study guide economics 2

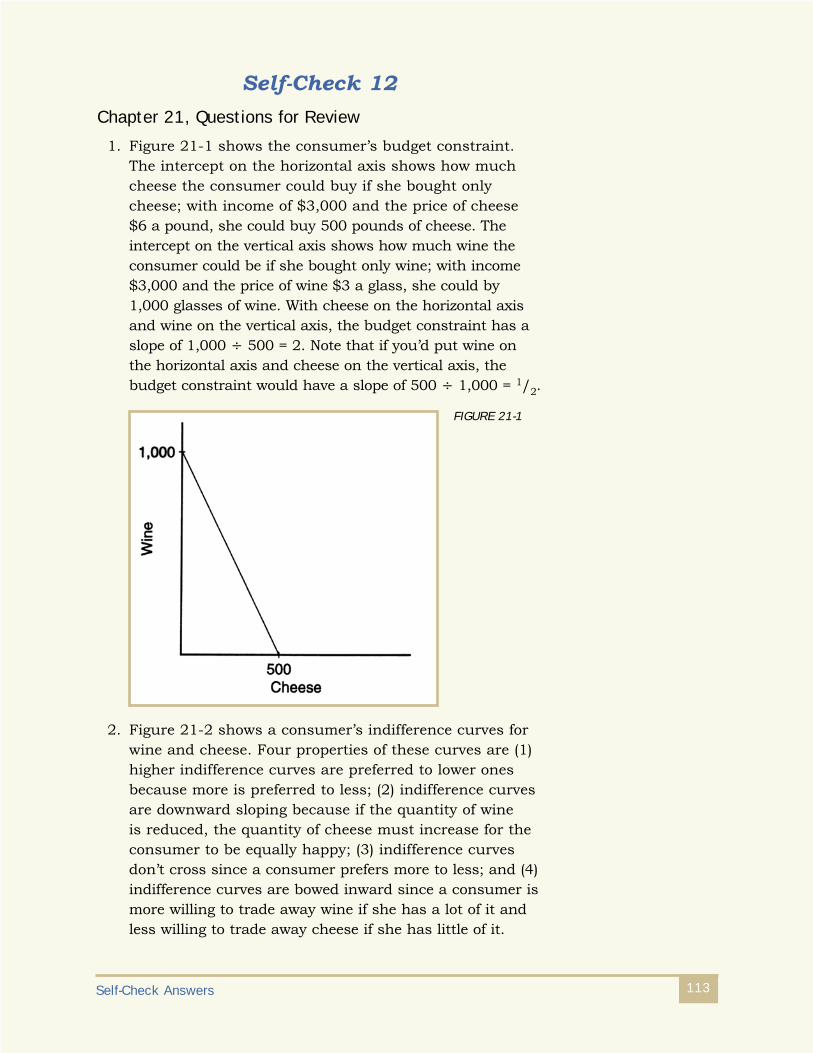

TRANSCRIPT

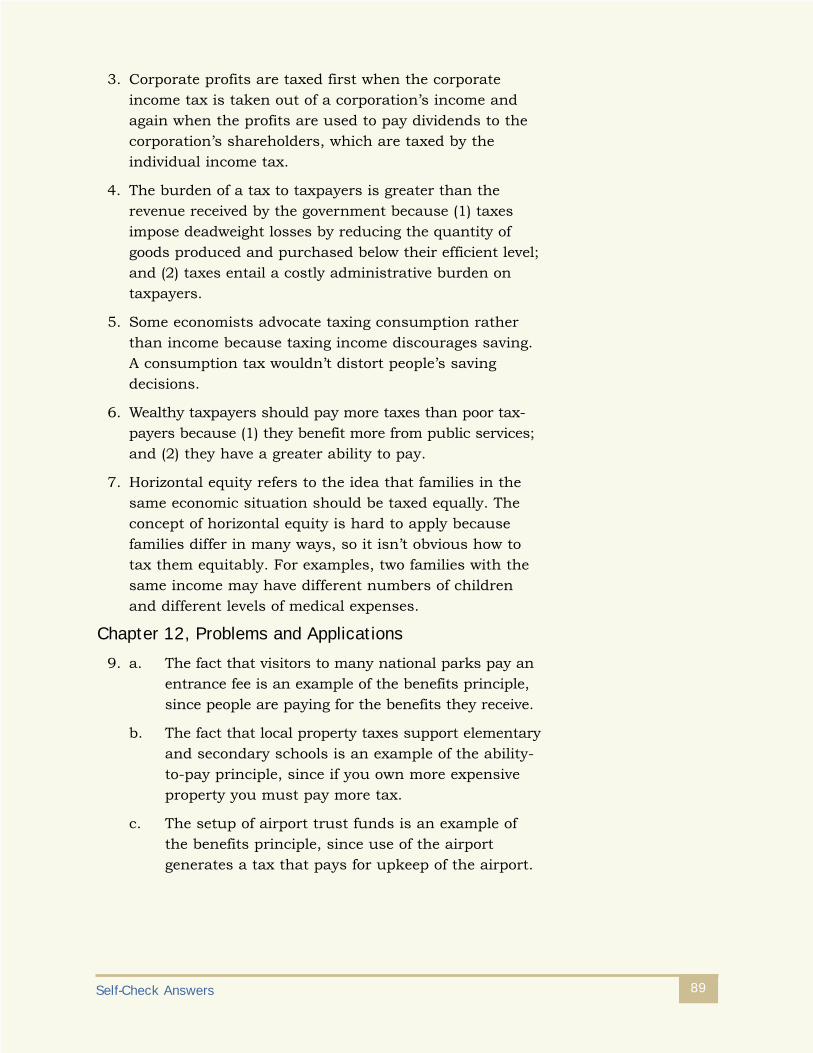

Study Guide

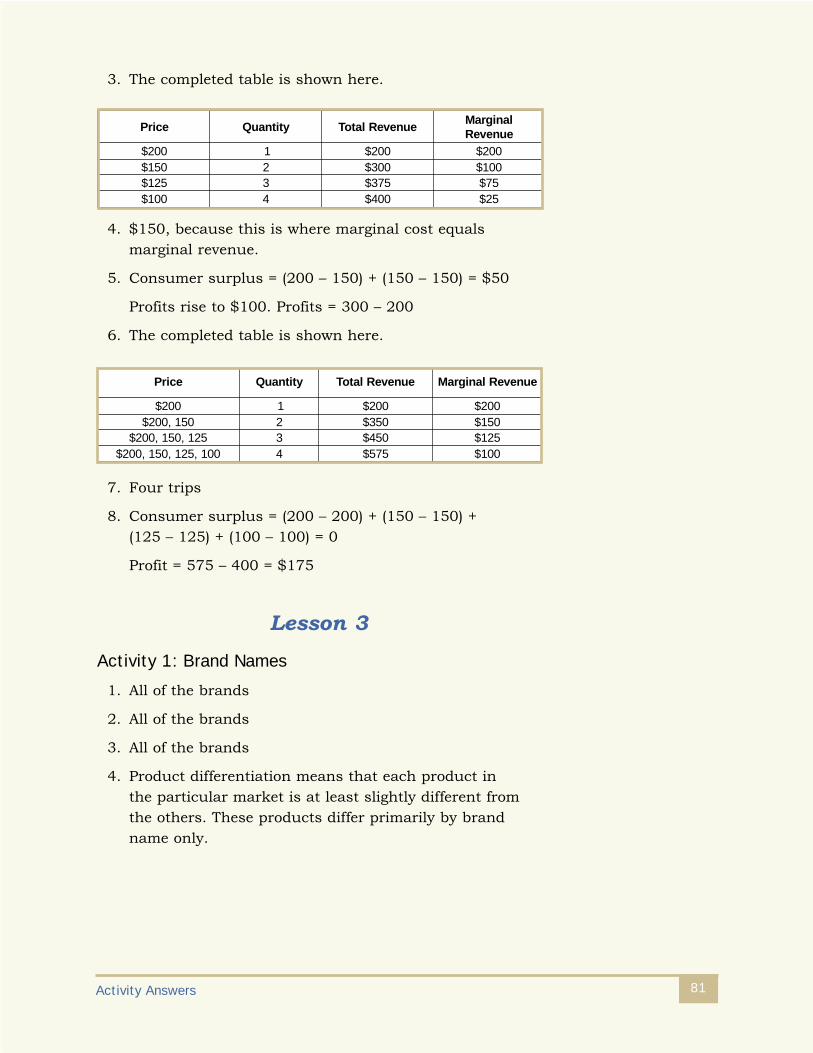

Economics 2

INSTRUCTIONS TO STUDENTS 1

LESSON ASSIGNMENTS 5

LESSON 1: THE ECONOMICS OF THEPUBLIC SECTOR 7

EXAMINATION—LESSON 1 19

LESSON 2: FIRM BEHAVIOR AND MONOPOLIES 23

EXAMINATION—LESSON 2 37

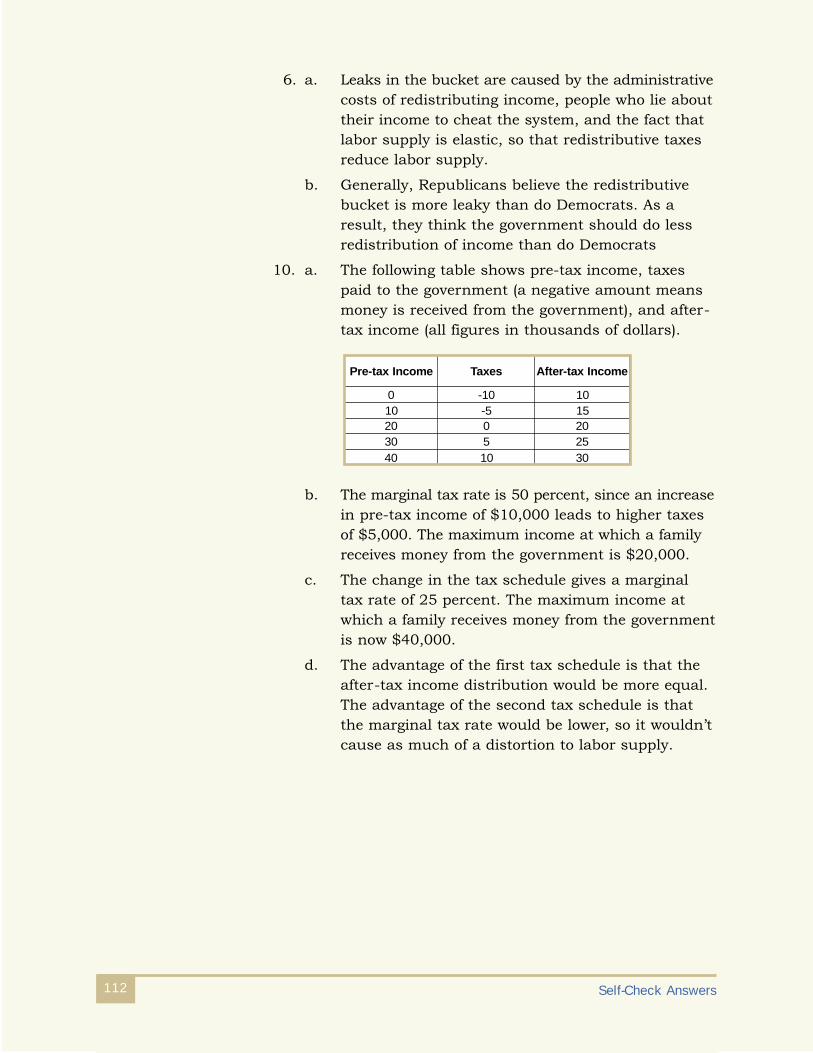

LESSON 3: OLIGOPOLY, MONOPOLISTIC COMPETITION, AND THE FACTORS OF PRODUCTION 41

EXAMINATION—LESSON 3 53

LESSON 4: LABOR MARKETS; FURTHERAPPLICATIONS OF MICROECONOMICS 57

EXAMINATION—LESSON 4 75

ACTIVITY ANSWERS 79

SELF-CHECK ANSWERS 85

iii

Co

nt

en

ts

Co

nt

en

ts

1

YOUR COURSEWelcome to Economics 2! This course is designed to introduceyou to the world of economics. If you’re not planning onbecoming an economist, you may wonder, why bother learningabout economics? Well, the author of your textbook, Principlesof Microeconomics, offers a few very convincing and practicalreasons. First, you’ll gain a better understanding of the worldin which you live. For instance, after completing this courseyou’ll know why airlines charge less for a round-trip ticket if a traveler stays over a Saturday night and why an NFLquarterback makes so much money. Second, when you havea fundamental knowledge of economics, you’re an informedparticipant in the economy. This knowledge will help you tomake better decisions on how much of your income to spend,how much to save, and how to invest your savings. Third,you’ll be better equipped to make logical voting decisions if youunderstand the potential and limits of economic policy. As avoter, you choose the candidate who makes the policies thatguide the allocation of society’s resources. Economic questionsare considered when making decisions about taxation, welfareprograms, and free trade. As you can see, the principles ofeconomics are useful in many of life’s everyday situations.

OBJECTIVESWhen you complete this course, you’ll be able to

■ Use economic data to measure the cost of living

■ Describe the forces that determine key economic variables

■ Explain the importance of the monetary systems indetermining the long-run behavior of nominal variables

■ Identify the significant factors in a nation’s economicinteractions with other nations

■ Explain short-run economic fluctuations

KNOW YOUR TEXTBOOKYour textbook, Principles of Microeconomics, is the heart ofthis course. It’s very important that you read the material inthe text and study it until you’re completely familiar with it.This is the material that your examinations will be based on.

Instru

ctio

ns

Instru

ctio

ns

Instructions to Students2

Now that you have an idea of what to expect from your course,take a moment to read through the following description ofthe learning materials that you received.

1. Your textbook, Principles of Microeconomics, FourthEdition, by N. Gregory Mankiw, will introduce you to the basic concepts of microeconomics. It contains theassigned readings and review exercises that are assignedas self-checks.

2. This study guide, which includes an introduction to yourcourse and presents a summary of the material you’llcover in each lesson. This guide also contains the following features:

■ An assignments page that lists all of the readingassignments for your textbook

■ Introductions to your lessons

■ Self-checks for each lesson

■ Suggested Activities for each lesson

■ Answers to the self-checks and Suggested Activities (at the back of this study guide)

■ The examinations for your course

A STUDY PLAN

We’ve divided the contents of Principles of Microeconomicsinto four lessons for you to study. You’ll note that the lessonassignments in this study guide begin with Chapter 10. (Thefirst nine chapters in the textbook are identical to the firstnine chapters you studied if you completed the Economics 1course. Before you start this course, you may want to reviewthose chapters.)

For each lesson, you’ll read part of the textbook. Then, you’ll complete an examination on the material you read forthe lesson. This study guide contains a list of your lessonassignments as well as the lesson examinations. Be sure toread all the material in both the textbook and the study guidebefore you attempt to complete your examinations.

Instructions to Students 3

To get the most benefit out of each of your lessons, we suggest that you follow these steps:

Step 1: Start by reading the introduction to Lesson 1 in this study guide. Then, begin to read Assignment 1.This is the first reading assignment of Lesson 1.Pay attention to the new ideas and concepts thatare introduced, and carefully note the pages inyour textbook where the reading assignmentbegins and ends.

Step 2: Very briefly, skim the assigned pages in your textbook to get a general idea of their contents.

Step 3: Now, read the assigned pages in the textbook. Try to see the “big picture” of the material duringthis first reading.

Step 4: Next, go back and study the assigned pages inyour textbook carefully. Pay careful attention to all details, including the graphs that are includedin the textbook. It’s a good idea to take notes onthe important points and terms in a notebook. We also encourage you to enter your self-checkanswers and suggested activity answers in thesame notebook. Your notebook will be a helpfulstudy tool.

Step 5: At the end of each reading assignment, reviewwhat you’ve learned by completing the self-check.The self-checks consist of selected Questions forReview and Problems and Applications from yourtextbook. Write out the answers to these questionsin your notebook or on a separate piece of paper.Try to answer the questions on your own withoutlooking in the textbook. Don’t worry about makinga mistake. The purpose of answering these questionsis to review the material and to help you recognizethe areas that you may need to study again.

When you’ve completed each self-check, check youranswers against those provided at the back of thisstudy guide. If you answered any of the questionsincorrectly, go back and review the material for that

Instructions to Students4

topic until you’re sure that you understand it.Remember that the self-checks are provided only for you to review your learning. You won’t begraded on these questions in any way. Do notsend your answers to the school.

