suggested solution - j.k. shah classesprelims)(fnj4018).pdf · statement of calculation of average...

TRANSCRIPT

1 | P a g e

SUGGESTED SOLUTION

FINAL NOV. 2014 EXAM

FINANCIAL REPORTING

Prelims (Test Code - F N J 4 0 1 8)

Head Office : Shraddha, 3rd Floor, Near Chinai College, Andheri (E), Mumbai – 69.

Tel : (022) 26836666

2 | P a g e

Ans. 1

(a) Computation of EPS 1. Basic EPS

Particulars

Net profit for the year `5,00,00,000

No. of equity shares 1,00,00,000

Basic EPS `5

2. Diluted EPS

Particulars Year ended 31st March 2012

Net profit for the year `5,00,00,000

Add: Interest on debentures (1,25,000 100 11%) `13,75,000

Less: Tax saving on interest on debentures `4,12,500

Net profit attributable to equity shareholders after considering effects of dilution.

`5,09,62,500

No. of equity shares after considering effect of dilution (1,00,00,000) (1,25,000 8)

1,10,00,000

Diluted EPS `4.63 (approx.)

(b) As per AS 30 on 'Financial Instruments Recognition and Measurement', Financial Instrument is

any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity. M/s Naresh Ltd. always settles the account by delivery. In case the account is always settled by delivery then there is no option, involved in it. In that case it will not be treated as a financial instrument under AS 30.

(c)

Capital base `1,00,00,000

Actual profit `11,00,000

Target profit @ 12.5% `12,50,000

Expected profit on employing the particular executive `12,50,000 `2,50,000

`15,00,000

Additional profit Expected profit Actual profit

`15,00,000 `11,00,000 `4,00,000

Maximum bid price Additional profit/(Rate of ROI)

400000/12.5 100 `32,00,000

Maximum salary that can be offered 12.5% `32,00,000 `4,00,000

Therefore, maximum salary offered to that particular executive would be `4 lakhs.

(d)

1. Bad debts for third quarter (Q3) will be `40,000. Mohan Ltd. has recognised `20,000 (50% of `40,000) in Q3. Hence, `20,000 is to be deducted from `7,20,000.

2. Treatment adopted is correct. 3. Treatment adopted is correct.

Thus, the quarterly income would be `7,00,000 (`7,20,000 `20,000).

Ans. 2 (a)

1. Statement of calculation of average capital employed (`'000)

Item 31.3.2012 31.3.2013 31.3.2014

Goodwill (since goodwill has paid for, it is included) 2,000 1,600 1,200

Building & Machinery (revalued assumed after depreciation)

3,600 4,000 4,400

Inventories (revalued) 2,400 2,800 3,200

Sundry debtors 40 320 880

Cash and bank 240 400 800

Total Assets 8,280 9,120 10,480

Less: Sundry creditors (1,200) (1,600) (2,000)

Closing capital employed (A) 7,080 7,520 8,480

Opening capital employed (B) 7,320 7,080 7,520

3 | P a g e

Average capital employed (A B)/2 7,200 7,300 8,000

2. Statement of calculation of super profit: (`'000)

Item 31.3.2012 31.3.2013 31.3.2014

Net profit per question 840 1,240 1,640

Less: Opening balance (240) (280) (320)

600 960 1,320

Adjustments

Add: Undervaluation of stock 400 400 400

Less: Adjustment for valuation in opening stock - (400) (400)

Add: Goodwill written off - 400 400

Add: Transfer to reserves 400 400 400

Maintainable profit (A), 1,400 1,760 2,120

Less: Normal return (12.5% on average capital) (B) (900) (912.5) (1,000)

Super profit (A B) 500 847.5 1,120

Average super profit (500 847.5 1120)/3 822.5

3. Statement of valuation of goodwill

Goodwill 5 years purchase of super profit as in 2 above. 5 `8,22,500 `41,12,500 4. Statement of valuation of business (`'000)

Total net assets (31.3.2014) 8,480

Less: Goodwill (1,200)

7,280

Adsd: Goodwill as in 3 above 4,112.5

Value of business 11,392.5

Hence value of business works out to `1,13,92,500

(b)

1. Statement of capital employed

Item `in crores

Share capital 1600.00

Reserves & surplus 3200.00

Shareholders' funds 4800.00

Debt fund - long term debt 320.00

Capital employed 5120.00

2. Statement of calculation of cost of debt (post tax)

Item `in crores

Total debt 320.00

Interest @ 10% 32.00

Less: Tax rate 30%

Post tax cost of debt

(1 0.30) 32/320 7%

3. Statement of calculation of cost of equity

Item %

Cost of equity Risk free rate Beta (market rate of return risk free rate) 10% 1.05 (14 10)

14.2%

4. Statement of calculation of WACC (weighted average cost of capital)

Item `in crores

Total shareholders' funds 4800

Cost of equity 14.2%

Total debt 320

Cost of debt (net of tax) 7%

Weighted average cost of capital (WACC)

