study of rice processing, marketing and … of rice processing, marketing and distribution in ......

TRANSCRIPT

STUDY OF Rice Processing, Marketing and Distribution in Sierra Leone

By

Dunstan Spencer, Sanusi Deen, Agidi Gbagbo and Chrispin Wilson With

Pious Sesay

June 7, 2014

DISCLAIMER This publication was produced as consultant to the Rural Private Sector Development

Project (RPSDP). However, the results presented and views expressed are the sole responsibility of the authors and do not in any way engage the RPSDP, the Government

of Sierra Leone or the World Bank

Sanusi S. Deen Dunstan S. C. Spencer Chrispin E. Wilson Senior Partner Senior Partner Senior Partner Tel: +23276608663 Tel: +23276610441 Tel: +23276787890

Email: [email protected] Email: [email protected] Email: [email protected]

ENTERPRISE DEVELOPMENT SERVICES LTD 15 Mudge Farm, Off Sir Samuel Lewis Road

Freetown ~ Sierra Leone www.eds-sl.com

ii

EXECUTIVE SUMMARY

The study objectives are to assess the current processing, marketing and distribution mechanisms for rice and propose technically and economically feasible recommendations.

The dynamics involved in the process of rice production, marketing and trade, and the impact of policy intervention are examined in the study using a conceptual framework developed by IFPRI A which links the operations of markets, the macro environment, and growth in the agricultural sector.

In addition to extensive literature review, field data was collected for a representative sample of each significant market type identified in Value Chain Mapping (periodic markets, retail markets, wholesale markets, rice processing establishments), using structured questionnaires.

Government and Donor Policies

Since 2005, national development strategies and actions have been guided by Poverty Reduction Strategy (PRS) documents. Government’s current agricultural strategy and objectives are summarized in the current PRSP as follows:

To increase the production of staple food crops for food security:

To increase the production and export of cash-crops:

Improve access to Finance for Farmers:

Strengthen the capacity of MAFFS

An analysis of donors and development partners’ interventions under PRSPs I and II reveal that their assistance policies have been supportive of the agricultural sector in the areas of infrastructure development and access to finance and markets.

Value Chain Mapping

The marketing of a commodity, in this case rice starts with production and sale by farmers. In Sierra Leone rice is produced mainly by small producers. Ninety-five percent of the marketed surplus of rice is estimated to come from small producers.

Export of domestic rice

There are good prospects for increased export of rice which should be exploited: Data presented in the report shows that Sierra Leone has a comparative advantage not only in producing rice to supply its domestic markets but also for regional trade. As discussed above the country already has substantial exports to neighbouring countries. There are good prospects for further expansion of exports to regional markets. Regional demand for rice is high and growing rapidly, and Sierra Leone’s location is ideal for supplying regional rice markets. The country’s policy should therefore be to exploit its comparative advantage by:

a) Formalizing the export trade in local rice through trade negotiations with the importing countries

b) Investing in domestic value addition to maximize export revenues from the commodity c) Establishing an export processing zone in an appropriate location, with appropriate

infrastructure, services and amenities to function at international standards for such facilities.

Formalizing informal rice export activities would provide more reliable revenue streams for the state and enhanced security for traders through improved knowledge and enforcement of rights and responsibilities of all stakeholders at the border. In order to bring informal trading activities into formality and expand the tax base, a number of steps need to be taken to simplify business registration, harmonize and simplify import and export procedures, eliminate harassment, extortion

iii

and other corrupt practices at the borders, and provide targeted support to small firms that register formally.

Imported rice trade

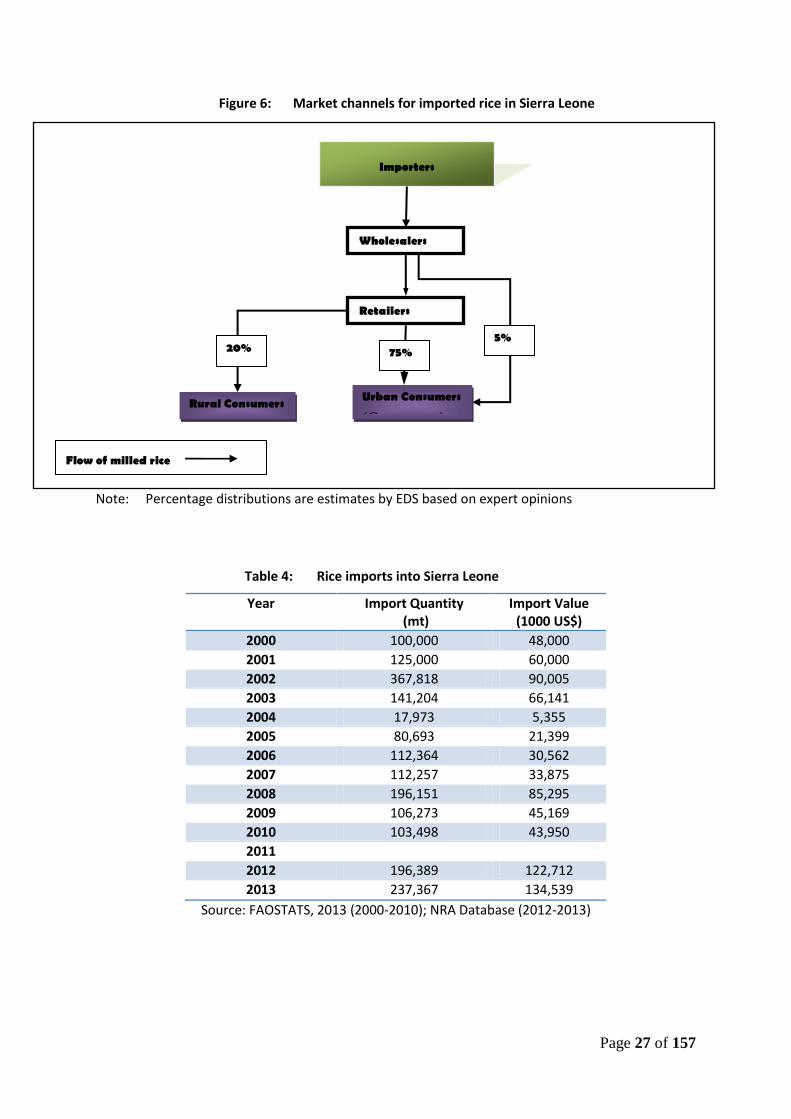

The marketing system for imported rice is much simpler than that for domestic rice. Until the intervention of the MTI in October 2013, all importation of rice was undertaken by the private sector. The key government agencies and parastatals involved in the rice trade during the 1970s and 1980s included the Rice Department, the Rice Corporation and the Sierra Leone Produce Marketing Board (SLPMB), but by the late 1980s the private sector had assumed the dominant role in the marketing of both local and imported rice.

The quantity and value of rice imports have increased substantially in the last five years indicating that claimed increases in domestic rice production have had minimal effect on imports.

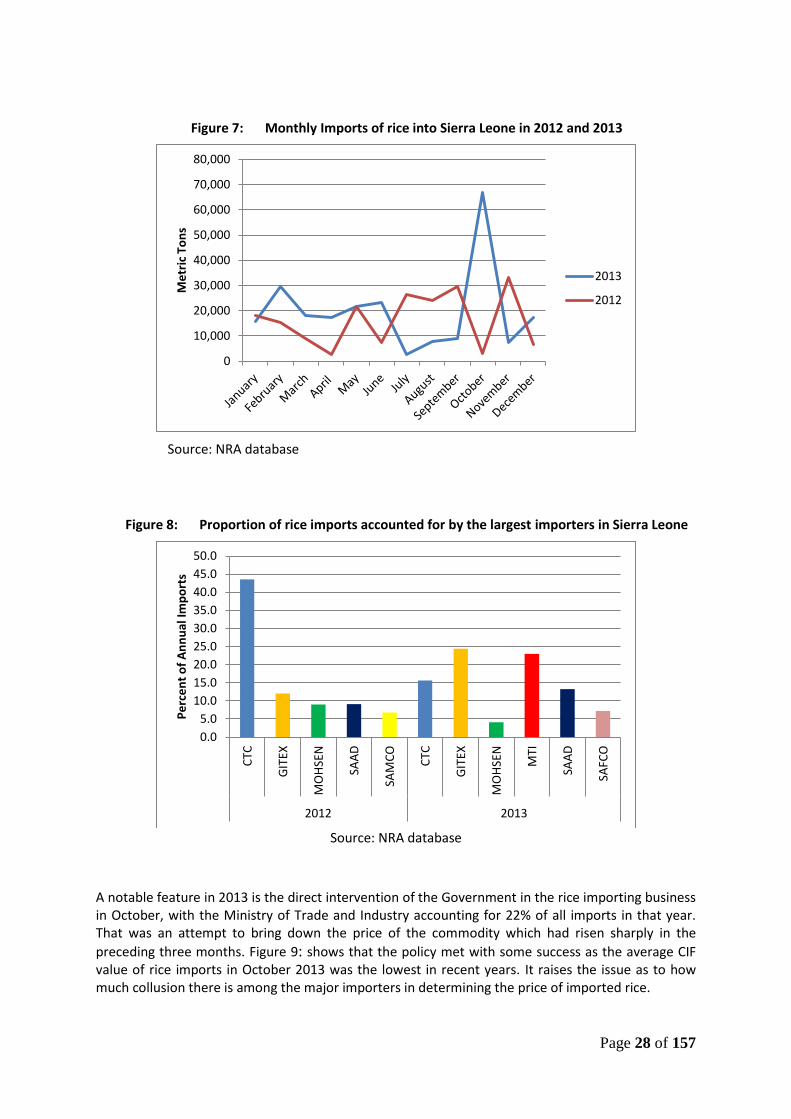

The six (6) largest importers of rice in Sierra Leone accounted for over 80% of all rice imports in the last two years. The situation has therefore not changed much in the last 30 years in terms of the number of importers dominating the trade, although their relative importance change from time to time.

A notable feature in 2013 is the direct intervention of the Government in the rice importing business in October, with the Ministry of Trade and Industry accounting for 22% of all imports in that year. That was an attempt to bring down the price of the commodity which had risen sharply in the preceding three months. It appears that the policy met with some success as the average CIF value of rice imports in October 2013 was the lowest in recent years.

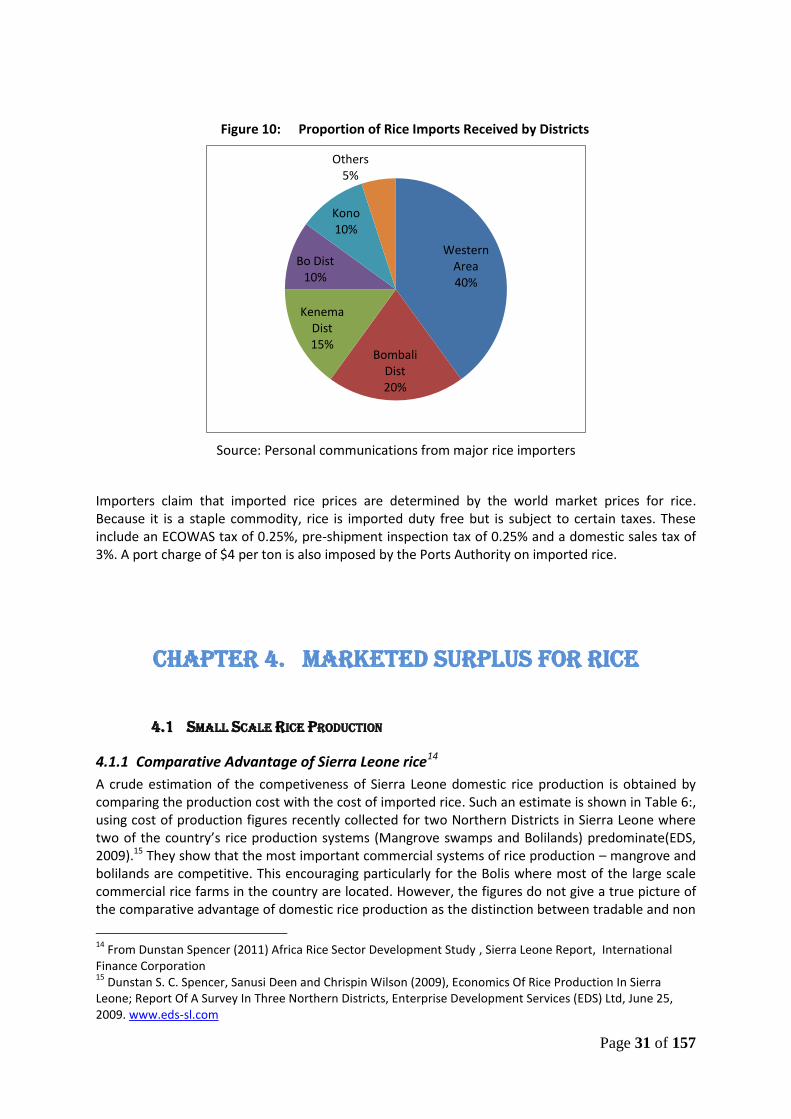

The importers do not keep records of the destination of their sales and could only provide estimates based on their knowledge where wholesalers normally carry on their business. From their estimates, approximately 40% of importers sales are made to Western Area rice traders. Provincial traders account for approximately 60% the trade in imported rice, led by the Bombali District traders who take approximately 20% of imported rice. Kenema Districts accounts for approximately 15% followed by Bo and Kono Districts which consume approximately 10% each. The other districts account for relatively little (5%) consumption of imported rice.

Need to improve production and marketing statistics

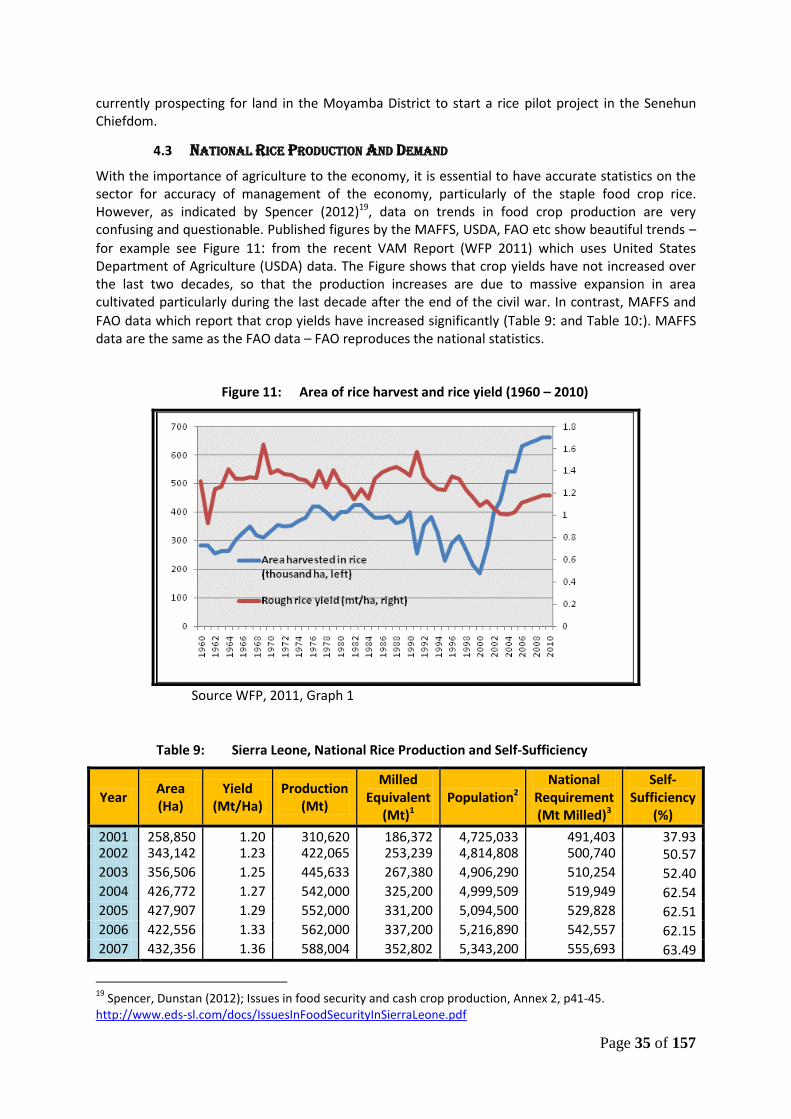

With the importance of agriculture to the economy, it is essential to have accurate statistics on the sector for accuracy of management of the economy, particularly of the staple food crop rice. However, data on trends in food crop production are very confusing and questionable.

