storyboard - financialservices.royalcommission.gov.au · sharon simcoe 171017 this is the audit...

TRANSCRIPT

1

Message Train eLearning | Commercial in Confidence

StoryboardClient: Westpac Module: Automotive Accreditation Program - Responsible Lending

File Name: RL_Storyboard_Audit_ready_171017 Date: 17/10/17

1. How to use this document.Queries directed to you will be marked with a highlight Westpac– and a question from us. Please provide answers or feedback to the best of your ability. Should several people review this document, please ensure the main reviewer consolidates all comments.Please make all changes with Track Changes ON. You may make direct changes to the text appearing on screen, as well as notes in the right-hand column.Please provide us with your comments in “3. Review Log” below

2. How this document worksId Screen Details Screen shot of current courseNew Page – This Row indicates a new screen will display1.0 Title: Page title in bold

Text in black will be displayed on screen.

Text in grey is voice over and will not appear on screen.

Text in blue will not appear on screen.

<This format indicates an incomplete area.>

Icon represents the main learning strategy used in this section of the course.

Note, when the learner has completed an activity the next button will become active, and a prompt labelled ‘Click to continue’ will appear above the arrow.

3. Review LogReviewer Name Review Date CommentsSharon Simcoe 171017 This is the audit ready script for modules online. Please note this was transferred to our storyboard template for audit

script purposes only for MT to provide to Westpac for AUDIT – the Instructional Design on the original project was completed by the Westpac team and provided in power-points.

WBC.100.009.4879CONFIDENTIAL

R

• ~

• =

• ~

• =

2

Message Train eLearning | Commercial in Confidence

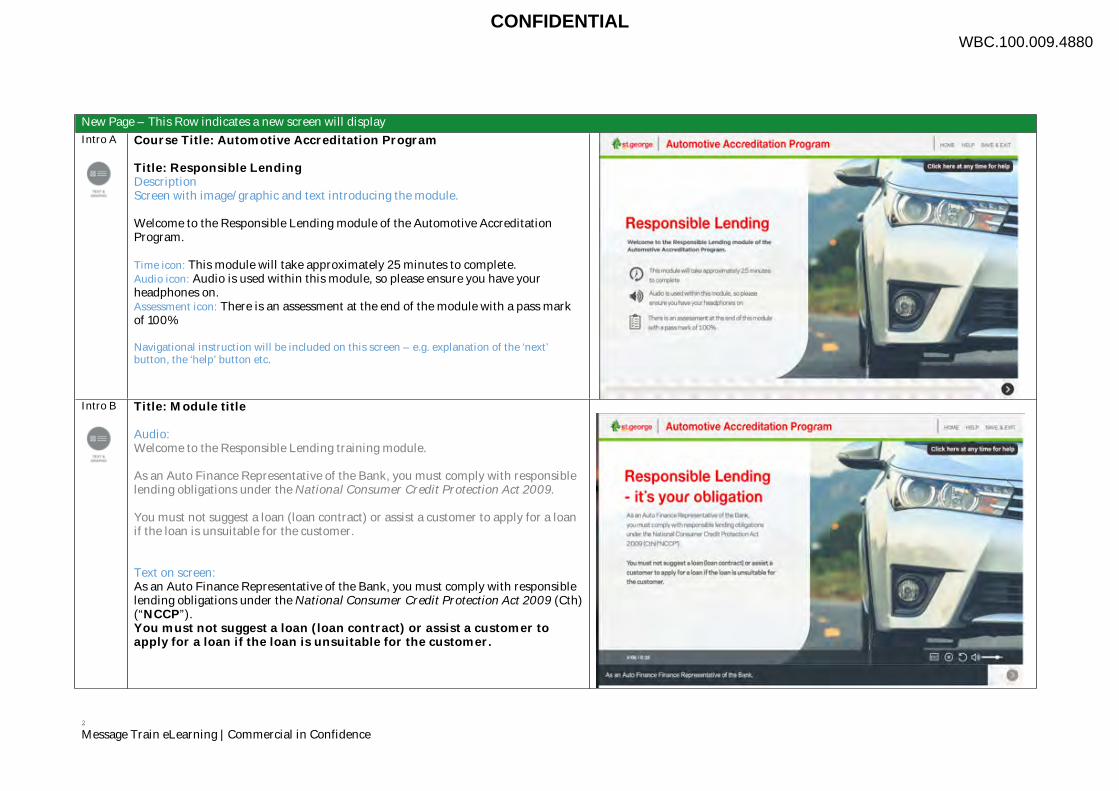

New Page – This Row indicates a new screen will displayIntro A Course Title: Automotive Accreditation Program

Title: Responsible LendingDescriptionScreen with image/graphic and text introducing the module.

Welcome to the Responsible Lending module of the Automotive Accreditation Program.

Time icon: This module will take approximately 25 minutes to complete. Audio icon: Audio is used within this module, so please ensure you have your headphones on. Assessment icon: There is an assessment at the end of the module with a pass mark of 100%

Navigational instruction will be included on this screen – e.g. explanation of the ‘next’ button, the ‘help’ button etc.

Intro B Title: Module title

Audio:Welcome to the Responsible Lending training module.

As an Auto Finance Representative of the Bank, you must comply with responsible lending obligations under the National Consumer Credit Protection Act 2009.

You must not suggest a loan (loan contract) or assist a customer to apply for a loan if the loan is unsuitable for the customer.

Text on screen:As an Auto Finance Representative of the Bank, you must comply with responsible lending obligations under the National Consumer Credit Protection Act 2009 (Cth) (“NCCP”).You must not suggest a loan (loan contract) or assist a customer to apply for a loan if the loan is unsuitable for the customer.

WBC.100.009.4880CONFIDENTIAL

•

•

RespOrlSible Lending

------~----'" .. --..0_-"',~ .-" ..... __ .. -........ ----~ "', _u_~ .... ~ ... _ IO! ....... _."""

Responsible Lending • it's your obligation ~.,'-.-~---.... , ~-.-- -_ .. _--_ .. -""--_. -_. _ .. _ ...... ,_.---

•

•

RespOrlSible Lending

------~----'" .. --..0_-"',~ .-" ..... __ .. -........ ----~ "', _u_~ .... ~ ... _ IO! ....... _."""

Responsible Lending • it's your obligation ~.,'-.-~---.... , ~-.-- -_ .. _--_ .. -""--_. -_. _ .. _ ...... ,_.---

3

Message Train eLearning | Commercial in Confidence

Id Screen Details Screen shot of current courseNew Page – This Row indicates a new screen will display1.0

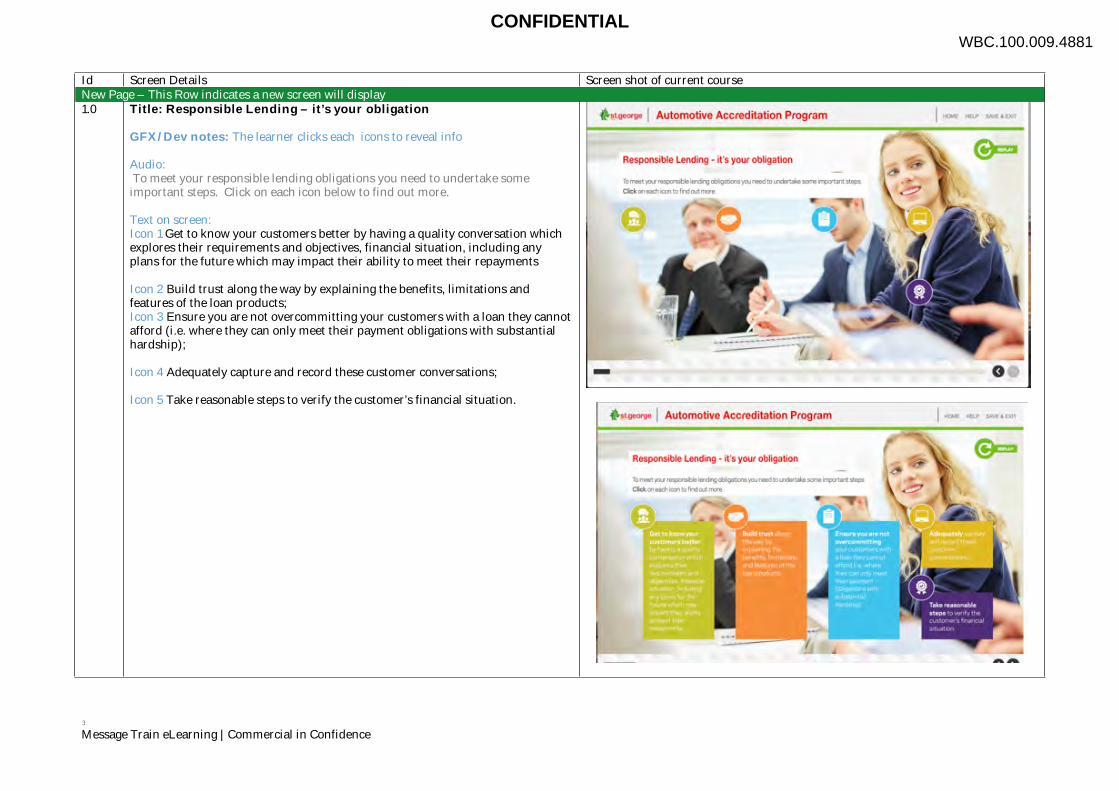

Title: Responsible Lending – it’s your obligation

GFX/Dev notes: The learner clicks each icons to reveal info

Audio: To meet your responsible lending obligations you need to undertake some important steps. Click on each icon below to find out more.

Text on screen:Icon 1 Get to know your customers better by having a quality conversation which explores their requirements and objectives, financial situation, including any plans for the future which may impact their ability to meet their repayments

Icon 2 Build trust along the way by explaining the benefits, limitations and features of the loan products;Icon 3 Ensure you are not overcommitting your customers with a loan they cannot afford (i.e. where they can only meet their payment obligations with substantial hardship);

Icon 4 Adequately capture and record these customer conversations;

Icon 5 Take reasonable steps to verify the customer’s financial situation.

WBC.100.009.4881CONFIDENTIAL

1-

.. ~,-.,. "'-......; ." .... ..... -

._--..... _""_._---_. __ ... a<_

-

1-

.. ~,-.,. "'-......; ." .... ..... -

._--..... _""_._---_. __ ... a<_

-

4

Message Train eLearning | Commercial in Confidence

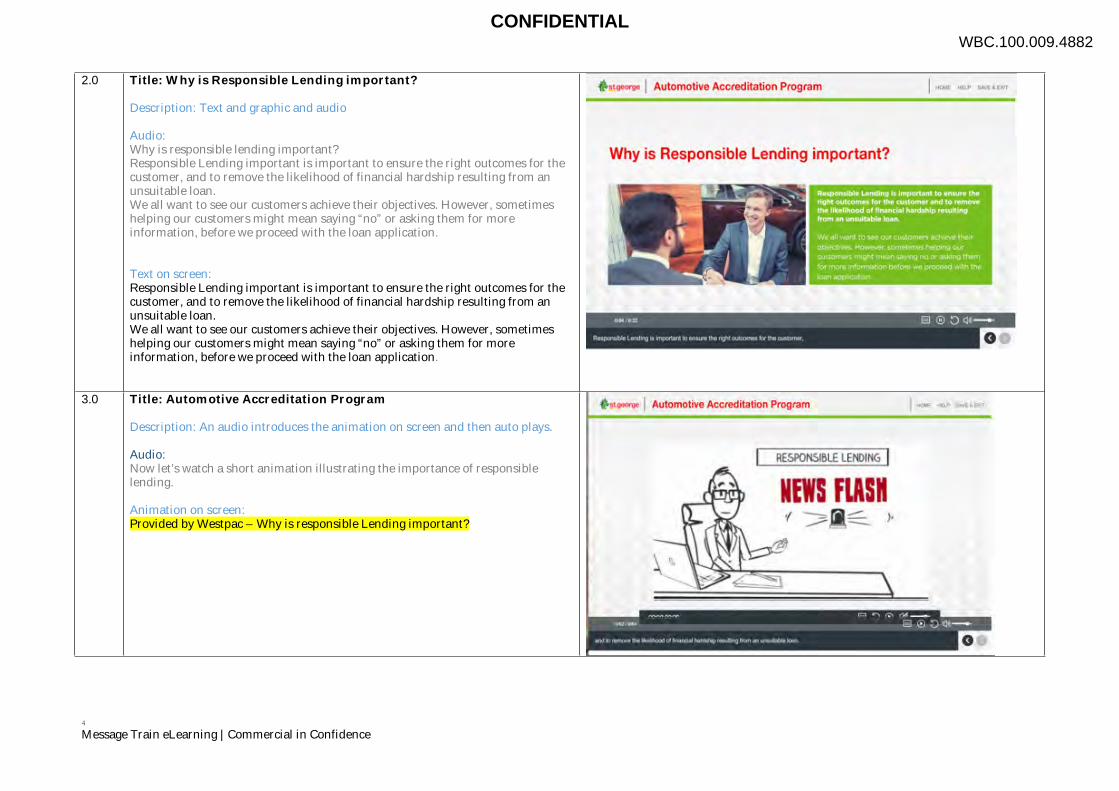

2.0 Title: Why is Responsible Lending important?

Description: Text and graphic and audio

Audio:Why is responsible lending important?Responsible Lending important is important to ensure the right outcomes for the customer, and to remove the likelihood of financial hardship resulting from an unsuitable loan.We all want to see our customers achieve their objectives. However, sometimes helping our customers might mean saying “no” or asking them for more information, before we proceed with the loan application.

