stop loss - software solution designed to protect your assets from theft and fraudulent

TRANSCRIPT

— SOFTWARE SOLUTION DESIGNED TO PROTECT YOUR

ASSETS FROM THEFT AND FRAUDULENT

USING INFORMATION TECHNOLOGIES FOR REVEALING OF FRAUD

© 2015. Stop-Loss. All rights reserved.

FRAUDULENT

CAN YOU TRUST TO YOUR MANAGERS?

DO THEY REALLY WORK FOR YOU

OR FOR THEMSELVES?

DON'T YOU WANT TO KNOW THIS EXACTLY,

NOR ASSUME?

FRAUDULENT

The Stop-Losstm system is a fundamentally new approach tosolve the any type of work place crime and fraudulentproblem.

It works without human participation, what advantageouslydiffer it from other systems, where analytical queries aremade by specialists. This approach ensures the validity of thedata, which you receiving. Thus, nobody have possibility toaccess to sensitive documents prohibited for him. The Stop-Loss system makes the prevention of employee’s thefts soeffective as never before, and you get whole informationabout what is happening with your investments and assetswithout interfering with the operation of the corporation.

FRAUDULENT

For the Stop-Loss system it is no matter what kind of businessyou are in. What do you manage: finance, production, transport,retail or the whole country — it is all can be analyzed by thesystem using any kind of electronic documents from any types ofdatabases about any sort of business activity or transactions.

The Stop-Loss system detects the unauthorized withdrawal ofassets and fraudulent incidents and then writes a report aboutthe situation, which includes the relevant documents inattachment, and send it by e-mail to you and/or in chargemanagers.

Previously, to achieve such results it is required a "whole army"of high level professionals.

FRAUDULENT

Now Stop-Loss system deliver possibility to solve theproblem of office crime in a systematic way and achievenew level of the control over crime activity.

Fraudulent widespread both at the government level andin private business. For example, dishonest supply agentwhen making purchases can buy goods at an inflated pricefrom the seller, who share pay with him. A dishonest sellercan sell the goods at a reduced price or simply assign partof the proceeds. All these and many other means of illicitenrichment can be detected and prevented by the Stop-Loss system.

FRAUDULENT

FROM FINANCIAL AUDITORS THE STOP-LOSS SYSTEM DIFFERS BY:

Incorruptibility

Productivity

It cannot be inattentive

It can operate huge amounts of data

Imagine that your internal auditors and security office willalso have a new high-tech, invisible "army" which remainsactive 24 hours a day, 7 days a week, 365 days a year.

THE PROBLEM IS MORE THAN MONEY

Besides evidently loss of income, thefts also cause situations that can seem not related, but if you look closer, you find a thief in the epicenter of the mess.

If you have noticed the following, probably the swindlers and “receivers of illegal dividends” are already working all over their schemes:

Non-transparent business processes

Thieves consider that non transparent business processes is a best gift for

them, because their opportunities for illicit gain become wide-open.

Therefore, specific occasions, unusual situations and extraordinary events

regular occurs and broader power are required more often.

Failure to making staff accomplished tasksNon execution concealed by excuses why this cannot be done – excessive workload, lack of resources etc. Not only loafers will tell you "impossible", "uncomfortable", "we are out of time" and "we have not anyone". More often, it is the thieves tend to avoid order and better control.

THE PROBLEM IS MORE THAN MONEY

Frauds are in opposite to organization efforts, them Ignoring and bring to degrade the business processes, standards, etcThis is manifested as a critique of the flaws supposedly inherent changes, that is the pretext for endless improvements, resurfacing and complications. Once weakens supervision – starts a failure to comply of any new rules and regulations. But it was still the same frauds necessity in the opacity.

You receive many contradiction and equivocal data while trying to resolve the situation Fraudulent documentation contains conflicting information, the fraudsters provide false explanations and excuses, they support a big mess – this ensures that nobody will have the strength to deal with what they are doing.

High level of criticism and low level of loyalty Frauds need in justifications for their activities, so they will criticize management and founders. As result of this activity loyalty level of other personal are decreased.

THE PROBLEM IS MORE THAN MONEY

Tax services complaints False financial records, created for concealment fraudulent, will sooner or later lead to tax services complaints.

Implementation of regulations and control mechanisms becomes too

complexity Thieves need to “muddy the water” of business, so they do everything to make their activity and documents not under control.

Leakiness of the loyal and productive employees from the companyFraud people are in opposition to honest workers and try to get them fired through the moral pressure, slanders and uninteresting or useless work.

The problem of financial losses grows with time Authors of fraudulent schemes involves more staff members in his activities. They create more effective and complicated fraudulent schemes. While people remain unpunished, they steal more and more. Watching these well-organized groups all other employees are also start to embezzling.

FRAUDULENT

DOING NOTHING

WITH THE FRAUD PROBLEM

LEADS TO DISASTER

HOW TO DISCLOSE AND STOP FRAUD

STOP-LOSS – SOFTWARE SOLUTION FOR DETECT AND PREVENT THEFTS AND FRAUD

There is no such business sphere where you can be free from the fraudulentproblem. Too many people find that it is totally normal thing to resolve theirfinancial problems abuse their positions and using employers money.

With Stop-Loss system you can automate process to detect and discoverfraudulent incidents. The honest, loyal and productive employees are bulliedand made to leave by means of moral pressure, slander, making him or her acan carrier or just by snowing a person with uninteresting, non-core ormeaningless work.

