study of afghan telecom industry - aisa€¦ · · 2014-11-07this report is based on sample...

TRANSCRIPT

Study of Afghan Telecom Industry

(MNOs, ISPs)

Rahima Baharustani

May 2013

Research, Planning & Policy Directorate, AISA

Study of Afghan Telecom Industry 2013

II

Disclaimer: Views of the author expressed in this report do not necessarily reflect the official position of Afghanistan Investment Support Agency.

Note: Exchange rate of 1$=50 AFN has been considered throughout the report.

Study of Afghan Telecom Industry 2013

III

Acknowledgments

This study was researched and written by Afghanistan investment support agency, which was authored by Rahima Baharustani. “I would like to express my deepest appreciation to higher management of AISA, particularly Mr. Wafiullah Iftekhar CEO/President of AISA, and Mr. Junaidullah Shahrani, Research Policy and Planning Director for their continuous encouragement, tremendous support and help. In addition, I would like to thank the participant of survey Mr. Ahmad Zaki, and Dr. Fazel Rabi, who willingly shared their precious time during the process of interviewing. Furthermore, I acknowledge all key informants who helped us in providing the required information”.

Study of Afghan Telecom Industry 2013

IV

Table of Contents

ACKNOWLEDGMENTS...........................................................................................................................................III

TABLE OF CONTENTS.............................................................................................................................................IV

EXECUTIVE SUMMARY..........................................................................................................................................VI

CHAPTER: 1. INTRODUCTION .................................................................................................................................1

SAMPLE AND METHODOLOGY...........................................................................................................................................1

CHAPTER: 2.TELECOM SECTOR...............................................................................................................................3

AFGHAN TELECOMMUNICATION AND REGULATORY AGENCY (ATRA) ........................................................................................4IMPORT OF ICT GOODS ...................................................................................................................................................5INVESTMENT IN TELECOM SECTOR .....................................................................................................................................5REVENUE GENERATED BY TELECOM SECTOR.........................................................................................................................7JOB CREATION ...............................................................................................................................................................8

CHAPTER: 3.MOBILE NETWORK PROVIDERS ..........................................................................................................9

RULES AND REGULATIONS................................................................................................................................................9PRODUCTION...............................................................................................................................................................10ACCOUNTABILITY..........................................................................................................................................................10COMPETITION..............................................................................................................................................................11

CHAPTER: 4.DEMAND SIDE (DETAILED FINDINGS OF SURVEY) ............................................................................. 12

FACTORS FOR BUYING SIMS ............................................................................................................................................12QUALITY.....................................................................................................................................................................13AFFORDABILITY ............................................................................................................................................................14FIXED AND MOBILE DIGITAL PHONES EXPANSION.................................................................................................................14

CHAPTER: 5. INTERNET SERVICE PROVIDERS........................................................................................................ 15

PRODUCTION...............................................................................................................................................................18JOB OPPORTUNITIES BY ISPS...........................................................................................................................................19COMPETITION..............................................................................................................................................................20FUTURE PLAN OF ISPS ...................................................................................................................................................21

CHAPTER: 6. DEMAND SIDE (KEY FINDINGS) ........................................................................................................ 22

AFFORDABILITY ............................................................................................................................................................24QUALITY.....................................................................................................................................................................25COMPARISON ..............................................................................................................................................................27SWOT ANALYSIS OF ISPS ..............................................................................................................................................28

CHAPTER: 7.GROWTH AVENUES .......................................................................................................................... 29

OPPORTUNITIES IN MNOS.............................................................................................................................................29OPPORTUNITIES IN ISPS ................................................................................................................................................30

PROBLEMS AND CHALLENGES.............................................................................................................................. 31

Study of Afghan Telecom Industry 2013

V

PROBLEMS AND CHALLENGES FACED BY MNOS..................................................................................................................31PROBLEMS AND CHALLENGES FACED BY ISPS......................................................................................................................31PROBLEMS AND CHALLENGES FACED BY USERS....................................................................................................................31

RECOMMENDATIONS .......................................................................................................................................... 32

RECOMMENDATIONS BY MNOS: ....................................................................................................................................32RECOMMENDATION BY ISPS:..........................................................................................................................................32RECOMMENDATIONS BY TELECOM SERVICE USERS: .............................................................................................................33

CONCLUSION ....................................................................................................................................................... 34

ACRONYMS.......................................................................................................................................................... 35

SOURCES CONSULTED:......................................................................................................................................... 36

APPENDICES......................................................................................................................................................... 37

APPENDIX A: ...............................................................................................................................................................37APPENDIX B: ...............................................................................................................................................................42APPENDIX C: ...............................................................................................................................................................44

Study of Afghan Telecom Industry 2013

VI

Executive Summary

Introduction of new technology in communication has become important part of daily life, facilitating easy, fast, and reliable communication all over the world. Telecommunications apply to social and economic benefits, healthcare, education, digital economy, businesses, and in creation of new jobs. All these are potential opportunities that can benefit telecommunication infrastructure. Afghanistan telecom sector after years of conflict has made tremendous growth as to fulfill the demand of customers. Telecom industry in Afghanistan has contributed more to country’s GDP. First MNO started its operation in October 1998 during Taliban, followed by Roshan mobile network operator who generated more revenue by attracting customers at an extraordinary rate. Currently, 88 percent of afghan population has access to mobile phones.

Similarly, number of internet users increased since 2002, previously price of internet was too high and now has reduced to almost 92 percent. Prior to 2005 internet was not available via satellite so the prices were high, afterwards, by usage of satellite prices has reduced and by completion of fiber optic prices will further decrease and would provide internet facilities in all over country.

This report is based on sample survey of 10 telecom companies, all located in Kabul city, some of them having branches in other major cities of country. By surveying these companies we came to know that among the biggest problems that these companies face are: discrimination by regulators as well as high tax rate on ISPs, which might result in closing of some of ISPsbusinesses.

Furthermore, 185 telecom service users surveyed to inquire quality of telecom services as well as know about their level of satisfaction from telecom services that they avail. Survey results indicated that majority of customers complained of high calling rates, signal and coverage problems.

At the end we came to know that market for mobile network operators has saturated and there in no place to new MNO to enter market, but still opportunities are there in the form of investment in new technology by existing MNOs to increase network coverage as well as reduce prices by offering wide variety of new value added services.

ISPs, cover only 20 percent of Afghan population, further investment is needed in this area as to increase internet facilities to remaining 80 percent. Survey results show that there is place for a local or foreign company with large amount of investment that could bring new technology and offer internet facilities both in urban and rural areas.

Study of Afghan Telecom Industry 2013

1

Chapter: 1. Introduction

Since the existence of human life, human’s need arose for communication. In early days, communication was difficult due to lack of proper communication means, uncertainty, and time consumption, so need for efficient means of communication arose. Innovation in new means of technology has made communication easier. Today, use of various means of telecommunication became an integrated part of society. Industrial revolution in information technology has removed geographical borders and distances and made the world into a global village, by fast and reasonable communication all over the world.

In today’s world, no life can be imagined without telecommunication as it became the important part of each and every society. In every sector of economy, telecommunication plays unavoidable role. In early stages of development telecommunication means are considered to be too expensive and confined to rich people, but revolution in this sector made all the means available at lesser cost to middle and low class people, who play vital role in the growth of economy.

Information and communication technology has improved condition of Afghanistan socially, and economically. Afghanistan’s telecommunication has had advancement in the past decade which is considered a big achievement despite problems and challenges. Achievements in this sector are but not limited to development of information and communication technology, extension of fiber optic cable, increase in government revenues, employment opportunities and many more.

Sample and Methodology

This report is based on sample survey of 10 telecom companies and 185 service users, making total of 195.Survey started in mid March 2013 and ended in mid May 2013.

This study both has quantitative and qualitative aspect. Study of telecom consists of three surveys, which assessed both suppliers of telecom operators and the users (demand side) of provided by telecom operators.

The quantitative survey include 10 telecom companies in Kabul, all are registered, to have assessment of telecom industry particularly of MNOs and ISPs operating in Afghanistan, find out new investment opportunities that could contribute more to growth of this sector, furthermore, to pinpoint problems and challenge and have recommendations to correct these problems and challenges that are ahead.

The purpose of qualitative survey was to have assessment of users of telecom services and inquire customer’s satisfaction (quality) from the services that they avail from telecom operators, to know features that current services lacks, future perspective of their products and services, and possibilities of future demand to avail new telecom products and services.

Surveyed customers related to different categories of life such as: students, teachers, shopkeepers, businessman, and employee of both governmental and nongovernmental

Study of Afghan Telecom Industry 2013

2

organizations. Majority of surveyed customers had bachelors’ degree (59) and working 8 hours per day with median salary of 15,000 AFN ($300) per month.

The survey was conducted in seven major cities of Afghanistan namely: Balkh, Herat,Kabul, Kandahar, Khost,Kunduz, and Nangarhar.

Best effort was made to get the required information form telecom companies/individuals, however, certain companies/individuals did not respond with certainquestions.

Moreover, constraints faced during survey were: First of all, due to security issues and shortage of funding, survey conducted in areas where AISA have offices in regional areas. Secondly, due to shortage of time. Thirdly, lack of awareness and due to high illiteracy rate certain individuals who lived in remote areas could not respond accurately.

Study of Afghan Telecom Industry 2013

3

Chapter: 2.Telecom Sector

Decades of bitter war destroyed Afghanistan’s infrastructure. People in Afghanistan faced problems while communicating with each other’s especially while making international calls, limited public phone booths were available in Kabul city for which people used to wait for long hours to use phone. While others used to go to neighboring countries to make an international call.

Now, Afghanistan telecom sector has shown tremendous growth over last decade as compared to some of neighbor countries. Telecom sector contributed more to the GDP of economy and brought revenue to government in the form of tax payment by individual companies as well as revenue to their self, and created job opportunities which ended in high living standards, and economic & social development. By passage of each year revenue of this sector has increased showing increase in demand for telecom products and services. Afghan telecom services can be divided predominantly into basic, mobile and internet services. Postalservices, media (television, radio services), technical assistance to make electronic identity cards, digital television, introduction of electronic government, and planned to launch satellite. Growth of this sector mostly came from MNOs and ISP as compared to other mentioned areas of telecom. Currently, there are total of 5 MNO operators in Afghanistan, facilitating over 88percent of afghan population almost in every part of the country. Number of ISPs has increased since 2002, with facilities provided to limited population (20 percent). There are 49 ISPs operating in major cities of Afghanistan.