((4800 14.2%) (320 7%))/(4800 320) 13.75%

4 | P a g e

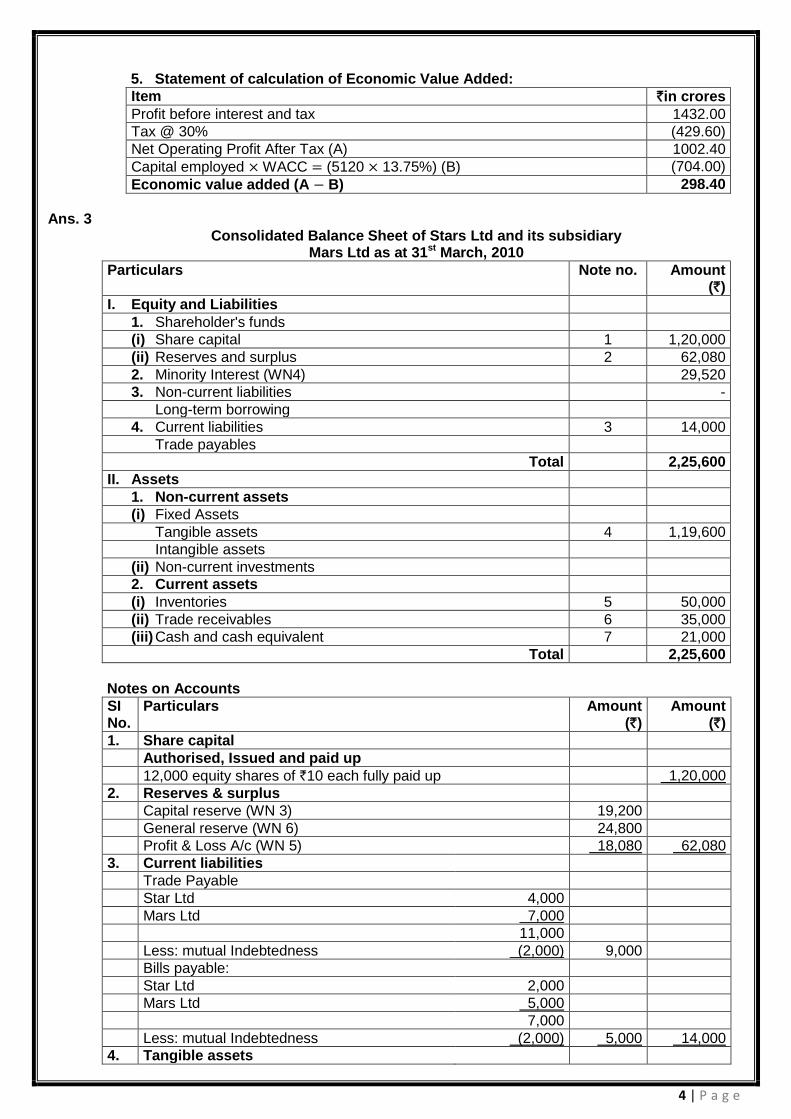

5. Statement of calculation of Economic Value Added:

Item `in crores

Profit before interest and tax 1432.00

Tax @ 30% (429.60)

Net Operating Profit After Tax (A) 1002.40

Capital employed WACC (5120 13.75%) (B) (704.00)

Economic value added (A B) 298.40

Ans. 3

Consolidated Balance Sheet of Stars Ltd and its subsidiary Mars Ltd as at 31st March, 2010

Particulars Note no. Amount (`)

I. Equity and Liabilities

1. Shareholder's funds

(i) Share capital 1 1,20,000

(ii) Reserves and surplus 2 62,080

2. Minority Interest (WN4) 29,520

3. Non-current liabilities -

Long-term borrowing

4. Current liabilities 3 14,000

Trade payables

Total 2,25,600

II. Assets

1. Non-current assets

(i) Fixed Assets

Tangible assets 4 1,19,600

Intangible assets

(ii) Non-current investments

2. Current assets

(i) Inventories 5 50,000

(ii) Trade receivables 6 35,000

(iii) Cash and cash equivalent 7 21,000

Total 2,25,600

Notes on Accounts

SI No.

Particulars Amount (`)

Amount (`)

1. Share capital

Authorised, Issued and paid up

12,000 equity shares of `10 each fully paid up 1,20,000

2. Reserves & surplus

Capital reserve (WN 3) 19,200

General reserve (WN 6) 24,800

Profit & Loss A/c (WN 5) 18,080 62,080

3. Current liabilities

Trade Payable

Star Ltd 4,000

Mars Ltd 7,000

11,000

Less: mutual Indebtedness (2,000) 9,000

Bills payable:

Star Ltd 2,000

Mars Ltd 5,000

7,000

Less: mutual Indebtedness (2,000) 5,000 14,000

4. Tangible assets

5 | P a g e

Star Ltd 44,000

Mars Ltd (84000 12000 3600) 75,600 1,19,600

5. Inventories

Star Ltd 10,000

Mars Ltd 40,000 50,000

6. Trade receivable

Star Ltd 6,000

Mars Ltd (`15000 `2000 cheque In transit) 13,000

19,000

Less: mutual Indebtedness (2,000) 17,000

Bills receivable

Star Ltd 4,000

Mars Ltd 16,000

20,000

Less: mutual Indebtedness (2,000) 18,000 35,000

Cash and Cash equivalents

Star Ltd 6,000

Mars Ltd 13,000 19,000

Remittance in transit 2,000 21,000

Working Notes: 1. Group structure

Star Ltd.