Text on screen:Responsible Lending important is important to ensure the right outcomes for the customer, and to remove the likelihood of financial hardship resulting from an unsuitable loan.We all want to see our customers achieve their objectives. However, sometimes helping our customers might mean saying “no” or asking them for more information, before we proceed with the loan application.

3.0 Title: Automotive Accreditation Program

Description: An audio introduces the animation on screen and then auto plays.

Audio: Now let’s watch a short animation illustrating the importance of responsible lending.

Animation on screen:Provided by Westpac – Why is responsible Lending important?

WBC.100.009.4882CONFIDENTIAL

Why is Responsible Lending import.::lnt?

_ _ .-., " ~ "'-. ... .

MEWS flASI f -- ,..~ }o ~ .. -

-

Why is Responsible Lending import.::lnt?

_ _ .-., " ~ "'-. ... .

MEWS flASI f -- ,..~ }o ~ .. -

-

5

Message Train eLearning | Commercial in Confidence

4.0 Title: How will you comply with your responsible lending obligations?

Description: Audio introduces 3 steps – the screen comes to life in colour as the voice over explains the steps.

Audio:Meeting your responsible lending obligations will require you to take three steps.Make reasonable inquiries about your customer’s requirements and objectives.Make reasonable inquiries about your customer’s financial situation.Assess the loan as “not unsuitable” for your customer based on steps 1 and 2.

But what does “reasonable inquiries” and reasonable steps to verify” mean? Continue to find out more.

Text on screen:1. REQUIREMENTSAND OBJECTIVESMake reasonable inquiries about the customer’s requirements and objectives.2FINANCIALSITUATIONMake reasonable inquiries about the customer’s financial situation.3SUITABILITY ASSESSMENTAssess the loan as “not unsuitable” for your customer based on steps 1 and 2

Continue to find out what “reasonable inquiries” and “reasonable steps to verify” mean

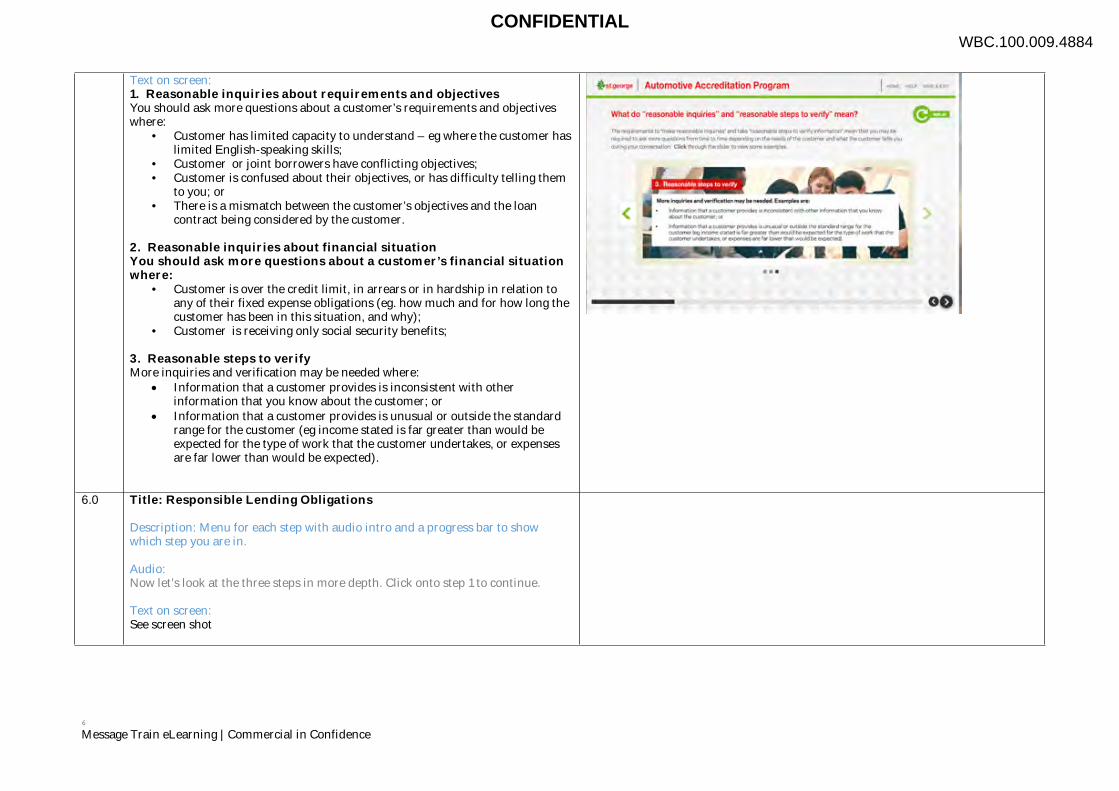

5.0 Title: What do “reasonable inquiries” and “reasonable steps to verify” mean?

Audio introduces screen and to click through the slider.

Audio:The requirements to “make reasonable inquiries” and take “reasonable steps to verify information” mean that you may be required to ask more questions from time to time depending on the needs of the customer and what the customer tells you during your conversation. Click through the slider to view some examples..

WBC.100.009.4883CONFIDENTIAL

Ho'" w;U you compll .. ~h yourfespomible Iinding obIi1l~tion.7

--.~-----,-

1010,", will you comply with ~'OUI IMPGnsibio

I!nding obligations?

,--....... ""'" .~ ....... ----. -.-~-. - .- -~-- .. ~----~--.-

••

Ho'" w;U you compll .. ~h yourfespomible Iinding obIi1l~tion.7

--.~-----,-

1010,", will you comply with ~'OUI IMPGnsibio

I!nding obligations?

,--....... ""'" .~ ....... ----. -.-~-. - .- -~-- .. ~----~--.-

••

6

Message Train eLearning | Commercial in Confidence

Text on screen:1. Reasonable inquiries about requirements and objectives You should ask more questions about a customer’s requirements and objectives where:

• Customer has limited capacity to understand – eg where the customer has limited English-speaking skills;

• Customer or joint borrowers have conflicting objectives;• Customer is confused about their objectives, or has difficulty telling them

to you; or • There is a mismatch between the customer’s objectives and the loan

contract being considered by the customer.

2. Reasonable inquiries about financial situation You should ask more questions about a customer’s financial situation where:

• Customer is over the credit limit, in arrears or in hardship in relation to any of their fixed expense obligations (eg. how much and for how long the customer has been in this situation, and why);

• Customer is receiving only social security benefits;

3. Reasonable steps to verify More inquiries and verification may be needed where:

Information that a customer provides is inconsistent with other information that you know about the customer; or

Information that a customer provides is unusual or outside the standard range for the customer (eg income stated is far greater than would be expected for the type of work that the customer undertakes, or expenses are far lower than would be expected).

6.0 Title: Responsible Lending Obligations

Description: Menu for each step with audio intro and a progress bar to show which step you are in.

Audio:Now let’s look at the three steps in more depth. Click onto step 1 to continue.

Text on screen:See screen shot

WBC.100.009.4884CONFIDENTIAL

_ I.........,... __ p_ 1- , ",

...... "--"- _~--r_

~ ~-.------"----~------... -.--.. ~,.-.. ---~ ---_ .. _---~ ~ < •. __ . __ ....... ___ ~h ~ , ___ . _____ ON_._; n w _________ h_

•• • " ,

eo

_ I.........,... __ p_ 1- , ",

...... "--"- _~--r_

~ ~-.------"----~------... -.--.. ~,.-.. ---~ ---_ .. _---~ ~ < •. __ . __ ....... ___ ~h ~ , ___ . _____ ON_._; n w _________ h_

•• • " ,

eo

7

Message Train eLearning | Commercial in Confidence

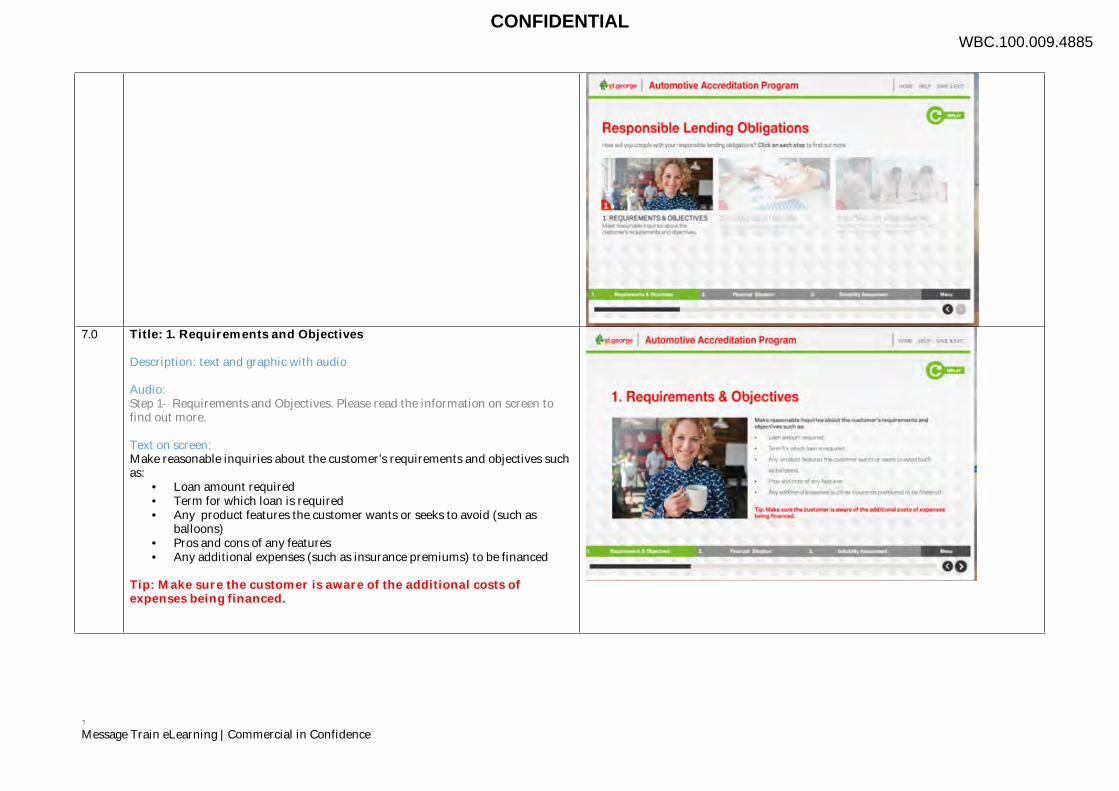

7.0 Title: 1. Requirements and Objectives

Description: text and graphic with audio

Audio:Step 1- Requirements and Objectives. Please read the information on screen to find out more.

Text on screen:Make reasonable inquiries about the customer’s requirements and objectives such as:

• Loan amount required• Term for which loan is required• Any product features the customer wants or seeks to avoid (such as

balloons)• Pros and cons of any features• Any additional expenses (such as insurance premiums) to be financed

Tip: Make sure the customer is aware of the additional costs of expenses being financed.

