status, prospects and challenges for offshore wind...

TRANSCRIPT

Quelle: PrognosFootnoteSource

STICKER

Status, Prospects and Challenges for Offshore Wind Energy in Germany - incl. Legal Framework and Presentation of cost reduction study results

Ecomondo Fair, 6 Nov. 2013

Andreas WAGNER managing director

Stiftung OFFSHORE-WINDENERGIEGerman Offshore Wind Energy Foundation

Quelle: PrognosFootnoteSource

STICKER

I. Stiftung OFFSHORE-WINDENEGIE - who we are

II. Status and Prospects for Offshore Wind in Germany

III. Legal Framework for Grid Connection, Renewable Energy Act

IV. Cost reduction potentials

2

Overview

Quelle: PrognosFootnoteSource

STICKER

3

I. German Offshore Wind Energy Foundation

o Independent, non-partisan institution to support the development of offshore wind energy, founded in 2005

o Platform for offshore wind (and maritime) industry, for policy-makers and research-oriented stakeholders

o Board of Trustees - key industry & policy stakeholders

o PR and public acceptance activities, o Policy initiatives & studies• OffWEA project

Consulting and support for the federal government in realising and advancing the German offshore wind energy strategy

• WINDSPEED• SEANERGY 2020• Interreg Projects:

4POWER, South Baltic OFF.E.R.

Quelle: PrognosFootnoteSource

STICKER

I. The OffWEA Project

Consulting and support for the federal government in realising and advancing the German offshore wind energy strategy.

The German Offshore Wind Energy Foundation and its project partners on behalf of the Federal Ministry for the Environment

