost specialists on the subject highlights the influence of the state over industry in such collaborative efforts:

Extremely significant ... in these MITI-initiated joint research projects is that the MITI officials ... often exert leadership quite openly. This clearly reflects MITI's desires to ensure that effective and full research cooperation will take place among the scientific personnel sent to the joint research project by the participating firms. ... it is not an overstatement to observe that the MITI officials are exhibiting a strong sense of "mission" and unusual zeal in promoting joint R&D activities and are playing a much more visible, as well as important, role in determining the research agendas than they ever did in promoting the technological capabilities of the major industries during the rapid growth period [through 1973]. 83

The VLSI project in particular has been singled out as the major promotional vehicle for the Japanese semiconductor industry in the late 1970s.84 The rationale for

17 selecting this case study is provided by the fact that the project

is viewed as the most successful example of Japanese industrial policy in high technology . . . it is the integrated circuit-type research focusing on a particular product area that Japan's critics call industrial "targeting." 85

In sum, the strong Japanese state should have a commanding influence over Japanese computer and semiconductor manufacturers. State capacity analysis combined with industrial structure analysis would point to the VLSI project as an excellent case where one should see the heavy hand of the Japanese government, the most potent form of Japan Inc., and the most developed collusion among Japanese firms. We have, once again, what should be an easy and therefore crucial test; this time for both explanatory frameworks. The American VHSIC Program: Government-Industry Antagonism? There is some evidence to support the pessimistic expectations of industrial structure analysis for the fate of the VHSIC program among American merchant semiconductor producers. In a major blow to the program, one of the most successful and innovative merchants, Intel, vigorously opposed the Pentagon initiative. Intel officials charged first, that the development of specialized military technology represented a divergence from mainstream commercial technology. For instance, circuits with high radiation tolerances would have little commercial application. Second, Intel criticized VHSIC for exacerbating the scarcity of skilled manpower by draining away scientists and engineers from commercial to military work. It was feared that the diversion of limited talent and the crowding out of commercial R&D would harm the industry's international, technological competitiveness. These criticisms were picked up in the popular press86 as well as by most outside observers of the semiconductor industry (i.e., academics).87 Whether or not these arguments are valid is, first, yet to be determined and, second, irrelevant to the present analysis. What is of importance from the perspective of this article is the actual reaction of the broader merchant industry to VHSIC. One observer has claimed that "many merchant semiconductor firms have been reluctant to participate in the [VHSIC] program."88 Yet to the contrary, ten of the top fifteen merchant producers have been involved or sought involvement with VHSIC (see Table 3). These ten VHSIC contractors or aspirants accounted for 63% of merchant integrated circuit production in 1982. In point of fact, only Intel resolutely opposed the VHSIC initiative.89 Of the other four top 15 companies that have not bid for VHSIC contracts, Advanced Micro Devices, Mostek and RCA seriously considered joining the program.

18

Why did VHSIC attract the support of ten leading merchants? Interviews with eight of these manufacturers confirm that military-related factors played only a limited role in corporate motivations to seek VHSIC participation. Reflecting the nonmilitary nature of the issue, decisions to participate in VHSIC were vested not with officials from the military or government divisions of the firms but with senior corporate executives responsible for strategic business and technology initiatives. The VHSIC question was treated as an issue of broad corporate strategy rather than a strictly military affair. Rather than resting upon military factors, the dominant rationale for seeking VHSIC participation was the assessment of complementarity between VHSIC technology and mainstream commercial technology. The program's objectives were seen as matching those of in-house technology efforts and VHSIC participation was sought to accelerate those efforts. This view of convergence between VHSIC and commercial technology was manifested in the organization of VHSIC work by those merchant houses that were awarded VHSIC contracts. Rather than relegating VHSIC to peripheral military divisions within companies, VHSIC activities were integrated into mainstream commercial and technology efforts. For instance, everyday VHSIC activities at Texas Instruments, Motorola and National Semiconductor were directed by corporate vice presidents responsible for overall semiconductor research and development. At Motorola

