strategic implication of a segmentation and positioning

TRANSCRIPT

c'r,21G11C ilffiffLi11D CAITHCON ©IF A

EIGM-Emmrsaal AN 23EMONIEG MODIL W© ULM EDMITE MICCA\N CAD CW2MT KEE:11G tl\MA rflr GO

CC CCCD:M OundwilnaulfirnEolotz= G la I

'aunclliaff2 Ke. gi'OD22,60

CONTENTS TOPIC PAGE

CHAPTER 1 : AN INTRODUCTION 1 - 3

1.1 Marketing Approaches Over Time 3 - 7

1.2 Statement of the Problem 7 - 8

1.3 Objectives of the Study 8 - 9

1.4 Methodology 9 - 10

1.5 Demarcation of the Study 10

1.6 Chapter Outline 10 - 11

CHAPTER 2 : MARKET SEGMENTATION, TARGETING AND 12 POSITIONING AS RELATED TO THE SOUTH AFRICAN GOLD MINING INDUSTRY

2.1 How gold Mines Purchase Explosives 13 -16

2.2 The Nature of Explosives Purchasing 16 - 17

2.2.1 Understanding Individual Behaviour 17 - 20

f.

2.2.2 Motivating Behaviour 20 - 22

2.2.3 The Buyer Decision Making Process 22 - 25

2.3 Market Segmentation 25 - 26

2.3.1 Market Segmentation Approaches Reviewed 26 - 29

2.3.2 Difficulties in Segmenting the Narrow Reef Explosives Market 29 - 31

2.4 A Segmentation Approach for this Study 31 - 36

2.5 Targeting Market Sectors 36 - 38

2.6 Product Positioning 38 - 41

TOPIC PAGE

CHAPTER 3 : DEVELOPMENT OF A SEGMENTATION MODEL 42

3.1 First Step - Define the Business Environment 42

3.1.1 Who is the Customer 43 - 47

3.1.2 Where are the Mines Located 47 - 48

3.1.3 What product is going Where? 48 - 49

3.1.4 What Market Needs Exit? 49 - 53

3.1.5 How can the Gold Explosives Market be Quantified? 53 - 56

3.1.6 Who Competes for the Market? 56 - 57

3.1.7 What Physical and Cultural Environment Exist in Gold Mines? 57 - 58

3.2 Second Step - Understanding Buyer Behaviour 58 - 63

3.3 Third Step - Identify the Base Variables and Segment the Market 63

3.3.1 Identification of the Base Variables 63 - 66

3.3.2 Segmenting the Market r.

66 - 69

3.4 Final Step - Verify the Result 69 - 70

CHAPTER 4 : TARGETING, POSITIONING AND STRATEGIC IMPLICATION 71

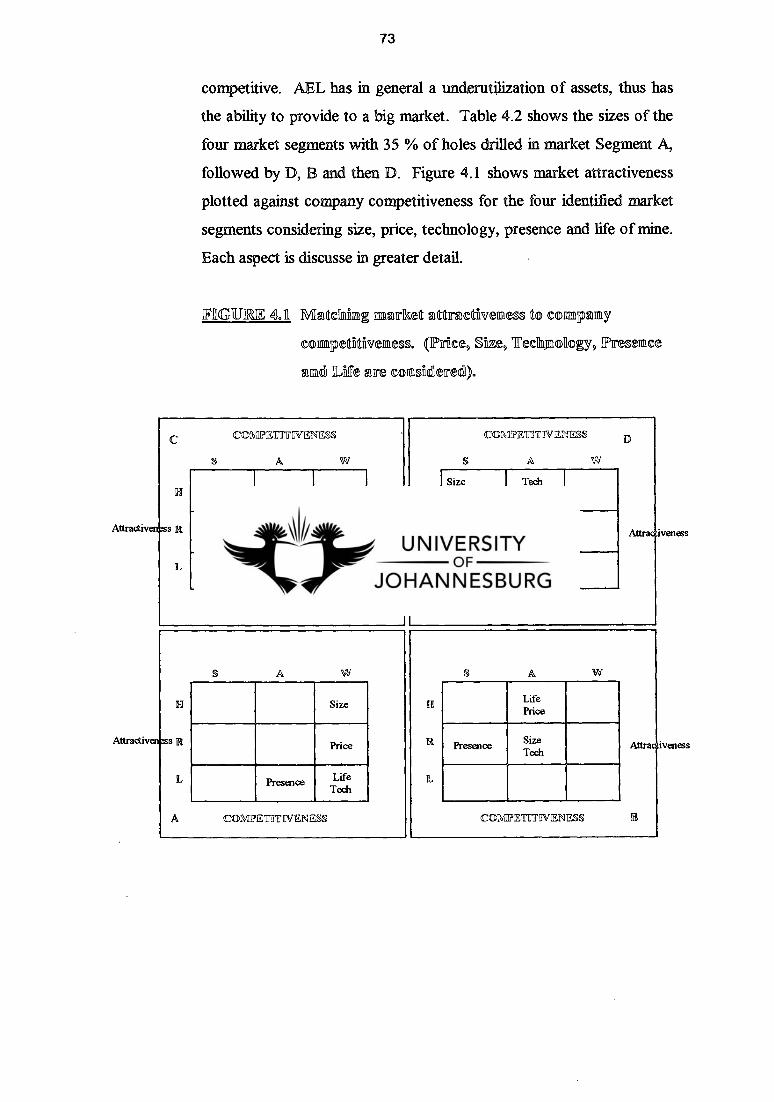

4.1 Business Strengths and Market Attractiveness in Relation to Market Segments 71 - 72

4.1.1 Market Attractiveness Versus the Market Position 72 - 76

4.1.2 Economical/Technological Needs Versus Capability 76

4.1.3 Competitive Position Versus Market Interaction 76 - 77

4.1.4 Market Targeting 77 - 82

TOPIC

4.2 Product and Service Positioning

4.2.1 Product Positioning in Market Sector A

4.2.2 Product Positioning in Market Sector B

4.2.3 Product Positioning in Market Sector C

4.2.4 Product Positioning in Market Sector D

PAGE

82 - 84

84 - 85

85 - 87

87 - 88

88 - 90

4.3 A Corporate Image 90

CHAPTER 5 : CONCLUSION AND RECOMMENDATIONS 91

5.1 A Summary 91

5.1.1 Study Objectives Reviewed 91 - 92

5.1.2 The Segmentation Model, Targeting and Positioning 92 - 95

5.2 Conclusion 95 - 96

5.3 Recommendations 96 - 97

BIOGRAPHY 98 - 99

FIGURES

Figure 2.1 : The Gold Mine Supply 14

Figure 2.2 : Individual-Behavioural Framework (Gibson et al, 1994: 99) 17

Figure 2.3 : A graphic comparison of the Maslow and Hertzberg motivational theories 21

Figure 2.4 : The stages of decision making ( Bateman and Zeithaml, 1990: 90) 24

Figure 2.9 :

Figure 3.1 :

Figure 3.2 :

Figure 3.3 :

Figure 4.1 :

Figure 4.2 :

Figure 4.3 :

Figure 4.4 :

Figure 4.5 :

Figure 4.6 :

Figure 4.7 :

PAGE

Major potential bases for segmentation according to the nested approach (Bingham and Raffiled, 1990: 202) 27

Dayle and Saunders industrial market segmentation model focusing on product benefits (Eckles, 1990 : 126) 28

The variable filtering approach to market segmentation 32

Implication of alternative positions within the Market Attractiveness/ Competitive Position Matrix (Walker et al, 1992: 197) 37

Strategic competitive positions for the U.S. Heavy-Duty Truck Market as measured by Return on Investment (Walker et al., 1992,305)

40

Geographic location of the gold mines of South Africa 48

Effect of cost and revenue for low and high cost producers 53

The gold explosives market as defined by operational excellence and affordability 67

Matching market attractiveness to company competitiveness (Size, Price, Technology, Presence and Life are considered) 73

The strategic implication cells of the Walker matrix (Figure 2.8) to be consulted for guidance in Market Segment A 78

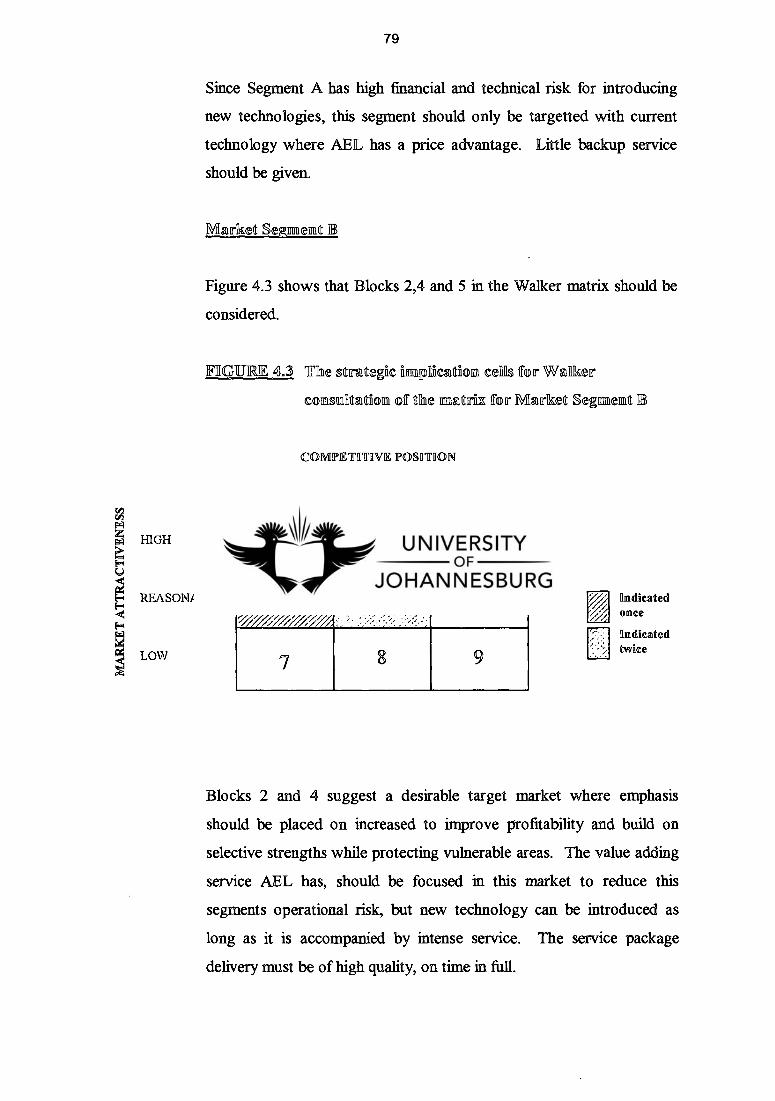

The strategic implication cells for Walker consultation of the matrix for Market Segment B 79