Study of Afghan Telecom Industry 2013

4

Graph: 1. Different areas of telecom

Source: ministry of information and communication

Ministry of communication and information technology is the governing body in communication and IT sector to create grounds that could ensure effective and efficient development of telecommunication in the country. MCIT is responsible to ensure provision of best services with reasonable prices, increase the application of telecom and IT system in socio-economic development of country.

Reason for growth of telecom sector is:

Afghan telecom sector has been booming for last couple of years, it’s because of increase in level of education and increase in earning power to avail telecom services, other reasons are:

Free market Digital business, provides communication line across world Quick and easy communication Need of each sector for advanced technology, provides more facilities People demand/ expectations

Afghan telecommunication and regulatory agency (ATRA)

ATRA, afghan telecommunication regulatory agency is the regulatory agency for this industry, the regulatory environment within telecommunication sector in Afghanistan has been developed over the past decade. ATRA currently work within framework of the MCIT independently to regulate functions related to telecommunication sector. ATRA is working to implement international best practices in Afghanistan so that the telecom sector of Afghanistan could compete with international level. ATRA has the responsibility of issuing licenses to telecommunication and IT companies, and control and supervise telecom companies.

ATRA is committed to bring new and advanced technology to better facilitate telecom companies, and individual users. To increase telecommunication services and coverage areas, ARTA has increased the installation of base transceiver station as following diagram showsincrease in BTS.

MNOs

ISP

Postal services

Radio

Digital TV

Study of Afghan Telecom Industry 2013

5

Graph: 2. Increase in number of BTS since 2003

Source: Ministry of communication and information technology

Import of ICT goods

Afghanistan imports ICT goods because, currently, Afghanistan is not in the position to produce these technological tools and equipments by itself. ICT equipments that are mostly imported from other companies are computer related equipment, electronic components, and other information and communication technology goods. Excluding software tools. Total ICT goods import for the year 2008 was 0.5 percent, 0.3 percent in 2009 and 0.4 percent for the year 2010 (according to World Bank) data for recent years was NA.

Investment in Telecom sector

Following graph shows investment in telecom projects along with private participation. These projects include operation and management contracts, green field projects, and divestitures, excluding investment in movable assets and small projects. Total investment in telecom sector with participation of private sector.

0

1000

2000

3000

4000

5000

6000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Base Transceiver Stations (2003-12)

Study of Afghan Telecom Industry 2013

6

Graph: 3. Total Investment in Telecom (Amount in USD)

Source: World Bank Statistics

Private investment

Investment by private sector in telecom has reached 1.9 million dollars by 2012 with average annual growth of 8.01 percent since 2002. Denoting interest of private investors in telecom sector over past decade.

Graph: 4. Cumulative investment by private sector (2002-2012)

Source: Ministry of communication and information technology

0100000000200000000300000000400000000500000000600000000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Investment in Telecom Sector

0

500

1000

1500

2000

2500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Cumulative Investment (million USD)

Study of Afghan Telecom Industry 2013

7

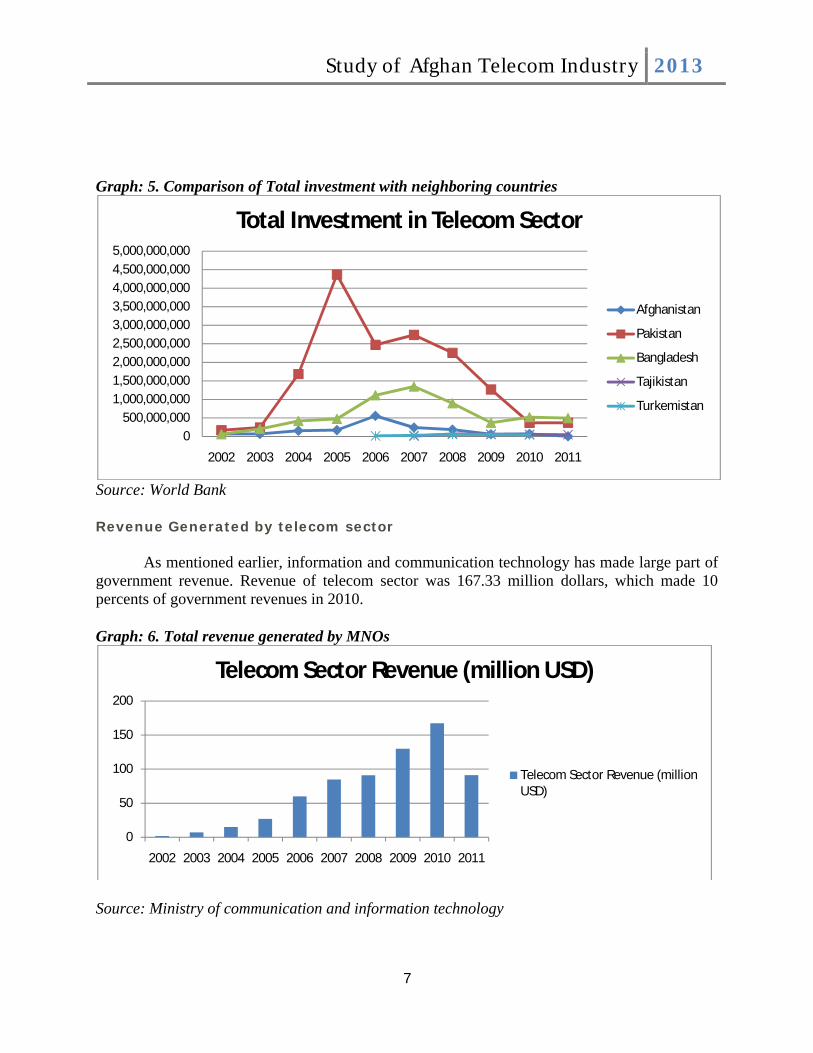

Graph: 5. Comparison of Total investment with neighboring countries

Source: World Bank

Revenue Generated by telecom sector

As mentioned earlier, information and communication technology has made large part of government revenue. Revenue of telecom sector was 167.33 million dollars, which made 10 percents of government revenues in 2010.

Graph: 6. Total revenue generated by MNOs

Source: Ministry of communication and information technology

0500,000,000

1,000,000,0001,500,000,0002,000,000,0002,500,000,0003,000,000,0003,500,000,0004,000,000,0004,500,000,0005,000,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Total Investment in Telecom Sector

Afghanistan

Pakistan

Bangladesh

Tajikistan

Turkemistan

0

50

100

150

200

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Telecom Sector Revenue (million USD)

Telecom Sector Revenue (million USD)

Study of Afghan Telecom Industry 2013

8

Job creation

This sector has created job opportunities for large amount of people as just for the year 2010 created total of 100000 jobs, both hiring directly and indirectly. Direct jobs of 20000 professionally working in MNOs and ISPs, while remaining 80000 were employed indirectly.

Study of Afghan Telecom Industry 2013

9

Chapter: 3.Mobile Network Providers

First mobile network operator in Afghanistan started its operation in year 1998 with more than $50 million, while security condition was severe in the country. Since then many improvement have been seen in MNOs, products and services of mobile network operators have improved along with decrease in overall prices.

Survey covered local, JV and foreign MNOs, who covered almost all provinces of the country. As compared to ten years back products and services of MNOS have improved, currently, MNOs provide all GSM services including VAS services, leased line services, prepaid & post paid data services, and digital telephones. Each mobile network operator is trying to provide unique services as to boost their sales by attracting more customers.

According to survey 3 percent of staff who work in these companies was experts with 2-5 percent of the staff being females.

Rules and Regulations

Rules and regulations of government regarding telecom industry is considered to be, 33 percent very effective, 34 percent less effective and 33 percent did not respond.

Support and supervision of government is considered to be an important factor in success of any business, when companies were asked regarding support and supervision of regulatory agencies, 33 percent stated that support and supervision to be highly supportive, while 34 percent considered it to be less supportive.

Study of Afghan Telecom Industry 2013

10

Majority (67 percent)of companies observe telecommunication law to be effective, but stated that it further needs to be revised since it cannot fulfill some of current issues, and stressed on proper implementation of law on all companies equally.

Production

Operators undertake to offer quality services by bringing new technology and offer variety of services with cheap prices as to attract more customers. From current situation it seems that in near future prices may further decrease.33 percent of companies observed increasing trend of overall sale of their products and services, while 34 percent decreasing trend, on the other hand, 33 percent did not respond.

Mobile users in 2010 increased by 8.2% as compared to previous year, which resulted tomake approximately 16.33 million people.

Graph: 7. Trend of mobile phone users (for period of 2002-2012)

Source: Ministry of communication and information technology

MNOs market their products and services through SMS, TV, radio, retail, road show and bill boards. During survey we came to know that some people are being disturbed by marketing through SMS and asked companies to use other means of marketing rather marketing through SMS.

Accountability

To get cure many ill of MNOs, that harms customers ATRA has created strict environment so that no operator could violate the law. In case of violation of law ATRA fines Mobile network operators as in the year 1389 ATRA fined 13.64 million AFN due to poor

0

5

10

15

20

25

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Phone Users (million)

Study of Afghan Telecom Industry 2013

11

service quality. ATRA just controls interconnection rates and does not control prices offered by individual operators, as they have kept market free.

Competition

There is tough competition going on among mobile companies as everyone is trying to get largest share of market for their selves. Intense competition has resulted in reduction of cost over past decade. Competition in market has resulted in price reductions to buy sim cards and avail other telecom services. Prices of Sims provided by private companies which were 15000 ($ 300) in 1381, has reduced to 5000-50 AFN ($ 100-$1) depending on the type and features provided by companies, showing reduction of 99 to 90 percent since 2003. Local calls per minute charged 18 AFN (36 cents) in 1385 (2006) which has now reduced to 7-1 AFN (0.14-0.02 cents). Similarly, international call rates have reduced from 100 AFN ($2) to 5 AFN ($ 0.1).

