strategies for executive compensation: design and tax ...seminar index strategies for executive...

TRANSCRIPT

MONTRÉAL OTTAWA TORONTO CALGARY VANCOUVER NEW YORK CHICAGO LONDON BAHRAIN AL-KHOBAR* BEIJING SHANGHAI* blakes.com

*Associated Office Blake,Cassels & Graydon LLP

Strategies for

Executive Compensation:

Design and Tax Issues for

a Turbulent Environment

Tuesday, April 10, 2012

SEMINAR INDEX

STRATEGIES FOR EXECUTIVE COMPENSATION:

DESIGN AND TAX ISSUES FOR A TURBULENT ENVIRONMENT

TUESDAY, APRIL 10, 2012

TAB

1. WELCOME LETTER

2. AGENDA

3. INCENTIVE AND STOCK COMPENSATION ARRANGEMENTS FOR

PRIVATE EQUITY TRANSACTIONS

ELIZABETH BOYD AND JEREMY FORGIE

4. INCENTIVE COMPENSATION ISSUES IN CORPORATE TRANSACTIONS

DAVID CRAWFORD AND BILL SUTHERLAND

5. LONG TERM INCENTIVE PLAN CLAWBACKS: DESIGN, TAX AND OTHER

LEGAL ISSUES

KATHRYN BUSH

6. UPDATE ON CANADA REVENUE AGENCY POSITIONS ON LONG TERM

INCENTIVE PLAN CONVERSIONS AND CROSS BORDER CASH BASED

INCENTIVE PLANS

ELIZABETH BOYD

7. TOWER WATSON PROFILES

DAVID CRAWFORD

BILL SUTHERLAND

April 10, 2012

Strategies for Executive Compensation: Design and Tax Issues for a Turbulent

Environment

As hosts, we welcome you to today's session.

This morning you will be hearing Speakers from the Blakes Pensions, Benefits and Executive

Compensation Group and the Towers Watson Executive Compensation Group review and

consider various issues relating to the design and taxation of executive compensation

arrangements, with a particular focus on private equity and mergers and acquisition

transactions.

We are particularly pleased to be joined for this morning’s session by David Crawford and

Bill Sutherland of Towers Watson.

Each of the presentations, as well as additional related materials, is available electronically by

visiting http:///www.blakes.com/StrategiesforCompensation.

Profiles of the Blakes presenters and other lawyers in the Blakes Pensions, Benefits and

Executive Compensation Group are available on our website at www.blakes.com. For your

convenience profiles for David Crawford and Bill Sutherland are included in our booklet.

This morning’s presenters will be available during breakfast and at the end of the session to

meet with you.

Thank you for taking the time to join us this morning. Enjoy the seminar.

SEMINAR AGENDA

7:30 - 8:00 A.M. BREAKFAST

INTRODUCTION

8:05 - 8:40 A.M. INCENTIVE AND STOCK COMPENSATION ARRANGEMENTS

FOR PRIVATE EQUITY TRANSACTIONS

ELIZABETH BOYD AND JEREMY FORGIE

8:40 - 9:15 A.M. INCENTIVE COMPENSATION ISSUES IN CORPORATE

TRANSACTIONS

DAVID CRAWFORD AND BILL SUTHERLAND

9:15 - 9:35 A.M. LONG TERM INCENTIVE PLAN CLAWBACKS: DESIGN, TAX

AND OTHER LEGAL ISSUES

KATHRYN BUSH

9:35 - 9:50 A.M. UPDATE ON CANADA REVENUE AGENCY POSITIONS ON

LONG TERM INCENTIVE PLAN CONVERSIONS AND CROSS

BORDER CASH BASED INCENTIVE PLANS

ELIZABETH BOYD

9:50 - 10:00 A.M. Q & A AND CLOSING REMARKS

1

Incentive And Stock

Compensation Arrangements For

Private Equity Transactions

Presented by:

Elizabeth BoydJeremy Forgie

April 10, 2012

2

Overview of Presentation

• Types of Private Equity Transactions• Corporate Governance Considerations• Participation of Target/Portfolio Company

Management

• Exit Strategies and Investment Horizons• Key Design Considerations and Commonly

Used Incentive Arrangements

3

Overview of Presentation (cont’d)

• Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock Option Rules

• Share purchase loans• Cash Based Long Term Incentive Plans and the

SDA Rules

• Non-Portfolio Company Incentives• Focus on employee-level tax issues – corporate

tax considerations may also affect compensation design

2

4

Types of Private Equity Transactions

• The structure of the transaction and objectives of the principal investors will have a significant impact on design of incentive compensation arrangements –resulting in differences from public company equity and incentive compensation arrangements

5

Types of Private Equity Transactions (cont’d)

• Most common are leveraged buyouts of

target (or portfolio company), often with the participation of management

• Transaction may be structured as a take-over bid, court-approved plan of

arrangement, amalgamation or sometimes as an asset sale

6

Types of Private Equity Transactions (cont’d)

• In some cases, a private equity fund or firm will take a minority equity position in the portfolio company or invest in debt of the company with the possibility of taking a longer-term equity stakeSources: Getting the Deal Through: Private Equity 2011, David I. Walker, Executive Pay Lessons from Private Equity, Boston Law Review May 2011 (survey of 144 U.S. portfolio companies) and September 2011 Blakes Study Recent Developments in Canadian Private Equity and Private Equity: 2012 Trends

3

7

Types of Private Equity Transactions (cont’d)

• After initial investment by private equity

fund or firm in portfolio company, there will often be “follow-on” investment that is

intended to raise further capital to facilitate additional growth of the portfolio

company’s business

8

Types of Private Equity Transactions (cont’d)

• The private equity fund will also often recapitalize the business of the portfolio

company by re-leveraging and taking out invested funds - those funds can then be distributed to investors in the private equity fund,

deployed by the fund to make new investments or even redirected to other portfolio companies in which the private equity fund invests

9

Corporate Governance Considerations

• Private equity fund or manager will often

prefer to be the majority shareholder so that it retains ultimate decision-making

power over the portfolio company

4

10

Corporate Governance Considerations (cont’d)

• Where there are minority shareholders (including management and other institutional

investors) following the transaction, the shareholders’ agreement will typically dictate the manner in which the target company is

governed, including any negotiated veto rights for minority shareholders and special liquidity events for shareholders including management

11

Participation of Target/Portfolio Company Management

• A private equity fund will often regard management of the portfolio company as being critical; for example, where the portfolio company is in an industry that is not familiar to the private equity fund or where the portfolio company’s existing management team was a significant factor in the attractiveness of the investment

12

Participation of Target/Portfolio Company Management (cont’d)

• From the perspective of the private equity

fund and other investors, the objective will often be to emphasize retention and

improvement in the portfolio company’s business and downplay compensation tied

to the closing of the transaction

5

13

Participation of Target/Portfolio Company Management (cont’d)

• Often there will be employment contracts

with key management and target financial performance hurdles that may be

incorporated into equity and other incentive compensation arrangements

14

Participation of Target/Portfolio Company Management (cont’d)

• Bearing in mind (particularly in a take-over bid) disclosure requirements relating to proposed management incentive compensation arrangements, it is quite common for there to be negotiation between members of key management and the private equity fund of different (and, in some cases, enhanced) salary, bonus and incentive compensation arrangements compared to what existed when the company was still a public company

15

Exit Strategies andInvestment Horizons

• Due to the additional debt that is incurred

by the portfolio company, leveraged buyouts can present greater potential risk

to equity investors

6

16

Exit Strategies and

Investment Horizons (cont’d)

• The private equity firm or fund will usually

develop a strategy that is intended to result in adding value to the portfolio

company’s business with the objective of realizing on its investment in the portfolio

company as soon as is practical

17

Exit Strategies and

Investment Horizons (cont’d)

• The mechanism for realization (i.e., the

exit strategy) may be a private sale or initial public offering together with

subsequent secondary offerings

18

Exit Strategies and

Investment Horizons (cont’d)

• The time horizon for a liquidity event or

exit can vary significantly – for example, the private equity fund may have a long-

term investment strategy with the objective of recouping its investment along with a

return

7

19

Exit Strategies and

Investment Horizons (cont’d)

• On the other hand, there could be other factors which make a faster exit attractive including opportunistic events such as a particular buyer (or type of buyer) becoming interested in the portfolio company due to a variety of different factors including tax, regulatory or competition law considerations

20

Exit Strategies and

Investment Horizons (cont’d)

• Portfolio company shareholder agreements often contain provisions dealing with anticipated

liquidity events such as merger, sale to another corporation or initial public offering and, where there is an initial public offering, ensuring that

shareholders, including management, have freely trading shares in the event of an IPO