The strategic implication cells for Walker consultation of the matrix for Market Segment C 80

The strategic implication cells for Walker consultation of the matrix for Market Segment D 81

Product Position Space matrix with product positions in Market Sector A 85

Product Position Space matrix with product positions in Market Sector B 86

TOPIC

Figure 2.5 :

Figure 2.6 :

Figure 2.7 :

Figure 2.8 :

TOPIC PAGE

Figure 4.8 : Product Position Space matrix with relative product positions in • Market Sector C

88

Figure 4.9 : Product Position Space matrix with relative product positions in Market Sector D

89

Figure 5.1 : The Market Segmentation Model explaining Explosives buyer behaviour in the Gold Narrow Reef Market

93

TABLES

Table 1 : Mining Houses and Associated Mines 2

Table 2.1 : Pros and Cons of using groups to make decisions (Bateman and Zeithaml, 1993 : 97) 25

Table 2.2 : Motivational Score Card 34

Table 3.1: Annual Number of holes drilled which serves as quantification for the explosives market 55

Table 3.2 : Relative Market Share of Explosives Companies in South Africa 56

Table 3.3 : Operational and Performance variables describing the Gold Mines of South Africa. 59

Table 3.4 : Relative importance of filters with regard to motivation of buying behaviour 64

Table 4.1 : Market Attractiveness and Business Strengths to be considered in targeting a market segment 72

Table 4.2 : The size of Segments A,B,C and D measured in million holes drilled annually, with the life of mine also indicated 74

Table 4.3 : The major product groups offered in the Gold Narrow Reef Market 83

Table 5.1 : Attractiveness and Competitive factors considered in market targeting 94

APPENDIX 1: SENIOR MINING PEOPLE PLOTTING THEIR MINES IN THE MARKET FIELD

CHAPTER 1

AN INTRODUCTION

INTRODUCTION

When the first 51 gold diggers settled in 1885 at Kromdraai west of where

Johannesburg would develop in later years, the foundation was set for a synergistic

growth between the narrow reef gold industry and an industrial complex supplying the

gold mines of equipment and commodities necessary to unlock the riches of the earth.

Although the South African industrial development largely resulted from the mining

industry, the latter was saved many times by the innovativeness and ingenuity of the

mining supplier industry (Anon, 1986:5). For example, improved hoist rope

technologies helped to reach the deeper lying reefs, sequential firing facilitated higher

mining rates and the cyanide beneficiation process allowed gold recovery to continue

when the state of the art technologies of the time failed to do so.

Today the South African Gold Mining Industry is in a mature stage, but still produces

almost 500 tons of gold annually, about 40 % of annual world production. The gold is

mined from deep narrow reefs, extending spatially over large areas and dipping

between 10° and 30°. The rock sufrounding the gold bearing reefs is typically hard but

strong allowing mining at great depths. However, the high quartz content of the rock

makes it highly abrasive on steel mining tools, one of the major factors inhibiting full

mechanization of the mining process. Mining is still conducted by labour intensive drill

and blast techniques. The pneumatic rock drills are hand held, although air legs are

assisting in forward pressure. Explosives are inserted by hand or pneumatic means.

Broken rock is removed by electric driven rope scraper winches and trammed by rail to

vertical ore-pass systems which collects all broken rock at shaft bottom to be hoisted

to surface.

There are currently 33 large operating gold mines owned by or associated with six

mining houses. Roughly one third of these mines are old and marginal with large

infrastructures to be maintained resulting in mining operations being far from the

2

shafts. The remaining mines can be divided into two groups; those that are established

with a 10 to 25 year life of mine left, or those established with new mines to be

developed from current mine infrastructure. These mines have life of mine

expectancies of over 25 years. Table I provides a summary of the mines with their life

expectancies (Von Below, 1996:17).

TABLE I : Mining Houses and Associated Mines

MINING HOUSE

••:mi[xs::::: - I.i.opyriort,::::: ANNUAL ootp: - - - • • : ::PROD(TONS): •

LIFE OF ::: - 'MINE

Amgold (Anglo Elandsrand Carltonville 15,4 20+ American) Freegold Welkom 92,7 20

Vaal Reefs Orkney 66,2 30+ Western Deep Levels Carltonville 35,8 30

Anglovaal Hartebeestfontein Stilfontein 25,2 10 Loraine Allanridge 6;6 5+ E T Cons Barberton 3,2 11

Goldfields Deelkraal Carltonville 6,6 19 Drie Cons Carltonville 50,6 25+ Kloof Randfontein 43,5 24

JCI HJ Joel Welkom 4,1 16+ Randfontein Randfontein 23,0 25+ Western Areas Randfontein 17,3 65+

Gengold Beatrix ..• Welkom 14,6 20 Kinross c' Evander 8,5 16 Leslie Evander 2,4 6 St Helena Welkom 5,3 7 Winkelhaak Evander 8,8 10 Fairview Barberton 1.5 -

Randgold Blyvooruitzicht Carltonville 4,0 11 Buffelsfontein Stilfontein 8,9 17 Doornfontein Carltonville 3,7 - Durban Deep Roodepoort 2,0 24 ERPM Germiston 8,2 6 Grootvlei Boksburg 2; 5 16 Harmony Virginia 20,1 9 Unisel Welkom 4,2 22 West Wits Randfontein 3,7 6 Stilfontein Stilfontein 0,6 -

Other Benoni Benoni 2,0 19 Cons Modder Boksburg 1,5 12 Knights Springs 1,3 25 Lindum Springs 1,7 7

Source : Von Below : 1996, 17

3

Three major explosives companies supply explosives products to the narrow reef gold

mining market, but other local and foreign suppliers are distributing explosives

products in association with these major suppliers or try to enter the market

independently. The major suppliers are AECI Explosives Limited (AEL), Sasol Mining

Explosives (SMX) and Bulk Mining Explosives (BME). SMX and BME are wholly

owned subsideries of Sakil Limited and Omnia Limited respectively. AEL, however, is

a joint venture between Imperial Chemical Industries Plc and AECI Limited.

This study is an attempt to segment the gold mining industry in relation to explosives

requirements in order for AEL to target and position itself successfully in a market

they still dominate but has been losing market share over the last ten years.

1.1 MARKETING APPROACHES OVER TIME

Until recently, AEL was effectively the only supplier of explosives to the South

African Gold Mining Industry and therefore monopolistic in nature. Right from

the origins of the gold industry, the old Transvaal Government discouraged

competition to maintain some control over the mining activities on the

Witwatersrand. The mining rush attracted foreigners in such numbers that it

became a threat to the Old Transvaal Boer Republic. Only one dynamite

concession was granted to Edouard Lippert, a cousin of Alfred Beit (Anon,

1986:12). Explosives manufacturing started at Modderfontein close to

Johannesburg and operated effectively as a monopoly. In reaction, Cecil John

Rhodes started an explosives company in Somerset West near Cape Town. In

later years these two companies amalgamated to form the African Explosives

and Chemical Industries. This amalgamation maintained AECI as a monopoly,

a situation that persisted until Sasol Mining Explosives was formed in the early-

eighties.

As the only supplier of Explosives products in South Africa, AECI had an

explosives supply agreement with the Chamber of Mines. All supply

requirements were expected to be met. In the nineteen eighties competition in

5

❑ Differentiated Market Strategy

(Mid-Eighties to early Nineties)

The mines became less tolerant to companies such as AECI which was

inflexible in their product offering and which harboured inefficiencies due to the

monopolistic nature of their business. At the time Sasol Industries became

interested in the fertilizer and explosives industries in order to develop a market

for the large volumes of ammonia produced as a by-product of the synthetic

fuel process. Sasol Mining Explosives started in 1985 and soon AECI started

losing market share, especially in mines associated with the Gold Fields mining

group. Sasol Mining Explosives entered the market with a low pricing policy.

AECI reacted by differentiation of its explosives products and marketing mix

and succeeded in obtaining a premium. The differentiation was based on the

nitro glycerine range of products which were extremely popular in the narrow

reef market due to its strength and forgiving nature in conditions of low

operational discipline. AECI was still the only supplier of blasting accessories,

that is detonators, fuse and igniter cord and was the only supplier which could

offer a full blasting system, that is both explosives and initiating systems.

Differentiation from its competitors was also achieved through high service

levels which included a welt trained and competent sales force. Better technical

advice was offered, better blast design using software developed in conjunction

with ICI was included in the service package. Central bargaining with the

Chamber of Mines was discontinued by the mines in 1985, which resulted in

centralised mining house price negotiations where a pricing structure designed

for each mining house and based on different discounts from the National Price

List was annually re-negotiated.