19 and National Semiconductor, VHSIC engineers were drawn from and worked closely with the company's advanced technology labs. These same engineers were part of larger company programs, in place well before VHSIC, to develop state-of-the-art Very Large-Scale Integration (VLSI) technology. In this way, VHSIC work was fused with and designed to intensify in-house commercial VLSI efforts. At Texas Instruments, a distinct VHSIC organization was not even been established. Instead, VHSIC activities were divided among and integrated with the broader responsibilities of the company's semiconductor, computer, and research divisions. Related to envisioned technological complementarity, VHSIC support was won by the prospect of commercial payoffs from participating in the defense program. Commercial spinoffs are especially expected in areas of process technology such as lithography, circuit technology, design approaches, and computer-aided design. In all, VHSIC supporters from the ranks of merchant semiconductor producers have disagreed with Intel's assessment of the program. Whether or not the assumptions of VHSIC's complementarity with mainstream technology and its commercial payoffs prove valid is, once again, irrelevant to this analysis. Of significance is the nature of those assumptions. In essence, semiconductor producers have elected to welcome a government program that they view as contributing to their technological and international competitiveness. By the late 1970s, most chip manufacturers began to look beyond their respective corporate confines for capital and technological support. VHSIC was viewed as helping to serve those needs. Their assessment may prove to be wrong, but the fact that these firms were willing to look to government for support constitutes our critical incontrovertible point. To the extent that industrial policies are aimed at promoting international competitiveness, corporate support for VHSIC is evidence that the American semiconductor industry may not be as inimical to such policies as generally assumed. As outlined earlier, the exact opposite conclusion would naturally follow from industrial structure analysis. This is not to argue that industrial policies may find as fertile ground in the semiconductor industry as in other industrial sectors. But the fact that a fragmented, highly dispersed, competitive and innovative industry can -- along with larger, more mature or oligopolistic industries -- welcome government initiatives leads to the conclusion that the cross-sector explanatory power of industrial structure analysis proves to be quite limited. The explanatory framework fails this best test. The VLSI Project: Japan Incorporated? State capacity and industrial structure analyses offer a cavalcade of reasons to expect extensive levels of government influence over and industrial collaboration within the Japanese electronics industry. Two features of the VLSI project would seem to confirm these expectations. First, responsibility for general coordination of the project was vested in the VLSI Technology Research Association. The association was composed of high-ranking officials, top executives, engineers, and administrators from MITI, the five member companies, and Nippon Telephone and Telegraph. Major policy, technical, and funding decisions were made this government-industry body. A second significant feature of the VLSI project was the establishment of a central

20 research facility, the Cooperative Laboratory. To enforce a degree of joint effort, the cooperative lab brought together at one site nearly 100 researchers from the member companies and MITI. Six research teams were established within the cooperative to work on lithography (three teams), crystal, process, and device technologies. Each team was deliberately staffed with researchers from more than just one company. Project officials sought to encourage exchange among the six teams via joint meetings and "open houses" for all research labs. Neither the Technology Research Association nor the Cooperative Lab have any parallel in the American VHSIC program (see Chart 1). VHSIC was managed not by a joint government-industry council, but by Defense Department officials. Research projects were selected by all-government technical teams evaluating company proposals rather than by multifirm committees. VHSIC contractors did meet at annual Pentagon conferences. The purpose, however, was neither to make policy nor to engage in technical consultation, but to report on and review contract work. Indeed, all other contractors were excused when the VHSIC activities of each company were evaluated by Defense Department officials. In short, there was no effort at joint industry coordination as takes place in the VLSI Technology Research Association. Neither was there anything comparable to the VLSI cooperative lab in the VHSIC program. There was no effort to enforce collaboration at a technical working level among VHSIC contract teams. Not only did the six major contract teams not work together at a single site, even work among companies within the same team was not conducted at one location. For instance, in the Westinghouse team, the prime contractor worked on computer architecture and one set of circuits in Maryland; National Semiconductor on another set of chips and silicon wafer processing in California; Control Data on computer-aided design in Minnesota; and Harris on communications systems in Florida. The VLSI Technology Research Association and Cooperative Lab have attracted virtually all the attention of observers of the project and have contributed to visions of "Japan Inc."90 The establishment of a government-industry coordinating body and a central research lab is taken as evidence of the strength of the Japanese state and propensity for industry collusion. Even the most careful of analysts have reported that MITI was able to persuade "the five leading semiconductor producers to suspend their normally intense sense of rivalry and mistrust in order to achieve common research objectives" and that "researchers from rival companies worked side-by-side with government scientists and engineers."91 Interviews with government and industry officials in Japan reveal, however, that the project's work was overwhelmingly conducted by individual Japanese firms with little intervention from either MITI or other firms. To begin with, while the member companies welcomed government subsidies, they vigorously opposed the notion of cooperative research in a joint research lab. MITI was able to prevail over industry only after the companies realized that without the cooperative lab the entire project -- including the much-needed subsidies -- would be placed in jeopardy.92 The firms conceded, however, only as a tactical move to solidify support for the subsidies. Once the lab was established, the companies maneuvered to minimize the role of the joint facility and maximize corporate autonomy. As an initial strategy, some of the companies sought to limit the project to the mere inspection and analysis of imported semiconductor

