sulphur market outlook - fertilizer industry round table | 2016 - sulphur...sulphur market outlook...

TRANSCRIPT

Sulphur Market Outlook

Meena ChauhanHead of Sulphur and Sulphuric AcidInteger Research

The Fertilizer Institute Outlook and Technology conferenceFort Lauderdale, Florida

www.integer‐research.com

Founded in 2002, Integer Research is a leading consultancy in the fertilizer sector

• Publications• Consultancy

• Nitrogen• Phosphates• Potash• Sulphur and sulphuric acid

• London• Beijing• Tokyo

• ICIS • LMC International• Environ• Expert sub‐consultants

SERVICES PRODUCTS GEOGRAPHY PARTNERS

Sulphur market overview

www.integer‐research.com

Sulphur: changing market sentiment from by‐product to ‘yellow gold’

www.integer‐research.com

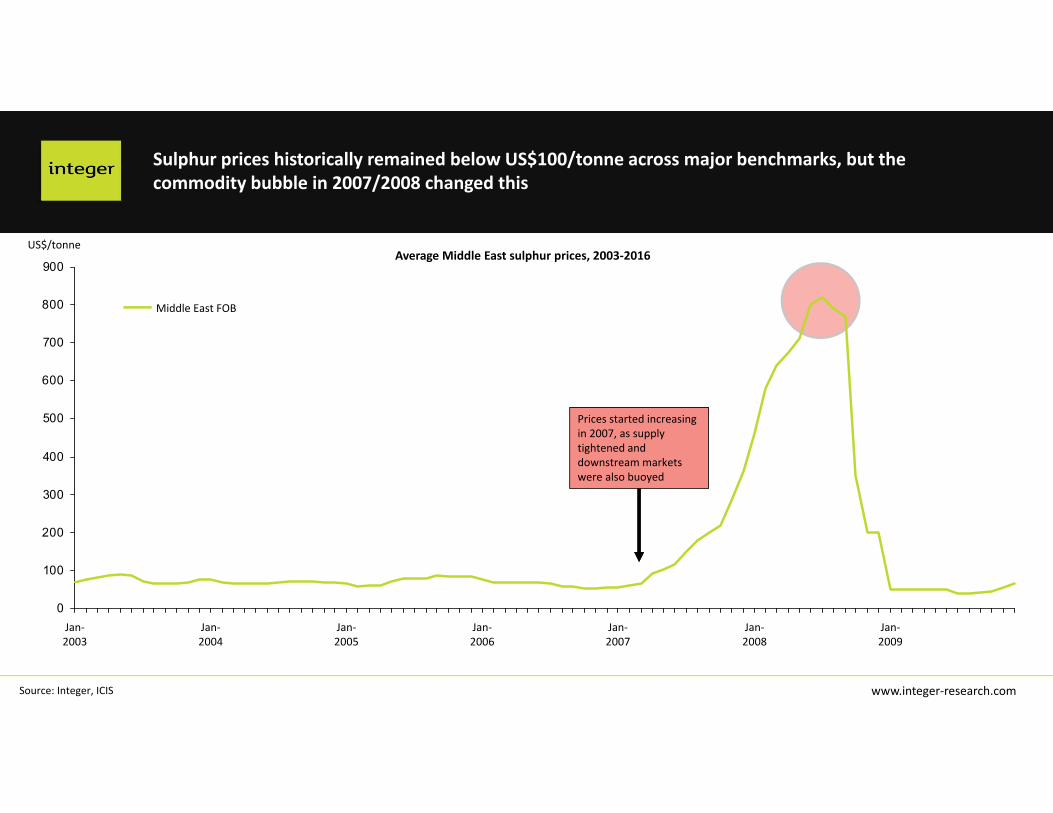

Sulphur prices historically remained below US$100/tonne across major benchmarks, but the commodity bubble in 2007/2008 changed this

0

100

200

300

400

500

600

700

800

900

Jan‐2007

Jan‐2006

Jan‐2005

Jan‐2004

Jan‐2003

Jan‐2008

Jan‐2009

Middle East FOB

Prices started increasing in 2007, as supply tightened and downstream markets were also buoyed

Average Middle East sulphur prices, 2003‐2016

Source: Integer, ICIS

US$/tonne

www.integer‐research.com

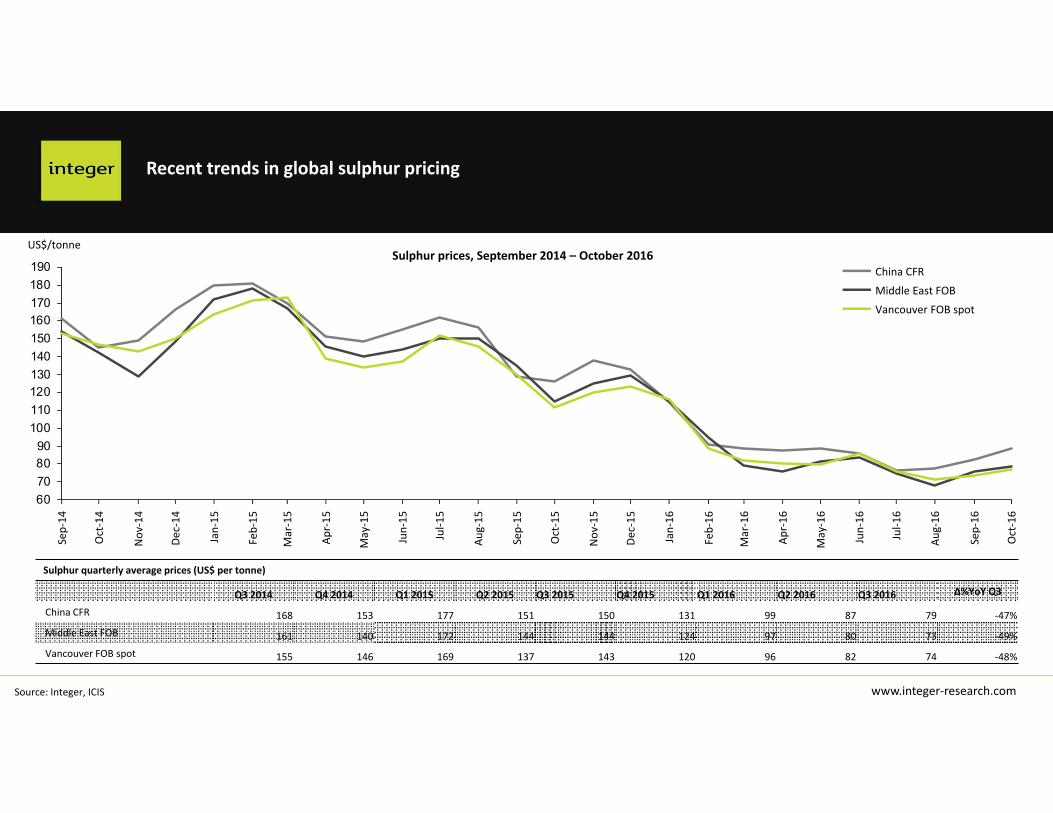

Sulphur prices, September 2014 – October 2016

Sulphur quarterly average prices (US$ per tonne)