Share in Mars Ltd Share in minorities in Mars Ltd 80% 20%

2. Analysis of profits of Mars Ltd

Capital Profits Revenue Reserve

Revenue Profits

` ` ` `

i. General Reserve as on 1.4.2007 30,000

Less: Bonus issue (1/10 of `2,00,000) (20,000) 10,000 - -

ii. Increase in General Reserve (annual transfer of `2,000 for 3 years) (`36,000 `30,000)

6,000

iii. Profit and Loss Account balance as on 1.4.2007

16,000

Less: Dividend paid for the year 2007-2008 (10,000) 6,000

iv. Increase in Profit (`20,000 `6,000) 14,000

v. Loss on revaluation [(84,000 100/70 i.e. 1,20,000) 1,08,000]

(12,000)

vi. Additional depreciation written back (10% `12000) 3

3,600

4,000 6,000 17,600

Star Ltd's share (80%) 3,200 4,800 14,080

Minority Interest (20%) 800 1,200 3,520

3. Cost of Control

` `

Cost of investments in Mars Ltd. 88,000

Less: Dividend of capital profits (8,000) 80,000

Less: face value of investment (including bonus shares)

(80000 80000 1/5)

96,000

Capital profit 3,200 99,200

Capital reserve 19,200

6 | P a g e

4. Minority Interest

`

Equity share capital including bonus share (20000 20000 1/5) 24,000

Capital profits 800

Revenue reserve 1,200

Share of revenue profit 3,520

29,520

5. Profit and Loss Account - Star Ltd.

` `

Balance 12,000

Less: Dividend credited to investment (8,000)

4,000

Add: Share in Mars Ltd 14,080

18,080

6. General reserve - Star Ltd.

`

Balance 20,000

Add: Share in Mars Ltd. 4,800

24,800

Tutorial note: With regards to Bills receivable of Star Ltd it may be alternatively assumed that out of bills of Star Ltd accepted by Mars Ltd `2,000, `1,500 have been discounted. In such case, only `500 will be deducted as mutual indebtedness from bills receivable and bills payable in the balance sheet instead of `2,000.

Ans. 4 (a)

Gross Value Added Statement of German Ltd For the year ended 31st March 2014

Item ` lakhs ` lakhs

Sales 5,010

Less: Cost of raw materials, stores and other service Consumed 2,720

Administrative expenses 125

Interest on loan from bank for working capital 35 (2,880)

Value added by manufacturing and trading activities 2,130

Add: Other Income 130

Gross Value Added 2,260

Application of Value Added

Item `in lakhs `in lakhs %

To pay employees

Wages, salaries-and bonus 610 26.99

To pay directors

Salaries and commission to directors 60 2.66

To pay Government

Local taxes including cess 220

Income tax 280 500 22.12

To pay providers of capital

Interest on debentures 200

Preference dividend 100

Equity dividend 300 600 26.55

To provide for maintenance and

Expansion of the company

Depreciation 370

Transfer to general reserve 100

Retained profit `(60 40) lakhs 20 490 21.68

7 | P a g e

Total application of value added 2,260 100.00

Statement of reconciliation between Gross Value Added with Profit before Taxation

Item `

in lakhs `

in lakhs

Profit before taxation 800

Add back:

Wages, salaries and bonus 610

Salaries and commission to directors 60

Local taxes including cess 220

Depreciation 370

Interest on fixed loan 200 1,460

Gross Value Added 2,260

(b)

Accounting entries in 2013-14

Date Particulars Dr. ` Cr. `

31.12.13 Investment in X Ltd (5000 `40) Dr. 2,00,000

Investment in Y Ltd (4000 `60) Dr. 2,40,000

To Bank A/c 4,40,000

(Being investment acquired from X Ltd and Y Ltd)

31.03.14 Profit & Loss A/c (5000 `2) Dr. 10,000

To Investment in X Ltd 10,000

(Being the reduction in value of investment in X Ltd)

31.03.14 Investment in Y Ltd (4000 `4) Dr. 16,000

To Unrealised appreciation reserve A/c 16,000

(Being the increase in value of investment in Y Ltd given effect)

Accounting entries in 2014-15

Date Particulars Dr. ` Cr. `

01.04.14 Unrealised Appreciation reserve A/c Dr. 16,000

To Investment in Y Ltd 16,000

(Being the increase in value of investment in Y Ltd now reversed)

30.06.14 Bank A/c (5000 `37) Dr. 1,85,000

Profit & Loss A/c (5000 `1) Dr. 5,000

To Investment in X Ltd (5000 `38) 1,90,000

(Being the investment in X Ltd sold and loss on sale charged to Profit & Loss A/c)

30.06.14 Bank A/c (4000 `67) Dr. 2,68,000

To Investment in Y Ltd (4000 `60) 2,40,000

To Profit & Loss A/c (4000 `7) 28,000

(Being the investment in Y Ltd sold and profit on sale credited to Profit & Loss A/c)

