summary in finance, mba20011 summary of courses in finance (state exam) mihály ormos

TRANSCRIPT

Summary in finance, MBA2001 1

Summary of Coursesin Finance

(State Exam)

Mihály Ormos

Summary in finance, MBA2001 2

Some Words on the State Exam

20 questions in four different blocks (subjects)–Basics of Business Economics (3 Theorems)

–Accounting (3 Theorems)

–Corporate Finance (9 Theorems)

–Macro-Finance (5 Theorems)Only one out of twenty should be drawn4 - 5 for the answerConversationCoherent knowledgePreparation timeTwo or three different boards, with two membersImmediate mark as in the course unit exam

Summary in finance, MBA2001 3

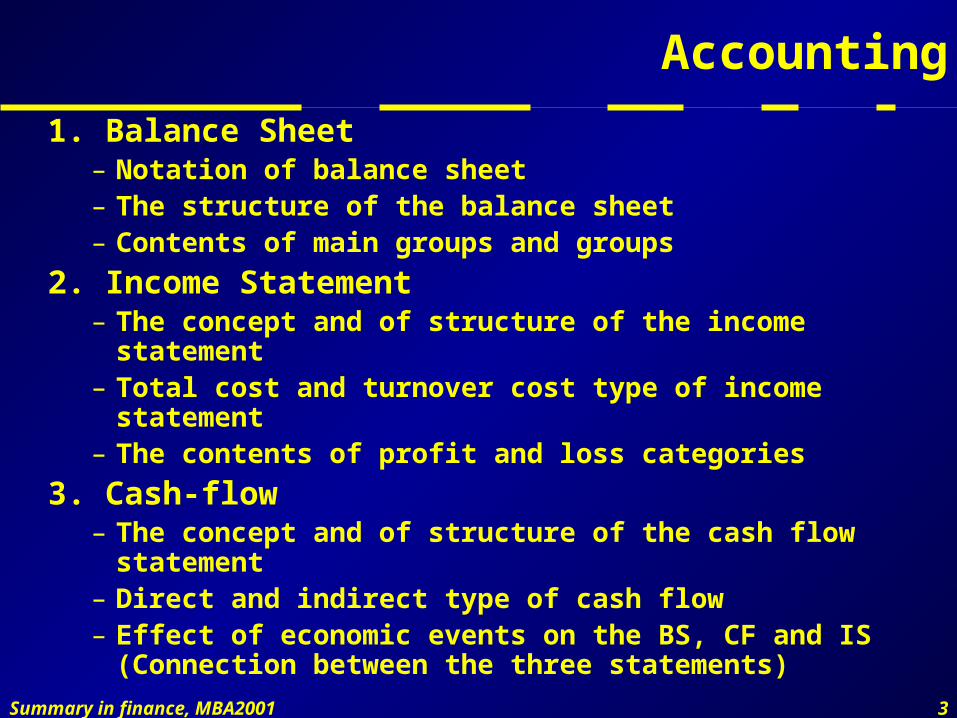

Accounting

1. Balance Sheet– Notation of balance sheet– The structure of the balance sheet– Contents of main groups and groups

2. Income Statement– The concept and of structure of the income statement– Total cost and turnover cost type of income statement– The contents of profit and loss categories

3. Cash-flow– The concept and of structure of the cash flow statement– Direct and indirect type of cash flow– Effect of economic events on the BS, CF and IS

(Connection between the three statements)

Summary in finance, MBA2001 4

Accounting

Summary in finance, MBA2001 5

Balance Sheetas the Part of the Financial Report (Statement)

Report

Analytical records

Documents (i.e. invoices)

Ledger(Continuous record of

economic events)

Balance SheetIncome StatementNotes to the ReportBusiness Report

Disclosure

Ord

er o

f doc

umen

tsAudit

Stocktaking

Summary in finance, MBA2001 6

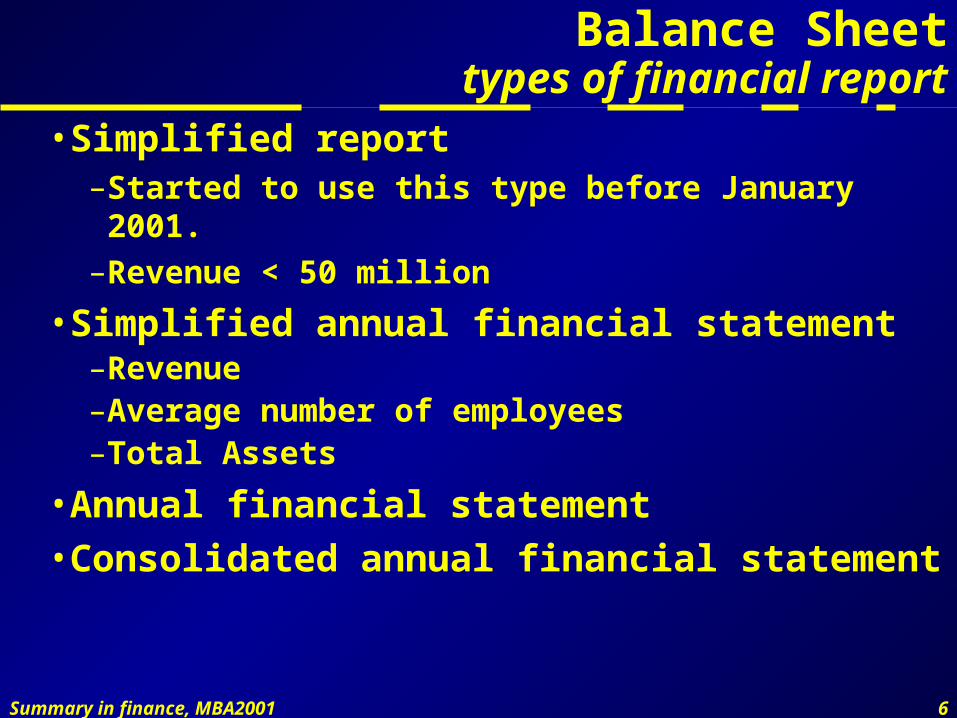

Balance Sheettypes of financial report

• Simplified report–Started to use this type before January 2001.