21 manufacturing equipment. Other companies sent their second-rate engineers to the cooperative. As mentioned earlier, the cooperative's research was carried out by six research teams. The most important feature of these teams was that each was directed and dominated by a different company. Fujitsu, Hitachi and Toshiba each headed a fine-line lithography section; Mitsubishi directed the process technology section; and NEC managed the testing and device technology team. A sixth section on silicon crystal technology was directed by MITI's Electrotechnology Laboratory. Each team was not only directed by one company, but each was primarily staffed by researchers from the one company. On average, only two members out of a team of 17 researchers came from companies different from that of the team leader. Managers of the VLSI project admitted that this staffing compromise was made in order to assure tangible research results. It was feared that attempts at enforcing true multifirm cooperation would have been frustrated by corporate rivalry. Indeed, once a research section became affiliated with one and only one company, the commitment of its staff to the lab's work was enhanced. Relations between the six research teams were characterized by suspicion and distrust, and little substantive exchange took place among them. Measures were even taken to prevent leaks from spreading between teams -- including the construction of physical barriers between labs. The sharing of information between companies was even rare among the three lithography labs. Each worked on their own and pursued different technological approaches. In fact, these three teams, instead of collaborating, were organized to be in competition with each other. Indeed, the technological achievements of the cooperative can, in large part, be attributed to the competitive environment maintained within the lab. As limited as the "cooperation" was in the VLSI central research facility, it is important to point out that the cooperative lab constituted only a small portion of the project's work. Reflecting the industry's opposition to cooperative research, only 20% of the project's funding went to the central lab. Most of the project's efforts and money was, instead, devoted to the two group labs. Work on all-important applied research with direct ramifications for the marketplace was reserved for the group labs securely located on company premises rather than at the cooperative lab. The functional segmentation and competition seen in the cooperative lab was reflected as well in the two group labs. To begin with, there was little collaboration between the group labs and the central lab. No attempts were made to follow-up on and extend the cooperative's basic research in the applications-oriented group labs. While the progress of the group labs was reviewed by managers of the VLSI project, the labs received little external technical support or direction. In theory there was to be a free flow of information between the two group labs. Yet from their very inception, the labs operated separately. The Fujitsu-Hitachi-Mitsubishi group (Computer Development Labs, CDL) worked on IBM-compatible technologies while the NEC-Toshiba team (NEC-Toshiba Information Systems, NTIS) worked on non-IBM technologies. As observed by the U.S. Semiconductor Industry Association -- in a report designed to demonstrate collusion among Japanese firms (along

