summer project report 2012

TRANSCRIPT

i

DECLARATION

I, Ritesh Biharilal Sarve, a student of MBA (Power Management) 2011-13 batch at Centre for

Advanced Management and Power Studies (CAMPS), NPTI, Faridabad, Roll No.

1120812256,completed my summer internship of eight weeks at Rural Electrification

Corporation Ltd, hereby declare that Summer Internship Report titled “A) Entity Appraisal

and Project Appraisal of Private Transmission Project in Western Grid and B) Financing &

Implementation of RAPDRP scheme in Amritsar under PSPCL” is an original work and the

same has not been submitted to any other institute for award of any other degree.

A Seminar presentation of the Training report was made on 31/08/12 and the suggestions as

approved by the faculty were duly incorporated.

Presentation In-charge Ritesh Biharilal Sarve

NPTI, Faridabad MBA in Power Management

NPTI, Faridabad

Counter Signature

(Director/Principal of the institute)

ii

ACKNOWLEDGEMENT

Words often fail to pay one‟s gratitude oneself, still I would like to convey my sincere thanks

to the people who helped and extended their support in this Endeavour.

I would like to express my sincere thanks to Mr. Sanjeev Kumar Gupta, G.M. T&D, for

providing me with an opportunity to gain such an enriching exposure in this esteemed

Organization.

I also express my thanks to all the staff at REC, from all departments I got in touch with,

specially Mrs. H.K.Chani, Chief Manager (T&D) for providing us scholarly guidance

throughout the project which helped me to develop an insight into the project topic through

personal consultations. Without whom this dissertation would not have been possible. I

would also like to thanks Mrs. Valli Natarajan, DGM (T&D), Mr. Vivek aggarwal, Dy.

Manager (T&D), Mr. Debashish Mitra, Dy Manager (T&D) and Mr. Raman Garg, Engineer

(T&D) for their valuable inputs in completion of this project.

I also express my gratitude to my college authority and Mr. J.S.S. Rao, Principal Director,

National Power Training Institute, Mr. S.K. Choudhary, Principal Director, (CAMPS) NPTI

& Mrs. Manju Mam, Mrs. Indu Maheshwari, & Mr. Rohit Verma, Dy. Director,NPTI & Mr.

Amit Mishra, Asst.Director, NPTI for arranging my summer internship program with Rural

Electrification Corporation Ltd.

Ritesh Biharilal Sarve

10th

Batch

MBA (Power Management)

National Power Training Institute

iii

EXECUTIVE SUMMARY

The Mission of the Government is to provide quality power to all at reasonable rates.

The enactment of the Electricity Act in June 2003 was a major milestone, which paved the

way for development of the power sector within a competitive and liberal framework while

protecting the interests of the consumers, as well as creating a conducive environment for

attracting investments in the sector.

To ensure that the benefits of the increased availability of power reaches the poorest of the

poor living in the rural areas, the Government has implemented the Rajiv Gandhi Grameen

Vidyutikaran Yojana with vigour and determination. The Government‟s R-APDRP initiative

aims at reducing AT&C losses through application of IT for energy auditing and accounting

and through technological up gradation and strengthening of distribution infrastructure. Apart

from availability and access, it is imperative to supply reliable and quality power.

Rural Electrification Corporation Ltd. working towards fulfilling power sector borrower‟s

requirements by providing timely and prompt services and by mobilizing the funds from

various sources at lowest possible cost and strive to improve the customer‟s satisfaction on

continual basis.

During the period of 8weeks of my summer internship, I as a student of MBA (Power

Management) got an opportunity of thorough study of the two projects viz.

A) Entity Appraisal and Project Appraisal for the private transmission project in

western grid.

The main objective of this project is setting up 400kv D/C (Quad Conductor) transmission

line, LILO of existing 400KV S/C transmission line & 400 KV D/c (Twin Conductor)

transmission line and Substation work at various locations.

In this project I learned about the procedure of entity appraisal for private utilities. Two

stages of entity appraisal process i.e. a) Preliminary stages and b) Detailed Evaluation

Process.

In project Appraisal, I have studied various technical details of project, Clearances from all

concern entities and financial details of borrower.

iv

B) Financing and Implementation of RAPDRP scheme in Amritsar under PSPCL.

