statistical, economic and social research · pdf filestatistical, economic and social research...

TRANSCRIPT

STATISTICAL, ECONOMIC AND SOCIAL RESEARCH AND

TRAINING CENTRE FOR ISLAMIC COUNTRIES (SESRIC)

Mazhar Hussain, Senior Researcher

Economic and Social Research Department

101 102

3734

2005 2014

World

OIC

# of Countries Reported Data

10911046

384

267

2005 2014

# of MFIs Reported Data

2005

384 MFIs in 37 OIC countries accounted for 35% of the total MFIs reported data

2014

267 MFIs in 34 OIC countries accounted for 26% of the total MFIs reported data

# of MFIs Reported Data

47

106

25 27

2005 2014

Active Borrowers - Millions

World

OIC

18

88

5

16

2005 2014

Gross Loan Portfolio –Billions$

2005

25 million active borrowers (53% of the total) with a gross loan portfolio of USD 5 billion (29%)

2014

27 million active borrowers (26% of the total) with a gross loan portfolio of USD 16 billion

(18%)

Active Borrowers- Millions Gross Loan Portfolio- Billion USD

Bangladesh

64%

Pakistan6% Nigeria

6%

Azerbaijan4%

Morocco3%Indonesia2%

Egypt2%

Kyrgyzstan2%

Uganda1%

Tajikistan1%

Rest of MCs9%

Bangladesh

33%

Azerbaijan24%Uzbekistan

7%

Morocco4%

Tajikistan4%

Pakistan3%

Nigeria3%

Uganda3%

Kyrgyzstan2%

Benin2% Rest of

MCs15%

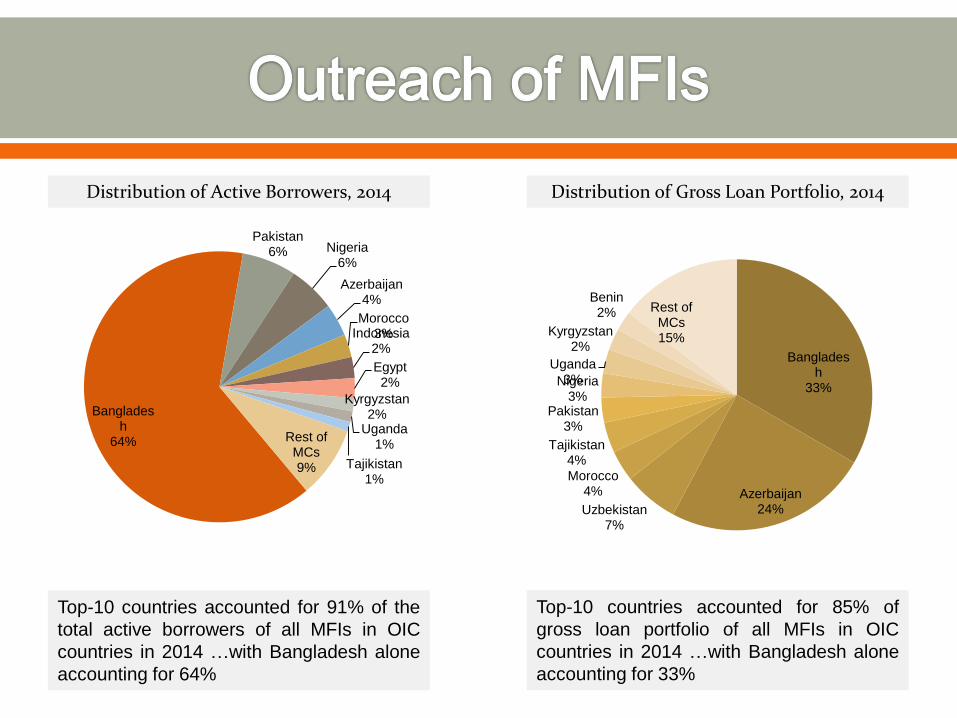

Top-10 countries accounted for 91% of the

total active borrowers of all MFIs in OIC

countries in 2014 …with Bangladesh alone

accounting for 64%

Top-10 countries accounted for 85% of

gross loan portfolio of all MFIs in OIC

countries in 2014 …with Bangladesh alone

accounting for 33%

Distribution of Active Borrowers, 2014 Distribution of Gross Loan Portfolio, 2014