22 with MITI) -- "the two groups developed different (i.e., nonduplicative) technologies in their respective efforts."93 Even cooperation among firms within the same group lab proved severely limited. Group lab work was primarily conducted by each member company on its own premises with little participation by other members of the lab. Within each lab, each company worked on different technologies. For example in NTIS, Toshiba worked on crystal technology, while NEC focused on wafer processing techniques. In CDL, intercompany collaboration was checked by intense competition and hostilities between Fujitsu, Hitachi and Mitsubishi. Efforts by MITI to enforce cooperation at the level of group labs, as in the cooperative lab, were thwarted by corporate independence and interfirm rivalries. The degree of autonomy enjoyed by companies in the group labs exceeded even that of the loosely organized central cooperative. A final indicator of the lack of cooperation that permeated the VLSI project relates to the patent applications that resulted from the research. Despite its "cooperative" label, only 16% of the project's 1000 patents went to joint inventions by engineers from different companies. The rest of the patents went to applicants from a single company. In summary, the ability of the "strong" Japanese state to orchestrate industrial affairs and the alleged proclivities towards collusion among Japanese firms proved quite limited in the VLSI project. Despite the advantages that the Japanese government should have had in dealing with the domestic electronics manufacturers, and despite industrial characteristics amenable to multifirm collaboration, little cooperation and substantive technical exchange was enforced within the VLSI cooperative lab, between the cooperative and group labs, between the two group labs, and among companies within the same group. Indeed, the conduct of research undertaken in the VLSI project closely resembles the organization of work in the American VHSIC program. The segmentation of work and competition between the six teams of the VLSI cooperative mirrors relations between the six major VHSIC contract teams. The VHSIC teams worked independently, pursued distinct technological approaches, and designed circuits for different systems applications.94 Because they were rivals for future VHSIC contracts, relations between the six teams were intensely competitive. In addition, the division of labor within the VLSI group labs parallels the segmentation of functions within VHSIC contract teams. For instance, in the TRW team, the prime contractor works on one circuit technology, Motorola on different circuit technology, and Sperry on computer-aided design. MITI officials would empathize with Defense Department managers who acknowledged that industry competition and the preservation of corporate autonomy significantly constrained efforts at inducing multifirm cooperation in the VHSIC program. The operational features of the Japanese VLSI project, then, bear close resemblance to those of the American VHSIC program. Despite the fact that the VLSI project should have more than confirmed the usefulness of state capacity and industrial structure analyses, expectations of strong governmental influence over industrial behavior and of multifirm collusion were not borne out. This is a highly critical conclusion since the contrasting domestic structures of the American and Japanese political economies should

23 have been reflected in similarly contrasting operational and organizational experiences in the two technology programs. Implications Twenty years ago, the analyses of industrial structure and state capacity would have provided much insight into the political economies of the American and Japanese semiconductor industries. By the mid-1960s, the American industry had turned away from the military as its major customer and was embarking upon the microprocessor revolution that would open vast new consumer and industrial markets. Barriers to entry were low, ushering in one of the industry's most dynamic eras as technological frontiers were broadened with the formation of each new company. The industry's position in world markets stood unchallenged. In these circumstances the industry would have ignored any attempt by the government to influence the development of semiconductor technology. Twenty years ago, the Japanese electronics industry had yet to emerge from the technological backwoods. The industry was still producing simple transistors while a good portion of U.S. production was devoted to the more sophisticated integrated circuit. In 1966 MITI put together its first strategic game plan for developing a competitive computer industry. A series of research and development projects, producer cartels, and government-sponsored joint ventures soon followed. Interest and expertise in electronics were developed or enhanced within MITI, the trade associations, and Japan's Liberal Democratic Party. Government-industry consultation over computer policy intensified via MITI's Industrial Structure Council. The enactment of the 1971 Law for Provisional Measures to Promote Specific Electronics and Machinery Industries empowered MITI with new authority in targeting advanced technologies. MITI's influence over a dependent electronics industry was at its zenith. The experiences of the American VHSIC program and Japanese VLSI project represent significant breaks with the immediate past. The U.S. semiconductor industry, by welcoming the VHSIC program, has displayed an unprecedented amenability to government support. The VLSI project illustrates severe constraints limiting the powers of the state as well as the incidence of intra-industry collaboration in Japan. Neither set of outcomes are compatible with the analyses of state capacity and industrial structure. These findings hint at large-scale changes in the American and Japanese political economies: the dismantling of the strong state and erosion of collaborative government-buiness and intra-industry relations in Japan; and the forging of a closer relationship between public and private sectors in the U.S. While such profound generalizations may prove valid, the present case studies carry more theoretical than empirical, more disconfirming than affirming implications. The cases demonstrate that a significant incongruence has emerged between governmental and industrial structures on the one hand and political-economic behavior on the other. The VHSIC program and VLSI project exhibit much greater similarities than broader contrasting features of the American and Japanese political economies would suggest. The VHSIC program provides evidence of enhanced opportunities for industrial policy-making in the United States while the VLSI experience highlights the problematic conduct of Japanese industrial policy. This is not to say that the VHSIC experience can