The main objective of the scheme is to reduce the AT & C loss ≤ 15% and make the system

economically viable and improve the reliability of supply to project Area.

This project gave me the thorough idea of RAPDRP programme of the government of India.

Also I came to know the financial benefits and other benefits under this scheme.

v

LIST OF TABLES

Table 1: Category of Schemes Financed Under T&D ............................................................................ 8

Table 2: Business Analysis ................................................................................................................... 23

Table 3: Market Analysis ...................................................................................................................... 24

Table 4: Score Table ............................................................................................................................. 24

Table 5: Financial Capability ................................................................................................................ 24

Table 6: Past Financial Position ............................................................................................................ 25

Table 7: ROCE ...................................................................................................................................... 25

Table 8: Operating Margin .................................................................................................................... 26

Table 9: DSCR ...................................................................................................................................... 27

Table 10: Total Debt to Net Worth ....................................................................................................... 27

Table 11: Cash Flow ............................................................................................................................. 28

Table 12: Finacial Flexibility ................................................................................................................ 29

Table 13: Equity Funding Potential ...................................................................................................... 29

Table 14: Raising of Fund ..................................................................................................................... 30

Table 15: Project Cost & Indicating Score ........................................................................................... 31

Table 16: Management Analysis........................................................................................................... 31

Table 17: Final Analysis for Preliminary Stage .................................................................................... 32

Table 18: Business Analysis ................................................................................................................. 35

Table 19: Financial Analysis ................................................................................................................ 35

Table 20: Management Analysis........................................................................................................... 36

Table 21: Final Analysis for Detailed Evaluation ................................................................................. 36

Table 22: Transmission Line ................................................................................................................ 37

Table 23: Sub-station ............................................................................................................................ 38

Table 24: Technical Details .................................................................................................................. 38

Table 25: Status of Clearances .............................................................................................................. 40

Table 26: Project Cost ........................................................................................................................... 45

Table 27 : Financing Plan ..................................................................................................................... 47

Table 28: Operational Cost, Price & Assumptions ............................................................................... 48

Table 29: Cost Benefit Analysis ........................................................................................................... 53

Table 30: Pre-Construction ................................................................................................................... 53

Table 31: Construction .......................................................................................................................... 54

Table 32: Post Construction .................................................................................................................. 54

Table 33: Items Included by the Utility Under Part-B .......................................................................... 64

Table 34: Brief Profile of State/Utility ................................................................................................. 67

Table 35: Project Area Details .............................................................................................................. 68

Table 36:Commercial Information........................................................................................................ 68

Table 37:Project Funding ...................................................................................................................... 70

Table 38:Financial Benefits .................................................................................................................. 70

Table 39: AT&C Losses ....................................................................................................................... 71

vi

ABBREVIATIONS AND ACRONYMS

ACSR Aluminium Conductor with steel reinforcement

APDRP Accelerated Power Development & Reform Program

AT&C Aggregate Technical and Commercial Losses

CEA Central Electricity Authority (of India)

CO Corporate Office

COD Commercial Operation Date

CPM Chief Project Manager

CPSU Central Public Sector Undertaking (India)

DPR Detailed Project Report

EHT Extra High Tension

EPC Engineering Procurement& Construction

EPS Electric Power Survey (of India)

FI Financial Institution

FIRR Financial Internal Rate of Return

GIS Geographic Information System

GOI Government of India

HT:LT Ratio High Tension: Low Tension Ratio

HVDS High Voltage Distribution System

IE Intensive Electrification

LILO Line in line out

LVDS Low Voltage Distribution System

MOP Ministry Of Power

MOEF Ministry of Environment & Forest

NEF National Electricity Fund

NHA National Highway Authority

NTPC National Thermal Power Corporation Ltd

PFC Power Finance Corporation Ltd.

