strategy & economy - ambitreports.ambitcapital.com/reports/ambit_strategyeconomy_thematic... ·...

TRANSCRIPT

STRATEGY &ECONOMY

Research Analysts:

India - A Billion Splendid Suns!

Ritika Mankar Mukherjee, [email protected]: +91 22 3043 3175

January 2018

Phase 1: 1965 - 1980 Phase 2: 1980 - 1995

Phase 3: 1995 - 2017 Phase 4: 2017 - ?

Sumit [email protected]: +91 22 3043 3229

Aditi [email protected]: +91 22 3043 3284

ConsultantAnupam [email protected]

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 2

CONTENTS Section 1 of PAGES: Why India made the POLICY choices ………………………7 it did and what happens next?

Policy phase#1: India accords top priority to agriculture ……………………….7 (and unknowingly breaks away from socialism) (FY1965-1980)

Section A: The political backdrop – a country mocked by the world …………………19

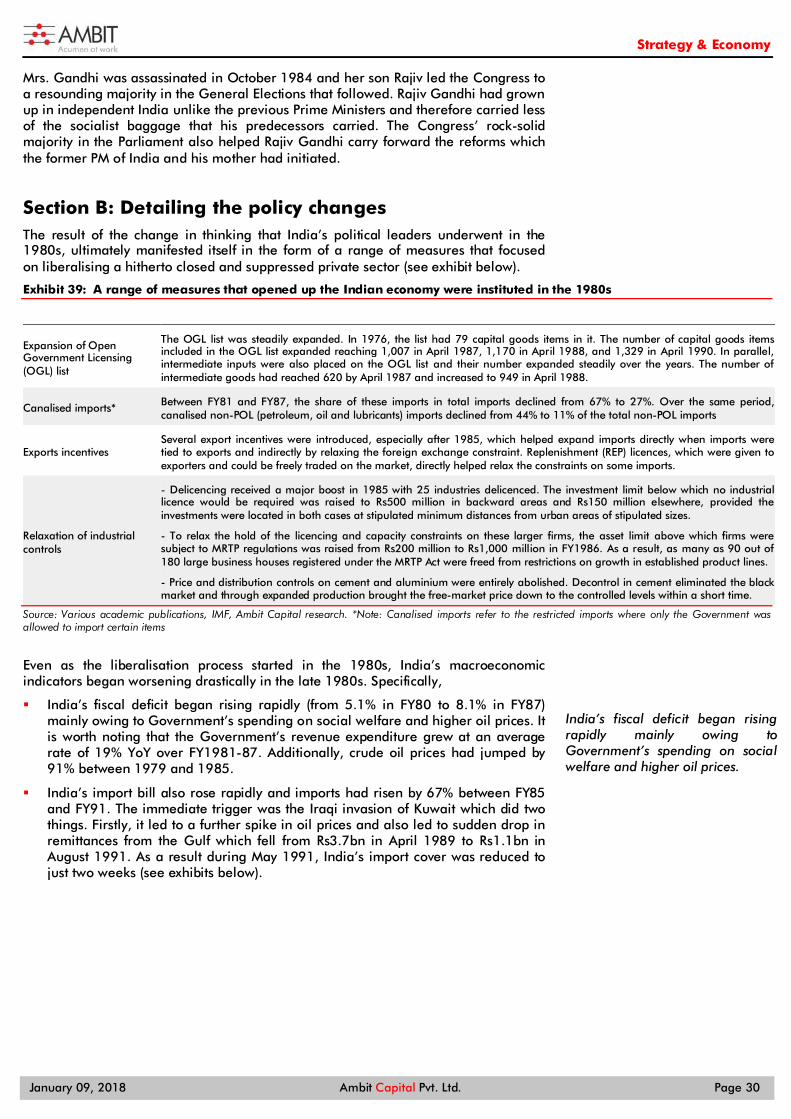

Section B: Detailing the policy changes ………………………………………………….22

Section C: The economic impact - India became self-sufficient on ………………….25 food, inequality reduced but headline GDP growth remained weak

Impact on GDP growth - Whilst farm sector growth picked up, …………………25 non-farm sector growth decelerated!

Impact on inflation - Low oil prices and improvement in food …………………..26 supply lowered inflation

Impact on equality - The reforms of FY1965-80 lowered inequality ……………27

Policy phase#2: From socialism to liberalisation (FY1980-95) ………………27

Section A: The political backdrop – Rising political competition ……………………..28 and the rise of classical liberalism globally

Section B: Detailing the policy changes ………………………………………………….30

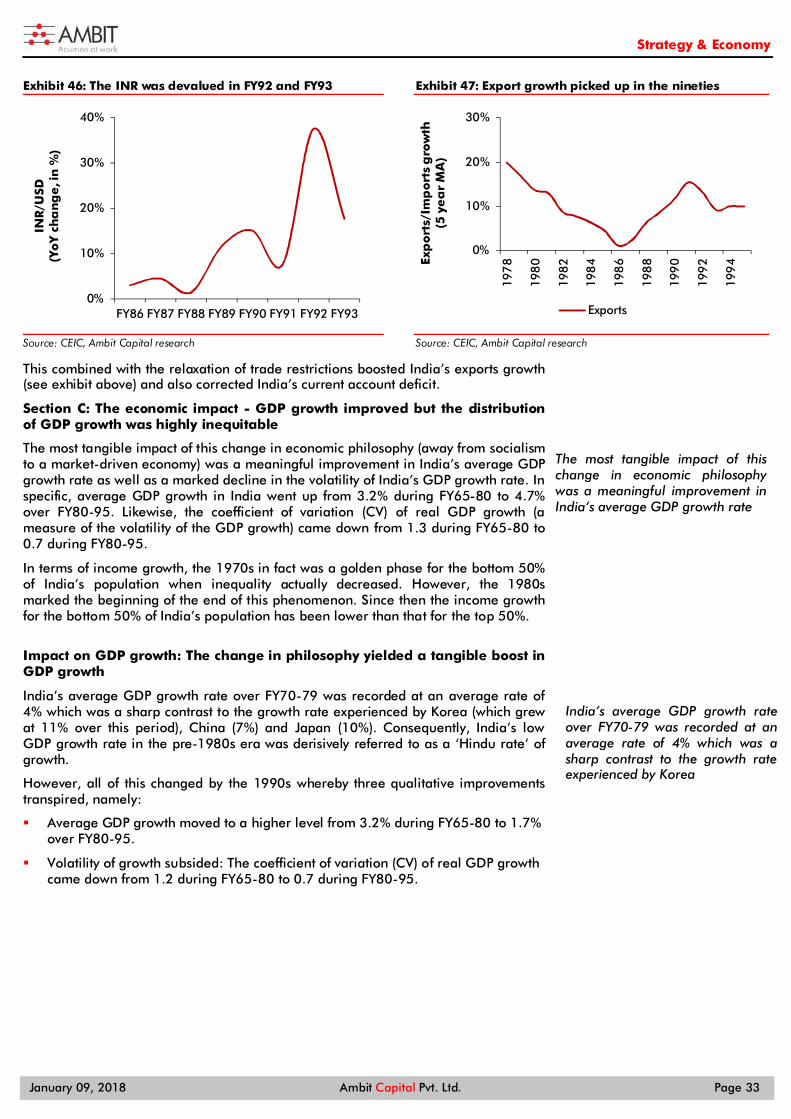

Section C: The economic impact - GDP growth improved but the ………………….33 distribution of GDP growth was highly inequitable

Impact on GDP growth: The change in philosophy yielded a ……………………33 tangible boost in GDP growth

Impact on inflation: Interest rate deregulation and reigning …………………….35 n the fiscal deficit helped control inflation

Impact on inequality: The reforms of FY1980-95 ………………………………….35 exacerbated inequality

Policy phase#3: India creates networks (FY1995-2018) ……………………….37

Section A: The political backdrop – Two non-Congress ………………………………..38 Governments complete a full term and usher in a focus on networks

Section B: Detailing the policy changes …………………………………………………41

Section C: The economic impact - GDP growth scaled new highs …………………..50 but once again the distribution of the growth was highly inequitable

Impact on GDP growth: GDP growth scaled new highs …………………………..50

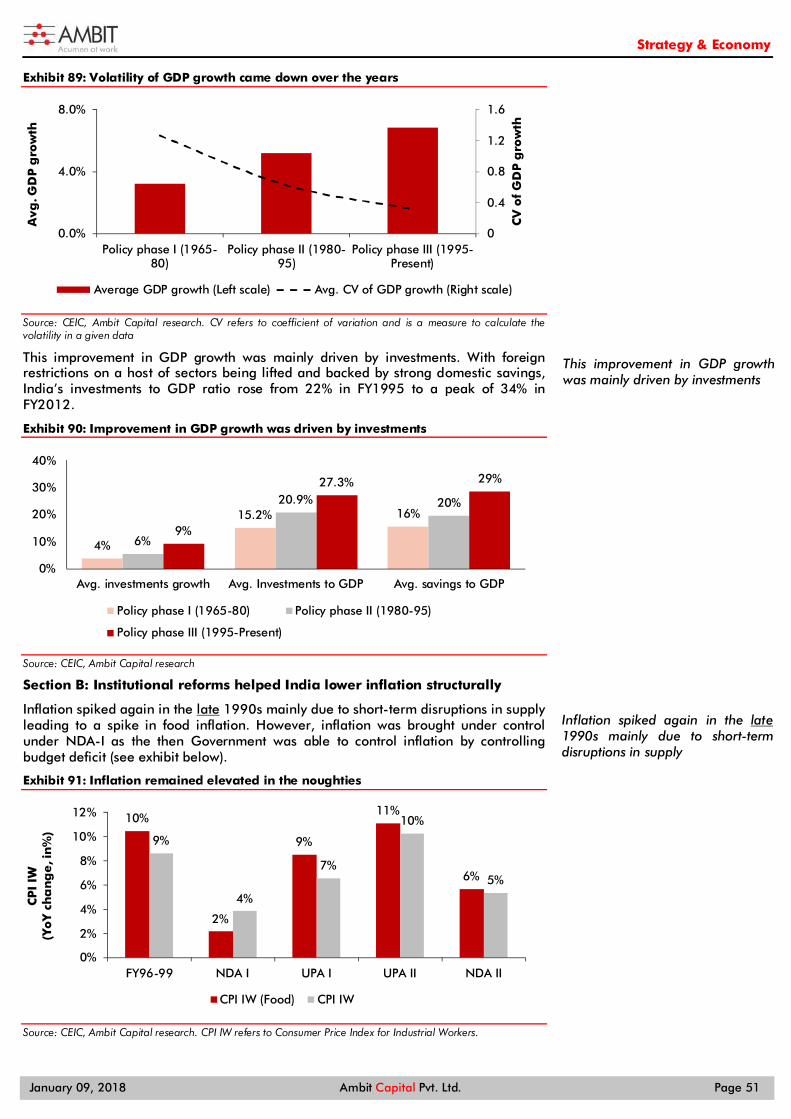

Impact on inflation: Institutional reforms helped India …………………………..51 lower inflation structurally

Impact on inequality: Inequality remained elevated and ………………………..52 in fact widened over this policy phase

Where is policy making headed now? ……………………………………………..52

What has driven policy making in India thus far? …………………………………53

Where do we go from here? ………………………………………………………….54

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 3

Section 2 of PAGES: The ASPIRATIONS that defined India ……………………11 over FY1960-2018

Aspiration phase #1: Discontent and frustration (1965-80) ……………………..60

Aspiration phase#2: Reimagining India (1980-95) ………………………………64

Aspiration phase#3: A billion mutinies now! (1995-2017) ……………………..71

What is the future of aspirations in India? ………………………………………….13

Section 3 of PAGES: What is likely to be the impact …………………………….14 of these changes in POLICY and ASPIRATIONS on GDP growth?