Ans. 5

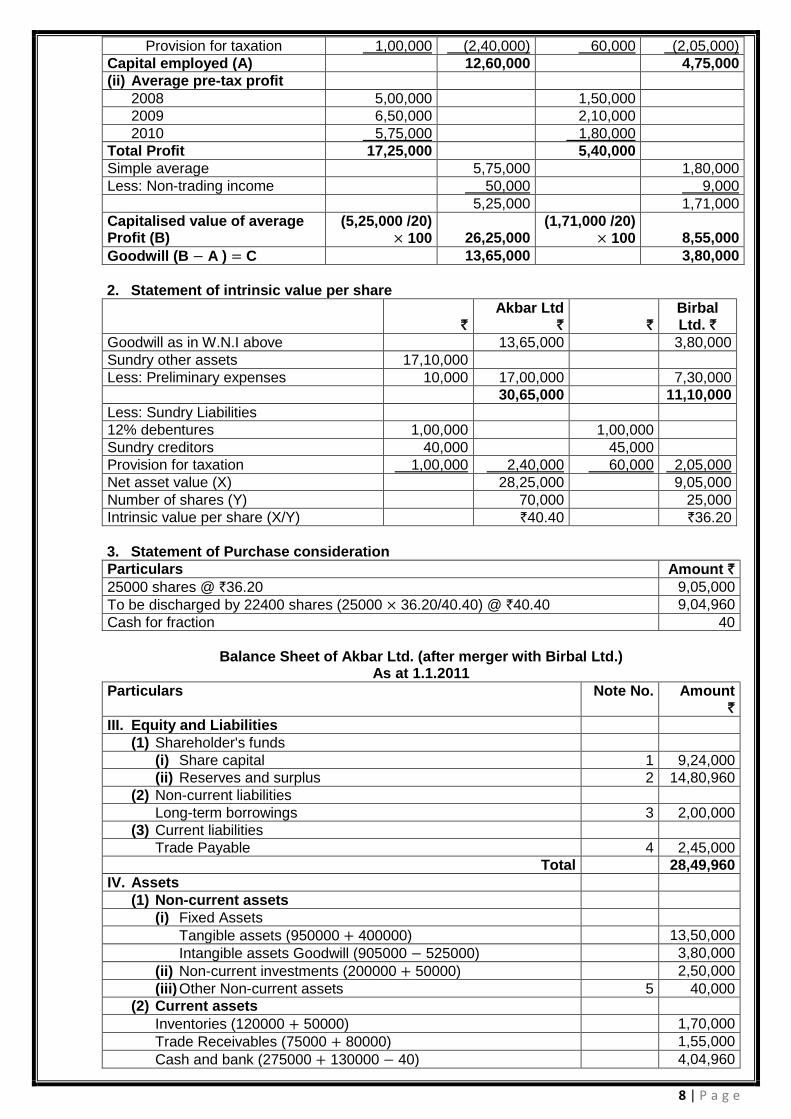

1. Statement of valuation of Goodwill

` Akbar Ltd.` ` Birbal Ltd. `

(i) Capital employed

Sundry assets as per Balance Sheet

17,10,000 7,30,000

Less: Preliminary expenses 10,000 -

Non-trade investment 2,00,000 2,10,000 50,000 50,000

15,00,000 6,80,000

Less: Sundry liabilities

12% debentures 1,00,000 1,00,000

Sundry creditors 40,000 45,000

8 | P a g e

Provision for taxation 1,00,000 (2,40,000) 60,000 (2,05,000)

Capital employed (A) 12,60,000 4,75,000

(ii) Average pre-tax profit

2008 5,00,000 1,50,000

2009 6,50,000 2,10,000

2010 5,75,000 1,80,000

Total Profit 17,25,000 5,40,000

Simple average 5,75,000 1,80,000

Less: Non-trading income 50,000 9,000

5,25,000 1,71,000

Capitalised value of average Profit (B)

