strategies for mergers and acquisitions - … for mergers and acquisitions sydney finkelstein tuck...

TRANSCRIPT

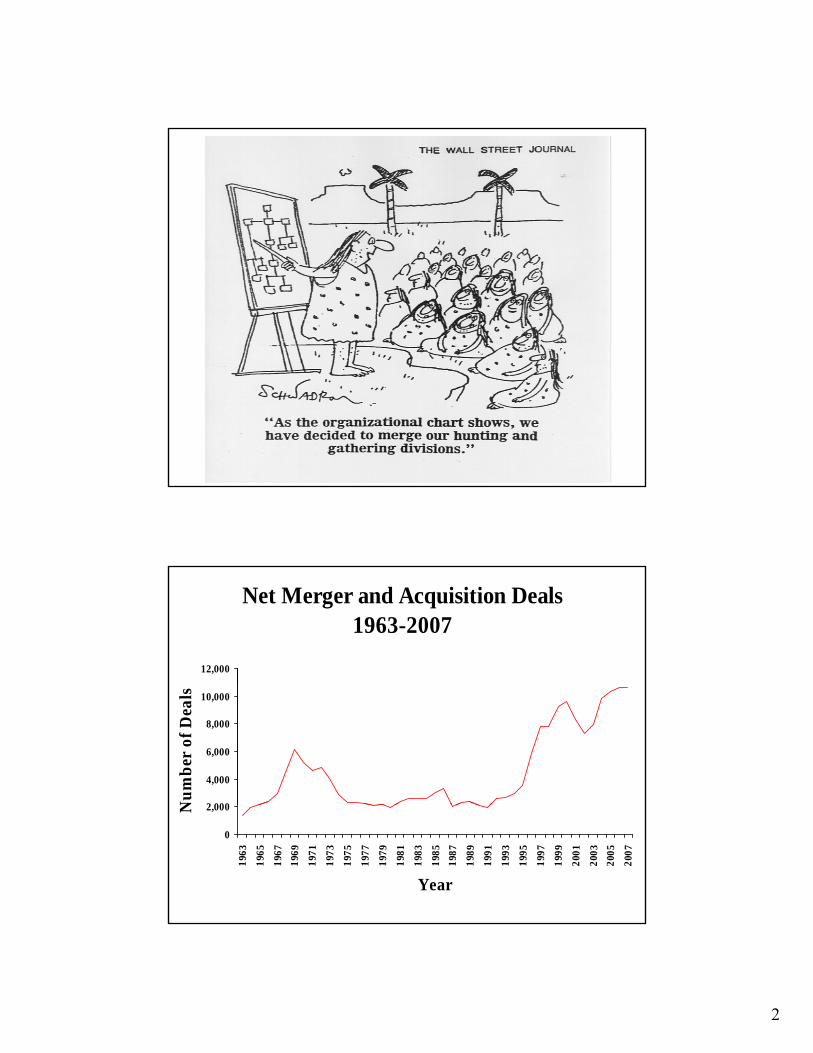

1

Strategies for Mergers and AcquisitionsStrategies for Mergers and Acquisitions

Sydney FinkelsteinSydney FinkelsteinTuck School of Business at DartmouthTuck School of Business at Dartmouth

Telephone: (603) 646Telephone: (603) 646--28642864Fax: (603) 646Fax: (603) 646--13081308

[email protected]@dartmouth.edusyd ey. e s e @d ou .edusyd ey. e s e @d ou .eduwww.tuck.dartmouth.edu/thinkagainwww.tuck.dartmouth.edu/thinkagain

2

Net Merger and Acquisition Deals 1963-2007

12,000

2 000

4,000

6,000

8,000

10,000

Num

ber

of D

eals

0

2,000

1963

1965

1967

196 9

197 1

1973

1975

1977

1979

1981

1983

1985

198 7

198 9

199 1

199 3

199 5

199 7

199 9

200 1

200 3

2 005

2 007

Year

N

3

Inflation-Adjustment Dollar Value of M&As (Year 2007 Billions of Dollars)

