steven e. koonin chief scientist, bp...

TRANSCRIPT

Energy trends and technologies in the coming decadesSteven E. Koonin

Chief Scientist, BP plc

GUIRR

February 19, 2007

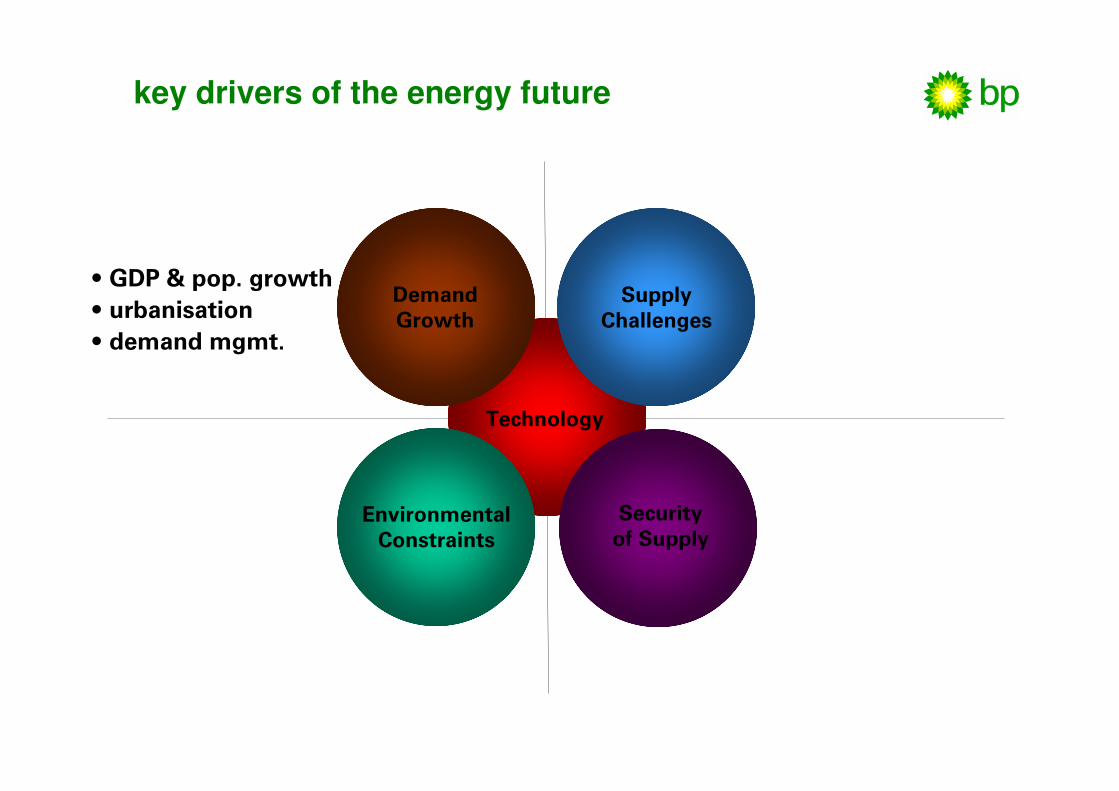

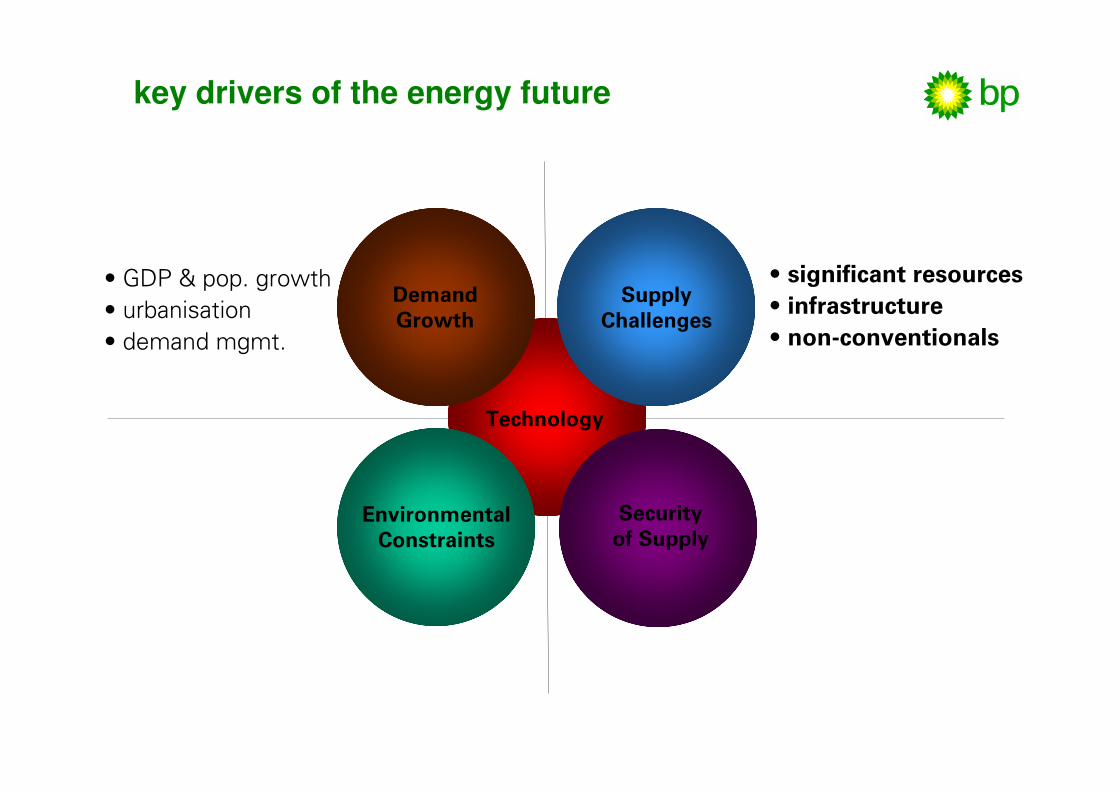

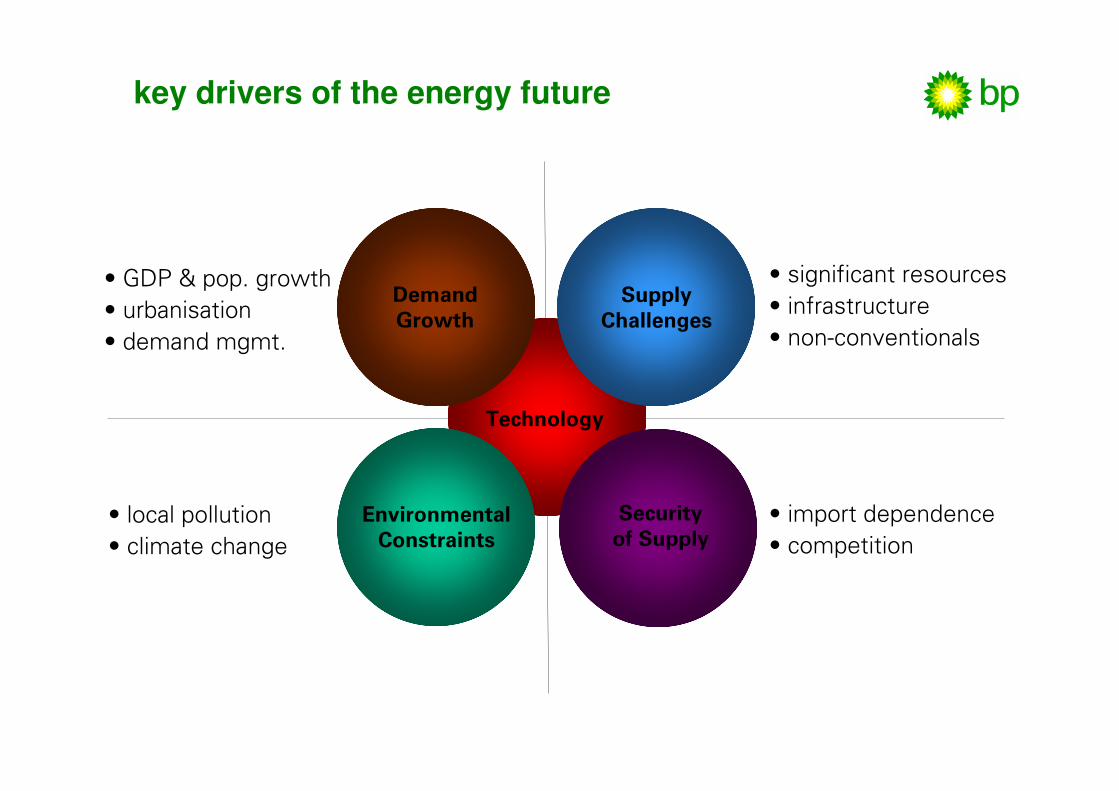

Technology

Demand Growth

• GDP & pop. growth

• urbanisation

• demand mgmt.

Security of Supply

Environmental Constraints

Supply Challenges

key drivers of the energy future

0

50

100

150

200

250

300

350

400

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

GDP per capita (PPP, $2000)

Prim

ary

Energ

y p

er capita (G

J)

Source:�UN�and�DOE�EIA

Russia�data�1992-2004�only

energy�use�grows�with�economic�development

US

Australia

Russia

BrazilChina

India

S.�Korea

Mexico

Ireland

Greece

France

UKJapan

Malaysia

energy demand and GDP per capita (1980-2004)