Section A: Capturing the transition of India’s supply-side ………………………86 GDP over the three policy-phases

Section B: Capturing the transition of the demand-side over …………………..87 the three policy-phases

Section C: Forecasting GDP growth and its constitution in ………………………88 India over FY17-22

Section 4 of PAGES: Earnings growth over the next ten years ……………….91

Are Sensex earnings and nominal GDP growth correlated? Yes ………………91

What does the regression tell us? 9% earnings growth ahead …………………91

The future of stock returns in India – lower than in the past ……………………92

Section 5 of PAGES: The Sensex’s constitution over the next ten years ……..93

Tracing the evolution of the Sensex …………………………………………………93

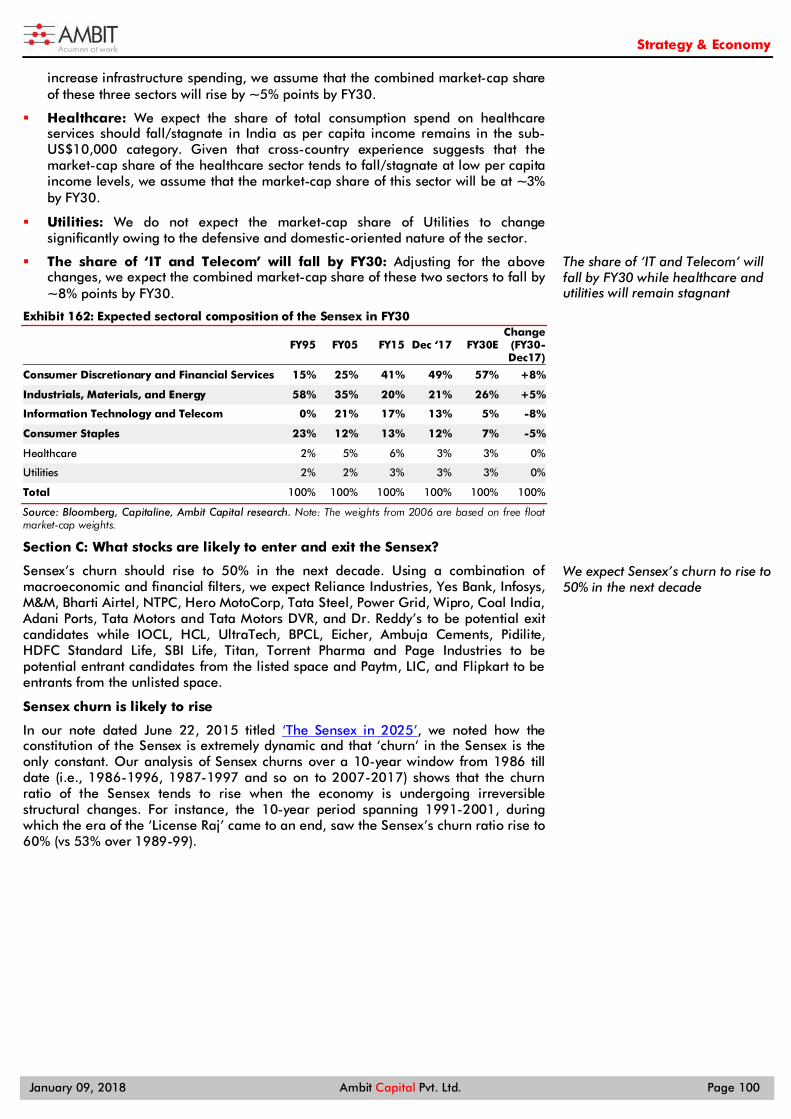

What is the constitution of Sensex likely to look like in FY30?……………………98

What stocks are likely to enter and exit the Sensex? ……………………………..100

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 4

This page has been intentionally left blank

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

India - A Billion Splendid Suns!

With a headstrong PM in charge, it is easy to assume that this strongman will shape India’s narrative in the near future. However, our deep-dive into India’s Policies, Aspirations, GDP growth, Earnings and Sensex constitution (i.e. PAGES) over FY65-18 points to a clear multi-decadal pattern to India’s development process. Hereon, we expect the Aspirations of India’s billion plus population to come to life, resulting in the Government continuing to build networks as well as pursuing Policies aimed at reducing inequality. This Policy thrust is likely to result in India’s real GDP growth being recorded at 8.1%, nominal Earnings growing at 9% and 50% of the Sensex undergoing churn over FY18-30.

Three distinct Policy and Aspirations’ phases from FY65-17 India’s history over the last five decades can be divided into three policy phases (see exhibit A), namely: Policy phase#1 from FY65-80 when Independent India pursued reforms to boost agricultural productivity, Policy phase#2 from FY80-95 when India transitioned from socialism to a mixed economy, and Policy phase#3 from FY95-18 when India created networks and infrastructure. As the Indian economy changed so did the Aspirations of its people. Policy phase#1 was characterised by a great deal of discontent and political volatility in a country which was in that era mocked by the world; policy phase#2 is when Indians began reimagining their identity, and finally policy phase#3 marked the beginning of a confident, assertive India finding its feet in the world.

Where do we go from here? The CY14 General Elections resulted in the rise of an all-powerful PM in India. Heuristically, it is convenient today to believe that this strongman will shape India’s narrative for the next decade. However, India’s evolution shows that not only are policies more powerful than personalities, but also that there is a clear multi-decadal pattern to India’s ‘PAGES’. With income inequality in India rising consistently for more than 30 years, we expect the Government to continue to clamp down on black money. This along with a concerted effort to build networks is likely to remain a focus area for politicians as more than a billion upwardly mobile people assert their need to communicate, to travel, to sell their produce and their labour and to find their place in the world.

How will these Policies & Aspirations impact GDP growth and Earnings? Assuming that the Government continues to build ‘networks’ and formalise the economy, we expect GDP growth over FY18-30 to be recorded at an average of 8.1% YoY, marking a 150bps acceleration as compared to FY95-18. History points to a surprisingly strong relationship between nominal GDP growth and Sensex earnings (65% correlation). Using this relationship and assuming 12% nominal GDP growth (8% real growth + 4% inflation), we expect earnings growth and, hence, Sensex returns to be around 9% p.a. over FY18-30.

50% of the Sensex to undergo churn over FY18-30 We expect the Sensex’s churn to rise to 50% over the next ten years (compared to 33% over the preceding decade) with major names (RIL, Yes Bank, Infosys and M&M amongst others) exiting whilst better capital allocators (HCL Tech, Eicher Motors, Pidilite, HDFC Life and SBI Life amongst others) enter the Sensex (see the right margin for a full list of entrants and section 5 for the list of exits). Sectors that will gain the most market-cap share over the next ten years are Consumer Discretionary, Financial services, Industrials, Materials and Energy whilst sectors that will lose share are Consumer Staples, IT, and Telecom.

THEMATIC January 09, 2018

Strategy & Economy

Exhibit A: India has undergone three policy phases thus far

Source: CEIC, Ambit Capital research

Exhibit B: Sector market cap share weights in the Sensex will change

Dec ‘17

FY30E Change

(FY30-Dec17)

Cons. Disc + Fin. Services

49% 57% +8%

Industrials+ Materials+Energy 21% 25% +5%

IT + Telecom 13% 5% -8%

Cons. Staples

12% 7% -5%

Healthcare 3% 3% 0%

Utilities 3% 3% 0%

Source: Ambit Capital research

Exhibit C: Potential entrants into the Sensex over the next decade

IOCL Ambuja Cements Torrent Pharma

HCL Pidilite Page

Ultratech HDFC Standard Life LIC

BPCL SBI Life Paytm

Eicher Titan Flipkart

Source: Ambit Capital research

Research Analysts

Ritika Mankar Mukherjee, CFA +91 22 3043 3175 [email protected]

Sumit Shekhar +91 22 3043 3229 [email protected]

Aditi Singh +91 22 3043 3284 [email protected]

Consultant Anupam Gupta [email protected]

3.2%4.7%

6.6%8.1%

0%

4%

8%

12%

FY65-8

0

FY80-9

5

FY95-1

8

FY18-3

9 (E

)Rea

l GD

P g

row

th(Y

oY c

ha

ng

e, i

n%

)

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 6

Summary of the forward looking implications Policy: From a forward-looking perspective, we expect four trends to emerge in India on the policy making front:

Trend#1: We expect subsequent Indian Governments to continue focusing on the pursuance of a black money crackdown. This can be a key tool that political parties deploy to weaken the Opposition’s access to election funding and to boost acceptability amongst the economically backward classes.

Trend#2: Creation of networks will be a fundamental trend wherein the Government will focus on infrastructure creation to boost growth and to meet aspirations of an increasingly mobile and connected India.

Trend#3: Politically, the rise of the Right is likely to continue following a 70-year period that saw the Congress and Congress-like parties dominate Indian politics.

For instance, it is worth noting that the BJP and its allies control 18 Indian States which account for 60% of India’s GDP. This kind of entrenched dominance in Indian politics was last seen in 1967 when the Congress controlled a similar number of states.

Trend#4: “Strongman economics”, i.e. ad-hoc policy-making, is likely to remain the flavour of the coming decade at the national as well as state level as compared to capitalism or socialism being the dominant economic philosophies in the previous few decades.

Aspirations: From a forward-looking perspective, we expect three trends to emerge, namely: A shift towards a broader and muscular assertion of India’s greatness from the

Nehruvian era of liberal-secular ideals. The lower middle class and poor will demand better services and aspire for a

better quality of life in the next decade. Asset ownership aspirations will shift from traditional physical assets (like homes)

to financial assets (like mutual funds).

GDP growth: The pick-up in GDP growth over FY18-30 (to 8.1% p.a.) is likely to be driven by three sets of factors namely, (1) the continued creation of physical, financial and virtual networks which in turn is likely to drive productivity growth, (2) the continued focus of subsequent Governments on a black money crackdown is likely to formalize the economy, and (3) liberalization continuing to be a policy theme thereby resulting in the continued opening up of the broader economy.

Earnings: Our forecast of 12% (8% real + 4% inflation) nominal GDP growth implies 9% Sensex earnings growth over FY18-30E. Hence, Sensex returns will moderate to 9% over FY18-30E as a maturing economy shifts cost of capital lower in the next two decades. (Note: FY95-2018 Sensex returns have been 11% p.a.)

Sensex: In the period FY18-30, we expect the market-cap share of Consumer Discretionary + Financial Services + Industrials + Materials + Energy to increase even as we move to per capita income of US$5000 by CY30. On the other hand, Consumer Staples + IT + Telecom are likely to lose market-cap share. Healthcare and Utilities are likely to remain stable. Owing to the structural changes that will materialise on the policy front, we expect the Sensex’s churn to rise to 50% in the next decade (vs 33% in the preceding decade). Using a combination of macroeconomic and financial filters, we expect Reliance Industries, Yes Bank, Infosys, M & M, Bharti Airtel, NTPC, Hero Motor, Tata Steel, Power Grid, Wipro, Coal India, Adani Ports, Tata Motors and Tata Motors DVR, and Dr Reddy’s to be potential exit candidates. IOCL, HCL, UltraTech, BPCL, Eicher Motors, Ambuja Cements, Pidilite, HDFC Standard Life, SBI Life, Titan, Torrent Pharma, and Page Industries are potential entrants from the listed space and Paytm, LIC and Flipkart are potential entrants from the unlisted space.

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 7

An illustrated executive summary We have divided India’s past into three distinct phases and have also attempted to project what will happen over the next decade (see exhibit below).

Indicators through various phases Exhibit 1:

Indicator Policy phase 1 (FY65-80)

Policy phase 2 (FY80-95)

Policy phase 3 (FY95-18) FY18-30 E

GDP growth 3.2% 4.7% 6.6% 8.1%

Sensex returns CAGR NA 35% 11% NA

Sensex EPS growth NA NA 14% 9%

Congress seat share in Lok Sabha 58% 51% 22% NA

Gini coefficient (period end)* 0.32 0.34 0.37 NA

Source: CEIC, Bloomberg, Election Commission of India, World Bank, Ambit Capital research. *The Gini coefficient measures the inequality among values of a frequency distribution. A Gini coefficient of zero expresses perfect equality, whereas Gini coefficient of 1 expresses maximal inequality among value

Section 1 of PAGES: Why India made the POLICY choices it did and what happens next?