–Revenue < 50 million

• Simplified annual financial statement–Revenue–Average number of employees–Total Assets

•Annual financial statement•Consolidated annual financial statement

Summary in finance, MBA2001 7

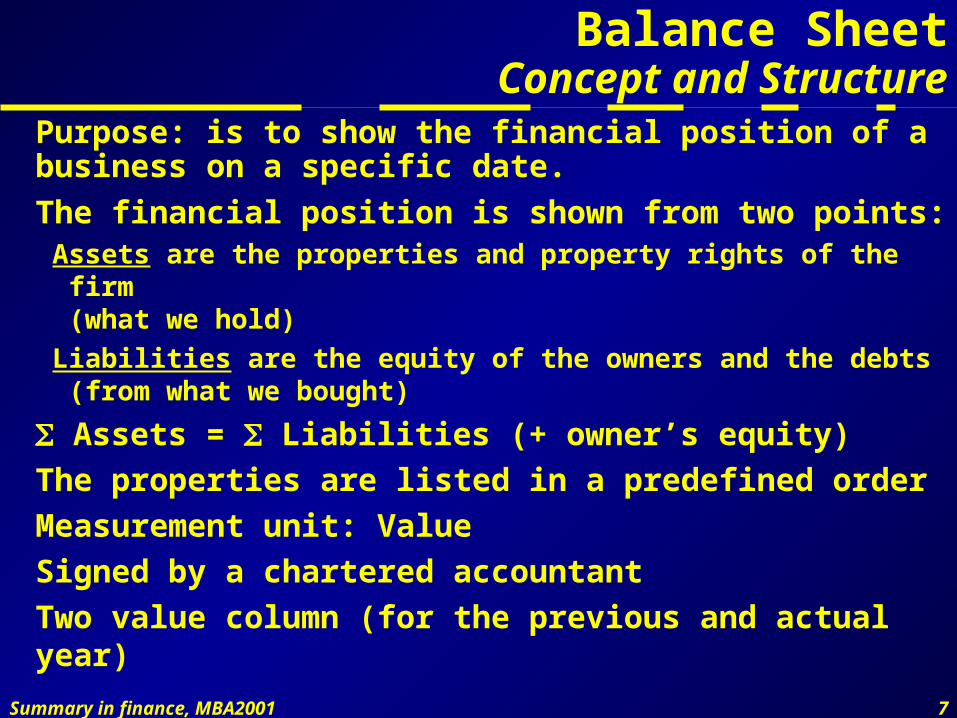

Balance SheetConcept and Structure

Purpose: is to show the financial position of a business on a specific date.

The financial position is shown from two points:Assets are the properties and property rights of the firm

(what we hold)

Liabilities are the equity of the owners and the debts(from what we bought)

Assets = Liabilities (+ owner’s equity)

The properties are listed in a predefined order

Measurement unit: Value

Signed by a chartered accountant

Two value column (for the previous and actual year)

Summary in finance, MBA2001 8

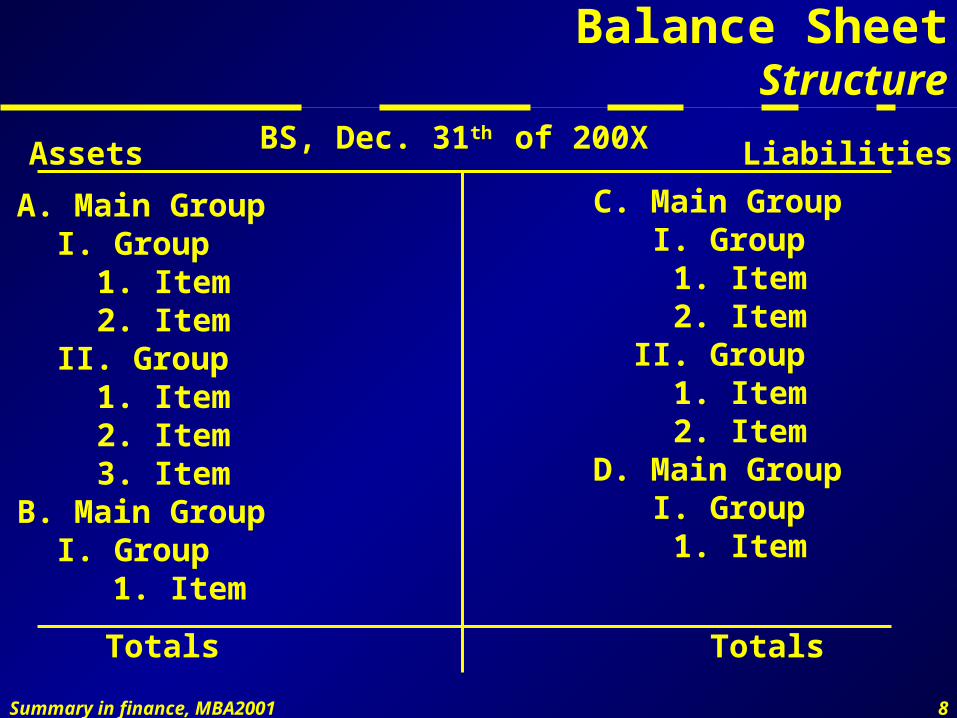

Balance Sheet Structure

BS, Dec. 31th of 200X LiabilitiesAssets

A. Main GroupI. Group

1. Item2. Item

II. Group1. Item2. Item3. Item

B. Main GroupI. Group

1. Item

C. Main Group I. Group

1. Item2. Item

II. Group1. Item2. Item

D. Main Group I. Group

1. Item

Totals Totals

Summary in finance, MBA2001 9

Balance SheetMain Groups and Groups

Balance Sheet, 200X. Dec.. 31. LiabilitiesAssets

A. Fixed AssetsB. Current AssetsC. Accrued Incomes and prepaid expenses

D. Owners equityE. ProvisionsF. Liabilities (Debts)G. Passive Accruals and deferred items

Total Assets Total liabilities

Summary in finance, MBA2001 10

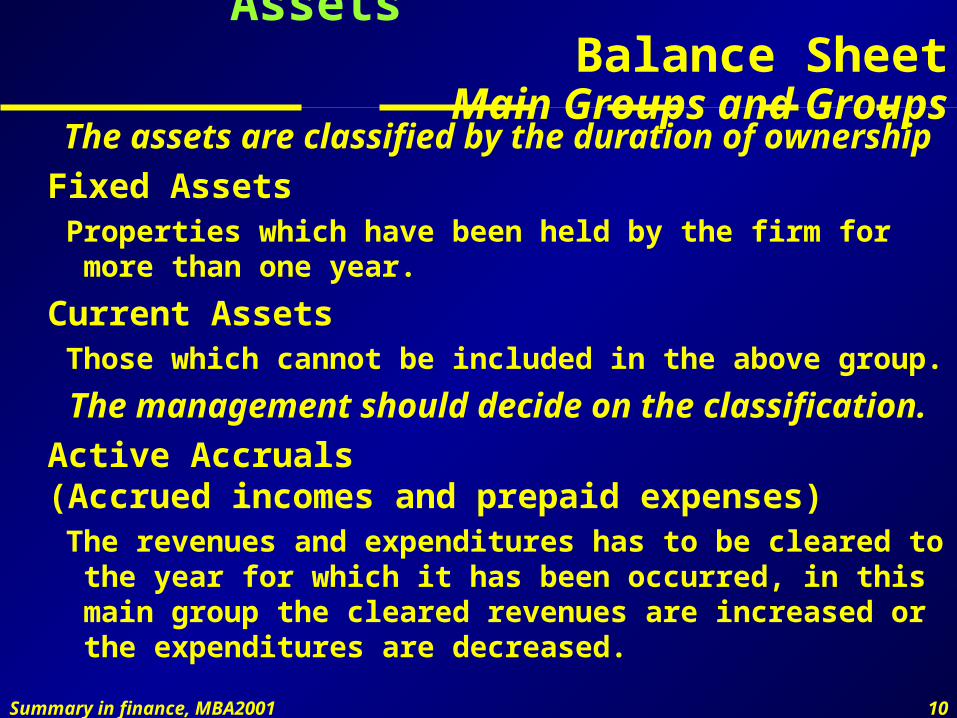

Assets Balance SheetMain Groups and Groups

The assets are classified by the duration of ownership

Fixed AssetsProperties which have been held by the firm for more than one

year.

