strategic financial management

TRANSCRIPT

1

Strategic Financial Management

By

Binoy john varghese

Strategic Financial ManagementStrategic financial management refers to both, financial implications or aspects of various business strategies, and strategic management of finance.

It is an approach to management that relates financial techniques, tools and methodologies to strategic decisions making to have a long-term futuristic perspective of financial well being of the firm to facilitate growth, sustenance and competitive edge consistently.

Strategic Financial ManagementAn approach to management that applies financial techniques to strategic decision making.

Definition: “the application of financial techniques to strategic decisions in order to help achieve the decision-maker's objectives”

Strategy: a carefully devised plan of action to achieve a goal, or the art of developing or carrying out such a plan

Strategic Financial Management

Strategic Financial Management refers to both, financial implications or aspects of various business strategies, and strategic management of finances.

Strategic Financial DecisionsStrategic Financial Management Deals with:

1. Investment decisions Long Term Investment Decisions Short Term Investment Decision

1. Financing Decisions Best means of financing- Debt Equity Ratio

1. Liquidity Decisions Organization maintain adequate cash reserves or

kind such that the operations run smoothly

1. Dividend Decisions Disbursement of Dividend to Share holder and

Retained Earnings

5. Profitability Decisions

Strategic Financial DecisionsStrategic Financial Management also Deals with:

1. Valuation of the firm

2. Strategic Risk Management

3. Strategic investments analysis and capital budgeting

4. Corporate restructuring and financial aspects

5. Strategic financial evaluation

6. Strategic capital restructuring

7. Strategic international financial management

8. Strategic financial engineering and architecture

9. Strategic market expansion planning

10.Strategic compensation planning

11.Strategic innovation expenditure

12.Other business challenges

Investment decisionsThe investment decision relates to the selection of assets in which funds will be invested by a firm. The assets which can be acquired fall into two broad groups: (a) long-term assets (Capital Budgeting) (b) short-term or current assets (Working Capital Management).

(a) Long Term Investment Decisions

Capital Budgeting Capital budgeting is probably the most crucial financial decision of a firm. It relates to the selection of an asset or investment proposal or course of action whose benefits are likely to be available in future over the lifetime of the project.

Capital Budgeting decisions

Use Pay Back period, NPV, IRR, etc. for evaluation

Investment Decisions

(b)Short Term Investment DecisionWorking Capital Management : Working capital management is concerned with the management of current assets. It is an important and integral part of financial management as short-term survival is a prerequisite for long-term success.

Fixed Part of working capital –managed from long term funds

Fluctuating Part of Working Capital –managed from short term funds

Financing DecisionsThe second major decision involved in financial management is the financing decision. The investment decision is broadly concerned with the asset-mix or the composition of the assets of a firm. The concern of the financing decision is with the financing-mix or capital structure or leverage. There are two aspects of the financing decision.

First, the theory of capital structure which shows the theoretical relationship between the employment of debt and the return to the shareholders. The second aspect of the financing decision is the determination of an appropriate capital structure, given the facts of a particular case. Thus, the financing decision covers two interrelated aspects: (1) the capital structure theory, and (2) the capital structure decision.

Dividend DecisionsTwo alternatives are available in dealing with the profits of a firm.

(1)They can be distributed to the shareholders in the form of dividends or

(2)They can be retained in the business itself.

It depends on the dividend-pay out ratio, that is, what proportion of net profits should be paid out to the share holders.

It depends upon the preference of the shareholders and investment opportunities available within the firm

Profitability Management

The source of revenue has to be pre-decided to obtain profits in future.

It is closely related to investment decisions as revenue generation will be from operations, investments and divestments.

12

Working Capital Decision

Gross working capital (GWC) GWC refers to the firm’s total investment in current assets.

Current assets are the assets which can be converted into cash within an accounting year (or operating cycle) and include cash, short-term securities, debtors, (accounts receivable or book debts) bills receivable and stock (inventory).

13

Concepts of Working Capital

Net working capital (NWC).NWC refers to the difference between current

assets and current liabilities. Current liabilities (CL) are those claims of

outsiders which are expected to mature for payment within an accounting year and include creditors (accounts payable), bills payable, and outstanding expenses.

NWC can be positive or negative. Positive NWC = CA > CLNegative NWC = CA < CL

14

Concepts of Working CapitalGWC focuses on

– Optimization of current investment – Financing of current assets

NWC focuses on – Liquidity position of the firm– Judicious mix of short-term and long-tern

financing

15

Operating CycleOperating cycle is the time duration required to convert sales, after the conversion of resources into inventories, into cash. The operating cycle of a manufacturing company involves three phases:– Acquisition of resources such as raw material, labour,

power and fuel etc.– Manufacture of the product which includes conversion

of raw material into work-in-progress into finished goods.– Sale of the product either for cash or on credit. Credit

sales create account receivable for collection.

Working Capital ManagementReceivables Management

Investment in receivable• volume of credit sales• collection period

Credit policy• credit standards• credit terms• collection efforts

Cash Management

Working Capital ManagementInventory Management

Stocks of manufactured products and the material that make up the product.

Components:

• raw materials

• work-in-process

• finished goods

• stores and spares (supplies)

Working Capital Management

Cash Management

Cash management is concerned with the managing of:– cash flows into and out of the firm,– cash flows within the firm, and– cash balances held by the firm at a point of

time by financing deficit or investing surplus cash

Functions of Financial Manager

1. Financial Forecasting and Planning

2. Acquisition of funds

3. Investment of funds

4. Helping in Valuation Decisions

5. Maintain Proper Liquidity

Financial PolicyCriteria describing a corporation's choices regarding its debt/equity mix, currencies of denomination, maturity structure, method of financing investment projects, and hedging decisions with a goal of maximizing the value of the firm to some set of stockholders.Hedging: A strategy designed to reduce investment risk using call options, put options, short-selling, or futures contracts. Its purpose is to reduce the volatility of a portfolio by reducing the risk of loss.

Strategic planningStrategic planning is an organization's process of defining its strategy, or direction, and making decisions on allocating its resources to pursue this strategy, including its capital and people. Various business analysis techniques can be used in strategic planning, including SWOT analysis (Strengths, Weaknesses, Opportunities, and Threats ), PEST analysis (Political, Economic, Social, and Technological), STEER analysis (Socio-cultural, Technological, Economic, Ecological, and Regulatory factors), and EPISTEL (Environment, Political, Informatic, Social, Technological, Economic and Legal).

Strategic planning Strategic planning is the formal consideration of an organization's future course.

All strategic planning deals with at least one of three key questions:

"What do we do?"

"For whom do we do it?"

"How do we excel?"

In business strategic planning, some authors phrase the third question as "How can we beat or avoid competition?". (Bradford and Duncan, page 1). But this approach is more about defeating competitors than about excelling.

Strategic planning In many organizations, this is viewed as a process for determining where an organization is going over the next year or - more typically - 3 to 5 years (long term), although some extend their vision to 20 years.

In order to determine where it is going, the organization needs to know exactly where it stands, then determine where it wants to go and how it will get there. The resulting document is called the "strategic plan."

It is also true that strategic planning may be a tool for effectively plotting the direction of a company; however, strategic planning itself cannot foretell exactly how the market will evolve and what issues will surface in the coming days in order to plan your organizational strategy. Therefore, strategic innovation and tinkering with the 'strategic plan' have to be a cornerstone strategy for an organization to survive the turbulent business climate.

Characteristics of Strategic planning

Successful Strategic planning constitutes the following features. It should:

1. Exhibit impacts in daily routine

2. Facilitate dynamic, forward and backward thinking process

3. Counters repetitive patterns of mistakes, especially human tendencies

4. Remain clear and simple

5. Ensure planning is complete only when it is properly implemented

6. Designate a core planning team with a level of autonomy

7. Constitute collective leadership and involvement of key stakeholders in decision making

Mission and VisionMission: Defines the fundamental purpose

of an organization or an enterprise, succinctly describing why it exists and what it does to achieve its Vision

A Vision statement outlines what the organization wants to be, or how it wants the world in which it operates to be. It concentrates on the future. It is a source of inspiration. It provides clear decision-making criteria.

26

Finance FunctionsInvestment or Long Term Asset Mix

Decision

Financing or Capital Mix Decision

Dividend or Profit Allocation Decision

Liquidity or Short Term Asset Mix Decision

Strategic Financial PlanningA Financial Plan is statement of what is to be done in a future time.

Most decisions have long lead times, which means they take a long time to implement.

In an uncertain world, this requires that decisions be made far in advance of their implementation

Strategic Financial PlanningIt formulates the method by which financial goals are to be achieved.

There are two dimensions:

1. A Time Frame– Short run is probably anything less than a year.

– Long run is anything over that; usually taken to be a two-year to five-year period.

2. A Level of Aggregation– Each division and operational unit should have a plan.

– As the capital-budgeting analyses of each of the firm’s divisions are added up, the firm aggregates these small projects as a big project.

Strategic Financial PlanningScenario AnalysisEach division might be asked to prepare three

different plans for the near term future:1. A Worst Case- This plan would require making the worst

possible assumptions about the companies products and the state of the economy

2. A Normal Case- This plan would require making the most likely assumptions about the company and the economy

3. A Best Case- Each divisions would be required to work out a case based on optimistic assumptions. It could involve new products and expansion.

Components of Financial StrategyStart-Up Costs

A new business venture, even those started by existing companies, has start-up costs. An existing manufacturer looking to release a new line of product has costs that may include new fabricating equipment, new packaging and a marketing plan. Include your start-up costs in your financial strategy.

Competitive Analysis

Your competition affects how you make money and how you spend money. The products and marketing activities of your competition should be included in your financial strategy. An analysis of how the competition will affect revenue needs to be included in your planning.

Ongoing Costs

Revenue

Components of Financial Strategy

Ongoing CostsThese include labor, materials, equipment maintenance, shipping and facilities costs, such as lease and utilities. Break down your ongoing cost projections into monthly numbers to include as part of your financial strategy.

RevenueIn order to create an effective financial strategy, you need to forecast revenue over the length of the project. A comprehensive revenue forecast is necessary when determining how much will be available to pay your ongoing costs, and how much will remain as profit.

Objectives and Goals

Goal: The Financial Goal of the firm should be shareholder’s wealth maximization, as reflected in the market value of the firm’s share.

Firms’ primary objective is maximizing the welfare of owners, but, in operational terms, they focus on the satisfaction of its customers through the production of goods and services needed by them

1-33

Objectives Of Financial ManagementThe term objective is used to in the sense of a goal or decision criteria for the three decisions involved in financial managementThe goal of the financial manager is to maximise the owners/shareholders wealth as reflected in share prices rather than profit/EPS maximisation because the latter ignores the timing of returns, does not directly consider cash flows and ignores risk. As key determinants of share price, both return and risk must be assessed by the financial manager when evaluating decision alternatives. The EVA is a popular measure to determine whether an investment positively contributes to the owners wealth.

1-34

Objectives Of Financial Management

However, the wealth maximizing action of the finance managers should be consistent with the preservation of the wealth of stakeholders, that is, groups such as employees, customers, suppliers, creditors, owners and others who have a direct link to the firm.

35

Finance Manager’s Role• Raising of Funds

• Allocation of Funds

• Profit Planning

• Understanding Capital Markets

Financial Goals• Profit maximization (profit after tax)

• Maximizing Earnings per Share

• Shareholder’s Wealth Maximization

36

Profit Maximization

Maximizing the Rupee Income of Firm – Resources are efficiently utilized

– Appropriate measure of firm performance

– Serves interest of society also

37

Objections to Profit MaximizationIt is VagueIt Ignores the Timing of ReturnsIt Ignores RiskAssumes Perfect CompetitionIn new business environment profit

maximization is regarded as UnrealisticDifficultInappropriate Immoral.

38

Maximizing EPS

Ignores timing and risk of the expected benefit

Market value is not a function of EPS. Hence maximizing EPS will not result in highest price for company's shares

Maximizing EPS implies that the firm should make no dividend payment so long as funds can be invested at positive rate of return—such a policy may not always work

39

Shareholders’ Wealth Maximization

Maximizes the net present value of a course of action to shareholders.

Accounts for the timing and risk of the expected benefits.

Benefits are measured in terms of cash flows.

Fundamental objective—maximize the market value of the firm’s shares.

40

Risk-return Trade-offRisk and expected return move in tandem;

the greater the risk, the greater the expected return.

Financial decisions of the firm are guided by the risk-return trade-off.

The return and risk relationship: Return = Risk-free rate + Risk premium

Risk-free rate is a compensation for time and risk premium for risk.

41

Managers Versus Shareholders’ GoalsA company has stakeholders such as employees, debt-holders, consumers, suppliers, government and society.

Managers may perceive their role as reconciling conflicting objectives of stakeholders. This stakeholders’ view of managers’ role may compromise with the objective of SWM.

Managers may pursue their own personal goals at the cost of shareholders, or may play safe and create satisfactory wealth for shareholders than the maximum.

Managers may avoid taking high investment and financing risks that may otherwise be needed to maximize shareholders’ wealth. Such “satisfying” behaviour of managers will frustrate the objective of SWM as a normative guide.

42

Financial Goals and Firm’s Mission and Objectives

Firms’ primary objective is maximizing the welfare of owners, but, in operational terms, they focus on the satisfaction of its customers through the production of goods and services needed by themFirms state their vision, mission and values in broad terms

Wealth maximization is more appropriately a decision criterion, rather than an objective or a goal.

Goals or objectives are missions or basic purposes of a firm’s existence

43

Financial Goals and Firm’s Mission and Objectives

The shareholders’ wealth maximization is the second-level criterion ensuring that the decision meets the minimum standard of the economic performance.

In the final decision-making, the judgement of management plays the crucial role. The wealth maximization criterion would simply indicate whether an action is economically viable or not.

What Will the Planning Process Accomplish?

InteractionsThe plan must make explicit the linkages between

investment proposals and the firm’s financing choices.

OptionsThe plan provides an opportunity for the firm to weigh its

various options.

Feasibility- The different plans must fit into the overall corporation objective of maximizing shareholder wealth

Avoiding SurprisesOne of the purpose of financial planning is to avoid surprise.

Strategic Planning Process

Strategic Planning

Strategic Planning relates to planning in advance for a long period of time.

This facilitates predicting the future and devising a course of action well in advance.

It deals with future course of action consistent with the business environment changes.

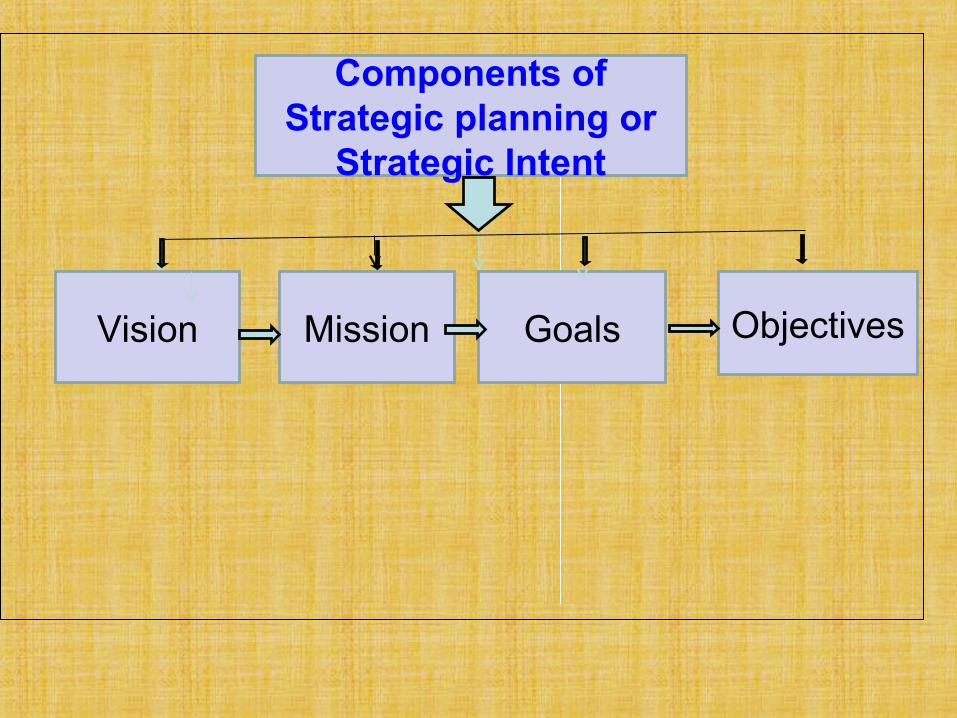

Components of Strategic Planning 1. Vision- Organization visualizes what it would like to in

future

2. Mission- Deals with distinctive purpose which an organization is striving for. It declares the main concerns or priorities and principles of the business firm.

3. Goals – They are concrete aims which enhance the motivation of organization teams which prepare themselves in specific aspects.

4. Objectives- intend to put forward in precise terms what an organization wants to achieve, where it wants to be in future, what are the tasks that needs to be achieved in short spans of time.

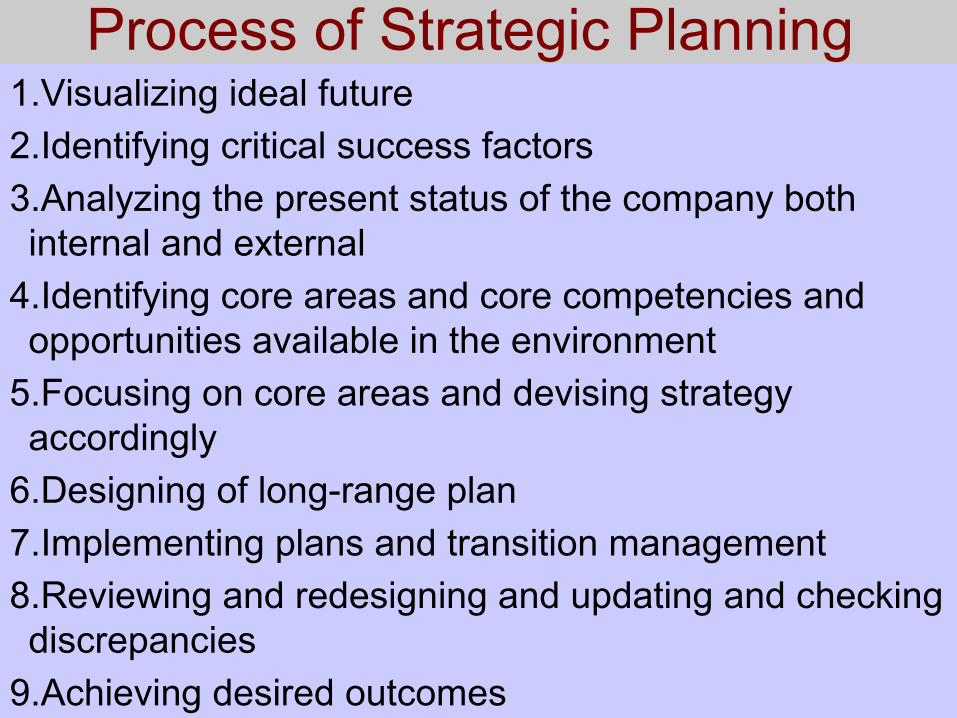

Process of Strategic Planning 1.Visualizing ideal future

2.Identifying critical success factors

3.Analyzing the present status of the company both internal and external

4.Identifying core areas and core competencies and opportunities available in the environment

5.Focusing on core areas and devising strategy accordingly

6.Designing of long-range plan

7.Implementing plans and transition management

8.Reviewing and redesigning and updating and checking discrepancies

9.Achieving desired outcomes

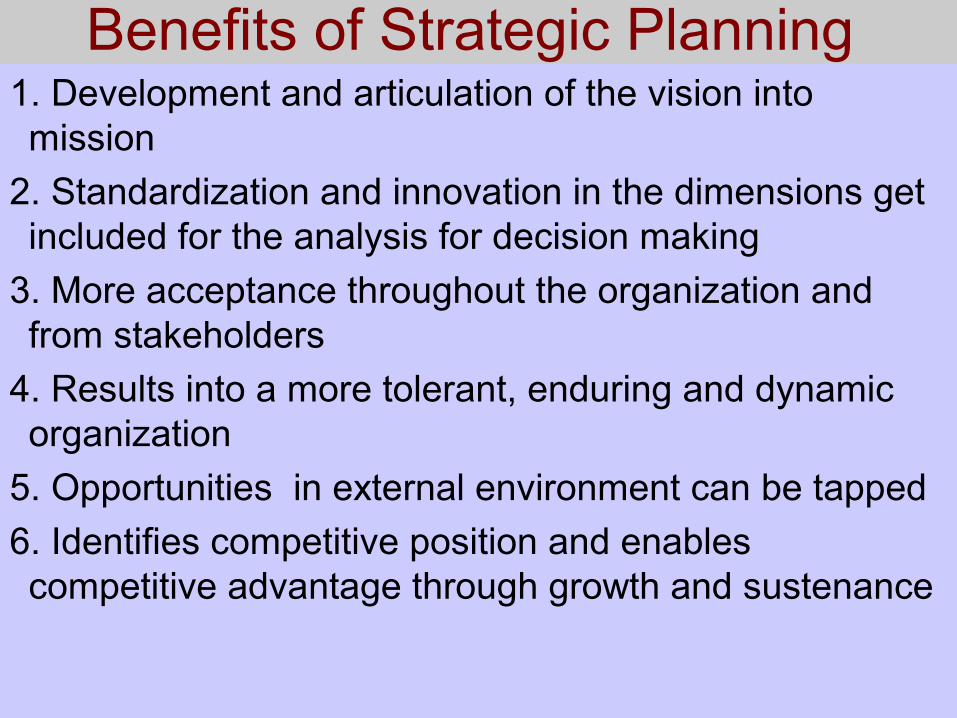

Benefits of Strategic Planning 1. Development and articulation of the vision into mission