21

Key Design Considerations and Commonly Used

Incentive Compensation Arrangements

• Plan governance – compared to public

companies (board reacting to management proposals), in many cases,

compensation decisions such as approval of management contracts, equity grants

and other incentive compensation plans

require only approval of principal investors

8

22

Key Design Considerations and Commonly Used Incentive Compensation Arrangements (cont’d)

• Performance objectives – because of significant leveraging, promoting cash flow and debt service are often important objectives which impact on plan design – incentive compensation plans may be designed, for example, to reward management’s contribution to control of discretionary costs, improving productivity, strategic repositioning and growth of the business that exceeds the rate of return assumed by the principal investors

23

Key Design Considerations and Commonly Used Incentive Compensation Arrangements (cont’d)

• Importance of equity-based incentives –

studies noted above suggest that for portfolio companies:

– equity-based incentives for key management often represent 65% to 70% of total

compensation opportunity

24

Key Design Considerations and Commonly Used Incentive Compensation Arrangements (cont’d)

– providing a piece of the total appreciation in value of the portfolio company is a main driver as opposed to competitive equity grants

– relatively large up-front equity grants for key management – most often in the form of stock options, a portion of which may be subject to time-based vesting and a portion subject to performance-based vesting, including measures such as EBITDA and internal rate of return (IRR)

9

25

Key Design Considerations and Commonly Used Incentive Compensation Arrangements (cont’d)

– expectation that key management (e.g., CEO) will make a significant personal equity

investment in the portfolio company at the outset and investment in the company following the liquidity event

26

Key Design Considerations and Commonly Used Incentive Compensation Arrangements (cont’d)

• Equity grants will often be reserved for key

management and principal investors may be reluctant to authorize increase in

available option or equity pool – provision in original pool for additional grants to

employees promoted into key

management roles and new hires

27

Key Design Considerations and Commonly Used Incentive Compensation Arrangements (cont’d)

• Equity grants may not be available for management beneath the top “key

management” tier, in which case, cash-based long-term incentive plans can be important, including appreciation rights, cash-settled

restricted share units (RSUs), cash-settled performance share units (PSUs) and sometimes even cash-settled deferred share units (DSUs)

which incorporate vesting provisions

10

28

Key Design Considerations and Commonly Used Incentive Compensation Arrangements (cont’d)

• Private equity fund often wants to limit ability of portfolio company executives to liquidate their

equity holdings prior to an IPO or other defined liquidity event. Sometimes, there will be an exception for shares already acquired by the

executive as opposed to outstanding stock options or in some cases for certain narrowly defined events (e.g., death or disability).

29

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules

• Employee stock options and other equity awards granted by a Canadian-controlled corporation (CCPC) have preferential Canadian income tax treatment:

- taxable employment benefit arises when shares are disposed of (subsection 7(1.1) of Income Tax Act (Canada) (ITA)) – the exercise of the stock option or the issuance of shares under a stock bonus or share-settled restricted share unit is not a taxable event

30

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

– the employee may claim a 50% deduction (paragraph 110(1)(d.1)) against the taxable

employment benefit (e.g., in-the-money amount when the option was exercised or in the case of a stock bonus, the fair market

value of the share at the time it was issued) provided:

11

31

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• the employee does not dispose of the share (other than because of death) or exchange the share within 2 years of the date the employee acquired the share

• the employee has not claimed the regular stock option deduction under paragraph 110(1)(d)

• Alternatively, employee may be able to claim the 50% deduction under paragraph 110(1)(d) that is also available for “ordinary” non-CCPC options

32

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• Unlike with publicly traded companies subject to stock exchange rules, there is no requirement that private company options be issued at fair market value provided that when shares are issued they are “fully paid” in cash, past services or a combination

• “Fully paid” requirement can be an issue with stock bonuses or immediately exercisable discounted options for new employees or employees of a new entity

33

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• For some CCPCs, employee may be able to claim capital gains exemption for “qualified small

business corporation shares” (sections 110.6(1) and 110.6(2.1)) although this is subject to various restrictions where the taxpayer has

cumulative net investment losses (CNIL) and allowable investment business losses (ABIL) and claiming the deduction may trigger

alternative minimum tax (AMT)

12

34

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• The determination of whether the portfolio company is a CCPC is not always

straightforward

• A CCPC is a Canadian corporation (generally a

corporation resident in Canada constituted under the laws of Canada or a province) that is not controlled by a publicly listed corporation or

by one or more non-residents

35

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• In determining CCPC status “control” in the ordinary sense is not required – where the

shares of a corporation are widely held by non-residents and/or publicly listed corporations such that none of those shareholders controls the

corporation, the corporation will not be a CCPC if it would be controlled by one person if that person owned all of the shares held by such

non-residents and publicly listed corporations

36

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• By “ordinary stock options,” we refer to an agreement by a particular corporation that is not a CCPC (or mutual fund trust) to sell or issue its shares (or trust units) to an employee or an employee of a corporation (or mutual fund trust) with which the particular company does not deal at arm’s length

• General stock option tax treatment: (i) no tax on grant; (ii) tax on benefit arising on exercise; (iii) benefit equals excess of fair market value of shares acquired under the option over the exercise price (i.e., the in-the-money amount)

13

37

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• Employee can claim a 50% deduction under paragraph 110(1)(d) against the taxable benefit arising on the exercise of the options if the following conditions are met:– the exercise price is at least equal to the fair market value of the

shares at the time the options were granted

– the employee deals at arm’s length with the corporation granting the option and the employee’s employer (if different from the grantor of the option)

– the shares are “prescribed shares” under Regulation 6204

38

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

– paragraph 110(1)(d) deduction can apply to ordinary options or to CCPC options where deduction under paragraph 110(1)(d.1) does not apply

– threshold question – is there an agreement to sell or issue shares of the employer or a corporation with which the employer does not deal at arm’s length?

– query whether there is such an agreement where option provides that it can only be exercised on a liquidity event and will be automatically cashed out

– fair market value exercise price can also be a challenge to establish in a private company context – “fair market value” is not a defined term under the ITA and CRA generally does not provide rulings on valuation issues

39

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• Arm’s-length requirement – generally,

employees, including senior management, are considered at arm’s length from their

employer but where management is part of control group, arm’s-length requirement

for paragraph 110(1)(d) deduction would

not be met

14

40

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

• Prescribed shares under Regulation 6204

– where dividends or liquidation entitlements are limited to a maximum or fixed at a minimum, shares will not be prescribed shares

– where shares can be reacquired by issuer or person with whom the issuer does not deal at arm’s length, this may preclude shares being prescribed shares

– conversion rights can also be problematic

41

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

– some exceptions to repurchase restrictions if price does not exceed fair market value and/or to provide a market or protect employee from loss

– relevant dividend, liquidity and repurchase provisions can be in share terms or under an agreement in respect of a share or its issue, which could include shareholders agreement, credit agreement, etc.

– prescribed share test is at time shares are issued (or would have been issued in the case of a cash-out)

42

Stock Options – Rules for Canadian-Controlled Private Corporations and Ordinary Stock

Option Rules (cont’d)

– paragraph 110(1)(d) deduction will not be available on an option cash-out unless company that granted option files election under subsection 110(1.1) to forego any deduction of cash-out amount

• subsection 110(1.1) election is made on employee’s T4 for the year in which the option is cashed out

• where options cashed out on exit event, purchaser will control company at time T4s are prepared

• commitment from purchaser to cause election to be made can be included in purchase agreement but employees may not be parties

15

43

Share Purchase Loans

• Management investment can be facilitated through a share purchase loan, as loans generally not included in income unless forgiven

• Where employee is a shareholder, need to consider shareholder loan tax rules, in particular, subsections 15(2) and 15(2.4), as well as section 80.4 which provides for a taxable benefit where employee receives a low interest or interest-free loan as a consequence of his/her office or employment

44

Share Purchase Loans (cont’d)

• Under s. 5(2), the amount of a loan received by a shareholder of a corporation from the corporation, a related corporation or a partnership of which the corporation or related corporation is a member, is included in the shareholder’s income for the year in which the loan was received, subject to certain exceptions:

45

Share Purchase Loans (cont’d)

• S.15(2.4) provides that s.15(2) will not apply where the loan is provided to an individual who is both an employee and a shareholder of the lending corporation or of a related corporation to enable the individual to acquire newly issued shares of the lending corporation or a related corporation where:– it is reasonable to conclude that the loan was provided because

of the individual’s employment and not because he/she is a shareholder

– at the time the loan is made, bona fide arrangements were made for repayment within a reasonable time

16

46

Share Purchase Loans (cont’d)

