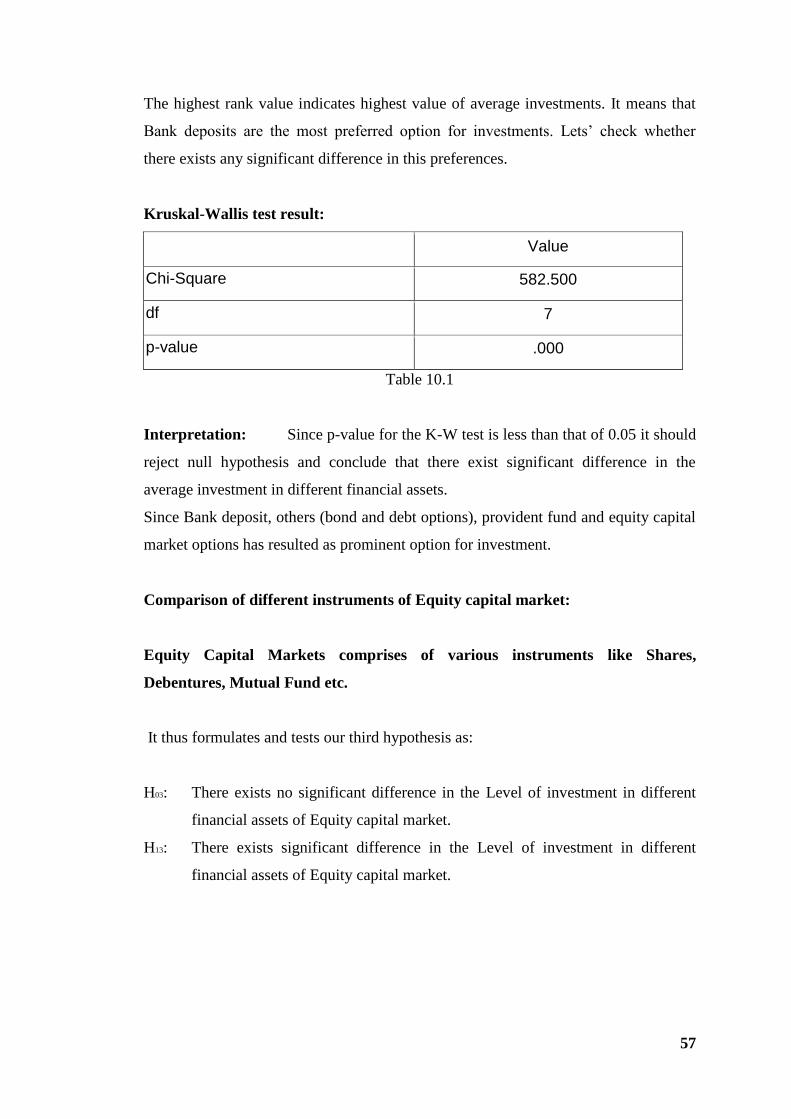

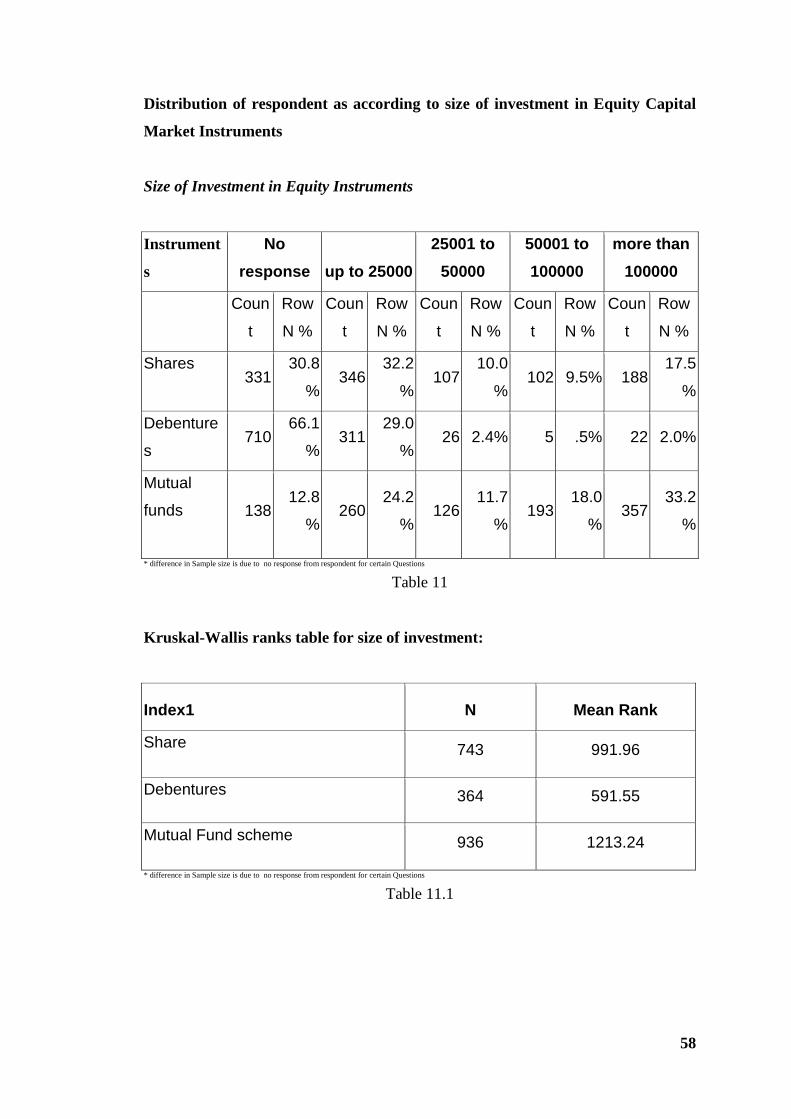

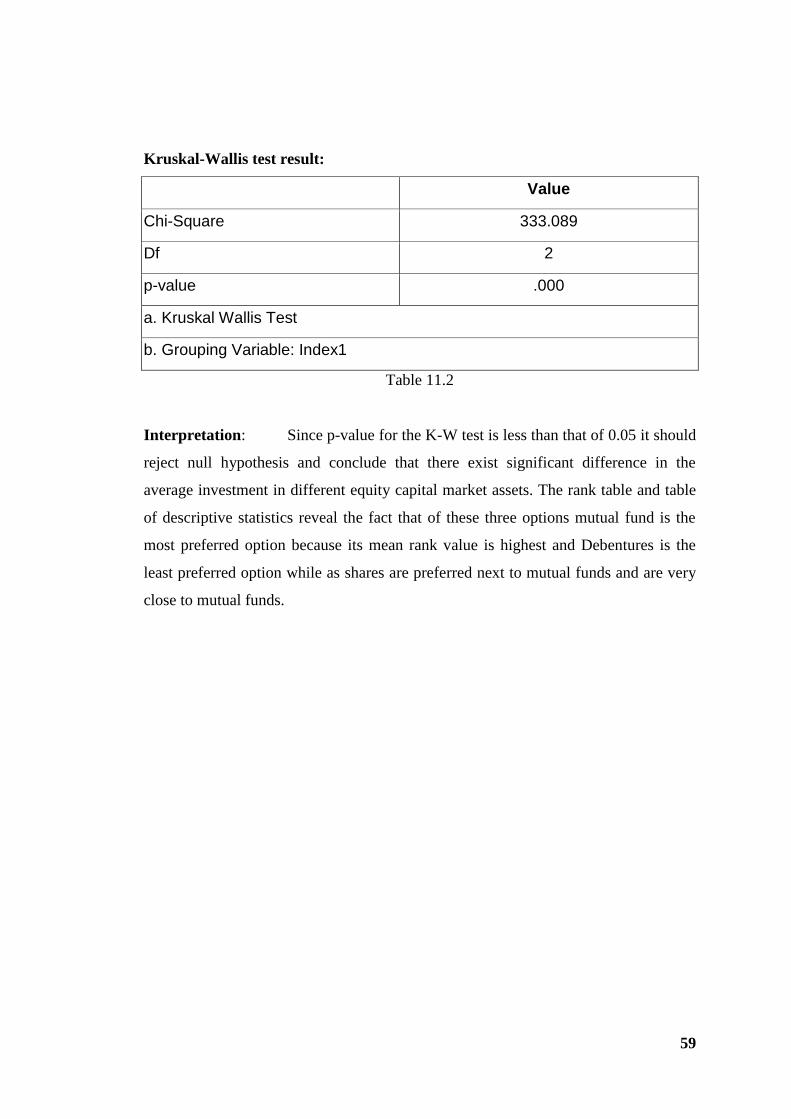

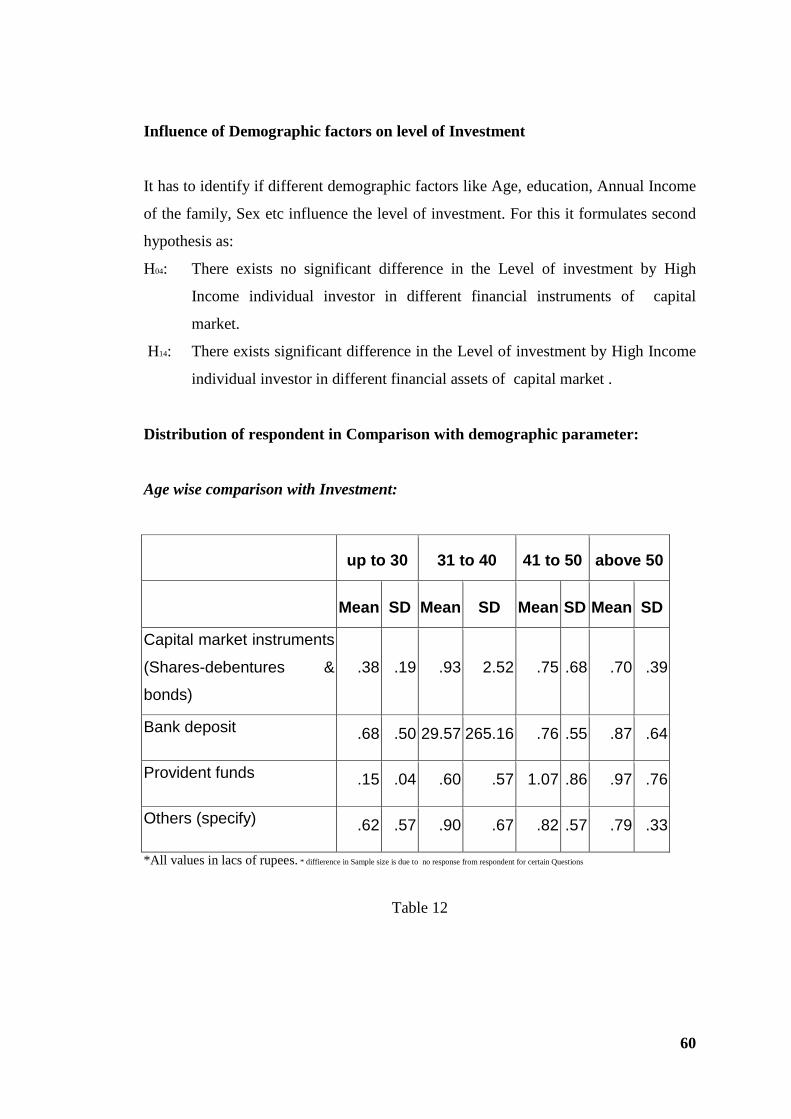

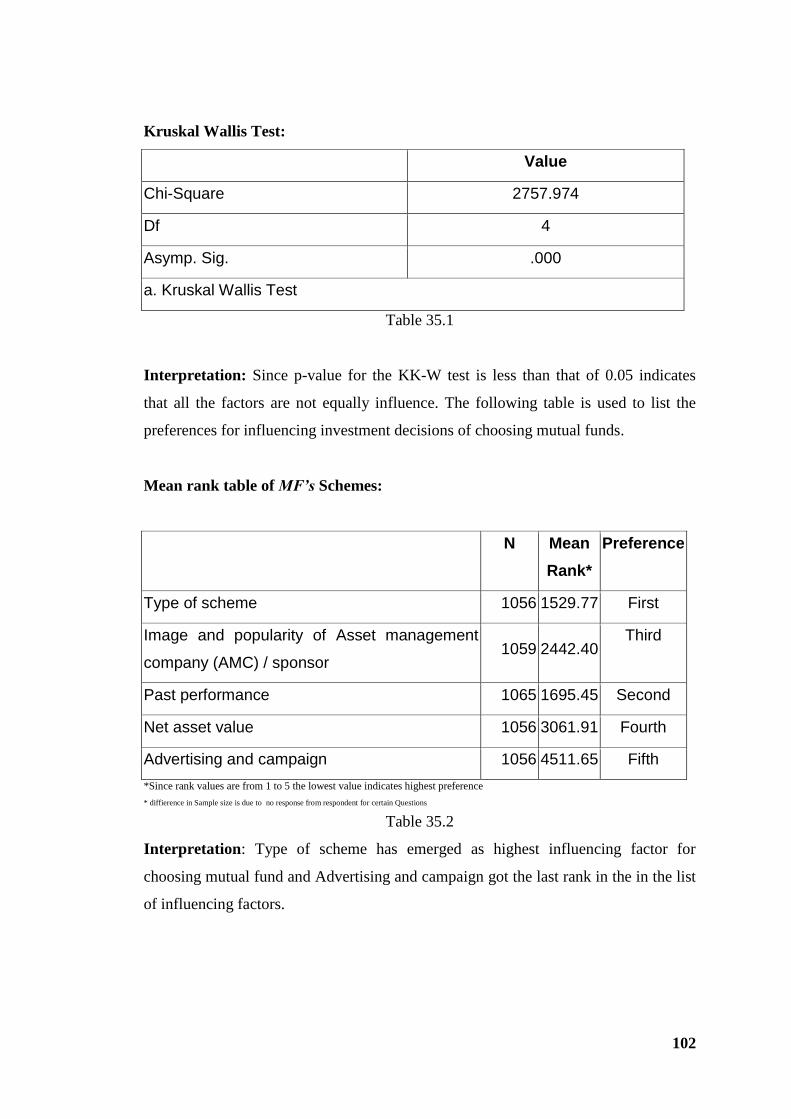

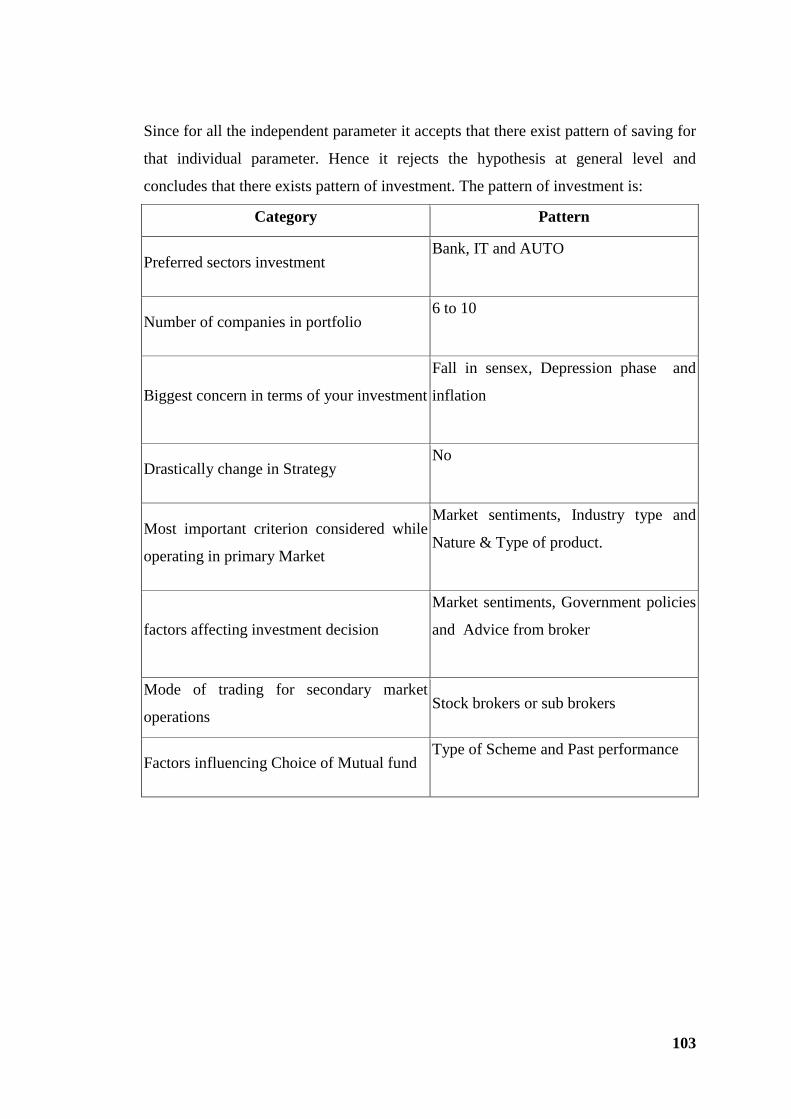

study on high income group individual investors preferences … · study on high income group...

TRANSCRIPT

Study on High Income Group Individual Investors Preferences In

Capital Market With Respect To Risk On Investment: Special

Reference to Mumbai and Pune.

Dissertation Submitted

To

D.Y. Patil University, Navi Mumbai

Department of Business Management

In partial fulfillment of the requirements

For the award of Degree of

Master of Philosophy

In

Business Management

Submitted By

Mrs. Anamika Mitra

( Enrollment No.- DYP-M.Phil-11010 )

Research Guide

Professor Dr. Pradip Manjrekar

Dean

D.Y. Patil University, Navi Mumbai

Department of Business Management

Sector-4, Plot No. 10, CBD Belapur, Navi Mumbai

August 2014

Study on High Income Group Individual Investors Preferences In

Capital Market With Respect To Risk On Investment: Special

Reference to Mumbai and Pune.

DECLARATION

I hereby declare that the work presented in the thesis entitled “Study on High Income

Group Individual Investors preferences in Capital Market with respect to Risk

On Investment: Special reference to Mumbai and Pune.” Submitted for the Award

of Master of Philosophy in Business Management at the Dr. D. Y. Patil University,

Department of Business Management is my original work and the dissertations has

not formed the basis for the award of any degree, associate ship, fellowship or any

other similar titles.

The material borrowed from other sources and incorporated in the dissertation has

been duly acknowledge.

I understand that I myself could be held responsible and accountable for plagiarism, if

any, detected later on.

The research paper published based on the research conducted out of an in the course

of the study are also based on the study and not borrowed from other sources.

Ms. Anamika Mitra

Date: Aug,2014 M. Phil Scholar

Place: Navi Mumbai Enrollment No. :DYP-M.Phil-11010

CERTIFICATE

This is to certify that the dissertation entitled “Study on High Income Group

Individual Investors preferences in Capital Market with respect to Risk On

Investment : Special reference to Mumbai and Pune ” Is the bonafide research

work carried out by Ms. Anamika Mitra, in partial fulfillment of the requirements for

the award of the Degree of Master of Philosophy in Business Management and that

the dissertation has not formed the basis for the award previously of any degree,

associateship, fellowship or any other similar title of any University or Institution.

Also certified that the dissertation represents an independent work on the part of the

candidate.

