subhranshu sekhar das frost sullivan asia pacific market overview

DESCRIPTION

frostTRANSCRIPT

Regional Aircraft MRO Dynamics

Airlines E&M, Asia pacific

Frost & Sullivan

Aerospace & Defense Practice

Asia Pacific

Agenda of Presentation

2

Asia Pacific Fleet Dynamics 3

MRO Dynamics 14

Frost & Sullivan Value Proposition 20

Global Aircraft Fleet Dynamics

Special focus on Asia Pacific and North Asia

Global Aircraft Fleet Dynamics

4

7,550

North America

2,950

Latin

America 1,070

Africa

7,450

Europe

1,330

CIS &

Russia

13,460

Asia Pacific 2,950

Middle

East

(a) Open Skies agreements; and (b) New airlines expected to be certified in China, including

LCCs in all North Asia markets (c) Primary and secondary airports being built and upgraded

36,770 New Aircraft deliveries expected globally between 2014-2034

Source : Frost & Sullivan

Global Market Share of Aircraft Deliveries by Region (2014-2034)

5

26%

32%

21%

6% 6% 6%

3%

Asia Pacific 36%

North America 22%

Europe 18%

Middle East 8%

Latin America 9% CIS

4% Africa

3%

Global Market Share of Aircraft Deliveries by Region (2014-2034)

Region with

largest fleet

Region with 2nd

largest fleet

2014

2033

Nearly half of the world's air traffic growth will be driven by travel to, from, or within the Asia-

Pacific region in the next 20 years

Source : Frost & Sullivan

APAC share of world

GDP will expand

from its current 28%

to 36% by 2032

Manufacturing Market Forecast

6

The narrow and wide body aircraft market is large but the supply chain is set and entry is