(5,25,000 /20) 100

26,25,000

(1,71,000 /20) 100

8,55,000

Goodwill (B A ) C 13,65,000 3,80,000

2. Statement of intrinsic value per share

` Akbar Ltd

`

` Birbal Ltd. `

Goodwill as in W.N.I above 13,65,000 3,80,000

Sundry other assets 17,10,000

Less: Preliminary expenses 10,000 17,00,000 7,30,000

30,65,000 11,10,000

Less: Sundry Liabilities

12% debentures 1,00,000 1,00,000

Sundry creditors 40,000 45,000

Provision for taxation 1,00,000 2,40,000 60,000 2,05,000

Net asset value (X) 28,25,000 9,05,000

Number of shares (Y) 70,000 25,000

Intrinsic value per share (X/Y) `40.40 `36.20

3. Statement of Purchase consideration

Particulars Amount `

25000 shares @ `36.20 9,05,000

To be discharged by 22400 shares (25000 36.20/40.40) @ `40.40 9,04,960

Cash for fraction 40

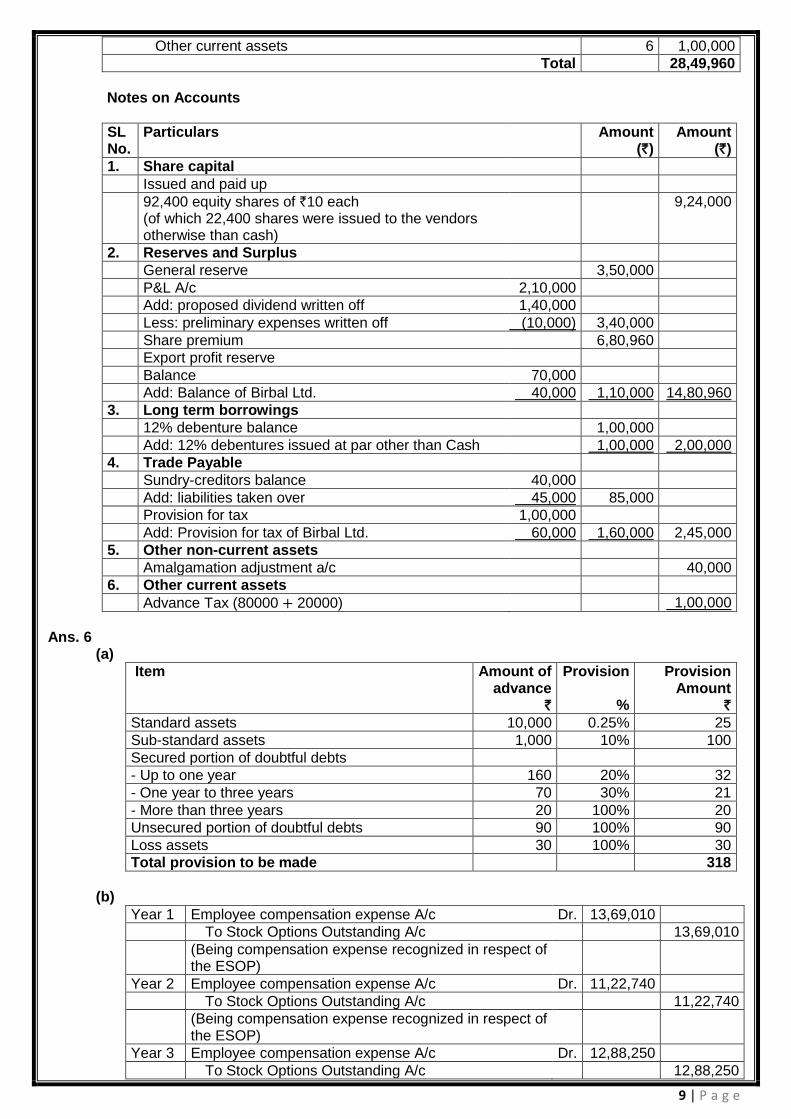

Balance Sheet of Akbar Ltd. (after merger with Birbal Ltd.)

As at 1.1.2011

Particulars Note No. Amount `

III. Equity and Liabilities

(1) Shareholder's funds

(i) Share capital 1 9,24,000

(ii) Reserves and surplus 2 14,80,960

(2) Non-current liabilities

Long-term borrowings 3 2,00,000

(3) Current liabilities

Trade Payable 4 2,45,000

Total 28,49,960

IV. Assets

(1) Non-current assets

(i) Fixed Assets

Tangible assets (950000 400000) 13,50,000

Intangible assets Goodwill (905000 525000) 3,80,000

(ii) Non-current investments (200000 50000) 2,50,000

(iii) Other Non-current assets 5 40,000

(2) Current assets

Inventories (120000 50000) 1,70,000

Trade Receivables (75000 80000) 1,55,000

Cash and bank (275000 130000 40) 4,04,960

9 | P a g e

Other current assets 6 1,00,000

Total 28,49,960

Notes on Accounts

SL No.

Particulars Amount (`)

Amount (`)

1. Share capital

Issued and paid up

92,400 equity shares of `10 each (of which 22,400 shares were issued to the vendors otherwise than cash)

9,24,000

2. Reserves and Surplus

General reserve 3,50,000

P&L A/c 2,10,000

Add: proposed dividend written off 1,40,000

Less: preliminary expenses written off (10,000) 3,40,000

Share premium 6,80,960

Export profit reserve

Balance 70,000

Add: Balance of Birbal Ltd. 40,000 1,10,000 14,80,960

3. Long term borrowings

12% debenture balance 1,00,000

Add: 12% debentures issued at par other than Cash 1,00,000 2,00,000

4. Trade Payable

Sundry-creditors balance 40,000

Add: liabilities taken over 45,000 85,000

Provision for tax 1,00,000

Add: Provision for tax of Birbal Ltd. 60,000 1,60,000 2,45,000

5. Other non-current assets

Amalgamation adjustment a/c 40,000

6. Other current assets

Advance Tax (80000 20000) 1,00,000

Ans. 6

(a)

Item

Amount of advance

`

Provision

%

Provision Amount

`

Standard assets 10,000 0.25% 25

Sub-standard assets 1,000 10% 100

Secured portion of doubtful debts

- Up to one year 160 20% 32

- One year to three years 70 30% 21

- More than three years 20 100% 20

Unsecured portion of doubtful debts 90 100% 90

Loss assets 30 100% 30

Total provision to be made 318

(b)

Year 1 Employee compensation expense A/c Dr. 13,69,010

To Stock Options Outstanding A/c 13,69,010

(Being compensation expense recognized in respect of the ESOP)

Year 2 Employee compensation expense A/c Dr. 11,22,740

To Stock Options Outstanding A/c 11,22,740

(Being compensation expense recognized in respect of the ESOP)

Year 3 Employee compensation expense A/c Dr. 12,88,250

To Stock Options Outstanding A/c 12,88,250

10 | P a g e

(Being compensation expense recognized in respect of ESOP)