• Requirement for bona fide arrangements for repayment within a reasonable time does not require all of the loan terms be “commercial”, e.g., would not preclude an interest-free loan and may not require specific contractual repayment terms, but does require that arrangements for repayment exist when the loan is granted and the loan be repayable within a “reasonable time”

• Requirement for repayment on termination of employment, sale of shares or other event, the timing of which is uncertain, is unlikely to constitute bona fide arrangement for repayment within a reasonable time

47

Share Purchase Loans (cont’d)

• Interest-free loans and loans at an interest rate below the “prescribed rate” for employee loans will result in a taxable benefit under s. 80.4

• Essentially, benefit equals difference between the prescribed rate and amount of interest actually paid by the employee for the year and not later than 30 days after year-end

48

Share Purchase Loans (cont’d)

• S. 80.4 applies to loans provided because of or as consequence of an individual’s previous, current or intended office or employment

• Taxable benefit under s. 80.4 is deemed under section 80.5 to be interest for purposes of paragraph 20(1)(c), which may allow employee to deduct interest benefit (provided shares can be said to have been acquired to earn income)

17

49

Cash-Based Long-Term Incentive Plans and the SDA Rules

• Where real equity reserved for key executives, other employees typically receive cash-based long-term incentives, including:– restricted share units

– performance share units

– unitized awards not based on shares values

– appreciation rights

50

Cash-Based Long-Term Incentive Plans and the SDA Rules (cont’d)

• Salary deferral arrangement (SDA) rules

will be relevant

• Components of SDA definition

– right to receive an amount after the year

– in respect of an amount on account of salary

or wages for services in the year or a preceding year

51

Cash-Based Long-Term Incentive Plans and the SDA Rules (cont’d)

• Components of SDA definition (cont’d)

– must be reasonable to consider that one of the main purposes is to postpone tax

– includes a right subject to conditions unless there is a substantial risk one such condition

will not be satisfied

18

52

Cash-Based Long-Term Incentive Plans and the SDA Rules (cont’d)

• There is virtually no jurisprudence relating to the SDA rules

• Deferred compensation plans generally designed to minimize CRA assessing risk

• Commentary to date suggests the following about CRA’s position with respect to the SDA rules– time-based vesting is not sufficient to create a

substantial risk of forfeiture

53

Cash-Based Long-Term Incentive Plans and the SDA Rules (cont’d)

• Share unit plans that pay out by the end of the third year following the year in which the

relevant services are rendered should fall within the paragraph (k) exception to the SDA definition applicable to bonuses and similar payments

• Share appreciation rights should not result in an SDA provided payments occur promptly

following vesting

54

Cash-Based Long-Term Incentive Plans and the SDA Rules (cont’d)

• Where awards subject to genuine, reasonably stringent performance conditions, there may be a substantial risk that one of the conditions will not be satisfied such that no SDA arises

• In private equity context, may want to tie settlement/vesting to liquidity event to retain employees and limit cash drain

19

55

Cash-Based Long-Term Incentive Plans and the SDA Rules (cont’d)

• Where incentive is based on appreciation rights model, some concern that CRA may challenge if

share value is based on a formula that reflects financial measures (e.g., EBITDA, sales etc.) but not necessarily a commercial fair market value

or where appreciation not based on share values at all but on increases in a notional unit, although favourable rulings have been granted

in the past

56

Non-Portfolio Company Incentives

• Private equity incentives sometimes provided at “holdco” level

• Common where “holdco” is U.S. LLC to provide employees with “profits interests” in LLC

• LLC not specifically recognized under ITA but CRA position to date seems to be that LLCs will generally be treated as corporations, while in U.S. they are considered to be a flow-through entity akin to a partnership

57

Non-Portfolio CompanyIncentives (cont’d)

• Profits interests share in increases in the value of the LLC only after the agreed upon value is allocated to other LLC units

• Profits interest should be a security under Canadian securities laws so in principle should result in same tax treatment as acquisition by employee of any other security as a result of employment

20

58

Non-Portfolio CompanyIncentives (cont’d)

• If LLC is a corporation for Canadian tax

purposes, profits interest may be a share for purposes of section 7 of ITA

• Regardless of whether section 7 applies, if profits interest granted to employee, it

appears that fair market value at grant would be taxable benefit of employment

59

Non-Portfolio CompanyIncentives (cont’d)

• Profits interests generally have no intrinsic value at grant since if LLC liquidated at that time holders of profits interest would receive nothing

• In U.S., current tax rules allow profits interests to be granted at zero value (i.e., no income inclusion on grant) and any increase to be taxed as a capital gain

60

Non-Portfolio Company

Incentives (cont’d)

• Would expect profits interests to have

some positive fair market value for ITA purposes, but can be difficult to establish

• Appears to be no published CRA commentary on taxation of profits interests

granted to employees as a form of incentive compensation

21

61

Non-Portfolio Company

Incentives (cont’d)

• Where “holdco” or “opco” is actually a partnership for ITA purposes, this may affect available forms of incentive compensation

• In particular, partnerships cannot grant options on partnership units under section 7, although CRA’s published statements indicate that employees may still benefit from section 7 where options granted by partners that are corporations

• Not clear how CRA’s position applies with multi-tiered partnerships or structures involving trusts; sometimes see separate management holdco established which grants options subject to section 7

1

© 2012 Towers Watson. All rights reserved.

David CrawfordBill Sutherland

April 10, 2012

Incentive Compensation Issues in Corporate Transactions

towerswatson.com 2

Introduction

• A thorough assessment of incentive compensation programs is often

overlooked during corporate transactions

• At times, a thorough assessment does not get completed until well after the

transaction has been completed

• Our discussion today will aim to highlight some of the issues that can

materialize for organizations that put themselves in play and for organizations

looking to make an acquisition

2

towerswatson.com 3

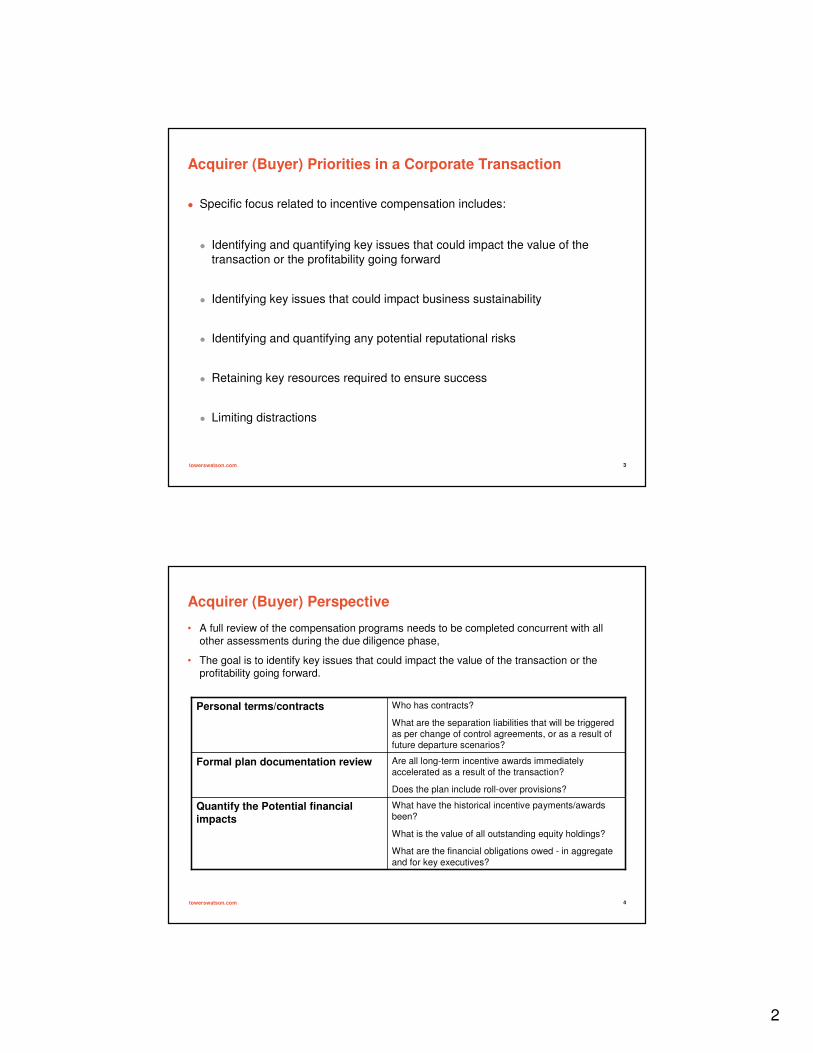

Acquirer (Buyer) Priorities in a Corporate Transaction

� Specific focus related to incentive compensation includes:

� Identifying and quantifying key issues that could impact the value of the

transaction or the profitability going forward

� Identifying key issues that could impact business sustainability

� Identifying and quantifying any potential reputational risks

� Retaining key resources required to ensure success

� Limiting distractions

towerswatson.com 4

Acquirer (Buyer) Perspective

What have the historical incentive payments/awards

been?

