steel industry outlook federal reserve bank of chicago

TRANSCRIPT

Steel Industry OutlookFederal Reserve Bank of ChicagoDecember 4, 2009

Robert J. DiCianniArcelorMittal USA

Confidential 1

Outline

• 2009 Steel Market

• 2010 U.S. Outlook

• Global Steel Outlook/Costs/Risks

• Summary

Confidential 2

RecessionsPeak to Trough GDP Change vs Steel ASC Change

-1.8%

-12.9%

-2.7%

-22.6%

-3.8%

-22.3%

-1.7%

-5.7%

-1.1%

-5.4%-3.1%

-28.2%

-2.8%

-27.6%

-1.3%

-9.7%

-3.3%

??

-30%

-25%

-20%

-15%

-10%

-5%

0%

1948 1953 1957 1960 1970 1973 1981 1990 2008

GDPASC

The peak was actually November 1973. Given that late year peak, this analysis shows the delta between 1974 and 1975 AISI data, AM analysis

Confidential 3

Weekly US Raw Steel Production Capacity Utilization (Capacity reduced as demand fell)thru November 21

30%

40%

50%

60%

70%

80%

90%

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Oct-08

Dec-08

Feb-09

Apr-09

Jun-09

Aug-09

Oct-09

33.5% Dec 27

Source: American Iron & Steel Institute

Confidential 4

Raw Steel Production 2008 and 2009

• 1st Quarter 2008: 27.5m tons, 2.1m tons / wk• 2nd Quarter 2008: 27.6m tons 2.1m tons / wk• 3rd Quarter 2008: 27.2m tons 2.0m tons / wk• 4th Quarter 2008: 18.5m tons 1.5m tons / wk • 2008 total: RSP 100.8; ASC 107

• 1st Quarter 2009: 13.6m tons 1.03m tons / wk• 2nd Quarter 2009: 13.8m tons 1.06 / wk• 3rd Quarter 2009: 16.8m tons 1.3 / wk • 4th Quarter 2009: 18.8m tons 1.4 / wk (est.)• 2009 total: RSP 63; ASC 66 (est.)

Source: American Iron and Steel Institute data, AM USA analysis

Confidential 5

U. S. Steel Service CenterTotal Shipments & InventoriesCarbon Flat RolledSource: MSCI; Based on a representative sample of the U.S. Service Center Industry

1300

1800

2300

2800

3300

'02 A J O '03 A J O '04 A J O '05 A J O '06 A J O '07 A J O '08 A J O '09 A J O

2,500

3,500

4,500

5,500

6,500

7,500

8,500Monthly Shipments 3 Mo Rolling AveMonth End Inventory

Monthly Shipments ,000 Tons Ending Inventory ,000 Tons

Confidential 6

2010 Steel Outlook

Confidential 7

GDP Growth Forecast

-0.7%

1.5%

-2.7%

-5.4%

-6.4%

-0.7%

2.8%

2.2%2.5%

1.8% 1.8%

2.7%

1Q'08 2Q'08 3Q'08 4Q'08 1Q'09 2Q'09 3Q'09 4Q'09 1Q'10 2Q'10 3Q'10 4Q'10

Actual Forecast

•GDP decline moderated to -0.7% in Q209.

•Large inventory liquidation of manufactured goods in 1H’09 driving up 2H’09 and 2010 growth

•Credit conditions remain tight

•Unemployment rate to peak at 10.2% in early 2010

•Housing starts in 2010, although improved from 2009, will still be 50% lower than average starts in 2002-2007.

•Non-residential construction continues to contract but will see some improvement in public works spending from stimulus funds.

Source: Global Insight, October 2009

2.1%

0.4%

-2.5%

2.1%

2007 2008 2009 2010

On the slow path to recovery...

Confidential8

Industrial Production & Capacity UtilizationManufacturing Component 2000 – October 2009

60

65

70

75

80

85

2000-01 2001-01 2002-01 2003-01 2004-01 2005-01 2006-01 2007-01 2008-01 2009-01

% C

apac

ity U

tiliz

atio

n

90

95

100

105

110

115

Indu

stri

al P

rodu

ctio

n In

dex

Capacity Util - Manufacturing IP Manufacturing

“V” Shaped recovery?

The consensus estimate sees this as very unlikely.

