statewide accounts receivable management report - oregon fy2016 final… · 30-06-2016 · overall...

TRANSCRIPT

STATEWIDE

ACCOUNTS RECEIVABLE

MANAGEMENT REPORT

F I S C A L Y E A R E N D I N G J U N E 3 0 , 2 0 1 6

i

Dec. 23, 2016 To the members of the Oregon Legislative Assembly, Enclosed is the Statewide Accounts Receivable Management Report as required by Oregon Revised Statute 293.252(1)(e). The report identifies important issues and significant trends in state agency debt collection practices and describes efforts by state agencies to improve the collection of liquidated and delinquent debt. The report references liquidated and delinquent account activity reported by state agencies to the Legislative Fiscal Office for the fiscal year ending June 30, 2016. This is the first report issued under the statute mentioned above. Sincerely,

George Naughton Chief Financial Officer

Department of Administrative Services Chief Financial Office

155 Cottage Street NE

Salem, OR 97301

PHONE: 503-378-3106

FAX: 503-373-7643

Kate Brown, Governor

Fiscal Year 2016 Statewide Accounts Receivable Management Report

ii

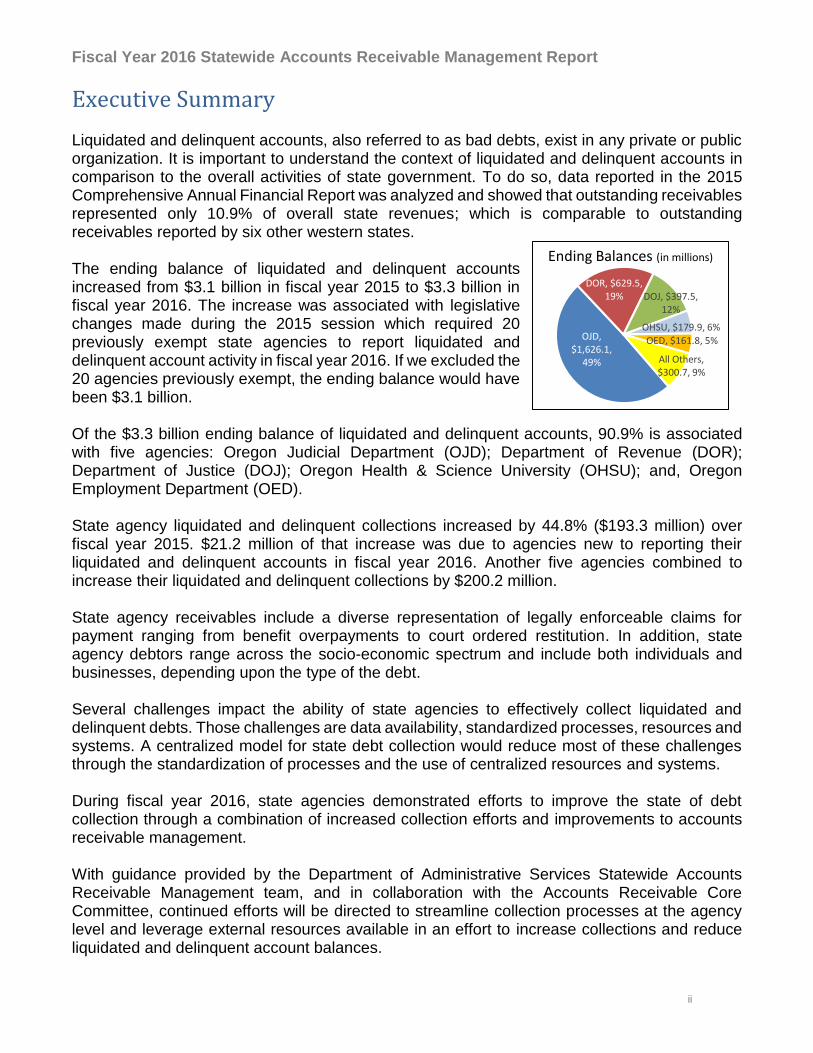

Executive Summary Liquidated and delinquent accounts, also referred to as bad debts, exist in any private or public organization. It is important to understand the context of liquidated and delinquent accounts in comparison to the overall activities of state government. To do so, data reported in the 2015 Comprehensive Annual Financial Report was analyzed and showed that outstanding receivables represented only 10.9% of overall state revenues; which is comparable to outstanding receivables reported by six other western states. The ending balance of liquidated and delinquent accounts increased from $3.1 billion in fiscal year 2015 to $3.3 billion in fiscal year 2016. The increase was associated with legislative changes made during the 2015 session which required 20 previously exempt state agencies to report liquidated and delinquent account activity in fiscal year 2016. If we excluded the 20 agencies previously exempt, the ending balance would have been $3.1 billion. Of the $3.3 billion ending balance of liquidated and delinquent accounts, 90.9% is associated with five agencies: Oregon Judicial Department (OJD); Department of Revenue (DOR); Department of Justice (DOJ); Oregon Health & Science University (OHSU); and, Oregon Employment Department (OED). State agency liquidated and delinquent collections increased by 44.8% ($193.3 million) over fiscal year 2015. $21.2 million of that increase was due to agencies new to reporting their liquidated and delinquent accounts in fiscal year 2016. Another five agencies combined to increase their liquidated and delinquent collections by $200.2 million. State agency receivables include a diverse representation of legally enforceable claims for payment ranging from benefit overpayments to court ordered restitution. In addition, state agency debtors range across the socio-economic spectrum and include both individuals and businesses, depending upon the type of the debt. Several challenges impact the ability of state agencies to effectively collect liquidated and delinquent debts. Those challenges are data availability, standardized processes, resources and systems. A centralized model for state debt collection would reduce most of these challenges through the standardization of processes and the use of centralized resources and systems. During fiscal year 2016, state agencies demonstrated efforts to improve the state of debt collection through a combination of increased collection efforts and improvements to accounts receivable management. With guidance provided by the Department of Administrative Services Statewide Accounts Receivable Management team, and in collaboration with the Accounts Receivable Core Committee, continued efforts will be directed to streamline collection processes at the agency level and leverage external resources available in an effort to increase collections and reduce liquidated and delinquent account balances.

OJD, $1,626.1,

49%

DOR, $629.5, 19% DOJ, $397.5,

12%

OHSU, $179.9, 6%

OED, $161.8, 5%

All Others, $300.7, 9%

Ending Balances (in millions)

Fiscal Year 2016 Statewide Accounts Receivable Management Report

iii

Table of Contents

Introduction ................................................................................................................................................. 1

How the State Collects Debt ....................................................................................................................... 1

Executive Branch Agencies .................................................................................................................... 1

Judicial Branch Agencies ........................................................................................................................ 4

Statewide Accounts Receivable Management ............................................................................................ 4

Accounts Receivable Core Committee ................................................................................................... 4

Communication Subcommittee ............................................................................................................... 4

Performance Metrics Subcommittee ....................................................................................................... 5

Policy Development and Review Subcommittee .................................................................................... 5

Tools and Process Improvement Subcommittee ..................................................................................... 5

Factors in Collecting Receivables ............................................................................................................... 5

Types of Receivables .............................................................................................................................. 5

Types of Debtors ..................................................................................................................................... 6

Collection Tools .......................................................................................................................................... 8

Data Analysis .............................................................................................................................................. 9

Overall Receivable Analysis from Comprehensive Annual Financial Report ....................................... 9

Liquidated and Delinquent Account Analysis ...................................................................................... 10

Five Agencies with the Largest Ending Balance .................................................................................. 11

Changes in Liquidated and Delinquent Account Balances ................................................................... 13

Current State of Debt Collections ......................................................................................................... 15

Collection Trends ...................................................................................................................................... 16

Bankruptcy Filings ................................................................................................................................ 16

Unemployment ...................................................................................................................................... 17

Liquidated and Delinquent Trends ........................................................................................................ 18

Statewide Efforts to Improve Collections ................................................................................................. 19

SWARM Efforts ................................................................................................................................... 19

Agency Efforts ...................................................................................................................................... 20

Collection Issues and Challenges.............................................................................................................. 22

Data Availability ................................................................................................................................... 22

Systems ................................................................................................................................................. 22

Standardization ..................................................................................................................................... 22

Resources .............................................................................................................................................. 23

Social Security Number Collection and Use ........................................................................................ 23

Future of State Debt Collections ............................................................................................................... 24

Conclusion ................................................................................................................................................ 25

Fiscal Year 2016 Statewide Accounts Receivable Management Report

iv

Acknowledgments..................................................................................................................................... 26

Appendix A – Unassigned Accounts Greater Than 90 days by Agency ............................................ 27

Appendix B – Collection Workflows ..................................................................................................... 32

Appendix C – Glossary of Terms .......................................................................................................... 34

1

Introduction

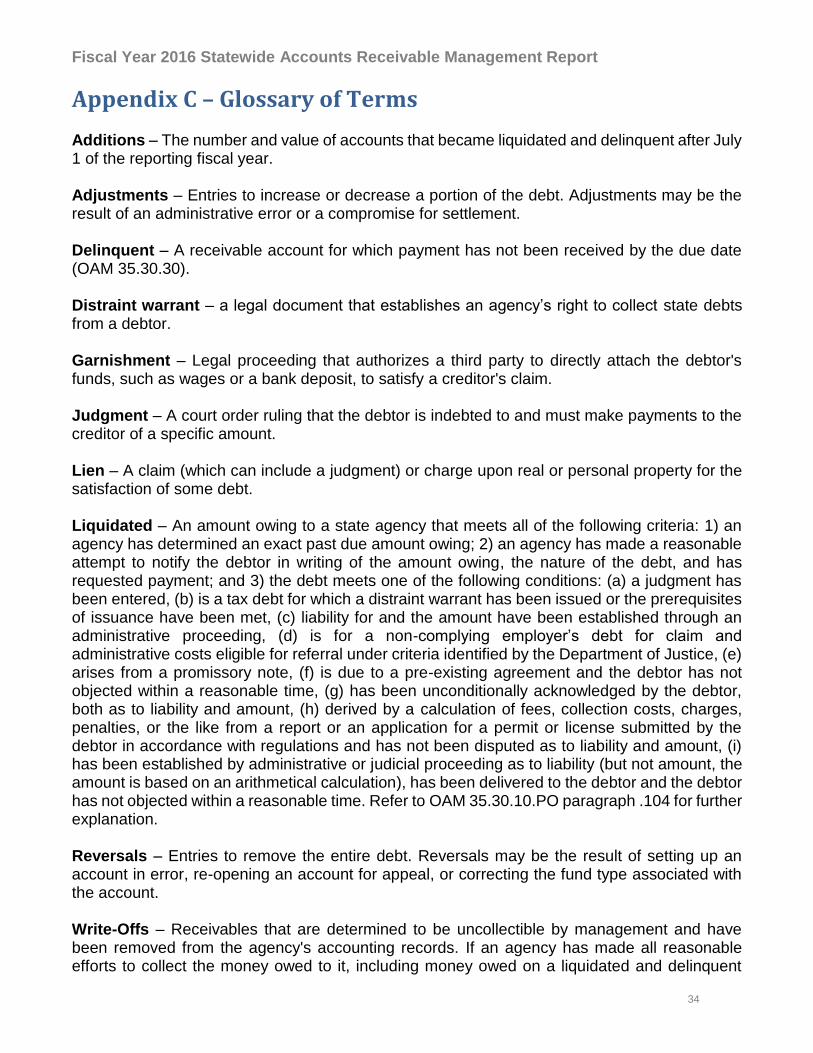

As required by Oregon Revised Statute (ORS) 293.252, the Department of Administrative Services (DAS) hereby submits the annual Statewide Accounts Receivable Management report to the Legislative Assembly in conjunction with the Legislative Fiscal Office’s (LFO) Report on Liquidated and Delinquent Accounts Receivable.1 The Statewide Accounts Receivable Management Report identifies important issues and significant trends in state agency debt collection practices and describes efforts by state agencies to improve the collection of delinquent debt. The receivables data referenced in this report represents liquidated and delinquent accounts as of June 30, 2016, as reported by state agencies to LFO. The accounts include debts between state agencies and an individual or entity in which the debt was not paid by the due date and the debtor was notified of the debt and given an opportunity to dispute the debt. For reference purposes, terms that are bold in this report are defined in Appendix C.

How the State Collects Debt The statutory requirements pertaining to collecting liquidated and delinquent debt are documented in two chapters of the ORS based upon the applicable branch of state government. The collection and assignment provisions of ORS Chapter 1 apply to agencies within the judicial branch2 and the provisions of ORS Chapter 293 apply to agencies within the administrative or executive branch.3 Statewide policies and procedures pertaining to accounts receivable management are documented in Oregon Accounting Manual (OAM) Chapter 35 and are applicable to administrative or executive branch agencies subject to report financial activity in the Comprehensive Annual Financial Report. 4

Executive Branch Agencies Agencies have an obligation to bill for goods provided, or services rendered, in a timely manner. When an account is not paid by the due date it becomes delinquent. The state agency is then responsible for conducting preliminary collection activities. These activities include contacting the debtor by phone or sending a series of escalating letters to notify the debtor of the amount of the debt and to request payment. The letters also serve to notify the debtor of: procedures and deadlines to dispute the debt; interest costs; the account assignment to the Department of Revenue-Other Agency Accounts (DOR-OAA) unit or a private collection agency (PCA); and the additional collection costs associated with assigning the account. Letters are a common method used to liquidate an account. However, accounts may also become liquidated as the result of a court or administrative order; written agreement between the state agency and the debtor; or by the debtor acknowledging the debt. 5

1 ORS Chapter 293.252(1)(e) 2 ORS Chapter 1.194-1.202 documents the collection of court account requirements; including, but not limited to, account assignment provisions. 3 Agencies required to report liquidated and delinquent accounts annually to LFO identified in ORS 293.229(4) are exempt from the assignment provisions of ORS 293.231. 4 Agencies required to report financial information in the Comprehensive Annual Financial Report are subject to the statewide policies and procedures outlined in the Oregon Accounting Manual. 5 OAM 35.30.30 definition of liquidated and delinquent accounts.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