WBC.100.009.4885CONFIDENTIAL

- _ .. ResI)(lnsibl8 Lending OOltg~lions

,"-"._ .... ___ ... _.R ---_.- . -- - -

0 0

1. Reqyirementl & Objective3 ____ R __ _ ---"--_._''-..... .- _._-- -.. __ • __ M ', __ M_._. ___ ._ --

_.- -_. -- -00

- _ .. ResI)(lnsibl8 Lending OOltg~lions

,"-"._ .... ___ ... _.R ---_.- . -- - -

0 0

1. Reqyirementl & Objective3 ____ R __ _ ---"--_._''-..... .- _._-- -.. __ • __ M ', __ M_._. ___ ._ --

_.- -_. -- -00

8

Message Train eLearning | Commercial in Confidence

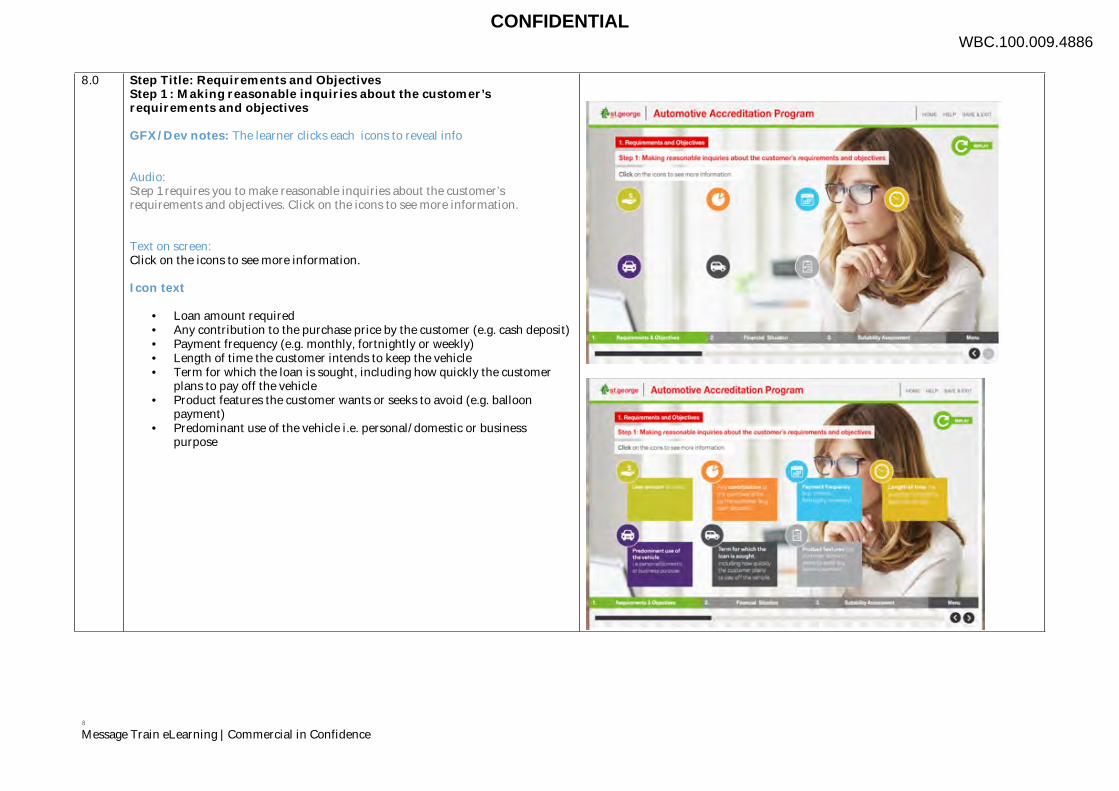

8.0 Step Title: Requirements and ObjectivesStep 1 : Making reasonable inquiries about the customer’s requirements and objectives

GFX/Dev notes: The learner clicks each icons to reveal info

Audio:Step 1 requires you to make reasonable inquiries about the customer’s requirements and objectives. Click on the icons to see more information.

Text on screen:Click on the icons to see more information.

Icon text

• Loan amount required• Any contribution to the purchase price by the customer (e.g. cash deposit) • Payment frequency (e.g. monthly, fortnightly or weekly)• Length of time the customer intends to keep the vehicle• Term for which the loan is sought, including how quickly the customer

plans to pay off the vehicle• Product features the customer wants or seeks to avoid (e.g. balloon

payment) • Predominant use of the vehicle i.e. personal/domestic or business

purpose

WBC.100.009.4886CONFIDENTIAL

... Ii

'" " _. -~ .. -.---

c

... Ii

'" " _. -~ .. -.---

c

9

Message Train eLearning | Commercial in Confidence

9.0 Title: Requirements and ObjectivesStep 1 : You also need to do the followingDescription: Text in blue will not appear on screen.

Audio:You also need to do the following:Click on the icons to see more information.

Text on screen:Click on the icons to see more information.

Icon text

You also need to do the following:• explain fees and charges (e.g. early termination fees and break costs)• if a balloon payment is requested, discuss the implications and

additional costs• discuss options for dealing with negative equity (if applicable)• ensure the sale of any third party add-on insurance products are

reasonable and appropriate for the customer

10.0 Title: 1.Requirements and ObjectivesMaking reasonable inquiries about predominant use of the vehicle

Audio:The National Credit Code (“NCC”) applies to loans given for predominantly personal, domestic or household purposes. Please read the information on screen to find out more.

Text on screen:The National Credit Code (“NCC”) applies to loans given for predominantly personal, domestic or household purposes.The NCC does not apply if the loan is wholly or predominantly for business purposes i.e. if the asset is being used for more than 50% for business purposes. You have a responsibility to make reasonable enquiries to ensure that this is the case. If a customer requests a business product, a business purpose declaration (BPD) must be signed by the customer before entering into the loan contract.A BPD cannot be relied on if you knew it was false or reasonable enquiries would have proved otherwise. In this case an offence may have been committed.To avoid any likelihood of a breach, if a customer does not have an Australian Business Number (“ABN”), the only product that should be offered is a consumer Fixed Rate Loan.

WBC.100.009.4887CONFIDENTIAL

-...... -----~ .. -... _ ....... __ ... _ .. _.

~-.-~-

~ ... --.. -.-.-.-.--.-----~-~-.-------'._--_._---_ .. _--_ ..... -... _._ ... __ ._------.~-----,--_ .. _. __ ._.--------.-.. ---... -~-. ---.. --.~-_._ ._- ,-- ...

00

-...... -----~ .. -... _ ....... __ ... _ .. _.

~-.-~-

~ ... --.. -.-.-.-.--.-----~-~-.-------'._--_._---_ .. _--_ ..... -... _._ ... __ ._------.~-----,--_ .. _. __ ._.--------.-.. ---... -~-. ---.. --.~-_._ ._- ,-- ...

00

10

Message Train eLearning | Commercial in Confidence

Tip: Additional supporting evidence will be required for approval if an individual without an ABN insists on a business loan.

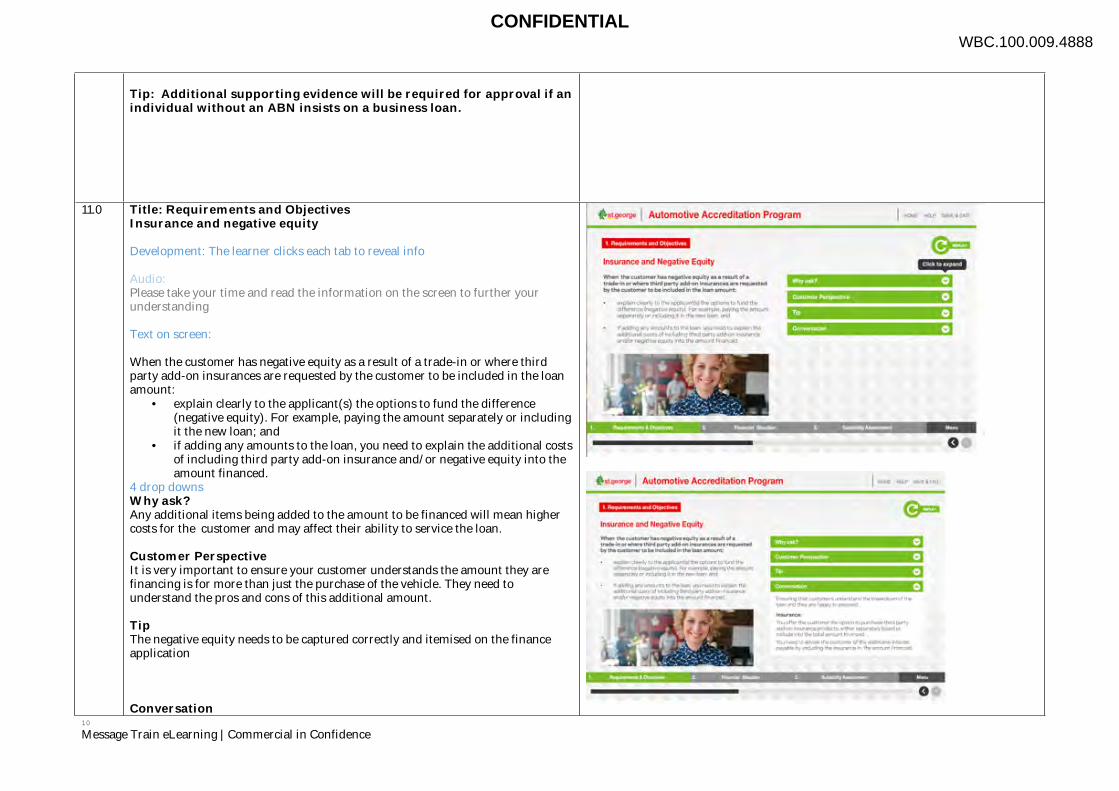

11.0 Title: Requirements and ObjectivesInsurance and negative equity

Development: The learner clicks each tab to reveal info

Audio:Please take your time and read the information on the screen to further your understanding

Text on screen:

When the customer has negative equity as a result of a trade-in or where third party add-on insurances are requested by the customer to be included in the loan amount:

• explain clearly to the applicant(s) the options to fund the difference (negative equity). For example, paying the amount separately or including it the new loan; and

• if adding any amounts to the loan, you need to explain the additional costs of including third party add-on insurance and/or negative equity into the amount financed.

4 drop downsWhy ask?Any additional items being added to the amount to be financed will mean higher costs for the customer and may affect their ability to service the loan.

Customer PerspectiveIt is very important to ensure your customer understands the amount they are financing is for more than just the purchase of the vehicle. They need to understand the pros and cons of this additional amount.

TipThe negative equity needs to be captured correctly and itemised on the finance application

Conversation

WBC.100.009.4888CONFIDENTIAL

" p p i -----.. -'--......... ~. _._ ... _-----~-------~-- ~-... -~-----~,.-----.-.. ~-- .. . ---.~---"---' ---- .. -~

_ ... _-

--

--. ----.. ----~-- .. ---------

,. -

.-~~ ... -- .... ~-..-------~-- .. -.--------- ---

-- , -- . -- -.0

.. ~.

••

" p p i -----.. -'--......... ~. _._ ... _-----~-------~-- ~-... -~-----~,.-----.-.. ~-- .. . ---.~---"---' ---- .. -~

_ ... _-

--

--. ----.. ----~-- .. ---------

,. -

.-~~ ... -- .... ~-..-------~-- .. -.--------- ---

-- , -- . -- -.0

.. ~.

••

11

Message Train eLearning | Commercial in Confidence

Ensuring that customers understand the breakdown of the loan and they are happy to proceed. InsuranceYou offer the customer the option to purchase third party add-on insurance products, either separately (cash) or include into the total amount financed. You need to advise the customer of the additional interest payable by including the insurance in the amount financed.

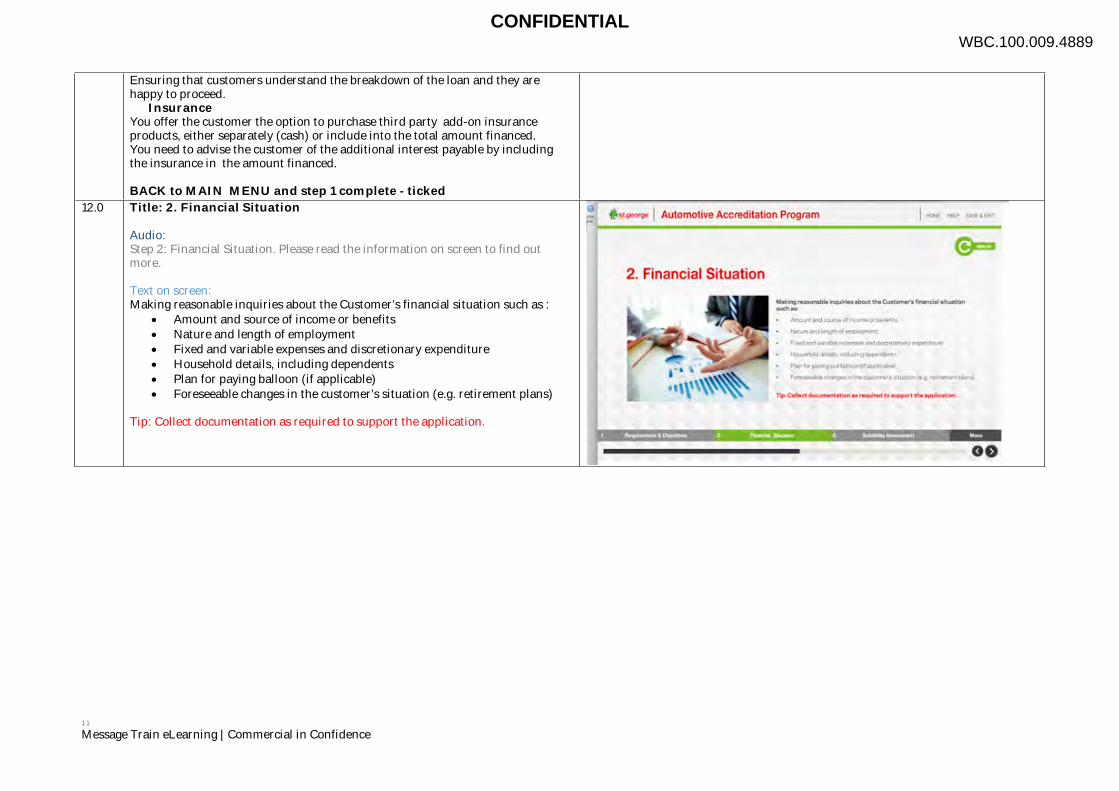

BACK to MAIN MENU and step 1 complete - ticked12.0 Title: 2. Financial Situation

Audio:Step 2: Financial Situation. Please read the information on screen to find out more.

