stock appreciation rights (sar) and employee stock ownership plan (esop)

TRANSCRIPT

1 Jay Martin September 2015 SAR ESOP.ppt

Presentation:

CLIENT

Chief Innovation

Jay Martin

CLIENT

Employee Equity

Participation Plans

Options & Valuation

2 Jay Martin September 2015 SAR ESOP.ppt

Client was looking at creating a method to reward key staff, as well as obtain an estimated valuation(s) from a financial model.

• The original research was focused on implementing an ESOP plan.

• Two additional options, which we believe are more viable given the current situation, are Phantom Stock and SARs (Stock Appreciation Rights). We will discuss these as well so as to understand the contrast.

• We assumed SARs as best and laid out close to 50 issues.

• Final preparations are best made by an attorney with your accountant.

• The valuation has a number of options, but a cash flow analysis based one appears to be the best (really only) option.

• The challenge on the valuation is that of the three businesses (online, retail and international), two of them are in their infancy.

• Our financial model was already provided, and needs to be discussed and refined with the Client Team.

CLIENT Introduction

3 Jay Martin September 2015 SAR ESOP.ppt

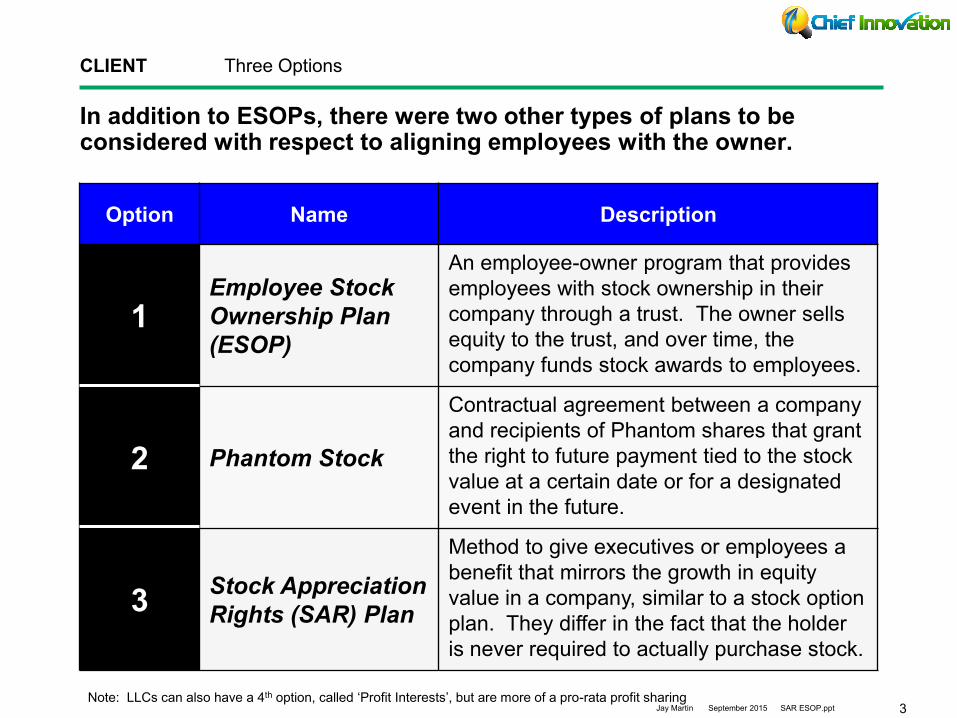

In addition to ESOPs, there were two other types of plans to be considered with respect to aligning employees with the owner.

CLIENT Three Options

Option Name Description

1 Employee Stock

Ownership Plan

(ESOP)

An employee-owner program that provides

employees with stock ownership in their

company through a trust. The owner sells

equity to the trust, and over time, the

company funds stock awards to employees.

2 Phantom Stock

Contractual agreement between a company

and recipients of Phantom shares that grant

the right to future payment tied to the stock

value at a certain date or for a designated

event in the future.

3 Stock Appreciation

Rights (SAR) Plan

Method to give executives or employees a

benefit that mirrors the growth in equity

value in a company, similar to a stock option

plan. They differ in the fact that the holder

is never required to actually purchase stock.