Market sectors were roughly arranged according to mining house with the

belief that some mining houses were more interested in technical and other

services while others were only interested in low priced explosives

commodities. In practice, however, high service levels were given to all mines

at all times. In 1993, ICI obtained a majority share of the explosives interest of

6

AECI, and the formation of a joint venture between AECI and ICI was formed

and called AECI Explosives Limited. AECI Explosives Limited stopped

producing water based explosives which was not ICI technology, but these

prOducts are still toll manufactured by a new player, Dantex Explosives on

behalf of AEL. Meanwhile, in first world countries, ICI discontinued the

manufacture of nitro glycerine based explosives, mainly due to the

environmental hazards of the manufacturing process and the physiologic effect

these explosives have on mine workers.

Dispite these changes to its micro environment, AEL still operated as if it were

all things to all customers. In addition to the water gel and nitro glycerine

explosives, water based emulsion explosives, which is an ICI technology, was

manufactured. In 1994, a huge accidental explosion in the nitro glycerine

manufacturing plant occurred, 11 AEL employees were killed. It was decided

to discontinue the manufacture of nitro glycerine explosives and to expand the

emulsion technology to replace it.

Competitors reacted to the way AEL differentiated on the basis of service

levels. They started to develop and grow their technical competence. AEL

attempted to reduce overl4ad cost, and reduced the sales force in 1995. During

1996, little difference could be detected between AEL and SMX technical

service. BME decided in 1995 to enter the underground explosives market and

erected a manufacturing plant near Fochville in the West Rand region and are

now trying to enter the market by undercutting both AEL and SMX on price.

AEL, dispite the intense competition, still succeeded in maintaining a high

market share in explosives. AEL also acts as the price setter, where SMX and

BME adjust prices accordingly. However, the intense price struggle lowered

margins of packaged explosives products to such an extent that a loss is

currently made on these products.

AEL still dominates the initiating system market, but companies specializing in

initiating systems from the international arena entered the market recently in

7

association with local competitors. For example, Ensign Bickford entered the

market in association with SMX and Famesa in association with BME.

The basis on which AEL differentiated itself has thus been eroded away by

recent events in the market place and it became clear that a more concentrated

market strategy is required to maintain market share and retain and improve

profitability.

❑ A More Concentrated Marketing Strategy Required

(Early Nineties to Current)

With the competitive edge being lost in the market to competitors who are

copying the service and marketing approach AEL is following, it became

necessary to readjust the strategy. It is too expensive to try and service all

market segments, since some market sectors might exist where these activities

only adds cost without earning a premium. Currently, AEL realises changes are

required and is looking for a credible segmentation model which will allow

clear and decisive focus in the market. The objective will be to stabilise market

share in the face of increased competition by serving selected markets best

suited to the company's infrastructure, technology and culture. It is important

to maintain a large market share, as economy of scale ensures price

competitiveness. Large investment will also be decided on the basis of the

segmentation. New technologies currently in an introductory phase, can

potentially replace the older technologies if clear markets exist. To summarise,

AEL is currently in stage of creative chaos, where it is clear change is required,

but it is not clear what the direction should be.

1.2. STATEMENT OF THE PROBLEM

Many variables exist that influence buyer behaviour in the narrow reef gold

mining market. Since some variables are real but subjective in nature, such as

the opinion and charisma of mine managers or influential individuals, it is

difficult to quantify and analyse them. The question is ? Which variables,

8

quantifiable or not, are more dominant in shaping buyer behaviour and how

should they be prioritised?

What is needed is a logical segmentation model which reflects true buyer

behaviour in order to shape future strategies in AEL so that the overall

company objectives can be met. Each segment should then be analysed and

considered regarding attractiveness in satisfying needs and the ability to add

value both to the customer and to AEL. It is also required to target market

segments and develop a marketing mix for them so that AEL is correctly

positioned to retain the markets it choose to compete in.

The problem is the failure to identify market areas of similar response

which are relatively stable and can be used to select areas where maximum

value can be added to the customer and to the company and can be used to

shape and define future direction.

1.3. OBJECTIVES OF THE STUDY

The following objectives have been set for this study: r.

- The establishment of a market segmentation model which will identify and

explain the basis of similarities and differences in buyer behaviour groups which

is sufficiently large and stable in order to focus future strategies.

- The interpretation of the segmentation model in the light of the strengths,

weaknesses, opportunities and threats of the company in order to target

markets best suited to the potential of the company.

- Development of strategies and positioning in the target markets to strengthen

the chance of success.

9

1.4 METHODOLOGY

Market segmentation can be either pre-determined or market-defined (Struhl,

1992:10). Pre-determined or a priori segmentation involves the collection of

available information of a market, selecting groups from a population and

finding-if they are segments. Market-defined or post hoc segmentation is more

objective and first consult the market and then analyse answers and survey

questions to predict marketplace responses.

The universe investigated here consists only of 33 user entities (the mines),

represented by 6 purchasing organizations (mining houses). Although hundreds

of people influence the decision making process, the physical realities of the

user environment, such as deep or shallow mines, low grade or high grade,

must logically be assumed the dominant factors that are driving human decision

making. A pre-determined process will therefore be followed. As much

information regarding operational variables, organizational demographics,

situational factors and purchasing approaches will be collected. The variables

will be prioritised and relationships will be sought for between the top variables

to be captured in a simple behavioural segmentation model. Prioritization will r.

be achieved by adjustment of McDonald and Dunbars's interrogative

segmentation technique. They developed a market segmention approach where

the current flow of product is plotted followed by interrogatory questions to

explain current product flow such as; Who buys? What is bought? Where?,

When? and How it is bought? (McDonald and Dunbar, 1995:1).

To ensure a reasonable coverage of possible variables that do influence buyer

decision making, Bonoma and Shapiro's nested approach will be followed for

identification of variables and then subjected to the McDonald and Dunbar

technique (Shapiro and Sviokla. 1992:72).

It is expected that two or three base variables will be identified, or variables so

dominant in influence that they can form the basis of the segmentation. Other

10

variable will be used as descriptor variables which provides depth of

understanding of a certain segment.

An attempt to varify the accuracy of the pre-determined segmentation exercise

will be made by interviewing consulting mining engineers and testing their

views on what is required from suppliers.

Perceptual mapping will be used to illustrate two-dimensionally the basis of

positioning, that can be technology, price, quality, distribution or service.

Adjustment in Company strategies will be recomended.

1.5 DEMARCATION OF THE STUDY

The study will focus on segmentation of the narrow reef gold mining

environment. Although the segmentation model has a wider application for all

suppliers to the gold mining industry, the study will focus on the supply of

explosives and initiating systems. Although hundreds of products are offered to

the gold mines, only the broad product groups will be considered, such as fuse

and ignitor cord, shocktube products etc.

The investigation will also be limited to South African gold mines, while a small

number of key consulting engineers and mine managers will be interviewed to

help verify the model.

1.6 CHAPTER OUTLINE

This study will consist of five chapters. Chapter 1 do constitute the scope and

methods of the study and contain an introduction, an explanation of marketing

approaches over time, a problem statement, objectives and a demarcation of the

study. Chapter 2 explore literature in search of techniques to assist in

segmenting targetting and positioning of business to business markets. The

theory is reviewed briefly and conceptually applied in order to test applicability.

11

The chapter concludes with a proposed methodology. Chapter 3 gives the

application of theory, namely the development of a segmentation model and

validation of the accuracy of the model, in other words, how well does the

segmentation model represent real life buyer behaviour. Validation is obtained

by a set of interviews, which also will serve as the foundation of decision

making to position AECI Explosives Limited in such a way that their objectives

can be met. In Chapter 4, sector targeting and positioning are considered. The

chapter also explore the strategic implications of the proposed positioning.

Finally, Chapter 5 summarise the major findings and recommendations as to

possible changes in strategic position of AECI Explosives Limited.

12

CHAPTER 2

MARKET SEGMENTATION, TARGETING AND POSITIONING

AS RELATED TO THE SOUTH AFRICAN GOLD MINING INDUSTRY.

All markets•consist of buyers, and buyers differ in their wants, needs and attitudes.

Each buyer is potentially a separate market. For a whole market, however, save

geographic, demographic, psychographic or other characteristics are shared by more

than one customer and as a result will influence their buying behaviour in a similar way

(Kotler and Amstrong, 1994, 274). The secret is to identify groups that might respond

similarly to communication, product positioning and product configurations (Struhl,

1992, 2). If deep and shallow gold mines, for example, use the same explosives

products, a market structure rather than a segment has been identified. A segment is

defined by an unit of similar behaviour when confronted with the same market stimuli.

Once the behavioural or "segments" has been identified, the company must determine

which market segments they will focus their efforts and why these segments is

attractive to them. Once the targeting decision has been made, the product or service

perception in the customer mind must be designed so that he will find the product f.

desirable.

Accurate product positioning provides a enduring advantage over current and future

competitors (Orville et el., 1992, 174).

This chapter will explain as a starting point, the buying process that gold mines follow.

Once the buying process is understood, buyer behaviour can be investigated which

forms the basis of market segmentation. By briefly reviewing different segmentation

technique for this study will be developed. The market attractiveness factors that will

identify target segments, will be reviewed, followed by a short description how

physical and perceptual product positioning will be achieved.

13

2.1 HOW GOLD MINES PURCHASE EXPLOSIVES

The South African Gold Mining Industry developed from large mining finance

houses, formed by pioneers such as Cecil Rhodes, Barney Benarto, Alfred Beit,

Herman Eckstein and Joseph Robinson. Each financing house, or Mining

House, generally fully owns prospecting companies as subsidiaries. If a gold

prospect has potential, a mining company is created, initially fully owned by the

Mining House. As confidence grows, further capital is raised by rights issues.