Also, regional trade in agricultural products is generally under-represented in official statistics, especially as it takes places through informal channels and with partners that may not keep proper records of this trade. An integrated mechanism is therefore needed to monitor and record informal trade flows to get a better handle on the full scope and scale of trade volumes. The informal cross-border data collection system that Uganda established in 2007 could provide a framework for a similar mechanism to monitor and record informal trade statistics for Sierra Leone. Establishing and implementing such a mechanism would require close collaboration between key entities such as Statistics Sierra Leone, National Revenue Authority, Ministry of Trade and Industry, and the Bank Of Sierra Leone, among others.

Marketable Surplus

Marketed surplus has generally been defined as that proportion of production that actually enters the market. Because of the uncertainly regarding the true level of production of rice in the country, the analysis in this study is based on two levels of production in 2009 which is used as the baseline year – a high variant based on FAO/MAFFS production data, and a low variant based on AHTS data.

iv

With the combination of high and low variants for rice production and marketed surplus, four different estimated quantities of domestic rice marketed are obtained representing:

1. FAO/MAFFS production data (allocated by District using the AHTS distributions) + EDS Market surplus ratios (187,118.3mt paddy in 2009, projected to 473,051.8 by 2025)

2. FAO/MAFFS production data (allocated by District using the AHTS distributions) + ATS Market surplus ratios (106,345.4mt in 2009, projected to 268,850.6mt by 2025)

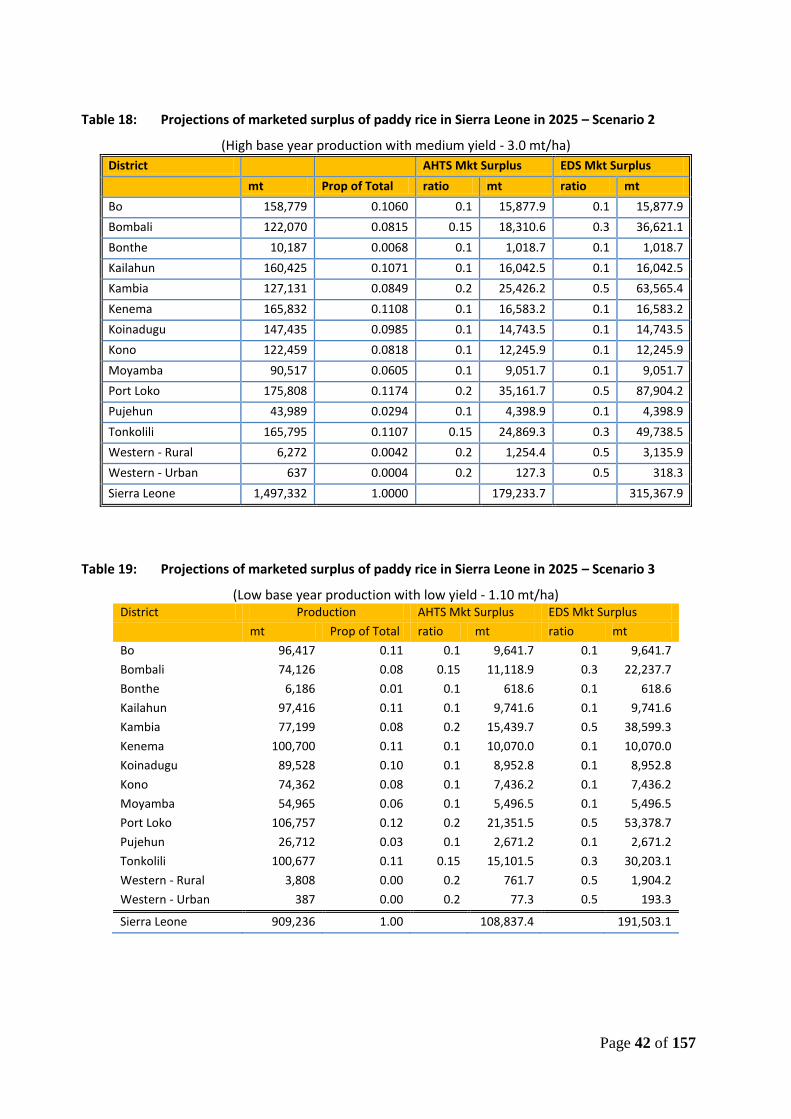

3. ATHS production data by Districts + EDS Market surplus ratios (76,280.2 in 2009 projected to 191,503.1mt by 2025)

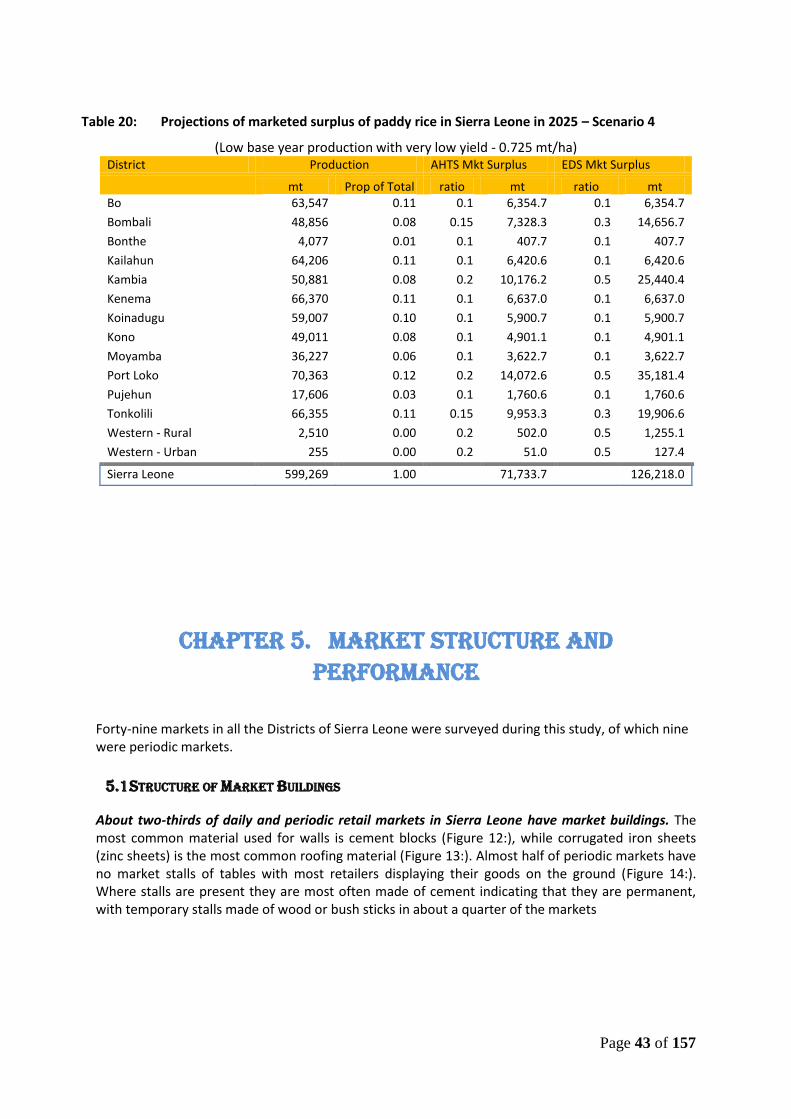

4. ATHS production data by Districts + AHTS Market surplus ratios (43,352.5mt in 2009 projected to 108,837.4mt by 2025)

Installed Milling Capacity

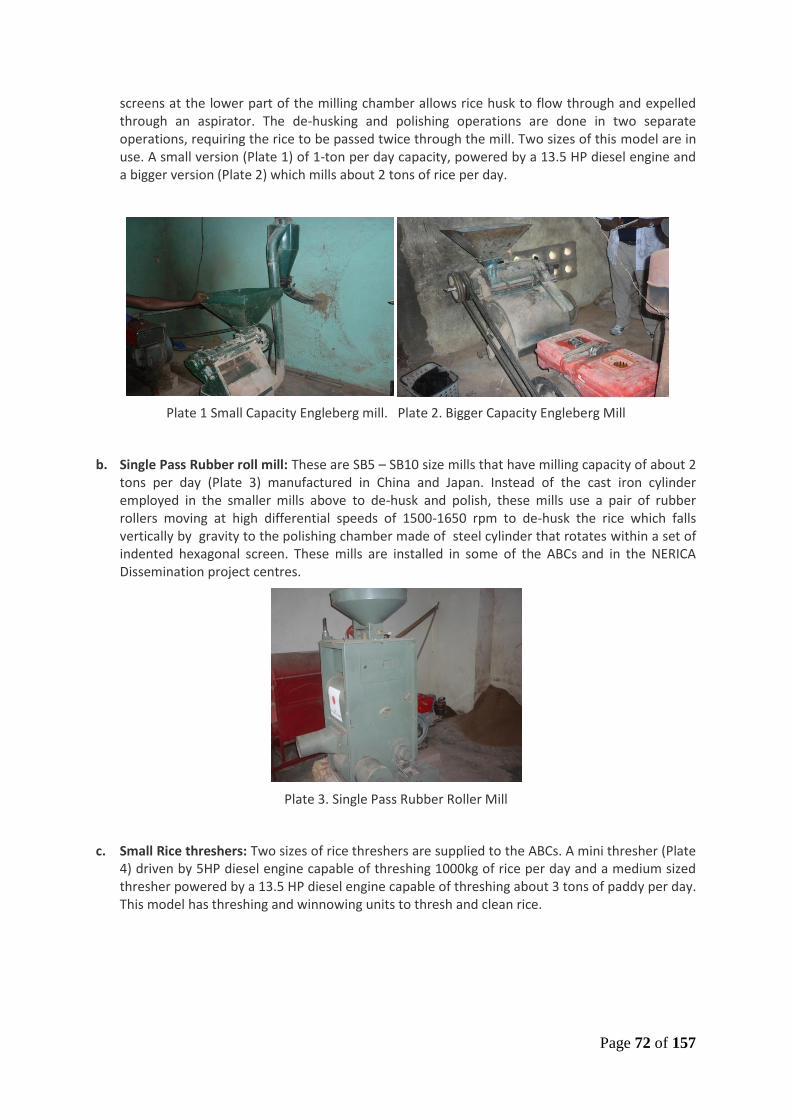

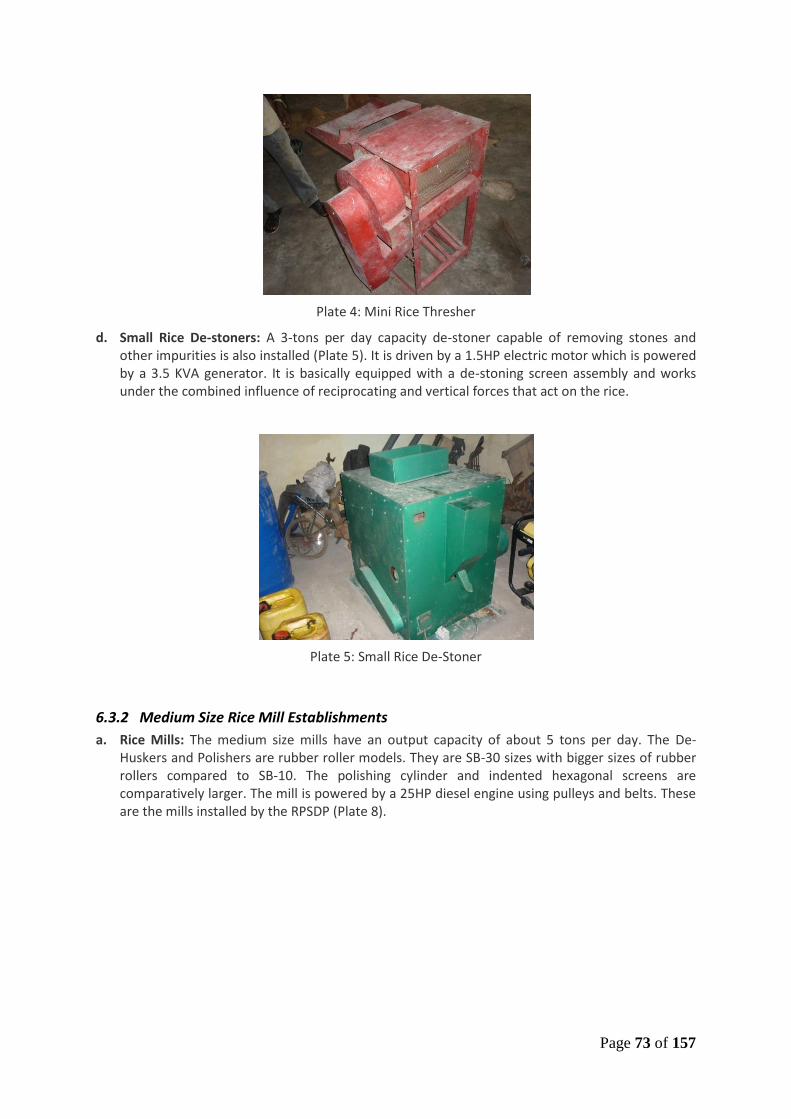

The national inventory of rice mills in Sierra Leone revealed the existence of approximately 401 rice mills installed in all the districts in the country, up from the 53 estimated to be operational after the civil war. Thirty-eight (9.5%) of the mills are not operational, primarily because of breakdowns, or in the case of the large mills, lack of proper business plans for their operation. As to be expected, the there is a concentration of rice mills in the major rice producing Districts, led by Port Loko District with 67 operational mills, Kambia with 59, Tonkolili and Bombali with 29 and 30 operational mills respectively. Kailahun District is not in one of the country’s rice belts but has a significantly large number of mills (34) due to its large farming population.

