stephen boyd ee103 stanford university december 8, 2017 · annualized return and risk i mean return...

TRANSCRIPT

Portfolio Optimization

Stephen Boyd

EE103Stanford University

December 8, 2017

Outline

Return and risk

Portfolio investment

Portfolio optimization

Return and risk 2

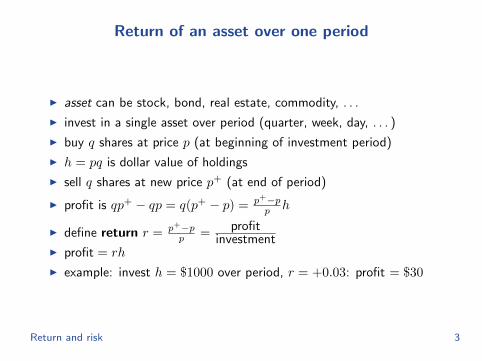

Return of an asset over one period

I asset can be stock, bond, real estate, commodity, . . .

I invest in a single asset over period (quarter, week, day, . . . )

I buy q shares at price p (at beginning of investment period)

I h = pq is dollar value of holdings

I sell q shares at new price p+ (at end of period)

I profit is qp+ − qp = q(p+ − p) = p+−pp h

I define return r = p+−pp =

profitinvestment

I profit = rh

I example: invest h = $1000 over period, r = +0.03: profit = $30

Return and risk 3

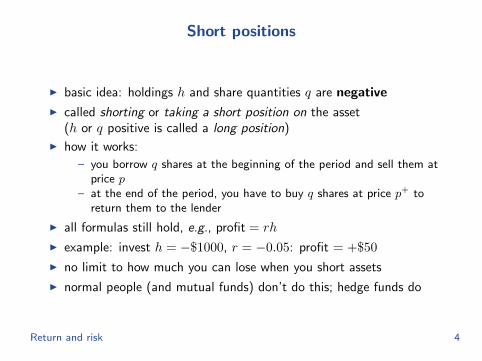

Short positions

I basic idea: holdings h and share quantities q are negative

I called shorting or taking a short position on the asset(h or q positive is called a long position)

I how it works:

– you borrow q shares at the beginning of the period and sell them atprice p

– at the end of the period, you have to buy q shares at price p+ toreturn them to the lender

I all formulas still hold, e.g., profit = rh

I example: invest h = −$1000, r = −0.05: profit = +$50

I no limit to how much you can lose when you short assets

I normal people (and mutual funds) don’t do this; hedge funds do

Return and risk 4

Examples

prices of BP (BP) and Coca-Cola (KO) for last 10 years

0 500 1000 1500 2000 25000

10

20

30

40

50

60

70

Days

Price

s

KO

BP

Return and risk 5

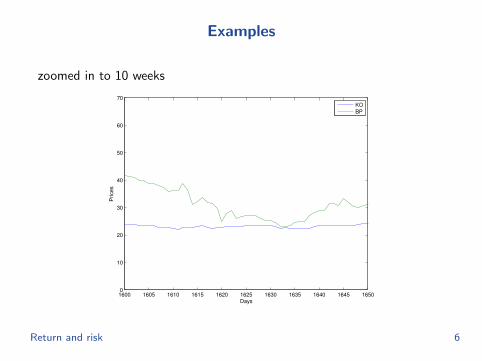

Examples

zoomed in to 10 weeks

1600 1605 1610 1615 1620 1625 1630 1635 1640 1645 16500

10

20

30

40

50

60

70

Days

Price

s

KO

BP

Return and risk 6

Examples

returns over the same period

1600 1605 1610 1615 1620 1625 1630 1635 1640 1645 1650−0.2

−0.15

−0.1

−0.05

0

0.05

0.1

0.15

0.2

Days

Re

turn

s

KO

BP

Return and risk 7

Return and risk

I suppose r is time series (vector) of returns

I average return or just return is avg(r)

I risk is std(r)

I these are the per-period return and risk

Return and risk 8

Annualized return and risk

I mean return and risk are often expressed in annualized form(i.e., per year)

I if there are P trading periods per year

– annualized return = P avg(r)– annualized risk =

√P std(r)

(the squareroot in risk annualization comes from the assumptionthat the fluctuations in return around the mean are independent)

I if returns are daily, with 250 trading days in a year

– annualized return = 250avg(r)– annualized risk =

√250 std(r)