What is the value of all outstanding equity holdings?

What are the financial obligations owed - in aggregate

and for key executives?

Quantify the Potential financial

impacts

Are all long-term incentive awards immediately

accelerated as a result of the transaction?

Does the plan include roll-over provisions?

Formal plan documentation review

Who has contracts?

What are the separation liabilities that will be triggered

as per change of control agreements, or as a result of future departure scenarios?

Personal terms/contracts

• A full review of the compensation programs needs to be completed concurrent with all other assessments during the due diligence phase,

• The goal is to identify key issues that could impact the value of the transaction or the profitability going forward.

3

towerswatson.com 5

Transaction Scenarios

� Acquired company’s incentive compensation plan tends to disappear

� May include a standstill agreement that leaves plans unchanged for a

period of time

Acquisition

A purchases B

� Bigger executive role

� Anticipate pay disclosure and governance scrutiny

IPO

� Incentive plans can take on a ‘yours, mine, or ours’ mindset

� Provides an opportunity to take the ‘best-of’

Merger

A and B combine

� Can lead to dramatically different reward cultures and pay philosophies

� Highly focused/customized incentive plans created – opportunity to

experiment

Joint Venture

A and B create C

� New ownership

� Equity focused on deal price

Go Private

� Acquired business tends to see its incentive plans disappear or, at the very

least, significantly modified to align with the new cultureSale/Divestiture

A sells part of its

business to B

towerswatson.com 6

Company In-Play or Reviewing Strategic Alternatives

� May require the creation of retention programs to ensure that critical talent

is retained and key executives are acting in the best interests of the desired transaction efforts.

� Need to ensure that any amounts are responsible in the context of the

entire pay package.

Additional

Retention Incentives

� Providing clarity around the equity treatment could provide a strong

incentive to retain key talent – particularly if potential value is meaningful.

� Important to also ensure responsible treatment to allow for retention beyond transaction.

Program

Treatment

� Understanding termination benefits can foster significant retention for ‘at-

risk’ positions.

� Formalize/clarify understanding of severance protection.

Security /

Protection

� Implication for management: May have Winners and/or Losers

� Bigger Job, Same Job, Smaller Job, No Job

4

towerswatson.com 7

Program Treatment – Equity Compensation (LTI)

� Consider the following principles:

� A technical change-of-control (COC) should not result in automatic vesting.

— If there is an ongoing share price and/or company performance can still be

reasonably measured, there is no need to automatically vest or wind down the plans

� Participants should not be penalized

— If the plans cannot, from a practical point of view, continue (e.g., no share price available or acquiring company does not want the equity continuing), full value should ultimately be settled.

— A participant whose employment is terminated as part of the COC should receive the full benefit of the LTIP awards (i.e., fully vested)

towerswatson.com 8

Stock Option in Transaction

� 3 types of treatment for stock options on a change-in-control:

1. Accelerate vesting and settle on transaction price;

2. Accelerate vesting and exchange options for those of the acquiring company (maintaining the option holders economic value); or

3. Maintain vesting and exchange options for that of the acquiring company (maintaining the option holders economic value).

� The 3rd treatment is preferable with acceleration only if:

� The participant is actually or constructively terminated, or

� It is not practical to exchange the options (e.g., no publicly-traded share is available).

5

towerswatson.com 9

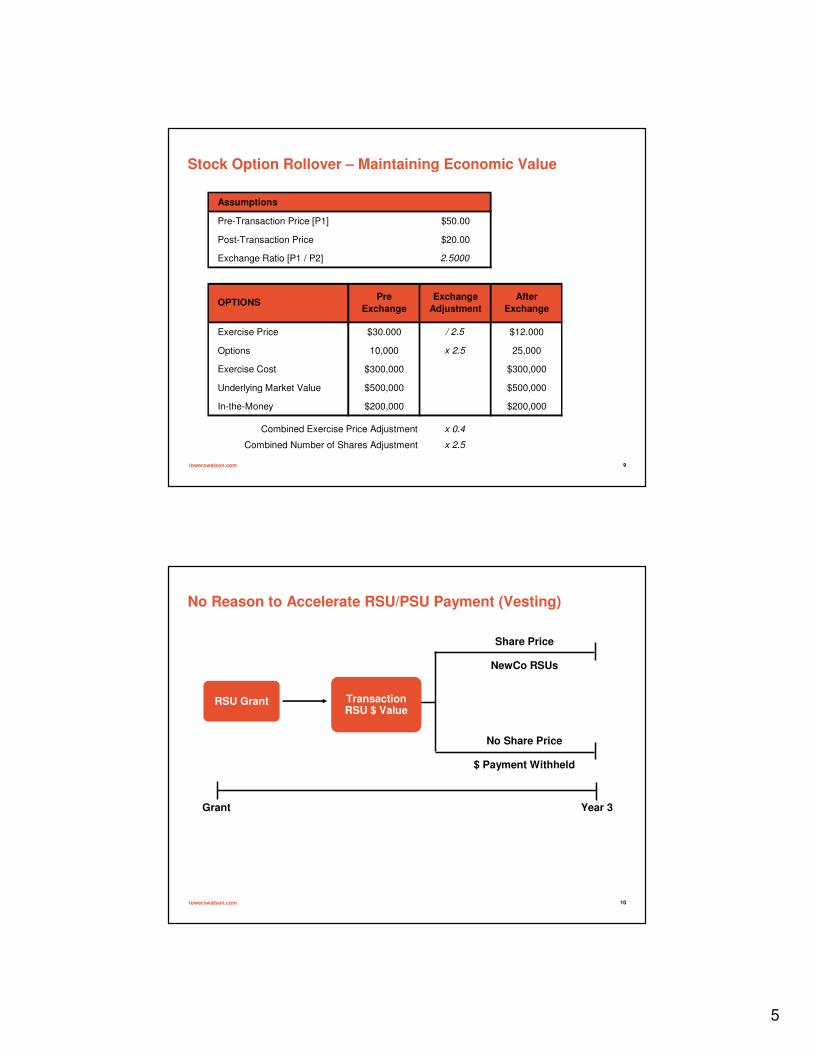

Stock Option Rollover – Maintaining Economic Value

Assumptions

Pre-Transaction Price [P1] $50.00

Post-Transaction Price $20.00

Exchange Ratio [P1 / P2] 2.5000

Exercise Price $30.000 / 2.5 $12.000

Options 10,000 x 2.5 25,000

Exercise Cost $300,000 $300,000

Underlying Market Value $500,000 $500,000

In-the-Money $200,000 $200,000

Combined Exercise Price Adjustment x 0.4

Combined Number of Shares Adjustment x 2.5

Pre

Exchange

After

ExchangeOPTIONS

Exchange

Adjustment

towerswatson.com 10

No Reason to Accelerate RSU/PSU Payment (Vesting)

Grant Year 3

TransactionRSU $ Value

RSU Grant

Share Price

NewCo RSUs

No Share Price

$ Payment Withheld

6

towerswatson.com 11

Dollar Amount Converted to RSUs/DSUs

� Company in black-out, or

� Company anticipating IPO

Grant Year 3

$ Denominated Retention

Convert to DSUs

Remain Cash

Convert to RSUs

Settle

Settle

Continue

towerswatson.com 12

Key Points

� Ensure a complete review of all contracts and plan terms

� Understand the financial obligations triggered as a result of the transaction

� Understand specific program treatment

� Immediate vesting is not always a requirement

� Pay particular attention to retaining key talent

1

Long Term Incentive Plan Clawbacks: Design, Tax and

Other Legal Issues

Presented by:Kathryn Bush

April 10, 2012

2

Introduction

• Since 2008, substantial growth of the use of clawbacks in Canada

• Blakes Bulletin: “Clawbacks Coming to Canada” dealing with securities and corporate law aspects

• Current public examples

• Design issues

• Canadian tax issues

3

U.S. Statutory Clawbacks

• Sarbanes-Oxley Act of 2002 (SOX)– negative revision of financial results– executive misconduct

– material non-compliance in the financial results

– any incentive payments and entire payment– 1-year period

– CEO and CFO– enforced by SEC

2

4

U.S. Statutory Clawbacks (cont’d)

• Dodd-Frank Wall Street Reform &

Consumer Protection Act (DFW)

– applies in wider circumstances and to more employees than SOX

– any material non-compliance that results in a financial restatement

– all current and former executives

5

U.S. Statutory Clawbacks (cont’d)

– 3-year look back

– absolute liability

– excessive portion of the award

– enforced by the Issuer

6

Financial Stability Board Principles

• FSB co-ordinating national financial

authorities

• Bank of Canada, OSFI and federal

Ministry of Finance are FSB members

• Principles for Sound Compensation Practices - Implementation Standards

3

7

Financial Stability Board Principles (cont’d)

• OSFI best practices for Canadian financial

institutions

• Canadian issuers which are subject to

SEC listing requirements

8

Contractual Clawbacks in Canada and the U.S.