400

600

800

1000

1200

1400

1600

0

200

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Year

A GoodA Good--Looking Merger Doesn’t Guarantee Great ResultsLooking Merger Doesn’t Guarantee Great Results

4

Stock price of acquirers from 1997Stock price of acquirers from 1997--99 trailed S&P 500 by 14 percentage 99 trailed S&P 500 by 14 percentage points, peer group by 4 points, after deals were announcedpoints, peer group by 4 points, after deals were announced

--Salomon Smith BarneySalomon Smith Barney

Over ten years only 23% of mergers recover the costs incurred in the dealOver ten years only 23% of mergers recover the costs incurred in the deal

ARE M&As PROFITABLE?

Over ten years, only 23% of mergers recover the costs incurred in the deal.Over ten years, only 23% of mergers recover the costs incurred in the deal.--McKinsey & Co.McKinsey & Co.

For M & As completed between 1994For M & As completed between 1994--97, average acquirer’s stock was 97, average acquirer’s stock was 3.7% lower than its industry peer group one year after the deal.3.7% lower than its industry peer group one year after the deal.

--PricewaterhouseCoopers LLPPricewaterhouseCoopers LLP

In a study of 700 big deals between 1996In a study of 700 big deals between 1996--98, 83% of M&As did not boost 98, 83% of M&As did not boost shareholder value and 53% actually reduced shareholder valueshareholder value and 53% actually reduced shareholder valueshareholder value, and 53% actually reduced shareholder value.shareholder value, and 53% actually reduced shareholder value.--KPMG InternationalKPMG International