Step 6: Next, complete the Suggested Activities that are provided at the end of selected reading assignments. The Suggested Activities are prac-tical application exercises that allow you to use the knowledge and information you’ve gained fromthe reading assignments. Write out the answers to the Suggested Activities in your notebook or on a separate piece of paper.

When you’ve completed the Suggested Activities foreach lesson, check your answers against those pro-vided at the back of this study guide. You won’t begraded on your Suggested Activity work. Do notsend your answers to the school.

Step 7: Repeat Steps 1 through 6 for each of the remaining reading assignments in the lesson.

Step 8: When you’ve finished reading all of the assigned textbook pages for a lesson and you’re sure that you’re comfortable with the material, com-plete the examination for that lesson. The lesson examinations are contained in this study guide.

Step 9: Repeat these steps until all four lessons have been completed.

Remember, you may e-mail your instructor for help wheneveryou need it.

Now, look over the lesson assignments. Then, begin yourstudy of Principles of Microeconomics with Lesson 1.

Good luck with your course!

5

Lesson 1: The Economics of the Public Sector

For: Read in the Read instudy guide: Principles of

Microeconomics:

Assignment 1 Pages 8–11 Pages 203–220

Assignment 2 Pages 11–13 Pages 223–237

Assignment 3 Pages 14–16 Pages 241–261

Examination 05066700 Material in Lesson 1

Lesson 2: Firm Behavior and Monopolies

For: Read in the Read instudy guide: Principles of

Microeconomics:

Assignment 4 Pages 24–26 Pages 267–284

Assignment 5 Pages 26–29 Pages 289–307

Assignment 6 Pages 29–32 Pages 311–339

Examination 05066800 Material in Lesson 2

Lesson 3: Oligopoly, Monopolistic Competition, and theFactors of Production

For: Read in the Read instudy guide: Principles of

Microeconomics:

Assignment 7 Pages 42–45 Pages 345–367

Assignment 8 Pages 45–47 Pages 373–387

Assignment 9 Pages 47–49 Pages 393–410

Examination 05066900 Material in Lesson 3

Assig

nm

en

tsA

ssig

nm

en

ts

Lesson Assignments6

Lesson 4: The Economics of Labor Markets

For: Read in the Read instudy guide: Principles of

Microeconomics:

Assignment 10 Pages 58–61 Pages 413–428

Assignment 11 Pages 61–65 Pages 431–450

Assignment 12 Pages 65–68 Pages 455–478

Assignment 13 Pages 68–72 Pages 483–501

Examination 05067000 Material in Lesson 4

7

The Economics of thePublic Sector

INTRODUCTION

In Economics 1, we developed the rationale for the market as a means to maximize society’s well-being. Markets are anefficient way to decide how to use society’s scarce resources.You learned that voluntary exchange is a win-win situationin which both parties (and society as a whole) are made better off.

Now, in this lesson, we’ll consider the situation in which themarket doesn’t perform efficiently. This occurs when decisionmakers don’t bear all the costs or realize all the benefits oftheir actions. Government plays a role in correcting suchmarket imperfections. We’ll also look at government’s role inthe allocation of public goods, which are those that are avail-able free of charge. Public goods aren’t subject to the marketforces that would normally allocate resources. You’ll learnabout the government’s role in regulating public goods thatare consumed simultaneously by multiple users who don’tpay for them.

Obviously, the government must generate revenues to payfor its expenditures in correcting the problems caused byexternalities and public goods. This is done through taxes.We’ll analyze the characteristics and economic impact of the U.S. tax system. You’ll learn about the efficiency cost or deadweight loss from taxes, the incidence of taxes, andthe equity effects of taxation.

OBJECTIVES

When you complete this lesson, you’ll be able to

■ Explain why externalities can make market outcomes inefficient

■ Discuss private solutions and government solutions to problems of externalities

Le

ss

on

1

L

es

so

n

1

Economics 28

■ Explain graphically the effects of positive and negative externalities

■ Use the Coase theorem to explain when an externality can be negotiated through the market

■ List the defining characteristics of a public good and a common resource

■ Evaluate cost-benefit analysis as it applies to government programs

■ Discuss the significance of poorly defined propertyrights in overconsumption of common resources

■ Describe how the U.S. government raises and spends money

■ Describe the tradeoff between efficiency and equityin the design of a tax system

■ Identify the major sources of revenue for our government at the federal, state, and local level

ASSIGNMENT 1Read this introduction to Assignment 1. Then, studyChapter 10, “Externalities,” on pages 203–220 in the textbook Principles of Microeconomics.

So far in your study of microeconomics, we’ve assumed thatthe producer bears all costs of production and the buyercaptures all benefits of consumption. In reality, a third partycan be affected by an activity, either by bearing some of thecosts or by receiving some of the benefits. We call this impacton the third party an externality.

The market equilibrium isn’t efficient when these externalitiesoccur. When externalities exist, decision makers make choiceswithout taking into account all of the marginal effects oftheir actions, namely, the effects on others. If externalitiesare negative (as in the case of pollution), production will beexcessive because the external portion of the marginal cost of production is ignored.

The supply curve represents the private costs of the decisionmaker without taking into account the external social cost ofpollution. For the outcome to be socially optimal, the supplycurve must include all the social costs of production, even

Lesson 1 9

those that are external to the producer. These additionalcosts would reduce the supply (shift the supply curve to theleft), reducing equilibrium quantity and raising price. Inshort, negative externalities result in too much productionbeing sold at too low a price for efficiency.

When positive externalities exist, the market underproduces.In the case of consumption externalities, the private valuefrom the product is less than the social value, including benefits to third parties. The result is a private demandcurve that understates the benefits of the product to society.An example is education. Much of the benefit from educa-tion goes to society at large. Consequently, without a publicsubsidy, an individual would look only at his or her personalbenefits and underconsume education relative to society’soptimal level.