India’s history over the last five decades can in fact be divided into three distinct and thematic policy phases (see exhibit below).

The three policy phases of India Exhibit 2:

Source: CEIC, Election Commission of India, World Bank, Ambit Capital research. *Note: (1) The Gini coefficient measures the inequality among values of a frequency distribution. A Gini coefficient of zero expresses perfect equality, whereas Gini coefficient of 1 expresses maximal inequality among value, (2) Seat share of Congress refers to seat share in Lok Sabha (lower house of the Parliament).

To be more specific, the three policy phases can be demarcated as follows: Policy phase 1 (FY65-80): India accords top priority to agriculture

“What kind of pride and prejudice this country [India] was up against is best illustrated by an interview Vijayalakshmi Pandit, [Nehru's sister, then ambassador to the US] had with Sam Rayburn, Speaker of the House and a legendary figure on the Hill at that time, from which she returned in a towering rage. It had gone something like this:

Rayburn: "Why don't you buy wheat from Pakistan which has wheat in surplus? The only reason you don't is because Hindu India wants to do down Muslim Pakistan,"

She tried to control her temper as best she could and said testily, “India was not Hindu India, and that it had more Muslims than Muslim Pakistan."

Rayburn: "Oh, you have Muslims in India! Honey, why didn't you say so earlier?"

Ambassador: "Sam, I have been saying this for two years, ever since I came here, but you don't hear and you don't understand."

58%51%

22%

0.32 0.33 0.36

0%

1%

2%

3%

4%

5%

6%

7%

8%

0%

20%

40%

60%

80%

Policy Phase 1 (FY65-80) Policy Phase 2 (FY80-95) Policy phase 3 (FY95-18)

GD

P g

row

th

Sea

t sh

are

/Gin

i co

eff

.*/S

ense

x re

turn

s

Seat share of Congress (Left scale) Gini coeff. (Left scale)

Sensex returns (left scale) GDP growth (Right scale)

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 8

Whereupon Rayburn's tone suddenly changed, and he said: "No, no, now that I know, now you will have no trouble. If they give you any more trouble, honey, you just tell me."

-‘Swallowing the humiliation’ by Inder Malhotra for the Indian Express on July 12, 2010

Policy phase#1 was hence characterised by low GDP growth, the political dominance of the Congress and the persistence of a high degree of income inequality (see exhibit below). During most of this era, India was a desperately poor country which was mocked by the world and constantly warring with its neighbours.

Policy phase#1 was characterised by low GDP growth, political dominance of the Congress and the persistence of Exhibit 3:a high degree of inequality

Source: CEIC, Election Commission of India, World Bank, Ambit Capital research. *Note: (1) The Gini coefficient measures the inequality among values of a frequency distribution. A Gini coefficient of zero expresses perfect equality, whereas Gini coefficient of 1 expresses maximal inequality among value, (2) Seat share of Congress refers to seat share in Lok Sabha (lower house of the Parliament).

*Note: Average GDP growth during this period was recorded at 3.2% YoY in real terms as compared to the FY65-18 average of 5.2% YoY, the average Gini coefficient during this period was recorded at 0.32 as compared to the FY65-18 average of 0.34 and the average seat share of the Congress during this period was recorded at 58% as compared to the FY65-18 average of 44%.

During this phase India’s policymakers were forced to focus on enhancing the productivity of the agricultural sector and did so by embracing the ‘Green Revolution’ which was transforming crop yields in the developing world. This policy choice was a critical one as the focus on agriculture allowed India to begin breaking away from the previous policy thrust that was centered on: (a) Soviet-style planning; and (b) growing state-owned enterprises (SOEs) that were thus far revered as the temples of modern India.

Policy phase 2 (FY80-95): From socialism to liberalisation

“No power on earth can stop an idea whose time has come”

- Dr. Manmohan Singh quoting Victor Hugo in his landmark budget speech (July 1991)

Policy phase#2 was characterised by a major improvement in GDP growth, superior stock market returns (35% CAGR), a rise in political competition and a rise in income inequality (see exhibit below).

73%

54%

68%

28%

67%

4%

3%

5%

3%2%

2%

3%

4%

5%

0%

20%

40%

60%

80%

FY62 FY67 FY71 FY77 FY80

GD

P g

row

th

Sea

t sh

are

/Gin

i*

Seat share of Congress (Left scale) Gini coeff. (Left scale) Avg. GDP growth (Right scale)

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 9

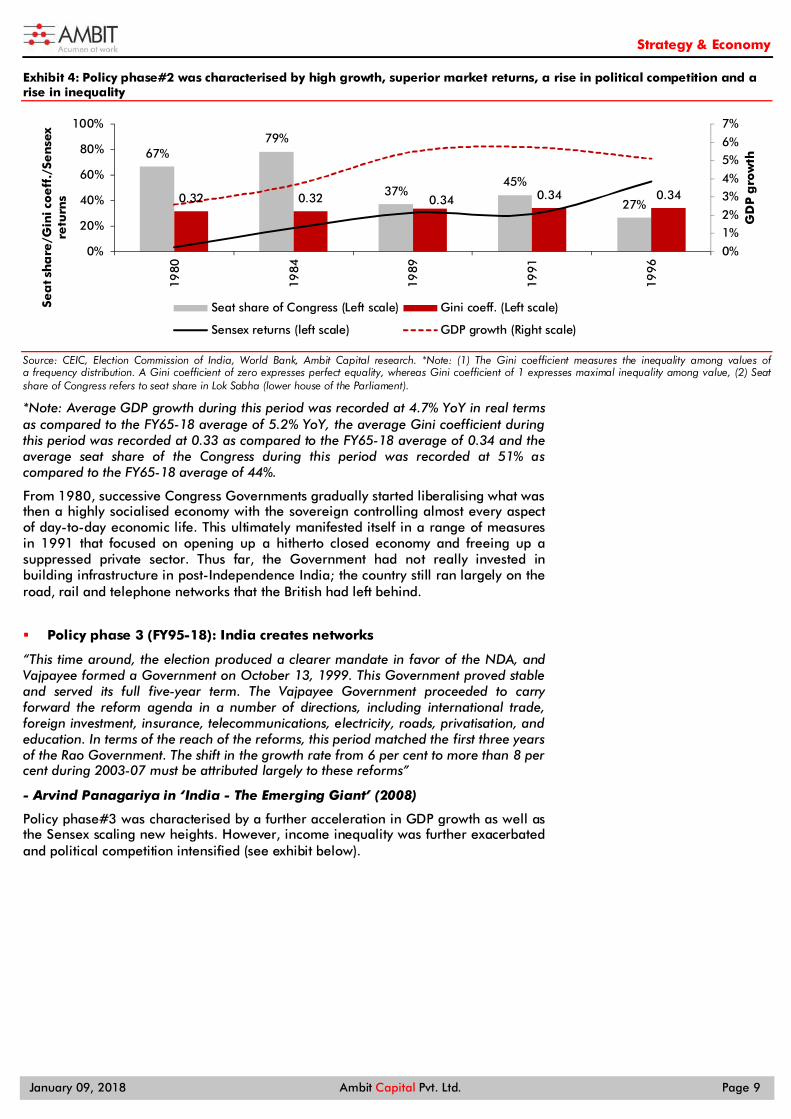

Policy phase#2 was characterised by high growth, superior market returns, a rise in political competition and a Exhibit 4:rise in inequality

Source: CEIC, Election Commission of India, World Bank, Ambit Capital research. *Note: (1) The Gini coefficient measures the inequality among values of a frequency distribution. A Gini coefficient of zero expresses perfect equality, whereas Gini coefficient of 1 expresses maximal inequality among value, (2) Seat share of Congress refers to seat share in Lok Sabha (lower house of the Parliament).

*Note: Average GDP growth during this period was recorded at 4.7% YoY in real terms as compared to the FY65-18 average of 5.2% YoY, the average Gini coefficient during this period was recorded at 0.33 as compared to the FY65-18 average of 0.34 and the average seat share of the Congress during this period was recorded at 51% as compared to the FY65-18 average of 44%.

From 1980, successive Congress Governments gradually started liberalising what was then a highly socialised economy with the sovereign controlling almost every aspect of day-to-day economic life. This ultimately manifested itself in a range of measures in 1991 that focused on opening up a hitherto closed economy and freeing up a suppressed private sector. Thus far, the Government had not really invested in building infrastructure in post-Independence India; the country still ran largely on the road, rail and telephone networks that the British had left behind.

Policy phase 3 (FY95-18): India creates networks

“This time around, the election produced a clearer mandate in favor of the NDA, and Vajpayee formed a Government on October 13, 1999. This Government proved stable and served its full five-year term. The Vajpayee Government proceeded to carry forward the reform agenda in a number of directions, including international trade, foreign investment, insurance, telecommunications, electricity, roads, privatisation, and education. In terms of the reach of the reforms, this period matched the first three years of the Rao Government. The shift in the growth rate from 6 per cent to more than 8 per cent during 2003-07 must be attributed largely to these reforms”

- Arvind Panagariya in ‘India - The Emerging Giant’ (2008)

Policy phase#3 was characterised by a further acceleration in GDP growth as well as the Sensex scaling new heights. However, income inequality was further exacerbated and political competition intensified (see exhibit below).

67%79%

37%45%

27%0.32 0.32 0.34 0.34 0.34

0%

1%2%

3%4%

5%6%

7%

0%

20%

40%

60%

80%

100%

1980

1984

1989

1991

1996

GD

P g

row

th

Sea

t sh

are

/Gin

i co

eff

./Se

nse

x re

turn

s

Seat share of Congress (Left scale) Gini coeff. (Left scale)

Sensex returns (left scale) GDP growth (Right scale)

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 10

The third policy phase was characterised by GDP growth as well as the Sensex scaling new heights, inequality Exhibit 5:worsening and political competition remaining high

Source: CEIC, Election Commission of India, World Bank, Ambit Capital research. *Note: (1) The Gini coefficient measures the inequality among values of a frequency distribution. A Gini coefficient of zero expresses perfect equality, whereas Gini coefficient of 1 expresses maximal inequality among value, (2) Seat share of Congress refers to seat share in Lok Sabha (lower house of the Parliament).

*Note: Average GDP growth during this period was recorded at 6.7% YoY in real terms as compared to the FY65-18 average of 5.2% YoY, the average Gini coefficient during this period was recorded at 0.33 as compared to the FY65-18 average of 0.36 and the average seat share of the Congress during this period was recorded at 22% as compared to the FY65-18 average of 44%.

If the FY80-95 era was about liberalising the economy and letting animal spirits loose, the next 20 years were about India building infrastructure – physical, financial and virtual. The creation of these infrastructure networks allowed Indians – workers and entrepreneurs - to travel: (a) across the country and (b) across the wider global economy in search of economic opportunities. That in turn created for the first time since 1947 a recognisably self-confident nation.

What to expect from policy making?

From a forward-looking perspective, much in line with the international experience, we expect four trends should emerge.

Trend#1: We expect subsequent Indian Governments to continue focusing on the pursuance of black money crackdown. This can be a key tool that political parties deploy to weaken the opposition’s access to finance and to boost acceptability amongst the economically backward classes.

Trend#2: Creation of networks will be a fundamental trend where the Government will focus on quality infrastructure creation to boost growth.

Trend#3: Politically, the rise of the right wing is likely to continue following a 70-year period that saw the Congress and Congress-like parties dominate Indian politics.

For instance, it is worth noting that the BJP and its allies control 18 Indian States which account for 60% of India’s GDP. This kind of entrenched dominance in Indian politics was last seen in 1967 when the Congress controlled a similar number of states (see exhibit below).

Trend#4: “Strongman economics”, i.e. ad-hoc policy-making, is likely to remain the flavour of the coming decade at the national as well as state level as compared to capitalism or socialism being the dominant economic philosophies in the previous few decades.