Place: Navi Mumbai

Date: Aug,2014

Prof. Dr. R Gopal Prof. Dr. Pradip Manjrekar

Director & Head of Department Dean & Research Guide

Department of Business Management Department of Business Management

D.Y. Patil University, Navi Mumbai D.Y. Patil University, Navi Mumbai

ACKNOWLEDGEMENTS

I am grateful to Department of Business Management, D.Y. Patil University, Navi

Mumbai for giving me an opportunity to pursue M.Phil. I am especially grateful to

Prof. Dr. Gopal, Director and Head of the Department, Department of Business

Management, D.Y. Patil University, Navi Mumbai for encouragement and guidance.

I would specially like to express deep gratitude to my Guide Prof. Pradip Manjrekar,

Dean, Department of Business Management, D. Y. Patil University, Navi Mumbai. It

would be no exaggeration to say that this research would not have been completed

today without his rock steady guidance and moral support.

I sincerely thank my family for supporting me for this M. Phil research work and thus

have helped me in completing the M. Phil research work successfully.

Last I also wish to thank all my near and dear ones who have been directly or

indirectly instrumental in the completion of my dissertation.

Place: Navi Mumbai Ms. Anamika Mitra

Date: Aug,2014 M. Phil Scholar

INDEX

CHAPTER

NO.

TITLE PAGE NO.

List of Tables

List of Graphs

Executive Summary

1. INTRODUCTION

1-12

Indian Capital Market 1

Broad Constituents in the Indian Capital

Markets

2

Concepts and Definitions 3

Risk on Investment

7

Role Of SEBI In Indian Capital Market 7

Reforms In Capital Market Of India 8

Factors Affecting the Investors Preferences 10

Need For the Study 11

2. LITERATURE REVIEW 13-29

Research Gap 28

3. OBJECTIVE, HYPOTHESIS &

RESEARCH METHODOLOGY

30-37

Scope Of The Study

30

Objective of the study 31

Hypotheses of the study 31

Research Methodology 32

Limitation of Study 37

4.

PROFILE OF STUDY AREA AND

SAMPLE POPULATION

38-49

A Brief Profile of Mumbai and Pune city 38

Stock Exchanges in Mumbai and Pune 39

Profile Of Sample Population 42

5. ANALYSIS AND INTERPRETATION

OF DATA

50-103

6. FINDINGS AND CONCLUSION 104-109

7. RECOMMENDATIONS

110

8. BIBLIOGRAPHY

111-123

Annexure I - Questionnaire

123-128

LIST OF TABLES

Table No. List Of Tables Page No.

