strategies and structures in the european dairy co ... · the firm has a strong influence on the...

TRANSCRIPT

14

Introduction

The European dairy industry is undergoing majorchanges. Numerous mergers as well asacquisitions have resulted in fewer and largerdairy processors. These structural changes arelinked to the dairy processors’ market strategies.Dairy processors see a need to adapt theirstrategies when their markets are undergoingchanges. Moreover changes in the agriculturalpolicies imply that the markets for dairy productsare becoming more competitive.

This study deals with the changes of the dairyprocessors’ market strategies and organisationalstructures. The aim is to identify the implicationsthat the dairy co-operatives’ growth has for themembers’ possibilities to control the operationsand to finance them.

The point of departure for the discussion isFigure 1. It expresses a contingency approachto organisational design (Miles and Snow, 1978).The top three boxes state that when marketconditions change, firms have to adapt theirstrategies accordingly (Nilsson and Ohlsson,2007). For these market strategies to beimplemented well, the firms have to modify theirorganisational attributes. This sequence isnecessary in the long run; therefore, thedownward-pointing arrows are fat. In the shortrun, ie before the adaptations have beenconducted, it is necessary to use existingresources to create best possible marketstrategies and to try to influence the market –see the thin upward-pointing arrows.

The bottom box of Figure 1 states that alsomember conditions exert an influence when theco-operatives are conducting market adaptationmeasures. Members may find that some marketadaptations imply that the co-operatives nolonger operate in their interest, and thusinvolvement, trust, solidarity and loyalty are

Strategies and Structures in the European DairyCo-operative IndustryJerker Nilsson and Petri Ollila

Dairy processing seems to have substantial economies of scale. Moreover a development towardsdifferentiated business gives advantages to large dairy processors. Given these trends, it is hypothesisedthat dairy co-operatives are gradually losing their raison-d’être as co-operative firms. On the basis of someprior studies, this study discusses the implications that the co-operatives’ growth have for the members. Itshows that the trend towards differentiation, large scale operations and internationalisation is so strong thatmembers have difficulties governing and financing the co-operatives. Reorganisational measures may occuramong the traditionally organised dairy co-operatives.

fading. Further, the members may not be ableto control the business operations of theco-operative, or not have incentives to investtime and effort in assessing the business, orwant to free-ride by hoping that others willconduct the necessary control, etc. Finally,members may not have enough capital tofinance the expansion of their co-operative, orthey may not be willing to allow external investorsto invest sufficient amounts, or if they allowexternal investors, they may not be willing toremunerate these investors enough to attractsufficient capital.

The figure indicates that problems mayaccrue when the two arrows, pointing at the“co-operative organisational model” box implyopposing signals. Therefore the co-operativehas to adapt in different directions, and so itbecomes poorly adapted to both the market andthe members.

The article is structured in accordance withFigure 1. The next section discusses the marketstrategies that dairy processors are choosingto be competitive. In the subsequent section, theco-operatives’ choice of organisationalstructures is presented. Then follows an accountthat presents farmer-members’ preferences andopinions in terms of control of the co-operativesand financial obligations. The article ends withsome conclusions.

Strategies

The most recognised classification of marketstrategies is the one presented by Porter (1980).It comprises three main classes, namely costleadership, differentiation, and focus strategies.All these three are common in the dairy industry,and all of them are used by dairy co-operatives.

Both the cost leadership strategy and thedifferentiation strategy are best pursued if the