Current AssetsThose which cannot be included in the above group.

The management should decide on the classification.

Active Accruals(Accrued incomes and prepaid expenses)

The revenues and expenditures has to be cleared to the year for which it has been occurred, in this main group the cleared revenues are increased or the expenditures are decreased.

Summary in finance, MBA2001 11

Liabilities Balance SheetMain Groups and Groups

Shareholder’s EquityCapital which is placed at owner's disposal for permanent use.

ProvisionsProvisions are liabilities, which created in charge of the

Earnings Before Interest and Tax (EBIT) by definition, so it formulate transition between shareholder's equity and liabilities.

Liabilitiesare acknowledged debts that has to be performed in money

Passive Accruals(Deferred incomes and accrued expenses)

in this main group the cleared revenues are decreased or the expenditures are increased.

Summary in finance, MBA2001 12

Balance SheetMain Groups and Groups

Balance Sheet, 200X. Dec.31. LiabilitiesAssetsA. Fixed Assets

I. Intangible AssetsII.Tangible AssetsIII. Invested Financial Assets

B. Current AssetsI. InventoriesII. ReceivablesIII. SecuritiesIV. Cash

C. Active accruals

D. EquityI. Subscribed CapitalII. Unpaid Subscribed CapitalIII. Capital ReserveIV. Committed ReserveV. Accumulated profit ReserveVI. Evaluation ReserveVII. Retained Earnings

E. ProvisionF. Liabilities

I. Junior DebtII. Long-term DebtIII. Short-term Debt

G. Passive Accruals

Total Assets Total Liabilities

Summary in finance, MBA2001 13

Fixed Balance SheetAssets Main Groups and Groups

Intangible assetsTradable, non-material assets which permanently (for more than

one year) serve the firm.Constituents

Rights representing pecuniary value, Goodwill, Intellectual product,

R&D, Value of establishment or reorganisation, Revaluation upwards

Tangible assetsMaterial assets which directly or indirectly and permanently

serve the company.Constituents

Land, buildings and connecting property rights, Machinery and equipment, Other equipment, Investments, Advance payments towards investments, Revaluation upwards

Depreciation

Summary in finance, MBA2001 14

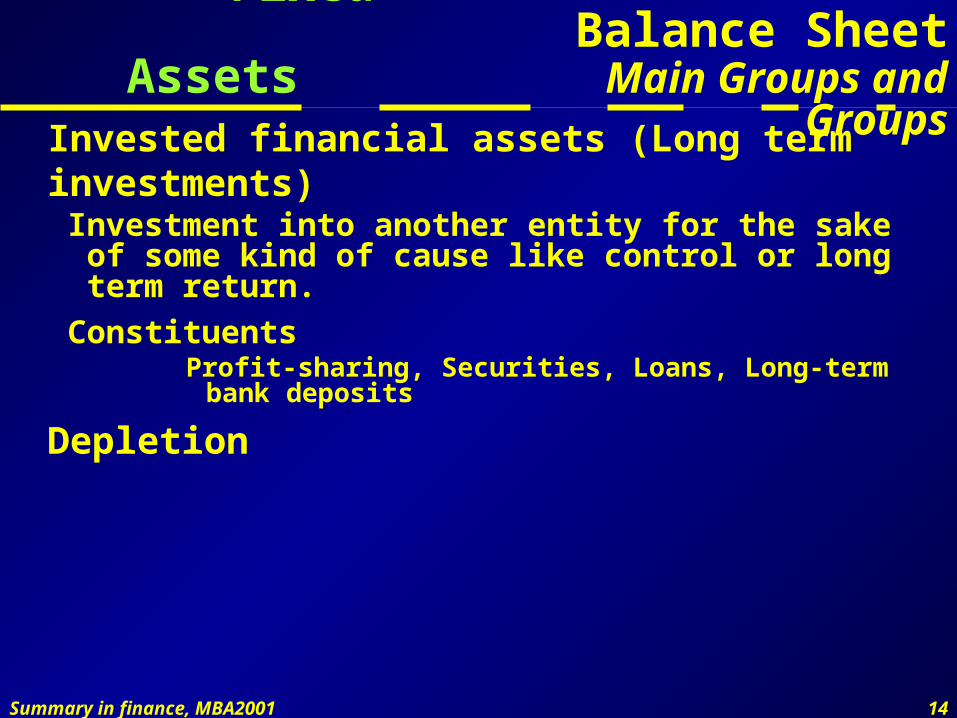

Fixed Balance SheetAssets Main Groups and Groups

Invested financial assets (Long term investments)Investment into another entity for the sake of some kind of

cause like control or long term return.

ConstituentsProfit-sharing, Securities, Loans, Long-term bank deposits

Depletion

Summary in finance, MBA2001 15

Current Balance SheetAssets Main Groups and Groups

InventoriesThose current assets, which can be stocked, and have

quantitative measure, likeStock (in hand),Goods,Advance payments made towards inventories,Livestock,Work in progress and semi-finished products,Finished products

ReceivablesContractual claims that acknowledged by the partner.Constituents

Accounts receivable (buyers),Draft receivables,(Unpaid issued capital),Other receivables

Summary in finance, MBA2001 16

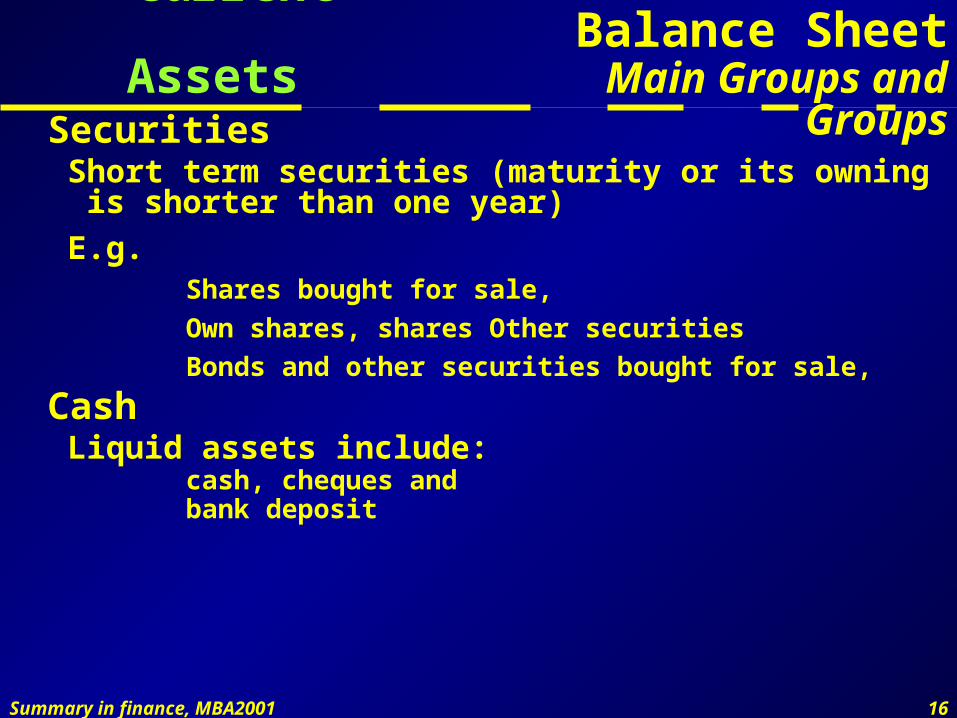

Current Balance SheetAssets Main Groups and Groups

SecuritiesShort term securities (maturity or its owning is shorter than one

year)