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Δ%YoY Q3

China CFR 168 153 177 151 150 131 99 87 79 ‐47%

Middle East FOB 161 140 172 144 144 124 97 80 73 ‐49%

Vancouver FOB spot 155 146 169 137 143 120 96 82 74 ‐48%

US$/tonne

Source: Integer, ICIS

Recent trends in global sulphur pricing

60708090

100110120130140150160170180190

Oct‐15

Sep‐15

Aug‐15

Jul‐1

5

Jun‐15

Oct‐16

May‐15

Apr‐15

Mar‐15

Jan‐15

Dec‐14

Nov

‐14

Oct‐14

Sep‐14

Feb‐15

Sep‐16

Aug‐16

Jul‐1

6

Jun‐16

May‐16

Apr‐16

Mar‐16

Feb‐16

Jan‐16

Dec‐15

Nov

‐15

Vancouver FOB spot

Middle East FOB

China CFR

www.integer‐research.comSource: Integer

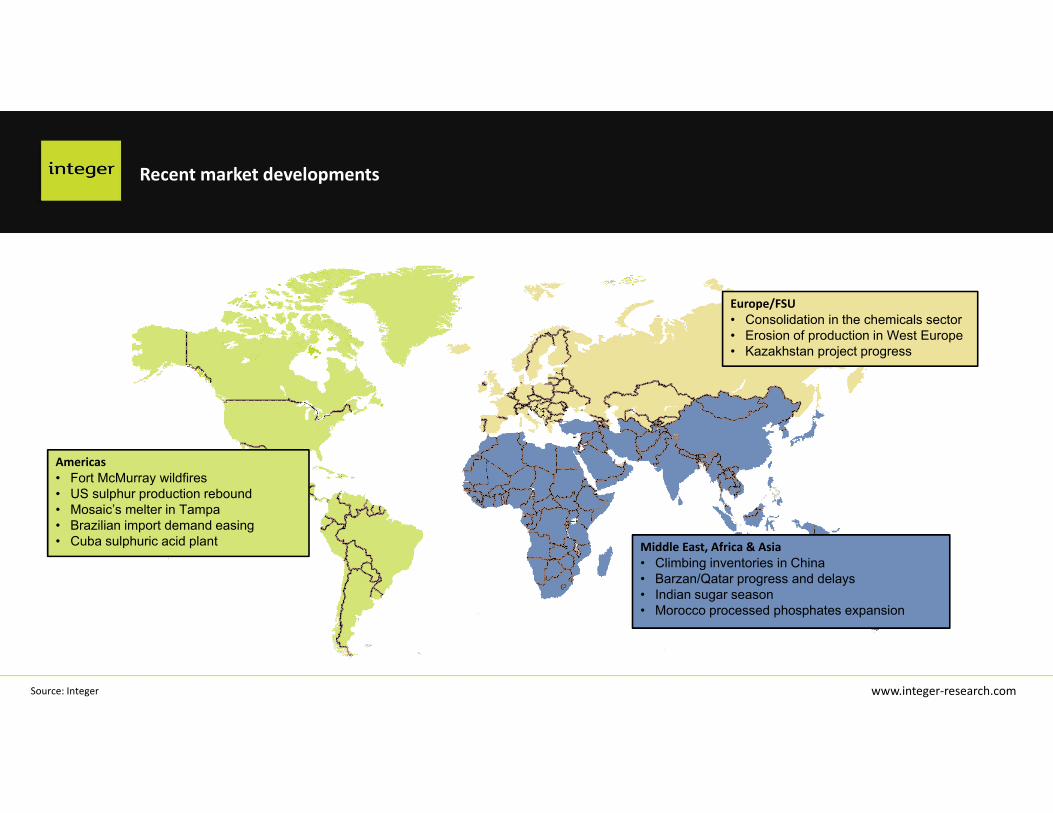

Recent market developments

Europe/FSU• Consolidation in the chemicals sector• Erosion of production in West Europe• Kazakhstan project progress

Americas• Fort McMurray wildfires• US sulphur production rebound• Mosaic’s melter in Tampa• Brazilian import demand easing• Cuba sulphuric acid plant Middle East, Africa & Asia

• Climbing inventories in China• Barzan/Qatar progress and delays• Indian sugar season• Morocco processed phosphates expansion

Supply

www.integer‐research.com

Million tonnes

Source: Integer

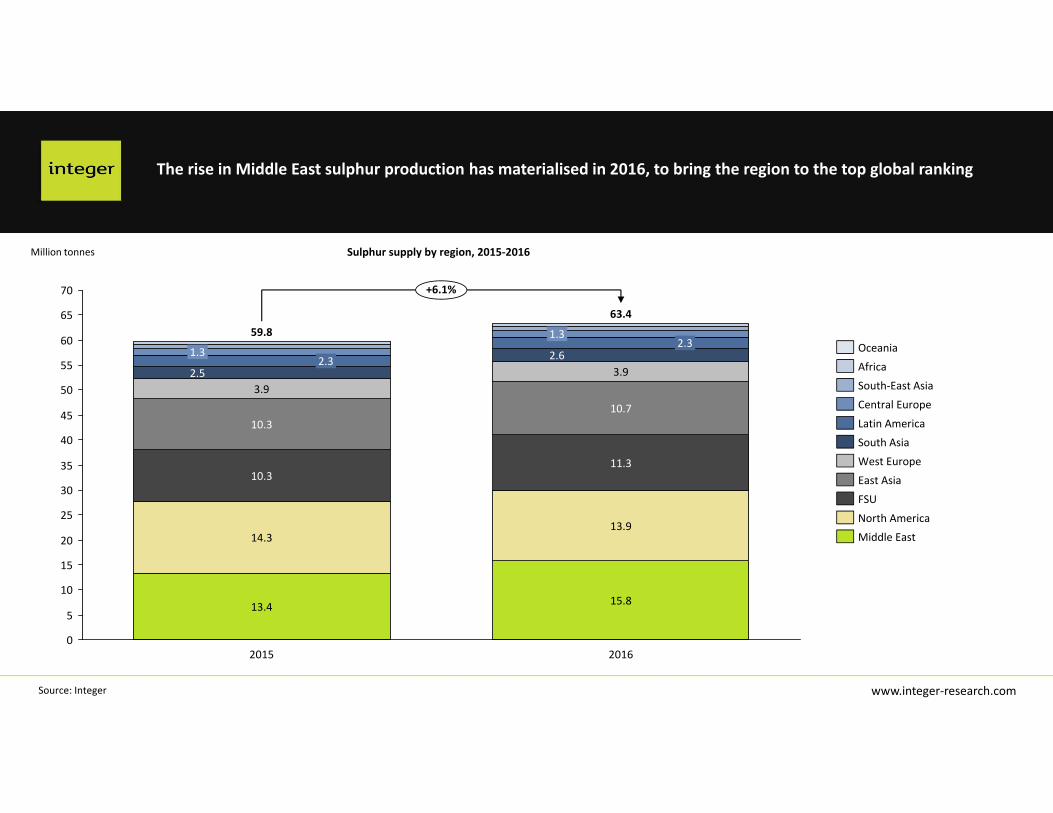

The rise in Middle East sulphur production has materialised in 2016, to bring the region to the top global ranking