In view point of regulators current MNOs can fulfill need of afghan citizens and there is no need for new company to enter the market, market is saturated.

Study of Afghan Telecom Industry 2013

12

Chapter: 4.Demand side (Detailed Findings of survey)

Random sample of 185 customers was chosen with median age of 26 and median salary of 15000 AFN ($ 300)

Majority of surveyed entity used more than one sim as just 38 percent had just one sim.Large number of surveyed individuals stated that they are using more than one sim to reduce cost, and sometimes due to signal and coverage problems, poor customer service, get benefit of different packages, and use different sims one for calling and other for using internet.

Graph: 8. Number of Sims used by surveyed individuals

Source: Mobile network users

In Afghanistan due to low socio economic condition most of population use cell phones which don’t support internet connection, this is the reason that majority (71 percent) of MNOs customers use mobile just for calling.

Factors for buying Sims

Before buying sim the factors that are mainly considered in Afghanistan are:

More facilities Free messages Less charges Coverage and signal Quality of voice with reasonable cost Registration of sim Fast connection and active network Good customer service

0

10

20

30

40

50

60

1 2 3 4 5 6 no response

Number of SIMs

Study of Afghan Telecom Industry 2013

13

Quality

Network accessibility and coverage differs across country which affect quality of MNOs.In response to question regarding quality of mobile network, 10 percent rated excellent, 31 percent good, 29 percent average, 13 percent poor, and 15 percent stated that the quality is too poor. Moreover, 2 percent declared voice quality to be excellent, 34 percent good, 47 percent average, 11 percent poor, and 5 percent abysmal.

20 percent of surveyed individuals rated speed of mobile excellent, 5 percent good, 24 percent average, 47 percent poor, and finally 4 percent abysmal. Due to poor signal, network coverage, and high rates 37 percent of individuals changed their Mobile networks, while 63 percent stated that they have not changed yet, but have more than one sims. Reasons forchanging their mobile networks was lack of satisfaction from mobile network operators, to find out better alternative in terms of fast connectivity and better customer services with less cost, better coverage and less cost.

29 percent stated that the biggest cause of their dissatisfaction from MNO is high cost and prices,24 percent due to unfair charges, and 22 percent was dissatisfied because of dropped calls/lack of signal/lack of coverage, other causes of dissatisfaction is mentioned in graph below.

Graph: 9. Causes of dissatisfaction from Mobile network operators

Source: responded by surveyed customers

0 5 10 15 20 25 30 35

Other

Dropped messages/messages arrive late

Cost/Price/Too expensive

Poor customer service

Problems with roaming (poor reception, overlapping areas)

Unfair charges

Dropped calls/lack of signal/lack of coverage

Causes of Dissatisfaction

Study of Afghan Telecom Industry 2013

14

Affordability

Prices and calling rates have reduced tremendously since 2003, but still 29 percent of surveyed individuals observed prices to be highly expensive, majority (51 percent) expensive, and 3% reasonable. According to surveyed individuals the MNOs who have good network coverage/signal but rates are highly expensive.

Fixed and mobile digital phones expansion

Landline phones are available in major cities as proper infrastructure is not available to connect remote areas. Up to end of 2012 there were 9017 landlines all over the country. Ministry of telecom has planned to increase landlines all over country. Fund for this project would be provided by development budget.

In Afghanistan there is more trend of using mobile phones as compared to landline phones, 53 percent of surveyed individuals stated that they don’t use landline and prefer mobile phones, while other 44 percent used landline. Landline is used mostly in offices and according to informal source digital landlines has failed in Afghanistan as there is less demand for it.

Study of Afghan Telecom Industry 2013

15

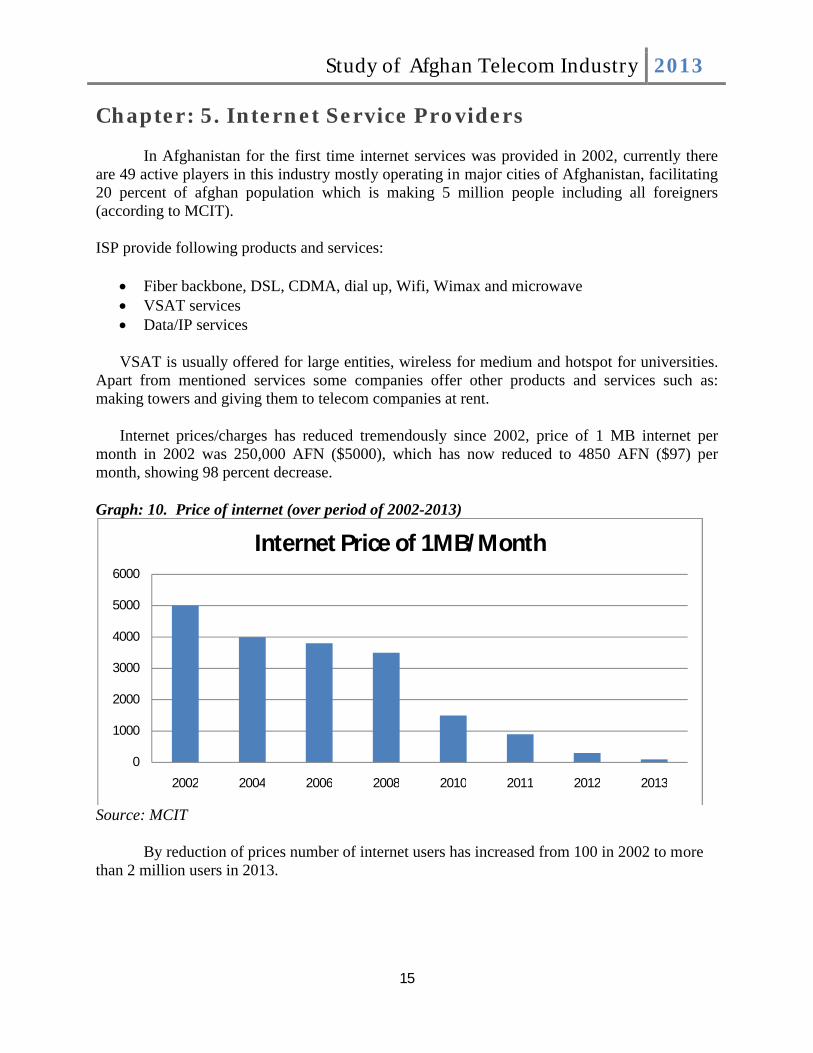

Chapter: 5. Internet Service Providers

In Afghanistan for the first time internet services was provided in 2002, currently there are 49 active players in this industry mostly operating in major cities of Afghanistan, facilitating 20 percent of afghan population which is making 5 million people including all foreigners(according to MCIT).

ISP provide following products and services:

Fiber backbone, DSL, CDMA, dial up, Wifi, Wimax and microwave VSAT services Data/IP services

VSAT is usually offered for large entities, wireless for medium and hotspot for universities. Apart from mentioned services some companies offer other products and services such as: making towers and giving them to telecom companies at rent.

Internet prices/charges has reduced tremendously since 2002, price of 1 MB internet per month in 2002 was 250,000 AFN ($5000), which has now reduced to 4850 AFN ($97) per month, showing 98 percent decrease.

Graph: 10. Price of internet (over period of 2002-2013)

Source: MCIT

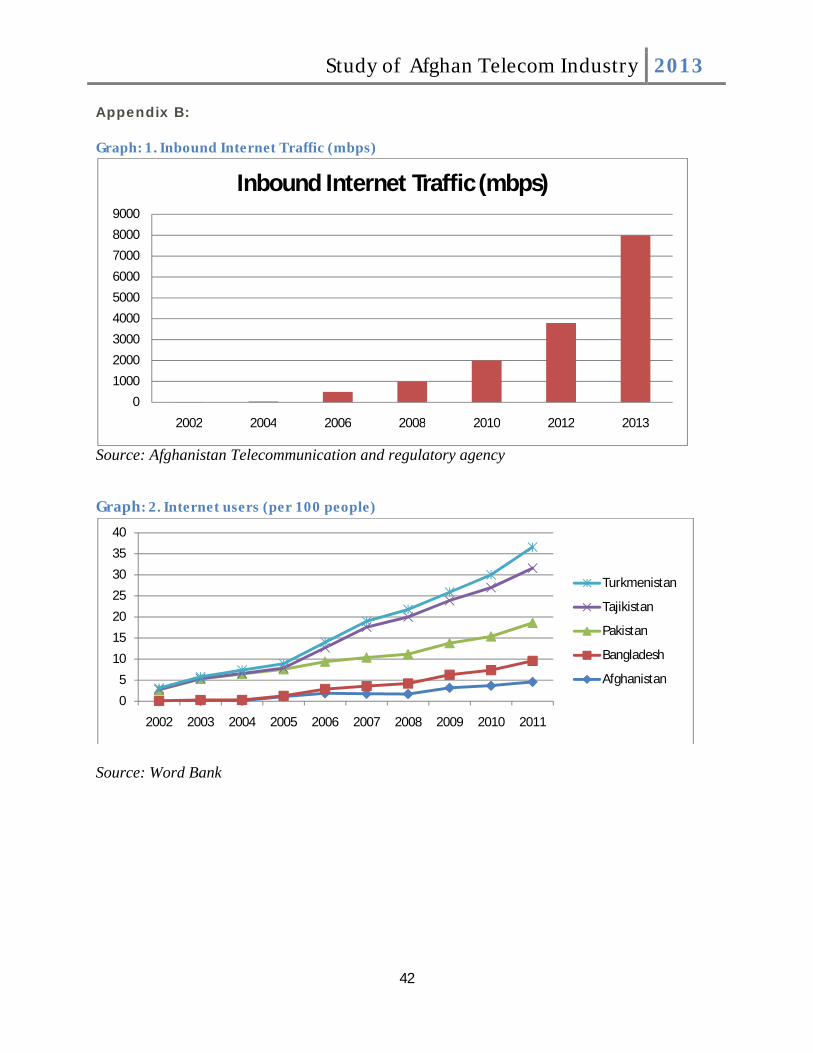

By reduction of prices number of internet users has increased from 100 in 2002 to more than 2 million users in 2013.