• Executive misconduct or bad behaviour

• Joining a competitor

• Movement to absolute liability

9

Type and Relative Prevalence ofClawbacks in the U.S. and Canada

• 450 public companies surveyed by Hay Group– > 50% use clawbacks– 82% of Fortune 100 companies use

clawbacks

– clawbacks used in• annual incentives• stock options• RSUS

4

10

Type and Relative Prevalence ofClawbacks in the U.S. and Canada

(cont’d)

– less frequent in Canada except top-tier banks and insurance companies are almost 100%

now

– typical 2 or 3-year look back

11

Three Major Categories of Clawbacks

• Bad faith (including breach of non-

compete)

• Fraud, negligence or intentional

misconduct resulting in a financial result revision

• Any restatement of financial results

(growing in prevalence)

12

Three Major Categories of Clawbacks (cont’d)

Paper includes 9 examples of U.S. and

Canadian clawback provisions in 2011 proxies

5

13

Canadian Taxation

• Clawback in current year poses no

difficulty

• Clawback in later year creates problems

due to section 8 of Income Tax Act(Canada)

14

Potential Tax Relief forLater Year Clawbacks

• Filing an Amended Tax Return– Armstrong - CRA discretion

15

Potential Tax Relief forLater Year Clawbacks (cont’d)

• Mistake– “If the parties base their contract on a fundamental

error about the assumptions supporting their agreement, and neither party agrees to bear the risk of the assumption turning out be false, the contract can be held void on the basis of the doctrine of common-law mistake.”

– procedural and jurisdictional hurdles - Fradette

6

16

Potential Tax Relief forLater Year Clawbacks (cont’d)

• Remission– “The Governor in Council may, on the

recommendation of the appropriate Minister, remit any tax or penalty, including any interest paid or payable thereon, where the Governor in Council considers that the collection of the tax or the enforcement of the penalty is unreasonable or unjust or that it is otherwise in the public interest to remit the tax or penalty”

– no public record of such a remission order having ever been granted in the case of a clawback

17

Potential Tax Relief forLater Year Clawbacks (cont’d)

• Unjust enrichment

– enrichment without juristic reason

18

Potential Tax Relief forLater Year Clawbacks (cont’d)

• Rectification– “In order for a party to succeed on a plea of

rectification, he must satisfy the Court that the parties, all of them, were in complete agreement as to the terms of their contract but wrote them down incorrectly. It is not a question of the Court being asked to speculate about the parties’ intention, but rather to make an inquiry to determine whether the written agreement properly records the intention of the parties as clearly revealed in their prior agreement.”

7

19

Design Alternatives to Avoid Adverse

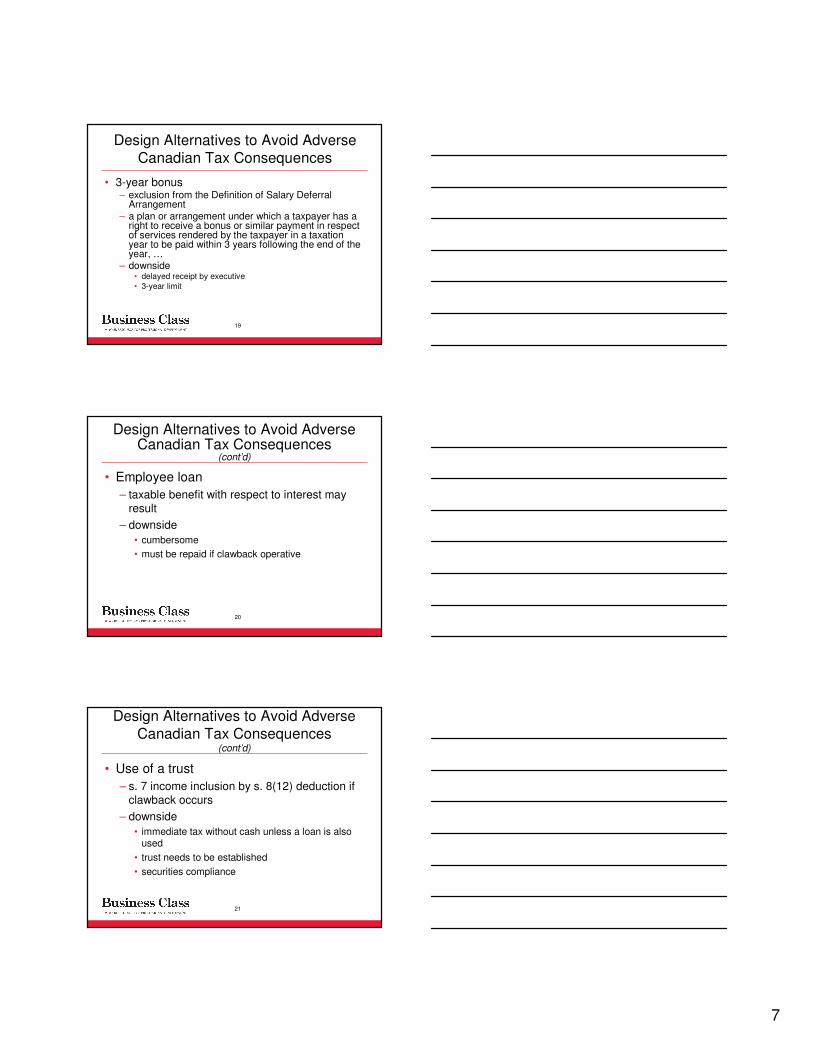

Canadian Tax Consequences

• 3-year bonus– exclusion from the Definition of Salary Deferral

Arrangement– a plan or arrangement under which a taxpayer has a

right to receive a bonus or similar payment in respect of services rendered by the taxpayer in a taxation year to be paid within 3 years following the end of the year, …

– downside• delayed receipt by executive

• 3-year limit

20

Design Alternatives to Avoid Adverse Canadian Tax Consequences

(cont’d)

• Employee loan

– taxable benefit with respect to interest may result

– downside

• cumbersome

• must be repaid if clawback operative

21

Design Alternatives to Avoid Adverse

Canadian Tax Consequences(cont’d)

• Use of a trust

– s. 7 income inclusion by s. 8(12) deduction if clawback occurs

– downside

• immediate tax without cash unless a loan is also used

• trust needs to be established

• securities compliance

8

22

Conclusion

• Clawbacks in Canada seem to be growing

in prevalence and scope

• Canadian tax result likely to be harsh

unless there is planning at the time of the relevant award

Long Term Incentive Plan Clawbacks:

Design, Tax and Other Legal Issues

Kathryn Bush

Partner

416.863.2633

Blake, Cassels & Graydon LLP

Barristers, Solicitors

199 Bay Street

Suite 4000, Commerce Court West

Toronto, ON Canada

M5L 1A9

www.blakes.com

Long Term Incentive Plan Clawbacks: Design, Tax and

Other Legal Issues

Kathryn Bush, Blake, Cassels & Graydon LLP

1. INTRODUCTION

In recent years, particularly since the global financial crisis, the use of clawback

provisions in executive compensation plans has become more widespread in Canada.

Basically, clawbacks are arrangements under which an employee’s compensation that

has previously been awarded is forfeited or ‘clawed back’. Canadian public companies

listed in the United States are subject to statutory clawbacks for certain employees. As

well, certain Canadian financial institutions regulated by the Office of the Superintendent

of Financial Institutions (“OSFI”) have adopted clawbacks as an OSFI-recommended

best practice. Other Canadian public companies are not required to adopt clawbacks,

but may choose to do so by agreement with affected employees. The increasing use of

these provisions in Canadian employment contracts raises a series of interesting and

potentially difficult issues that should be kept in mind when designing executive

incentive plans. A potentially problematic example is the income tax consequences of

compensation clawbacks in the context of the Canadian income tax laws. As will be

discussed, the potentially harsh tax treatment of the clawed back amounts in Canada is

an added layer of complexity that should be taken into account, particularly when using

existing U.S. policies as a source for drafting Canadian clawback provisions.