E.g.Shares bought for sale,

Own shares, shares Other securities

Bonds and other securities bought for sale,

CashLiquid assets include:

cash, cheques and bank deposit

Summary in finance, MBA2001 17

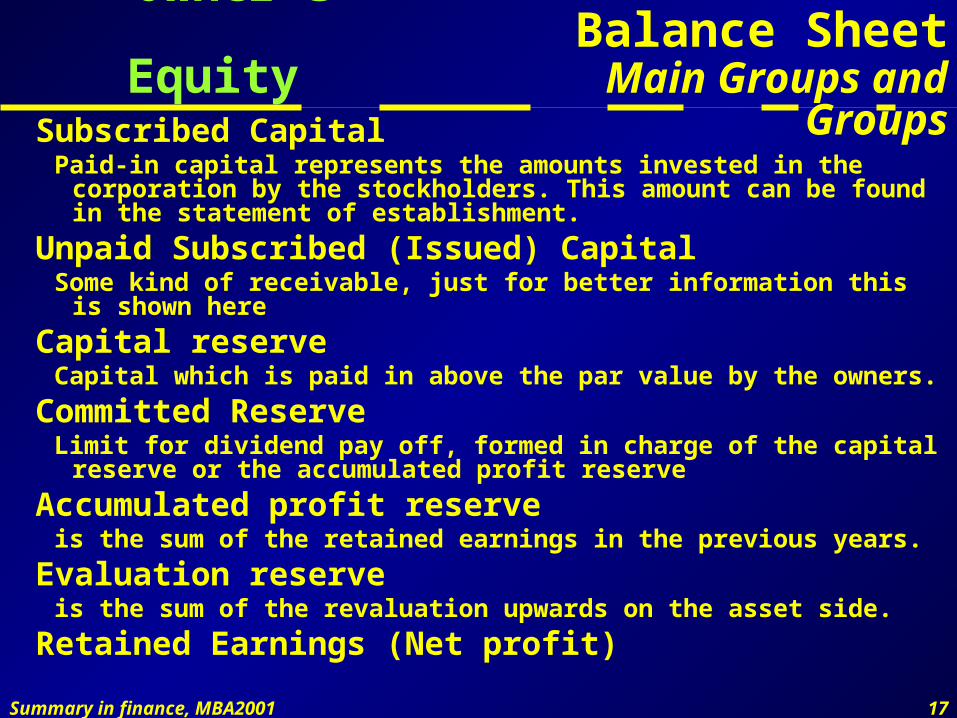

Owner’s Balance SheetEquity Main Groups and Groups

Subscribed CapitalPaid-in capital represents the amounts invested in the corporation by the

stockholders. This amount can be found in the statement of establishment.

Unpaid Subscribed (Issued) CapitalSome kind of receivable, just for better information this is shown here

Capital reserveCapital which is paid in above the par value by the owners.

Committed ReserveLimit for dividend pay off, formed in charge of the capital reserve or the

accumulated profit reserve

Accumulated profit reserveis the sum of the retained earnings in the previous years.

Evaluation reserveis the sum of the revaluation upwards on the asset side.

Retained Earnings (Net profit)

Summary in finance, MBA2001 18

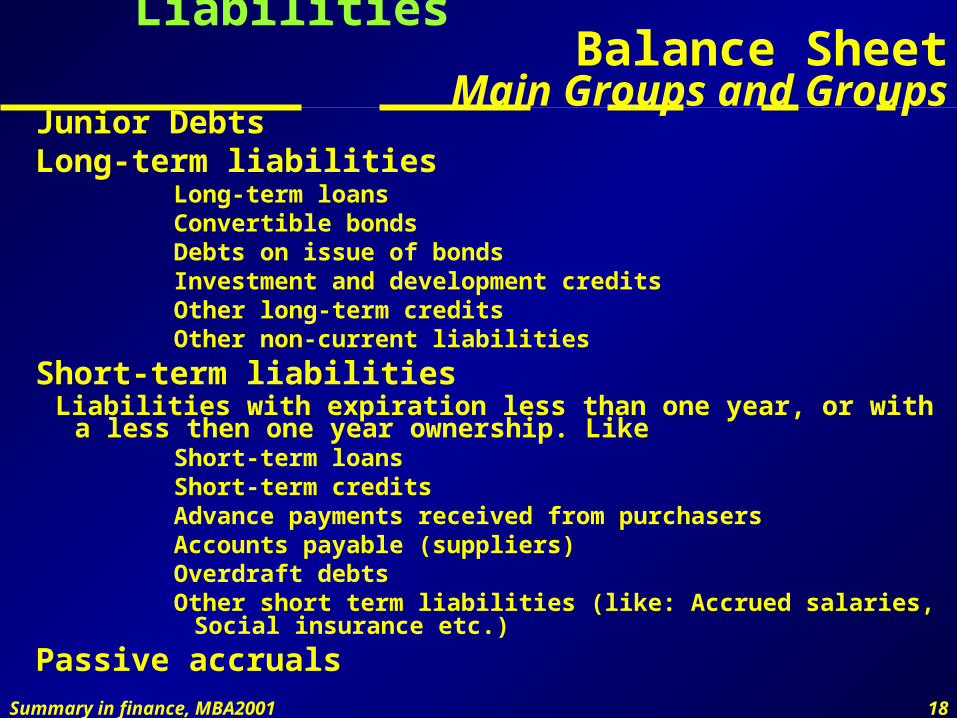

Liabilities Balance SheetMain Groups and Groups

Junior DebtsLong-term liabilities

Long-term loansConvertible bondsDebts on issue of bondsInvestment and development creditsOther long-term creditsOther non-current liabilities

Short-term liabilitiesLiabilities with expiration less than one year, or with a less then one year

ownership. LikeShort-term loansShort-term creditsAdvance payments received from purchasersAccounts payable (suppliers)Overdraft debtsOther short term liabilities (like: Accrued salaries, Social insurance etc.)

Passive accruals

Summary in finance, MBA2001 19

Income Statement As the Part of the Financial Report

Report

Analytical records

Documents (i.e. invoices)

Ledger(Continuous record of

economic events)

Balance SheetIncome StatementNotes to the ReportBusiness Report

Disclosure

Summary in finance, MBA2001 20

Income Statement Concept and Structure

The income statement shows the difference of the annual revenues and expenditures.