challenging owing to certifications

$ 100 Billion in next 20 years CAGR 5% UAV

$ 360 Billion in next 20 years CAGR 2% General Aviation

Aircraft

$ 74 Billion in next 20 years CAGR 4% Regional

Turboprops

$ 80 Billion in next 20 years CAGR (1)% Regional Jets

$ 2.3 Trillion in next 20 years CAGR 5% Narrow Body

$ 2.5 Trillion in next 20 years CAGR 4% Wide Body

Source : Frost & Sullivan

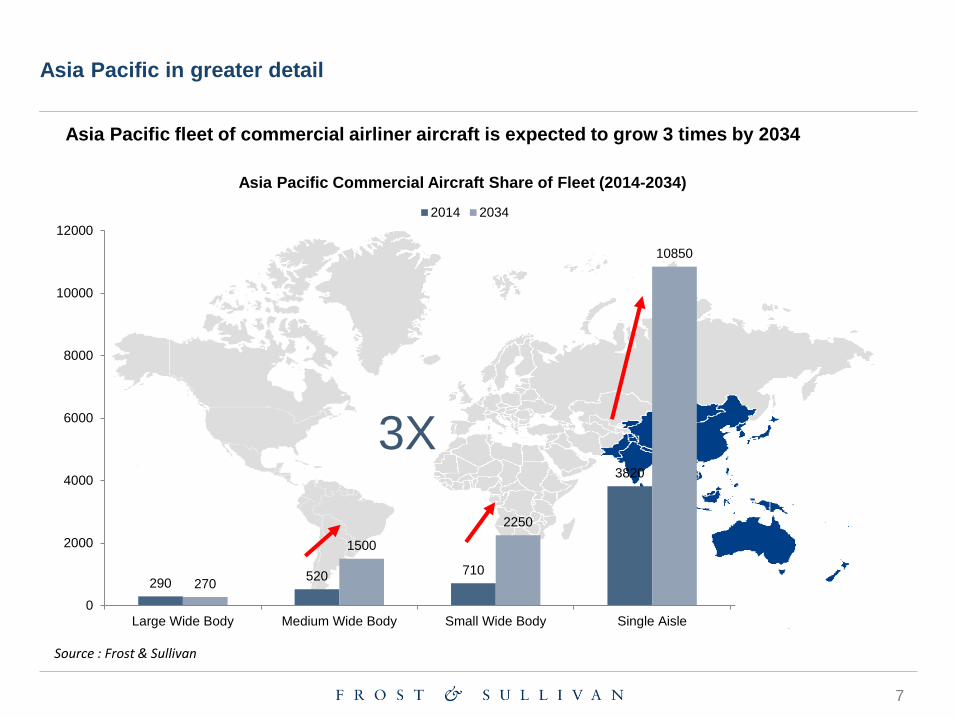

Asia Pacific in greater detail

7

Asia Pacific fleet of commercial airliner aircraft is expected to grow 3 times by 2034

290 520 710

3820

270

1500

2250

10850

0

2000

4000

6000

8000

10000

12000

Large Wide Body Medium Wide Body Small Wide Body Single Aisle Regional Jets

3X

Asia Pacific Commercial Aircraft Share of Fleet (2014-2034)

2014 2034

Source : Frost & Sullivan

Global MRO Market

8

The total global MRO market is estimated to be close to $US 68.5 billion for 2015

The Asia Pacific region is ripe for investment into MRO business as it has the optimum market size with

strong growth rate as compared to Western Europe and North America

The Asia Pacific MRO market is forecasted to grow at 6.4% CAGR

The current MRO market size is forecasted at $US 12.3 billion

Middle East $77.97B

North America $209.92 B

Western Europe $191.63 B

Eastern Europe $41.6 B

Latin America $51.9 B

India $17.07 B

China $78.9 B

Asia Pacific $167.2 B

Africa $26.81 B

0

50

100

150

200

250

300

0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 18.00%

MR

O M

ark

et S

ize in $

US

mill

ion

Growth rate (CAGR) %

Global MRO Spending Forecast Comparison, By Region, 2015-2024

9

Asia Pacific region will receive a total of 2276 firm commercial aircraft orders from 2015-2024 which hold

potential for strong growth potential for MRO in the region

Majority of the orders are for single aisle aircraft, followed by twin-aisle long range

Regional Single AisleTwin Aisle -Long Range

Twin Aisle -MediumRange

Twin Aisle -Short Range

Twin Aisle -Ultra Large

2015-2024 148 1510 519 67 0 32

0

200

400

600

800

1000

1200

1400

1600

Air

cra

ft O

rde

rs

Aircraft Firm Orders, Asia Pacific (ex-China, India), 2015-2024

Asia Pacific Aircraft Orders

2,276 Aircraft deliveries

New Generation aircraft orders in Asia Pacific

10

The current generation fleet will be quickly replaced over next 10 years by new generation

aircraft ; MRO strategy needs to plan for future rather than present

Choice of MRO capacity to be developed should be A320neo & B737 MAX looking at large

orders and fleet commonality amongst operators

4341 Total Operating Fleet (2015)

7793 Total Operating Fleet (2024)

A320/321 neo (2) (1172)

B737MAX (0) (597)

ATR72-600 (88) (502)

A350-900/1000 (0) (383)

B777-8/9 (0) (96)

B787-8/9/10 (110) (493)

B777-300ER (179) (304)

6.03% CAGR Growth

Next Generation Most Promising Opportunities (Main Fleet Types Only)

Asia Pacific

Distribution between Airbus & Boeing in Asia Pacific

11

Single aisle aircraft are going to dominate the Asian skies with massive orders of close to

1510 aircraft to be delivered in next 10 years (approx ~ 150 aircraft a year) followed by 519

units of twin aisle long range aircraft (approx ~ 50 aircraft a year)

Airbus A320 and A320neo will together constitute

69.0% of the total orders.

Boeing 737 new generation aircraft such as B737-

8/9 and B737MAX are going to hold 30.0% of the

market share.

Others, 6, 1%

777-300ER, 56, 11%

787-8/9/10, 215, 41%

A350-900/1000, 242, 47%

Aircraft Firm Orders, Asia Pacific (ex-China, India), Twin Aisle Long Range, 2015-2024

737-6/7/8/900, 172, 11%

737-MAX, 284, 19%

A320/321, 250, 17%

A320/321NEO, 792, 52%

Others, 11, 1%

Aircraft Firm Orders, Asia Pacific (ex-China, India), Single Aisle 2015-2024

Airbus A350 will constitute 47.0% of the total wide

body long range aircraft orders.