2. Standardization and innovation in the dimensions get included for the analysis for decision making

3. More acceptance throughout the organization and from stakeholders

4. Results into a more tolerant, enduring and dynamic organization

5. Opportunities in external environment can be tapped

6. Identifies competitive position and enables competitive advantage through growth and sustenance

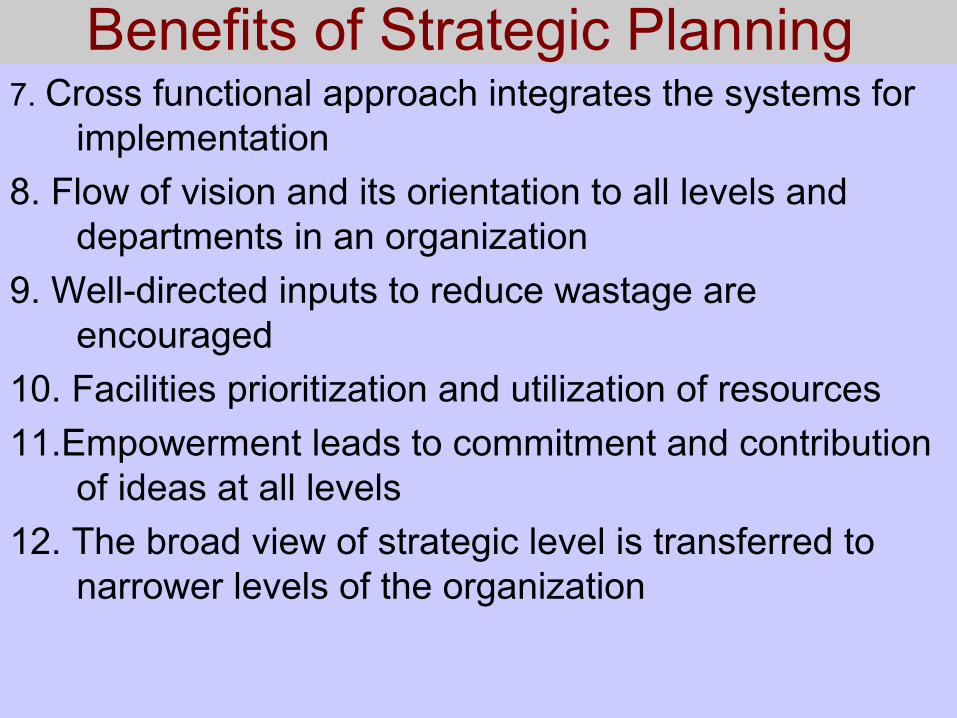

Benefits of Strategic Planning 7. Cross functional approach integrates the systems for

implementation

8. Flow of vision and its orientation to all levels and departments in an organization

9. Well-directed inputs to reduce wastage are encouraged

10. Facilities prioritization and utilization of resources

11.Empowerment leads to commitment and contribution of ideas at all levels

12. The broad view of strategic level is transferred to narrower levels of the organization

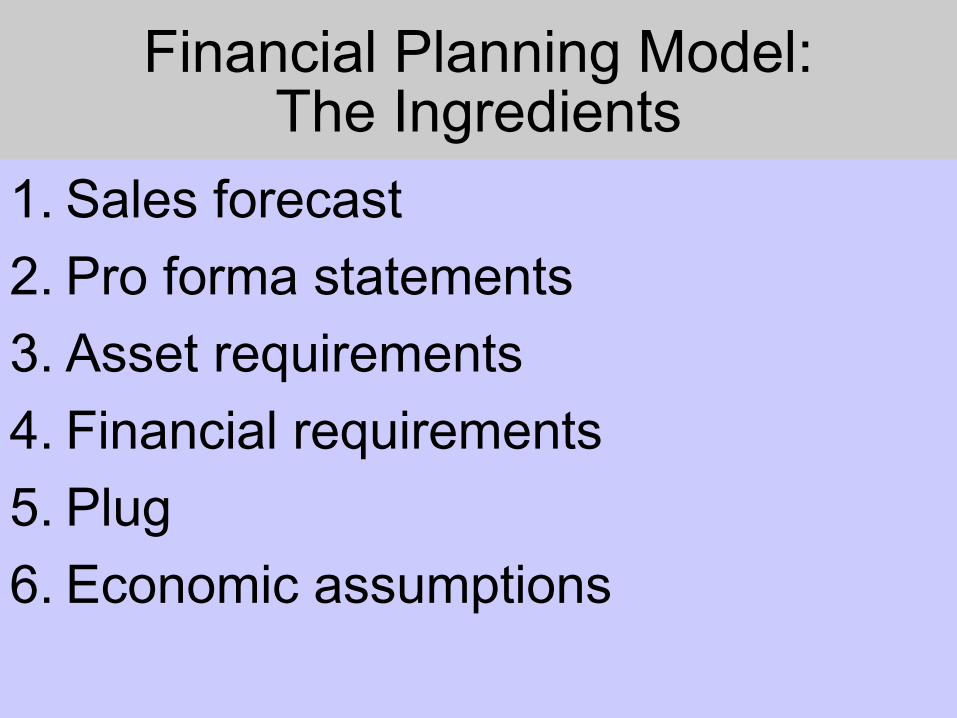

Financial Planning Model:The Ingredients

1. Sales forecast

2. Pro forma statements

3. Asset requirements

4. Financial requirements

5. Plug

6. Economic assumptions

3-52

1. Sales Forecast All financial plans require a sales

forecast. Perfect foreknowledge is impossible

since sales depend on the uncertain future state of the economy.

Businesses that specialize in macroeconomic and industry projects can be help in estimating sales.

3-53

2. Pro Forma Statements

The financial plan will have a forecast balance sheet, a forecast income statement, and a forecast sources-and-uses-of-cash statement.

These are called pro forma statements or pro formas.

3-54

3. Asset Requirements

The financial plan will describe projected capital spending.

In addition it will the discuss the proposed uses of net working capital.

3-55

4. Financial Requirements

The plan will include a section on financing arrangements.

Dividend policy and capital structure policy should be addressed.

If new funds are to be raised, the plan should consider what kinds of securities must be sold and what methods of issuance are most appropriate.

3-56

5. Plug Compatibility across various growth targets will

usually require adjustment in a third variable. Suppose a financial planner assumes that

sales, costs, and net income will rise at g1. Further, suppose that the planner desires assets and liabilities to grow at a different rate, g2. These two rates may be incompatible unless a third variable is adjusted.

For example, compatibility may only be reached if outstanding stock grows at a third rate, g3.

Compatibility across various growth targets will usually require adjustment in a third variable.

Suppose a financial planner assumes that sales, costs, and net income will rise at g1. Further, suppose that the planner desires assets and liabilities to grow at a different rate, g2. These two rates may be incompatible unless a third variable is adjusted.

For example, compatibility may only be reached if outstanding stock grows at a third rate, g3.

3-57

6. Economic Assumptions

The plan must explicitly state the economic environment in which the firm expects to reside over the life of the plan.

Interest rate forecasts are part of the plan.

The plan must explicitly state the economic environment in which the firm expects to reside over the life of the plan.

Interest rate forecasts are part of the plan.

9S Model of SFMNine S Model combines the quantitative and qualitative skills of a strategist.

1.Sanctity

2.Selectivity

3.System

4.Strategic Cost Management

5.Sensitivity

6.Sustainability

7.Superiority

8.Structural Flexibility

9.Soul Searching

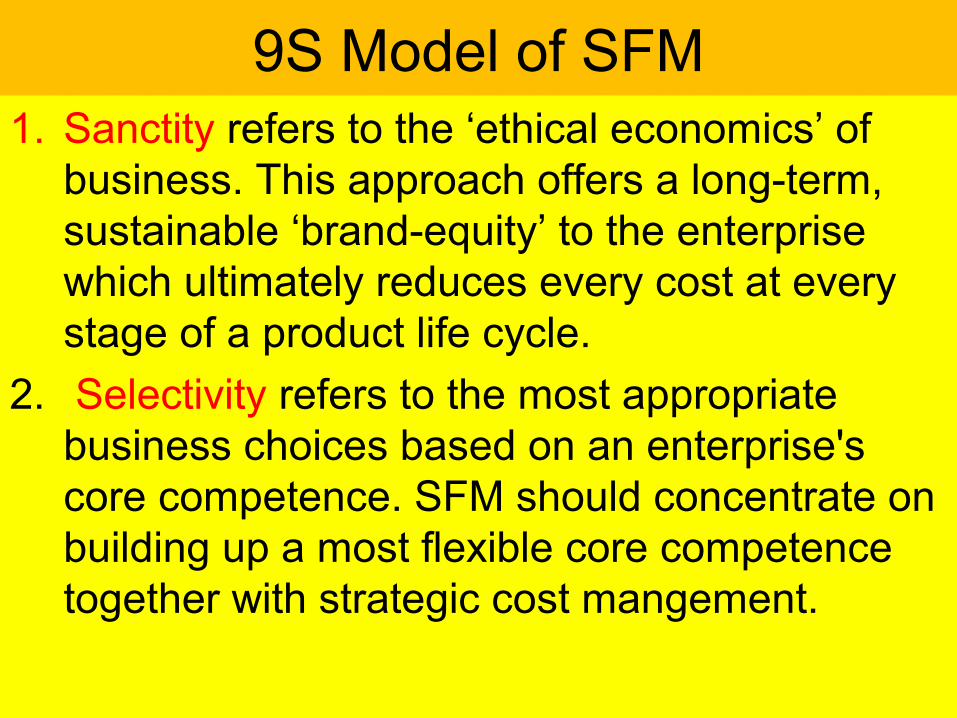

9S Model of SFM1. Sanctity refers to the ‘ethical economics’ of

business. This approach offers a long-term, sustainable ‘brand-equity’ to the enterprise which ultimately reduces every cost at every stage of a product life cycle.

2. Selectivity refers to the most appropriate business choices based on an enterprise's core competence. SFM should concentrate on building up a most flexible core competence together with strategic cost mangement.

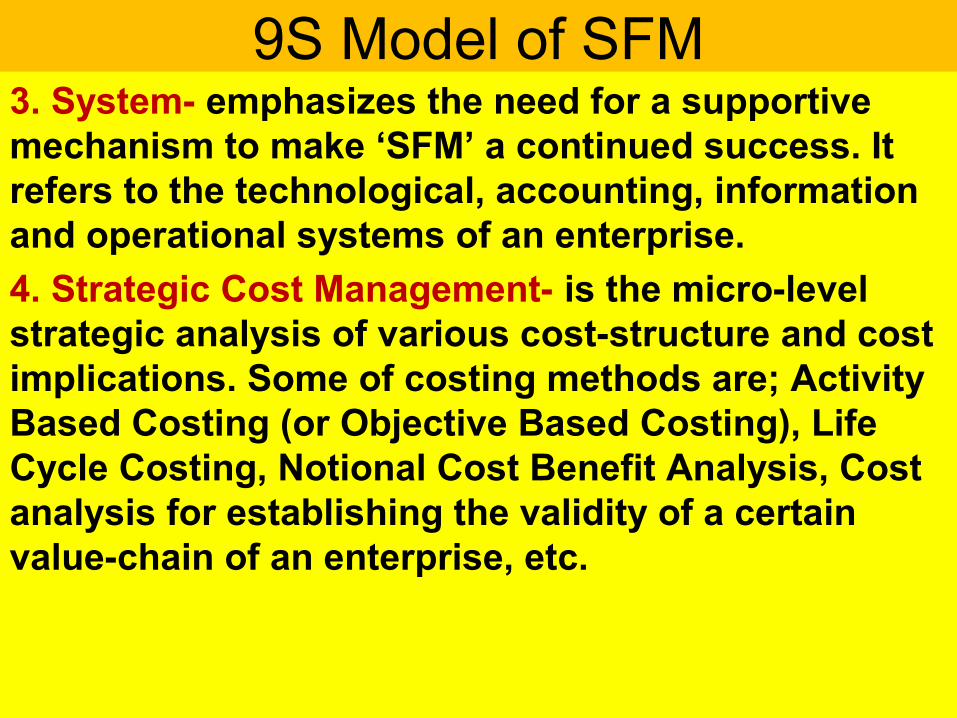

9S Model of SFM3. System- emphasizes the need for a supportive mechanism to make ‘SFM’ a continued success. It refers to the technological, accounting, information and operational systems of an enterprise.

4. Strategic Cost Management- is the micro-level strategic analysis of various cost-structure and cost implications. Some of costing methods are; Activity Based Costing (or Objective Based Costing), Life Cycle Costing, Notional Cost Benefit Analysis, Cost analysis for establishing the validity of a certain value-chain of an enterprise, etc.

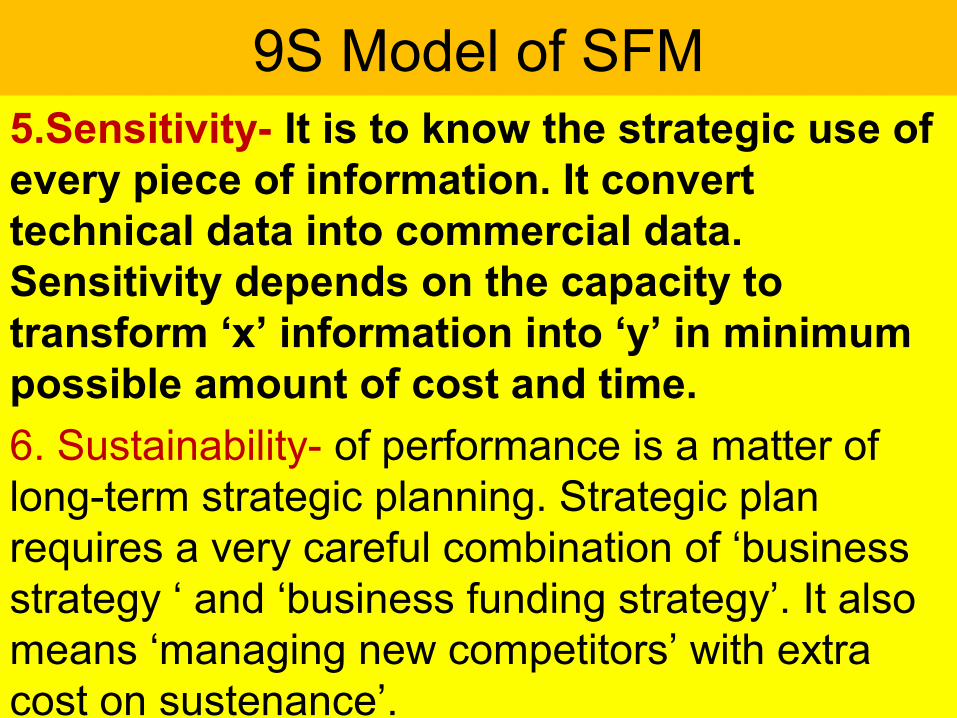

9S Model of SFM5.Sensitivity- It is to know the strategic use of every piece of information. It convert technical data into commercial data. Sensitivity depends on the capacity to transform ‘x’ information into ‘y’ in minimum possible amount of cost and time.

6. Sustainability- of performance is a matter of long-term strategic planning. Strategic plan requires a very careful combination of ‘business strategy ‘ and ‘business funding strategy’. It also means ‘managing new competitors’ with extra cost on sustenance’.

Superiority

Structural Flexibility

Soul Searching

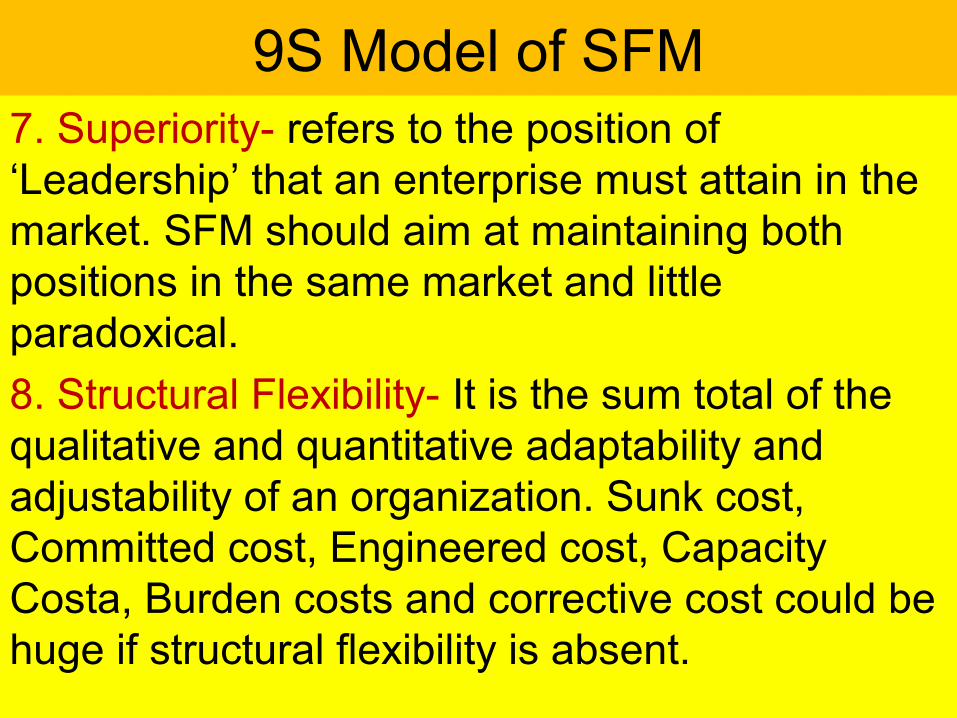

9S Model of SFM7. Superiority- refers to the position of ‘Leadership’ that an enterprise must attain in the market. SFM should aim at maintaining both positions in the same market and little paradoxical.

8. Structural Flexibility- It is the sum total of the qualitative and quantitative adaptability and adjustability of an organization. Sunk cost, Committed cost, Engineered cost, Capacity Costa, Burden costs and corrective cost could be huge if structural flexibility is absent.

9S Model of SFM9. Soul Searching- It is based on continuous bench marking and requires a tremendous amount of financial alertness, innovation and total exposure to new variables and parameters.

It also refers to establishing new heights of achievement and newer core-competences.

The 9 references of SFM ultimately aim for, ‘Wealth Maximization through the accelerating Effect’.

Strategic planningStrategic planning is an organization's process of defining its strategy, or direction, and making decisions on allocating its resources to pursue this strategy, including its capital and people.

Strategic planningVarious business analysis techniques can be used in strategic planning, including SWOT analysis (Strengths, Weaknesses, Opportunities, and Threats ), PEST analysis (Political, Economic, Social, and Technological), STEER analysis (Socio-cultural, Technological, Economic, Ecological, and Regulatory factors), and EPISTEL (Environment, Political, Informatic, Social, Technological, Economic and Legal).

Strategic planning Strategic planning is the formal consideration of an organization's future course.

All strategic planning deals with at least one of three key questions:

"What do we do?"

"For whom do we do it?"

"How do we excel?"

In business strategic planning, some authors phrase the third question as "How can we beat or avoid competition?". (Bradford and Duncan, page 1). But this approach is more about defeating competitors than about excelling.

Strategic planning In many organizations, this is viewed as a process for determining where an organization is going over the next year or - more typically - 3 to 5 years (long term), although some extend their vision to 20 years.

In order to determine where it is going, the organization needs to know exactly where it stands, then determine where it wants to go and how it will get there. The resulting document is called the "strategic plan."

It is also true that strategic planning may be a tool for effectively plotting the direction of a company; however, strategic planning itself cannot foretell exactly how the market will evolve and what issues will surface in the coming days in order to plan your organizational strategy. Therefore, strategic innovation and tinkering with the 'strategic plan' have to be a cornerstone strategy for an organization to survive the turbulent business climate.

Characteristics of Strategic planningSuccessful Strategic planning constitutes the following features. It should:

1. Exhibit impacts in daily routine

2. Facilitate dynamic, forward and backward thinking process

3. Counters repetitive patterns of mistakes, especially human tendencies

4. Remain clear and simple

5. Ensure planning is complete only when it is properly implemented

6. Designate a core planning team with a level of autonomy

7. Constitute collective leadership and involvement of key stakeholders in decision making

Vision Goals

Components of Strategic planning or

Strategic Intent

Mission Objectives

Components of Strategic Planning 1. Vision- Organization visualizes what it would like to in

future

2. Mission- Deals with distinctive purpose which an organization is striving for. It declares the main concerns or priorities and principles of the business firm.

3. Goals – They are concrete aims which enhance the motivation of organization teams which prepare themselves in specific aspects.

4. Objectives- intend to put forward in precise terms what an organization wants to achieve, where it wants to be in future, what are the tasks that needs to be achieved in short spans of time.

VisionA Vision statement outlines what the organization wants to be, or how it wants the world in which it operates to be. It concentrates on the future. It is a source of inspiration. It provides clear decision-making criteria.Every organization visualizes what it would like to be in future.Vision describes a wishful long-term desire of the company with out mentioning the steps or plans to be used in order to set the target.

MissionMission: Defines the fundamental purpose of an organization or an enterprise, describing why it exists and what it does to achieve its Vision.

Mission deals with a distinctive Purpose which a organization is striving for. A well defined mission statement declares the main concerns or priorities and principles of the business firm

ObjectivesObjectives intend to put forward in precise terms what an organization wants to achieve where it wants to be in future, what are the tasks that needs to be achieved in short spans of time to achieve the future objectives and goals.

GoalsGoals are the concrete aims or targets which enhance the motivation of the organizational teams which prepare themselves in specific aspects.

Goals provide the benefit of breaking down or fragmenting the broader mission into more concert and clear tasks that are understandable, and responsibilities are allocated to individuals and teams in the organization.

Financial Objectives and Goals

Goal: The Financial Goal of the firm should be shareholder’s wealth maximization, as reflected in the market value of the firm’s share.

Firms’ primary objective is maximizing the welfare of owners, but, in operational terms, they focus on the satisfaction of its customers through the production of goods and services needed by them

1-77

Objectives Of Financial ManagementThe term objective is used to in the sense of a goal or decision criteria for the three decisions involved in financial managementThe goal of the financial manager is to maximise the owners/shareholders wealth as reflected in share prices rather than profit/EPS maximisation because the latter ignores the timing of returns, does not directly consider cash flows and ignores risk. As key determinants of share price, both return and risk must be assessed by the financial manager when evaluating decision alternatives. The EVA is a popular measure to determine whether an investment positively contributes to the owners wealth.

1-78

Objectives Of Financial Management

However, the wealth maximizing action of the finance managers should be consistent with the preservation of the wealth of stakeholders, that is, groups such as employees, customers, suppliers, creditors, owners and others who have a direct link to the firm.

79

Finance Manager’s Role• Raising of Funds

• Allocation of Funds

• Profit Planning

• Understanding Capital Markets

Financial Goals• Profit maximization (profit after tax)

• Maximizing Earnings per Share

• Shareholder’s Wealth Maximization

Strategic Financial PlanningA Financial Plan is statement of what is to be done in a future time.

Most decisions have long lead times, which means they take a long time to implement.

In an uncertain world, this requires that decisions be made far in advance of their implementation

Strategic Financial PlanningIt formulates the method by which financial goals are to be achieved.

There are two dimensions:

1. A Time Frame– Short run is probably anything less than a year.

– Long run is anything over that; usually taken to be a two-year to five-year period.

2. A Level of Aggregation– Each division and operational unit should have a plan.

– As the capital-budgeting analyses of each of the firm’s divisions are added up, the firm aggregates these small projects as a big project.

Strategic Financial PlanningScenario AnalysisEach division might be asked to prepare three

different plans for the near term future:1. A Worst Case- This plan would require making the worst

possible assumptions about the companies products and the state of the economy

2. A Normal Case- This plan would require making the most likely assumptions about the company and the economy

3. A Best Case- Each divisions would be required to work out a case based on optimistic assumptions. It could involve new products and expansion.

Components of Financial StrategyStart-Up Costs

A new business venture, even those started by existing companies, has start-up costs. An existing manufacturer looking to release a new line of product has costs that may include new fabricating equipment, new packaging and a marketing plan. Include your start-up costs in your financial strategy.

Competitive Analysis

Your competition affects how you make money and how you spend money. The products and marketing activities of your competition should be included in your financial strategy. An analysis of how the competition will affect revenue needs to be included in your planning.

Ongoing Costs

Revenue

Components of Financial Strategy

Ongoing CostsThese include labor, materials, equipment maintenance, shipping and facilities costs, such as lease and utilities. Break down your ongoing cost projections into monthly numbers to include as part of your financial strategy.