As explained in the Blakes Bulletin “Clawbacks Coming to Canada”, clawback

provisions can take a variety of forms and be triggered by different types of events.1

They may apply to vested and unvested awards, affecting different forms of

compensation from annual bonuses to long term incentive awards of equity and non-

The author acknowledges the assistance in the preparation of this paper of Atbin Dezfuli, Articling

Student.

- 2 -

equity compensation. Triggers range from fraudulent misconduct to bad faith behaviour

and even the mere occurrence of a negative restatement of financial results.

2. U.S. STATUTORY CLAWBACKS

Specific types of clawbacks are statutorily mandated under the U.S. Sarbanes-Oxley

Act of 2002 (“SOX”), and Dodd-Frank Wall Street Reform and Consumer Protection Act

(“DFW”). These measures are relevant for Canadian corporations which are foreign

private issuers under U.S. securities laws. These provisions are also of more general

interest since the concepts introduced and developed in the U.S. statutory clawbacks

are widely adopted by both US and Canadian issuers in drafting their contractual

clawback policies.

The clawback provisions in SOX adopted the basic notion, incorporated in most current

clawback policies, that executive bonuses based on materially inaccurate financial

results that are subsequently subject to a negative revision should be forfeited. The

forfeiture, or clawback, is conditioned on a finding of executive misconduct that has

resulted in the material non-compliance in the financial results. These provisions apply

to any incentive payments, covering both cash and equity awards, in the one-year

period following the issue of the financial results that later had to be restated. The

clawback is mandatory for U.S. public companies but only applies to the CEO and the

CFO. However, the misconduct required to trigger the provision is not required to be

that of the CEO or the CFO.2

The DFW introduced ‘bigger and better’ clawbacks that apply in a wider set of

circumstances to a wider base of employees. Under these provisions, any material

non-compliance with reporting requirements that necessitates a restatement of financial

results triggers a clawback mechanism that applies to incentive awards received by all

current or former executives. There is a three year look-back period, which means that

incentive awards handed out during the three years preceding the date of restatement

1 J. Tuzyk, Blakes Bulletin on Securities “Clawbacks Coming to Canada?”, November 2011, available at

http://www.blakes.com/english/view_bulletin.asp?ID=5026

- 3 -

are subject to recoupment. It is significant to note the absolute-liability nature of these

provisions in that there is no misconduct requirement for the DFW clawbacks to be

triggered.

DFW measures apply in addition to the already in place SOX provisions discussed

above, yet they are in one aspect narrower: DFW clawbacks only apply to the excessive

portion of the award that was received by the executive based on inaccurate financial

results, whereas, under the SOX, the entire payment may be subject to forfeiture. This

is probably an appropriate policy choice in light of the no-fault nature of DFW

clawbacks. Also unlike SOX, which tasks the SEC with enforcing the clawbacks by

litigation, the DFW provisions are required to be enforced by the issuer, who should

disclose its policies for doing so as part of its securities reporting requirements.3

3. FINANCIAL STABILITY BOARD (“FSB”) PRINCIPLES AND CANADIAN

ADVISORY POLICIES

The FSB is an international organization co-ordinating national financial authorities of

countries such as the U.S., and Canada. Bank of Canada, OSFI and the Federal

Ministry of Finance are members of FSB, which has issued FSB Principles for Sound

Compensation Practices – Implementation Standards. The Principles espouse the

basic notion that executive incentives based on inaccurate financial results that are

subsequently subject to downward revision should trigger some form of recoupment or

clawback mechanism. Further, unvested portions of deferred compensation should also

be clawed back based on the actual performance of the business in the year of vesting.

There are no regulatory or statutorily mandated clawbacks in Canada. However,

Canadian issuers which are subject to SEC listing requirements are subject to clawback

provisions, and clawbacks following the general guidelines of FSB Principles are

recommended by OSFI as a best practice to the Canadian financial institutions that it

2 Ibid

3 Ibid

- 4 -

regulates. As the OSFI-regulated entities are not subject to a specific legislative

provision in this regard, there is no prescribed form of clawback as in the U.S.4

4. CONTRACTUAL CLAWBACKS IN CANADA AND THE U.S.

The Canadian clawback is therefore primarily a contractual measure. In drafting

contractual provisions, Canadian companies have tended to follow the U.S. precedent,

which has a longer and more established history of using such provisions. The

historical use of U.S. contractual clawbacks has been directed at executive misconduct

or bad behaviour, a common example being situations where employees left to join

competitors.

Following the example of U.S. lawmakers, however, clawback provisions are

increasingly being used to address a much more far reaching set of issues, going

beyond ‘bad behaviour’ to include absolute liability-type situations where a negative

restatement leads to disgorgement regardless of executive fault. This signals a new

understanding of clawbacks as a risk-management mechanism and more generally a

“corporate governance tool to deter management from taking actions that could

potentially harm the company’s financial position”.5

5. TYPES AND RELATIVE PREVALENCE OF CLAWBACKS IN U.S. AND

CANADA

According to the HayGroup report, a survey conducted over 450 US public companies

with revenues over $4 billion showed (i) more than half of them adopting some form of

clawback; (ii) this figure is at 82% for Fortune 100 companies; (iii) clawbacks are

applied to annual incentives as well as unexercised stock options and restricted

stock/share units (RS/RSU), (iv) clawbacks are a much less frequent sight in Canada

overall, apart from top tier banks and insurance companies which have been almost

unanimous in adopting some form of recoupment policy since 2009, and (v) as in the

4 supra note 1

5 HayGroup, Executive Briefing—Canada, Issue 1, March 2011

- 5 -

U.S., a wide range of incentives are subject to disgorgement in Canada, with a typical

look-back period of two to three years.6

Clawback provisions have been commonly categorized into the following three major

categories:

(1) the first category covers “bad faith” conduct which includes the breach of

non-compete policies, and more generally conduct that is not in good faith

and goes against the best interests of the company.

(2) The second major category covers fraud, negligence or intentional

misconduct, where the employee has unearned income as a result of

fraudulent or negligent conduct leading to financial results that need to be

revised at a later point.

(3) The third major categories are clawbacks that are triggered directly by a

restatement of financial results, with no need for the company to show a

causal link between the negative revision and employee misconduct.

Companies may adopt a combination or all of these measures in their clawback

policies, and the following examples will demonstrate that companies may adopt

language that is not clearly caught by these categories. Overall, it seems however, that

the inclusion of strict restatement clawbacks is increasingly common, particularly in

Canadian entities that adopt such provisions.

6 Ibid

- 6 -

6. EXAMPLES OF U.S. AND CANADIAN CLAWBACK PROVISIONS IN

2011 PROXIES

(a) U.S. Public Issuers Clawbacks; DEF 14A forms available on EDGAR

(i) General Motors Company

GMC’s initial clawback policy was adopted in response to TARP measures and covered

fraud, negligence and intentional misconduct. More recently, the board has

expanded the recoupment policy to cover material inaccuracy in financial statements,

applying to any SEO and the next top 20 earners of the company. The policy however

adds a knowledge condition for recoupment which separates it from the absolute-liability

type provisions:

“Recoupment Policy on Incentive Compensation

On September 8, 2009, our Board reaffirmed and expanded our policy regarding the

recoupment of incentive compensation paid to executive officers in situations involving

financial restatement due to employee fraud, negligence, or intentional misconduct and

posted it on our website, www.gm.com/investors, consistent with the requirements for

TARP recipients. Our recoupment policy now provides that if our Board or an

appropriate committee thereof has determined that any bonus, retention award, or

incentive compensation has been paid to any SEO or any of the next 20 most highly

compensated employees of the Company based on materially inaccurate misstatement

of earnings, revenues, gains, or other criteria, the Board or Compensation Committee

shall take, in its discretion, such action as it deems necessary to recover the

compensation paid, remedy the misconduct, and prevent its recurrence. For this

purpose, a financial statement or performance metric shall be treated as

materially inaccurate with respect to any employee who knowingly engaged in

providing inaccurate information or knowingly failed to timely correct information

relating to those financial statements or performance metrics. We will continue to

- 7 -

review our policy to assure that it is consistent with evolving best practices and SEC

and NYSE requirements.”7

(ii) CISCO Systems, Inc.