Remember that the inefficiency from externalities resultsbecause the marginal costs and marginal benefits to the indi-vidual fail to include effects on a third party. If a change inbehavior would benefit a third party, then it’s reasonable tothink that the third party could negotiate with the decisionmakers to change their behavior. If the change in behavior is worth more to the third party than it would cost the deci-sion makers, then together they should be able to make adeal that would benefit everyone concerned. This is the basicpremise of the Coase theorem: When the interested partiescan get together to negotiate, they can work out a voluntarydeal that makes everyone better off and increases society’swell-being. For example, those who are hurt by pollutionfrom a paper mill can negotiate a solution with the com-pany. They can either pay the mill to cut back on pollutionor negotiate compensation for the damage that they incurfrom the mill’s pollution in its future production decisions.Once a deal is struck, the externality disappears.

Unfortunately, such private solutions don’t always work.Negotiating involves cost, especially when it requires coordi-nating the actions of a large number of people throughout a large geographic area. Private solutions work best whenthere are small numbers of third-party victims who are easilyidentified and can be organized to work together in negotiat-ing a solution.

Economics 210

Traditional control of externalities such as pollution hasbeen in the form of direct regulation. With regulation, thegovernment simply mandates the level of cleanup that mustoccur. This works reasonably well in cases in which theexternal costs to society are so high that fine-tuning the levelof cleanup isn’t as important as simply stopping pollutionquickly. For example, after the publication in 1969 of RachelCarson’s book Silent Spring, which described the long-termenvironmental damage done by certain pesticides, the gov-ernment banned the use of the pesticide DDT. In most cases,however, the proper level of cleanup is difficult to determine.Direct regulation puts the entire burden for measuring socialcosts and benefits on the government, and it provides noincentive for polluters to develop better cleanup technology.On the contrary, if producers develop new technology, thegovernment might respond simply by tightening the environ-mental standards.

Instead of regulation, society can use market-based policiesthat provide incentives for individual decision makers to takeinto account all of the relevant costs of production. Theseincentives can take the form of pollution taxes, subsidies, or tradable pollution permits. Each of the policies has thesame effect. It causes the decision makers to internalize the external cost of pollution by raising the opportunity costof polluting. Instead of mandating the level of reduction ofsulfur dioxide by a paper mill, for example, the EPA couldimpose a $5 tax on each unit of pollutant emitted. Clearly,this would raise the private opportunity cost of polluting by $5/unit. However, as suggested by the Coase theorem, a $5-per-unit subsidy to not pollute would have the sameeffect as a $5 tax on each unit of pollution. If pollutingmeans giving up a $5 subsidy, then the opportunity cost of polluting is still $5 under the subsidy, just as it wouldhave been under the tax.

Similarly, if the EPA distributes pollution permits that aretradable, then the opportunity costs of using a permit torelease sulfur into the atmosphere is the foregone incomefrom selling the permit. If the permit has a market value of$5, then the opportunity costs of polluting is still $5.

In each case, the market-based policy internalizes the cost of pollution. Unlike the case of direct regulation, such market-based policies also provide an incentive for the polluter to

Lesson 1 11

develop better technology to reduce the internal cost of pollution. In the previous example, every one-unit reductionin pollution saves the firm $5, unlike direct regulation, whichprovides no financial incentive to reduce the quantity of pollution below the mandated maximum level.

After you’ve carefully read pages 203–220 in Principlesof Microeconomics, complete Self-Check 1. Check youranswers with those provided at the back of this studyguide. When you’re sure that you understand the mate-rial from Assignment 1, move on to Assignment 2.

ASSIGNMENT 2Read this introduction to Assignment 2. Then, readChapter 11, “Public Goods and Common Resources,” onpages 223–237 in the textbook Principles of Microeconomics.

In this chapter, you’ll learn how governments can sometimesimprove market outcomes. Private market forces aren’t atwork when a good doesn’t have a price attached to it. Thesegoods aren’t necessarily produced and consumed in theproper amounts. To understand which type of good is regu-lated by a competitive marketplace and which type of goodisn’t, you must know how goods are categorized.

Self-Check 1

At the end of each section of Economics 2, you’ll be asked to pause and check your under-standing of what you’ve just read by completing a “Self-Check.” Writing the answers to thesequestions will help you review what you’ve studied so far. Please complete Self-Check 1 now.

Write a definition for each of the Key Concepts listed on page 220 of your textbook. Then,answer Questions for Review 2, 5, and 6 on pages 220–221 of your textbook. Finally, in the Problems and Applications section on pages 221–222, solve Problem 11.

Check your answers against those on page 85.

Economics 2

For the market to allocate goods efficiently, the goods mustbe both excludable and rival. An excludable good is one thatother people can be prevented from using. A rival good is agood for which one person’s consumption takes away fromanother’s enjoyment. Goods can be categorized according tothose criteria. Consider the following classifications: Privategoods are those that are both excludable and rival, such ashamburgers. Public goods are neither excludable nor rival,such as national defense. Common resources are goods thatare rival but not easily excludable, such as whales in theocean. A natural monopoly exists when there’s a market for agood that’s excludable but not rival, such as cable-televisionsignals.

A public good is available to everyone free of charge. Publicgoods are neither excludable nor rival in consumption. Itisn’t feasible to exclude those who don’t pay for a publicgood, and additional users can consume the good withoutdetracting from the satisfaction received by consumers.National defense is a public good. The security provided bya nuclear submarine, for example, is nonexcludable in thesense that it protects the entire country, not just those whopaid for it. It’s also nonrival in that it can protect a growingpopulation without reducing the benefits received by theoriginal consumers.

Because it’s not feasible to exclude those who don’t pay fornational defense, there’s a “free-rider” problem (some userswon’t pay their share) when the production of nationaldefense is left to the private market. Governments may alsoprovide goods that are essentially private (excludable andrival), such as a congested state campground. Similarly,markets may provide goods that are essentially public(nonexcludable and nonrival). Commercial television signals,for example, are essentially public goods, with infeasibleexclusion (without using different broadcast technology) andnonrival consumption (additional viewers don’t detract fromothers’ enjoyment). To avoid the free-rider problem, broad-casters use commercial advertising to pay for the good.

Other goods that don’t have a price tag are commonresources. Common resources share the characteristic ofnonexcludability with public goods. Unlike public goods,however, common resources are rival. One person’s

12

consumption of a common resource detracts from other people’s consumption. Common resources differ from privategoods in that they lack clearly defined and enforced propertyrights. This makes exclusion difficult or impossible. To betterunderstand this, consider two children who must share abox of popcorn at the movies. Each child might prefer to eat slowly, making the popcorn last for the entire movie. IfChild A eats too slowly, however, Child B may finish off thepopcorn and get a larger share of it. This possibility promptsboth children to eat faster to make sure that each gets a fair share.

Another example of a common resource is undergroundpetroleum reserves. If one company pumps the oil out ofthe ground, then that oil is no longer available for others.However, it’s difficult to define and protect the propertyrights to underground oil. Not only can it extend underseveral owners’ property, but drillers can drill diagonallyto reach oil under someone else’s land. Iraq made this claimabout Kuwait’s petroleum exploration just before invadingKuwait. If property rights to underground petroleum wereclear-cut, then petroleum reserves would be a simple caseof a private good that the market could allocate efficiently.Because oil reserves are a common resource, the markettends to overproduce under the “use it or lose it” mentality.

After you’ve carefully read pages 223–237 in Principlesof Microeconomics, complete Self-Check 2. Check youranswers with those provided at the back of this studyguide. When you’re sure you understand the materialfrom Assignment 2, move on to Assignment 3.

Lesson 1 13

Self-Check 2

Write a definition for each of the Key Concepts listed on page 237 of your textbook. Then,answer Questions for Review 1, 2, and 4 on page 237 of your textbook. Finally, in theProblems and Applications section on pages 237–239, solve Problems 1 and 6.

Check your answers with those on pages 87.

ASSIGNMENT 3Read this introduction to Assignment 3. Then, readChapter 12, “The Design of the Tax System,” pages241–261 in the textbook Principles of Microeconomics.

According to Ben Franklin, the only things that are certain inour lives are death and taxes. This assignment takes a closerlook at one of these certainties—our tax system. The UnitedStates has a system of fiscal federalism in which federal, state,and local governments collectively comprise “the government.”The federal government uses roughly two-thirds of all taxesthat we pay to fund federal programs. The federal governmentrelies primarily on the individual income tax, followed closelyby payroll taxes. A third source of federal revenue is the cor-poration income tax. These revenues are used to fund SocialSecurity, national defense, welfare, interest on the nationaldebt, Medicare, health, and other programs (in order of great-est expenditure). State and local governments rely primarilyon sales taxes, followed closely by property taxes, and thenfederal funding, as revenue sources. The individual incometax ranks fourth as a source of state revenue, with corporateincome taxes a distant fifth.

Taxes reduce private purchasing power. They also imposeefficiency costs on the economy in the form of deadweightlosses (when they alter people’s behavior), levy complianceand administrative costs, and impose compliance andadministrative burdens. There are expenses involved inadministering taxes. Like the deadweight loss, the adminis-trative cost is an efficiency loss because there’s a cost to oneperson without an offsetting gain to someone else. The timethat you spend filling out your tax forms benefits nobody.

Although we can imagine hypothetical taxes that cause nodeadweight loss to society, all real-world taxes impose effi-ciency losses on the economy. Taxes that reduce inefficiencyoften violate society’s standards of equity. A lump-sum taxwould avoid the distortion of individuals’ behavior because it would be unavoidable, but it would be unacceptable onequity grounds. It would require the billionaire and thehomeless person to pay the same number of dollars in taxes.On equity grounds, the individual income tax is more accept-able to most people, even though there may be a deadweight

Economics 214

loss when a high marginal tax rate (the rate on the last dollar earned) discourages work effort. This efficiency loss is especially pronounced under the progressive tax rates that many people support on ability-to-pay grounds.

If efficiency were the only consideration, tax policy would bemuch easier to implement. However, tax equity is also a majorcriterion for evaluating tax proposals. Unfortunately, equityis difficult to assess because fairness is very subjective.

One way to determine the fairness of a tax is through thebenefits principle, which states that taxes should be assessedaccording to the benefits that people receive from the govern-ment programs that these taxes finance. Unfortunately, mosttaxes go into general revenue funds and can’t easily belinked to the benefits received.

An alternative way to determine the fairness of a tax is theability-to-pay principle, which states that taxes should beassessed according to taxpayers’ financial capability. Thegoal is both vertical and horizontal equity. Vertical equitymeans that taxpayers with more ability to pay should paymore taxes. Horizontal equity means that taxpayers with similar ability to pay should pay similar taxes.

Taxes can be proportional (all taxpayers pay the same percentof income), progressive (the rich pay a higher percent), orregressive (the rich pay a lower percent). To determine taxequity, you must first determine the tax incidence—whoactually pays the taxes. For example, many people argue for increasing corporate tax rates without realizing that thepeople ultimately pay those taxes. Consumers pay throughhigher prices, employees pay through lower wages, andstockholders pay through lower profits and lower dividends.