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

15

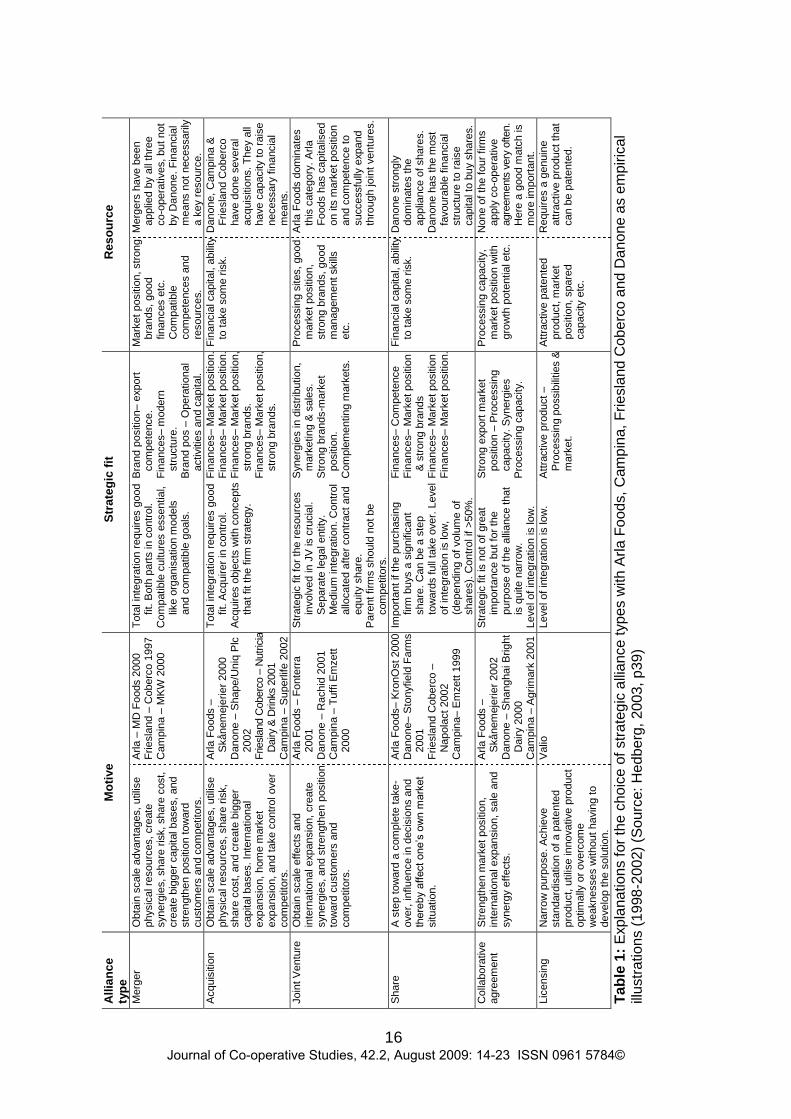

processing firms enjoy economies of scale.Large-scale operations are important for mostdairy processors. There are different ways ofattaining growth. Table 1 presents six growthstrategies as well as the firms’ motive for thechoice of strategy, the strategic fit between thepartnering firms and the resource needs that areneeded for the strategies. These concepts arerooted in the Resource-Based Theory (see forexample Wernerfelt, 1984; Das and Teng, 2000).

An observation is that one expansion strategydoes not exclude another one. Arla Foods, forexample, is found in all the six categories of Table2. At the same time it must be recognised thatthe alliance types are interrelated. If Arla Foodswere not so large it would be less interesting asa partner in a collaborative agreement and wouldhave fewer financial resources for acquiringother firms. A large size stimulates even moregrowth, and small processors have smallchances to expand in other ways than bymerging with or being bought by large firms.

The six growth strategies are notsubstitutable, ie, they fulfil different purposes.The ones that produce the most strength aremergers and acquisitions, as the result is asingle firm with good integration between allbusiness activities. Joint ventures may be risky,eg, the partner may become acquired byanother firm; the share owners may assumeother interests than those they had when theshares were bought; collaborative agreementscan easily be broken; licensing does not givemuch power.

Different types of dairy processors tend to

use different types of alliances. Co-operativesare more prone to merge, while IOF (Investor-Owned Firm) dairy processors tend to buy otherfirms, as is indicated in Table 2. During the five-year period covered by the table, the threeco-operatives (Arla Foods, Friesland andCampina) have conducted many mergers andjoint ventures but relatively few acquisitions. Theonly IOF in the table, Danone, has not mergedeven once but has acquired ownership in manyother firms – five complete acquisitions andbought shares in other f irms on twelveoccasions. The three co-operatives have boughtshares in other firms only to a limited extent.

A hypothesis is that the capital structure ofthe firm has a strong influence on the dairyprocessors’ choice of growth strategy. IOFs caneasily expand their capital base, whileco-operatives have difficulties doing so. ArlaFoods is almost completely f inanced byunallocated equity capital, and the membershave no incentive to invest in the co-operative.The two Dutch co-operatives have a largeramount of individualised capital and themembers have incentives to invest. Frieslandalso has external financiers. This may be areason why Friesland and Campina have mademore acquisitions than Arla Foods and why ArlaFoods has had to compensate its capitalconstraints by involving itself in more jointventures.

One way to obtain large scale isinternationalisation, ie, expansion to othermarkets. Guillouzo and Ruffio (2005) analysed33 EU dairy co-operatives’ internationalisation.

Market conditions • Market changes (retailing, manufacturing, market size, consumption trends, etc. • Poli tical changes

Strategies

Co-operative organisational model; Organisational attributes

Member attributes in terms of governance and financial capacities • Demand for member benefits • Member control • Member financing

Figure 1: Influences on co-operative organisational models

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

Alli

ance

ty

pe

Mot

ive

Stra

tegi

c fit

R

esou

rce

Mer

ger

O

btai

n sc

ale

adva

ntag

es, u

tilis

e ph

ysic

al re

sour

ces,

cre

ate

syne

rgie

s, s

hare

risk

, sha

re c

ost,

crea

te b

igge

r cap

ital b

ases

, and

st

reng

then

pos

ition

tow

ard

cust

omer

s an

d co

mpe

titor

s.

Arla

– M

D F

oods

200

0 Fr

iesl

and

– C

ober

co 1

997

Cam

pina

– M

KW 2

000

Tota

l int

egra

tion

requ

ires

good

fit

. Bot

h pa

rts in

con

trol.

Com

patib

le c

ultu

res

esse

ntia

l, lik

e or

gani

satio

n m

odel

s an

d co

mpa

tible

goa

ls.

Bra

nd p

ositi

on– e

xpor

t co

mpe

tenc

e.

Fina

nces

– m

oder

n st

ruct

ure.

B

rand

pos

– O

pera

tiona

l ac

tiviti

es a

nd c

apita

l.

Mar

ket p

ositi

on, s

trong

br

ands

, goo

d fin

ance

s et

c.

Com

patib

le

com

pete

nces

and

re

sour

ces.

Mer

gers

hav

e be

en

appl

ied

by a

ll th

ree

co-o

pera

tives

, but

not

by

Dan

one.