Project runs from 08/2011 to 08/2014

Information Platform

www.offshore-windenergie.net

4© SOW E.ON Netz D. Gehring© SOW E.ON Netz D. Gehring © SOW E.ON Netz D. Gehring

Quelle: PrognosFootnoteSource

STICKER

5

Cumulative and annual offshore wind installations

in Europe

Source: EWEA, European Offshore Statistics 2012

Quelle: PrognosFootnoteSource

STICKER

6

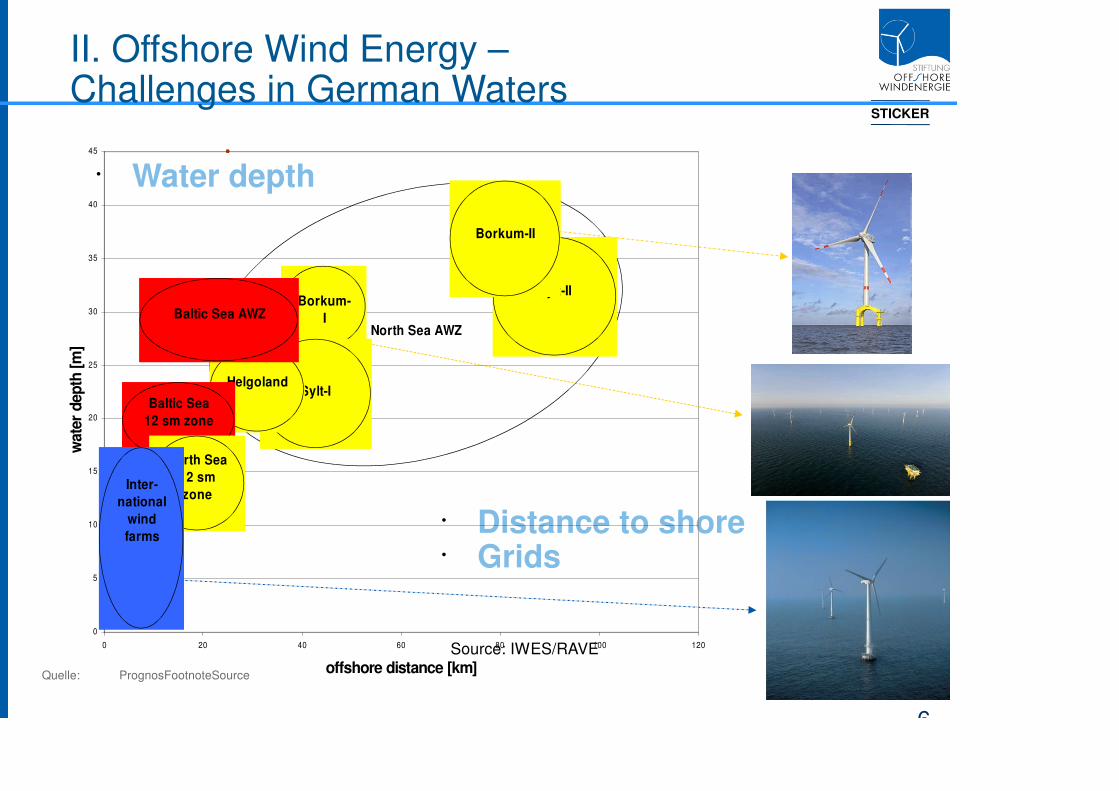

II. Offshore Wind Energy – Challenges in German Waters

Source: IWES/RAVE

• Distance to shore• Grids

• Water depth

0

5

10

15

20

25

30

35

40

45

0 20 40 60 80 100 120

offshore distance [km]

wate

r d

ep

th [

m]

North Sea AWZ

Borkum-

I

Sylt-I

Sylt-II

Helgoland

Borkum-II

Baltic Sea AWZ

Baltic Sea

12 sm zone

North Sea

12 sm

zoneInter-

national

wind

farms

Quelle: PrognosFootnoteSource

STICKER

II. Spatial Plan for EEZ (North Sea)

Off

Sho

e Wind Ene

gy in Ge

many

Quelle: PrognosFootnoteSource

STICKER

II. Status Quo Licensing

95 applications for offshore wind farms in German EEZ (78 in North Sea), 33 projects licensed (incl. 3 prototype turbines) – Total capacity 8-10 GW

North Sea > 80 % of projects, Baltic Sea < 20 %

Quelle: PrognosFootnoteSource

STICKER

9

3 GW under construction in 2012/2013

of which 520 MW in operation (10/2013)

Borkum Riffgrund 1 (2013-2015, 320 MW)

Baltic Sea

cons

truc

tion

unde

rway

Nordergründe (2014-2015, 125 MW)

Baltic 2 (2013-2014, 288 MW)

Butendiek (2014-2015, 288 MW)

Amrumbank West (2013-2015, 400 MW)

Dan Tysk (2012-2014, 288 MW)

Borkum West 2, (2012-2014, 200 MW)

BARD Offshore 1 (2010-2013, 400 MW)

Borkum Riffgat, (2012-2013, 108 MW)

Global Tech I(2012- 2014, 400 MW)

Nordsee Ost (2012-2014, 295 MW)

Meerwind (2012-2014, 288 MW)

Quelle: PrognosFootnoteSource

STICKER

10

10

Pioneering project alpha ventus

First Offshore Wind Farm (OWF) in Germany,

constructed 2008-10

� 12 wind turbines (à 5 MW) � 60 MW� 2 turbine manufacturers (AREVA/Multibrid,REpower)� 2 types of foundations (tripods, jackets)� 60 km distance to shore, 30 m water depth

� Permits acquired by SOW in 2005� Leased to DOTI (EWE, E.ON, Vattenfall)� Commissioning in 2009/10� Extensive ecological and technological research

funded by the German Ministry for Environment - 50 M€ R&D program (RAVE)

� Impressive operational results – 50 % capacity factor (4,450 full load hours)

Quelle: PrognosFootnoteSource

STICKER

11

Commercial OWF in operation (08-2013)

EnBW Baltic 1 (Inauguration May 2011) Within the 12-nm-zone (Baltic Sea)

� 21 Siemens turbines (à 2,3 MW) � 48,3 MW

� 16-19 m water depth

� Monopile foundations,

� AC grid connection

� Construction during 2010-2011

BARD Offshore 1 (inaugurated 27 Aug. 2013)