Twenty-five percent (25%) of the mills are privately owned and operated, all being small capacity mills. The five large integrated rice milling plants, installed in Bo, Kenema, Makeni, Torma Bum and Mambolo are each of 1 ton per hour capacity. Four (4) are of Indian manufacture, installed by MAFFS, each with a Bricketing machine, while the mill in Bo is of Chinese manufacture and was installed by the Chinese Government as a gift to Sierra Leone. None of these mills is in operation.

This study shows that Sierra Leone has sufficient installed milling capacity. Even with the high estimates of production and marketable surplus (the EDS estimates), the mills installed and assessed as “operational” have enough capacity to mill all the marketed rice in Sierra Leone operating only one shift of 8 hours per day, 24 days a month and 9 months a year. The recent investments by the Government and donor partners in increasing the rice milling capacity of the country through the ABCs and RPSDP as well as private sector investments have provided the country with sufficient milling capacity to serve its needs over the next five to ten years. But the distribution across Districts is not optimal, with substantial excess capacity in Kailahun, Koinadugu, Kenema, Kono, Moyamba and Pujehun Districts. The largest deficits are in Tonkolili and Port Loko Districts. The case for investment in additional milling capacity in Sierra Leone is therefore quite weak. However, there is a very strong case for greatly increased, and more efficient use of the installed capacity.

Efficiency of rice milling operations

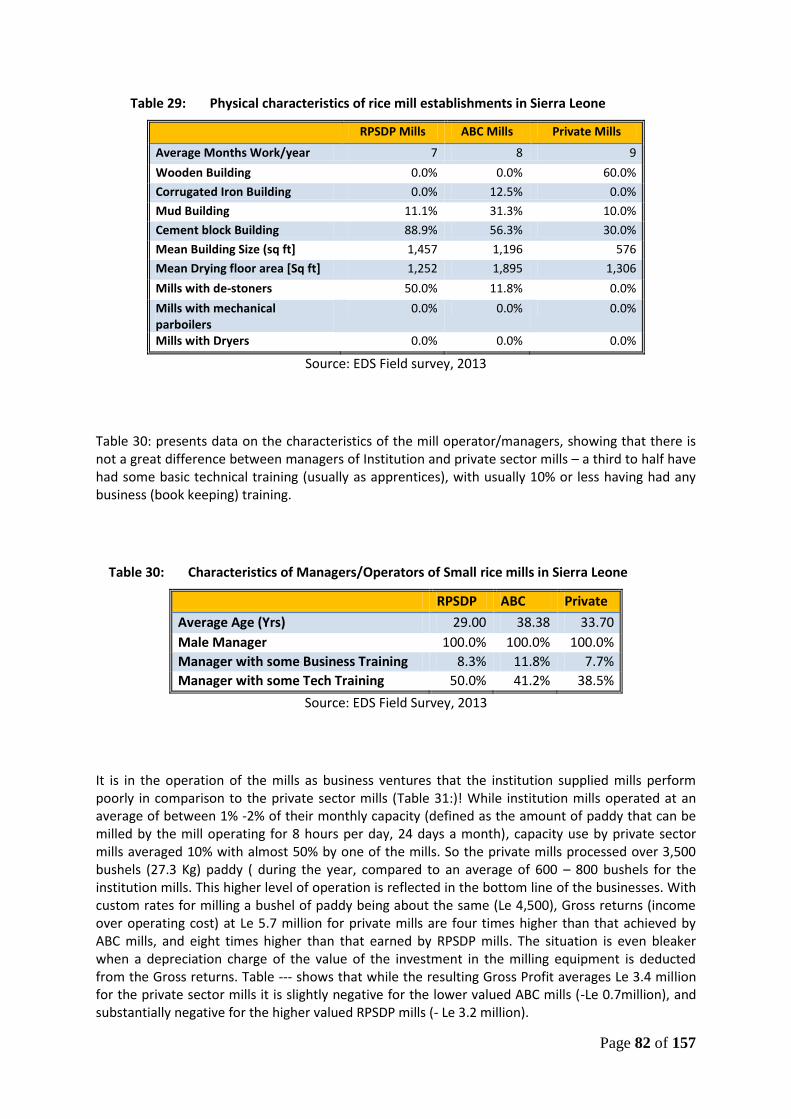

It is evident from the data gathered in this study that private sector mills have less capital investment that the institution mills. This is a result of Government policy of “modernizing” the sector through the Government funded projects.

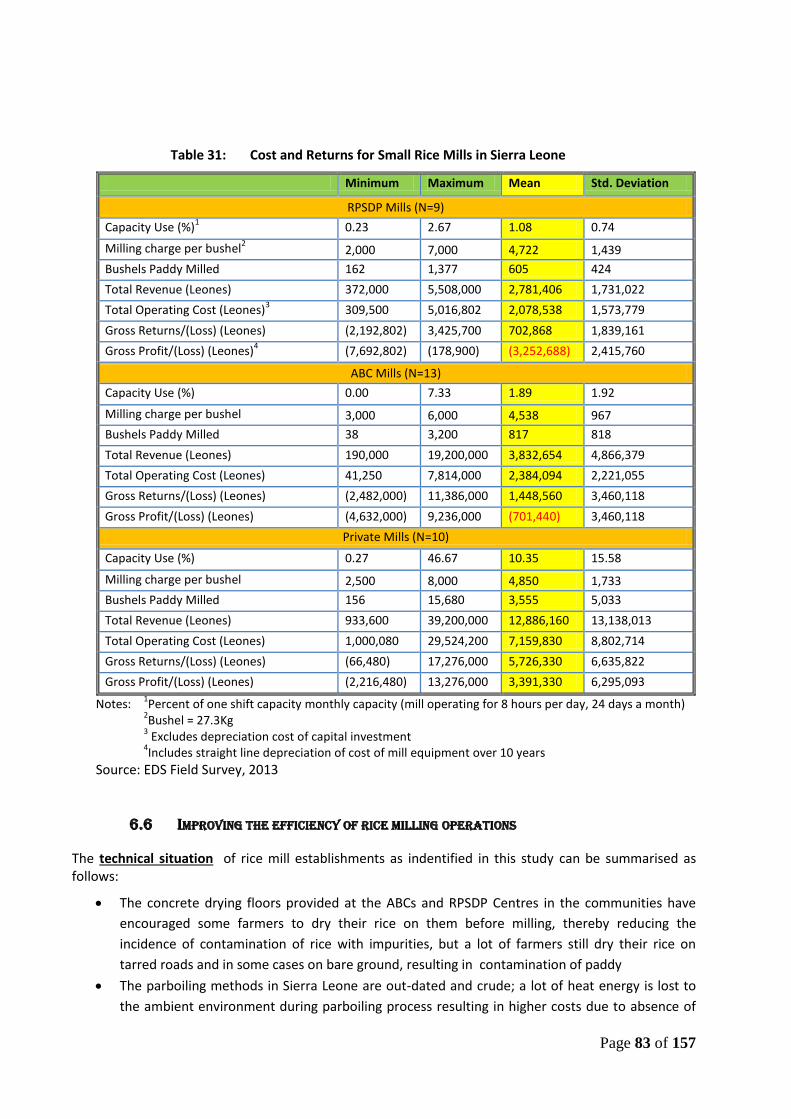

On the average the mills operated for 7 – 9 months during the year with the privately owned mills operating for longer than the ABC or RPSDP established mills. While institution mills operated at an average of between 1% -2% of their monthly capacity (defined as the amount of paddy that can be milled by the mill operating for 8 hours per day, 24 days a month), capacity use by private sector mills averaged 10% with almost 50% by one of the mills. So the private mills processed over 3,500 bushels (27.3 Kg) paddy ( during the year, compared to an average of 600 – 800 bushels for the institution mills. This higher level of operation is reflected in the bottom line of the businesses.

v

With custom rates for milling a bushel of paddy being about the same (Le 4,500), Gross returns (income over operating cost) at Le 5.7 million for private mills are four times higher than that achieved by ABC mills, and eight times higher than that earned by RPSDP mills. The situation is even bleaker when a depreciation charge of the value of the investment in the milling equipment is deducted from the Gross returns. While the resulting Gross Profit averages Le 3.4 million for the private sector mills it is slightly negative for the lower valued ABC mills (-Le 0.7million), and substantially negative for the higher valued RPSDP mills (- Le 3.2 million).

Why are the institution supplied mills performing so poorly, compared to the private sector mills? The answer lies in the lack of entrepreneurial drive of the managers and beneficiaries of the institution mills, and the poor location of most of the mills relative to the sources of supply of paddy for custom milling. The vast majority of private sector mills are located in the Scarcies area (Kambia & Port Loko Districts) the major surplus rice producing area of the country, while the institution mills are distributed all over the country, obviously for social and political reasons, but with sometime difficult access to sufficient customers for higher capacity use.

Business plans (BPs) for profitable private sector operation of the model mill establishments demonstrate, using state-of-the-art technologies, how rice can be marketed and sold profitably, by ensuring that the most effective and efficient processes are employed. The models are for large, medium and small scale businesses that purchase enough paddy rice in bulk during the buying season that normally lasts from November to March for milling during the rest of the year. Sufficient storage capacity is required to enable the Companies to store enough paddy to keep the mills busy for 280 working days. The rice will be marketed through different channels. To achieve a reasonable level of profitability (around 12% for small mills to 25% annual return on equity capital for small and large mills) the businesses must:

Make significant capital investment in structures and equipment ( $230,000 for small mills to $2million for large mills)1

Have sufficient operating capital to purchase and store paddy over a five month period for milling and sale of the product throughout the year (equity and loans amounting $130,000 for small mills up to $2 million for the large mill)

Recommendation on rice processing

The identified problems can be solved mainly in the following ways:

Modernization of existing Small, Medium and Large Scale Processing Centres in major rice production zones of the country, to equip them with the full complement of milling equipment. This should include provision of improved mechanical parboiling systems.

Provision of appropriate storage facilities- warehouses and Silos. The Sierra Leone Produce Marketing Company should be capacitated to erect and manage public warehouses and silos in the major rice producing districts, in association with the private mills.

Training should be provided in improved modern rice processing technology especially on threshing, parboiling, drying and milling, including in the organization and management of paddy supply systems for:

o Extension officers in all the Districts who will go to the communities to train the farmers

o Small and Medium Scale Processing groups who will directly apply them in their mills

1 Where existing business (all of which now operate on custom milling establishment) are to be transformed to

the model businesses (which will mill mainly on own account) the required capital investment will be significantly reduced due to the taking over of existing plant and equipment.

vi

Full privatisation of all institution mills (ABC, RPSPP, etc.). This analysis has clearly shown that institution operated mills are inefficient compared to the privately owned and operated mills. However, there are social issues associated with this recommendation which will have to be addressed in the privatisation process since the mills were provided as public goods by the financing institutions.

Market Infrastructure

About two-thirds of daily and periodic retail markets in Sierra Leone have market buildings. However, almost half of periodic markets have no market stalls of tables with most retailers displaying their goods on the ground.

Water and sanitation facilities in markets are inadequate: About a third of daily markets and over half of periodic markets have no toilet facilities Over half of both daily or periodic markets have no source of drinking water. Only about 10% have taps. The report recommends that there is a to invest to improve facilities in markets

But market buildings are often not used by retailers. Although there are permanent buildings with cement walls and corrugated iron sheets in about 80% of markets in Sierra Leone, about 70% of the rice traders in the markets, and 60% of traders in general, sell outside the structures. Traders give a variety of reasons for not selling in the market structures including the inappropriateness of the structures (too hot etc), poor accessibility to customers, etc. But the most often cited reason is that they will be disadvantaged if they locate in the buildings as customers would be high jerked by other traders who display their wares outside the market on the foot paths into the market. This calls into question continued investment in market infrastructure

A concerted campaign called for to:

Locate and design structures according to requirements of traders (need strong consultations)

Create conditions that remove incentives for traders to sell outside the structure (e.g. grouping traders by commodities, and enforcing no street trading laws)

Market entry

On the average rice traders in Sierra Leone have had some post-primary education. But the vast majority of rice traders do not have any formal business training, with about half having learnt the trade under the apprenticeship usually of a parent or close family member. Market entry appears to be liberal, this study found no evidence of significant entry barriers.