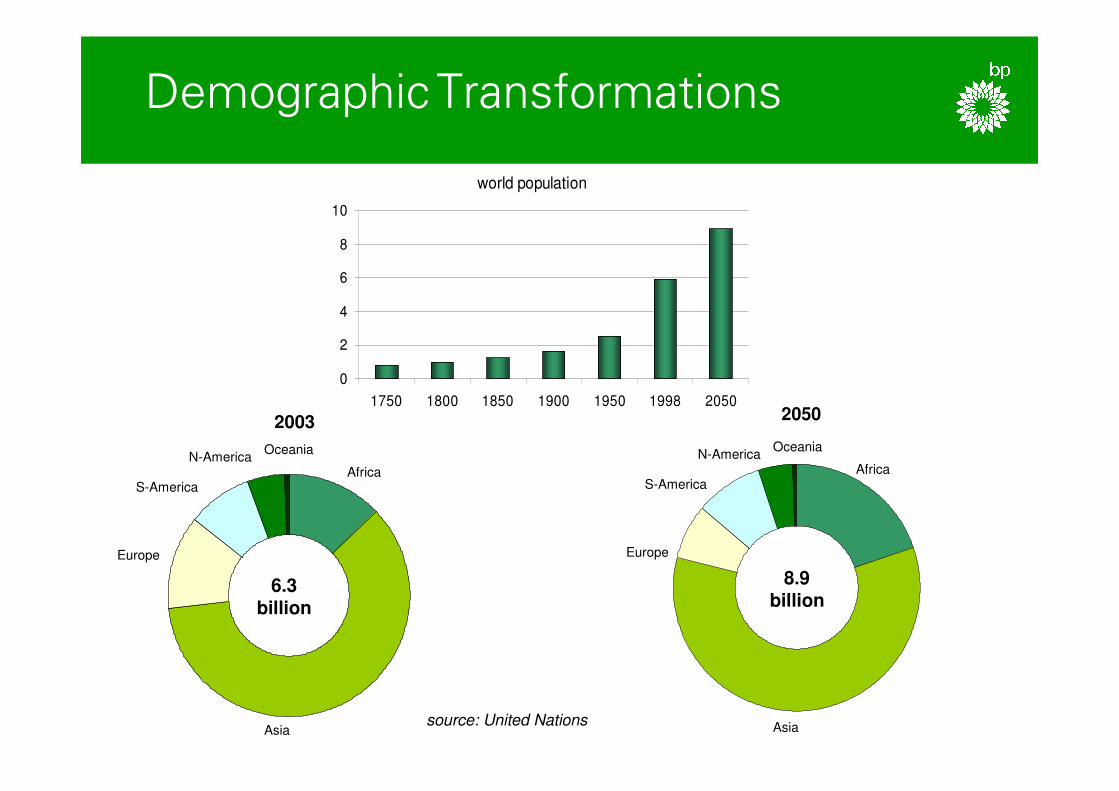

DemographicTransformations

world population

0

2

4

6

8

10

1750 1800 1850 1900 1950 1998 2050

2003 2050

source: United Nations

6.3billion

8.9billion

Oceania

AfricaN-America

S-America

Europe

Asia

Oceania

AfricaN-America

S-America

Europe

Asia

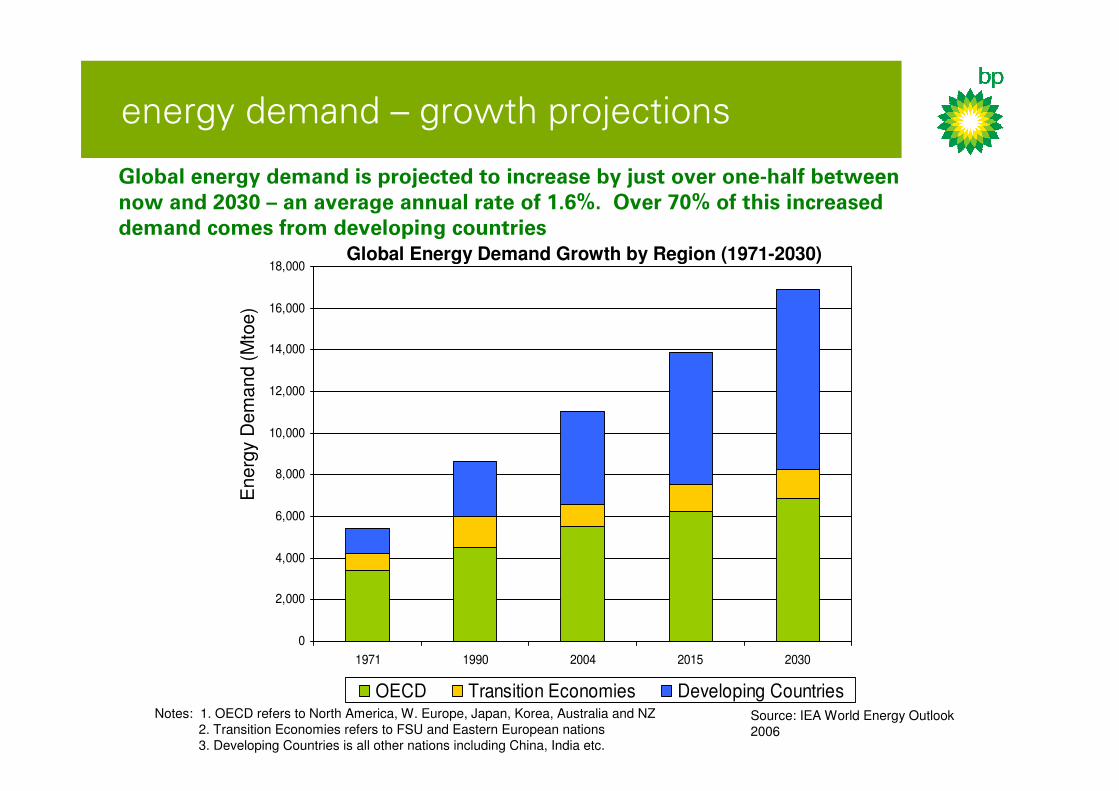

energy�demand�– growth�projections

Source: IEA World Energy Outlook 2006

Notes: 1. OECD refers to North America, W. Europe, Japan, Korea, Australia and NZ2. Transition Economies refers to FSU and Eastern European nations3. Developing Countries is all other nations including China, India etc.

Global Energy Demand Growth by Region (1971-2030)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1971 1990 2004 2015 2030

OECD Transition Economies Developing Countries

Energ

y D

em

and (

Mto

e)

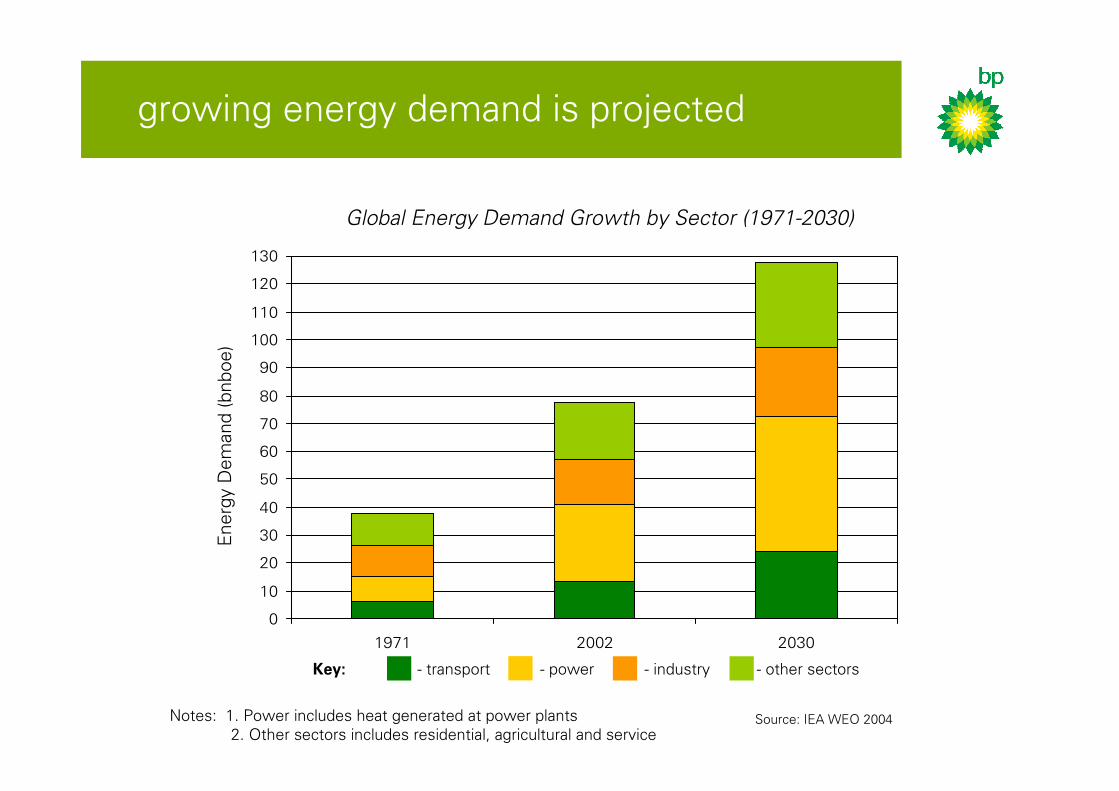

Global energy demand is projected to increase by just over one-half between now and 2030 – an average annual rate of 1.6%. Over 70% of this increased demand comes from developing countries

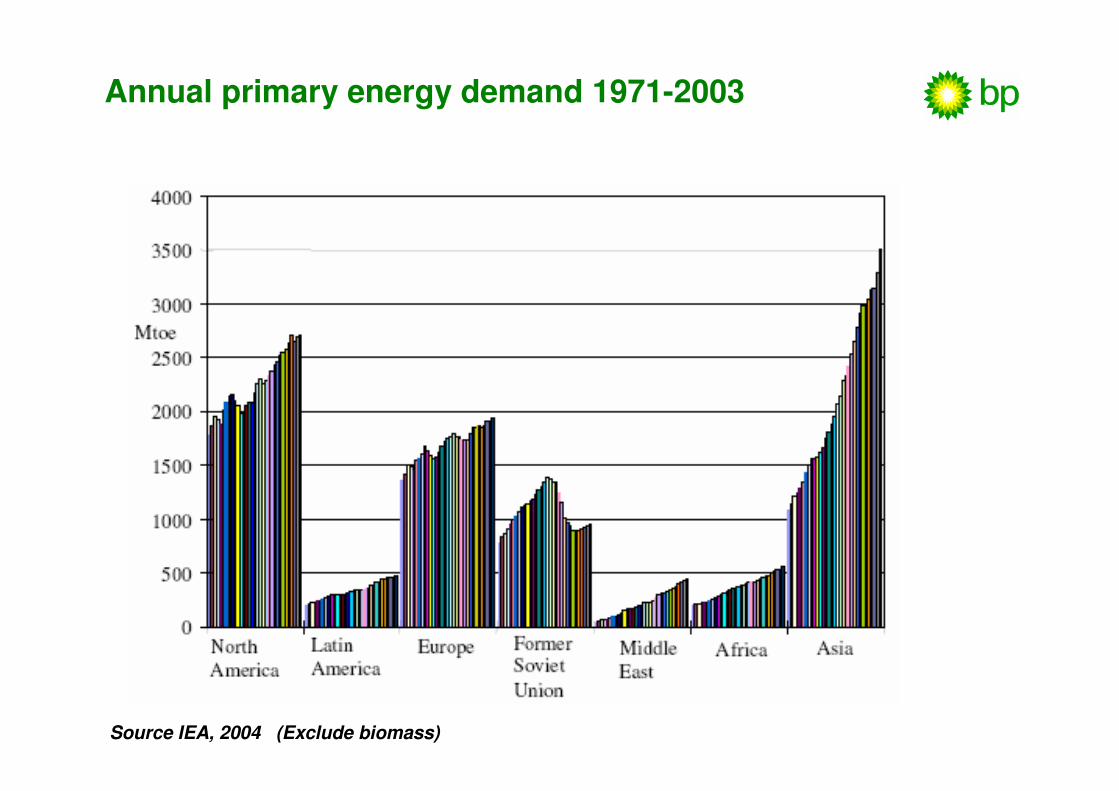

Annual primary energy demand 1971-2003

Source IEA, 2004 (Exclude biomass)

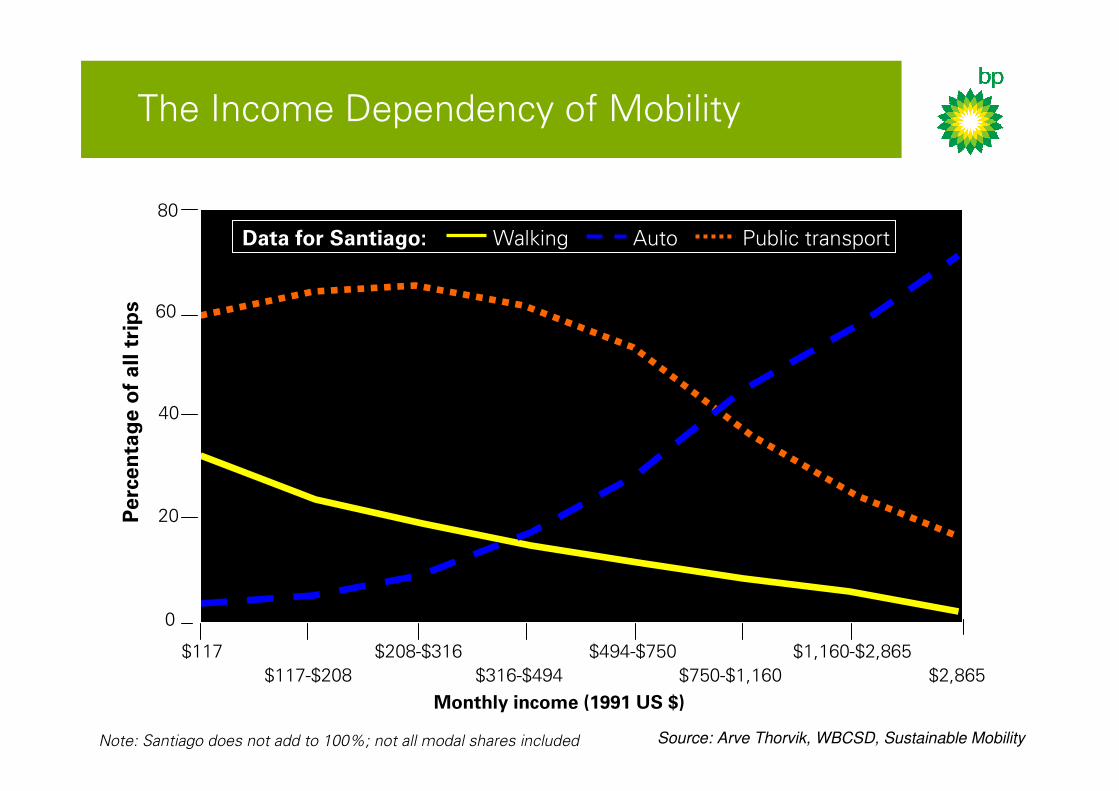

The�Income�Dependency�of�Mobility

Walking Auto Public�transport

$117

$117-$208

$208-$316

$316-$494

$494-$750

$750-$1,160

$1,160-$2,865

$2,865

Monthly income (1991 US $)