RevenueIn order to create an effective financial strategy, you need to forecast revenue over the length of the project. A comprehensive revenue forecast is necessary when determining how much will be available to pay your ongoing costs, and how much will remain as profit.

85

Objections to Profit MaximizationIt is VagueIt Ignores the Timing of ReturnsIt Ignores RiskAssumes Perfect CompetitionIn new business environment profit

maximization is regarded as UnrealisticDifficultInappropriate Immoral.

86

Maximizing EPS

Ignores timing and risk of the expected benefit

Market value is not a function of EPS. Hence maximizing EPS will not result in highest price for company's shares

Maximizing EPS implies that the firm should make no dividend payment so long as funds can be invested at positive rate of return—such a policy may not always work

87

Shareholders’ Wealth Maximization

Maximizes the net present value of a course of action to shareholders.

Accounts for the timing and risk of the expected benefits.

Benefits are measured in terms of cash flows.

Fundamental objective—maximize the market value of the firm’s shares.

88

Risk-return Trade-offRisk and expected return move in tandem;

the greater the risk, the greater the expected return.

Financial decisions of the firm are guided by the risk-return trade-off.

The return and risk relationship: Return = Risk-free rate + Risk premium

Risk-free rate is a compensation for time and risk premium for risk.

89

Managers Versus Shareholders’ GoalsA company has stakeholders such as employees, debt-holders, consumers, suppliers, government and society.

Managers may perceive their role as reconciling conflicting objectives of stakeholders. This stakeholders’ view of managers’ role may compromise with the objective of SWM.

Managers may pursue their own personal goals at the cost of shareholders, or may play safe and create satisfactory wealth for shareholders than the maximum.

Managers may avoid taking high investment and financing risks that may otherwise be needed to maximize shareholders’ wealth. Such “satisfying” behaviour of managers will frustrate the objective of SWM as a normative guide.

90

Financial Goals and Firm’s Mission and Objectives

Firms’ primary objective is maximizing the welfare of owners, but, in operational terms, they focus on the satisfaction of its customers through the production of goods and services needed by themFirms state their vision, mission and values in broad terms

Wealth maximization is more appropriately a decision criterion, rather than an objective or a goal.

Goals or objectives are missions or basic purposes of a firm’s existence

91

Financial Goals and Firm’s Mission and Objectives

The shareholders’ wealth maximization is the second-level criterion ensuring that the decision meets the minimum standard of the economic performance.

In the final decision-making, the judgement of management plays the crucial role. The wealth maximization criterion would simply indicate whether an action is economically viable or not.

What Will the Planning Process Accomplish?

InteractionsThe plan must make explicit the linkages between

investment proposals and the firm’s financing choices.

OptionsThe plan provides an opportunity for the firm to weigh its

various options.

Feasibility- The different plans must fit into the overall corporation objective of maximizing shareholder wealth

Avoiding SurprisesOne of the purpose of financial planning is to avoid surprise.

Costs and BenefitsFinancial executives do financial cost benefit analysis. IRR is a method of cost analysis in certain cases and Economic Rate of Return (ERR) should replace the IRR for adequate and rational appraisal of the same project in both the economy.

Indicative Cost –Benefit-Analysis may be useful for highly subjective decisions or judgments.

The indicative or relative significance of various variables deciding the ultimate outcome of the decision making process can be used for approximate cost benefit analysis.

Costs and BenefitsOngoing business processes require a quick ‘incremental Cost-Benefit analysis’ for quick conclusions.

As long as incremental profit exceeds incremental costs, the project is worth while.

Sustainable Net incremental Benefit is very often a strategic decision. It also require a lot of strategic analysis based on a long-tem appraisal of the uncertainty involved.

Costs and BenefitsThe long term project will have to be assessed with an average Cost Benefit Analysis (CBA) for the project’s life cycle.

CBA with strategic perspective is of vital significance.

Multi-product or multi-locational enterprises always makes use of CBA in totality.

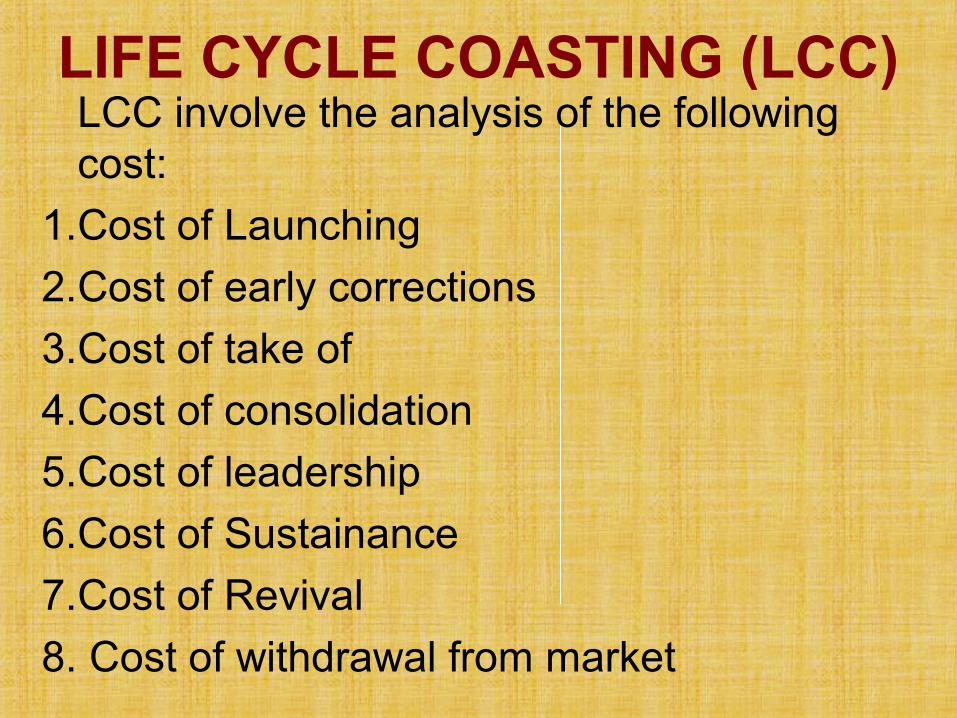

LIFE CYCLE COASTING (LCC) is commonly used of the ‘life-cycle strategy formulations of a project.

LIFE CYCLE COASTING (LCC)LCC involve the analysis of the following cost:

1.Cost of Launching

2.Cost of early corrections

3.Cost of take of

4.Cost of consolidation

5.Cost of leadership

6.Cost of Sustainance

7.Cost of Revival

8. Cost of withdrawal from market

97

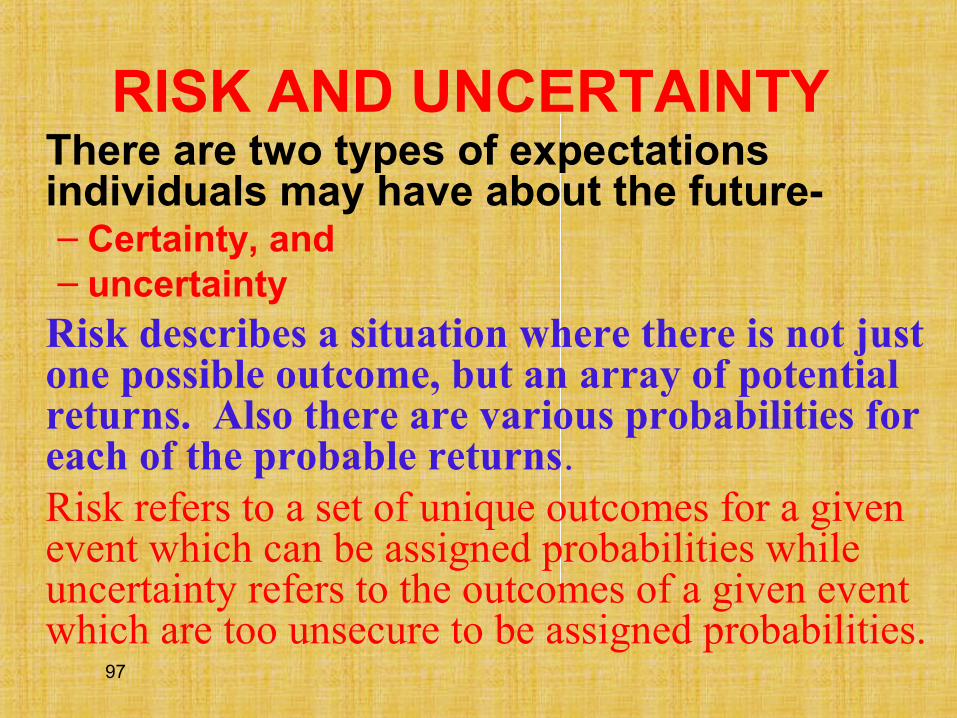

RISK AND UNCERTAINTY There are two types of expectations individuals may have about the future- – Certainty, and – uncertainty

Risk describes a situation where there is not just one possible outcome, but an array of potential returns. Also there are various probabilities for each of the probable returns.Risk refers to a set of unique outcomes for a given event which can be assigned probabilities while uncertainty refers to the outcomes of a given event which are too unsecure to be assigned probabilities.

12 - 98

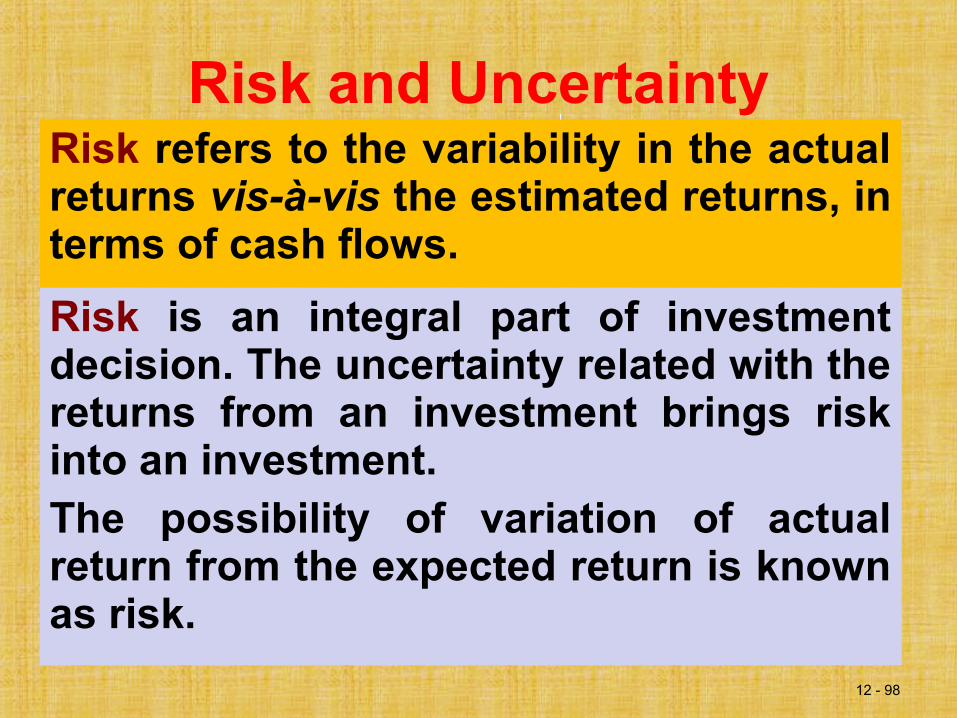

Risk and UncertaintyRisk refers to the variability in the actual returns vis-à-vis the estimated returns, in terms of cash flows.

Risk is an integral part of investment decision. The uncertainty related with the returns from an investment brings risk into an investment.The possibility of variation of actual return from the expected return is known as risk.

12 - 99

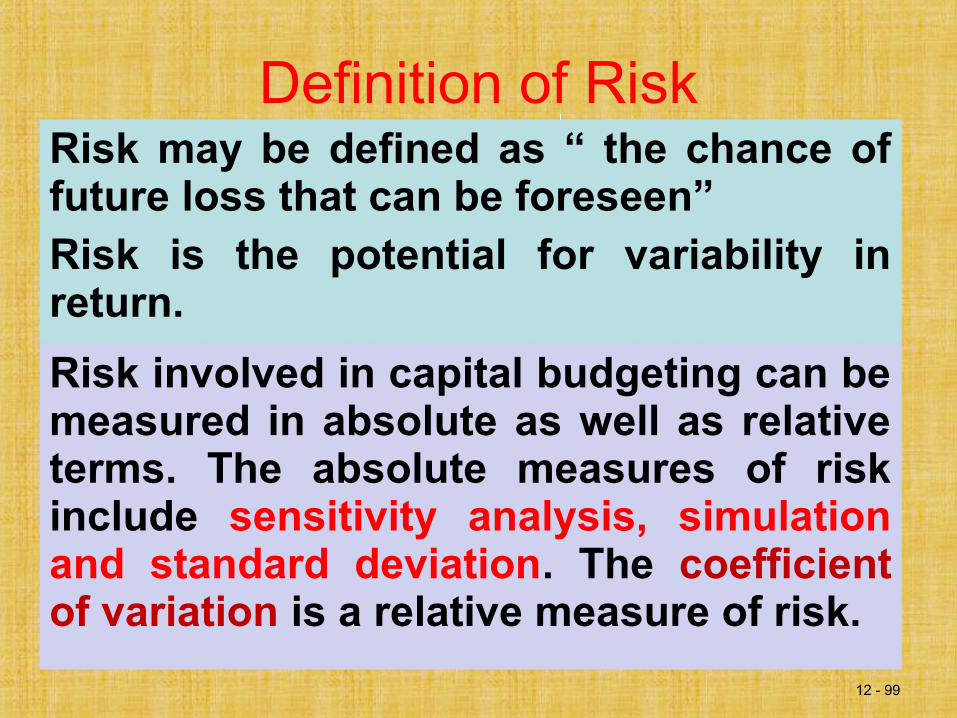

Definition of RiskRisk may be defined as “ the chance of future loss that can be foreseen”Risk is the potential for variability in return.

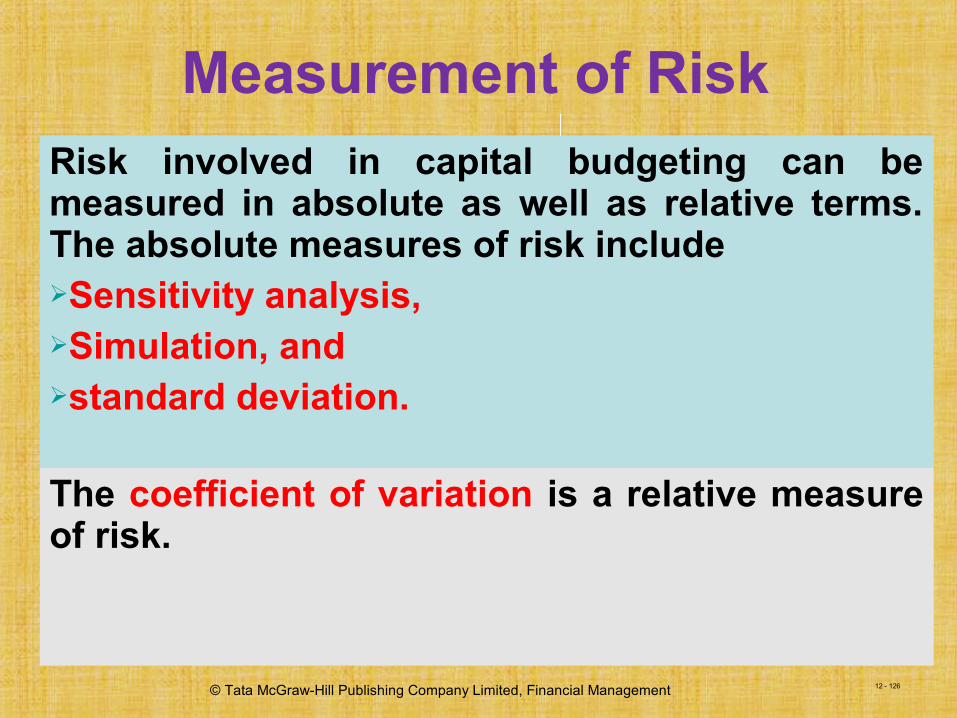

Risk involved in capital budgeting can be measured in absolute as well as relative terms. The absolute measures of risk include sensitivity analysis, simulation and standard deviation. The coefficient of variation is a relative measure of risk.

100

Nature of RiskRisk exists because of the inability of the decision-maker to make perfect forecasts.In formal terms, the risk associated with an investment may be defined as the variability that is likely to occur in the future returns from the investment.Three broad categories of the events influencing the investment forecasts:

– General economic conditions – Industry factors – Company factors

101

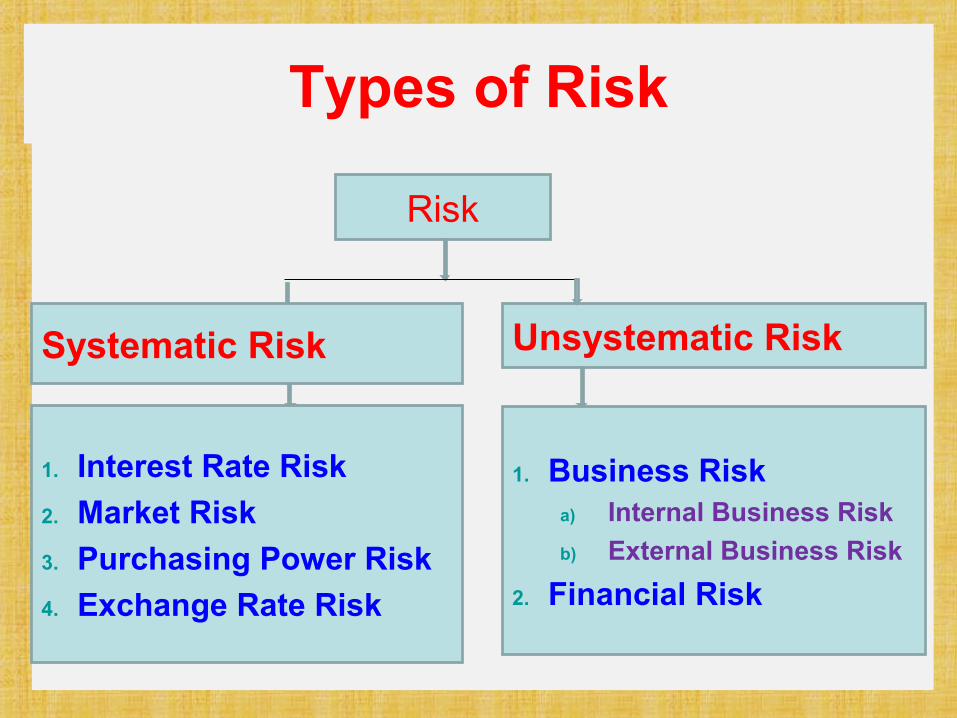

Types of Risk

Risk

1. Business Riska) Internal Business Risk

b) External Business Risk

2. Financial Risk

Unsystematic Risk

1. Interest Rate Risk

2. Market Risk

3. Purchasing Power Risk

4. Exchange Rate Risk

Systematic Risk

12 - 102

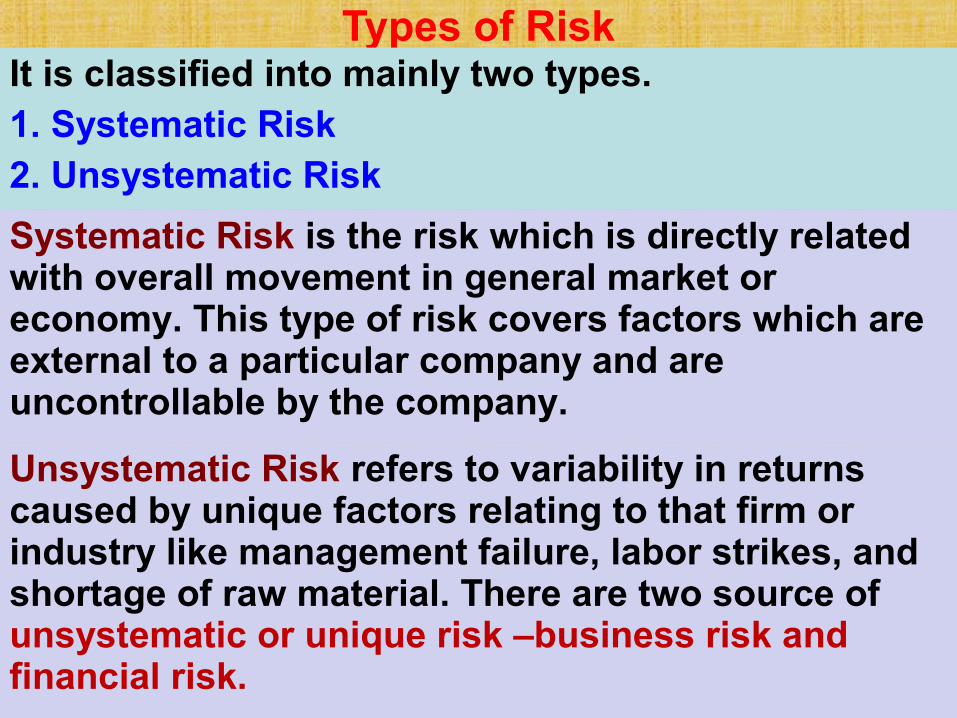

Types of RiskIt is classified into mainly two types.1. Systematic Risk2. Unsystematic Risk

Systematic Risk is the risk which is directly related with overall movement in general market or economy. This type of risk covers factors which are external to a particular company and are uncontrollable by the company.

Unsystematic Risk refers to variability in returns caused by unique factors relating to that firm or industry like management failure, labor strikes, and shortage of raw material. There are two source of unsystematic or unique risk –business risk and financial risk.