Return and risk 9

Risk-return plot

I annualized risk versus annualized return of various assets

I up (high return) and left (low risk) is good

0 10 20 30 40 50 600

5

10

15

20

25

BRCM

GS

MMM

SBUX

USDOLLAR

Annualized Risk

Annualized R

etu

rn

Return and risk 10

Outline

Return and risk

Portfolio investment

Portfolio optimization

Portfolio investment 11

Portfolio of assets

I n assets

I n-vector ht is dollar value holdings of the assets

I total portfolio value: Vt = 1Tht (we assume positive)

I wt = (1/1Tht)ht gives portfolio weights or allocation(fraction of total portfolio value)

I 1Twt = 1

Portfolio investment 12

Examples

I (h3)5 = −1000 means you short asset 5 in investment period 3 by$1,000

I (w2)4 = 0.20 means 20% of total portfolio value in period 2 isinvested in asset 4

I wt = (1/n, . . . , 1/n), t = 1, . . . , T means total portfolio value isequally allocated across assets in all investment periods

Portfolio investment 13

Portfolio return and risk

I asset returns in period t given by n-vector r̃tI dollar profit (increase in value) over period t is r̃Tt ht = Vtr̃

Tt wt

I portfolio return (fractional increase) over period t is

Vt+1 − VtVt

=Vt(1 + r̃Tt wt)− Vt

Vt= r̃Tt wt

I rt = r̃Tt wt is called portfolio return in period t

I r is T -vector of portfolio returns

I avg(r) is portfolio return (over periods t = 1, . . . , T )

I std(r) is portfolio risk (over periods t = 1, . . . , T )

Portfolio investment 14

Compounding and re-investment

I VT+1 = V1(1 + r1)(1 + r2) · · · (1 + rT )

I product here is called compounding

I for |rt| small (say, ≤ 0.01) and T not too big,

VT+1 ≈ V1(1 + r1 + · · ·+ rT ) = V1(1 + T avg(r))

I so high average return corresponds to high final portfolio value

I Vt ≤ 0 (or some small value like 0.1V1) called going bust or ruin

Portfolio investment 15

Constant weight portfolio

I constant weight vector w, i.e., wt = w for t = 1, . . . , T

I requires rebalancing to weight w after each period

I define T × n asset returns matrix R with rows r̃TtI so Rtj is return of asset j in period t

I then r = Rw

Portfolio investment 16

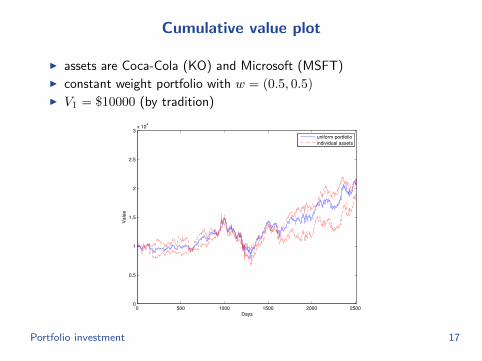

Cumulative value plot

I assets are Coca-Cola (KO) and Microsoft (MSFT)I constant weight portfolio with w = (0.5, 0.5)I V1 = $10000 (by tradition)

0 500 1000 1500 2000 25000

0.5

1

1.5

2

2.5

3x 10

4

Days

Valu

e

uniform portfolio

individual assets

Portfolio investment 17

Cumulative value plot

I w = (−3, 4)I portfolio goes bust (drops to 10% of starting value)

0 500 1000 1500 2000 25000

0.5

1

1.5

2

2.5

3x 10

4

Days

Valu

e

leveraged portfolio

individual assets

Portfolio investment 18

Outline

Return and risk

Portfolio investment

Portfolio optimization

Portfolio optimization 19

Portfolio optimization

I how should we choose the portfolio weight vector w?

I we want high (mean) portfolio return, low portfolio risk

I we know past realized asset returns but not future ones

I we will choose w that would have worked well on past returns

I . . . and hope it will work well going forward (just like data fitting)

Portfolio optimization 20

Portfolio optimization

minimize std(Rw)2 = (1/T )‖Rw − ρ1‖2

subject to 1Tw = 1, avg(Rw) = ρ

I w is the weight vector we seek

I R is the returns matrix for past returns

I Rw is the (past) portfolio return time series

I require mean (past) return ρ

I we minimize risk for specified value of return

I we are really asking what would have been the best constantallocation, had we known future returns