“The U.S. economy has fallen off a cliff” – Warren BuffettSource: U.S. Federal Reserve Bank Statistical Release November, 2009

Confidential9

ISM Manufacturing Purchasing Managers Index (PMI)

PMI, January 2000-October 2009

25

30

35

40

45

50

55

60

65

J-00

M-00 S-00 J-01

M-01 S-01 J-02

M-02 S-02 J-03

M-03 S-03 J-04

M-04 S-04 J-05

M-05 S-05 J-06

M-06 S-06 J-07

M-07 S-07 J-08

M-08 S-08 J-09

M-099/3

1/200

9

New Orders Index, Jan 2007- Oct 2009

2025303540455055606570

J-07

A-07 J-07

O-07 J-08

A-08 J-08

O-08 J-09

A-09 J-09

O-09

Production Index, Jan 2007- Oct 2009

2025303540455055606570

J-07 M-07 S-07 J-08 M-08 S-08 J-09 M-09 S-09

New orders above 50% in May for first time since Nov

2007; Oct. still shows growth

Production rises above 50% in June-Sep with boost from new

orders; August at 55.7%.

Sep = 52.6% Highest since June 2007

First time above 50 since January 2008

Confidential 10

Steel Markets

Confidential 11

Automotive Production • 2009 forecast is the lowest

production total since the early 1980’s.

• 2009 capacity utilization rate is 51%. 2014 rate will be 81%.

• Detroit 3 account for 56% of production in 2009, down from 63% in 2007 & 58% in 2008. Detroit 3 will account for 53% in 2014.

• U.S imports dropped in 2008, 3.4 million, but gain in share, 26% vs 23% in 2007. Imports are forecast to stay near trend,

NA production(millions of units)

Source: CSM, November 2009

17.1

16.3

15.9

15.7

15.6

15.2

15.0

12.6

8.6

10.5

12.1

13.5

14.9 15

.3

14.8

14.4

7.2

9.2

11.2

13.2

15.2

17.2

19.2

2000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

1016

Confidential 12

Where will steel demand come fromAuto Production

• 2009 auto production will be the lowest production total since the early 1980’s.

• 2009 capacity utilization rate is 51%.

• Detroit 3 account for 55% of production in 2009, down from 63% in 2007 & 58% in 2008.

• Auto production is beginning a gradual increase starting in the third quarter of 2009.

11.21.41.61.8

22.22.42.62.8

Q12009

Q32009

Q12010

Q32010

Millions of units per quarter

Source: CSM Worldwide

Confidential 13

Appliance MarketAppliance sales have been hurt by the housing market but the replacement market kept appliance sales above the drop in housing starts. Rapid de-stocking by the industry occurred in January 2009.

Appliance shipments in 2009 are down 12% September YTD vs. the same period in 2008. As inventory liquidation occurred early in the year, we expect that shipments will improve slightly and that the year will end at -10% to -12%. Consumer rebates from Stimulus Plan for new Energy Star appliance purchases should spur appliance sales late this year or early 2010.

Appliance shipments will improve in 2010 from improvement in housing starts and the increasing replacement base. Delayed appliance replacements from 2008-2010 provide excellent future market potential.

Millions of Units

Source: AHAM, ArcelorMittal USA Marketing forecast

USA Core Appliance Shipments*

*Core appliances = washers, dryers, refrigerators, ranges, dishwashers, and freezers

Confidential14

Housing Starts

1.711.854

1.952.073

1.812

1.342

0.9

0.586

0.873

1.305

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

ActualForecast2002-2007 Average

Millions of units

As the inventory of new homes has finally subsided, we begin to see recovery in housing starts from Q2’09 bottom. The annual rate of starts in Q4’10 forecast to be nearly double Q2’09 rate.

Source: Global Insight, Oct 2009

Q2’09 Q3’09 Q4’09 Q1’10 Q2’10 Q3’10 Q4’10

Starts (in millions, SAAR) 0.540 0.601 0.677 0.764 0.824 0.899 1.005

Confidential 15

USA Energy Market Steel Demandmillion of tons

0

1

2

3

4

5

6

line pipe OCTG

20062007200820092010

Source: History and forecast, Preston Pipe & Tube Report, November 2009

Confidential 16

Wind Energy Growth

502,250

4001,500

4002,350 2,400

5,100

8,558

5,0004,750 5,1506,650 7,050

9,40011,800

16,900

25,300

30,300

2,500

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Additions Total installed

State government renewables target along with a reauthorization of wind generated electricity subsidies from the Federal Government will continue to drive wind energy projects. Financing and right of way for transmission have constrained 2009 additions.