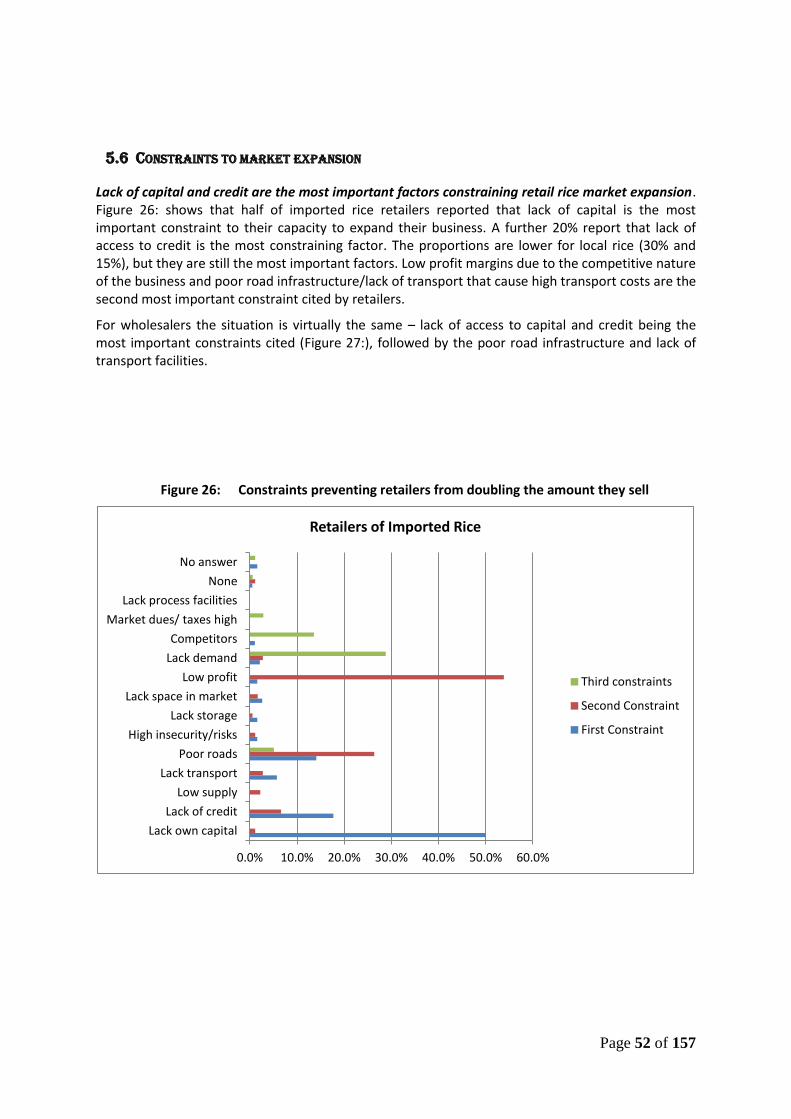

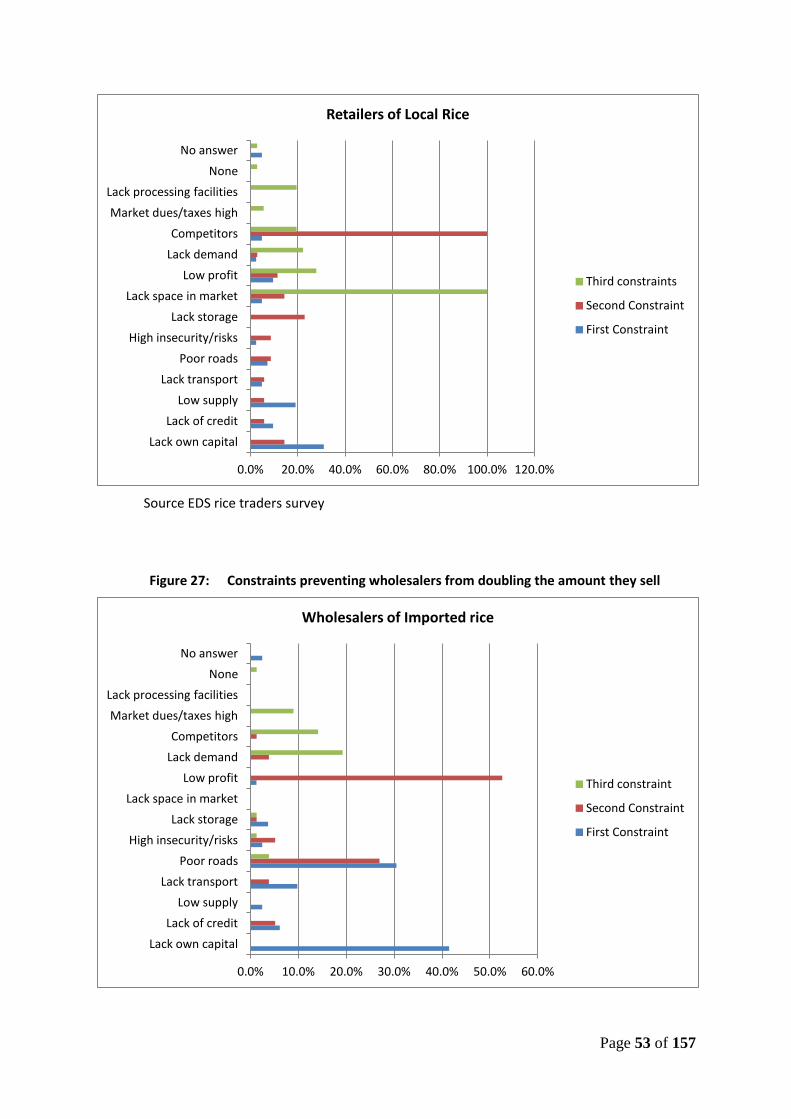

Credit constraints

Lack of capital and credit are the most important factors constraining retail rice market expansion. Half of imported rice retailers reported that lack of capital is the most important constraint to their capacity to expand their business. A further 20% report that lack of access to credit is the most constraining factor. The proportions are lower for local rice (30% and 15%), but they are still the most important factors. Low profit margins due to the competitive nature of the business and poor road infrastructure/lack of transport that cause high transport costs are the second most important constraint cited by retailers. For wholesalers the situation is virtually the same – lack of access to capital and credit being the most important constraints cited. Easier access to credit will oil wheel of rice trading

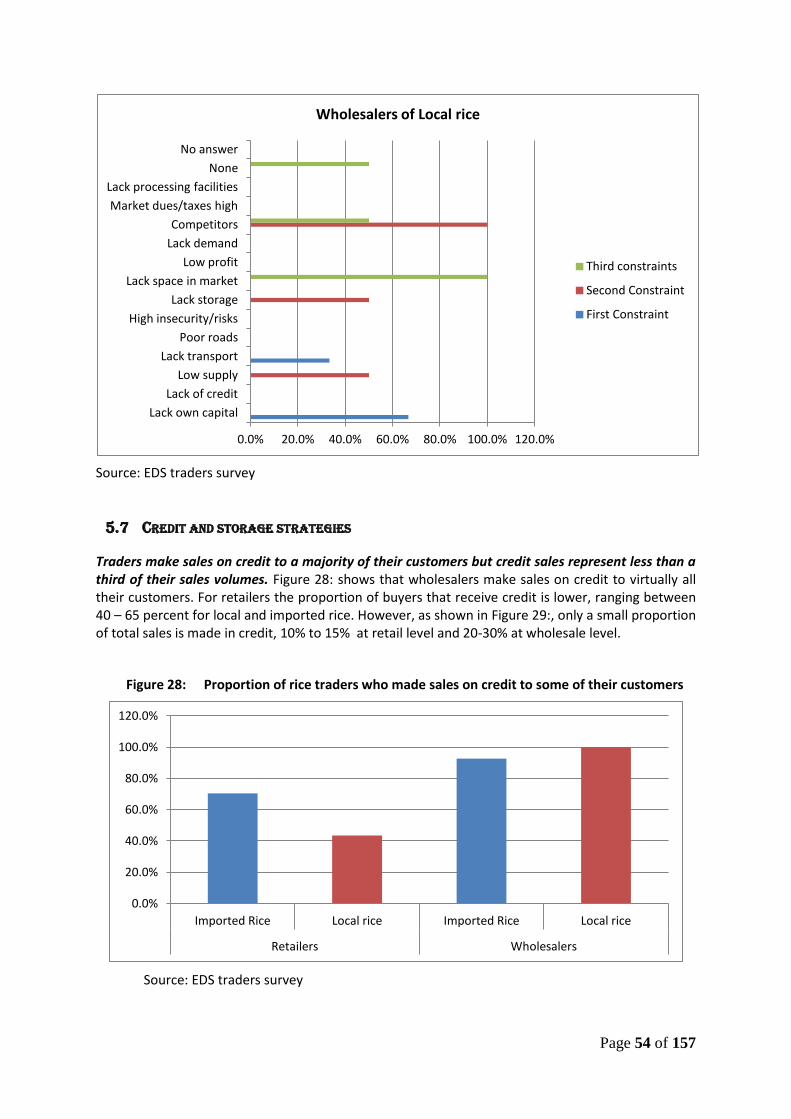

Traders make sales on credit to a majority of their customers but credit sales represent less than a

third of their sales volumes. Figure 28:Wholesalers make sales on credit to virtually all their customers. For retailers the proportion of buyers that receive credit is lower, ranging between 40 – 65 percent for local and imported rice. However, as shown in Figure 29:, only a small proportion of total sales is made in credit, 10% to 15% at retail level and 20-30% at wholesale level.

vii

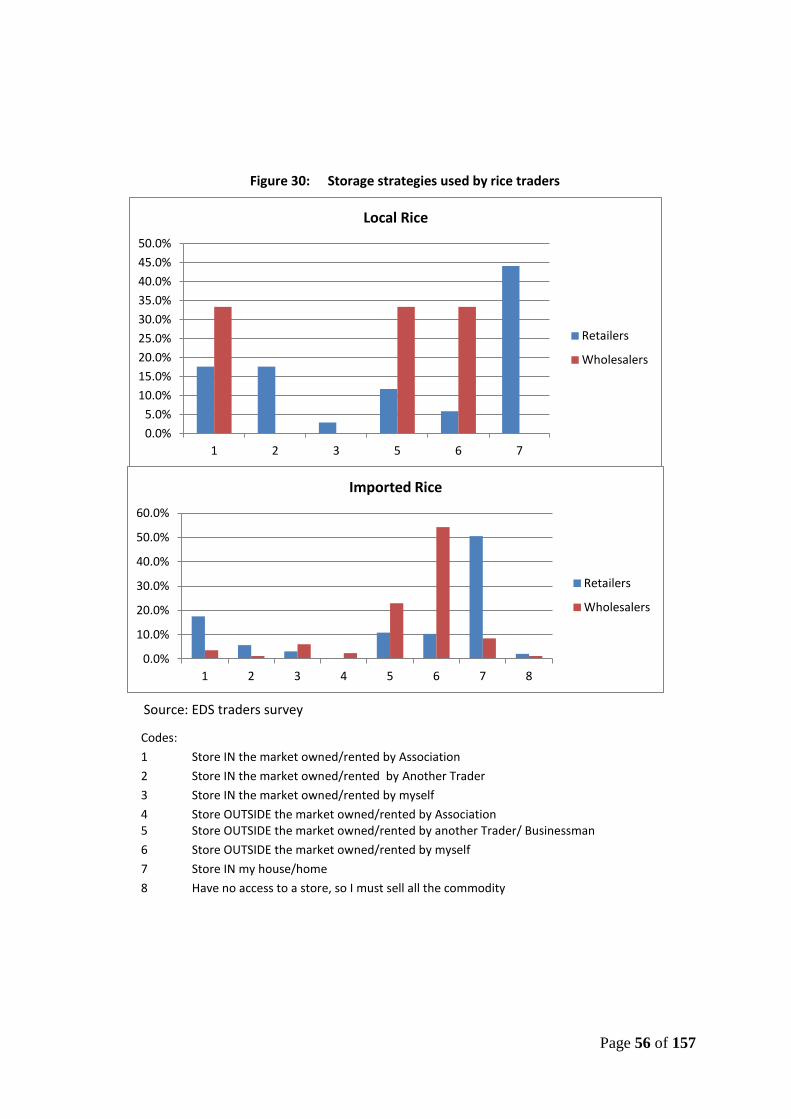

Storage Use

Most retailers store produce overnight in their homes. Virtually all rice traders have access to storage facilities and store produce at least overnight. Very few traders (less than 2%) report that they do not have access to storage facilities and must sell all their stock the same day. But the majority of retailers store their commodity overnight in their homes. Next in importance for retailers (about 15% of traders) is storage in a communal facility in the market owned or rented by their Traders Association.

Although home storage provides security and reduces risks of losses to retailers, it is an inefficient commodity storage strategy. Markets should have sufficient and secure storage facilities which can be rented by Associations for use by their members.

Most wholesalers have access to dedicated store. Most wholesalers store their commodity in individual stores that they own or rent themselves and are located outside, but usually very close to markets,

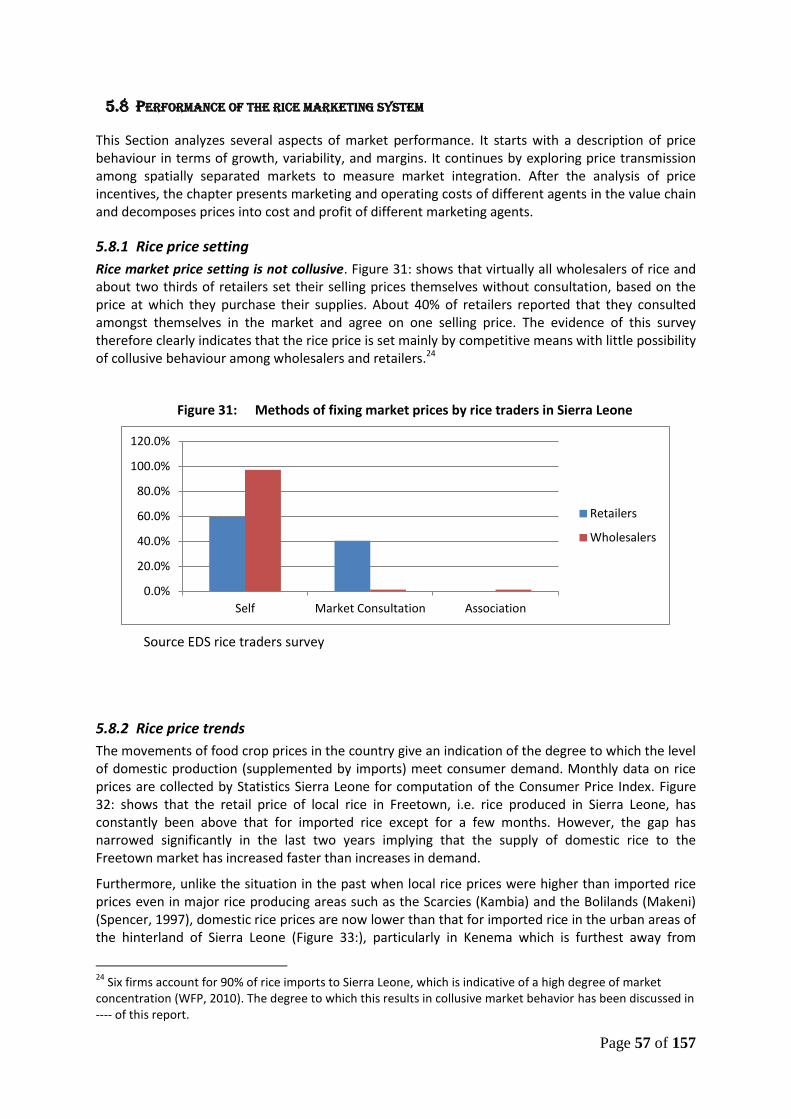

Rice price setting

Wholesale and retail rice market price setting is not collusive, but there are questions relating to price setting by importers. Virtually all wholesalers of rice and about two thirds of retailers set their selling prices themselves without consultation, based on the price at which they purchase their supplies. About 40% of retailers reported that they consulted amongst themselves in the market and agree on one selling price. The evidence of this survey therefore clearly indicates that the rice price is set mainly by competitive means with little possibility of collusive behaviour among wholesalers and retailers.

However there is some recent evidence that there may be collusive behaviour among rice importers. Six firms account for over 80% of rice imports to Sierra Leone, which as stated by WFP (2010) is indicative of a high degree of market concentration. This situation is not new in Sierra Leone as for example Spencer et. al. (2007) reported that four firms handled all rice imports in 1996 (Spencer et all, 2007, but there was no evidence of collusive behaviour.

A notable feature in 2013 is the direct intervention of the Government in the rice importing business in October, with the Ministry of Trade and Industry accounting for 22% of all imports in that year. That was an attempt to bring down the price of the commodity which had risen sharply in the preceding three months. That intervention met with success as the average CIF value of rice imports in October 2013 was the lowest in recent years. It raises the issue as to how much collusion there is among the major importers in determining the price of imported rice. This analysis has shown that in two months in 2012 and four in 2013 the reported CIF prices for Sierra Leone are 128% to 242% of maximum expected prices. There is need for strict monitoring of rice importers, and application of sanctions if necessary, to ensure that they do not collude to earn monopolistic profits.

Rice price trends The movements of food crop prices in the country give an indication of the degree to which the level of domestic production (supplemented by imports) meet consumer demand. Monthly data on rice prices are collected by Statistics Sierra Leone for computation of the Consumer Price Index. Figure 32: shows that the retail price of local rice in Freetown, i.e. rice produced in Sierra Leone, has constantly been above that for imported rice except for a few months. However, the gap has narrowed significantly in the last two years implying that the supply of domestic rice to the Freetown market has increased faster than increases in demand.