0

1000

2000

3000

4000

5000

6000

2002 2004 2006 2008 2010 2011 2012 2013

Internet Price of 1MB/Month

Study of Afghan Telecom Industry 2013

16

Graph: 11. Increasing trend of Internet services users

Source: MCIT

Majority of surveyed ISPs operate and have branches in large cities of Afghanistan such as: Balkh, Herat, Nangarhar, Kunduz, and Kabul. ISP services are mostly provided by private sector, private players have witnessed growth due to introducing of new technologies and strong impetus. The quality and penetration of these services have undergone changes.

Sample included internet service providers operating in Kabul. Most (87%) of ISP had well established businesses in providing internet facilities while 13 percent of them newly got the license of ISP and are on their primary stages of providing internet facilities, while previously they provided ICT services.

57 percent of surveyed companies operate as private local company, 29 percent foreign and 14 percent local. 50 percent of surveyed companies declared their investment to be remained same as it was at first year, 33 percent witnessed average increase of 65 percent, while remaining17 percent declared their investment to be decreased. ISPs price their services based on operative expenses plus mark up, prices are negotiable, and they wave certain amount for their valued customers. To expand businesses, firms usually reinvests portion of their revenue. In response to reinvesting the revenue received from sales, 57 percent of surveyed companies stated that they invest on average 62 percent of revenue obtained from sales. People who mostly use internet belong to category of youth either in offices or at home.

0

500000

1000000

1500000

2000000

2500000

3000000

2002 2004 2006 2008 2010 2011 2012 2013

Internet Users

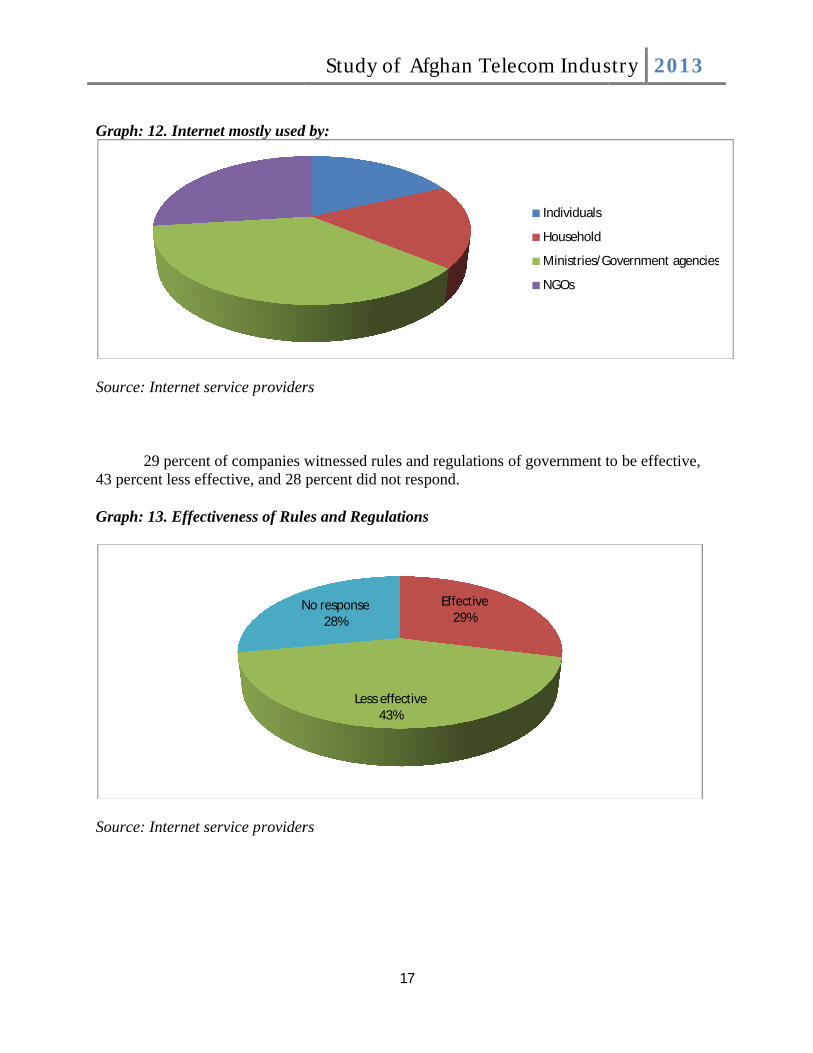

Graph: 12. Internet mostly used by:

Source: Internet service providers

29 percent of companies witnessed rules and regulations of government to43 percent less effective, and 28 percent did not respond.

Graph: 13. Effectiveness of Rules and Regulations

Source: Internet service providers

No response

Study of Afghan Telecom Industry

17

Internet mostly used by:

Source: Internet service providers

29 percent of companies witnessed rules and regulations of government to28 percent did not respond.

Effectiveness of Rules and Regulations

Source: Internet service providers

Individuals

Household

Ministries/Government agencies

NGOs

Effective 29%

Less effective 43%

No response 28%

Telecom Industry 2013

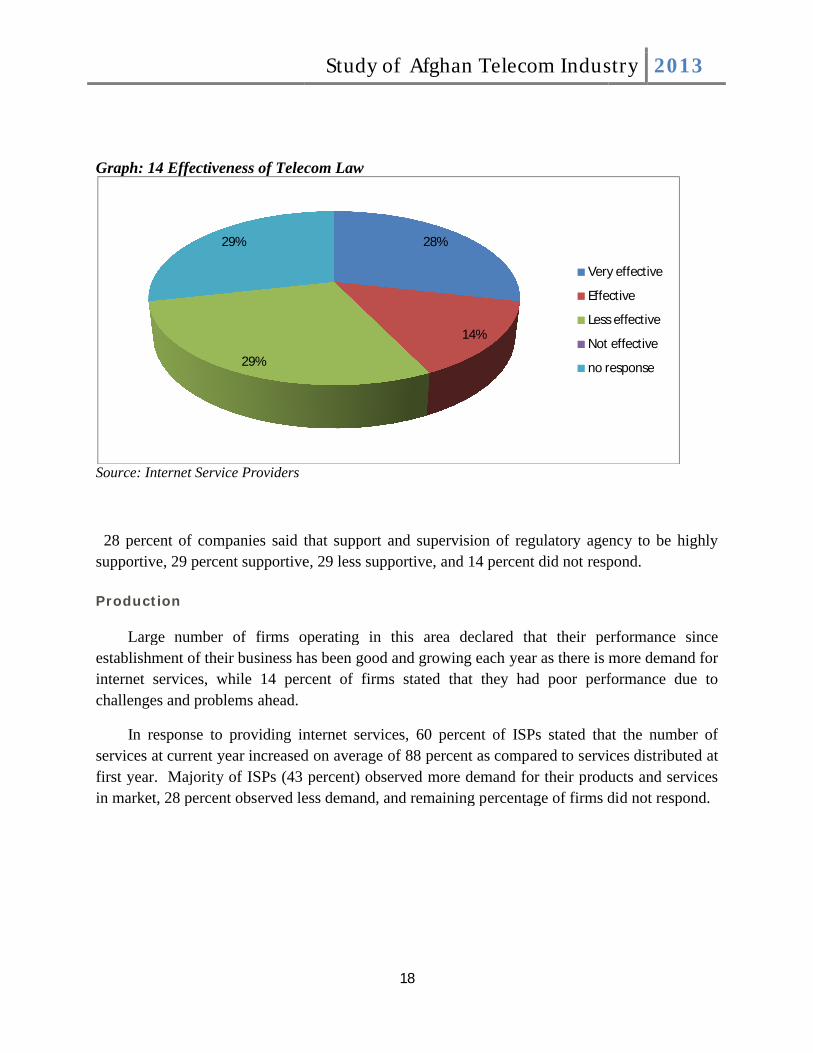

29 percent of companies witnessed rules and regulations of government to be effective,

Ministries/Government agencies

Graph: 14 Effectiveness of Telecom Law

Source: Internet Service Providers

28 percent of companies said that support and supervision of regulatory agency to be highly supportive, 29 percent supportive

Production

Large number of firms operating in this area establishment of their business has beeninternet services, while 14 percent of firms stated that they had poor performance due to challenges and problems ahead.

In response to providing internet services, 60 percent of ISPs stated that the number of services at current year increased on average first year. Majority of ISPs (43 percent) observed more demand for their pin market, 28 percent observed less demand, and remaining percentage of firms did not respond.

29%

29%

Study of Afghan Telecom Industry

18

Effectiveness of Telecom Law

percent of companies said that support and supervision of regulatory agency to be highly percent supportive, 29 less supportive, and 14 percent did not respond.

Large number of firms operating in this area declared that their performance since blishment of their business has been good and growing each year as there is more demand for

internet services, while 14 percent of firms stated that they had poor performance due to

onse to providing internet services, 60 percent of ISPs stated that the number of services at current year increased on average of 88 percent as compared to services distributed at first year. Majority of ISPs (43 percent) observed more demand for their products and services in market, 28 percent observed less demand, and remaining percentage of firms did not respond.

28%

14%

Very effective

Effective

Less effective

Not effective

no response

Telecom Industry 2013

percent of companies said that support and supervision of regulatory agency to be highly percent did not respond.

their performance since good and growing each year as there is more demand for

internet services, while 14 percent of firms stated that they had poor performance due to

onse to providing internet services, 60 percent of ISPs stated that the number of 88 percent as compared to services distributed at

roducts and services in market, 28 percent observed less demand, and remaining percentage of firms did not respond.