70

45

60

55

50

40

35

30

25

20

15

10

5

0

65

2.5

13.9

1.3

+6.1%

2016

63.4

2.3

15.8

11.3

10.7

3.92.6

2.31.3

2015

14.3

59.8

13.4

10.3

10.3

3.9 South‐East Asia

Oceania

Central Europe

Africa

East Asia

FSU

West Europe

South Asia

North America

Middle East

Latin America

Sulphur supply by region, 2015‐2016

www.integer‐research.com

Million tonnes

Source: Integer

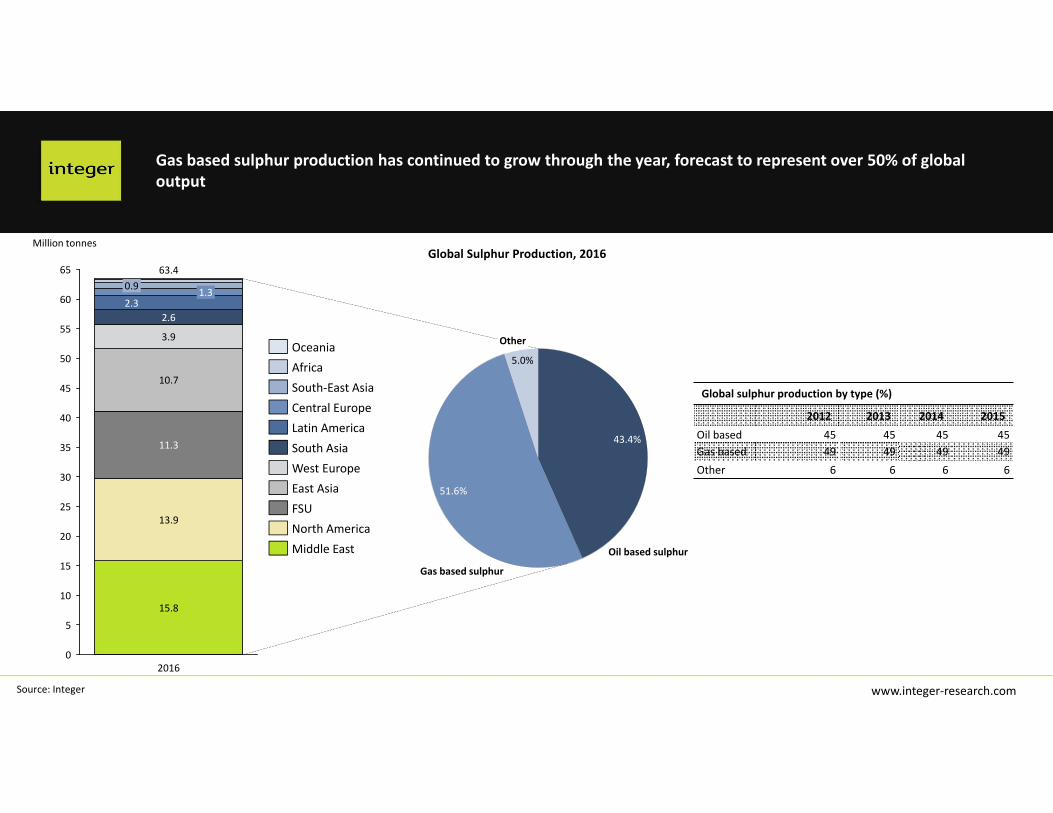

Gas based sulphur production has continued to grow through the year, forecast to represent over 50% of global output

65

60

55

50

45

40

35

30

25

20

15

10

5

0

63.4

2016

15.8

13.9

11.3

10.7

3.9

2.62.3

1.30.9

Global Sulphur Production, 2016

Other

5.0%

Gas based sulphur

51.6%

Oil based sulphur

43.4%

Global sulphur production by type (%)

2012 2013 2014 2015Oil based 45 45 45 45Gas based 49 49 49 49Other 6 6 6 6

North AmericaMiddle East

FSUEast AsiaWest EuropeSouth AsiaLatin AmericaCentral EuropeSouth‐East AsiaAfricaOceania

www.integer‐research.com

US$/bbl

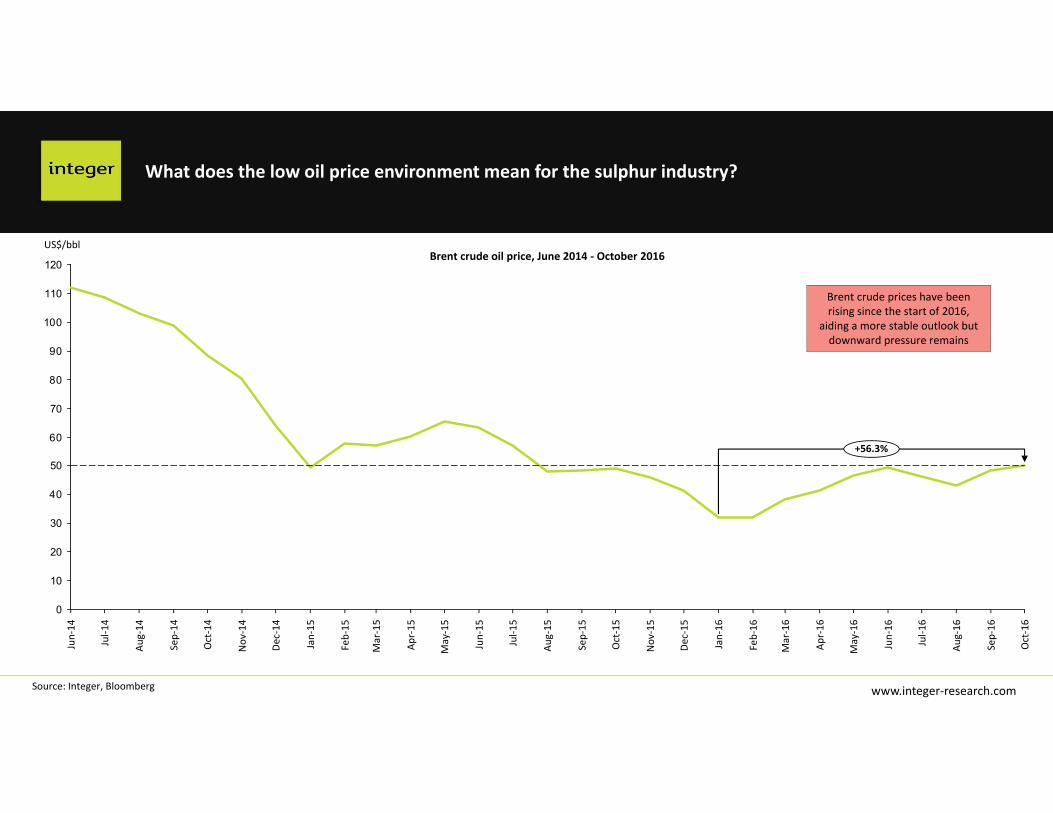

What does the low oil price environment mean for the sulphur industry?