Uniform structure, predefined earning categories.

It gives information on the profit gaining capability of the firm.

It is a report about the derivation of retained earnings.

By the law of accounting:“The profit and loss account shall contain the breakdown of the entrepreneur's balance-sheet net profit figure, that is the after-tax profit retained by the entrepreneur, the main factors influencing the development of profits and losses,...“

Summary in finance, MBA2001 21

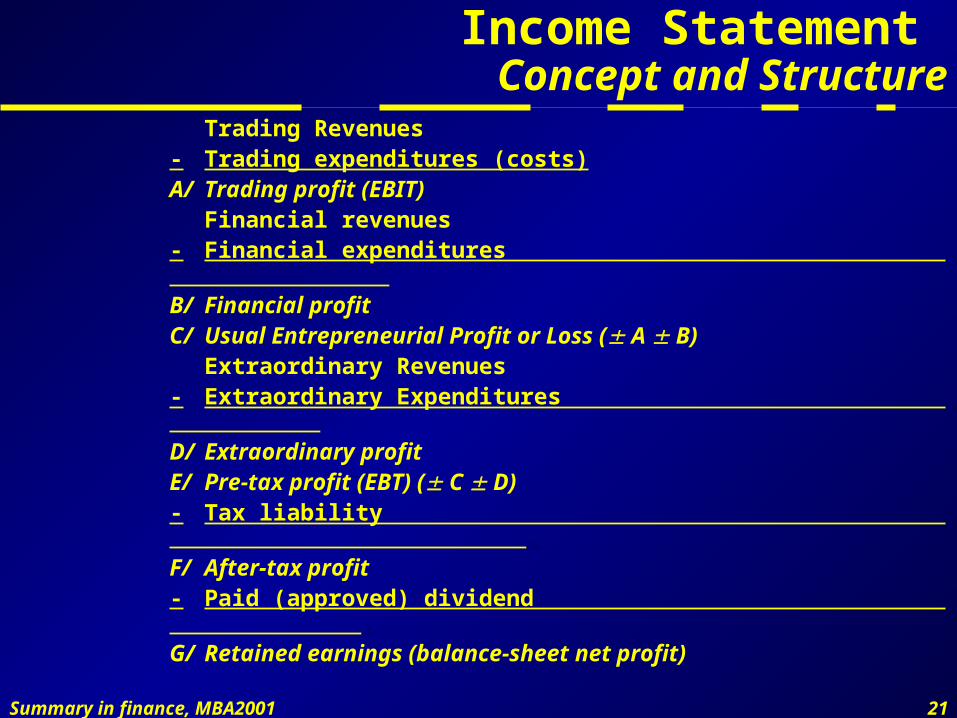

Income Statement Concept and Structure

Trading Revenues- Trading expenditures (costs)A/ Trading profit (EBIT)

Financial revenues- Financial expenditures .B/ Financial profitC/ Usual Entrepreneurial Profit or Loss ( A B)

Extraordinary Revenues- Extraordinary Expenditures .D/ Extraordinary profitE/ Pre-tax profit (EBT) ( C D)- Tax liability .F/ After-tax profit - Paid (approved) dividend .G/ Retained earnings (balance-sheet net profit)

Summary in finance, MBA2001 22

Income Statement Types

In Hungary:–Total Costs profit and loss account procedure (“A”)

–Turnover costs profit and loss account procedure (“B”)

(US, UK GAAP: single step and multiple step)

The differences between the two types can be found in the derivation of the trading profit.

Summary in finance, MBA2001 23

Income Statement Types

Total cost typeNet sales revenues

Other revenues

Capitalised value of own performance

Trading Incomes

Annual total costs

Other expenditures

Trading expenditures .

A/ Trading (Business) profit

Turnover cost typeNet sales revenues

Other revenues

Trading incomes

Costs of sales

Other expenditures

Trading expenditures .

A/ Trading (Business) profit

Summary in finance, MBA2001 24

Net sales Income Statement

Revenues TypesThe consideration –value of sold inventories (products, materials, good etc), and

services performed,

–accepted by the partner,

–not including the VAT

– increased by the subsidies and extra charges and

–reduced by consumption tax and any reductions shall be entered as net revenues

• Net Domestic Sales Revenue• Net Export Sales Revenue

Revenues Cash inflow

Summary in finance, MBA2001 25

Other Income Statement

Revenues TypesOther revenues are revenues not forming part of the net sales revenues which arise in the course of regular activity (business), like:–Received compensation–Received penalty–Revenues from intangible and tangible asset sold–Utilisation of the previous year’s provisions formed

Summary in finance, MBA2001 26

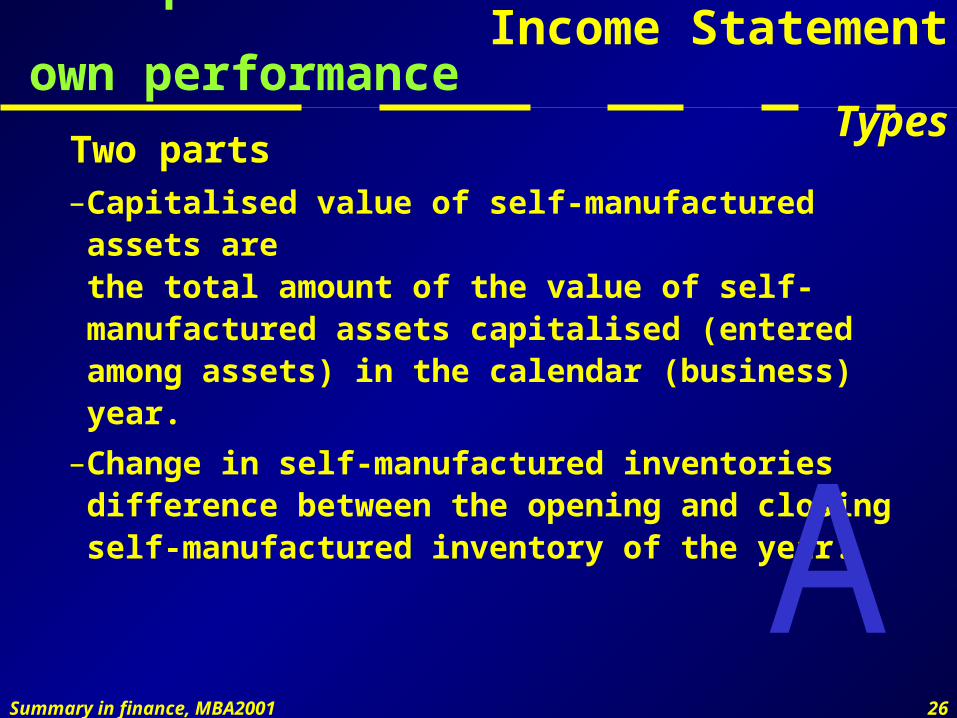

Capitalised value of Income Statementown performance Types

Two parts–Capitalised value of self-manufactured assets are

the total amount of the value of self-manufactured assets capitalised (entered among assets) in the calendar (business) year.