12 - 103

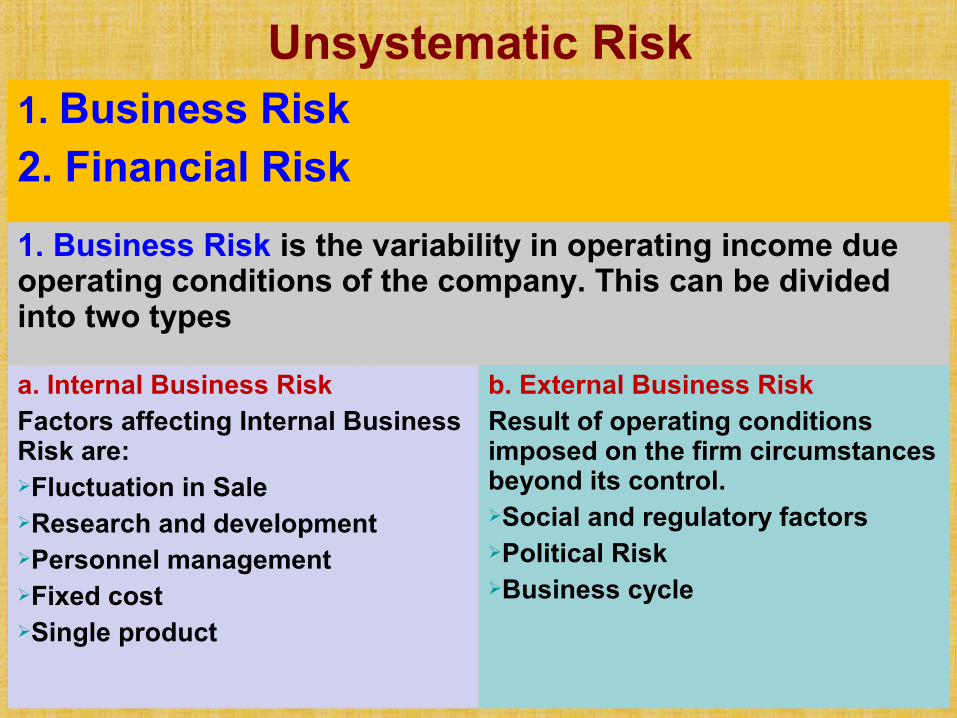

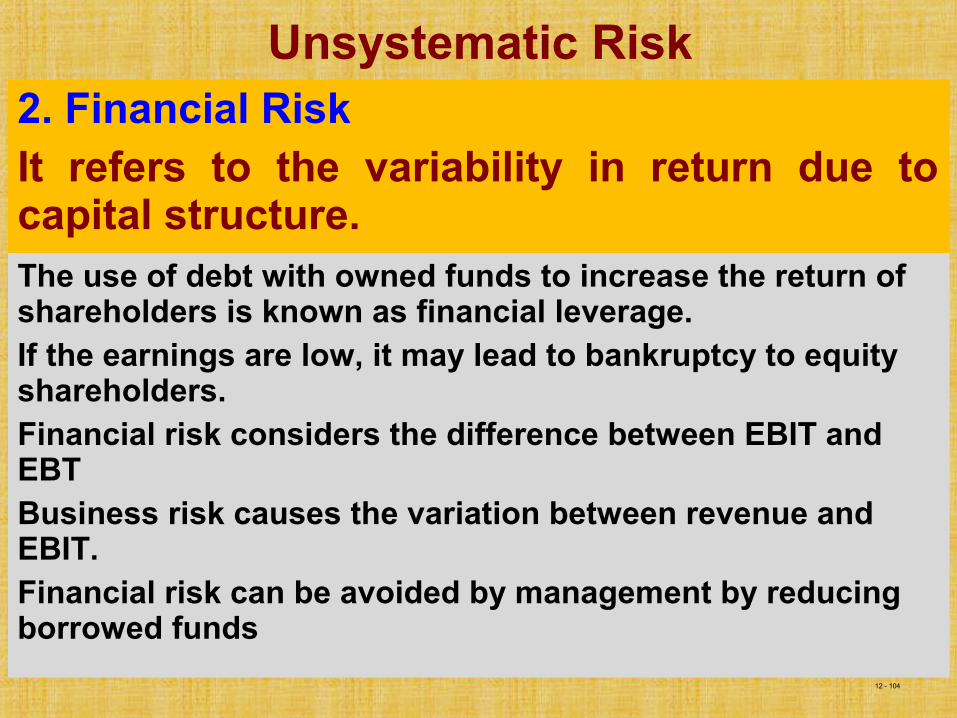

Unsystematic Risk 1. Business Risk2. Financial Risk

1. Business Risk is the variability in operating income due operating conditions of the company. This can be divided into two types

a. Internal Business RiskFactors affecting Internal Business Risk are:Fluctuation in SaleResearch and developmentPersonnel managementFixed costSingle product

b. External Business RiskResult of operating conditions imposed on the firm circumstances beyond its control.Social and regulatory factorsPolitical RiskBusiness cycle

12 - 104

Unsystematic Risk 2. Financial RiskIt refers to the variability in return due to capital structure.The use of debt with owned funds to increase the return of shareholders is known as financial leverage.If the earnings are low, it may lead to bankruptcy to equity shareholders.Financial risk considers the difference between EBIT and EBT Business risk causes the variation between revenue and EBIT. Financial risk can be avoided by management by reducing borrowed funds

12 - 105

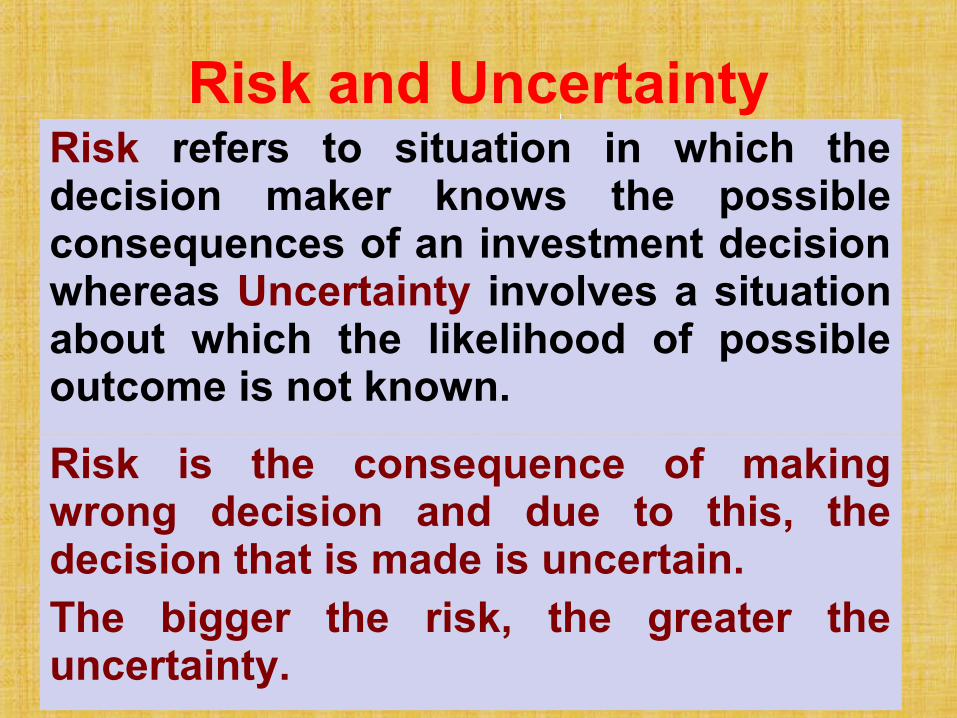

Risk and UncertaintyRisk refers to situation in which the decision maker knows the possible consequences of an investment decision whereas Uncertainty involves a situation about which the likelihood of possible outcome is not known.

Risk is the consequence of making wrong decision and due to this, the decision that is made is uncertain.The bigger the risk, the greater the uncertainty.

12 - 106

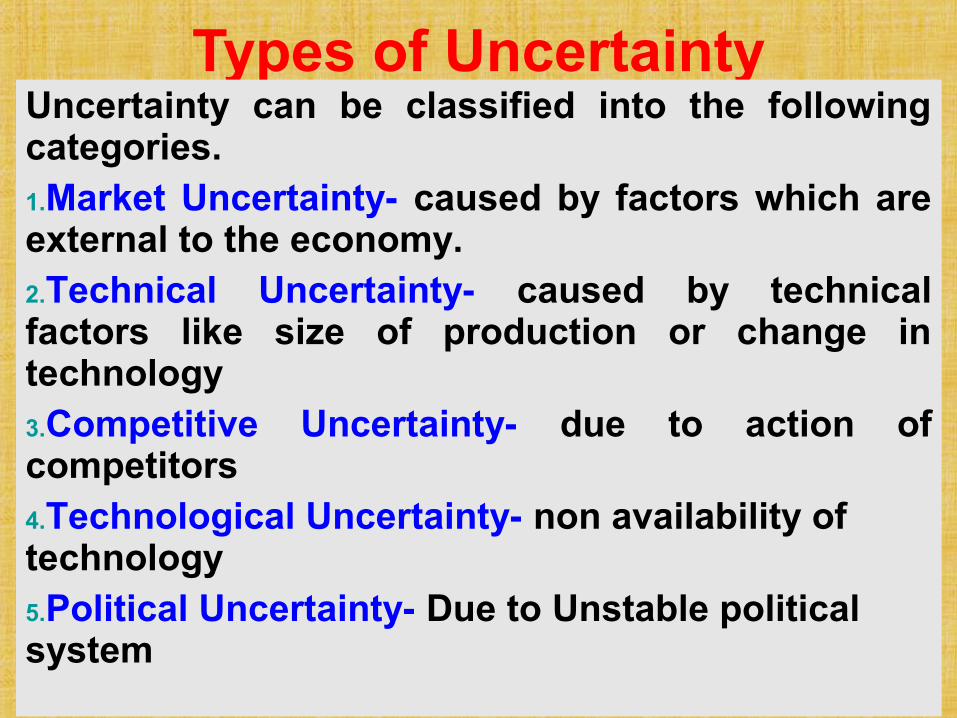

Types of UncertaintyUncertainty can be classified into the following categories.1.Market Uncertainty- caused by factors which are external to the economy.2.Technical Uncertainty- caused by technical factors like size of production or change in technology3.Competitive Uncertainty- due to action of competitors4.Technological Uncertainty- non availability of technology5.Political Uncertainty- Due to Unstable political system

12 - 107

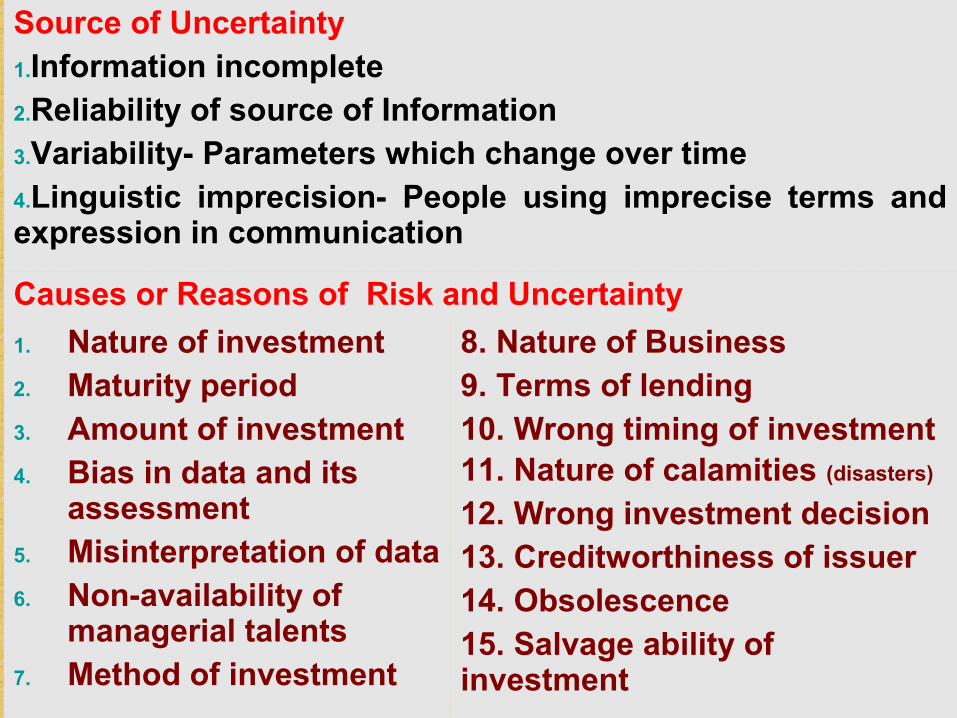

Source of Uncertainty1.Information incomplete2.Reliability of source of Information3.Variability- Parameters which change over time4.Linguistic imprecision- People using imprecise terms and expression in communication

Causes or Reasons of Risk and Uncertainty

1. Nature of investment2. Maturity period3. Amount of investment4. Bias in data and its

assessment5. Misinterpretation of data6. Non-availability of

managerial talents7. Method of investment

8. Nature of Business9. Terms of lending10. Wrong timing of investment11. Nature of calamities (disasters)

12. Wrong investment decision13. Creditworthiness of issuer14. Obsolescence15. Salvage ability of investment

12 - 108

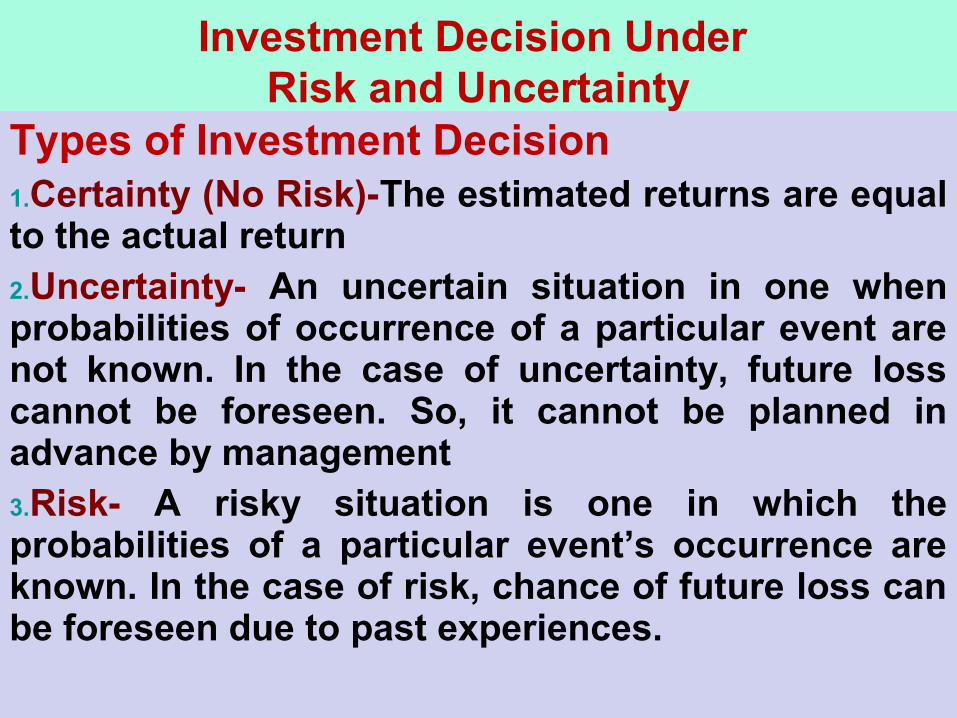

Investment Decision Under Risk and Uncertainty

Types of Investment Decision1.Certainty (No Risk)-The estimated returns are equal to the actual return2.Uncertainty- An uncertain situation in one when probabilities of occurrence of a particular event are not known. In the case of uncertainty, future loss cannot be foreseen. So, it cannot be planned in advance by management3.Risk- A risky situation is one in which the probabilities of a particular event’s occurrence are known. In the case of risk, chance of future loss can be foreseen due to past experiences.

12 - 109

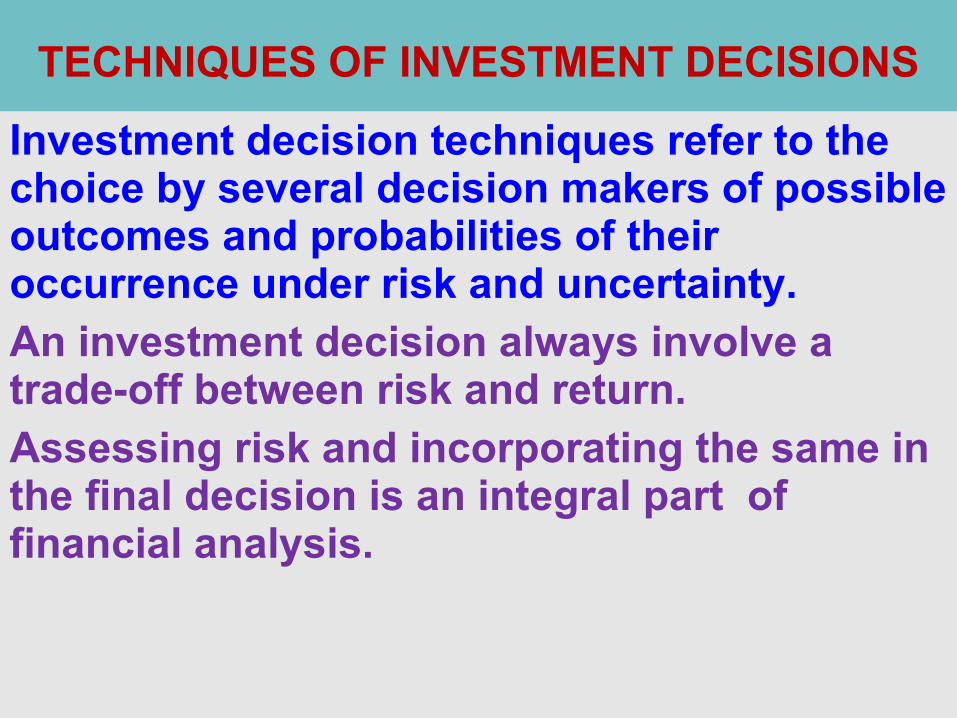

TECHNIQUES OF INVESTMENT DECISIONS

Investment decision techniques refer to the choice by several decision makers of possible outcomes and probabilities of their occurrence under risk and uncertainty.An investment decision always involve a trade-off between risk and return.Assessing risk and incorporating the same in the final decision is an integral part of financial analysis.

12 - 110

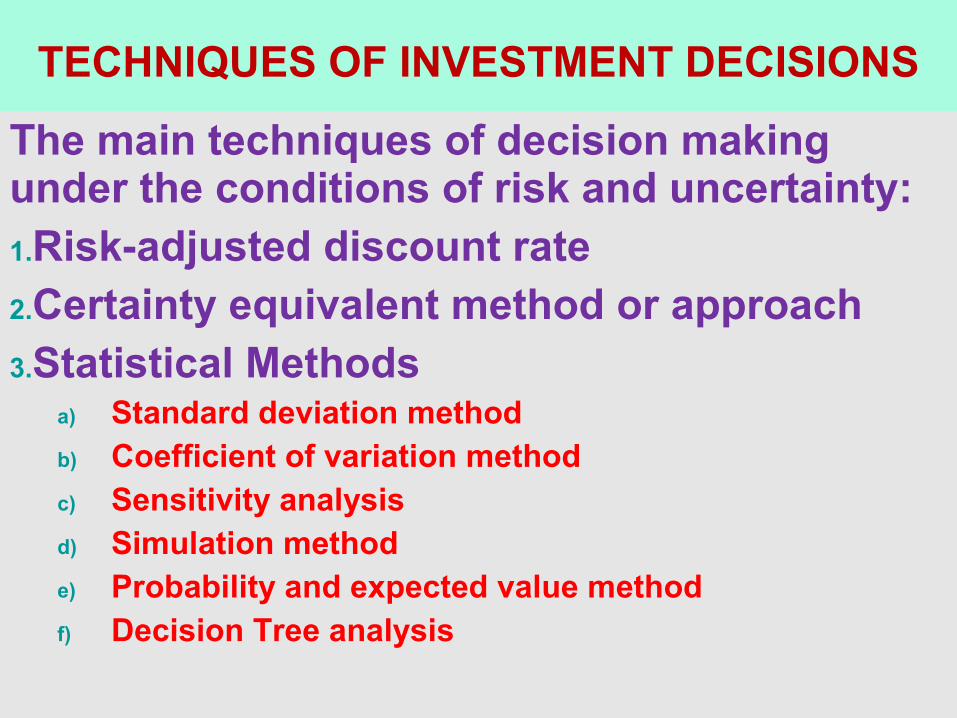

TECHNIQUES OF INVESTMENT DECISIONS

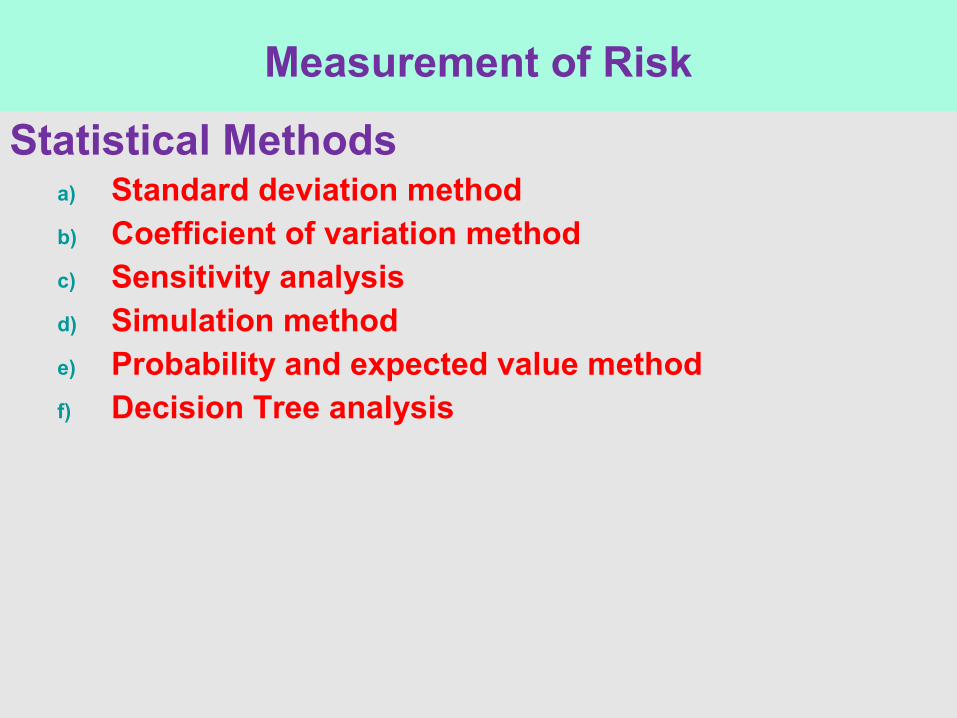

The main techniques of decision making under the conditions of risk and uncertainty:1.Risk-adjusted discount rate2.Certainty equivalent method or approach3.Statistical Methods

a) Standard deviation methodb) Coefficient of variation methodc) Sensitivity analysisd) Simulation methode) Probability and expected value methodf) Decision Tree analysis

12 - 111

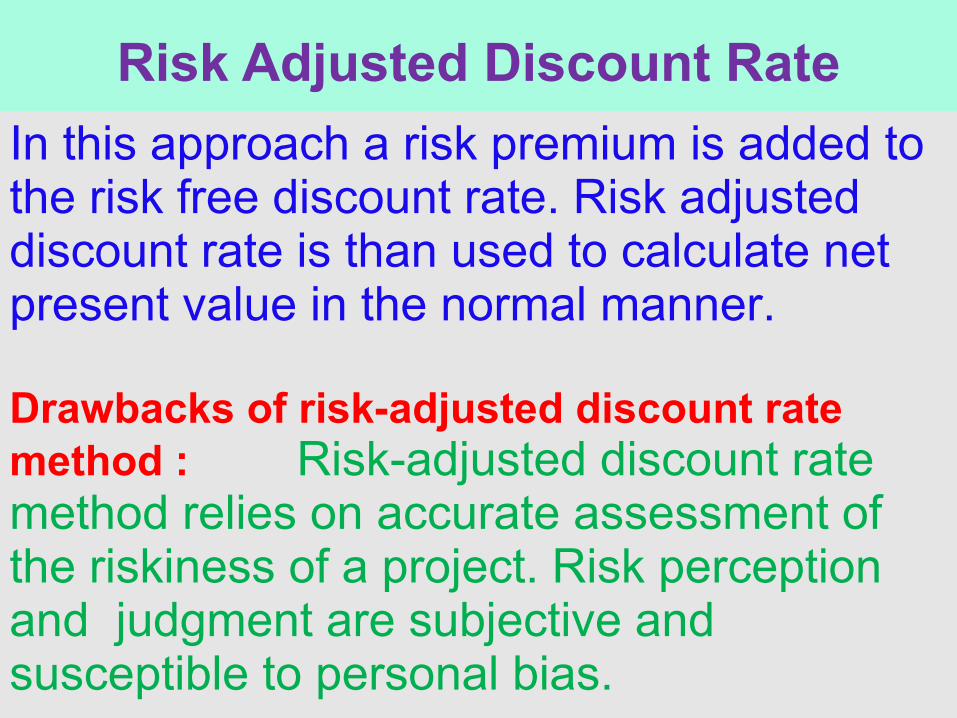

Risk Adjusted Discount Rate

In this approach a risk premium is added to the risk free discount rate. Risk adjusted discount rate is than used to calculate net present value in the normal manner.