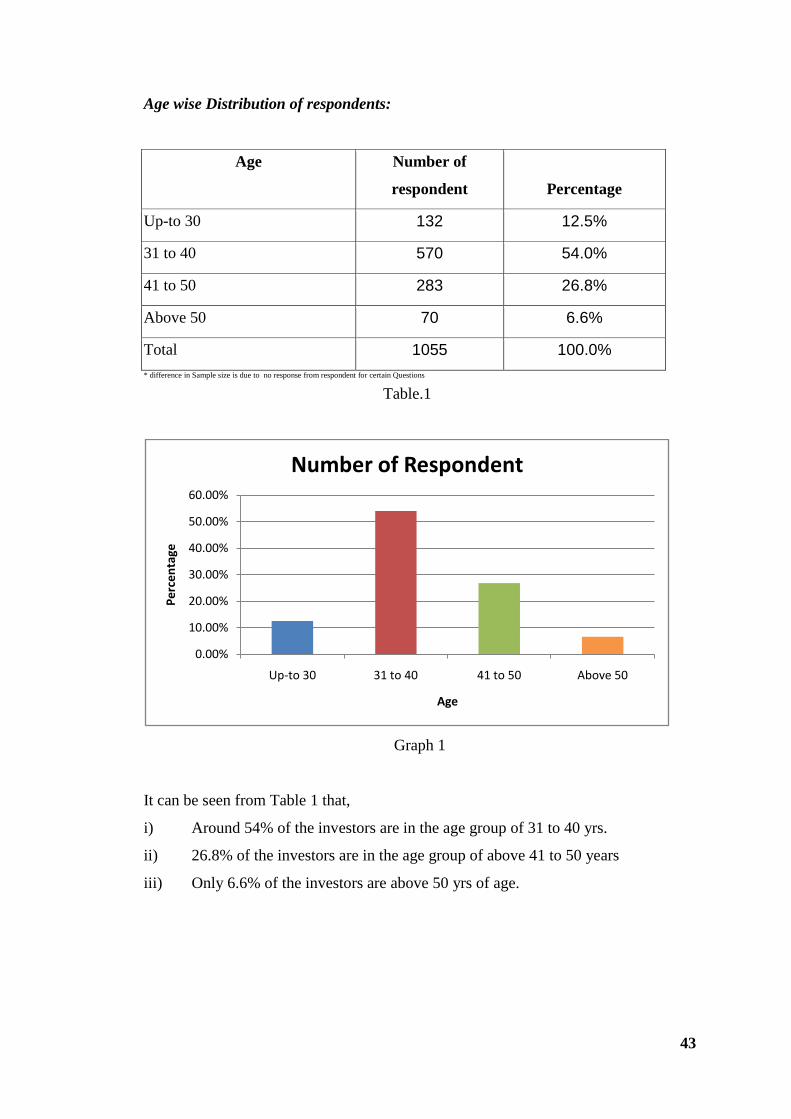

1 Age wise Distribution of respondents 43

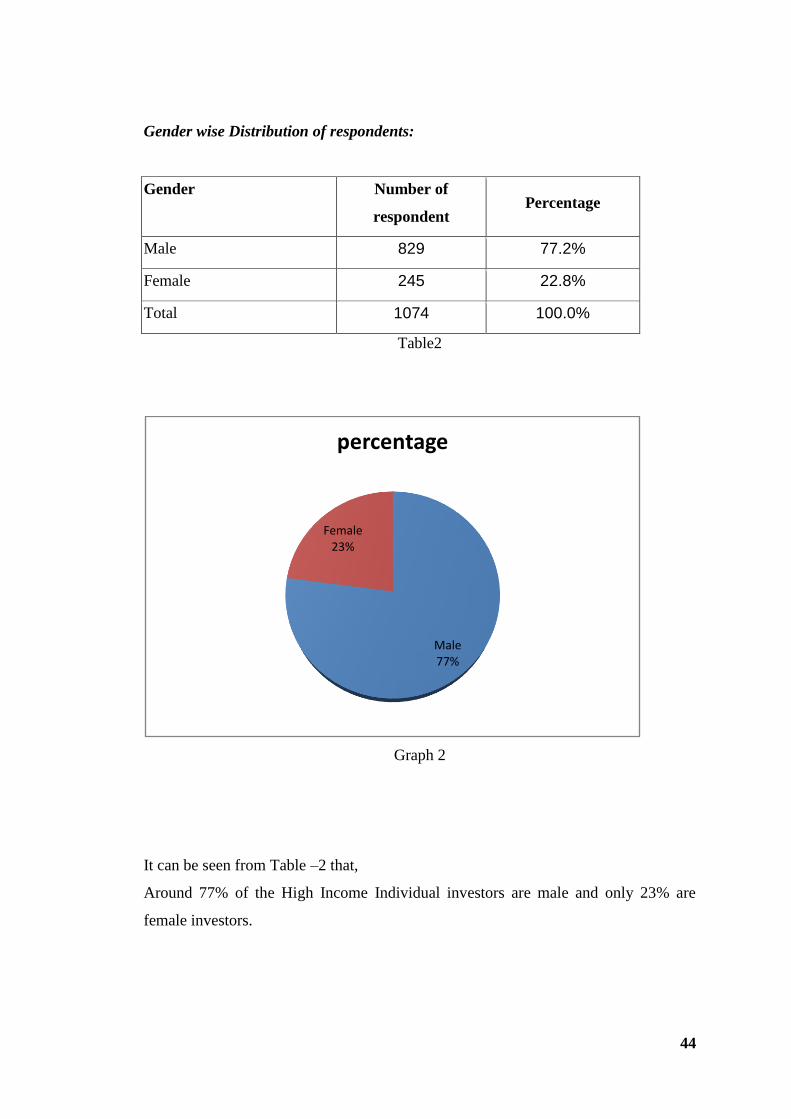

2 Gender wise Distribution of respondents 44

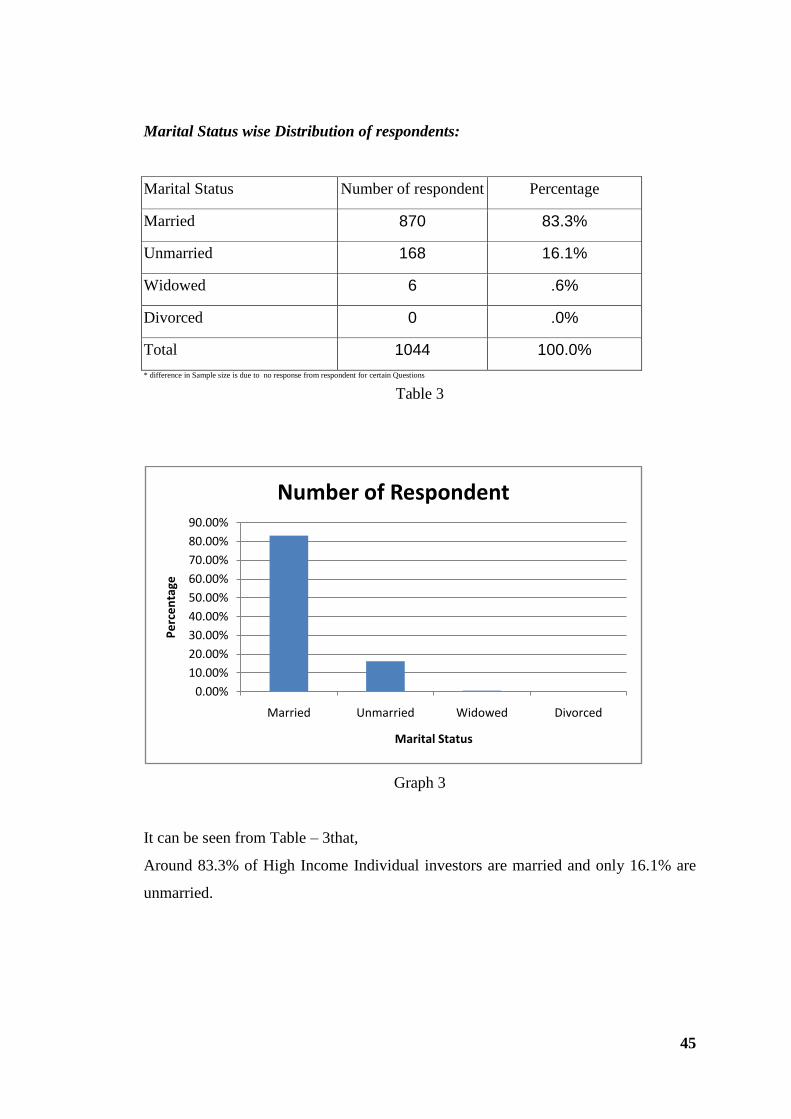

3 Marital Status wise Distribution of respondents 45

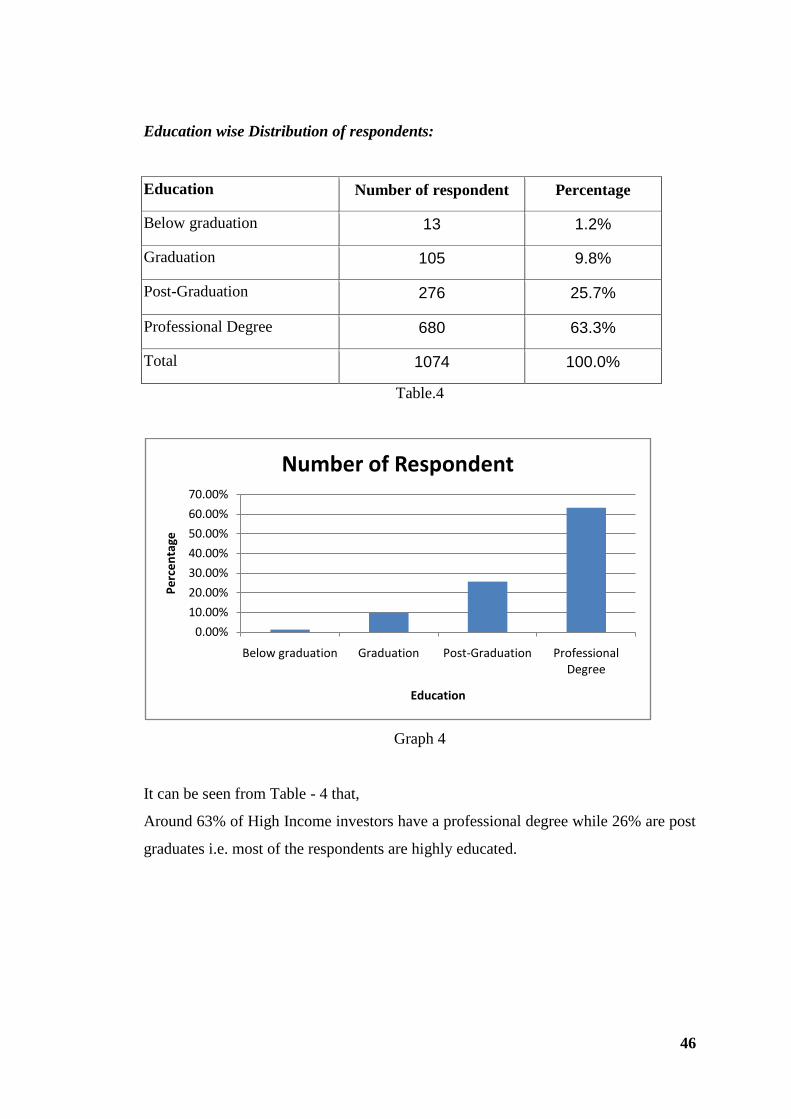

4 Education wise Distribution of respondents 46

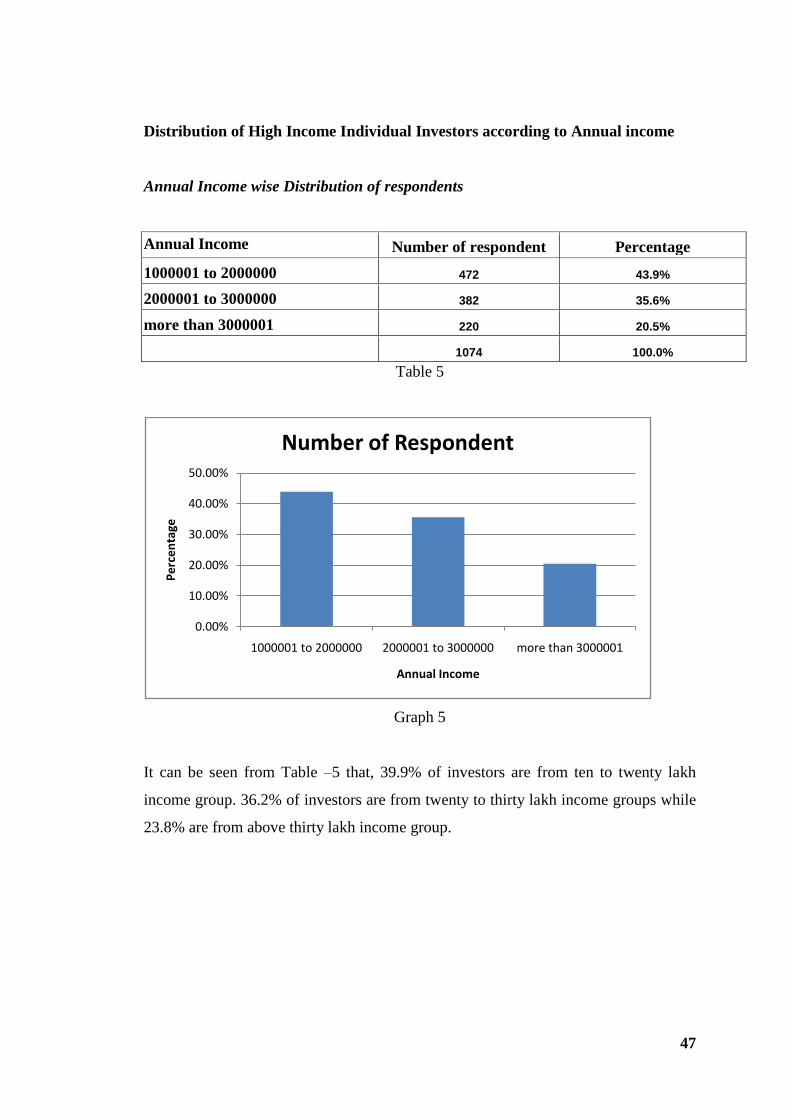

5 Annual Income wise Distribution of respondents 47

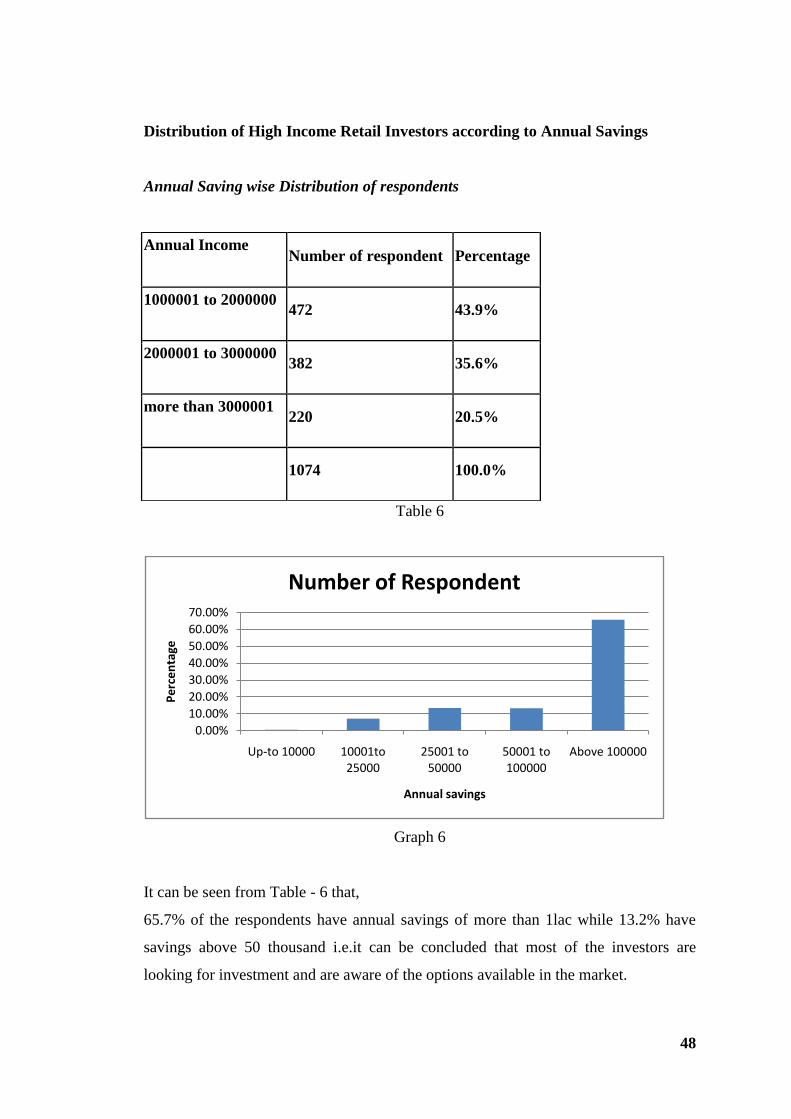

6 Annual Saving wise Distribution of respondents 48

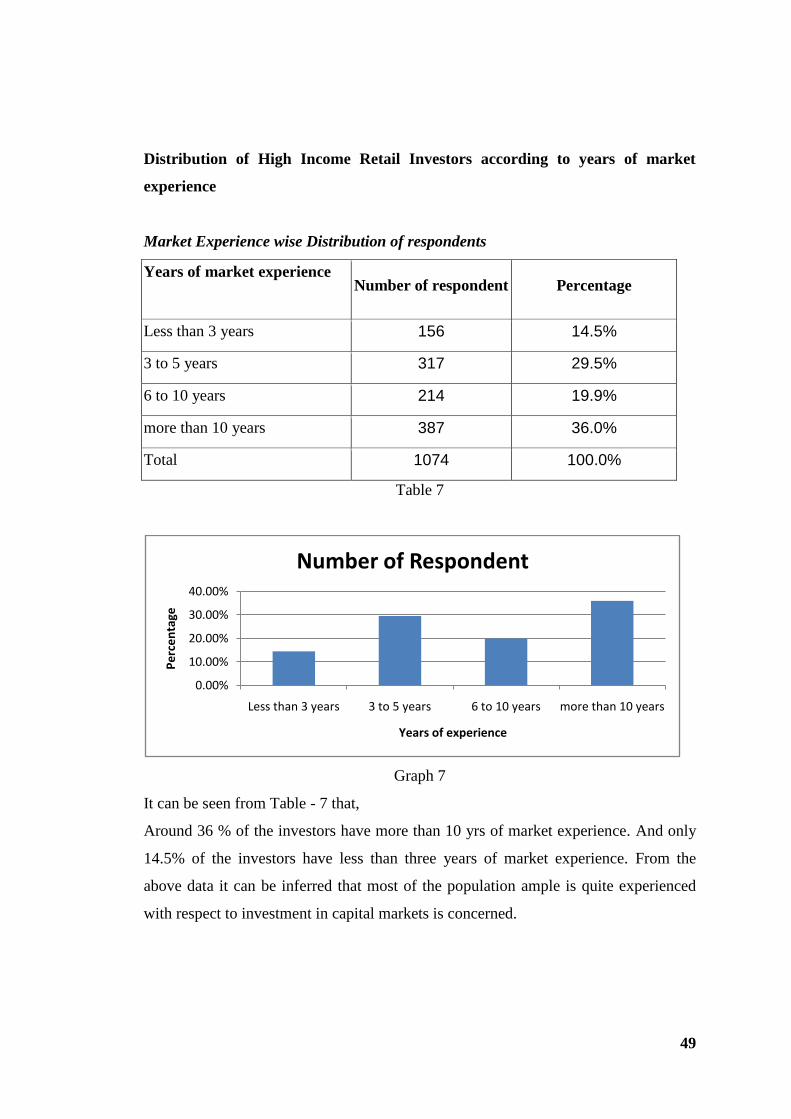

7 Market Experience wise Distribution of respondents 49

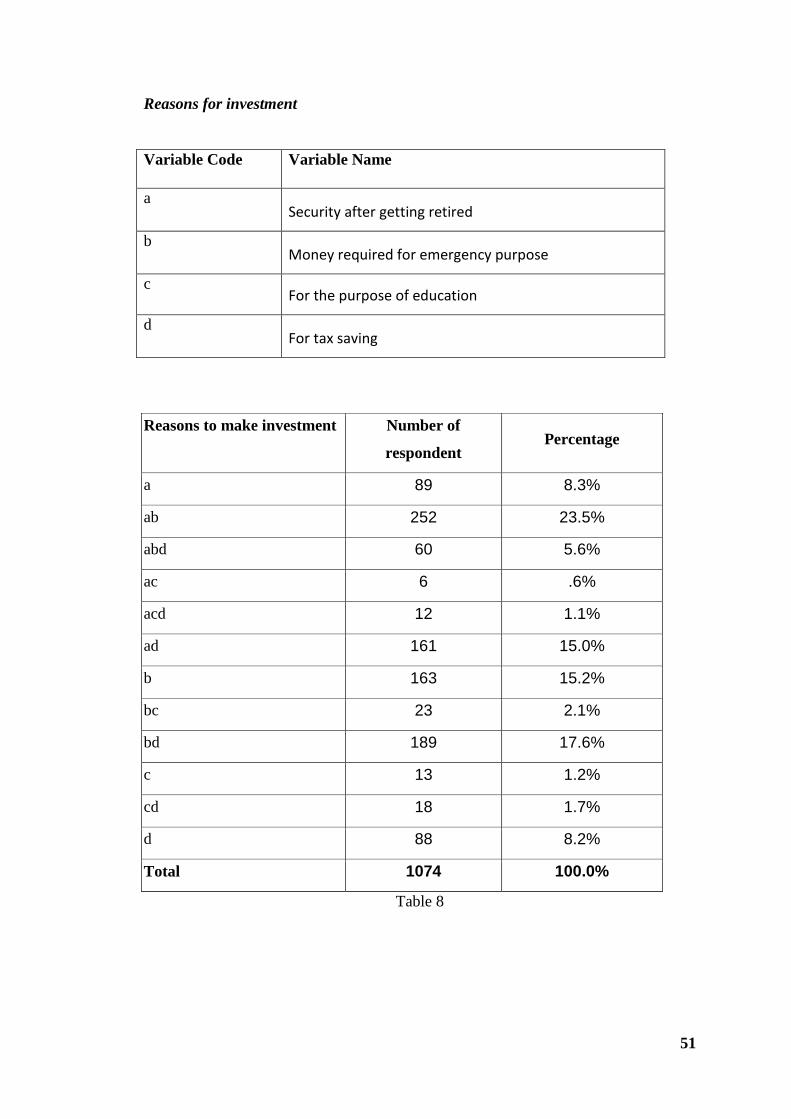

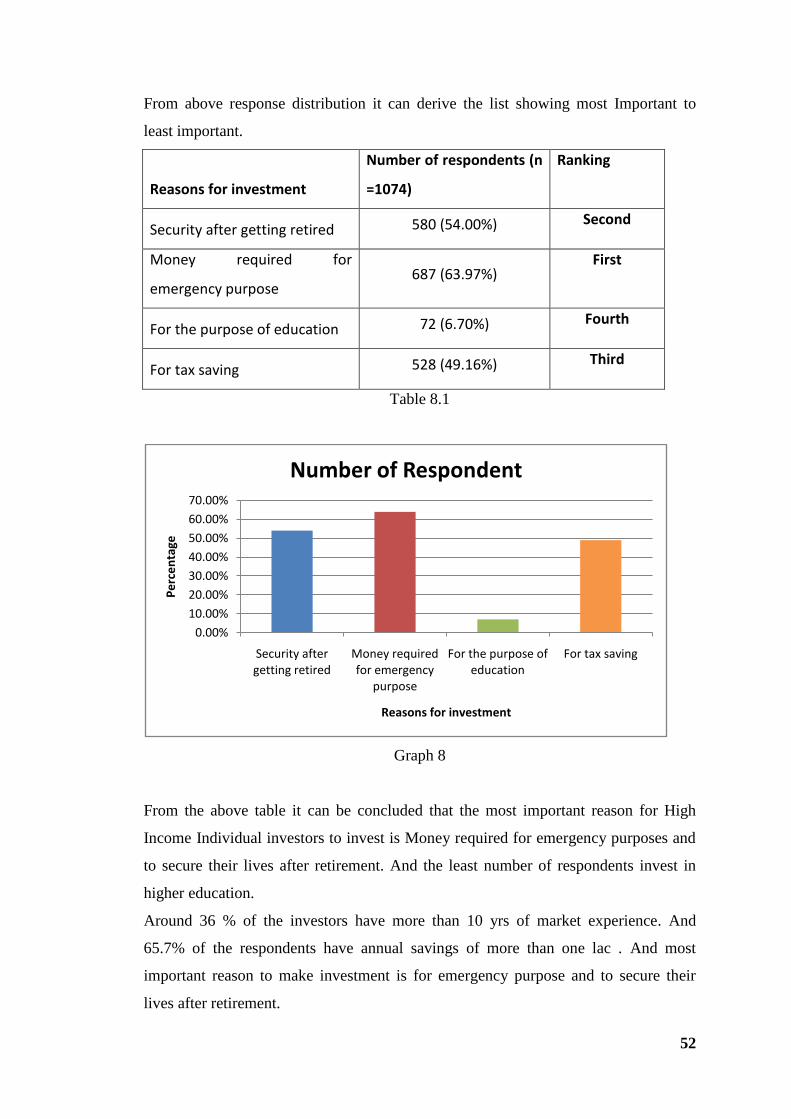

8 Percentage wise Reasons for investment 51

8.1 Rank wise Reason for investment 52

9 Test of Normality for Investment options 54

9.1 Average Investment in Different financial assets 55

10 Rank Table of average Investment in Different financial

assets

56

11 Size of Investment in Equity Instruments 58

12 Age wise comparison with Investment 60

12.1 Rank Table of Age wise comparison with Investment 61

13 Education wise comparison with Investment 63

13.1 Rank Table of Education wise comparison with

Investment

64