2

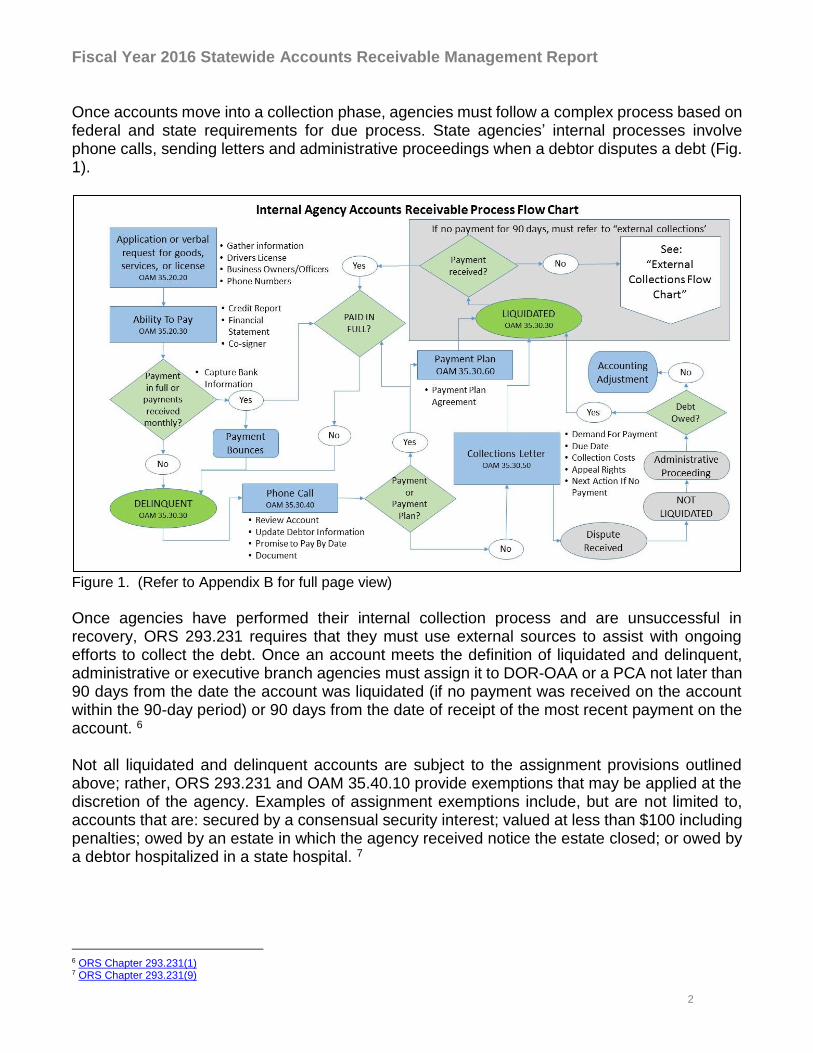

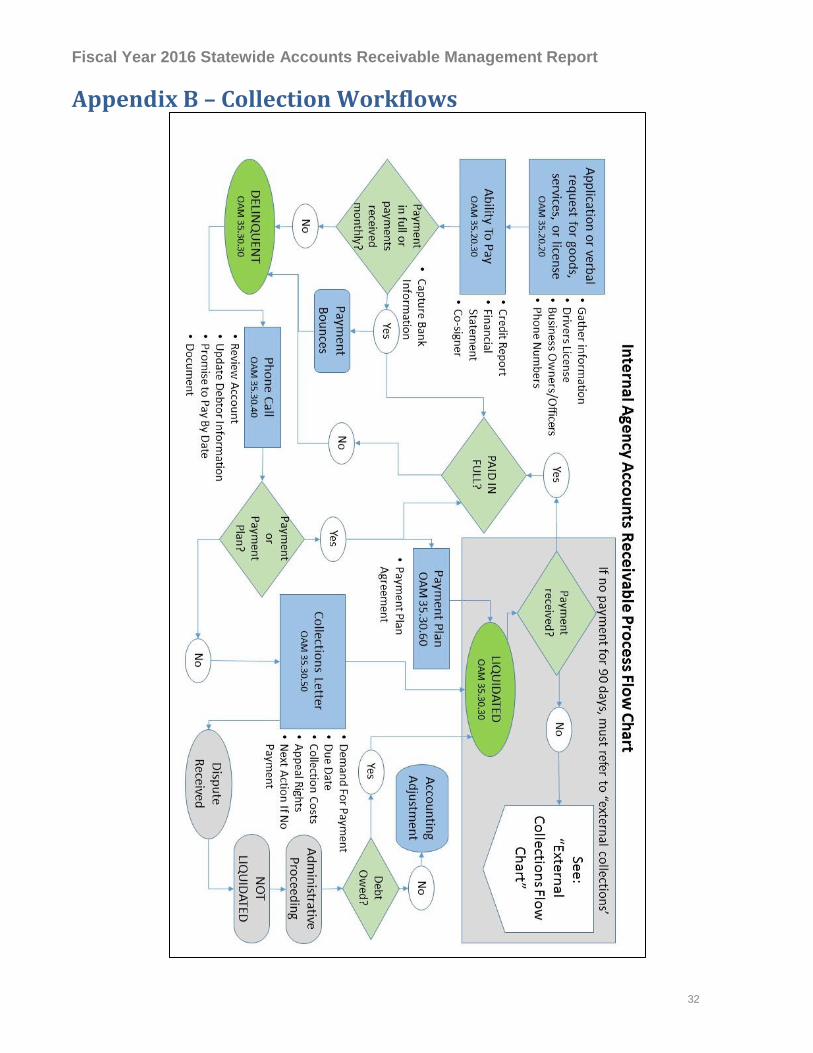

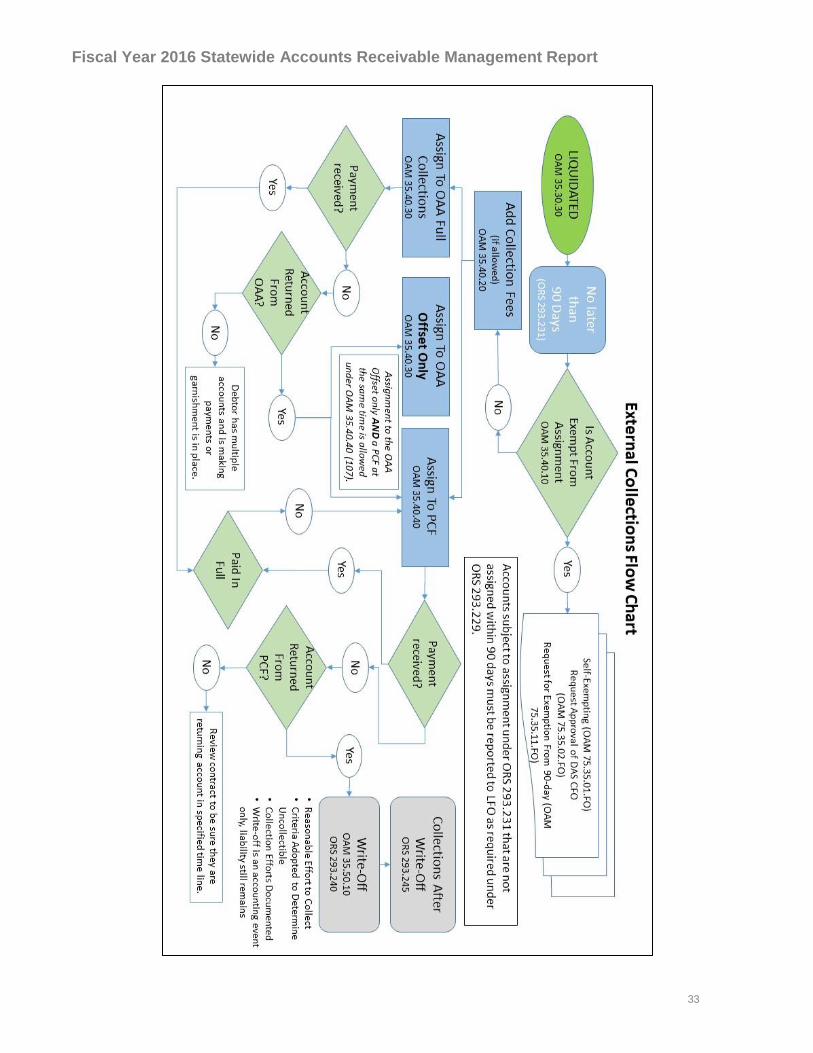

Once accounts move into a collection phase, agencies must follow a complex process based on federal and state requirements for due process. State agencies’ internal processes involve phone calls, sending letters and administrative proceedings when a debtor disputes a debt (Fig. 1).

Figure 1. (Refer to Appendix B for full page view)

Once agencies have performed their internal collection process and are unsuccessful in recovery, ORS 293.231 requires that they must use external sources to assist with ongoing efforts to collect the debt. Once an account meets the definition of liquidated and delinquent, administrative or executive branch agencies must assign it to DOR-OAA or a PCA not later than 90 days from the date the account was liquidated (if no payment was received on the account within the 90-day period) or 90 days from the date of receipt of the most recent payment on the account. 6 Not all liquidated and delinquent accounts are subject to the assignment provisions outlined above; rather, ORS 293.231 and OAM 35.40.10 provide exemptions that may be applied at the discretion of the agency. Examples of assignment exemptions include, but are not limited to, accounts that are: secured by a consensual security interest; valued at less than $100 including penalties; owed by an estate in which the agency received notice the estate closed; or owed by a debtor hospitalized in a state hospital. 7

6 ORS Chapter 293.231(1) 7 ORS Chapter 293.231(9)

Fiscal Year 2016 Statewide Accounts Receivable Management Report

3

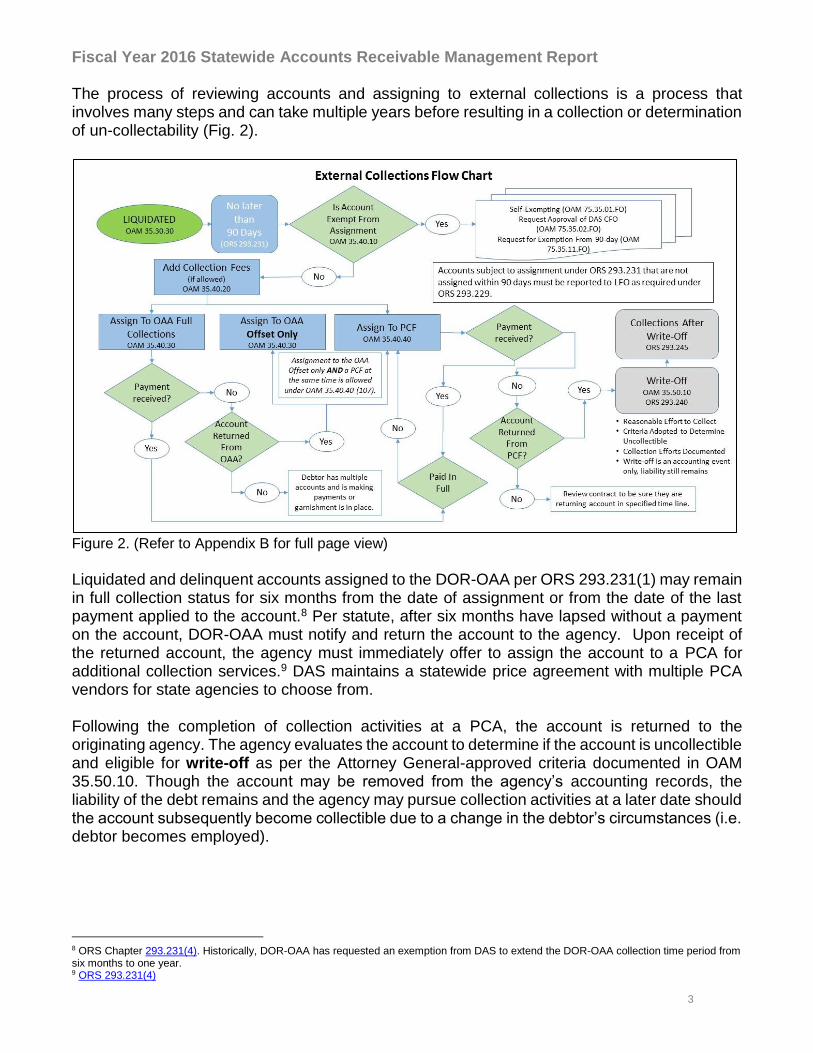

The process of reviewing accounts and assigning to external collections is a process that involves many steps and can take multiple years before resulting in a collection or determination of un-collectability (Fig. 2).

Figure 2. (Refer to Appendix B for full page view)

Liquidated and delinquent accounts assigned to the DOR-OAA per ORS 293.231(1) may remain in full collection status for six months from the date of assignment or from the date of the last payment applied to the account.8 Per statute, after six months have lapsed without a payment on the account, DOR-OAA must notify and return the account to the agency. Upon receipt of the returned account, the agency must immediately offer to assign the account to a PCA for additional collection services.9 DAS maintains a statewide price agreement with multiple PCA vendors for state agencies to choose from. Following the completion of collection activities at a PCA, the account is returned to the originating agency. The agency evaluates the account to determine if the account is uncollectible and eligible for write-off as per the Attorney General-approved criteria documented in OAM 35.50.10. Though the account may be removed from the agency’s accounting records, the liability of the debt remains and the agency may pursue collection activities at a later date should the account subsequently become collectible due to a change in the debtor’s circumstances (i.e. debtor becomes employed).

8 ORS Chapter 293.231(4). Historically, DOR-OAA has requested an exemption from DAS to extend the DOR-OAA collection time period from six months to one year. 9 ORS 293.231(4)

Fiscal Year 2016 Statewide Accounts Receivable Management Report

4

Judicial Branch Agencies Per ORS 1.19710, agencies within the judicial branch of state government shall offer to assign liquidated and delinquent accounts not later than one year from the date the account was liquidated (if no payment was received on the account within that year) or one year from the date of receipt of the most recent payment on the account. Furthermore, DOR-OAA has one year to collect on liquidated and delinquent accounts assigned by agencies of the judicial branch. If DOR-OAA does not collect a payment on the account within one year, or if one year has lapsed since the date of receipt of the most recent payment on the account, DOR-OAA must notify and return the account to the respective judicial branch agency who must then immediately offer to assign the account to a PCA. The Oregon Judicial Department maintains an agreement with multiple vendors on behalf of judicial branch agencies. Similar to administrative or executive branch agencies, some liquidated and delinquent accounts may be exempt from the one year assignment provisions referenced above. As provided in ORS 1.199, the State Court Administrator may establish policies and procedures for exempting accounts in addition to the exemptions referenced in ORS 1.198. Agencies of the judicial branch of state government are not subject to the statewide policies and procedures referenced in the OAM.

Statewide Accounts Receivable Management The 2015 Legislature directed DAS to monitor state agency debt collection functions and assist state agencies in efforts to improve the collection of delinquent debts.11 To meet the requirements, DAS created the Statewide Accounts Receivable Management (SWARM) team to provide training on processing and managing accounts receivable; offer technical assistance in resolving accounts receivable challenges; and develop performance standards for state debt collection. In an effort to improve the collection of delinquent debts and foster improved agency communication, SWARM leads the Accounts Receivable Core Committee (ARCC).

Accounts Receivable Core Committee The ARCC is comprised of accounts receivable representatives from state agencies who meet monthly to discuss current collection practices and assist SWARM in developing strategies to improve statewide accounts receivable management. The ARCC also serves as a forum for state agency accounts receivable professionals to collaborate with peers from other state agencies and to discuss successful collection strategies, lessons learned and best practices. To assist in meeting the objectives of the ARCC, four subcommittees were established to address specific statewide accounts receivable management topics: communication; performance metrics; policy review and development; and tools and process improvements.

Communication Subcommittee The role of the Communication Subcommittee is to improve communication between state agencies, debtors and debt collection stakeholders. The method and content of accounts

10 ORS Chapter 001.197 11 Oregon Laws 2015, Chapter 766

Fiscal Year 2016 Statewide Accounts Receivable Management Report

5

receivable-related messages are evaluated for effectiveness and efficiency. Subcommittee members identify existing communication methods and assist SWARM in developing enhancements to communication methods to ensure collection expectations, requirements and regulations are clearly communicated to stakeholders.