THIS INFORMATION SYSTEM IS NOTABLE FOR:

Integrity

Productivity

That it cannot be inattentive

That it can operate large amounts of data

HOW TO DISCLOSE AND STOP FRAUD

POSSIBILITIES OF APPLICATION OF STOP-LOSS SOLUTION

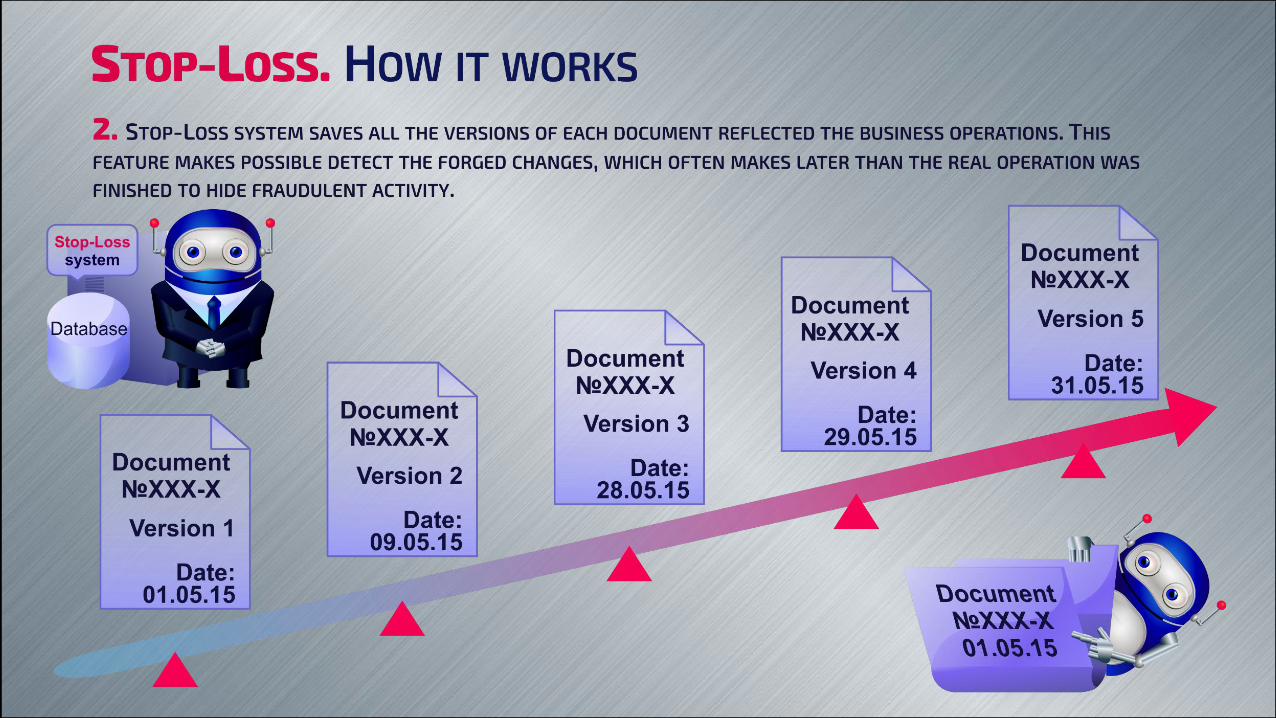

