statement of cash flows chapter 5. objectives of the statement of cash flows the statement of cash...

TRANSCRIPT

Statement of Cash Statement of Cash FlowsFlows

Chapter 5

Objectives of the Statement of Cash Flows• The statement of cash flows

provides information about a firm's inflows and outflows of cash during a period of time.– It states where a firm's money

comes from and how it is used.

Objectives of the Statement of Cash Flows• The statement of cash flows

provides information about a firm's inflows and outflows of cash during a period of time.– This information is not that easy to

find by simply studying the other three financial statements.

Objectives of the Statement of Cash FlowsObjectives of the Statement of Cash Flows

• The statement also explains the change in the Cash account from the beginning to the end of the period.

Objectives of the Statement of Cash FlowsObjectives of the Statement of Cash Flows

• SFAS No. 95 requires a business to prepare a statement of cash flows.

The statement helps readers assess the following:The statement helps readers assess the following:

• A firm's ability to generate positive future net cash flows.

• A firm's ability to meet its obligations, its ability to pay dividends, and its needs for external financing.

The statement helps readers assess the following:The statement helps readers assess the following:

• The reasons for differences between net income and associated cash receipts and payments.

The statement helps readers assess the following:The statement helps readers assess the following:

• The effects on a firm's financial position of both its cash and noncash investing and financing transactions.

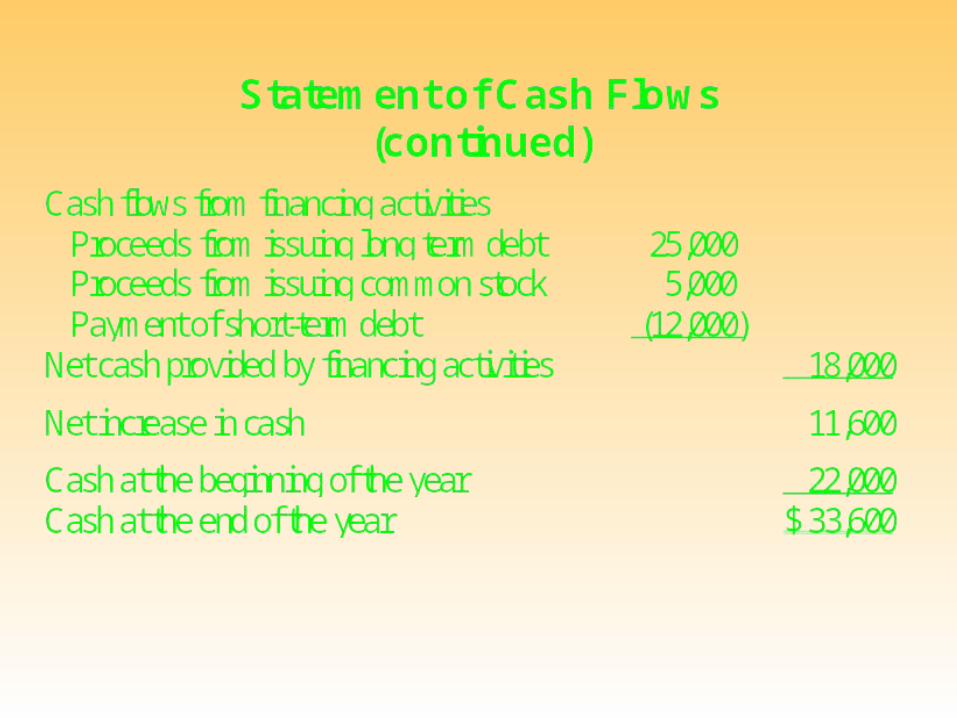

Statement of Cash FlowsCash flows from operating activities:

Cash received from customers $ 68,200Interest received 1,300Payments to employees (17,100)Payments to suppliers (40,500)Interest paid (800)Taxes paid (2,000)

Net cash provided from operating activities $ 9,100

Cash flows from investing activitiesPurchase of equipment (3,500)Purchase of equipment and shares (12,000)

Net cash used in investing activities (15,500)

The Nature of Accrual Earnings and Cash FlowsThe Nature of Accrual Earnings and Cash Flows

• Accrual earnings do not necessarily reflect cash flows. – For example, depreciation expense

reduces accrual net income but is not related at all to cash flow.