Performance Metrics Subcommittee The goal of the Performance Metrics Subcommittee is to assist SWARM in the identification of performance metrics to measure statewide accounts receivable management efforts. While some agencies have existing internal metrics for measuring accounts receivable management performance, other agencies have limited data available to measure performance. Subcommittee members provide SWARM with feedback regarding available data and resources to enable SWARM to successfully establish and implement effective statewide performance metrics.

Policy Development and Review Subcommittee The objective of the Policy Development and Review Subcommittee is to review existing accounts receivable policies, reflected in OAM Chapter 35, and to assist SWARM in developing new statewide accounts receivable policies based on administrative or legislative changes. Subcommittee members provide feedback to SWARM regarding the language and application of the policies as reference for modifying and clarifying the policies.

Tools and Process Improvement Subcommittee The purpose of the Tools and Process Improvement Subcommittee is to identify best practices and effective collection tools available to state agencies for accounts receivable management. Subcommittee members assist SWARM with evaluating available collection tools and collection processes for the purpose of sharing those resources with state agency accounts receivable professionals. The ARCC and its subcommittees include a diverse membership from large agencies, small agencies, semi-independent agencies, the Oregon Judicial Department, PCAs, DOR-OAA, as well as members from the Willamette University Institute for Modern Government. The work of the ARCC and its subcommittees are essential components to improving statewide debt collections and overall accounts receivable management practices through the collaboration, partnership and forward thinking of accounts receivable professionals.

Factors in Collecting Receivables Key factors of the collectability of a receivable are: the type of the receivable; the socio-economic status of the debtor; and the debtor’s ability and willingness to pay.

Types of Receivables State agency receivables include a diverse representation of legally enforceable claims for payment ranging from benefit overpayments to court ordered restitution (Table 1).

Fiscal Year 2016 Statewide Accounts Receivable Management Report

6

Table 1.

Types of State Agency Receivables

Administrative hearing orders Loans

Benefit overpayments (unemployment or public assistance)

Medical services

Contract or service level agreements Restitution

Court orders (civil or criminal judgment) Support orders (child or spousal)

Employee overpayments (current or former employee)

Taxes

Fees, fines and penalties Tuition

Licensing (application or renewal)

Generally, some types of receivables are easier to collect than others. For example, a licensing agency can suspend or revoke a license if the debt is not paid; therefore, the debtor is more likely to voluntarily pay.

Types of Debtors State agency debtors range across the socio-economic spectrum and can be either individuals, businesses or organizations depending on the type of the debt (Table 2). However, state agencies often do not get to choose their customers and cannot deny services based on ability to pay; therefore, a reactive approach to accounts receivable management is common. Table 2.

Type of State Agency Debtors

Corporations, partnerships, LLCs, etc. Medical care recipients

Employed individuals Not-for-profit organizations

Hospitalized individuals Out-of-state individuals

Incarcerated individuals Students

Individuals on state assistance Unemployed individuals

Individuals with limited income Unlicensed individuals or businesses

Licensed professionals Veterans

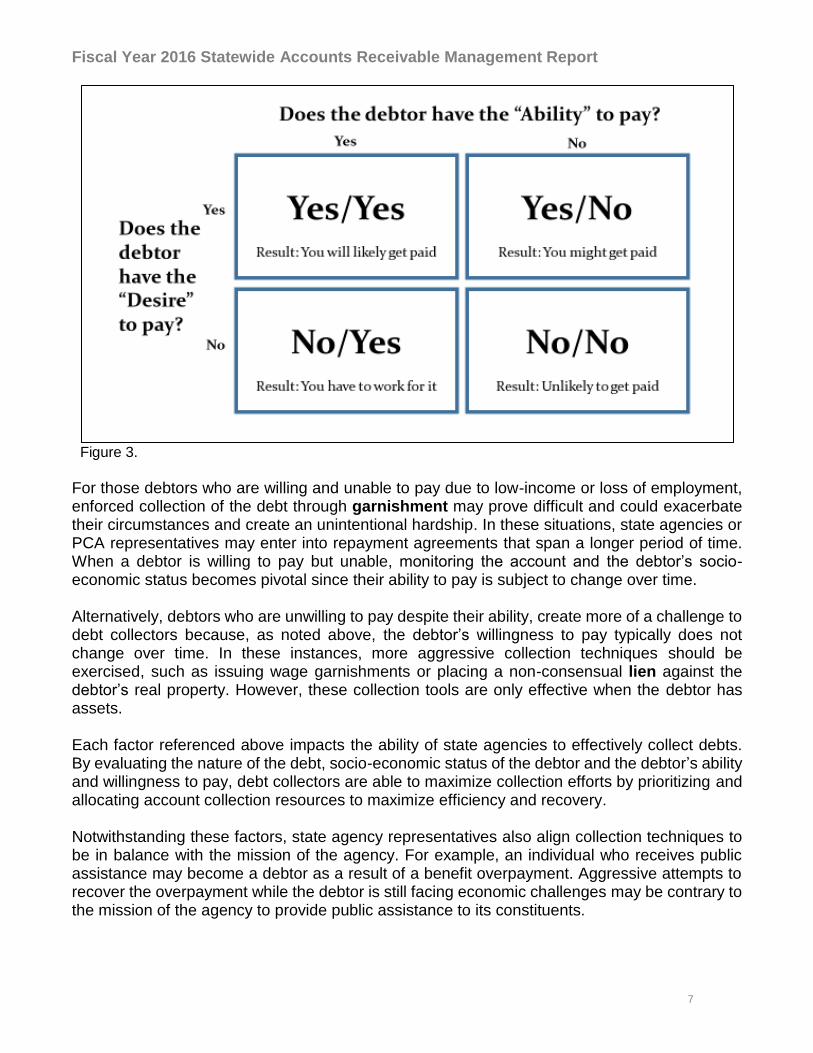

Collectability of a debt expands beyond type of debtor and includes evaluation of the debtor’s ability and willingness to pay. A common matrix used by PCAs assesses whether the debtor may be: able and willing to pay; able to pay but unwilling; unable to pay but willing; or unable and unwilling to pay (Fig. 3). Evaluating this probability of collection is valuable for determining the most cost effective and efficient method of pursuing the debt. It is important to understand that over time a debtor’s ability to pay is subject to change based on adjustments in their socio-economic status, while their willingness to pay typically does not change.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

7

Figure 3. For those debtors who are willing and unable to pay due to low-income or loss of employment, enforced collection of the debt through garnishment may prove difficult and could exacerbate their circumstances and create an unintentional hardship. In these situations, state agencies or PCA representatives may enter into repayment agreements that span a longer period of time. When a debtor is willing to pay but unable, monitoring the account and the debtor’s socio-economic status becomes pivotal since their ability to pay is subject to change over time. Alternatively, debtors who are unwilling to pay despite their ability, create more of a challenge to debt collectors because, as noted above, the debtor’s willingness to pay typically does not change over time. In these instances, more aggressive collection techniques should be exercised, such as issuing wage garnishments or placing a non-consensual lien against the debtor’s real property. However, these collection tools are only effective when the debtor has assets. Each factor referenced above impacts the ability of state agencies to effectively collect debts. By evaluating the nature of the debt, socio-economic status of the debtor and the debtor’s ability and willingness to pay, debt collectors are able to maximize collection efforts by prioritizing and allocating account collection resources to maximize efficiency and recovery. Notwithstanding these factors, state agency representatives also align collection techniques to be in balance with the mission of the agency. For example, an individual who receives public assistance may become a debtor as a result of a benefit overpayment. Aggressive attempts to recover the overpayment while the debtor is still facing economic challenges may be contrary to the mission of the agency to provide public assistance to its constituents.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

8

Collection Tools State agencies have several tools available for use in collecting debts (Table 3). Some tools are limited for use by agencies with unique statutory authority while other tools are available for use by all state agencies regardless of the nature of the receivable. Table 3.

Collection Tools

Collection letter, demand notice Non-consensual real property lien

DOR-OAA (full service collections) PCA (full service collections)

DOR-Refund Offset (restricted collections) Phone call

Garnishment Skip-tracing

Judgment Unclaimed property claim

State agencies are responsible for performing preliminary collection activities which include contacting the debtor by phone; sending collection letters or demand notices; and updating debtor contact information. When the debt becomes liquidated and delinquent, state agencies subject to statutory assignment provisions must assign the account to either DOR-OAA or a PCA. Once accounts are assigned to DOR-OAA or a PCA, full service collection activities commence. Full service collection activities include the preliminary collection activities referenced above, as well as: locating a debtor or debtor assets; recording real property liens; offsetting tax refunds; submitting a claim with the Department of State Lands against a debtor’s unclaimed property; issuing judgments; and issuing garnishments. State agencies with internal collection units perform full service collection activities prior to assigning a liquidated and delinquent account to DOR-OAA or a PCA. Many licensing and regulatory agencies, such as the Board of Accountancy and the Department of Environmental Quality, have statutory authority to issue civil penalties against individuals or businesses that operate without a license or violate a statutory or administrative regulation. These agencies have additional tools available to collect debts. More specifically, upon issuance of a final civil penalty order, the agency may record the order in a county lien register thus enabling the agency to issue garnishments or record a lien against real property owned by the debtor. The Department of Revenue, Oregon Employment Department, Department of Human Services, Oregon Health Authority, Department of Transportation and Department of Consumer and Business Services have distraint warrant authority which, similar to civil penalty authority, allows the agency to docket the warrant in a county lien register thus enabling the agency to issue garnishments or record a lien against real property owned by the debtor. Though a limited number of state agencies have distraint warrant authority, all liquidated and delinquent accounts assigned to DOR-OAA have the ability for a distraint warrant to be issued using DOR-OAA’s statutory authority. However, if DOR-OAA is unable to collect the liquidated and delinquent

Fiscal Year 2016 Statewide Accounts Receivable Management Report

9

account within the statutory or administrative timelines, the distraint warrant will be cancelled and the account will be returned to the originating agency for subsequent assignment to a PCA. Five state agencies have authority granted by the federal government to participate in the Treasury Offset Program (TOP), a program which intercepts federal tax refunds to offset delinquent tax debts, public assistance debts, and unemployment insurance debts. Access to the TOP program is limited for use by the Oregon Employment Department, Department of Human Services, Oregon Health Authority, Department of Justice and the Department of Revenue. Additionally, Oregon law allows the Department of Justice, the Department of Human Services and the Oregon Health Authority to intercept lottery proceeds awarded to debtors with outstanding monies owed to these state agencies. These two tools (TOP and lottery offset) were excluded from the above table since they are available to a limited number of state agencies per federal or state law.

Data Analysis

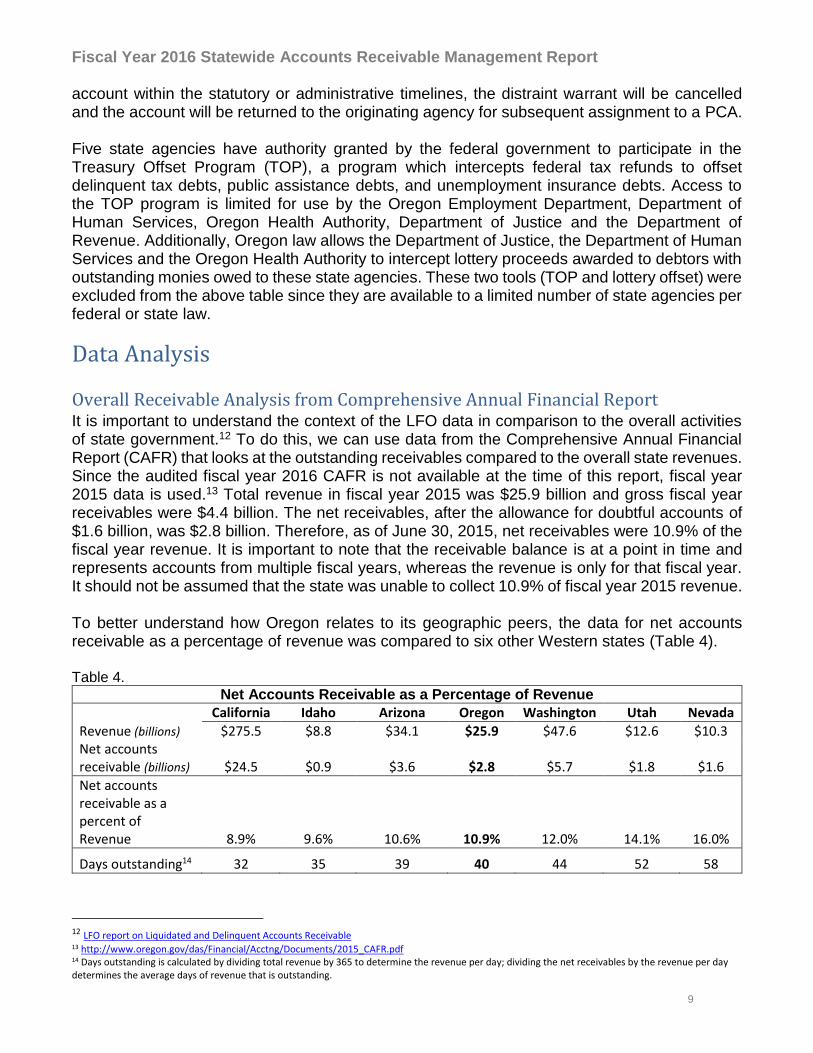

Overall Receivable Analysis from Comprehensive Annual Financial Report It is important to understand the context of the LFO data in comparison to the overall activities of state government.12 To do this, we can use data from the Comprehensive Annual Financial Report (CAFR) that looks at the outstanding receivables compared to the overall state revenues. Since the audited fiscal year 2016 CAFR is not available at the time of this report, fiscal year 2015 data is used.13 Total revenue in fiscal year 2015 was $25.9 billion and gross fiscal year receivables were $4.4 billion. The net receivables, after the allowance for doubtful accounts of $1.6 billion, was $2.8 billion. Therefore, as of June 30, 2015, net receivables were 10.9% of the fiscal year revenue. It is important to note that the receivable balance is at a point in time and represents accounts from multiple fiscal years, whereas the revenue is only for that fiscal year. It should not be assumed that the state was unable to collect 10.9% of fiscal year 2015 revenue. To better understand how Oregon relates to its geographic peers, the data for net accounts receivable as a percentage of revenue was compared to six other Western states (Table 4). Table 4.