Fin

anci

al

mea

ns n

ot n

eces

saril

y a

key

reso

urce

. A

cqui

sitio

n O

btai

n sc

ale

adva

ntag

es, u

tilis

e ph

ysic

al re

sour

ces,

sha

re ri

sk,

shar

e co

st, a

nd c

reat

e bi

gger

ca

pita

l bas

es. I

nter

natio

nal

expa

nsio

n, h

ome

mar

ket

expa

nsio

n, a

nd ta

ke c

ontro

l ove

r co

mpe

titor

s.

Arla

Foo

ds –

S

kåne

mej

erie

r 200

0 D

anon

e – S

hape

/Uni

q P

lc

2002

Fr

iesl

and

Cob

erco

– N

utric

ia

Dai

ry &

Drin

ks 2

001

Cam

pina

– S

uper

life

2002

Tota

l int

egra

tion

requ

ires

good

fit

. Acq

uire

r in

cont

rol.

A

cqui

res

obje

cts

with

con

cept

s th

at fi

t the

firm

stra

tegy

.

Fina

nces

– M

arke

t pos

ition

. Fi

nanc

es– M

arke

t pos

ition

. Fi

nanc

es– M

arke

t pos

ition

, st

rong

bra

nds.

Fi

nanc

es– M

arke

t pos

ition

, st

rong

bra

nds.

Fina

ncia

l cap

ital,

abilit

y to

take

som

e ris

k.

Dan

one,

Cam

pina

&

Frie

slan

d C

ober

co

have

don

e se

vera

l ac

quis

ition

s. T

hey

all

have

cap

acity

to ra

ise

nece

ssar

y fin

anci

al

mea

ns.

Join

t Ven

ture

O

btai

n sc

ale

effe

cts

and

inte

rnat

iona

l exp

ansi

on, c

reat

e sy

nerg

ies,

and

stre

ngth

en p

ositi

on

tow

ard

cust

omer

s an

d co

mpe

titor

s.

Arla

Foo

ds –

Fon

terra

20

01

Dan

one

– R

achi

d 20

01

Cam

pina

– T

uffi

Emze

tt 20

00

Stra

tegi

c fit

for t

he re

sour

ces

invo

lved

in J

V is

cru

cial

. S

epar

ate

lega

l ent

ity.

Med

ium

inte

grat

ion.

Con

trol

allo

cate

d af

ter c

ontra

ct a

nd

equi

ty s

hare

. P

aren

t firm

s sh

ould

not

be

com

petit

ors.

Syn

ergi

es in

dis

tribu

tion,

m

arke

ting

& sa

les.

S

trong

bra

nds-

mar

ket

posi

tion.

C

ompl

emen

ting

mar

kets

.

Pro

cess

ing

site

s, g

ood

mar

ket p

ositi

on,

stro

ng b

rand

s, g

ood

man

agem

ent s

kills

et

c.

Arla

Foo

ds d

omin

ates

th

is c

ateg

ory.

Arla

Fo

ods

has

capi

talis

ed

on it

s m

arke

t pos

ition

an

d co

mpe

tenc

e to

su

cces

sful

ly e

xpan

d th

roug

h jo

int v

entu

res.

Sha

re

A s

tep

tow

ard

a co

mpl

ete

take

-ov

er, i

nflu

ence

in d

ecis

ions

and

th

ere

by a

ffect one’s

ow

n m

ark

et

situ

atio

n.

Arla

Foo

ds– K

ronO

st 2

000

Dan

one–

Sto

nyfie

ld F

arm

s 20

01

Frie

slan

d C

ober

co –

N

apol

act 2

002

Cam

pina

– E

mze

tt 19

99

Impo

rtant

if th

e pu

rcha

sing

fir

m b

uys

a si

gnifi

cant

sh

are.

Can

be

a st

ep

tow

ards

full

take

ove

r. Le

vel

of in

tegr

atio

n is

low

, (d

epen

ding

of v

olum

e of

sh

ares

). C

ontro

l if >

50%

.

Fina

nces

– C

ompe

tenc

e Fi

nanc

es– M

arke

t pos

ition

&

stro

ng b

rand

s Fi

nanc

es– M

arke

t pos

ition

Fi

nanc

es– M

arke

t pos

ition

.

Fina

ncia

l cap

ital,

abilit

y to

take

som

e ris

k.

Dan

one

stro

ngly

do

min

ates

the

appl

ianc

e of

sha

res.

D

anon

e ha

s th

e m

ost

favo

urab

le fi

nanc

ial

stru

ctur

e to

rais

e ca

pita

l to

buy

shar

es.

Col

labo

rativ

e ag

reem

ent

Stre

ngth

en m

arke

t pos

ition

, in

tern

atio

nal e

xpan

sion

, sal

e an

d sy

nerg

y ef

fect

s.

Arla

Foo

ds –

S

kåne

mej

erie

r 200

2 D

anon

e – S

hang

hai B

right

D

airy

200

0 C

ampi

na –

Agr

imar

k 20

01

Stra

tegi

c fit

is n

ot o

f gre

at

impo

rtanc

e bu

t for

the

purp

ose

of th

e al

lianc

e th

at

is q

uite

nar

row

. Le

vel o

f int

egra

tion

is lo

w.