Clawbacks in CISCO are limited to the cash incentives for restatement triggered

provisions, going back to July, 2007. The proxy however also mentions possible

forfeiture of equity awards for detrimental activities and termination for misconduct:

“Since March 2008, Cisco has maintained a recoupment policy for cash incentive

awards paid to executive officers under Cisco’s annual cash incentive plan, the EIP. In

the event of a restatement of incorrect financial results, this policy would enable the

Compensation Committee, if it determined appropriate and subject to applicable laws, to

seek reimbursement of the incremental portion of EIP awards paid to executive officers

in excess of the awards that would have been paid based on the restated financial

results. This policy also was applied to the discretionary cash incentive awards paid to

executive officers for fiscal 2009. Cisco’s variable cash incentive and long-term, equity-

based incentive award plans also generally provide for forfeiture if a named executive

officer participates in activities detrimental to Cisco or is terminated for misconduct.”8

“Cisco has adopted a senior executive compensation recoupment policy. This policy is:

In the event of a restatement of incorrect financial results, the Compensation and

Management Development Committee (the “Compensation Committee”) will review all

cash incentive awards under the Executive Incentive Plan (“bonuses”) that were paid to

executive officers (within the meaning of Rule 3b-7 of the Securities Exchange Act of

1934, as amended) for performance periods beginning after July 28, 2007 which occur

during the restatement period. If any such bonus would have been lower had the

level of achievement of applicable financial performance goals been calculated

based on such restated financial results, the Compensation Committee will, if it

determines appropriate in its sole discretion, to the extent permitted by governing

7 DEF 14A filed 2011-04-21

- 8 -

law, require the reimbursement of the incremental portion of the bonus in excess

of the bonus that would have been paid based on the restated financial results.”9

(iii) Dell Inc.

Dell’s clawback is a straightforward restatement-based policy that applies to all awards

made in the restatement period:

“Recoupment Policy for Performance-Based Compensation

If Dell restates its reported financial results, the Board will review the bonus and other

awards made to the executive officers based on financial results during the period

subject to the restatement, and, to the extent practicable under applicable law, Dell will

seek to recover or cancel any such awards which were awarded as a result of

achieving performance targets that would not have been met under the restated

financial results.”10

(iv) Exxon Mobil Corporation

Exxon’s recoupment policy is a straightforward restatement-triggered clawback that

applies only to cash awards. The look-back period and the employees to whom the

clawback would be applied are not made clear in the proxy:

“The annual bonus and retirement benefits also align the interests of senior executives

with the priority of long-term, sustainable growth in shareholder value. Specifically, 50

percent of the annual bonus payout is delayed based on earnings performance, as

described in the CD&A, and the entire annual bonus is subject to recoupment. In

addition, pension values are highly dependent on executives remaining with the

Company for a career and performing at the highest levels.

(...)

8 DEF 14A filed 2011-10-18

9 available at http://investor.cisco.com/contacts.cfm

10 DEF 14A filed 2011-05-26

- 9 -

Cash and Earnings Bonus Unit payments are subject to recoupment in the event

of material negative restatement of the Corporation’s reported financial or

operating results. Even though a restatement is unlikely given ExxonMobil’s high

ethical standards and strict compliance with accounting and other regulations applicable

to public companies, a recoupment policy was approved by the Board of Directors to

reinforce the well-understood philosophy that incentive awards are at risk of forfeiture

and that how we achieve results is as important as the actual results.”11

(v) Qwest Communications International Inc

Qwest’s restatement clawback, adopted in 2005, applies to performance based awards

made in the restatement period to executives:

“Our Board has adopted a policy whereby, in the event of a substantial restatement of

previously issued financial statements, our Board will review all performance-based

compensation awarded to executives that is attributable to performance during the time

periods restated. Our Board will determine whether the restated results would have

resulted in the same performance-based compensation for the executives. If not, the

Board will consider:

Whether the restatement was the result of executive misconduct;

the amount of additional executive compensation paid as a result of the previously

issued financial statements;

our best interests in the circumstances; and

any other legal or other facts or circumstances our Board deems appropriate for

consideration in the exercise of its fiduciary obligations to us and our shareholders.

If our Board then deems that an executive was improperly compensated as the

result of the restatement and that it is in our best interests to recover the

11

DEF 14A filed 2011-04-13

- 10 -

performance-based compensation paid to that executive, our Board will pursue

all reasonable legal remedies to recover that performance-based compensation.

We have not been required to take any action under this policy since its adoption in

January 2005.”12

(b) Canada; Proxies available on SEDAR

(i) Brookfield Asset Management Inc.

Members of Brookfield’s management committee are subject to clawbacks upon the

occurrence of ‘certain events’. A material restatement leads to clawbacks for only the

CEO and CFO. Other members of the management committee are subject to

clawbacks for materially detrimental conduct after leaving the company, including

breach of confidentiality agreements and defamation. The look-back period is two

years:

“Reimbursement of Incentive and Equity-Based Compensation Specified executives,

including all members of the Management Committee, are required to pay to the

Corporation an amount equal to some or all of any Bonus or other incentive-based or

equity-based compensation and the profits realized from the sale of securities of the

Corporation upon the occurrence of certain events. The amount, if any, will be

determined by the Compensation Committee which will recommend appropriate action

to the Board and will take appropriate steps to ensure that such amount is recovered. In

the case of a significant restatement of financial results, the Chief Executive

Officer and the Chief Financial Officer may be required to make such a payment.

In order to protect the Corporation’s reputation and competitive ability, members

of the Management Committee may be required to make such a payment if they

engage in conduct that is materially detrimental to the Corporation after the

cessation of their employment with the Corporation. Detrimental conduct includes

participating in transactions involving the Corporation and its clients which were

12

DEF 14A filed 10-03-17

- 11 -

underway or contemplated at the time of termination, solicitation of clients or

employees, disclosing confidential information or making inappropriate or defamatory

comments about the Corporation or its clients. The policy relates to any amounts or

benefits received within two years prior to the event giving rise to the claim and includes

both monetary payments and shares received from exercise of options or redemption of

RSUs and DSUs.”13

(ii) Nexen Inc.

A material restatement of financial results may lead to clawback but only “as required by

law”, and not as a contractual measure. Nexen identifies barriers in Canada for formally

enacting US-type clawbacks, including employment, taxation, and enforcement issues.

“Reimbursement

If, as a result of wilful misconduct, Nexen’s performance results were restated in

a way that would have resulted in lower incentive awards, the CEO and CFO

would reimburse Nexen proportionately as required by law. While Nexen is aligned

and committed to the US model for clawbacks, we are monitoring the development of

proposed US requirements and are consulting with industry leaders and shareholder

advisory groups to better understand the development of clawback policy models in

Canada. Identified barriers to implementation include employment law, enforcement

and tax issues. Nexen is working on a more formal solution that effectively addresses

alignment of shareholder and executive interests by ensuring that compensation is not

increased as a result of wilful misconduct.”14

(iii) Royal Bank of Canada

RBC uses explicit risk-control language that goes beyond financial results to cover

inappropriate or extreme risk-taking behaviour. The policy is applied to a wide range of

13

Proxy filed March 28, 2011 14

Proxy filed March 25, 2011

- 12 -

executives, and includes a financial restatement trigger as well as a broader misconduct

trigger covering any failure to follow internal policies and procedures:

“Addresses situations in which individuals might profit from business activities

that are conducted inappropriately or outside of approved risk limits and

tolerances, or from financial results, financial reporting or financial statements

that are erroneous or misstated.

Applicability

The CEO, members of the Group Executive, all executives of RBC and Capital Markets

employees who participate in the RBC Capital Markets Compensation Program. Under

the policy, the financial restatement trigger applies to the CEO and the CAO and CFO,

and all other members of the Group Executive.

Key features

• Allows RBC to recoup incentive awards that have been paid or vested and

cancel unvested mid and long-term incentive awards in the event of

misconduct, including failure to follow internal policies and procedures.

• A financial restatement trigger permits RBC to recoup incentive awards that have

been paid or vested and to cancel unvested mid and long-term incentive awards

in excess of the amount that would have been received under the restated

financial statements, subject to the board’s discretion.

• Additionally, performance-based incentive programs at RBC include provisions

that would revoke certain awards to the CEO, members of the Group Executive,

and other participants if their employment is terminated for cause. In the event of

termination for cause and consistent with the law of the jurisdictions in which we

- 13 -

operate, the terminated participant would forfeit all previously awarded unvested

mid and long-term incentive awards.”15

(iv) Sun Life Financial Inc.

The clawback here applies to all employees, disgorging incentive payments made under

inaccurate financial results with a two year look-back. Interestingly, the policy, adopted

in 2010, includes instances of omission such as any failure to report or take action to

stop misconduct of another employee that an employee knew, or ought to have known,

about:

“New clawback provision for all employees

The board adopted a new clawback provision that allows it to recoup incentive

compensation if an incidence of misconduct led to an overpayment of incentive

compensation. This new provision is consistent with emerging competitive practice

and regulatory principles.