� EEZ (North Sea) - 90 km from shore

� 80 wind turbines (à 5 MW) � 400 MW

� Electricity for 400,000 households

� 40 m water depth

Quelle: PrognosFootnoteSource

STICKER

12

Commercial OWF completed/under construction (08-2013)

Borkum Riffgat – OWF completed (EWE)30 turbines (3,6 MW) – 108 MW, Construction 2012-13BUT Grid connection delayed until 2014

Borkum West 2 (Trianel)Phase 1: 40 turbines (5 MW) – 200 MWConstruction 2012-14, grid connection delays

Borkum Riffgrund (DONG)77 turbines (3.6 MW) – 277 MW, Construction 2013-14

Dan Tysk (Vattenfall/SWM)80 turbines (3,6 MW) – 288 MW, Construction 2012-14

Quelle: PrognosFootnoteSource

STICKER

13

Commercial OWF completed/under construction (10-2013) Helgoland Cluster – grid connection delayed

Meerwind Süd/Ost - WindMW (Blackstone)80 turbines (3.6 MW) - 288 MW, Construction 2012-14

Nordsee Ost – RWE Innogy48 turbines (6.15 MW) – 295 MW, Construction 2012-14

� Amrumbank West – E.ON Climate & Renewables

80 turbines (3.6 MW) . 288 MW, Construction 2013-15

Quelle: PrognosFootnoteSource

STICKER

14

Commercial OWF completed/under construction (10-2013) Global Tech 1 – investor consortium led by SWM

80 turbines (5 MW) – 400 MW, Construction 2012-14

Baltic 2 - EnBW (Baltic Sea)

80 turbines (3,6 MW) – 288 MW,

Construction 2013-14

Quelle: PrognosFootnoteSource

STICKER

15

Offshore Wind Energy in Germany – An illustration of initial positive results

Positive operational results: - alpha ventus: > 4.450 full load hours in 2011 (267 GWh)

� 15 % above expectations, - Baltic I – similar results; turbine availability 98 %

� Important contribution to energy system reliability!

� 1 billion Euro already invested along the German coast - Port infrastructure, production facilities (offshore turbines/components), construction vessels, (converter) platforms etc. � Vast opportunities for maritime industries!

> 10 billion Euro investment for Offshore Wind Farms �8 OWP under construction in 10/2013

18,000 jobs created by 2012 (98,000 jobs in onshore wind) � Need for new and adjusted professional and vocational training

Quelle: PrognosFootnoteSource

STICKER

16

16

Status & Outlook - Offshore Wind in Germany

3 GW+ unconditional orders � 3.5 GW online by 2015/16Ambitious government targets - 10 GW by 2020; Delays caused by political uncertainty and delays in grid connection! 20-25 GW by 2030 � 85-100 TWh = 15 % of German electricity demand =Total investment of € 75 – 100 bn by 2030 New growth opportunity for machinery & engineering sector, construction and maritime industries 18,000 new jobs, doubling possible by 2023 Germany strong in R&D, turbine & component technology (5-6 MW turbine developments), port infrastructure development Vast project pipeline (> 30 licensed OWFs, almost 100 in application)

Quelle: PrognosFootnoteSource

STICKER

17

17

…BUT

Challenges to meet government targets

Regulatory and financing issues (grids!) need to be resolved

Long lead times of projects � Next phase of OWP investments requires urgent solution of financing issues

Infrastructure development and logistics

O&M concepts (incl. HSE), Education and training

New technology solutions, (environmental) R&D

Quelle: PrognosFootnoteSource

STICKER

Diagramm durch Klicken auf Symbol hinzufügen

The German Wind Energy Market

Gross Electricity Consumption from RE in Germany 20121)

of renewable energies Prognosis of yearly installed offshore capacity (in GW)1)

Renewable Energies (RE) have a share of 23% (2012) of German electricity consumption.Today, 1/3 of RE comes from wind (onshore) – wind will be the main driver for future growth.