Note: LLCs can also have a 4th option, called ‘Profit Interests’, but are more of a pro-rata profit sharing

4 Jay Martin September 2015 SAR ESOP.ppt

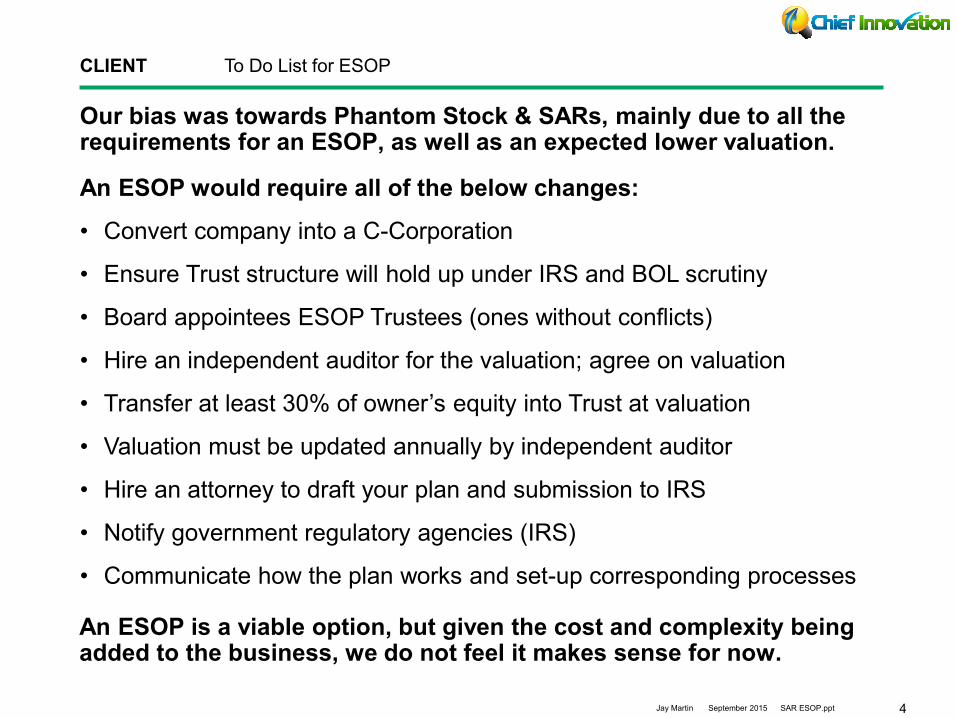

Our bias was towards Phantom Stock & SARs, mainly due to all the requirements for an ESOP, as well as an expected lower valuation.

An ESOP would require all of the below changes:

• Convert company into a C-Corporation

• Ensure Trust structure will hold up under IRS and BOL scrutiny

• Board appointees ESOP Trustees (ones without conflicts)

• Hire an independent auditor for the valuation; agree on valuation

• Transfer at least 30% of owner’s equity into Trust at valuation

• Valuation must be updated annually by independent auditor

• Hire an attorney to draft your plan and submission to IRS

• Notify government regulatory agencies (IRS)

• Communicate how the plan works and set-up corresponding processes

CLIENT To Do List for ESOP

An ESOP is a viable option, but given the cost and complexity being added to the business, we do not feel it makes sense for now.

5 Jay Martin September 2015 SAR ESOP.ppt

Below is a contrast between these Phantom Stock and SARs and some of their differences and similarities.

CLIENT Phantom Stock versus SAR contrasts

Subject Phantom Stock Stock Appreciation Rights

Value Basis Stock or cash value based on share

number specified.

Cash value on the appreciation of

specific amount of shares or equity value

Taxable Upon receipt, deductible by company.

More likely to require a set aside. Upon receipt, deductible by company

Dividends Possibly incorporated and

accumulates Not applicable

Payout Cash or shares. May require

purchase of stock.

Cash or shares, but there is no

requirement to actually purchase stock.

Timing Typically paid out at end of a period

of time

Typically paid out upon departure or an

event, could be employee choice.

Typically do not have dates.

Ties Possibly tied to personal or corporate

objectives, like Sales or Metrics

Treated more as a bonus, not sure if

Metric basis is applicable or not

Other Information Need to ensure you are avoiding

ERISA (both), avoid broad group

Used by Private Equity and Hedge Funds

to avoid IRS 457a

6 Jay Martin September 2015 SAR ESOP.ppt

Below are Pros and Cons, but the comparison is to qualified plans, not each other. These two are very similar in nature and structure.

CLIENT Pros & Cons

Phantom Stock Stock Appreciation Rights

Pro

• No employee investment required

• Simple and inexpensive to administer

• Flexible structure

• Can make awards in stock

• Awards treated as earned income for

employees upon receipt

• Exempt from Section 409 of the Internal

Revenue Code ‘if’ structured correctly

• Favorable accounting treatment

• No need for a stock sale

• Awards treated as earned income for

employees upon receipt

Con

• No tax deduction for the company

• Need an outside appraiser

• Require annual status to participants

• Employee awards not Capital Gains

• Structure may impact valuation

• ‘Appreciation Only’ plans could be

worthless, depending on company

performance

• Multiple other issues regarding payments

• No voting

• No dividends

• Could become worthless, depending on

company performance

Though we are continuing to research the differences, we are assuming that a SARs program was the best option for the Client.