Very effective

Effective

Less effective

Not effective

no response

Study of Afghan Telecom Industry 2013

19

Graph: 15. Demand for ISP Products/Services

Source: Internet Service Providers

Job opportunities by ISPs

ISPs usually have fewer work forces as people hired directly are less in number but have created more job opportunities indirectly. As shown in graph majority of ISPs have 1 to 99 staff it’s because majority of ISPs have fewer branches usually 1 to 4 branches in major cities. Out of this number on average 49 percent of these staff are professionals.

Previously, more foreigners were involved in each and every area of the economy, but nowadays every business is trying to hire local staff as to create more job opportunities for local citizens, as witnessed in telecom industry number of foreign staff has decreased gradually. Surveyed companies (50 percent) stated that previously they had more foreign staff who worked in technical areas, but now foreign staff has decreased, while remaining 50 percent stated that they have no foreigner staff. In Afghanistan females has less participation in technical positions, as in telecom industry less participation of females has been noticed, on average 25 females were hired by these companies.

Increasing demand 43%

Decreasing demand

28%

No response29%

Study of Afghan Telecom Industry 2013

20

Graph: 16. Number of Workers Employed by Internet Service Providers

Source: Internet Service Providers

Competition

Tough competition is going on in market among internet service providers, which sometime cause companies to forgo profit to keep their customers. 71 percent of surveyed firms observed competition to be tough, and healthy, 15 percent stated that competition is unfair due discrimination in giving facilities by regulatory agencies. Remaining percentage did not respond.

Graph: 17. Factors Hampering ISP Businesses

Source; Internet Service Providers

0

0.5

1

1.5

2

2.5

3

3.5

1-99 100-500 more than 500

Number of Workers Employed

0 5 10 15 20 25 30 35

Security issues

Lack of coordination

Short of skilled labor

High tax rate

Shortage of land

Airport problems

Insufficient demand for product

Closing of NGOs

Factors Hampering ISP businesses

Study of Afghan Telecom Industry 2013

21

Future plan of ISPs

ISPs are planning to expand internet services all over the country with reasonable prices by establishing branches, Upgrade Wimax infrastructure in cities and provinces. Soon O3B would be launched which is a global satellite service provider that is deploying a next generation satellite network which combines the reach of satellite with speed of fiber which is called O3B.

Chapter: 6. Demand side

Random sample of 93 internetuse internet mostly in office, and only 8 percent of surveyed customers used internet at Cable modem which is comparatively reasonable is mostly used by individuals 54 percent followed by DSL, dial up and 3G provided by MNOs.

Graph: 18. Type of internet mostly used

Source: internet service users

In today’s world internet has become major part of each and everyone’s life, it can be used for many purposes, according to our survey, people work/business (21 percent) and education (21 percent),followed by communication with others (20 percent) and gathering information for personal use.

25%

Dial up 13%

Study of Afghan Telecom Industry

22

Demand side (Key Findings)

Random sample of 93 internet users were chosen out of which 69 percent stated that they use internet mostly in office, and only 8 percent of surveyed customers used internet at

modem which is comparatively reasonable is mostly used by individuals 54 percent 3G provided by MNOs.

Type of internet mostly used

In today’s world internet has become major part of each and everyone’s life, it can be used for many purposes, according to our survey, people in Afghanistan mostly use internet for work/business (21 percent) and education (21 percent),followed by communication with others (20 percent) and gathering information for personal use.

Cable modem 54%DSL

25%

Dial up 13% 3G

8%

Types of Internet

Telecom Industry 2013

users were chosen out of which 69 percent stated that they use internet mostly in office, and only 8 percent of surveyed customers used internet at home.

modem which is comparatively reasonable is mostly used by individuals 54 percent

In today’s world internet has become major part of each and everyone’s life, it can be in Afghanistan mostly use internet for

work/business (21 percent) and education (21 percent),followed by communication with others

Graph: 19. Purpose of using internet for

Source: internet service users

When asked regarding usage of internet per day, 30 percent used up to one hour, 20 percent one to 3 hours, 19 percent 3

Graph: 20. Usage of internet per day

Source: internet service users

Education

Entertainment

Communication with others

Shopping/gathering product information

Work/business

Gathering information for personal use

Wasting time

Other

19%

17%

14%

Usage of Internet per Day

Study of Afghan Telecom Industry

23

Purpose of using internet for:

When asked regarding usage of internet per day, 30 percent used up to one hour, 20 percent one to 3 hours, 19 percent 3-5 hours and 17 percent used more than 5 hours.

Usage of internet per day

9%

5%

1%

5%

Education

Entertainment

Communication with others

Shopping/gathering product information

Work/business

Gathering information for personal use

Wasting time

Other

Usage of internet

30%

20%

Usage of Internet per Day

Up to one hour

One to 3 hours

3 to 5 hours

More than 5 hours

No response

Telecom Industry 2013

When asked regarding usage of internet per day, 30 percent used up to one hour, 20 5 hours and 17 percent used more than 5 hours.

21%

20%

21%

18%

Up to one hour

One to 3 hours

3 to 5 hours

More than 5 hours

No response

Affordability

44 percent of respondents observed internet prices to be highly expensive, 29 percent expensive, while 13 percent stated

Graph: 21. Internet service prices

Source: internet users

Almost one in three respondents (35 percent) paid 1000by 25 percent who paid less than 500 AFN($30), while 18% did not respond.

Graph: 22. Internet users pay for internet services per month

Source: internet service users

44%

25%

Less than 500 1000

Paying for Internet per month

Study of Afghan Telecom Industry

24

44 percent of respondents observed internet prices to be highly expensive, 29 percent expensive, while 13 percent stated it’s reasonable.

service prices

respondents (35 percent) paid 1000-1500 AFN ($20by 25 percent who paid less than 500 AFN ($10), and 22 percent paid more than 1500 AFN

, while 18% did not respond.

users pay for internet services per month

13%

29%

14%

Internet Charges

35%

22%18%

1000-1500 More than 1500 Not responded

Paying for Internet per month

Telecom Industry 2013

44 percent of respondents observed internet prices to be highly expensive, 29 percent

($20-$30), followed and 22 percent paid more than 1500 AFN

Reasonable

Expensive

Highly expensive

No response

18%

Not responded

Quality

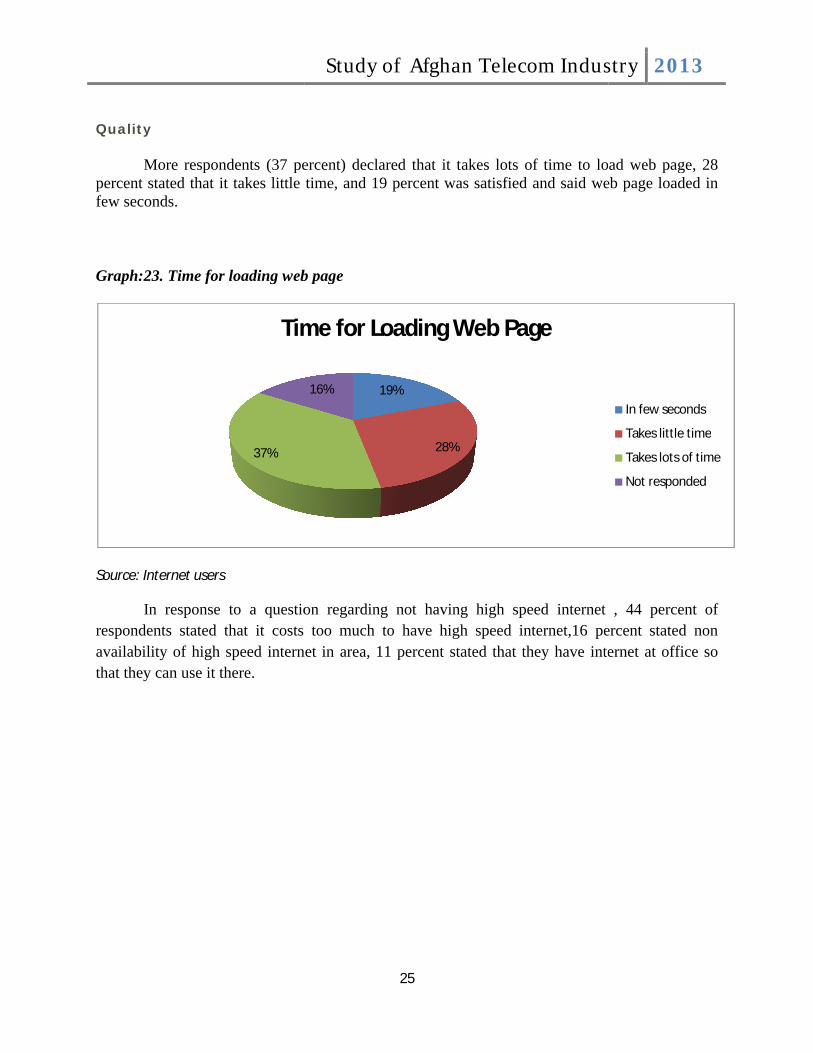

More respondents (37 percent) declared that it tpercent stated that it takes little time, and 19 percent was satisfied and said web page loaded in few seconds.

Graph:23. Time for loading web page

Source: Internet users

In response to a question respondents stated that it costs too much to have high speed internet,16 percent stated non availability of high speed internet in area, 11 percent stated that they have internet at office so that they can use it there.