0

10

20

30

40

50

60

70

80

90

100

110

120

Jan‐16

Dec‐15

Apr‐16

Oct‐16

Sep‐16

Aug‐16

Jul‐1

6

Jun‐16

May‐16

Mar‐16

Feb‐16

Oct‐14

Sep‐14

Aug‐14

Jul‐1

4

Jun‐14

Nov

‐15

Oct‐15

Sep‐15

Aug‐15

Jul‐1

5

Jun‐15

May‐15

Apr‐15

Mar‐15

Feb‐15

Jan‐15

Dec‐14

Nov

‐14

+56.3%

Brent crude oil price, June 2014 ‐ October 2016

Source: Integer, Bloomberg

Brent crude prices have been rising since the start of 2016,

aiding a more stable outlook but downward pressure remains

www.integer‐research.com

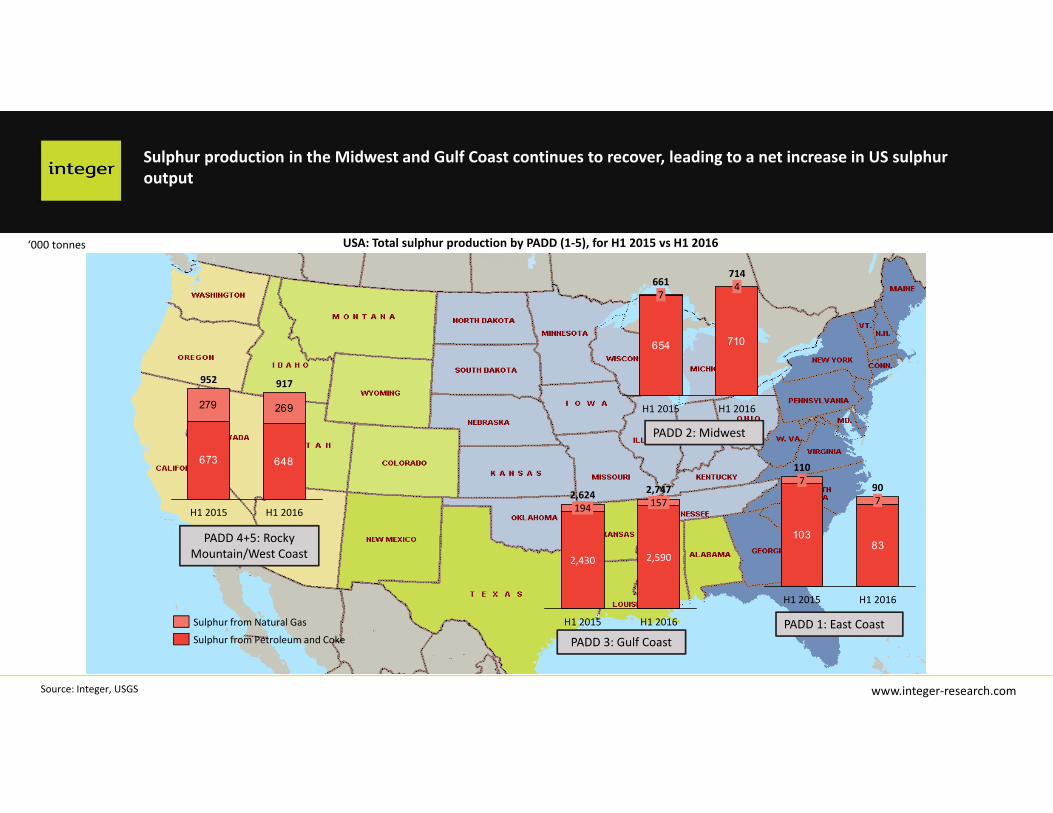

USA: Total sulphur production by PADD (1‐5), for H1 2015 vs H1 2016

Sulphur production in the Midwest and Gulf Coast continues to recover, leading to a net increase in US sulphur output

10383

H1 2016

7

1107

H1 2015

90

Sulphur from Petroleum and Coke

Sulphur from Natural Gas

654 710

H1 2016

6617

H1 2015

7144

H1 2016

1572,624

2,430

194

H1 2015

2,747

2,590

673 648

279 269

H1 2015

917952

H1 2016

Source: Integer, USGS

PADD 1: East Coast

PADD 2: Midwest

PADD 3: Gulf Coast

PADD 4+5: Rocky Mountain/West Coast

‘000 tonnes

www.integer‐research.com

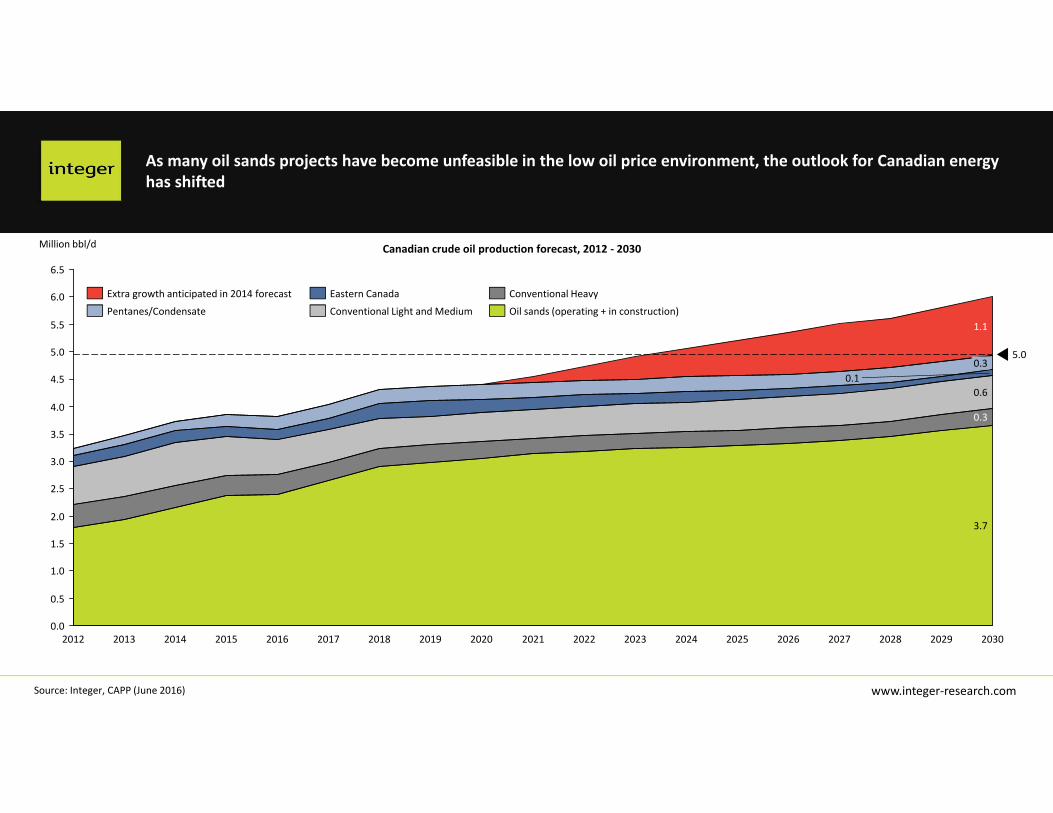

Million bbl/d

As many oil sands projects have become unfeasible in the low oil price environment, the outlook for Canadian energy has shifted

5.0

6.5

6.0

5.5

2.5

4.5

4.0

3.5

3.0

2.0

1.5

1.0

0.5

0.0

5.0

2030

3.7

0.3

0.60.1

0.3

1.1

202920282027202620252024202320222021202020192018201720162015201420132012

Pentanes/Condensate

Extra growth anticipated in 2014 forecast

Oil sands (operating + in construction)

Conventional Heavy

Conventional Light and Medium

Eastern Canada

Source: Integer, CAPP (June 2016)

Canadian crude oil production forecast, 2012 ‐ 2030

www.integer‐research.com

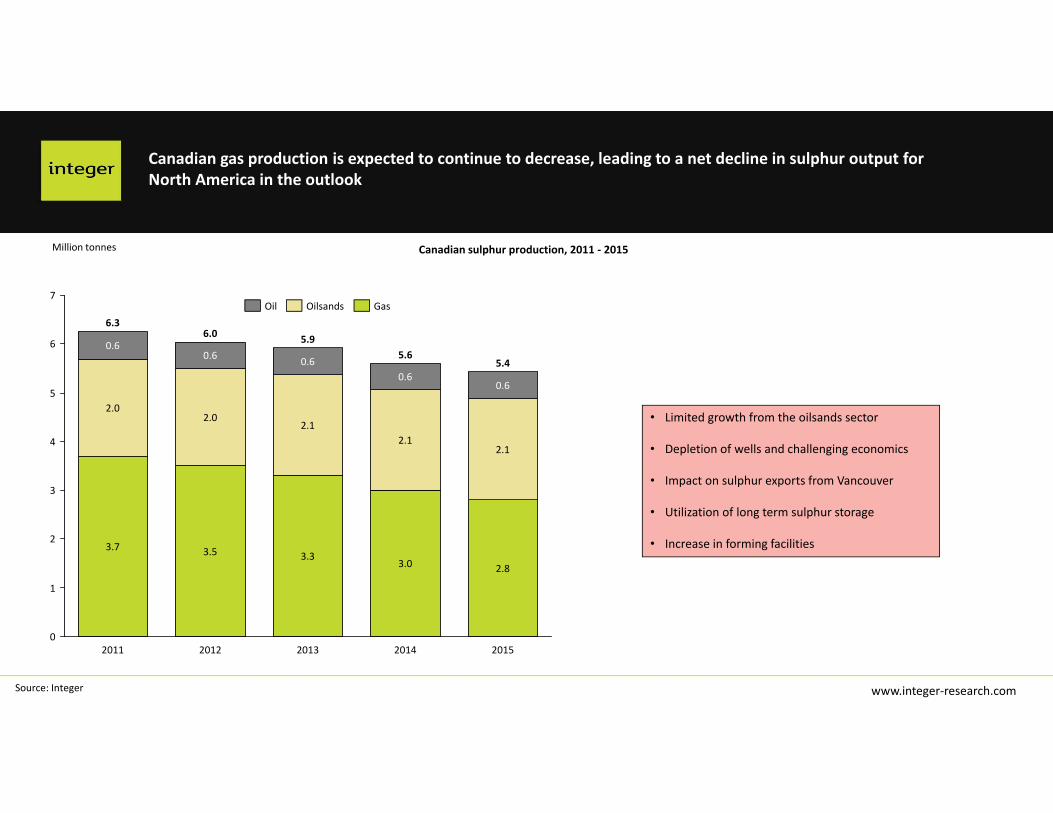

Million tonnes

Canadian gas production is expected to continue to decrease, leading to a net decline in sulphur output for North America in the outlook