Text on screen:Making reasonable inquiries about the Customer’s financial situation such as :

Amount and source of income or benefits Nature and length of employment Fixed and variable expenses and discretionary expenditure Household details, including dependents Plan for paying balloon (if applicable) Foreseeable changes in the customer’s situation (e.g. retirement plans)

Tip: Collect documentation as required to support the application.

WBC.100.009.4889CONFIDENTIAL

1--,

.2. Fin80ciBI Situ8ti"n ---_ .. ----------- --- -- -----.-.. ------- -_ .. -

o.

1--,

.2. Fin80ciBI Situ8ti"n ---_ .. ----------- --- -- -----.-.. ------- -_ .. -

o.

12

Message Train eLearning | Commercial in Confidence

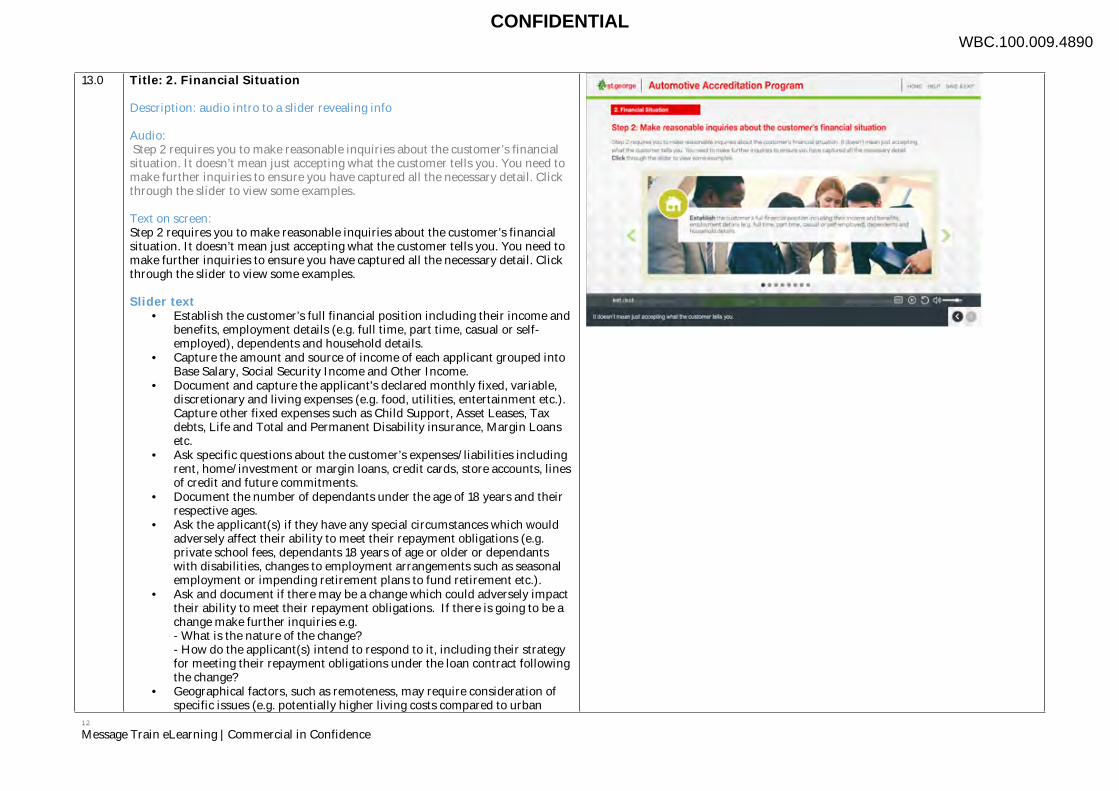

13.0 Title: 2. Financial Situation

Description: audio intro to a slider revealing info

Audio: Step 2 requires you to make reasonable inquiries about the customer’s financial situation. It doesn’t mean just accepting what the customer tells you. You need to make further inquiries to ensure you have captured all the necessary detail. Click through the slider to view some examples.

Text on screen:Step 2 requires you to make reasonable inquiries about the customer’s financial situation. It doesn’t mean just accepting what the customer tells you. You need to make further inquiries to ensure you have captured all the necessary detail. Click through the slider to view some examples.

Slider text• Establish the customer’s full financial position including their income and

benefits, employment details (e.g. full time, part time, casual or self-employed), dependents and household details.

• Capture the amount and source of income of each applicant grouped into Base Salary, Social Security Income and Other Income.

• Document and capture the applicant's declared monthly fixed, variable, discretionary and living expenses (e.g. food, utilities, entertainment etc.). Capture other fixed expenses such as Child Support, Asset Leases, Tax debts, Life and Total and Permanent Disability insurance, Margin Loans etc.

• Ask specific questions about the customer’s expenses/liabilities including rent, home/investment or margin loans, credit cards, store accounts, lines of credit and future commitments.

• Document the number of dependants under the age of 18 years and their respective ages.

• Ask the applicant(s) if they have any special circumstances which would adversely affect their ability to meet their repayment obligations (e.g. private school fees, dependants 18 years of age or older or dependants with disabilities, changes to employment arrangements such as seasonal employment or impending retirement plans to fund retirement etc.).

• Ask and document if there may be a change which could adversely impact their ability to meet their repayment obligations. If there is going to be a change make further inquiries e.g.- What is the nature of the change? - How do the applicant(s) intend to respond to it, including their strategy for meeting their repayment obligations under the loan contract following the change?

• Geographical factors, such as remoteness, may require consideration of specific issues (e.g. potentially higher living costs compared to urban

WBC.100.009.4890CONFIDENTIAL

_ .. -~----- .. -.--.-,--.---~-.--.--.,-_h __ ,.. __ • ___ a~ ___ • __ _ --.. ---_.

_ .. -~----- .. -.--.-,--.---~-.--.--.,-_h __ ,.. __ • ___ a~ ___ • __ _ --.. ---_.

13

Message Train eLearning | Commercial in Confidence

areas).

14.0 Title: 2. Financial SituationForeseeable changes or special circumstances example

Audio:Let’s take a closer look at Step 2 “Financial situation” using the example of foreseeable changes and special circumstances.

Text on screen:Let’s take a closer look at Step 2 “Financial situation” using the example of foreseeable changes and special circumstances.

WBC.100.009.4891CONFIDENTIAL

.. i!

ForeMOablc d>e~~or apccial circumon"",,, • . ~""" -_.-..... _'._ ...... --'--" --

.. i!

ForeMOablc d>e~~or apccial circumon"",,, • . ~""" -_.-..... _'._ ...... --'--" --

14

Message Train eLearning | Commercial in Confidence

15.0 Title: 2. Financial SituationForeseeable changes or special circumstances example

Development: The learner clicks each tab to reveal info

Audio: Please take your time to read the information on the screen to further your understanding.

Text on screen:To delve deeper into the customer’s financial situation, you will need to explore whether:

• there are any special circumstances which may have an impact on their future income or expenses; and

• the customer anticipates or plans any changes which would adversely affect their ability to meet their loan obligations over the loan term.

Drop down text;

Why ask?To prompt customers to think about any future changes and how it would impact their ability to service their loan.

Customer PerspectiveKnowing our customer’s financial situation to provide them with an affordable and suitable loan contract.It is your responsibility to prompt customers to think about their future and how any changes may impact their ability to make repayments.

TipIn ALL instances, any likely changes to income or expenses that are regular or ongoing need to be considered and documented

ConversationThe customer mentions they have school aged children, inquire about any future education expenses e.g. paying private school fees.The customer may mention they are retiring and their income may be reduced slightly. Enquire if their superannuation or benefit payments will cover their repayments.The customer tells you they are planning to go on maternity leave in 6 months. Enquire if they will be receiving paid parental leave or if they plan to go back to work.Prompt the customer to think about any future plans that may impact their financial situation e.g. purchase of a new home, renovations, extended holiday etc. Back to MAIN MENU with Step 2 ticked off

WBC.100.009.4892CONFIDENTIAL

Ii

--- . .... _- .--,.,,,, -..... _--_ .... --_ ..... _------.-~--=.:-- -- .-----

~.- . .::::---:--~"':' .. -~:-~-~~ .-... -~-~ .". -_. -...-.. - -~ .. - -----... _--... ---..--~_. =!::':= .. ~-~ - .. -"---, -- ... _ ... -=-=- w _ _ ~ __

- ,- ,-- ,-- -00

Ii

--- . .... _- .--,.,,,, -..... _--_ .... --_ ..... _------.-~--=.:-- -- .-----

~.- . .::::---:--~"':' .. -~:-~-~~ .-... -~-~ .". -_. -...-.. - -~ .. - -----... _--... ---..--~_. =!::':= .. ~-~ - .. -"---, -- ... _ ... -=-=- w _ _ ~ __

- ,- ,-- ,-- -00

15

Message Train eLearning | Commercial in Confidence

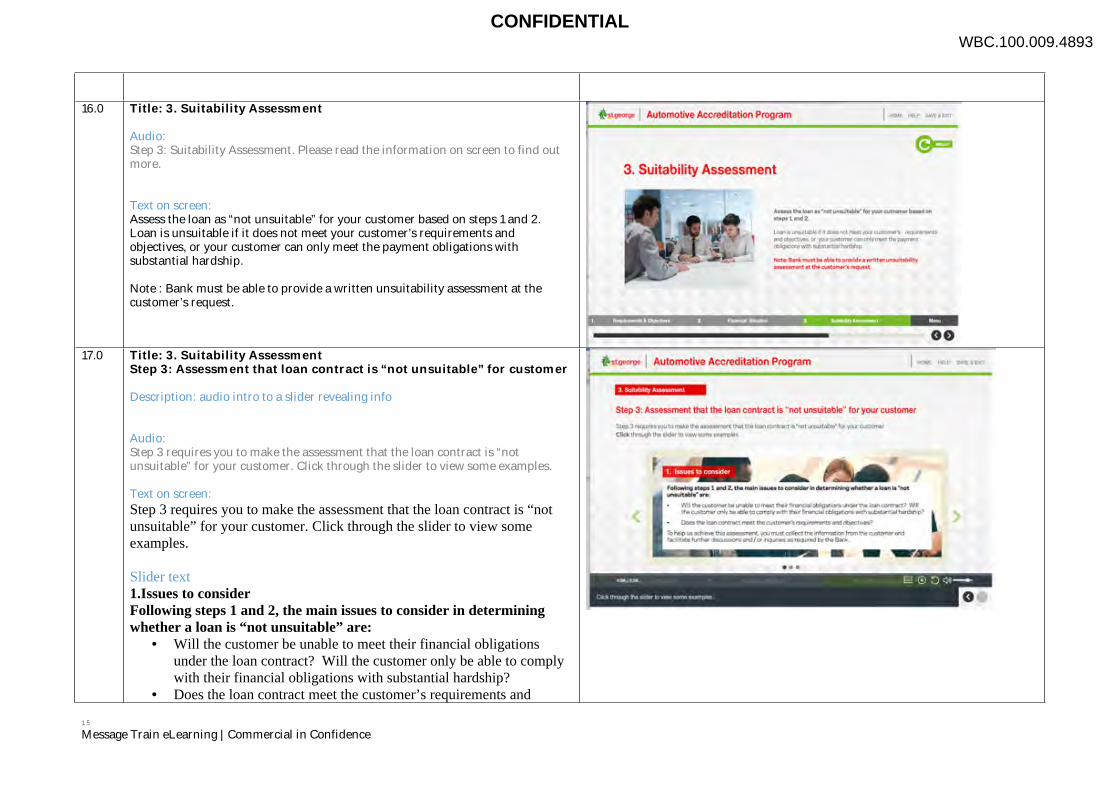

16.0 Title: 3. Suitability Assessment

Audio: Step 3: Suitability Assessment. Please read the information on screen to find out more.