24 necessarily be transferred across all industrial sectors, or that the strength of the Japanese state will be undercut in all cases or reduced to levels shared by other industrial countries, particularly the United States.95 The case studies do suggest, however, that differentials in political-economic behavior across sectors and across countries may not be as great as anticipated by the analyses of state capacity and industrial structure. The VHSIC and VLSI experiences are, of course, but two cases that do not happen to sustain the two explanatory frameworks. Other episodes of government-industry interaction might more closely reflect the expectations of the models. But if, as is argued, the two technology programs represent crucial test cases for industrial structure and state capacity analyses, then the negative findings cannot be easily dismissed. As Eckstein observes regarding crucial cases, "it [is] extremely difficult, or clearly petulant, to dismiss any finding contrary to theory as simply 'deviant' ...."96 Two major modes of analyses have been found wanting in cases that more than should have upheld their predictions. These results should reinforce the search for explanatory models of the Japanese and American political economies. Determining, for instance, why the U.S. semiconductor industry has become more receptive to government support and why Japanese industrial collaboration and the powers of the Japanese state have become increasingly constrained may lead to modifications in or alternatives to industrial and state structural analyses.

25

NOTES This article is based upon research conducted in collaboration with Michael Yoshino and his support is greatly appreciated. I am also grateful to Peter Katzenstein for comments on an earlier draft. Unless indicated otherwise, program-specific details reported here draw upon personal interviews with government and industry officials in the United States and Japan conducted between November 1982 and February 1984. This research was sponsored by the Division of Research at the Harvard University Graduate School of Business Administration. 1 For an introduction to the policy debate in the U.S., see Joseph Badaracco and David Yoffie, "Industrial Policy: It Can't Happen Here," Harvard Business Review, 83 (November-December 1983); Robert Hayes and William Abernathy, "Managing Our Way to Economic Decline," Harvard Business Review, 58 (July-August 1980); Paul R. Krugman, "Targeted Industrial Policies: Theory and Evidence" in Federal Reserve Bank of Kansas City, Industrial Change and Policy (Kansas City: Federal Reserve, August 24-26, 1983); Robert Z. Lawrence, Can America Compete? (Washington: Brookings, 1984); Ira C. Magaziner and Robert B. Reich, Minding America's Business (New York: Harcourt, 1982). 2 See Peter J. Katzenstein, ed., Between Power and Plenty: Foreign Economic Policies of Advanced Industrial States (Madison: University of Wisconsin Press, 1978); John Zysman, Governments, Markets, and Growth: Financial Systems and the Politics of Industrial Change (Ithaca: Cornell University Press, 1983); and John Zysman and Laura Tyson, eds., American Industry in International Competition: Government Policies and Corporate Strategies (Ithaca: Cornell University Press, 1983). 3 As used in this article, industrial policy refers to government initiatives -- for instance, subsidies, credit schemes, tax measures, trade policies, antitrust regulations, and research and development programs -- explicitly designed to develop and/or retrench various industries to maintain global competitiveness. Public policies that have unintended consequences for industrial competitiveness and exclusively private-sector competitive strategies would not be considered industrial policies. 4 While important technical distinctions exist between them, the terms "semiconductors," "integrated circuits," and "microelectronics" are used interchangeably in this article. 5 See selections in Zysman and Tyson, American Industry in International Competition as well as Margaret E. Dewar, ed., Industry Vitalization: Toward a National Industrial Policy (New York: Pergamon Press, 1982); Lawrence G. Franko and Sherry Stephenson, "The Micro Picture: Corporate and Sectoral Developments" in Louis Turner and Neil McMullen, eds., The Newly Industrialized Countries: Trade and Adjustment (London: George Allen and Unwin, 1982); James R. Kurth, "The Political Consequences of the Product Cycle: Industrial History and Political Outcomes," International Organization, 33 (Winter 1979); and Kurth, "Industrial Change and Political Change: A European perspective" in David Collier, ed., The New Authoritarianism in Latin America (Princeton: Princeton University Press, 1979). 6 Industrial structure analysis constitutes an important component of a broader body of literature on industrial sectors. The larger literature examines not just structural features of industrial production and markets, but also considers such variables as international competitiveness, position in an industry life-cycle, and transnational linkages. Analytical precision can be advanced by distinguishing domestic variables such as industrial structure from what are essentially international variables relating to competitiveness and transnational ties. As such, the analysis in this article applies only to the domestic structural component of the literature.