PSIPSI

P x S x IP x S x I

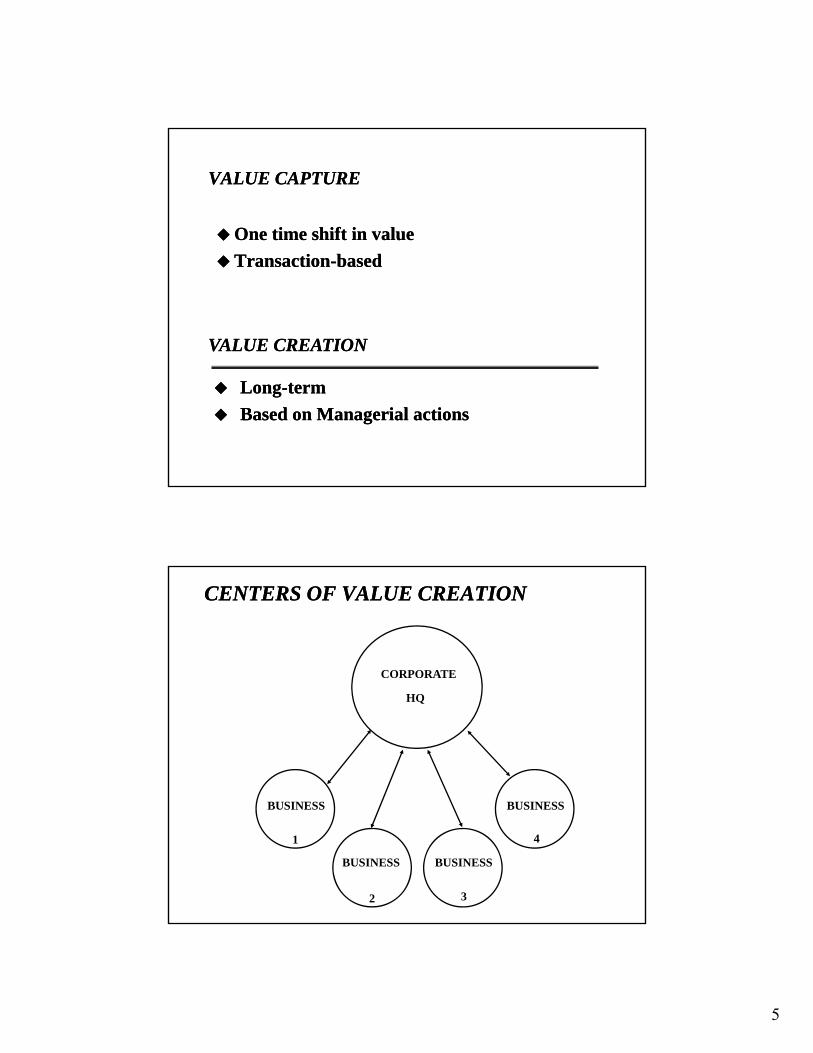

5

VALUE CAPTUREVALUE CAPTURE

One time shift in valueOne time shift in valueTransactionTransaction--basedbased

VALUE CREATIONVALUE CREATION

LongLong--termtermBased on Managerial actionsBased on Managerial actions

CENTERS OF VALUE CREATIONCENTERS OF VALUE CREATION

CORPORATE

HQ

BUSINESS BUSINESSBUSINESS

1

BUSINESS

2

BUSINESS

3

BUSINESS

4

6

The Concept of “Parenting Advantage”The Concept of “Parenting Advantage”

DefinitionDefinition

•• The ability to create more value than any The ability to create more value than any other parent could for the same set of other parent could for the same set of businesses.businesses.TestsTests

•• Aggregate > IndependentAggregate > Independent•• Aggregate > RivalsAggregate > Rivals

Sources of Parenting AdvantageSources of Parenting Advantage

•• Value Creation InsightsValue Creation Insights•• Distinctive Parenting CharacteristicsDistinctive Parenting Characteristics•• Heartland BusinessesHeartland Businesses

7

Value Creation OpportunitiesValue Creation Opportunities

RevenueRevenue

CostCost

Syne

rgie

sSy

nerg

ies

SimilarSimilar Complementary Complementary RelationshipRelationship

CostCost

Value Creation OpportunitiesValue Creation Opportunities

Market powerCritical massService bigger customersT k t tit

Full product lineBundlingCross-sellingO h

CostCost

RevenueRevenue

Syne

rgie

sSy

nerg

ies Take out a competitor

Lower risk improves CoCPrestige attracts talent

Economies of scaleLower overhead

One-stop shopReputationDistribution for productsLearning opportunities

Lower overheadLower risk improves CoC

SimilarSimilar Complementary Complementary RelationshipRelationship

CostCostBetter capacity utilization Financial discipline

8

How Eaton beats the odds: The Pricing ChallengeHow Eaton beats the odds: The Pricing Challenge

Eaton’s SolutionEaton’s Solution Specific ActionsSpecific Actions

Discount sales synergies significantlyDiscount sales synergies significantly –– hardhard

Disciplined Disciplined Pricing ProcessPricing Process

Discount sales synergies significantlyDiscount sales synergies significantly –– hard hard to predict, easy to overestimateto predict, easy to overestimate

Thoroughly execute cost synergies Thoroughly execute cost synergies ––substantiated through due diligencesubstantiated through due diligence

Corporate Development & Planning Corporate Development & Planning ––reinforces objectivity, “balances” an enthusiastic reinforces objectivity, “balances” an enthusiastic operating teamoperating team

BuyBuy--in & accountability from deal champion in & accountability from deal champion –– a senior person from relevant Group signs off a senior person from relevant Group signs off on the numbers, and accepts the challenge of on the numbers, and accepts the challenge of meeting them (linked to compensation)meeting them (linked to compensation)

Price is what you pay Price is what you pay ––value is what you keep & createvalue is what you keep & create

P iP i V lV lPricePrice ValueValueSeller expectation driven, Seller expectation driven, but ultimately market but ultimately market basedbasedNegotiated exchange of Negotiated exchange of valuevalue

The BThe B--School toolsSchool toolsIn depth understanding In depth understanding of value driversof value driversThorough due diligence, Thorough due diligence, leading to a conservativeleading to a conservative

Affected by one side’s Affected by one side’s position of strength position of strength ––find the winfind the win--win to avoid win to avoid the winner’s cursethe winner’s curse

leading to a conservative leading to a conservative and realistic valuationand realistic valuation

9

Lessons from QuakerLessons from Quaker--SnappleSnapple

• History counts!“We virtually built Gatorade from scratch. We had double-digit growthand an 80% market share despite Coke and Pepsi. People used to say about Coke and Pepsi ‘they will bury you’ but we survived Theyabout Coke and Pepsi – ‘they will bury you’ – but we survived. Theycouldn’t beat us, so they bought us.”