Text on screen:Assess the loan as “not unsuitable” for your customer based on steps 1 and 2.Loan is unsuitable if it does not meet your customer’s requirements and objectives, or your customer can only meet the payment obligations with substantial hardship.

Note : Bank must be able to provide a written unsuitability assessment at the customer’s request.

17.0 Title: 3. Suitability AssessmentStep 3: Assessment that loan contract is “not unsuitable” for customer

Description: audio intro to a slider revealing info

Audio:Step 3 requires you to make the assessment that the loan contract is “not unsuitable” for your customer. Click through the slider to view some examples.

Text on screen:Step 3 requires you to make the assessment that the loan contract is “not unsuitable” for your customer. Click through the slider to view some examples.

Slider text1.Issues to considerFollowing steps 1 and 2, the main issues to consider in determining whether a loan is “not unsuitable” are:

• Will the customer be unable to meet their financial obligations under the loan contract? Will the customer only be able to comply with their financial obligations with substantial hardship?

• Does the loan contract meet the customer’s requirements and

WBC.100.009.4893CONFIDENTIAL

~, .........,...-- .,... ...

3_ Suitabi lity A.S$Msment

- .. - ... -~---~ -'''' --.,-~-----_ .... -_ .. ---------_ .. __ ._--~~--

•• 1-

Ii ....... ........ __ ...... .-.--.. ... --,-----.... --.--~-..... _ .. _._--

I

~,-~.~::.;-:.::.::-:.-::.:-:-:~.:.::-::.:-:::.~ .. ---- .----- .' I - .. --~- .. --.. - I .... ~-.. -,., .... -.. --.. - .. -~-,~--~ .. -. --... -- , " -- ,.-.. ~.~~~.,-,----

~, .........,...-- .,... ...

3_ Suitabi lity A.S$Msment

- .. - ... -~---~ -'''' --.,-~-----_ .... -_ .. ---------_ .. __ ._--~~--

•• 1-

Ii ....... ........ __ ...... .-.--.. ... --,-----.... --.--~-..... _ .. _._--

I

~,-~.~::.;-:.::.::-:.-::.:-:-:~.:.::-::.:-:::.~ .. ---- .----- .' I - .. --~- .. --.. - I .... ~-.. -,., .... -.. --.. - .. -~-,~--~ .. -. --... -- , " -- ,.-.. ~.~~~.,-,----

16

Message Train eLearning | Commercial in Confidence

objectives? To help us achieve this assessment, you must collect the information from the customer and facilitate further discussions and / or inquiries as required by the Bank.

2. Written Unsuitability Assessment If requested by the customer, the Bank must provide a customer with a copy of the assessment that the loan contract is not unsuitable for the customer (“Written Unsuitability Assessment”). A Written Unsuitability Assessment cannot be requested if the credit application did not proceed or was not approved by the Bank.All requests MUST be immediately referred to your Relationship Manager on the day the request is received, as there is strict timing on providing the response. The Bank will arrange to prepare the written assessment for the customer.We must keep a record of all material that forms the basis of the assessment in a way that will assist us to give the customer a written copy of the assessment.

3. Note Timing requirements for written assessment:

• If a request is made prior to a loan contract being entered into, the written assessment is to be provided by the Bank as soon as possible after receiving the request from the customer.

• If the request is made after the loan contract is entered into, and the request is within 2 years of contract commencement, the customer must be provided with a written assessment within 7 business days . Otherwise, it must be provided within 21 business days.

WBC.100.009.4894CONFIDENTIAL

17

Message Train eLearning | Commercial in Confidence

18.0 Title: 3. Suitability Assessment Balloon Payment

Audio:Let’s take a closer look at Step 3 “Suitability Assessment” using the example of a balloon payment.

Text on screen:Let’s take a closer look at Step 3 “Suitability Assessment” using the example of a balloon payment.

19.0 Title: 3. Suitability Assessment Balloon Payment

Development: The learner clicks each tab to reveal info

Audio:Please take your time and read the information on the screen to further your understanding.

Text on screen:You are required to determine whether the loan contract’s features, as determined by the customer’s requirements and objectives, are not unsuitable for the customer. This is the case when a customer requests for a balloon amount.Why ask?To clearly understand and document the customer’s requirements and objectives for a balloon and their plan for successfully making the balloon payment at the end of the period.Customer perspectiveA failure to explain and discuss this feature carefully with your customer can result in them having an unexpected payment at the end of the loan term and could cause financial distress.You should confirm that they have carefully considered the pros and cons of this feature, and whether this is the right choice for them.Tip You must ensure the customer understands the implications of having a balloon payment in their loan – that they may be paying higher interest because of it and how they will make this lump sum payment at the end of the loan term.

WBC.100.009.4895CONFIDENTIAL

Ii

Balloon Payment ............ _-.'....... -~.--

-

_.- . -- . ---- . -

--_n ___ n __ ----.. --_.-_ .. ------- 0

-.---.--~.

1 _.- . -- . ","-- -

••

Ii

Balloon Payment ............ _-.'....... -~.--

-

_.- . -- . ---- . -

--_n ___ n __ ----.. --_.-_ .. ------- 0

-.---.--~.

1 _.- . -- . ","-- -

••

18

Message Train eLearning | Commercial in Confidence

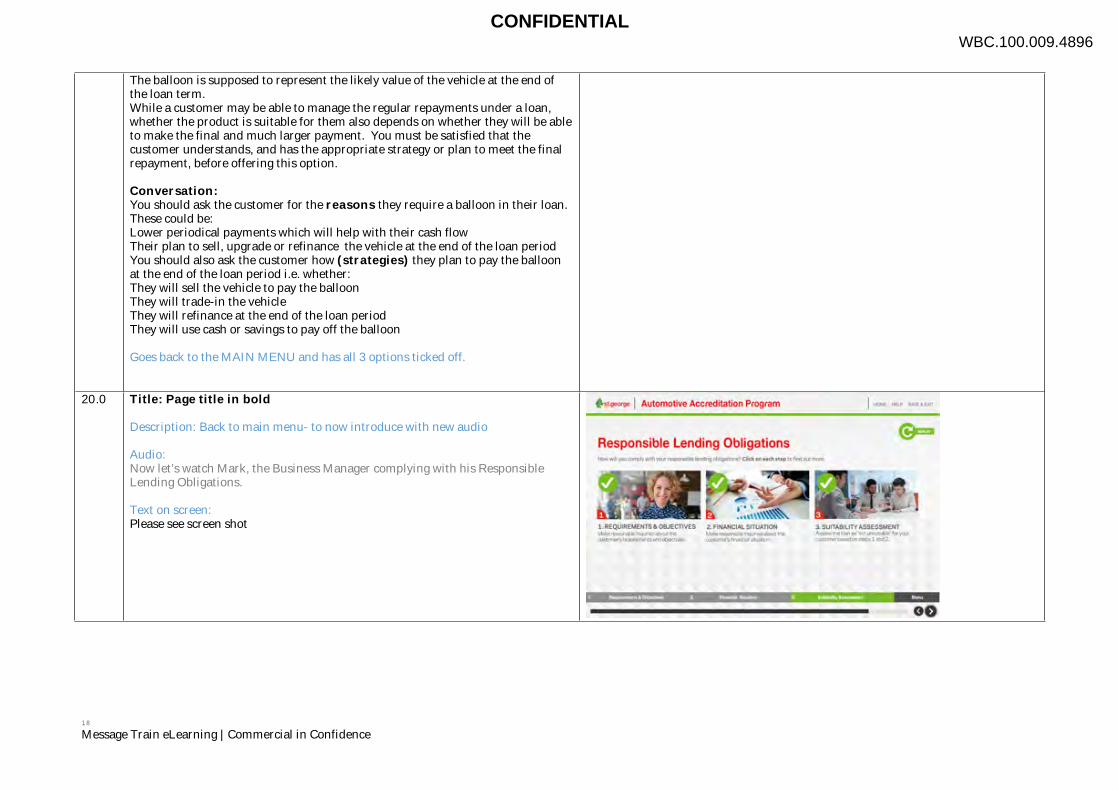

The balloon is supposed to represent the likely value of the vehicle at the end of the loan term. While a customer may be able to manage the regular repayments under a loan, whether the product is suitable for them also depends on whether they will be able to make the final and much larger payment. You must be satisfied that the customer understands, and has the appropriate strategy or plan to meet the final repayment, before offering this option.

Conversation:You should ask the customer for the reasons they require a balloon in their loan. These could be:Lower periodical payments which will help with their cash flowTheir plan to sell, upgrade or refinance the vehicle at the end of the loan periodYou should also ask the customer how (strategies) they plan to pay the balloon at the end of the loan period i.e. whether:They will sell the vehicle to pay the balloonThey will trade-in the vehicleThey will refinance at the end of the loan periodThey will use cash or savings to pay off the balloon

Goes back to the MAIN MENU and has all 3 options ticked off.

20.0 Title: Page title in bold

Description: Back to main menu- to now introduce with new audio

Audio:Now let’s watch Mark, the Business Manager complying with his Responsible Lending Obligations.

Text on screen:Please see screen shot

WBC.100.009.4896CONFIDENTIAL

ResponsltJIe lending OblgaUoo, _ .. _ ... _-d' ' '/ o-"'''W' , ". , . ,-_.--. -- .. --- .. -

--

-- . -- ,- -

ResponsltJIe lending OblgaUoo, _ .. _ ... _-d' ' '/ o-"'''W' , ". , . ,-_.--. -- .. --- .. -

--

-- . -- ,- -

19

Message Train eLearning | Commercial in Confidence

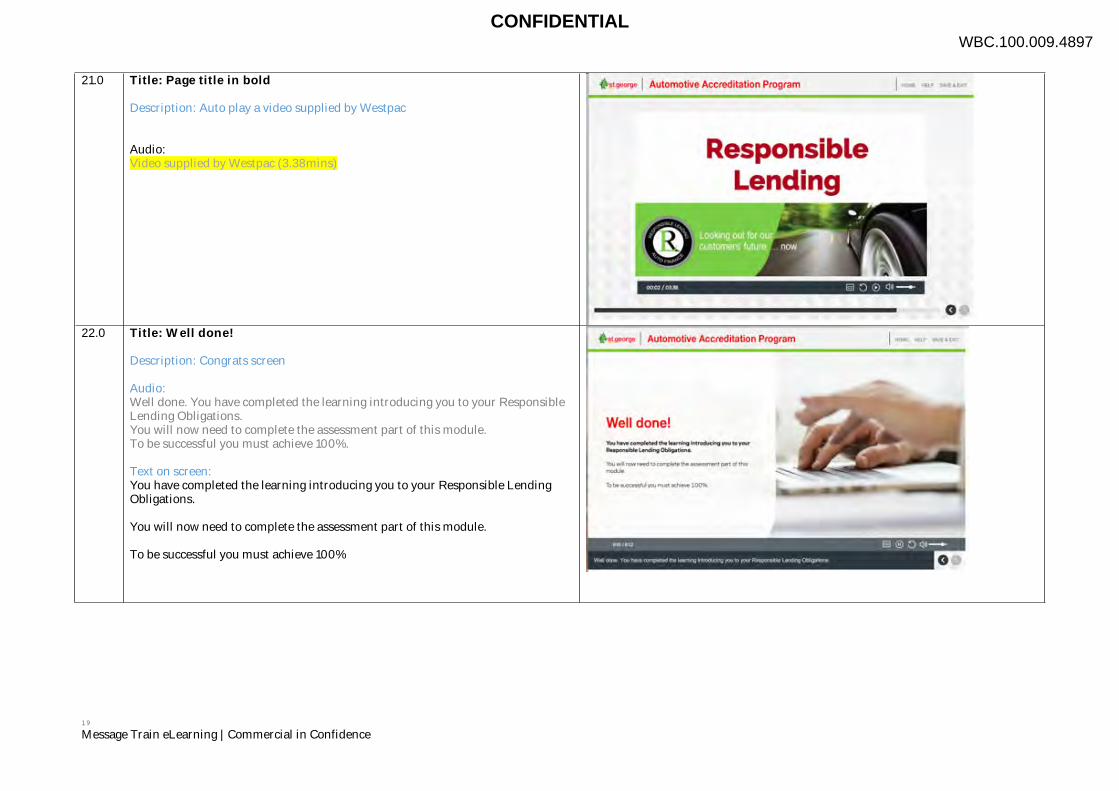

21.0 Title: Page title in bold

Description: Auto play a video supplied by Westpac

Audio: Video supplied by Westpac (3.38mins)

22.0 Title: Well done!

Description: Congrats screen

Audio:Well done. You have completed the learning introducing you to your Responsible Lending Obligations.You will now need to complete the assessment part of this module.To be successful you must achieve 100%.