14 Annual Income wise comparison with Investment 65

14.1 Rank Table of Annual Income wise comparison with

Investment

66

15 Gender-wise comparison with Investment 67

15.1 Rank Table of Gender-wise comparison with Investment 67

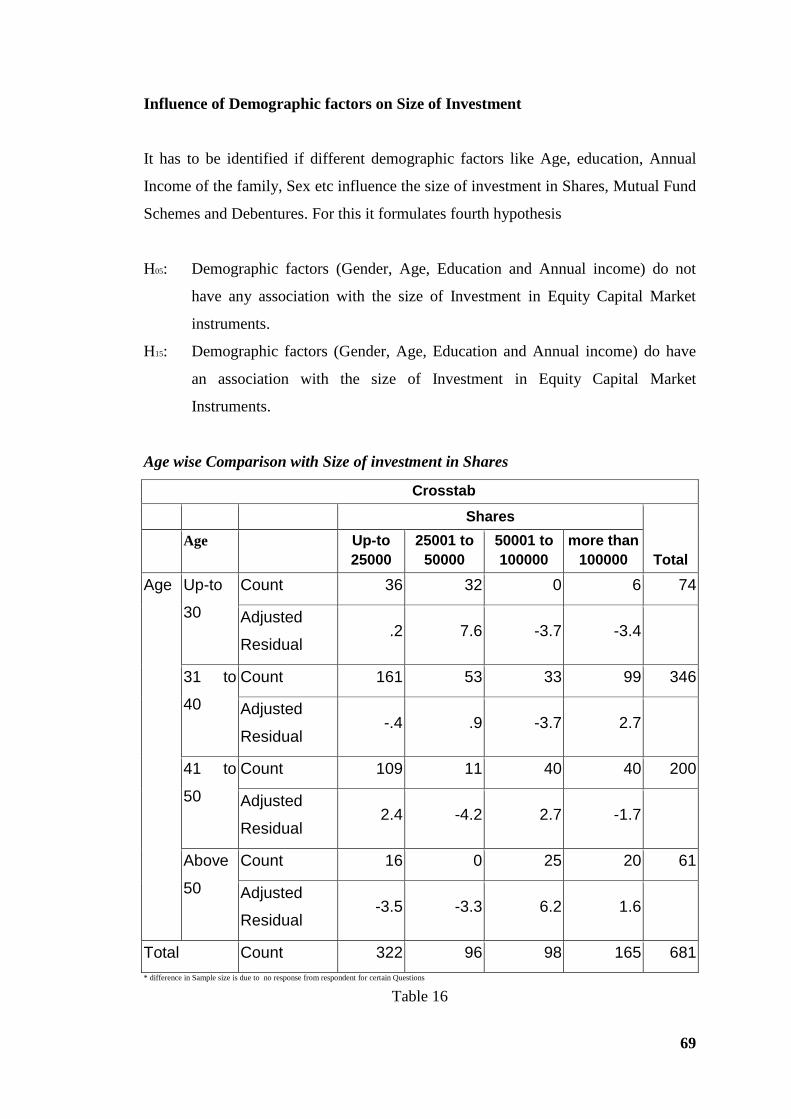

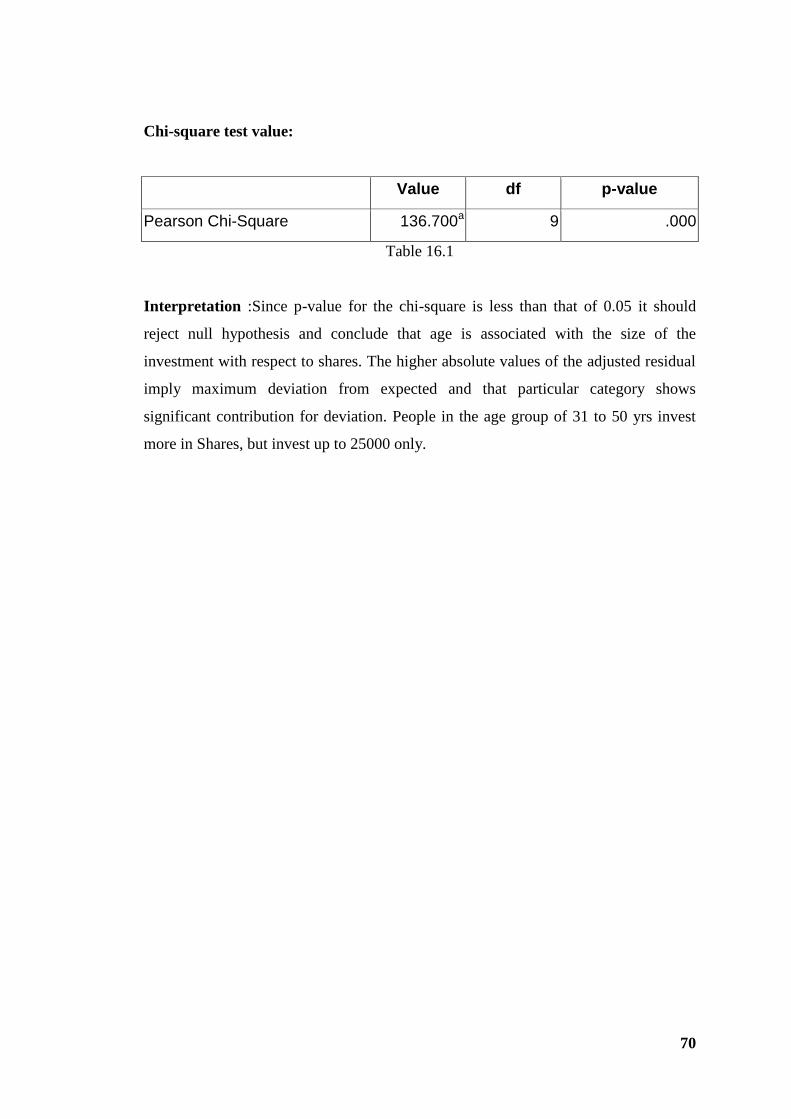

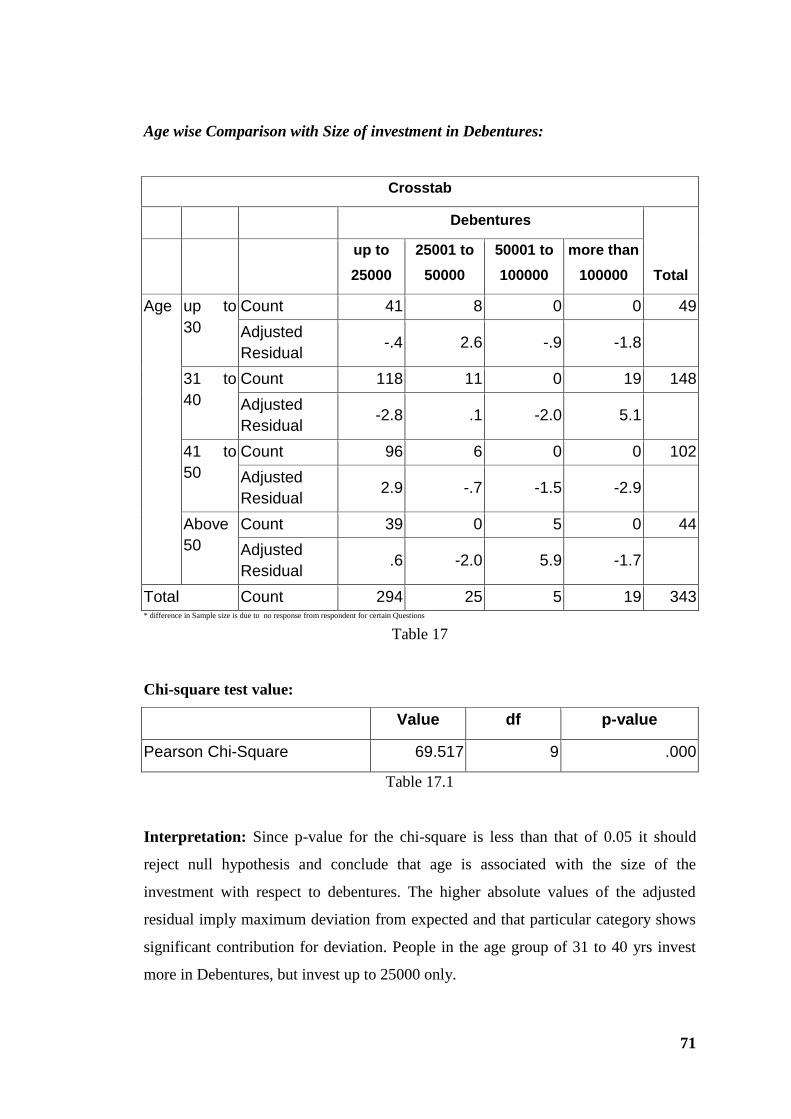

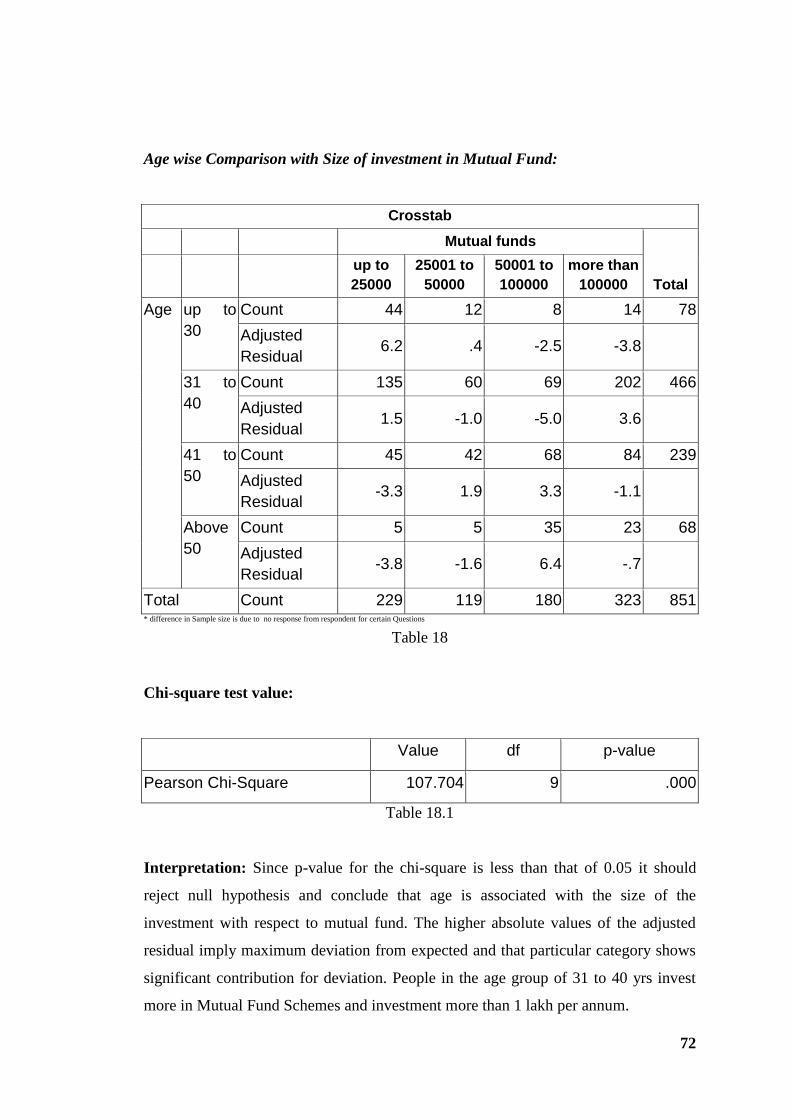

16 Age wise Comparison with Size of investment in Shares

69

17 Age wise Comparison with Size of investment in

Debentures

71

18 Age wise Comparison with Size of investment in Mutual

Funds

72

19 Gender wise Comparison with Size of investment in

Shares

73

20 Gender wise Comparison with Size of investment in

Debentures

74

21 Gender wise Comparison with Size of investment in

Mutual Funds

75

22 Education wise Comparison with Size of investment in

Shares

76

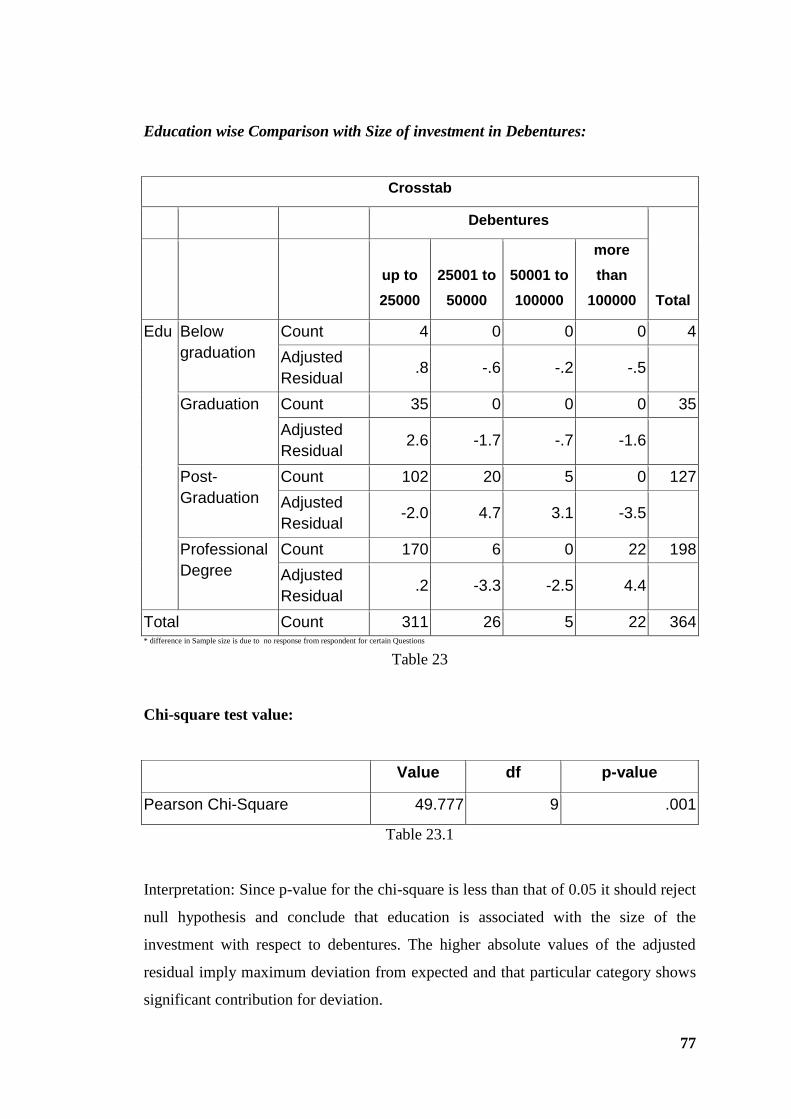

23 Education wise Comparison with Size of investment in

Debentures

77

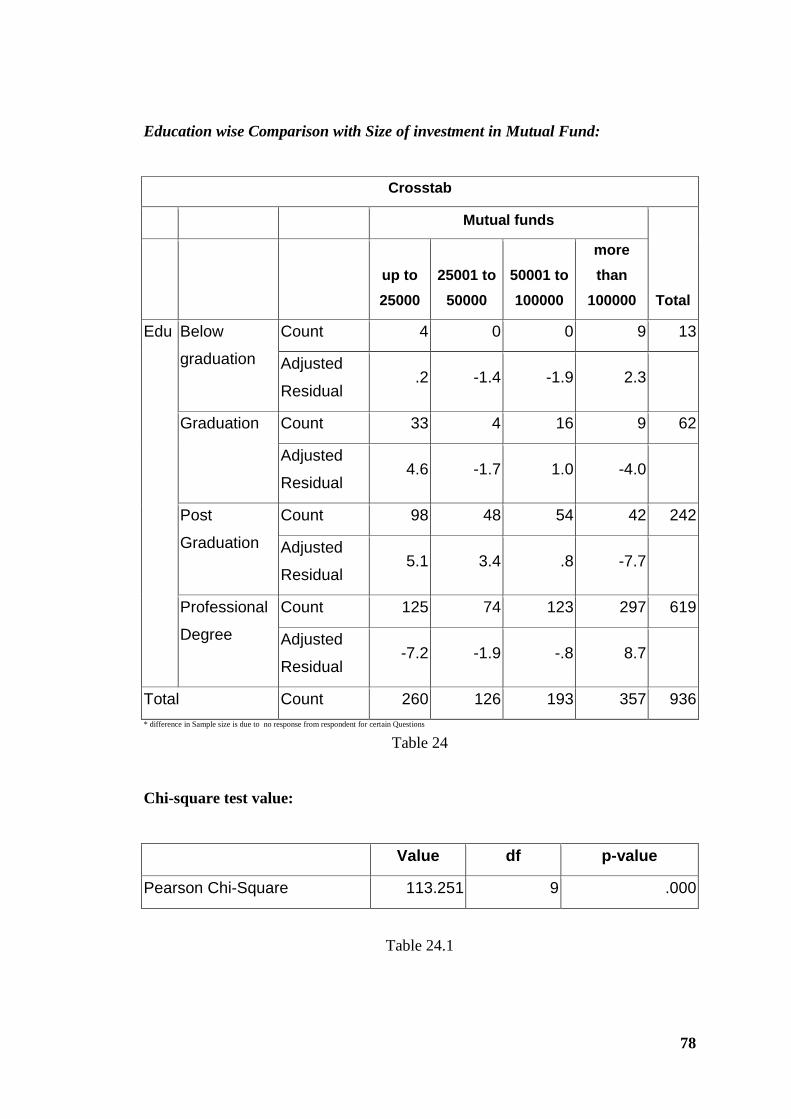

24 Education wise Comparison with Size of investment in

Mutual Funds

78

25 Annual Income wise Comparison with Size of investment

in Shares

80

26 Annual Income wise Comparison with Size of investment

in Debentures

81