7 Jay Martin September 2015 SAR ESOP.ppt

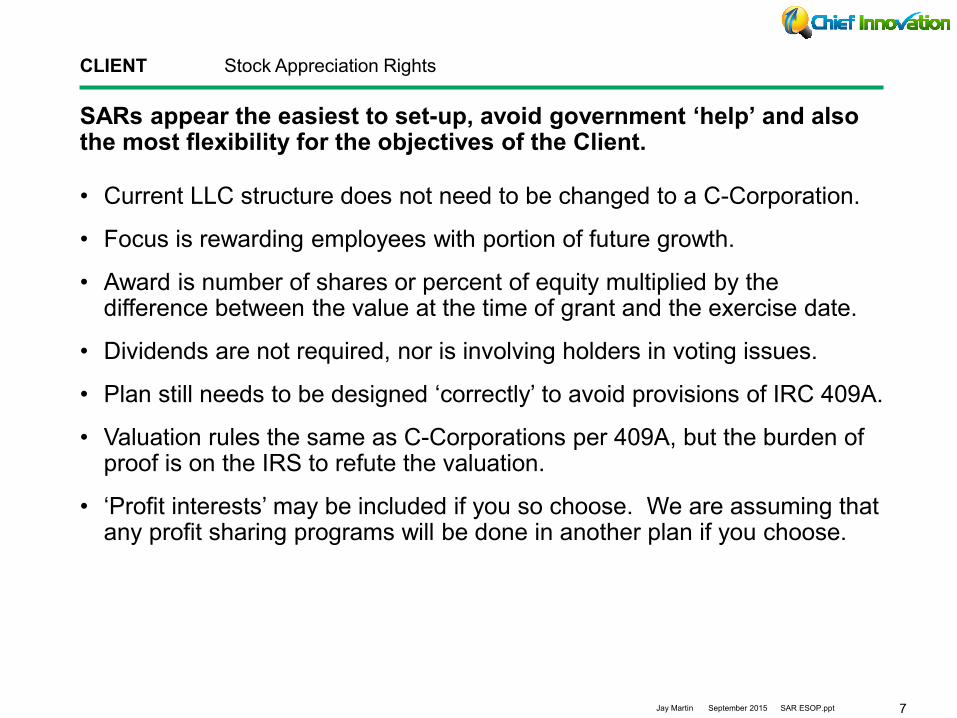

SARs appear the easiest to set-up, avoid government ‘help’ and also the most flexibility for the objectives of the Client.

• Current LLC structure does not need to be changed to a C-Corporation.

• Focus is rewarding employees with portion of future growth.

• Award is number of shares or percent of equity multiplied by the difference between the value at the time of grant and the exercise date.

• Dividends are not required, nor is involving holders in voting issues.

• Plan still needs to be designed ‘correctly’ to avoid provisions of IRC 409A.

• Valuation rules the same as C-Corporations per 409A, but the burden of proof is on the IRS to refute the valuation.

• ‘Profit interests’ may be included if you so choose. We are assuming that any profit sharing programs will be done in another plan if you choose.

CLIENT Stock Appreciation Rights

8 Jay Martin September 2015 SAR ESOP.ppt

Some of the major components and things to understand are below.

• Grant Date – date the award is made & valuation on that date

• Exercise Date – date the employee exercises the SARs

• Spread – difference in valuation from Grant to Exercise Date

• Vesting Schedule – how long until the employee ‘can’ exercise them

• Vesting Milestones – does Client prefer to have ‘targets’ for vesting?

• Award Value – share number or equity multiplied by the spread

• Valuation – drives equity value for both dates, needs consistency

• Transferability – usually transferable to 3rd party, but not sure for PP

• Stock Payout – payout could be in stock, but adds complexity for LLC

• Clawback Provisions – are there any stipulations where the company would want payouts returned? Going to competitor? Bankruptcy?

CLIENT Major Components & Details - SARs

In the next section, we detail out almost 50 questions and options to discuss. Some will be easy/obvious, while others justify discussion.