0

20

40

60

80

Perc

enta

ge o

f all t

rips

Note: Santiago does not add to 100%; not all modal shares included

Data for Santiago:

Source: Arve Thorvik, WBCSD, Sustainable Mobility

0

10

20

30

40

50

60

70

80

90

100

110

120

130

1971 2002 2030

Source:�IEA�WEO�2004Notes:��1.�Power�includes�heat�generated�at�power�plants

2.�Other�sectors�includes�residential,�agricultural�and�service

Global Energy Demand Growth by Sector (1971-2030)E

nerg

y�D

em

and�(bnboe)

growing�energy�demand�is�projected

Key: - industry- transport - power - other�sectors

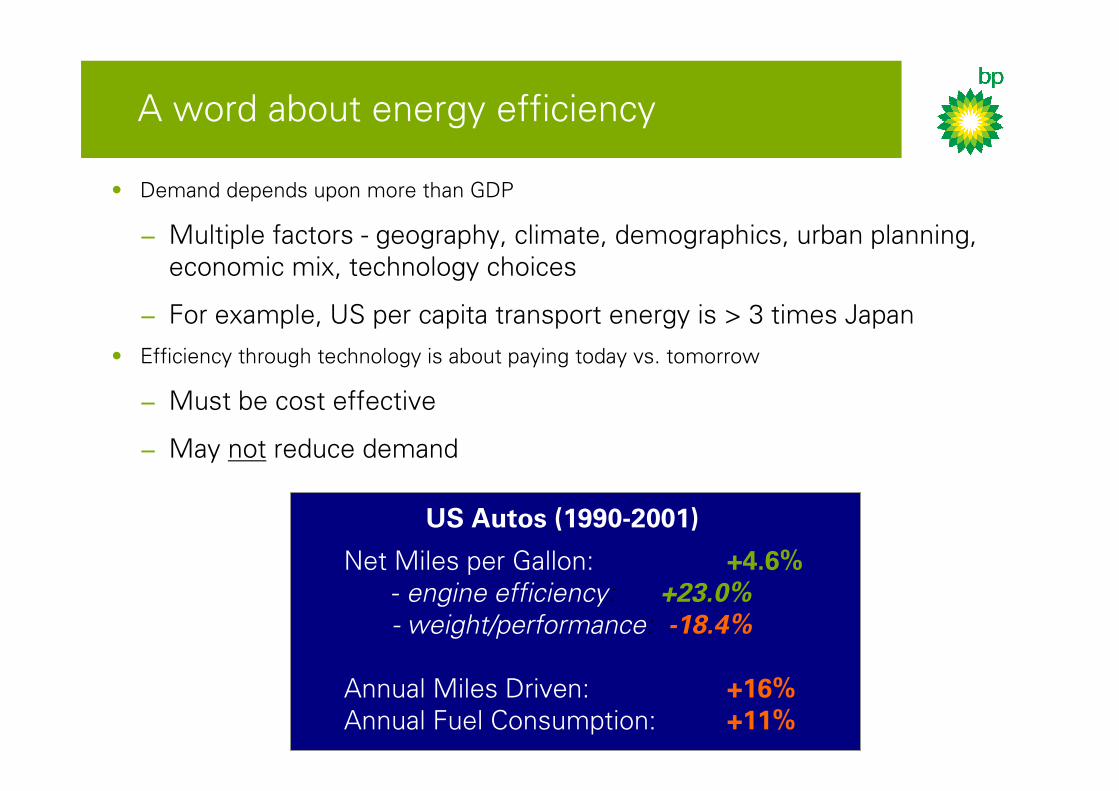

A�word�about�energy�efficiency

• Demand�depends�upon�more�than�GDP

− Multiple�factors�- geography,�climate,�demographics,�urban�planning,�

economic�mix,�technology�choices

− For�example,�US�per�capita�transport�energy�is�>�3�times�Japan�

• Efficiency�through�technology�is�about�paying�today�vs.�tomorrow

− Must�be�cost�effective

− May�not reduce�demand

US Autos (1990-2001)

Net�Miles�per�Gallon:� +4.6%- engine efficiency: +23.0%

- weight/performance: -18.4%

Annual�Miles�Driven:� +16%Annual�Fuel�Consumption: +11%

Technology

Demand Growth

• GDP�&�pop.�growth

• urbanisation

• demand�mgmt.

Security of Supply

Environmental Constraints

Supply Challenges

• significant resources

• infrastructure

• non-conventionals

key drivers of the energy future

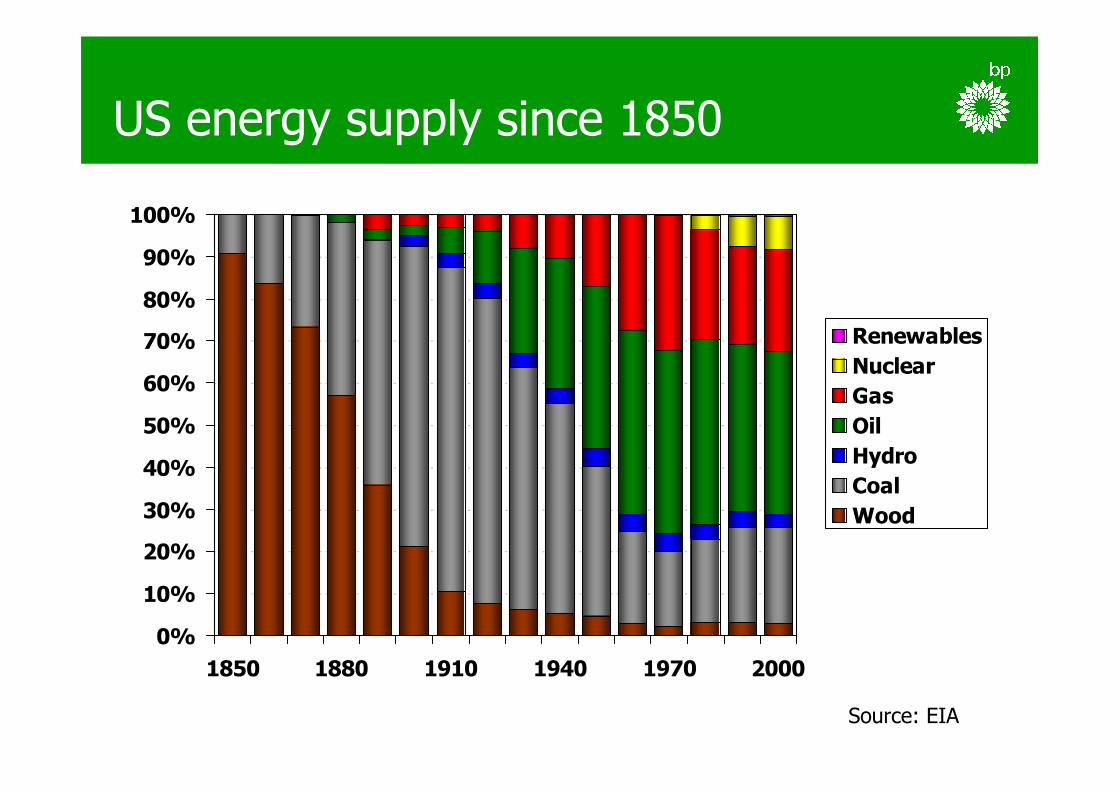

US energy supply since 1850

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1850 1880 1910 1940 1970 2000

Renewables

Nuclear

Gas

Oil

Hydro

Coal

Wood

Source: EIA

2002�US�energy�(Net�primary�consumption�=�103�Exajoules)

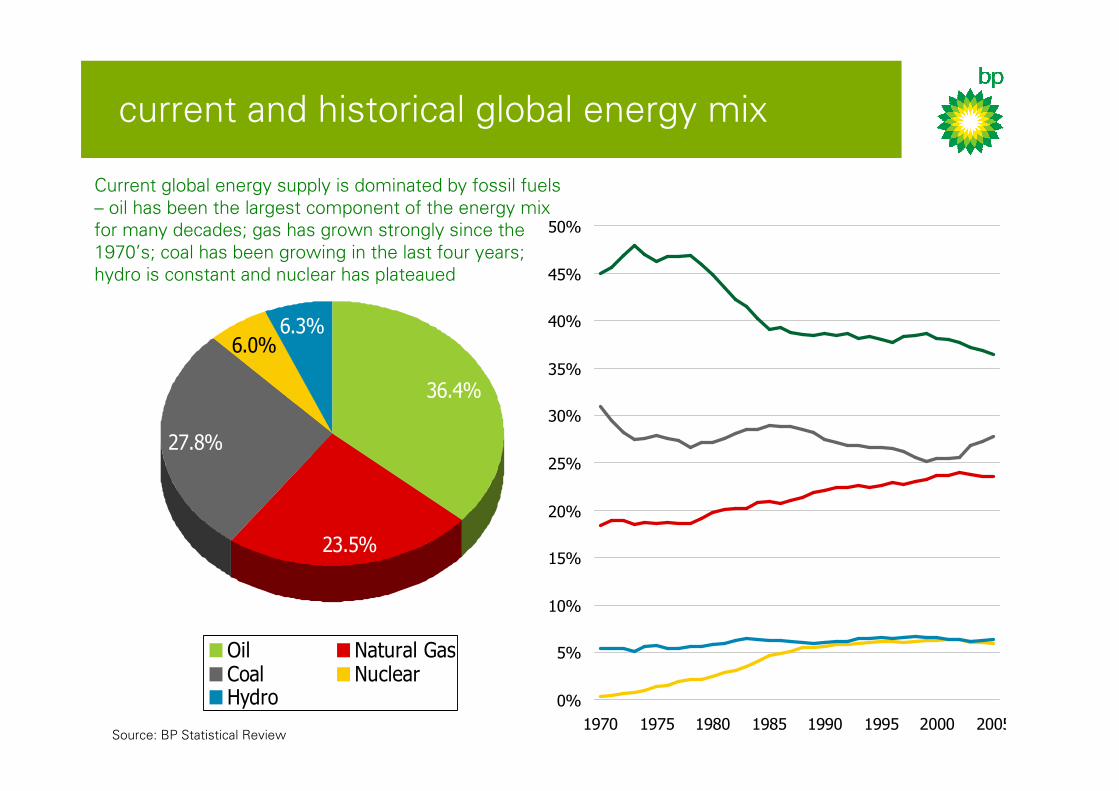

current�and�historical�global�energy�mix

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1970 1975 1980 1985 1990 1995 2000 2005