Stro

ng e

xpor

t mar

ket

posi

tion

– P

roce

ssin

g ca

paci

ty. S

yner

gies

P

roce

ssin

g ca

paci

ty.

Pro

cess

ing

capa

city

, m

arke

t pos

ition

with

gr

owth

pot

entia

l etc

.

Non

e of

the

four

firm

s ap

ply

co-o

pera

tive

agre

emen

ts v

ery

ofte

n.

Her

e a

good

mat

ch is

m

ore

impo

rtant

. Li

cens

ing

Nar

row

pur

pose

. Ach

ieve

st

anda

rdis

atio

n of

a p

aten

ted

prod

uct,

utilis

e in

nova

tive

prod

uct

optim

ally

or o

verc

ome

wea

knes

ses

with

out h

avin

g to

de

velo

p th

e so

lutio

n.

Val

io

Leve

l of i

nteg

ratio

n is

low

.

Attr

activ

e pr

oduc

t –

Pro

cess

ing

poss

ibilit

ies

&

mar

ket.

Attr

activ

e pa

tent

ed

prod

uct,

mar

ket

posi

tion,

spa

red

capa

city

etc

.

Req

uire

s a

genu

ine

attra

ctiv

e pr

oduc

t tha

t ca

n be

pat

ente

d.

Tabl

e 1:

Exp

lana

tions

for t

he c

hoic

e of

stra

tegi

c al

lianc

e ty

pes

with

Arla

Foo

ds, C

ampi

na, F

riesl

and

Cob

erco

and

Dan

one

as e

mpi

rical

illu

stra

tions

(199

8-20

02) (

Sour

ce: H

edbe

rg, 2

003,

p39

)

16 Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

17

The authors identify six main strategiesalthough three of them can be divided into twotypes. All these strategies aim at attaining largersize but in different ways and for differentpurposes.

• The co-operatives, pursuing a Raw milkprocurement strategy, are doing sobecause they need larger volumes forserving their customers appropriately.

• The Market diversification strategy hasthe purpose of expanding the operationsby selling existing products to foreignmarkets.

• The Commercial asset strategyexpresses economies of scale in theproduct development activities, ie gainingrevenues from the sales of licenses.

• Activity oriented leadership implies thata firm, working in a well-defined marketwith specialty products tries to expand themarket size, thereby acquiring economiesof scale.

• European expansion of nationalmarkets involves exports of products,most often but not necessarily toneighbouring countries.

• Multinationalism means that theco-operative sells large volumes of low-processed products in the world market,in spite of this market being extremelycompetitive.

Guillouzo and Ruffio (2005) also specify someorganisational attributes that are necessary fora co-operative to succeed with the chosenstrategy. The general impression is that thesefirms must be quite advanced in terms ofproduct quality, financial assets and humanresources. Certainly not all co-operativescould have success with these strategies.Especial ly the most ambit ious growthstrategies – European expansion of nationalmarkets, and Multinationalisation – are highlydemanding. The resource types that are ofspecial importance seem to be productportfolio, product quality, financial resources,brands, and technical knowledge. All theseresource types are mainly found in the co-operatives, which are already large and havegood financial strength.

In a study of the expansion strategies ofthe 15 largest dairy processors in theEuropean Union, van der Krogt, Nilsson andHøst (2007) identify some patterns. Seven of

the processors are co-operatives while eightare investor-owned firms. The expansionstrategies were:

1) Mergers2) Acquisitions3) Strategic share holdings4) Joint ventures5) Licensing6) General collaboration agreements.

During a five-year period (1998-2002) the 15dairy processors conducted 198 expansionactivities.

Distinctive differences between the two typesof organisation were found, and thesedifferences were shown to be due to twoattributes, inherent in the organisationalstructures. Co-operatives are by nature risk-averse, the reason being that the farmer-members consider the co-operative to be theirdefence against problematic markets, and sothey do not want their co-operative to follow anoffensive strategy. Further, members are neitherable, nor willing, to invest sufficiently largeamounts of capital in the co-operatives, andthus, there is a capital constraint, preventingthe co-operatives from conducting costly growthstrategies.

Co-operative f irms prefer mergers,collaboration agreements, joint ventures, andlicensing. All of these are low in terms of risks,and they demand limited amounts of equitycapital. Investor-owned firms focus on take-overstrategies – acquisitions and share holdings,both of which involve large investments.

A conclusion from the studies presentedabove is that the large dairy processing firmswant to expand, seemingly without any limits.The co-operatives have, however, a more limitedrepertory of action than the IOF competitorshave.

Co-operative organisational models

Dairy co-operatives’ growth as a response tochanging markets has resulted in a strong needfor capital. As many scholars have pointed out,acquiring capital is not the most salientcharacteristic of the co-operative business form.Members are often not willing to increase theirself-f inancing to the extent required forexpansion needs. According to Vitaliano (1983),among reasons for members’ low willingnessto invest in their co-operatives are free rider,

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

18

horizon and portfolio problems because of non-transferable ownership restricted to members,and that the residual is distributed according topatronage rather than the amount of investment.Even if members were willing to self-finance,Albæk and Schultz (1997) argue that thefinancing of an investment by retained patronagerefunds would lead to efficiency distortion unlessthe financing rule is according to members’ “size”independent of the voting rule.