–Change in self-manufactured inventoriesdifference between the opening and closing self-manufactured inventory of the year.

A

Summary in finance, MBA2001 27

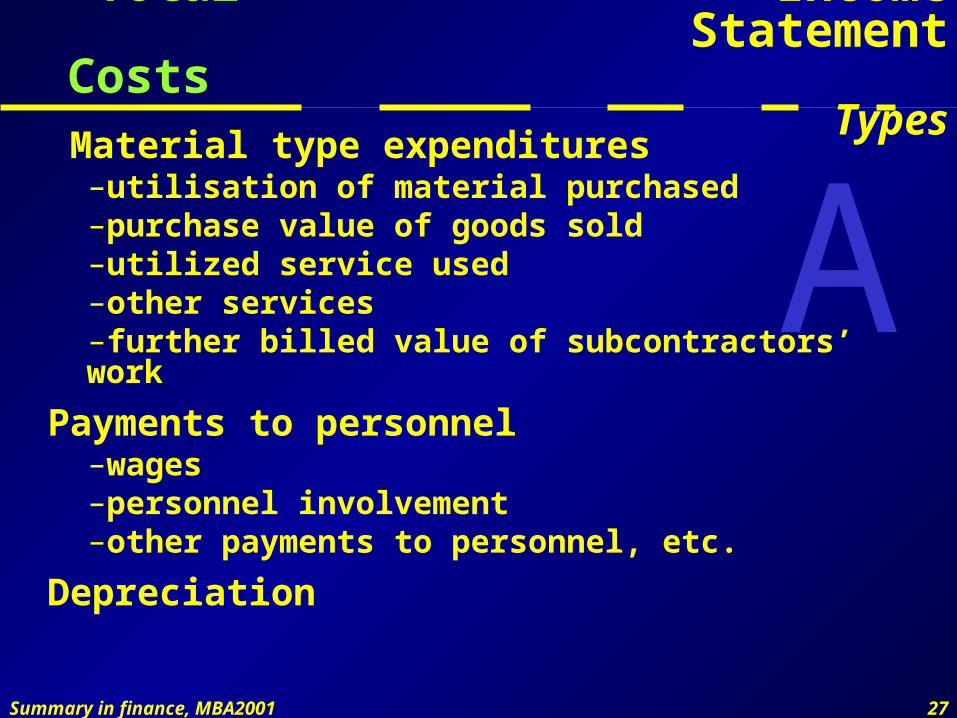

Total Income StatementCosts Types

Material type expenditures–utilisation of material purchased–purchase value of goods sold–utilized service used–other services–further billed value of subcontractors’ work

Payments to personnel–wages–personnel involvement–other payments to personnel, etc.

Depreciation

A

Summary in finance, MBA2001 28

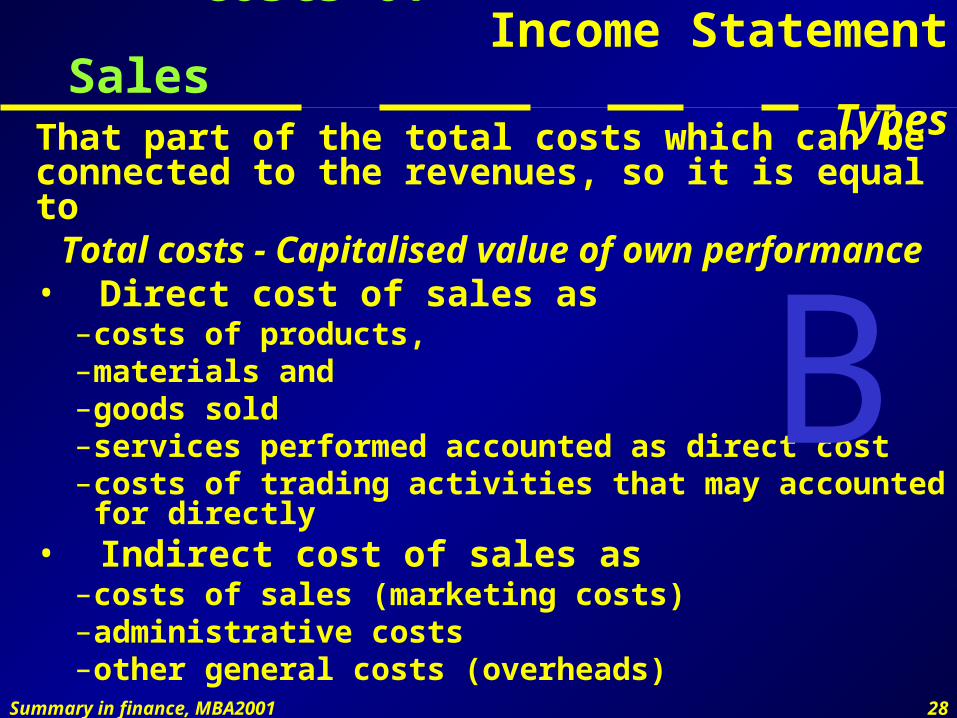

Costs of Income StatementSales Types

That part of the total costs which can be connected to the revenues, so it is equal to

Total costs - Capitalised value of own performance• Direct cost of sales as–costs of products,–materials and–goods sold– services performed accounted as direct cost–costs of trading activities that may accounted for directly

• Indirect cost of sales as–costs of sales (marketing costs)–administrative costs–other general costs (overheads)

B

Summary in finance, MBA2001 29

Other Income StatementExpenditures Types

Other expenditures are costs and payments not connected directly or indirectly to the net sales revenues which are incurred in the course of the regular activity (business).–Paid compensation–Paid penalty–Expenditures of (i.e. book value) of intangible and tangible

asset sold–Provisions formed–etc.