9 Jay Martin September 2015 SAR ESOP.ppt

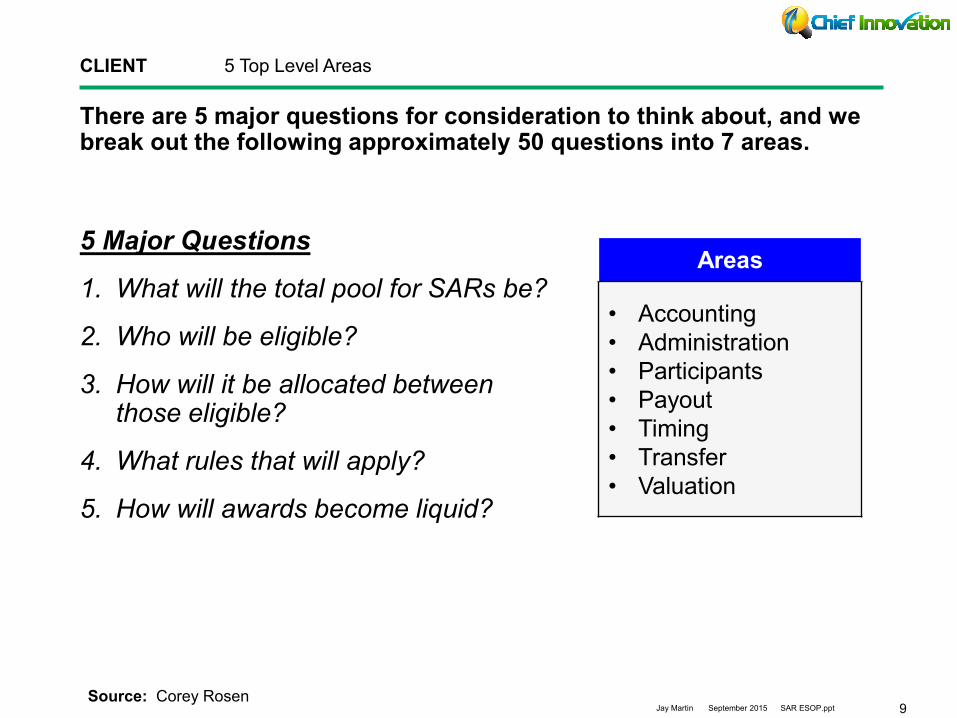

There are 5 major questions for consideration to think about, and we break out the following approximately 50 questions into 7 areas.

5 Major Questions

1. What will the total pool for SARs be?

2. Who will be eligible?

3. How will it be allocated between those eligible?

4. What rules that will apply?

5. How will awards become liquid?

CLIENT 5 Top Level Areas

Areas

• Accounting

• Administration

• Participants

• Payout

• Timing

• Transfer

• Valuation

Source: Corey Rosen

10 Jay Martin September 2015 SAR ESOP.ppt

Below are some of the questions to be answered. Page 1

CLIENT Questions to Answer

# Subject Area Question Assumption/Considerations

1 Participants Who will we have participate? Assumption is senior management, need

to be wary of too broad for IRS issues.

2 Timing How long will it go for?

Need to decide, was thinking that a

yearly percentage vesting would allow for

progress payments and new entrants?

3 Payout Cash settled or stock settled? Cash settled avoids the issue of

additional stock owners.

4 Payout Will there be a dividend to the

owners incorporated in valuation?

Need to settle on what comes out or

goes into the profit for the company?

5 Valuation What will the Grant price be based

off of?

Discussion needed for this. Does not

make sense to have a starting valuation

based on ‘what we think’ will happen.

6 Valuation Annual or other? Assuming annual, too much

administration work if more.

7 Participants How much will each person get?

Just a reminder to be wary of giving too

much away since more employees will

be coming on with hyper-growth.

11 Jay Martin September 2015 SAR ESOP.ppt

Below are some of the questions to be answered. Page 2

CLIENT Questions to Answer

# Subject Area Question Assumption/Considerations

8 Transfer Will the SAR be transferred in the

event of death?

Yes is assumed, but the question of

when the liquidation would occur needs

to be resolved.

9 Transfer In the event of death, would it be

liquidated or allow to be held?

Assume liquidated, since employee will

not be around to impact company

through the end of the SAR date.

10 Transfer Can the SAR be sold or used as

collateral?

Assume this is no, since default on the

employees fault would result in a non-

employee as an owner of the SAR.

11 Payout Would the SAR be paid out if

employee resigned before date?

Need to decide, a vesting schedule is

probably best.

12 Timing What expenses should be taken

out for the valuation?

Owner expenses need to be reviewed

and agreed upon as to whether to be

incorporated in model or thresholds.