0

7

6

5

4

3

2

1

5.6

3.0

2.1

0.6

2013

5.9

3.3

6.3

2.1

2.0

0.6

0.6

2014

2.0

0.6

2011

2.1

0.6 5.4

2.8

2015

6.0

3.5

2012

3.7

Oilsands GasOil

Source: Integer

Canadian sulphur production, 2011 ‐ 2015

• Limited growth from the oilsands sector

• Depletion of wells and challenging economics

• Impact on sulphur exports from Vancouver

• Utilization of long term sulphur storage

• Increase in forming facilities

Trade: changing dynamics

www.integer‐research.comSource: Integer, GTIS

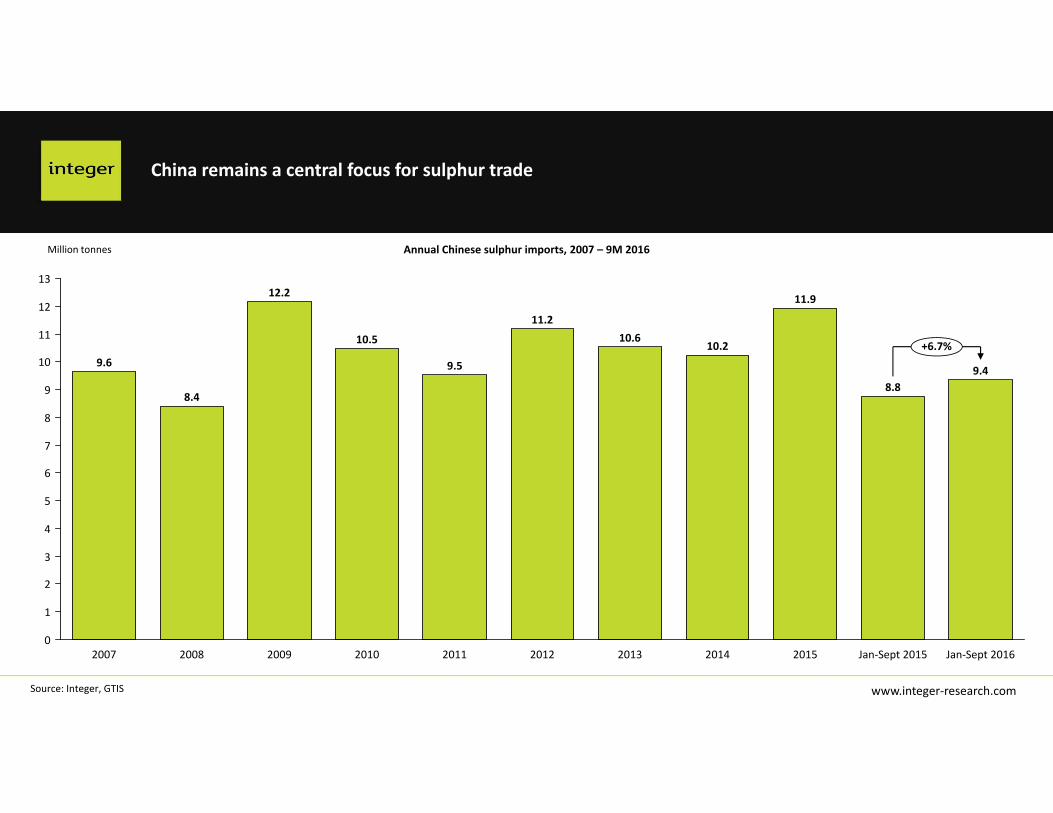

China remains a central focus for sulphur trade

Million tonnes

10

8

9

12

1

0

11

13

7

6

5

4

3

2

2007 2008 2009

+6.7%9.6

12.2

Jan‐Sept 2016

9.5

2010

10.5 10.6

2012

11.2

2011

11.9

2014

10.2

2013

9.4

Jan‐Sept 2015

8.8

2015

8.4

Annual Chinese sulphur imports, 2007 – 9M 2016

www.integer‐research.comSource: Integer, GTIS

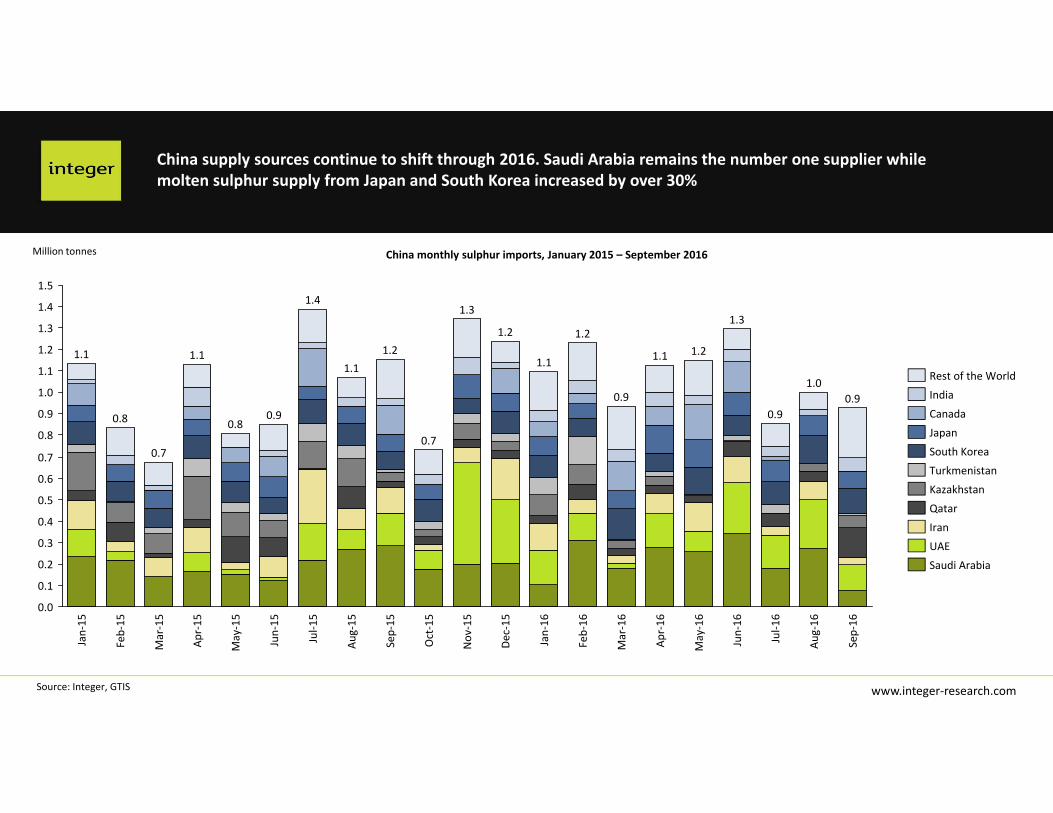

China supply sources continue to shift through 2016. Saudi Arabia remains the number one supplier while molten sulphur supply from Japan and South Korea increased by over 30%

