summarised audit

TRANSCRIPT

www.nao.gm | [email protected]

S u m m a r i s e d

A U D I T R E P O R TF i n a n c i a l Y e a r 2 0 1 6

This is the first summarised report that the NAO has produced, we welcome any feedback to make further documents more simplified for the public.

Please send all suggestions and recommendations to [email protected].

CONTENTS

Acknowledgement Findings Key terms and alerts

About us Our biggest challenges Audit process

Who is this summary for?

THANKS

We would like to acknowledge the partnership and commitment of Gambia Participates in promoting transparency and accountability in the use of public resources.

This document was developed in consultation and partnership with them, in their capacity as a CSO and representative of the public.

This summarised report was developed for citizens of the Republic of The Gambia to enhance their understanding of audit findings in a more accessible way. The office will also be adopting this new approach as part of the fulfillment of our Constitutional mandate as Supreme Audit Institution (SAI).

Members of the public and CSOs can access this document online on the NAO website. The full report can be accessed here: http://nao.gm/wp-content/uploads/2020/08/Auditor-Generals-Cert-Report_2016.pdf and management letter here: https://nao.gm/wp-content/uploads/2020/08/FINAL-ML_2016-GoTG-financial-statements.pdf. The report Appendixes can also be found on the website.

Please visit the NAO office in Kanifing for hard copies of the full report and this summary.

2

MISSING DOCUMENTATION

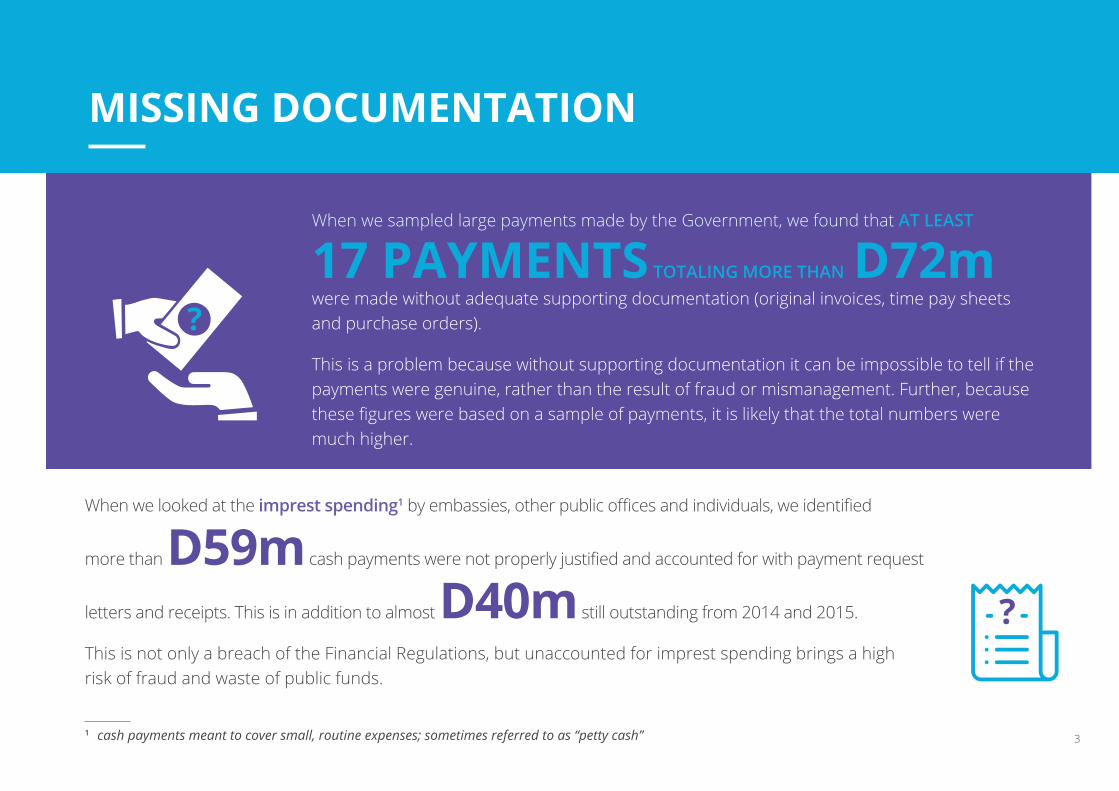

were made without adequate supporting documentation (original invoices, time pay sheets and purchase orders).