Portfolio optimization 21

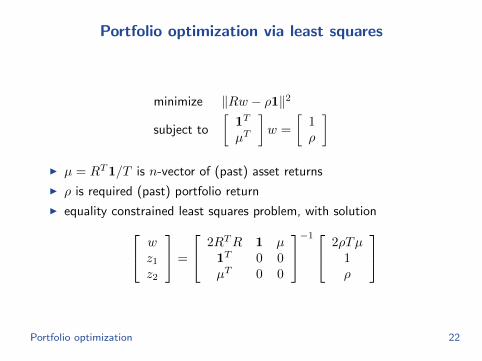

Portfolio optimization via least squares

minimize ‖Rw − ρ1‖2

subject to

[1T

µT

]w =

[1ρ

]I µ = RT1/T is n-vector of (past) asset returns

I ρ is required (past) portfolio return

I equality constrained least squares problem, with solution wz1z2

=

2RTR 1 µ1T 0 0µT 0 0

−1 2ρTµ1ρ

Portfolio optimization 22

Examples

I optimal w for annual return 1% (last asset is risk-less with 1%return)

w = (0.0000, 0.0000, 0.0000, . . . , 0.0000, 0.0000, 1.0000)

I optimal w for annual return 13%

w = (0.0250,−0.0715,−0.0454, . . . ,−0.0351, 0.0633, 0.5595)

I optimal w for annual return 25%

w = (0.0500,−0.1430,−0.0907, . . . ,−0.0703, 0.1265, 0.1191)

I asking for higher annual return yields

– more invested in risky, but high return assets– larger short positions (‘leveraging’)

Portfolio optimization 23

Cumulative value plots for optimal portfolios

cumulative value plot for optimal portfolios and some individual assets

0 500 1000 1500 2000 2500

104

105

Days

Va

lue

optimal portfolio, rho=0.20/250

optimal portfolio, rho=0.25/250

individual assets

Portfolio optimization 24

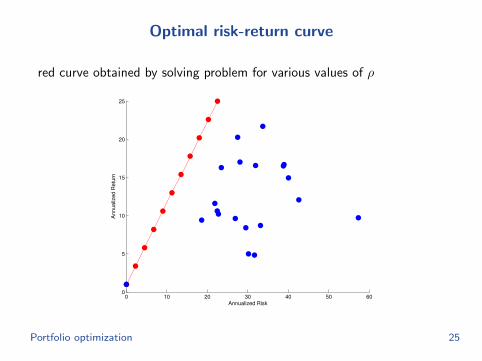

Optimal risk-return curve

red curve obtained by solving problem for various values of ρ

0 10 20 30 40 50 600

5

10

15

20

25

Annualized Risk

Annualized R

etu

rn

Portfolio optimization 25

Optimal portfolios

I perform significantly better than individual assets

I risk-return curve forms a straight line

– one end of the line is the risk-free asset

I two-fund theorem: optimal portfolio w is an affine function in ρ wz1z2

=

2RTR 1 µ1T 0 0µT 0 0

−1 RT11ρT

Portfolio optimization 26

The big assumption

I now we make the big assumption (BA):

future returns will look something like past ones

– you are warned this is false, every time you invest– it is often reasonably true– in periods of ‘market shift’ it’s much less true

I if BA holds (even approximately), then a good weight vector for past(realized) returns should be good for future (unknown) returns

I for example:

– choose w based on last 2 years of returns– then use w for next 6 months

Portfolio optimization 27

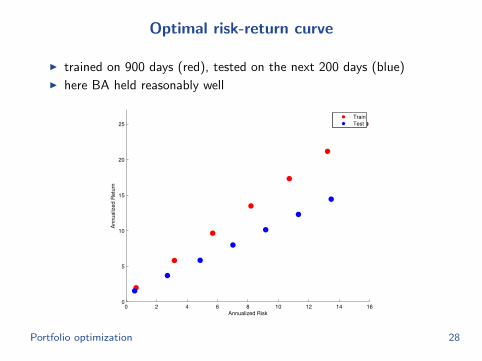

Optimal risk-return curve

I trained on 900 days (red), tested on the next 200 days (blue)I here BA held reasonably well