67%79%

37%45%

27%0.32 0.32 0.34 0.34 0.34

0%

1%

2%

3%

4%

5%

6%

7%

-20%

0%

20%

40%

60%

80%

100%

1998

1999

2004

2009

2014

GD

P g

row

th

Sea

t sh

are

/Gin

i co

eff

icie

nt/

Sen

sex

retu

rns

Seat share of Congress (Left scale) Gini coeff. (Left scale)

Sensex returns (left scale) GDP growth (Right scale)

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 11

Section 2 of PAGES: The ASPIRATIONS that defined India over FY60-18

As the Indian economy changed so did the aspirations of its youth. We see three broad phases of aspirations: from the trials and tribulations of a volatile post-Independence era (FY65-80) to the early stages of an open-market economy (FY80-95). As the open economy grew and evolved, a more vibrant, more self-confident was born and that generation is at war today with the previous generation that still rules it (FY95-18) Aspiration phase #1: Discontent and frustration (1965-80)

"To the historian, the late 1960s are reminiscent of the late 1940s, likewise a time of crisis and conflict, of resentment along lines of class, religion, ethnicity and region, of a Centre that seemed barely to hold."

"Indian democracy, circa 1975, could reconcile the Valley of Kashmir to the Union of India, but not Indira Gandhi with Jayaprakash Narayan."

- Ramachandra Guha in ‘India After Gandhi’ (2007)

The Nobel laureate VS Naipaul was pessimistic about India during his travels for ‘An Area of Darkness’ (1964) and ‘A Wounded Civilization’ (1977). He traveled widely whilst writing these books and what he saw – deep-rooted poverty, social injustice, the misery of the lower castes, lack of development, lack of sanitation and a general sense of frustration – moved him to despair about the future of the country. The frustration and anger felt by the “Midnight’s Children” (the memorable name given by Salam Rushdie in his epic novel to those who were born on 15th August 1947) was the defining theme of this era. Most ambitious Indians sought to emigrate from India in this era especially if they could not get a job in the civil service or could not become a doctor or an engineer.

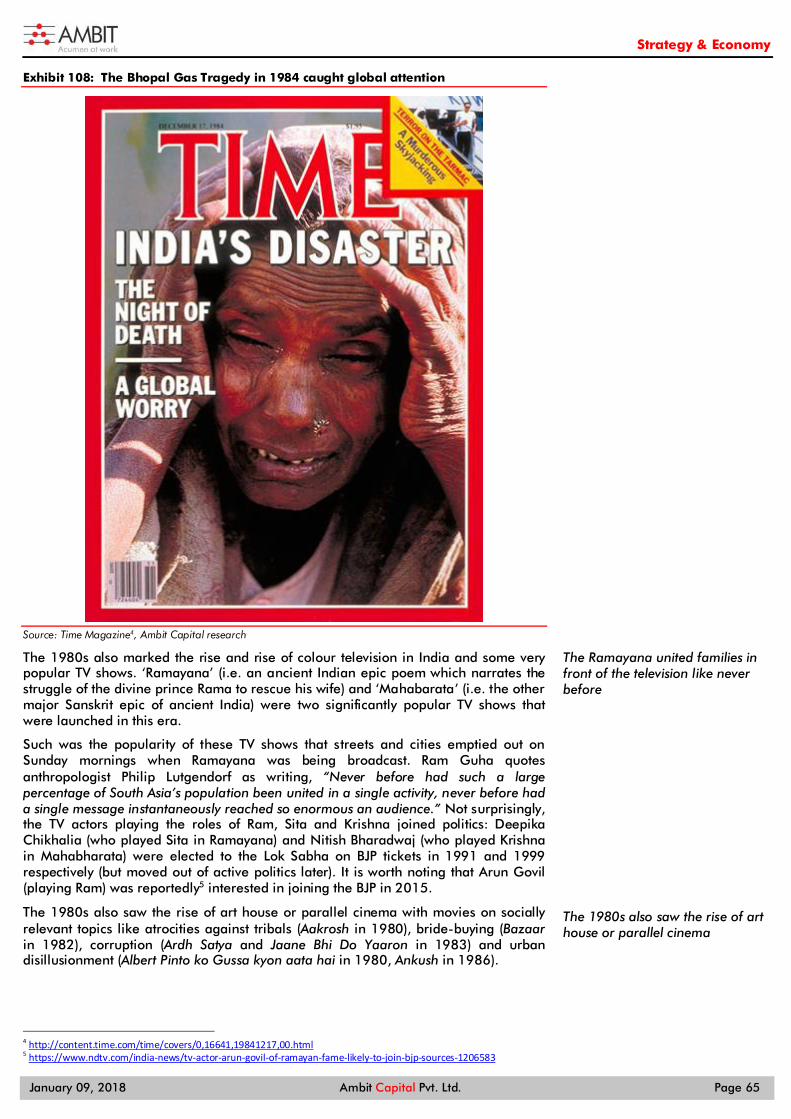

V S Naipaul’s books painted a depressing picture of India in the 1960s and Exhibit 6:the 1970s

Source: Amazon.com, Pan McMillan, Ambit Capital research.

Aspiration phase#2: Reimagining India (1980-95)

“Rajiv Gandhi never quarreled with the principle of secularism, yet during his premiership the relations between Hindus and Muslims degenerated to their lowest level since the holocaust of partition. [..]

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 12

Democracy was not faring too well either when Rajiv Gandhi was assassinated. [..] Even in opposition Rajiv remained an isolated figure, dependent for information and advice on a small coterie who had no political clout of their own."

- Mark Tully in ‘No full stops for India’, (1991)

The 1980s saw the dawn of colour television in India and the arrival of religious soap operas like the ‘Ramayana’, a TV series aired in 1987-88. Streets and cities emptied on Sunday mornings when the Ramayana and subsequently the Mahabharata were broadcast. Whilst emigrating from India remained popular, for the first time since Independence, Indian youth found that even if they could not get a job in the civil services, there were a few remunerative jobs to be found in the private sector.

The other defining theme of this era was the rise of big ticket corruption scandals which, for the first time, involved politicians and civil servants working in cahoots with corporate houses. The template for these scams was memorably captured in hit art house movies of this era like Ardh Satya and Jaane Bhi Do Yaaron.

Parallel cinema rose in the 1980s and captured the growing nexus between Exhibit 7:politicians and business houses

Source: IMDB.com, Neo Films, Shemaroo, NFDC, Ambit Capital research

Aspiration phase#3: A billion mutinies now! (1995-2017)

“…India was, in the simplest way, on the move, that all over the vast country men and women had moved out of the cramped ways and expectations of their parents and grandparents and were expecting more.”

– V S Naipaul in ‘India: A million mutinies now’ (1989)

Economic liberalisation transformed India. A new class of executives and business owners arose on the back of the opportunities unleashed by the opening up of the economy and by strong GDP growth during FY2003-FY2008. The proliferation of mobile telephony and internet coupled with a huge ramp-up in road infrastructure (the Golden Quadrilateral linking metro cities of Delhi, Mumbai, Chennai and Kolkata) brought small-town India closer to cities, opening up career and business opportunities like never before. This upbeat narrative was punctuated by corruption scams which had a common template – crony capitalists allying with politicians and civil servants to game either regulations and/or the Government spending engine.

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 13

Modi’s victory resounded across the world Exhibit 8:

Source: Time.com, Economist.com, Ambit Capital research

What is the future of aspirations in India?

We see three big areas of aspirations for the Indian youth. These are:

(1) Muscular assertion of identity: With the rise of the BJP, there is a clear move to disassociate India from the liberal-secular ideals of the Nehruvian era and shift the narrative of a new generation to a broader, more muscular assertion of India’s greatness. This is already evident in Government initiatives such as suggesting an International Yoga Day to the United Nations, dedicating a Ministry and Minister for the erstwhile Department of Ayurveda, Yoga and Naturopathy, Unani Siddha and Homeopathy (AYUSH), etc. We expect these trends to continue and fuel aspirations for today’s youth to be patriotic, proud of India’s past, and self-confident in the assertion of their own identity.

(2) The rise of the lower middle class and the aspirations of the poor: As the Golden Quadrilateral and the launch of mobile telephony in Phase 3 (1995- 2017) drove the aspirations of the middle class, we believe that the Government’s initiatives such as the Bharatmala Road Project (34,800km of roads to be constructed at an investment of Rs5.350tn) and the increasing penetration of the ‘Jan Dhan-Aadhaar-Mobile’ Yojana will, over the next decade, fuel aspirations of the lower middle class and the poor. The poor will aspire to services and products such as aviation, housing, and mobile data services on low-cost feature-phones.

(3) Asset ownership aspirations – from physical to financial: With demonetisation, there has been a shift from physical savings towards financial savings, which is gradually picking up pace and should continue in the next decade. This shift is being fueled by the unaffordability of real estate in metro cities (bloated prices), the freezing of cash transactions in real estate (due to demonetisation), and the booming stock markets. Thus, over the longer term, we expect affordable housing to fulfill the aspirations of the lower middle class even as the urban youth question the need for owning an expensive house and shift, instead, toward building a portfolio of stocks and mutual funds for securing their financial future.

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 14

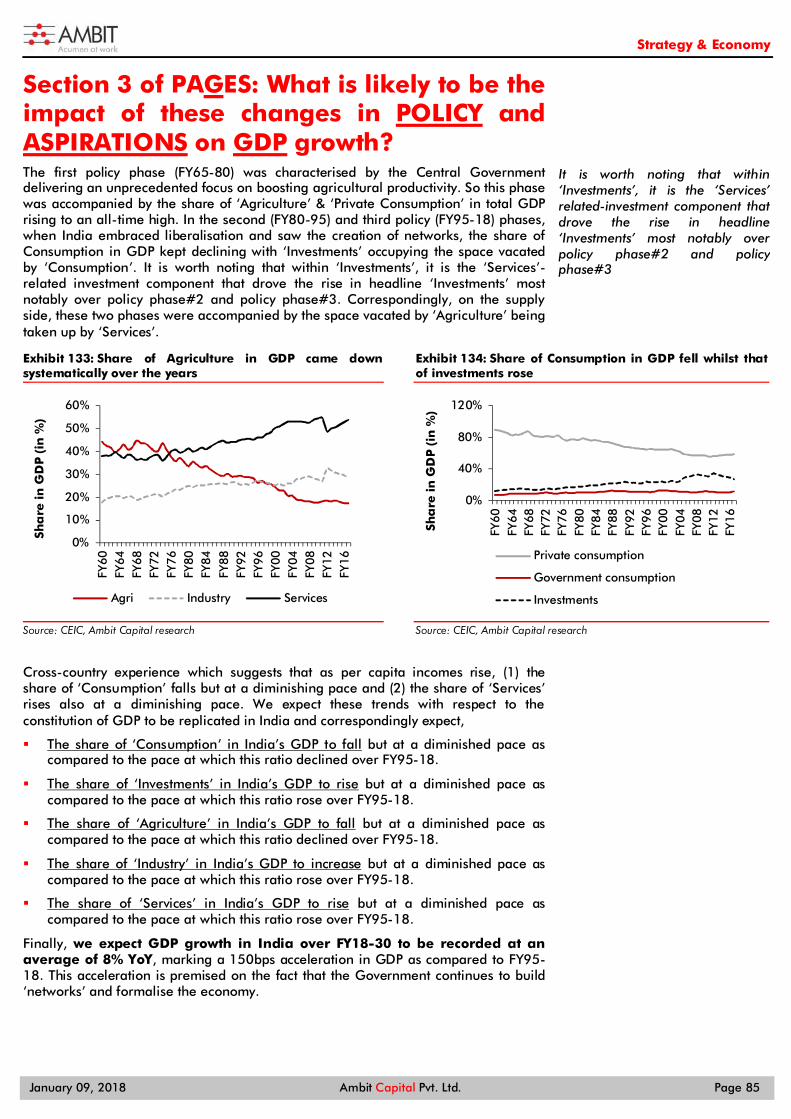

Section 3 of PAGES: What is likely to be the impact of these changes in POLICY and ASPIRATIONS on GDP growth?

Cross-country experience suggests that as capita incomes rise, (1) the share of ‘Consumption’ falls but at a diminishing pace; and (2) the share of ‘Services’ rises but also at a diminishing pace (see exhibit below).