36.4%

23.5%

27.8%

6.3%6.0%

Oil Natural GasCoal NuclearHydro

Source:�BP�Statistical�Review

Current�global�energy�supply�is�dominated�by�fossil�fuels�

– oil�has�been�the�largest�component�of�the�energy�mix�

for�many�decades;�gas�has�grown�strongly�since�the�

1970’s;�coal�has�been�growing�in�the�last�four�years;�

hydro�is�constant�and�nuclear�has�plateaued

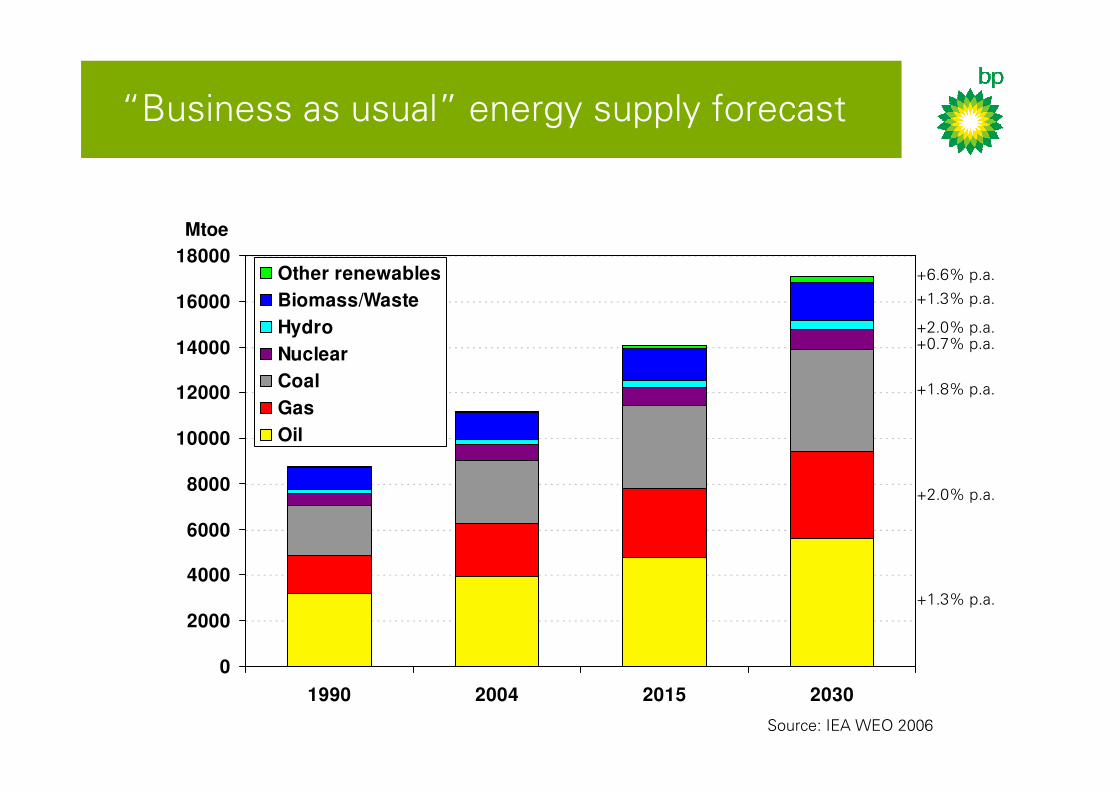

“Business�as�usual” energy�supply�forecast

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

1990 2004 2015 2030

Other renewables

Biomass/Waste

Hydro

Nuclear

Coal

Gas

Oil

Mtoe

Source:�IEA�WEO�2006

+1.3%�p.a.

+2.0%�p.a.

+1.8%�p.a.

+0.7%�p.a.+2.0%�p.a.

+1.3%�p.a.

+6.6%�p.a.

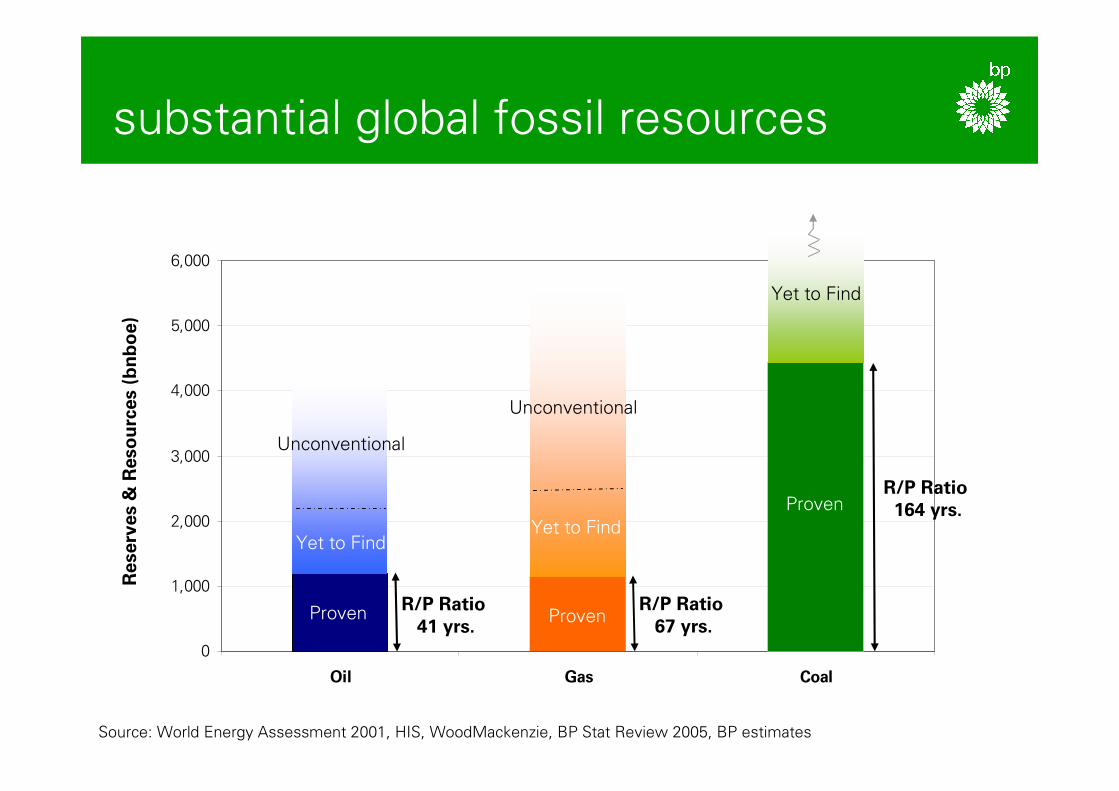

0

1,000

2,000

3,000

4,000

5,000

6,000

Oil Gas Coal

substantial�global�fossil�resources

R/P Ratio 41 yrs.

R/P Ratio 67 yrs.

R/P Ratio 164 yrs.

Proven Proven

Proven

Yet�to�FindYet�to�Find

Yet�to�Find

Source:�World�Energy�Assessment�2001,�HIS,�WoodMackenzie,�BP�Stat�Review�2005,�BP�estimates

Unconventional

Unconventional

Reserv

es &

Resourc

es (bnboe)

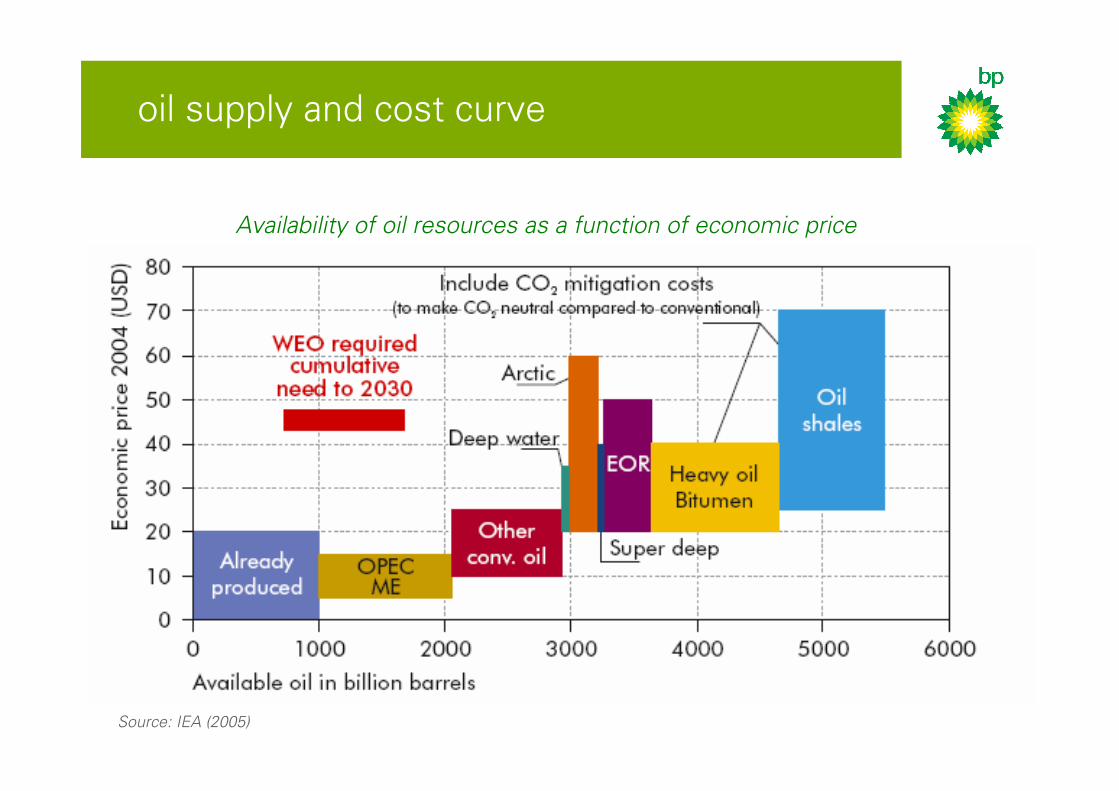

oil�supply�and�cost�curve

Availability of oil resources as a function of economic price

Source: IEA (2005)

Technology

Demand Growth

• GDP�&�pop.�growth

• urbanisation

• demand�mgmt.

Security of Supply

• import dependence

• competition

Environmental Constraints

Supply Challenges

• significant�resources

• infrastructure

• non-conventionals

key�drivers�of�the�energy�future

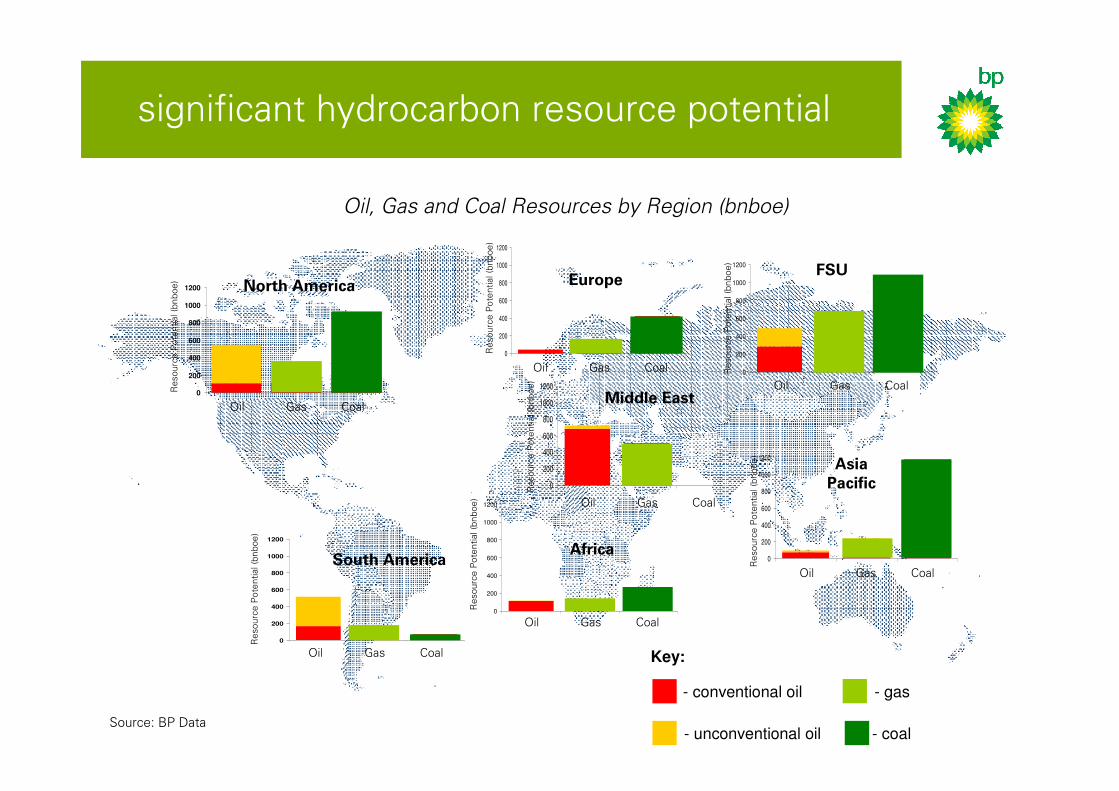

Source:�BP�Data

significant�hydrocarbon�resource�potential

0

200

400

600

800

1000

1200

South America

0

200

400

600

800

1000

1200 North America

Oil Gas Coal

Oil Gas Coal

Resourc

e�P

ote

ntial�(b

nboe

)