Sources: 1) BDEW, 2013; 2) DLR, Fraunhofer IWES, IfnE, 2012

Prognosis of Electricity Production (in TWh/A) from Wind in Germany2)

0

2

4

6

8

10

12

18

Quelle: PrognosFootnoteSource

STICKER

III. Legal Framework for Offshore Wind Energy

The Renewable Energy Act - EEGSupport for renewable energy - specifies remuneration, technology differentiation since 2000

Issues in the past for offshore wind (prior to 2009)

� No investments due to insufficient remuneration for offshore wind energy (9,1 ct/kWh)

EEG of 2008 (entered into force on 1st Jan. 2009)

�Increase of initial Feed-in-Tariff (FiT) to 13.0 ct/kWh, plus starter bonus of 2 ct, granted for 12 years after commissionig (if commissioning before 1 January 2016)

EEG of 2011(entered into force on 1st Jan. 2012)

�Compressed FiT: Option to claim an increased initial rate of 19 ct/kWh – only granted for 8 years after commissioning, afterwards FiT drops to 3.5 ct/kWh

�Important boost for investment decisions

New issues emerged in 2013

Off

Sho

e Wind Ene

gy in Ge

many

Quelle: PrognosFootnoteSource

STICKER

III. Legal Framework for Offshore Wind The Electricity and Gas Supply Act

(EnWG) Regulates on- and off-shore grid connections in Germany

Issues in the past

� Obligation for private Transmission System Operators (TSO) to enable the connection

� North Sea: TenneT, Baltic Sea: 50Hertz

� Grid connection must be “on time” – wind farm initiated process - TSOs had to react

Result Delay of grid connections

Several reasons for the delay

� Investment decision requires confirmation on grid connection by TSO

� TenneT was (and still is?) seriously underfunded for this task

� Matter of liability for compensation due to delay was unclear

� Most importantly: Lack of cables and converter stations

Off

Sho

e Wind Ene

gy in Ge

many

Quelle: PrognosFootnoteSource

STICKER

III. Reform of Electricity and Gas Supply Act (2012)

Solution - System Change – "Change of paradigm and compensation“

BFO - Federal Off-shore Grid Plan by BSH (Federal Maritime and Hydrographic Agency)

– Comparable with a spatial plan for grid connections

– Identifies cable routes and locations for converter stations

– Does not regulate the order of grid connections

ONEP - Off-shore Grid Development Plan (TSO)

– TSO sets dates for the connection of the grid

– Wind farms lose their individual right of connection

– Confirmed by the Federal Network Agency (BNetzA)