0 2 4 6 8 10 12 14 160

5

10

15

20

25

Annualized Risk

An

nu

alize

d R

etu

rn

Train

Test

Portfolio optimization 28

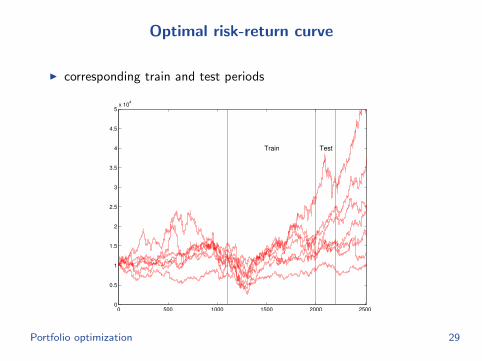

Optimal risk-return curve

I corresponding train and test periods

0 500 1000 1500 2000 25000

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5x 10

4

Train Test

Portfolio optimization 29

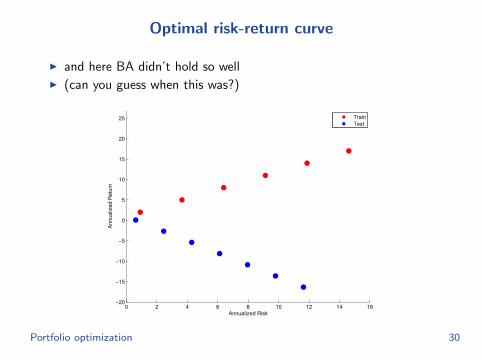

Optimal risk-return curve

I and here BA didn’t hold so wellI (can you guess when this was?)

0 2 4 6 8 10 12 14 16−20

−15

−10

−5

0

5

10

15

20

25

Annualized Risk

An

nu

alize

d R

etu

rn

Train

Test

Portfolio optimization 30

Optimal risk-return curve

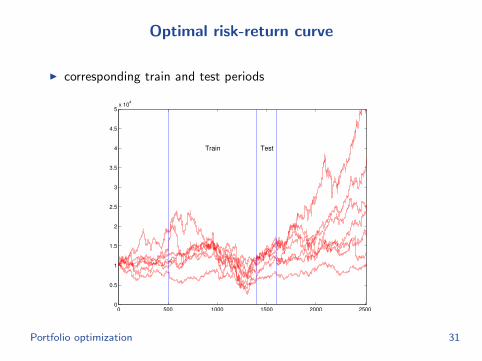

I corresponding train and test periods

0 500 1000 1500 2000 25000

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5x 10

4

Train Test

Portfolio optimization 31

Rolling portfolio optimization

for each period t, find weight wt using L past returns

rt−1, . . . , rt−L

variations:

I update w every K periods (say, monthly or quarterly)

I add cost term κ‖wt − wt−1‖2 to objective to discourage turnover,reduce transaction cost

I add logic to detect when the future is likely to not look like the past

I add ‘signals’ that predict future returns of assets

(. . . and pretty soon you have a quantitative hedge fund)

Portfolio optimization 32

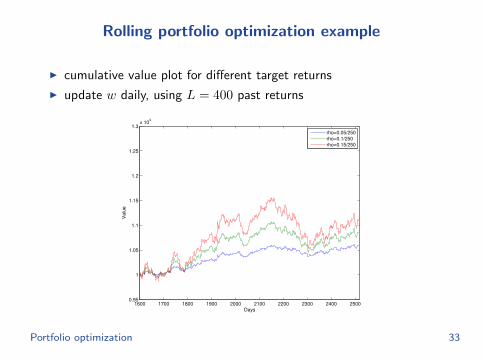

Rolling portfolio optimization example

I cumulative value plot for different target returns

I update w daily, using L = 400 past returns

1600 1700 1800 1900 2000 2100 2200 2300 2400 25000.95

1

1.05

1.1

1.15

1.2

1.25

1.3x 10

4

Days

Valu

e

rho=0.05/250

rho=0.1/250

rho=0.15/250

Portfolio optimization 33

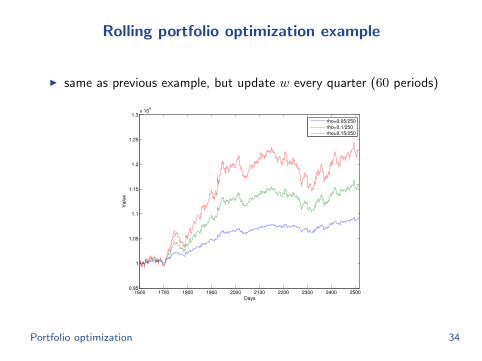

Rolling portfolio optimization example

I same as previous example, but update w every quarter (60 periods)

1600 1700 1800 1900 2000 2100 2200 2300 2400 25000.95

1

1.05

1.1

1.15

1.2

1.25

1.3x 10

4

Days

Valu

e

rho=0.05/250

rho=0.1/250

rho=0.15/250

Portfolio optimization 34