64%

28%

5%2%

1%

EAP MENA SA SSA ECA

225IMFIs in

19 Countries

225 IMFIs in 19 countries as of

March 2013 compared to 126

IMFIs operating in 14 countries

IMFIs are highly concentrated in

East Asia and Pacific and MENA

regions… accounting for 92% of

the total IMFIs in 2013

Source: CGAP Focus Note 84, March 2013

Active Clients

35%

33%

14%

18%

Bangladesh SudanIndonesia Other

1.28 million

Clients

IMFIs provided sharia-compliant

products and services to 1.28

million clients in 2013 compared

to 0.3 million clients in 2008

82% of total clients are living in

three OIC countries: Bangladesh

(35%), Sudan (33%) and

Indonesia (14%)

Despite an upward trend

still….accounting for only 5% of

OIC and 1% of world total in

2014

Loan Portfolio

IMFIs were managing 625

million$ worth of fund portfolio in

2013 compared to 198 million$ in

2008

91% of total portfolio is

distributed in three OIC

countries: Indonesia (55%),

Lebanon (21%) and

Bangladesh (15%)

55%

21%

15%

9%

Indonesia Lebanon

Banglades Rest

625Million $

worth of

portfolio

Supply of Islamic Microfinance

accounts for a tiny fraction

(0.7%) of the world and 4% of the

OIC total MFIs loan portfolio

Micro credit

Qard hasan

Murabaha

Bai bithaman ajil

Ijarah

Salam

Micro Equity

Mudaraba

Musharaka

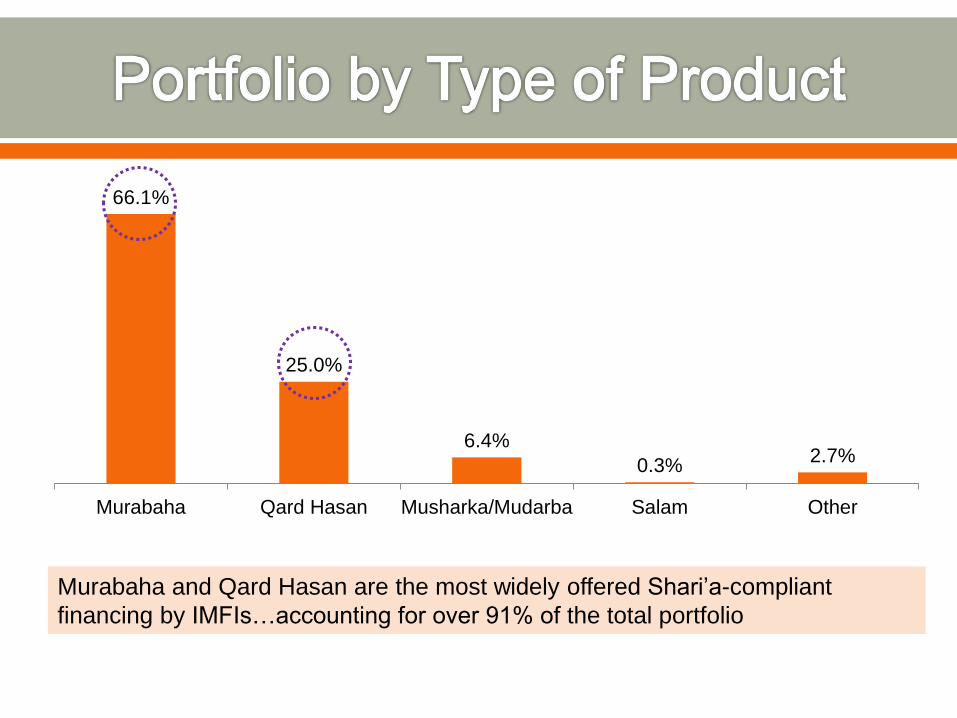

66.1%

25.0%

6.4%

0.3%2.7%

Murabaha Qard Hasan Musharka/Mudarba Salam Other

Murabaha and Qard Hasan are the most widely offered Shari’a-compliant

financing by IMFIs…accounting for over 91% of the total portfolio

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Regulation and supervision of microcredit portfolios Formation of regulated/supervised microcredit institutions