27 Annual Income wise Comparison with Size of investment

in Mutual Funds

82

28 Mean Preferences with respect to Mutual Fund Schemes

84

28.1 Actual Mean of Preferences 85

29 Sector wise investment in Shares 87

29.2 Mean rank table of Sector wise Investment Preferences in

Shares

88

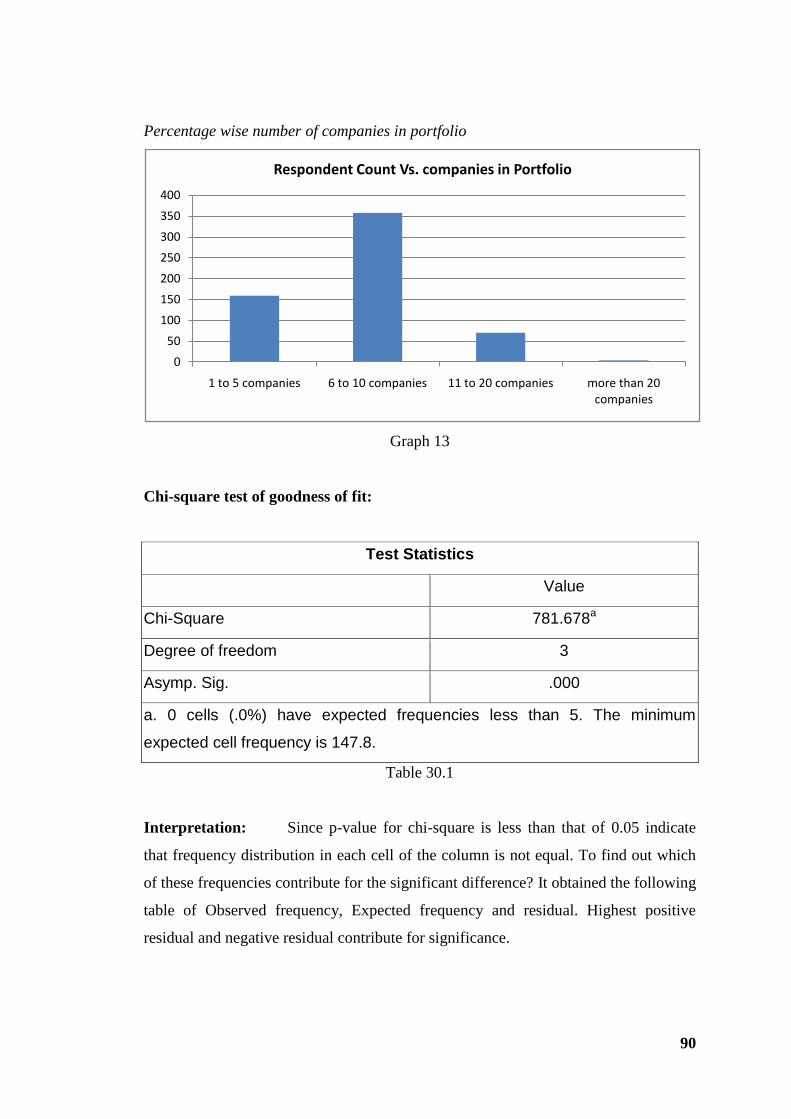

30 Percentage wise number of companies in portfolio 89

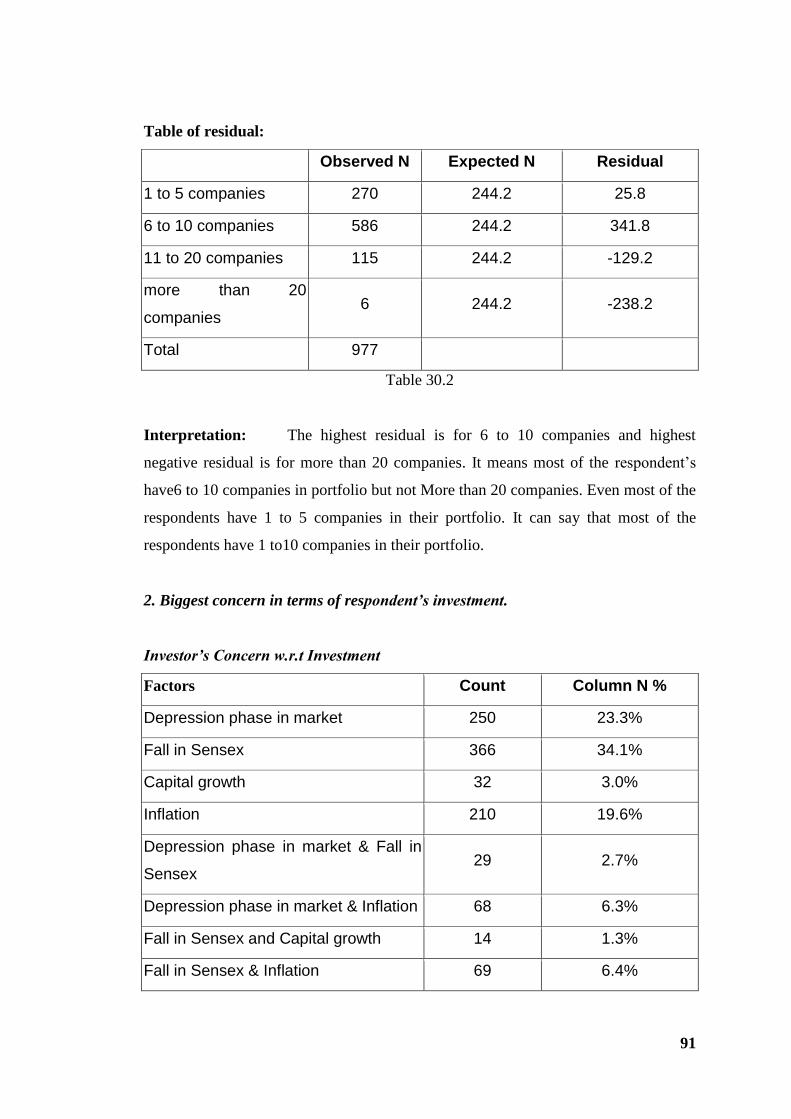

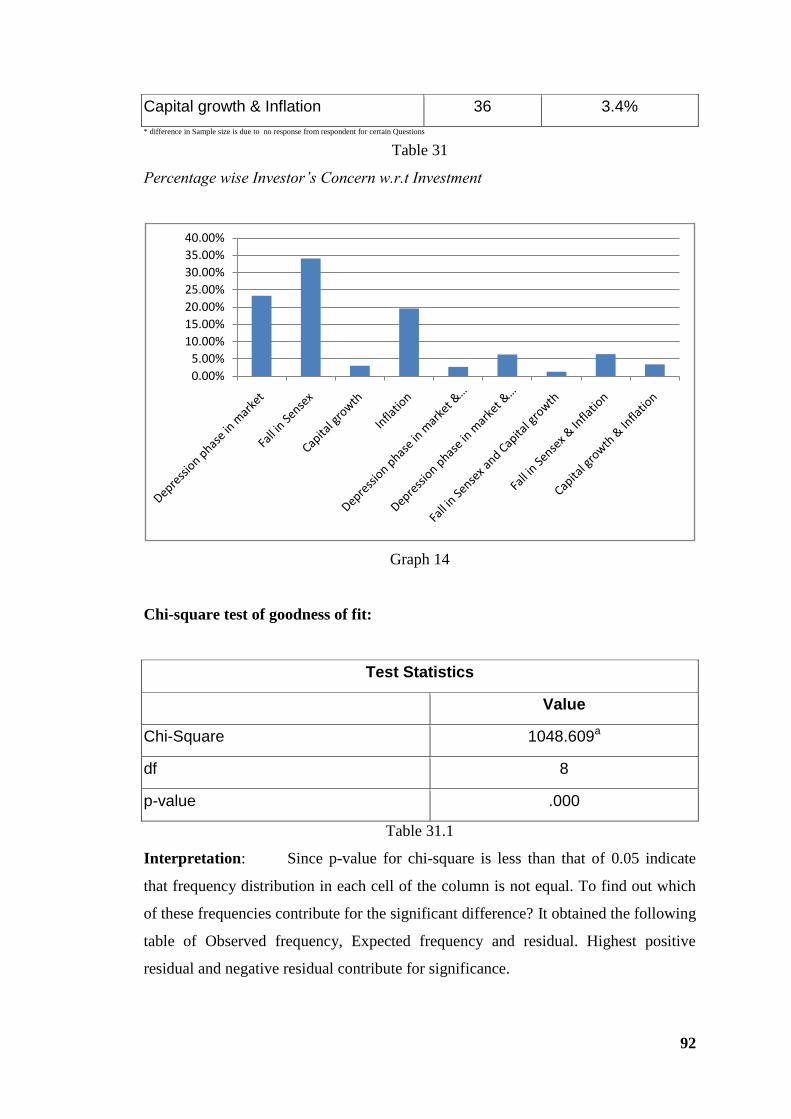

31 Investor’s Concern w.r.t Investment 91

31.2 Table of residual for Investor’s Concern w.r.t investment 93

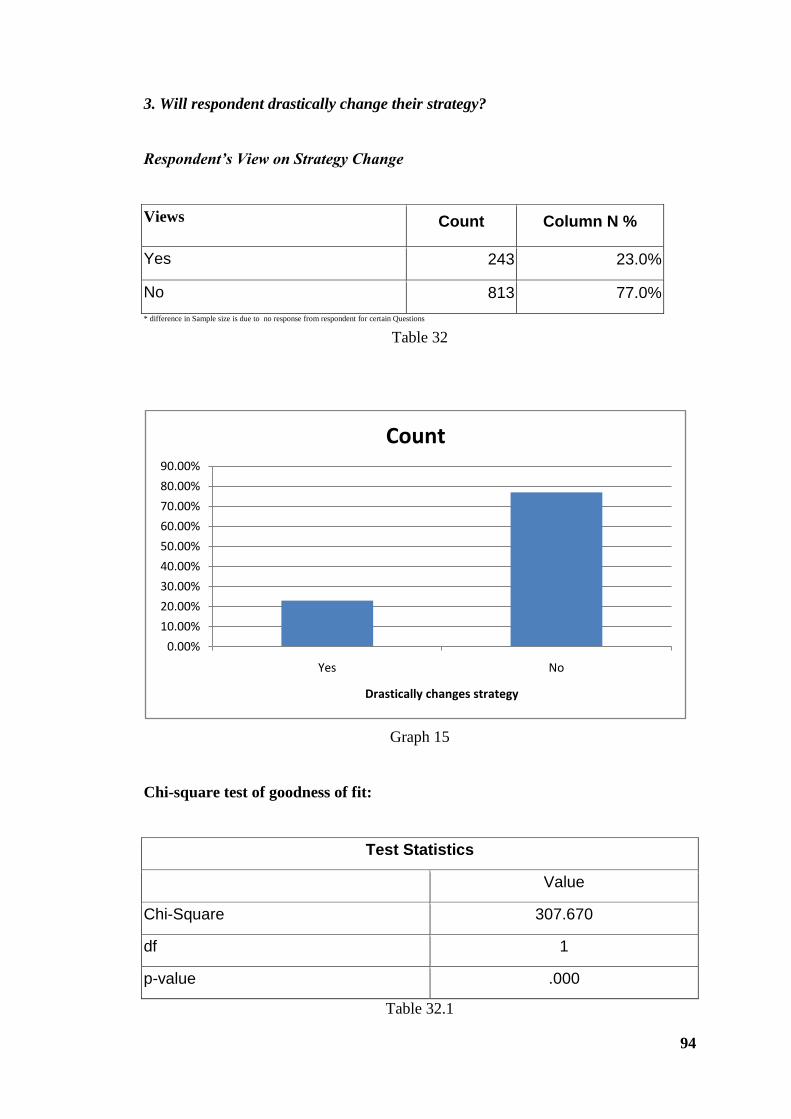

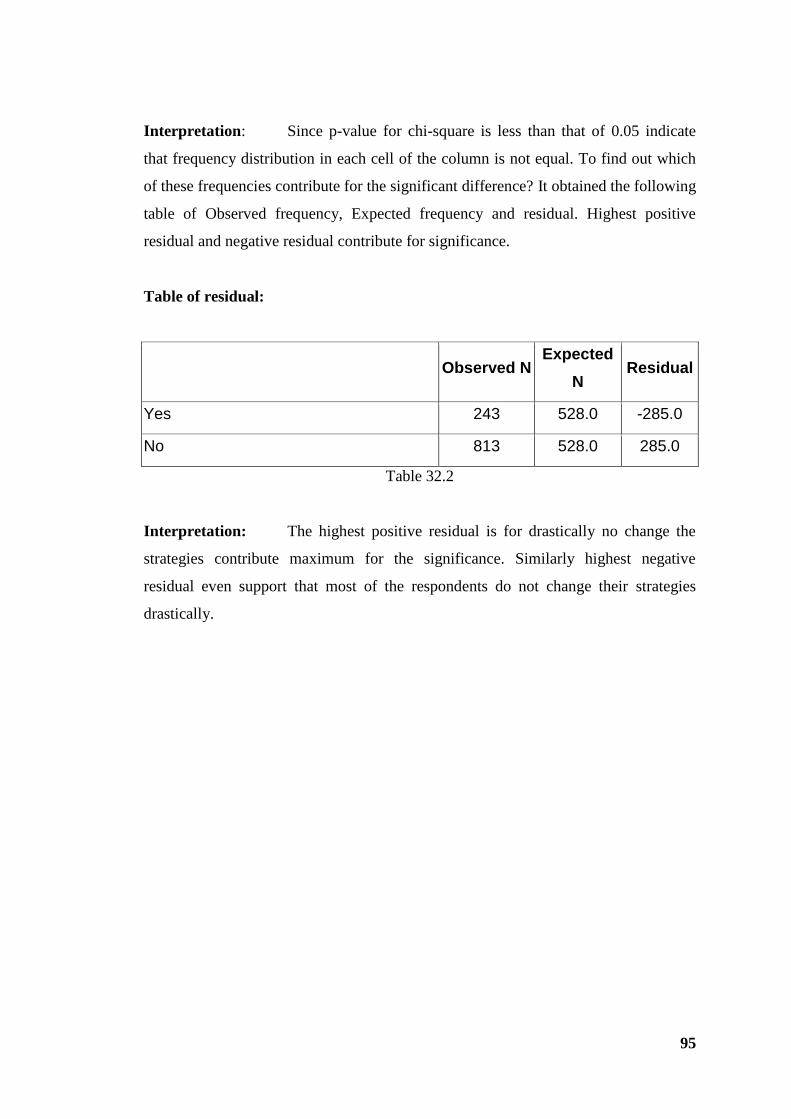

32 Respondent’s View on Strategy Change 94

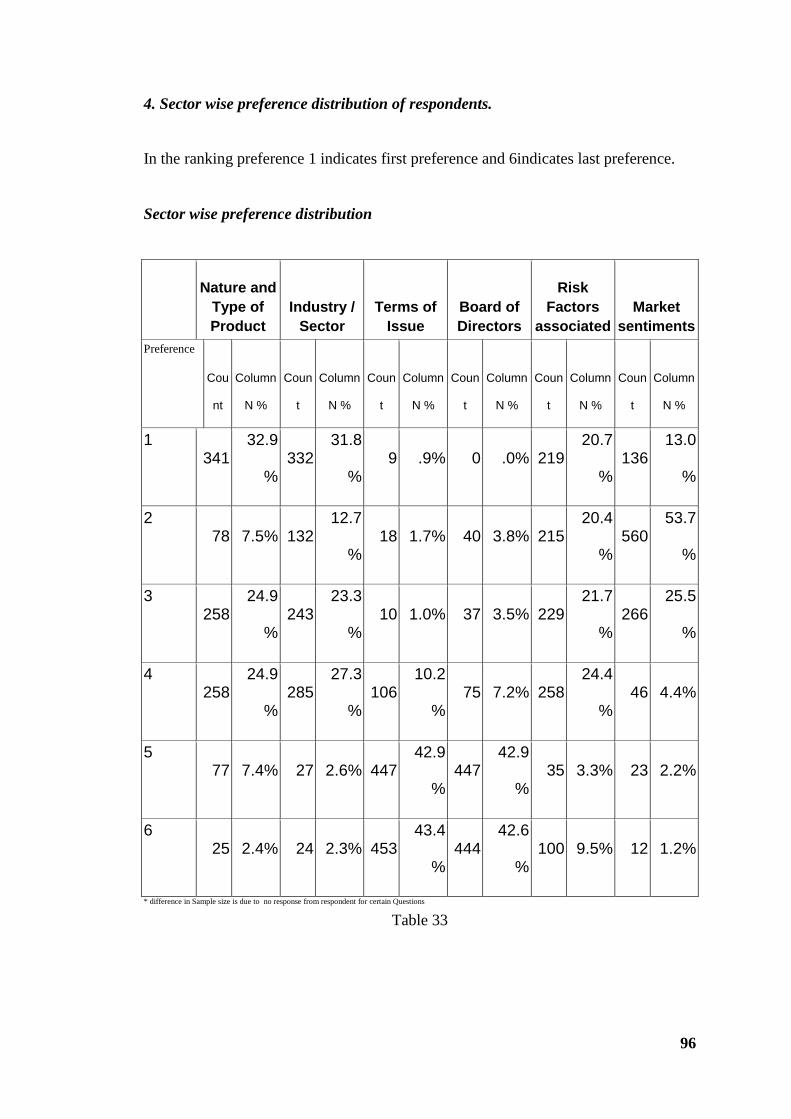

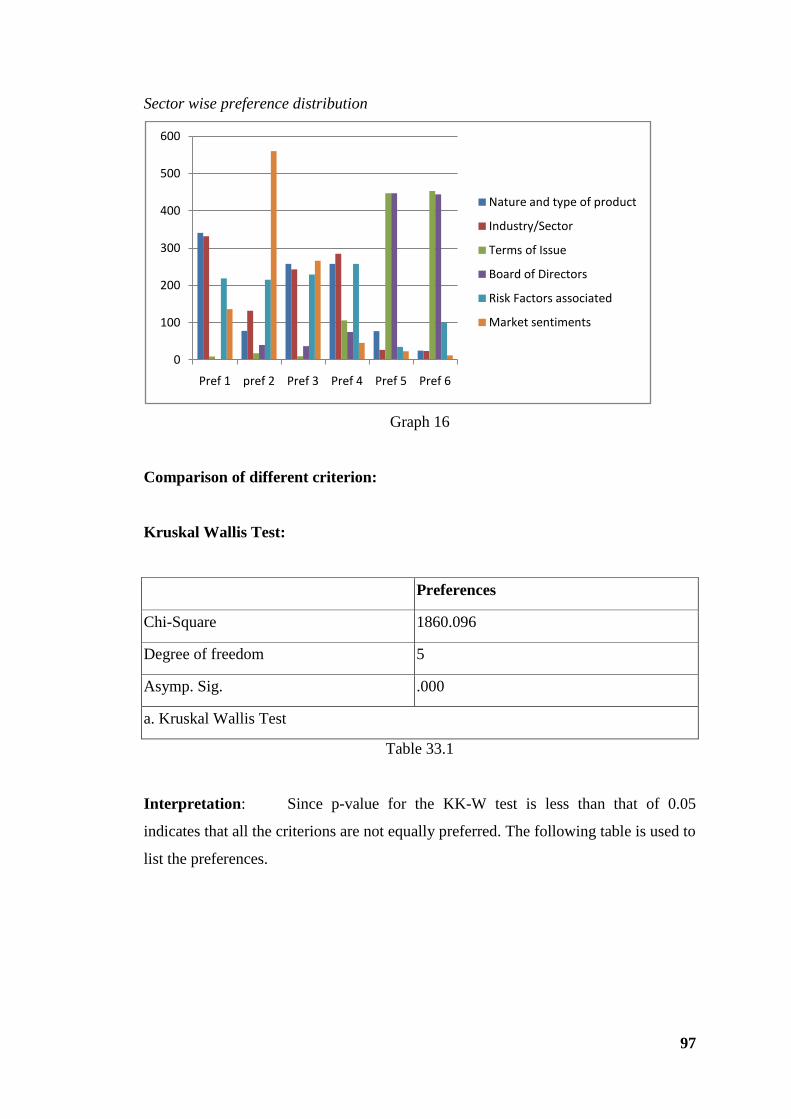

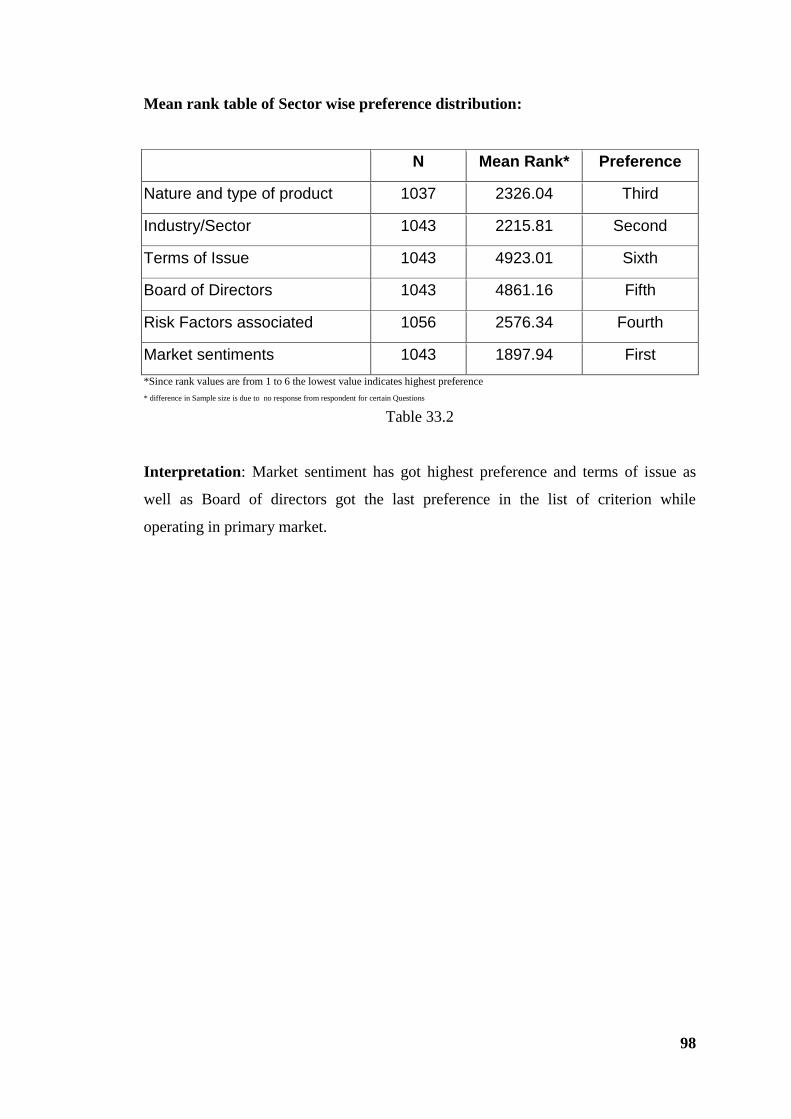

33 Sector wise preference distribution 96

33.2 Mean rank table of Sector wise preference distribution 98

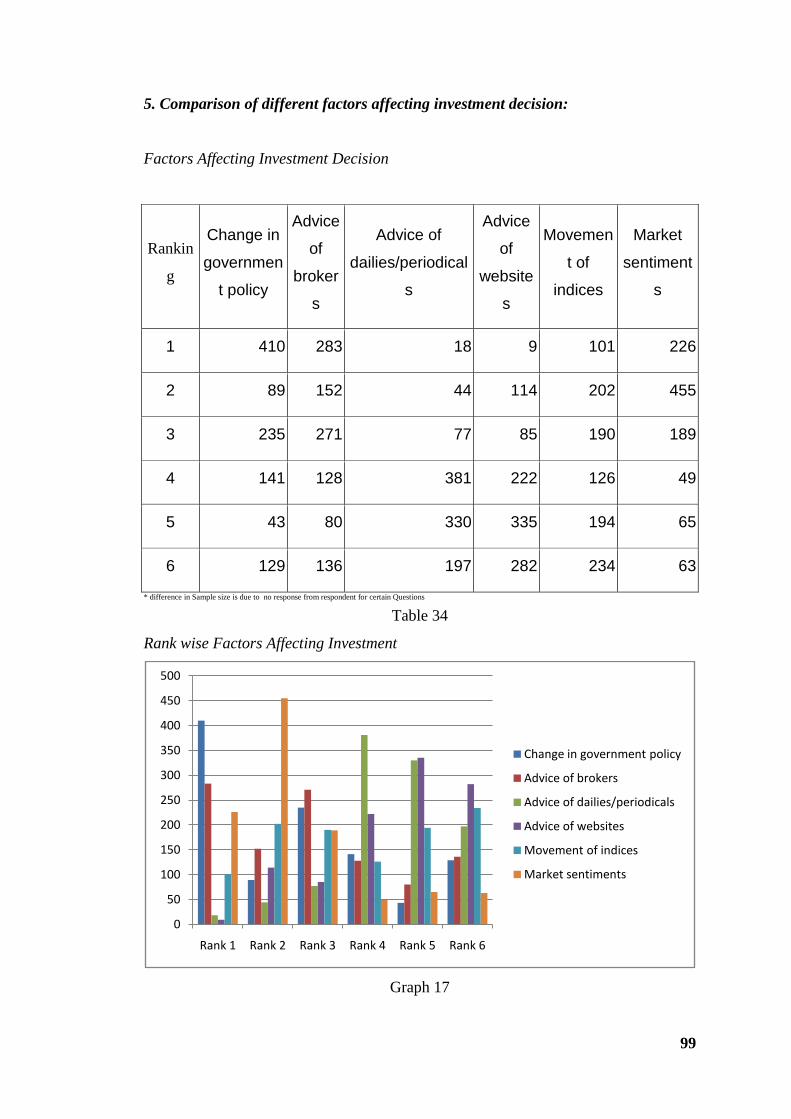

34 Factors Affecting Investment Decision 99

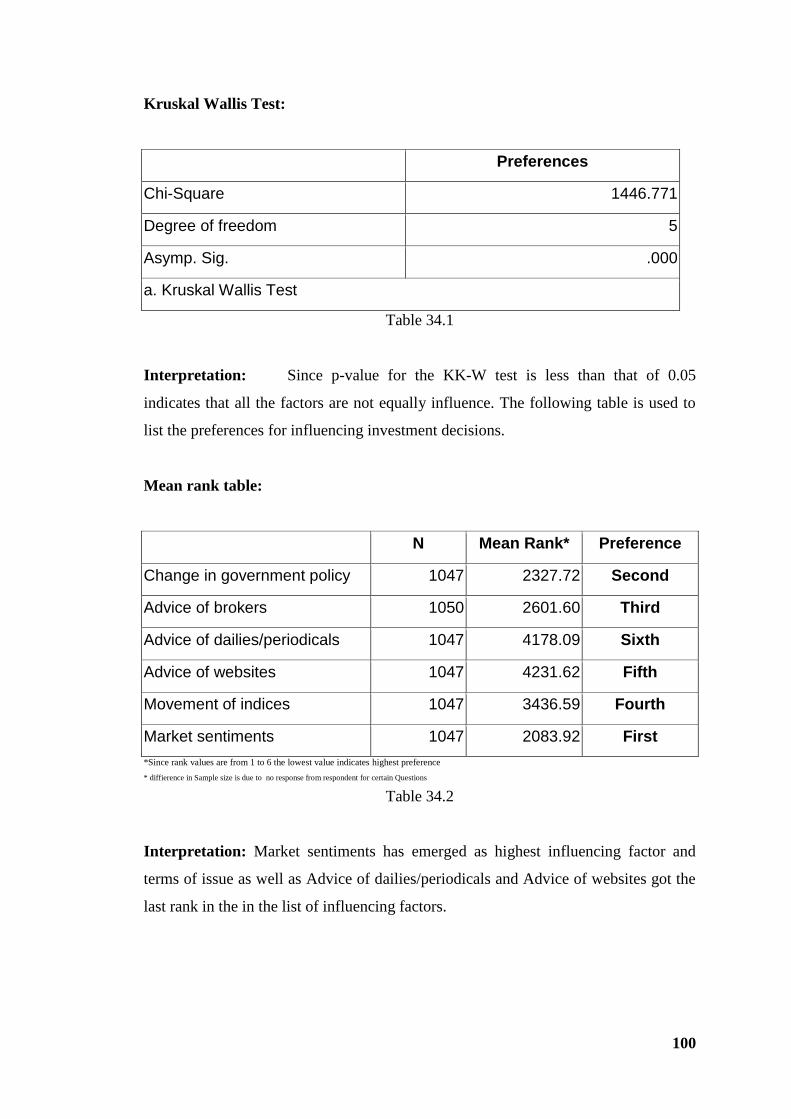

34.2 Mean rank table of Factors Affecting Investment Decision 100

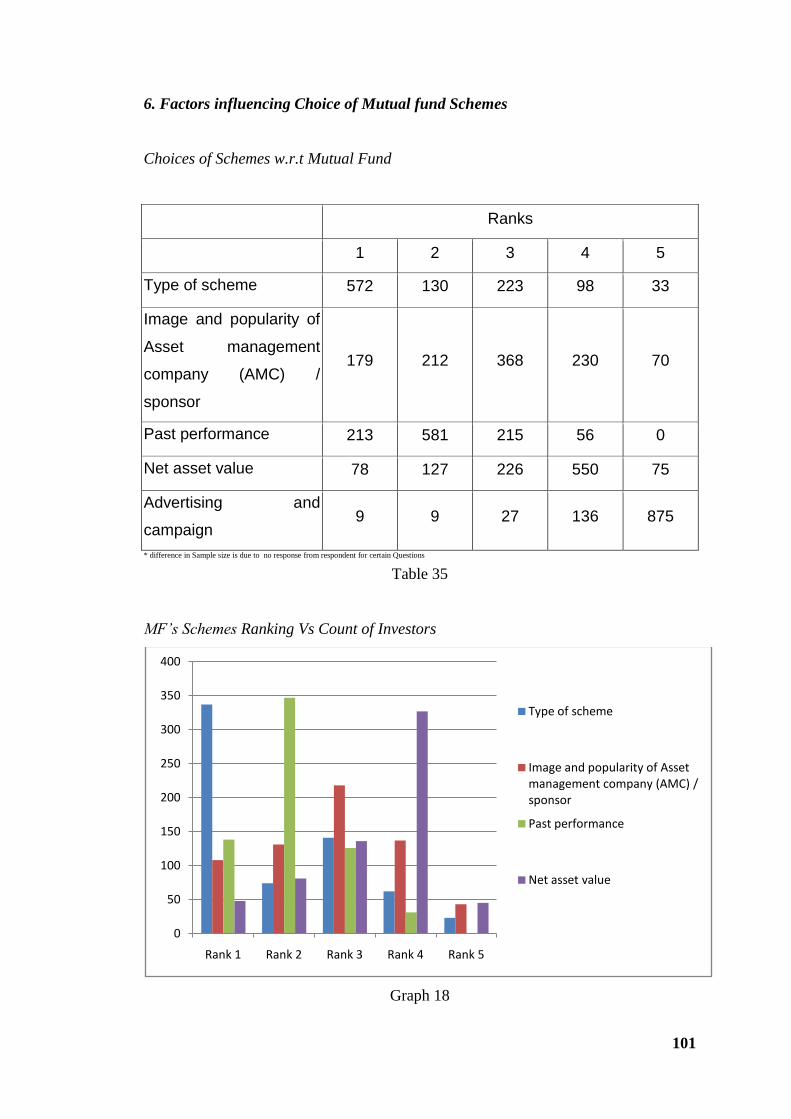

35 Choices of Schemes w.r.t Mutual Fund 101

LIST OF GRAPHS

Graph No. List Of Graph Page No.