Million tonnes

0.1

0.6

0.9

1.5

0.2

0.8

0.0

1.2

0.3

1.3

1.0

0.4

1.1

0.5

1.4

0.7

Aug‐16

1.0

Jul‐1

6

0.9

Jun‐16

Sep‐16

Aug‐15

Jan‐16

Dec‐15

1.2

0.9

Apr‐16

1.1

1.3Jul‐1

51.3

Mar‐16

Feb‐16

1.1

1.21.2

May‐16

1.2

Nov

‐15

Sep‐15

1.4

0.9

0.7

1.1

0.7

0.8

May‐15

0.8

1.1

Oct‐15

Feb‐15

Jan‐15

Mar‐15

1.1

Apr‐15

0.9

Jun‐15

Iran

Qatar

Saudi Arabia

UAE

Rest of the World

Canada

Turkmenistan

India

Kazakhstan

South Korea

Japan

China monthly sulphur imports, January 2015 – September 2016

www.integer‐research.comSource: Integer, GTIS

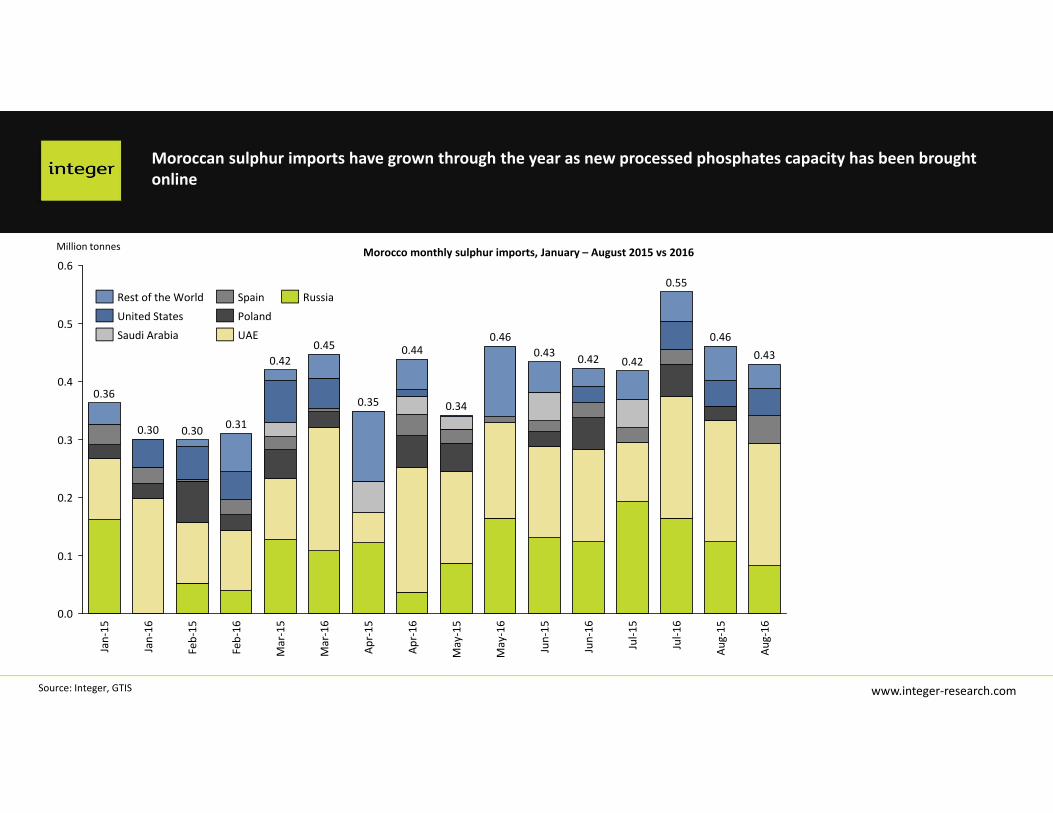

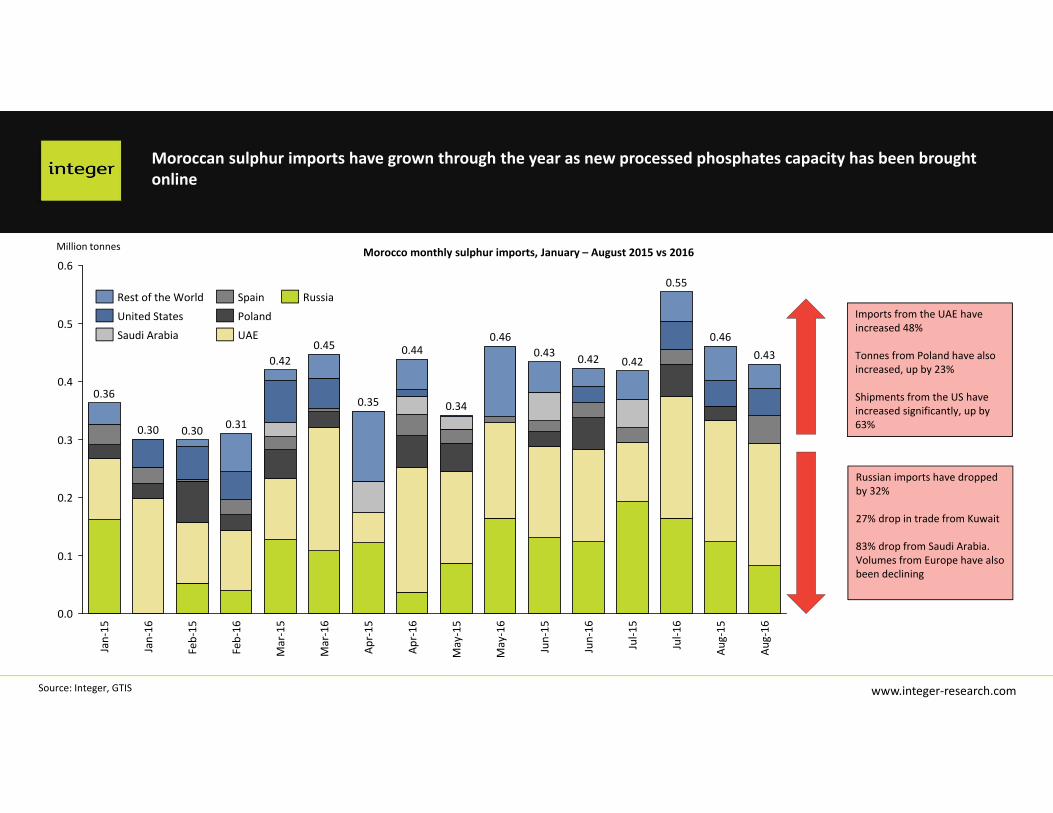

Moroccan sulphur imports have grown through the year as new processed phosphates capacity has been brought online

Million tonnes

0.4

0.1

0.6

0.5

0.3

0.2

0.0

Jan‐16

0.30

Jan‐15

0.36

Jul‐1

5

Jul‐1

6

Aug‐16

0.55

0.42 0.430.46

Aug‐15

Feb‐16

0.31

Feb‐15

0.34Ap

r‐16

0.44Ap

r‐15

0.35

Mar‐16

0.45

Mar‐15

0.42

0.30

Jun‐16

0.42

Jun‐15

0.43

May‐16

0.46

May‐15

Spain

Poland

Russia

United States

UAESaudi Arabia

Rest of the World

Morocco monthly sulphur imports, January – August 2015 vs 2016

www.integer‐research.comSource: Integer, GTIS

Moroccan sulphur imports have grown through the year as new processed phosphates capacity has been brought online