We expect the share of ‘Services’ in GDP to continue rising but at a Exhibit 9:diminished pace

Period Average

Agriculture (as a % of GDP)

Average Industry (as a % of GDP)

Average Services (as a % of GDP)

Average real GDP growth

FY65-80 40% 21% 38% 3.2%

FY80-95 31% 26% 43% 4.7%

Delta for Phase 2 -9% +5% +5% +1.5%

FY95-18 21% 28% 51% 6.6%

Delta for Phase 3 -10% +2% +8% +1.9%

FY18-30 (E) 14% 30% 56% 8.1%

Level in FY17 17% 29% 54% 5.8%

Delta for Phase 4 (E) -7% +2% +5% +1.5%

Source: CEIC, Ambit Capital research

We expect GDP growth to accelerate by 150bps during FY18-30. In other words, we expect GDP growth to average at 8.1% during FY18-30 as compared to an average of 6.6% during FY95-118 (see exhibit below).

We expect GDP growth to accelerate by 150bps during FY18-30 Exhibit 10:

Source: CEIC, Ambit Capital research

Section 4 of PAGES: The future of India’s earnings

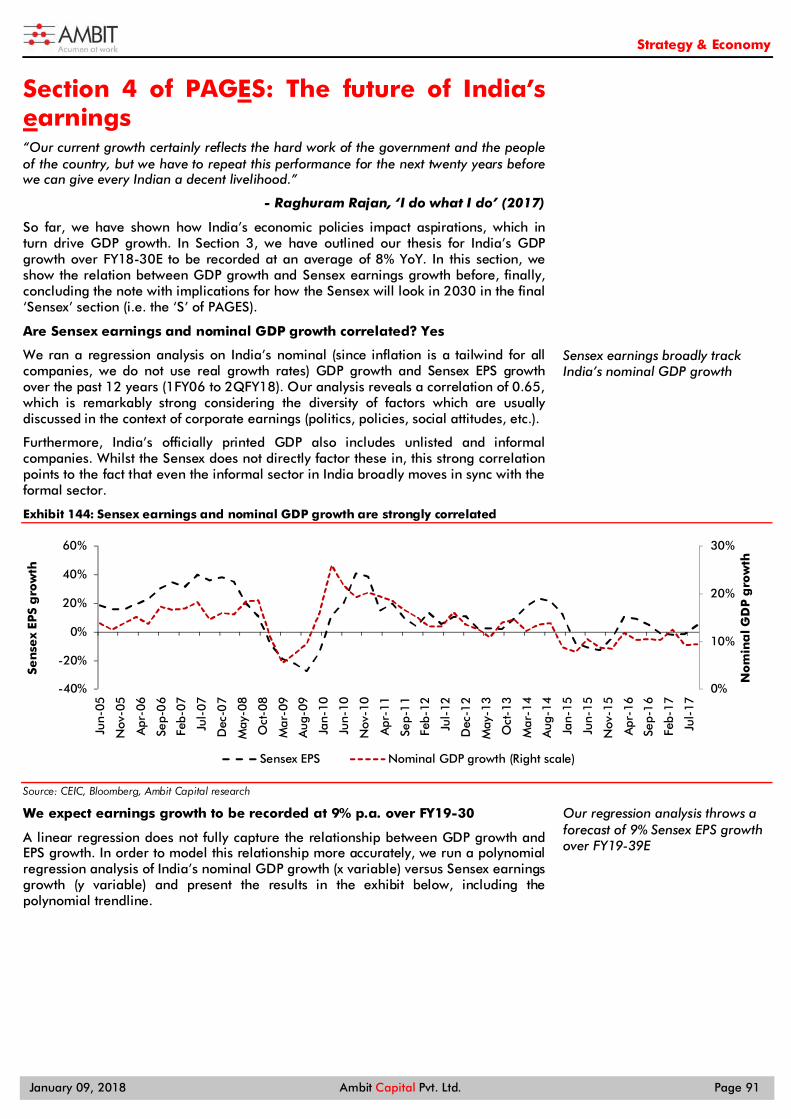

As regards earnings, history points to a surprisingly strong correlation between nominal GDP growth and Sensex earnings growth (see exhibit below).

Sensex earnings and nominal GDP growth broadly move in sync Exhibit 11:

Source: CEIC, Bloomberg, Ambit Capital research

3.2%

4.7%

6.6%

8.1%

0%

2%

4%

6%

8%

10%

FY65-80 FY80-95 FY95-18 FY18-39 (E)

Re

al G

DP

gro

wth

(Ave

rag

e o

ver

spe

cifi

ed

p

eri

od

)

(60)

(40)

(20)

0

20

40

60

Mar

-01

Nov

-01

Jul-

02

Mar

-03

Nov

-03

Jul-

04

Mar

-05

Nov

-05

Jul-

06

Mar

-07

Nov

-07

Jul-

08

Mar

-09

Nov

-09

Jul-

10

Mar

-11

Nov

-11

Jul-

12

Mar

-13

Nov

-13

Jul-

14

Mar

-15

Nov

-15

Jul-

16

Mar

-17

Nominal GDP growth (%) Sensex EPS growth (%)

(%Yo

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 15

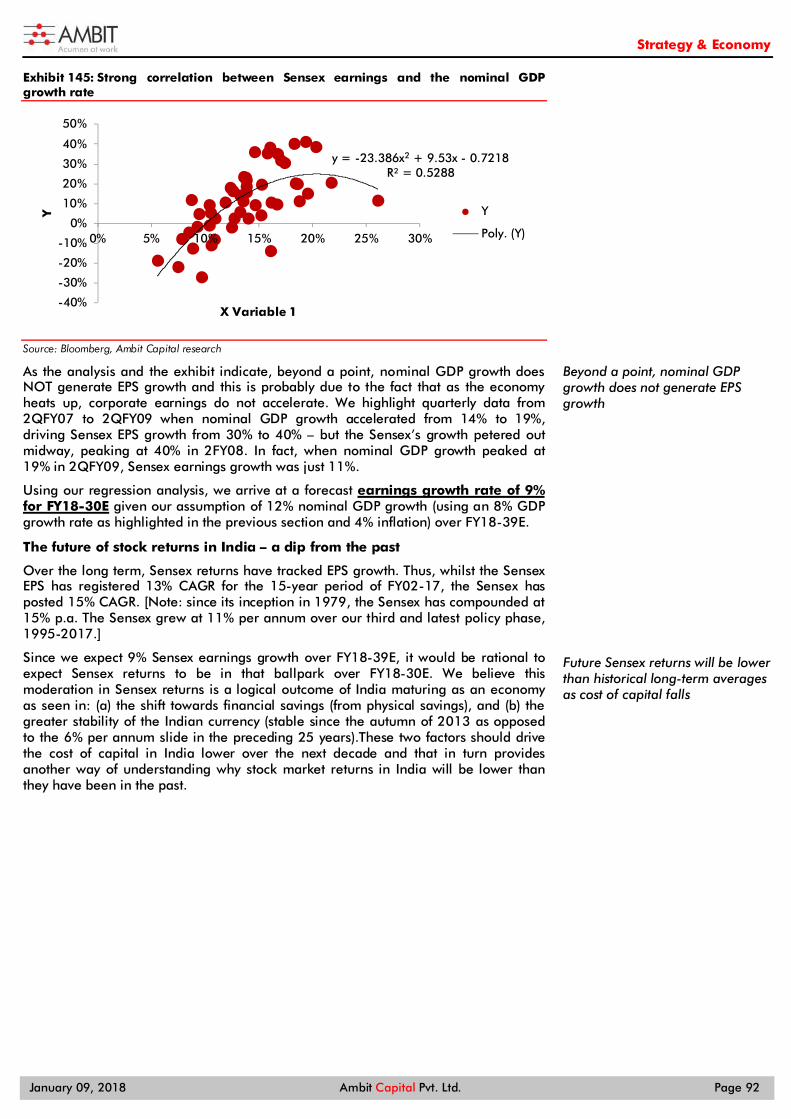

A linear regression does not fully capture the relationship between GDP growth and EPS growth. In order to model this relationship more accurately, we run a polynomial regression analysis of India’s nominal GDP growth (x variable) versus Sensex earnings growth (y variable) and present the results in the exhibit below, including the polynomial trend line.

Strong correlation between Sensex earnings and the nominal GDP growth Exhibit 12:rate

Source: Bloomberg, Ambit Capital research. The data pertains from 1QFY06-2QFY18 (50 quarters)

Using this relationship and assuming nominal GDP growth of 12% (i.e. 8% real GDP growth + 4% inflation), we expect earnings growth to be recorded at 9% p.a. in nominal terms over FY18-30. Since long-term stock market returns are defined by long-term EPS growth, this suggests that the Sensex will give returns of around 9% p.a. over the next 10 years. [Note: the Sensex has compounded at 15% since its inception in 1979.]

Section 5 of PAGES: The Sensex’s constitution

In the period FY18-30, we expect the market-cap share of consumer discretionary + financials and industrials + materials + energy to increase even as we move to per capita income of US$5000 by CY30. On the other hand, consumer staples and IT + telecom are likely to lose market-cap share. Healthcare and utilities are likely to remain stable. Owing to the structural changes that will materialise on the policy front, we expect Sensex’s churn to rise to 50% in the next decade. Using a combination of macroeconomic and financial filters, we expect Reliance Industries, Yes Bank, Infosys, M&M, Bharti Airtel, NTPC, Hero Motor, Tata Steel, Power Grid, Wipro, Coal India, Adani Ports, Tata Motors and Tata Motors DVR, and Dr Reddy’s to be potential exit candidates. IOCL, HCL, UltraTech, BPCL, Eicher, Ambuja Cements, Pidilite, HDFC Standard Life, SBI Life, Titan, Torrent Pharma, and Page Industries are potential entrants from the listed space and Paytm, LIC and Flipkart are potential entrants from the unlisted space.

Sector weights evolution Exhibit 13:

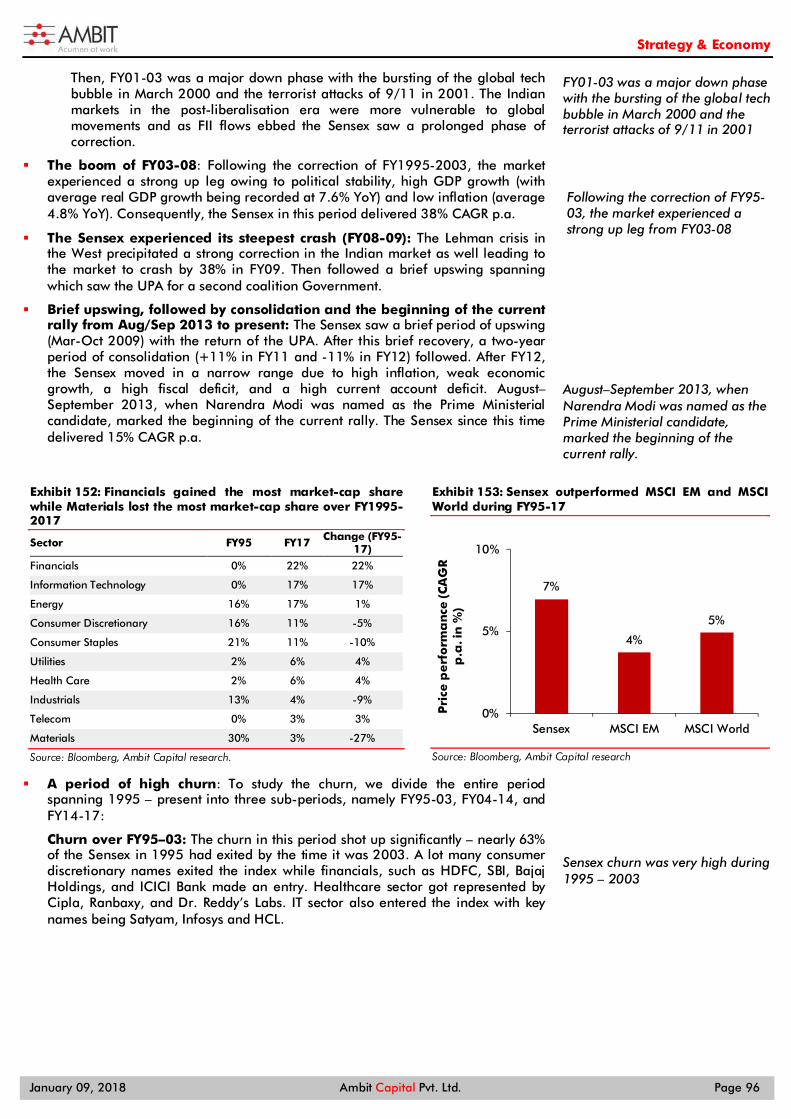

Sector FY95 FY05 FY15 Dec ‘17 FY30E Change

(FY30-Dec17)