Furthermore, unlike the situation in the past when local rice prices were higher than imported rice prices even in major rice producing areas such as the Scarcies (Kambia) and the Bolilands (Makeni)

viii

(Spencer, 1997), domestic rice prices are now lower than that for imported rice in the urban areas of the hinterland of Sierra Leone particularly in Kenema which is furthest away from Freetown the source of all imported rice, indicating that transportation costs of imported rice to provincial towns is now enough to remove the slight competitive advantage that imported rice may still have in Freetown.

Price volatility The coefficient of variation (CV), computed as the ratio of the standard deviation to the mean, is a useful tool to compare the degree of variation of different data series. Being an indicator for the dispersion of prices from their average, it provides useful hints to assess how prices change through the market in space and time for different actors (WFP, 2011b).

Intra-year rice price variability in Sierra Leone is reasonably low, with the CV usually under 0.20. Price variability is higher for local than for imported rice, with Freetown having an equal or higher variability than the provincial cities which are closer to the producing areas.

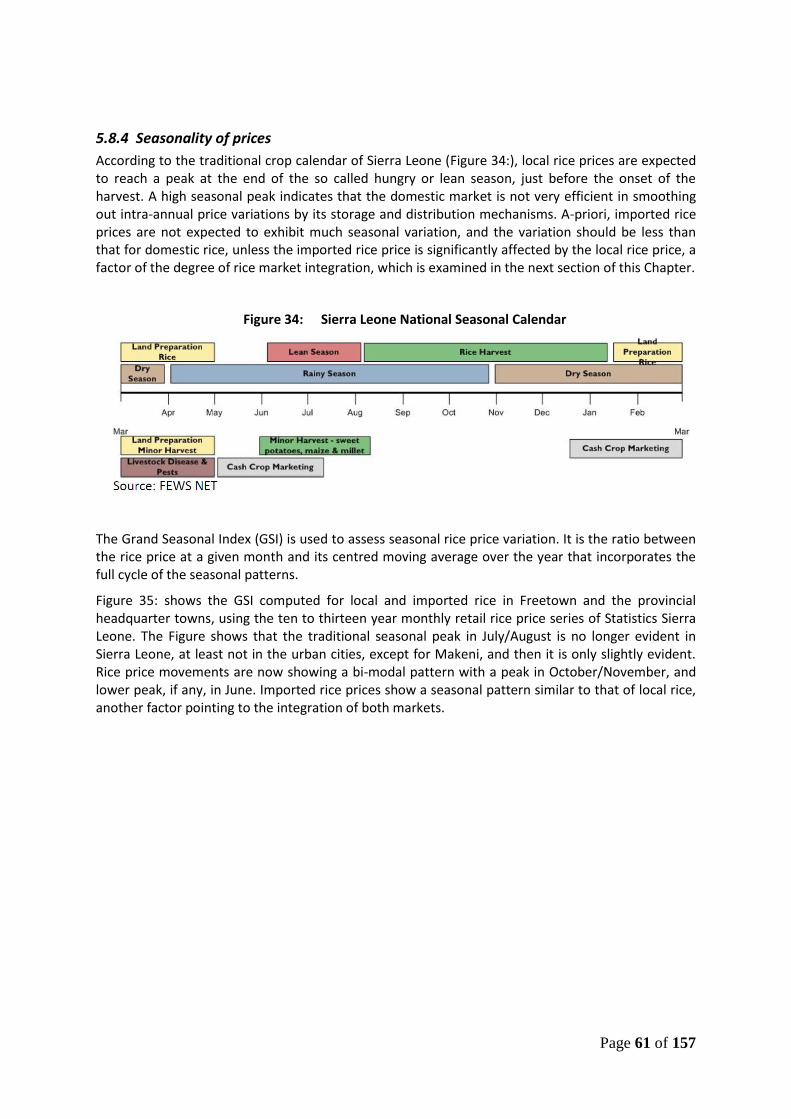

Price Seasonality

According to the traditional crop calendar of Sierra Leone (Figure 34:), local rice prices are expected to reach a peak at the end of the so called hungry or lean season, just before the onset of the harvest. A high seasonal peak indicates that the domestic market is not very efficient in smoothing out intra-annual price variations by its storage and distribution mechanisms.

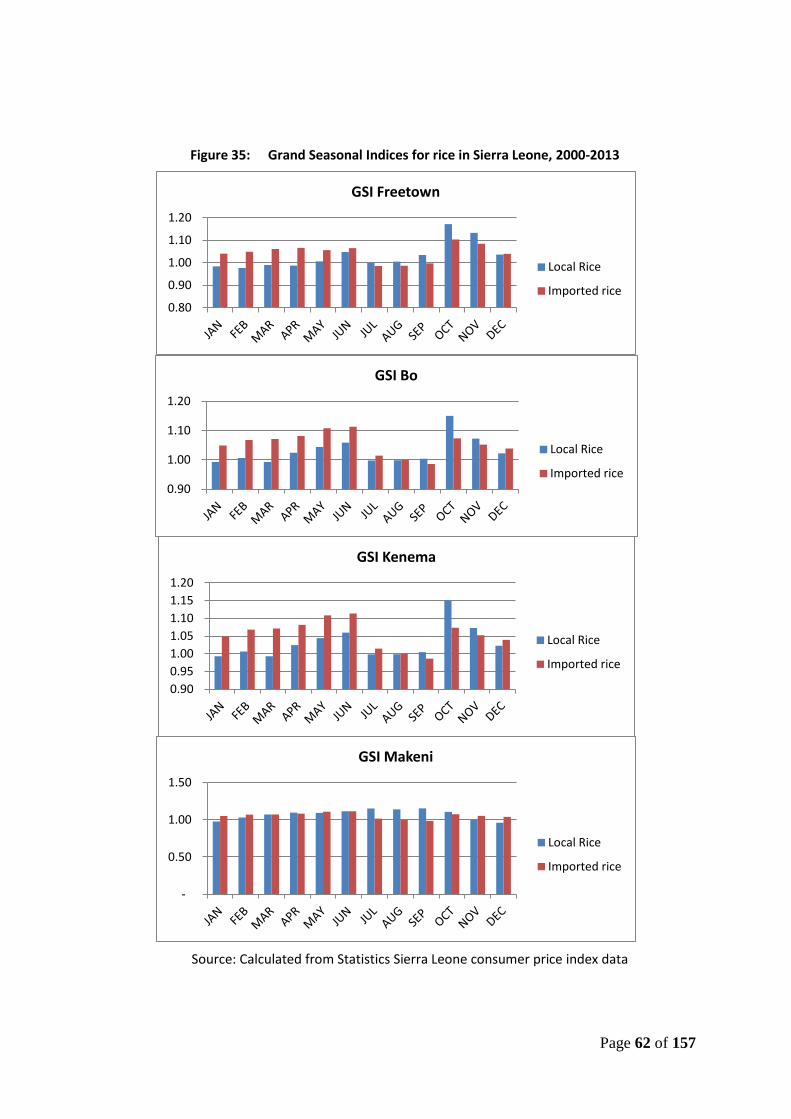

The Grand Seasonal Index (GSI) is used to assess seasonal rice price variation. It is the ratio between the rice price at a given month and its centred moving average over the year that incorporates the full cycle of the seasonal patterns.

GSI computed for local and imported rice in Freetown and the provincial headquarter towns, using the ten to thirteen year monthly retail rice price series of Statistics Sierra Leone, show that the traditional seasonal peak in July/August is no longer evident in Sierra Leone, at least not in the urban cities, except for Makeni, and then it is only slightly evident. Rice price movements are now showing a bi-modal pattern with a slight peak in October/November, and an even lower peak, if any, in June. Imported rice prices show a seasonal pattern similar to that of local rice, another factor pointing to the integration of both markets. Access to imported rice during the traditional hungry season has apparently led to a smoothing of the seasonal peak or rice prices in recent times.

Market Integration

Rice markets have a fair degree of integration in the country. Analysing price trends, volatility and seasonality, there are indications that the rice market in Sierra Leone is fairly well integrated. There are also indications that the price of locally produced rice is determined by the price of imported rice in addition of course, to the level of production in the country. In addition to the international price for imported rice domestic transportation cost play a part in determining imported rice prices in the different urban areas of the country.

The results of Granger Causality Test for Freetown and the three Provincial City Markets (Bo, Kenema and Makeni) for which retail rice price series are available, reveal that the Freetown rice market is integrated with the provincial markets for both imported and local rice. For the linkages between the Provincial Markets – while the Bo and Kenema markets for both local and imported rice appear to be linked to those in Makeni, the reverse is not the case. However, while the Bo and Kenema imported rice markets appear not to be linked, the local rice markets appear to be linked.

We can conclude that the rice markets in Sierra Leone are well integrated. Freetown rice market prices for local as well as imported rice are linked to those in the provincial markets, Provincial rice markets for local rice are also integrated, although less so for imported compared to local rice.

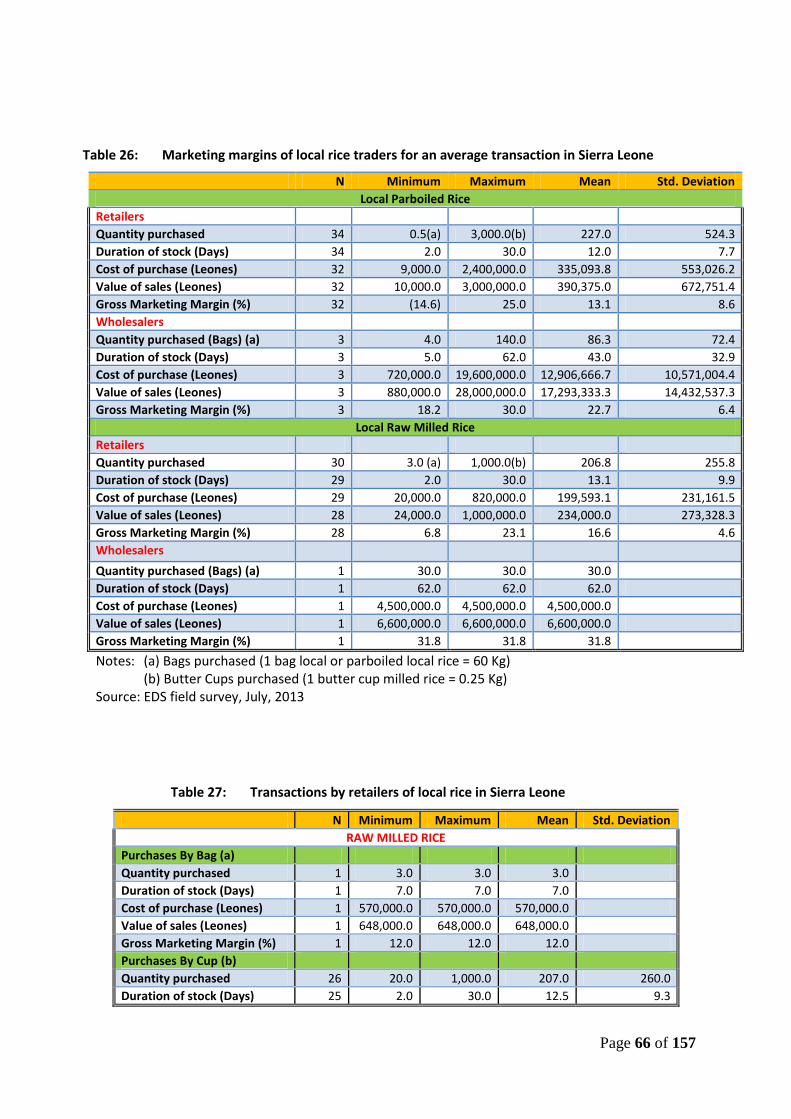

Marketing Margins

ix

Marketing costs are incurred each time a commodity (in this case rice) is exchanged through a distribution system. It is critical to the efficiency of the system that these marketing costs be as low as possible in order to bridge the gap between consumer and farmer prices. One way to achieve that is to promote a competitive environment whereby marketing agents do not have the opportunity to exploit either ends of the marketing chain, namely farmers or consumers.

Price incentives affect the revenues and the procurement decisions of marketing agents; together with marketing and other costs, they affect profits. The analysis of operating costs and profits of traders allows one to understand the relative efficiency of various marketing agents and indicates the constraints that need to be removed in order to improve the marketing system.

Generally margins are higher for retailers of imported rice compared to retailers of local rice - around 24% for imported rice and 15% for local rice. However, wholesalers of local rice earn a higher margin (20-30%) than wholesalers of imported rice (about 8%). The GMM obtained in this study are not considered as excessive, and indicate that the rice trade in Sierra Leone, which is completely in the hands of the private sector, is competitive at both the wholesale and retail levels.

Need for improved physical access to markets

Availability and access to markets are strong incentives for investment in and production of agricultural commodities. National food security will be difficult to achieve without the development of the necessary organised and accessible market for rice. Meaningful efforts to develop the domestic rice industry must therefore address issues of access, input and innovations in the domestic rice market.

Poor access is the greatest setback domestic rice producers, both large and small, face in commercializing their businesses. All-weather feeder roads to Chiefdom market centres are often not available to enable farmers and farmers groups access these markets with ease and negotiate spot prices. Both large and small producers in major rice producing regions face the same challenge in marketing rice after harvests due to the poor state of the trunk roads linking these regions to regional markets. For example, the road from Mange on the Freetown/Kambia highway to the Scarcies mangrove swamp rice belt around Mambolo is not paved and in the rainy season is traversed with great difficulty for passengers and goods. This scenario is also true for the roads from the Port Loko into the Loko Massama rice bowls of Gbinti wala, Kalangba etc. In all weather conditions, the roads to the Bonthe and Pujehun rice belts around Torma Bum and Gbondapi respectively are barely passable and are far from being the commercial rice routes they are supposed to be. Upgrade of the following trunk roads will enhance the domestic rice trade:

Mange to Mambolo

Port Loko to Kalangba and to Rhombe

Bo to Torma Bum

Bo to Gbondapi

Magburaka to Mile 91

Marketing Innovations

The SLPMC and Sierra Leone Standards Bureau should establish and regulate systems for standardizing, branding and certifying locally produced rice that are consistent with international norms. It is well known that locally produced rice is exported to neighbouring countries under an informal trading regime. The MTI through the agency of the SLPMC should regularize this trade with a view to expanding the market for locally produced rice and by so doing, stimulating increased local production. An incentive scheme should be established to encourage collaboration from rice mills and traders. For example State procurement rules would preclude doing business with traders and mills that are not in compliance with the new marketing regulations.

x

xi

ACRONYMS

Acronym Description

ABC Agricultural Business Centres AfDB African Development Bank

AHTS Agricultural Household Tracking Survey

ASREP Agriculture Sector Rehabilitation Project

AU African Union

BDS Business Development Services

CAADP Comprehensive Africa Agriculture Development Programme

CBO Community Based Organisation

CET Common External Tariff

CI Confidence Interval

CORAD Consortium for Rehabilitation and Development

CORAD Consortium for Rehabilitation and Development

DFID United Kingdom Department for International Development

DRC Domestic Resource Cost

DTIS Diagnostic Trade Integration Study

EA Enumeration Area

EBA EU’s Everything But Arms agreement

ECOWAP ECOWAS Agricultural Policy

ECOWAS Economic Community of West African States

EDS Enterprise Development Services Ltd

EPA West Africa–EU Economic Partnership Agreement

EU European Union

EU European Union

FAO Food and Agriculture Organisation of the United Nations

FCE Farmer Controlled Enterprise

FFS Farmer Field Schools

FFS Farmer Field Schools

FIB First International Bank

FSCA Food Security through Commercialization of Agriculture

GDP Gross Domestic Product

GSI Grand Seasonal Index

GTZ Gesellschaft für Technische Zusammenarbeit (German aid agency)