Million tonnes

0.4

0.1

0.6

0.5

0.3

0.2

0.0

Jan‐16

0.30

Jan‐15

0.36

Jul‐1

5

Jul‐1

6

Aug‐16

0.55

0.42 0.430.46

Aug‐15

Feb‐16

0.31

Feb‐15

0.34Ap

r‐16

0.44Ap

r‐15

0.35

Mar‐16

0.45

Mar‐15

0.42

0.30

Jun‐16

0.42

Jun‐15

0.43

May‐16

0.46

May‐15

Spain

Poland

Russia

United States

UAESaudi Arabia

Rest of the World

Morocco monthly sulphur imports, January – August 2015 vs 2016

Imports from the UAE have increased 48%

Tonnes from Poland have also increased, up by 23%

Shipments from the US have increased significantly, up by 63%

Russian imports have dropped by 32%

27% drop in trade from Kuwait

83% drop from Saudi Arabia.Volumes from Europe have also been declining

www.integer‐research.comSource: Integer, Port Metro

We expect the US share of Canadian sulphur trade to decline in the outlook

Sulphur exports from Canada, 2015

United States

Mexico

Brazil

Chile Australia

China

Canada

30%

10%

1%

5%20%

20%

www.integer‐research.com

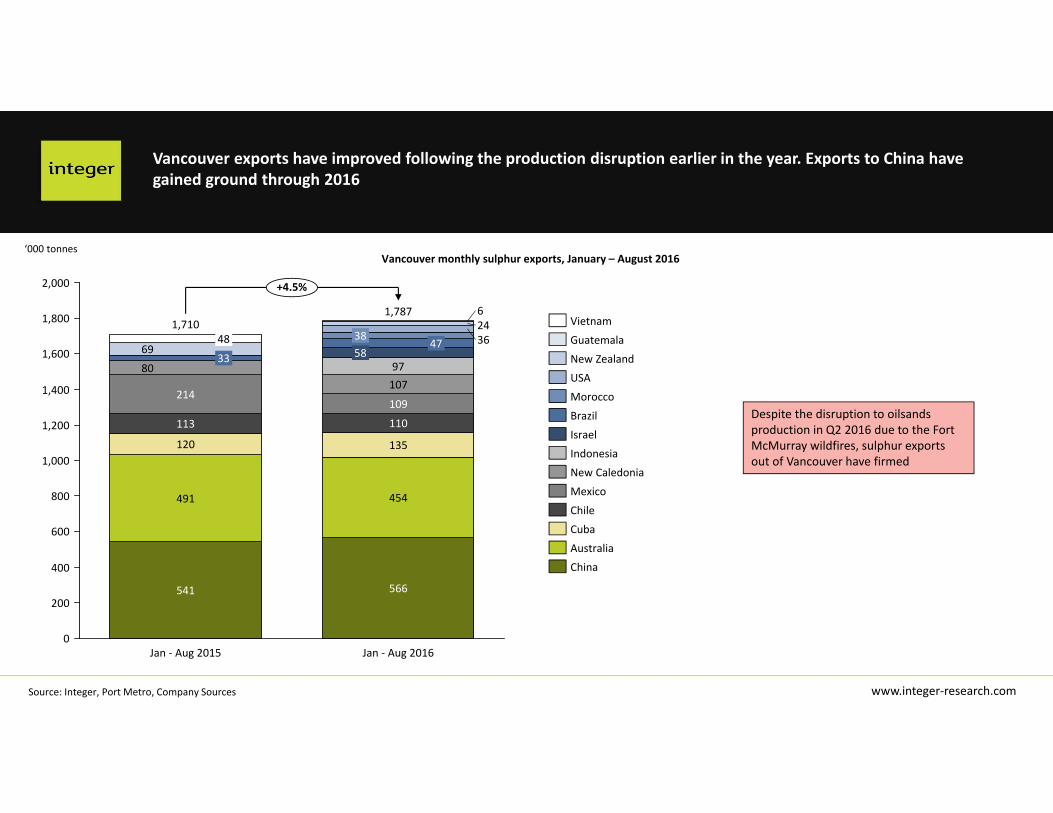

Vancouver monthly sulphur exports, January – August 2016

Source: Integer, Port Metro, Company Sources

Vancouver exports have improved following the production disruption earlier in the year. Exports to China have gained ground through 2016

‘000 tonnes

1,400

2,000

1,800

1,600

1,200

1,000

800

600

400

200

0

+4.5%

Jan ‐ Aug 2016

1,787

566

454

135

110

109

10797

5847

38 36246

Jan ‐ Aug 2015

1,710

541

491

120

113

214

8033

6948

China

Australia

Cuba

Chile

Mexico

New Caledonia

Indonesia

Israel

Brazil

Morocco

USA

New Zealand

Guatemala

Vietnam

Despite the disruption to oilsands production in Q2 2016 due to the Fort McMurray wildfires, sulphur exports out of Vancouver have firmed

Demand

www.integer‐research.com

Million tonnes

Source: Integer

Sulphur demand is set to grow by over 2% year on year in 2016, led by developments in Africa

55

5

0

65

60

50

45

40

35

30

25

20

15

10

1.3 1.3

+2.4%

2016

61.8

18.1

10.0

9.3

4.8

4.7

3.8

3.63.2

1.71.3 1.3

2015

60.4

18.0

10.0

8.4

4.8

4.5

3.73.6

3.11.7

East Asia

North America

Africa

FSU

Latin America

South Asia

West Europe

Middle East

Southeast Asia

Oceania

Central Europe

Sulphur demand by region, 2015‐2016

www.integer‐research.comSource: Integer

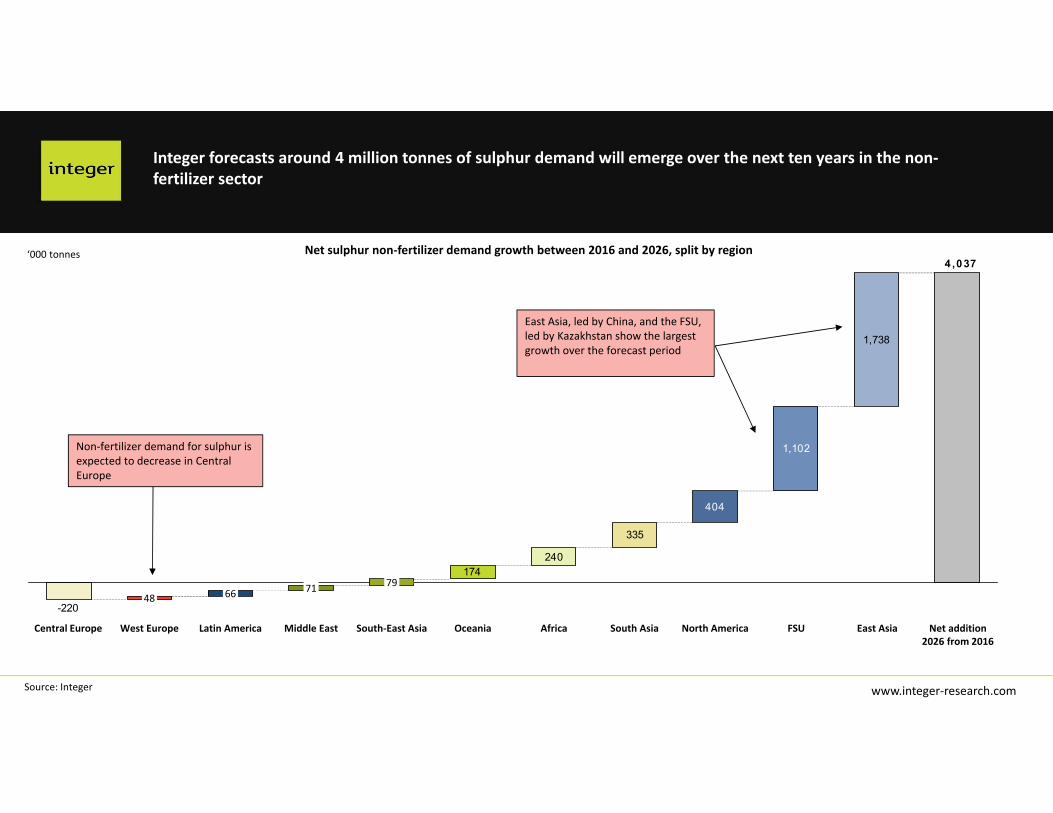

Integer forecasts around 4 million tonnes of sulphur demand will emerge over the next ten years in the non‐fertilizer sector