1 Age wise Distribution of respondents 43

2 Gender wise Distribution of respondents 44

3 Marital Status wise Distribution of respondents 45

4 Education wise Distribution of respondents 46

5 Annual Income wise Distribution of respondents 47

6 Annual Saving wise Distribution of respondents 48

7 Market Experince wise Distribution of respondents 49

8 Percentage wise Reasons for investment 52

9 Average Investment in Different financial assets 55

10 Rank wise distribution of average Investment in

Different financial assets

56

11 Mean Investment Vs Investment Preferences in MF 86

12 Sector wise Investment Preferences in Shares 87

13 Respondent Count Vs. companies in Portfolio 90

14 Percentage wise Investor’s Concern w.r.t

Investment

92

15 Respondent’s View on Strategy Change 94

16 Sector wise preference distribution 97

17 Rank wise Factors Affecting Investment 99

18 MF’s Schemes Ranking Vs Count of Investors 101

EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

Capital Market is a one of the significant aspect of any financial market. Individual

investors represent a vital element for the functioning of capital market. But In India,

though the saving rate is high, barely two percent of these savings goes into financial

markets. With the rise in income, consumption patterns have changed and a new High

class has emerged, which is growing at a fast pace. There are large numbers of

investment opportunities available today. In this research work, it is going to briefly

examine how the High Income Group Individual Investor in Mumbai and Pune

manage their investments- their investment behaviour, their perception on investment

and if there exists a trend in their investment decisions. The study has been done to

find out the factors influencing their decisions on the Choice, Level and Size of

investment in different financial instruments in Capital Market. The study is based on

primary sources of data which are collected by distribution of a close ended

questionnaire. The data has been analyzed using percentage and chi-square test with

the help of statistical software. The results highlight that certain factors like education

level, awareness about the current financial system, age of investors etc... make

significant impact while deciding the investment avenues and there exists a trend in

the pattern of investment. Our descriptive analyses sheds new light on the links

between income and investments.

A well-organized and regulated capital market facilitates sustainable development of

the economy by providing long-term funds in exchange of financial assets to

investors. Investment is the employment of funds on assets with the aim of earning

income or capital appreciation. Investment is the most important things today. In spite

of such widespread interest of Indian investors in shares, investment knowledge is

very much lacking in them. This is evident from the fact that most of them usually get

attracted towards the stock exchanges like moths to a candle in periods of boom and

rising prices in a bid to become rich quickly. A proper understanding of money, its

value, the available avenues for investment, various financial institutions, the rate of

return/risk etc., are essential to successfully manage one’s finance for achieving life’s

goal. What are the fundamentals? And risk/return equations? And if investors are

ready to invest, how do they access the investments? Are there are restrictions or

disincentives that change the risk/return equation for the investors? These are some of

the questions that have been attempted to answer through this study. Actually, the

present research identifies the preferred investment avenues among the High Income

individual investors in Mumbai and Pune .

It is conferred that the most important reason for High Income Individual investors to

invest is Money required for emergency purposes and to secure their lives after

retirement. It is observe that there exists significant difference in the average

investment in different financial assets. Since Bank deposit, bond and other debt

options, provident fund and equity capital market options has resulted as prominent

option for investment. Bank, IT and Auto sector in shares is the most preferred sector

of investment. Most of the respondents have 6 to 10 companies in their portfolio. It

may conclude that people with Professional Degrees or Post graduation degrees have

a better understanding and willingness to invest in Capital Market Instruments.

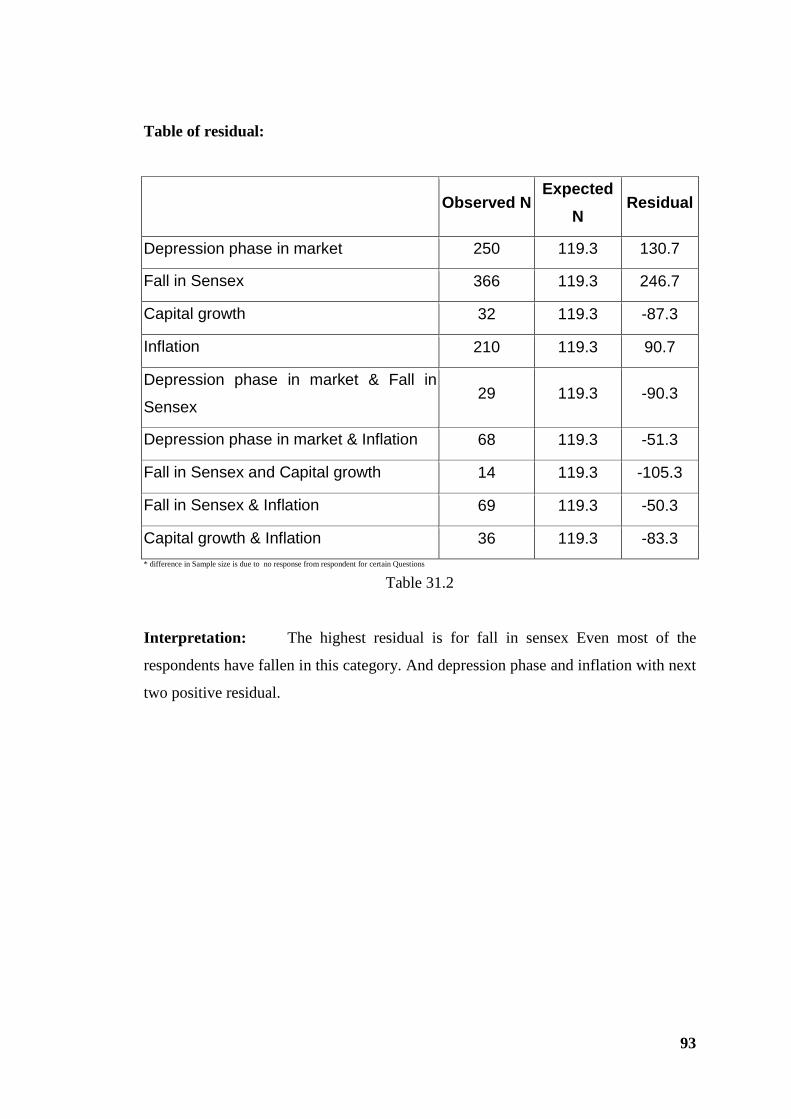

Biggest concern in terms of respondent’s investment is for “Fall in sensex” Even most

of the respondents have fall in the category of “depression phase” and “inflation” with

next two positive residual.

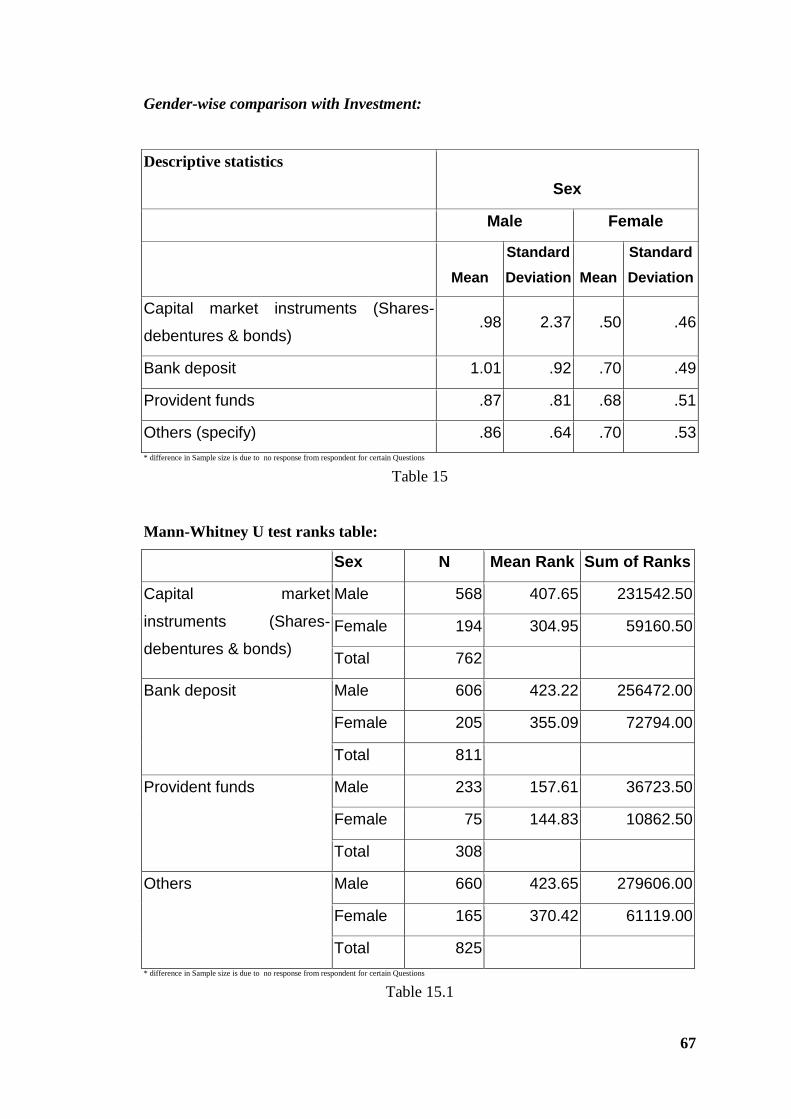

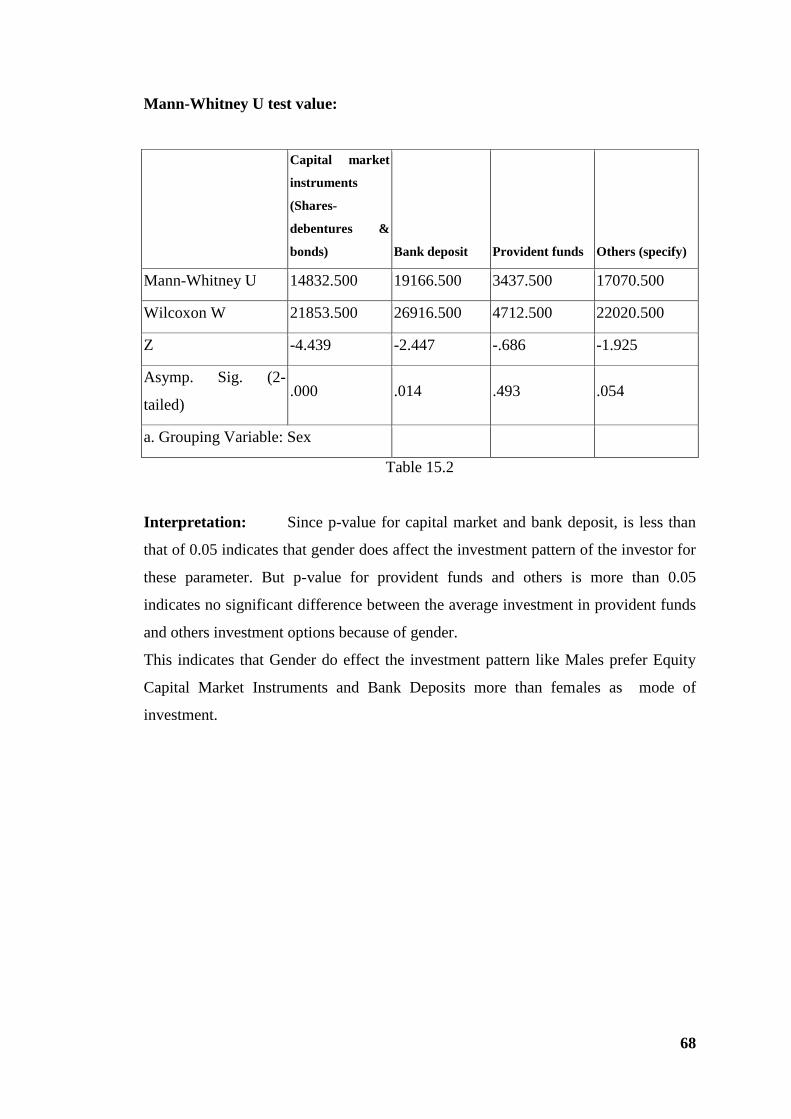

Study indicates that Gender do effect the investment pattern like Males prefer Equity

Capital Market Instruments and Bank Deposits more than females as mode of

investment. Male population invest more than females in Shares. The Major concern

in terms of investment is Depressing phase in the market, risk associated with fall in

sensex and rising inflation. The most important criterion considered while operating

in Equity Market is Market Sentiments and the industry, Nature and type of Product.

Among the various capital market instruments available, Mutual Funds Schemes are

the most preferred instruments among investors followed by Shares and debentures.

Majority of investors have an experience of more than three years in capital market

investment.

The study indicates that majority of retail investors are investing major portion of

their savings in non-capital market instruments. The overall experience of investors

on capital market investment is that it is rewarding to majority of investors. Investors

mainly suggested the extension of more powers to SEBI on investor protection with a

view to improving capital market operations.

1

CHAPTER 1

INTRODUCTION

Indian Capital Market

Capital Market is a one of the significant aspect of any financial market. It is a market

for financial assets which has long or indefinite maturity. It is an institutional

arrangement for borrowing and lending money for a long period of time. Capital

markets involve various instruments which can be used for financial transactions.

Financial institutions like UTI, IDBI, ICICI, LIC etc play the role of lenders in the

capital markets. Business units and corporate are the borrowers in the capital market.

In short it can be said that Capital Markets are the financial market in which long term

debt and equity are traded. Capital markets acts as a means through which scattered

saving of investors are directed into productive activities of corporate entities.

Behavior of Indian capital Market, specially, stock market is always interesting,

challenging and if one understands it, it becomes pleasantly rewarding.

The history of the capital market in India dates back to the eighteenth century when

East India Company securities were traded in the country. Until the end of the

nineteenth century securities trading was unorganized and the main trading centers

were Bombay (now Mumbai) and Calcutta (now Kolkata). The Bombay Stock

Exchange was inaugurated in 1899 when the brokers formally established a stock

market in India. Thus, the Stock Exchange at Bombay was consolidated. After that

more & more stock exchanges have emerged in India & this forms a huge capital

market in India.

The 1990s witnessed the emergence of the securities market as a major source of

finance for trade and industry. Equity markets provided the required platform for

companies and start-up businesses to raise money through IPOs, VC, PE, and finance

from HNIs. As a result, stock markets became a people‘s market, flooded with

primary issues. In the first 11 months of 2007, the new capital raised in the global

public equity markets through IPOs accounted for $107 billion in 382 deals out of the

total of $255 billion raised by the four BRIC countries. This was a sizeable growth

2

from $90 billion raised in 302 deals in 2006. Today, the corporate sector prefers

external sources for meeting its funding requirements rather than acquiring loans from

financial institutions or banks.

With the onset of globalization and the subsequent policy reforms, significant

improvements have been made in the area of securities market in India.

Dematerialization of shares was one of the revolutionary steps that the government

implemented. This led to faster and cheaper transactions, and increased the volumes

traded by many folds. The adoption of the market-oriented economic policies and

online trading facility transformed Indian equity markets from a broker-regulated

market to a mass market. This boosted the sentiment of investors in and outside India

and elevated the Indian equity markets to the standards of the major global equity

markets.

Since 2003, Indian capital markets have been receiving global attention especially

from sound investors, due to the improving macroeconomic fundamentals. The

emergence of Indian Capital Market as an attractive avenue for international investors

has been financial story of recent times. The entry of world players has revolutionized

Indian markets, largely for the better. But In India, though the saving rate is high,

barely two percent of these savings goes into financial markets. Investors investing a

portion of their savings in equity are marginal compared to traditional investments

like banks, insurance and others. Indian Capital Market has transformed, regulated

capital market facilities and developed a world class services which are more

transparent and has been developed to gain the confidence of individual investors to

invest in various capital market instruments like shares, debentures and mutual funds.

Broad Constituents in the Indian Capital Markets

Fund Raisers are companies that raise funds from domestic and foreign sources, both

public and private. The following sources help companies raise funds.

Fund Providers are the entities that invest in the capital markets. These can be

categorized as domestic and foreign investors, institutional and retail investors. The

list includes subscribers to primary market issues, investors who buy in the secondary

3

market, traders, speculators, FIIs/ sub accounts, mutual funds, venture capital funds,

NRIs, ADR/GDR investors, etc.

Intermediaries are service providers in the market, including stock brokers, sub-

brokers, financiers, merchant bankers, underwriters, depository participants, registrar

and transfer agents, FIIs/ sub accounts, mutual Funds, venture capital funds, portfolio

managers, custodians, etc.

Organizations include various entities such as BSE, NSE, other regional stock

exchanges, and the two depositories National Securities Depository Limited (NSDL)

and Central Securities Depository Limited (CSDL).

Market Regulators include the Securities and Exchange Board of India (SEBI), the

Reserve Bank of India (RBI), and the Department of Company Affairs (DCA).

Participants in the Securities Market SAT, regulators (SEBI, RBI, DCA, DEA),

depositories, stock exchanges (with equity trading, debt market segment, derivative

trading), brokers, corporate brokers, sub-brokers, FIIs, portfolio managers, custodians,

share transfer agents, primary dealers, merchant bankers, bankers to an issue,

debenture trustees, underwriters, venture capital funds, foreign venture capital

investors, mutual funds, collective investment schemes.

Concepts and Definitions

Individual Investor

Any individual employing his funds for personal investment in the capital market with

the objective of receiving future benefits and who takes the financial decisions of his

own. It includes a person who owns any capital market instrument through

inheritance.

Security

The term security means a capital market instrument, which may be a share,

debentures or mutual fund scheme.

4

Capital Market

Capital Market is a market for long term financial instruments consisting of shares,

debentures and mutual fund schemes. It covers both primary market and secondary

market.

Primary Market

Primary market is that segment of capital market where new financial instruments like

shares, debentures and mutual fund schemes are offered to investors for cash which

are issued at par, at premium or at discount. It includes initial public offering,

subsequent issues and private placement.

Secondary Market

Secondary market is that segment of capital market where existing instruments are

listed in the stock exchanges, which facilitate buying and selling of the securities. It

includes any off-market transactions entered through a stockbroker.

Equity Market

The Indian Equity Market is more popularly known as the Indian Stock Market. The

securities market is divided into two interdependent segments:

The primary market provides the channel for creation of funds through issuance of

new securities by companies, governments, or public institutions. In the case of new

stock issue, the sale is known as Initial Public Offering (IPO).

The secondary market is the financial market where previously issued securities and

financial instruments such as stocks, bonds, options, and futures are traded.

The Indian market has 22 stock exchanges. The larger companies are enlisted with

BSE and NSE. The smaller and medium companies are listed with OTCEI (Over The

counter Exchange of India)

Share

A share is a form of capital market instrument, which evidences fractional ownership

of a corporate body and includes both equity shares and preference shares held in

physical or electronic form.