26

7 Michael Borrus, "The Politics of Competitive Erosion in the U.S. Steel Industry" in American Industry in International Competition; and Eugene J. Kaplan, Japan: The Government-Business Relationship (Washington: U.S. Department of Commerce, February 1972), Appendix C. 8 Vinod K. Aggarwal with Stephen Haggard, "The Politics of Protection in the U.S. Textile and Apparel Industries" in American Industry in International Competition; and Lynn Krieger Mytelka, "The French Textile Industry: Crisis and Adjustment" in Harold K. Jacobson and Dusan Sidjanski, eds., The Emerging International Economic Order (Beverely Hills: Sage, 1982). 9 Mytelka; and Aggarwal with Haggard. 10 Borrus, "The Politics of Competitive Erosion;" James E. Millstein, "Decline in an Expanding Industry: Japanese Competition in Color Televisions" in American Industry in International Competition; and Aggarwal with Haggard. 11 Thomas L. Ilgen, "Better Living Through Chemistry: The Chemical Industry in the World Economy," International Organization, 37 (Autumn 1983); Richard R. Nelson, "Government Stimulus of Technical Progress: Lessons from American Industry" in Nelson, ed., Government and Technical Progress: A Cross-Industry Analysis (Elmsford: Pergamon Press, 1982); and Nelson and Sidney G. Winter, An Evolutionary Theory of Economic Change (Cambridge: Harvard University Press, 1982), pp. 392-393. 12 David B. Yoffie, "Adjustment in the Footwear Industry: The Consequences of Orderly Marketing Agreements" in American Industry in International Competition; and Millstein. 13 See selections in Katzenstein, Between Power and Plenty as well as Peter B. Evans, Dietrich Rueschemeyer, and Theda Skocpol, eds., Bringing the State Back In (Cambridge: Cambridge University Press, 1985); Peter A. Hall, Governing the Economy: The Politics of State Intervention in Britain and France (New York: Oxford, 1986); Katzenstein, "International Relations and Domestic Structures: Foreign Economic Policies of Advanced Industrial States," International Organization, 30 (Winter 1976); Stephen D. Krasner, Defending the National Interest: Raw Materials Investments and U.S. Foreign Policy (Princeton: Princeton University Press, 1978); Krasner, "Approaches to the State: Alternative Conceptions and Historical Dynamics," Comparative Politics, 16 (January 1984); Eric Nordlinger, On the Autonomy of the Democratic State (Cambridge: Harvard, 1981); Theda Skocpol and Kenneth Finegold, "State Capacity and Economic Intervention in the Early New Deal," Political Science Quarterly, 97 (Summer 1982); and Zysman, Governments, Markets, and Growth. 14 Most analyses of state structure consider the composition of political coalitions along with institutional variables. This article considers only the institutional argument and does not reflect upon the utility of coalitional analysis. 15 Chalmers Johnson, MITI and the Japanese Miracle: 1925-75 (Stanford: Stanford University Press, 1982); Johnson, "The Institutional Foundations of Japanese Industrial Policy" in Claude E. Barfield and William Scambra, eds., The Politics of Industrial Policy (Washington: AEI, 1985; Kaplan; Ira C. Magaziner and Thomas M. Hout, Japanese Industrial Policy (Berkeley: Institute of International Studies, 1980); T.J. Pempel, "Japanese Foreign Economic Policy: The Domestic Bases for International Behavior" in Between Power and Plenty; Pempel, Policy and Politics in Japan (Philadelphia: Temple, 1982); Miyohei Shinohara, Industrial Growth, Trade, and Dynamic Patterns in the Japanese Economy (Tokyo: University of Tokyo, 1982); Bernard Silberman, "The Bureaucratic State in Japan: The Problem of Authority and Legitimacy" in T. Najita and J.V. Koschman, eds., Conflict in Modern Japanese History: The Neglected Tradition (Princeton: Princeton, 1982); and John Zysman and Stephen S. Cohen, The Mercantilist