Clawbacks

Our CEO and CFO are required by law to reimburse their incentive compensation if

there is an incidence of misconduct and we need to restate our financial statements. In

2010 the board approved a new clawback policy, allowing it to demand that former or

current employees pay back any or all of the incentive the compensation they received

or realized in the previous 24 months if: employee was involved in misconduct (such as

fraud, dishonesty, negligence or non-compliance with legal requirements or Sun Life

Financial’s policies, any other act or omission that would justify termination of

employment for cause, and any failure to report or take action to stop misconduct of

another employee that an employee knew, or ought to have known, about), and the

15

Proxy filed February 6, 2012

- 14 -

misconduct directly or indirectly resulted in the employee receiving or realizing a higher

amount of incentive or deferred compensation.”16

CANADIAN TAXATION

From the Canadian tax perspective, a clawback occurring in the same taxation year as

the receipt of the compensation should pose no difficulty. The employer and employee

can adjust the compensation and the related source deductions, prior to making the

required tax filings in respect of the year. The difficulty arises when the clawback

occurs in a subsequent year.

Limitations of Section 8 of the Income Tax Act

The difficulty stems from subsection 8(2) of the Income Tax Act, (Canada) (the “Act”)

which reads as follows:

Except as permitted by this section, no deductions shall be

made in computing a taxpayer’s income for a taxation year

from an office or employment.

The balance of section 8 of the Act provides for a number of express deductions in

computing income from employment, including deductions for:

• the reimbursement of amounts included in income for periods during

which no services were rendered (8(1) (n)).

• amounts previously included in income but forfeited under a salary

deferral arrangement; (8(1) (o)) and

• expenses incurred by employees engaged in the selling of property or

negotiating of contracts, which deduction may provide relief in respect of a

clawback in limited circumstances. (8(1) (f)). (See CRA Document 2004-

0103391E5, where a commission salesperson was unable to make full

16

Proxy filed March 29, 2011

- 15 -

use of the provision where amounts had to be repaid to his former

employer.)

None of the deductions set out in section 8 expressly covers the scenario where a

reimbursement or forfeiture of a bonus is required.

Accordingly, relief would have to be sought elsewhere.

Filing an Amended Tax Return

The taxpayer subject to a clawback could simply file an amended return for the year in

which the bonus was received. However, there is no general, statutory right to file an

amended return as established in Armstrong v. The Queen, 2006 DTC 6310 (FCA).

While the Act contains specific provisions that permit or mandate the filing of an

amended return in specific circumstances, (See, for example, paragraph 164(6) (e),

regarding the carry back of losses to a deceased’s terminal year.) No provision

expressly permits an employee to do so in the case of a clawback.

Accordingly, relief would depend on the discretion of the Canada Revenue Agency

(“CRA”) to assess on the basis of the amended return.

The Law of Mistake

A taxpayer may argue that the prior income inclusion ought to be reversed on the basis

of a mistake of fact which rendered the agreement to pay the bonus void. A clawback

would not seem to meet the Canadian definition of a mistake:

“If the parties base their contract on a fundamental error about the assumptions

supporting their agreement, and neither party agrees to bear the risk of the assumption

turning out be false, the contact can be held void on the basis of the doctrine of

common-law mistake.”17

17

Bell v. Lever Bros. Ltd., [1932] A.C. 161, [1931] All E.R. Rep. 1 (H.L.).

- 16 -

Even if the clawback could meet the test of a mistake under Canadian law, which

seems very unlikely, the taxpayer would have to navigate the procedural and

jurisdictional hurdles.

In Fradette v. The Queen, [20] the taxpayer mistakenly received approximately $26,000

from a provincial pension commission over a period of years, which was included in the

taxpayer’s income and subject to provincial and federal income tax. When the payer

discovered the error years later, it required the taxpayer to repay the sums paid in error,

which the taxpayer did.

While Revenue Quebec agreed to reimburse the taxpayer for the provincial tax paid on

the repaid amount, the CRA did not so agree, and issued a nil assessment for the year

of the final repayment. The taxpayer’s appeal to the Court was met with the Crown’s

motion to dismiss on the basis that no appeal lies from a nil assessment. The Crown’s

motion was successful. However, Mr. Justice Tardif made the following comments:

This is a very special case which causes one to have great

sympathy for the appellant, who must bear unaided the

consequences of a mistake in which he had no part.

Unfortunately, I have no jurisdiction to correct this injustice

except that I would like to think that Parliament had such a

situation in mind when it adopted the [Financial

Administration Act].

Remission

Remission orders are extraordinary measures that provide for complete or partial relief

from taxes, interest or penalties. Remission orders are granted by the Governor

General in Council, under the authority of subsection 23(2) of the Financial

Administration Act:

The Governor in Council may, on the recommendation of the

appropriate Minister, remit any tax or penalty, including any

- 17 -

interest paid or payable thereon, where the Governor in

Council considers that the collection of the tax or the

enforcement of the penalty is unreasonable or unjust or that

it is otherwise in the public interest to remit the tax or

penalty.

A remission order must be sponsored internally by the CRA and the procedure is time-

consuming. The CRA will generally require evidence of extreme hardship or incorrect

action or advice from the CRA that led to additional tax. There is no public record of a

remission order ever been provided in the case of a clawback.

Unjust Enrichment

Unjust enrichment is another remedy that might be considered. This equitable remedy

requires an enrichment of one party, a corresponding deprivation of another, and the

absence of any juristic reason for the enrichment. The remedy has been raised by

taxpayers in a number of cases, with mixed results.

One difficulty in raising the remedy is that it will often conflict with the legislation on

which the particular assessment is based. In the British Columbia Ferry Corp. v.

M.N.R., [2000] FCJ 227 F.C.T.D. in which the plaintiff sought a determination of whether

it had overpaid taxes on fuel oil, the Court concluded that the Excise Tax Act constituted

a complete code and excluded any equitable remedy that might otherwise have been

available.

Another difficulty with the remedy in the case of a clawback is that there may arguably

be a juristic reason for the enrichment and deprivation, namely the operation of the Act

as it applies to the receipt of employment income in a particular taxation year.

- 18 -

Rectification

Rectification is another equitable remedy that has been used by taxpayers in a number

of tax cases. In H.F. Clarke Ltd. v. Thermidaire Corp. Ltd., [1937] 2 OR 57, at 64-65

(C.A.) the doctrine of rectification was described as follows:

In order for a party to succeed on a plea of rectification, he

must satisfy the Court that the parties, all of them, were in

complete agreement as to the terms of their contract but

wrote them down incorrectly. It is not a question of the Court

being asked to speculate about the parties’ intention, but

rather to make an inquiry to determine whether the written

agreement properly records the intention of the parties as

clearly revealed in their prior agreement.

As rectification requires an error in the recording of an agreement, it would appear this

would be of little use in the case of a clawback.

DESIGN

Based on the above, there does not appear to be a clear and certain way in which the

negative tax impact of a clawback may be reversed. The following are some methods

by which a clawback could be structured to take advantage of existing tax rules.

(a) Three-Year Bonus

An exception to the salary deferral arrangement definition in paragraph 248(1)(k)

permits a bonus for services rendered in a year to be deferred for three years:

“salary deferral arrangement”, in respect of a taxpayer,

means a plan or arrangement, whether funded or not, under

which any person has a right in a taxation year to receive an

amount after the year where it is reasonable to consider that

one of the main purposes for the creation or existence of the

- 19 -

right is to postpone tax payable under this Act by the

taxpayer in respect of an amount that is, or is on account or

in lieu of, salary or wages of the taxpayer for services

rendered by the taxpayer in the year or a preceding taxation

year (including such a right that is subject to one or more

conditions unless there is a substantial risk that any one of

those conditions will not be satisfied), but does not include ...

a plan or arrangement under which a taxpayer has a right to

receive a bonus or similar payment in respect of services

rendered by the taxpayer in a taxation year to be paid within

3 years following the end of the year, ...

The deferred bonus may be subject to conditions during the deferral period, which could

include the absence of a financial restatement or wrongdoing. If such a condition

materialized, the bonus would not be paid and there would never have been an income

inclusion to reverse. Of course, the downside is that the employee does not have

access to the bonus amount during the deferral period. Further, under this approach,

the clawback period would have to be restricted to three years and the particular three

years drafted carefully. Nevertheless, this is likely the easiest way to implement a tax-

neutral clawback under the current state of the law.

(b) Employee Loan

The employer and the employee could agree to arrange a loan, equal to the amount of

the bonus, for a term equal to the duration of the desired clawback regime. During the