• Beware of negative transferSnapple Gatorade“Image” drink “Fluid replacement product”Quirky marketing of cult drink Classic marketingEntrepreneurial distributors Warehouse system

• Problems in due diligence“[Quaker] just didn’t know our business.”

• Don’t lose tacit knowledge“I was the Executive Vice President in charge of nothing”

Lessons from Sony Pictures EntertainmentLessons from Sony Pictures Entertainment

• History counts!Betamax redux!

• Cultural differences hurtSony Columbia PicturesBuying software Finding a Sugar DaddyJapan HollywoodSony! Big talk – big moneySony! Big talk big money

• Don’t pay too much• Foreign buyers phobia

10

Lessons from Citi TravelersLessons from Citi Travelers

• History counts!Sandy builds empires, and wanted to do it againBut, strategy of cross-selling traditionally not successful

• One stop shoppingCustomers must prefer convenience to price and privacyTop companies tend to be category killers more than

department stores Culture clash between investment/commercialCulture clash between investment/commercial,

insurance/banking, etc.• The “hype” factor• The short, and unhappy, life of Co-CEOs

STANDSTAND--ALONE INFLUENCEALONE INFLUENCE

11

LINKAGE INFLUENCELINKAGE INFLUENCE

12

CENTRALIZED FUNCTIONS AND SERVICESCENTRALIZED FUNCTIONS AND SERVICES

Value Creation (present value)Value Creation (present value) XXXX

VALUE CREATION STATEMENTVALUE CREATION STATEMENT

Less:Less: Cost of realizing synergiesCost of realizing synergies XXXXPremium paidPremium paid XXXXTransaction costsTransaction costs XXXX

Extraordinary ItemsReduction in vulnerability to other competitors XX

Net Value Creation After Acquisition XX

Opportunity cost of buying rather than making XXPresent value of expected change in value of assets over time XX XX

Bottom Line XX

13

“The market, like the Lord, helps those who help “The market, like the Lord, helps those who help themselves But unlike the Lord the market does notthemselves But unlike the Lord the market does notthemselves. But unlike the Lord, the market does not themselves. But unlike the Lord, the market does not forgive those who know not what they do ... a too high forgive those who know not what they do ... a too high purchase price for the stock of an excellent company purchase price for the stock of an excellent company can undo the effects of a subsequent decade of can undo the effects of a subsequent decade of favorable business developments.”favorable business developments.”

——Warren Buffett, Chairman, Berkshire HathawayWarren Buffett, Chairman, Berkshire Hathaway

Critical First StepsCritical First Steps

First payrollFirst payrollFirst payrollFirst payrollBill Walsh Football StrategyBill Walsh Football StrategyIntegration teams and championsIntegration teams and championsSWAT team or personSWAT team or personFind the gems and keep them!Find the gems and keep them!Find the gems and keep them!Find the gems and keep them!CommunicationCommunication

14

Date What Happens Announcement date (Day -60) Acquired company CEO announces acquisition to ( y ) q p y q

her employees. “Welcome to the team” coffee mugs distributed to

employees of acquired company. List of contact names from Cisco, with phone

numbers and email, distributed to employees (often includes Cisco top management contact coordinates as well).

Detailed comparison of benefits package from Cisco and acquired company distributed to employees. Cisco integration people on acquired company Cisco integration people on acquired company premises to answer questions

Day -40 Outsourcing arrangements, if necessary, in place Plan for sales force integration in place Day -30 Job assignments for acquired company employees

in place Closing date (Day 0) New employee IDs and business cards distributed Day 7 Computer system switchover to Cisco

15

Seven Important Lessons on Value Seven Important Lessons on Value Creation in MergersCreation in Mergers1.1. All mergers are different.All mergers are different.2.2. Develop a merger scorecard.Develop a merger scorecard.3.3. Don’t let “deal breakers” disrupt integration.Don’t let “deal breakers” disrupt integration.4.4. All synergies are not created equally.All synergies are not created equally.5.5. Don’t forget about transferring “tribal Don’t forget about transferring “tribal

knowledge” across companies.knowledge” across companies.g pg p6.6. Mergers can create critical stakeholder Mergers can create critical stakeholder

vulnerabilities.vulnerabilities.7.7. People want to be part of a winning organization.People want to be part of a winning organization.