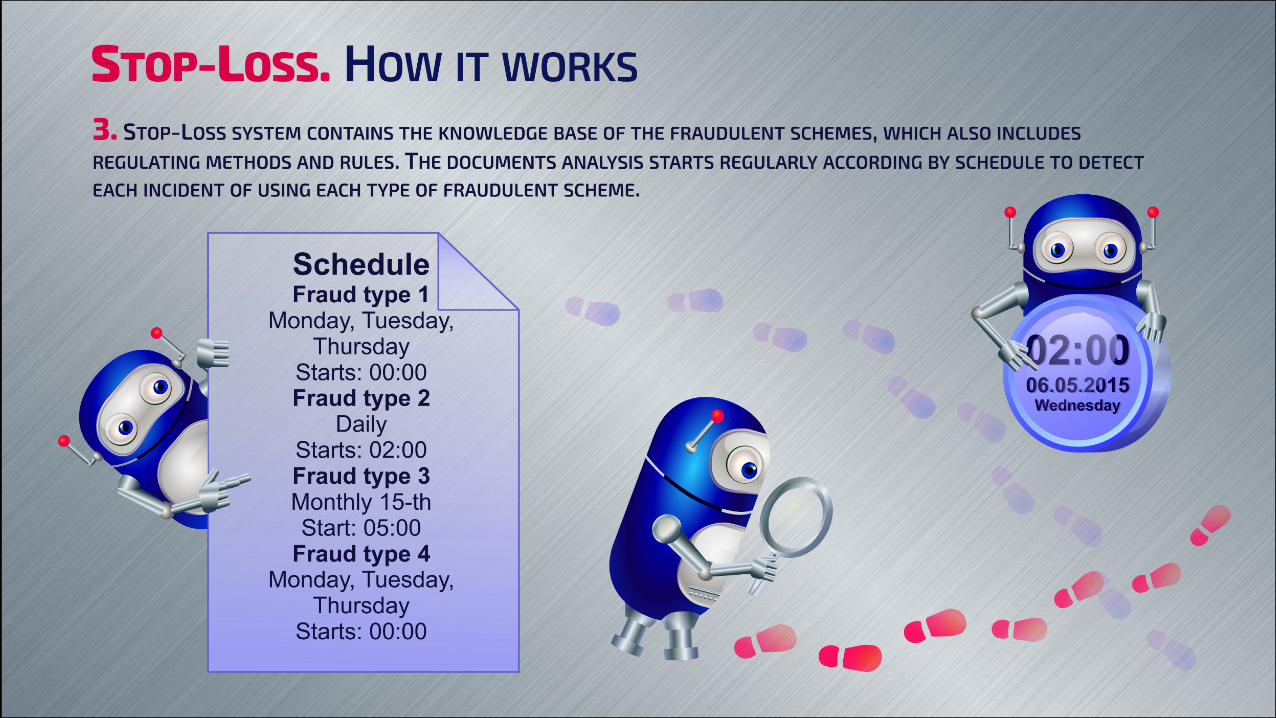

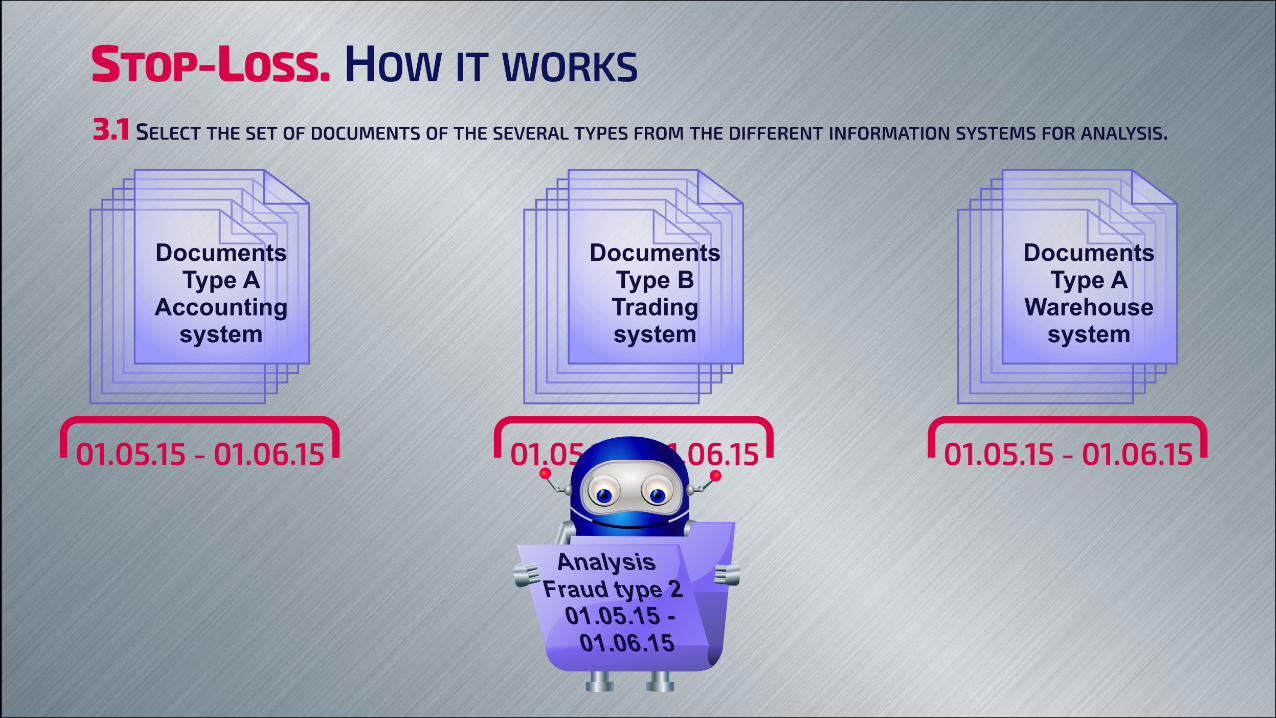

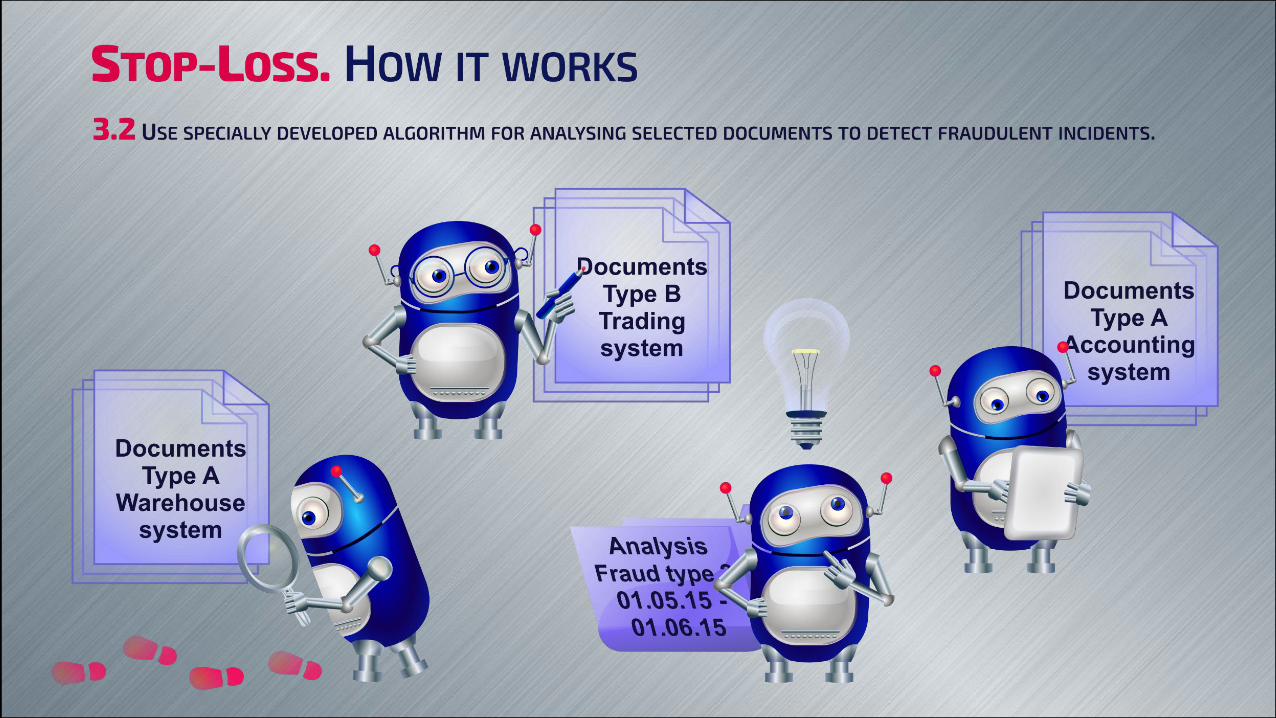

The thing is that thieves forge documents for their frauds, and these documents inevitably contain inconsistencies that can be identified by conducting data analysis.