Consumer Discretionary and Financial Services 15% 25% 41% 49% 57% +8%

Industrials, Materials, and Energy 58% 35% 20% 21% 26% +5%

Information Technology and Telecom 0% 21% 17% 13% 5% -8%

Consumer Staples 23% 12% 13% 12% 7% -5%

Healthcare 2% 5% 6% 3% 3% 0%

Utilities 2% 2% 3% 3% 3% 0%

Total 100% 100% 100% 100% 100% 100%

Source: Bloomberg, Ambit Capital research

y = -23.386x2 + 9.53x - 0.7218R² = 0.5288

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0% 5% 10% 15% 20% 25% 30%

Y

X Variable 1

Y

Poly. (Y)

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 16

The probable exits from Sensex Exhibit 14:Exits Ticker Mcap ($bn) GICS Sector

Reliance RIL IN 94 Energy

Infosys INFO IN 37 IT

Airtel BHARTI IN 33 Telecom

Coal India COAL IN 27 Energy

Wipro WPRO IN 24 IT

NTPC NTPC IN 23 Utilities

Tata Motors TTMT IN 22 Cons. Discr

Tata Motors - DVR TTMT/A IN 22 Cons. Discr

Power Grid PWGR IN 17 Utilities

M&M MM IN 15 Cons. Discr

Adani Ports ADSEZ IN 14 Utilities

Hero Motors HMCL IN 12 Cons. Discr

Tata Steel TATA IN 11 Materials

Yes Bank YES IN 11 Financials

Dr Reddy's DRRD IN 6 Health Care

Source: Bloomberg, Ambit Capital research

The possible entrants into the Sensex Exhibit 15:

Entrants Ticker Mcap ($bn) GICS Sector

IOCL IOCL IN 30 Energy

HCL HCLT IN 20 Information Technology

Ultratech UTCEM IN 19 Materials

BPCL BPCL IN 17 Energy

Eicher EIM IN 12 Industrials

Ambuja Cements ACEM IN 9 Materials

Pidilite PIDI IN 7 Materials

HDFC Standard Life HDFCLIFE IN 12 Financials

SBI Life SBILIFE IN 11 Financials

Titan TTAN IN 12 Consumer Discretionary

Torrent Pharma TRP IN 4 Health Care

Page PAG IN 4 Consumer Discretionary

Paytm - - Financials

Flipkart - - Consumer Discretionary

LIC - - Financials

Source: Bloomberg, Ambit Capital research

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 17

Section 1 of PAGES: Why India made the policy choices it did? “There comes a time in the life of every nation when it stands at the crossroads of history and must choose which way to go. But for us there need to be no difficulty or hesitation, no looking to right or left.”

- Lal Bahadur Shastri in his first address as PM of India (June 11, 1964)

Whilst Indian policymakers’ choices can seem ad-hoc, lacking any pattern in the way they behave, India’s history over the last five decades can be divided into three distinct and thematic policy phases, namely: Policy phase#1 (FY1965-80): When Independent India pursued reforms to

boost agricultural productivity (refer to pg 18 to 27 for details), Policy phase#2 (FY1980-95): When India transitioned from socialism to a

mixed economy (refer to pg 27 to 36 for details); and Policy phase#3 (FY1995-2018): When India created internal networks and

infrastructure (refer to pg 37 to 52 for details).

This segmentation of India’s policy choices into these three policy phases yields several key insights that the subsequent section spanning will elaborate upon. The chief finding that stands out is that Indian policymakers opted for pro-market reforms and pro-business policy changes only to ensure the longevity of political power. Contrary to popular belief, liberalisation was not necessitated by India’s twin deficits in the 1990s but by a range of financial compulsions that gradually crept up on the Indian Government through the 1980s.

The private sector in India was ignored until 1980, i.e. the point in time until political competition in India was low and the Congress had near monopoly control over India. As political competition grew, political parties that held power ensured that they undertook greater opening-up of the Indian economy and also facilitated infrastructure development so as to fulfill two goals, namely:

Raise the monies required for funding General Elections (which were becoming exorbitant affairs owing to rising political competition); and

Foster GDP growth rate so as to grow tax collections at a healthy clip which could then be used to provide sops to the masses.

In fact, this phenomenon probably explains why the rise in political competition in India has been accompanied by higher GDP growth in India (see exhibit below).

The increase in political competition in India has been accompanied by Exhibit 16:higher GDP growth

Source: Election Commission of India, CEIC, Ambit Capital research. Note: The effective number of parties is a concept which provides for an adjusted number of political parties in a country's party system. The idea behind this measure is to count parties and, at the same time, to weight the count by their relative strength. The relative strength refers to their vote share ("effective number of electoral parties") or seat share in the parliament ("effective number of parliamentary parties")

0%

2%

4%

6%

8%

10%

0

1

2

3

4

5

6

7

1952

1957

1962

1967

1971

1977

1980

1984

1989

1991

1996

1998

1999

2004

2009

GD

P g

row

th

(Yo

Y ch

an

ge

, in

%)

Effe

ctiv

e n

o. o

f p

oli

tica

l p

art

ies

(se

ats

)*

India opted for pro-market reforms and pro-business policy changes only to ensure longevity of political power

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 18

The other key finding that stands out is that Indian policymakers’ decisions are heavily influenced by the international policy narrative prevalent at a particular point in time. This could because Indian politicians have seldom possessed intellectual conviction when it comes to making policy decisions; more often than not, their policy decisions are driven by the need to hurt rival politicians and consolidate their political power. This helps explain why India swung from pursuing left of centre economic policies from FY1947-64 to right of centre economic policies from FY1980.

The Soviet Union’s economic model of Central Exhibit 17:command-and-control heavily influenced Indian policies from FY1947-64

Source: Ambit Capital research

The apparent success of classical liberalism Exhibit 18:

and free markets created an imprint on Indian policy from the 1980s

Source: Ambit Capital research

The subsequent part of this section elaborates on each of the three policy phases that India has traversed since FY1960 to date.

Each of the three policy phase related sections in turn is divided into three convenient parts, namely: (1) the political backdrop; (2) the policy choices made; and finally (3) the macroeconomic ramifications of the policy choices made on GDP growth, inflation and extent of inequality.

Policy phase#1: India accords top priority to agriculture (FY1965-80) “A nation’s strength ultimately consists in what it can do on its own, and not in what it can borrow from others.”

- Indira Gandhi (1970)

When India became independent in 1947, it had been administered and controlled by the British for two centuries. By the sixties, i.e. two decades after being an independent sovereign, and after the initial exhilaration around India’s independence abated, Indian politicians were overwhelmed by the demands of managing a country of this size and complexity.

Hence, it is no surprise that India’s adolescence spanning FY1965-80 was marked by extensive trouble and strife. The adversities that India faced over this period (both internally and externally) thus played a critical role in shaping the policy choices India made during this period.

First, India ran into trouble with its neighbours and ended up fighting two full-scale wars with Pakistan (in 1965 and then in 1971) and also fought against and lost to China (1962). Then, just when policymakers were grappling with the fact that a war was a luxury that a fledgling and poor country like India could ill afford, it ran into another primitive problem, i.e. the shortage of food. India’s rapid population growth and inadequate food production capabilities meant that India had to rely on developed countries for food aid which was given with humiliating riders.

Indian policymakers’ policy decisions are heavily influenced by the international policy narrative prevalent at a particular point in time

Indian politicians were overwhelmed by the demands of managing a country of this size and complexity

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 19

Against this backdrop of a weakened global positioning and a domestic food shortage, India’s policymakers were forced to focus on enhancing the productivity of the agricultural sector and did so by embracing the ‘Green Revolution’ which was transforming agriculture in the developing world. This policy choice was a critical one as the focus on agriculture allowed India to unknowingly begin breaking away from the previous policy thrust that was centered on Soviet-style planning and growing state-owned enterprises (SOEs) that were thus far revered as the temples of modern India.

The remaining part of this policy phase section spanning FY1965-80 is divided into three sections:

The first sub-section (spanning pg 19 to pg 22) sets up the political backdrop under which the specific policy decisions were taken. It answers questions, such as what prompted India to focus on self-sufficiency in food grain production.

The second sub-section (spanning pg 22 to pg 25) details the policy changes that were affected and what specific steps were taken to enhance agricultural productivity.

The third and final sub-section (spanning pg 25 to pg 27) quantifies the macroeconomic impact of these policy changes. Our findings suggest that agricultural productivity increased substantially although there were regional disparities. This era also saw inequality decreasing.

The chart below graphically shows how this phase was characterised by:

Low GDP growth whereby the average GDP growth over FY1965-80 was recorded at 3.1% YoY as compared to the average growth rate of 6% recorded over FY1980-18.

The Congress dominating national politics, accounting for a median of 70% of seats during the General Elections held over this phase.

Inequality in India was the lowest over FY1965-80 especially so when compared to the deterioration this metric would undergo in the subsequent policy phases.

Policy phase#1 was characterised by low GDP growth, political dominance of the Congress and the persistence Exhibit 19:of a high degree of inequality

Source: CEIC, Election Commission of India, World Bank, Ambit Capital research. *Note: (1) The Gini coefficient measures the inequality among values of a frequency distribution. A Gini coefficient of zero expresses perfect equality, whereas Gini coefficient of 1 expresses maximal inequality among value. (2) Average GDP growth during this period: 3.2%, Average Gini coefficient: 0.32 and Average seat share of Congress: 58%.

Section A: The political backdrop – a country mocked by the world

“What kind of pride and prejudice this country [India] was up against is best illustrated by an interview Vijayalakshmi Pandit, [Nehru's sister, then ambassador to the US] had with Sam Rayburn, Speaker of the House and a legendary figure on the Hill at that time, from which she returned in a towering rage. It had gone something like this:

Rayburn: "Why don't you buy wheat from Pakistan which has wheat in surplus? The only reason you don't is because Hindu India wants to do down Muslim Pakistan,"

73%

54%

68%

28%

67%

0.33 0.31 0.31 0.32 0.324%

3%

5%

3%

2%

2%

3%

3%

4%

4%

5%

5%

0%

20%

40%

60%

80%

FY62 FY67 FY71 FY77 FY80

GD

P g

row

th

Sea

t sh

are

/Gin

i*

Seat share of Congress (Left scale) Gini coeff. (Left scale) Avg. GDP growth (Right scale)

India’s rapid population growth and inadequate food production capabilities meant that India had to rely on developed countries for food aid

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 20

She tried to control her temper as best she could and said testily, “India was not Hindu India, and that it had more Muslims than Muslim Pakistan." Rayburn: "Oh, you have Muslims in India! Honey, why didn't you say so earlier?"

Ambassador: "Sam, I have been saying this for two years, ever since I came here, but you don't hear and you don't understand." Whereupon Rayburn's tone suddenly changed, and he said: "No, no, now that I know, now you will have no trouble. If they give you any more trouble, honey, you just tell me."

-‘Swallowing the humiliation’ by Inder Malhotra for the Indian Express on July 12, 2010

The two decades leading to 1965 were marked by a range of socio-economic as well as foreign policy related developments which in more ways than one necessitated a shift away from Nehru’s thrust on ‘temples of modern India’ to a never-before-seen thrust on agriculture. First and foremost, India’s population growth rate was undergoing a period of rapid acceleration as birth rates expanded (see exhibit below). As compared to the current population growth rate of 1.2% YoY in FY17, India’s population growth rate had accelerated to an average of 2.1% over FY1960-65 as compared from an already high level of 1.9% YoY recorded immediately post-independence over FY1952-59.