Megawatts

Over 8,500 megawatts installed in 2008. Renewable energy incentives will drive wind, solar and bio-fuel manufacture.

Source: American Wind Energy Association

12/3/2009Confidential 17

Architecture Billings Index (ABI) Source: AIA

*McGraw-Hill

Non-Residential Floor Area (Square Footage)

-22.3%-3.8%

Non-Residential Construction

53.4

43.441.4

33.3

43.142.8

35.334.734.136.2

47.646.146.8

39.741.8

45.5

55.0

50.7

54.8

52.0

54.4

37.7

42.9

55.4

58.858.556.5

53.353.452.9

43.7

43.1

Jan '07 Apr Jul Oct Jan '08 Apr Jul Oct Jan '09 Apr Jul

A score above 50 indicates an increase in billings, and it is a leading indicator

for nonresidential construction spending over the next six to nine months

ABI was 43.1 in September, up from August. Based on the index, the

nonresidential construction market will be suffering into at least mid 2010.

The Inquiries index has been above 50 for 6 straight months, but it is reported that this only because customers are

shopping around more and most don’t end in realized projects.

Non-residential building construction will continue to be a challenge in 2010. Public works projects will show year-over-year increases.

Confidential 18

Stimulus Bill Steel Consumption Potential• Highway Construction

– Bridges – Plate & Rebar – 400,000 tons– Roads – Rebar 800,000 tons – Crash Barriers – 55,000 tons

• Electricity Grid– Pylons – 250,000 tons– Steel Wire - 100,000 tons

• Renewable / Clean Energy– Wind Towers – plate and hot rolled - 500,000 tons– Solar Installation – sheets 190,000 tons

• Federal Infrastructure – Green Buildings – various products 200,000 tons

• Clean Water– Steel Pipes (Standard Pipe) 300,000 tons

• Education Modernization – various products 200,000 tons

Source: AISI & AMUSA analysis

Confidential 19

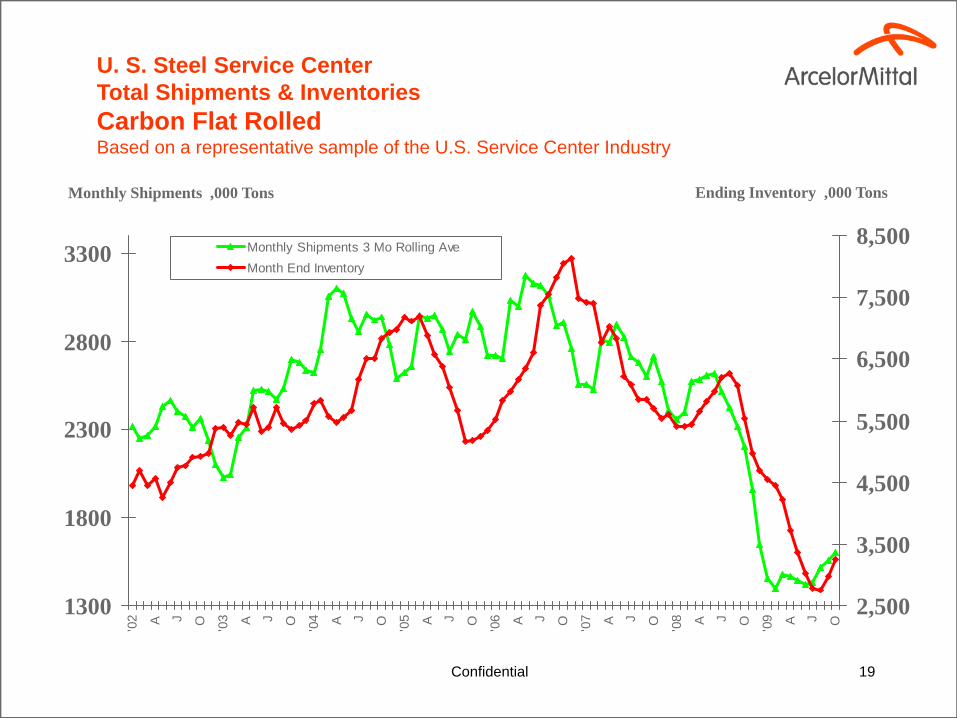

U. S. Steel Service CenterTotal Shipments & InventoriesCarbon Flat RolledBased on a representative sample of the U.S. Service Center Industry