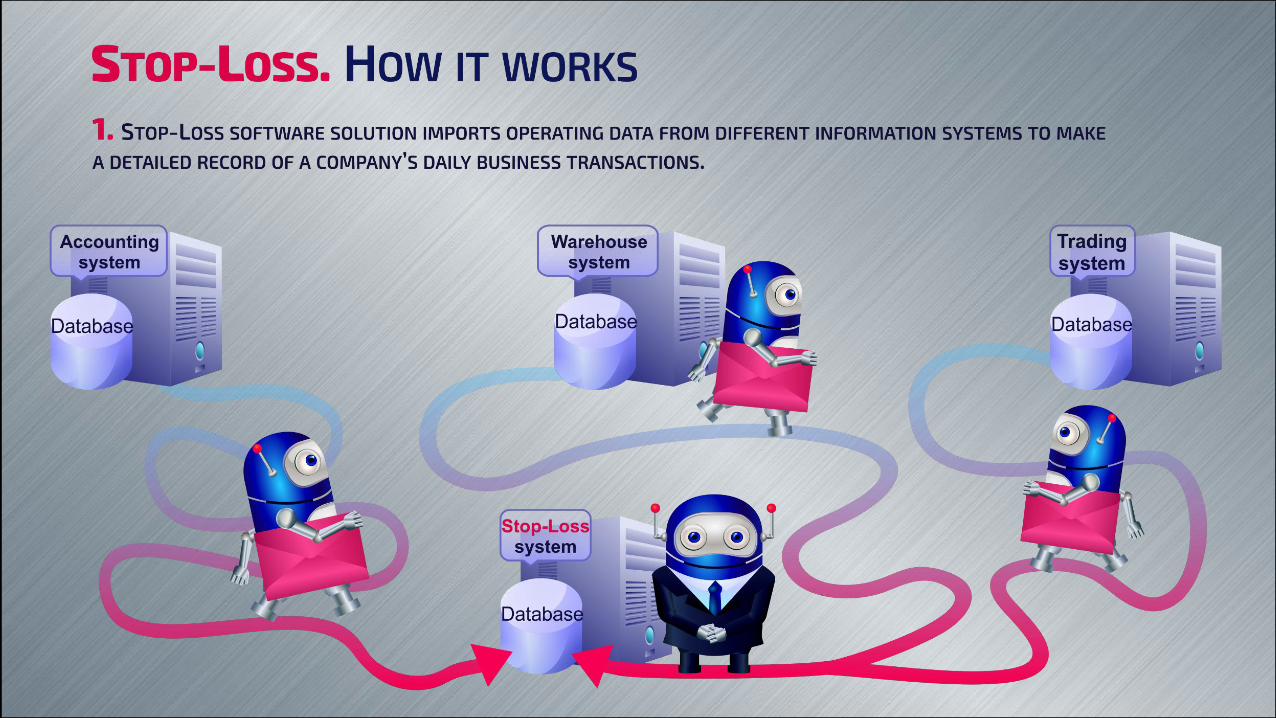

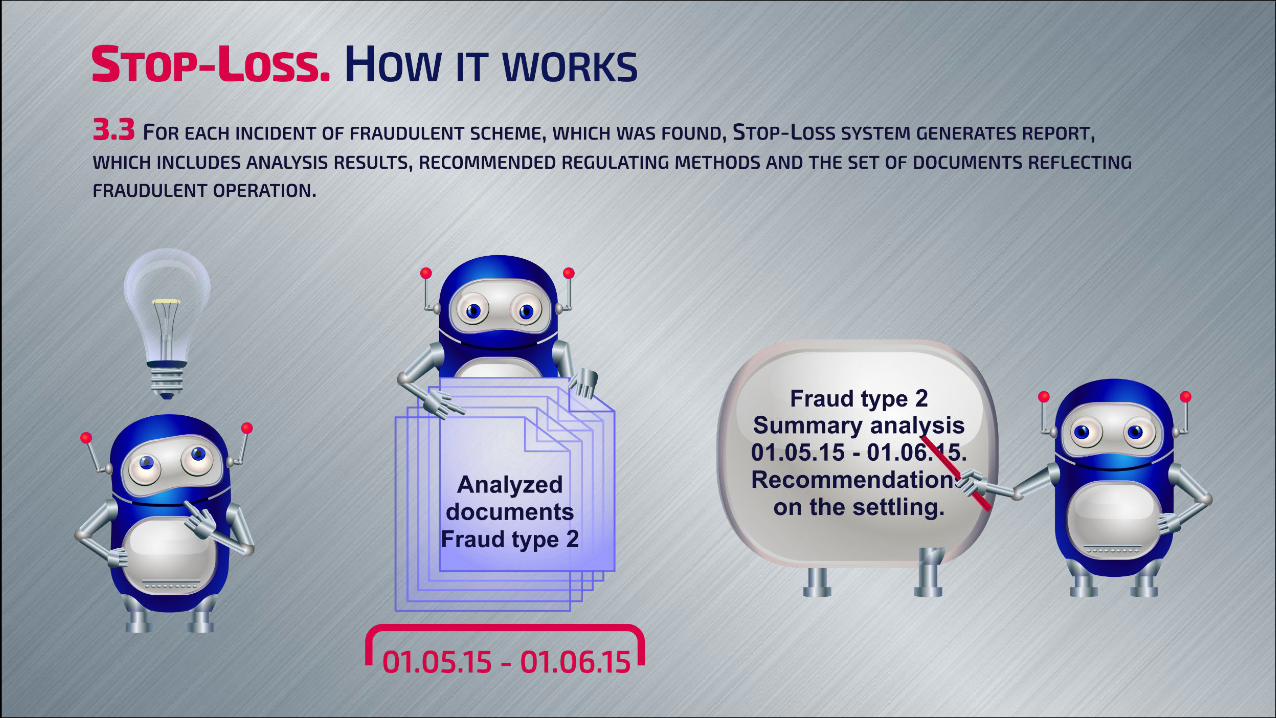

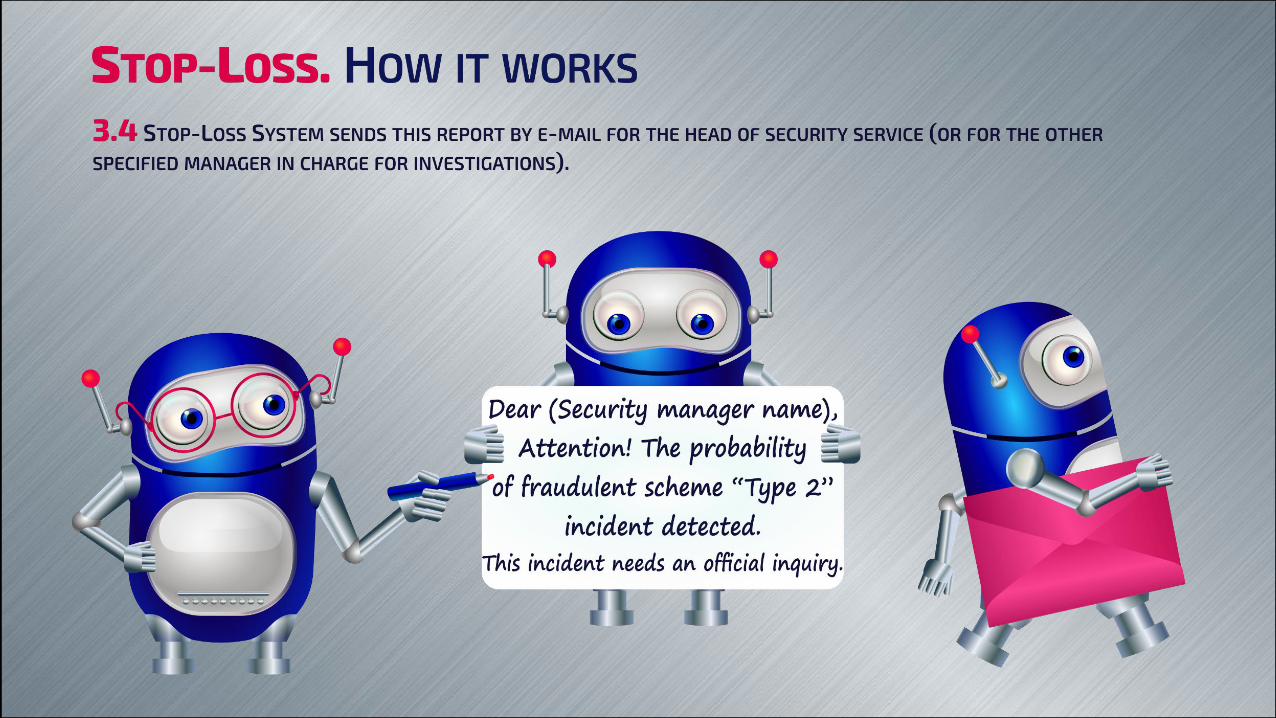

The Stop-Loss system searches are conducted according to the set timetable, which is based on data obtained from various information systems. The analysis is carried out using algorithms of suspicious documents detection and a knowledge bases of fraud schemes. In case of detection of signs of thefts the system generates and directs reports to appropriate authorities describing all identified discrepancies and indicating probable fraudulent scheme which can be seen from the nature of “weird things” found in the documentation.

THE FRAUD SCHEMES IN EXAMPLES

FRAUD SCHEME: OVERSHOOTING OF PRICES OF VENDORS

This scheme is widely used in the trading companies, when employees of Purchasing Department enter into collusion with vendors. As a result, the vendor supplies his or her products at a higher price, and the employee of the Purchasing Department receives “rake-off”. This scheme has a negative impact on profitability, and it is especially critical in a period of erosion of purchasing power of people.

Scheme disclosing: You can detect the use of this scheme in analysis of system data of electronic exchange of documents with vendors for which each vendor sends his complete “electronic price list” – in this way you can organize a knowledge database to compare prices of different vendors, detect facts of purchases at inflated prices and obtain statistical data about who is the most “loyal” to expensive vendors in the Purchasing Department.

THE FRAUD SCHEMES IN EXAMPLES

FRAUD SCHEME: COINCIDENCE OF PAYMENTS

This scheme is characterized with payments of the same amounts effected twice to the same counterparty. In fact only one payment is made to the counterparty, and the second is made on the account of the scammer. To cover this there is a record about purchase from a big vendor on one of the accounts that is rarely checked. The payment to vendors allows providing supporting documents if necessary.

Scheme disclosing: This method of fraud can be disclosed by searching of payments of the same amounts in the accounting system and comparing data on such payments with the data presented in the statements downloaded from the banking system. These data will point to the real recipient of the duplicate payment.