Boeing 787 new generation aircraft such as B787-

8/9/10 and B777-30ER are going to hold 52.0% of

the market share.

Airbus Boeing Airbus

Boeing

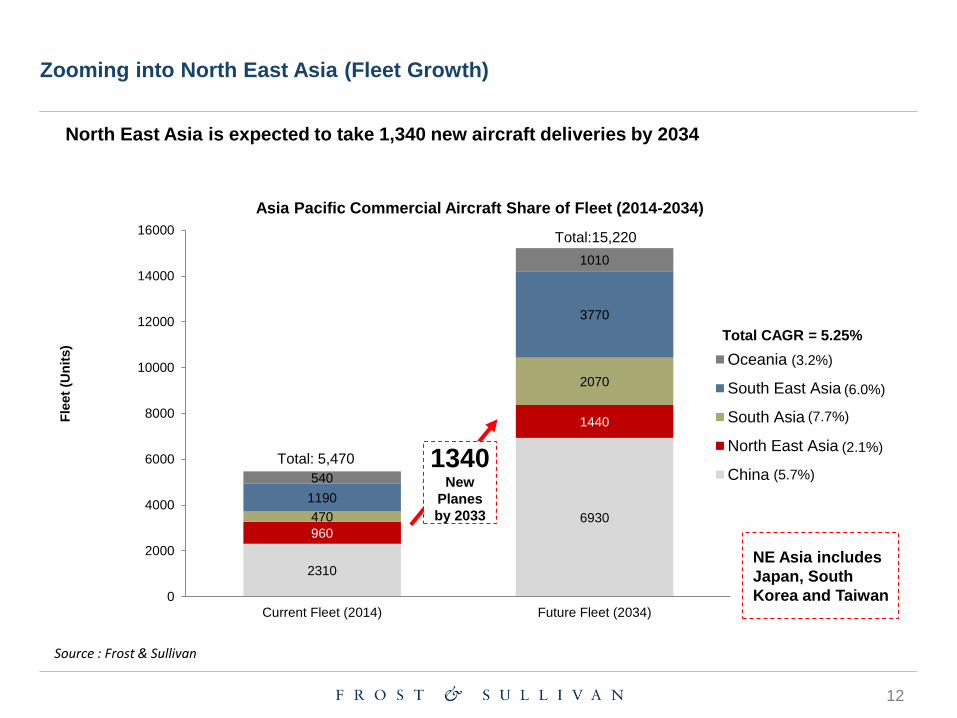

Zooming into North East Asia (Fleet Growth)

12

North East Asia is expected to take 1,340 new aircraft deliveries by 2034

2310

6930 960

1440

470

2070

1190

3770

540

1010

0

2000

4000

6000

8000

10000

12000

14000

16000

Current Fleet (2014) Future Fleet (2034)

Fle

et

(Un

its)

Asia Pacific Commercial Aircraft Share of Fleet (2014-2034)

Oceania

South East Asia

South Asia

North East Asia

China

NE Asia includes

Japan, South

Korea and Taiwan

1340 New

Planes

by 2033

Total:15,220

Total: 5,470

Total CAGR = 5.25%

(6.0%)

(7.7%)

(3.2%)

(2.1%)

(5.7%)

Source : Frost & Sullivan

Zooming into North East Asia (Type of Aircraft)

13

More concentration of wide body aircraft is expected as routes in North Asia will get thicker

Large Wide Body, 70

Medium Wide Body, 320

Small Wide Body, 340

Single Aisle, 560

Regional Jet, 50

0 100 200 300 400 500 600

New Aircraft Fleet (Units)

Asia Pacific Commercial Aircraft Share of Fleet (2014-2034)

Large

concentration

of Wide Body

Aircraft

1340 New

Planes

by 2033

Source : Frost & Sullivan

MRO Dynamics

How MRO is changing around the world

15

The Asia Pacific MRO suppliers have

historically concentrated more on Boeing

aircraft however Airbus capacity is increasing

rapidly.