13 Timing When during the year do we want

to update the valuation and do

payouts?

Not sure fiscal schedule, but assuming

January or start of year if otherwise.

14 Payout What metrics, if any, will the

performance be tied to?

Not sure you will have any metrics other

than the valuation, but in case.

12 Jay Martin September 2015 SAR ESOP.ppt

Below are some of the questions to be answered. Page 3

CLIENT Questions to Answer

# Subject Area Question Assumption/Considerations

15 Payout What timing will the benefit be paid

out for?

Assumption was 100% upon departure or

maturity, but could spread out. This is

usually done for less profitable firms.

16 Valuation Equity percent or Share-based? Not sure which you’d prefer, question

comes as ‘can it be diluted’ or not.

17 Valuation Get participants involved on the

valuation or just offer it?

Your choice, but getting them involved

could help build trust/avoid issues.

18 Administration Does she have an official Board of

Directors? Will she have one?

Not sure how the plan can be managed

without a Board if one is not planned.

19 Administration Who would serve in a role of

Compensation Committee?

Someone has to administer the plan, in

some cases it is a Comp Committee?

20 Administration Are you going to change to a C-

Corp in the future?

Not sure if this has been discussed with

the Pros and Cons, or given time frame.

21 Payout Has a thought of an initial amount

been given, or the cap?

Need to think of what will we start at and

a maximum. The plan should begin with

an amount issued into the plan to start.

13 Jay Martin September 2015 SAR ESOP.ppt

Below are some of the questions to be answered. Page 4

CLIENT Questions to Answer

# Subject Area Question Assumption/Considerations

22 Payout Will you allow people to do partial

vesting?

Unless there will be another bonus plan,

think this would be preferable.

23 Payout How long for company to complete

the payment?

Minor detail, had seen 10 days, but 30

might be better for a small company.

24 Administration Do SARs have any voting rights or

other non-financial benefits?

None. They are not stock, not voting

rights or other influence on the company.

25 Administration What type of dilution and

adjustment provisions will there be?

Need to think through the impact of

mergers, other investors, etc. on this.

26 Administration Secured or unsecured? Think it has to be unsecured, though that

is her decision to make.

27 Accounting Funded or unfunded? Not sure what you want to do, but could

be held in cash like retained earnings.

28 Accounting Terminating the Plan

Company should have right to terminate

the plan, but not eliminate outstanding

balance of payments.

14 Jay Martin September 2015 SAR ESOP.ppt

Below are some of the questions to be answered. Page 5

CLIENT Questions to Answer

# Subject Area Question Assumption/Considerations

29 Administration Can whoever is administrating it

modify the plan?

Think this has to be yes, but need to

respect previous agreements.

30 Administration Impact of modifications on existing

SARs awards?

Assume no. Without a no here, adds too

much risk for participants.

31 Administration What state should the law be

under?

Assumption is Texas, but if you make a

C-Corp, not sure what state to use.

32 Administration Would you want an arbitration

clause in the agreement? Not sure what your preference is.

33 Administration Clarification of timing of SARs is

not a guarantee of employment?

Just a reminder, that just because the

term is X years, they can still get the axe.

34 Payout What is the exercise period for

them to receive it after it vests?

Should discuss, want to provide flexibility

but also not leave it around forever.

35 Payout What precautions for IRC 162(m)

should you take?

Not sure on the comp plan, but hopefully

Awards will cross this threshold ($1MM)