Net Accounts Receivable as a Percentage of Revenue

California Idaho Arizona Oregon Washington Utah Nevada

Revenue (billions) $275.5 $8.8 $34.1 $25.9 $47.6 $12.6 $10.3 Net accounts receivable (billions) $24.5 $0.9 $3.6 $2.8 $5.7 $1.8 $1.6

Net accounts receivable as a percent of Revenue 8.9% 9.6% 10.6% 10.9% 12.0% 14.1% 16.0%

Days outstanding14 32 35 39 40 44 52 58

12 LFO report on Liquidated and Delinquent Accounts Receivable 13 http://www.oregon.gov/das/Financial/Acctng/Documents/2015_CAFR.pdf 14 Days outstanding is calculated by dividing total revenue by 365 to determine the revenue per day; dividing the net receivables by the revenue per day determines the average days of revenue that is outstanding.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

10

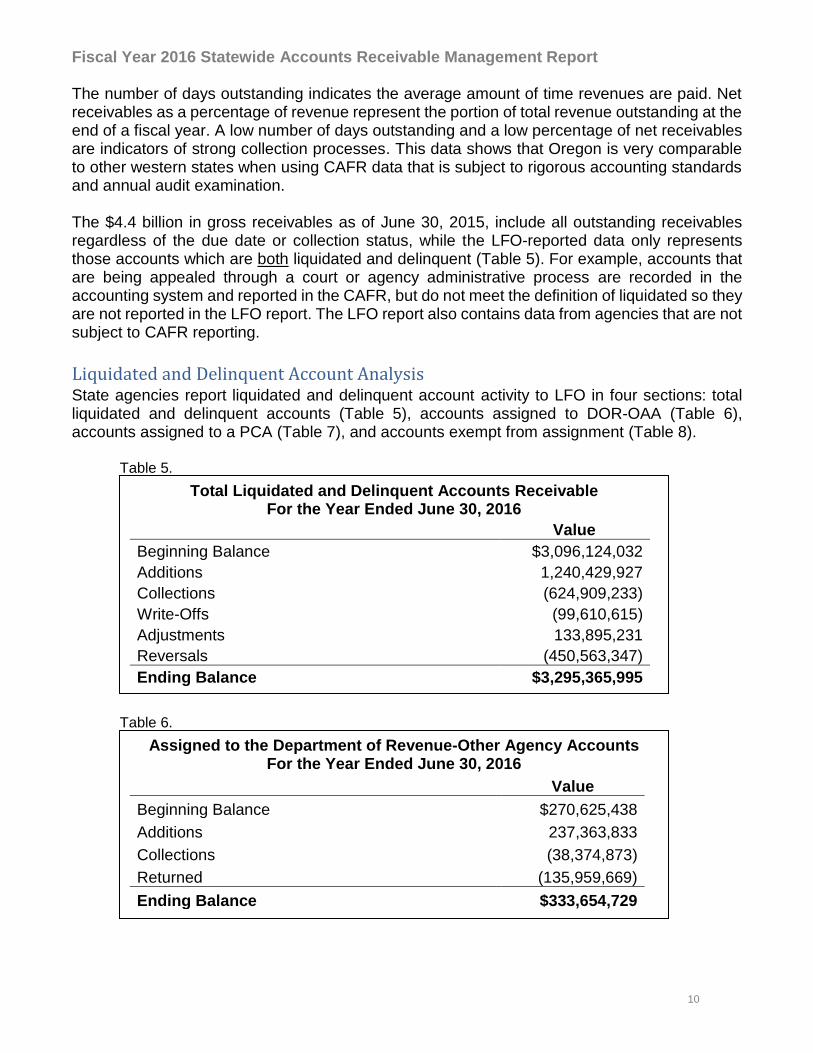

The number of days outstanding indicates the average amount of time revenues are paid. Net receivables as a percentage of revenue represent the portion of total revenue outstanding at the end of a fiscal year. A low number of days outstanding and a low percentage of net receivables are indicators of strong collection processes. This data shows that Oregon is very comparable to other western states when using CAFR data that is subject to rigorous accounting standards and annual audit examination. The $4.4 billion in gross receivables as of June 30, 2015, include all outstanding receivables regardless of the due date or collection status, while the LFO-reported data only represents those accounts which are both liquidated and delinquent (Table 5). For example, accounts that are being appealed through a court or agency administrative process are recorded in the accounting system and reported in the CAFR, but do not meet the definition of liquidated so they are not reported in the LFO report. The LFO report also contains data from agencies that are not subject to CAFR reporting.

Liquidated and Delinquent Account Analysis State agencies report liquidated and delinquent account activity to LFO in four sections: total liquidated and delinquent accounts (Table 5), accounts assigned to DOR-OAA (Table 6), accounts assigned to a PCA (Table 7), and accounts exempt from assignment (Table 8).

Table 5.

Table 6.

Total Liquidated and Delinquent Accounts Receivable For the Year Ended June 30, 2016

Value

Beginning Balance $3,096,124,032

Additions 1,240,429,927

Collections (624,909,233)

Write-Offs (99,610,615)

Adjustments 133,895,231

Reversals (450,563,347)

Ending Balance $3,295,365,995

Assigned to the Department of Revenue-Other Agency Accounts For the Year Ended June 30, 2016

Value

Beginning Balance $270,625,438

Additions 237,363,833

Collections (38,374,873)

Returned (135,959,669)

Ending Balance $333,654,729

Fiscal Year 2016 Statewide Accounts Receivable Management Report

11

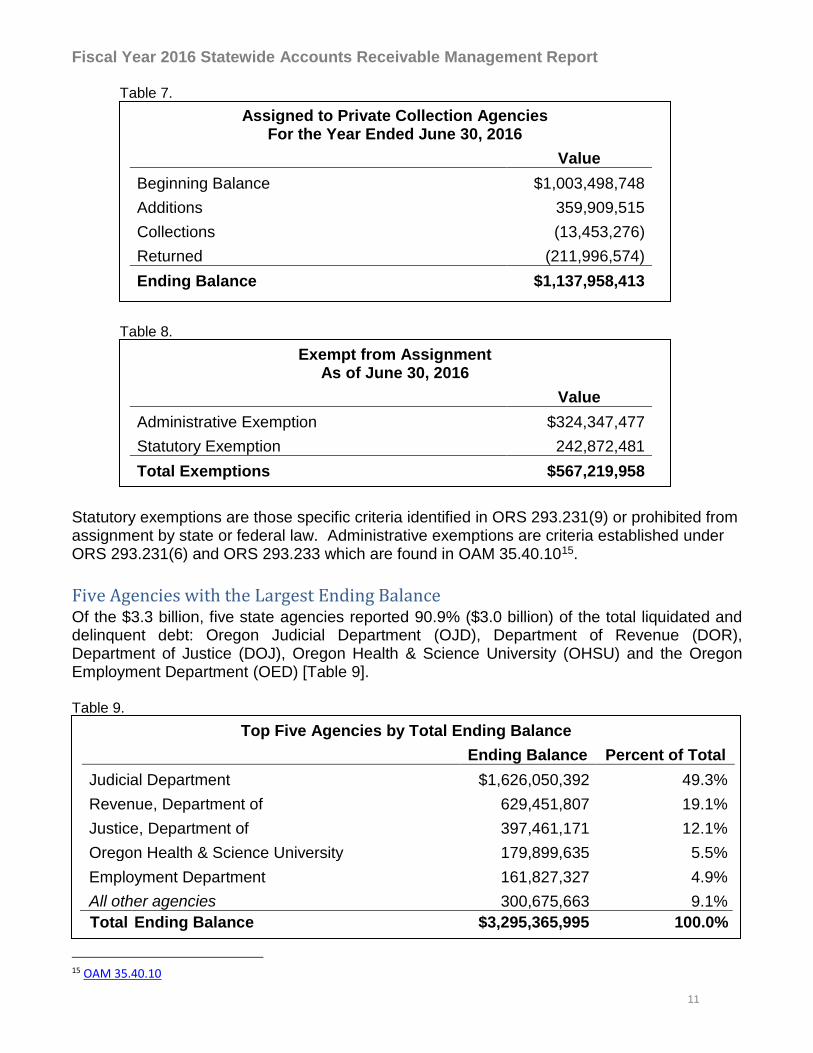

Table 7.

Table 8.

Statutory exemptions are those specific criteria identified in ORS 293.231(9) or prohibited from assignment by state or federal law. Administrative exemptions are criteria established under ORS 293.231(6) and ORS 293.233 which are found in OAM 35.40.1015.

Five Agencies with the Largest Ending Balance Of the $3.3 billion, five state agencies reported 90.9% ($3.0 billion) of the total liquidated and delinquent debt: Oregon Judicial Department (OJD), Department of Revenue (DOR), Department of Justice (DOJ), Oregon Health & Science University (OHSU) and the Oregon Employment Department (OED) [Table 9]. Table 9.

15 OAM 35.40.10

Assigned to Private Collection Agencies For the Year Ended June 30, 2016

Value

Beginning Balance $1,003,498,748

Additions 359,909,515

Collections (13,453,276)

Returned (211,996,574)

Ending Balance $1,137,958,413

Exempt from Assignment As of June 30, 2016

Value

Administrative Exemption $324,347,477

Statutory Exemption 242,872,481

Total Exemptions $567,219,958

Top Five Agencies by Total Ending Balance

Ending Balance Percent of Total

Judicial Department $1,626,050,392 49.3%

Revenue, Department of 629,451,807 19.1%

Justice, Department of 397,461,171 12.1%

Oregon Health & Science University 179,899,635 5.5%

Employment Department 161,827,327 4.9%

All other agencies 300,675,663 9.1%

Total Ending Balance $3,295,365,995 100.0%

Fiscal Year 2016 Statewide Accounts Receivable Management Report

12

Oregon Judicial Department – 49.3% of total debt Debt balances reported by OJD primarily include fines, fees, assessments, restitution and recovery of court-appointed counsel amounts ordered by the court as part of a judgment. Amounts due are sanctions imposed pursuant to law as determined by the 36 trial courts, the Tax Court, the Court of Appeals, and the Oregon Supreme Court. Ability to pay is not a primary consideration. Liquidated and delinquent amounts are due from individuals who are unable to pay in full at the time of final judgment. Debtors may be incarcerated, homeless or unemployed. Collection activities for amounts ordered in criminal cases can continue for up to 50 years after entry of the judgment. Recipients of amounts collected are primarily state and local governments and crime victims. Department of Revenue – 19.1% of total debt Debt balances reported by DOR include taxes, fees, penalties and interest owed to the state by individuals and businesses. The debts are primarily payable to the General Fund. The majority of the debt balances reported by DOR are related to personal income tax. Accounts collected by DOR-OAA are not included in this amount as they are reported by the agency that assigned the account. Department of Justice – 12.1% of total debt Debt balances reported by DOJ are comprised primarily of child support recoveries which are passed to the custodial parent when collected, punitive damages awarded to the Crime Victims Services Division and court judgments from the Financial Fraud, Consumer Protection and Charities programs. The debts are primarily payable to Federal Funds, Other Funds and Other Funds-Pass Through. Oregon Health & Science University – 5.5% of total debt Debt balances reported as Other Funds by OHSU are primarily associated with the patient’s portion of billable costs resulting from medical care provided. Medical care includes hospital inpatient, outpatient, and physician services. Oregon Employment Department – 4.9% of total debt Debt balances reported by OED include unemployment insurance (UI) employer-paid taxes and benefit overpayments. UI benefit overpayments result from administrative decisions that a claimant was not eligible to receive benefits. UI benefit overpayments arise from claimant error, non-claimant error or fraud. Both types of UI debts include amounts that have accumulated over many years and may have been subject to additional penalties and interest. The debts are payable to the Other Funds.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

13

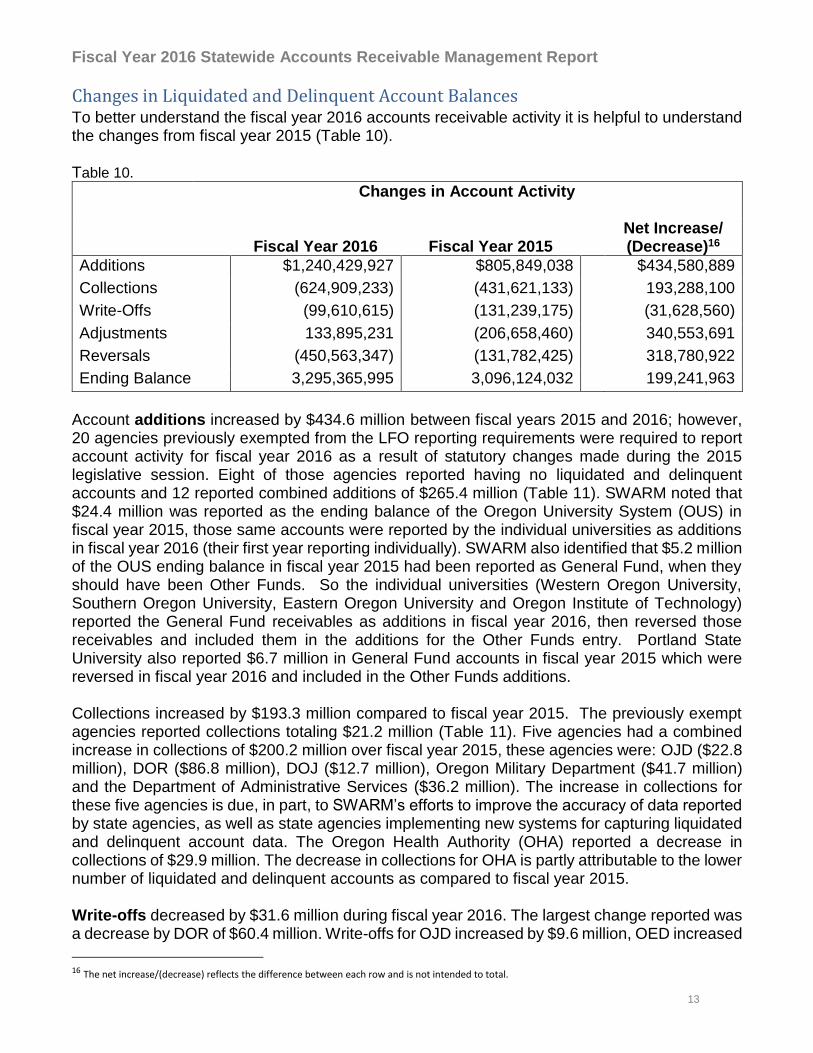

Changes in Liquidated and Delinquent Account Balances To better understand the fiscal year 2016 accounts receivable activity it is helpful to understand the changes from fiscal year 2015 (Table 10). Table 10.