This is a problem because without supporting documentation it can be impossible to tell if the payments were genuine, rather than the result of fraud or mismanagement. Further, because these figures were based on a sample of payments, it is likely that the total numbers were much higher.

When we sampled large payments made by the Government, we found that AT LEAST

17 PAYMENTS TOTALING MORE THAN D72m

When we looked at the imprest spending1 by embassies, other public offices and individuals, we identified

more than D59m cash payments were not properly justified and accounted for with payment request

letters and receipts. This is in addition to almost D40m still outstanding from 2014 and 2015.

This is not only a breach of the Financial Regulations, but unaccounted for imprest spending brings a high risk of fraud and waste of public funds.

1 cash payments meant to cover small, routine expenses; sometimes referred to as “petty cash” 3

UNDISCLOSED BANK ACCOUNTS

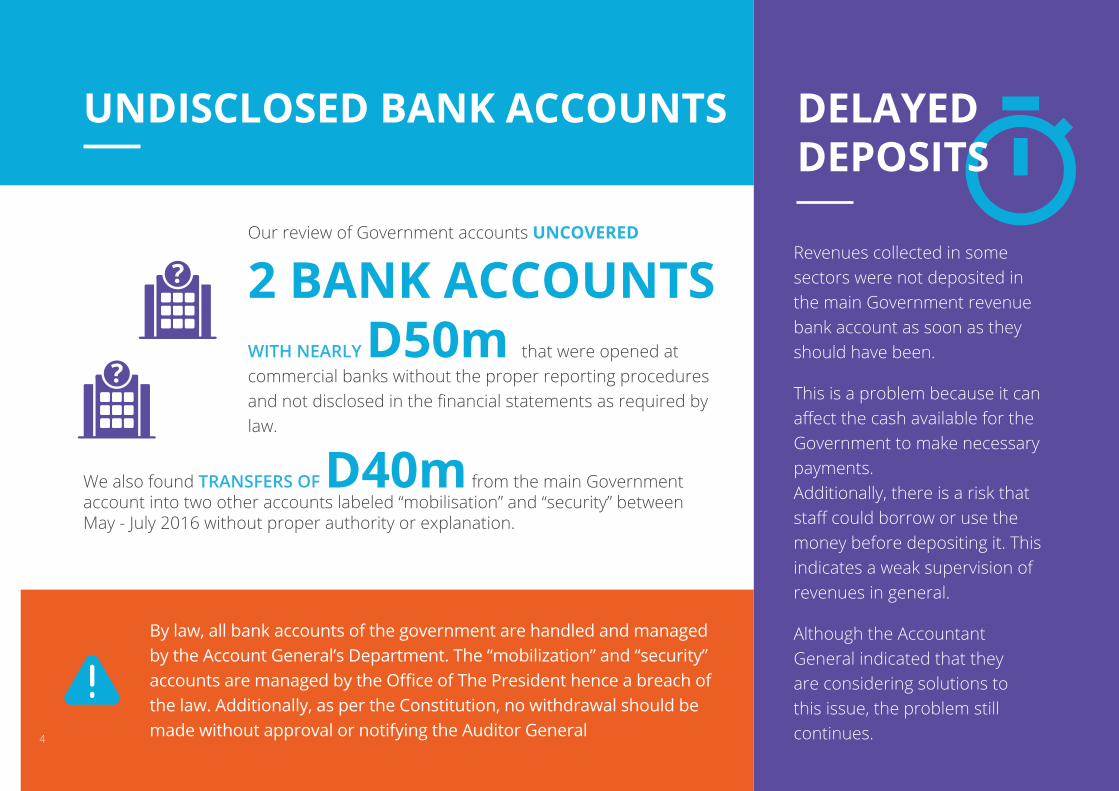

Revenues collected in some sectors were not deposited in the main Government revenue bank account as soon as they should have been.