Summary in finance, MBA2001 30

Comparison Income Statementof the two types Types

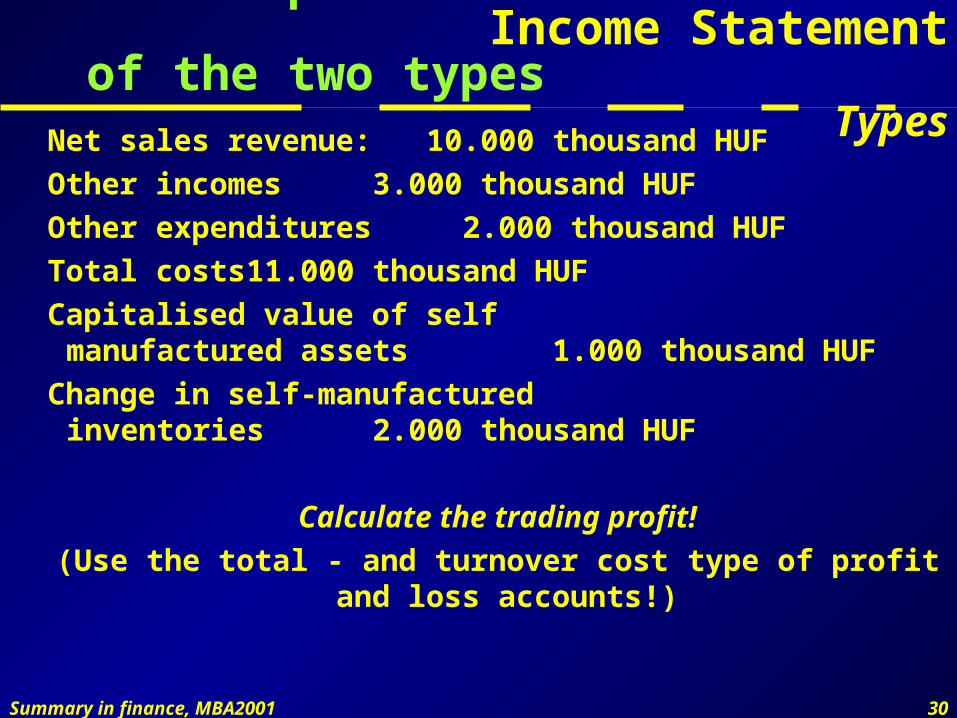

Net sales revenue: 10.000 thousand HUF

Other incomes 3.000 thousand HUF

Other expenditures 2.000 thousand HUF

Total costs 11.000 thousand HUF

Capitalised value of selfmanufactured assets 1.000 thousand HUF

Change in self-manufacturedinventories 2.000 thousand HUF

Calculate the trading profit!

(Use the total - and turnover cost type of profit and loss accounts!)

Summary in finance, MBA2001 31

Comparison Income Statementof the two types Types

1. Calculate the capitalised value of own performance:1000+2000=3000 thousand HUF

2. Determine the costs of sales:11000-3000=8000 thousand HUF

Type „A”Net sales revenues 10000

Other revenues 3000

Capitalised value of own performance 3000

Trading Incomes 16000

Yearly total costs 11000

Other expenditures 2000

Trading expenditures 13000.

A/ Trading (Business) profit 3000

Type „B”Net sales revenues 10000

Other revenues 3000

.

Trading incomes 13000

Costs of sales 8000

Other expenditures 2000

Trading expenditures 10000 .

A/ Trading (Business) profit 3000

Summary in finance, MBA2001 32

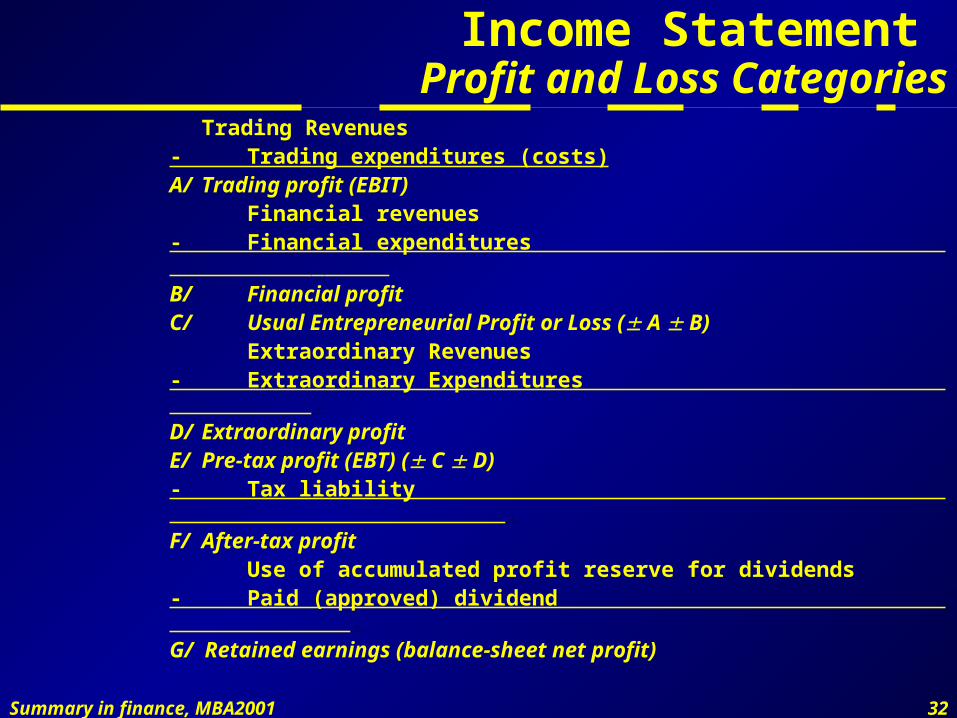

Income Statement Profit and Loss Categories

Trading Revenues- Trading expenditures (costs)A/ Trading profit (EBIT) Financial revenues- Financial expenditures .B/ Financial profitC/ Usual Entrepreneurial Profit or Loss ( A B) Extraordinary Revenues- Extraordinary Expenditures .D/ Extraordinary profitE/ Pre-tax profit (EBT) ( C D)- Tax liability .F/ After-tax profit Use of accumulated profit reserve for dividends- Paid (approved) dividend .G/ Retained earnings (balance-sheet net profit)

Summary in finance, MBA2001 33

Financial Income StatementProfit Profit and Loss Categories

Financial profit is the difference of the revenues and expenditures of financial transactions.

Financial revenues:– interest received– interest related revenues–dividends–profit-sharing–other revenues of financial transactions

Financial expenditures– interest paid– interest related payments–write-off (depletion) of financial investments dividends–other expenditures of financial transactions

Summary in finance, MBA2001 34

Usual Entrepreneurial Income StatementProfit or Loss Profit and Loss Categories

The sum of the trading (business) profit or loss and the financial profit or loss.

Gives information on the profit gaining capability of the firm’s normal course of activity.

Summary in finance, MBA2001 35

Extraordinary Income StatementProfit Profit and Loss Categories

Extraordinary profit figure is the difference of the extraordinary revenues and extraordinary expenditures.

Extraordinary revenues and extraordinary expenditures are independent of the entrepreneurial activity i.e. fall outside of the entrepreneur’s normal course of business, they are listed in the law of accounting.

Summary in finance, MBA2001 36

Cash-Flow Concept and Structure

The statement of cash-flows focuses on cash receipts and cash payments, so the main question to be answered is:

Did the company’s cash balance increase or decrease during the year and, why?

The statement shows why cash changed over the period by reporting net cash provided or used by–operating activities,–investing activities and–financing activities.

Summary in finance, MBA2001 37

Cash-Flow Direct and indirect method

Direct methodinvolves listing each major class of cash receipts transactions and cash disbursements transactions for each of the three activity areas.The operating activity transactions include cash received from customers, cash paid to merchandise or raw material suppliers, cash paid to employees for salaries or wages, and cash paid for other operating expenses etc.

Indirect methodThis method shows the net incomes as the first source of operating cash,derives cash flows from operating activities by explaining the CHANGE in each of the non-cash operating accounts in the balance-sheet.