THE FRAUD SCHEMES IN EXAMPLES

FRAUD SCHEME: OVERSTATEMENT OF NORMS OF CONSUMPTION OF RAW MATERIALS

This scheme is used at production sites and can be expressed in growth of volume of disposal of raw materials in the production of finished products. For example, the commercial kitchen produces apple pies. A standard recipe includes consumption of 0.0027 kg of sugar for one pie. If a technologist “changes” the recipe even a bit by putting 0.027 kg of sugar, this non-significant change will allow to dispose a ton of sugar per month. Finally, the accountant shall agree with the vendor about supply of a non-existing ton of sugar and make payment – and all participants of the scheme will have profit.

Scheme disclosing: You can track the changes in recipes or process cards (you will need to have their “reference” samples not corrupted by the violators). Another indicator is a significant change in the statistics of consumption of raw materials along with minor changes in the production of finished products. Also the disposal of raw materials before its delivery will indicate the fraud scheme. The changes in the cost disproportionate to the growth of prices of vendors is another alarm signal.

THE FRAUD SCHEMES IN EXAMPLES

FRAUD SCHEME: OVERSTOCKING

“Rake-off” from vendors can provoke the Purchasing Department to create stocks of raw materials or products much larger than it is optimal. Besides, if the warehouse is overstocked it prevents safety control, and the loss of multiple units becomes negligible.

Scheme disclosing: The mechanisms of remains and/or ADRmanagement in the system of enterprise management which use data on the remains and turnover can be really helpful. It is important not to leave such mechanisms merely as information tools for managers who place orders, but to perform the gap analysis of statistics on the costs of raw materials or turnover of products and analysis of data on actual purchases and to identify the employees who condone overstocking the most actively.

THE FRAUD SCHEMES IN EXAMPLES

FRAUD SCHEME: “NATURAL LOSS” OF PRODUCTS

There are rules for withdrawal of goods due to shrinkage loss, natural damage (vegetables/fruit) or breakage (for products in glass containers). Scammers can manipulate these norms in such a way as to adjust the loss to standards.

Scheme disclosing: If the withdrawal in storage or trading system are constantly in the upper limit of normal (there are no “jumps” up and down in different time periods, for example seasonal), you can check withdrawals which are sharply different from usual ones in dates and amounts, as the scammers can make a sort of “schedule” of execution of such transactions (once a week, once a month), when they draw the balances and adjust the numbers to those in standards.

THE FRAUD SCHEMES IN EXAMPLES

FRAUD SCHEME: OVERRATING THE COST OF WORKS

A sticky fingered accountant can decide to “make hay” and overrate the cost of works executed by your company for another legal entity or entrepreneur. For example, the cost of some services in accordance with the Statement of Acceptance is 38.150 rubles. When it’s time to draw up the invoice the accountant writes in a different amount – for example 39.150 rubles. If someone notices it the accountant will easily ascribe this error to fatigue, then apologize and draw up the invoice again.

If by the nature of activity of the company there is a large flow of such documents, the losses can be much bigger than 1.000 rubles.

Scheme disclosing: This scheme can be easily identified by comparing the amounts from invoices with the Statement of Acceptance or any other additional agreements and contracts that specify the scope and cost of works.

THE INFORMATION SYSTEM IS AN INCORRUPTIBLE ANALYST

With the growth of enterprise it becomes impossible to control all the flows of material assets movement for searching of fraud schemes — it is beyond the limit of human capability, and internal audit and security specialists cannot track all the precedents.

The Stop-Loss system is a tool that provides monitoring of suspicious activity on all financial and assets flows and provides a quick, competent and varied analysis for specialists of internal audit and security managers.

Therefore, the Stop-Loss system opens brand new resource for financial growth and prosperity.

THE INFORMATION SYSTEM IS AN INCORRUPTIBLE ANALYST

System contains a knowledge base of variety fraudulent schemes and method of their settlement

Receives and saves data from various systems, also saves history of documents changes