India’s population growth rate accelerated Exhibit 20:post-independence…

Source: CEIC, Ambit Capital research

…even as foodgrain production was undergoing Exhibit 21:a deceleration!

Source: CEIC, Ambit Capital research

To compound matters, this period also saw the pace of foodgrain production slow down drastically from an average of 5.8% YoY over FY1952-59 to an average of 2.6% YoY over FY1960-65 (see exhibit above). This deceleration in foodgrain production growth rates could be mainly attributed to: (1) India’s excessive dependence on monsoons with only 10% of land having irrigation cover in FY60 (as compared to 60% now); (2) India experiencing three droughts in the 1960s (in 1965, 1966 and 1968); and (3) the exhaustion of the land’s productive capacity.

The combination of rising demand for food and slowing pace of food grain production meant that India had to deal with a crippling food scarcity problem. To meet the food shortage and to stabilise the prices, India was forced to import increasing amounts of food. The Government of India signed the controversial Trade Development and Assistance Act of 1954, commonly known as PL–480 scheme with the USA in 1956 to facilitate these imports. However, rather than being a standardised agreement, India was subjected to a great deal of humiliation in the run up to this scheme being approved by the US Congress.

The US openly looked down upon India with an air of condescension. And yet, India’s need for wheat was so pressing that it had no choice but continue negotiating with

1.9%

2.1%

2.3%

1.6%

1.8%

2.0%

2.2%

2.4%

FY52-59 FY60-65 FY65-80

Avg

. po

pu

lati

on

gro

wth

(Yo

Y ch

an

ge

, in

%)

FY52-59 FY60-65 FY65-80

5.8%

2.6%

0.0%

2.0%

4.0%

6.0%

8.0%

FY52-59 FY60-65

Avg

. fo

od

gra

in p

rod

uct

ion

g

row

th (

YoY

cha

ng

e, i

n %

)

FY52-59 FY60-65

The two decades leading to 1965 were marked by a range of socio-economic as well as foreign policy related developments

This period also saw the pace of foodgrain production slow down drastically

The combination of rising demand for food and slowing pace of foodgrain production meant that India had to deal with a crippling food scarcity problem

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 21

the US to ensure that the wheat supplies reached hungry Indian mouths. More importantly, the US took the liberty to be blatantly critical of India's foreign policy of non-alignment, i.e. neither aligning with the US nor with the USSR in the Cold War. Given the towering standing that the US enjoyed on the global stage and given that India was an inconsequential country on the global stage at this point in time, America’s treatment of India affected India’s ability to operate as a sovereign.

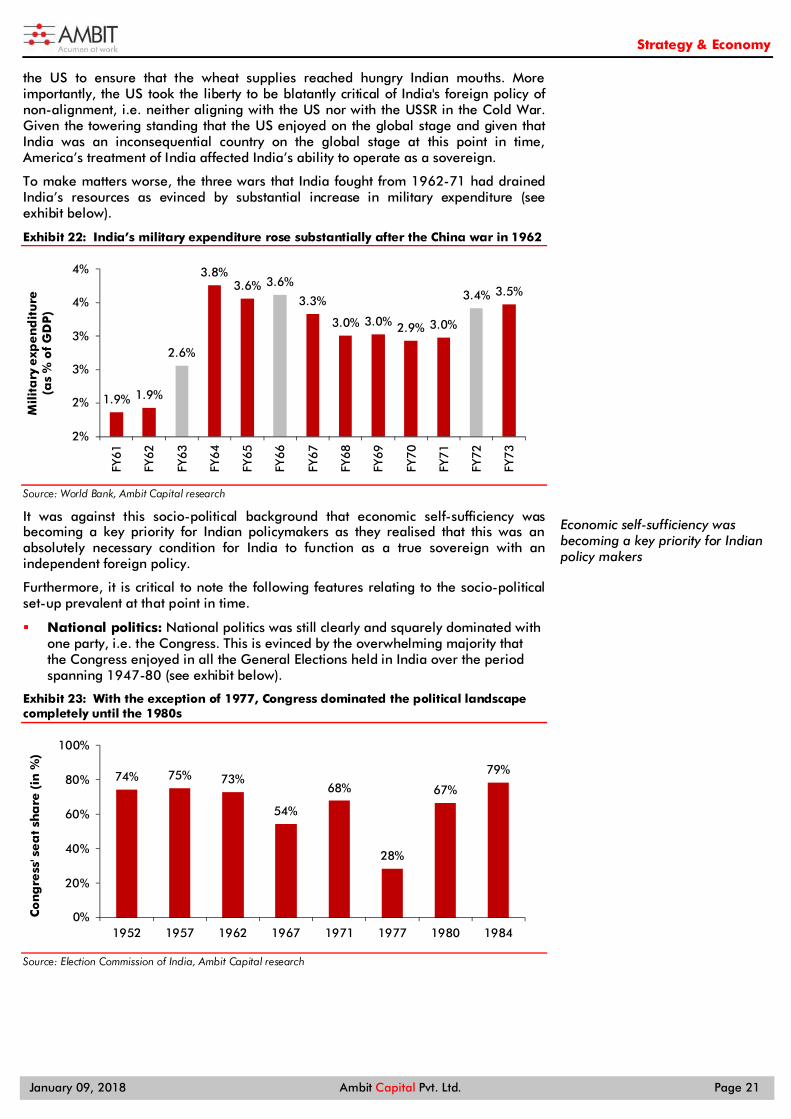

To make matters worse, the three wars that India fought from 1962-71 had drained India’s resources as evinced by substantial increase in military expenditure (see exhibit below).

India’s military expenditure rose substantially after the China war in 1962 Exhibit 22:

Source: World Bank, Ambit Capital research

It was against this socio-political background that economic self-sufficiency was becoming a key priority for Indian policymakers as they realised that this was an absolutely necessary condition for India to function as a true sovereign with an independent foreign policy.

Furthermore, it is critical to note the following features relating to the socio-political set-up prevalent at that point in time.

National politics: National politics was still clearly and squarely dominated with one party, i.e. the Congress. This is evinced by the overwhelming majority that the Congress enjoyed in all the General Elections held in India over the period spanning 1947-80 (see exhibit below).

With the exception of 1977, Congress dominated the political landscape Exhibit 23:completely until the 1980s

Source: Election Commission of India, Ambit Capital research

1.9% 1.9%

2.6%

3.8%3.6% 3.6%

3.3%

3.0% 3.0% 2.9% 3.0%

3.4% 3.5%

2%

2%

3%

3%

4%

4%

FY61

FY62

FY63

FY64

FY65

FY66

FY67

FY68

FY69

FY70

FY71

FY72

FY73

Mil

ita

ry e

xpe

nd

itu

re(a

s %

of

GD

P)

74% 75% 73%

54%

68%

28%

67%

79%

0%

20%

40%

60%

80%

100%

1952 1957 1962 1967 1971 1977 1980 1984

Co

ng

ress

' se

at

sha

re (

in %

)

Economic self-sufficiency was becoming a key priority for Indian policy makers

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 22

The fact that Indian politics was a single-player game mattered, because this was one of the main reasons why the Congress was only focused on solving immediate economic problems (like that of food scarcity) rather than pursuing goals, such as economic liberalisation or infrastructure creation.

The party’s grip on power over FY1965-80 was such that it did not feel the need to boost the prospects of India’s private sector as there was no other political party with which it was competing for access to political funding.

Indian politics would become a multi-player game from the 1980s and this would coincide with policymakers according a high priority to boosting GDP growth, to economic liberalisation and to growing infrastructure networks (see pg 27 of this note for the section titled “Policy phase#2: From Socialism to Liberalisation FY1980-1995” and see pg 37 of this note for the section titled “Policy phase#3: India creates networks FY1995-2018”).

The international context: The world economy had been split into two camps with political affiliations as well as economic philosophy determined by Cold War alliances. Those aligned with the US were opting for the Western model of capitalism and whilst those aligned with the USSR were leaning towards Communism. India’s fierce desire to be non-aligned also meant it did not want to explicitly embrace capitalism at this point in time and hence opted to be a ‘mixed economy’.

Hence, it was only after the intensity of the Cold War softened in the 1980s that Indian policymakers became ready to embrace an economic system where the Government did not play a central role.

State of infrastructure & networks: It is critical to note that in this era the roads and railway networks created by the British were still sufficient to service the Indian populace.

Thus, building ‘networks’ was not a pressing demand made by the electorate, and consequently this was not a priority for Indian policymakers at this stage.

The need for creating networks would rise as a top priority from 1995 as India’s gaping infrastructure deficit would threaten to stall India’s GDP growth rate (see pg 27 of this note for the section titled Policy phase#3: India creates networks FY1995-2018).

Section B: Detailing the policy changes

The phenomenon of Green Revolution is defined as a series of research, development, innovation and technology transfer initiatives that were launched in the developing world from the 1960s and that resulted in increasing India’s agriculture production.

Norman Borlaug, an American agronomist, is credited as being the father of Green Revolution was awarded the Padma Vibhushan - India’s second highest civilian honour - in 2006 for his role in boosting agricultural productivity in India. The other thinkers and leaders who played a critical role in precipitating India’s Green Revolution were C. Subramaniam (India’s Agriculture minister over 1964-66), Indira Gandhi (the then Prime Minister) and MS Swaminathan (agricultural scientist).

Eminent people associated with Green Revolution Exhibit 24:Person Designation

Norman Borlaug American Agronomist and Father of Green Revolution

C. Subramaniam India’s Agriculture minister over 1964-66

MS Swaminathan Agricultural Scientist (Indian Agricultural Research Institute [IARI]).

Indira Gandhi India’s Prime Minister over 1966-77

Source: Ambit Capital research

The process for increasing foodgrain productivity started in 1962 when Borlaug’s hybrid seeds were tested in Punjab and Haryana. Thereafter, severe food shortage forced India to adopt high yielding variety (HYV) seeds (which Norman Borlaug has developed) and the use of fertilisers to boost agricultural productivity thereby leading other regions, such as Eastern and Southern India to adopt the same (see exhibit below).

The world economy had been split into two camps with political affiliations as well as economic philosophy determined by Cold War alliances

The process for increasing foodgrain productivity started in 1962

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 23

How the Green Revolution spread in India over the 1960s Exhibit 25:

Time period Description

March 1962 Borlaug’s dwarf spring wheat strains were grown in the fields of the Indian Agricultural Research Institute (IARI) in Pusa, New Delhi.

March 1963 Rockefeller Foundation and the Mexican Government sent Borlaug and Dr. Robert Glenn Anderson to India to continue his work.

October 1965 New policy was put into practice when 114 districts (out of 325) were selected by the Ministry of Agriculture for an Intensive Agricultural Areas Programme (I.A.A.P.).

November 1965 Food Ministry was ready for the implementation of a High Yielding Varieties Programme in districts that had already been selected for intensive development under the I.A.D.P. and I.A.A.P. schemes

September 1966 India spent USD2.5 million for 18,000 tons of Mexican wheat seed, the largest purchase and import of any seed in the world at that time.

Source: Ministry of Agriculture, Ambit Capital research

Following the rapid introduction of high yielding wheat varieties, the production of wheat in India consistently started exceeding the 20-million tonne mark which was significantly more than the previous peak output of 12.3-million tonne achieved in the last good weather year of FY65 (see exhibit below).

Wheat production increased substantially after the Green Revolution Exhibit 26:

Source: Ministry of Agriculture, Ambit Capital research

Even as India’s wheat production grew rapidly over this period, it is worth noting that the Green Revolution in India did not have the far reaching impact it ought to have had owing to a range of political and socio-economic reasons.

Firstly, regionally, in India, the greatest impact of the Green Revolution was in the wheat-growing areas of Punjab, Haryana and Western Uttar Pradesh. Unfortunately, the rest of India experienced only a marginal improvement in productivity (see exhibit below).