15 Jay Martin September 2015 SAR ESOP.ppt

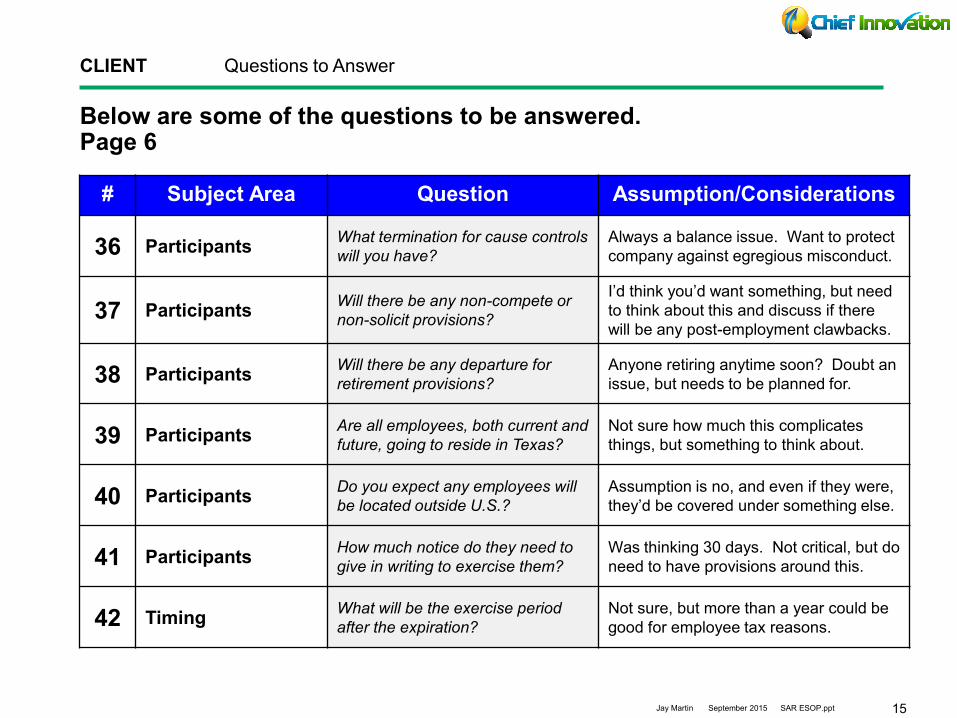

Below are some of the questions to be answered. Page 6

CLIENT Questions to Answer

# Subject Area Question Assumption/Considerations

36 Participants What termination for cause controls

will you have?

Always a balance issue. Want to protect

company against egregious misconduct.

37 Participants Will there be any non-compete or

non-solicit provisions?

I’d think you’d want something, but need

to think about this and discuss if there

will be any post-employment clawbacks.

38 Participants Will there be any departure for

retirement provisions?

Anyone retiring anytime soon? Doubt an

issue, but needs to be planned for.

39 Participants Are all employees, both current and

future, going to reside in Texas?

Not sure how much this complicates

things, but something to think about.

40 Participants Do you expect any employees will

be located outside U.S.?

Assumption is no, and even if they were,

they’d be covered under something else.

41 Participants How much notice do they need to

give in writing to exercise them?

Was thinking 30 days. Not critical, but do

need to have provisions around this.

42 Timing What will be the exercise period

after the expiration?

Not sure, but more than a year could be

good for employee tax reasons.

16 Jay Martin September 2015 SAR ESOP.ppt

Below are some of the questions to be answered. Page 7

CLIENT Questions to Answer

# Subject Area Question Assumption/Considerations

43 Timing Will the payout be reduced if not

exercised in a certain period?

Assumption is no, but could have a

reduction after a certain time for a push.

44 Participants If someone resigns, will there be a

clawback?

Assume no. Also, assume all vested can

be liquidated.

45 Timing What to do with mid-year awards

and starting valuation.

How will you get new executives into

program? Start at last or next year value

46 Valuation Can it go negative in a year, i.e.

stock price is lower than previous?

Assume yes, that if stock drops, then

unexercised values go down.

47 Payout In the event of a major transaction,

what value will it be paid out on? Assumption is the most recent year.

48 Accounting How will we account for it? SARs go on Balance Sheet as a Liability

if the employee can receive cash?

49 Participants What and how much information

will plan share with participants?

Need to think about and discuss, assume

everything given exec level, but not sure.

17 Jay Martin September 2015 SAR ESOP.ppt

The regulations of IRC 409A are important, and there are three tests to ensure that a SARs plan does not violate this.

CLIENT IRC 409(a)

# Subject Test Strategy

1 Valuation SAR base value is at least equal

to fair market value at the time of

the grant.

Multiple Safe Harbors here, with most

relevant relating to an independent

appraisal. Others include analysis of

stock transactions, which are n/a.

2 Employment SAR pertains to common stock of

the entity the option holder works

for or a parent company.

For PP, should be easy and obvious.

Need to ensure the LLC issue has no

impact on this, but straightforward.

Also, any non W2 employees?

3 Deferral

Rights No additional deferral rights are

added to the SAR. Easy to accommodate, just avoid

allowing additional deferrals.

The first is the most important for us to think about and focus on. The other two are completely under our control for compliance.

18 Jay Martin September 2015 SAR ESOP.ppt

Some relevant points regarding valuations. The regulatory focus is to ensure a fair valuation, and to avoid valuations being ‘too low’.

• Independent / outside appraisal conducted annually.

• Within 12 months of before the grant of the SAR

• Use a formula which is consistently applied to both compensatory and noncompensatory transactions of the issuers shares.