Analysis data to detect the presence of signs of abuse and stealing

Finds every fraud incident

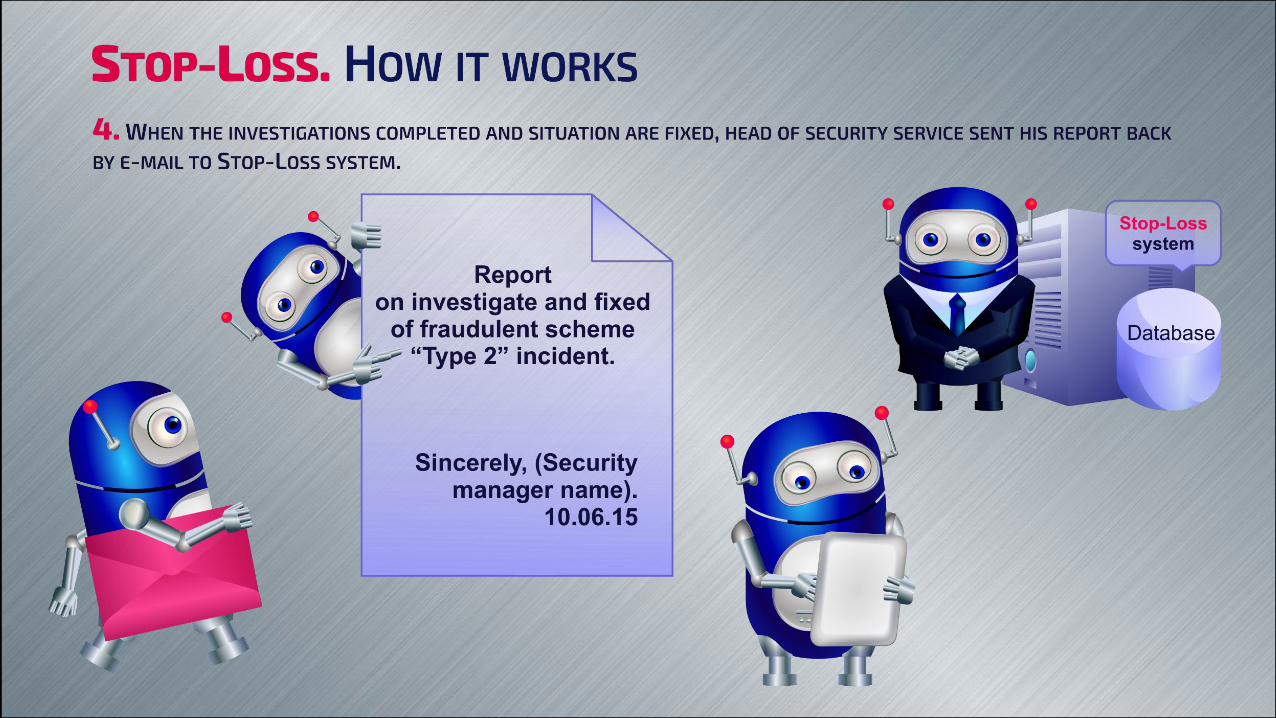

Writes reports to security managers with the results of analysis and recommended regulating method