The tradeoff between equity and efficiency is one of thebiggest issues in economics, so it shouldn’t be surprising tofind that this tradeoff is a major obstacle to reaching consen-sus on proper tax policy. People often disagree because theyweigh these two goals differently. Political leaders differ intheir views, and economics alone can’t determine the bestsolution to balancing equity and efficiency. Economics canoffer insight on understanding the tradeoffs society faces and help us avoid policies that are inequitable.

Lesson 1 15

After you’ve carefully read pages 241–261 in Principlesof Microeconomics, complete Self-Check 3. Check youranswers with those provided at the back of this studyguide. When you’re sure that you completely understandthe material from Assignment 3, go to the SuggestedActivities for Lesson 1.

Suggested Activities for Lesson 1Read through these Suggested Activities, then write out theanswers to the questions in your notebook or on a separatepiece of paper.

Activity 1: Externalities on a River

As little children, we learn that our actions have conse-quences. This principle is the premise of the economic exter-nality, which produces external costs and market failures.This exercise will demonstrate negative externalities.

Instructions: Follow these steps to complete the activity.

Step 1: On a separate piece of paper, draw a simple pictureof a river. (Two curving lines are sufficient.) Add a rectangle labeled “FACTORY” at one end of theriver. Draw a stick figure of a person about half-way down the river. Add another rectangle labeled“BREWERY” at the other end of the river.

Economics 216

Self-Check 3

Write a definition for each of the Key Concepts listed on page 261 of your textbook. Then,answer Questions for Review 1, 3, 4, 5, 6, and 7 on page 261 of your textbook. Finally, in the Problems and Applications section on pages 262–263, solve Problems 9 and 10.

Check your answers with those on page 88.

Your drawing represents three users of a naturalresource. Tiffany owns a sweater factory on the river.Dan enjoys going to a beach on the river. Pat ownsa brewery that uses water from the river. Draw anarrow from the river into the brewery. Add a beachumbrella on the side of the river for Dan. Draw anarrow pointing away from the factory into the riverto represent a discharge pipe.

Step 2: Next, on another sheet of paper, draw a demandcurve for Tiffany’s sweaters. The market for hersweaters is based on consumers’ tastes, incomes,the prices of substitutes and complements, and the number of consumers in the market.

Step 3: Add the supply curve for Tiffany’s sweaters to yourgraph, based on all of the costs of production.Label this “Supply with production costs.”

Step 4: Write out the answers to these questions.

1. How would the supply curve shift if Tiffany got her materials for free?

2. How would the supply curve shift if she didn’t have topay her workers?

Step 5: One of the by-products of sweater production istoxic sludge. This sludge is dumped in the river.Draw thick lines representing the sludge from thefactory’s discharge pipe. Draw more thick lines ofsludge over the stick figure and into the brewery.So, here are some consequences: Dan’s day at thebeach is ruined. He’s covered with sludge. Pat’sbeer is ruined—the entire production run has beencontaminated. These are real costs associated withTiffany’s sweater production, but Dan and Pat paythese costs. Tiffany doesn’t consider these externalcosts when making supply decisions. Return toyour supply-and-demand graph and add a newsupply curve labeled “Supply with social costs.”Keeping these facts in mind, answer the followingquestion.

3. Your graph illustrates a negative externality to production.How would you explain the new optimum productionpoint in terms of quantity of sweaters and price?

Lesson 1 17

Activity 2: Taxes, Taxes

Two things in life are certain—death and taxes. There’s alwaysplenty of heated debate over tax issues. This exercise exam-ines a new tax and how it will affect the taxpayer. You’ll seethe importance of classifying a tax as progressive, regressive,or proportional.

Instructions: Congress has just approved a new tax to fundscientific research on clones. Everyone will pay $1,000 ayear. Keeping these facts in mind, write out the answers tothe following questions.

1. Is this tax progressive, regressive, or proportional?Explain your answer in terms of income percentages of Taxpayer A, who makes $1,000 per year, as opposedto Taxpayer B, who makes $100,000 per year.

2. If Taxpayer A and Taxpayer B had to pay 1 percent,what would each owe? Would this tax be progressive,regressive, or proportional?

When you’ve completed the Suggested Activities for Lesson 1,check your answers with those provided at the back of thisstudy guide. When you’re sure that you completely under-stand the material from these three assignments, you cancomplete the examination for Lesson 1.

Economics 218

19

Lesson 1

The Economics of the Public Sector

When you feel confident that you have mastered the material inLesson 1, go to http://www.takeexamsonline.com and submityour answers online. If you don’t have access to the Internet, youcan phone in or mail in your exam. Submit your answers for thisexamination as soon as you complete it. Do not wait until anotherexamination is ready.

Questions 1–20: Select the one best answer to each question.

1. Which of the following statements about marginal and averagetax rates is correct?

A. Marginal tax rates are a better measure of taxpayer sacrifice.

B. Average tax rates are a better measure of tax effects onincentives.

C. Marginal tax rates are a better measure of tax effects onincentives.

D. Average tax rates are used to determine deadweight lossfrom a tax.

2. Goods that are nonrival in consumption

A. are congested in consumption.B. are typically consumed jointly.C. can’t be provided in the private sector.D. are always excludable.

Ex

am

ina

tion

Ex

am

ina

tion

EXAMINATION NUMBER:

05066700Whichever method you use in submitting your exam

answers to the school, you must use the number above.

For the quickest test results, go to http://www.takeexamsonline.com

Examination, Lesson 1 20

3. To encourage the production of honey, several beekeepers place their beehives in afarmer’s orchards and fields. As the bees gather nectar to make honey, they pollinate the orchards and fields, thereby increasing the yields of the fruit and grain crops. This arrangement results in

A. a positive externality that benefits the farmer.B. no significant additional benefit to anyone.C. a positive externality that benefits the consumer.D. a negative externality for which the farmer should be compensated.

4. Which of the following statements is correct?

A. Tradable pollution permits exempt a firm from paying for its pollution.B. Pigovian taxes from polluting firms are used to fund pollution permits.C. There are no advantages to allowing a market for pollution permits.D. Tradable pollution permits may be preferred to Pigovian taxes in some cases.

5. Deadweight costs from taxation are associated with

A. taxes that influence the decisions that people make.B. taxes that target expenditures on survivor benefits for Social Security.C. taxes that have no efficiency losses.D. lump-sum taxes.

6. When the government reverts to command-and-control policy to solve an externality, it

A. is usually the most effective policy option available.B. creates policies that directly regulate behavior.C. usually involves taxing consumption of a commodity.D. typically refers to the Coase theorem to structure the policy.

7. Which of the following would be considered a nonrival but excludable good?

A. A viewing of a movie in a crowded theaterB. An ice-cream coneC. A visit to a noncrowded museumD. A fish in the ocean

8. Environmentalists argue that we should protect the environment as much as possible,regardless of the cost involved. Which of the following is one of these costs?

A. Lower levels of nutrition and inadequate health careB. A higher standard of living, but less available housingC. Increasing technological advancementD. More expensive utilities, but lower taxes

Examination, Lesson 1 21

9. Which of the following goods would not be subject to the Tragedy of the Commons?

A. A small public park C. The game animals in a small forestB. A stream passing through a town D. A fishing hole on private land

10. Which of the following statements about lump-sum taxes is correct?

A. Lump-sum taxes are most frequently used to tax real property.B. Lump-sum taxes aren’t distortionary.C. Lump-sum taxes are the most distortionary tax.D. Lump-sum taxes are used in taxing sales.

11. In the presence of externalities, society’s interest in a market outcome includes the well-being of

A. buyers and sellers only. C. bystanders and regulatory agencies.B. bystanders only. D. buyers, sellers, and bystanders.

12. One reason that markets fail to allocate common resources efficiently is that

A. prices change in irregular ways.B. social optimum doesn’t occur at market equilibrium.C. property rights aren’t well established.D. social welfare isn’t maximized at market equilibrium.

13. Which of the following is based on a person’s taxable income?

A. Federal tax return C. Social insurance taxB. Tax liability D. Consumption tax

14. Imagine that Steve owns a lion whose roaring annoys Steve’s neighbor Terri. Suppose thatthe benefit of owning the lion is worth $500 to Steve and that Terri bears a cost of $700from the roaring. Which of the following is a possible private solution to this problem?

A. Terri pays Steve $450 to get rid of the lion.B. Steve pays Terri $650 for her inconvenience.C. Terri pays Steve $650 to get rid of the lion.D. There’s no private solution that will improve this situation.

15. Which of the following would be considered to be a public good?

A. A pizzaB. Half-time entertainment at the Super BowlC. A local dance clubD. A light bulb

Examination, Lesson 1 22

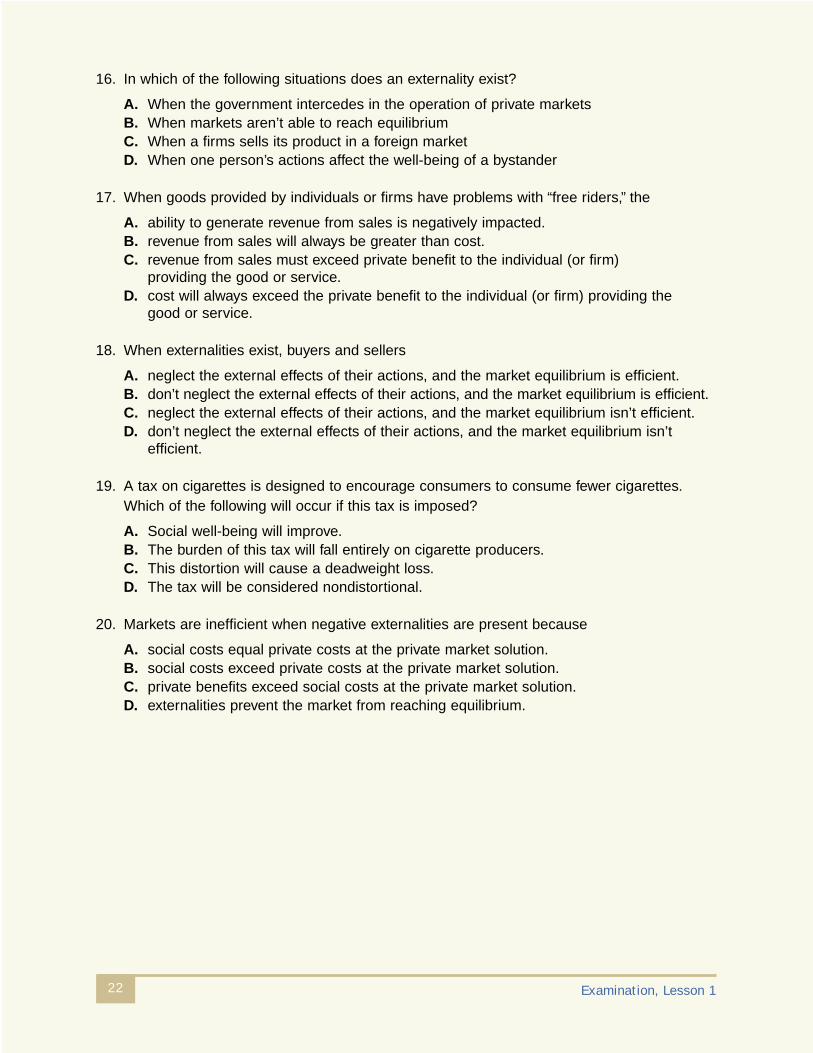

16. In which of the following situations does an externality exist?

A. When the government intercedes in the operation of private marketsB. When markets aren’t able to reach equilibriumC. When a firms sells its product in a foreign marketD. When one person’s actions affect the well-being of a bystander

17. When goods provided by individuals or firms have problems with “free riders,” the

A. ability to generate revenue from sales is negatively impacted.B. revenue from sales will always be greater than cost.C. revenue from sales must exceed private benefit to the individual (or firm)

providing the good or service.D. cost will always exceed the private benefit to the individual (or firm) providing the

good or service.