The Nature of Accrual Earnings and Cash FlowsThe Nature of Accrual Earnings and Cash Flows

• Earnings and cash flows should be viewed as complements, not substitutes—each has information not necessarily contained in the other.

The Nature of Accrual Earnings and Cash FlowsThe Nature of Accrual Earnings and Cash Flows

• The statement provides information about a firm's liquidity and financial flexibility.

The Nature of Accrual Earnings and Cash FlowsThe Nature of Accrual Earnings and Cash Flows

• It helps gauge the ability to respond to unexpected events by altering the amounts and timing of its cash flows.

Cash and Cash Equivalents

• A firm must decide whether to focus the statement on cash or on cash and cash equivalents.– Cash equivalents are short-term,

highly liquid financial instruments with maturities of less than months.

– They include money market funds, treasury bills, and certificates of deposit (CDs).

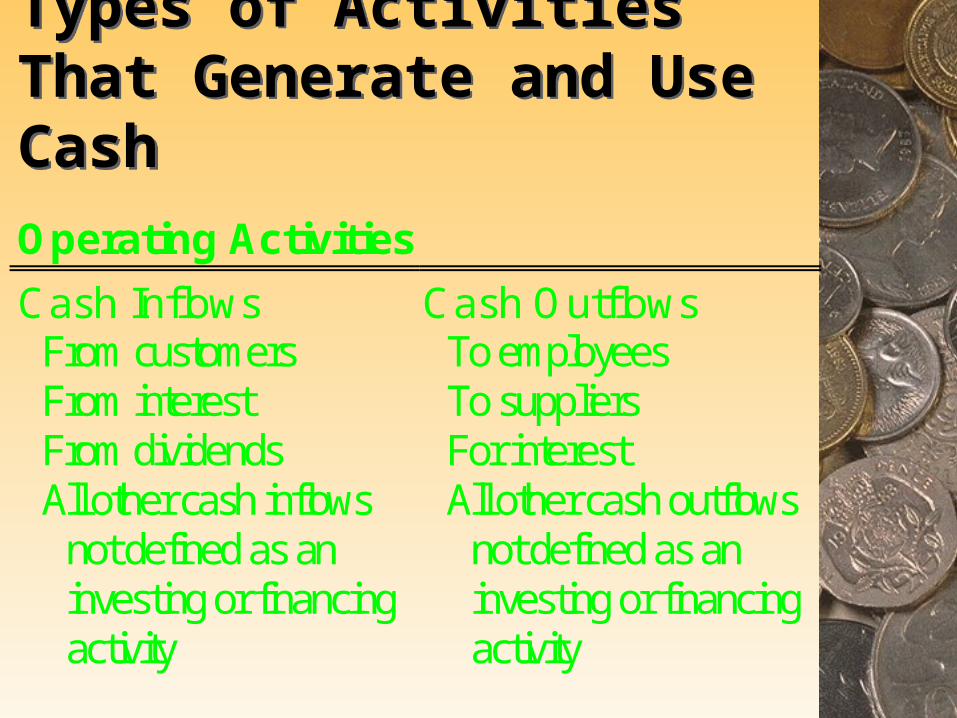

Types of Activities That Generate and Use CashTypes of Activities That Generate and Use Cash

• Operating Activities • Investing Activities• Financing Activities

Operating Activities Operating Activities

• Operating activities involve transactions related to providing goods and services to customers.– They show the cash flow effects of the

typical transactions which appear on the income statement.

– Examples include receipt of payment from customers and payments to employees and suppliers.