27

Challenge to the Liberal International Trade Order (Washington: U.S. Congress, Joint Economic Committee, November 1982). 16 Edward J. Lincoln, Japan's Industrial Policies: What Are They, Do They Matter, and Are They Different from those in the United States? (Japan Economic Institute, April 1984), p. 17. 17 Johnson, MITI and the Japanese Miracle, p.26; and "Government-Business Relations in Japan," JEI Report, March 15, 1985, p. 1. See also Sinohara, p. 21. 18 Johnson, MITI and the Japanese Miracle, p.26. 19 Louis Hartz, The Liberal Tradition in America (New York: Harcourt, 1955); Samuel P. Huntington, Political Order in Changing Societies (New Haven: Yale, 1968), chapter 3; Stephen D. Krasner, "U.S. Commercial and Monetary Policy: Unravelling the Paradox of External Strength and Internal Weakness" in Between Power and Plenty; Krasner, Defending the National Interest; and Stephen Skowronek, Building a New American State: The Expansion of National Administrative Capacities, 1877-1920 (New York: Cambridge, 1982). For both country cases, also see Peter J. Katzenstein, "Conclusion: Domestic Structures and Strategies of Foreign Economic Policy" in Between Power and Plenty. 20 Magaziner and Reich, p. 257. 21 Ibid., Part III. 22 Grant McConnell, Private Power and American Democracy (New York: Knopf, 1966); Thomas K. McCraw, "Business and Government: The Origins of the Adversary Relationship," California Management Review, 27 (Winter 1984); Andrew Shonfield, Modern Capitalism: The Changing Balance of Public and Private Power (London: Oxford, 1965), chapter 13; and David Vogel, "Why Businessmen Distrust Their State: The Political Consciousness of American Corporate Executives," British Journal of Political Science, 8 (January 1978). 23 Kaplan; and Pempel, Policy and Politics in Japan. 24 For overviews of the debate, see John Creighton Campbell, "Policy Conflict and Its Resolution within the Governmental System" in Ellis S. Kraus, et.al., eds., Conflict in Japan (Honolulu: University of Hawaii, 1984); and Haruhiro Fukui, "Studies in Policymaking: A Review of the Literature" in T.J. Pempel, ed., Policymaking in Contemporary Japan (Ithaca: Cornell, 1976). 25 Campbell, "Policy Conflict;" John Creighton Campbell, Contemporary Japanese Budget Politics (New York: Columbia, 1977); Gerald L. Curtis, "Big Business and Political Influence" in Ezra F. Vogel, ed., Modern Japanese Organization and Decision-making (Berkeley: University of California, 1975); Krauss, Conflict in Japan; and Michio Muramatsu and Ellis S. Krauss, "The Conservative Policy Line and the Development of Patterned Pluralism" in Kozo Yamamura and Yasukichi Yasuba, eds., The Political Economy of Japan, Volume I: The Domestic Transition (Stanford: Stanford University Press, 1987). 26 Lincoln; Hugh Patrick and Henry Rosovsky, eds., Asia's New Giant: How the Japanese Economy Works (Washington: Brookings, 1975); Richard J. Samuels, The Business of the Japanese State (Ithaca: Cornell, 1987); Gary Saxonhouse, "What is All This About Industrial Targeting in Japan?" World Economy (September 1983); Philip H. Tresize with Yukio Suzuki, "Politics, Government, and Economic Growth in Japan" in Asia's New Giant; and Tresize, "Industrial Policy in Japan" in Industry Vitalization.