37%

Time for Loading Web Page

Study of Afghan Telecom Industry

25

More respondents (37 percent) declared that it takes lots of time to load web page, 28 little time, and 19 percent was satisfied and said web page loaded in

Time for loading web page

question regarding not having high speed internet , 44 percent of costs too much to have high speed internet,16 percent stated non

internet in area, 11 percent stated that they have internet at office so

19%

28%

16%

Time for Loading Web Page

Telecom Industry 2013

lots of time to load web page, 28 little time, and 19 percent was satisfied and said web page loaded in

not having high speed internet , 44 percent of costs too much to have high speed internet,16 percent stated non

internet in area, 11 percent stated that they have internet at office so

In few seconds

Takes little time

Takes lots of time

Not responded

Study of Afghan Telecom Industry 2013

26

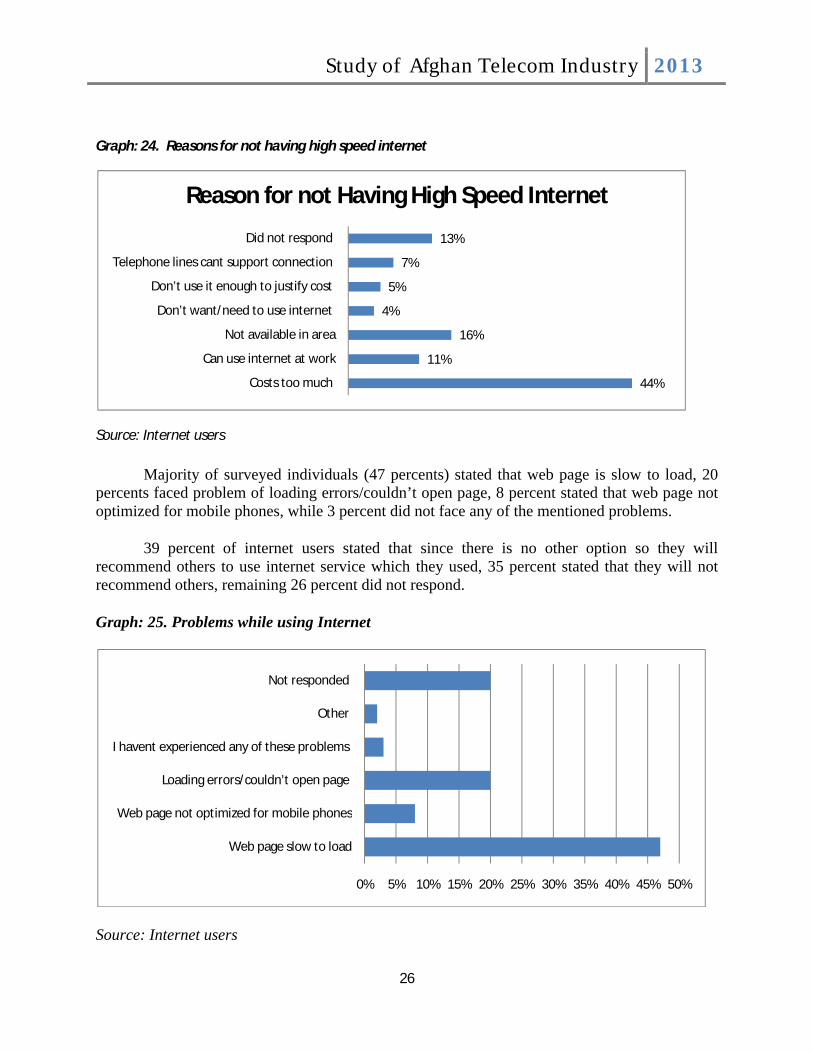

Graph: 24. Reasons for not having high speed internet

Source: Internet users

Majority of surveyed individuals (47 percents) stated that web page is slow to load, 20 percents faced problem of loading errors/couldn’t open page, 8 percent stated that web page not optimized for mobile phones, while 3 percent did not face any of the mentioned problems.

39 percent of internet users stated that since there is no other option so they will recommend others to use internet service which they used, 35 percent stated that they will not recommend others, remaining 26 percent did not respond.

Graph: 25. Problems while using Internet

Source: Internet users

44%

11%

16%

4%

5%

7%

13%

Costs too much

Can use internet at work

Not available in area

Don’t want/need to use internet

Don’t use it enough to justify cost

Telephone lines cant support connection

Did not respond

Reason for not Having High Speed Internet

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Web page slow to load

Web page not optimized for mobile phones

Loading errors/couldn’t open page

I havent experienced any of these problems

Other

Not responded

Study of Afghan Telecom Industry 2013

27

Cheap and reasonable internet would be available by completion of fiber optic project. Fiber optic is a ring around Afghanistan. Fiber optic would be a big achievement for Afghanistan, the installation of the fiber optic started in 2007 and its work is in progress which will connect all Afghanistan to its neighboring countries.80 percent of internet cost would be decreased by completion of this project

Comparison

Business differences are there among countries in region. Despite many problems and challenges which exist in the country, Afghanistan is still in the position to compete with certain countries in the region as ISPs in Afghanistan can compete with certain neighboring countries and it’s much advanced as compared to them. Following graph shows that Afghanistan is much better in region than Turkmenistan as well as from Uzbekistan and in some cases better than Tajikistan.

Secure servers are servers using encryption technology in Internet transactions. In Afghanistan one in per 1 million is secure internet servers, using encryption technology in internet transactions, better than Turkmenistan.

Graph: 28.Secure Internet servers (per 1 million people)

Source: Word Bank

050

100150200250

2003 2004 2005 2006 2007 2008 2009 2010 2011

Afghanistan

Bangladesh

Pakistan

Tajikistan

Turkmenistan

Study of Afghan Telecom Industry 2013

28

SWOT analysis of ISPs

Strength

More growth due to higher demand by citizens

Fiber optic ring across country which will provide cheap internet

Experienced, clear objective

World view

Good government Policies

Control of policy with foreigner professional

Limitations

Limited connectivity in most provinces Lack of coordination Security as could not expand the fiber

optic to all provinces of the country

Not proper planning of other organizations

Electricity

Not proper infrastructure

Public awareness

Policy of other sectors

Opportunities

Sell more to existing customers by lowering prices

Penetration, Convert strong brand value into

opportunity easy Simple offers to its subscribers,

Familiarizing people with new technology

Expansion of ISPs in areas where required

Threats

Security issues Unhealthy competition in certain areas Discrimination by regulators Close of certain NGOs

Study of Afghan Telecom Industry 2013

29

Chapter: 7.Growth Avenues

Telecom is one of fastest growing sector of afghan economy. There are many reasons why to invest in Afghanistan telecom sector.

Growing economy. More growth in telecom sector as compared to some of neighboring countries.

More revenue Cheap labor Liberal foreign investment regime Offering high rates of return Large untapped potential in afghan economy, untapped market More demand Low telecom penetration

In both MNOs and ISPs investment opportunities are there in areas of technology and expansion of their services.

Opportunities in MNOs

Market for MNOs, is believed to be saturated up to some extent while there are more opportunities still exists as to increase network coverage to remote areas and provide advanced quality services used in daily life as 3G/LTE can evolve the data market and mobile money can change the banking system.

MNOs have fully responded to demand by afghan economy by covering 88 percent of afghan population almost in all provinces of country. MNOs provide almost all value added services based on need of afghan economy.

However, existing MNOs can invest in areas of using new technology and equipments to increase voice quality, speed of connectivity, and strong signal and coverage.

Furthermore, there is demand for innovation in services offered by MNOs in the form of:

CPP (calling party pays), there is need for this since in certain remote areas due to unavailability of top up cards or other means of getting credit this can be helpful.

Introduction of advertisement portal to sell and purchase property, home appliances, cars and etc.

Payments (secure transactions) via mobile network without GPRS or internet connections, inside and outside country

Paying utility bills and billing inquiries Checking account balance and fund transfer to other bank account and interbank funds

transfer

Study of Afghan Telecom Industry 2013

30

Opportunities in ISPs

Investment opportunities are there with large untapped potential to the country’s increasing population, currently only 20 percent of afghan population has access to internet facilities. As per need of afghan population it is considered that the demand for internet services will continue to increase in future by reduction of its cost.

There is need that the regulatory agency must make uniform practices to become fully digitized which will ultimately help increase the consumption of internet.

Expanding coverage to all provinces of the country Centers for providing internet facilities More investment in terms of bringing advanced technology so that internet could be

accessible to all with cheaper rates and quality services, this requires large investment at first and then will result in higher return.

Address instruction through mobile internet Bring new advanced technology to make it hub Sell more to existing customers by lowering prices Penetration Simple and easy offers to its subscribers Familiarizing people with new technology Focus on rural areas Introduction of new technology as to control ones home and shops by a single chip. This

new technology is called next-generation network (NGN), which is a packet based and uses IP to transport the various types of traffic (voice, video, data and signaling)

Furthermore, ISPs should focus on growth of market in strategic areas, such as cloud communication and vertical industries.Evolution of MNOs provides ongoing opportunities for handset/device manufacturers and other equipment manufacturers that could support internet.

Study of Afghan Telecom Industry 2013

31

Problems and Challenges

Majority of telecom companies stated that security as most operators expansion strategy getting hampered, and shortage of skilled labor is mostly hampering their investment activities, other factors that are causing problems are listed below:

Problems and challenges faced by MNOs.

High tax structure Lack of proper supervision Deceptive advertisement by other MNOs Illiterate customers to adopt new technological services Electricity shortage High opex puts operators limited options Over regulation, barriers on entry Outdated technology Bureaucracy and discrimination by regulators Tariff regulation by ATRA

Problems and challenges faced by ISPs

Less support from government Prices of net cafes must be controlled Government policy is not according to current market situation Unhealthy competition 10 percent BRT is too expensive on ISPs and unfair since 10 % is charged on both GSM

and ISPs although GSM companies are providing variety of services ISP services are not Secure as data can be viewed by foreigners No control on illegal sim boxes Lack of professionalism in government agencies

Problems and challenges faced by users

Majority of surveyed individuals had problem with the prices, they declared calling prices both for national and international to be too expensive, furthermore, lack of signal and coverage in most areas and sudden disconnections.