0

200

400

600

800

1000

1200

Africa

Oil Gas Coal

Resourc

e�P

ote

ntial�(b

nboe

)

Resourc

e�P

ote

ntial�(b

nboe

)

0

200

400

600

800

1000

1200FSU

Oil Gas Coal

Resourc

e�P

ote

ntial�(b

nboe

)

Gas Europe

0

200

400

600

800

1000

1200

Resourc

e�P

ote

ntial�(b

nboe

)

Oil Gas Coal

0

200

400

600

800

1000

1200

Middle East

Oil Gas Coal

Resourc

e�P

ote

ntial�(b

nboe

)

0

200

400

600

800

1000

1200Asia

Pacific

Oil Gas Coal

Resourc

e�P

ote

ntial�(b

nboe

)

Key:

- unconventional oil

- conventional oil - gas

- coal

Oil, Gas and Coal Resources by Region (bnboe)

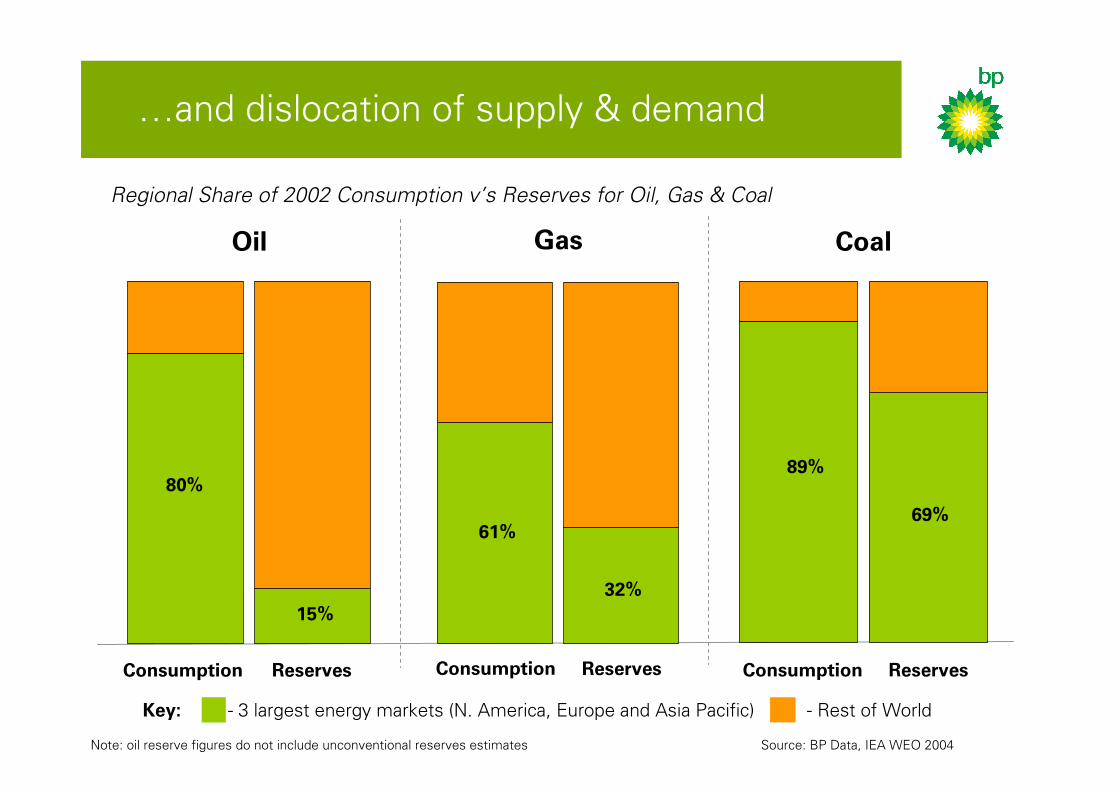

…and�dislocation�of�supply�&�demand

Regional Share of 2002 Consumption v’s Reserves for Oil, Gas & Coal

- Rest�of�World- 3�largest�energy�markets�(N.�America,�Europe�and�Asia�Pacific)Key:

Note:�oil�reserve�figures�do�not�include�unconventional�reserves estimates�� Source:�BP�Data,�IEA�WEO�2004

Oil

80%

15%

Consumption Reserves

Gas

61%

32%

Consumption Reserves

Coal

89%

69%

Consumption Reserves

energy�security�- import�dependence

-20

-15

-10

-5

0

5

10

15

1991 1993 1995 1997 1999 2001 2003

US

Iraq

ME�OPEC�(excl�Iraq)

Other�Dev.�

China

FSU

Importers

Exporters -150

-100

-50

0

50

100

150

200

250

1993 1995 1997 1999 2001 2003

EU

US

Asian�LNG(Japan,�Korea�Taiwan)

Russia�ex�FSU

Other�Europe�pipeline

�Pacific/ME�LNG

Canada

Atlantic�LNG

Importers

Exporters

bcmMb/dOil Natural gas

Import dependence is rising in all the key markets; oil and gas production is also shifting increasingly away from OECD countries to non-OECD

Technology

Demand Growth

• GDP�&�pop.�growth

• urbanisation

• demand�mgmt.

Security of Supply

• import�dependence

• competition

Environmental Constraints

• local pollution

• climate change

Supply Challenges

• significant�resources

• infrastructure

• non-conventionals

key drivers of the energy future

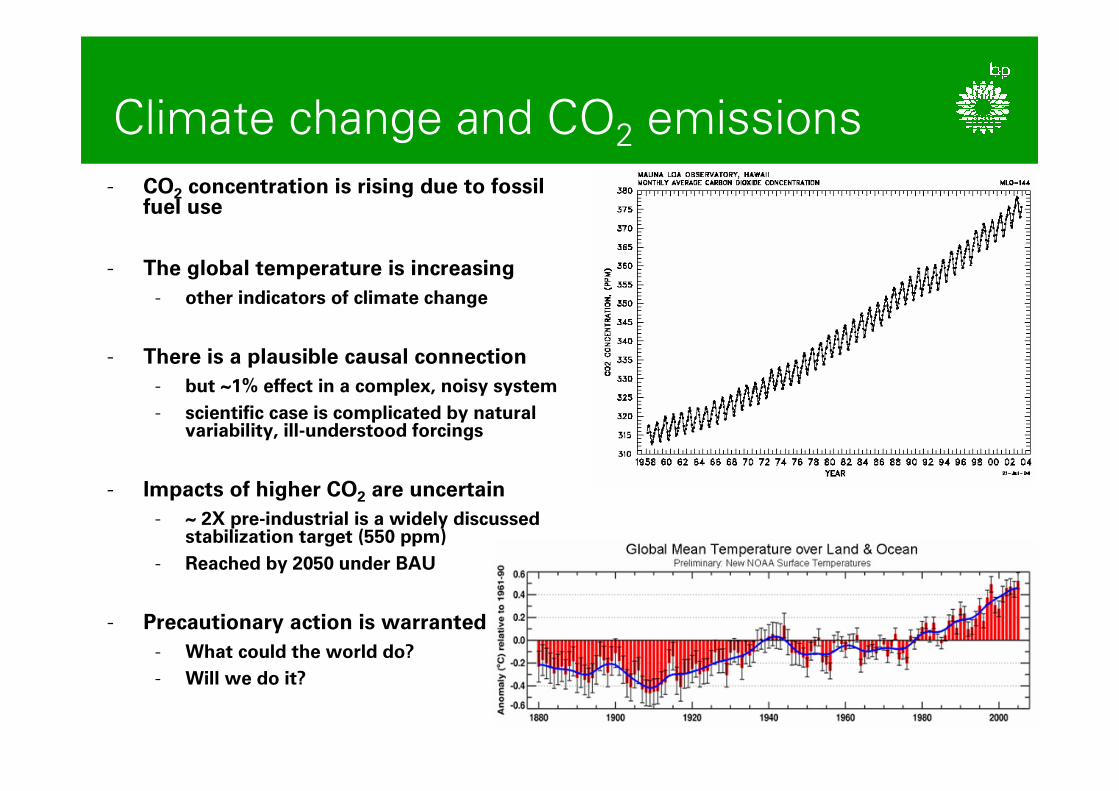

Climate�change�and�CO2 emissions

- CO2 concentration is rising due to fossil fuel use

- The global temperature is increasing

- other indicators of climate change

- There is a plausible causal connection

- but ~1% effect in a complex, noisy system

- scientific case is complicated by natural variability, ill-understood forcings

- Impacts of higher CO2 are uncertain

- ~ 2X pre-industrial is a widely discussed stabilization target (550 ppm)

- Reached by 2050 under BAU

- Precautionary action is warranted

- What could the world do?

- Will we do it?

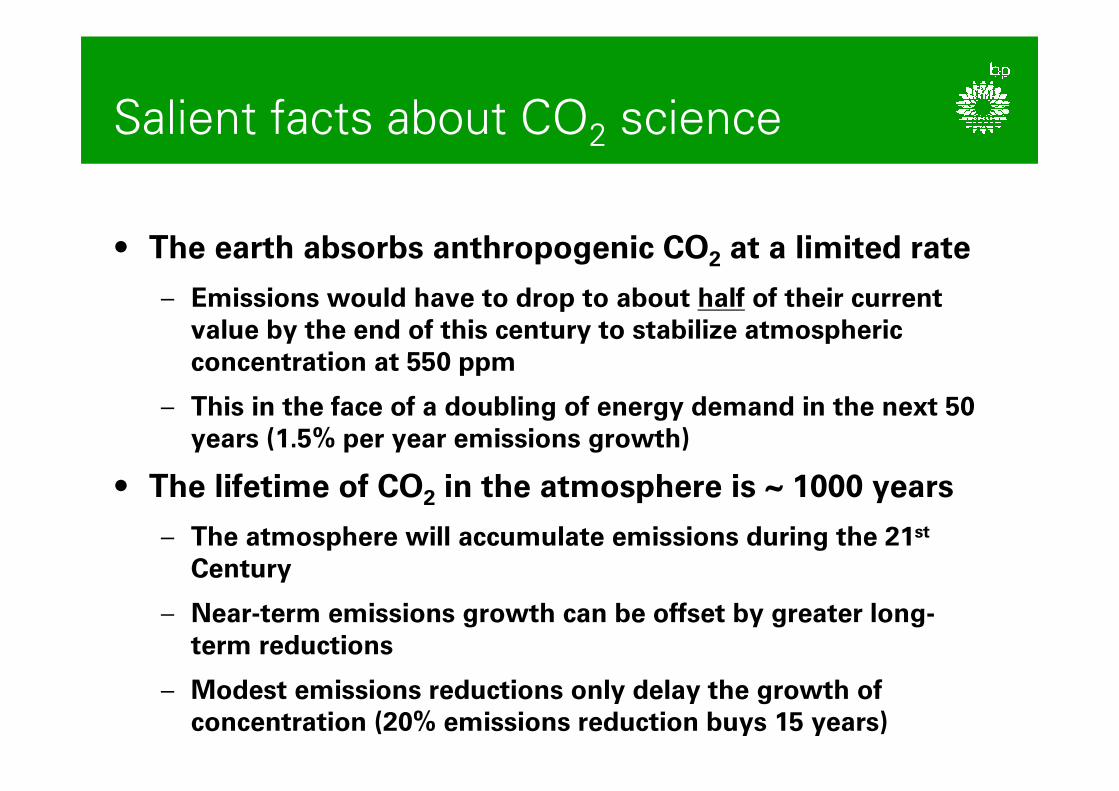

Salient�facts�about�CO2 science

• The earth absorbs anthropogenic CO2 at a limited rate

– Emissions would have to drop to about half of their current value by the end of this century to stabilize atmospheric concentration at 550 ppm

– This in the face of a doubling of energy demand in the next 50 years (1.5% per year emissions growth)

• The lifetime of CO2 in the atmosphere is ~ 1000 years

– The atmosphere will accumulate emissions during the 21st

Century

– Near-term emissions growth can be offset by greater long-term reductions

– Modest emissions reductions only delay the growth of concentration (20% emissions reduction buys 15 years)