18. When externalities exist, buyers and sellers

A. neglect the external effects of their actions, and the market equilibrium is efficient.B. don’t neglect the external effects of their actions, and the market equilibrium is efficient.C. neglect the external effects of their actions, and the market equilibrium isn’t efficient.D. don’t neglect the external effects of their actions, and the market equilibrium isn’t

efficient.

19. A tax on cigarettes is designed to encourage consumers to consume fewer cigarettes.Which of the following will occur if this tax is imposed?

A. Social well-being will improve.B. The burden of this tax will fall entirely on cigarette producers.C. This distortion will cause a deadweight loss.D. The tax will be considered nondistortional.

20. Markets are inefficient when negative externalities are present because

A. social costs equal private costs at the private market solution.B. social costs exceed private costs at the private market solution.C. private benefits exceed social costs at the private market solution.D. externalities prevent the market from reaching equilibrium.

23

Firm Behavior andMonopolies

INTRODUCTIONThis lesson focuses on a detailed analysis of the market system, examining its business structure and operation. The first assignment of the lesson looks at a firm’s cost ofproduction, revenue, and profit. It also examines how eco-nomic cost and profit differ from traditional accounting costand profit. You’ll learn how all firms, from the largest to thesmallest, behave under different types of market conditions.Assignment 5 discusses the analysis used by competitivefirms to achieve profit maximization in the short and long run. A competitive market exists if each buyer and seller is small compared to the size of the market. Assignment 6extends market analysis to look at the operation of a monop-oly. Monopolies occur when barriers to market entry protecta single seller from competition. These barriers to entry allowmonopolists to earn economic profit in the long run. Themonopolist, as you’ll learn, is a price maker. The competitivefirm is a price taker.

OBJECTIVESWhen you complete this lesson, you’ll be able to

■ Calculate average total cost and marginal cost anddiscuss their relationship to one another

■ Describe short-run and long-run costs of a firm■ Use total cost to derive both marginal and average

cost■ Describe the characteristics and operation of a

competitive market■ Explain the profit-maximization rule for

competitive firms■ Explain why firms decide to enter or leave a

competitive market■ Discuss why some markets have only one seller

Le

ss

on

2

L

es

so

n

2

Economics 224

■ Analyze how a monopoly determines what quantityto produce and what price to charge

■ Compare and contrast profit maximization for perfect competitors and monopolists

■ Explain how and why the monopolist uses price discrimination

ASSIGNMENT 4Read this introduction to Assignment 4. Then, readChapter 13, “The Costs of Production,” on pages 267–284in the textbook Principles of Microeconomics.

This chapter provides the tools you need to understandhow all firms, from the largest to the smallest, behave underdifferent types of market conditions. A firm’s goal is to maxi-mize profit. Profit is simply the total revenue that it receivesfrom selling its product minus the total cost of producingthat product. Total revenue is simply the price of an itemtimes the quantity sold.

Total costs can be a bit tricky to calculate, however. To aneconomist, cost means opportunity cost. It includes the explicitcosts or money outlays that comprise accounting costs, ofcourse, but it also includes implicit costs of resources usedby the firm that could have been used elsewhere. A smallbusiness that shows an accounting profit actually may belosing money in an economic sense, if we deduct all of theimplicit costs of resources that the owner ties up in the firmrather than using elsewhere. The owner’s labor, for example,is a real cost of operating the business even if no actual salaryis paid. The cost is the earnings the owner gives up by notworking for someone else, rather than the owner’s actualsalary from his or her own business. Similarly, the lost interestincome on money the owner invests in the business is a realcost of doing business even though it’s not an accounting cost.

You’ll also learn how a firm’s production process is related to its costs. The production function shows the relationshipbetween inputs and outputs. In the short run, this meanslooking at the relationship between the amount of labor usedand the amount of output produced. We define the short run

Lesson 2 25

as a time period that’s too short to allow increases in otherinputs. Adding more labor increases output, although atsome point additional workers are subject to diminishingmarginal product. The property of diminishing marginal product means that the last unit of labor hired adds less to total output than did the previous one. Imagine growingstrawberries in your backyard in a plot that’s only 20 feet by 10 feet. You might be able to pick three pints of strawber-ries in 15 minutes. However, additional workers in the samesmall plot couldn’t be expected to maintain that level of output per worker. Eventually, the marginal product of anadditional worker will fall because land and capital are fixed.The marginal product actually becomes negative when thepatch is so crowded that workers are getting in each other’sway and trampling the berries. Diminishing marginal productoccurs when workers are added without additional capitaland land.

In the long run, expansion doesn’t always result in diminishingmarginal product because land, labor, and capital can beincreased simultaneously. As marginal product diminishes,the firm’s total cost begins to rise at a more rapid ratebecause additional units of output cost more to produce.That is, the same wage per worker results in less additionaloutput, so the cost per additional unit produced rises.

The costs of production, as you’ll see, are analyzed in boththe short and long run. Because we define the long run asthe time period long enough to vary capital and all otherinputs, all costs become variable in the long run. As a result,diminishing marginal product is no longer a problem. Thereare no fixed inputs. Given enough time, firms can vary theirscale of operation by acquiring more land and building morefactories in addition to hiring more labor. They also can cutback on their use of all inputs. It’s helpful to understandthat the distinction between short run and long run in eco-nomics is somewhat arbitrary. The short run is a period inwhich some inputs (typically capital and land) are fixed whileat least one (typically labor) is variable. Although arbitrary, itmakes a lot of sense: a firm that desires to increase outputquickly could expand labor immediately, but it would take awhile to build a new factory.

Economics 226

After you’ve read pages 267–284 in Principles ofMicroeconomics carefully, complete Self-Check 4.Check your answers against those provided at the back of this study guide. When you’re sure that you completely understand the material from Assignment 4,move on to Assignment 5.

ASSIGNMENT 5Read this introduction to Assignment 5. Then, readChapter 14, “Firms in Competitive Markets,” on pages289–307 in the textbook Principles of Microeconomics.

You’re familiar with the idea of competition from the world ofsports. This assignment focuses on the perfectly competitivemarket. This exists when there are so many buyers and sell-ers of a standardized good that no individual buyer or sellercan influence price. In addition, competitive markets have no barriers to entry, so firms can enter or exit the industryeasily in response to changing market conditions.

Just as other firms do, competitive firms desire to maximizeprofit. Let’s take a closer look at one of the Ten Principles ofEconomics that rational people use to make decisions at themargin. Everyone (individuals, firms, and societies) seeks tomaximize well-being by following a general decision-makingrule: Do anything as long as marginal benefit is greater thanor equal to marginal costs, and stop when the marginal benefitequals the marginal costs. For a business trying to maximizeprofit, this rule becomes: Produce as long as the marginal rev-enue is equal to or greater than the marginal costs, and stopwhen marginal revenue equals marginal cost.

Self-Check 4

Write a definition for each of the Key Concepts listed on page 285 of your textbook. Then,answer Questions for Review 1, 2, 5, and 7 on page 284 of your textbook. Finally, in theProblems and Applications section on page 285, solve Problems 1, 6, and 9.

Check your answers with those on page 91.

Lesson 2

Keep in mind that fixed costs are irrelevant for makingfuture decisions. Economists refer to fixed costs as sunkcosts because once they’re incurred, they can’t be recovered.In the short run, a business can’t avoid its fixed costs evenby shutting down. This is why it’s rational for a business tocontinue to produce at a loss in the short run as long as itsrevenues cover the variable costs. Any revenues in excess ofthe variable cost will offset part of the fixed cost and reducelosses. However, if the firm shuts down, it will incur lossesequal to the full fixed cost. A firm determines how much out-put to produce by equating marginal revenue and marginalcost, neither of which is affected by fixed cost.

A competitive firm must consider that all sales occur at themarket price, which doesn’t change as the firm increasesoutput. As a result, in perfect competition, average revenueequals marginal revenue equals price. That is,

AR = MR = P

To maximize profit using marginal analysis, the perfectlycompetitive firm produces until marginal revenue equalsprice equals marginal cost (see Figure 1 on page 294 in yourtextbook).

MR = P = MC

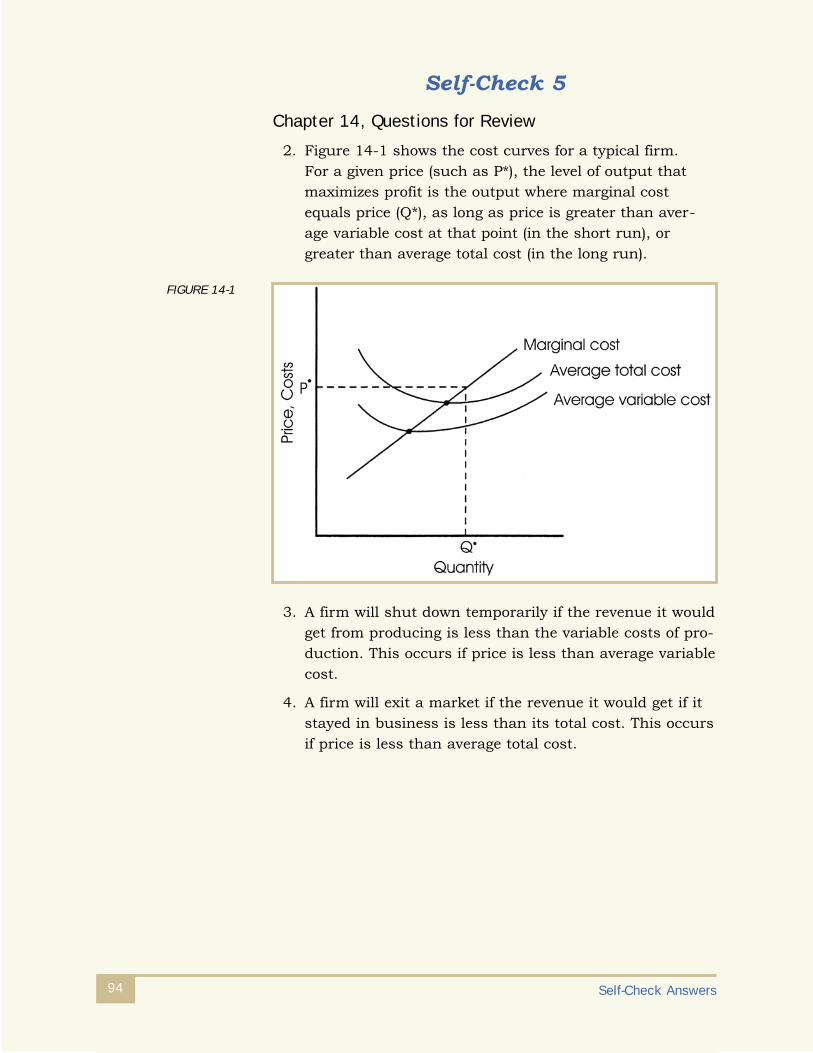

So for any price, the firm will choose the quantity suppliedby looking at the marginal-cost curve (MC), which makes thatcurve the firm’s supply curve. The only qualification is thatfirms won’t sell at a price below the average variable cost. Ifprice is below average variable cost, the firm is losing moremoney than if it were to shut down. Therefore, the competi-tive firm’s supply curve in the short run is the portion of the marginal-cost curve above the average variable cost. The analysis is similar in the long run, except that all costs are variable.