5

Debenture

It is a credit instrument issued by a corporate body including a public sector

undertaking whether convertible into shares or not and which carries a fixed rate of

interest.

Derivative Markets

The emergence of the market for derivative products such as futures and forwards can

be traced back to the willingness of risk adverse economic agents to guard themselves

against uncertainties arising out of price fluctuations in various asset classes. This

instrument is used by all sections of businesses, such as corporate, SMEs, banks,

financial institutions, retail investors, etc. According to the International Swaps and

Derivatives Association, more than 90 percent of the global 500 corporations use

derivatives for hedging risks in interest rates, foreign exchange, and equities.

Three broad categories of participants—hedgers, speculators, and arbitragers—trade

in the derivatives market.

Hedgers

They face risk associated with the price of an asset. They belong to the business

community dealing with the underlying asset to a future instrument on a regular basis.

They use futures or options markets to reduce or eliminate this risk.

Speculators

They have a particular mindset with regard to an asset and bet on future movements in

the asset‘s price. Futures and options contracts can give them an extra leverage due to

margining system.

Arbitragers

They are in business to take advantage of a discrepancy between prices in two

different markets. For example, when they see the futures price of an asset getting out

of line with the cash price, they will take offsetting positions in the two markets to

lock in a profit.

6

Mutual Fund Market

The Mutual Fund industry in India started in 1963 with the formation of Unit Trust of

India, at the initiative of the Government of India and Reserve Bank of India. Mutual

funds perform a crucial task as efficient allocators of resources in such transition

period. The process of liberalization, deregulation and restructuring of the Indian

economy has further created the necessity for efficient allocation of resources. In this

process of development, mutual funds have emerged as strong financial

intermediaries and are playing an important role in bringing stability to the financial

system and efficiency to the resource allocation process. As at the end of September

2006, there were 34 funds, which manage assets of Rs.291206 crores under 609

schemes. Performance of Mutual Funds in India is measured through growth of

Assets Under management.

Mutual fund scheme

A mutual fund scheme is a capital market instrument, issued by a mutual fund

organization, whether open-ended or close-ended and includes any type of scheme.

Debt Market

Debt market refers to the financial market where investors buy and sell debt

securities, mostly in the form of bonds. These markets are important source of funds,

especially in a developing economy like India. India debt market is one of the largest

in Asia. The most distinguishing feature of the debt instruments of Indian debt market

is that the return is fixed. This means, returns are almost risk free. This fixed return on

the bond is often termed as the 'coupon rate' or the 'interest rate'. Therefore, the buyer

(of bond) is giving the seller a loan at a fixed interest rate, which equals to the coupon

rate. Debt Instruments: There are various types of debt instruments available that one

can find in Indian debt Market like Government Securities, Corporate Bonds,

Certificate of Deposit, Commercial Papers etc.

Private Placement

It is a method of primary market operations in which new financial instruments are

offered directly to investors on a private basis without complying with all legal

formalities including the issue of prospectus.

7

Risk on Investment

You can't plan financially without understanding investment risk. Many people, when

they hear about 'risk', think automatically about the chance of being defrauded or not

getting all their money back. This 'capital' risk is important, but it isn't the only type.

Other types of risk involve uncertainty and unpredictability. When you make an

investment, it can be difficult to say with any certainty what you'll get back when you

finally cash it in. Share prices fluctuate, interest rates vary and inflation is a risk too.

Just concentrating on capital risk and ignoring these other risks can mean you take too

cautious an approach. Understanding risk means identifying your own attitude

towards it and identifying the different types of risk. Then you can pick up tips for

minimising the chances of things going wrong.

Role of SEBI in Indian Capital Market

The Securities and Exchange Board of India (SEBI) was incorporated as an investor

protection body in 1992 by virtue of a special enactment, the SEBI Act, 1992. The

basic functions of SEBI are to protect the interest of investors in securities and to

promote the development of, and to regulate the securities market and for matters

connected therewith or incidental thereto‖. The SEBI Act came into force on 30th

January, 1992 and with its establishment, all public issues are governed by the rules &

regulations issued by SEBI. SEBI was formed to promote fair dealing in issue of

securities and to ensure that the capital markets function efficiently, transparently and

economically in the better interests of both the issuers and the investors.

The following functions have been entrusted to SEBI:

a) Regulating the business in stock exchanges and any other securities markets.

b) Registering and regulating the working of stockbrokers, sub-brokers, bankers

to issue, registrars to issue, merchant bankers, underwriters and such other

intermediaries who may be associated with securities markets in any manner.

c) Registering and regulating the working of collective investment schemes

including mutual funds.

d) Promoting and regulating self-regulatory organizations.

8

e) Prohibiting fraudulent and unfair trade practices relating to securities markets.

f) Promoting investors‘ education and training of intermediaries of securities

market.

g) Prohibiting insider trading in securities.

h) Regulating substantial acquisition of shares and takeover of companies.

i) Calling for information from, undertaking inspection, conducting inquiries and

audits of the stock exchanges, intermediaries and self regulatory organizations

in the securities market.

j) Conducting research for the above purposes.

k) Performing such other functions as may be prescribed.

Reforms in Capital Market of India

The major reform undertaken in capital market of India includes Establishment of

SEBI: The Securities and Exchange Board of India (SEBI) was established in 1988. It

got a legal status in 1992. SEBI was primarily set up to regulate the activities of the

merchant banks, to control the operations of mutual funds, to work as a promoter of

the stock exchange activities and to act as a regulatory authority of new issue

activities of companies.

Establishment of Creditors Rating Agencies:

Three creditors rating agencies viz. The Credit Rating Information Services of India

Limited (CRISIL -1988), the Investment Information and Credit Rating Agency of

India Limited (ICRA 1991) and Credit Analysis and Research Limited (CARE) were

set up in order to assess the financial health of different financial institutions and

agencies related to the stock market activities. It is a guide for the investors also in

evaluating the risk of their investments.

Increasing of Merchant Banking Activities:

Many Indian and foreign commercial bank shave set up their merchant banking

divisions in the last few years. These divisions provide financial services such as

underwriting facilities, issue organizing, consultancy services, etc.

9

Rising Electronic Transactions:

Due to technological development in the last few years. The physical transaction with

more paper work is reduced. It saves money, time and energy of investors. Thus it has

made investing safer and hassle free encouraging more people to join the capital

market.

Growing Mutual Fund Industry

The growing of mutual funds in India has certainly helped the capital market to grow.

Public sector banks, foreign banks, financial institutions and joint mutual funds

between the Indian and foreign firms have launched many new funds. A big

diversification in terms of schemes, maturity, etc. has taken place in mutual funds in

India. It has given a wide choice for the common investors to enter the capital market.

Growing Stock Exchanges:

The numbers of various Stock Exchanges in India are increasing. Initially the BSE

was the main exchange, but now after the setting up of the NSE and the OTCEI, stock

exchanges have spread across the country. Recently a new Interconnected Stock

Exchange of India has joined the existing stock exchanges.

Investor's Protection:

Under the purview of the SEBI the Central Government of India has set up the

Investors Education and Protection Fund (IEPF) in 2001. It works in educating and

guiding investors. It tries to protect the interest of the small investors from frauds and

malpractices in the capital market.

Growth of Derivative Transactions:

Since June 2000, the NSE has introduced the derivatives trading in the equities. In

November 2001 it also introduced the future and options transactions. These

innovative products have given variety for the investment leading to the expansion of

the capital market.

These reforms have resulted into the tremendous growth of Indian capital market.

10

Factors Affecting the Investors Preferences

The Investors‘ preferences are influenced by various factors. Investors ‗choice is

unique and is influenced by various factors. The major factors which influence their

choice of investment alternatives can be listed below:

i) Stage in Life Cycle: People investment preferences are influenced to some extent

by the stage of the life cycle they exist in. An investor being a bachelor and below the

age group of 30 may be ready to take high risk compared to the investor who is

married and having two grown up children. In most of the cases the stage in life cycle

is inversely related to the degree of investments made in risky assets.

ii) Life Style : Life style relates to the activities, interests and opinions. People‘s life

style undoubtedly affects their investment choices.

iii) Income: Income is another important factor which influences the investors‘

choices. The Low Income individuals are expected to take higher risk to get more

income when compared to the high-income individuals.

iv) Household Size: Household size is another variable that may have an impact on

the investors‘ choices. Investors with many dependents adopt a conservative

investment policy. Smaller the size of the household, higher will be the disposable

income available for investment and consequently the choices of risky investment

alternatives.

v) Personality Characteristics: An individual‘s personality is usually described in

terms of traits that influence behavior. The market practices reveal that compulsive

people invest differently from cautious investors. The investment choices of introverts

are quite different from the investment choices of gregarious people.

vi) Market Condition: The market condition also plays a considerable role in

influencing the investment choices of the investors. The Boom in the capital market

pulls the investors towards the risky investments. The changes in the interest rates

also influence the asset selection decision of the investor.

11

vii) Commodity Trading: Along with the trading of ordinary securities, the trading in

commodities is also recently encouraged. The Multi Commodity Exchange (MCX) is

set up. The volume of such transactions is growing at a splendid rate.

Need For the Study

The individual investors numbering millions constitute the backbone of Indian capital

market. Any developing economy like India needs a growing amount of investor

savings to flow to the corporate world to mobilize sufficient funds required for

development and ensures continuous liquidity in the capital market.

Investment is the employment of funds on assets with the aim of earning income or

capital appreciation. Investment is the most important things today. The real

household disposable income has more than doubled since 1985. A proper

understanding of money, its value, the available avenues for investment, various

financial institutions, the rate of return/risk etc., are essential to successfully manage

one‘s finance for achieving life‘s goal. What drives High Income Group investors to

use different investment options available and what could be the motivators- reasons

for saving money/making long term investments, sources of information/key

Influencers , Financial investment options aware of, performance of industry and

economy, income and risk factors, play a significant role while selecting different

products of Capital Market, as it can create an opportunity for one product and may

not for other. Analyzing the impact of income and risk on investment pattern of

investment provide the valuable insight.

You can't plan financially without understanding investment risk. Many people, when

they hear about 'risk', think automatically about the chance of being defrauded or not

getting all their money back. This 'capital' risk is important, but it isn't the only type.

Other types of risk involve uncertainty and unpredictability. When you make an

investment, it can be difficult to say with any certainty what you'll get back when you

finally cash it in. Share prices fluctuate, interest rates vary and inflation is a risk too.

Just concentrating on capital risk and ignoring these other risks can mean you take too

cautious an approach.

12

Understanding risk means identifying your own attitude towards it and identifying the

different types of risk. Then you can pick up tips for minimising the chances of things

going wrong.

In this context the present study is planned to study High Income Individual investor‘s

preferences in terms of investment with respect to risk in capital Market instruments

in Mumbai and Pune Region.

13

CHAPTER 2

REVIEW OF LITERATURE

The behavior of investors in the capital market is influenced by various factors. Many

scholars have made studies on investor‘s behavior, investment patterns and

perceptions on Capital Market, and still many studies are going on. Researchers have

done extensive study to identify the factors which influence the participation of

investors in capital markets. Some literature covering different aspects of investment

with investor‘s perception is attempted here.

G. Manju (2012) carried out a study to analyze the level of satisfaction among

investors and the problems faced by investors in Indian stock market. The study

confirms the relationship between savings, status, marital status and gender of the

investors. And the researcher also affirms that investors need to be educated about

investment and options available in the market. The factors according to ranking by

investors refrains the investors from investing in capital markets are- High

Commissions, Wrong information from agents , uncertainty of returns, market

volatility and Lack of rules and regulatory agents.

Mahabaleswara Bhatta H.S. (2009) made an attempt to throw light on the investors‘

biases that influence decision making process. The researcher opined that the studies

on the unpredictable human behavior would help the investors to critically inspect

their investing decisions.

FatenZoghlemi and Hamadi Matoussi( 2009), carried out a study to identify the

psychological biases that influence the Tunisian investor‘s behavior. Following are

the relevant findings of the study:-The overconfident tendency seems not to be

popular among the Tunisian investors. The Tunisian investors seem to be under

optimistic and very risk averse. The Tunisian investors seem to be very sensitive to

rumors. Majority of the Tunisian investors (81%)are conservative, they seem to

conserve so long the past data and past evidence and continue to react according to

them ignoring the current data and Mast of the Tunisian investors (61%) emit

progressive reactions to news and they don‘t react fully and instantly to current news.

14

The average propensity to save shows that the level of savings is related to the level of

income L.C.Prasad (2008) conducted a survey to find out the preferences of

household investors and the relevant findings of the study are as follows, a. The

household investors most preferred type of investment was found to be shares.

Systematic Investment plan (SIP) is the most popular type of scheme among various

types of mutual funds. The too much price fluctuations were found to be the major

worry of the investors in the stock market.

Jasim Y. Al-Ajmi (2008) explores the relationship between risk tolerance and

demographic characteristics of investors. The study was conducted to investigate the

effect of Gender, Education, Age and Wealth of the investors on the risk tolerance

level .Major findings were as follows:-1) Men are more risk tolerant than Men are less

risk averse than women 2) Less educated investors are less likely to take risk. 3)The

effect of age on risk tolerance is complex 4) Wealthy investors the less wealthy

investors.

Kannadasan M (2006), analysed the behavioral pattern of the retail Investors, based

on various dependent variables viz., Age, Gender, Marital Status, Educational Level,

income Level, awareness, preference and Risk bearing capacity. The following are the

major findings of the study:- 1) Only 25percent of the sample respondents were

aware at all the investment avenues available in the capital Market. However all of

them are aware of at least one of them. 2) 90 percent of the retail investors are not

aware of the measures taken by the government to protect the interest of investors.

3)79 percent of the retail investors are interested to invest in shares and Debentures as

well. 4)The risk bearing capacity of the retail investors was not influenced by age.

The retail investor‘s age is not a criterion to decide their investment behavior and

investment option. 5)The investment strategy of the investors is influenced by their

income level. The retail investor‘s income level is playing a predominant role in

deciding their investment behavior and investment strategy as well. 6)The major

attributes of risk in investment are dividend, redemption period and value

appreciation.

15

Bodla and Turani( 2005), studies if the retail investor‘s perception about risk of a

security is consistent with the return perceived concerning the security. The study is

based on primary data and the respondents were asked to rank 11 investment

vehicle(blue chip stocks, small company stocks, Preference shares, debenture/Bonds,

Stock futures and options, Mutual fund , NSC/PPF/PF, Fixed deposits, Insurance

policies, Real Estate, and Gold/Silver) by risk and return on a 5 point scale. Some of

the relevant findings are as follows:- Most of the retail investors do not believe in the

dictate of financial theory-‗Higher the risk, Higher the return‘. The perceptions of the

investors vary according to the income level of investors. The perception appears to

be somewhat different between investors of various age groups. The return and risk

rankings for all the assets except one asset (FDs) do not match each other. Specially

the perceived returns of four assets i.e., blue chip stocks, debentures/Bonds,

NSC/PPF/PF, and insurance policies, are higher than the risk attached to them.

Rajarajan (2003) identifies that a strong association exists between demographic

characteristics and the risk bearing capacity of Indian investors. This study confirms

the earlier findings with regard to the relationship between age and income and the

risk bearing capacity of investors. He opines that information on risk bearing capacity

of investors will help the financial product designers to develop products, which suit

the risk characteristics of the investors. And also this information will help the

financial product marketers to target the prospective investors for the products instead

of approaching every individual with an array of products, which may not suit them at

all.

Jaspal and Subhash (2003) made an attempt to read the back of the mind of the

general investor as regards their expectations from mutual funds, taking into

consideration their age group and the occupation they are in. The following are the

findings of the study:-Majority of the investors belonging to salaries and retired

categories and those in the age group of more than 60 years gave maximum weightage

to ―past record of the organization‖ before deciding about investment in mutual funds.

The analysis of options expected in a mutual fund reveals that the investors belonging

to business category have given maximum weightage to the option of ―repurchase of

the units‖ by the fund followed by ―easy transferability‖ option. Age wise analysis

16

reveals that the investors in the age group of35-50 years also give more importance to

―repurchase facility‖ and easy transferability‖. As regards the performance appraisal

of mutual funds the respondents in the salaried category and in the age group of 35-

50years give highest importance to the ―return provided on investment by the fund‖ to

be the best criteria of performance appraisal of a fund.

Renu and Bosire (2003) analyzed the factors that influence the investors to choose

various schemes of mutual funds. The following are the major findings of the study:-

A drastic shift of interest towards private sector mutual funds was noticed in the

study. 65% of the investors preferred private sector sponsored mutual funds, 20%

preferred public sector and only 15%preferred foreign sponsored mutual funds.

Capital Appreciation was considered as a major influencing factor for selecting a

scheme/fund, followed by regular and stable income. The scheme proposed objectives

influence the investor in choosing particular scheme/fund. While past performance

and nature of products offered hold same influencing affect upon respondents. Most

of the investors (90%) preferred open ended schemes over the closed ended schemes.

Furqan Qamar (2003) analyzed the savings behavior and investment preferences

among average urban middle class of Delhi. The following are the relevant findings of

the study:- Despite financial sector reforms and entry of private, domestic and foreign

banks into the country, the nationalized commercial banks seem to be the favorite

choice of an average household. Capital market imperfections and associated risk

have not been a deterrent for many households as they were found investing in

debentures and share either directly or indirectly. The saving behavior and investment

preferences of average urban household seem to be significantly influenced by the

level of educational attainments and income of the respondents.

Murali (2002) has indicated that new issues market focuses on decreasing information

asymmetry, easy accessibility of capital by large sections of medium and small

enterprises, national level participation in promoting efficient investments, and

increasing a culture of investments in productive sector. In order that these goals are

achieved, a substantial level of improvement in the regulatory standards in India at the

voluntary and enforcement levels is warranted. The most crucial steps to achieve

these goals would be to develop measures to strengthen the new issues market.

17

Madhusudhan K (2001) suggests that Life Insurance Policy is found to be most

popular investment avenue. Other assets selected by majority of investors include

recurring deposits in post office, recurring deposits in banks, bank fixed deposits, etc.

The study suggests that investors are in general are risk – averse. Very few investors

who are educated and belong to high-income categories only have invested in shares

and debentures. He opines that risk aversion appears to decrease with education and

income. He also finds that the investors gave highest priority for safety while taking

investment decision.

Barber and Odean (2001) compare the performance of men and women using data

from the LDB dataset. The study is motivated by the two observations: (1) men tend

to be more prone to overconfidence than women in areas culturally perceived to be in

the male domain and (2) models that assume investors are overconfident tend to

predict investors will trade excessively and to their detriment. When combined, these

observations predict that men will trade more than women and that excessive trading

will hurt their performance. The annual turnover rates of men are about 80%, while

those of women are 50%. The excessive trading of men leads to poor returns. While

both men and women earn poor returns, men perform worse. Virtually all of the

gender based difference in performance can be traced to the fact that men tend to

trade more aggressively than women. Neither men nor women appear to have stock

selection ability (i.e., the gross returns earned on their trades are similar), so men‘s

tendency to trade aggressively and the resulting trading costs drag down men‘s

returns.

Shanmugham (2000) conducted a survey of 201 individual investors to study the

information sourcing by investors, their perceptions of various investment strategy

dimensions and the factors motivating share investment decisions, and reports that

among the various factors, psychological and sociological factors dominated the

economic factors in share investment decisions.

Ahmed Naseem (2000) in his study opined that bonus shares are considered a mover

of market sentiments which in turn sets an upbeat trend inequity price movement.