The mining house retains a dominant share of the mine, securing a management

contract. These contracts are traditionally expensive, but maintains head office

expertise in the following fields: geology, mining, finance, training,

administration and human resource development. It also provides funding for

further expansion within the industry.

These management contracts were recently under pressure with the inflow of

foreign capital. Randgold reduced head office personnel to 60 people, while

Gengold also restructured and sold off their management contracts. All six

mining houses, however, make use of central bargaining for their mining

companies. r.

An existing trend is to decentralise contract administration and results in only

20 % of contracts administrated by head office for central bargaining [80 % of

the value]; the rest are negotiated by the individual mining companies

themselves. Explosives fall in the former category, but lower levels of

management are being enabled to increase their influence over the purchasing

decisions.

Figure 2.1 explains diagramatically the recurring buying process.

DECIDERS Mine Management is Informed - Evaluates agains criteria

BUYING ROLES Buying Process ricsigragadier

Individual Suppliers Applies for an

Price Increase

INFLUENCER Volume Price (Preceeding) X (New)

Central Purchasing Unit (Mining House)

Calculate effect of increase to Mines. Evaluate against Criteria Alternative supplier ratio's or product mixes are considered

INFLUENCER

DECIDER o o 5 Ot)

The Mine

BUYERS

Consults on-mines purchasers + stores

INFLUENCERS Consult middle management

Influenced and USERS presurised by

users

FIGURE 2.1 The Gold Milne Sappily

14

Supply on

Orders Received from on-mine

purchasing unit

Somme e Anon o AEL Internal Hies, 1996

15

The process can be broken down into the following steps: .

Step 1: All mines associated to a mining house combine their needs and task the

central purchasing unit to negotiate with the supplier on their behalf. The supplier uses

the previous year's volumes as a basis, multiply it by both the old and new unit prices

and calculate the increases. Unit prices are calculated from applying a discount to the

National List Price of the product. The proposal (almost a tender) is forwarded to the

central purchasing unit of the particular mining house. The supplier influences the

buying decision in various ways. First, the account managers, blasting engineers and

technical representatives ensure during the proceeding year that the explosives are used

correctly so that maximum value is obtained from the supply contract. This is achieved

through technical service, training and regular consulting. Secondly a promotions

policy that includes sports days, advertisements, tokens etc. maintains maximum

awareness amongst customers.

Step 2: The Central Purchasing Department takes the tender prices and after analysis

advises the individual mines how they will be affected and what could be done to

optimise their situation. For example, product mix or suppliers mix can be changed.

The supplier credibility and reliability of supply are examples of aspects the mine s,

management is advised on by central purchasing before a decision is made. The final

supplier mix is decided by the central purchasing department and acts therefore as both

an influencing and a deciding body. Their purchasing units mission is to obtain the

required goals and services at the required quality, specification and best price and so

contributes to the groups cost competitiveness (Anon, 1996,1)

Step 3: Mine Management considers the supply proposal and consults the on-mine

purchasing unit (the buyers), middle management and the users. Direct contact with

the supplier sales force provides them with further information. The actual users of the

product recently started playing a much more direct role through workshop forums in

influencing the buying decision. Safety implications and product stewardship plays as a

result, a much more important role in buyer decision making.

16

Step 4: After evaluating the value a supplier can add to the mines operation,

essentially balancing price benefits or needs satisfaction, the mine management makes a

decision. The buying decision is communicated to the central purchasing department.

Mine management, which can be the general manager, mine- or production manager

or a committee, is therefore the most powerful deciding centre.

Step 5: If the decision is not to buy, the central purchasing unit re-negotiate the terms

with the supplier. On rare occasions, if agreement cannot be reached, no supply

contract is agreed on. Mines can then still buy directly from the supplier, but usually at

National List Price. Alternatively, arbitration can be an option.

Step 6: If agreement is reached, a supply contract is compiled and signed by

representatives of both parties. The process repeats itself a year later, when the

supplier again gives notice for the price adjustment for the following yera.

2.2 THE NATURE OF EXPLOSIVES PURCHASING

To understand the nature of explosive purchase decision making, individual and

group behaviour needs to be understood .

The process is essentially a decision-making process through communication

between individuals and groups. The supplier tender is compiled by a work

group and communicated by a negotiation team (one or more individuals). The

evaluation and decision making is done on a consultative basis between a

management group and a central purchasing group. Individual charisma and

personality plays an important part in the decision making process. Groups

are made up of individuals and can be dominated by individuals. Groups,

formal or informal, acts as a powerful equaliser and a mechanism where

balanced views are generated in order to make decisions and satisfy needs.

(Gibson et al, 1994:311)

17

Buying behaviour is shaped by individual and group behaviour. Behavioural

patterns form the basis of segmentation. The logical starting point to

understand buyer behaviour is to study the psychological and motivational

factors of individuals and groups and how decision making for buying of

explosives is affected by these variables.

2.2.1 Illunders

raclignEllnndividuai Behaviour t ,

Various variables influence individual behaviour. Figure 2.2 is an useful

framework constructed by Gibson et el. grouping variables that

influence behaviour in two groups, environmental and individual.

MIGURIE 2.2 laglifiviidund- eheviiounall 1Frramewout

The FAIN 11'011111CM rile Indi% idu al BehaN ior. Outcomes

q \ H!!!!.. , .wd ,,L,11 , 1'r. ■ 111.111- , ,,, 1\ in: Performance - In' , dt.-.11.In Hui) II\ 1),,,i,.,21,,11n,1 I Junking plocc, , - Lang-term - ( )! : Ain ;111-culi ,tml..tur.. ....n.olirilit N ( I t11 muntcation - ShOrt-terM

l'(' I k. ■ '...• tnd , 11H. L2t, cption - I ,ilknIF Personal developmen - t ,...,,,icl.111 ,, , \ ilitli,k, - L. 1 q,n in,..2. Relations with othci-s - Rcv,..mid , ,in„ -.iiktion, - R._-,..lit Lt..---

1 2.i(11111.,2 ..,1p,IC ON

\..,-..:

c )b'r LA k anon!,

\ lo \ ,...mcnt Satisfaction

- I .,1/4.4 , 11t1MIL. ,

--.“,r1 \\()14,.

ROL L .

`-..•.

- I- in c; 1 k I - \ p,._ pc.r..k:

- 1_,Asure anti hoMlles

Source a Gibson et el e 1994, 99

18

How can these variables influence the behaviour of individuals on a

mine or a mining house purchasing department when buying explosives?

A few variables from Figure 2.2 are elaborated upon to illustrate the

point. Most definitions is taken from Gibson et el. The examples are

imaginary.

Abilities and Skills - Ability is a learned trait that permits a person to

do something mental or, physical. The explosives user might , have a

problem connecting up fuse and ignitor cord, since the products were

not designed considering the human ability to perceive spatial patterns

and manipulate the cord in a confined space. The product becomes

unpopular which is communicated to middle and finally senior

management.

Senior management's memory span, the ability to recall perfectly past

experience, might reject the claim. His ability to make comparisons

might allow him to consider other products and anticipate the

effectiveness and cost consequences of a change. r.

Race Age or Sex - The supplier attitude to human diversity is crucial.

If the negotiator of the Central Purchasing Department is a woman, and

the supplier negotiator is overly chauvinistic, she might influence mine

management not to buy. Both white and black races are users of

explosives products, and product names should be selected carefully not

to offend (e.g. if names are overly colonial, black races might feel

offended or perceive the company as "Afrikaans" or "English").

Perception - The process by which an individual gives meaning to the

environment. It involves arranging and interpreting various stimuli into

a psychological experience. Explosives suppliers must concentrate on

good and clear communication, so that stereotyping can be avoided and

19

a good perception of the need and desires of the customer can be built.

The user of explosives might perceive an explosive to be weak, but the

poor performance might be a consequence of too large a interhole

spacing.

Attitudes - Positive or negative feelings or a state of mental readiness

learned through experience to direct behaviour towards people, objects

and situations. A mine manager might feel inferior if an explosive

supplier continuously tell him the explosives are performing sub-optimal

in his mine due to inadequate discipline over drill crews. He might

decide to select a supplier who does not get involved in operational

matters, but only the supply of the commodity.

Values - The guidelines and beliefs an individual uses when

confronted with a situation in which a choice must be made. For

example, the Anglo American mine manager might believe that new

technology can only work if the workforce is convinced it is

appropriate. The human involvement value directed his behaviour.

Personality - The set of characteristics and tendencies that determine

commonalties and differences in people's behaviour. The manner in

which a person acts reflects his personality. It is influenced by

hereditary, cultural and social factors. The mining environment is

usually structured and disciplined, eliminating participative type

managerial personalities and change them to more autocratic thinkers.

It is possible that a mine manager with charisma can alone decide

singularly which explosive supplier is to be chosen and inform the mine

personnel that that is how it will be. Recent changes to the Labour Law

encourages joint decision making, and this behaviour is on the decline.

20

2.2.2 Motivating Behaviour

What motivates behaviour? Maslow's theory assumes that people's

needs depend on what they already have. People's needs are

phsysiological, safety, belongingness, esteem and self-actualisation.

Herzberg's two - factor theory view job satisfaction as resulting form

the presence of dissatisfier - satisfier aspects or hygiene-motivators

factors.. Salary, job security, working conditions, status, company

procedures, quality of interpersonal relationships and supervision are

conditions when present, which do not necessarily motivates, but when

absent cause dissatisfaction. Achievement, recognition, responsibility,

advancement, work content and possible growth are strong motivators

when present, but absence doesn't prove highly dissatisfying. Figure

2.3 illustrates the motivation models diagramatically.