Changes in Account Activity

Fiscal Year 2016

Fiscal Year 2015

Net Increase/ (Decrease)16

Additions $1,240,429,927 $805,849,038 $434,580,889

Collections (624,909,233) (431,621,133) 193,288,100

Write-Offs (99,610,615) (131,239,175) (31,628,560)

Adjustments 133,895,231 (206,658,460) 340,553,691

Reversals (450,563,347) (131,782,425) 318,780,922

Ending Balance 3,295,365,995 3,096,124,032 199,241,963

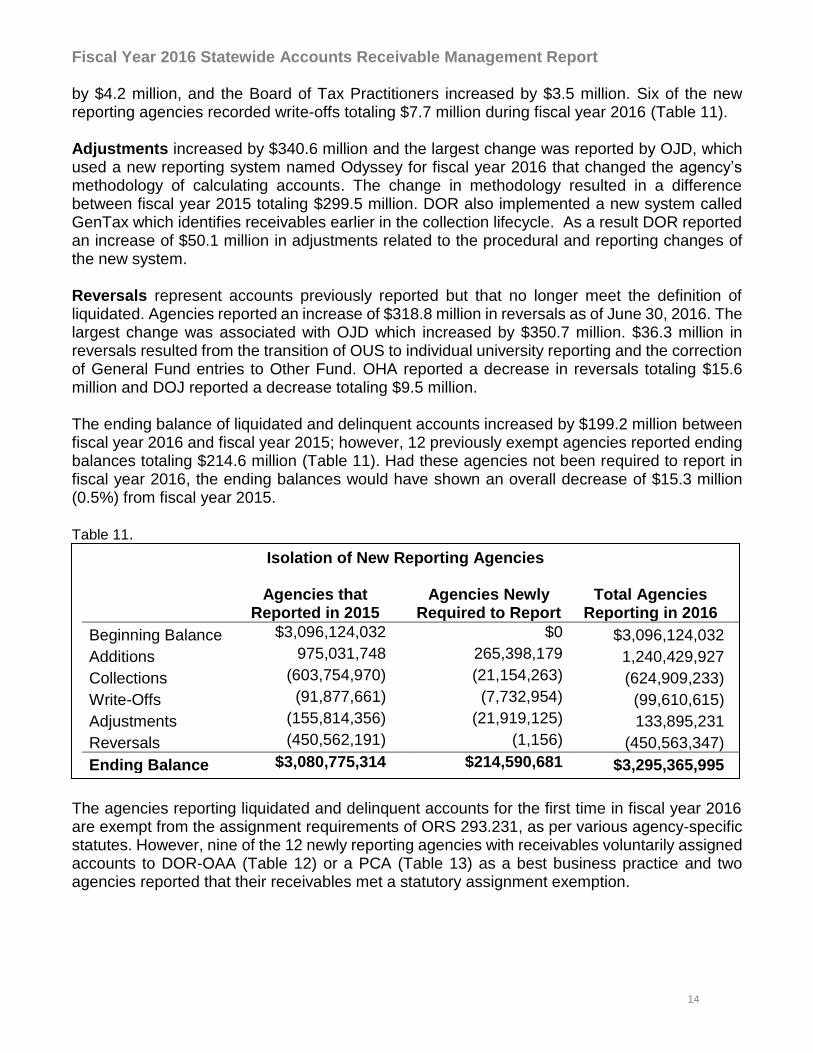

Account additions increased by $434.6 million between fiscal years 2015 and 2016; however, 20 agencies previously exempted from the LFO reporting requirements were required to report account activity for fiscal year 2016 as a result of statutory changes made during the 2015 legislative session. Eight of those agencies reported having no liquidated and delinquent accounts and 12 reported combined additions of $265.4 million (Table 11). SWARM noted that $24.4 million was reported as the ending balance of the Oregon University System (OUS) in fiscal year 2015, those same accounts were reported by the individual universities as additions in fiscal year 2016 (their first year reporting individually). SWARM also identified that $5.2 million of the OUS ending balance in fiscal year 2015 had been reported as General Fund, when they should have been Other Funds. So the individual universities (Western Oregon University, Southern Oregon University, Eastern Oregon University and Oregon Institute of Technology) reported the General Fund receivables as additions in fiscal year 2016, then reversed those receivables and included them in the additions for the Other Funds entry. Portland State University also reported $6.7 million in General Fund accounts in fiscal year 2015 which were reversed in fiscal year 2016 and included in the Other Funds additions. Collections increased by $193.3 million compared to fiscal year 2015. The previously exempt agencies reported collections totaling $21.2 million (Table 11). Five agencies had a combined increase in collections of $200.2 million over fiscal year 2015, these agencies were: OJD ($22.8 million), DOR ($86.8 million), DOJ ($12.7 million), Oregon Military Department ($41.7 million) and the Department of Administrative Services ($36.2 million). The increase in collections for these five agencies is due, in part, to SWARM’s efforts to improve the accuracy of data reported by state agencies, as well as state agencies implementing new systems for capturing liquidated and delinquent account data. The Oregon Health Authority (OHA) reported a decrease in collections of $29.9 million. The decrease in collections for OHA is partly attributable to the lower number of liquidated and delinquent accounts as compared to fiscal year 2015. Write-offs decreased by $31.6 million during fiscal year 2016. The largest change reported was a decrease by DOR of $60.4 million. Write-offs for OJD increased by $9.6 million, OED increased

16 The net increase/(decrease) reflects the difference between each row and is not intended to total.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

14

by $4.2 million, and the Board of Tax Practitioners increased by $3.5 million. Six of the new reporting agencies recorded write-offs totaling $7.7 million during fiscal year 2016 (Table 11). Adjustments increased by $340.6 million and the largest change was reported by OJD, which used a new reporting system named Odyssey for fiscal year 2016 that changed the agency’s methodology of calculating accounts. The change in methodology resulted in a difference between fiscal year 2015 totaling $299.5 million. DOR also implemented a new system called GenTax which identifies receivables earlier in the collection lifecycle. As a result DOR reported an increase of $50.1 million in adjustments related to the procedural and reporting changes of the new system. Reversals represent accounts previously reported but that no longer meet the definition of liquidated. Agencies reported an increase of $318.8 million in reversals as of June 30, 2016. The largest change was associated with OJD which increased by $350.7 million. $36.3 million in reversals resulted from the transition of OUS to individual university reporting and the correction of General Fund entries to Other Fund. OHA reported a decrease in reversals totaling $15.6 million and DOJ reported a decrease totaling $9.5 million. The ending balance of liquidated and delinquent accounts increased by $199.2 million between fiscal year 2016 and fiscal year 2015; however, 12 previously exempt agencies reported ending balances totaling $214.6 million (Table 11). Had these agencies not been required to report in fiscal year 2016, the ending balances would have shown an overall decrease of $15.3 million (0.5%) from fiscal year 2015. Table 11.

The agencies reporting liquidated and delinquent accounts for the first time in fiscal year 2016 are exempt from the assignment requirements of ORS 293.231, as per various agency-specific statutes. However, nine of the 12 newly reporting agencies with receivables voluntarily assigned accounts to DOR-OAA (Table 12) or a PCA (Table 13) as a best business practice and two agencies reported that their receivables met a statutory assignment exemption.

Isolation of New Reporting Agencies

Agencies that

Reported in 2015

Agencies Newly

Required to Report Total Agencies

Reporting in 2016

Beginning Balance $3,096,124,032 $0 $3,096,124,032

Additions 975,031,748 265,398,179 1,240,429,927

Collections (603,754,970) (21,154,263) (624,909,233)

Write-Offs (91,877,661) (7,732,954) (99,610,615)

Adjustments (155,814,356) (21,919,125) 133,895,231

Reversals (450,562,191) (1,156) (450,563,347)

Ending Balance $3,080,775,314 $214,590,681 $3,295,365,995

Fiscal Year 2016 Statewide Accounts Receivable Management Report

15

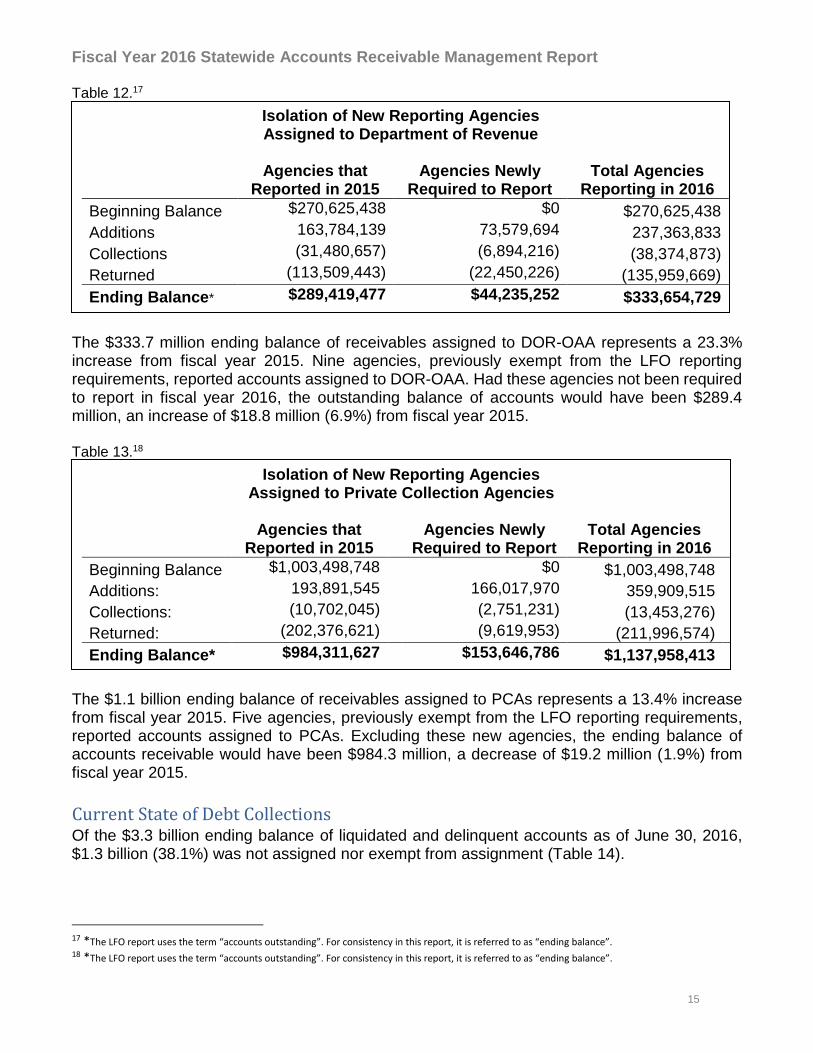

Table 12.17

The $333.7 million ending balance of receivables assigned to DOR-OAA represents a 23.3% increase from fiscal year 2015. Nine agencies, previously exempt from the LFO reporting requirements, reported accounts assigned to DOR-OAA. Had these agencies not been required to report in fiscal year 2016, the outstanding balance of accounts would have been $289.4 million, an increase of $18.8 million (6.9%) from fiscal year 2015. Table 13.18

The $1.1 billion ending balance of receivables assigned to PCAs represents a 13.4% increase from fiscal year 2015. Five agencies, previously exempt from the LFO reporting requirements, reported accounts assigned to PCAs. Excluding these new agencies, the ending balance of accounts receivable would have been $984.3 million, a decrease of $19.2 million (1.9%) from fiscal year 2015.

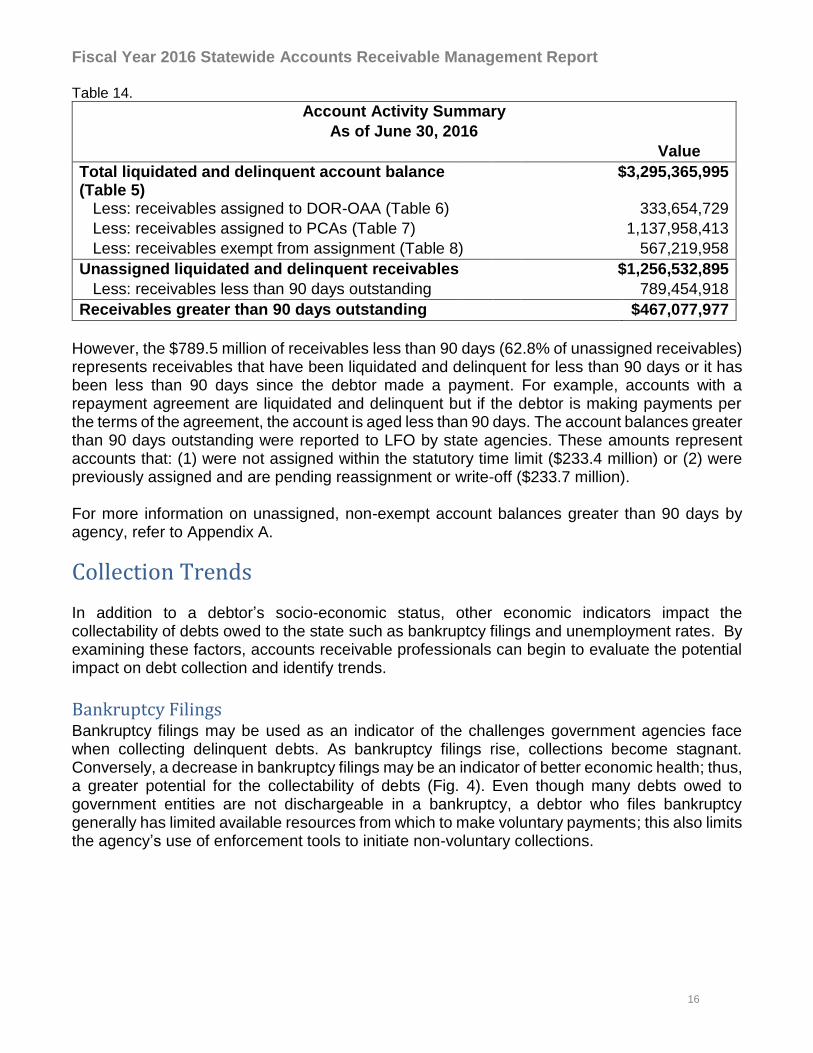

Current State of Debt Collections Of the $3.3 billion ending balance of liquidated and delinquent accounts as of June 30, 2016, $1.3 billion (38.1%) was not assigned nor exempt from assignment (Table 14).

17 *The LFO report uses the term “accounts outstanding”. For consistency in this report, it is referred to as “ending balance”. 18 *The LFO report uses the term “accounts outstanding”. For consistency in this report, it is referred to as “ending balance”.

Isolation of New Reporting Agencies Assigned to Department of Revenue

Agencies that Reported in 2015

Agencies Newly Required to Report

Total Agencies Reporting in 2016

Beginning Balance $270,625,438 $0 $270,625,438

Additions 163,784,139 73,579,694 237,363,833

Collections (31,480,657) (6,894,216) (38,374,873)

Returned (113,509,443) (22,450,226) (135,959,669)

Ending Balance* $289,419,477 $44,235,252 $333,654,729

Isolation of New Reporting Agencies Assigned to Private Collection Agencies

Agencies that Reported in 2015

Agencies Newly Required to Report

Total Agencies Reporting in 2016

Beginning Balance $1,003,498,748 $0 $1,003,498,748

Additions: 193,891,545 166,017,970 359,909,515

Collections: (10,702,045) (2,751,231) (13,453,276)

Returned: (202,376,621) (9,619,953) (211,996,574)

Ending Balance* $984,311,627 $153,646,786 $1,137,958,413

Fiscal Year 2016 Statewide Accounts Receivable Management Report

16

Table 14.

Account Activity Summary

As of June 30, 2016 Value

Total liquidated and delinquent account balance (Table 5)

$3,295,365,995

Less: receivables assigned to DOR-OAA (Table 6)

333,654,729

Less: receivables assigned to PCAs (Table 7)

1,137,958,413

Less: receivables exempt from assignment (Table 8)

567,219,958

Unassigned liquidated and delinquent receivables

$1,256,532,895

Less: receivables less than 90 days outstanding 789,454,918

Receivables greater than 90 days outstanding $467,077,977

However, the $789.5 million of receivables less than 90 days (62.8% of unassigned receivables) represents receivables that have been liquidated and delinquent for less than 90 days or it has been less than 90 days since the debtor made a payment. For example, accounts with a repayment agreement are liquidated and delinquent but if the debtor is making payments per the terms of the agreement, the account is aged less than 90 days. The account balances greater than 90 days outstanding were reported to LFO by state agencies. These amounts represent accounts that: (1) were not assigned within the statutory time limit ($233.4 million) or (2) were previously assigned and are pending reassignment or write-off ($233.7 million). For more information on unassigned, non-exempt account balances greater than 90 days by agency, refer to Appendix A.

Collection Trends In addition to a debtor’s socio-economic status, other economic indicators impact the collectability of debts owed to the state such as bankruptcy filings and unemployment rates. By examining these factors, accounts receivable professionals can begin to evaluate the potential impact on debt collection and identify trends.