The Green Revolution’s effect was not evenly distributed across India Exhibit 27:

Source: CEIC, Ambit Capital research

Secondly, the Green Revolution resulted in a meaningful boost for India’s wheat productivity even as rice productivity rose by a lesser degree (see exhibit below).

1012

10 11

1719

20

2426

25

0

5

10

15

20

25

30

FY64 FY65 FY66 FY67 FY68 FY69 FY70 FY71 FY72 FY73

Wh

ea

t p

rod

uct

ion

(in

mil

lio

n t

on

ne

s)

-4%

0%

4%

8%

Mah

aras

htra

Punj

ab

Har

yana

Goa

Guj

arat

Wes

t Ben

gal

Kar

nata

ka

And

hra

Prad

esh

Indi

a

Tam

il N

adu

Him

acha

l…

Utta

r Pr

ades

h

Raja

stha

n

Biha

r

Ori

ssa

Ker

ala

Mad

hya

Prad

esh

Exp

on

en

tia

l gro

wth

of

Ag

ri(F

Y71

-80

)

Following the rapid introduction of high yielding wheat varieties, the production of wheat in India consistently started exceeding the 20-million tonne

Green Revolution in India did not have the far reaching impact it ought to have had owing to a range of political and socio-economic reasons

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 24

The Green Revolution only boosted productivity of wheat Exhibit 28:

Source: Ministry of Agriculture, Ambit Capital research

Thirdly, it is worth noting that the adoption and success of the Green Revolution related technology was affected to a great extent by the historical property relations (i.e. tenancy laws for agricultural lands) prevalent in India at that point in time. These systems held back agricultural sector growth mainly because there was no incentive for the cultivator/tenant to boost agricultural productivity leading to the rise of a classic agency-principal problem.

The table below details the extent of economic inefficiencies created by each of these land relations’ systems (see exhibit below).

The land tenure system set up by the British especially the zamindari system were unproductive Exhibit 29:Land tenure system Details

Zamindari or landlordism

-Under this system, most of the land was owned by a handful of people called the landlords. This landlord was entrusted by the British to collect taxes. This person, the Zamindar, thus had free reign and was able to set the terms of engagement for all of his peasants which were often unfair. - Not only could the landlord expel peasants who did not pay their taxes, but if a peasant did not pay taxes then his land was confiscated. This set the stage for social disparity as those who could not afford land were stripped of their ownership rights. Why was this system problematic from the perspective of adopting high yielding varieties? The zamindari system was inherently opposed to the capitalistic way of farming where the tenant had no incentive to increase productivity as it was appropriated by the landlord.

Raiyatwari

- Under the Raiyatwari system, taxes were collected directly from the cultivator, or raiyat. This meant that the cultivator actually owned the rights to their land. The taxes were not fixed as they were with the Zamindari system and instead they were calculated based on average annual output. - Furthermore, taxes then varied from place to place depending on soil types and were adjusted in response to changes in the productivity of the land. Why was this system less problematic from the perspective of adopting high yielding varieties? As the cultivator owned the rights of the land, it was in his incentive to adopt practises which could yield high growth.

Mahalwari

- This was a system prevalent in the Northwest states of India as well as Punjab. - As per this system the village was jointly owned by a group of cultivators who as a group were responsible for the collection of taxes. This system was very flexible and inconsistent; in some cases the groups in charge consisted of many people and in others there was only one or a few in charge, making it similar to Zamindari tenure. Why was this system also less problematic from the perspective of adopting high yielding varieties? Peasants or tenants have direct incentive to increase productivity unlike the zamindari system

Source: Ambit Capital research

0

1,000

2,000

3,000FY

61

FY63

FY65

FY67

FY69

FY71

FY73

FY75

FY77

FY79

FY81

FY83

FY85

FY87

FY89

Yie

ld(K

g/h

ect

are

)

Rice Wheat

Adoption and success of the Green Revolution related technology was affected to a great extent by the historical property relations

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 25

The acceptance of Green Revolution technology was low in areas Exhibit 30:dominated by the Zamindari system (refer to areas highlighted in pink below)

Source: Indmaps, Ambit Capital research, Note: The region highlighted in pink was characterised by the Zamindari system.

Consequently, the new technology made available under the Indian Green Revolution was more readily accepted in areas (such as Punjab and Haryana) where pre-existing property relations were conducive to capitalist farming. Areas such as Bengal, Bihar, Orissa, modern-day Madhya Pradesh, Tamil Nadu and Andhra Pradesh that were historically under Zamindari system were able to imbibe very little of the Green Revolution technology.

Section C: The economic impact - India became self-sufficient on food, inequality reduced but headline GDP growth remained weak

The Central policymakers’ thrust on agriculture boosted the farm sector’s share of GDP from 38% in FY60 to 43% by FY80. This yielded two sets of benefits, namely: (1) India became self-sufficient on the food front, and (2) inequality in India abated as 75% of India’s population was employed in the farm sector.

However, just when India was able to manage a degree of order domestically, a whole host of Asian countries successfully overtook India on headline GDP growth rates as they successfully re-invented their economies. Moreover, average GDP growth in India came down during FY1965-80 at 3.2% as compared to 4.4% during FY1952-65. Likewise, the coefficient of variation (CV) of real GDP growth (a measure of the volatility of the GDP growth) remained high during FY1965-80 at 1.2 as compared to 0.5 during FY1952-65.

Impact on GDP growth - Whilst farm sector growth picked up, non-farm sector growth decelerated!

Whilst farm sector growth received an instant shot in the arm as a result of Green Revolution, the impact of these reforms on overall GDP growth was insignificant (see exhibit below).

A whole host of Asian countries successfully overtook India on headline GDP growth rates as they successfully re-invented their economies

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 26

The period spanning FY1965-80 saw farm sector growth pick-up Exhibit 31:but headline growth remained lackluster

Period Growth rate (in %)

GDP Non-farm Farm

Pre-Green Revolution (FY51-65) 3.9% 5.6% 2.7% Green Revolution period (FY66-80) 3.6% 4.4% 2.8%

Delta +30bps -120bps +10bps

Source: CEIC, Ambit Capital research

Whilst the rest of Asia at this point in time was undergoing rapid industrialisation, such was the absence of all-round economic reforms in India that India’s GDP growth started lagging that of Asian peers (see exhibit below).

India’s GDP growth started lagging behind that Exhibit 32:of the Asian countries in the 1970s

Source: CEIC, Ambit Capital research

India’s per capita income started lagging Exhibit 33:behind that of China in the seventies

Source: CEIC, Ambit Capital research

Unsurprisingly, by the 1970s India’s GDP per capita fell behind that of China’s (see exhibit above).

Impact on inflation - Low oil prices and improvement in food supply lowered inflation

Consumer price inflation in India went into double digits over FY1964-67 due to a fall in agricultural production triggered by the frequent drought of the sixties. Then, the combination of contained oil prices and the Green Revolution driven increase in agricultural production resulted in the lowering of inflation by the late 1960s. However, the oil price shock of the early 1970s again pushed inflation back into double digits (see exhibit below).

Inflation levels in India were volatile over FY1965-80 Exhibit 34:

Source: CEIC, Ambit Capital research

-10%

0%

10%

20%

30%

197

0

197

2

197

4

197

6

197

8

198

0Re

al G

DP

gro

wth

(in

%)

India

China

Indonesia

Japan

Korea

6

7

8

9

10

1950

1957

1964

1971

1978

1985

1992

1999

2006

GD

P p

er

cap

ita

, 19

90

US$

(in

lo

g) India

China

South-EastAsia

2% 4% 3%

13%9%11%

13%

3%1%

5% 3%6%

17%

29%

6%

-8%

8%

3%6%

11%

-10%

0%

10%

20%

30%

40%

FY61

FY62

FY63

FY64

FY65

FY66

FY67

FY68

FY69

FY70

FY71

FY72

FY73

FY74

FY75

FY76

FY77

FY78

FY79

FY80

CP

I (Y

oY

cha

ng

e, i

n %

)

India’s GDP growth started lagging that of Asian peers

Consumer price inflation in India went into double digits over FY1964-67 due to a fall in agricultural production triggered by the frequent drought of the sixties

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 27

After the first oil shock of early 1970s, consumer inflation remained under control in the late 1970s before it started rising again starting 1980.

Impact on equality - The reforms of FY1965-80 lowered inequality

The most progressive development over this policy phase was the fact that inequality not only remained low in India compared to the other South East Asian nations, but it actually reduced over this period. This dynamic of a reduction in income inequality would elude India over the two subsequent policy phases (see exhibit below).

Inequality in India remained low during FY1965-80 Exhibit 35:

Source: World Bank, Ambit Capital research. * Gini coefficient is a measure of statistical dispersion intended to represent the income or wealth distribution of a nation's residents, and is the most commonly used measure of inequality. Higher the Gini coefficient higher the inequality

Policy phase#2: From socialism to liberalisation (FY1980-95) “No power on earth can stop an idea whose time has come”

- Dr. Manmohan Singh quoting Victor Hugo in his landmark budget speech (July 1991)

Contrary to popular belief, India began the process of transitioning away from socialism in the 1980s and not in 1991. Even as the dream team comprising of PV Narsimha Rao (India’s PM from 1991- 96), Manmohan Singh (FM from 1991-96) and S.P. Shukla (Finance Secretary in 1991) are credited with initiating this transition, in more ways than one, this change was initiated a decade ago by the Gandhi family and some unsung heroes (see exhibit below for details).

The unsung heroes of India’s liberalisation process Exhibit 36:

Prime Ministers Finance Ministers Key civil servants

Indira Gandhi (1980-84)

R Venkataraman, Pranab Mukherjee P. C. Alexander (Principal Secretary to the PM) and I.G. Patel (Governor, RBI)

Rajiv Gandhi (1985-89) V.P Singh Sam Pitroda (Technological Advisor to Rajiv Gandhi)

PV Narsimha Rao (1991-96) Manmohan Singh

A.N Verma (Principal Secretary to the Prime Minister), Suresh Mathur (Industry Secretary), Naresh Chandra (Cabinet secretary), S.P. Shukla (Finance Secretary), Montek Singh Ahluwalia (Finance secretary)

Source: Ambit Capital research

The remaining part of this policy phase spanning FY1980-95 is divided into three sections.

The first sub-section (spanning pg 28 to pg 30) sets up the political backdrop that caused a relatively agrarian and poor country’s transition from socialism to a more pro-business and pro-market economy. We hypothesise that a combination of rising political competition and international pressure led the politicians of a poor country like India to embrace pro-market reforms.

0.24

0.28

0.32

0.36

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

Gin

i co

eff

icie

nt f

or

ine

qu

ali

ty*

India South-East Asia

The most progressive development over this policy phase was the fact that inequality not only remained low in India compared to the other South East Asian nations, but also reduced.

India began the process of transitioning away from socialism in the 1980s and not in 1991

Strategy & Economy

January 09, 2018 Ambit Capital Pvt. Ltd. Page 28

The second sub-section (spanning pg 30 to pg 33) details the policy changes that were affected. This section describes in detail what market-oriented and industry-friendly policies were pursued in order to unshackle India’s economy from the licence-permit-quota raj.

The third and final section (spanning 33 to pg 36) quantifies the macroeconomic impact of these policy changes. Our findings suggest that, whilst the change in economic philosophy clearly boosted India’s GDP growth and brought India’s inflation rates lower, the changes worsened indicators relating to income inequality.

Policy phase#2 was characterised by high growth, superior market returns, a rise in political competition and a Exhibit 37:rise in inequality

Source: Bloomberg, CEIC, World Bank, Election Commission of India, Ambit Capital research *Note: (1) The Gini coefficient measures the inequality among values of a frequency distribution. A Gini coefficient of zero expresses perfect equality, whereas Gini coefficient of 1 expresses maximal inequality among value. (2) Average GDP growth during this period: 4.7%, Average Gini coefficient: 0.33, Average seat share of Congress: 51% and Average Sensex returns: 27%