Text on screen:You have completed the learning introducing you to your Responsible Lending Obligations.

You will now need to complete the assessment part of this module.

To be successful you must achieve 100%

WBC.100.009.4897CONFIDENTIAL

Responsible Lending

r-"-~

'-"-1----'*""'-

Well done! ... __ .. _-----.-. -... -~-- ....

1- - -.-

•• 1-

_ ..

,., '-"d",,_ ... _.- -.--"'.~.- ... --.~--

Responsible Lending

r-"-~

'-"-1----'*""'-

Well done! ... __ .. _-----.-. -... -~-- ....

1- - -.-

•• 1-

_ ..

,., '-"d",,_ ... _.- -.--"'.~.- ... --.~--

20

Message Train eLearning | Commercial in Confidence

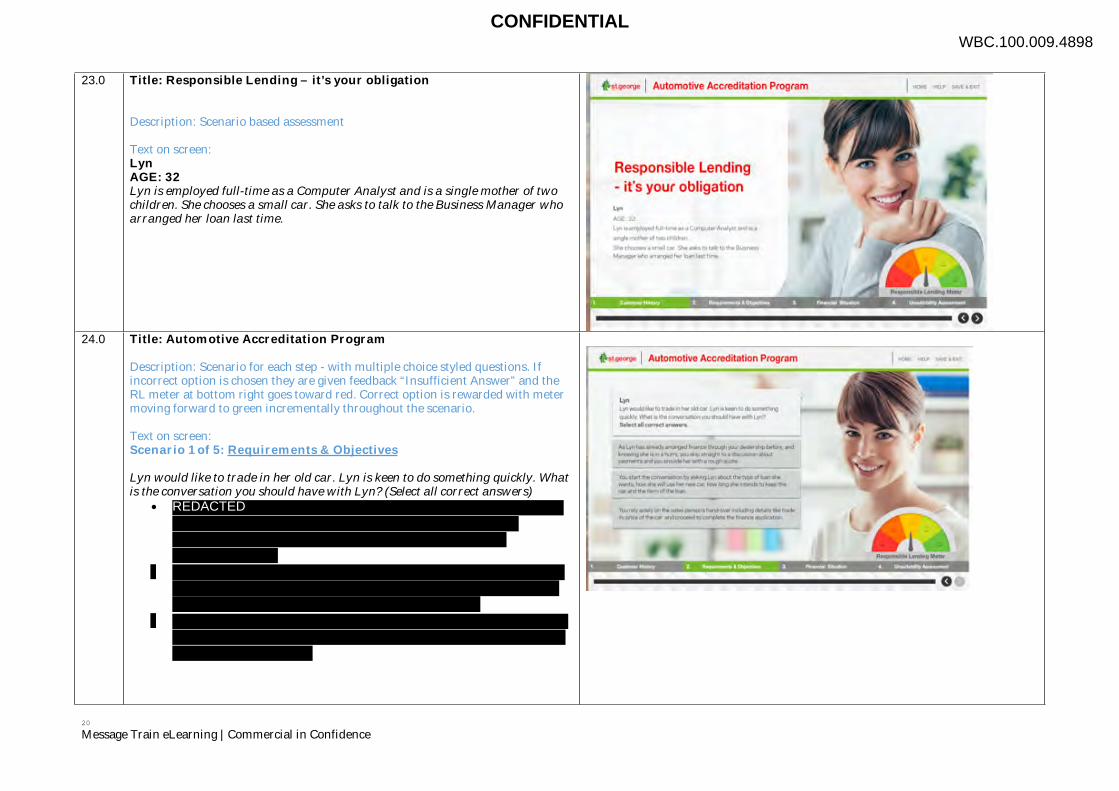

23.0 Title: Responsible Lending – it’s your obligation

Description: Scenario based assessment

Text on screen:LynAGE: 32Lyn is employed full-time as a Computer Analyst and is a single mother of two children. She chooses a small car. She asks to talk to the Business Manager who arranged her loan last time.

24.0 Title: Automotive Accreditation Program

Description: Scenario for each step - with multiple choice styled questions. If incorrect option is chosen they are given feedback “Insufficient Answer” and the RL meter at bottom right goes toward red. Correct option is rewarded with meter moving forward to green incrementally throughout the scenario.

Text on screen:Scenario 1 of 5: Requirements & Objectives

Lyn would like to trade in her old car. Lyn is keen to do something quickly. What is the conversation you should have with Lyn? (Select all correct answers)

WBC.100.009.4898CONFIDENTIAL

REDACTED

I

I

Reliponsible Lending - it's your obligation ---_._-.. _, ... ~ .. _ .... _0...

--~--

-~_ ... ,_ ... .. _, __ o_ -_ .. __ .... - ... _0_- -.... ------ --. ... ----_ .. _---_ ..... _--_ ... _, ~.-.---------------.-~ ---_._-... _---_._----~ ...... -- - ...... -..

_. -

-- . -.- . -- . --•• I

I

Reliponsible Lending - it's your obligation ---_._-.. _, ... ~ .. _ .... _0...

--~--

-~_ ... ,_ ... .. _, __ o_ -_ .. __ .... - ... _0_- -.... ------ --. ... ----_ .. _---_ ..... _--_ ... _, ~.-.---------------.-~ ---_._-... _---_._----~ ...... -- - ...... -..

_. -

-- . -.- . -- . --••

21

Message Train eLearning | Commercial in Confidence

Scenario 2 of 5You know that Lyn is already a finance customer but it has been 3 years since Lyn bought her car. Lyn now runs a small business, in addition to her full time job. She uses her car on a regular basis to attend to clients as well as for driving to and from her full time job. Lyn uses her car approximately 50% of the time for business use. (Select all correct answers)

Scenario 3 of 5You know that Lyn is in a hurry and you want to make sure you provide excellent customer service, especially as she is a repeat customer. (Select all correct answers)

Scenario 4 of 5You find out that there will be a $3000 shortfall on Lyn‘s trade-in of her car and she asks how she can cover the $3000 shortfall (negative equity). (Select all that apply)

WBC.100.009.4899CONFIDENTIAL

REDACTEDR

R

D

REDACTEDR

REDACTEDR

REDACTEDR

I

I

I

I

I

I

.... "-- .;.:-.. ---

•• --- I

I~~~·· -

---". ::;-:.-.!",:;-.;;:= ---

I

I

I

I

I

I

.... "-- .;.:-.. ---

•• --- I

I~~~·· -

---". ::;-:.-.!",:;-.;;:= ---

22

Message Train eLearning | Commercial in Confidence

Scenario 5 of 5Lyn has mentioned she would like monthly repayments but asks whether she can change the frequency of her payments during the term of the loan e.g. change from monthly to fortnightly in future. (Select all that apply)

Incorrect

WBC.100.009.4900CONFIDENTIAL

REDACTED

REDACTEDR

R

A

REDACTED

I

I

I

I

I

• ..... ~ .. -.... --~-.-. .......... _ ........ _------

--~.--.. -.. __ ......... _----.. -.--~-... ----. .~-.. -

• -_. __ ._._-_ ....... ~ ... w .... _______ .. --_._-

• -..... _ ..... _ .......... _"----_._._ ... '~-' --.---.--.

•

1--I

I

I

I

I

• ..... ~ .. -.... --~-.-. .......... _ ........ _------

--~.--.. -.. __ ......... _----.. -.--~-... ----. .~-.. -

• -_. __ ._._-_ ....... ~ ... w .... _______ .. --_._-

• -..... _ ..... _ .......... _"----_._._ ... '~-' --.---.--.

•

1--

23

Message Train eLearning | Commercial in Confidence

Congratulations

WBC.100.009.4901CONFIDENTIAL

REDACTED

REDACTED

Incorrect

-- .--------.--~--

C<)n9r~ lulotions

-~-------. ~ ---_A .. M ___ " -.--------------_ ... _----------... -~- ... --.. -. -.----.... ~ ...... -- .. --.----.---_ .. _- .. ~----.-----~. ------------... -.. ----

Incorrect

-- .--------.--~--

C<)n9r~ lulotions

-~-------. ~ ---_A .. M ___ " -.--------------_ ... _----------... -~- ... --.. -. -.----.... ~ ...... -- .. --.----.---_ .. _- .. ~----.-----~. ------------... -.. ----

24

Message Train eLearning | Commercial in Confidence

25.0 Title: Automotive Accreditation Program

Description: Scenarios continued – Financial Situation

Text on screen:Scenario 1 of 5 – Financial SituationLyn is really excited about the purchase of her new vehicle and wants to know when she can have it. What do you do next? (Select all that apply)

Scenario 2of 5You ask Lyn about her plans for the future and she mentions her plans to marry her partner and have an extended holiday over the next 12 months. (Select all correct answers)

Scenario 3 of 5Lyn is a little surprised at the extra questioning and is becoming impatient. (Select all correct answers)

WBC.100.009.4902CONFIDENTIAL

REDACTED

R

A

REDACTEDR

I

I

I

I

I

- '-,.,------ .---- .... ~.-.... ~ -----... _---_._-.------. -----.~~--- _. -~--.. -==---. -- ...

I

I

I

I

I

- '-,.,------ .---- .... ~.-.... ~ -----... _---_._-.------. -----.~~--- _. -~--.. -==---. -- ...

CONFIDENTIAL

"

I

Scenario 4 of 5 While you are capturing her income, expenses and liabilities, Ly" tells you that her living expenses are $1000 a month. (Select all correct answers)

Scenario 5 of 5 When asking Lyn if she is in arrears or excess with any loans, she advises that she is over her Credit Card limit . (Select all correct answers)

I

Message Train eLearning I Commercial in Confidence

~

~- ..... -..... --.. --_ ...... __ ......... --.-~-;;:==:==::' -.- '"---" ==-----=-.- -_._-

-- -.............. ------_._-<-.__._-- .. _-----_ .. -......... --" ... __ ... -----_ .. _... _--

Congratulations

""---~----,--

---_ .. _- -• . ---. --"'---

WBC.100.009.4903

•

•

CONFIDENTIAL

"

I

Scenario 4 of 5 While you are capturing her income, expenses and liabilities, Ly" tells you that her living expenses are $1000 a month. (Select all correct answers)

Scenario 5 of 5 When asking Lyn if she is in arrears or excess with any loans, she advises that she is over her Credit Card limit . (Select all correct answers)

I

Message Train eLearning I Commercial in Confidence

~

~- ..... -..... --.. --_ ...... __ ......... --.-~-;;:==:==::' -.- '"---" ==-----=-.- -_._-

-- -.............. ------_._-<-.__._-- .. _-----_ .. -......... --" ... __ ... -----_ .. _... _--

Congratulations

""---~----,--

---_ .. _- -• . ---. --"'---

WBC.100.009.4903

•

•

26

Message Train eLearning | Commercial in Confidence

Incorrect

Congratulations

WBC.100.009.4904CONFIDENTIAL

REDACTED

REDACTED

Cong"'lula~Qns .. _ .. _._------~-".-.

••

Cong"'lula~Qns .. _ .. _._------~-".-.