The need of larger operations and marketpower includes a controversial interest ofmaintaining membership control. In theircategorisation of co-operative models Chaddadand Cook (2004) make a distinction between theownership rights (residual claim) and the controlrights. Members’ interests may be a hindranceto market adaptation. This is especially relevantin co-operatives that have a sizeable amount ofunallocated capital.

Hendrikse and Veerman (2001) argue that inaddition to capital needs, new organisationalforms are also developed to take better care oftransaction specific assets. In order to managethe problem of capital needs for growth,co-operatives have introduced severalorganisational solutions. Van Bekkum andBijman (2006) have categorised co-operatives,which have a need for larger amounts of equitycapital:

1. Internally tradable shares: In addition toretained patronage refunds, manyco-operatives have introduced another

possibility for members to finance theirco-operatives. Even though this way offinancing the co-operative to some extentrestricts the principle of paying the farmersaccording to their patronage, the membershipretains full control. Examples of such dairyco-operatives are Campina in theNetherlands and Dairygold in Ireland. Nilssonand Bärnheim (2000) report about a similarkind of arrangement in the Swedish dairyco-operative Skånemejerier. In manyco-operatives such internally tradable sharesare connected with delivery rights. If so, thecontrol right is indirectly affected in the longrun.

2. Externally tradable bonds: Externalsubordinate bonds are external investmentsthat have a lower rank as capital than theretained patronage refund. Such bonds area way of gaining external capital withoutaffecting members’ control right. A problemwith such bonds is that they often classify asdebt rather than equity. Arla Foods hasfinanced the acquisition of its UK operationsby using such bonds with fixed dividend.

3. External corporate investors: Externalinvestor as special members or shareholdersis a model applied in some co-operatives. Awell performing co-operative with innovativeproduct ideas may provide a low-risk andprofitable business for investment. However,this organisational model includes twosources of potential conflicts. First, whodecides how much will be paid to members

Firm Number of alliances by type Mergers Acquisi-

tions Joint

ventures Shares Collaborative

agreements Licensing Sum

Arla Foods (DK & SE)1

3 1 8 3 2 2 19

Friesland (NL)2 2 7 - 3 - - 12 Campina (NL)3 2 7 1 2 1 - 13 Danone (FR)4, 5 - 5 1 12 (1) - 19 Sum 7 19 10 20 4 2 63

Table 2: Number of alliances by type made by four firms in the European dairy industry1998-2002 (Source: Hedberg, 2003, p33)

1 Arla Foods is the largest dairy processor in Denmark and Sweden. It is a co-operative.2 Friesland Coberco was the largest dairy processor in the Netherlands. It merged in early 2009

with Campina, whereby the world’s largest dairy co-operative was formed.3 Campina was the second largest dairy processor in the Netherlands. It merged in early 2009

with Friesland Coberco, whereby the world’s largest dairy co-operative was formed.4 Danone is the largest dairy processor in France. It is a limited liability company, listed at the

Stock Exchange in Paris.5 The brackets express that Danone’s collaborative agreement is only minor.

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

19

according to use, compared with the amountpaid to investors as interest? Second, ifmember interests conflict with profitabilityrequirements, who decides what is themeaning of member sovereignty with respectto control rights? Despite potential conflicts,some dairy co-operatives like Sodiaal inFrance have applied such a model.

4. Public listing with preferential shares: Away of coping with the conflict of memberand investor governance is to have severalsets of shares having different decision-making power. In this way member controlcan, to a large extent, be maintained and stillsuch external capital can be regarded asequity. However, the conflict about how todivide the surplus remains. This conflict mayhamper the external investors’ willingness tobuy shares. Van Bekkum and Bijman (2006)report that Dairy Farmers of America haveapplied such a model. The Finnish meatprocessing co-operative LSO has formed aseparate company for meat processing thatis financially 37 per cent owned by theco-operative but has about 85 per cent ofvoting rights. The rest of the ownership istraded in the Helsinki Stock Exchange. Thus,LSO has kept the most importantco-operative-ruled function – the meatdeliveries – in its own hands and has becomea kind of holding company for the processingfunction together with external investors.

5. Conversion into farmer-owned IOFs:Chaddad and Cook (2004) regard IOFs asthe other polar end to the traditionalco-operative model. At a quick glance, onemay believe that there are no differencesbetween a co-operative and an IOF ownedby the suppliers. However, there arefundamental differences. Firstly, in an IOF thesurplus is divided according to capitalinvested whereas a co-operative divides itaccording to patronage. Secondly, thedecision-making power is divided accordingto the number of shares instead of the oftenapplied “one member one vote” principle. Inan IOF also the principle of free entry may berestricted. An advantage is that in an IOFthere is an objective way of measuring theperformance, which is not possible in aco-operative. The Finnish Dairy co-operativeValio has moved towards a share companystructure as it is owned by local and regionaldairy co-operatives. This development maybe interpreted as logical as the relative

advantage of the co-operative formdiminishes after milk collecting and deliveryto the processing phase (Ollila 1989, p260).At the same time the processes becomeincreasingly complex and, thus, more difficultfor members to control the performance inthe co-operative form “hierarchicaldecomposition” (Williamson 1981).