Study of Afghan Telecom Industry 2013

32

Recommendations

Recommendations by MNOs, ISPs, and individual users are listed below respectively:

Recommendations by MNOs:

Equally implementation of rules, regulation on each company Coordination must be there among MNOs Provide uniform technology opportunities to all operators Review telecom policy according to current market situation Bilateral service agreements Regulators should control prices as same prices must be charged by every company Government should have proper control over MNOs, so that to get rid of fake

advertisements/deceiving people. Actuality of advertisement must be traced Government must play its role so as to get rid of bureaucracy and corruption in telecom

sector to better serve people Government should encourage more investment and increase competitions among current

companies Spread awareness on usage of mobile and internet services, reduce rates and better

facilitate people Security must be provided to MNOs to get rid of signal problems during night time AISA must trace hiring of foreigners as it must be reduced day by day

Recommendation by ISPs:

Lots of effort is needed to advance ISP in the country as first of all current policy of ISP must be revised

Government should put more effort to ensure security of ISPs, this would re-enforce the investors to better improve industry

Install more towers in mountainous areas to have good signal and coverage even in remote areas

M-commerce, M-health-banking must be implemented in all organizations BRT tax must be reduced from 10 percent to 5-2 percent Government should support both MNOs and ISPs equally, no ISPs can provide voice

services, but MNOs provide ISP services which is considered unfair by companies Commission by AISA to solve issues of investors, free of bureaucracy and corruption Ministry of telecom must control and supervise companies properly during probationary

period as either to put penalty or terminate license if could not provide ISP quality services

Ministry of telecom to control all ISPs and make them provide excellent facilities Foreigners must be hired to train locals It would be more beneficial if Afghan telecom operate as a wholesaler rather retailer

Study of Afghan Telecom Industry 2013

33

AISA must supervise companies on yearly basis Spread awareness of using fiber backbone services Paving the path and protect via a standardized method

Recommendations by Telecom service users:

Companies must reduce Prices of both national and international calls. Calling charges must be per seconds

Offer different packages for different categories of people Quality of voice call must be improved New companies must enter market with advanced technology as to provide better

facilities No sim card must be sold unless registered, moreover, sim card prices must be increased

to get rid of teasing/bothering. MNOs must increase their coverage and should start to operate in remote areas so as to

cover all provinces Products and services must be according to international standard Must keep privacy, as no one should have access/view to others call history Provide quality services with reasonable prices, durability and reliability Fast connectivity Good customer services Proper utilization of tools and equipments government and companies Attention must be paid to DSL cables since it’s too weak. License must be issued based on quality of company’s services Strict control must be there to ban immoral sites Government should encourage more investment Improve services and get rid of fake advertisements

Study of Afghan Telecom Industry 2013

34

Conclusion

Telecom sector in one of the fastest growing sector of afghan economy, which added more revenue to the treasury of government as well as provided easy communication and created job opportunities of more than 100,000.

Mobile operators have dominated telecom industry, there are 5 active players most of them foreign owned businesses which has provided facilities to 88 percent of afghan population. Tough competition is going on among MNOs which has resulted in price reductions over past decade as every MNO is trying to get larger share of market by offering fewer prices. MNOs are free to set prices of products and services, ATRA is just interfering in interconnection rates.

It is concluded that market has saturated and there is no place for any other MNOs to enter the market. However, there are certain problems with current operators such as: high calling rates, disconnections, lack of signal and coverage, but still people are satisfied with their network and sometime use more than one sims to reduce the possibilities of these problems. More work is needed in MNOs to bring their products and services according to international level. CDMA is almost failed in Afghanistan as majority of surveyed individuals said that Mobile networks are good as compared to CDMA.

The other important area of telecom is ISPs, currently there are 49 ISPs operating mostly in Kabul and other major provinces of the county. Currently prices of internet is considered to be too expensive by surveyed individuals soon by completion of fiber optic project internet accessibility of internet would be increased with reduced prices.

Survey results show that in Afghanistan youths mostly use mobile and internet services, while landline is mostly used by offices and houses respectively. Previously, internet prices were too expensive but by the passage of time it has reduced and as per necessities internet must be accessible to all people at reasonable prices so that everyone could avail internet facilities.

Market is not saturated, there is place for new businesses with large investment to enter market as currently only 20 percent of afghan population has access to internet. Higher demand for internet requires more investment in this sector, regulators should give license to those who could provide quality services and dissolve license of those who can’t compete. Discrimination is a big problem that some of companies are facing and stated that it’s a big hurdle in development of this sector.

Users faced problems of high cost, weak or no coverage, poor customer service, and low speed are the problems they mostly face.

Further they recommended that telecom companies must introduce new internet technologies, Network expansion to ensure vast connectivity, better quality of services, technology, and bringing new innovations in value added services.

Study of Afghan Telecom Industry 2013

35

Acronyms

AISA Afghanistan investment support agencyARPU Average revenue per userATRA Afghanistan telecommunication regulatory agencyBTS Base Transceiver StationsGPRS General Packet radio serviceICT Information and communication technologyISPs Internet service providersJV Joint ventureLTE Long term evolutionMCIT Ministry of communication and information technologyMNOs Mobile network operatorsNGN Next generation networkOPEX Operating costSIM Subscriber identity moduleVAS Value added servicesVSAT Very small aperture technology

Study of Afghan Telecom Industry 2013

36

Sources Consulted:

Ministry of communication and information website: http://mcit.gov.af Central statistical organization: http://cso.gov.af/en/page/7108

World bank statistics: http://data.worldbank.org/indicator

Network dynamics associations LLC-April 23,2004, report on: Afghan telecom brief, published in New Delhi, India

Primary data obtained from telecom companies, and telecom service users

Appendices

Appendix A:

Table: 1. List of MNOs in Afghanistan:NO Name Date of

establishment 1 AWCC 0ctober

28,1998

2 Roshan 2003

3 MTN July 2005

4 Afghan telecom

April,2006

5 Etisalat August 2007

Source: Ministry of communication and information technology

Table: 2. List of internet service providers

No. NameType of License

1 Insta Telecom National

2 Neda Telecom National

3 Sarferaz Bahader Local

4 K B I National

5 CereTechs National

6 New Dunia National

7 IO Global National

Study of Afghan Telecom Industry

37

List of MNOs in Afghanistan:

establishment Type of Company

Address Logo

JV Darul-Aman,Kabul

Foreign owned

Wazir Akbar Khan,Kabul

Shahre-Naw,Kabul

Public Mohammad jan Khan watt

Foreign owned

Share-Naw,Kabul

Source: Ministry of communication and information technology

List of internet service providers

Type of License

National [email protected]

National [email protected],[email protected]

[email protected],[email protected]

National [email protected]

National [email protected]

National [email protected], [email protected]

National [email protected], akarim@io

Telecom Industry 2013

[email protected],[email protected]

[email protected], akarim@io-

Study of Afghan Telecom Industry 2013

38

global.com

8RANA Technologies

National [email protected]

9 Multinet National [email protected], [email protected]

10 Liwal National [email protected], [email protected]

11 Afghan Wireless National [email protected]

12 Atlas Telecom [email protected], [email protected]

13Ariana Network Service

National [email protected]

14 Pactect National [email protected], [email protected]

15 AFSAT National [email protected]

16 Streamlink National [email protected]

17Afghan ICT Solution

National [email protected]

18 MTN National [email protected]

19 NETZONE National [email protected], [email protected]

20 Asix National [email protected], [email protected]

21Universal Telecom Service

National [email protected]

22 Wizocom National [email protected], [email protected]

23 ALPHAWAVES Local [email protected]

24 Etisalat National [email protected]

25 Melat Networks National [email protected], [email protected]

26 STAN Telecom National [email protected]

27 ARIASAT LTD National [email protected]

28 ACG National [email protected]

29 Quality Net [email protected], [email protected]

30 Wasel Telecom National [email protected], [email protected]

31 Afghan Cyber National [email protected]

32 Global Entourage National [email protected], [email protected]

33 Connect Telecom National [email protected]

34AfghanYar Technology

National [email protected]

35 CastGlobe National [email protected], [email protected]

36 Giganor National [email protected]

37 Kayenat Technology National [email protected], [email protected]

Study of Afghan Telecom Industry 2013

39

38 IDIL National [email protected]

39 Arian Technologies National [email protected]

40Witel Telecommunications

National [email protected]

41Arian Afghan Network

National [email protected], [email protected]

42 Afnet Local [email protected]

43 TiiTACS National [email protected], [email protected]

44 Kandahar Jillani Local [email protected], www.jelani-group.com

45 Giganet Local www.gignt.com

46Unique Atlantic TelecommunicationLtd

National [email protected]

47 San Technology National [email protected], www.stis.af

48Empower IT Services

National [email protected]

49 Safa Telecom National [email protected]

Source: Ministry of communication and information technology

Table: 3. Internet users (per 100 people) 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Afghanistan 0.0 0.1 0.1 1.1 1.9 1.8 1.7 3.2 3.7 4.6Bangladesh 0.1 0.2 0.2 0.2 1.0 1.8 2.5 3.1 3.7 5.0China 4.6 6.2 7.3 8.5 10.6 16.0 22.7 29.0 34.4 38.4India 1.5 1.7 2.0 2.4 2.8 4.0 4.4 5.1 7.5 10.1Iran 4.6 6.9 7.5 8.1 8.8 9.5 10.2 11.1 16.0 21.0Kazakhstan 1.7 2.0 2.7 3.0 3.3 4.0 11.0 17.9 31.0 44.0Pakistan 2.6 5.0 6.2 6.3 6.5 6.8 7.0 7.5 8.0 9.0Tajikistan 0.1 0.1 0.1 0.3 3.8 7.2 8.8 10.1 11.6 13.0Turkmenistan 0.3 0.4 0.8 1.0 1.3 1.4 1.8 2.0 3.0 5.0

Source: World Bank

Table: 4. Fixed broadband Internet subscribers 2003 2004 2005 2006 200

72008 2009 2010 2011

Afghanistan

200 220 500 500 500 1000 1500

Bangladesh

43,710

50000 55000 60000 65000

China 11,2 24,939,630

37,350,000

50,853,000

66,414,000

82,879,000

103,978,000

126,337,000 156,487,000

Study of Afghan Telecom Industry 2013

40

19,010

India 140,362235,000

1,348,000 2,300,000 3,130,000

5,280,000 7,745,710 10,990,000 12,830,000

Iran 18,700 100,000 200,000

300,000 400,000 962,250 1,772,867

Kazakhstan

998 1,997 2,996 30,500 270,370

660,818 577,200 1,426,800 1,215,700

Pakistan 14,600 26,611 45,153

148,470 302,829 531,787 737,778

Tajikistan 10 3645 3,658 4,400 4,700 5,020

Turkmenistan

75 465 723 1,100

Source: World Bank

Table: 5. Secure Internet servers 2003 2004 2005 2006 2007 2008 2009 2010 2011

Afghanistan

1 1 1 2 6 6 9 20 22

Bangladesh 1 3 3 3 6 15 29 47 96China 182 293 426 588 900 1238 1579 2569 3260India 825 1121 1462 1796 2601 3545Iran 20 24 55 76Kazakhstan 31 52 85 105Pakistan 89 105 169 197Tajikistan 2 3 4Turkmenistan