Summary in finance, MBA2001 38

Direct Cash-Flowmethod Structure

Cash-flows from operating activitiesCash received from customersCash paid to suppliersPayments for compensation of employeesOther operating expenses paidInterest paidTaxes paid .Net cash provided by operating activities

Cash-flows from investing activitiesProceeds from sale of landInvestment in plant and equipment .Net cash used for investing activities

Cash flows from financing activitiesAdditional long-term borrowingPayment of long-term debtPurchase of treasury stockPayment of dividends on common stocks .Net cash used for financing activities

Summary in finance, MBA2001 39

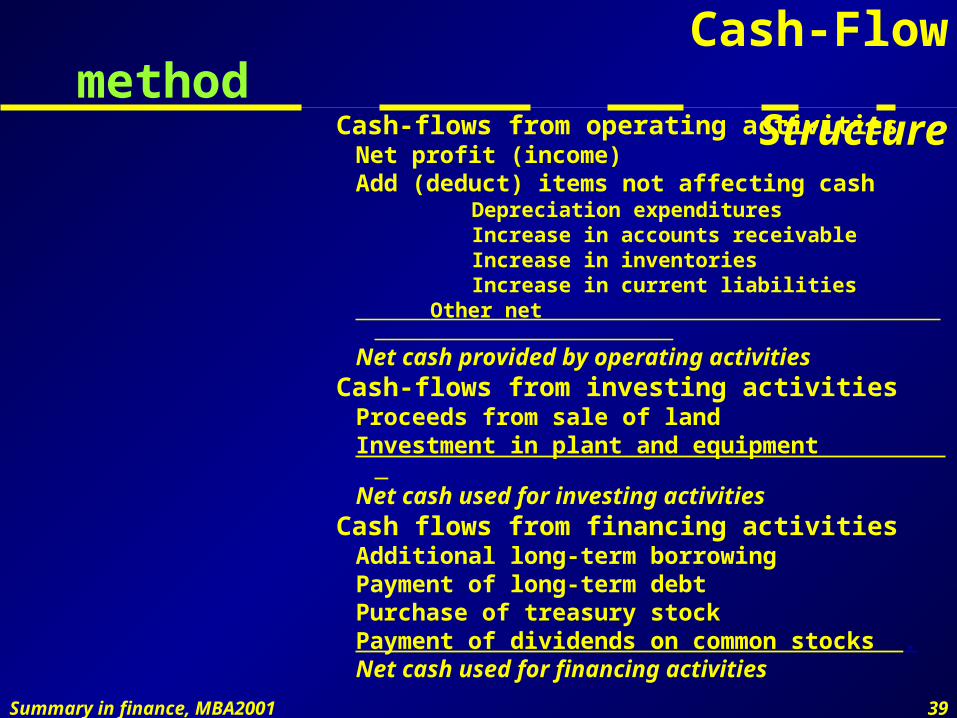

Indirect Cash-Flowmethod Structure

Cash-flows from operating activitiesNet profit (income)Add (deduct) items not affecting cash

Depreciation expendituresIncrease in accounts receivableIncrease in inventoriesIncrease in current liabilities

Other net .Net cash provided by operating activities

Cash-flows from investing activitiesProceeds from sale of landInvestment in plant and equipment .Net cash used for investing activities

Cash flows from financing activitiesAdditional long-term borrowingPayment of long-term debtPurchase of treasury stockPayment of dividends on common stocks .Net cash used for financing activities

Summary in finance, MBA2001 40

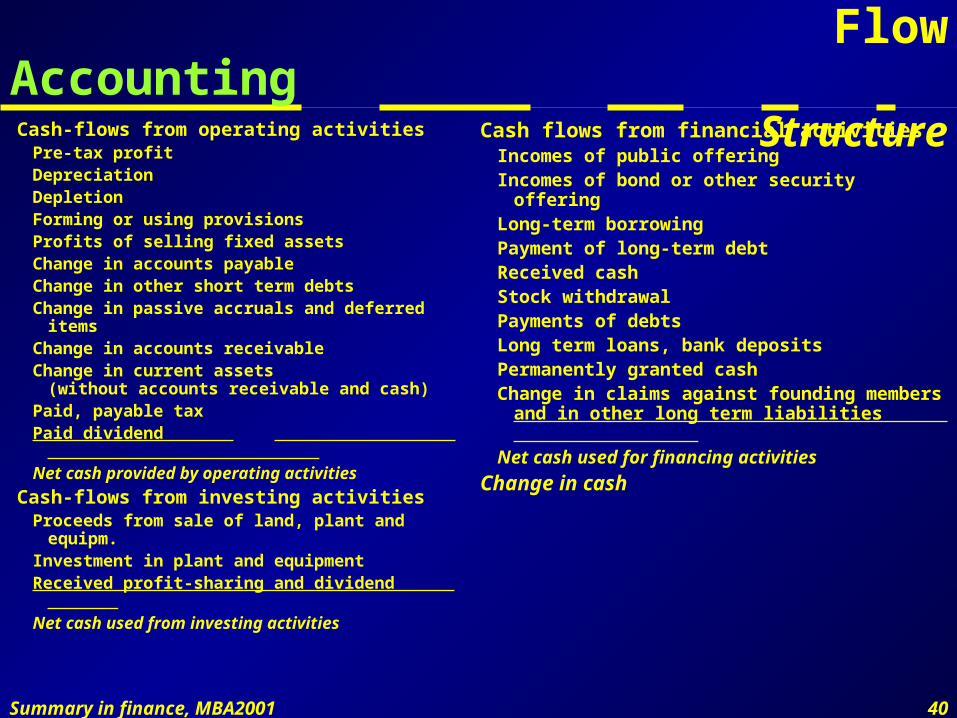

Law of Cash-FlowAccounting StructureCash-flows from operating activities

Pre-tax profitDepreciationDepletionForming or using provisionsProfits of selling fixed assetsChange in accounts payableChange in other short term debtsChange in passive accruals and deferred itemsChange in accounts receivableChange in current assets

(without accounts receivable and cash)Paid, payable taxPaid dividend .Net cash provided by operating activities

Cash-flows from investing activitiesProceeds from sale of land, plant and equipm.Investment in plant and equipmentReceived profit-sharing and dividend .Net cash used from investing activities

Cash flows from financial activitiesIncomes of public offeringIncomes of bond or other security offering Long-term borrowingPayment of long-term debtReceived cashStock withdrawalPayments of debtsLong term loans, bank depositsPermanently granted cashChange in claims against founding members

and in other long term liabilities .Net cash used for financing activities

Change in cash

Summary in finance, MBA2001 41

Cash-FlowConnection between the CF, the IS, and the BS

Balance sheet vs. income statement:–Retained earnings can be found in both statements

–Change in cash cannot be seen in the profit and loss account

Cash-flowthis statement can be compiled from the data presented in the

balance-sheet and income statement

Both the balance-sheet and income statement use accrual accounting (recognises revenue when it is earned, expenses when they are incurred) while the cash-flow uses cash-flow accounting (recognises transactions when cash has been received or paid).

Summary in finance, MBA2001 42

An economic evente.g. provision

IS:Cleared as other expenditure, so decreasing the pre-tax profit

BS:Increasing in provision

Decreasing in retained earnings

CF:The pre-tax profit is decreased (-)

Provisions formed (+)