6. Entire or partial public listing: Completepublic listing has been exercised a few timesin situations where a co-operative has beenin serious financial trouble. Even suchattempts have been temporary as in the caseof Australian Dairy Vale Foods, which wassoon bought by another company. Despitelatent conf l ict between co-operat ivemembers and investors through stockexchange, partial public listing has beensuccessfully applied in a few co-operatives,as mentioned above.

Increased capital needs for growing operationshas been the most important reason for thevarious co-operative organisational modelsdescribed above. The explanation for the varietyof organisational models is membership’sdesire to maintain co-operative features,especially the control rights. If either the controlrights or the ownership rights have been at stake,the control right has been regarded as moreimportant. However, those two sets of rights areto such an extent inseparable that their completeseparation seems to be difficult to avoid.Because the ownership means residualclaimants, this is always a function of thecontrol right.

The growth of dairy co-operatives also meansincreasing heterogeneity in the memberships.This may become a growing hindrance formember governance. Even more problems mayarise when co-operatives become transnational(Nilsson and Madsen, 2007). Danish-Swedishdairy co-operative Arla Foods has indicateddifficulties in uniting memberships in twocountries.

Member attributes in terms ofgovernance and financial capacities

The preceding sections argue that agriculturalco-operatives tend to become ever larger andget ever more complex structures andstrategies. The memberships becomeextremely large and heterogeneous. Thissection proceeds to discuss the members’

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

20

reactions to increased size and increasedcomplexity.

Based on observations of the changesamong many of the major U.S. agriculturalco-operatives during the last decade, Hogeland(2006) suggests a diagnosis. She claims that,in order to gain strength relative to the competingIOFs, the co-operatives are striving for large sizeand diversif ied operations, whereby themembers do no longer feel affiliated to theirco-operatives. In the eyes of the members,co-operatives have adopted almost all the traitsof the IOF competitors. Thus, the traditionalco-operative culture has vanished. Thisobservation is in line with several otherobservations (Cook, 1995; Fulton, 1995; Bager,1996; Harte, 1997; Nilsson, 1998; Holmström,1999). Lang (2006) provides a detailed accountof the process that resulted in the collapse ofone traditionally organised co-operative,Saskatchewan Wheat Pool.

Nilsson, Kihlén and Norell (in press) presentan empirical test of these propositions, basedon a survey among members of a large andcomplex Swedish co-operative, Lantmännen.The authors find that the members do notunderstand the business operations of theco-operative very well. The members are littleinvolved in the co-operative and they have limitedtrust in the board of directors and in themanagement. Finally, the authors investigatewhether it is possible for the co-operative toconduct remodelling measures such that themembers again would be involved and havetrust, but they find that this is not the case.Hence, the findings support what Hogeland(2006) suggests.

It is often said that members of a co-operativefirst and foremost appreciate good prices andother economic conditions, which contribute toprofitability in their farm operations (Fulton andAdamowicz, 1993; Gray and Kraenzle, 1998;Karantininis and Zago, 2001; Lind and Åkesson,2005; Berlin and Erikson, 2007). Severalempirical studies do, however, indicate that thisis not the whole truth (Bravo-Ureta and Lee,1988; Cain, Toensmeyer and Ramsey, 1989;Jensen, 1990). Of course the farmers musthave revenues, which more than cover theircosts, but this does not necessary mean profitmaximisation. At the same time the membersappreciate good service, closeness, socialrelations and many other so-called soft factorseven higher (Fulton and Giannakas, 2001;Borgen, 2001; Bhuyan, 2007). Such factors

foster member commitment to the co-operative.This is of utmost importance as without such,there is a risk that member supplies will decline,and this is disastrous for everybody (Staatz,1989; Fulton, 1999; Anderson and Henehan,2005; Zeuli and Betancor, 2005). Bremmers andZuurbier (1999) argue that in the global businessenvironment the entire member reward systemmust be renewed.

Österberg and Nilsson (2009) found that thesingle most important explanation to members’satisfaction with their co-operative is not theproduct price levels but the members’ perceptionof their participation in the governance. It is notnecessary that they actually control theco-operative, but at least they should feel thattheir opinions are taken seriously by the board.The study is based on a sample of 1,170Swedish farmers who are members ofco-operatives in a variety of industries.

A related issue is that the Chief ExecutiveOfficer (CEO) gets increased power in the verylarge co-operatives as members have difficultyin understanding many business operations(Cook and Iliopoulos, 2000; Hendrikse, 2007).Hence, not only member control is beingweakened but also the directors’ control.

Laursen (2005) investigated whethermembers’ satisfaction with their co-operativesand their participation in the member democracymight be related to:

1) The structure of the member democracy.2) The economic relations between the

co-operative and the members.3) The co-operative’s degree of diversified

business activities.4) The co-operative’s member communication

and member education.5) The member ’s dependency on the

co-operative.

The study was based on a survey amongmembers of the three largest Danish farmerco-operatives, all of them traditionally organised.The study indicates that farmers attach muchimportance to the member governance of theco-operative. This factor is crucial for membersatisfaction and for the co-operatives’ businesssuccess.

Empirical studies specifically focused onmembers’ view of co-operative financing areless common. Fahlbeck (2007), in a surveyamong members of a variety of Swedishco-operatives, found that the members have

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

21

strong preferences for large unallocated funds.They do not want to have individual ownership,and they do not recognise either any horizonproblem, or any portfolio problem. The study byLaursen (2005) comes to the same conclusionas does the study by Borgen (2001). There isno study which has investigated how memberslook at the possibility of inviting externalfinanciers as co-owners of the co-operative.