1300

1800

2300

2800

3300

'02 A J O '03 A J O '04 A J O '05 A J O '06 A J O '07 A J O '08 A J O '09 A J O

2,500

3,500

4,500

5,500

6,500

7,500

8,500Monthly Shipments 3 Mo Rolling AveMonth End Inventory

Monthly Shipments ,000 Tons Ending Inventory ,000 Tons

Confidential 20

U. S. Steel Service CenterNumber of Months Shipments on HandBased on a representative sample of the U.S. Service Center IndustryCarbon Flat Rolled

1.5

2

2.5

3

3.5

4

'02 M S '03 M S '04 M S '05 M S '06 M S '07 M S '08 M S '09 M SM

onth

s-on

-Han

d

Actual Long Term Average

2.0

months

Confidential 21

Flat Roll Monthly Imports (,000) mt

200

300

400

500

600

700

800

900

1,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

200720082009

Flat roll import licenses are up in October for 4th straight month. Source: AISI and DOC data

Confidential 22

Steel demand change - 2010

Auto

Residential Construction

Non-residential Construction

Machinery

Agriculture

Electric motors

Infrastructure

Renewable Energy

Pipe & Tube*

* Pipe & tube demand will be improved by the capacity additions of a number of new spiral pipe mills in the USA as well as a drop in imported pipe.

Source: AMUSA analysis

Confidential 23

Global Markets• 2008 Steel Consumption 1.3b tons• 2009 Steel Consumption 1.2b tons (est)• 2010 Steel Consumption 1.3b tons (est)• China

– Domestic demand has been strong – Production has outpace demand– Producers have cut production by 3% from August highs.– Inventory will take months to work off – Excess steel will continue to be exported

• Europe– Return to growth in Q3– Real demand muted by consumers, tight credit, strong euro– Q4 demand rate expected through first half of 2010

• CIS– domestic market situation is still-weak – seasonal slow-down in the construction market– sector is concerned about Chinese exports.

• Brazil– Industrial production rising – rising real demand will continue to improve– underpin the attractiveness of the Brazilian market for major exporters.

Confidential 24

Steelmaking input costs

• Scrap has declined by $75 in the past 2 months. December price increase expected.

• Source: AMM

• Pig iron prices weaken with scrap market - producers are focusing on higher priced domestic market in Brazil.

• Source SBB

$420$410$430

$600

$720$785$890

$570

$170$215

$315 $310$265

$340

$215

$305

$260$255

$220

$850

$125

$290 $195

J-08

F-08

M-08

A-08

M-08

J-08

J-08

A-08

S-08

O-08

N-08

D-08

J-09

F-09

M-09

A-09

M-09

J-09

J-09

A-09

S-09

O-09

N-09

2008 2009

$358$377$395

$510

$653

$731$796

$241$214$234$245$252

$302$313$277$259

$227

$613

$417

$740

$250

$789

$290

J-08

M-08

M-08

J-08

S-08

N-08

J-09

M-09

M-09

J-09

S-09

N-09

2008 2009

Scrap: #1 Busheling-Chicago

Pig Iron: Brazil$/s.ton, Brazil export FOB Ponta da Madeira

Confidential25

Evolution of Zinc Market IndicatorsZinc monthly prices LME cash $/T Market Indicator Evolution:

LME cash $/T

Source: Purchasing based on LME

Zinc Metal MB EU Special High Grade for Rotterdam $ per ton; Source: Metal Bulletin

Confidential 26

Steelmaking raw materials costs

Source: Ryan’s Notes

Confidential 27

Risks

• Credit markets stall• Unemployment higher than anticipated• Double Dip Recession• Quickly increasing energy prices restrain growth• Steel imports greater than expected• Cap and trade• Wars

Confidential 28

Summary

• Inventory liquidation in 1H 2009 greatly depressed manufacturing activity and steel consumption.

• A real demand bottom has now been seen. Steel demand in second of 2009 and the first half of 2010 will have to equal end use consumption.

• Slow GDP growth is now expected in NAFTA

• Global growth in steel consumption is now evident.

• Global steel production is increasing.

Confidential 29

Questions