Some�stabilization�scenarios

Emissions Concentration

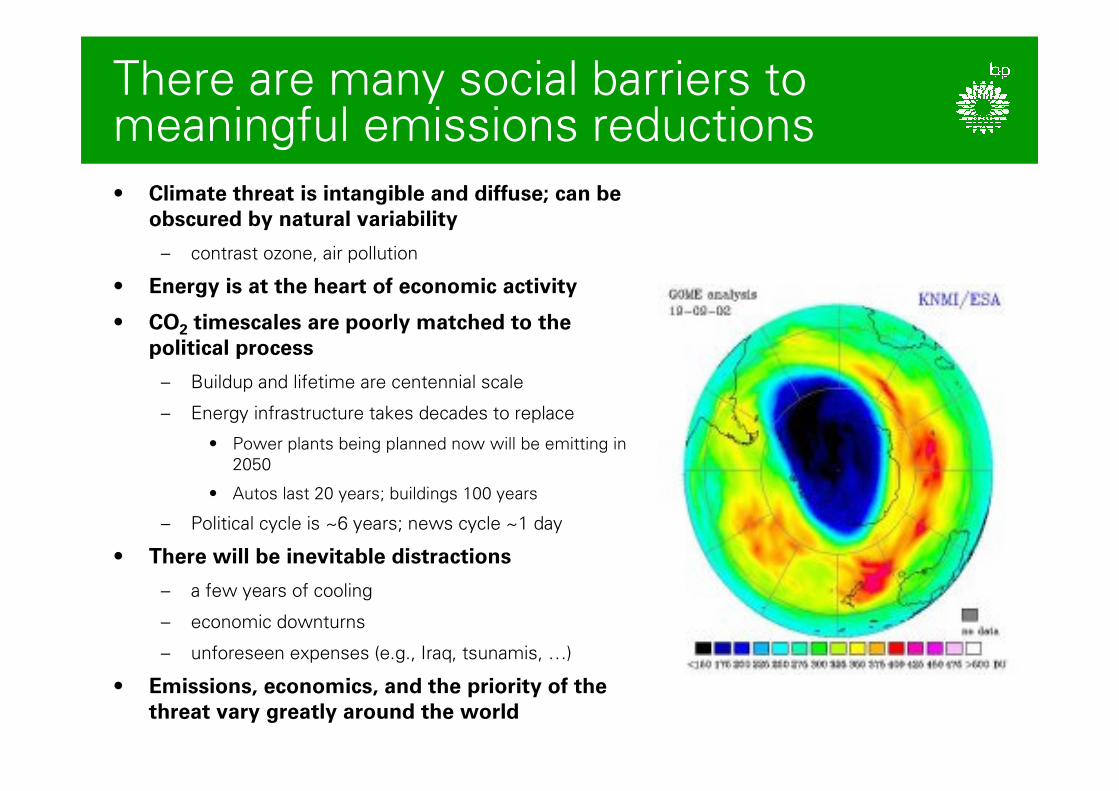

There�are�many�social�barriers�to�meaningful�emissions�reductions

• Climate threat is intangible and diffuse; can be obscured by natural variability

– contrast�ozone,�air�pollution

• Energy is at the heart of economic activity

• CO2 timescales are poorly matched to the political process

– Buildup and�lifetime�are�centennial�scale

– Energy�infrastructure�takes�decades�to�replace

• Power�plants�being�planned�now�will�be�emitting�in�

2050

• Autos�last�20�years;�buildings�100�years

– Political�cycle�is�~6�years;�news�cycle�~1�day

• There will be inevitable distractions

– a�few�years�of�cooling

– economic�downturns

– unforeseen�expenses�(e.g.,�Iraq,�tsunamis,�…)

• Emissions, economics, and the priority of the threat vary greatly around the world

0

5

10

15

20

25

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

GDP per capita (PPP, $2000)

CO

2 e

mis

sio

ns p

er capita (tC

O 2)

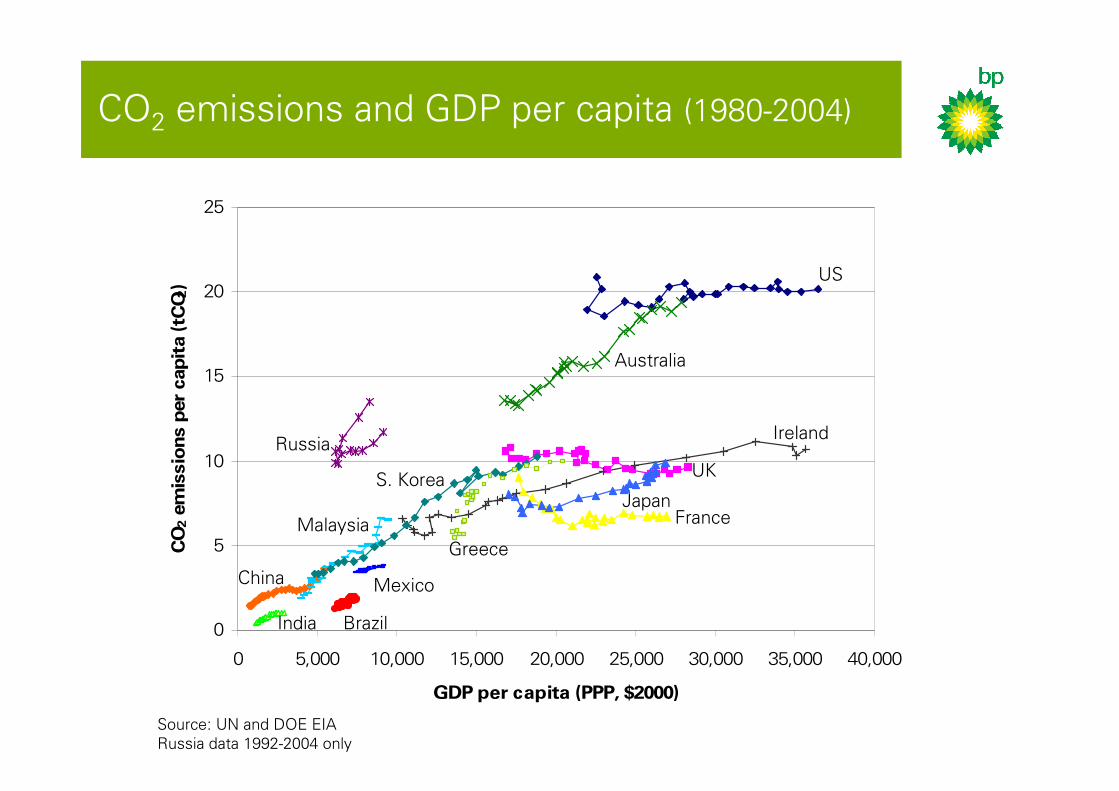

CO2 emissions�and�GDP�per�capita�(1980-2004)

US

Australia

Russia

Brazil

China

India

S.�Korea

Mexico

Ireland

Greece

France

UK

Japan

Malaysia

Source:�UN�and�DOE�EIA

Russia�data�1992-2004�only

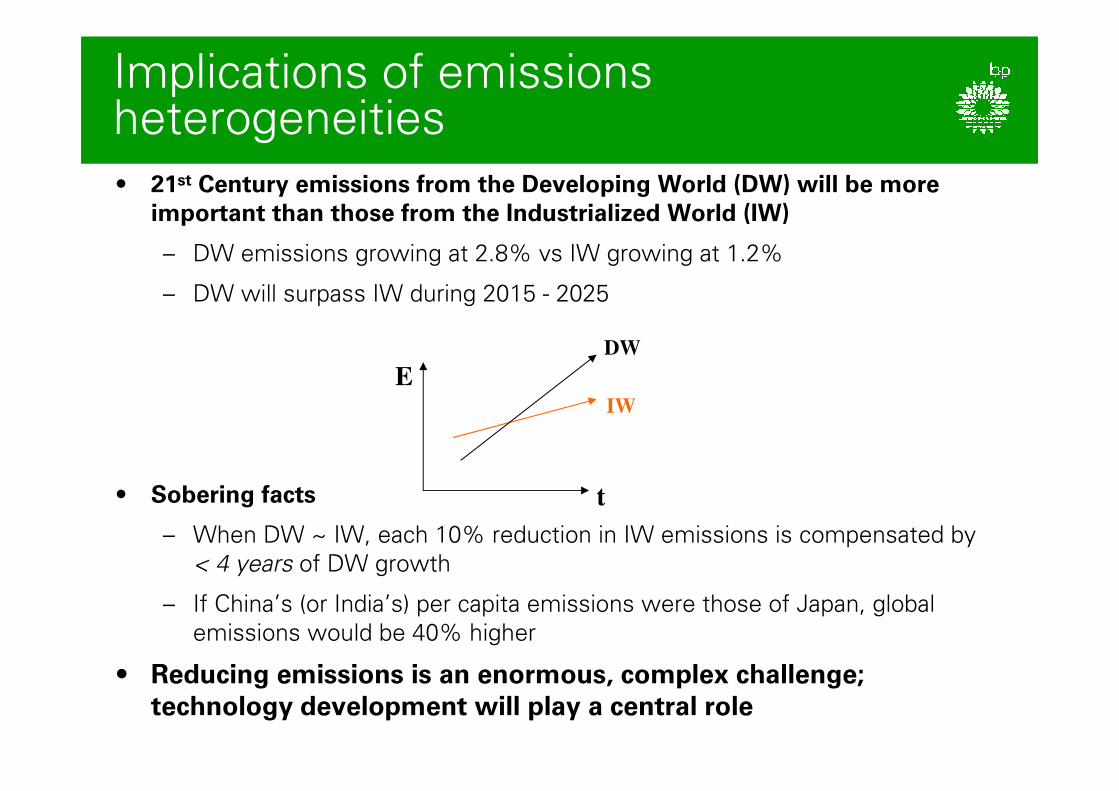

Implications�of�emissions�heterogeneities

• 21st Century emissions from the Developing World (DW) will be more important than those from the Industrialized World (IW)

– DW�emissions�growing�at�2.8%�vs IW�growing�at�1.2%

– DW�will�surpass�IW�during�2015�- 2025

• Sobering facts

– When�DW�~�IW,�each�10%�reduction�in�IW�emissions�is�compensated�by�

< 4 years of�DW�growth

– If�China’s�(or�India’s)�per�capita�emissions�were�those�of�Japan,�global�

emissions�would�be�40%�higher

• Reducing emissions is an enormous, complex challenge; technology development will play a central role

t

E

DW

IW

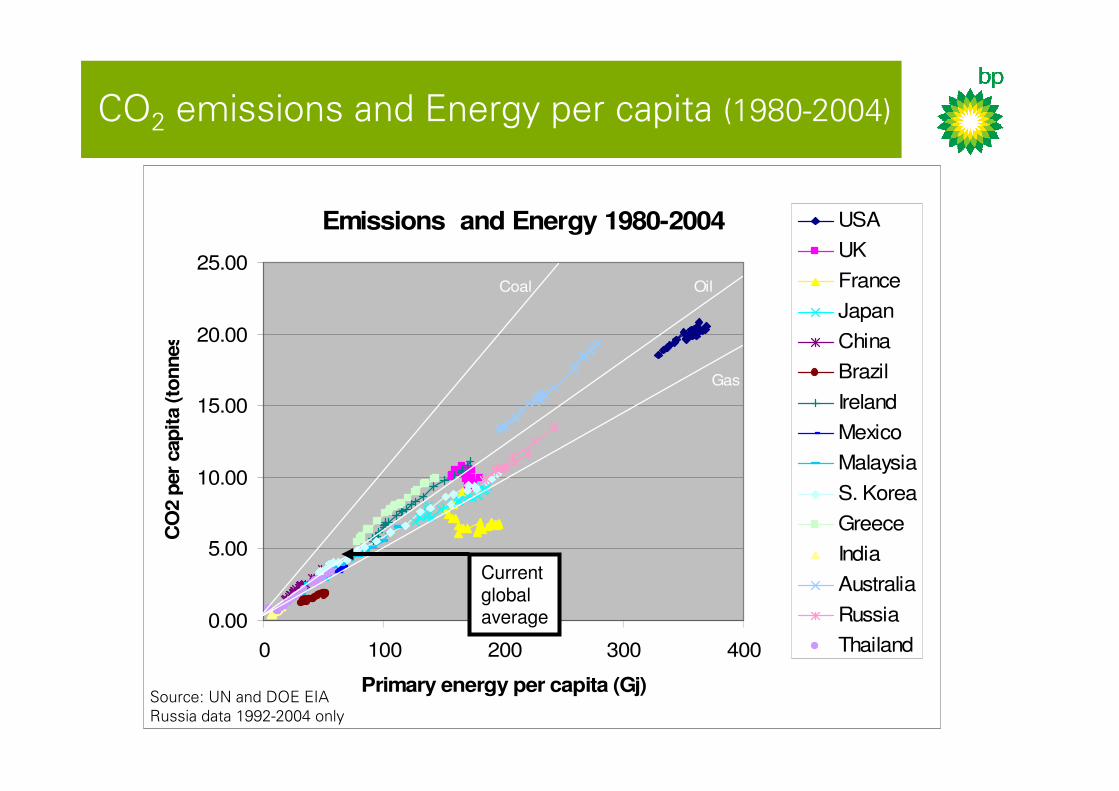

Emissions and Energy 1980-2004

0.00

5.00

10.00

15.00

20.00

25.00

0 100 200 300 400

Primary energy per capita (Gj)

CO

2 p

er

capit

a (

tonnes)

USA

UK

France

Japan

China

Brazil

Ireland

Mexico

Malaysia

S. Korea

Greece

India

Australia

Russia

Thailand

Coal Oil

Gas

Current global average

CO2 emissions�and�Energy�per�capita�(1980-2004)

Source:�UN�and�DOE�EIA

Russia�data�1992-2004�only

Technology

Demand Growth

• GDP�&�pop.�growth

• urbanisation

• demand�mgmt.