Formation/operation of non-regulated microcredit institutions Regulatory and supervisory capacity for microfinance

Regulatory framework for deposit-taking

0

0.5

1

1.5

2

2.5

3

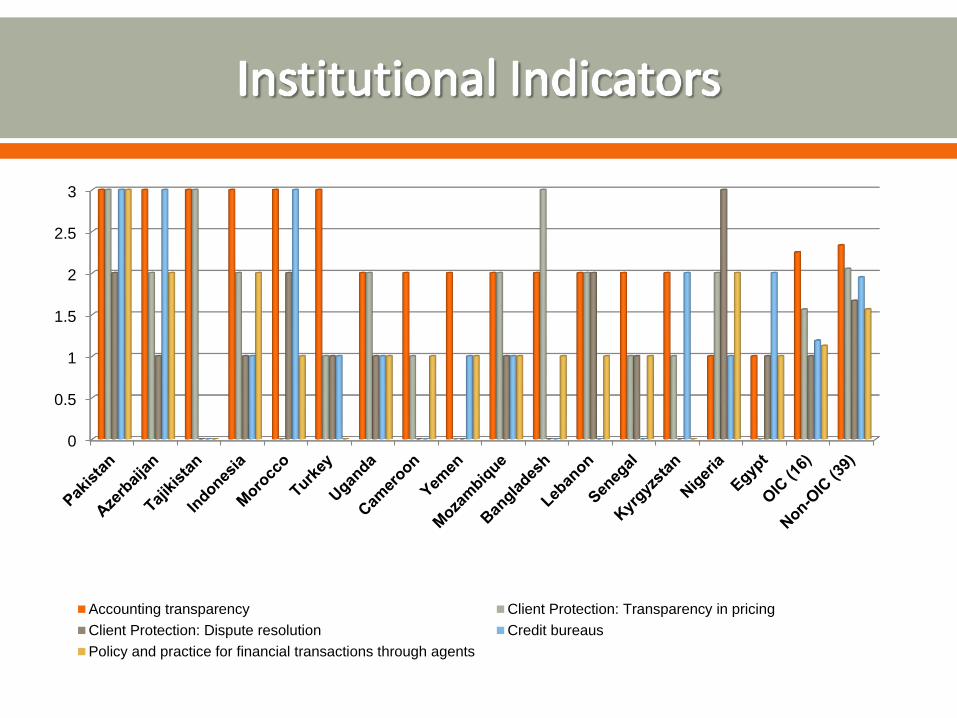

Accounting transparency Client Protection: Transparency in pricing

Client Protection: Dispute resolution Credit bureaus

Policy and practice for financial transactions through agents

High transaction

costs

Market Penetration

Less variety of products

Sustainability and funding

65% of respondents have stated that the higher cost of

microfinance drives beneficiaries into severe debt. This

indicates that the operations and transactions costs of

microfinance need to be reduced in order to better serve

the needs of the poor.

There should be a more standardized framework for

microfinance in order to increase effectiveness in

helping the poor.

Most survey respondents have stated that the way to

ensure Shariah compliance in microfinance is through

oversight by the Shariah boards. Good governance is

also essential so that operating costs will be formed on

the basis of pricing.

72% of respondents consider volunteerism to be an

important part of microfinance, as it will enable

microfinance institutions to reduce operating costs and

will also build relationships with the community and the

poor to further reduce financial and societal exclusion.

The establishments of skills empowerment centers that

ensure clients are given adequate training prior to being

provided financing as well as financial services.

Microfinance institutions continued to face two

primary challenges; access to affordable finance

and inadequate human resources confronted both

by the providers and recipients of services. Existing

models have largely failed to adequately overcome

all the challenges.

In order to address these two primary challenges,

this study aims to develop an Integrated Waqf-

based Islamic Microfinance (IWIM) model, which

comprises six components, namely Waqf, Islamic

microfinance, human resources, Takaful, project

financing and poverty alleviation, and validate and

test the IWIM model in the three selected countries.

Thank you for your

attention !