Conclusions

The review of studies concerning co-operativemembers in terms of socio-psychologicalmatters in the preceding section indicates thatthe very large and very complex co-operativeshave difficulties in terms of member relations.Farmers demand ins igh t in to the i rco-operat ive’s business. If farmers feeluninvolved in or even alienated from theco-operative, they lose their co-operativeidentity and become solely suppliers.

Especially, the members consider theirgovernance of the co-operative to be crucial.Attitudes to ownership are less clear-cut, butprobably even this factor is considered to beimportant. This refers to collective ownership,while farmers seem to be less attracted byextended individual ownership of theirco-operatives.

All in all, the expectation presented at theoutset of the article seems to have somesupport. As the co-operatives are becoming very

large and very complex, the memberships havedifficulties following. The members feel that theyhave too little influence and they do not want toinvest sufficient amounts of capital. Hence, theco-operatives have no other choice than to inviteexternal financiers and perhaps also to allowcertain influence from the side of thesefinanciers.

It is to be seen how the separation ofownership and control can be maintained in thelong run. In a co-operative there is no objectiveway of deciding what is the proportion of theresult to be paid to financers and what is theproportion paid to the members as patronagerefund. If the former is too low, there is noexternal financing. If the latter is too low, theremay be no members and no supplies of rawproducts. At present it seems that thecombination of external financing with members’interest can function. However, long-runexperiences are still very rare.

The overall conclusion is that the structuralattributes of the co-operatives seem to bedecided by the need for strong market strategiesrather than by the members’ demands (seeFigure 1). If co-operatives do not fulfil the marketrequirements, they will hardly survive in today’sintense competition. On the other hand, firmsmay survive if they do not meet the farmer-members’ requirements, although they maysurvive in another business form than that of atraditional co-operative.

Jerker Nilsson is professor of Co-operative Business and Marketing at the Department ofEconomics as well as at the Department of Work Science, Business Economics andEnvironmental Psychology, Swedish University of Agricultural Sciences, Uppsala andAlnarp, respectively, Sweden. He has, together with K Karantininis, edited Vertical Marketsand Cooperative Hierarchies (Springer, Dordrecht 2007). Petri Ollila is associate professorin food marketing in the Department of Economics and Management at the University ofHelsinki, Finland. He has published several articles and other publications applyingInstitutional Economics to co-operative enterprises.

References

Albæk, S and Schultz, T (1997) One cow, one vote? Scandinavian Journal of Economics 99: 597-615.Anderson, B L and Henehan, B M (2005) What gives agricultural co-operatives a bad name? The International

Journal of Co-operative Management 2 (2): 9-15.Bager, T (1996) Organisations in sectors. Explaining the dissemination of populations of formal organization in

economic sectors – bridging rational choice and institutional approaches. Esbjerg, Denmark: South JutlandUniversity Press.

Berlin, C and Erikson, L O (2007) A comparison of characteristics of forest and farm co-operative members.Journal of Co-operatives 20: 50-63.

Bhuyan, S (2007) The people’ factor in co-operatives: An analysis of members’ attitudes and behavior. CanadianJournal of Agricultural Economics 55: 275–298.

Borgen, S O (2001) Identification as a trust-generating mechanism in co-operatives. Annals of Public andCo-operative Economics 72: 208-228.

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

22

Bravo-Ureta, B E and Lee, T-C (1988) Socioeconomic and technical characteristics of New England dairyco-operative members and non-members. Journal of Agricultural Co-operation 3: 12-27.

Bremmers H and Zuurbier, P J P (1999) Co-operatives restructuring in a global environment – building upfarmer-co-operative commitment through changing reward and governance structures. IAMA World Foodand Agribusiness Conference, Florence, Italy.

Cain, J L, Toensmeyer, U C and Ramsey, S (1989) Co-operative and proprietary firm performance as viewed bytheir customers. Journal of Agricultural Co-operation 4: 81-88.

Chaddad, F and Cook, M L (2004) Understanding new co-operative models: An ownership-control rights typology.Review of Agricultural Economics 26: 348-360.

Cook, M L (1995) The future of US agricultural co-operatives. American Journal of Agricultural Research 77:1153-1159.

Cook, M L and Iliopoulos, C (2000) Ill-defined property rights in collective action: The case of US agriculturalco-operatives. In Ménard, C (ed) Contracts and Organizations. Perspectives from new institutional economics.Cheltenham: Edward Elgar.

Das, T K and Teng, B-S (2000) A Resource-Based Theory of Strategic Alliances. Journal of Management 26:31-61.

Fahlbeck, E (2007) The horizon problem in agricultural co-operatives – only in theory? In Karantininis, K andNilsson, J (eds) Vertical markets and co-operative hierarchies. Dordrecht: Springer, pp255-274.

Fulton, J R, and Adamowicz, W L (1993) Factors that influence the commitment of members to their co-operativeorganization. Journal of Agricultural Co-operatives 8: 39-53.

Fulton, M (1999) Co-operatives and member commitment, The Finnish Journal of Business Economics 48:418-437.