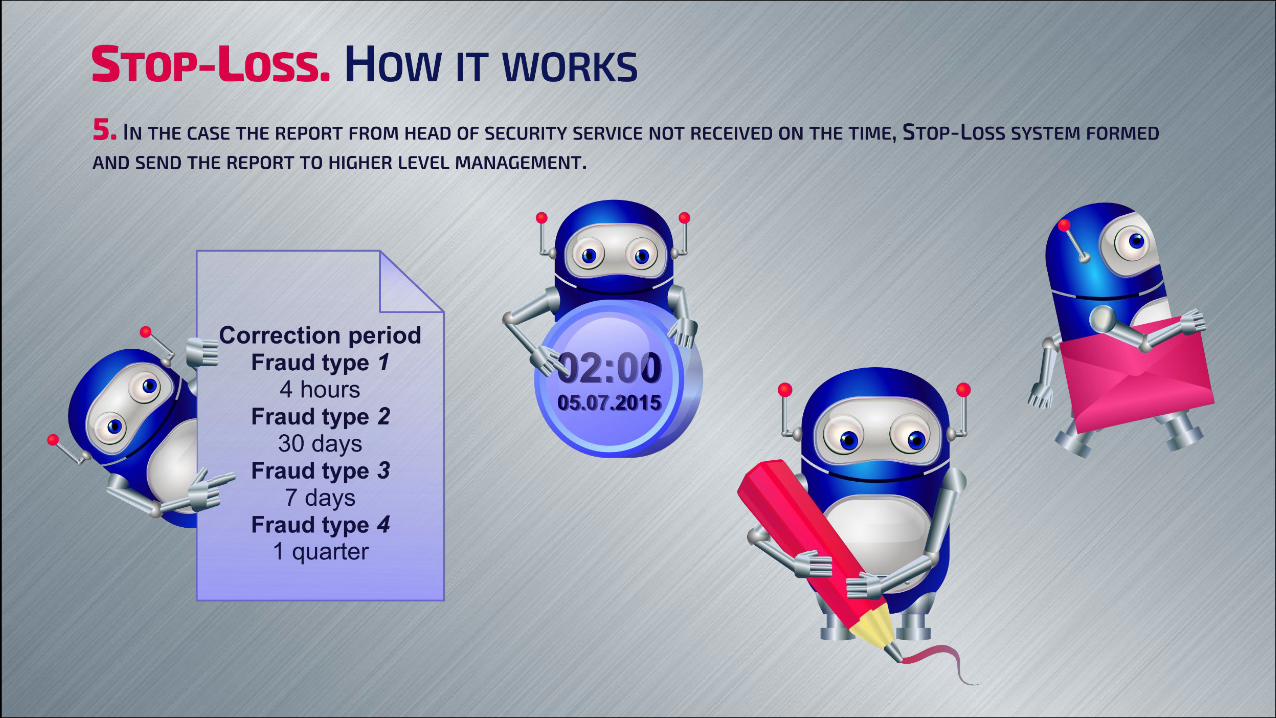

Requires reports about settling of the situations

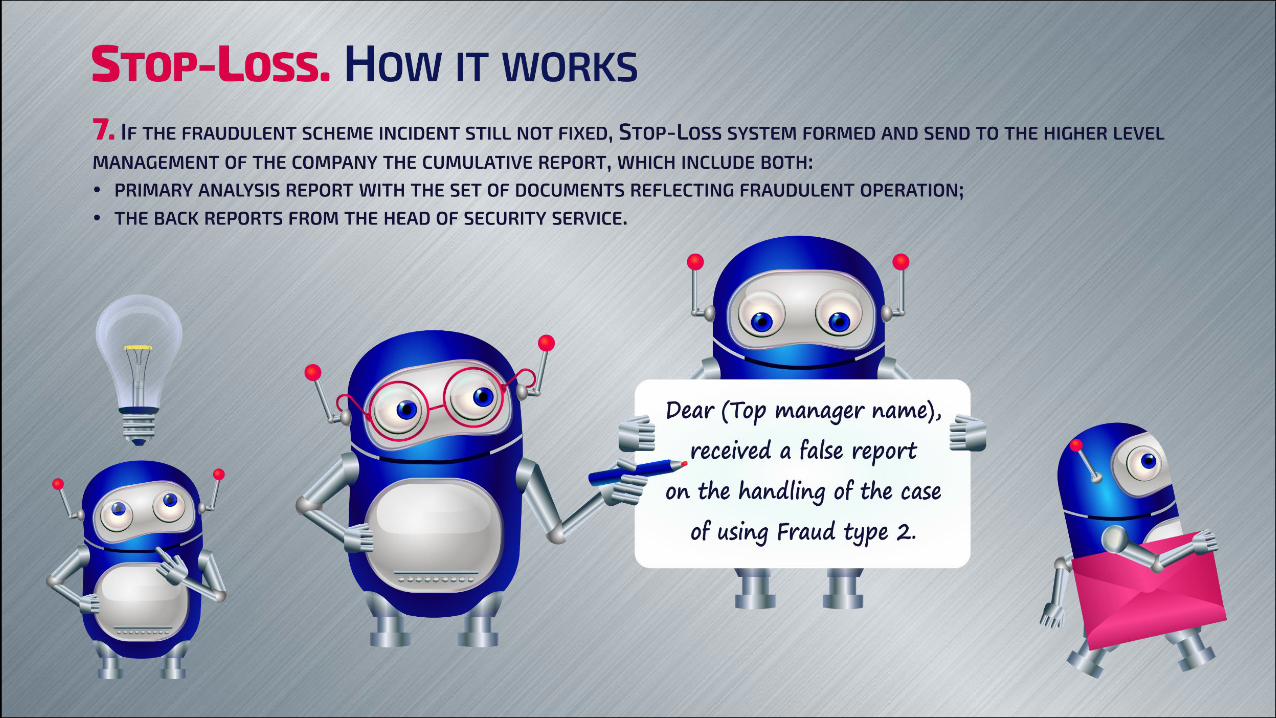

In case of non resolving incident satisfactorily, sends the report to the upper level of management

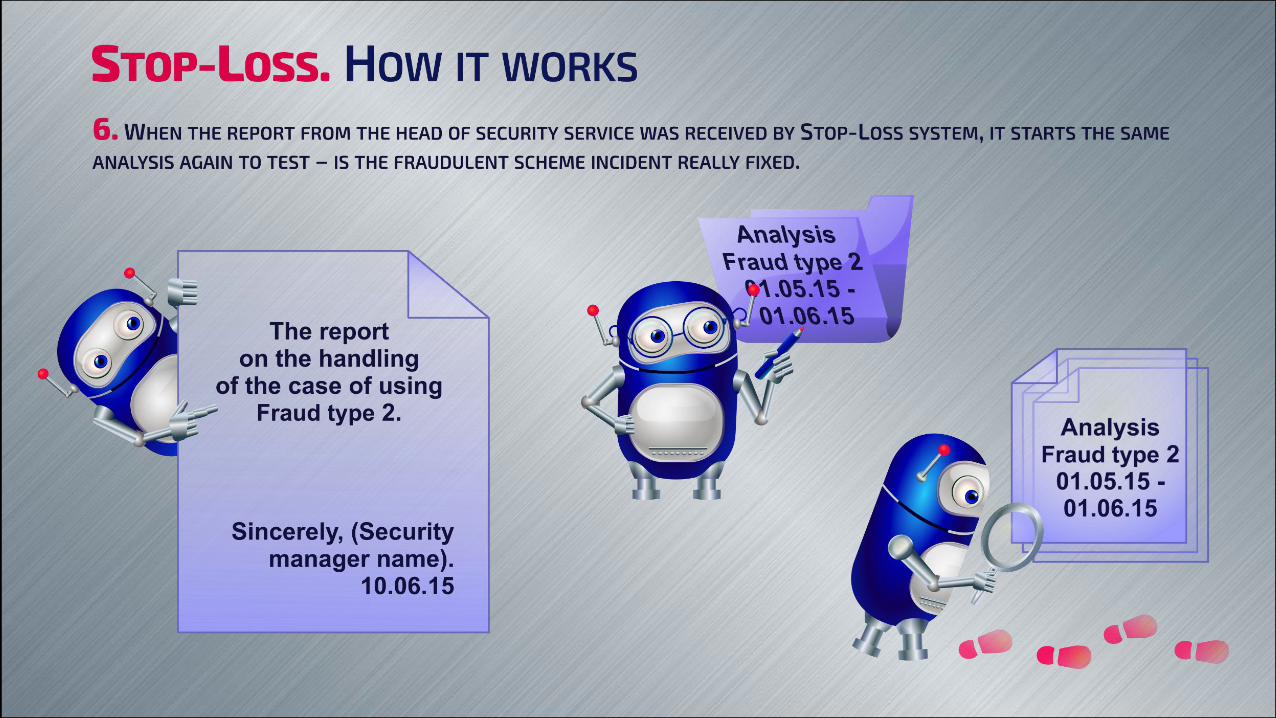

Upon receipt of the performance report the system repeats the analysis

If the violations have not been eliminated, the system sends report to the upper level of management (up to founders)

STOP-LOSS –ELECTRONIC GUARD OF YOUR ASSETSWorks on systems implementation provide all the needed data about specific aspects of this corporation:

Stage 1. Investigation with the purpose to detect fraudulent schemes specific for this corporation

Stage 2. Investigation of software tools and documents flows reflecting the movement of material assets

Stage 3. Development of the solutions for detect and prevent money leaks using administrative and technical tools

Stage 4. Preparation of the Technical specification for the system implementation, which specified functionality for detect and prevent fraudulent schemes and take into account specificity of documents flows

Stage 5. Development, configuration and implementation of Stop-Loss system

As a result of the information systems investigation, founders will have objective information about incidents of using several types of the fraudulent schemes in the corporation and have the opportunity to estimate the incidence of theft, as well as to develop solutions to reduce them.

ELECTRONIC GUARD OF YOUR ASSETS –

STOP-LOSS.CO

ORDER YOUR ENTERPRISE INSPECTION

PROTECT YOURSELF FROM UNNECESSARY LOSSES!

© 2015. Stop-Loss. All rights reserved.

Dmitry Lialin

+1 (727) 240-85-75

Boronin Sergei

+7 (906) 077-97-33

Boronina Olga

+7 (903) 226-56-77

ORDER YOUR

ENTERPRISE

INSPECTION