240

335

1,738

174

-220

4 ,037

1,102

404

Net addition 2026 from 2016

East AsiaFSUNorth AmericaSouth AsiaAfricaOceaniaSouth‐East Asia

79

Middle East

71

Latin America

66

West Europe

48

Central Europe

‘000 tonnes

Non‐fertilizer demand for sulphur is expected to decrease in Central Europe

Net sulphur non‐fertilizer demand growth between 2016 and 2026, split by region

East Asia, led by China, and the FSU, led by Kazakhstan show the largest growth over the forecast period

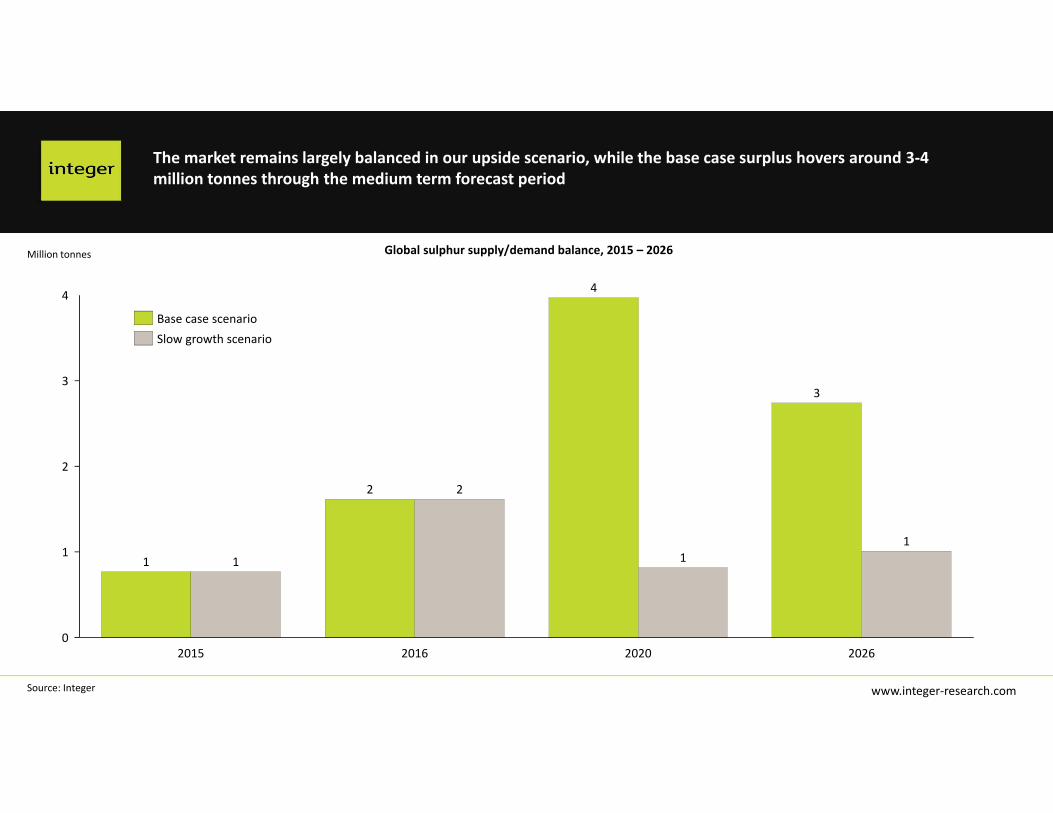

Global sulphur balance

www.integer‐research.comSource: Integer

The market remains largely balanced in our upside scenario, while the base case surplus hovers around 3‐4 million tonnes through the medium term forecast period

Million tonnes Global sulphur supply/demand balance, 2015 – 2026

4

3

2

0

1

2020

11

2016 20262015

22

4

11

3

Slow growth scenarioBase case scenario

Conclusions

www.integer‐research.comSource: Integer

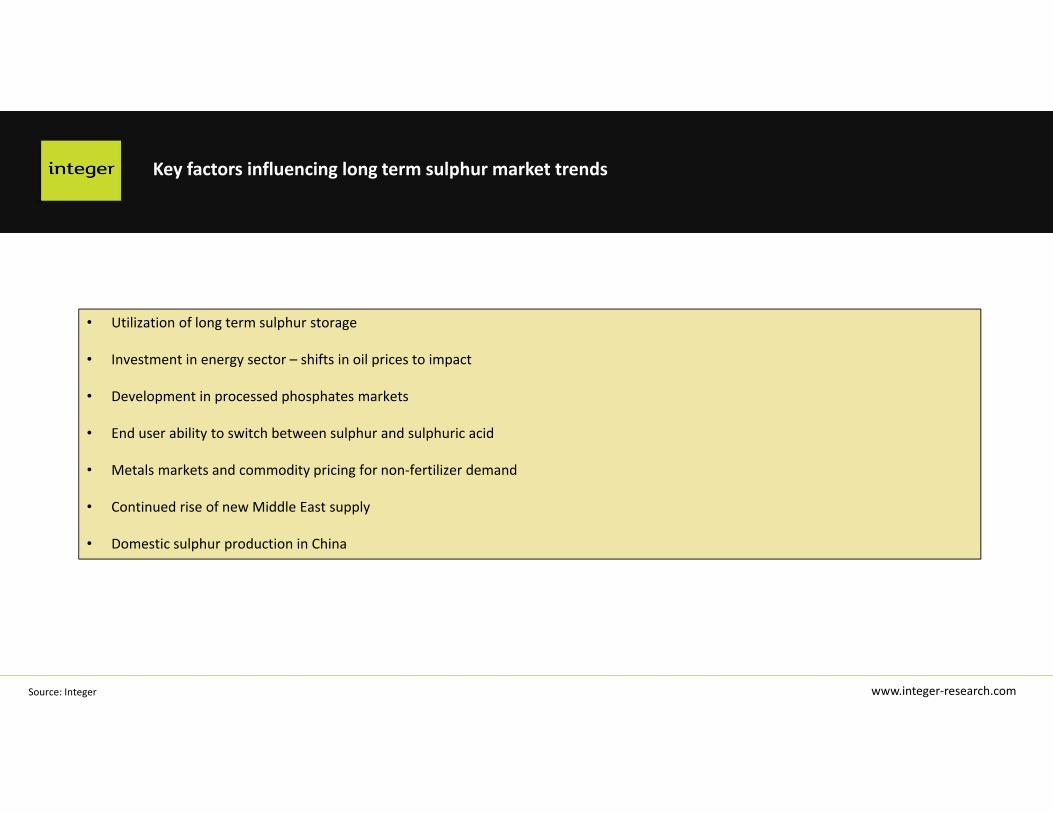

Key factors influencing long term sulphur market trends

• Utilization of long term sulphur storage

• Investment in energy sector – shifts in oil prices to impact

• Development in processed phosphates markets

• End user ability to switch between sulphur and sulphuric acid

• Metals markets and commodity pricing for non‐fertilizer demand

• Continued rise of new Middle East supply

• Domestic sulphur production in China

Thank you for your attentionAny questions?

All data in the presentation is taken from Integer’s Sulphur Market Dynamics Service

Meena ChauhanHead of Sulphur and Sulphuric AcidMeena.Chauhan@integer‐research.com+44 (0) 207 193 3990