What motivators or hygiene factors play a role in decision making in the

gold mining industry? Both higher order needs and basic needs (or

motivator hygienic needs) influence motivation of the decision maker to

buy or not to buy from an explosives supplier. In Figure 2.3, the

aspects which are assumed dominant in driving buyer motivation at

mine manager level, are highlighted.

Alk MOTIVATORS

HYGIENE CONDITIONS

QUALITY OF INTERPERSONAL RELATION SHIPS

MASLOW

SELF ACTUALIZATION

ESTEEM

EfIERTZSIERG

ACHIEVEMENT

ADVANCEMENT

GROWTH

BELONGINGNESS RESPONSIBILITY

JOB SECURITY

PHYSIOLOGICAL

WORKING CONDITIONS

SAFETY AND

SECURITY

21

FIGURE 2.3 A graphic comparison ofr the Maslow and Herzberg

motivational theories.

HIGHER ORDER NEEDS

V

BASIC NEEDS

Source a Co piled from Gibson et al , 11994: 1141

The buying process as shown in Figure 2.1, elevate§ mine managers as

the most prominent "decision makers". Currently, a third of the 33

gold mines are marginal with limited life spans. The career progression

prospects of mine managers becomes limited. Self actualisation by way

of career advancement can only happen if exceptional mine operational

or profit achievements are illustrated by these individuals. Managers

22

will be interested if the explosives company can contribute without

doubt to the productivity and efficiency of the mining process by

exposing him to improved or new technology, or new services that will

enhance his operation.

Recent political changes have reduced mine management's esteem in

the workplace. The up-liftment of less privileged people to participate

in decision making, changed an autocratic environment to a more

democratic environment. . Suppliers who listen carefully to mine

management's needs and address them, enhance his esteem.

Professional behaviour when dealing with mine management is

therefore critically important, and building a personal relationship to

enhance a sense of belonging. At the same time, the workforce needs

careful attention.

Job security, and in general safety and security, is absent in many mines.

That makes mine managers cost conscious, and again the survival of the

mining complex they manage is important drivers in motivating

behaviour. Suppliers who focus on partnering with mines to help f.

extend the life of mine or increase profitability by improving operational

excellence will address these needs and influence managers positively to

buy from them.

2.2.3 The Buyer Decision-Making Process

Decisions, as defined by Gibson et al., is a means to achieve some result

or to solve a problem. A decision is therefore an organisations'

response to a problem. Complex buyer decision-making models exist,

such as the Webster and Wind model, the Sheth model or the Choffray

and Lilien model, (Bingham and Raffield, 1990 : 120). These models

do not adequately describe the mine buying decision-making process

and are not expanded upon here. The fundamental philosophy

23

underlying these models is that organisational buying is a decision

making process carried out by individuals who interact with other

people within a formal organisational structure.

Bateman and Zeithaml describes six simple steps in decision making

which is shown in Figure 2.4. A necessary condition for a decision is a

problem (Gibson et al., 1994: 610). The decision maker is a problem

solver which selects from alternatives generated by advisors or himself.

What problems exist when deciding who to buy explosives from? The

answer is complex, but the extent of satisfying needs balanced against

price is the essence of the problem. Should alternative products be

used to obtain the same broken rock, or should other suppliers be use?

If other products or suppliers is considered, will the same effect

(sufficiently fragmented rock) be achieved?

r.

24

FIGURE 2.4 The stages of decision maildng

Source o Bateman and Zeithaml, 1990 a 90

In evaluating alternatives, the decision maker has some probabilistic

estimate or idea of the outcome of each alternative. That uncertainty is

25

called risk. A supplier which provides best satisfaction to needs,

reduces risk. Risk is a subjective concept. Decision makers vary

greatly in their propensity for taking risk. A decision maker with a low

aversion to risk defines a problem, generate alternatives and selects

solutions differently from a decision maker with a high aversion to risk.

Some decisions are made on gut feel with lower levels of logic

supporting the decision.

Decision making in groups such as task forces, committees and work

teams has complex group dinamics, but since individuals and groups in

an organisation is subjected to the same operational and cultural

influences, it is likely that groups decision making will follow the same

pattern of individual decision making. The pros and cons of group

generated decisions is summarised in Table 2.1.

TA 1:; LE 2.11 Pros End Cons oil' usfang groups to mike decisions

lPOTENTIIA,L ADVANTAGES EDOTENTIAL DISADVANTAGES

1. Large pool of information. 1. One person dominates.

2. More perspectives and approaches. Satisfycing.

Intellectual stimulation. 3. Groupthink.

4. People understand the decision. 4. Goal displacement

(winning the argument).

People are committed to the decision.

Source e Bateman Zeithanull, 1993 e 97

2.3 MARKET SEGMENTATION

Now that individual and group decision-making behaviour is better understood,

a methodology is needed to identify classes of simular behaviour amongst

26

buying decision makers in the mining industry. Segmentation, according to

Struhl, should follow from some sense that groups within the marketplace

might respond differently to alternative products and product related

communication. How can segments be identified, analysed and evaluated for

p6tential attractiveness?

2.3.1 Market Segmentation Approaches Reviewed

All segmentation approaches focus on either one of the following

characteristics; industry, customer organisation, customer decision

making and product benefits. Macro segmentation devides the market

into sub-groups based on the characteristics of the customer

organisation or industry (such as usage rates, product mix etc.). Micro

segmentation focuses on characteristics of the buyer decision making

process (where is the buying power, attitudes towards products or

vendors etc.). Some of segmentation methodologies are reviewed

namely: the nested approach, a product benefit approach and a product

flow approach.

The Nested Approach

The nested approach stresses the degree. of difficulty to identify and

obtain information in order to evaluate different criteria (Bingham and

Raffield, 1990: 201). Possible criteria on which segmentation can be

based, is arranged in layers or nests with the outer nest representing

criterial information easiest to obtain and assess. Increasingly more

complex criteria forms inner nests. Five nests, or segmentation criteria

groups are arranged as a nested hierarchy. Moving from the outer to

the inner, the groups of criteria are: demographics, operating variables,

customer purchasing approaches, situational factors and personal traits

of the buyers (Shapiro and Sviolela, 1993: 74). Figure 2.5 sets out the

major potential bases for segmentation.

Organizational demographics

Industry

Company size

Location

Operati t g variables

0 Technology

® User-nonuser status

® Customer capabilities

(financial)

Purchasing approaches

o Organization of DMU

o Purchasing policies

© Purchasing criteria

Situational factors

0 Urgency

o Application

Size of order

Personal characteristics

® Motivation

® Buyer-seller dyad

o Risk perceptions

27

FIGURE 2,5. Major potential bases for segmentation according to

the nested approach

General,

observable

(Macro)

(Intermediate)

Specific,

subtle

(Micro)

Somme o Bingham and Raffled, 1990: 202

Validating the

Strategy

Follow-up

Develop a Positioning

Strategy

Decide "How" it will

Compete

Develop the Marketing Mix

Product Design, Technical

Support, Service, Channels

Distribution, Promo, Pricing

28

ilDroduct merit Approach

Basic old-line industries such as mining, metals, forestry products and

chemicals are forced into survival strategies in the Western World due

to overcapacity and reduced order frequency resulting from fierce

global competition. These industries are in search of growing niche

markets, specialising in "value added" speciality products that requires

totally unfamiliar skills to meet user needs (Eckles, 1990: 126). Figure

2.6 sets out the product benefit approach schematically, as developed

by Dayle and Saunder and reported by Eckles.

FIGURE 2.6 Daylle End Saunders industriall market segmentation

=dell Tocusing on product benefits

Defining Objectives Determine Market Evaluate Attractiveness Select Target

Segments of Alternative Segments Market(s)

3-5 Yr.

Planning Horizon Segment by Produc Size, Growth Rates Focused Strategy

Market Benefits-not Competitor's Goals Toward Specific

Financial Customer Seller's Capabilities Goals

Source Eckles, 1990: 126

29

Re-Examination of Product Flow

McDonald and Dunbar developed an a priori segmentation approach

whereby a 'benefits list' is arrived at by plotting the product flow from

the original to the final user. Final product usage is evaluated by asking

questions.

Who buys? - to determine the profits of different buying groups

What is bought, where, when and how? - to determine frequencies,

methods of purchase and location of use.

Why is it bought? - Understand what each market segment lives to

achieve.

All micro segments that displays similarities are brought together and

final segments are then checked for sustainability, reachability and

compatibility with the company.

r.

2.3.2 Difficulties in Segmenting the Narrow Reef Explosives Market

The Narrow Reef Gold Mines historically used nitro-glycerine based

explosives and the fuse and ignitor cord initiating system in all rock

breaking situations. Today many alternatives are available, like

pneumatically pumpable prilled ammonium nitrate products, emulsion

and watergel cartridged explosives, shocktube and electronic initiating

systems. A benefit of one technology over the other, however is easily

obscured by the multitude of variables that . need to harmonize to deliver

the best result. For example, if the drilling pattern is perfectly drilled

but the rock formation changed somewhat but not observed by the

crew, the result might be disappointing. If a better blast is achieve, but

temporarily scraping cannot take place due to full ore passes, the

30

benefit of a good blast is negated. The variation in performance levels

of all required services and activities to advance a face, makes

measurement of benefits difficult in an underground situation. Due to

the labour intensive nature of the process, performance is highly

dependant on how well the labour force is. motivated and performing in

the dangerous, dark, confined and hot humid conditions in which they

operate.