Consequently, the profit-maximizing firm in the long runwon’t produce below the average-total-cost curve (ATC). WithP less than ATC, the firm is incurring losses and will go outof business. On the other hand, if P is greater than ATC, thefirm will earn an economic profit, encouraging it to stay inbusiness and encouraging other firms to enter the industry.

27

Keep in mind the difference between economic profit andaccounting profit. Economic profit includes all opportunitycosts of time and capital. When a firm has zero economicprofit, it’s enjoying a normal accounting profit. It’s for thisreason that firms are willing to continue to produce at apoint of zero economic profit. In addition, any positive economic profit provides an incentive for firms to enter the industry.

Market supply is the summation of all of the individual supplycurves. Long-run market supply includes potential as well as current competitors. If economic profits exist, new firmswill enter the market in the long run, increasing supply anddriving down price until the economic profits disappear. Ifeconomic losses exist, firms will exit the industry in the longrun, decreasing supply and resulting in rising prices untileconomic losses disappear. The situation stabilizes in thelong run only when economic profit equals zero, whichmeans that price equals average total cost. This long-runequilibrium occurs at minimum average total costs, witheach firm operating at its efficient scale.

Thinking at the margin is what distinguishes economistsfrom noneconomists. This assignment elaborates on whatthat really means. A business that’s maximizing profit ignoresfixed costs. This would indicate that in the short run (whenthere are some fixed costs), a business that just replaced anexpensive piece of equipment or made an expensive repairwon’t find it profitable to raise prices even by a slightamount. This is probably counterintuitive, but rememberthat the firm is already charging whatever the market willbear, up to the point at which MC equals MR. Just ask your-self this question: If it’s profitable for the firm to raise pricesnow to recoup the cost, why wasn’t it profitable to raiseprices before the big investment just to make more profit?The answer is that if the firm could raise prices to makemore profit, it would have already done so! If it’s a rational-thinking firm, it wouldn’t make the decision based on sunkcosts. Similarly, if you go to a concert that turns out to be awaste of time, you shouldn’t stay until the end just becauseyou paid $50 for a ticket. After all, the $50 is gone, so whymake yourself even more miserable by sitting through aworthless concert?

Economics 228

Lesson 2 29

After you’ve read pages 289–307 in Principles of Micro-economics carefully, complete Self-Check 5. Check youranswers against those provided at the back of this studyguide. When you’re sure that you completely understandthe material from Assignment 5, move on to Assignment 6.

ASSIGNMENT 6Read this introduction to Assignment 6. Then, read Chapter 15,“Monopoly,” on pages 311–339 in the textbook Principles ofMicroeconomics.

Assignment 5 introduced market structure by investigatingthe characteristics of perfect competition. This assignmentdiscusses the opposite of the perfectly competitive market, a situation known as a monopoly. A monopoly exists whenthere are barriers to market entry that protect a single sellerfrom competition. A monopolist is the sole seller of a productwithout close substitutes.

Monopolists can continue to earn economic profit in the longrun due to barriers to entry that prevent new competitorsfrom entering the industry and driving down price and profit.Such barriers to entry usually arise for one of three reasons:(1) control over a key resource, (2) exclusive-rights grants bygovernment, or (3) a falling average total cost that makes asingle producer more efficient than many smaller firms.

The primary difference between monopoly and competition is control over price. Monopolists are price setters who canalter price within the constraints of the demand curve.

Self-Check 5

Write a definition for each of the Key Concepts listed on page 307 of your textbook. Then,answer Questions for Review 2, 3, and 4 on page 307 of your textbook. Finally, in the Problems and Applications section on pages 308–309, solve Problems 2 and 12.

Check your answers with those on page 94.

Economics 230

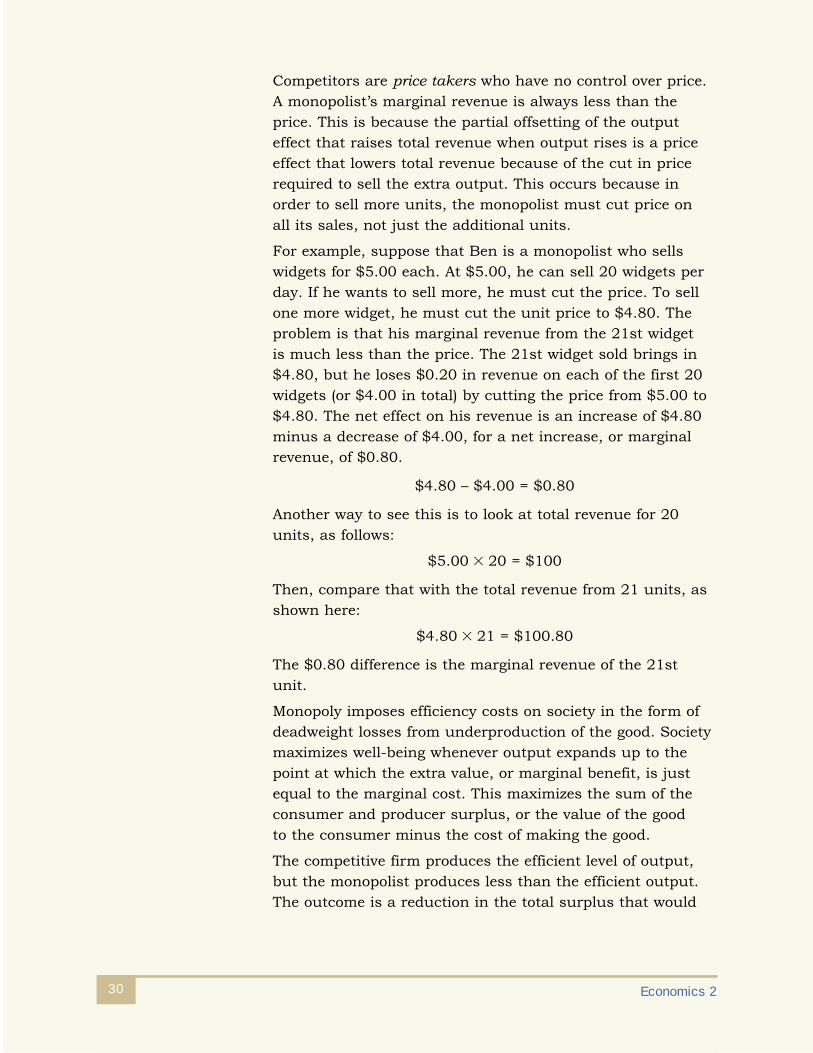

Competitors are price takers who have no control over price.A monopolist’s marginal revenue is always less than theprice. This is because the partial offsetting of the outputeffect that raises total revenue when output rises is a priceeffect that lowers total revenue because of the cut in pricerequired to sell the extra output. This occurs because inorder to sell more units, the monopolist must cut price onall its sales, not just the additional units.

For example, suppose that Ben is a monopolist who sellswidgets for $5.00 each. At $5.00, he can sell 20 widgets perday. If he wants to sell more, he must cut the price. To sellone more widget, he must cut the unit price to $4.80. Theproblem is that his marginal revenue from the 21st widgetis much less than the price. The 21st widget sold brings in$4.80, but he loses $0.20 in revenue on each of the first 20widgets (or $4.00 in total) by cutting the price from $5.00 to$4.80. The net effect on his revenue is an increase of $4.80minus a decrease of $4.00, for a net increase, or marginalrevenue, of $0.80.

$4.80 – $4.00 = $0.80

Another way to see this is to look at total revenue for 20units, as follows:

$5.00 � 20 = $100

Then, compare that with the total revenue from 21 units, asshown here:

$4.80 � 21 = $100.80

The $0.80 difference is the marginal revenue of the 21stunit.

Monopoly imposes efficiency costs on society in the form ofdeadweight losses from underproduction of the good. Societymaximizes well-being whenever output expands up to thepoint at which the extra value, or marginal benefit, is justequal to the marginal cost. This maximizes the sum of theconsumer and producer surplus, or the value of the good to the consumer minus the cost of making the good.

The competitive firm produces the efficient level of output,but the monopolist produces less than the efficient output.The outcome is a reduction in the total surplus that would

result from producing at the efficient output level. The dead-weight loss is the lost surplus on the withheld output. Thatis, the monopolist fails to produce some output that societyvalues more than it costs to produce. Although monopolycauses a social welfare loss, its seriousness is limited bythe inherent market controls over monopoly power. Not evena monopoly can charge whatever it wants if it cares aboutthe quantity that it sells. Monopolists can charge whateverthe market will bear, but are ultimately constrained by thedemand curve. Total and permanent barriers to entry arerare, and even in the cases of true monopoly, there areusually relatively close substitutes for the product.

Governments attempt to limit the inefficiency associatedwith monopoly in a variety of ways. To make monopoliesbehave more competitively, the government passes a seriesof antitrust laws, which tend to control monopoly power andpromote competition. Under these laws, government can pre-vent mergers that would lead to monopoly or near-monopoly,it can prevent price fixing and other anticompetitive behavior,and it can even split up large firms in extreme cases, suchas the breakup of AT&T in 1984.

Another alternative is to regulate monopoly pricing and otherbehaviors. It’s common for the government to regulate theprices charged by natural monopolies such as power compa-nies. However, it’s not possible to force them to set priceequal to marginal cost, as occurs in perfect competition,without driving them out of business.

The third option, public ownership, is common with naturalmonopolies in some countries, but not in the United States.Although it could eliminate the problem of underproductionif taxpayers were willing to make up the difference betweenprice and average total costs, we would lose the advantage of the profit motive to hold down cost. The final option,which is doing nothing, is the choice of those who feel thatthe inefficiency of monopoly underproduction is less than the inefficiency resulting from politically established economicpolicies, or that the good of society in general isn’t the propercriterion for establishing economic policy.

Lesson 2 31

A monopoly can also engage in price discrimination, whichmeans charging different prices to different customers for the same good. For example, airlines typically offer steeplydiscounted prices to customers who purchase in advanceand stay through a Saturday night. This is a way to discountfares to leisure travelers with highly elastic demand whilecontinuing to charge high fares to business travelers withinelastic demand who are unlikely to want to stay throughthe weekend. Firms price-discriminate in an attempt to getthe output effect from cutting price without the price effectthat would result if they lowered price to everyone. In thewidget case described earlier, if Ben could have sold the 21stunit for $4.80 while continuing to sell the first 20 units for$5.00 each, then marginal revenue would have equaled the$4.80 price.