Drawbacks of risk-adjusted discount rate method : Risk-adjusted discount rate method relies on accurate assessment of the riskiness of a project. Risk perception and judgment are subjective and susceptible to personal bias.

112

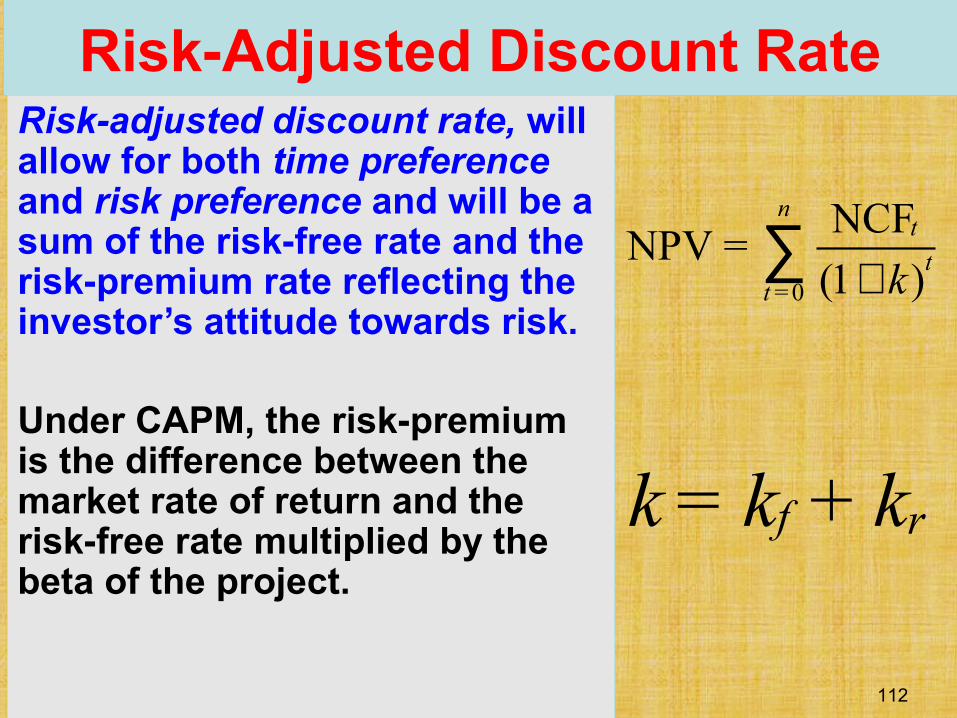

Risk-Adjusted Discount RateRisk-adjusted discount rate, will allow for both time preference and risk preference and will be a sum of the risk-free rate and the risk-premium rate reflecting the investor’s attitude towards risk.

Under CAPM, the risk-premium is the difference between the market rate of return and the risk-free rate multiplied by the beta of the project.

= 0

NCFNPV =

(1 )

nt

tt k+∑

f rk = k + k

12 - 113

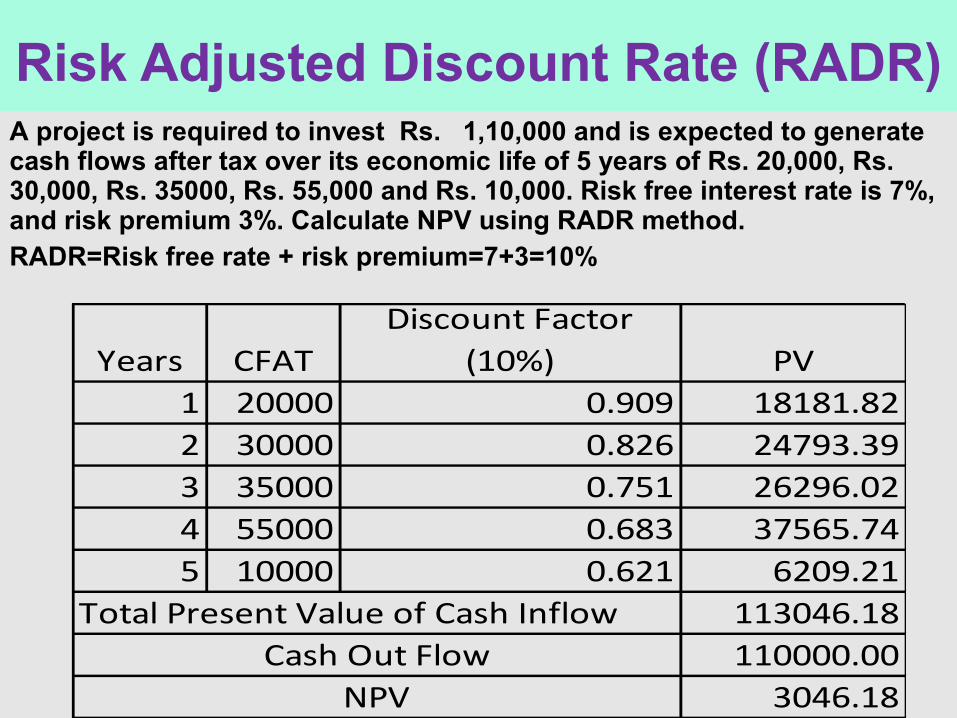

Risk Adjusted Discount Rate (RADR)A project is required to invest Rs. 1,10,000 and is expected to generate cash flows after tax over its economic life of 5 years of Rs. 20,000, Rs. 30,000, Rs. 35000, Rs. 55,000 and Rs. 10,000. Risk free interest rate is 7%, and risk premium 3%. Calculate NPV using RADR method.RADR=Risk free rate + risk premium=7+3=10%

Years CFATDiscount Factor

(10%) PV1 20000 0.909 18181.822 30000 0.826 24793.393 35000 0.751 26296.024 55000 0.683 37565.745 10000 0.621 6209.21

Total Present Value of Cash Inflow 113046.18110000.00

3046.18Cash Out Flow

NPV

114

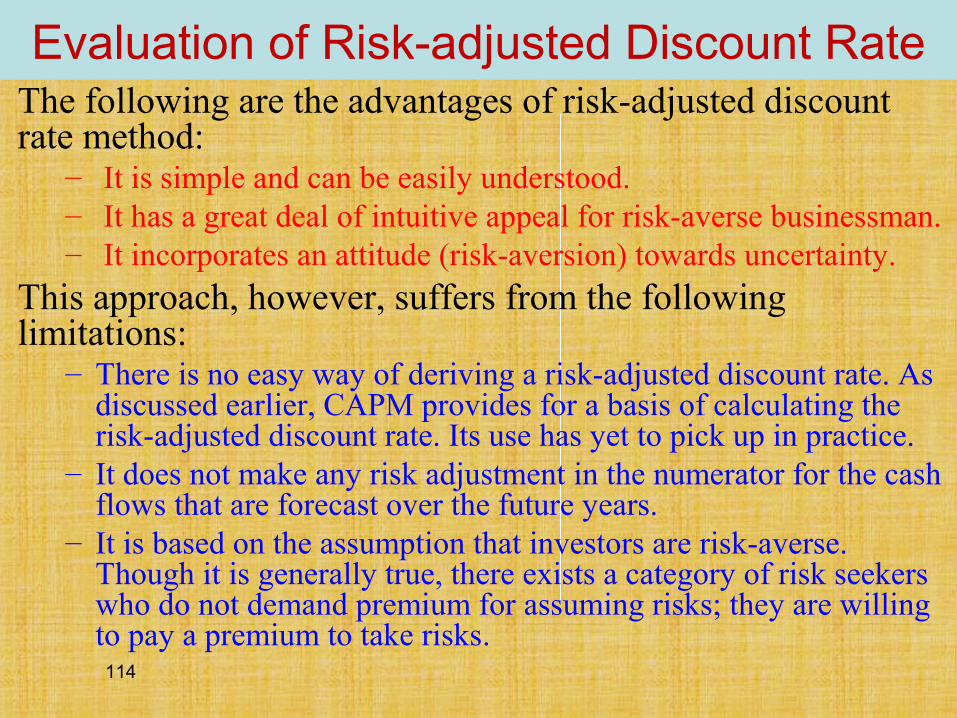

Evaluation of Risk-adjusted Discount RateThe following are the advantages of risk-adjusted discount rate method:

– It is simple and can be easily understood.– It has a great deal of intuitive appeal for risk-averse businessman.– It incorporates an attitude (risk-aversion) towards uncertainty.

This approach, however, suffers from the following limitations:

– There is no easy way of deriving a risk-adjusted discount rate. As discussed earlier, CAPM provides for a basis of calculating the risk-adjusted discount rate. Its use has yet to pick up in practice.

– It does not make any risk adjustment in the numerator for the cash flows that are forecast over the future years.

– It is based on the assumption that investors are risk-averse. Though it is generally true, there exists a category of risk seekers who do not demand premium for assuming risks; they are willing to pay a premium to take risks.

115

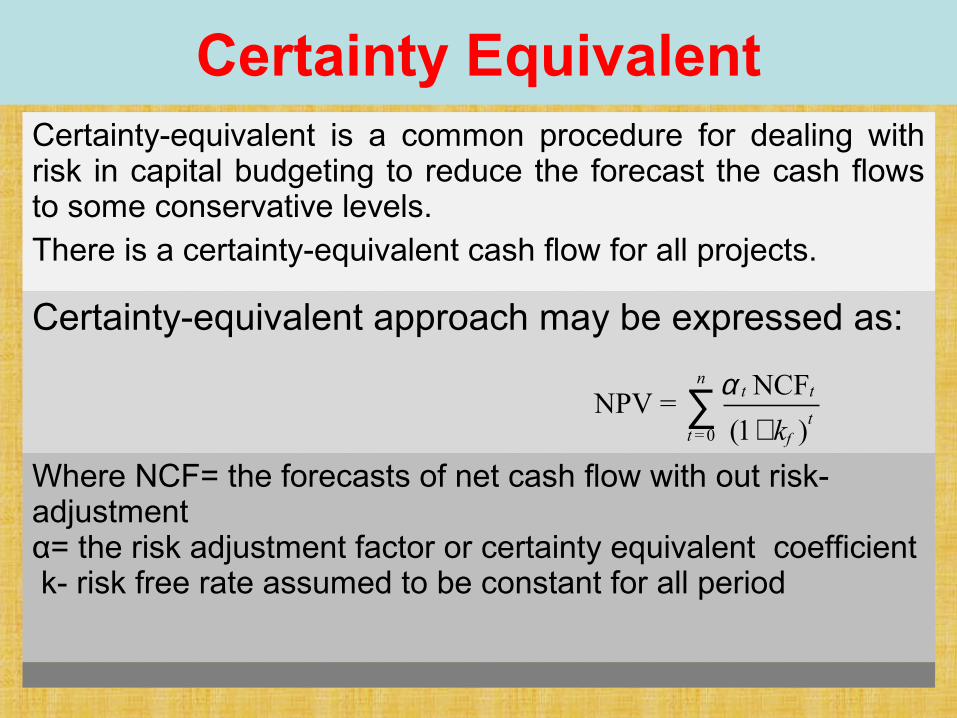

Certainty EquivalentCertainty-equivalent is a common procedure for dealing with risk in capital budgeting to reduce the forecast the cash flows to some conservative levels.There is a certainty-equivalent cash flow for all projects.

Certainty-equivalent approach may be expressed as:

Where NCF= the forecasts of net cash flow with out risk-adjustmentα= the risk adjustment factor or certainty equivalent coefficient k- risk free rate assumed to be constant for all period

= 0

NCFNPV =

(1 )f

nt t

tt k

α+

∑

116 Financial Management, Ninth Edition © I M Pandey

Vikas Publishing House Pvt. Ltd.

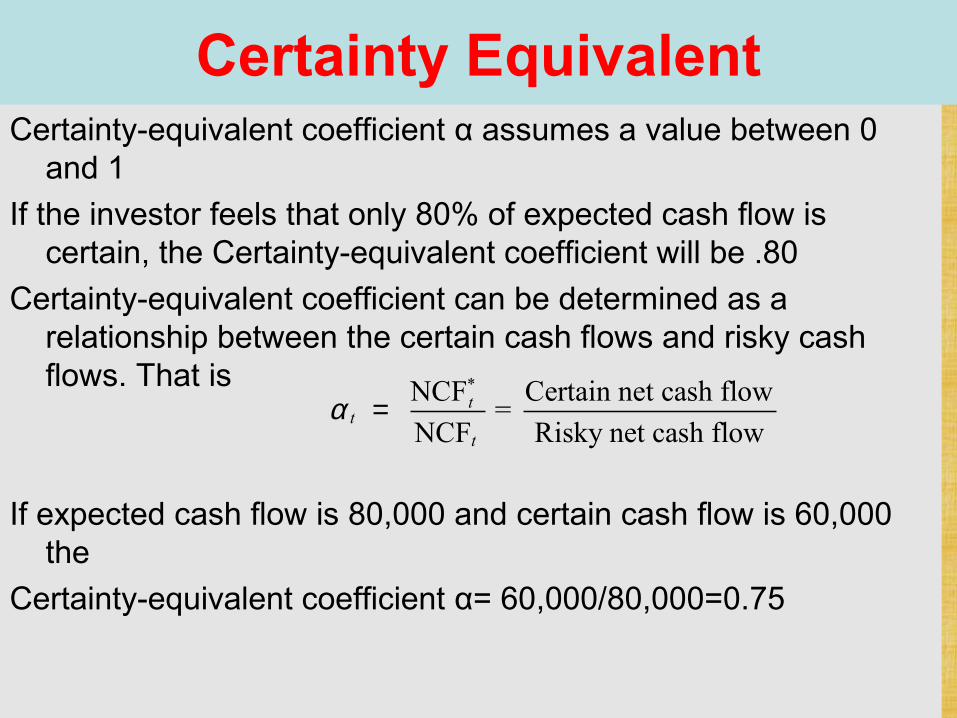

Certainty-equivalent coefficient α assumes a value between 0 and 1

If the investor feels that only 80% of expected cash flow is certain, the Certainty-equivalent coefficient will be .80

Certainty-equivalent coefficient can be determined as a relationship between the certain cash flows and risky cash flows. That is

If expected cash flow is 80,000 and certain cash flow is 60,000 the

Certainty-equivalent coefficient α= 60,000/80,000=0.75

*NCF Certain net cash flow =

NCF Risky net cash flowt

tt

α =

Certainty Equivalent

117

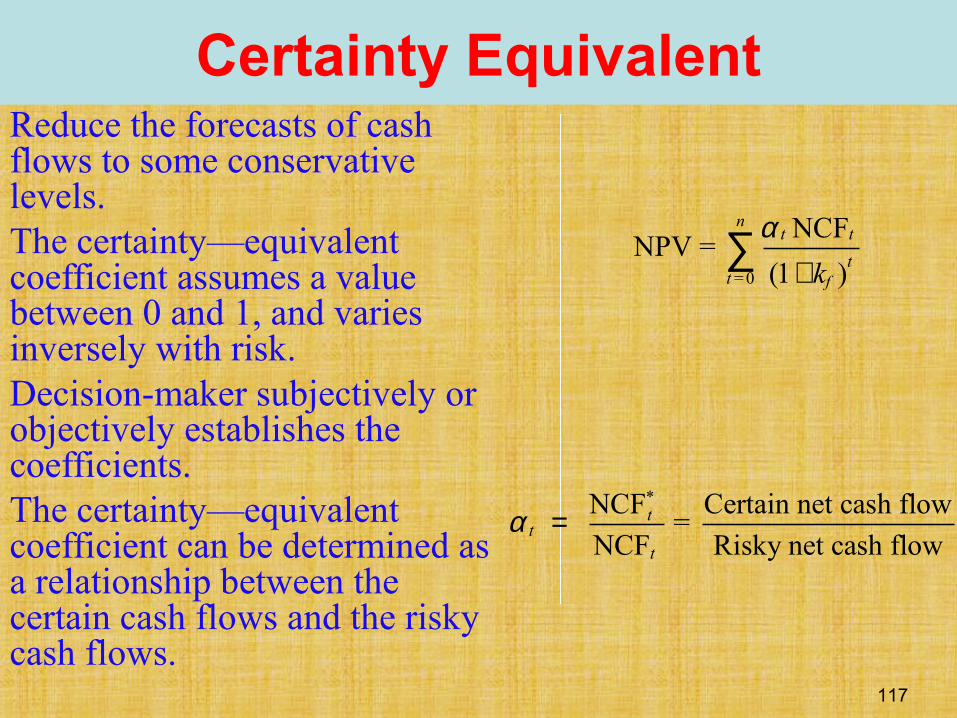

Reduce the forecasts of cash flows to some conservative levels.The certainty—equivalent coefficient assumes a value between 0 and 1, and varies inversely with risk. Decision-maker subjectively or objectively establishes the coefficients.The certainty—equivalent coefficient can be determined as a relationship between the certain cash flows and the risky cash flows.

= 0

NCFNPV =

(1 )f

nt t

tt k

α+

∑

*NCF Certain net cash flow =

NCF Risky net cash flowt

tt

α =

Certainty Equivalent

118

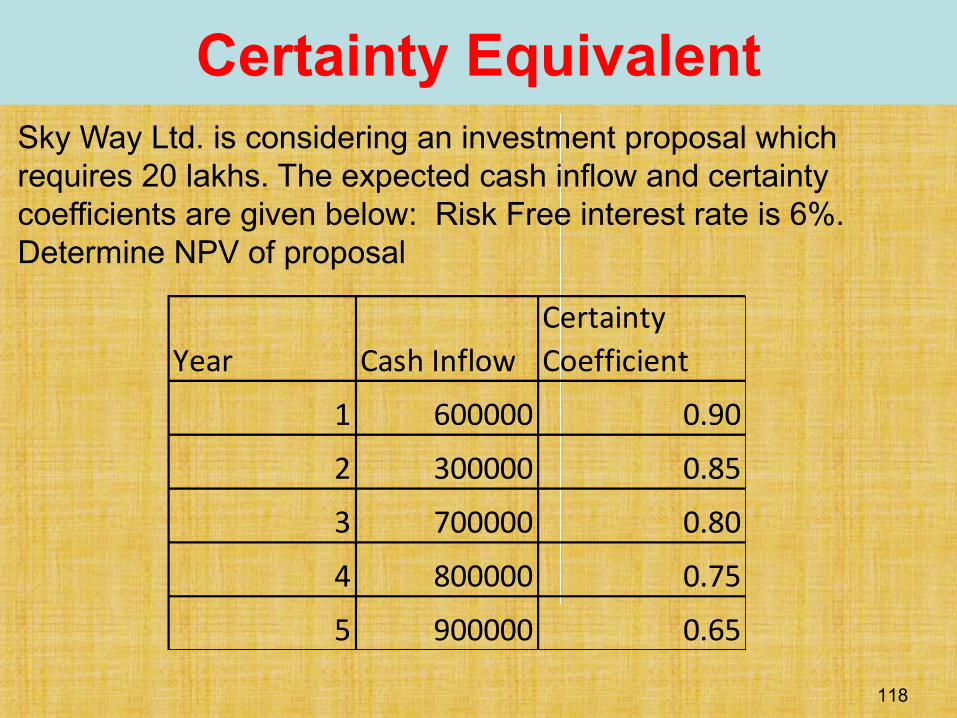

Certainty EquivalentSky Way Ltd. is considering an investment proposal which requires 20 lakhs. The expected cash inflow and certainty coefficients are given below: Risk Free interest rate is 6%. Determine NPV of proposal

Year Cash InflowCertainty Coefficient

1 600000 0.90

2 300000 0.85

3 700000 0.80

4 800000 0.75

5 900000 0.65

119

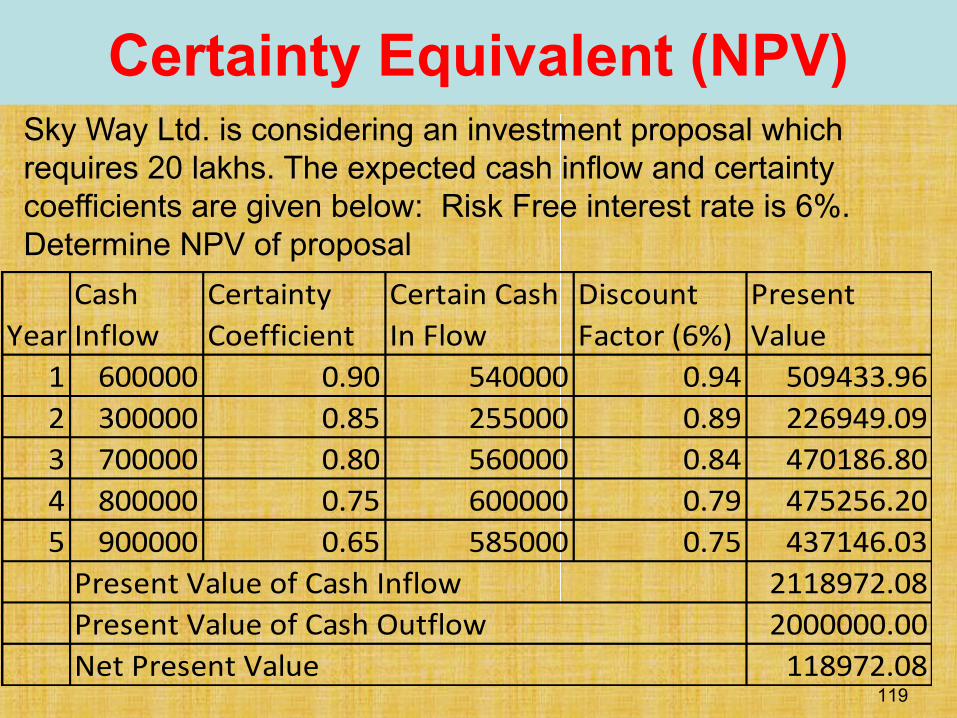

Certainty Equivalent (NPV)Sky Way Ltd. is considering an investment proposal which requires 20 lakhs. The expected cash inflow and certainty coefficients are given below: Risk Free interest rate is 6%. Determine NPV of proposal

YearCash Inflow

Certainty Coefficient

Certain Cash In Flow

Discount Factor (6%)

Present Value

1 600000 0.90 540000 0.94 509433.962 300000 0.85 255000 0.89 226949.093 700000 0.80 560000 0.84 470186.804 800000 0.75 600000 0.79 475256.205 900000 0.65 585000 0.75 437146.03

2118972.082000000.00

118972.08

Present Value of Cash InflowPresent Value of Cash OutflowNet Present Value

120

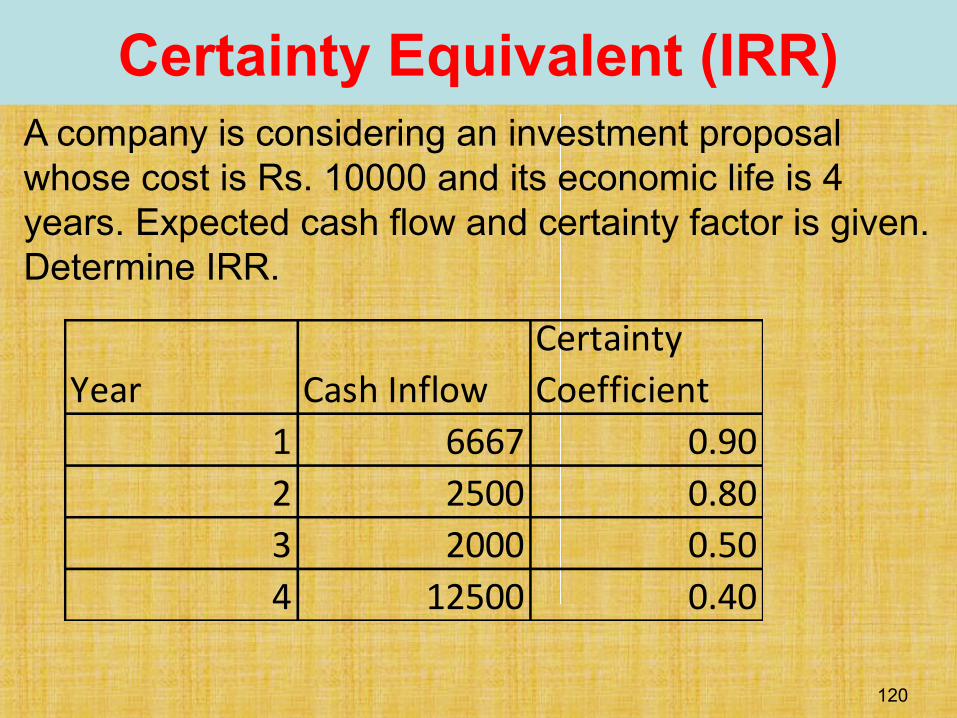

Certainty Equivalent (IRR)A company is considering an investment proposal whose cost is Rs. 10000 and its economic life is 4 years. Expected cash flow and certainty factor is given. Determine IRR.