••

27

Message Train eLearning | Commercial in Confidence

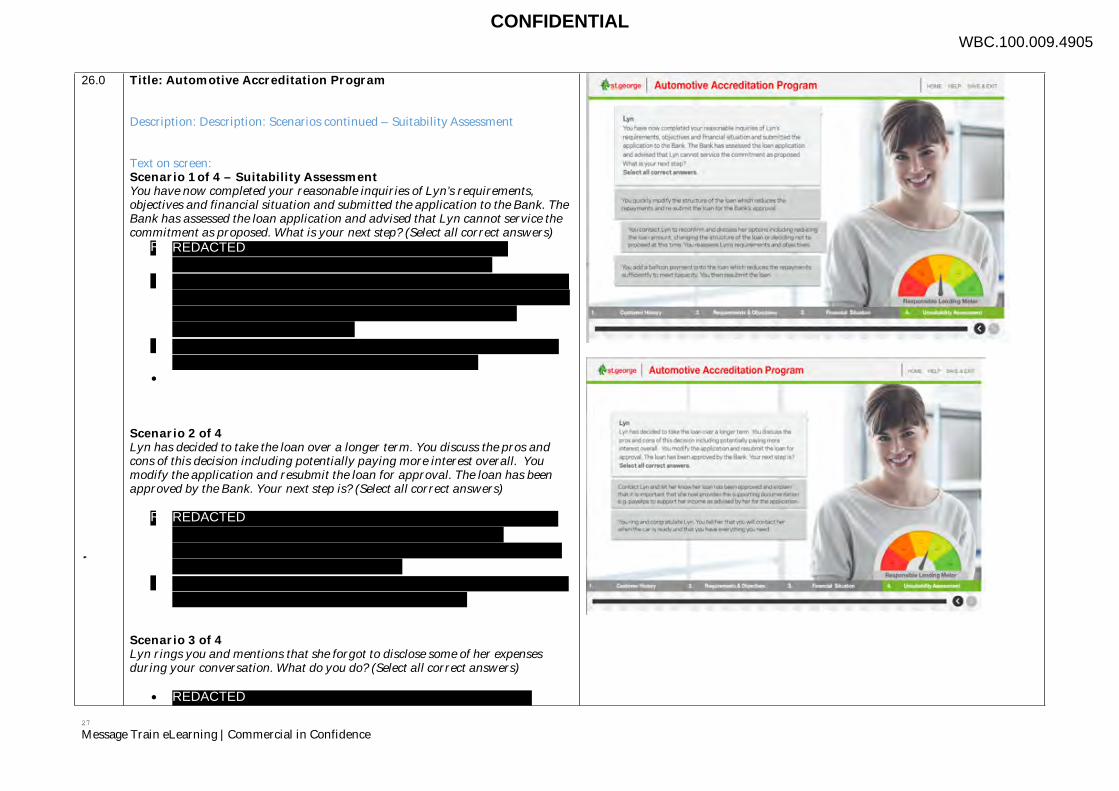

26.0 Title: Automotive Accreditation Program

Description: Description: Scenarios continued – Suitability Assessment

Text on screen:Scenario 1 of 4 – Suitability AssessmentYou have now completed your reasonable inquiries of Lyn’s requirements, objectives and financial situation and submitted the application to the Bank. The Bank has assessed the loan application and advised that Lyn cannot service the commitment as proposed. What is your next step? (Select all correct answers)

Scenario 2 of 4Lyn has decided to take the loan over a longer term. You discuss the pros and cons of this decision including potentially paying more interest overall. You modify the application and resubmit the loan for approval. The loan has been approved by the Bank. Your next step is? (Select all correct answers)

Scenario 3 of 4Lyn rings you and mentions that she forgot to disclose some of her expenses during your conversation. What do you do? (Select all correct answers)

WBC.100.009.4905CONFIDENTIAL

REDACTEDR

REDACTED

REDACTEDR

R

I

I

I

I

I

-... _______ '-r' -_ .. - ... _ ... _--------,..-----_._--_._-~ ___ N~_' ____ _ ____ .. ·r __ ..... __

-,~-- '-"_._"-------_._--... -----_ .. _ .. _-_ .. _ .. -,.. .. --_ ... _--" -----" .• _-----_...... --.. --.. -~,.-.--~-..... --

I

I

I

I

I

-... _______ '-r' -_ .. - ... _ ... _--------,..-----_._--_._-~ ___ N~_' ____ _ ____ .. ·r __ ..... __

-,~-- '-"_._"-------_._--... -----_ .. _ .. _-_ .. _ .. -,.. .. --_ ... _--" -----" .• _-----_...... --.. --.. -~,.-.--~-..... --

28

Message Train eLearning | Commercial in Confidence

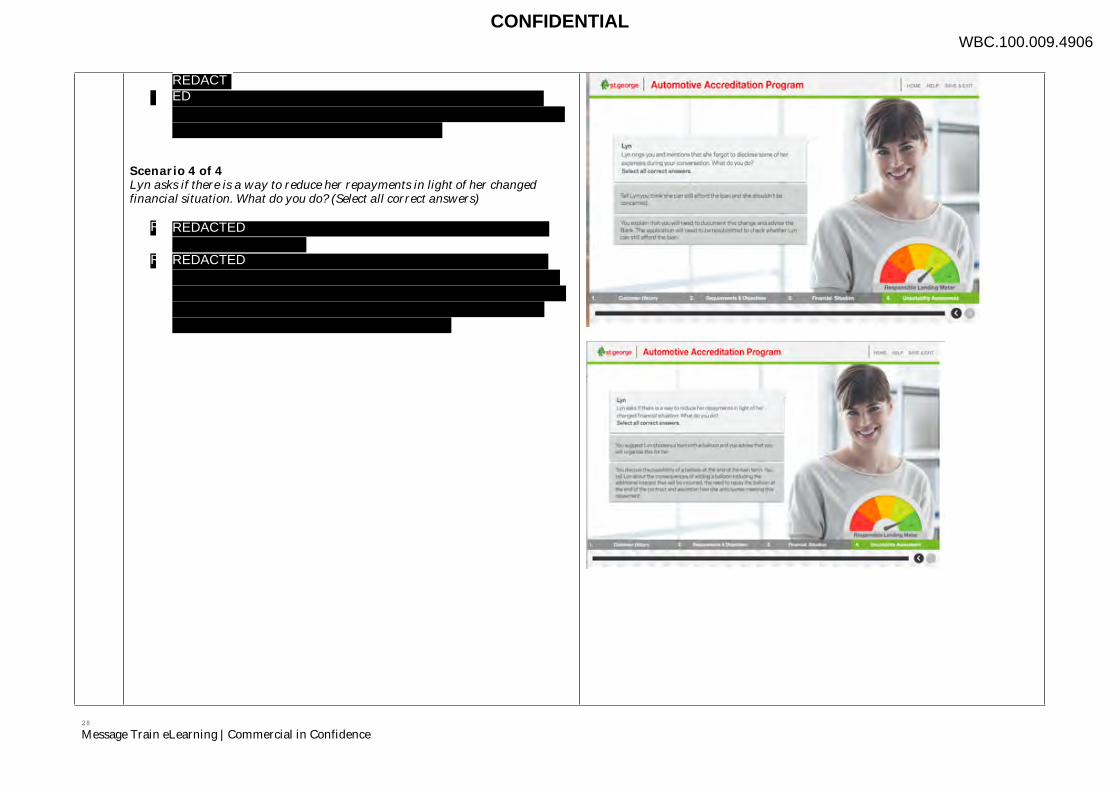

Scenario 4 of 4Lyn asks if there is a way to reduce her repayments in light of her changed financial situation. What do you do? (Select all correct answers)

WBC.100.009.4906CONFIDENTIAL

REDACTED

REDACTED

REDACTEDR

R

I

I

I

• ,~--.. - .... -.--.. ----_._----

• 40 . ...... ,. ... _ 1-:---

I

I

I

• ,~--.. - .... -.--.. ----_._----

• 40 . ...... ,. ... _ 1-:---

" Message Train eLearning I Commercial in Confidence

CONFIDENTIAL

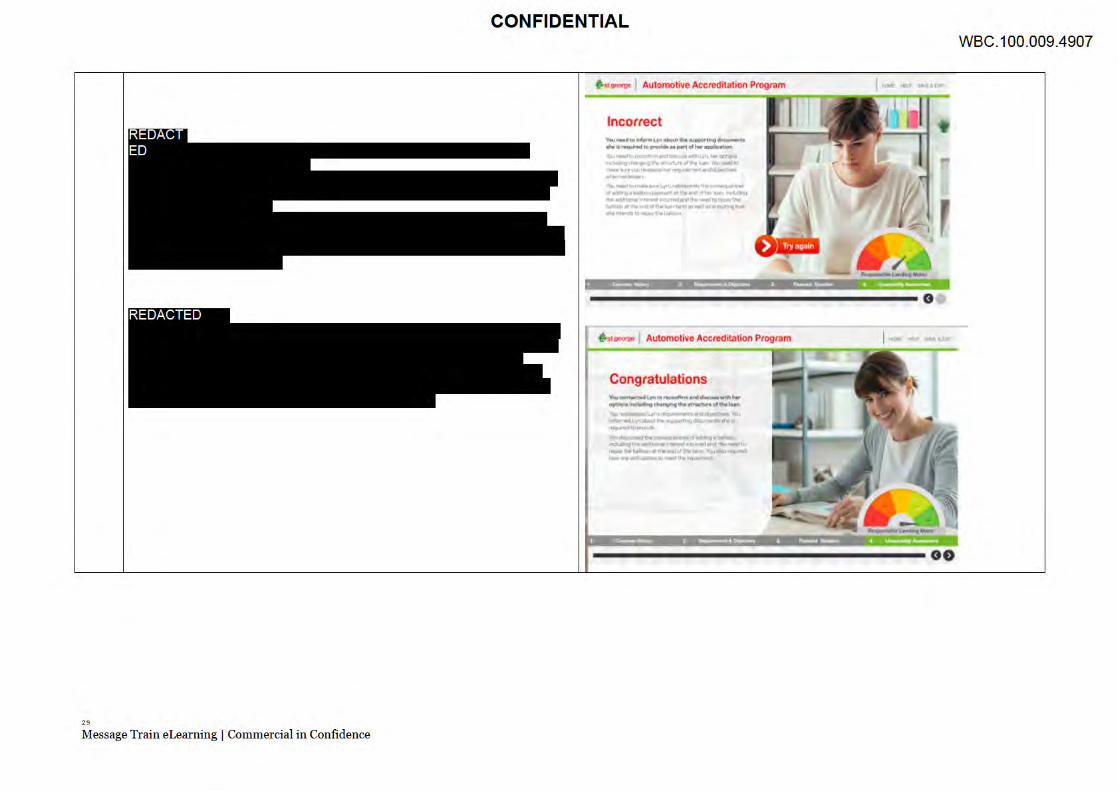

Incorrect -_ .. -... -... _..... _ .. _ .. _ ..... _-- .-_ .... _ ... -.-'---.-.. ----~- .. -~-". .. ........... -.. -----_ .. _ .. _ .... -.----_ .. -.. ----_ .. --- . _.- ,-- . --

Congratulations --...... -.. .... __ ... --_ ... _ ..... ---• ~..-~ .. -. "-" ... -_ ... -.. .... _ ..... - --_ .. _ ... -

o

WBC.100.009.4907

" Message Train eLearning I Commercial in Confidence

CONFIDENTIAL

Incorrect -_ .. -... -... _..... _ .. _ .. _ ..... _-- .-_ .... _ ... -.-'---.-.. ----~- .. -~-". .. ........... -.. -----_ .. _ .. _ .... -.----_ .. -.. ----_ .. --- . _.- ,-- . --

Congratulations --...... -.. .... __ ... --_ ... _ ..... ---• ~..-~ .. -. "-" ... -_ ... -.. .... _ ..... - --_ .. _ ... -

o

WBC.100.009.4907

30

Message Train eLearning | Commercial in Confidence

27.0 Title: Automotive Accreditation Program

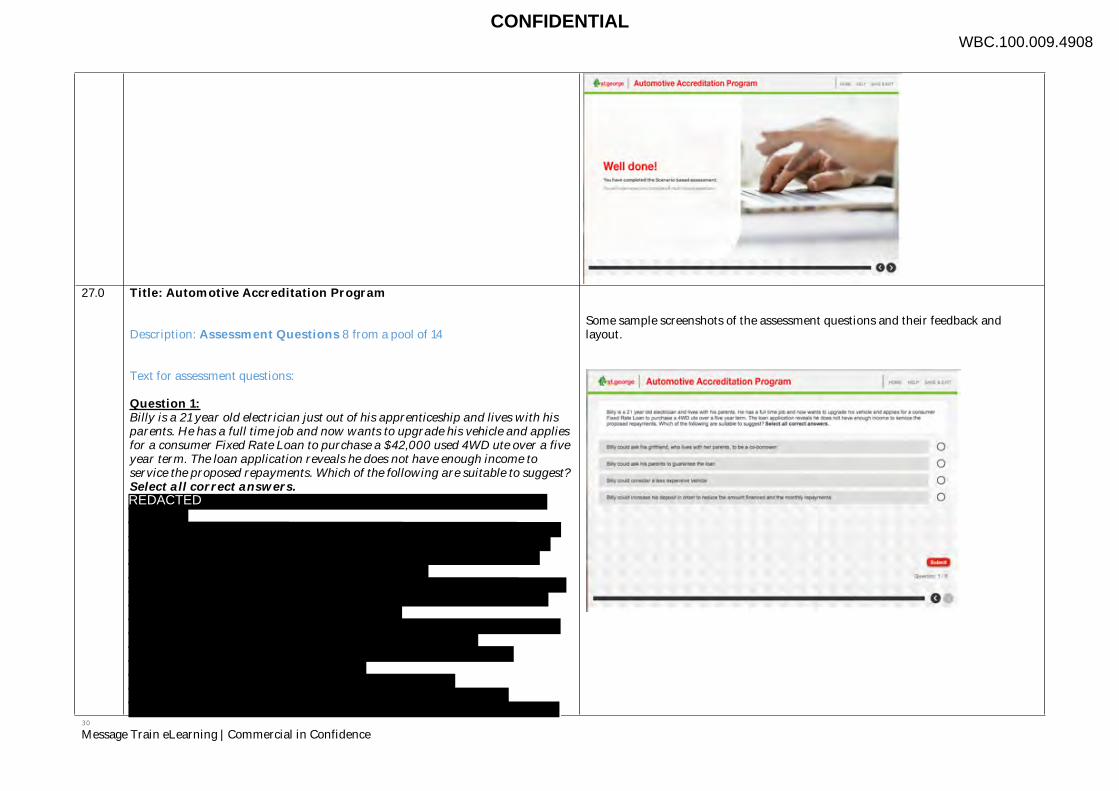

Description: Assessment Questions 8 from a pool of 14

Text for assessment questions:

Question 1: Billy is a 21 year old electrician just out of his apprenticeship and lives with his parents. He has a full time job and now wants to upgrade his vehicle and applies for a consumer Fixed Rate Loan to purchase a $42,000 used 4WD ute over a five year term. The loan application reveals he does not have enough income to service the proposed repayments. Which of the following are suitable to suggest? Select all correct answers.