In terms of engine or power plant MRO

capacity the focus has been on GE. Major

Rolls Royce facilities are SIA Engineering

Company, SAESL etc. HAESL though a major

Rolls Royce facility has not been considered

in APAC region and has been included in

China region. A small portion of Rolls Royce

engine MRO is done at Thai Airways as well.

Regional MRO Portfolio

16

Asia Pacific MRO suppliers provide airframe MRO services to other regions as well beyond Asia Pacific

mainly North America. However, apart from North America other operating regions such as India, China,

Latin America, Middle East do get their MRO services done in this part of the world.

Regional MRO Portfolio

17

Asia Pacific MRO suppliers provide a larger portion of engine repair and overhaul services beyond Asia

Pacific region. ERO services provided by Asia Pacific suppliers to APAC based airline carriers constitute

only 53.7% of the total capacity. They also serve China based airline operators constituting 11.9%, India

3.3%, Middle East based carriers 22.7% and Western Europe 4.8%. In conclusion, Asia Pacific based

ERO services have well established customers beyond the region.

Regional MRO Portfolio

MRO Dynamics - Standalone maintenance firms are under the greatest pressure because

they are increasingly squeezed between the OEMs and airline-affiliated MRO companies

18

OEM, 42% OEM, 50%

Independent, 33%

Independent, 40%

In-house, 20%

In-house, 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2020

OEM Presence in MRO Airlines

Lack of economies of scale

Need to squeeze out cost savings

Source : Frost & Sullivan

Independent MROs

Seeking partnerships with OEMs for new-

generation aircraft

Long history of cooperation but increasing

competition with OEMs now

OEMs

Aggressive vertical integration in to MRO

services – growing aftermarket influence

Relatively smaller presence in APAC but

growing rapidly

MRO Dynamics - APAC MRO market is projected to grow at 5.7% CAGR till 2023, driven by

an increasing share of the global airframe heavy maintenance market

19

2.12 2.32 3.14

4.01

14.04 13.91

18.85

3.61 2.97

5.51

10.26

25.86

16.20

20.67

0

5

10

15

20

25

30

Africa CIS & Russia Latin America Middle East APAC Europe North America

Global MRO Revenue by region ($ Billions) 2014 and 10 years CAGR

MRO Revenue, 2014

MRO Revenue, 2023

5.0%

2.3%

5.3%

8.9%

5.7%

1.4% 0.8%

Africa CIS & Russia Latin America Middle East APAC Europe North America

Source : Frost & Sullivan

MRO suppliers have been

signing JVs with APAC

airlines

Also setting up distribution

and repair centers in these

growth markets to be closer

to customers

E.g., Chinese airlines

prefer to have components

repaired in China

About Frost & Sullivan

Our Industry Coverage

21

Automotive &

Transportation

Aerospace & Defense Measurement &

Instrumentation

Information &

Communication Technologies

Healthcare Environment & Building

Technologies

Energy & Power

Systems

Chemicals, Materials

& Food

Electronics &

Security

Industrial Automation

& Process Control

Automotive

Transportation & Logistics

Consumer

Technologies

Minerals & Mining

Our Global Footprint: 40+ Offices

Scanning the Globe for Opportunities and Innovation

22

Our Coverage of the Aerospace, Defense and Security industries

23

Commercial Aviation Defense Civil Security

Frost & Sullivan, the Growth Partnership Company, works in collaboration with

clients to leverage visionary innovation that addresses the global challenges and

related growth opportunities that will make or break today’s market participants.

For more than 50 years, we have been developing growth strategies for the

Global 1000, emerging businesses, the public sector and the investment

community. Is your organization prepared for the next profound wave of industry

convergence, disruptive technologies, increasing competitive intensity, Mega

Trends, breakthrough best practices, changing customer dynamics and emerging

economies? Contact Us: Start the Discussion

www.frost.com