Interestingly, price discrimination can actually improve economic well-being. Remember that the monopolist under-produces because of the price effect of expanding output and moving down the demand curve. If everyone is charged adifferent price, then there’s no price effect, and the monopo-list will produce at the socially efficient output level.

After you’ve read pages 311–339 in Principles of Microeconomics carefully, complete Self-Check 6.Check your answers against those provided at the back of this study guide. When you’re sure that you completely understand the material from Assignment 6,move on to the Suggested Activities for Lesson 2.

Economics 232

Self-Check 6

Write a definition for each of the Key Concepts listed on page 339 of your textbook. Then,answer Questions for Review 3, 4, 5, and 8 on pages 339 of your textbook. Finally, in the Problems and Applications section on pages 340–343, solve Problems 5, 6, and 8.

Check your answers with those on page 97.

Lesson 2 33

Suggested Activities for Lesson 2Read through these Suggested Activities, then write out theanswers to the questions in your notebook or on a separatepiece of paper.

Activity 1: A Profitable Opportunity

This exercise reinforces the importance of marginal cost indecision making. It will show you how average costs can bemisleading.

Imagine that you’ve recently graduated from college and havelanded a job in production management for Sekin SneakersInc. You’re responsible for the entire production on weekends.Your costs are shown in the following table.

Your current level of production is 500 pairs of sneakers perweekend. All 500 units for the current weekend have beenordered by your regular customers. The phone rings. It’s anew customer who wants to buy 1 pair of sneakers. Thismeans that you would have to increase production to 501units. Your potential new customer offers to pay $50 for theone pair of sneakers.

1. Should you accept the new customer’s offer?

2. Calculate the marginal cost of producing 501 pairs ofsneakers.

3. Re-examine your decision as to whether or not to accept the new customer’s offer. Explain your decision in termsof marginal revenue and profits.

Activity 2: Price Discrimination and Time Travel

In Economics 1, you completed a time-travel activity. Now,we’ll take another look at time travel. This example illustrateshow a price-discriminating monopolist can earn even higherprofits than a monopolist charging a single price. You’ll useyour knowledge about calculating consumer surplus to look at monopoly profits.

ytitnauQ tsoClatoTegarevA

005 01$105 11$

Economics 2 34

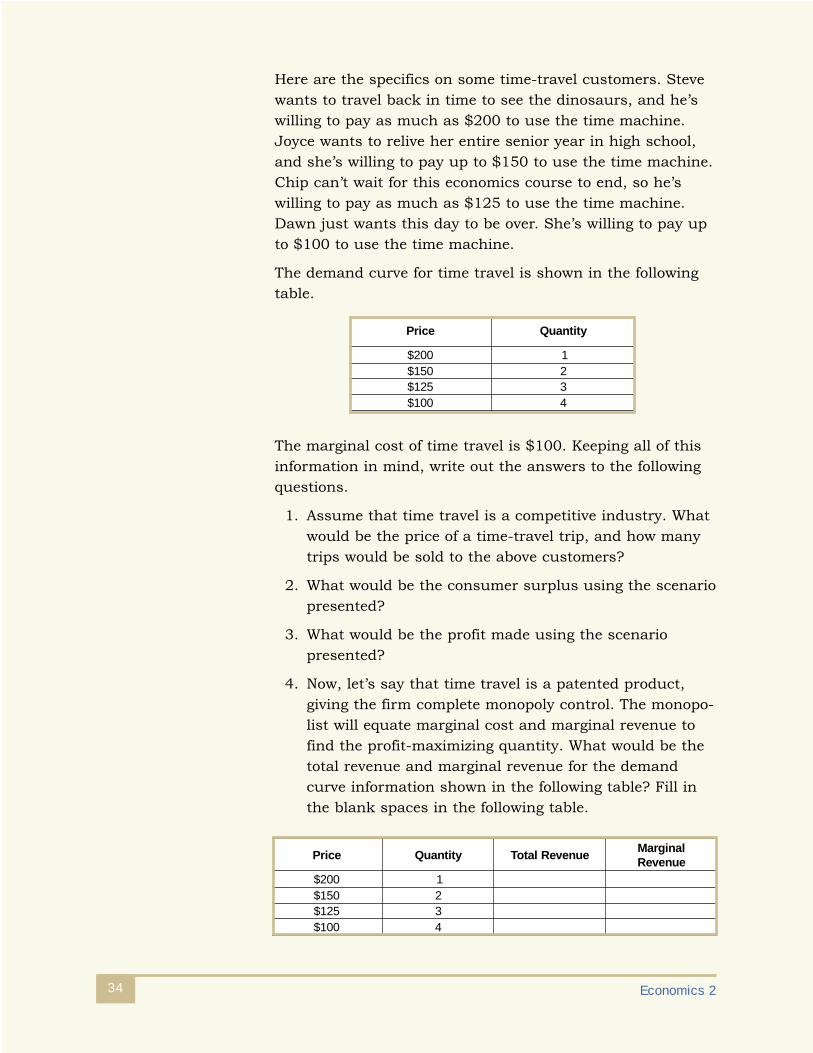

Here are the specifics on some time-travel customers. Stevewants to travel back in time to see the dinosaurs, and he’swilling to pay as much as $200 to use the time machine.Joyce wants to relive her entire senior year in high school,and she’s willing to pay up to $150 to use the time machine.Chip can’t wait for this economics course to end, so he’swilling to pay as much as $125 to use the time machine.Dawn just wants this day to be over. She’s willing to pay upto $100 to use the time machine.

The demand curve for time travel is shown in the followingtable.

The marginal cost of time travel is $100. Keeping all of thisinformation in mind, write out the answers to the followingquestions.

1. Assume that time travel is a competitive industry. Whatwould be the price of a time-travel trip, and how manytrips would be sold to the above customers?

2. What would be the consumer surplus using the scenario presented?

3. What would be the profit made using the scenario presented?

4. Now, let’s say that time travel is a patented product, giving the firm complete monopoly control. The monopo-list will equate marginal cost and marginal revenue tofind the profit-maximizing quantity. What would be thetotal revenue and marginal revenue for the demandcurve information shown in the following table? Fill inthe blank spaces in the following table.

ecirP ytitnauQ

002$ 1051$ 2521$ 3001$ 4

ecirP ytitnauQ euneveRlatoTlanigraMeuneveR

002$ 1051$ 2521$ 3001$ 4

Lesson 2 35

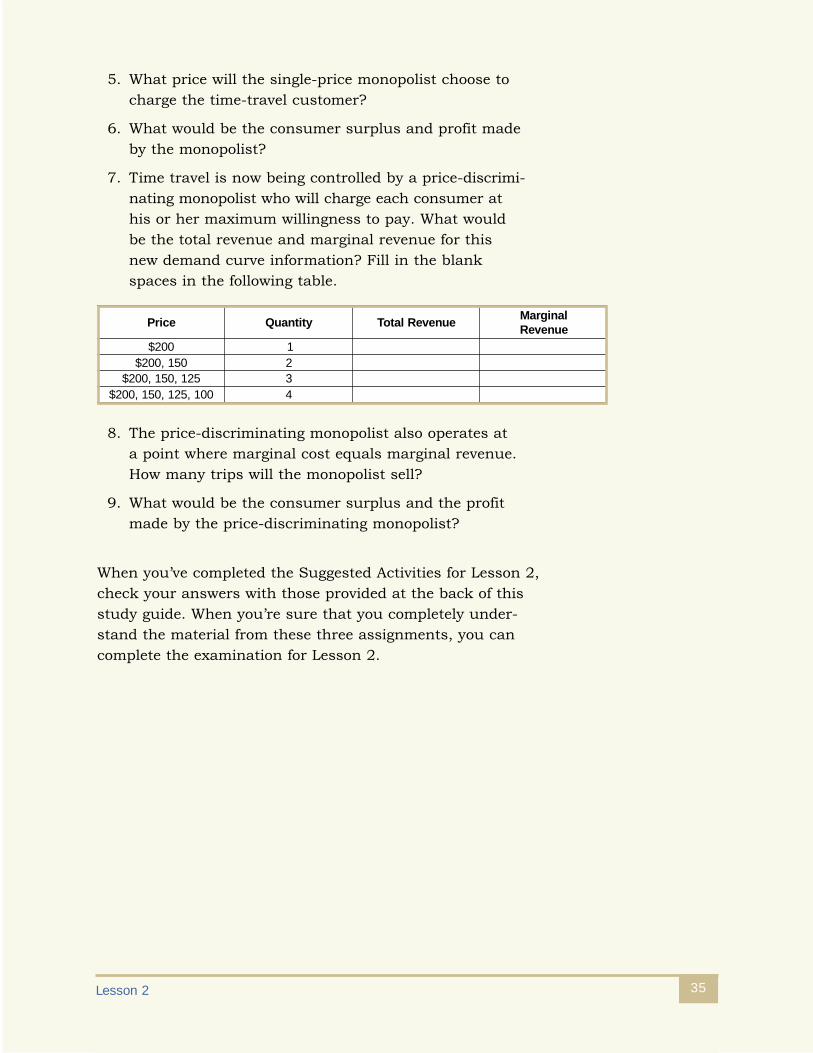

5. What price will the single-price monopolist choose tocharge the time-travel customer?

6. What would be the consumer surplus and profit madeby the monopolist?

7. Time travel is now being controlled by a price-discrimi-nating monopolist who will charge each consumer at his or her maximum willingness to pay. What would be the total revenue and marginal revenue for this new demand curve information? Fill in the blank spaces in the following table.

8. The price-discriminating monopolist also operates at a point where marginal cost equals marginal revenue.How many trips will the monopolist sell?

9. What would be the consumer surplus and the profitmade by the price-discriminating monopolist?

When you’ve completed the Suggested Activities for Lesson 2,check your answers with those provided at the back of thisstudy guide. When you’re sure that you completely under-stand the material from these three assignments, you cancomplete the examination for Lesson 2.

ecirP ytitnauQ euneveRlatoTlanigraMeuneveR

002$ 1051,002$ 2

521,051,002$ 3001,521,051,002$ 4

NOTES

Economics 236

37

Lesson 2

Firm Behavior and Monopolies

When you feel confident that you have mastered the material inLesson 2, go to http://www.takeexamsonline.com and submityour answers online. If you don’t have access to the Internet, youcan phone in or mail in your exam. Submit your answers for thisexamination as soon as you complete it. Do not wait until anotherexamination is ready.

Questions 1–20: Select the one best answer to each question.

1. The Wheeler Wheat Farm sells wheat to a grain broker inSeattle, Washington. Since the market for wheat is perfectlycompetitive, the Wheeler Farm

A. doesn’t choose the quantity of wheat to produce.B. doesn’t have any fixed costs of production.C. isn’t able to earn an accounting profit.D. doesn’t choose the price at which it sells its wheat.

2. Since monopolies have a downward-sloping demand curve,regulating monopolies by setting price equal to marginal costwould

A. cause the monopolist to operate at less than maximum profit.

B. maximize producer surplus.C. result in a less-than-optimal total surplus.D. cause many new firms to enter the market.

Ex

am

ina

tion

Ex

am

ina

tion

EXAMINATION NUMBER:

05066800Whichever method you use in submitting your exam

answers to the school, you must use the number above.