1 1 1

Source: World Bank

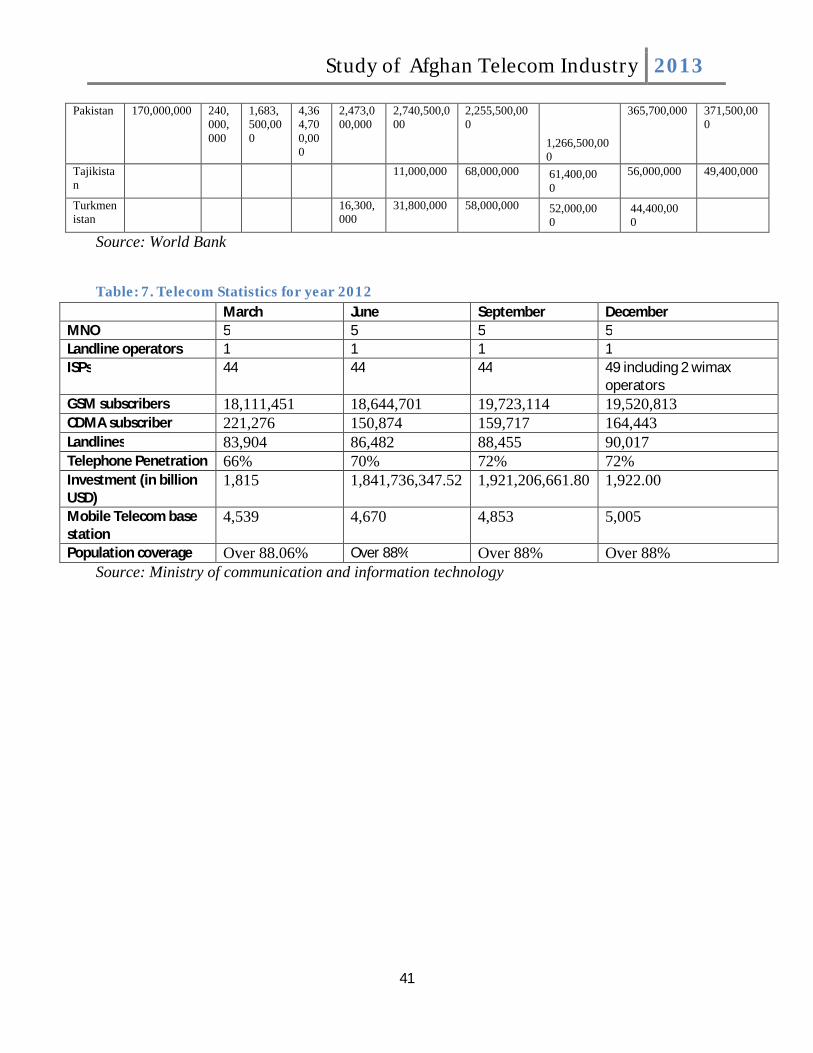

Table: 6. Investment in telecoms with private participation (current US$)2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Afghanistan

70,000,000

69,000,000

156,000,000

171,100,000

555,400,000

240,000,000

185,000,000 60,000,000

70,000,000

5,100,000

Bangladesh

60,900,000 205,000,000

420,000,000

473,000,000

1,113,000,000

1,348,800,000

896,000,000

372,000,000

520,500,000 494,000,000

China 1,430,000,000

1,140,000,000

India 5,008,400,000

2,079,700,000

3,701,220,000

5,665,750,000

6,823,200,000

8,168,250,000

9,933,800,000

7,829,800,000

20,335,300,000

4,147,000,000

Iran 5,000,000 340,000,000

350,000,000

221,000,000

802,000,000 483,000,000 486,000,000 514,400,000

Kazakhstan

115,000,000 139,000,000

275,700,000

484,500,000

635,200,000

876,100,000

1,062,600,000

596,300,000

596,300,000

952,700,000

Study of Afghan Telecom Industry 2013

41

Pakistan 170,000,000 240,000,000

1,683,500,000

4,364,700,000

2,473,000,000

2,740,500,000

2,255,500,000

1,266,500,000

365,700,000 371,500,000

Tajikistan

11,000,000 68,000,000 61,400,000

56,000,000 49,400,000

Turkmenistan

16,300,000

31,800,000 58,000,000 52,000,000

44,400,000

Source: World Bank

Table: 7. Telecom Statistics for year 2012 March June September December

MNO 5 5 5 5Landline operators 1 1 1 1ISPs 44 44 44 49 including 2 wimax

operatorsGSM subscribers 18,111,451 18,644,701 19,723,114 19,520,813CDMA subscriber 221,276 150,874 159,717 164,443Landlines 83,904 86,482 88,455 90,017Telephone Penetration 66% 70% 72% 72%Investment (in billion USD)

1,815 1,841,736,347.52 1,921,206,661.80 1,922.00

Mobile Telecom base station

4,539 4,670 4,853 5,005

Population coverage Over 88.06% Over 88% Over 88% Over 88%Source: Ministry of communication and information technology

Study of Afghan Telecom Industry 2013

42

Appendix B:

Graph: 1. Inbound Internet Traffic (mbps)

Source: Afghanistan Telecommunication and regulatory agency

Graph: 2. Internet users (per 100 people)

Source: Word Bank

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2002 2004 2006 2008 2010 2012 2013

Inbound Internet Traffic (mbps)

0

5

10

15

20

25

30

35

40

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Turkmenistan

Tajikistan

Pakistan

Bangladesh

Afghanistan

Study of Afghan Telecom Industry 2013

43

Graph: 3. Fixed broadband Internet subscribers

Source: Word Bank

0

100000

200000

300000

400000

500000

600000

700000

800000

2003 2004 2005 2006 2007 2008 2009 2010 2011

Afghanistan

Bangladesh

Pakistan

Tajikistan

Turkmenistan

Study of Afghan Telecom Industry 2013

44

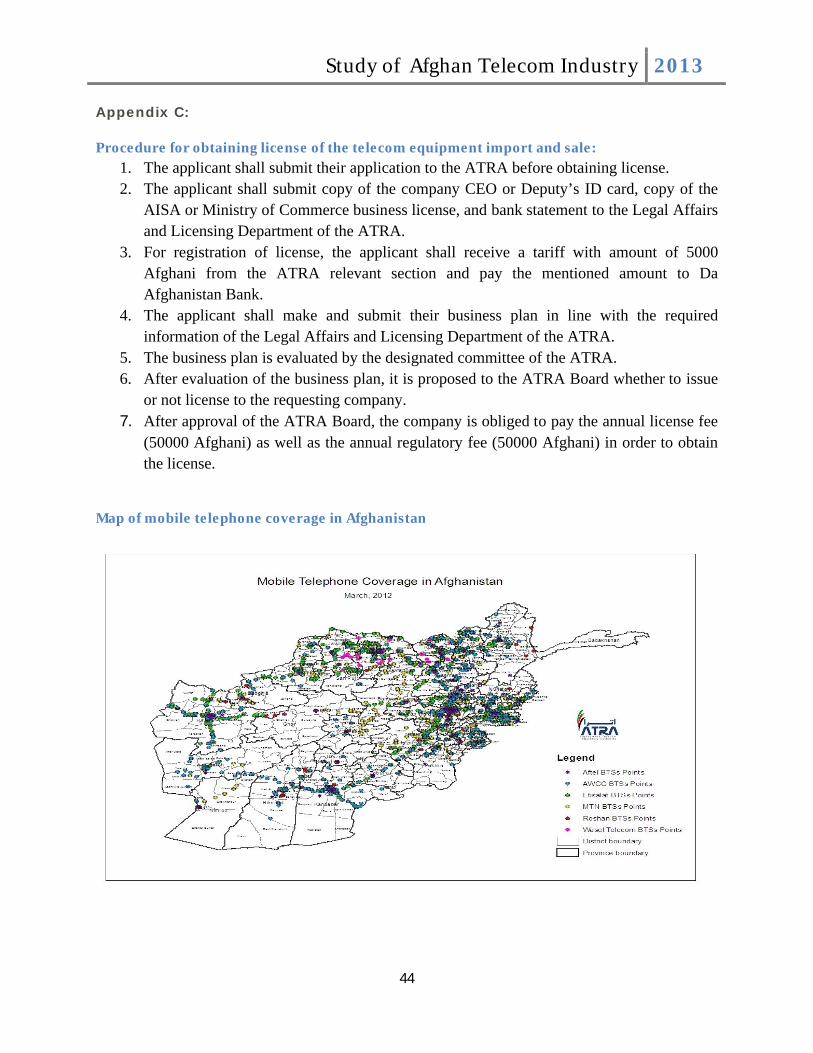

Appendix C:

Procedure for obtaining license of the telecom equipment import and sale:1. The applicant shall submit their application to the ATRA before obtaining license.2. The applicant shall submit copy of the company CEO or Deputy’s ID card, copy of the

AISA or Ministry of Commerce business license, and bank statement to the Legal Affairs and Licensing Department of the ATRA.

3. For registration of license, the applicant shall receive a tariff with amount of 5000 Afghani from the ATRA relevant section and pay the mentioned amount to Da Afghanistan Bank.

4. The applicant shall make and submit their business plan in line with the required information of the Legal Affairs and Licensing Department of the ATRA.

5. The business plan is evaluated by the designated committee of the ATRA.6. After evaluation of the business plan, it is proposed to the ATRA Board whether to issue

or not license to the requesting company.7. After approval of the ATRA Board, the company is obliged to pay the annual license fee

(50000 Afghani) as well as the annual regulatory fee (50000 Afghani) in order to obtain the license.

Map of mobile telephone coverage in Afghanistan