IBRD International Bank for reconstruction and Development (World Bank)

ICT Information and Communications Technology

IDA International Development Association

IDB Islamic Development Bank

IFAD International Fund for Agricultural Development

IFC International Finance Corporation, (World Bank Group)

IMC International Medical Corps

IPAM Institute of Public Administration and Management

IVS Inland Valley Swamps

JICA Japanese International Communications Agency

KfW Kreditanstalt für Wiederaufbau (Reconstruction Credit Institute)

xii

Acronym Description

LEAD Livelihood Enhancement and Asset Development Program

LINKS Promoting Linkages for Livelihood Security and Economic Development

MAFFS Ministry of Agriculture, Forestry and Food Security

MAFFS Ministry of Agriculture, Forestry and Food Security

MDA Ministries, Departments and Agencies

MDG Millennium Development Goals

ME Margin of Error MFI Micro Finance Institution

MICS Multiple Indicator Cluster Survey

MITAF Microfinance Investment and Technical Assistance Facility

MODEP Ministry of Development and Economic Planning

MRU Mano River Union

MT Metric Ton

MT Metric Ton

MTI Ministry of Trade and Industry

MTI Ministry of Trade and Industry

NaCSA National Commission for Social Action

NEPAD New Partnership for Africa’s Development

NERICA New Rice for Africa

NGO Non–Governmental Organization

NR Non Response

NRDS National Rice Development Strategy

NRM Natural Resource Management

NTE Non Traditional Exports

NU Njala University

PAGE Promoting Agriculture, Governance and the Environment

PAGE Promoting Agriculture, Governance and the Environment

PC Producer Companies

PL 480 Public Law 480 of the United States of America

PMP Performance Monitoring Plan

PRSP Poverty Reduction Strategy Paper

PSDSP Public Sector Development Strategy Project

RARC Rokupr Agricultural Research Centre

RCPRP Rehabilitation and Community-based Poverty Reduction Project

RFCIP Rural Financial and Community Improvement Project

RPSDP Rural Private Sector Development Project

RPSDP Rural and Private Sector Development Project

SCP Small Holder Commercialisation Project

SEZ Special Economic Zone

SLAA Sierra Leone Airports Authority

SLARI Sierra Leone Agricultural Research Institute

SLARI Sierra Leone Agricultural Research Institute

SLIBA Sierra Leone Indigenous Business Association

SLIEPA, Sierra Leone Investment and Export Promotion Agency

SLPA Sierra Leone Ports Authority

SLPMB Sierra Leone Produce Marketing Board

SLPMC Sierra Leone Produce Marketing Company

xiii

Acronym Description

SLRA Sierra Leone Roads Authority

SNAP SNAP Sustainable Nutrition and Agricultural Promotion

SPSS Statistical Program for Social Scientists

SSL Statistics Sierra Leone

UN United Nations Organization UNDAF United Nations Development Action Framework

UNDP United Nations Development Program

UNDP United Nations Development Programme

UNHCR United Nations High Commission for Refuges

UNICEF United Nations Children’s Fund

USAID United States Agency for International Development

USG United States Government

UTB Union Trust Bank

VAM Vulnerability Assessment and Mapping

VC Value Chain

VCA Value Chain Analysis

VS&L Village Savings and Loan Association

WAEMU West African Economic and Monetary Union

WB World Bank

WFP World Food Programme

WHO World Health Organization

WTO World Trade Organisation

WVSL World Vision Sierra Leone

xiv

TABLE OF CONTENTS

EXECUTIVE SUMMARY .......................................................................... II

ACRONYMS………….. ............................................................................... XI

TABLE OF CONTENTS ......................................................................... XIV

LIST OF FIGURES ................................................................................ XVII

LIST OF TABLES ................................................................................. XVIII

CHAPTER 1. BACKGROUND ..............................................................1

1.1: Rice in Sierra Leone ....................................................................................................... 1

1.2: The Rural and Private Sector development Project (RPSDP) ....................................... 1

1.3: Objectives of the Study .................................................................................................. 2

1.4: Study Methodology And Data Collection Techniques ................................................... 2

CHAPTER 2. GOVERNMENT AND DONOR POLICIES ..................3

2.1 Government Policies ........................................................................................................ 4

2.2 Requirements for Organizing an Efficient Rice Market ................................................. 6

2.3. Legal and Regulatory Framework .................................................................................. 7

2.4 Donors and Development Partners Policies................................................................... 8

CHAPTER 3. RICE OUTPUT MARKETS ........................................ 13

3.1 Value Chain Mapping ............................................................................................... 13

3.2 Domestic rice processing and trade .......................................................................... 17

3.3 The Export Rice Trade .............................................................................................. 21

3.3.1 The current informal rice export trade ................................................................... 21

3.3.2 The prospects for expanding the rice export trade ................................................. 21

3.4 Imported Rice Trade.................................................................................................. 26

CHAPTER 4. MARKETED SURPLUS FOR RICE ........................... 31

4.1 Small Scale Rice Production ..................................................................................... 31

4.1.1 Comparative Advantage of Sierra Leone rice ....................................................... 31

4.2 Large Scale Rice Production and Marketing ............................................................ 34

4.3 National Rice Production And Demand .................................................................... 35

4.4 Marketed Surplus For Domestic Rice ....................................................................... 38

4.5 Projections Of Marketed Surplus To 2025 ................................................................ 40

xv

CHAPTER 5. MARKET STRUCTURE AND PERFORMANCE ..... 43

5.1 Structure of Market Buildings ................................................................................... 43

5.2 Water and Sanitation Facilities ................................................................................ 45

5.3 Use of Market Buildings ............................................................................................ 46

5.4 Characteristics of rice traders .................................................................................. 47

5.5 Conduct of the rice trade ........................................................................................... 48

5.6 Constraints to market expansion ............................................................................... 52

5.7 Credit and storage strategies .................................................................................... 54

5.8 Performance of the rice marketing system ................................................................ 57

5.8.1 Rice price setting.................................................................................................... 57

5.8.2 Rice price trends .................................................................................................... 57

5.8.3 Price volatility ........................................................................................................ 60

5.8.4 Seasonality of prices .............................................................................................. 61

5.8.5 Market integration ................................................................................................. 63

5.8.2 Marketing costs and returns .................................................................................. 64

CHAPTER 6. EVALUATION OF COMMERCIAL RICE

PROCESSING AND STORAGE ............................................................. 67

6.1 National Inventory of rice mills ................................................................................ 67

6.2 Ownership of Rice Processing Machinery and Facilities ......................................... 69

6.2.1 The ABC Mills ........................................................................................................ 69

6.2.2 RPSDP Mills: ......................................................................................................... 70

6.2.3 Government Owned Mills ...................................................................................... 71

6.2.3 Private Mills........................................................................................................... 71

6.3 Types of Mill Establishments..................................................................................... 71

6.3.1 Small Scale Rice Mill Establishments: .................................................................. 71

6.3.2 Medium Size Rice Mill Establishments ................................................................. 73

6.3.3 Large Rice Mill Establishments: ........................................................................... 75

6.4 Processing methods and products ............................................................................. 78

6.5 Efficiency Of Current Rice Milling Operations ........................................................ 81

6.6 Improving the efficiency of rice milling operations .................................................. 83

6.7 Possible solutions to the identified problems ............................................................ 86

6.8 Efficient Rice Processing – Model Establishments ....................................................... 88

6.9 Efficient Rice Processing – Indicative Business Plans ................................................. 95

6.9.1 Large Scale Mill .................................................................................................... 95

6.9.2 Medium Sized Mill ................................................................................................. 99

6.9.3 Small Scale Mill ................................................................................................... 104

xvi

CHAPTER 7. CONCLUSIONS AND RECOMMENDATIONS ..... 108

ANNEXES……………….. ........................................................................ 116

Annex 1: Terms of Reference for the evaluation ............................................................... 117

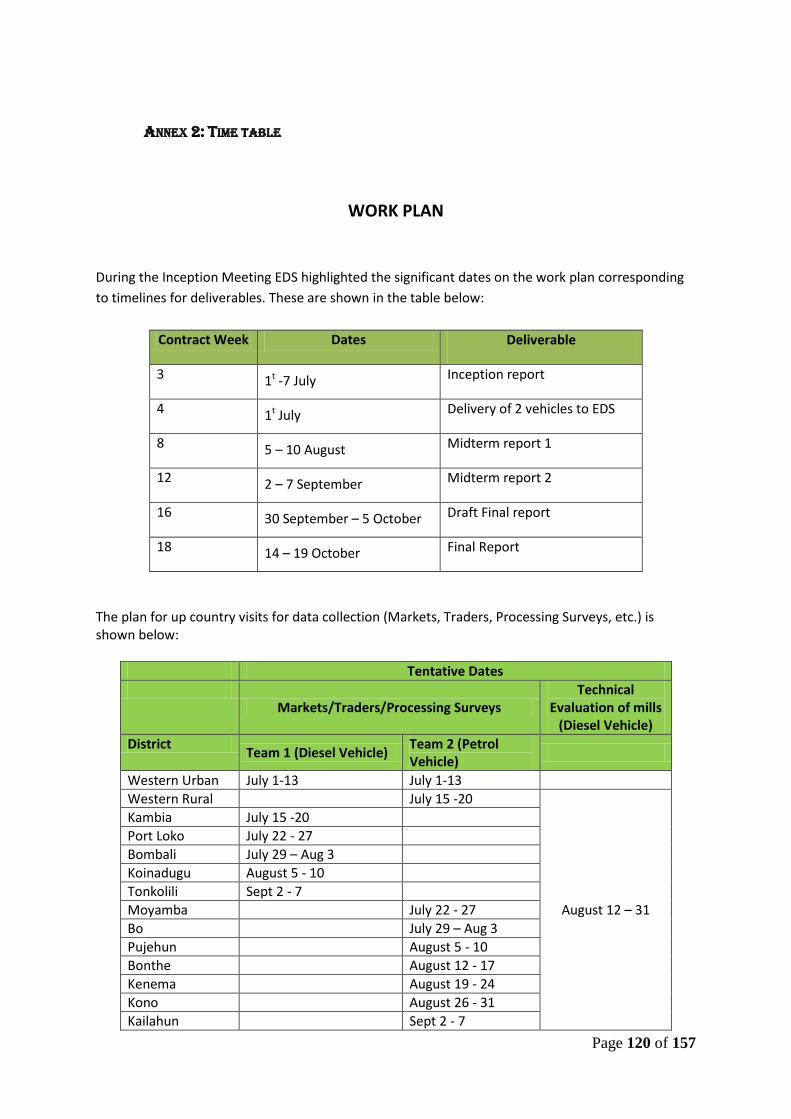

Annex 2: Time table ........................................................................................................... 120

Annex 3: List of documents and references ....................................................................... 123

Annex 4: Survey Instruments ............................................................................................. 126

xvii

LIST OF FIGURES

Figure 1: Conceptual framework for assessment of rice policies in Sierra Leone ............................. 4 Figure 2: Rice value chain map, Sierra Leone .................................................................................. 14 Figure 3: Market channels for marketed surplus 0f domestic rice in Sierra Leone ......................... 18 Figure 4: Current and Projected Regional Rice Imports 1961 – 2020 (metric tons) ........................ 22 Figure 5: Distances to major regional rice markets for Sierra Leone compared to other sources .. 23 Figure 6: Market channels for imported rice in Sierra Leone .......................................................... 27 Figure 7: Monthly Imports of rice into Sierra Leone in 2012 and 2013 ........................................... 28 Figure 8: Proportion of rice imports accounted for by the largest importers in Sierra Leone ........ 28 Figure 9: Average CIF price of rice imports by month in 2012 and 2013 ........................................ 29 Figure 10: Proportion of Rice Imports Received by Districts ......................................................... 31 Figure 11: Area of rice harvest and rice yield (1960 – 2010) ......................................................... 35 Figure 12: Structure of walls of market buildings in Sierra Leone ................................................. 44 Figure 13: Structure of the roofs of market buildings in Sierra Leone .......................................... 44 Figure 14: Structure of market stalls/tables in markets in Sierra Leone ....................................... 44 Figure 15: Toilet facilities available in markets in Sierra Leone ..................................................... 45 Figure 16: Sources of drinking water in markets in Sierra Leone .................................................. 45 Figure 17: Location of traders in markets in Sierra Leone ............................................................. 46 Figure 18: Gender of rice traders in Sierra Leone .......................................................................... 47 Figure 19: Average age and highest class attained by rice traders in Sierra Leone ....................... 47 Figure 20: Type of business training obtained by rice traders before they started trading .......... 48 Figure 21: Number of years that rice traders have been in their business ................................... 48 Figure 22: Distribution of customers of imported rice traders in Sierra Leone ............................. 49 Figure 23: Distribution of customers of local rice traders in Sierra Leone .................................... 50 Figure 24: Proportion of retailers that obtain their supplies within their Districts ....................... 51 Figure 25: Proportion of wholesalers that obtain their supplies within their Districts ................. 51 Figure 26: Constraints preventing retailers from doubling the amount they sell ......................... 52 Figure 27: Constraints preventing wholesalers from doubling the amount they sell ................... 53 Figure 28: Proportion of rice traders who made sales on credit to some of their customers ...... 54 Figure 29: Proportion of rice sales made on credit ........................................................................ 55 Figure 30: Storage strategies used by rice traders ........................................................................ 56 Figure 31: Methods of fixing market prices by rice traders in Sierra Leone .................................. 57 Figure 32: Trend of retail rice prices in Freetown .......................................................................... 58 Figure 33: Retail rice prices in provincial cities .............................................................................. 59 Figure 34: Sierra Leone National Seasonal Calendar ..................................................................... 61 Figure 35: Grand Seasonal Indices for rice in Sierra Leone, 2000-2013 ........................................ 62 Figure 36: Factory Layout for a model small scale rice processing facility in Sierra Leone ........... 89 Figure 37: Factory Layout for a model medium scale rice processing facility in Sierra Leone ...... 91 Figure 38: Factory Layout for a model large scale rice processing facility in Sierra Leone............ 93 Figure 39: Summary of projected performance of large scale model rice mill establishment...... 95 Figure 40: Summary of projected performance of medium sized model rice mill establishment ....................................................................................................................................100 Figure 41: Summary of projected performance of small scale model rice mill establishment ... 104