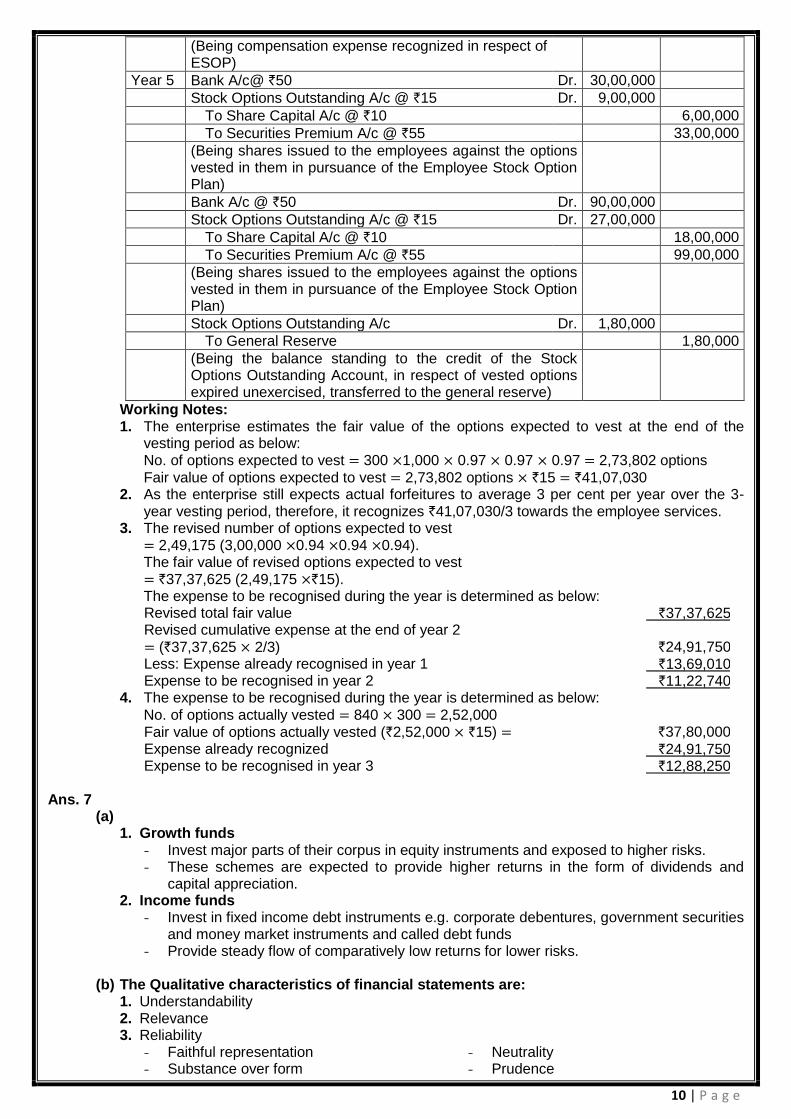

Year 5 Bank A/c@ `50 Dr. 30,00,000

Stock Options Outstanding A/c @ `15 Dr. 9,00,000

To Share Capital A/c @ `10 6,00,000

To Securities Premium A/c @ `55 33,00,000

(Being shares issued to the employees against the options vested in them in pursuance of the Employee Stock Option Plan)

Bank A/c @ `50 Dr. 90,00,000

Stock Options Outstanding A/c @ `15 Dr. 27,00,000

To Share Capital A/c @ `10 18,00,000

To Securities Premium A/c @ `55 99,00,000

(Being shares issued to the employees against the options vested in them in pursuance of the Employee Stock Option Plan)

Stock Options Outstanding A/c Dr. 1,80,000

To General Reserve 1,80,000

(Being the balance standing to the credit of the Stock Options Outstanding Account, in respect of vested options expired unexercised, transferred to the general reserve)

Working Notes: 1. The enterprise estimates the fair value of the options expected to vest at the end of the

vesting period as below: No. of options expected to vest 300 1,000 0.97 0.97 0.97 2,73,802 options

Fair value of options expected to vest 2,73,802 options `15 `41,07,030 2. As the enterprise still expects actual forfeitures to average 3 per cent per year over the 3-

year vesting period, therefore, it recognizes `41,07,030/3 towards the employee services. 3. The revised number of options expected to vest

2,49,175 (3,00,000 0.94 0.94 0.94). The fair value of revised options expected to vest `37,37,625 (2,49,175 `15). The expense to be recognised during the year is determined as below: Revised total fair value `37,37,625 Revised cumulative expense at the end of year 2

(`37,37,625 2/3) `24,91,750 Less: Expense already recognised in year 1 `13,69,010 Expense to be recognised in year 2 `11,22,740

4. The expense to be recognised during the year is determined as below:

No. of options actually vested 840 300 2,52,000 Fair value of options actually vested (`2,52,000 `15) `37,80,000 Expense already recognized `24,91,750 Expense to be recognised in year 3 `12,88,250

Ans. 7

(a) 1. Growth funds

- Invest major parts of their corpus in equity instruments and exposed to higher risks. - These schemes are expected to provide higher returns in the form of dividends and

capital appreciation. 2. Income funds

- Invest in fixed income debt instruments e.g. corporate debentures, government securities and money market instruments and called debt funds

- Provide steady flow of comparatively low returns for lower risks.