• Additional concerns include:

• Addition of payouts as deductions of compensation in valuation

• Stocks Not Readily Tradable on an Established Securities Market – “Where the taxpayer can otherwise demonstrate that the valuation was determined by the reasonable application of a reasonable valuation method, the standard will be met.” (Note: IRS Bulletin on following page)

• Given she is the sole owner, do not believe that there will be any needed consideration to recent stock transactions and valuations.

CLIENT Valuation Safe Harbor

Given that Client needs to ensure it does not undervalue the company, it could value then balance awards to reflect the high valuation.

19 Jay Martin September 2015 SAR ESOP.ppt

• c. Valuation - stock not readily tradable on an established securities market

• i. In general

• The final regulations adopt the provisions in the proposed regulations relating to the valuation of stock not readily tradable on an established securities market, subject to the modifications discussed in this section III.C.4.c. Accordingly, a valuation of stock based upon a reasonable application of a reasonable valuation method is treated as reflecting the fair market value of the stock. To meet this standard, it is not necessary that a taxpayer demonstrate that the value was determined by an independent appraiser. Where the taxpayer can otherwise demonstrate that the valuation was determined by the reasonable application of a reasonable valuation method, the standard will be met.

• One commentator requested that the factors to be considered in determining the fair market value of the stock should be modified to include consideration of any recent equity sales made by the corporation in arm’s-length transactions. The final regulations adopt this suggestion.

• The final regulations continue to require that in the case of a stock right issued with respect to stock that was not publicly traded at the time the right was issued, but becomes publicly traded before the right is exercised, the stock value for purposes of calculating the payment amount (in the case of a stock appreciation right) or the buyback amount (in the case of a stock option where the underlying stock is subject to a buyback agreement) must be based upon the rules governing stock that is publicly traded. This does not mean that the initial exercise price determined under the rules governing stock that is not publicly traded must be reset. Rather, this means only that the value at the time of exercise used to determine the payment amount or the buyback amount must be determined under the rules governing stock that is publicly traded. For example, if a service provider holds an excluded stock appreciation right with an exercise price of $1 that was fixed based on a valuation of the closely-held corporate stock at the time of grant, and before exercise the stock becomes readily tradable on an established securities market, the amount payable upon exercise must be the excess of the value of the stock based on its trading price over the $1 exercise price.

• ii. Safe harbor presumptions

• The final regulations adopt a presumption in specified circumstances that, for purposes of section 409A, a valuation of stock reflects the fair market value of the stock, rebuttable only by a showing that the valuation is grossly unreasonable. The presumption applies where the valuation is based upon an independent appraisal, a generally applicable repurchase formula (applicable for both compensatory and noncompensatory purposes) that would be treated as fair market value under section 83, or, in the case of illiquid stock of a start-up corporation, a valuation by a qualified individual or individuals applied at a time that the corporation did not otherwise anticipate a change in control event or public offering of the stock.

• Many of the comments with respect to these presumptions related to the presumption applicable to illiquid stock of start-up corporations. As set forth in the proposed regulations, the start-up corporation presumption would not apply if the service recipient or service provider could reasonably anticipate, as of the time the valuation is applied, that the service recipient would undergo a change in control event or make a public offering of securities within the 12 months following the event to which the valuation is applied. Commentators suggested that a 12-month period is too long, because changes occur so rapidly in the business world that it often is difficult or impossible to predict so far in advance whether such an event will occur. Commentators suggested that the service provider should retain the benefit of the presumption unless the issuing corporation entered into a definitive agreement or filed its registration statement with the Securities and Exchange Commission within a period of 15 or 30 days after issuing the stock right.

• The Treasury Department and the IRS believe that a 15-day or a 30-day period is too short. Although there is always a risk that a public offering will fail or that a corporate transaction will not occur, the Treasury Department and the IRS also believe that a person should reasonably be able to anticipate whether such a transaction will occur during a reasonable period before the transaction.

• Accordingly, the final regulations provide that the start-up corporation presumption will not apply if at the time the valuation is made, the service recipient or service provider may reasonably anticipate that the service recipient will undergo a change in control event in the next 90 days or an initial public offering within the next 180 days. As under the proposed regulations, the rule in the final regulations is concerned with what the parties may reasonably anticipate at the time the stock right is issued.

• Other comments requested examples of persons with sufficient knowledge, experience, and skill in valuing illiquid stock of a start-up corporation. Because knowledge, skill and training may be obtained in different ways, the final regulations do not provide specific examples. However, the regulations clarify that the standard to be applied is whether a reasonable individual, upon being apprised of such person’s relevant knowledge, experience, education and training, would reasonably rely on the advice of such person with respect to valuation in deciding whether to accept an offer to purchase or sell the stock being valued. The final regulations also clarify that significant experience generally means at least five years of relevant experience in business valuation or appraisal, financial accounting, investment banking, private equity, secured lending, or other comparable experience in the line of business or industry in which the service recipient operates.