Compensation Mechanism

– 90 % of feed-in tariff in case of delay

– Starting from 11th day of delay

Off

Sho

e Wind Ene

gy in Ge

many

Quelle: PrognosFootnoteSource

STICKER

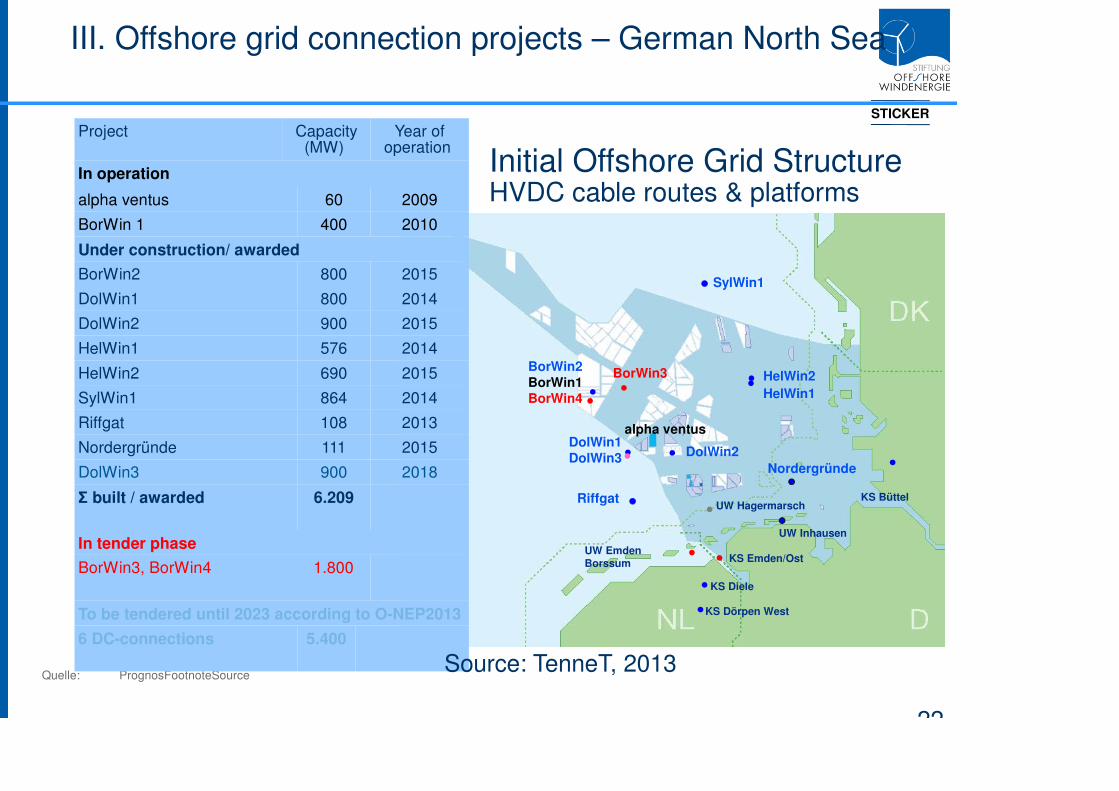

III. Offshore grid connection projects – German North Sea

22

Riffgat

KS Diele

KS Dörpen West

UW Emden Borssum

BorWin2

BorWin1

BorWin4 HelWin1

HelWin2

DolWin2DolWin1

DolWin3

alpha ventus

BorWin3

UW Inhausen

Nordergründe

KS Büttel

KS Emden/Ost

UW Hagermarsch

SylWin1

Project Capacity (MW)

Year of operation

In operation

alpha ventus 60 2009

BorWin 1 400 2010

Under construction/ awarded

BorWin2 800 2015

DolWin1 800 2014

DolWin2 900 2015

HelWin1 576 2014

HelWin2 690 2015

SylWin1 864 2014

Riffgat 108 2013

Nordergründe 111 2015

DolWin3 900 2018

Ʃ built / awarded 6.209

In tender phase

BorWin3, BorWin4 1.800

To be tendered until 2023 according to O-NEP2013

6 DC-connections 5.400

Source: TenneT, 2013

Initial Offshore Grid StructureHVDC cable routes & platforms

Quelle: PrognosFootnoteSource

STICKER

23

From Plan to Implementation – O-NEP (Offshore Grid Development Plan)

10-year Grid Development Plan (2023), plus 20 year perspective (2033) – based on Scenarios (TSOs, regulator)