This is a problem because it can affect the cash available for the Government to make necessary payments. Additionally, there is a risk that staff could borrow or use the money before depositing it. This indicates a weak supervision of revenues in general.

Although the Accountant General indicated that they are considering solutions to this issue, the problem still continues.

Our review of Government accounts UNCOVERED

2 BANK ACCOUNTS

WITH NEARLY D50m that were opened at commercial banks without the proper reporting procedures and not disclosed in the financial statements as required by law.

We also found TRANSFERS OF D40m from the main Government account into two other accounts labeled “mobilisation” and “security” between May - July 2016 without proper authority or explanation.

By law, all bank accounts of the government are handled and managed by the Account General’s Department. The “mobilization” and “security” accounts are managed by the Office of The President hence a breach of the law. Additionally, as per the Constitution, no withdrawal should be made without approval or notifying the Auditor General

DELAYED DEPOSITS

4

NO CONTINGENCY FUND

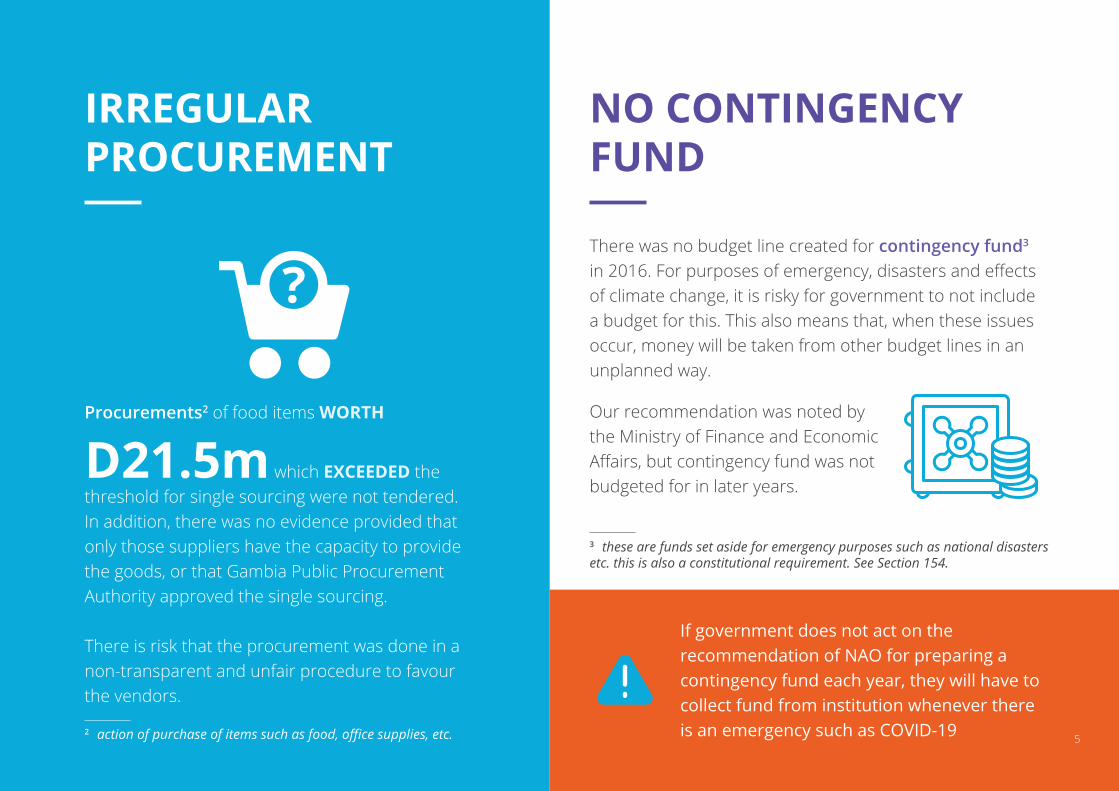

Procurements2 of food items WORTH

D21.5m which EXCEEDED the threshold for single sourcing were not tendered. In addition, there was no evidence provided that only those suppliers have the capacity to provide the goods, or that Gambia Public Procurement Authority approved the single sourcing.

There is risk that the procurement was done in anon-transparent and unfair procedure to favour the vendors.

There was no budget line created for contingency fund3 in 2016. For purposes of emergency, disasters and effects of climate change, it is risky for government to not include a budget for this. This also means that, when these issues occur, money will be taken from other budget lines in an unplanned way.

Our recommendation was noted by the Ministry of Finance and Economic Affairs, but contingency fund was not budgeted for in later years.

2 action of purchase of items such as food, office supplies, etc.

?

3 these are funds set aside for emergency purposes such as national disasters etc. this is also a constitutional requirement. See Section 154.

IRREGULARPROCUREMENT

If government does not act on the recommendation of NAO for preparing a contingency fund each year, they will have to collect fund from institution whenever there is an emergency such as COVID-19 5

UNANNOUNCED BUDGET CHANGES

About D61m WAS TAKEN from one institution to another without informing the entity from which the funds were initially budgeted for as required by the Financial Regulations.