xviii

LIST OF TABLES

Table 1: Requirements Addressed in the PRSP and Gaps ................................................................. 9 Table 2: Areas of donor activity and support in the Agricultural Sector of Sierra Leone ............... 12 Table 3: Key stakeholders and their activities along the rice value chain ...................................... 15 Table 4: Rice imports into Sierra Leone .......................................................................................... 27 Table 5: Comparison of Sierra Leones import and Thailand export rice prices .............................. 29 Table 6: Estimated competiveness of rice production and imports in Sierra Leone in 2009 ......... 33 Table 7: West African Domestic Resource Cost (DRC) Comparisons for Rice production .............. 34 Table 8: Comparative Advantage of Rice Production systems in Sierra Leone, 2003 .................... 34 Table 9: Sierra Leone, National Rice Production and Self-Sufficiency ............................................ 35 Table 10: Trends in rice (paddy) production in Sierra Leone ........................................................ 36 Table 11: Rice production by District in Sierra Leone ................................................................... 37 Table 12: Rice production by District in 2009 ............................................................................... 37 Table 13: Proportion of rice harvest consumed and sold by farmers in Sierra Leone, 2009 ....... 38 Table 14: Percentage of rice production that is sold .................................................................... 39 Table 15: Estimated marketed surplus of domestic husk rice production by District in Sierra Leone – High production variants ................................................................................. 39 Table 16: Estimated marketed surplus of domestic husk rice production by District in Sierra Leone – Low production variants .................................................................................. 40 Table 17: Projections of marketed surplus of paddy rice in Sierra Leone in 2025 – Scenario 1 .. 41 Table 18: Projections of marketed surplus of paddy rice in Sierra Leone in 2025 – Scenario 2 .. 42 Table 19: Projections of marketed surplus of paddy rice in Sierra Leone in 2025 – Scenario 3 .. 42 Table 20: Projections of marketed surplus of paddy rice in Sierra Leone in 2025 – Scenario 4 .. 43 Table 21: Ranking of commodities sold by rice traders in Sierra Leone ....................................... 49 Table 22: Linear equations for monthly rice price trends (Leones/Kg) ........................................ 60 Table 23: Coefficient of variation of monthly rice prices in Sierra Leone .................................... 60 Table 24: Pair wise Granger Causality Tests for Regional Rice Markets in Sierra Leone .............. 64 Table 25: Marketing margins of Imported rice traders for an average transaction in Sierra Leone ......................................................................................................................................65 Table 26: Marketing margins of local rice traders for an average transaction in Sierra Leone ... 66 Table 27: Transactions by retailers of local rice in Sierra Leone .................................................. 66 Table 28: Location, ownership and condition of rice mills in Sierra Leone, by District ................ 68 Table 29: Physical characteristics of rice mill establishments in Sierra Leone ............................. 82 Table 30: Characteristics of Managers/Operators of Small rice mills in Sierra Leone ................. 82 Table 31: Cost and Returns for Small Rice Mills in Sierra Leone .................................................. 83 Table 32: Adequacy of installed milling capacity in Sierra Leone ................................................. 87 Table 33: Cost of Capital Investment for Model Large Scale Rice Milling Enterprise ................... 97 Table 34: Forecasted sales and cost of sales for large scale model rice mill ................................ 97 Table 35: Projected profit and loss for large scale rice milling company ..................................... 98 Table 36: Projected Balance Sheet for model large scale rice mill in Sierra Leone ...................... 99 Table 37: Cost of Capital Investment for Model Medium Sized Rice Milling Enterprise ............ 101 Table 38: Forecasted sales and cost of sales for Medium Sized model rice mill ........................ 102 Table 39: Projected profit and loss for Medium Sized rice milling company ............................. 103 Table 40: Projected Balance Sheet for model medium sized rice milling enterprise ................. 103 Table 41: Cost of Capital Investment for Model Small Scale Rice Milling Enterprise ................. 105 Table 42: Forecasted sales and cost of sales for small scale model rice mill ............................. 106 Table 43: Projected profit and loss for small scale rice milling company ................................... 106 Table 44: Projected Balance Sheet for model small scale rice milling enterprise ...................... 107

Page 1 of 157

CHAPTER 1. BACKGROUND

1.1: RICE IN SIERRA LEONE

As indicated in the National Rice Development Strategy report (MAFFS, 2009)2 The West African state of Sierra Leone occupies 72,300 km2 of which 5.4 million ha are potentially cultivable. The crop sub sector with the staple food rice dominating contributes about 75 percent of agricultural GDP. Annual per capita consumption of rice (104 kg) in Sierra Leone is amongst the highest in sub Saharan Africa. About 70 percent of Sierra Leone’s 4.9 million people in 2004 were below the national poverty line, with 52% living on less than US$1 per day, while 26% could not afford minimum daily calorific requirements.

While climatic conditions are generally favourable for crop production including rice, biotic and abiotic factors such as diseases, pests, low soil fertility, in addition to the use of low yielding local varieties, poor extension services, and several socio-economic factors are considered to be limiting farmers’ productivity. Also, most small holder farmer’s yield is greatly reduced by post harvest losses due to poor crop management, inappropriate storage and marketing facilities.

The form of agriculture practiced by the vast majority of Sierra Leonean farmers is very rudimentary. Fewer than five percent of the households use fertilizers, insecticides, herbicides and basic machinery which are resources that could help enhance rice production. Rice is cultivated in both the upland and diverse lowland ecologies - Inland Valley Swamps, Bolilands, Mangrove Swamps and Riverine Grasslands. Rice yield in the upland is however generally lower than in the lowlands.

1.2: THE RURAL AND PRIVATE SECTOR DEVELOPMENT PROJECT (RPSDP)

The Government of Sierra Leone has been allocated grant funds from the International Development Association of the World Bank which are administered by the International Development Association (IDA) and executed by the project Coordinating Unit of the Rural and Private Sector Development Project (RPSDP).

The project supports initiatives to improve quality o f produce for domestic/export markets; assists in strengthening marketing organizations at the producer level as well as private trade engaged in domestic marketing and export; support value addition and provide limited support for filling critical gaps in infrastructure along the value chain, in conjunction with initiatives supported by Government/other donors. The project development Objective is to “increase production of selected agricultural commodities by twenty percent and sales by ten percent through improvement in efficiency along the value chain for target beneficiaries”

The project has four components:

Component A: Domestic Marketing Improvement. This component aims at improving domestic distribution channels for selected agricultural products to improve the ability of farmers and traders to market their goods in Freetown and other large domestic markets.

Component B: Agricultural Export Promotion. This component aims to provide the necessary tools and services for promoting agricultural exports o f commodities such as cocoa, coffee, cashew, oil palm, cassava and ginger. The component supports an export promotion initiative for these commodities identified as promising for export by the Diagnostic Trade

2 Ministry of Agriculture Forestry and Food Security (MAFFS), 2009; National Rice Development Strategy

(NRDS), Sierra Leone, Prepared for the Coalition for African Rice Development (CARD)

Page 2 of 157

and Investment Study. Target beneficiaries include agricultural producers, agricultural exporters and other private enterprises in the value chain.

Component C: Support to Farmer-based Organizations and Technology Improvement, aims at increasing farmers' access to improved agricultural technology and practices to support quality improvement o f commodities supported under Components A and B and strategic studies to identify support for additional commodities and markets. It targets rural producers.

Component D: Policy Regulations, Project Management, Monitoring and Evaluation; finances the development of key policy regulations, the project management function and monitoring and evaluation.

1.3: OBJECTIVES OF THE STUDY

The study objectives are to assess the current processing, marketing and distribution mechanisms for rice and propose technically and economically feasible recommendations.

1.4: STUDY METHODOLOGY AND DATA COLLECTION TECHNIQUES

Initial Consultations:

The study commenced with an inception meeting with RPSDP, as employer, to introduce the project team and discuss the Project Work Plan, logistical issues, focal points for consultations and reporting.

As an entry point for performing the assignment, EDS held consultations with the Ministry of Agriculture Forestry and Food Security and the Ministry of trade and Industry to officially apprise Government about the study proposal and obtain advice and commitment of support. Arrangements for the collaboration of the relevant District Directors of Agriculture during field work were made at the level of the Minister and Director General of Agriculture.

Consultations were also held with the Ministry of Local Government and the Decentralization Secretariat to secure arrangements for the collaboration of the relevant District Councils and their District Development Committees., and with key private sector stakeholders, including major commercial rice producers and major importers of rice.

Secondary Data Collection:

EDS conducted a comprehensive desk review of relevant studies and literature on production, processing and marketing of rice in Sierra Leone as well as neighbouring countries that are potential markets for rice produced in Sierra Leone. All reports were thoroughly reviewed to extract background information relevant for this assignment.

Field Data collection:

EDS assessed the efficiency of rice markets by undertaking a number of activities and analysis covering: value mapping to describe the different rice marketing channels, assessment of rice processing facilities, analysis of rice traders, and assessment of types and functioning of markets.

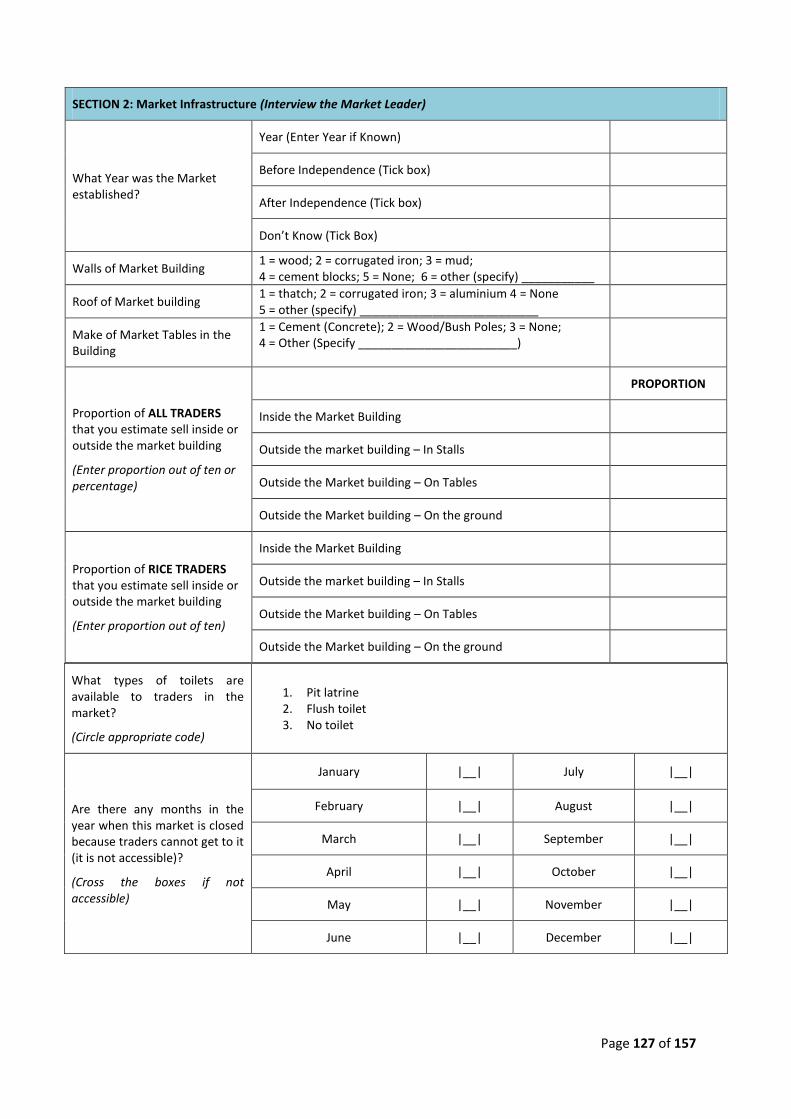

For each significant market type identified in the Value Chain Mapping (e.g. periodic markets, retail markets, wholesale markets etc.) a representative sample was selected and a market questionnaire (see Annex 4) administered to collect information on market infrastructure (Location, Type and sizes of buildings, storage facilities, hygiene, etc), number of traders in the market by commodity, quantities of rice and other major commodities on sale, market prices (current, last week, last month, and time series data if available from local authorities, etc), types and quantities of taxes/levies paid by traders, and number and profiles of people in the market.

Page 3 of 157

A purposive sample of each type of rice trader was selected and a Traders Questionnaire (see Annex 4) administered to collect data on the general characteristics of traders (age, sex, education, past experience, etc), trade volumes and flows – current, past, future projections (number of customers by period, quantities sold, and sources of supply), prices and transaction costs – current, past, future projections (purchases, sales), constraints and coping mechanisms, and credit and stocks strategy.

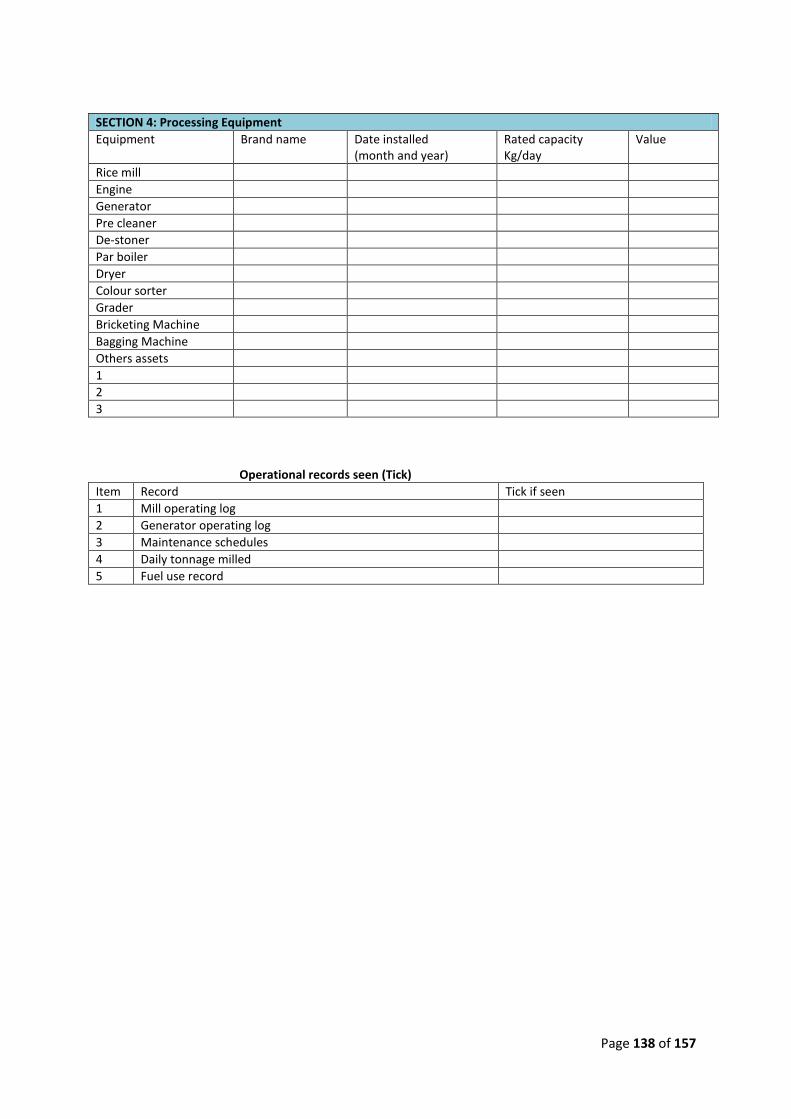

An evaluation of commercial rice processing and storage was undertaken by first of all carrying out a national inventory of all commercial rice processing and storage facilities in the country. Information was recorded on the location of each facility or group of facilities, the make and installed milling capacity at each location, and the capacity utilization of the facilities. A representative purposive sample of establishments (milling and storage) serving the five types of rice production agro-ecologies in the country (mangrove swamps, riverine grasslands, bolilands, inland valley swamps and uplands) was selected, and technical assessment of the facilities carried out to see if they can produce the quality output expected in the local and export market in the ECOWAS region, i.e. installation of pre-cleaning and cleaning equipment, facility for parboiling rice, quality of storage facilities, environmentally safe disposal of wastes, etc.).