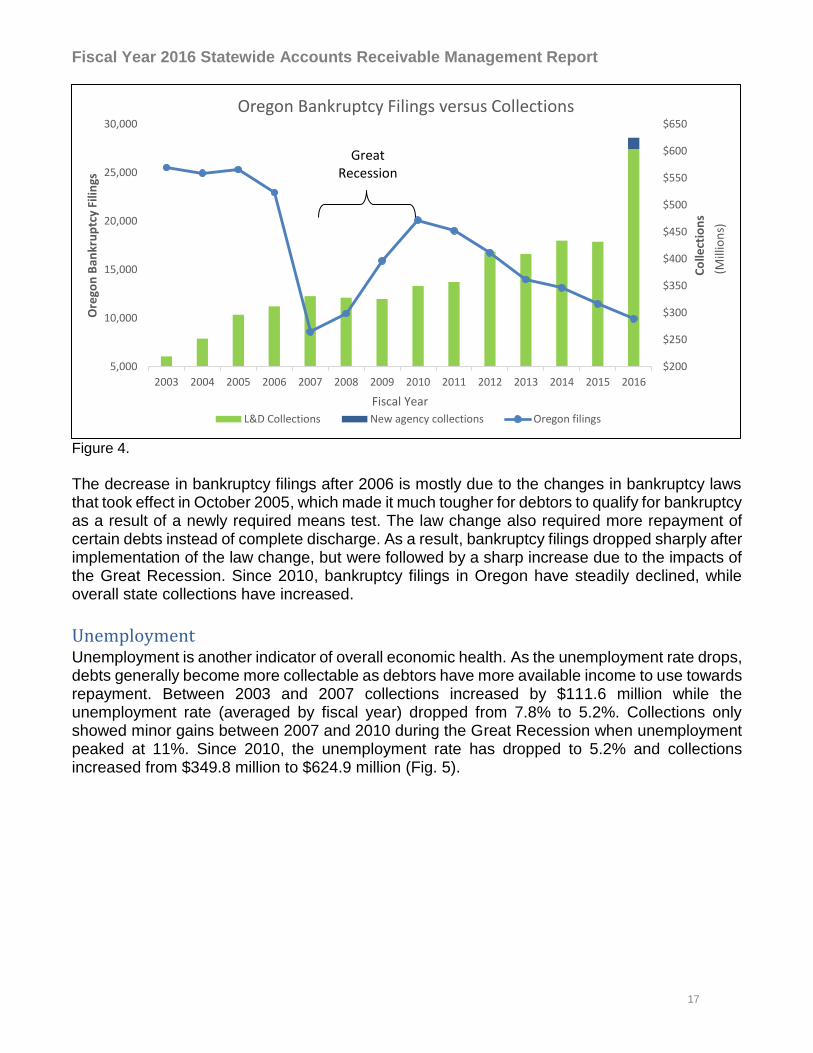

Bankruptcy Filings Bankruptcy filings may be used as an indicator of the challenges government agencies face when collecting delinquent debts. As bankruptcy filings rise, collections become stagnant. Conversely, a decrease in bankruptcy filings may be an indicator of better economic health; thus, a greater potential for the collectability of debts (Fig. 4). Even though many debts owed to government entities are not dischargeable in a bankruptcy, a debtor who files bankruptcy generally has limited available resources from which to make voluntary payments; this also limits the agency’s use of enforcement tools to initiate non-voluntary collections.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

17

Figure 4.

The decrease in bankruptcy filings after 2006 is mostly due to the changes in bankruptcy laws that took effect in October 2005, which made it much tougher for debtors to qualify for bankruptcy as a result of a newly required means test. The law change also required more repayment of certain debts instead of complete discharge. As a result, bankruptcy filings dropped sharply after implementation of the law change, but were followed by a sharp increase due to the impacts of the Great Recession. Since 2010, bankruptcy filings in Oregon have steadily declined, while overall state collections have increased.

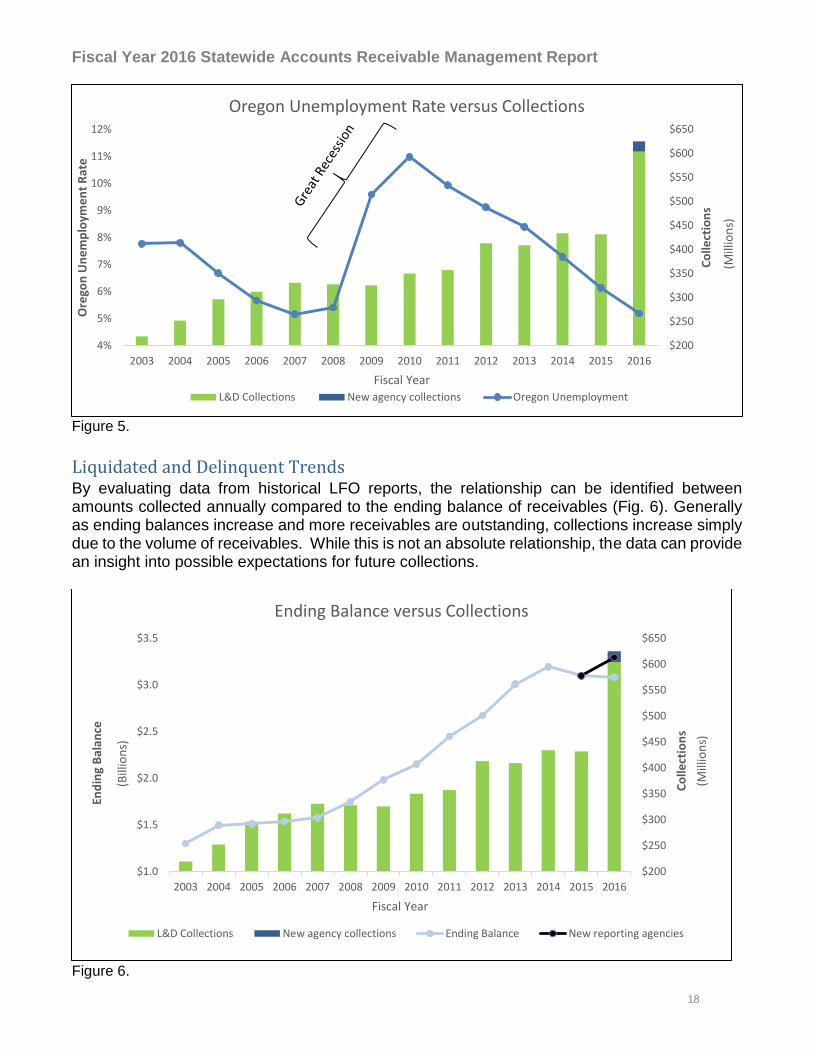

Unemployment Unemployment is another indicator of overall economic health. As the unemployment rate drops, debts generally become more collectable as debtors have more available income to use towards repayment. Between 2003 and 2007 collections increased by $111.6 million while the unemployment rate (averaged by fiscal year) dropped from 7.8% to 5.2%. Collections only showed minor gains between 2007 and 2010 during the Great Recession when unemployment peaked at 11%. Since 2010, the unemployment rate has dropped to 5.2% and collections increased from $349.8 million to $624.9 million (Fig. 5).

5,000

10,000

15,000

20,000

25,000

30,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

Ore

gon

Ban

kru

ptc

y Fi

lings

Fiscal Year

Co

llect

ion

s

(Mill

ion

s)

Oregon Bankruptcy Filings versus Collections

L&D Collections New agency collections Oregon filings

Great Recession

Fiscal Year 2016 Statewide Accounts Receivable Management Report

18

Figure 5.

Liquidated and Delinquent Trends By evaluating data from historical LFO reports, the relationship can be identified between amounts collected annually compared to the ending balance of receivables (Fig. 6). Generally as ending balances increase and more receivables are outstanding, collections increase simply due to the volume of receivables. While this is not an absolute relationship, the data can provide an insight into possible expectations for future collections.

Figure 6.

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

4%

5%

6%

7%

8%

9%

10%

11%

12%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Co

llect

ion

s

(Mill

ion

s)

Ore

gon

Un

em

plo

yme

nt

Rat

e

Fiscal Year

Oregon Unemployment Rate versus Collections

L&D Collections New agency collections Oregon Unemployment

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

Co

llect

ion

s

(Mill

ion

s)

Fiscal Year

End

ing

Bal

ance

(Bill

ion

s)

Ending Balance versus Collections

L&D Collections New agency collections Ending Balance New reporting agencies

Fiscal Year 2016 Statewide Accounts Receivable Management Report

19

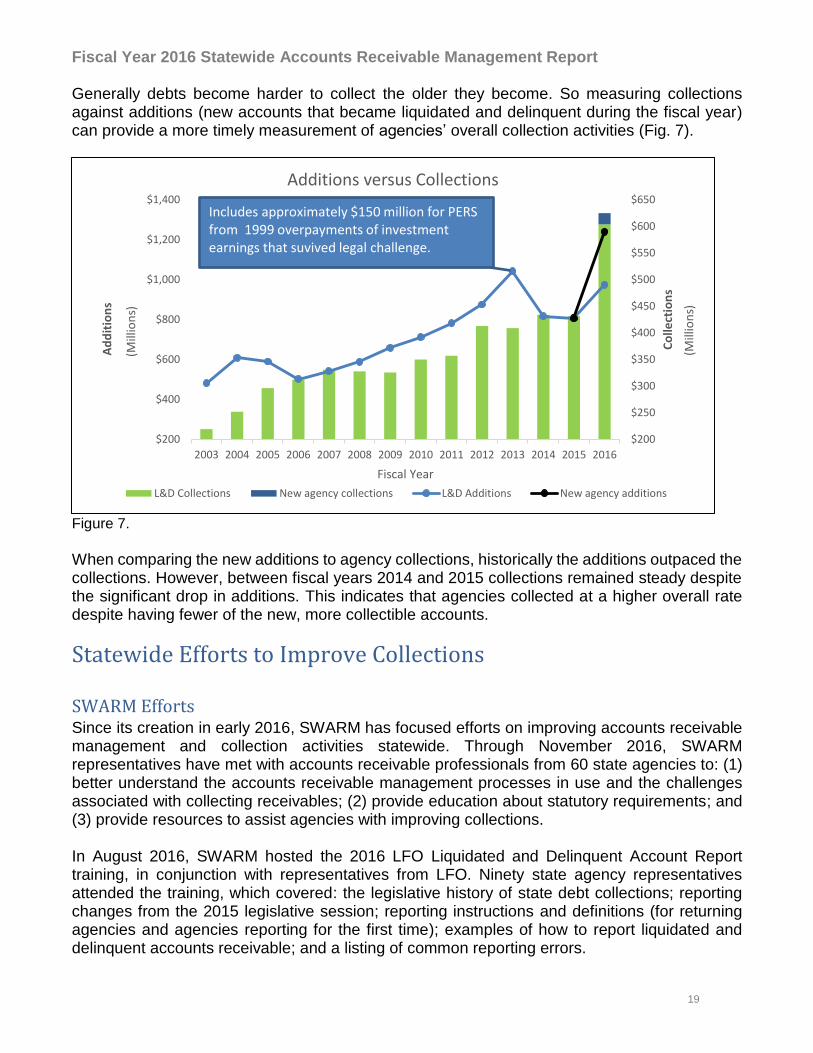

Generally debts become harder to collect the older they become. So measuring collections against additions (new accounts that became liquidated and delinquent during the fiscal year) can provide a more timely measurement of agencies’ overall collection activities (Fig. 7).

Figure 7.

When comparing the new additions to agency collections, historically the additions outpaced the collections. However, between fiscal years 2014 and 2015 collections remained steady despite the significant drop in additions. This indicates that agencies collected at a higher overall rate despite having fewer of the new, more collectible accounts.

Statewide Efforts to Improve Collections

SWARM Efforts Since its creation in early 2016, SWARM has focused efforts on improving accounts receivable management and collection activities statewide. Through November 2016, SWARM representatives have met with accounts receivable professionals from 60 state agencies to: (1) better understand the accounts receivable management processes in use and the challenges associated with collecting receivables; (2) provide education about statutory requirements; and (3) provide resources to assist agencies with improving collections. In August 2016, SWARM hosted the 2016 LFO Liquidated and Delinquent Account Report training, in conjunction with representatives from LFO. Ninety state agency representatives attended the training, which covered: the legislative history of state debt collections; reporting changes from the 2015 legislative session; reporting instructions and definitions (for returning agencies and agencies reporting for the first time); examples of how to report liquidated and delinquent accounts receivable; and a listing of common reporting errors.

$200

$400

$600

$800

$1,000

$1,200

$1,400

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

Ad

dit

ion

s

(Mill

ion

s)

Fiscal Year

Co

llect

ion

s

(Mill

ion

s)

Additions versus Collections

L&D Collections New agency collections L&D Additions New agency additions

Includes approximately $150 million for PERS from 1999 overpayments of investment earnings that suvived legal challenge.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

20

SWARM also leads the monthly ARCC meeting and the ARCC subcommittee meetings. Through November 2016 these meetings have resulted in:

Development of data elements for tracking performance metrics

Review and modification of five existing OAM policies and development of one new policy regarding offers of compromise and settlement

Identification of common tools used by agencies

Development of the accounts receivable centric website which provides up to date information regarding upcoming meetings, trainings and resources for state agency collection professionals

Committees continue to focus on:

Developing state policies for agency performance tracking and reporting regarding accounts receivable management

Reviewing and updating existing statewide accounts receivable management policies

Developing a toolkit for agencies to use that includes a matrix of available tools based on the type of debt

Developing a quarterly accounts receivable newsletter to communicate best practices for improving state debt collections

In collaboration with the Attorney General, SWARM has established a policy that includes criteria for agencies to use when determining if an account should be considered for compromise or settlement and the associated procedures for the approval and documentation of the account. SWARM will conduct training for agencies in 2017 on the compromise policy and its use in collections.