For this reason, many mines uses the same product mix providing them

simplicity. What is expected from a segmentation exercise is not only

identifying current behavioural similarities or differences, but also future

behavioural patterns. Most mines currently use fuse and ignitor cord

initiation systems. Who will change to shocktube, when will they

change and why? These answers are difficult to obtain in a environment

where benefits are be obscured in high background noise of operational

performance variability.

Another problem is the size of the . population within which

segmentation is tried to be achieved. There are only 33 buying entities, f.

and all information recording is structured around these entities. For

example, financial reporting to shareholders is done on a company

basis, that is on mine level. For particular sub-unit of a mine, like a

shaft complex, enough information to enable meaningful segmentation

might be impossible to obtain. Some distortion is associated when

using the mines as the individual population entities. Freegold or Vaal

Reefs, for example, is a union of more than one mines, while other

entities might be small in comparison.

31

2.4 A SEGMENTATION APPROACH FOR THIS STUDY

As explained above, product flow and product benefit segmentation approaches

will not adequately uncover what a particular mine wants to achieve. The

nested approach involves all macro and micro environmental aspects in a

logical fashion, but how these factors are prioritised to expand the dominant

decision leading variables remains a problem. Since the outer nests are more

visible due to easier accessable information, these nests might receive more

attention and distort the answer. Instead of starting at the outer nest and

working inward, the approach will here be to view the nests from the most

inner nest, namely the person making the decision. He sees the solution

through these nests, but the nests influence the decision makers view of the

solution and can therefore be compared with filters allowing less or more

illumination of the solution. Same base variables will lead the decision maker

stongly, which can be compared with a non-shaded filter allowing clear vision

of the solution. Other variables are less influencial, and are dark shaded filters,

only suggesting the solution to the decison maker.

The base variables dictate behaviour, while the others serves as discriptive

variables which help in identifying and differentiating the segments. Figure 2.7

illustrates the concept diagramatically.

32

FIGURE 2,1 The vganiablle Mitering approach to market segmentation

How do the `Decider' behave? How do he

o choose to solve sq" the Problem?

How can the intensity of these filters be determined? The best way is asking

the decison maker what he sees? Anticipate how a reasonable individual will

answer questions regarding his environment, his situation and how

demographics and purchasing styles influences him.

The McDonald and P unbar approach can be adjusted easily to accomodate this

approach expanded upon here. Four steps should be followed. First, a

business definition is obtained to set the scene. Secondly, the customer and

how he behaves in this environment is investigated. Thirdly, the base variables

are identified and the segmentation takes place. A segmentation model is then

compiled. The final and fourth step is to verify the validity of the model by

testing a saMple in each segment and check whether the behaviour corresponds

to what was anticipated.

33

Step 1 : Defining the Business Environment

The segmentation process will start by defining the gold industry and

giving a'business definition.

Define the market and map the product flow. The following questions

are asked;

Who are the customers?

Where are the customers situated?

What product is going where?

An understanding of what problems exist in the industry and what needs

are satisfied by explosive suppliers are investigated. Questions asked

are;

What are the market needs?

How can the market be quantified?

A description of other suppliers and their objectives;

Who are the other suppliers?

What are their strengths and weaknesses?

What strategies are they following?

r.

Step 2 : Seeking an Understanding of Buyer Behaviour in this

Environment

Now that the market needs are better understood, the likely behaviour of the

`decision maker' can be anticipated. The questions the buyer is asking in order

to reduce risk (the filters) are considered next.

How is productivity or efficiency influenced by the decision?

How affordable is the solution offered by the supplier?

What policies and direction is my mining group following?

What is my Central Purchasing Department telling me and what is the

suppliers, users and other influencers telling me?

34

The first three questions will appeal to the safety and security needs of the

decision maker, in other words what will best secure survival for his mine or

optimise the mine as an investment vehicle? The latter two questions appeal to

the deciders selfesteem, in other words how the mining house sees him and do

they approve of his actions so that he can progress or advance to self

actualization.

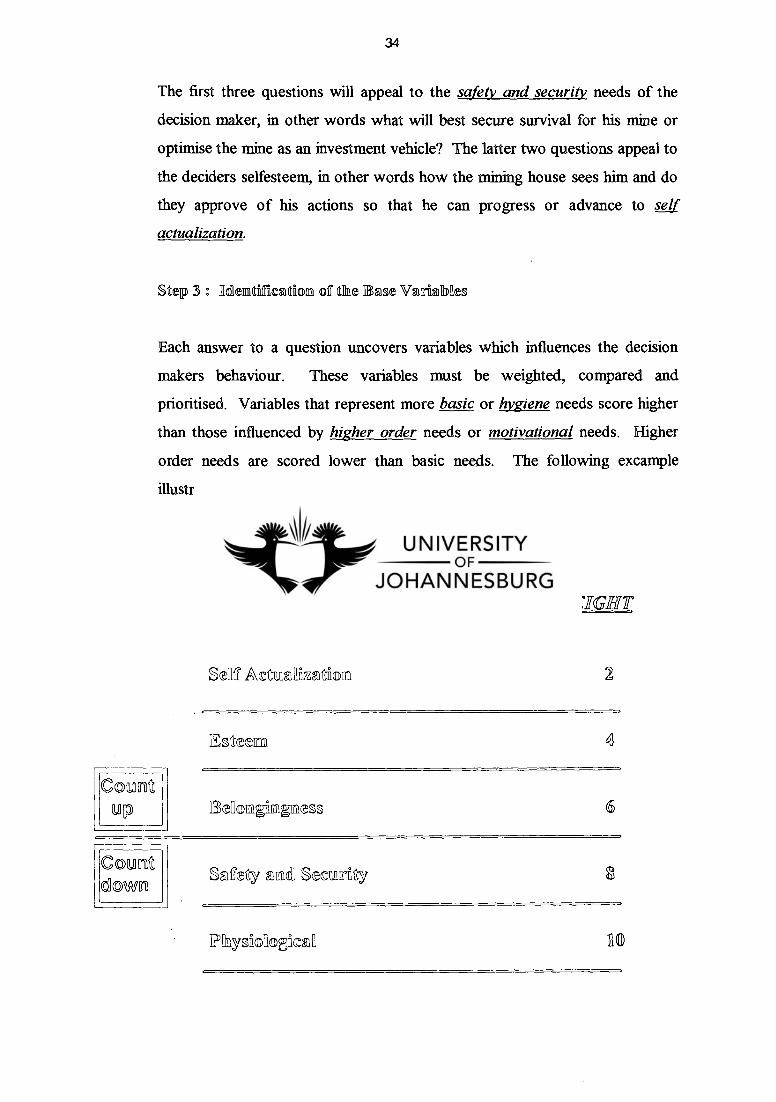

Step 3 o Ilelemitilfrication of the sine VarinNes

Each answer to a question uncovers variables which influences the decision

makers behaviour. These variables must be weighted, compared and

prioritised. Variables that represent more basic or hygiene needs score higher

than those influenced by higher order needs or motivational needs. Higher

order needs are scored lower than basic needs. The following excample

illustrates:

TA ILE 2.2 Motivational! Rowe Cant

MASLOW NEEDS WEIGHT

SellT Actazaztfioun 2

app 6

0

HI

Count down

Szfecy Secu11147

IPhyslolloecza

35

Question

How is productivity or efficiency influenced by the decision'?

A

How productive is the mine?

- Mine productivity very low.

How seriously is efficiency influencing the ultimate success of the mine?

- Mine can close as a result.

If it is improved, what does it mean to the decider, more profits (Esteem),

surviving the mine (safety and security) or both?

- Mine will survive, manager will have a job and will be considered for a

head-office job.

Condandon

Decision making to improve efficiency appeals most to Safety and Security

needs followed by Esteem. From Table 2.2 :

Score = (Surviving the Mine) + (Possible promotion) and have a job

= (Safety/Security + Physiological) + (Esteem + Self Actualization)

= (8+10) + (4+2)

= 18+6

= 24

The two top scoring needs will be used to segment the market and will act as

base variables.

36

Step 4 : Varify the Result

The objective of the segmentation process is to divide the market into groups

with simular needs or demands which results in similar behaviour. To varify

the segments, descripter variables can be used to test the correctiveness of the

behavioural expectation of a segment.

It is also necessary to select one or two samples from each segment and present

the model to these customers. If model prediction and customer expectation

correspond the market segments can be assumed accurately defined.