• With respect to the presumption based upon a generally applicable buyback formula, some commentators requested that the presumption apply where the formula is applicable to all compensatory stock transactions, but not also applicable to all noncompensatory stock transactions. The final regulations do not adopt this suggestion. However, the final regulations clarify that to meet the requirements of the presumption, the buyback formula is required to be applicable to compensatory and noncompensatory transactions with the issuer or a person owning 10 percent or more of the stock of the issuer, but is not required to be applicable to transactions with other persons or transactions that are part of an arm’s length transaction constituting the sale of all or substantially all of the stock of the issuer to an unrelated purchaser.

CLIENT http://www.irs.gov/irb/2007-19_IRB/ar07.html

20 Jay Martin September 2015 SAR ESOP.ppt

Valuation

CLIENT Appendix 1 – Valuation & ESOP Supporting Information

21 Jay Martin September 2015 SAR ESOP.ppt

There are three primary methods to complete a company valuation.

CLIENT Three Major Options

# Option Description Rationale for Client

1 Cash Flow

Value based on the future

cash flows of the company,

discounted using the time

value of those cash flows in

today’s dollars.

Calculation includes

historical cash flows and

growth/potential of the

business. This is expected

to be the best, but may

ignore the brand premium.

2 Assets

The value of the existing

assets, usually the ‘hard’

ones. This can also be an

estimate of the value of

building all the assets of the

business from the start.

Typically done for

companies without brands

and heavy in hard assets,

such as real estate or

machinery. Do not believe

this is worthwhile for Client.

3 Peer Companies

Comparison of transactions

or stock values of peer

group companies with

respect to an estimate of

what you might sell for. The

are numerous ratios for this.

Many options as to what

ratio to use to assess a

value using peer group data.

Client will be a challenge to

pick peers given it is a brand

strong category creator.

22 Jay Martin September 2015 SAR ESOP.ppt

We believe Cash Flow is the best option to use for the valuation.

CLIENT One Clear Choice – Maybe Second Possible Option

# Option Rationale for CLIENT

1 Cash Flow

• Calculation includes historical cash flows and

growth/potential of the business. This is expected to be

the best, but may ignore the brand premium.

• Cash flow is the only one that will properly recognize

potential of the business and growth.

2 Assets

• Applicable for heavy asset based companies

• Ignores brand value

• Minimizes intellectual property and loyalty

• Focus is ‘what would it take to recreate this’

• Do not believe this is an option even worth exploring

3 Peer Companies

• Peers will be difficult to chose given we are ‘new’

• Revenue ratios will ignore growth trajectory and potential

• EBITDA will be harder to find / understand calculation

• Future growth is strong, but may be at lower margins

given that Retail and International will not be direct

23 Jay Martin September 2015 SAR ESOP.ppt

For Option 1, Cash Flow, there are a number of major decisions and assumptions that should be discussed and made.

• Adjusted Expense Levels – What expenses do we currently incur that could be extricated to augment cash flows? What additional costs might be incurred if we transferred ownership of the company to others?

• Growth Rate – How much as the company grown? At what point will online sales ‘level-off’? How much will new Retail channels help? Where and when will international come into play?

• Discount Rate – What discount rate should we use? Why?

• Cases – How many cases should we create? Worst, Best and Base?

• Case Inputs – Which company factors should we have ranges for? What impact are macro-economic factors to our business? Do we care?

CLIENT Discounted Cash Flow Considerations

For Option 1, Cash Flow, there are a number of major decisions and assumptions that should be discussed and made.

24 Jay Martin September 2015 SAR ESOP.ppt

In identifying peers, we should remember that Client is both a Consumer Products Company as well as an Online Store.

CLIENT Option 3 - Peer NAICS Codes

NAICS Codes of Possible Peer Candidates

We should discuss ‘known’ companies who we think are peers.

25 Jay Martin September 2015 SAR ESOP.ppt

Below are some of the possible contents of a formal valuation report.

• Valuation Opinion Letter

• Executive Summary

• Company Profile

• Economic and Industry Outlook

• Financial Performance Guidance

• Identification of Guideline Companies

• Valuation Methods

• Discount for Lack of Control and Marketability

• Reconciliation and Conclusion on Value

CLIENT Possible Contents