(b) The Qualitative characteristics of financial statements are: 1. Understandability 2. Relevance 3. Reliability

- Faithful representation - Substance over form

- Neutrality - Prudence

11 | P a g e

- Completeness 4. Comparability These are explained below in brief : 1. Understandability: One of the principal characteristics of the financial statements is to

ensure understandability such that these documents are comprehensible by various user communities like investors, government agencies etc.

2. Relevance: The financial statements need to ensure relevance for decision making needs of the users. Information has the quality of relevance when it influences the economic decisions of users by helping them evaluate past, present or future events or confirming or correcting their past evaluations.

3. Reliability: These statements need to be reliable, free from any material errors of omission and commission and bias. The information appended therein can be depended upon by users to represent faithfully that which it either purports to represent or could reasonably be expected to represent. Reliability presupposes the following constituents: Faithful representation Information must depict faithfully the transactions it purports to represent in order to be reliable. There is always a risk that this may not necessarily hold true sometimes owing to inherent difficulties in identifying the transactions or an appropriate method of measurement or presentation. Substance over form Transactions and other events are accounted for and presented in accordance with their substance and economic reality and not merely their legal form. Faithful representation can only be possible if accounting of a transaction is according to its substance and economic reality, and not its legal form. Neutrality Information needs to be free from bias to be reliable. Neutrality is lost if the financial statements are prepared with a view to influence the user to make a judgment or decision in order to achieve a predetermined outcome. Prudence Prudence pre-supposes recognition of uncertainties in reporting through adequate disclo-sures. However, it may be borne in mind that prudence does not allow creation of hidden reserves or excessive provisions, understatement of assets or income or overstatement of expenses and liabilities. Completeness Financial information must be complete, within the restrictions of materiality and cost to be reliable. Omission may cause information to be misleading. Comparability: The financial statements need to stand on robust and consistent accounting policies to ensure that these are comparable between accounting periods within the entity as also between entities in the same industry. Users must be able to compare the financial statements I. through time to identify trends II. with other enterprise's statements, to evaluate their relative financial position, perfor-

mance and changes in financial position Consistency of treatment of accounting policies and effective disclosures of the same is particularly important to ensure effective comparability However, comparability is not the same as uniformity. Enterprises should change accounting policies if they become inappropriate over time to take care of business dynamics.

(c) The present case relates to the concept of ‘by-products’ under as 2 on ‘valuation of inventories’.

As per AS 2, where by-products, scrap or waste materials, by their nature, are immaterial, they may be measured at net realizable value and this value is deducted from the main product. Hence, the opinion of the auditor is correct that the by-products are inventory of the company and it should be valued at net Realizable value and brought into books of account.