Security of Supply

• import�dependence

• competition

Environmental Constraints

• local�pollution

• climate�change

Supply Challenges

• significant�resources

• infrastructure

• non-conventionals

key drivers of the energy future

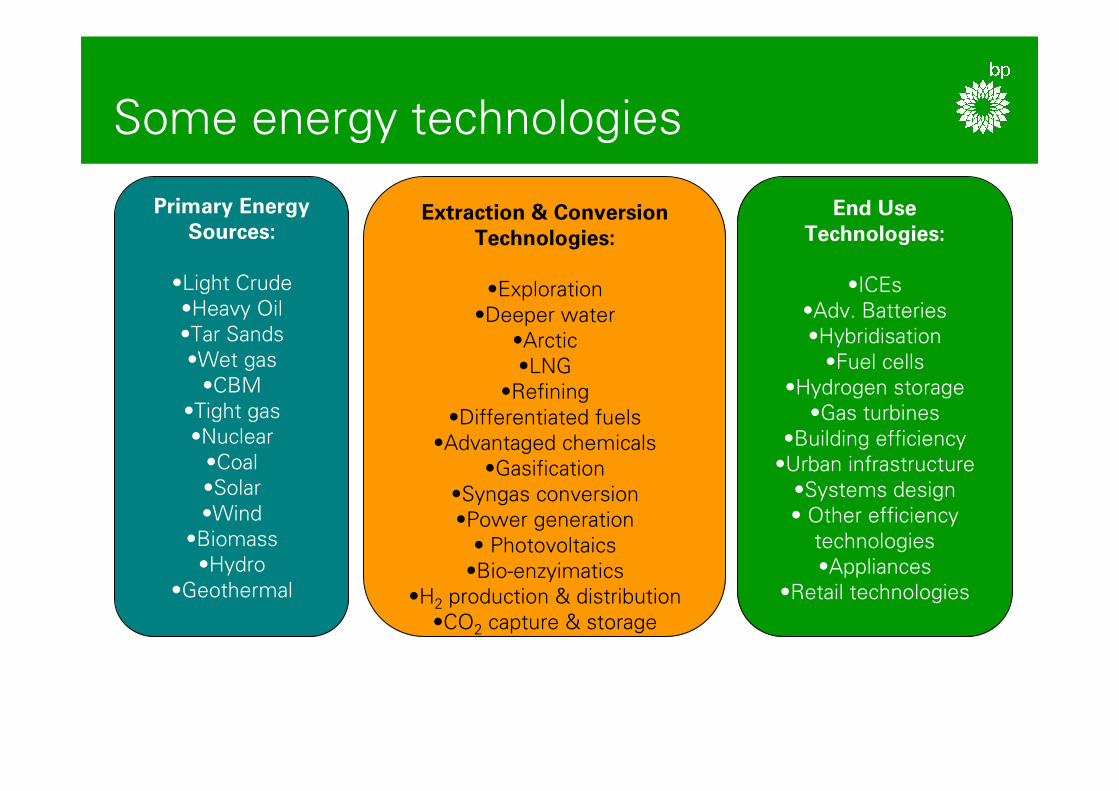

Some�energy�technologies

Primary Energy Sources:

•Light�Crude

•Heavy�Oil

•Tar�Sands

•Wet�gas

•CBM

•Tight�gas

•Nuclear

•Coal

•Solar

•Wind

•Biomass

•Hydro

•Geothermal

Extraction & Conversion Technologies:

•Exploration

•Deeper�water

•Arctic

•LNG

•Refining

•Differentiated�fuels

•Advantaged�chemicals

•Gasification

•Syngas�conversion

•Power�generation

• Photovoltaics

•Bio-enzyimatics

•H2 production�&�distribution

•CO2 capture�&�storage

End Use Technologies:

•ICEs

•Adv.�Batteries

•Hybridisation

•Fuel�cells

•Hydrogen�storage

•Gas�turbines

•Building�efficiency

•Urban�infrastructure

•Systems�design

• Other�efficiency�

technologies

•Appliances

•Retail�technologies

evaluating�energy�technology�options

• Current�technology status and�plausible�technical headroom

• Budgets for�the�three�E’s:

− Economic (cost�relative�to�other�options)

− Energy (output�how�many�times�greater�than�input)

− Emissions (pollution�and�CO2;�operations�and�capital)

• Materiality (at�least�1TW�=�5%�of�2050�BAU�energy�demand)

• Other costs - reliability,�intermittency�etc.

• Social�and�political�acceptability

But we also must know what problem we are trying to solve

Concern relating to Threat of Climate Change

Concern

over

Futu

re

Availabilit

y o

f O

il a

nd G

as

High

High

Low

Low

Adv. Biofuels

Carbon Free H2 for

Transport

CTL

GTL

Heavy Oil

EnhancedRecovery

Ultra Deep Water

Arctic

Capture�&�

Storage

Capture�&�

Storage

CNG

Hybrids

C&S

Vehicle Efficiency (e.g. light

weighting)

- supply�side�options

- demand�side�options

Key:Dieselisation

Conv. Biofuels

two�key�energy�considerations�– security�&�climate

The�fungibility of�carbon

Primary Energy Conversion Technology Products

Reforming

Coal

Natural�

Gas

Biomass

Extra�

Heavy�

Oil

Markets

SyngasConversion

- FT

- Oxygenates

- Chemicals

Gasification

Enzymatic/Biological�Conversion

PowerGeneration

Electricity

Fuels

Chemicals

Refining Processes- coking

- hydro-treating

- novel�thermal�processes

CO2 Capture

CO2 for EOR/Storage

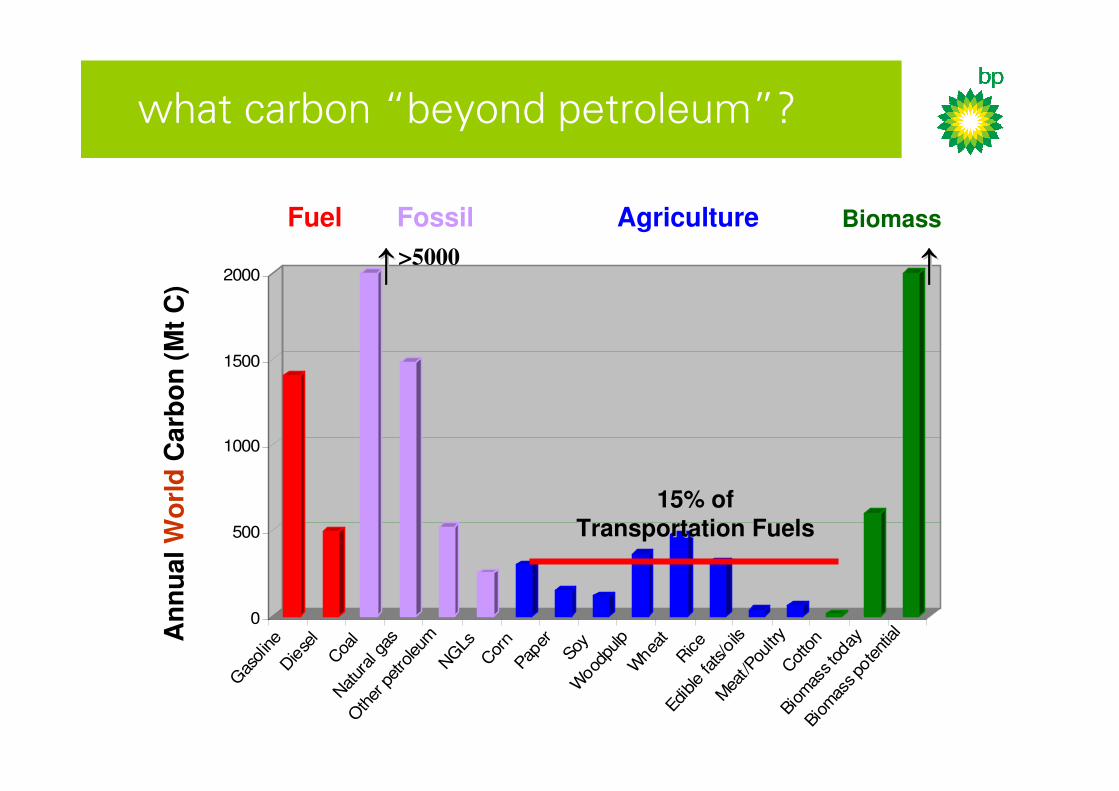

what�carbon�“beyond�petroleum”?

Fuel Fossil Agriculture Biomass

0

100

200

300

400

500

600

700G

asol

ine

Die

sel

Coa

lNat

ural

gas

Oth

er p

etro

leum

NG

LsCor

nPap

er

SoyW

oodpu

lpW

heat

Edible fa

ts/o

ilsM

eat/P

oultr

yCot

ton

Biom

ass to

day

Biom

ass po

tent

ial

An

nu

al U

S C

arb

on

(M

t C

)

↑↑

15% of 15% of

Transportation FuelsTransportation Fuels

what�carbon�“beyond�petroleum”?