18

Pratip Kar and Others (2000) on behalf of SEBI made a comprehensive survey to

help gauge the impact of the growth of the securities market on the households during

the decade of the 1990s and to analyse the quality of its growth. The survey was based

on a sample of 300000 geographically dispersed rural and urban households out of

which a sample of 25,000 households were chosen for detailed canvassing by field

staff through a pre-tested questionnaire.

Raj Kabila and Uma Kabila (1998) in its discussion paper pointed out that as the

process of economic reform continues and the share of the corporate sector in the

economy increases, the role of securities markets as a source of raising funds for

investment is expected to become more critical. If Indian markets are to serve the

need of firms as well as a nationwide community of investors, it is essential that

efforts to lower transaction costs and to increase the integrity and fairness of Indian

markets continue. While measures that have been taken by the government, SEBI,

exchanges and market intermediaries in this direction have led to an increase in

capital market activity and investor confidence, it is necessary to focus on further

changes that are still required.

The investment decision making process of individuals has been explored through

experiments by Barua and Srinivasan (1991). They conclude that the risk perceptions

of individuals are significantly influenced by the skewness of the return distribution.

This implies that while taking investment decisions, investors are concerned about the

possibility of maximum losses in addition to the variability of returns. Thus the mean

variance framework does not fully explain the investment decision making process of

individuals.

Amanullah and Kamaiah (1998) in their study attempted to test whether Capital Asset

Pricing Model (CAPM) can perform well in describing the stock return in India. They

opined that though the CAPM describes stock return well in the Indian context, it is

preferable that investor‘s investment decision may be decided with the help of other

relevant factors such as P/E ratio, EPS dividend, bonus and right issues besides the

CAPM estimates. The estimation of these variables call for information on historical

data from the company‘s financial statements. There is an on-going argument that the

company presents a rosy picture of financial estimates by manipulating its financial

statements such as profit and loss account and balance sheet. In such a case it is

19

difficult to obtains true and fair view of its financial position and hence investment

decisions based on these statements may not provide a meaningful estimation of stock

returns. Thus investors are required to take extra care in estimating stock returns to

construct the portfolio of securities.

Balkrishan and Nartha (1997) made a review of Indian securities market in the light

of economic liberalization measure initiated in India. According to him financial

markets are instrumental in allocating the savings in the most desirable way so that

the desired national objectives can be achieved. This facilitates efficient production of

goods and services. Thus it contributes to the well-being and raises the standard of

living not only of borrowers but also of others in the economy. Financial markets

perform this function by transmitting the nation‘s saving into the best possible

productive uses which in turn raises the output and employment level in a country.

Belgaumi (1995) in his study attempted to test whether the random walk hypothesis or

weak from of efficient market hypothesis holds good in the Indian Stock Market. 70

companies were taken as sample in the A group of the Bombay Stock Exchange

during 1991-92. He concluded that share price behavior in the Indian stock market

followed the random walk model. Hence the exchanges are weakly efficient in pricing

their shares.

Bhave (1998) in his study pointed out that setting up of securities depositories will

bring about a change in the capital market with significant impact for the banking

industry.

Cherian Samuel (1996) in his study opined that the stock market plays only a limited

role providing finance for both U.S. and Indian firms. In seeking funding a firm‘s

main choice is between external and internal financing. Internal finance plays less of a

role in Indian firms than for U.S. firms and external debt a bigger role. This is in

consistent with the theoretical prediction that information and agency problems are

less severe for Indian firms that for U.S. firms.

Cirvante (1956) in his study pointed out that capital market in India is in a process of

transition. A gradual shift in investment is taking place from the private sector

20

investment to the public sector. This is due to the inability of the private sector to

undertake large scale investment on account of the paucity of aggregate savings and

the direction of these savings into trading and speculative activities rather than into

fixed investment.

Claessens(1995)in his study on equity investment in developing countries points out

that the benefits available to an investor of equity investment in emerging markets

ultimately depend on a trade-off between the expected rate of return and its associated

risk. To assess this trade-off a number of factors are important: the underlying factors

driving the rate of return and its variability; the efficiency of the domestic stock

market; the regulatory, accounting and enforcement standards in the host country etc.

The risk-return trade-off should, however, be investigated from the point of view of

an internationally well diversified investor who is considering investing in emerging

markets.

Crockett Andrew (1998) in his study revealed that the past twenty five years have

witnessed a process of accelerating change in the world‘s financial markets. Driven

by an interacting process of liberalistion and innovation, regulations have been

removed, new products have emerged and old boundaries between financial

intermediaries have been blurred. Innovation has brought many advantages. The menu

of financial assets and liabilities available to end-users has been greatly enlarged. The

costs of financial intermediation have fallen. Risk management tools have become

increasingly sophisticated. Developing countries have found new ways to mobilize

domestic and international savings.

Desai Ashok (2000) in his paper mentioned that regulators are necessary to prevent

intermediaries from decamping with investor‘s money. But in India there are too

many regulators who have no co-ordination among themselves. In addition to that

multiple regulation of financial institution divides up their business in an inefficient

manner. Thus financial regulation needs to be takeout of the hands of zealous servants

of the government and placed in the hands-off a much smaller number of regulators

who would have the investor‘s interests at heart and who would concentrate on giving

investors more choice and a greater voice in the investment decisions of the

intermediaries.

21

Feldman and Kumar (1995) in their article examine the main characteristics of

emerging stock markets. They point out that the regulatory environment is particularly

important for countries eager to integrate their market with the international financial

system. Without effective regulation and enforcement, domestic and international

investors will be reluctant to commit resources tothese markets. Regulation to effect

governmental control should be restricted to those strictly necessary for correcting

market failures proves to occur in unregulated markets.

Gupta (1992)conducted a survey of 1755 investor households to make factual data

available on investor preferences to mutual funds. According to the report (1993) the

availability of the mutual fund vehicle has enabled investors to substantially reduce

the risk of equity investment. Only 41-48 per cent of household investors viewed

direct share investment as safe whereas indirect share investment through pure equity

schemes of mutual funds was considered safe by 75 per cent of household investors.

Regular income and growth schemes of Unit Trust of India or other mutual fund

companies were perceived as safe by over 80 per cent household investors. In the case

of directly held shares, buying on stock exchanges was considered somewhat less safe

than buying new issues.

Gupta and Choudhury (2000) in their study pointed out that index funds have gained

acceptance among investors because it was found that fund managers often did worse

than the market average. The index fund is an admission of failure of fund

management to beat the market.

Gupta and others (1994) in their study enquired into shareowners geographic

distribution covering a sample of 165819 shareholders and 63157debenture holders

from 80 companies. The study pointed out that despite the spectacular growth of

shareholding among Indian households over the last decade, individual shareholders

are still highly concentrated in a few traditional areas. The top 10 cities ranked by

their percentage share of the total accounted for nearly two-thirds (65.3percent) of

India‘s total number of shareholders in 1992. However, the degree of concentration of

shareowners in traditional areas is slowly coming down. Bombay‘s share had fallen

by about one-fifth from 35.3 per cent in 1983-84 to27.3 per cent in 1992.The absolute

22

number of shareowners has exploded everywhere rising from an estimated 30 lakhs

for the whole country in 1983-84 to roughly 125lakhs in 1992; most places show an

increase of 3-4 times in the number of shareowners over this period. The share

owning population in India is currently increasing by about 10 per cent per annum

(excluding indirect ownership through mutual fund schemes).

Jayadev (1998) in his study made an evaluation of the performance of mutual fund

schemes in India in terms of return and risk. He observed that the average returns of

the selected 62 schemes are 1.29 per cent per month and the average risk is 7.5 per

cent. As many as 36 schemes have an above average return out of 62 schemes, 33

have returns in conformity with the linear relationship of above average returns with

above average risk and vice versa. Sixteen schemes have above average returns with a

risk less than average and13 schemes have less return than the average with higher

risk. In terms of risk adjusted performance, 33 schemes have outperformed their

bench-marks interns of the total risk and 30 schemes have outperformed in terms of

systematic risk.

Jha and Natarajan (1999) in their study analysed the structure of Indian stock market

in terms of volatility and price efficiency of Bombay Stock Exchange and National

Stock Exchange. They pointed out that there are well defined relations between stock

prices in the long run in each of these markets. Hence market segmentation is strongly

ruled out. The short-run behavior of stock prices is such that no stock price can be

considered to be independent of the other. Short run price movements are mostly

random or unstable but the impulse response function analysis suggests that the

instability will not persist for long.

Kishore22 (1997) in his article pointed out that the FIIs are manipulating equity

market through price rigging even during GDR issues of Indian companies for their

own benefit at the cost of domestic investors. They also play a major role in shaping

the ‗equity price movement‘ in India since 1991.However, FIIs whose hot money

moves from one emerging equity market to other markets on whims and flimsy

ground is creating disasters like that in December 1994. Mexican crisis and July 1997

Thailand problem do not help in ‗equity market development‘ in India.

23

Lamba (1999) in his paper attempted to given empirical evidence to the general

perception that Indian Stock Market reacts to domestic as well as external influences.

His study revealed that during January 1993-July 1998Indian market appeared to be

quite isolated from external influences. However an examination of the behavior of

the India market during the bullish and bearish sub-periods indicates that the major

developed markets exert considerably more (less) influence on the Indian market

during the bearish(bullish) phase.

Lease(1972) and others conducted a survey of individual investors to find out who the

potential investor is, how he makes his decisions, how he deals with his broker, what

his portfolio consists of and how well he has done as a portfolio manager. A sample

of 3000 individuals was selected, stratified according to the geographical distribution

of all American share holders as reported by the NYSE surveys. According to the

survey report (1974) the individual investor has to be primarily a fundamental analyst

who perceives him to hold a balanced and well diversified portfolio of income and

capital appreciation securities. He asserts that he invests predominantly for the long

run and is prone to use one of the broad based market indices as the bench-mark by

which to judge his personal investment performance results. Long-term capital

appreciation is the paramount investment concern with dividend income and

intermediate-term gains running distance second.

Levine and Zervos (1996) in their study examined whether there was any association

between stock markets and long run growth. According to them stock markets may

influence economic activity through their liquidity. Many high-return projects require

a long run commitment of capital. Investors, however, are generally reluctant to

relinquish control of their savings for long periods. Therefore without liquid markets

or other financial arrangements that promote liquidity, less investment may occur in

the higher return projects.

Malhotra (1994)examines the empirical relationship between equity prices and

various explanatory variables like dividend per share, earning per share, book value to

par value, P/E ration, yield, and growth etc. for the period from1982 to 1985.

According to the study, the dividend per share and earnings per share are the strongest

determinants of market price.

24

Misra (1997) traced the evolution of Indian Capital Market and described important

aspects of development in its primary and secondary segments. He pointed out that

Indian Capital Market has evolved during the last fifty years (1947-1997) from a

dormant segment of the financial system too highly active and dynamic segment

characterized by institutional build up, technological advancement and modernization.

The reforms in the market have been vast and varied since 1992. While the primary

market has emerged as a major source of funding for the corporate entities both in the

public and private sectors, the secondary market has modernized itself through

advanced technology and transparent trading practices. The array of development

financial institutions also has played a crucial role in meeting long-term credit needs

of the industrial sector.

Mohana Rao (1998) made a survey of Mutual funds to address the following

issues:(a) Which mutual fund is popular amongst the investors?(b) Which factors

govern the choice of a mutual fund organization?(c)What type of scheme/schemes is

preferred by households?(d) Which type of financial asset is opted by

investors?(e)How are mutual funds helping to enhance capital market activities in

India? And following conclusions were reached by him:-(a) The top most popular

mutual fund amongst investors is Unit Trust of India followed by State Bank of India

Mutual Fund and Can bank Mutual Fund.(b) The most popular financial asset

preferred by the respondents is UTI products followed by debentures and products of

mutual funds.(c) The most important factors of choice for a mutual fund organization

are ‗investors service‘ followed by income-cum-growth and tax benefits and capital

appreciation.(d) A vast majority of respondents agreed that mutual funds are desirable

and necessary for growth of Indian capital and money markets.(e) Majority of

respondents showed their willingness to invest their savings in private sector mutual

funds.

Mohanthy (1997) in his study observed that the primary objective of market

regulation is avoidance of market failure. Symptoms of market failure emerge when

the risk-return balance breaks down. This can happen when accurate evaluation of

market risks is not possible under imperfect market conditions. Viewed from this

perspective the first and for most task of the market regulator is to identify imperfect

25

market conditions, evaluate the risks involved and take corrective measures. For

proper identification of market imperfections the capital market can be viewed as

being composed of three distinct market segments: (i) the Capital Allocation Market

where savings are distributed among the productive users of capital (i.e. Primary

Market); (ii) the Financial Securities Market where the stocks owned by the providers

of capitals are traded by them (i.e. secondary market) and (iii) the Financial

Information Market where information is transmitted by the productive users of

capital to the suppliers.

Nagaishi (1999) in his paper on stock market development and economic growth

viewed that Indian stock market development from the 1980sonwards has not played

any prominent role in domestic savings mobilization. Both GDS and the share of the

financial assets of the household sector have been stagnating since 1992, that is, in the

post reform period.

Nagaraj (1996) in his paper examined the trends in the capital market growth and its

implications for the economy and the corporate sector. He observed that financial

liberalization thesis posits its likely positive effect on the economy‘s savings

investment and efficiency. A well functioning stock market also has a screening and

monitoring role.

Nandi (1995) studied the international mobility of capital in the context of India and

the quantitative relation between Indian stock market and the stock markets of some

important developed countries. Experience of the capital mobility across the countries

show that irrespective of the existence of control on the mobility of capital and

exchange rate movement some sort of a relation gets established between the capital

markets of major countries. Wherever a pervasive control on the movement of capital

exists capital flight takes place without the approval of the government machinery.

Nartha (1992) endeavored a study of the trend and progress of underwriting capital

issues in India for the period from 1970-71 to 1988-89. In his study he pointed out

that underwriting activities increased with the availability of underwriting facilities

provided by the various underwriting agencies. Yet is showed a declining trend in the

decade of the eighties largely on account of the equity cult in the late eighties and the

26

good public response with the entrance of most of the middle class families in the

capital market. Panda studies the working and role of stock exchanges before and

after independence. It revealed that listed stocks covered four fifths of the joint stock

companies. The shares of government sector joint stock companies were not yet

quoted on the recognized stock exchanges. Investment in stocks and shares was no

longer the monopoly of any particular class or of a small group of people. It attracted

the interest of a large number of small and middle class individuals. The people in

general were not reluctant to invest in equity shares.

Paranjape (1992) made a study of investors‘ preference on rights issues made by

corporate bodies. It revealed that only a little more than 20 percent of the investors

always applied for rights in the past. Roughly an equal number participated depending

on the availability of funds. The remaining did so only after evaluating the merits of

the offer, either by themselves or on the basis of advice from experts. Investors

generally go by the future prospects of company, its overall standing and the merits of

the offer. However a small number are likely to base their decision on the state of the

market as well.

Rangarajan (1998) in his paper put forward a valid view regarding the major issues to

be addressed in order to strengthen the functioning of Indian Capital Market. He held

that effective and efficient capital market required as table and sturdy infrastructure of

payment, settlement and clearing system and setting up of depositories. This

infrastructure is the life-line of the securities market as it helps market participants to

exercise economic choice by prompt and credible transfer of value.

SEBI (1996)made an analysis of income and expenditure of 100schemes of 15 Mutual

Funds and 13 Asset Management Companies. The report revealed that it was difficult

to establish any correlation between expense ratio of similar type and size of scheme

within the same mutual funds or across mutual funds, the profitability of an Asset

Management Company(AMC) or Return On Net Worth (RONW) to the corpus

managed by a fund and its years of existence. Schemes of same size and type have

varied expense ratio, income ratio, AMCs which manage more assets, earn a larger

income but RONW for them may be lower than one which manages a smaller corpus.

All this understates the state of affairs of the mutual funds and fund manager and

27

raises concerns about the need for a greater degree of introspection on the part of the

AMCs to get their houses in order.

Singh (1994) in his study pointed out that the proper development and growth of

securities market plays a vital role for a faster growth of industry and economy. The

role of securities market can be judged by examining how efficiently and successfully

they meet the financial requirements of the industrial enterprises by mobilizing by the

saving of masses and their ability to provide a well organized market for sale and

purchase of the industrial securities. The securities market helps in distributing the

fruits of economic prosperity in a country amongst the masses through returns on

investment of surpluses in the securities.

Terrance (2011) examined the behavior of individual investors and found them

exhibiting disposition effects, that is, they realize their profitable stocks held as

investment at a much higher rate than their unprofitable ones. The disposition effect is

found to influence market prices; yet its economic significance is likely to be the

greatest for individual investors.

Vinayakam (1994) in his study viewed that with the introduction offered pricing in

1992, the total equity share issues were of the order of Rs.2792crores. Of these the

share of premium was a stupendous Rs.1945 crores, i.e., nearly 70 per cent of the

issue amount. This has resulted in failure of certain issues which had to be bailed out.

He suggested that apart from the investors‘ awareness, education and associations

which go a long way in giving the much needed protection to the small investors, a

separate legislation or compendium conferring protection to investors was the need of

the hour. The investors would have a sigh of relief just as consumers did with the

emergence of Consumer Protection Act and consumer courts in all trading centers in

the country.

Vinayakam and Charumathi (1995) in their study observed that equity cult had spread

to different parts of the country and millions of Indian investors invested their savings

in the booming stock markets. What was once considered as the exclusive game of the

rich and privileged class is now becoming a matter of day interest for millions of

middle and low income groups of investing public in India.

28

Research Gap

A variety of work in economics, accounting and finance would have some linkages

with capital markets. Different study elicited how the demographic variables

influenced in the investment of retail investors and suggested that the government and

regulatory bodies like SEBI creates lot of awareness and encourage in retail investors

in equities to become greater part of development of economic system for making

investment on long term basis. Despite the spectacular growth of shareholders among

Indian Households over the last decade, individual investors are highly concentrated

on a few traditional areas.

A number of research gaps and limitations in the theoretical and methodological

approaches involved in previous studies are identified and suggestions made for

further research. Madhusudhan K indicated in his study that very few investors who

are educated and belong to High income group invest in Shares and Debentures.

Study by G Manju confirms the relationship between savings, status and gender of the

investor, but fails to identify each income group investment pattern of investors.

Murleedharan D in 2008 has analysed the pattern of investment preferences among

different income groups in physical and financial assets, but does not through any

light on their investment in Capital Market instrumentsin specific.

Literature review reveals that Retail Investors income level plays a predominant role

in deciding their investment behavior and investment strategy. Their perception vary

according to their income level. Their exist a strong association between demographic

factors and risk bearing capacity of Indian investors. A survey on the saving behavior

and investment preferences of average urban household of Delhi reveal that Level of

Education and income have a significant influence on them.

From our review of the literature, we argue that an under-researched area concerns but

no study has been done with respect to investment behavior of High Income Group

investors, their perception on investment and if there exists a trend in their investment

decisions. Capital Market has become highly competitive due to the extraordinary

growth being experienced by it in terms of total funds being managed, number of

29

players and choice of new innovative schemes being offered to the investors .The

highly competitive nature of this industry necessitates that marketers must fully

understand the investment behaviour of individual investors of all class and income

groups to be able to effectively market their products . The current state of knowledge

about the investor behaviour is found not to be quite satisfactory and in fact it is

inadequate when applied to understand the investment behaviour of High Income

Group investors. This thesis fills the aforementioned research gap. The number of