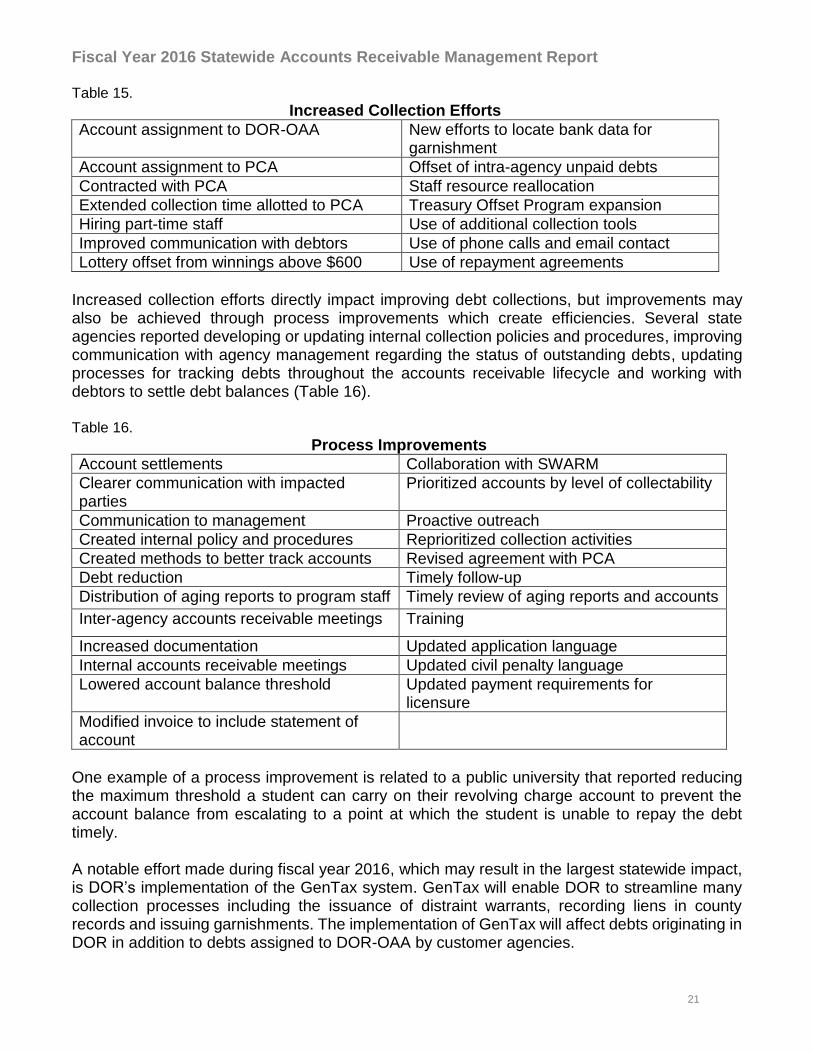

Agency Efforts During fiscal year 2016, state agencies demonstrated efforts to improve the state of debt collection through a combination of increased collection efforts and improvements to accounts receivable management. State agencies have attended training events hosted by private collection firms as well as regular inter-agency meetings hosted by SWARM. Both training events and inter-agency meetings included focused discussions about state collection requirements, annual reporting requirements and best practices. Through training events, inter-agency meetings and outreach, accounts receivable professionals have become more aware of statutory requirements, as well as resources available to improve existing collection processes and efforts. Highlights of state agencies’ increased collection efforts during the fiscal year include reallocation of existing staff resources, increasing communication with debtors, and increasing the number of accounts assigned to DOR-OAA or a PCA (Table 15).

Fiscal Year 2016 Statewide Accounts Receivable Management Report

21

Table 15.

Increased Collection Efforts

Account assignment to DOR-OAA New efforts to locate bank data for garnishment

Account assignment to PCA Offset of intra-agency unpaid debts

Contracted with PCA Staff resource reallocation

Extended collection time allotted to PCA Treasury Offset Program expansion

Hiring part-time staff Use of additional collection tools

Improved communication with debtors Use of phone calls and email contact

Lottery offset from winnings above $600 Use of repayment agreements

Increased collection efforts directly impact improving debt collections, but improvements may also be achieved through process improvements which create efficiencies. Several state agencies reported developing or updating internal collection policies and procedures, improving communication with agency management regarding the status of outstanding debts, updating processes for tracking debts throughout the accounts receivable lifecycle and working with debtors to settle debt balances (Table 16). Table 16.

Process Improvements

Account settlements Collaboration with SWARM

Clearer communication with impacted parties

Prioritized accounts by level of collectability

Communication to management Proactive outreach

Created internal policy and procedures Reprioritized collection activities

Created methods to better track accounts Revised agreement with PCA

Debt reduction Timely follow-up

Distribution of aging reports to program staff Timely review of aging reports and accounts

Inter-agency accounts receivable meetings Training

Increased documentation Updated application language

Internal accounts receivable meetings Updated civil penalty language

Lowered account balance threshold Updated payment requirements for licensure

Modified invoice to include statement of account

One example of a process improvement is related to a public university that reported reducing the maximum threshold a student can carry on their revolving charge account to prevent the account balance from escalating to a point at which the student is unable to repay the debt timely. A notable effort made during fiscal year 2016, which may result in the largest statewide impact, is DOR’s implementation of the GenTax system. GenTax will enable DOR to streamline many collection processes including the issuance of distraint warrants, recording liens in county records and issuing garnishments. The implementation of GenTax will affect debts originating in DOR in addition to debts assigned to DOR-OAA by customer agencies.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

22

Collection Issues and Challenges State agencies face several challenges impacting collection processes. In an effort to better understand these challenges, and to identify solutions for overcoming these challenges, one must analyze the type of challenges that exist: data availability, systems, standardization, resources, Social Security Number collection and use.

Data Availability Data availability is an integral component to achieving successful collections of liquidated and delinquent debt. Accurate, complete, and current data increases the collectability of any debt; however, the availability of the desired data varies depending upon the nature of the debt and the debtor. In the case of issuing a civil penalty to an individual for unlicensed practice, the individual may be operating under an alias or false identity; this impacts the ability of the agency to successfully collect the debt.

State agencies that provide goods or services are encouraged to obtain as much customer data as possible prior to providing the goods or services in the event the account becomes liquidated and delinquent. Since the process associated with obtaining additional data may create added resource burdens, state agencies must evaluate the cost associated with collecting more data on the front end compared to the likelihood of collection activity. State agencies that accept checks as a form of payment also accept the risk that the check may be returned for non-sufficient funds. In these cases, the state agency may only have data available from the face of the check; which could be stolen, fraudulent or outdated.

Systems Systems, much like data, are an integral component to enable state agencies to successfully collect liquidated and delinquent debt through the efficient and effective tracking of debts. Feedback from state agencies indicated that over 70% of state agencies use a Microsoft Excel spreadsheet to track and report accounts receivable while the remaining agencies use legacy or mainframe applications or third party software applications. Due to the complex nature of collection activities, transitions between liquidated and non-liquidated status, and assignment status, an Excel spreadsheet is not an ideal solution for effectively and efficiently managing accounts receivable transactions. In addition, given that spreadsheets are manual in nature, the risk of data error increases. Accounts receivable management applications, whether internally developed or purchased off-the-shelf, are recommended.

Some state agencies with diverse business units have unique systems available to track business activities for programmatic reporting. Meetings with these state agencies have shown that systems are often developed for the program purposes and a billing module is an ancillary function, and are not designed with the capability to effectively track the life of the receivable.

Standardization Standardizing processes is a challenge that some state agencies face when collecting liquidated and delinquent debt. Though agencies have the authority to establish internal processes to ensure compliance with applicable federal and state requirements, the diverse nature of business units limit the ability to create standardized processes within the agency. Diverse business units result in diverse types of debt with varying levels of requirements resulting in

Fiscal Year 2016 Statewide Accounts Receivable Management Report

23

unique processes for each business unit or type of debt. This challenge makes it difficult for state agencies to efficiently standardize collection processes; an important factor when limited resources are available to conduct effective and efficient collection activities. Even though state agencies may have similar regulatory functions and authorities such as civil penalties, numerous issues within each agency may result in varying methods of implementing those same authorities.

Resources Resource challenges affecting state agencies include not only the number of staff available to perform collection duties but also the training and expertise of the available staff. Often, collection work in state agencies is completed by accountants responsible for accounts receivable billing. Though this may seem like a natural fit, collection work and accounting work are different functions and require different skillsets. In addition, the primary purpose of an accounts receivable accountant is to bill for goods or services provided and to record the applicable accounting entries in the general ledger. A debt collector requires a specific set of skills that include: research methods to locate debtors and collectible assets; negotiation methods; and enforcement processes, such as garnishment and lien recording. The skills required for debt collection are not commonly listed in job requirements for accounting positions. Feedback received from many state agencies indicates the priority is to bill for goods or services provided while collection activities are often conducted as time allows and as staff are available. When an agency determines the percentage of accounts that become liquidated and delinquent are immaterial compared to the percentage of accounts that are paid timely, it is not surprising that agencies prioritize the work accordingly. Not only are resource challenges the result of limited staff, but so is staff expertise. Collection activities contain many complexities which make it difficult to effectively perform when only a portion of an employee’s position is allocated to infrequently performing such tasks.

Collection staff need to be well versed in applicable federal and state regulations to ensure due process is available to the debtor and that the appropriate notifications are made prior to escalating collection efforts. The debtor must be notified of potential consequences for failing to pay, such as: penalties, interest, garnishment, assignment of the account to DOR-OAA or a PCA, and the affiliated collection costs. Due process also provides many opportunities for the debtor to dispute or appeal the debt. Failure to provide proper notification to the debtor could result in the agency being legally liable for damages or penalties.

Social Security Number Collection and Use In 2015, ORS 293.22619 provided that agencies may request an individual’s social security number (SSN) on documents relating to any monetary obligation and provide notice that the SSN may be used for debt collection purposes. Availability of the SSN is an important step to increasing the collectability of an accounts receivable. The availability of the SSN is also critical to collection tools such as offset of state payments. Using the SSN for purposes of offset ensures that only payments made by specific debtors will be withheld and minimizes errors in the data matching process. There are certain determinations that must occur prior to the implementation of an offset program. Most notably, whether the individual has been notified that their SSN will be used for debt collection purposes, in accordance with Oregon and federal law

19 https://www.oregonlegislature.gov/bills_laws/ors/ors293.html

Fiscal Year 2016 Statewide Accounts Receivable Management Report

24

(Privacy Act of 1974); whether all or a portion of the payment should be subject to the offset; and the establishment of a control structure in a decentralized environment to ensure secure and accurate information and balances. SWARM will continue its efforts to help make these determinations in 2017, in conjunction with DOJ and agency partners.

Future of State Debt Collections In July 2010, the National Association of State Auditors, Comptrollers and Treasurers (NASACT) and CGI, a leading information technology and business process services firm, conducted a survey20 of states to identify the strategies, practices, and collection enforcement processes states are using to enhance debt collection capabilities. Generally, agencies follow a similar collection process at the highest level. The process begins with notices, which then may proceed to some additional action such as phone calls and some level of involuntary collection actions (i.e. offsets). In addition, all states reported that they utilize PCAs at some point in the process. State agencies in Oregon could benefit from a centralized model of debt collection. A recent survey indicated that over 75% of agencies have only one person (or portion of a full time equivalent) dedicated to collection of delinquent debts. The limited resources make it difficult to ensure proper collection steps are followed consistently. Over 75% of agencies also use Excel or Access to track delinquent accounts receivable; 13% use a legacy mainframe application and only 12% use a customized software solution. This requires most agencies to manually review spreadsheets and Access reports to determine when the next collection action is to be taken, resulting in errors and delays. Customized software uses automated actions to ensure consistent follow-up and timely actions. The 2010 NASACT survey ranked the most effective strategies for debt collection (Table 17).

Table 17.

Most Effective Strategies for Debt Collection

1. Offsetting state and federal tax returns 2. Liens, levies, garnishments and license holds (if available) 3. Automated notices and correspondence 4. Centralized collections 5. Better use of private collection agencies 6. Automated collection software 7. Electronic payments 8. Imposition of penalties and interest 9. Increased staffing

Centralizing debt collection functions would allow Oregon state government to implement or expand eight of the strategies referenced in Table 17 and would ensure consistent processes were followed to collect delinquent debts.

20 http://www.nasact.org/files/News_and_Publications/White_Papers_Reports/2010_08_01_CGI-NASACT_Debt_Collection_Survey.pdf

Fiscal Year 2016 Statewide Accounts Receivable Management Report

25

DOR-OAA currently performs offsets of state tax refunds (federal tax offsets are performed for state tax debts only); centralization would allow for the accounts to stay in the DOR-OAA system for a longer period of time ensuring future offsets occur. The DOR-OAA conversion to the GenTax system further expands DOR’s ability to automate the creation of collection letters and collection correspondence such as warrants, lien documents and garnishments. A centralized debt collection model also allows for a more coordinated approach to the use of PCAs and development of a performance-based contract model that rewards vendors with the highest performance. Debtors currently can make a payment many different ways, including electronic payments; however, not all agencies use the same options. Centralization will ensure that all debtors have the same options for paying debts including the use of electronic payments. The imposition of penalties and interest is established by the originating agency and requires notice be provided to the debtor before being charged. The GenTax system allows for the calculation of interest if the originating agency has provided the proper notice. Through centralization, the process of calculating interest would be consistent across all debts assigned to DOR-OAA. SWARM proposed legislative changes that would centralize the collection of state debts through the DOR-OAA once the accounts become liquidated and delinquent. The proposal keeps the agency requirement to provide notice to the debtor and liquidate the account, but after 90 days the agency would assign the accounts to DOR-OAA which would take responsibility for future collection activities. DOR-OAA has the systems available to automate correspondence and collection actions, including subsequent assignment to a PCA.

Conclusion

It is the opinion of SWARM that agencies have made efforts to improve the collection of their liquidated and delinquent accounts receivable as demonstrated by the increase of $193.3 million in collections from fiscal year 2015. OJD implemented its Odyssey system which provides better account management and reporting capabilities. DOR implemented the GenTax system for many of its tax programs and the Other Agency Accounts Unit was converted in November 2016. GenTax provides for more automated processes and notifications than DOR’s prior system. The child support division of DOJ is currently working on a project plan to upgrade its system which will enable better collection and monitoring of delinquent child support obligations. Between May and November 2016 SWARM met with 60 state agencies to understand the accounts receivable management processes used by agencies and the challenges they encounter when collecting receivables. SWARM has provided education about statutory requirements; and resources to assist agencies with improving collections. Based on recommendations provided by SWARM, many agencies reviewed internal processes or established new processes in an effort to ensure timely liquidation and assignment of accounts to DOR-OAA or a PCA. SWARM looks forward to meeting with remaining agencies in 2017.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

26

SWARM established the Accounts Receivable Core Committee to engage agencies in discussion about current collection practices and assist SWARM in developing strategies to improve statewide accounts receivable management. The ARCC serves as a forum for state agency accounts receivable professionals to collaborate with peers from other state agencies and to discuss successful collection strategies, lessons learned and best practices.