Fuel Fossil Agriculture Biomass

0

500

1000

1500

2000

Gas

oline

Diese

lCoa

lNat

ural g

as

Other

petro

leum

NG

LsCor

nPa

per

Soy

Woo

dpulp

Whe

atRice

Edible fa

ts/o

ilsMea

t/Pou

ltry

Cot

ton

Biom

ass to

day

Biom

ass po

tentialAn

nu

al W

orl

dC

arb

on

(M

t C

)

↑↑

15% of 15% of

Transportation FuelsTransportation Fuels

↑↑>5000

Evaluating�power�optionsC

oncern

over

Futu

re

Availabilit

y o

f O

il a

nd G

as

High

High

Low

Low

Hydro

Nuclear

Solar

Wind

Biomass

power sector

Coal

Gas CCGT

Geothermal

Hydrogen Power

Unconventional Gas

- power�generation�options

- supply�option

Key:

Concern relating to Threat of Climate Change

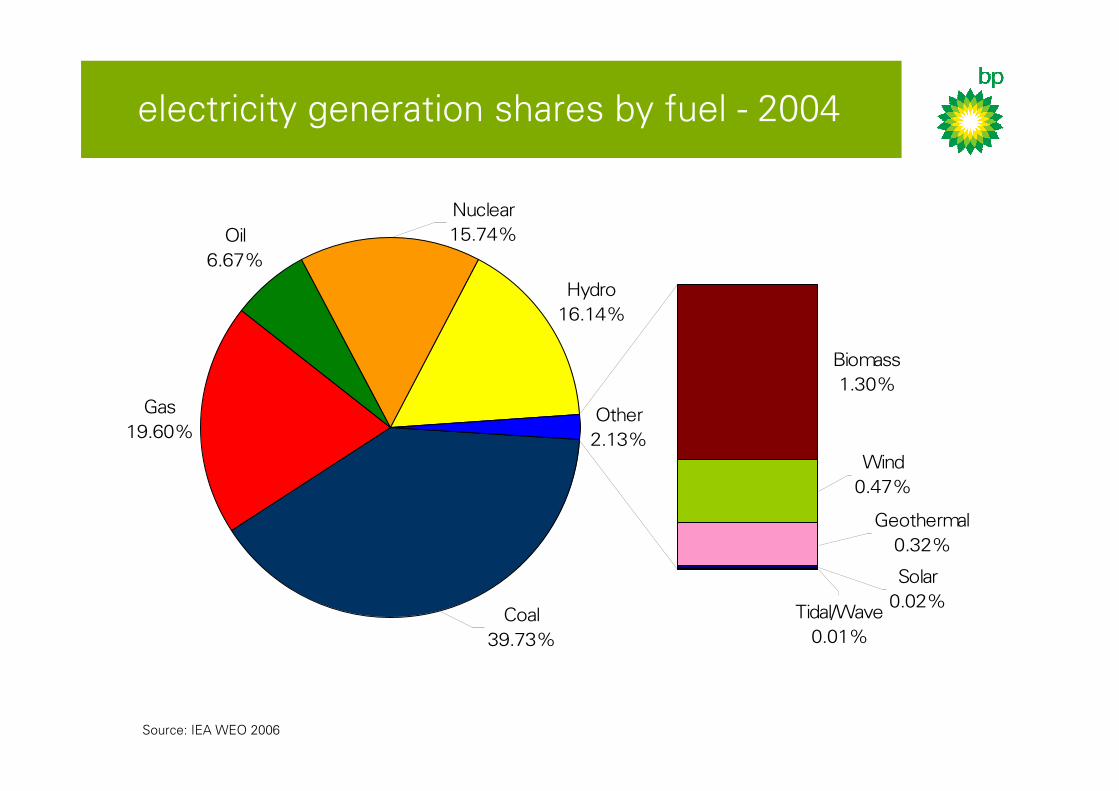

Source:�IEA�WEO�2006

Gas

19.60%

Oil

6.67%

Hydro

16.14%

Biomass

1.30%

Other

2.13%

Coal

39.73%

Nuclear

15.74%

Geothermal

0.32%

Wind

0.47%

Solar

0.02%Tidal/Wave

0.01%

electricity�generation�shares�by�fuel�- 2004�

0

25

50

75

100

125

150

175

200

225

CC

GT, gas

$4/m

mbtu

Coal $40/t

onne

Hydro

gen P

ow

er

Gas, $4/m

mbtu

Hydro

gen P

ow

er

Coal $40/t

onne

Nucle

ar

Onshore

Win

d

Offshore

Win

d

Bio

mass

Gasific

ation

Wave /

Tid

al

Sola

r (R

eta

il C

ost)

levelised�costs�of�electricity�generation

Low/Zero�carbon�energy�source Renewable�energy�sourceFossil�energy�source

Source: BP Estimates, Navigant Consulting

Cost

of Ele

ctr

icit

y G

enera

tion

9%

IR

R ($/M

Wh)

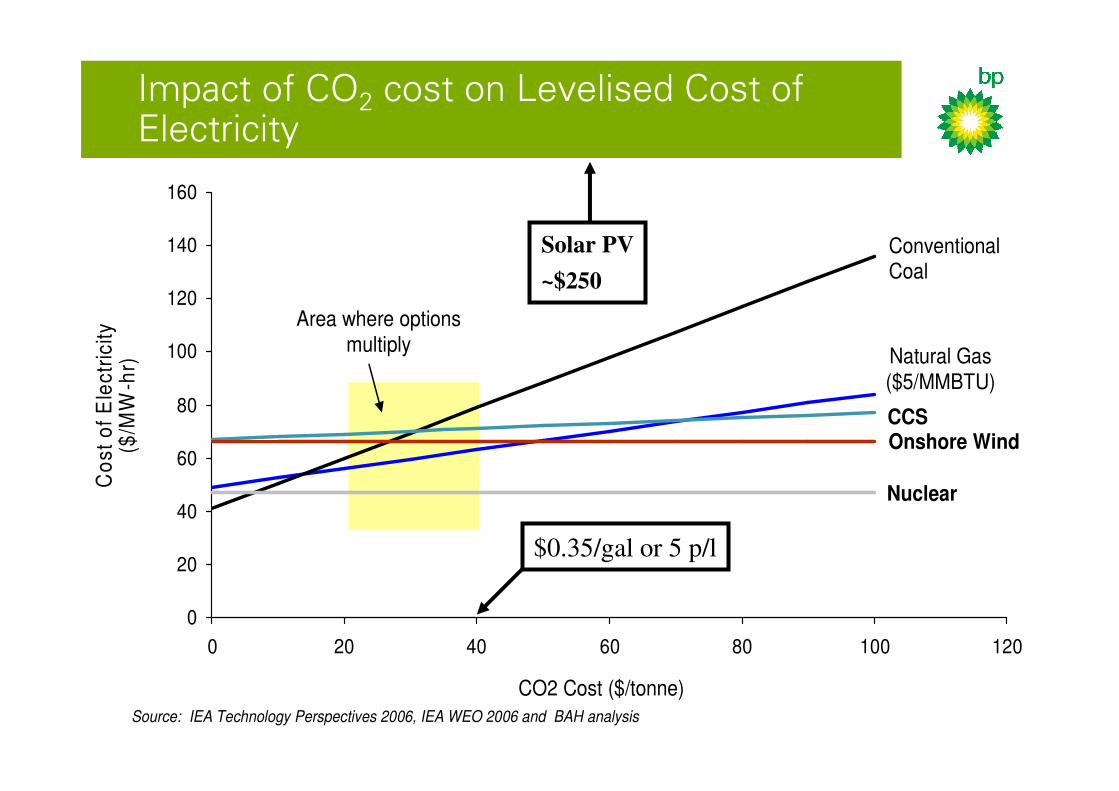

Impact�of�CO2 cost�on�Levelised Cost�of�Electricity

0

20

40

60

80

100

120

140

160

0 20 40 60 80 100 120

CO2 Cost ($/tonne)

Source: IEA Technology Perspectives 2006, IEA WEO 2006 and BAH analysis

Notes: 1) Add solar 2) $40/tonne CO2 cost or tax is $0.35/gallon of gasoline or $0.09 (or 5p)/litre

Co

st

of

Ele

ctr

icit

y($

/MW

-hr)

Conventional Coal

Natural Gas ($5/MMBTU)

CCS

Nuclear

Onshore Wind

Area where options multiply

$0.35/gal or 5 p/l

Solar PV

~$250

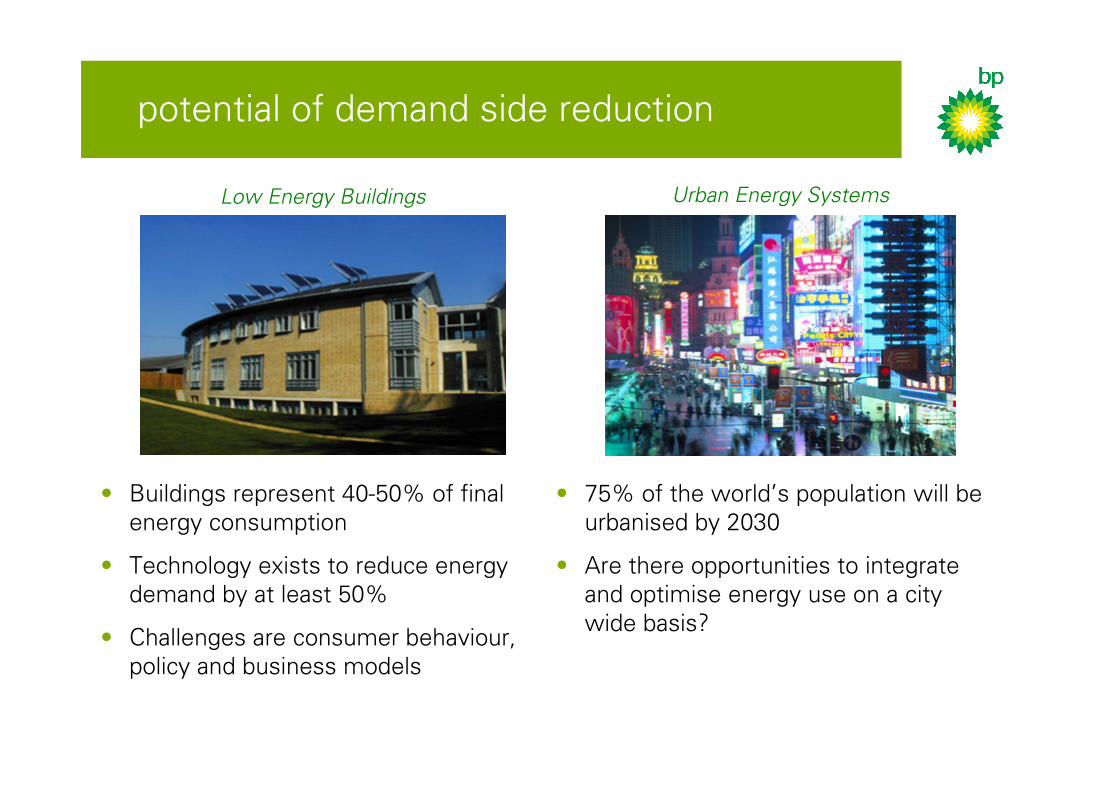

potential�of�demand�side�reduction

Low Energy Buildings

• Buildings�represent�40-50%�of�final�

energy�consumption

• Technology�exists�to�reduce�energy�

demand�by�at�least�50%�

• Challenges�are�consumer�behaviour,�

policy�and�business�models

Urban Energy Systems

• 75%�of�the�world’s�population�will�be�

urbanised�by�2030�

• Are�there�opportunities�to�integrate�

and�optimise�energy�use�on�a�city�

wide�basis?

Likely�30-year�energy�future

• Hydrocarbons will continue to dominate transportation (high energy density)

− Conventional�crude�/��heavy�oils�/��biofuels /�CTL�and�GTL�ensure�continuity�of�supply�at�

reasonable�cost

− Vehicle�efficiency�can�be�at�least�doubled�(hybrids,�plug-in�hybrids,�HCCI,�diesel)

− local�pollution�controllable�at�cost;�CO2 emissions�now�~20%��of�the�total

− Hydrogen�in�vehicles�is�a�long�way�off,�if�it’s�there�at�all

− No�production�method�simultaneously�satisfies�economy,�security, emissions

− Technical�and�economic�barriers�to�distribution�/�on-board�storage�/�fuel�cells

− Benefits�are�largely�realizable�by�plausible�evolution�of�existing�technologies

• Coal (security) and gas (cleanliness) will continue to dominate heat and power

− Capture�and�storage�(H2 power)�practiced�if�CO2 concern�is�to�be�addressed

− Nuclear�(energy�security,�CO2)�will�be�a�fixed,�if�not�growing,�fraction�of�the�mix

− Renewables will�find�some�application�but�will�remain�a�small�fraction�of�the�total

− Advanced�solar�a�wildcard

• Demand reduction will happen where economically effective or via policy

• CO2 emissions (and concentrations) continue to rise absent dramatic global action

Necessary�steps�around�the�technology

• Technically informed, coherent, stable government policies

− Educated�decision-makers�and�public

− For�short/mid-term�technologies�

− Avoid�picking�winners/losers�(emissions�trading)

− Level�playing�field�for�all�applicable�technologies

− For�longer-term�technologies�

− Support�for�pre-competitive�research

− Hydrates,�fusion,�advanced�[fission,�PV,�biofuels,�…]

• Business needs reasonable expectation of “price of carbon”

• Universities/labs must recognize and act on importance of energy research

− Technology�and policy

Questions/Comments/Discussion