Some sample screenshots of the assessment questions and their feedback and layout.

WBC.100.009.4908CONFIDENTIAL

REDACTED

00

"~" __ H __ ~_~ ___ "~ ___ M __ '''_ -----.---.-----.------....,-------_.-....... _._---.. ---_._--... __ ._--_____ • __ M _____ _

o o o o

------------------------0.

00

"~" __ H __ ~_~ ___ "~ ___ M __ '''_ -----.---.-----.------....,-------_.-....... _._---.. ---_._--... __ ._--_____ • __ M _____ _

o o o o

------------------------0.

31

Message Train eLearning | Commercial in Confidence

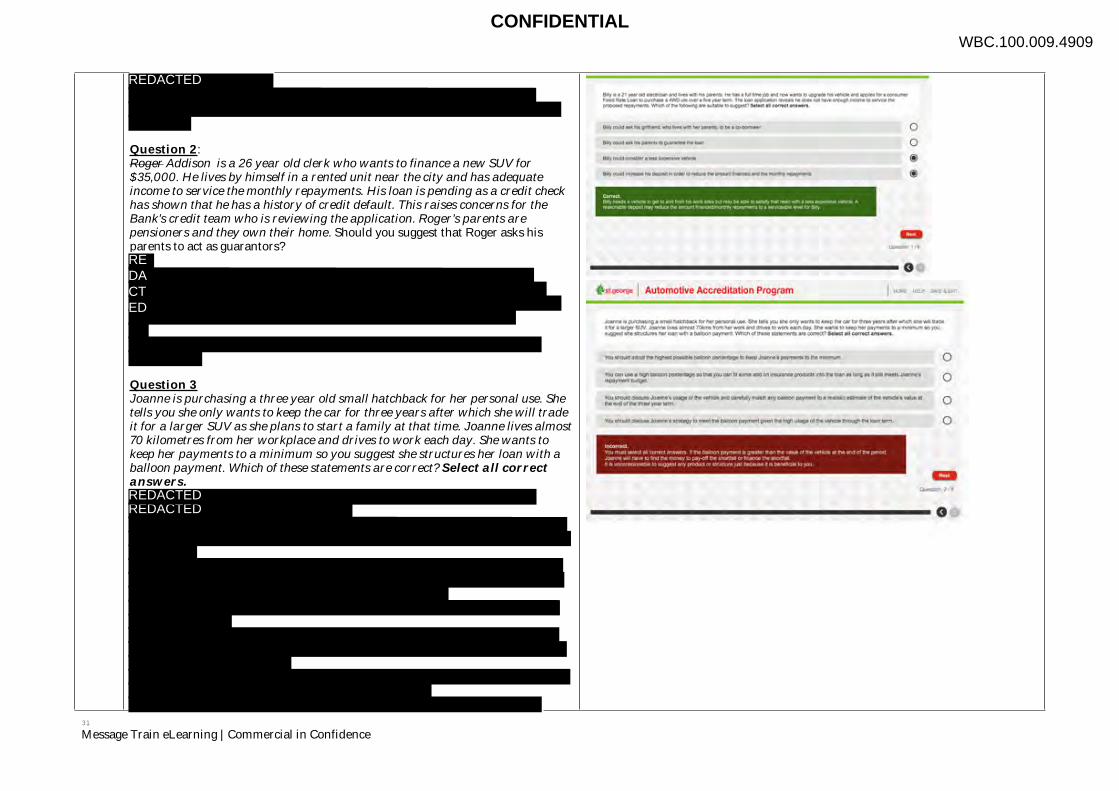

Question 2:Roger Addison is a 26 year old clerk who wants to finance a new SUV for $35,000. He lives by himself in a rented unit near the city and has adequate income to service the monthly repayments. His loan is pending as a credit check has shown that he has a history of credit default. This raises concerns for the Bank’s credit team who is reviewing the application. Roger’s parents are pensioners and they own their home. Should you suggest that Roger asks his parents to act as guarantors?

Question 3Joanne is purchasing a three year old small hatchback for her personal use. She tells you she only wants to keep the car for three years after which she will trade it for a larger SUV as she plans to start a family at that time. Joanne lives almost 70 kilometres from her workplace and drives to work each day. She wants to keep her payments to a minimum so you suggest she structures her loan with a balloon payment. Which of these statements are correct? Select all correct answers.

WBC.100.009.4909CONFIDENTIAL

REDACTED

REDACTED

REDACTEDREDACTED

~-~~-.---.. _---.. -----_._-------

. -

o o

• •

•• ••

~-.--~ .. ------.--~ .... ~-.. --.-... ,-=::;.-..:::--':.":''':!'.~-----~-----.... :.:= ... ---

--------_._--.... _--..... --_. __ . __ .. ........... _-.. _-- ,----....... _--_ ... _-_ ... _ .. _--_._. ----.-------... ----------.~-.--.:--; .:'::-;; .,-;,',:-- ........•..

o o o o

~-~~-.---.. _---.. -----_._-------

. -

o o

• •

•• ••

~-.--~ .. ------.--~ .... ~-.. --.-... ,-=::;.-..:::--':.":''':!'.~-----~-----.... :.:= ... ---

--------_._--.... _--..... --_. __ . __ .. ........... _-.. _-- ,----....... _--_ ... _-_ ... _ .. _--_._. ----.-------... ----------.~-.--.:--; .:'::-;; .,-;,',:-- ........•..

o o o o

32

Message Train eLearning | Commercial in Confidence

Question 4Wayne Ramesh works full time at a local café. When you ask him about his income he says that he brings home $2500 per week. Which response(s) describes the correct next step? Select all correct answers.

Question 5James and Kathy are both fully employed and have just agreed to buy a used ute and want to apply for a loan in joint names. As you progress with the finance application, it becomes evident that both incomes will be necessary to meet the capacity requirements. Lyn tells you that she is about eight months pregnant. What do you do? Select all correct answers.

WBC.100.009.4910CONFIDENTIAL

REDACTED

REDACTED

REDACTED

___ w _ _ ~ ____ . _ C

--__ .... _.__ c

~,::::::::=-.~_'!,.~-.-- .. --.. -.. n

-•

___ w _ _ ~ ____ . _ C

--__ .... _.__ c

~,::::::::=-.~_'!,.~-.-- .. --.. -.. n

-•

33

Message Train eLearning | Commercial in Confidence

Question 6Michael is purchasing a used car. He has told you that he has been driving a company vehicle recently but his employer is in the process of winding up the company. Michael is sure he will find a job. What do you do? Select all correct answers.

Question 7Daniel, who is single with no dependants, is enquiring about a loan for a new car. When you are obtaining the identification documents from Daniel, you notice that his Medicare card displays 3 names. What do you do? Select all correct answers.

WBC.100.009.4911CONFIDENTIAL

REDACTED

REDACTED

REDACTED

34

Message Train eLearning | Commercial in Confidence

assessment of the loan.

Question 8When is the most appropriate time to discuss the financing of additional such as third party insurance? Select all correct answers.

Question 9What type of expenses should be considered when assessing total Living Expenses? xv

Question 10You are having a needs based conversation with Fred and Mary when they mention they have to rush to go to a well-known private school for a parent teacher night. On review of their living expenses, you notice that their expenses do not reflect such private school fees as an item. What should you do? Select all correct answers.

WBC.100.009.4912CONFIDENTIAL

REDACTED

REDACTED

REDACTED

35

Message Train eLearning | Commercial in Confidence

Right: You need to make further inquiries if it seems unreasonable.

Question 11What are your primary responsible lending obligations as our representative? Select all correct answers.

Question 12What does making “reasonable inquiries” mean? Select all correct answers.

WBC.100.009.4913CONFIDENTIAL

REDACTED

REDACTED

36

Message Train eLearning | Commercial in Confidence

Question 13Which of the following do you consider meet the obligation of making “reasonable inquiries” about a customer’s financial situation? Select all correct answers.

Question 14What information does the Credit Guide provide? Select all correct answers.

WBC.100.009.4914CONFIDENTIAL

REDACTED

REDACTED

REDACTED

37

Message Train eLearning | Commercial in Confidence

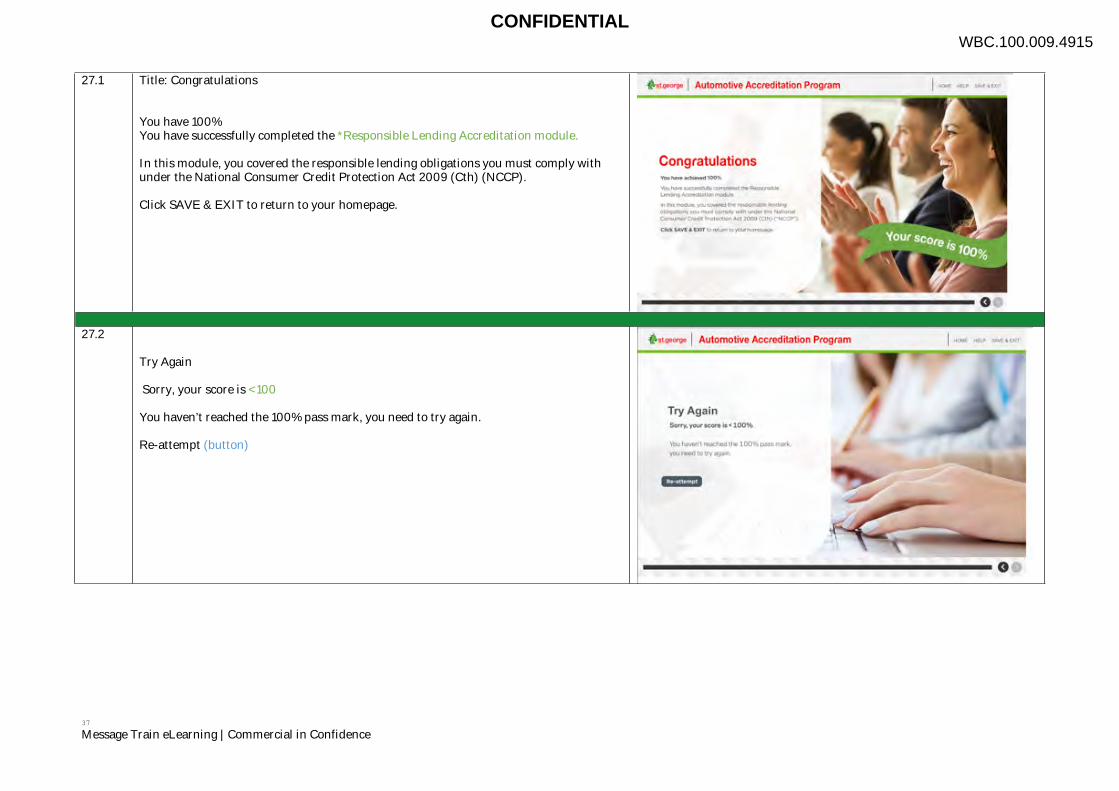

27.1 Title: Congratulations

You have 100%You have successfully completed the *Responsible Lending Accreditation module.

In this module, you covered the responsible lending obligations you must comply with under the National Consumer Credit Protection Act 2009 (Cth) (NCCP).

Click SAVE & EXIT to return to your homepage.

27.2

Try Again

Sorry, your score is <100

You haven’t reached the 100% pass mark, you need to try again.

Re-attempt (button)

WBC.100.009.4915CONFIDENTIAL

COn9(~blationc --- --------.--.------~ ----_ .. ------~ ~-.~ . -.--

-.-- -..,-"."- .--.'"'~ "-_. --.~-

COn9(~blationc --- --------.--.------~ ----_ .. ------~ ~-.~ . -.--

-.-- -..,-"."- .--.'"'~ "-_. --.~-