In 2016, Funds were diverted from the following ministries: MoBSE, MoHERST, MoH and Ministry of Agriculture. There is a risk that the activities planned for that year in those institutions will be affected and the overall key operations of that entity.

We noted that grants amounting UP TO D1.3b were DISBURSED to various sectors but were not reported during the year.

This is an indication of poor communication between the two departments responsible and failure to comply with the Financial Regulations.

UNDISCLOSED SECTOR GRANTS

6

UNSUSTAINABLE DEBT

UNPAID LOANS BYCABINET MINISTERS

Public debt is consistently HIGHER THAN

200% of domestically generated government revenue, which is unsustainable as per the COMSEC, an internationally recognised benchmark for sustainability analysis.

With no debt ceiling or borrowing limits set by government, unsustainable debt levels with high interests will make it difficult for the country to obtain loans in the future.

Of D6.5m LOAN GIVEN to cabinet ministers for purchase of cars and building of houses,

ONLY D1.6m WAS REPAID within the stated agreement, as of 2017.

There is a risk that these loans will never be repaid as the beneficiaries are no longer in the services of Government.

While most beneficiaries have repaid their loans by the time this summarised report is out, there is a possibility of current and future government beneficiaries acquiring loans and not repaying, especially cabinet ministers who are constantly being changed

DEBT

7

Out of the 86 FINDINGS in the 2016 Auditor

General’s Report, MORE THAN 30 of them involved ISSUES of irregular accounting and inadequate documentation. The rest were internal policy and structural issues.

During auditing, there were a lot of irregularities in terms of reporting. This could mean that the government is not following financial reporting standards and frameworks. This could also lead to misstatements in the financial statements. E.g non-disclosure of loans secured by government and given to State Owned Enterprises (SOEs)4 by government.

OVERALL ACCOUNTING ERRORS

4 revenue generating institutions owned by the government. E.g. NAWEC, Gamtel, GRA, GPA, etc.

ERROR

just accounting and documentation issues

8

ABOUT THE NATIONAL AUDIT OFFICE (NAO)

HOW CAN THISSUMMARY BE USED?

The NAO is the Supreme Audit Institution of The Gambia responsible for auditing government accounts, accounts of the courts, National Assembly and all public enterprises. Including any institution where government has a minority interest5.