Acknowledgments

SWARM appreciates the access to agency liquidated and delinquent accounts receivable data from the Legislative Fiscal Office. This report would not be possible without LFO’s support. DAS also extends thanks to state agencies for staff’s professionalism and dedication to improving accounts receivable data and collection processes.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

27

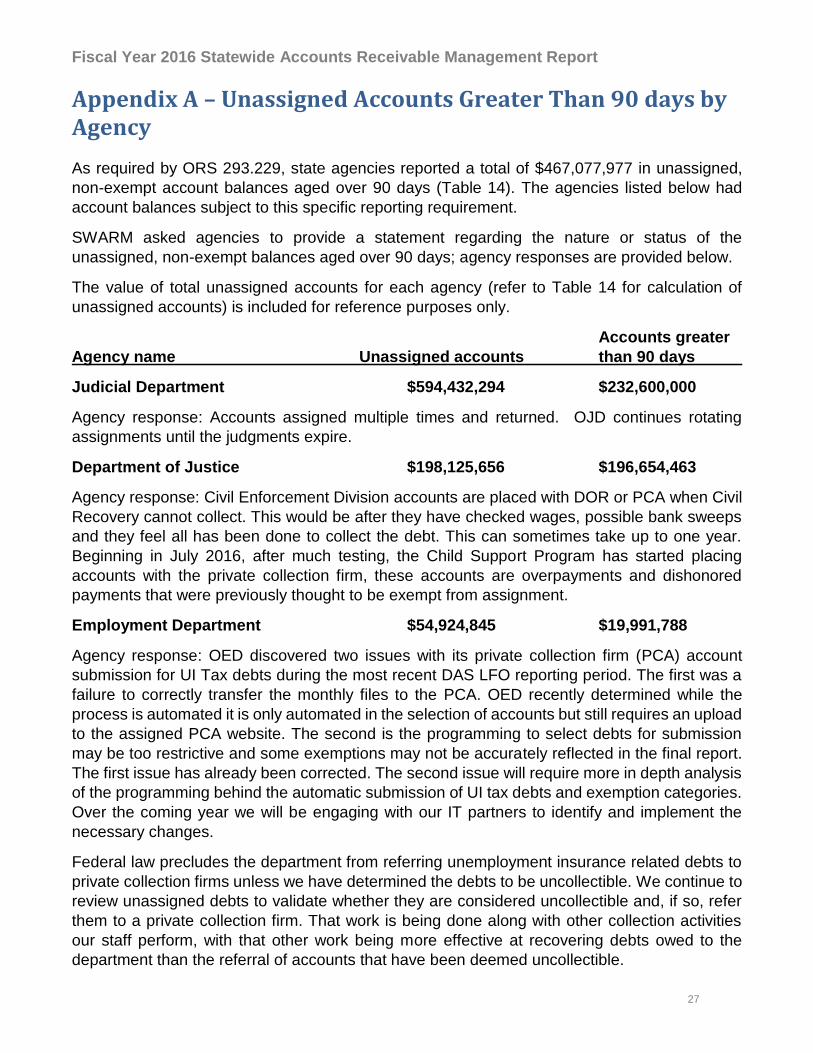

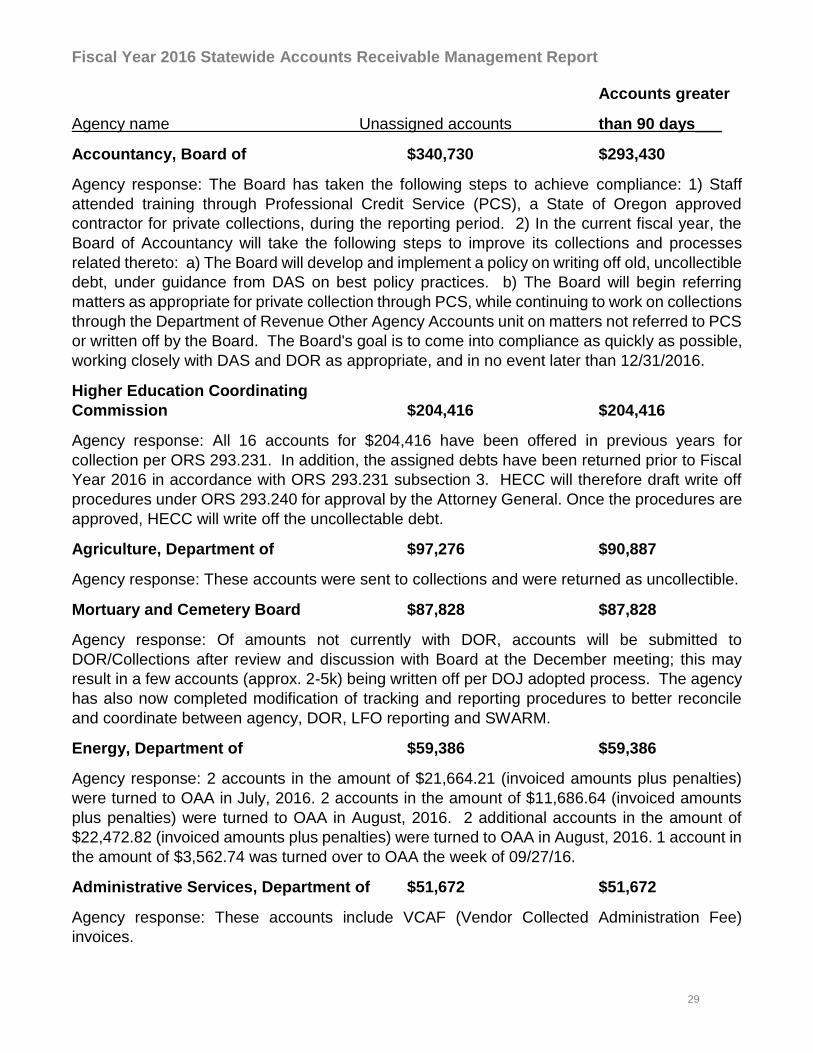

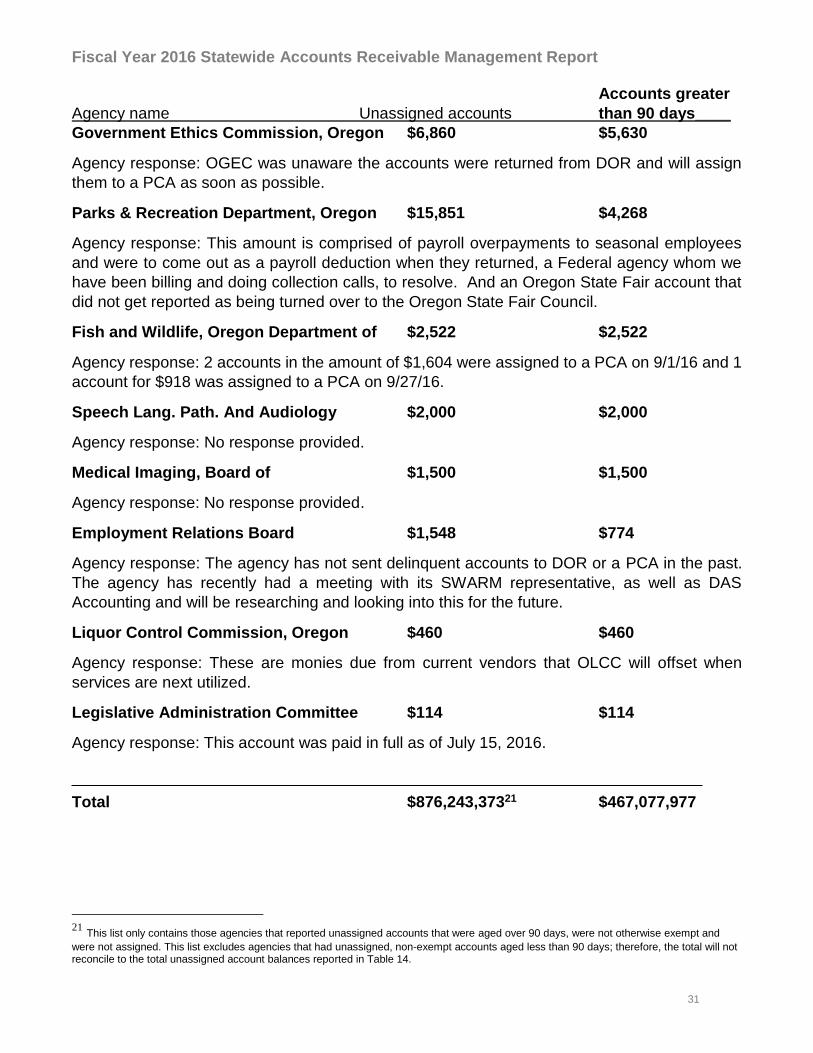

Appendix A – Unassigned Accounts Greater Than 90 days by Agency

As required by ORS 293.229, state agencies reported a total of $467,077,977 in unassigned,

non-exempt account balances aged over 90 days (Table 14). The agencies listed below had

account balances subject to this specific reporting requirement.

SWARM asked agencies to provide a statement regarding the nature or status of the

unassigned, non-exempt balances aged over 90 days; agency responses are provided below.

The value of total unassigned accounts for each agency (refer to Table 14 for calculation of

unassigned accounts) is included for reference purposes only.

Accounts greater

Agency name Unassigned accounts than 90 days

Judicial Department $594,432,294 $232,600,000

Agency response: Accounts assigned multiple times and returned. OJD continues rotating

assignments until the judgments expire.

Department of Justice $198,125,656 $196,654,463

Agency response: Civil Enforcement Division accounts are placed with DOR or PCA when Civil

Recovery cannot collect. This would be after they have checked wages, possible bank sweeps

and they feel all has been done to collect the debt. This can sometimes take up to one year.

Beginning in July 2016, after much testing, the Child Support Program has started placing

accounts with the private collection firm, these accounts are overpayments and dishonored

payments that were previously thought to be exempt from assignment.

Employment Department $54,924,845 $19,991,788

Agency response: OED discovered two issues with its private collection firm (PCA) account

submission for UI Tax debts during the most recent DAS LFO reporting period. The first was a

failure to correctly transfer the monthly files to the PCA. OED recently determined while the

process is automated it is only automated in the selection of accounts but still requires an upload

to the assigned PCA website. The second is the programming to select debts for submission

may be too restrictive and some exemptions may not be accurately reflected in the final report.

The first issue has already been corrected. The second issue will require more in depth analysis

of the programming behind the automatic submission of UI tax debts and exemption categories.

Over the coming year we will be engaging with our IT partners to identify and implement the

necessary changes.

Federal law precludes the department from referring unemployment insurance related debts to

private collection firms unless we have determined the debts to be uncollectible. We continue to

review unassigned debts to validate whether they are considered uncollectible and, if so, refer

them to a private collection firm. That work is being done along with other collection activities

our staff perform, with that other work being more effective at recovering debts owed to the

department than the referral of accounts that have been deemed uncollectible.

Fiscal Year 2016 Statewide Accounts Receivable Management Report

28

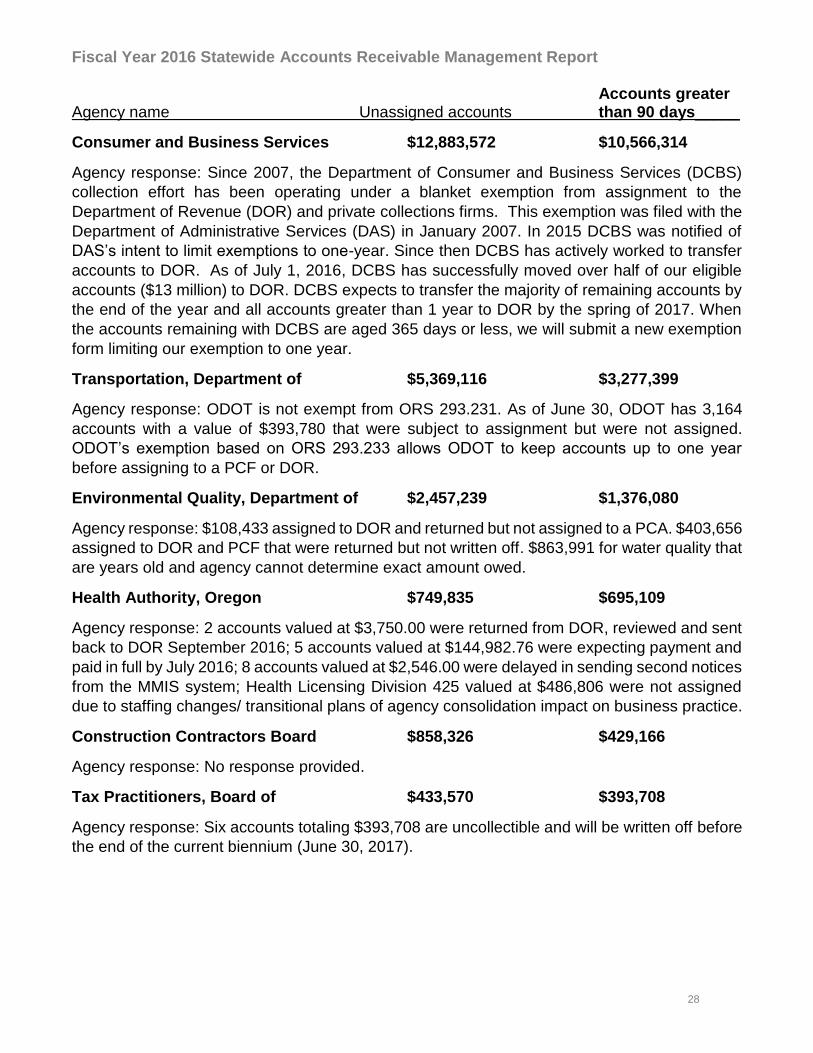

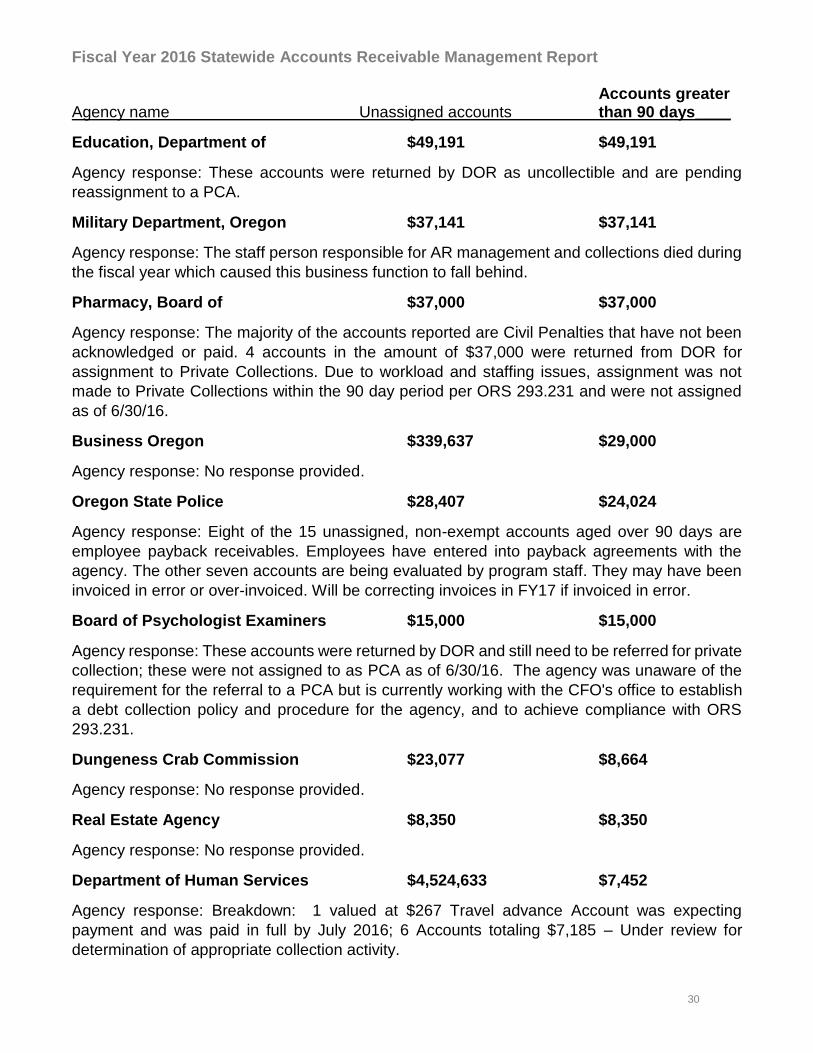

Accounts greater Agency name Unassigned accounts than 90 days_____

Consumer and Business Services $12,883,572 $10,566,314

Agency response: Since 2007, the Department of Consumer and Business Services (DCBS)

collection effort has been operating under a blanket exemption from assignment to the

Department of Revenue (DOR) and private collections firms. This exemption was filed with the