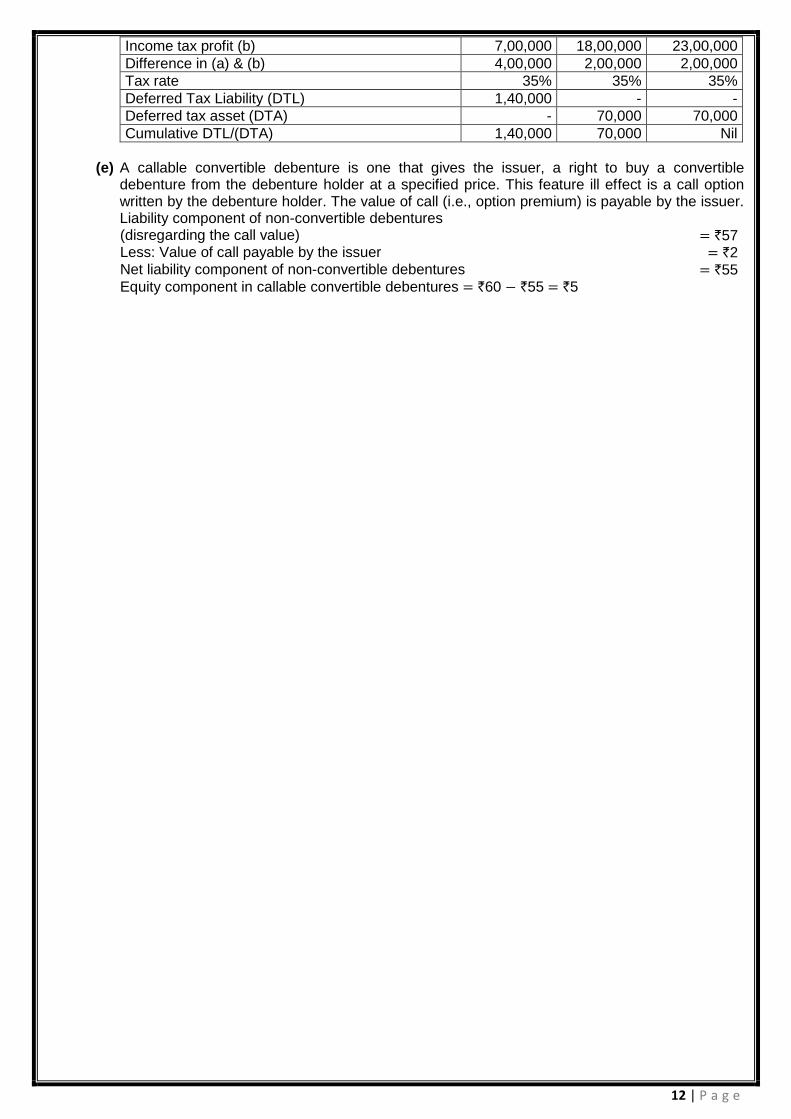

(d) Computation of Deferred Tax Asset / Liability

Year

2006 `

2007 `

2008 `

Accounting Profit (a) 11,00,000 16,00,000 21,00,000

12 | P a g e

Income tax profit (b) 7,00,000 18,00,000 23,00,000

Difference in (a) & (b) 4,00,000 2,00,000 2,00,000

Tax rate 35% 35% 35%

Deferred Tax Liability (DTL) 1,40,000 - -

Deferred tax asset (DTA) - 70,000 70,000

Cumulative DTL/(DTA) 1,40,000 70,000 Nil

(e) A callable convertible debenture is one that gives the issuer, a right to buy a convertible

debenture from the debenture holder at a specified price. This feature ill effect is a call option written by the debenture holder. The value of call (i.e., option premium) is payable by the issuer. Liability component of non-convertible debentures (disregarding the call value) `57 Less: Value of call payable by the issuer `2 Net liability component of non-convertible debentures `55 Equity component in callable convertible debentures `60 `55 `5

13 | P a g e

MARKS ALLOCATION SHEET

Que. No.

Sub point No.(if any)

Name of Chapter Description of Concept Mark Allocation

Total Marks

1 (a) AS-20 Computation of basic EPS 2

1 (a) AS-20 Computation of diluted EPS 3 5

1 (b) As-30 Provision 2

1 (b) As-30 Analysis 1

1 (b) As-30 Conclusion 2 5

1 (c) Human resource Accounting

Compotation of target profit 1

1 (c) Human resource Accounting

Computation of expected profit 1

1 (c) Human resource Accounting

Computation of additional profit 1

1 (c) Human resource Accounting

Computation of maximum bid price 1

1 (c) Human resource Accounting

Computation of maximum salary 1 5

1 (d) AS-25 Treatment of case (1) 2

1 (d) AS-25 Treatment of case (2) 1

1 (d) AS-25 Treatment of case (3) 1

1 (d) AS-25 Computation of quarterly income 1 5

2 (a) Valuation of business Computation of average capital employed 4

2 (a) Valuation of business Computation of super profit 3

2 (a) Valuation of business Computation of good will 1

2 (a) Valuation of business Computation of value of business 2 10

2 (b) Economic value added Calculation of capital employed 1.5

2 (b) Economic value added Calculation of cost of debt 1

2 (b) Economic value added Calculation of equity 1

2 (b) Economic value added Calculation of WACC 0.5

2 (b) Economic value added Calculation of EVA 2 6

3 - Consolidated financial statement

Preparation of consolidated balance sheet 6

3 - Consolidated financial statement

Analysis of profit of mars ltd 3

3 - Consolidated financial statement

Computation of cost of control 2

3 - Consolidated financial statement

Computation of minority interest 2

3 - Consolidated financial statement

Analysis of profit and loss of star ltd. 2

3 - Consolidated financial statement

Analysis of general reserve of sun ltd. 1 16

4 (a) VAS Computation of gross value added 3

4 (a) VAS Computation of value applied 4

4 (a) VAS Reconciliation 3 10

4 (b) Mutual fund Entry for investment acquired 1

4 (b) Mutual fund Entry for reduction in valve of investment in x ltd.

1

4 (b) Mutual fund Entry for increase in valve of investment in y ltd.

1

4 (b) Mutual fund Entry for in valve of investment in y ltd. now reversed

1

4 (b) Mutual fund Entry for sale of in valve of investment in x Ltd.

1

14 | P a g e

4 (b) Mutual fund Entry for sale of in valve of investment in y Ltd.

1 6

5 - Corporate restructuring

Calculation of good will of akbar ltd & birbal Ltd

6

5 - Corporate restructuring

Calculation of intrinsic value share of akbar Ltd & birbal Ltd.

3

5 - Corporate restructuring

Calculation of purchase consideration 2

5 - Corporate restructuring

Preparation of balance sheet 5 16

6 (a) NBFC Provision for standard ass.ets 0.5

6 (a) NBFC Provision for sub standard ass.et 0.5

6 (a) NBFC Provision for doubtful ass et 2

6 (a) NBFC Provision for loan ass et 0.5

6 (a) NBFC Total provision 0.5 4

6 (b) ESOP Computation of fair value of expense at the and of vesting period

2

6 (b) ESOP Calculation of expense recognized in year 2 & 3

4

6 (b) ESOP Journal entries 6 12

7 (a) Mutual fund 2 points of both types of funds 4 4

7 (b) Corporate financial reporting

Characteristics any-4 points 4 4

7 (c) AS-2 Provision 1.5

7 (c) AS-2 Analysis 0.5

7 (c) AS-2 Conclusion 2 4

7 (d) AS-22 Computation of deferred tax ass et 3

7 (d) AS-22 Computation of deferred tax liability 1 4

7 (e) AS-30 Provision 1.5

7 (e) AS-30 Calculation of liability component 2

7 (e) AS-30 Calculation of equity component 0.5 4