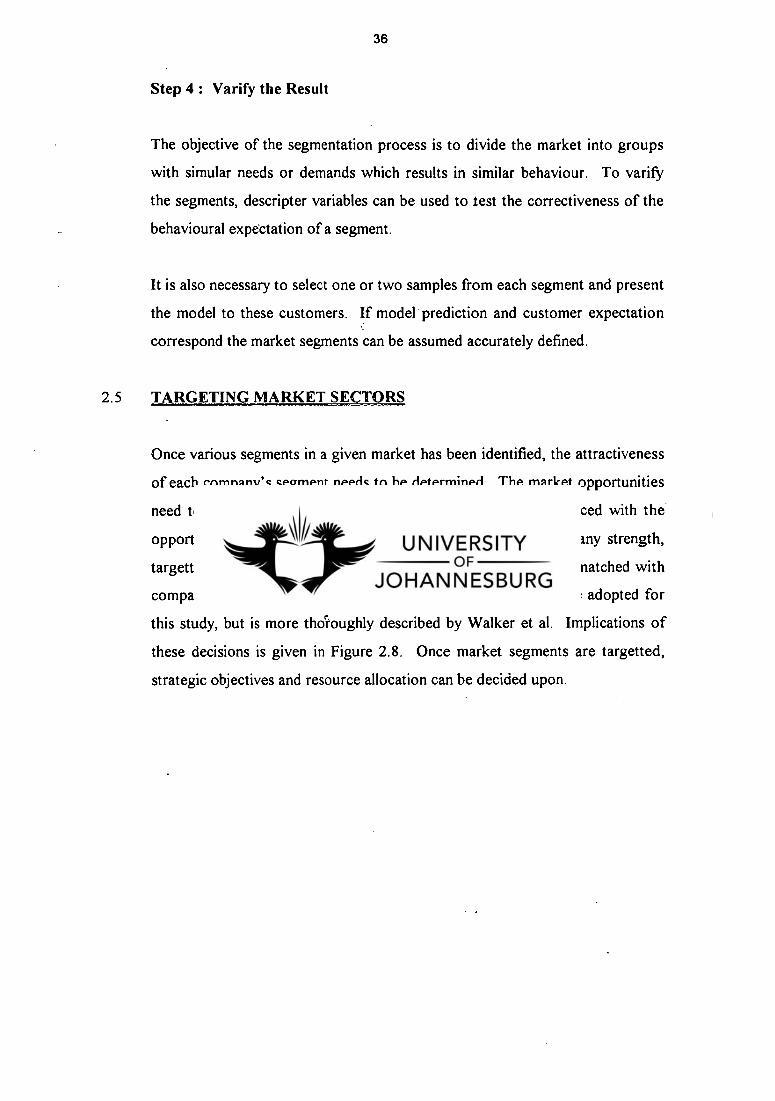

2.5 TARGETING MARKET SECTORS

Once various segments in a given market has been identified, the attractiveness

of each company's segment needs to be determined. The market opportunities

need to be identified, and the business strengths should be balanced with the

opportunities. Sectors where the opportunities match the company strength,

targetting comes naturally. Market attractiveness factors can be matched with

company strengths in matrix format, a methodology which will be adopted for

this study, but is more thdioughly described by Walker et al. Implications of

these decisions is given in Figure 2.8. Once market segments are targetted,

strategic objectives and resource allocation can be decided upon.

37

IFIfGURE 2.e kokplIfievatiofin oTsalltermiztive posfitto s wfithfha the Magket

Attrzetfiverness/Competitfive Ftsfitioral MeatIriLq

COMPETITIVE POSITION

Steil

Medium

Weak

llifyh

Medium

zz

E

Lc

.. • DESIRABLE . POTENTIAL TARGET `Pmtect p&dtion - • ;

- .. ;

- Inve3t in grow n row' rat ' maximum di3tible rcie . • .

,,. Cancentiabe on inMattjinin,n-trength .

.. D ESIRABLE • POTENTIAL TARGET . lleaveXt. to build , .

- Challenge for I .-eadel7ihip •

-' Build selectively mi'atrengths . - ReMfoice vulnerable areas' . . . ... . .

, . , / . • Build selectively

- Specialize around limited strengths - Seek ways to overcome weaknesses - Withdraw if indications of

sustainable growth are lacking

3

, . DESIRABLE POTENTIAL TARGET Baffd idectivelY ,

- - • , ; . • ._ ..-ais. riPhasizoPtorliamlitYbi: ulcr;•-1-sif'

prochictivity . - • ' - Build up ebilify to counter. ,

crmped:lion

..1-

•

-.

Manage for earnings

- Protect existing strengths - Invest to improve position

only in areas where risk is low

5 United expansion on- harvest

- Look for ways to expand without high risk; otherwise, minimize investment and focus operations

6

Protect and refocus

- Defend strengths - Seek ways to increase current

earnings without speeding market's decline

7 Manage for earnings

- Protect position - Minimize investment

$ Divest

- Sell when possible to maximize cash value

- Meantime, cut fixed costs and avoid further investment

9

Sotuarree a WsallIken- et all, 1992: 197

The following attractiveness factors should be considered for the marketing of

explosives:

Differentiation possibilities

Market gaps

Distribution

Investment Intensity

Technology

Industry Capacity

Competive Structure

Price

Business strength factors are:

Relative market share

38

Product/service differentiation

- Distribution

Capacity utilization

- Technological posision

- Salesforce

- Financial capaCity

Advertising

2.6 PRODUCT POSITIONING

A product position is the place the product occupies in the consumers mind

relative to competing products (Kotler and Armstrong, 1994: 258). It is the

perception of the customer as to how well the product offering is performing

relative to competitor offerings in satisfying needs in the targetted market

segments. The emphasis falls on identifying and stressing the competitive

advantage, which is based on quality, service or actual value added.

The products, services, sales personnel, and the company's image are all

aspects which can be used to differentiate, in the mind of the customer. One

way to assess a product offering in relation to competitor offerings is to

compare physical products characteristics (Walker et al, 1992: 205). For

example, the physical behaviour of emulsion explosives are different from

watergel explosives, but is used in the same environment. The high Velocity of

Detonation of Emulsions can be used to position the latter as a product that

does not break up the hanging wall. Physical positioning can be useful, but

does not provide a complete picture of reality, since ultimately, positioning

takes place in customers minds.

Walker et al. goes so far to state that "Many customers often do not want to be

bothered by information about a product's physical characteristics; they are

not buying these physical properties but rather the benefits they provide". The

consumer buys on what a product does rather than what it is. To return to the

39

comparison of emulsions and watergels, emulsions might be perceived as

"weak" explosives, nevermind the physical characteristics that might prove the

contrary. If the cusomer wants a 'strong' explosives, he will not buy

emulsions. Perceptual product positioning will be viewed in this study as the

more important to determine. The following methodology as suggested by

Waler et al, will be followed:

First, competitor offerings will be identified. The set of determinant attributes

which defines the borders of the possible perceptual space of a product is then

determined. Analize where products are 'positioned' currently and the

intensity of the position in the customers minds. Determine the customers most

preferred combination of determinant attributes in relation to market segment

needs, and select a positioning or repositioning strategy.

Product positioning and market strategy is interwoven. Positioning of

explosives products in the gold mining industry must be done with a realiation

that a mature market exists. Total volume is slowly declining, replacement

ptirchasers rather than first time buyers account for most of the volume. The

major objective is therefore to hold existing customers and to sustain a

competitive advantage thattwill sustain customer loyalty. Positioning in such a

market can only resolve around achieving and sustaining a lower delivered cost,

a perceived product quality or technological benefit or a customer service

superiority.

Evidence suggests that the ability to sustain a high level of differentiation or

maintaining a low cost position delivers success in a "mature" market. Walker

et al reports on a study by William K.Hall in 1980 comparing relative success,

measured in terms of 'Return On Investment' of seven heavy duty truck

suppliers in the U.S.A. Figure 2.9 shows Paccar and Ford to be the ROI

leaders, as indicated by the dark shaded area. Paccar offerred the most

differentiated product in terms of good performance, while Ford offered the

lowest relative delivered cost.

Rel

ativ

e pe

rfor

man

ce

High

Average

Low

% = ROI

White Motor 4.7

Ftprti 26

40

Figure 2,9 Strategic competitive positions for the U.S. Heavy-Duty

Truck Market as measured by Return on Investment

High

Average Relative delivered cost

Low

Source e WaIllker et ➢ 1992,305

Since SMX and BME has already stong perceptive positions as low price'

suppliers, AEL must focus on 'Value Added' approaches. However,

explosives systems has many sub-units, each viewed as a product. These

separate products must each be investigated and positioned to deliver the

overall supplier position in the customers mind.

The next chapter will be devoted to the development and validation of a

segmentation model, the first step in understanding market needs. A

subsequent chapter will be devoted to product postioning and market strategy.

Thompson and Strickland puts forward the following sentence as a

Competitive Strategic Principle! "Successful companies invest aggressively in

41

creating sustainable competitive advantage, for it is the single most dependable

contributer to above average profitability".

42

CHAPTER 3

DEVELOPMENT OF A SEGMENTATION MODEL

Although the South African Gold Industry can simplistically be defined as 33 or so

mines managed by six- mining groups, a closer look opens a profusion of a possible

segmentation criteria that easily baffles efforts to identify true behavioral groups that

illustrates similar buying behaviour.

The Variable Filtering segmentation technique developed and discribed in the previous

chapter, allows a structured analysis of the environment the industry operates in and

exposes at the same time a multiple possible variables that might define buying

behavioural segments. The segmentation method however, are focussed and highly

directed. By answering the five questions a buyer/decision maker would ask, a pattern

imediately emerges which allow market groups to fall into logical positions.

The four steps in the process are:

Step 1 : Define the business environment

Step 2 : Seek understanding of buyer behaviour in this environment

Step 3 : Identify and select the base variables

Step 4 : Varify the result

3.1 STEP 1 : DEFINE THE BUSINESS ENVIRONMENT

Important here is to establish an understanding of who the customers are,

where they situated, what product is currently going where, what the real

market needs are, how the market can be quantified and who the explosives

suppliers are? Each aspect is investigated separately.

43

3.1.1 Who is the Customer?

The 33 gold mines are listed in Table 1.1. in chapter 1. Also indicated,

is the mining house the mine is associated with. Since the mining house

manage the mine, the mine managers behaviours are influenced by the

cultures and the views that the mining houses represent. Four aspects

are of particular importance. First, how important are the workforce in

trying to achieve objectives. Does the mining house develop and

mature people, or do they view unions and workers as a negative

necesaty. Secondly, what role does technology play in future planning.