Year Cash InflowCertainty Coefficient

1 6667 0.902 2500 0.803 2000 0.504 12500 0.40

121

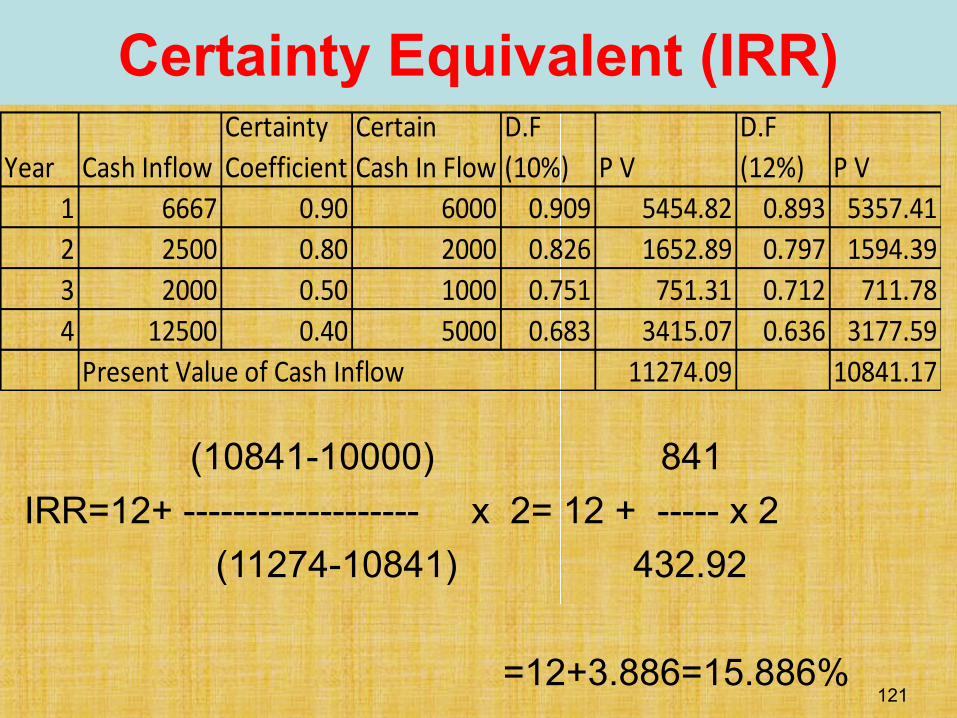

Certainty Equivalent (IRR)

(10841-10000) 841

IRR=12+ ------------------- x 2= 12 + ----- x 2

(11274-10841) 432.92

=12+3.886=15.886%

Year Cash InflowCertainty Coefficient

Certain Cash In Flow

D.F (10%) P V

D.F (12%) P V

1 6667 0.90 6000 0.909 5454.82 0.893 5357.412 2500 0.80 2000 0.826 1652.89 0.797 1594.393 2000 0.50 1000 0.751 751.31 0.712 711.784 12500 0.40 5000 0.683 3415.07 0.636 3177.59

11274.09 10841.17Present Value of Cash Inflow

122

Evaluation of Certainty—Equivalent

This method suffers from many dangers in a large enterprise:

– First, the forecaster, expecting the reduction that will be made in his forecasts, may inflate them in anticipation.

– Second, if forecasts have to pass through several layers of management, the effect may be to greatly exaggerate the original forecast or to make it ultra-conservative.

– Third, by focusing explicit attention only on the gloomy outcomes, chances are increased for passing by some good investments.

123 Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Risk-adjusted Discount Rate Vs. Certainty–Equivalent

The certainty—equivalent approach recognises risk in capital budgeting analysis by adjusting estimated cash flows and employs risk-free rate to discount the adjusted cash flows. On the other hand, the risk-adjusted discount rate adjusts for risk by adjusting the discount rate. It has been suggested that the certainty—equivalent approach is theoretically a superior technique.The risk-adjusted discount rate approach will yield the same result as the certainty—equivalent approach if the risk-free rate is constant and the risk-adjusted discount rate is the same for all future periods.

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 124

Statistical MethodsStatistical techniques are analytical tools for handling risky investments. This enable the decision-maker to make decisions under risk or uncertainty.

The concept of probability is fundamental to the use of the risk analysis techniques.

Probability may be described as a measure of someone’s opinion about the likelihood that an event will occur .

Most commonly used method is to use high, low and best guess estimates

12 - 125

Measurement of Risk

Statistical Methodsa) Standard deviation methodb) Coefficient of variation methodc) Sensitivity analysisd) Simulation methode) Probability and expected value methodf) Decision Tree analysis

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 126

Measurement of RiskRisk involved in capital budgeting can be measured in absolute as well as relative terms. The absolute measures of risk include Sensitivity analysis, Simulation, and standard deviation.

The coefficient of variation is a relative measure of risk.

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 127

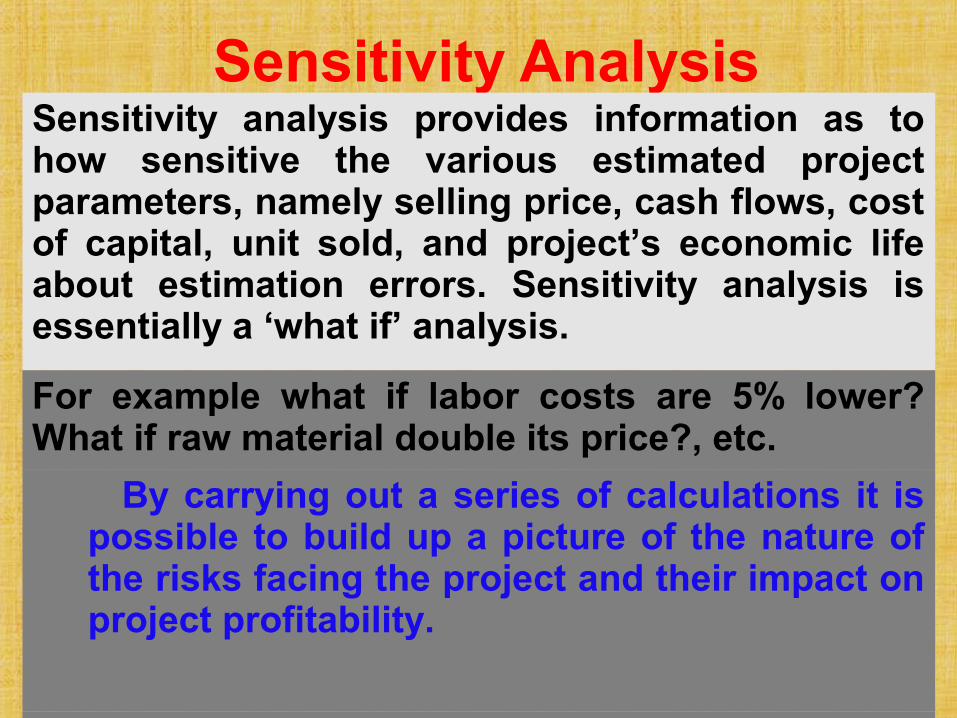

Sensitivity AnalysisSensitivity analysis provides information as to how sensitive the various estimated project parameters, namely selling price, cash flows, cost of capital, unit sold, and project’s economic life about estimation errors. Sensitivity analysis is essentially a ‘what if’ analysis.

For example what if labor costs are 5% lower? What if raw material double its price?, etc.

By carrying out a series of calculations it is possible to build up a picture of the nature of the risks facing the project and their impact on project profitability.

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 128

Sensitivity AnalysisAdvantageous of Sensitivity analysis:Information for decision makingTo direct search – sensitivity analysis points to some variables being more crucial than othersTo make contingency plans –managers can make contingency plans if the key parameters differ significantly from the estimates

Drawbacks of Sensitivity analysis:

The absence of any formal assignment of probabilities to the variations of the parameters is a potential limitation of sensitivity analysis

Another criticism of sensitivity analysis is that each variable is changed in isolation while all other factors remain constant. In practice factors change simultaneously

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 129

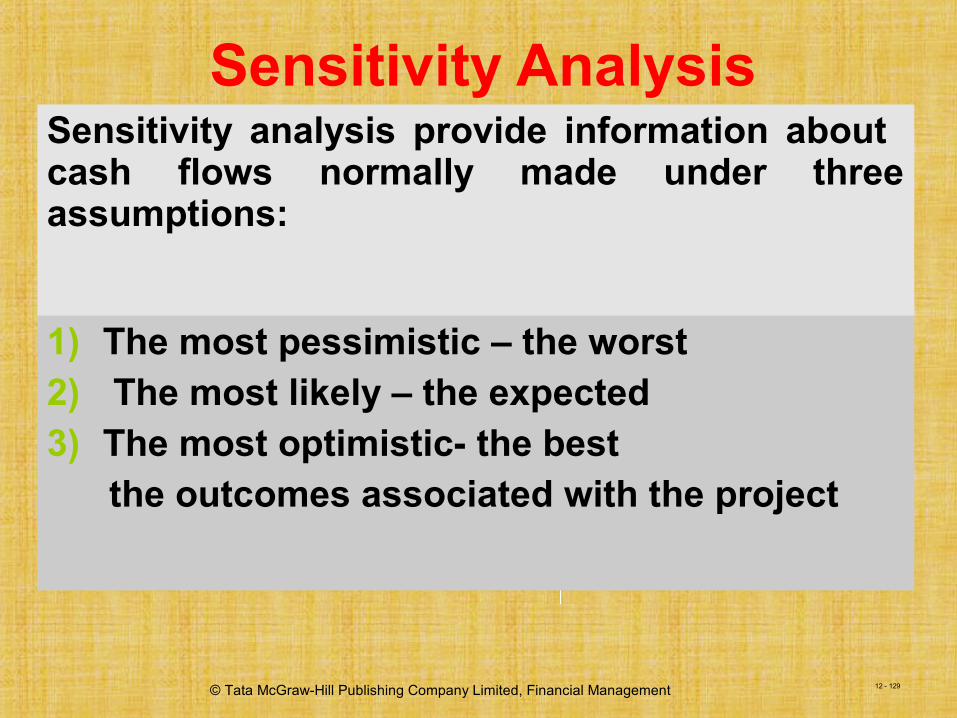

Sensitivity AnalysisSensitivity analysis provide information about cash flows normally made under three assumptions:

1) The most pessimistic – the worst2) The most likely – the expected3) The most optimistic- the best the outcomes associated with the project

12 - 130

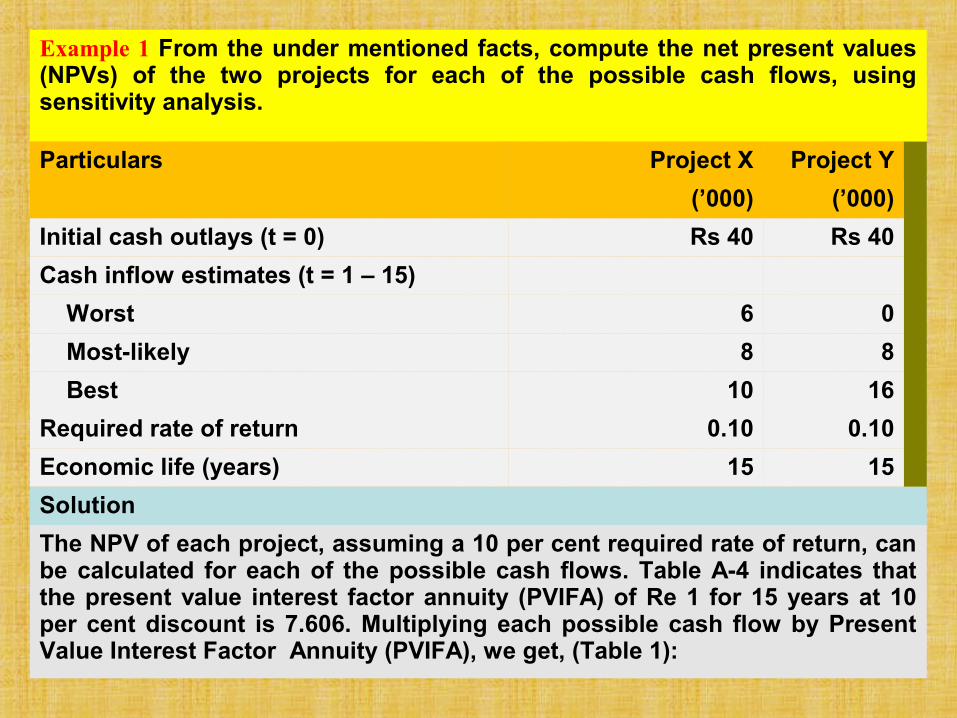

Example 1 From the under mentioned facts, compute the net present values (NPVs) of the two projects for each of the possible cash flows, using sensitivity analysis.

Particulars Project X Project Y

(’000) (’000)

Initial cash outlays (t = 0) Rs 40 Rs 40

Cash inflow estimates (t = 1 – 15)

Worst 6 0

Most-likely 8 8

Best 10 16

Required rate of return 0.10 0.10

Economic life (years) 15 15

Solution

The NPV of each project, assuming a 10 per cent required rate of return, can be calculated for each of the possible cash flows. Table A-4 indicates that the present value interest factor annuity (PVIFA) of Re 1 for 15 years at 10 per cent discount is 7.606. Multiplying each possible cash flow by Present Value Interest Factor Annuity (PVIFA), we get, (Table 1):

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 131

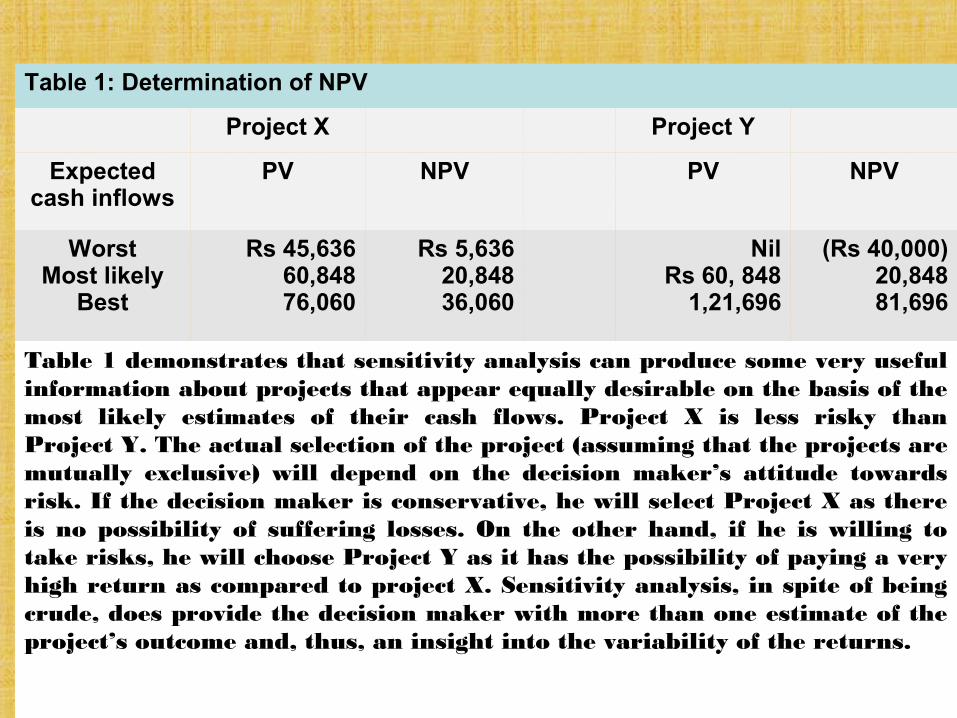

Table 1: Determination of NPV

Project X Project Y

Expected cash inflows

PV NPV PV NPV

WorstMost likely

Best

Rs 45,63660,84876,060

Rs 5,63620,84836,060

NilRs 60, 848

1,21,696

(Rs 40,000)20,84881,696

Table 1 demonstrates that sensitivity analysis can produce some very useful information about projects that appear equally desirable on the basis of the most likely estimates of their cash flows. Project X is less risky than Project Y. The actual selection of the project (assuming that the projects are mutually exclusive) will depend on the decision maker’s attitude towards risk. If the decision maker is conservative, he will select Project X as there is no possibility of suffering losses. On the other hand, if he is willing to take risks, he will choose Project Y as it has the possibility of paying a very high return as compared to project X. Sensitivity analysis, in spite of being crude, does provide the decision maker with more than one estimate of the project’s outcome and, thus, an insight into the variability of the returns.

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 132

Assigning Probability

It has been shown above that sensitivity analysis provides more than one estimate of the future return of a project. It is, therefore, superior to single-figure forecast as it gives a more precise idea regarding the variability of the returns. But it has a limitation in that it does not disclose the chances of occurrence of these variations. To remedy this shortcoming of sensitivity analysis so as to provide a more accurate forecast, the probability of the occurring variations should also be given. Probability assignment to expected cash flows, therefore, would provide a more precise measure of the variability of cash flows. The concept of probability is helpful as it indicates the percentage chance of occurrence of each possible cash flow.

For instance, if some expected cash flow has 0.6 probability of occurrence, it means that the given cash flow is likely to be obtained in 6 out of 10 times (i.e. 60 per cent). Likewise, if a cash flow has a probability of 1, it is certain to occur (as in the case of purchase–lease capital budgeting decision that is, the chances of its occurrence are 100 per cent). With zero probability, the cash flow estimate will never materialise. Thus, probability of obtaining particular cash flow estimates would be between zero and one.

12 - 133

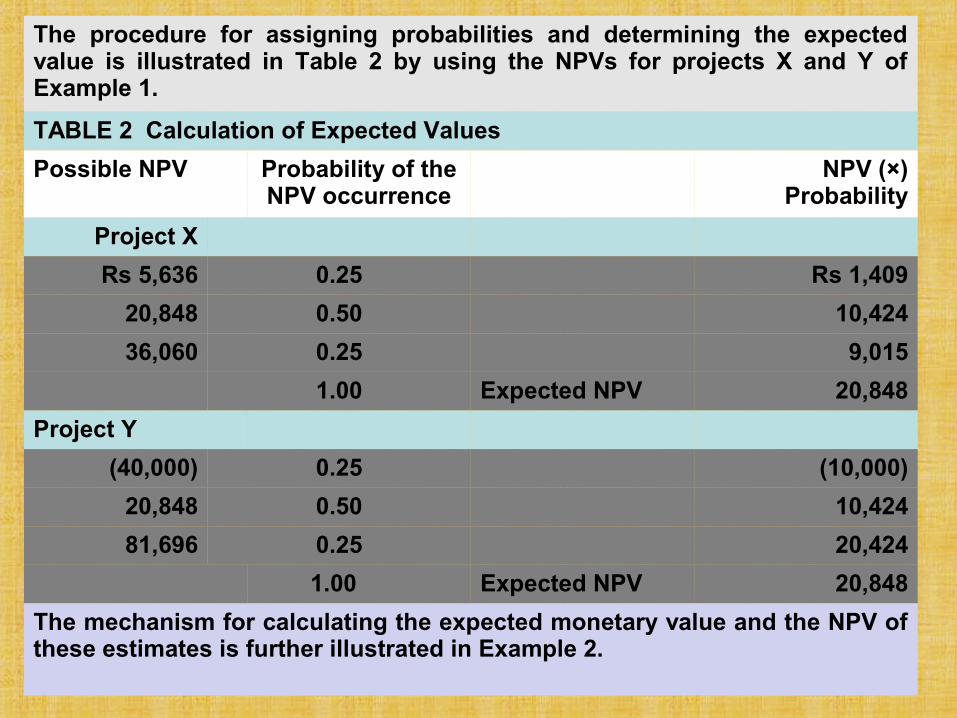

The procedure for assigning probabilities and determining the expected value is illustrated in Table 2 by using the NPVs for projects X and Y of Example 1.

TABLE 2 Calculation of Expected Values

Possible NPV Probability of the NPV occurrence

NPV (×) Probability

Project X

Rs 5,636 0.25 Rs 1,409

20,848 0.50 10,424

36,060 0.25 9,015

1.00 Expected NPV 20,848

Project Y

(40,000) 0.25 (10,000)

20,848 0.50 10,424

81,696 0.25 20,424

1.00 Expected NPV 20,848

The mechanism for calculating the expected monetary value and the NPV of these estimates is further illustrated in Example 2.