For the quickest test results, go to http://www.takeexamsonline.com

Examination, Lesson 2 38

3. When a producer is operating at the bottom of a U-shaped average-total-cost curve, theproducer is said to be operating at

A. decreasing returns to scale. C. the efficient scale.B. the inefficient scale. D. increasing returns to scale.

4. Which of the following statements is correct?

A. In a perfectly competitive market, changes in demand cause short-term changes inprice, and no changes in quantity supplied to the market.

B. In a perfectly competitive market, changes in demand cause no long-term changes inprice, and permanent changes in quantity supplied to the market.

C. In a perfectly competitive market, changes in demand cause no changes in price, andlong-term changes in quantity supplied to the market.

D. In a perfectly competitive market, changes in demand cause no changes in price, andpermanent changes in quantity supplied to the market.

5. A competitive firm will choose to increase production when marginal cost is less than

A. marginal revenue. C. average variable cost.B. the marginal average. D. average total cost.

6. The purpose of antitrust laws is to

A. increase competition.B. create government-controlled monopolies.C. protect and promote copyright and patent laws.D. limit the public’s trust in a monopoly.

7. Which of the following statements about fixed cost is correct?

A. Fixed cost is always large in the long run.B. Fixed cost is seldom larger than variable cost.C. Fixed cost is a short-run phenomenon.D. Fixed cost can never exceed variable cost in a profitable firm.

8. One problem with monopolies is that they can

A. profiteer at the expense of consumers.B. price their product at a level that forces consumers to pay more than they can afford.C. buy political favors with their excessive profits.D. restrict output below the socially efficient level of production.

Examination, Lesson 2 39

9. If a firm pays employees by the hour and guarantees every employee 40 hours of work perweek, how would the firm categorize its labor costs?

A. Fixed and independent of how many hours each employee worksB. Variable and independent of how many hours each employee worksC. Fixed if each employee works no more than 40 hoursD. Variable if each employee works no more than 40 hours

10. A perfectly competitive firm realizes an average revenue of $11 and an average total costof $10. Its marginal-cost curve crosses the marginal-revenue curve at an output level of100 units. The current profit is $100. What is likely to occur in this market?

A. The price will go down. C. Costs will go up.B. Firms will leave the market. D. Costs will go down.

11. When a monopolist faces a downward-sloping market demand curve, its

A. average revenue is always less than marginal revenue.B. marginal revenue is greater than the price of the units it sells.C. average revenue is less than the price of its product.D. marginal revenue is always less than the price of the units it sells.

12. In a perfectly competitive market where all firms have identical cost structures, the marketsupply curve would be equal to the

A. sum of supply curves for all firms in the market.B. product of supply curves for all firms in the market.C. sum of average variable cost curves for all firms in the market.D. sum of average total cost curves for all firms in the market.

13. Which of the following statements is correct?

A. In the short term, land is a variable cost.B. In the short term, electricity is a fixed cost.C. In the short term, raw materials are a fixed cost.D. In the short term, buildings are a fixed cost.

14. An example of an industry that benefits society by government-created monopoly is the

A. cable TV industry. C. pharmaceutical industry.B. local telephone industry. D. precious stones industry.

15. An example of an explicit cost of production would be

A. the cost of foregone labor earnings for an entrepreneur.B. the cost of stone for a sculptor.C. the value a business derives from using the owner’s computer to keep payroll records.D. all of the inputs to production.

Examination, Lesson 240

16. The production decisions of perfectly competitive firms follow the principle of economicswhich states that rational people

A. make the same production decisions in all markets.B. think at the margin.C. equate prices to the costs of production.D. eventually leave markets that experience zero profit.

17. Which of the following statements is correct?

A. A firm with fixed costs always has losses for low levels of output.B. A firm with fixed costs must incur economic losses if it chooses not to produce output.C. A firm with fixed costs can’t maximize profit in the short run.D. A firm with fixed costs is always able to sell its product for a price that exceeds

marginal revenue.

18. The cost to produce an additional unit of output is a firm’s

A. variable cost. C. marginal cost.B. average variable cost. D. opportunity cost.

19. By using the concept of total surplus as a measure of well-being, it’s possible to show that

A. profit-maximizing natural monopolists always make society better off.B. producer surplus for a perfectly competitive firm always exceeds that of a monopolist.C. consumer surplus in a monopoly market always exceeds consumer surplus in a

perfectly competitive market.D. society is worse off when monopolists set a price that maximizes their profit.

20. Firms in a perfectly competitive market are said to be price takers, because

A. if a firm charges more than the going price, it would sell all of its goods.B. a firm has no incentive to charge less than the going price.C. each firm can sell as much as it wants at a reduced price.D. select firms can take the market for their particular good.

41

Oligopoly, MonopolisticCompetition, and theFactors of Production

INTRODUCTION

In the previous lesson, you learned about perfect competitionand monopoly. These market structures provide useful infor-mation about how markets operate, even though most real-world industries are somewhere between the two extremes.The beginning of this lesson introduces you to imperfectcompetition, which includes a variety of firms between the two extremes. There are two types of imperfectly competitivefirms: oligopolies and monopolistic competitors.

An oligopoly is a market structure in which there are fewsellers who offer similar or identical products. Each of thesellers in this case has a large impact on price and industryoutput.

The other market situation that exists in the gray areabetween monopoly and competition is monopolistic competition.This category includes fast-food restaurants, gasoline stations,and the corner market. Many of the businesses we deal withevery day are monopolistic competitors, sharing some of the characteristics of a monopoly and some of a perfectlycompetitive industry.

This lesson ends with an explanation of the behavior of labormarkets. Specifically, how labor, land, and capital are com-pensated for the roles they play in the production process. At equilibrium, each factor of production earns the value of its marginal contribution to the production of goods andservices. The wages of workers reflect the market prices ofthe goods they produce.

Le

ss

on

3

L

es

so

n

3

Economics 242

OBJECTIVESWhen you complete this lesson, you’ll be able to

■ Describe possible market outcomes of an oligopoly

■ Apply the prisoners’ dilemma to oligopolies andother market situations

■ Evaluate the effectiveness of antitrust laws in promoting competition

■ Explain how product differentiation affects the pricing and output decisions of firms

■ Compare monopolistic competition to perfect competition

■ Analyze labor demand of competitive, profit-maximizing firms

■ Explain why equilibrium wages equal the value of the marginal product of labor

■ Discuss how changes in the supply of a factor ofproduction affect the value of the marginal product of other factors

ASSIGNMENT 7Read this introduction to Assignment 7. Then, read Chapter 16,“Oligopoly,” on pages 345–367 in Principles of Microeconomics.

Most businesses in the real world fall somewhere betweenthe extremes of perfect competition and monopoly. A marketstructure that contains elements of both competition andmonopoly is known as imperfect competition.

As you’ll learn in this assignment, imperfectly competitivefirms can be either monopolistic competitors or oligopolists.A monopolistically competitive industry has many firms withsome control over price. An oligopolistic industry has fewfirms, each of which has substantial impact on price andindustry output. A major characteristic of oligopoly is inter-dependence. Each firm knows that its decisions will affectdecisions by other firms.

Lesson 3 43

Oligopolies come in different sizes, but each one faces thesame obstacle—a lack of cooperation within the group. Thesimplest type of oligopoly is duopoly, which is a market withonly two sellers. If the duopolists cooperate to set price andoutput, they’ll produce where marginal revenue equals mar-ginal cost and set price from the demand curve (chargingwhatever the market will bear). To accomplish this, theduopolists would need to cooperate and form a cartel. Theproblem for the duopolist is reaching an agreement throughcollusion that satisfies each firm and is enforceable. Bothfirms have an incentive to try to cheat on the agreement andundercut the other firm to gain a larger share of the market.

When the duopolists set their production levels and corre-sponding prices, they choose the best strategy based on thestrategies that they expect their competitor to choose. Thisproduces an outcome known as a Nash equilibrium. Theresult is an output greater than the monopoly output butless than the competitive output. As the number of sellersrises, the output approaches the competitive level and priceapproaches marginal cost.

A good example of the problems inherent in an oligopoly is the Organization of Petroleum Exporting Countries (OPEC).This cartel of mainly Middle Eastern oil-producing countrieswas effective in reducing output to near-monopoly level inthe 1970s. The energy crisis of 1973 was a result of OPECefforts to restrict the supply of oil to the West. In 1979, afterthe overthrow of the Shah of Iran, OPEC was again able torestrict exports of petroleum and cause another energy cri-sis. However, members had a tremendous incentive to cheatin order to earn greater profits. The result is that the cartelis no longer effective, and world petroleum production is relatively competitive.

In this assignment, we’ll examine how people behave whencooperation is desirable, but difficult to attain. The study of how people behave in strategic situations is called game theory. In these situations, a person makes decisions by tak-ing into account the possible responses by others. A simpleexample of game theory is the prisoners’ dilemma. In its original version, police interrogate two accused criminalsseparately to get a confession. Even though they gain collec-tively when they refuse to confess, they eventually do confess.

Economics 244

This is because if either one caves in and confesses, he orshe will be far better off. If each could be sure that the otherwould honor the agreement not to confess, they both wouldgain by refusing to cooperate with the police. However, eachhas an individual incentive to confess because his or herindividual gain is maximized by confessing (regardless of the strategy chosen by the opponent). This action is some-times called the dominant strategy, which is an action that’sclearly superior no matter which alternative is chosen by theother person.

Oligopolists face incentives that are similar to those in the prisoners’ dilemma. Each seller individually has anincentive to overproduce relative to the monopoly output,even though collectively there’s an incentive to restrict out-put to the monopoly level. Self-interest leads to the eventualbreakdown of cooperation.

One of the Ten Principles of Economics states that govern-ments can sometimes improve market outcomes. With thisin mind, policymakers try to push firms in an oligopoly tocompete rather than cooperate. Beginning with the ShermanAntitrust Act of 1890, public policy has treated price fixingand other actions that restrain trade as criminal conspiracy.Some actions, such as price fixing, are clearly illegal and notin society’s interest. Other business actions are less clear-cut in terms of both legality and impact on society.

For example, resale price maintenance by producers prohibitsretailers from discounting price. In another example, tyingagreements are often used to increase sales of supplies oraccessories to be used with a piece of equipment. Criticsargue that both of these actions restrain trade and limit competition. Supporters argue that both actions are justifi-able. They point out that resale price maintenance and tyingagreements may be necessary to protect the reputation of the producer.

Competition between oligopolists along with antitrust lawsprevent the firms from colluding and jointly behaving likemonopolists. Antitrust laws can promote competition, butthey can also be used inappropriately, leading to a lesseningof competition.

After you’ve read pages 345–367 in Principles of Micro-economics carefully, complete Self-Check 7. Check youranswers against those provided at the back of this studyguide. When you’re sure that you completely understandthe material from Assignment 7, move on to Assignment 8.

ASSIGNMENT 8Read this introduction to Assignment 8. Then, read Chapter 17,“Monopolistic Competition,” on pages 373–387 in the textbookPrinciples of Microeconomics.