Final Integration Takeaways: Set Yourself Up to Win

♦ If you lose here forget about it!♦ If you lose here, forget about it!♦ Integration depends on strategy♦ No substitute for early agreement on strategic rationale ♦ Make sure to have integration talent on hand and ready♦ Details are the foundation of solid planningp g

16

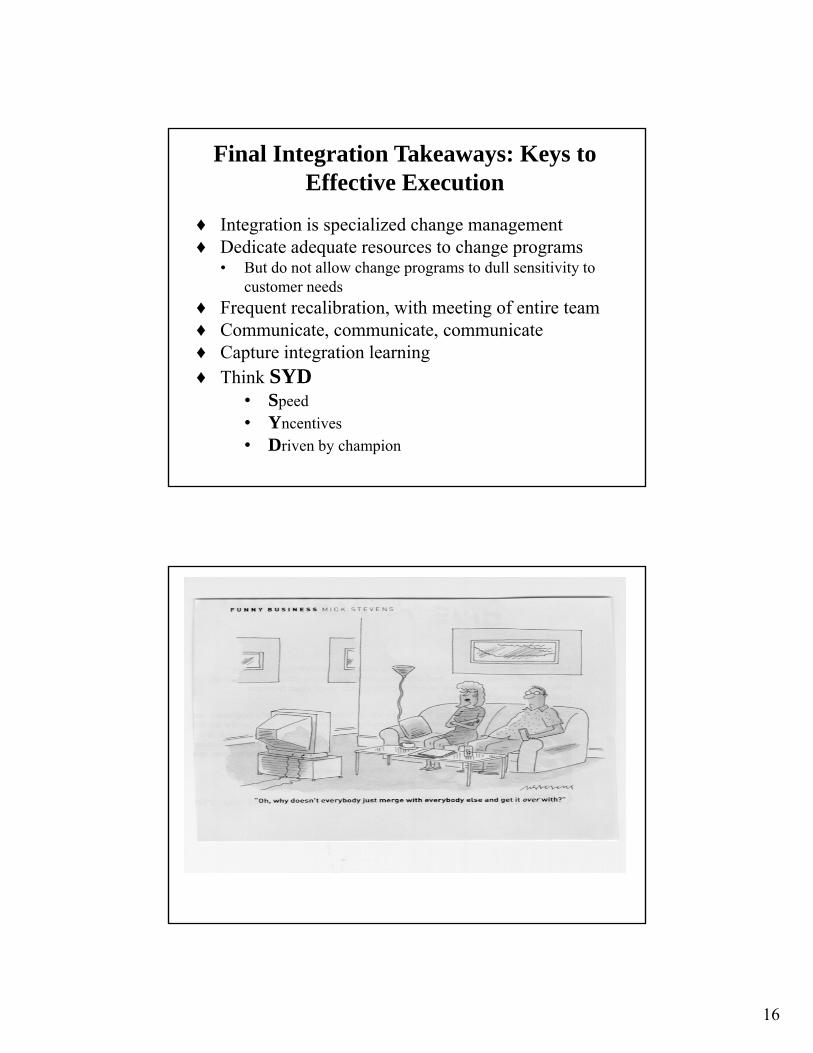

Final Integration Takeaways: Keys to Effective Execution

♦ Integration is specialized change management♦ Dedicate adequate resources to change programs♦ Dedicate adequate resources to change programs

• But do not allow change programs to dull sensitivity to customer needs

♦ Frequent recalibration, with meeting of entire team♦ Communicate, communicate, communicate ♦ Capture integration learning♦ Think SYD

• Speed• Yncentives• Driven by champion