If cost is everything, new technology will be a low priority. If new

technology is viewed as a gateway to improved performance, it is likely

to be tried, and more importantly, the people will have a seriousness in

making new technology work. Thirdly, how are suppliers viewed by

these mining houses? Are they viewed fundamental to the success of

their operations and as a result willing to partner, or do they focus on

their own buyer power and view suppliers as parasites that puts strain

on margins that are already under stress. Finally, how do they evaluate

product and services required in the mining process. Is price the

dominant criteria, di does energy exist to establish value obtained, value

added, as the discriminator. Based on interviews conducted with six

consulting engineers, one from each mining house and summarised in

Appendix I, the following short descriptions of the six mining houses

were arrived at:

An2lo American (Gold Division)

Anglo envisage developing the deep lying reefs south of Western Deep

Levels and the deeper areas of Vaal Reefs in the future. They would

like to be the ultra-deep mining experts. With above average

operational excellence they would like to save the Free State marginal

mines. Anglo central purchasing offered their buying power to improve

44

AEL's input cost. Amgold is eager to partner fully for mutual benefit.

Attitudes are as follows:

Workforce: Positive but strict. Want labour to feel jointly

responsible . Willing to train and develop.

Technology: Look actively at better technology and are

willing to try new things.

Suppliers: Willing to partner.

Value/Cost: Willing to be persuaded of value. Are not only

cost driven.

Randgold

They cancelled the management contracts and reduced head office to 60

people. They are very cost conscious and would like to be seen as the

experts in turning around marginal mines with a no-nonsense approach. r.

Attitudes are as follows:

Workforce: Try to improve productivity while maintaining good

labour relations. Organise stope crews in small

business units. Thinking of higher skilled stope workers.

Technology: Willing to try, but cost pressures limit experimentation.

Economy of scale is most important.

Suppliers: They pressure for a 0 % annual increase, or should be

convinced that there will be a productivity improvement

equal to the price increase. •

45

Value/Cost: Cost focused, but potential is there for partnering for

maximising value.

JCI

JCI are developing the South Deep mine from Western Areas. Their

mines represent all mining conditions namely, deep and shallow, thin

and thick reefs or good and bad hanging wall conditions. Purchasing is

interested in one supplier instead of administering a multitude of

suppliers, but they are cost focussed. Attitudes are as follows:

Workforce: Good labour relations. Leading in concept of

productivity linked to salary increases.

Technology: Traditionally leading in technology, (failed trackless

mining experiment changed that somewhat)

Suppliers: Interested in a single supplier..

Value/Cost: Cosf focused, but willing to experiment with

new technology.

Genkold

Gengold's approach to productivity is to retain only newer high grade

mines, and sell off marginal mines. They would like to have world class

operations with a much reduced, but more productive, workforce.

Attitudes are as follows:

Workforce: Willing to invest and develop the workforce.

Would like to increase blasting cycles and reduce

number of people.

46

Technology: Traditionally not interested in new technology, but signs

are there that they would like to move to shocktube or

EDD's.

Suppliers: Do not like a close partnership. Very critical and hard to

satisfy. They feel they can do things better

and suppliers have little to offer.

Value/Cost: Very cost driven in central bargaining, but can be

persuaded. They advocate efficiency based pricing .

Goldfields

With their high grade mines, they can afford new technology, but at the

same time are very cost conscious. Mines are generally less efficient

due to high profit margins resulting from higher than industry average

grades. Attitudes are as follows:

Workforce: Lots of labour problems, as illustrated recently

at Driefontein. Have a strained relationship with the

workforce.

Technology: Move easily to a new technology, but do not

gain the full benefit due to discipline or lack of

excellence.

Suppliers: Have an aggressive approach. Not easily willing

to partner. Maintain an adverse relationship with

suppliers.

Value/Cost: Make majority of decisions on cost.

47

A mgovaal

Anglovaal is developing new and deeper mines from Loraine. The new

project is called Target, but Sun and Oribi will be developed at a later

stage. They want to be world class, highly productive and are very

interested in new technology. However, their purchasing decisions are

now made at production manager level, while the administration

manager on the mine also influences decisions. Attitudes are as follows:

Workforce: Labour relations are strained due to an older style

or approach to management.

Technology: Very interested in newer technology for the new

deep mine projects. Very interested in rapid cycling on

all their mines.

Suppliers: Tend to play suppliers off against each other.

Do not partner easily.

Value/Cost: Cost-dnven, but look at value too.

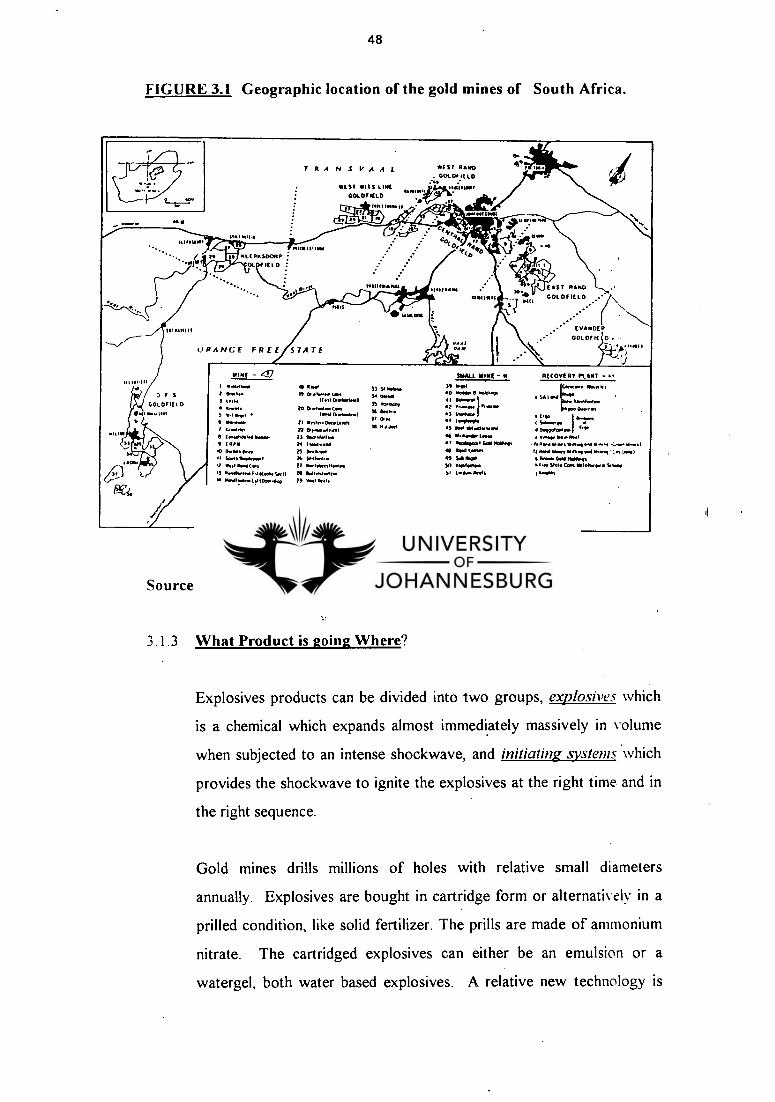

3.1.2 Where are the Mines Located?

The gold mines are situated in a golden arc stretching in the south from

Welkom in the Free State through the West Rand, Johannesburg, East

Rand and ending in the Evander area. Figure 3.1 is a map of the mines,

showing 51 mines, many of which are small or not operating any more.

lase ruse

"44ga 001t1111111010

AL IL PILSOORP

lar FIELD

•

4.

ORANGE FREE STATE

VINE -

I •.4411••• i 0■ •••1• 1 INN

awns

I •••,, • 4 ".'.n 1 frosiors

TRANSVAAL

NEST WITS LINE

Nola inr. 1 16•11.7"444,4'

GOLDFILD, .4/

1141bb' 00;:rmItIIIIN

O

Aftil Apr "alg. MINNA 110

USN RN

11NN

.1011011•

liftp

..04 VAII

IF ST RAND

GOLDI1t ID

ML1636611

0 CoN600040 I.... 13 04..1.414.• 46 41.6•NIN leo" 4 644440••• A•41 1 I a•so t• 1440,.40 • I 11•014.1.1 GNI NPIrqs , Is Pro Noes WINN osol Um, s(..osos ....a

OuNo• INN t3 ONPooN 40 Red L•Nel IT Ift..1 66.6n 4146,4.4116...1 .:,... ,..•1 II SosP011osaspoorl 16 50.41e4..• 01 So• ONO • &M• N GNI 11010•Ns It INN INN CON tr PosIoN•00•ON• SO 00•1004. • IN* SION Can 6141.16.0.<• •ry

IS ..41...101topieSso1 to 0.11•NN.N. SI Tod* Reels 1 0`9.4%

N Poo0aNN• I 0101•••Nots t9 POO KINN

SON.' SO I swat 4001sO1d O..,

IS 1.0.m MN, SI .1.• INN INN

4 ONS0NNI 0101111.44.1 a • II I.• to I••ss S••* tow 0 PO •0 44 40 too

1.4.0. 1. Mosel

AI 111441 If Do ••••••• Ow

11 NI 0•14.1.1

30 0.0..- Co. SION 0.0.000

il •N00. Nett...01 EP IINN•NrINNI

33 91 NON* 3. URN/

35 ........, 31 06.... 31 0 re 36 P./ Jorl

1!... 4104.1 ••losnoltes

NI

IWO .1111

14.4 N611

N.

N

a No

till. o' E•ST RAND

GOLDFIELD ...•

••• (VANDER

• GOLDFIELD •

1 4

111

D

GOLDFIELD

1.•M NO

MALL MINE -

RECOVERY PLANT - a.

44 1•••••••• 3 440 161.1••••••0

I S....4.44 I 4% 4 Deppeencw• "

lo 010 0p.m

34 RON 10 N40••• II •ANA,

2 Persou } 0 • 00.