Investing Activities Investing Activities

• Investing activities usually involve cash flows from the acquisition and disposal of noncurrent assets.– Examples include the purchase or

sale of property, plant, and equipment and the purchase or sale of investments in other corporations.

Financing Activities Financing Activities

• Financing activities include cash flows from obtaining and repaying financing.– This includes transactions involving

long-term liabilities and shareholders' equity.

– Examples include payment of dividends and buying back shares from shareholders.

Types of Activities That Generate and Use CashTypes of Activities That Generate and Use CashOperating Activities

Cash Inflows Cash OutflowsFrom customers To employeesFrom interest To suppliersFrom dividends For interestAll other cash inflows

not defined as aninvesting or financingactivity

All other cash outflowsnot defined as aninvesting or financingactivity

Types of Activities That Generate and Use CashTypes of Activities That Generate and Use Cash

Types of Activities That Generate and Use CashTypes of Activities That Generate and Use Cash

Methods of Presenting a Statement of Cash FlowsMethods of Presenting a Statement of Cash Flows

• Direct Versus Indirect Approach– SFAS No. 95 allows the use of the

direct or the indirect methods for preparation of the operating activities section of the statement of cash flows.

Direct Versus Indirect ApproachDirect Versus Indirect Approach

• Under the direct method, a separate line item is provided for each type of operating cash inflow and outflow.– These line items correspond to

categories on the income statement.– A major advantage of this method is

that the primary sources and uses of cash are listed.

Direct Versus Indirect ApproachDirect Versus Indirect Approach

• The indirect method begins with accrual-basis net income and makes adjustments to it in order to arrive at cash generated by operating activities.

Direct Versus Indirect ApproachDirect Versus Indirect Approach

• A major advantage of the indirect method is that the reasons for the difference between net income and cash generated by operations are detailed.

Direct Versus Indirect ApproachDirect Versus Indirect Approach

• While the FASB prefers the direct method, businesses use the indirect method more frequently.

Direct Versus Indirect ApproachDirect Versus Indirect Approach

• The indirect approach is similar to the approach used for preparation of the statement required before the issuance of SFAS No. 95.

Direct Versus Indirect ApproachDirect Versus Indirect Approach

• A firm using the direct approach must provide a schedule that reconciles net income with cash provided by operating activities.

Direct Versus Indirect ApproachDirect Versus Indirect Approach

• This schedule consists of the information contained in the indirect approach.

Noncash Investing and Financing ActivitiesNoncash Investing and Financing Activities

• Noncash investing and financing activities do not appear in the body of the statement.– They are summarized in a schedule that

appears at the end of the statement.– Examples include the purchase of land

by issuing common stock or the purchase of equipment by issuing a note payable.

Using Cash Flow InformationUsing Cash Flow Information

• Creditors, shareholders, and analysts find the statement's operating activities section to be very useful.

Using Cash Flow InformationUsing Cash Flow Information

• Many analysts prefer operating activities to net income as a performance measure because net income can be manipulated by accounting conventions.

Using Cash Flow InformationUsing Cash Flow Information

• A variety of ratios can be computed using the operating activities section.

Cash Return on AssetsCash Return on Assets

• Cash return on assets is calculated by dividing average total assets into the sum of cash flow from operating activities (CFOA), interest paid, and taxes paid.

Cash return on assets =CFOA + Interest paid

Average total assets

Cash Return on Assets Cash Return on Assets

• This ratio measures management's success in generating cash from operating activities, and a high ratio is desirable.

Cash Return on Assets Cash Return on Assets

• Some analysts use free cash flow instead of CFOA.

Cash Return on Assets Cash Return on Assets

• Free cash flow is calculated by subtracting from CFOA the cash payment necessary to replace worn-out equipment.

The Quality of Sales RatioThe Quality of Sales Ratio

• The quality of sales ratio is computed by dividing sales into cash received from customers.

Quality of sales =Cash received from customers

Sales

The Quality of Sales Ratio The Quality of Sales Ratio

• Cash received from customers can be computed by adding the beginning balance of accounts receivable and sales and then subtracting the ending balance of accounts receivable.