Quelle: PrognosFootnoteSource

STICKER

24

IV. Study on cost reduction potential for offshore

wind – launched on 22 Aug. 2013 in Berlin

Partners –

Commissioning organisations and companies

Quelle: PrognosFootnoteSource

STICKER

25

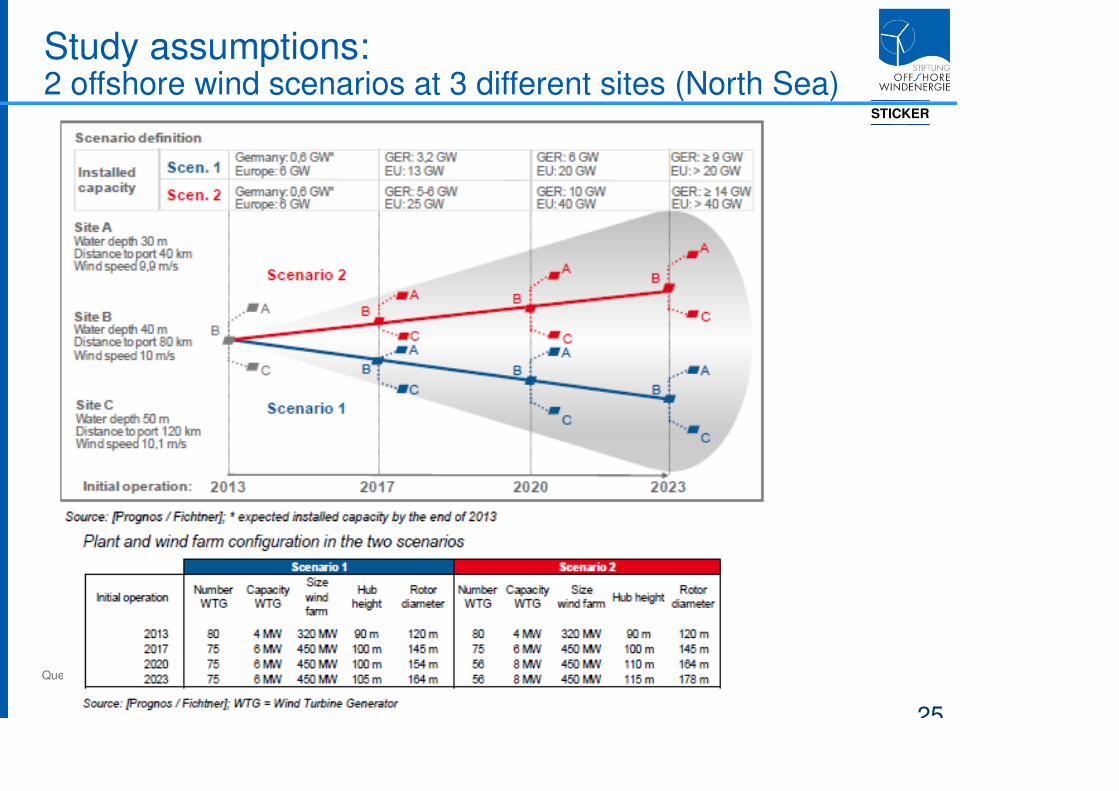

Study assumptions: 2 offshore wind scenarios at 3 different sites (North Sea)

Quelle: PrognosFootnoteSource

STICKER

26

Long lead times for OWF development prior to commissioning require long-term stable framework

4-6 Years

1-2 Years

2-4 Years

20 Years 5 Years

1-2 Years

Project development

Financial

Negotiations

Construction Operation Phase Extension of operation

Decommissioning

Total project lifetime 27-37 years

FID

Commissioning

Construction Permit

© Prognos/Fichtner

Idealized Project Schedule

Quelle: PrognosFootnoteSource

STICKER

27

Economies of scale and increasing competiton lead to higher cost reduction potential in scenario 2