Fulton, M and Giannakas, K (2001) Organizational commitment in mixed oligopoly: Agricultural co-operativesand investor-owned firms. American Journal of Agricultural Economics 5, 1258-1265.

Gray, T W and Kraenzle, C A (1998) Member participation in agricultural co-operatives: A regression and scaleanalysis. RBS Research Report 165. Washington DC: US Department of Agriculture, Rural Business –Co-operative Service.

Guillouzo, R and Ruffio, Ph (2005) Internationalisation of European dairy co-operatives. International Journal ofCo-operative Management 2 (2): 25-32.

Harte, L N (1997) Creeping privatisation of Irish co-operatives. A transaction cost explanation. In Nilsson, J andG van Dijk (eds) Strategies and structures in the agro-food industries. Assen, Netherlands: van Gorcum,pp31-53.

Hedberg, S (2003) Strategic alliances in the dairy industry – with special reference to Arla Foods. Masterthesis 342. Uppsala: Department of Economics, Swedish University of Agricultural Sciences. http://ex-epsilon.slu.se/archive/00000391/

Hendrikse, G (2007) Two vignettes regarding boards in co-operatives versus corporations – irrelevance andincentives. In Karantininis, K and Nilsson, J (eds) Vertical Markets and Co-operative Hierarchies. Dordrecht:Springer, pp137-150.

Hendrikse, G and Veerman, C (2001) Marketing co-operatives: An incomplete contracting perspective. Journalof Agricultural Economics 52: 53-64.

Hogeland, J A (2006) The economic culture of US agricultural co-operatives. Culture & Agriculture, 28: 67-79.Holmström, B (1999) The future of co-operatives: A corporate perspective. Finnish Journal of Business Economics

48: 404-417.Jensen, K (1990) Factors associated with the selection of co-operative vs. proprietary handlers of milk in

Tennessee. Journal of Agricultural Co-operation 5: 27-35.Karantininis, K and Zago, A (2001) Endogenous membership in mixed duopsonies. American Journal of

Agricultural Economics, 83: 1266-1272.Lang, K A (2006) Cognition, agency theory and organizational failure: A Saskatchewan Wheat Pool case study.

MSc thesis. Saskatoon: University of Saskatchewan.Laursen, C V (2005) Member satisfaction and participation in the modern danish co-operatives. MSc Thesis,

Copenhagen: The Royal Veterinary and Agricultural University.Lind, L W and Åkesson, E (2005) Pig producers’ choice of slaughterhouse – co-operative or investor-owned?

The International Journal of Co-operative Management 2 (2): 40-46.Miles, R E and Snow, C C (1978) Organizational strategy, structure, and process. New York: McGraw-Hill.Nilsson, J (1998) The Emergence of new organisational models for agricultural co-operatives, Swedish Journal

of Agricultural Research 28: 39-47.Nilsson, J and Bärnheim, M (2000) Remodelling a dairy producer co-operative in Schwarzweller, H K and

Davidson, A P (eds) Research in Rural Sociology and Development. Volume 8: Dairy Industry Restructuring.Elsevier/JAI Press, Amsterdam, 2000, pp325–353.

Nilsson, J, Kihlén, A and Norell, L (in press) The reasons behind shrinking satisfaction, involvement and trust ina traditionally organized agricultural cooperative.

Nilsson, J and Madsen, O Ø (2007) Cross-border mergers between agricultural co-operatives – a governanceperspective. Journal of Co-operative Studies 4: 27-38.

Nilsson, J and Ohlsson, C (2007) The New Zealand dairy co-operatives’ adaptation to changing market conditions.Journal of Rural Co-operation 35: 43-70.

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©

23

Ollila, P (1989) Coordination of supply and demand in the dairy marketing system – with special emphasis onthe potential role of farmer co-operatives as coordinating institutions, Journal of Agricultural Science inFinland 61: 135-321.

Österberg, P and Nilsson, J (2009) Members’ perception of their participation in the governance of co-operatives:The key to trust and commitment in agricultural co-operatives. Agribusiness. An International Journal 25(2): 181-197.

Porter, M (1980) Competitive strategy. Free Press, New York.van Bekkum, O F and Bijman, J (2006) Innovations in co-operative ownership: Converted and hybrid listed

co-operatives. Paper presented in 7th International Conference of Management in AgriFood Chains andNetworks, Ede, Netherlands, May 31–June 1.

van der Krogt, D, Nilsson, J and Høst, V (2007) The impact of co-operatives’ risk aversion and equity capitalconstraints on their inter-firm consolidation and collaboration strategies – with an empirical study of theEuropean dairy industry. Agribusiness – An International Journal, 23: 452-472.

Vitaliano, P (1983) Co-operative enterprise: An alternative conceptual basis for analyzing a complex institution.American Journal of Agricultural Economics, 65: 1078-1083.

Wernerfelt, B (1984) A resource based view of the firm. Strategic Management Journal 5, 171-180.Williamson, O E (1981) The modern corporation: Origins, evolution, attributes. Journal of Economic Literature

XIX: 1537-1568.Zeuli, K and Betancor, A (2005) The effects of co-operative competition on member loyalty. Paper presented at

the NCERE-194 2005 Annual Meeting, Minneapolis, MN, November 8-9.

Journal of Co-operative Studies, 42.2, August 2009: 14-23 ISSN 0961 5784©