The Quality of Sales Ratio The Quality of Sales Ratio

• This ratio is useful in analyzing firms that use liberal revenue recognition policies or firms which must exercise considerable judgment in selecting revenue recognition policies.

The Quality of Sales Ratio The Quality of Sales Ratio

• This ratio can reflect a firm's performance in collecting from customers.

The Quality of Sales Ratio The Quality of Sales Ratio

• A high ratio is desirable.

The Quality of Income RatioThe Quality of Income Ratio

• The quality of income ratio is computed by dividing net income into CFOA.

Quality of income =CFOA

Net income

The Quality of Income Ratio The Quality of Income Ratio

• This ratio indicates the proportion of income which has been realized in cash, and high levels of the ratio are desirable.

The Quality of Income Ratio The Quality of Income Ratio

• The ratio often exceeds 100%.

The Cash Interest Coverage RatioThe Cash Interest Coverage Ratio

• The cash interest coverage ratio is computed by adding CFOA and interest and tax payments and then dividing the total by interest payments.

Cash interest coverage =CFOA+ Interest paid +Taxes paid

Interest paid

The Cash Interest Coverage Ratio The Cash Interest Coverage Ratio

• It is used by creditors to assess a firm's ability to pay interest.

The Cash Interest Coverage Ratio The Cash Interest Coverage Ratio

• As is true with the three ratios discussed above, a high ratio is desirable.

Investing and Financing Activities Investing and Financing Activities

• The investing activities section of the statement of cash flows summarizes the cash in- and outflows from disposing and purchasing of investments.

Investing and Financing Activities Investing and Financing Activities

• These sections are scrutinized less closely by financial statement users.

Preparing a Statement of Cash Flows

Appendix 5

Preparing a Statement of Cash FlowsPreparing a Statement of Cash Flows

• Cash flows are inferred from items on the balance sheet and income statement.

Collections from CustomersCollections from Customers

• Equals beginning Accounts Receivable + Sales – ending Accounts Receivable

Interest ReceivedInterest Received

• Equals beginning Interest Receivable + Interest Revenue – ending Interest Receivable

Payments to Employees Payments to Employees

• Equals beginning Salaries Payable + Salary Expense – ending Salaries Payable

Interest Paid Interest Paid

• Equals beginning interest payable + interest expense – ending interest payable

Payments to Suppliers Payments to Suppliers

• First solve for cost of goods sold.

COGS = Beginning inventory + Purchases – Ending inventory

• Then rearrange the equation to solve for purchases.Purchases = COGS – Beginning inventory

+ Ending inventory

Payments to Suppliers Payments to Suppliers

• Then solve for Payments to SuppliersPayments to Suppliers = Beginning

accounts payable + Purchases – Ending accounts payable

General GuideGeneral Guide

• Depreciation expense is not considered when using the direct method.

• Do not consider gains and losses associated with nonoperating activities.

General GuideGeneral Guide

• Adjust remaining income statement items by the changes in related balance sheet accounts.

Indirect Approach Indirect Approach

• When using the indirect approach, accrual-basis net income is converted to cash flows from operating activities.

Indirect Approach Indirect Approach

• Expense items, such as depreciation, which have reduced net income must be added back because they do not involve cash flow.

Indirect Approach Indirect Approach

• Other items, such as Accounts Receivable, must be addressed.

Indirect Approach Indirect Approach

• If Accounts Receivable has increased during the period, then the increase must be deducted from accrual-basis net income because this indicates that credit sales, which do not involve cash flow, have increased the net income number.

Indirect Approach Indirect Approach

• The opposite will be true if Accounts Receivable has decreased during the period.

Indirect Approach Indirect Approach

• The investing and financing activities sections will be exactly the same under both the direct and the indirect methods.

Statement of Cash Statement of Cash FlowsFlows

End of Chapter 5