Development of levelised cost of energy in real terms, example of wind farm B

Quelle: PrognosFootnoteSource

STICKER

28

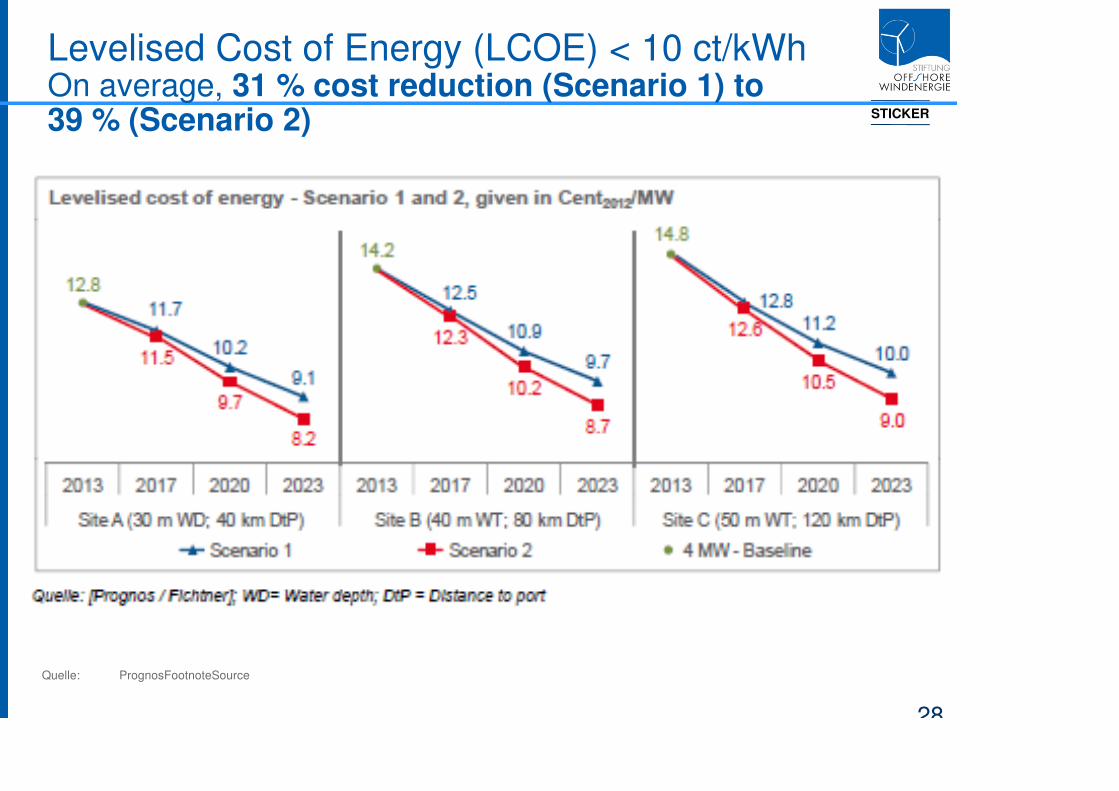

Levelised Cost of Energy (LCOE) < 10 ct/kWhOn average, 31 % cost reduction (Scenario 1) to 39 % (Scenario 2)

Quelle: PrognosFootnoteSource

STICKER

29

Recommendations - Policy and Regulatory Environment

� Stable legal and political framework conditions

� Define standards for components and for grid connection (platforms)

� Simplify certification and permitting criteria

Recommendations for Industry towards techology innovation:

� Optimise plant technologies towards maximum energy yield/operational hours

� Optimisation of existing support structures and development of new ones

� Improve installation logistics

� Intensify R&D efforts

Recommendations for Industry to improve efficiency

� Development of joint installation

and O&M concepts

� Intensified efforts for serial production

Realising cost reduction potentials requires active

commitment and participation of all stakeholders

Quelle: PrognosFootnoteSource

STICKER

EWEA Offshore 2013

Andreas Wagner

Stiftung Offshore-Windenergie

German Offshore Wind Energy Foundation

Quelle: PrognosFootnoteSource

STICKER

EWEA Off

hore 2013

31

31

About the event

19-21 November 2013Messe Frankfurt, Germany

International platform to present latest offshore wind energy products and services

Worlds largest offshore wind energy conference with more than 480 exhibitors and over 8200 participants (EOW 2011, Amsterdam)

Quelle: PrognosFootnoteSource

STICKER

EWEA Off

hore 2013

32

32

Important events with german participation

Day1 – Tuesday, 19. November:

12:10 press conference & high-level plenary: 2030 targets – the magic number?

15:40 CEO Q&A session

16:00 – 17:30 discussion forum about european energy policies (with German Ministry for Environment)

Day 2 – Wednesday, 20. November:

11:00 – 12:30 “Making offshore wind less expensive” with Prognos

13:00 – 14:00 press conference German Engineering Association and German Offshore Wind Energy Foundation

14:00 – 19:00 Franco-German offshore wind opportunities workshop

Quelle: PrognosFootnoteSource

STICKER

33

THANK YOU!

Andreas Wagner, managing director

Berlin OfficeSchiffbauerdamm 19, 10117 Berlin, GermanyPhone: +49-30-27595-141Fax: [email protected]

Varel OfficeOldenburger Str. 65, 26316 Varel, GermanyPhone: +49-4451-9515-161Fax: [email protected]

www.offshore-stiftung.de www.offshore-windenergie.net