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 134

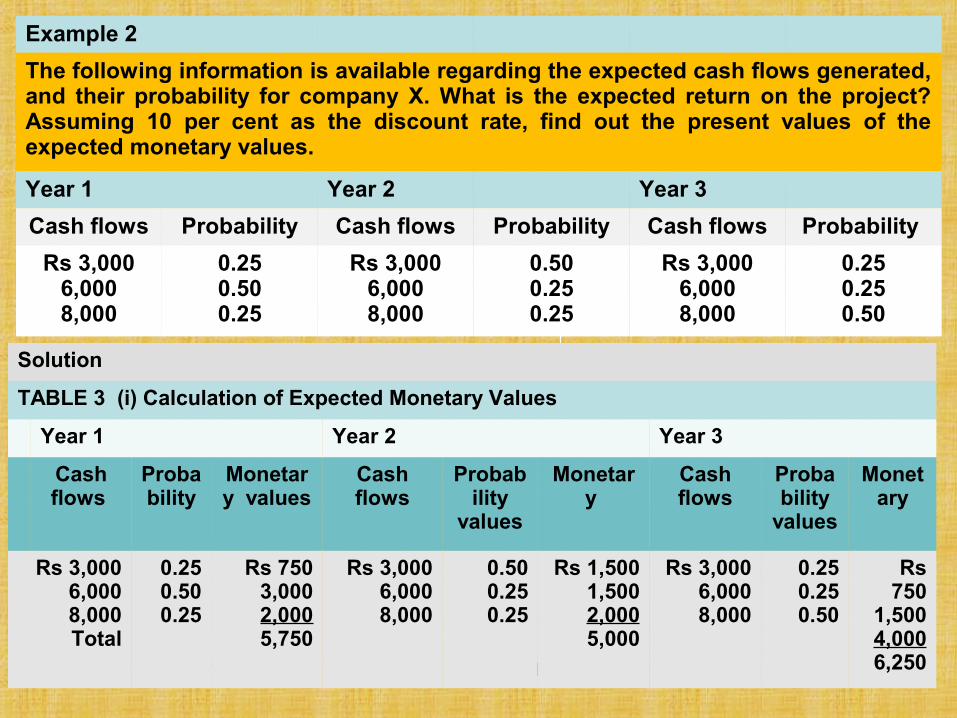

Example 2

The following information is available regarding the expected cash flows generated, and their probability for company X. What is the expected return on the project? Assuming 10 per cent as the discount rate, find out the present values of the expected monetary values.

Year 1 Year 2 Year 3

Cash flows Probability Cash flows Probability Cash flows Probability

Rs 3,0006,0008,000

0.250.500.25

Rs 3,0006,0008,000

0.500.250.25

Rs 3,0006,0008,000

0.250.250.50

Solution

TABLE 3 (i) Calculation of Expected Monetary Values

Year 1 Year 2 Year 3

Cash flows

Probability

Monetary values

Cash flows

Probability

values

Monetary

Cash flows

Probability

values

Monetary

Rs 3,0006,0008,000Total

0.250.500.25

Rs 7503,0002,0005,750

Rs 3,0006,0008,000

0.500.250.25

Rs 1,5001,5002,0005,000

Rs 3,0006,0008,000

0.250.250.50

Rs 750

1,5004,0006,250

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 135

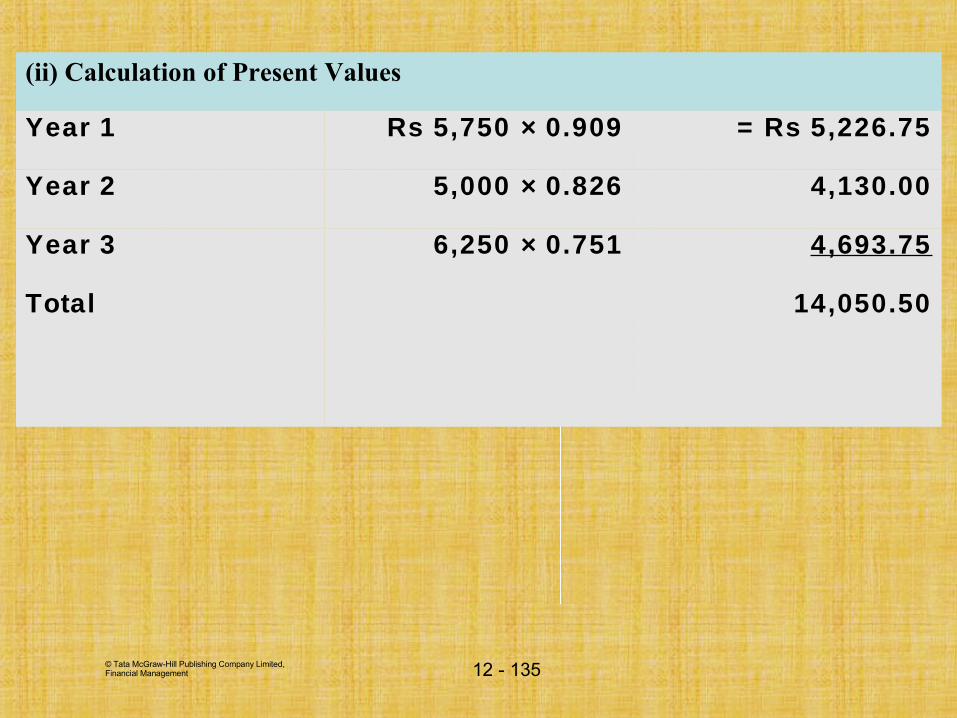

(ii) Calculation of Present Values

Year 1 Rs 5,750 × 0.909 = Rs 5,226.75

Year 2 5,000 × 0.826 4,130.00

Year 3 6,250 × 0.751 4,693.75

Total 14,050.50

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 136

Sensitivity analysis Sensitivity analysis can also be used to ascertain how change in key variables (say, sales volume, sales price, variable costs, operating fixed costs, cost of capital and so on) affect the expected outcome (measured in terms of NPV) of the proposed investment project.

For the purpose of analysis, only one variable is considered, holding the effect of other variables constant, at a point of time.

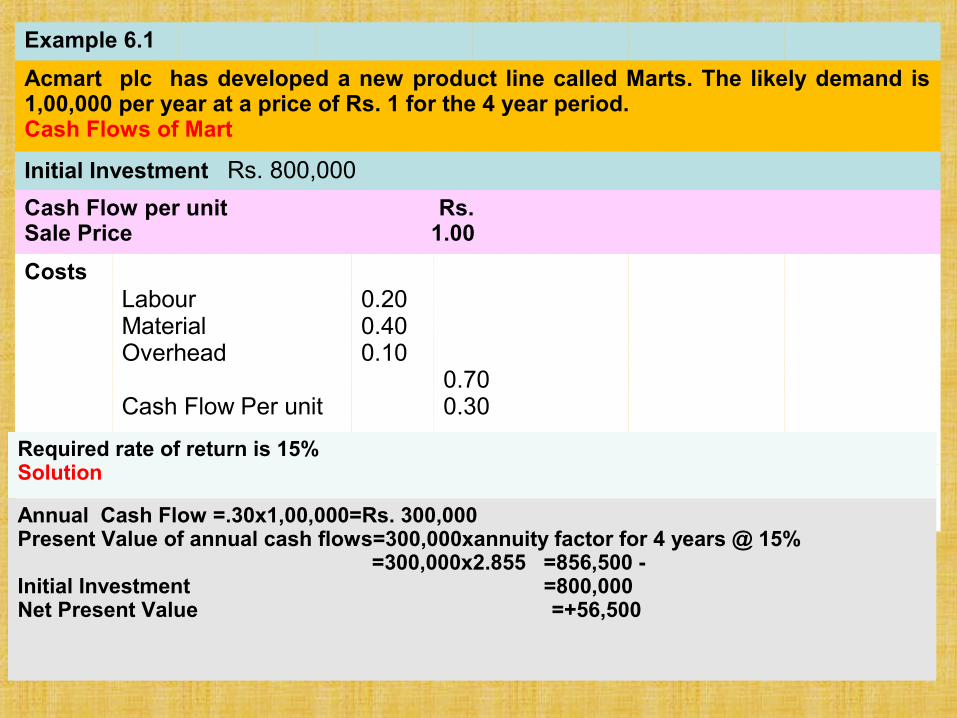

Example 6.1

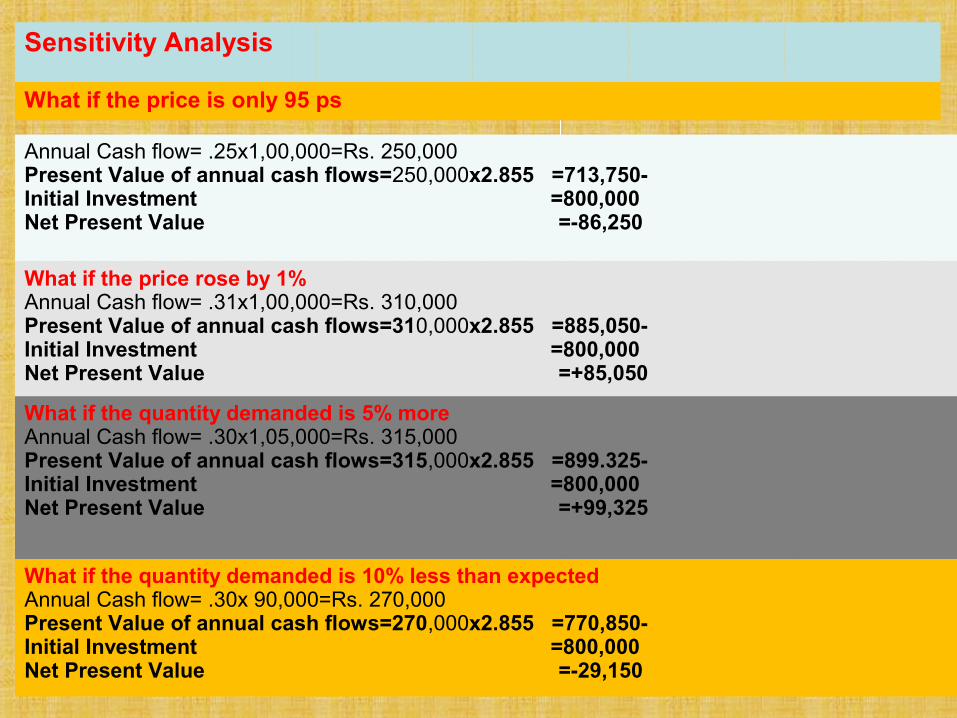

Acmart plc has developed a new product line called Marts. The likely demand is 1,00,000 per year at a price of Rs. 1 for the 4 year period. Cash Flows of Mart

Initial Investment Rs. 800,000

Cash Flow per unit Rs. Sale Price 1.00

CostsLabourMaterialOverhead

Cash Flow Per unit

0.200.400.10

0.700.30

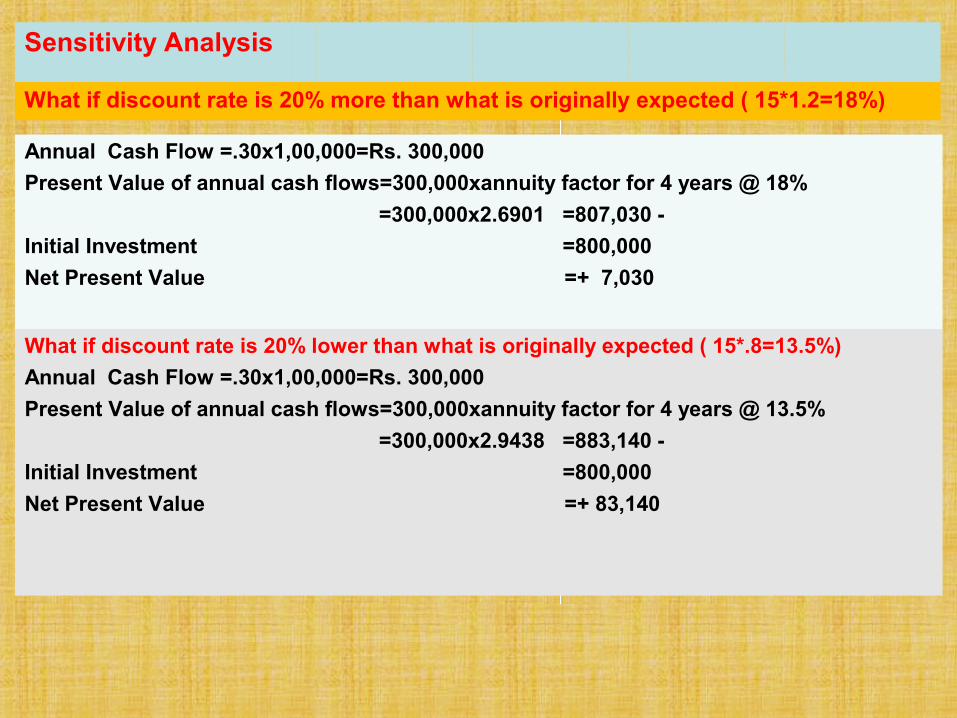

Required rate of return is 15%Solution

Annual Cash Flow =.30x1,00,000=Rs. 300,000Present Value of annual cash flows=300,000xannuity factor for 4 years @ 15% =300,000x2.855 =856,500 -Initial Investment =800,000Net Present Value =+56,500

Sensitivity Analysis

What if the price is only 95 ps

Annual Cash flow= .25x1,00,000=Rs. 250,000Present Value of annual cash flows=250,000x2.855 =713,750-Initial Investment =800,000Net Present Value =-86,250

What if the price rose by 1%Annual Cash flow= .31x1,00,000=Rs. 310,000Present Value of annual cash flows=310,000x2.855 =885,050-Initial Investment =800,000Net Present Value =+85,050

What if the quantity demanded is 5% moreAnnual Cash flow= .30x1,05,000=Rs. 315,000Present Value of annual cash flows=315,000x2.855 =899.325-Initial Investment =800,000Net Present Value =+99,325

What if the quantity demanded is 10% less than expectedAnnual Cash flow= .30x 90,000=Rs. 270,000Present Value of annual cash flows=270,000x2.855 =770,850-Initial Investment =800,000Net Present Value =-29,150

Sensitivity Analysis

What if discount rate is 20% more than what is originally expected ( 15*1.2=18%)

Annual Cash Flow =.30x1,00,000=Rs. 300,000

Present Value of annual cash flows=300,000xannuity factor for 4 years @ 18%

=300,000x2.6901 =807,030 -

Initial Investment =800,000

Net Present Value =+ 7,030

What if discount rate is 20% lower than what is originally expected ( 15*.8=13.5%)

Annual Cash Flow =.30x1,00,000=Rs. 300,000

Present Value of annual cash flows=300,000xannuity factor for 4 years @ 13.5%

=300,000x2.9438 =883,140 -

Initial Investment =800,000

Net Present Value =+ 83,140

Break-Even NPV

The Break-Even point is where NPV is zero. If the NPV is below zero the project is rejected, if it is above zero, it is accepted

Scenario Analysis

With Sensitivity Analysis we change one variable at a time and look at the result.

Managers are often interested in situation where a number of factors change.

They are interested in worst-case and best-case scenario. That is, what NPV will result if all the assumptions made initially turned out to be too optimistic? And what would be the result if, in the event, matters went extremely well on all fronts.

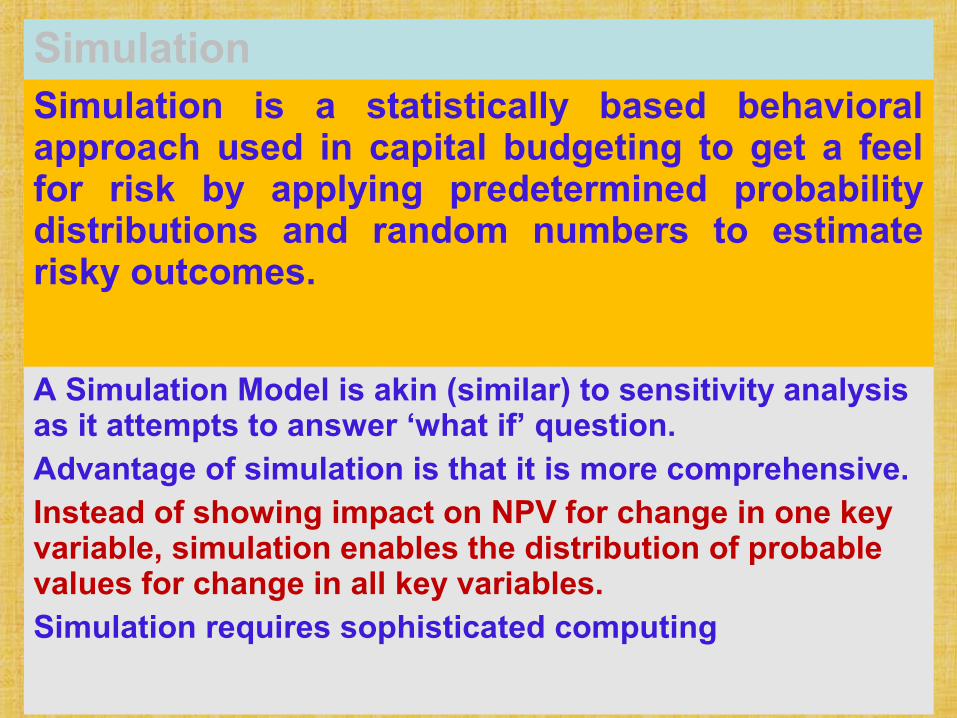

SimulationSimulation is a statistically based behavioral approach used in capital budgeting to get a feel for risk by applying predetermined probability distributions and random numbers to estimate risky outcomes.

A Simulation Model is akin (similar) to sensitivity analysis as it attempts to answer ‘what if’ question. Advantage of simulation is that it is more comprehensive.Instead of showing impact on NPV for change in one key variable, simulation enables the distribution of probable values for change in all key variables.Simulation requires sophisticated computing

143

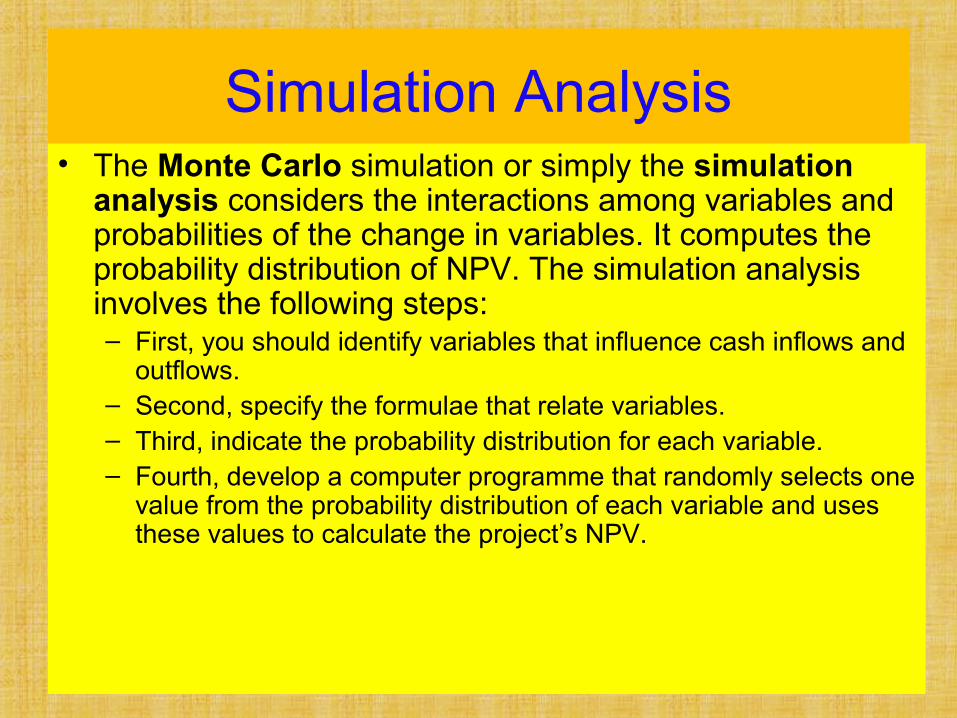

Simulation Analysis• The Monte Carlo simulation or simply the simulation

analysis considers the interactions among variables and probabilities of the change in variables. It computes the probability distribution of NPV. The simulation analysis involves the following steps:– First, you should identify variables that influence cash inflows and

outflows.– Second, specify the formulae that relate variables. – Third, indicate the probability distribution for each variable.– Fourth, develop a computer programme that randomly selects one

value from the probability distribution of each variable and uses these values to calculate the project’s NPV.

144

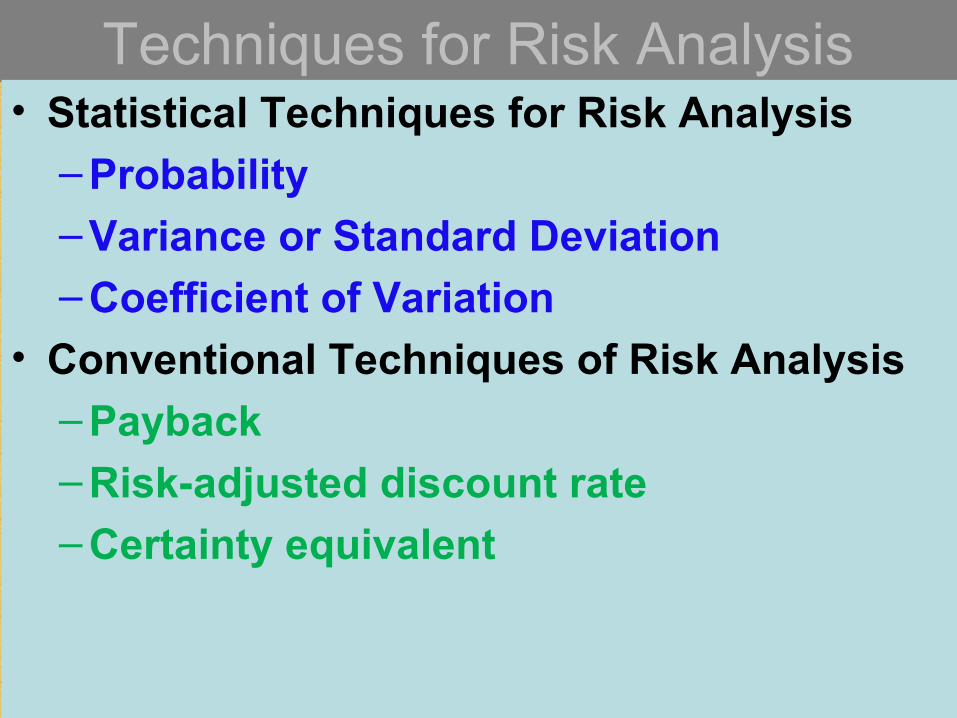

Techniques for Risk Analysis• Statistical Techniques for Risk Analysis

– Probability

– Variance or Standard Deviation

– Coefficient of Variation

• Conventional Techniques of Risk Analysis

– Payback

– Risk-adjusted discount rate

– Certainty equivalent

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 145

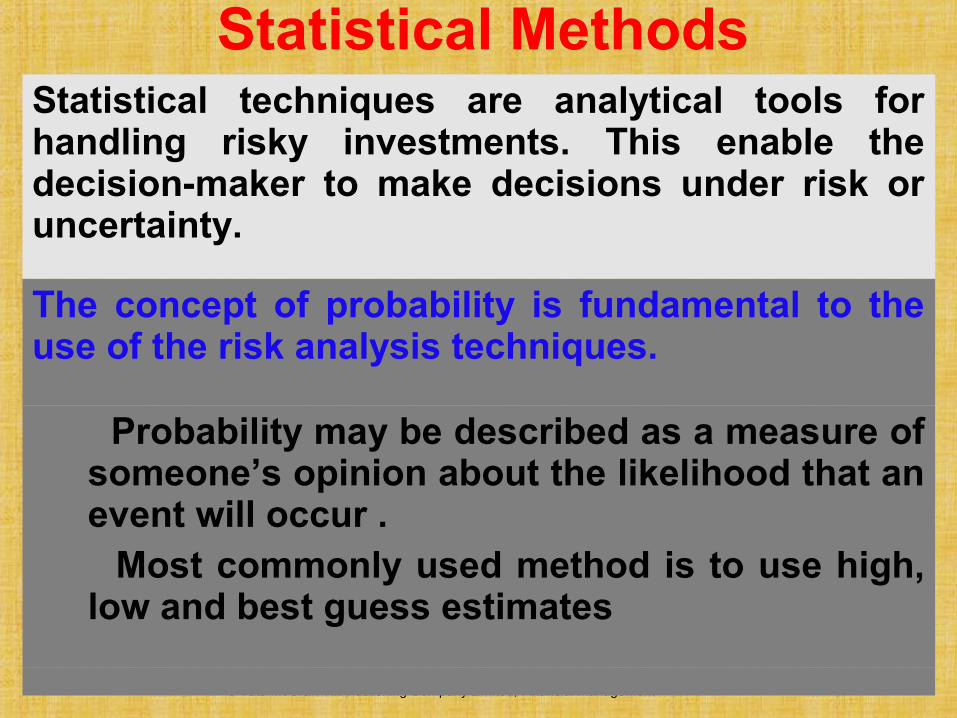

Statistical MethodsStatistical techniques are analytical tools for handling risky investments. This enable the decision-maker to make decisions under risk or uncertainty.