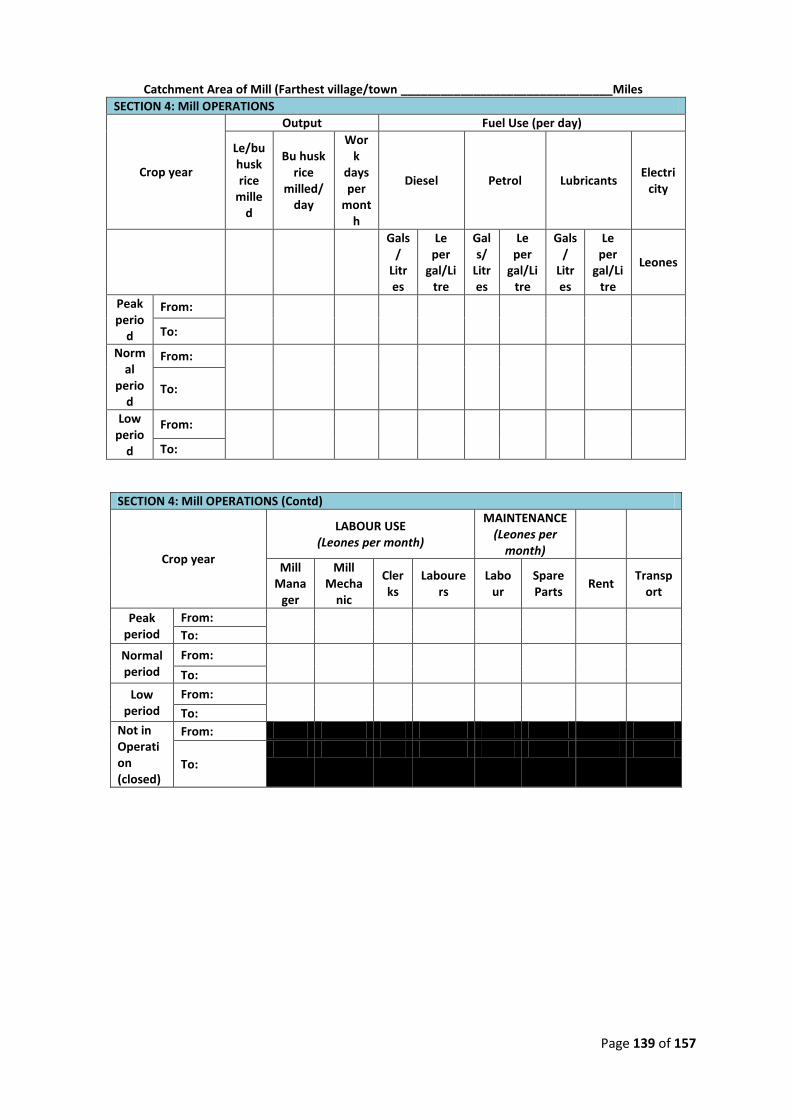

A rice processing questionnaire (see Annex 4) was administered to a purposive sample of milling establishments to collect data on: Demography (age and gender of mill manager, education/training of manager and operators); Mill Infrastructure (size of buildings and drying floors, make of walls and roofs); Processing equipment (brand, date installed, rated capacity, estimated investment cost); Mill operation (milling year, custom milling charge, quantity rice milled/ day, work days per month, labour use, fuel use, maintenance cost,)

Design of model rice processing establishments:

Using the information collected above, model rice processing establishments that are expected to meet the quality and environmental standards for a segmented market (i) the domestic rice market in Sierra Leone, and (ii) the ECOWAS market, which Sierra Leone might be expected to supply in the near future are designed. For each of the model establishments an indicative business plan is prepared. The business plans attempt to show the economic viability of the indicative models of commercial rice processing enterprises.

CHAPTER 2. GOVERNMENT AND DONOR POLICIES

The Sierra Leone rice market does not exist in a vacuum. In order to understand the constraints and incentives to its development and evaluate policy options for the medium-term, it is necessary to capture the various links between rice markets and the rest of the economy. A conceptual framework linking the operations of markets, the macro environment, and growth in the agricultural sector is needed (Figure 1:) in order to evaluate the impact of existing policies and guide the design and implementation of any reforms to be suggested by this study.

©

C

o

p

y

r

i

g

h

t

B

i

z

t

r

e

e

I

n

c

.

2

0

1

0

.

A

l

l

r

i

Page 4 of 157

Figure 1: Conceptual framework for assessment of rice policies in Sierra Leone

(after IFPRI, 1996)3

The dynamics involved in the process of rice production, marketing and trade, and the impact of policy intervention will be examined in the study. Following IFPRI (1996) these dynamics can be described as a sequence of mutually reinforcing processes:

1) reform-led improvements in the macro environment increase the efficiency of rice markets which improves the allocation of resources and promotes growth in the agricultural sector;

2) agricultural expansion, induced through specialization and associated with increased marketed surplus, increases liquidity in the agricultural sector, facilitating investment in improved inputs and the intensification of production;

3) this in turn raises supply in rice markets and demand in input markets, resulting in economies of scale in the distribution and delivery systems, which under competitive conditions translates into increased incentives to producers.

The success of market reforms may depend largely on the extent to which additional and facilitating measures are adopted to support the self-reinforcing sequence of specialization, intensification, and economies of scale. Examples of such measures to be examined in the study include provision of market information to strengthen the price transmission process across domestic markets, creation and functioning of the necessary legal environment that reduces the risk and uncertainty associated with market transactions, and supporting infrastructure for the marketing sector. This feedback system is also reinforced by expectations of a stable policy and macro environment; expectations that affect investment decisions in all sectors of the economy and stimulate growth.

2.1 GOVERNMENT POLICIES

Agricultural sector development policies have been the backbone of national development policies and strategies of successive governments of Sierra Leone during the last decade. As the staple food

3 International Food Policy Research Institute, 1996; Rice market monitoring and policy study, Final Report,

Prepared for the Asian Development Bank, Washington DC, December 1996)

Page 5 of 157

and most widely cultivated crop, produced by over two-thirds of the nation’s farmers, rice is the most important agricultural commodity produced and marketed in the country. The importance of this crop is evident from its share of the national economic output. It is estimated that agriculture contributes 45% of the national GDP with rice account for 35% of that national output.

Since 2005, national development strategies and actions have been guided by Poverty Reduction Strategy (PRS) documents developed through wide consultations with economic actors in all sectors of the economy and the support of donors and development partners. Since 2005, three Poverty Reduction Strategy Papers (PRSPs) have been formulated employing the participatory consultative approach and incorporation of lessons learnt from previous strategies. PRSP I covered a period of three years from 2005 to 2007. PRSP II (Agenda for Change) was in effect from 2008 to 2012. The current PRSP III was launched in July 2013 as a national Agenda for Prosperity and will be in effect for five years until 2018.

Government’s national development policy requires that the current Poverty Reduction Strategy Paper - PRSP and Millennium Development Goals MDGs shall be the official framework for all development activities in the country. All Government, donor and development partners’ development programmes and projects are required by this policy to be aligned to that framework and contribute towards the achievement of the outcomes specified in them, for each sector of the economy, within the indicated timelines.

Government’s current agricultural strategy and objectives are summarized in the current PRSP as follows:

To increase the production of staple food crops for food security:

Increase farmers’ access to agricultural inputs – fully operationalize the Agricultural Business Centres (ABCs), including construction and providing equipment; continue to provide extension services to farm households, providing them with improved chemicals, seeds, and tools.

Improve farmers’ use of technology – increase the activities of research and extension services, with plans that focus on use of technology.

Undertake land and water development programmes – rehabilitate inland valley swamps, and develop irrigated rice nucleus farms, which will be linked to out-grower schemes.

Improve the skills and organisation of farmers – roll out schemes for training on improved farming techniques, through Farmer Field Schools, and provide production support to new and existing Farmer-Based Organisations.

Encourage agricultural input markets to be led by the private sector – roll out the ‘agro-dealers’ support programme.

Improve animal health care to facilitate livestock production – establish District Livestock Clinics, provide training for middle-level personnel and Community Animal Health Workers, and provide support to cross-breeding and feed mill initiatives through ABCs.

Construct new feeder roads and rehabilitate existing feeder roads to facilitate the bringing of agricultural production to markets.

Operationalize a strategic grain reserve to ensure that food reserves are available in times of urgent need.

To promote and increase value-adding activities for agricultural goods:

Increase availability of processing facilities – provide agro-processing facilities at ABCs.

Page 6 of 157

Establish hubs of value-adding activities – promote value-adding activities for agricultural goods through the framework of SEZs, industrial Growth Centres and ‘Growth Poles’ (see Pillar 4 for more details).

To increase the production and export of cash-crops:

Facilitate better organisation of farmers: provide support towards the establishment and operationalization of smallholder cash-crop farmer cooperatives.

Rehabilitate existing plantations and facilitate the establishment of new plantations for cash-crop production by ensuring land lease agreement providing investment incentives.

Improve the institutional setup for export standards: build the capacity of the Standards Bureau to effectively monitor the quality of cash-crop exports.

Continue to increase regional and international integration: continue to participate in regional and international initiatives, including certification schemes and roundtables.

Improve access to Finance for Farmers:

Increase access to finance for agricultural workers and firms: build the capacity of financial institutions, including FSAs and Community Banks, to support small to medium scale investments in the agriculture sector, to lend to farmers of all sizes.

Strengthen the capacity of MAFFS

Provide support to the Agricultural Investment Task Force to coordinate agricultural investment and community impact, including the dissemination and enforcement of relevant guidelines as well as interacting regularly with the private sector to discuss challenges.

Strengthen the capacity of Ministry of Agriculture, Forestry and Food Security in the collection and analysis of quality of Agricultural statistics.

2.2 REQUIREMENTS FOR ORGANIZING AN EFFICIENT RICE MARKET

The minimum requirements for the development an efficient rice market in Sierra Leone are the following

1. Infrastructure a. All weather road network connecting production areas to processing facilities, domestic

market centres and export outlets b. Adequate weather-proof storage facilities at bulking and processing areas to reduce post

harvest losses to the barest minimum. c. Shipping and port facilities with adequate equipment for loading and unloading large

tonnages of bagged and bulk cargo.

2. Energy and Power a. Availability of affordable electricity supply for running processing plants. b. Reliable and affordable supplies of petroleum products for running generators and

transporting large cargos of produce from production to processing areas, market centres and port outlets

3. ICT a. Telecommunication facilities for transacting trade and other business activities in a

timely manner b. Information media (radio and print) for the dissemination of market information.

Page 7 of 157

c. Internet connectivity for rapid communication and for conduct trade and financial transactions.

4. Transportation a. Vehicle for haulage of cargos of products from farms to processing depots, market

centres and ports b. Air transportation for business travels into and out of the country as required. c. Sea transportation for movement of people and goods to and from coastal locations

5. Financial services

a. Banking for promoting investment and trade b. Insurance For investment protection and minimization of risk for financial institutions c. Availability of institutional credit for agricultural production and trade

6. Regulation, inspection and certification

a. Standards regulation b. Quality control c. Customs services

An assessment of the Minimum requirements met in the PRSP and the gaps is presented in Table 1:.

2.3. LEGAL AND REGULATORY FRAMEWORK

Rice is the most important agricultural product grown and traded in Sierra Leone. In an effort to create appropriate legal and regulatory framework for sustainable marketing and distribution of agricultural products in the country, the Government of Sierra Leone (GoSL) has passed legislations creating and empowering three strategic institutions:

1. The Sierra Leone Produce Marketing Company:

In 2009 the GoSL caused to be incorporated the Sierra Leone Produce Marketing Company as a limited liability company under the Companies Act No 5 of 2009. The purpose for which the company was formed was to carry on the business of dealers in agricultural products of all kinds. In practice the main activities of this company has been in the processing, packaging and marketing of local rice and in maintaining a buffer stock of this commodity with funding from government.

To enable the company carry out these functions, among others, the Sierra Leone Produce Marketing (Repeal) Act 2013 was legislated in July 2013 “Being an Act to repeal the Sierra Leone Produce Marketing Act, to dissolve the Sierra Leone Produce Marketing Board, to vest the property of the Board in the Sierra Leone Produce Marketing Company Limited…” With these resources vested in the SLPMC and funding for its rice purchases, the company is positioned to among other things, function like the former Rice Corporation, except that it is initially contracting with private mills to process its rice stock.

2. The Sierra Leone Produce Monitoring Board:

On the 13 September 2013, Government passed “The Produce Monitoring Board Act 2013”, being an Act to establish the Produce Monitoring Board to monitor the production, Processing and Marketing of produce…” . The purpose for which this Board was created are among other things to highlight just two are:

Initiate and encourage the processing of produce with the aim of adding value to them for export and for local consumption

Page 8 of 157

Regulate the internal marketing of produce.

3. The Sierra Leone Standards Bureau

The Bureau was created by the Standards Act No. 2 of 1996 (National Provisional Ruling Council Decree, Repeal and Amendment Act No. 3 of 1996) and went into force on the 18th December, 1996. It became operational on the 24th January 2000 assuming the Weights and Measures administration of the Ministry of Trade and Industry. The strategic vision of the bureau is aligned to the National development priorities especially in the Agricultural and Fisheries sectors for the export of agricultural products to international markets.

There is overlap in functions of these three institutions, the former two of which were established in

the same year 2013, specifically for the development and regulation of trade in locally produced

agricultural products. This anomaly must be addressed to avoid confusion in the markets for these

products. It would appear that the two new companies are re-creations of the former Rice

Corporation and the Sierra Leone Produce Marketing Board respectively. It would indeed be a good

idea if that was the case and conscious attempt is made to have them specialize in their functions,

while avoiding the mistakes and pitfalls that prevented the forms organizations in living up to the

great promise they held for the development of markets for the country’s agricultural products.

2.4 DONORS AND DEVELOPMENT PARTNERS POLICIES

To a large extent donor and development partners’ assistance policies to Sierra Leone are aligned to the Poverty Reduction Strategy framework as encapsulated in the PRSP documents. International Financial Institutions programmes also align with the PRSP. The United Nations agencies country programmes are more aligned to the achievement of the MDGs and follow the United Nations Development Action Framework (UNDAF), which is a programme document between government and the United Nations Country Team that describes the collective actions and strategies of the United Nations to the achievement of national development objectives. The UNDAF includes outcomes, activities and UN agency responsibilities that are agreed by government and shows where the United Nations can contribute most effectively to the achievement of national development priorities.