Our mandate is drawn from the 1997 Constitution of The Republic of The Gambia and NAO Act 2015. See sections 158-160 of the Constitution for more details about our office.

5 this refers to stakes or holdings in private institutions or projects etc

This summarised report can be used by the media, Civil Society Organizations and citizens working on Public Finance and Resource Management for advocacy and awareness raising.

It can also be used as resource material for trainings, workshops etc. This summarised report as well as the full report can also serve as research documents for students.

9

OUR BIGGEST CHALLENGES

Most of the offices we audit do not submit proper financial accounts. When they do, it is submitted very late in addition to slow responses for any additional information needed.

National Assembly does not always discuss our audit reports neither do they follow-up on recommendations mentioned in our reports for action and implementation.

Delay in printing of our reports affects submission timeline to the National Assembly.

For years, GoTG were not able to provide financial statements for auditing. 1991 -1995 accounts were completely audited in 2005, 2000-2005 audited in 2009 and so forth. Currently the office is working to catch up on the backlog with limited staff and resources.

We do not have all the capacity and resources to conduct our yearly audits as required by law.

Most of NAO’s work is done outside of our office, requiring transportation for staff to these work stations. Frequent commandeering of NAO vehicles by the police disrupts our services.

Presentation of reports to the NA by the Minister of Finance instead of the Auditor General. This undermines our independence and further contributes to reports not being discussed as they are not usually presented.

01. 02. 03. 04.

05. 06. 07.

10

THE AUDIT PROCESS

FINANCIALSTATEMENTS

1. Planning Auditees submit financial statements

We engage with them, agree timelines and request additional documentation if needed

We then review all the documents and discuss with auditees

Due to capacity, some auditees fail to produce standard financial statements, making the process longer than the stipulated time 11

Auditees take a lot of time to respond to our queries and sometimes they do not respond at all

2. Performing We carefully audit the financial statements and gather further evidence

Then we write audit queries (initial findings, questions and clarifications) and share with auditees

? ??? ?

?... ...

12

3. Reporting We conduct meetings with auditees on our findings and share a draft management letter6

We incorporate any auditee responses and additional information into our findings and recommendations

Then we finalise and print the final report and management letter

FINAL

REPORT

? ?? ...

DRAFT

DRAFTREPORT

6 Findings and issues in the audit report that are shared with management of institutions for implementation. this is also shared with NA along with the report. 13

4. Submission and Presentation We submit the report and management letter to the National Assembly

We then participate in the relevant National Assembly committee (FPAC) hearing where:

1. The Minister of Finance presents the report

2. The committee members discuss it and then ask questions

3. AG and NAO staff provide additional information and answer questions as experts

Many reports submitted to the National Assembly (including this 2016 report) have not been discussed for a long time, reducing the relevance and impact of findings

FINALREPORT FINALREPORT

......

14

5. Publication We publish the report for the general public on our website

We also send report to the national library

Reports are now also developed into summarised versions for dissemination

As per the 1997 Constitution, reports cannot be published unless discussed by the National Assembly. Although, the AG can publish if there is undue delay in discussing the report by the NA.

None of the performance audit reports submitted to the NA have been discussed. 15

6. Follow-Up National Assembly, Internal Audit, and other oversight actors in government track and push for implementation of recommendations

Auditees act on audit recommendations and findings

We review implementation progress and include outstanding recommendations in the next audits

For greater impact, improved management of public funds and mitigation of fraud, National Assembly and CSOs should ensure that recommendations are implemented by government

Get to know more about our work ...

In 2016, we conducted several other financial and performance audits. In addition to the GoTG 2016 Audit Report, we also submitted to the NA and published on our website the following Performance Audit Reports:

1.HIV/AIDS Prevention, Treatment, care and Support Programmes by National Aids Secretariat in The Gambia; and

2. Solid Waste Management by The Banjul City Council (BCC)