The concept of probability is fundamental to the use of the risk analysis techniques.

Probability may be described as a measure of someone’s opinion about the likelihood that an event will occur .

Most commonly used method is to use high, low and best guess estimates

146 Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Probability• A typical forecast is single figure for a period. This is

referred to as “best estimate” or “most likely” forecast:– Firstly, we do not know the chances of this

figure actually occurring, i.e., the uncertainty surrounding this figure.

– Secondly, the meaning of best estimates or most likely is not very clear. It is not known whether it is mean, median or mode.

• For these reasons, a forecaster should not give just one estimate, but a range of associated probability–a probability distribution.

• Probability may be described as a measure of someone’s opinion about the likelihood that an event will occur.

147 Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Assigning Probability • The probability estimate, which is based on a

very large number of observations, is known as an objective probability.

• Such probability assignments that reflect the state of belief of a person rather than the objective evidence of a large number of trials are called personal or subjective probabilities.

148

Expected Net Present Value• Once the probability

assignments have been made to the future cash flows the next step is to find out the expected net present value.

• Expected net present value = Sum of present values of expected net cash flows.

= 0

ENPV = (1 )

n

tt

ENCF

k+∑

ENCF = NCF × t jt jtP

149

Variance or Standard Deviation • Simply stated,

variance measures the deviation about expected cash flow of each of the possible cash flows.

• Standard deviation is the square root of variance.

• Absolute Measure of Risk.

2 2

=1

(NCF) = (NCF – ENCF)n

j jj

Pσ ∑

© Tata McGraw-Hill Publishing Company Limited, Financial Management 12 - 150

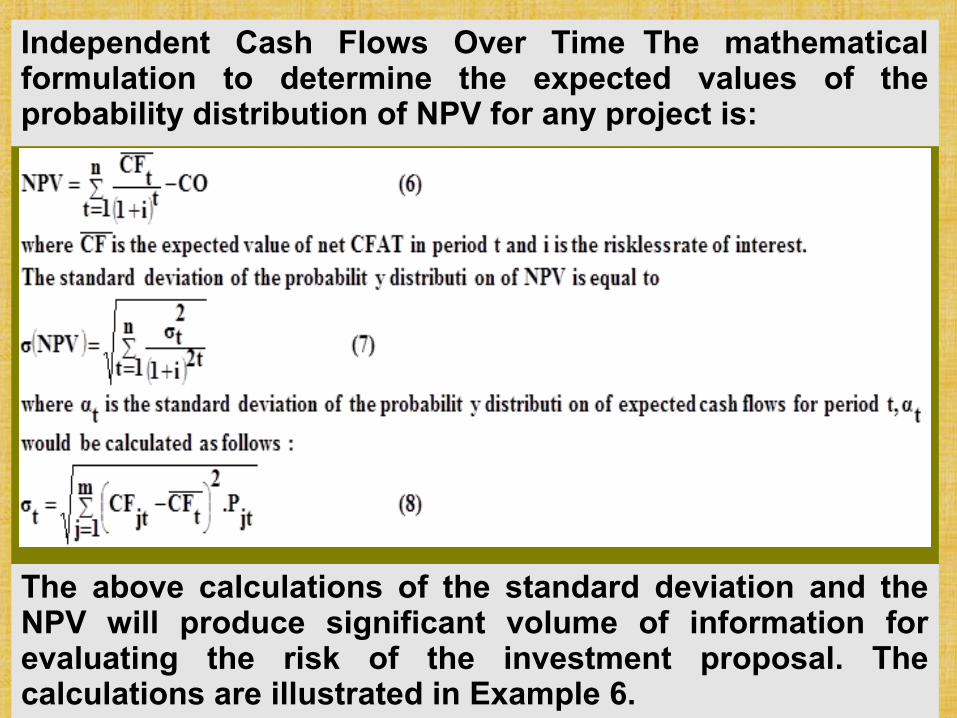

Independent Cash Flows Over Time The mathematical formulation to determine the expected values of the probability distribution of NPV for any project is:

The above calculations of the standard deviation and the NPV will produce significant volume of information for evaluating the risk of the investment proposal. The calculations are illustrated in Example 6.

12 - 151

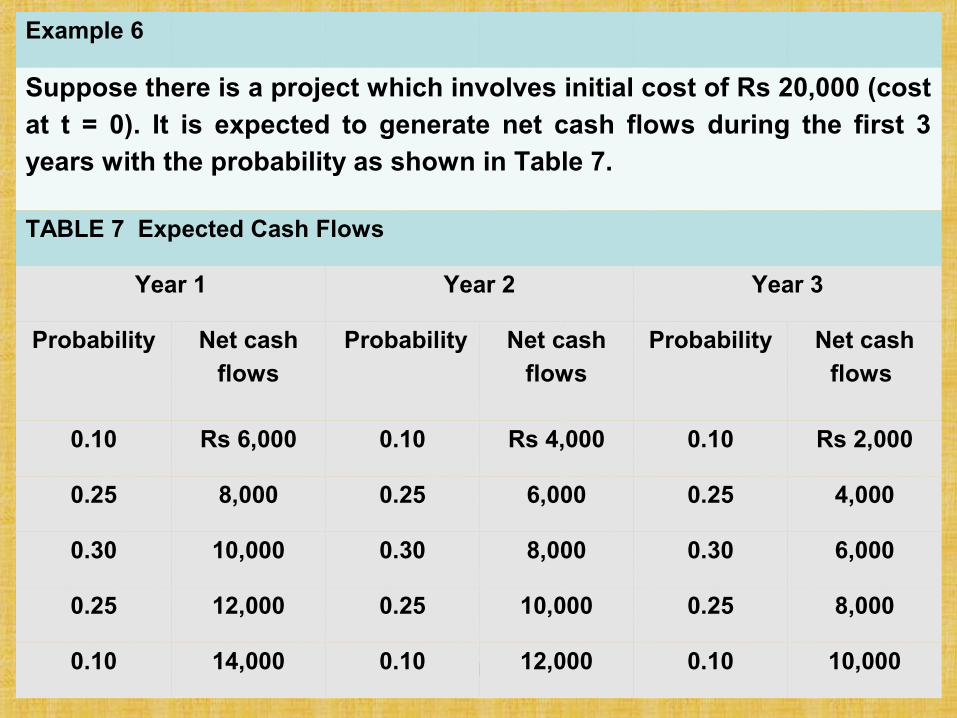

Example 6

Suppose there is a project which involves initial cost of Rs 20,000 (cost at t = 0). It is expected to generate net cash flows during the first 3 years with the probability as shown in Table 7.

TABLE 7 Expected Cash Flows

Year 1 Year 2 Year 3

Probability Net cash

flows

Probability Net cash

flows

Probability Net cash

flows

0.10 Rs 6,000 0.10 Rs 4,000 0.10 Rs 2,000

0.25 8,000 0.25 6,000 0.25 4,000

0.30 10,000 0.30 8,000 0.30 6,000

0.25 12,000 0.25 10,000 0.25 8,000

0.10 14,000 0.10 12,000 0.10 10,000

12 - 152

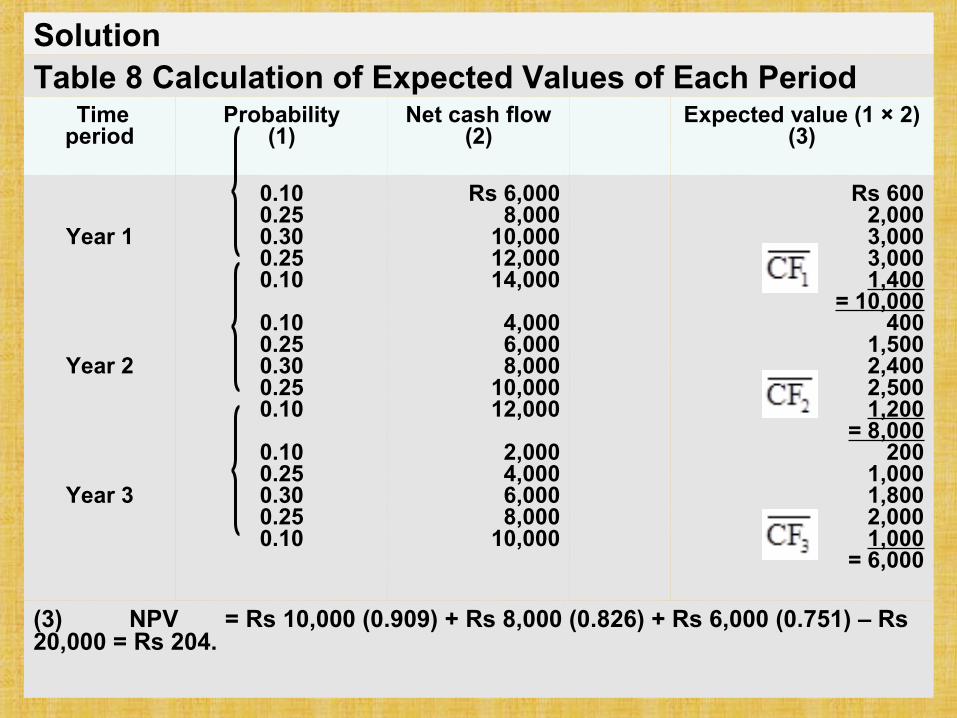

SolutionTable 8 Calculation of Expected Values of Each Period

Time period

Probability(1)

Net cash flow(2)

Expected value (1 × 2)(3)

Year 1

Year 2

Year 3

0.100.250.300.250.10

0.100.250.300.250.10

0.100.250.300.250.10

Rs 6,0008,000

10,00012,00014,000

4,0006,0008,000

10,00012,000

2,0004,0006,0008,000

10,000

Rs 6002,0003,0003,0001,400

= 10,000400

1,5002,4002,5001,200

= 8,000200

1,0001,8002,0001,000

= 6,000

(3) NPV = Rs 10,000 (0.909) + Rs 8,000 (0.826) + Rs 6,000 (0.751) – Rs 20,000 = Rs 204.

12 - 153

Solution

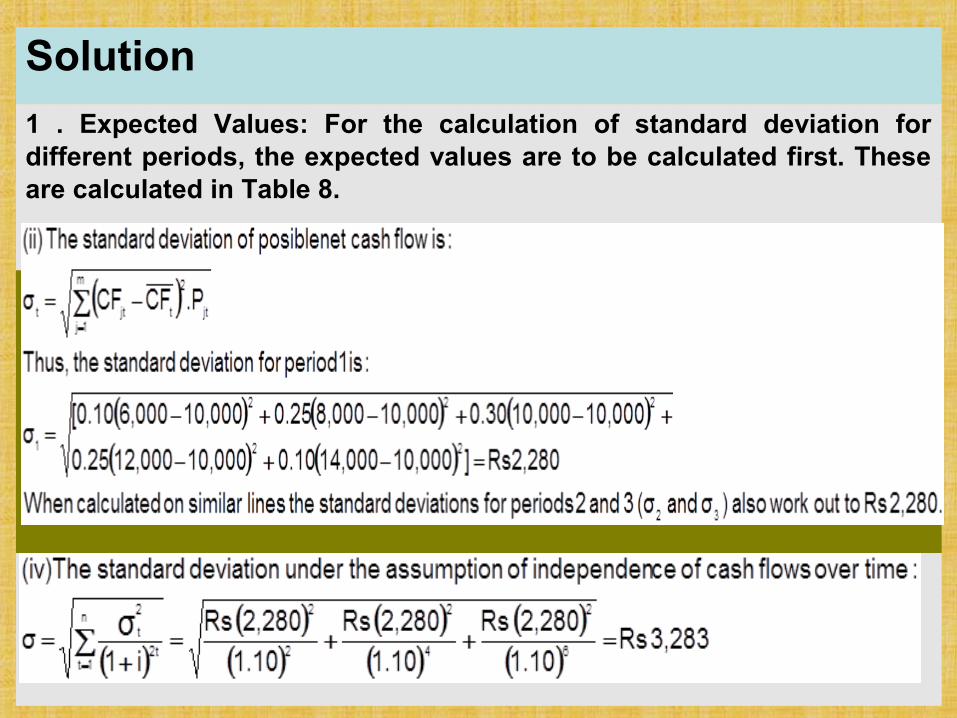

1 . Expected Values: For the calculation of standard deviation for different periods, the expected values are to be calculated first. These are calculated in Table 8.

154

Coefficient of Variation

Relative Measure of Risk

It is defined as the standard deviation of the probability distribution divided by its expected value:

Coefficient of Variation (CV)=

Standard deviation/Expected Value

155

Coefficient of Variation

• The coefficient of variation is a useful measure of risk when we are comparing the projects which have– (i) same standard deviations but different expected

values, or

– (ii) different standard deviations but same expected values, or

– (iii) different standard deviations and different expected values.

156

Scenario Analysis

• One way to examine the risk of investment is to analyse the impact of alternative combinations of variables, called scenarios, on the project’s NPV (or IRR).

• The decision-maker can develop some plausible scenarios for this purpose. For instance, we can consider three scenarios: pessimistic, optimistic and expected.

157 Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Shortcomings

• The model becomes quite complex to use.

• It does not indicate whether or not the project should be accepted.

• Simulation analysis, like sensitivity or scenario analysis, considers the risk of any project in isolation of other projects.

158

Capital Asset Pricing ModelCAPM deals with how the assets or securities should be priced in capital market. CAPM attempts to understand the behavioural aspects of the capital markets. It is a conservative but balanced approach.

It provides theoretical linear relationship between risk return trade-offs of individual securities/assets to market returns.

CAPM relates returns on individual stock and stock market returns over a period of time.

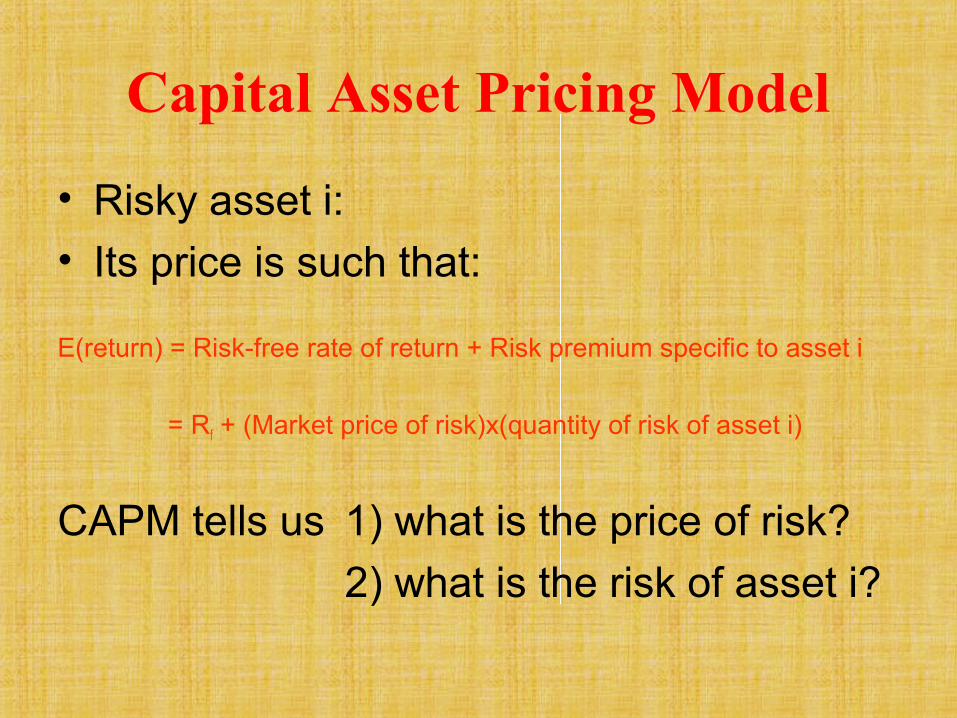

Capital Asset Pricing Model

• Risky asset i:

• Its price is such that:

E(return) = Risk-free rate of return + Risk premium specific to asset i

= Rf + (Market price of risk)x(quantity of risk of asset i)

CAPM tells us 1) what is the price of risk?

2) what is the risk of asset i?

11-160

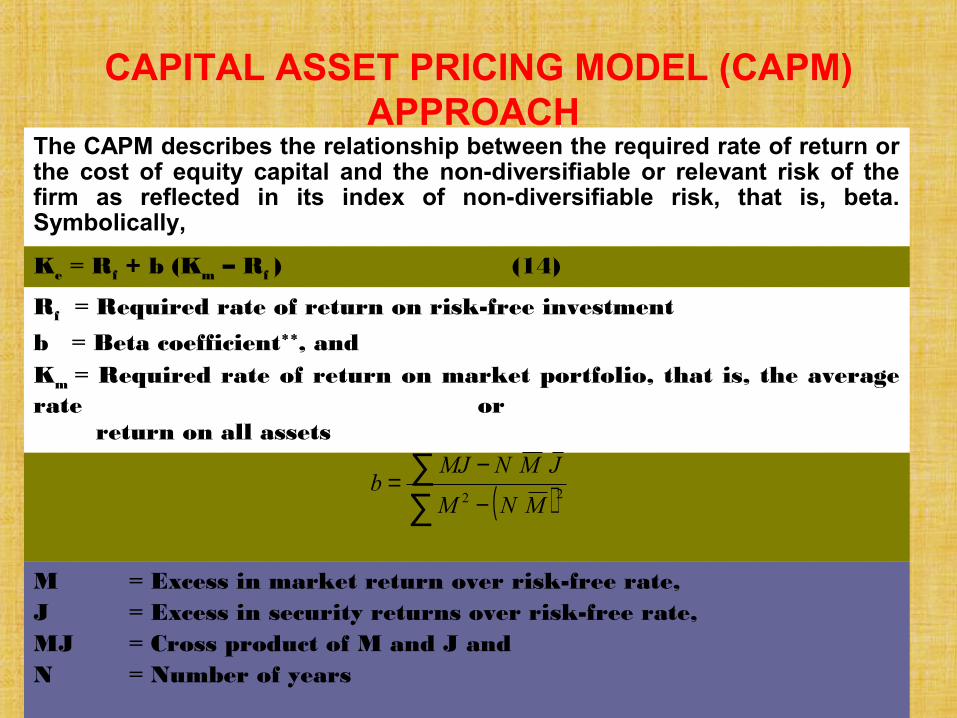

CAPITAL ASSET PRICING MODEL (CAPM) APPROACH

The CAPM describes the relationship between the required rate of return or the cost of equity capital and the non-diversifiable or relevant risk of the firm as reflected in its index of non-diversifiable risk, that is, beta. Symbolically,

Ke = Rf + b (Km – Rf ) (14)

Rf = Required rate of return on risk-free investment

b = Beta coefficient**, andKm = Required rate of return on market portfolio, that is, the average rate or return on all assets

M = Excess in market return over risk-free rate,J = Excess in security returns over risk-free rate,MJ = Cross product of M and J andN = Number of years

( )∑∑

−

−= 22 MNM

JMNMJb

161 Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Introduction• Corporate restructuring includes

mergers and acquisitions (M&As), amalgamation, takeovers, spin-offs, leveraged buy-outs, buyback of shares, capital reorganisation etc.

• M&As are the most popular means of corporate restructuring or business combinations.

Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Motives and Benefits of Mergers and Acquisitions

Utilise under-utilised resources–human and physical and managerial skills.

Displace existing management.Circumvent government regulations.Reap speculative gains attendant upon new

security issue or change in P/E ratio.Create an image of aggressiveness and

strategic opportunism, empire building and to amass vast economic powers of the company.

163Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Benefits of Mergers and Acquisitions

The most common advantages of M&A are:Accelerated GrowthEnhanced Profitability

Economies of scale Operating economies Synergy

Diversification of Risk

164Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Benefits of Mergers and Acquisitions

Reduction in Tax Liability Financial Benefits

Financing constraint Surplus cash Debt capacity Financing cost

Increased Market Power

165Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Costs of Mergers and Acquisitions External growth could be expensive if the

company pays an excessive price for merger. Price may be carefully determined and negotiated so that merger enhances the value of shareholders.

166

29-166

A Cost to Stockholders from Reduction in Risk

In a firm with debt, the gains are likely to be shared by both bondholders, and stock holders. The benefit gained by bond holders are on the expense of stock holders.

The gains to the creditors are at the expense of the shareholders if the total value of the firm does not change.

An acquisition can create an appearance of earnings growth, which may fool investors into thinking that the firm is worth than it really is.

167Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

29-167

A Cost to Stockholders from Reduction in Risk

The Base Case If two all-equity firms merge, there is no transfer of

synergies to bondholders, but if…

One Firm has Debt The value of the levered shareholder’s call option

falls.

How Can Shareholders Reduce their Losses from the Coinsurance Effect? Retire debt pre-merger.

168Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Benefits of Mergers and AcquisitionsThe most common advantages of M&A are:

Accelerated Growth

A company can achieve its growth objective by: Expanding its existing markets Entering into new markets

Mergers results into accelerated growth Enhanced Profitability

Combination of two or more companies may result in more than the average profitability due to cost reduction and efficient utilization of resources. This may happen because of the following reasons:

Economies of scale Operating economies Synergy

169Financial Management, Ninth Edition © I M PandeyVikas Publishing House Pvt. Ltd.

Benefits of Mergers and Acquisitions

Economies of scaleEconomics of scale arises when increase in the volume of production

leads to the decrease in cost of production per unit. Mergers may help to expand volume of production without a corresponding increase in fixed cost. It also helps in

Optimum utilization of management resources and systems and planning

Budgeting Reporting and control

Operating economies A combine firm may avoid or reduce overlapping functions and

facilities