PGCIL Power Grid Corporation of India Ltd

PTCC Power & Telecommunication Coordination Committee

P:SI Project System Improvement

PSPCL Punjab State Power Corporation Ltd

RAPDRP Restructured Accelerated Power Development

& Reform Programme

RGGVY Rajiv Gandhi Gramin Vidyutikaran Yojana

ROW Right of way

SCADA Supervisory Control and Data Acquisition

SERC State Electricity Regulatory Commission

STPS Super Thermal Power Station

vii

TABLE OF CONTENTS

Declaration…………………………………………………………………………...……..…i

Acknowledgement……………………………………………………………………....….....ii

Executive Summery…...……………………………………………………….………..........iii

List of tables..............................................................................................................................v

Abbreviations and Acronyms…………………………………………………………....…...vi

CHAPTER -1

INTRODUCTION

1.1 TRANSMISSION SECTOR IN INDIA.......………....……………..................................1

1.2 RAPDRP SCHEME IMPLEMENTATION........................................................................2

1.3 PROBLEM STATEMENT..................................................................................................2

1.4 OBJECTIVE.........................................................................................................................3

1.5 SCOPE OF WORK..............................................................................................................3

1.6 ORGANISATION PROFILE..............................................................................................5

1.6.1 Performance Highlights………..……………………………………………………....6

1.7 CATEGORY OF SCHEMES FINANCED UNDER T&D………………………….........8

CHAPTER-2

LITERATURE SURVEY, POLICY AND RESEARCH METHODOLOGY

2.1 REVIEW OF EXISTING LITERATURE ……..………………………….………….......9

2.2 TRANSMISSION POLICIES IN INDIA..................................................................…....12

2.2.1 The Guideline………………………………………………………………………..12

2.2.2 Objective of the Scheme……………………………………………………………..12

2.2.3 Scheme Area……………………………………………………………………...…12

2.2.4 Scope of Work.............................................................................................................13

2.2.5 Format of the Schemes………………………………………………………………14

2.2.6 Estimation of load Demand………………………………………………………….14

2.2.7 Entity Appraisal……………………………………………………………………...14

2.2.8 Extent of Exposure of Utility………………………………………………………..14

2.2.9 Cost Data………………………………………………………………………….....15

2.2.10 Project Implementation.............................................................................................15

viii

2.2.11 Deviation Proposal....................................................................................................16

2.2.12 Project Financing.......................................................................................................16

2.2.13 Enhancement of Loan Amount..................................................................................17

2.2.14 Interest during Construction (IDC)...........................................................................17

2.2.15 Disbursal of the Loan................................................................................................17

2.2.16 Financial Viability.....................................................................................................18

2.3 STEPS FOR APPROVAL PROCESS OF T&D SCHEMES............................................19

CHAPTER 3

ENTITY APPRAISAL AND PROJECT APPRAISAL OF PRIVATE TRANSMISSION

PROJECT IN WESTERN GRID

3.1 INTRODUCTION..............................................................................................................22

A) ENTITY APPRAISAL PROCESS FOR PRIVATE TRANSMISSION PROJECT.......22

A.1 PRELIMINARY APPRAISAL.......................................................................................22

A.1.1 Precondition for Evaluation......................................................................................22

A.1.2 Evaluation process...................................................................................................22

A.1.3 Scoring process.......................................................................................................22

A.1.4 Appraisal Process....................................................................................................23

A.1.4.1 Business Analysis................................................................................................23

A.1.4.2 Financial Analysis.................................................................................................24

A.1.4.3 Management Analysis Framework.......................................................................31

A.1.5 Final Analysis for Preliminary Stage.......................................................................32

A.1.6 Decisions Points based on the Result.....................................................................33

A.2 DETAILED APPRAISAL ..........................................................................................33

B) PROJECT APPRAISAL..................................................................................................37

B.1 Project Details.......................................................................................................37

B.2 Clearances and Approval........................................................................................41

B.3 Project Review........................................................................................................41

B.4 Implementation Plan...............................................................................................44

B.5 Project Cost.............................................................................................................45

B.6 Financial Plan.........................................................................................................47

B.7 Selling Arrangement...............................................................................................47

B.8 Operation Costs, Prices & Assumptions.................................................................48

B.9 Cost Benefit Analysis.............................................................................................53

B.10 Project Risk Analysis............................................................................................53

B.11 Strength & Weaknesses........................................................................................55

ix

B.12 Row & Forest Clearances Related issue ..............................................................56

CHAPTER 4

FINANCING AND IMPLEMENTATION OF RAPDRP SCHEME IN AMRITSAR

UNDER PSPCL

4.1INTRODUCTIOT TO RAPDRP PART-B.........................................................................62

4.2 PROJECT OBJECTIVE.....................................................................................................67

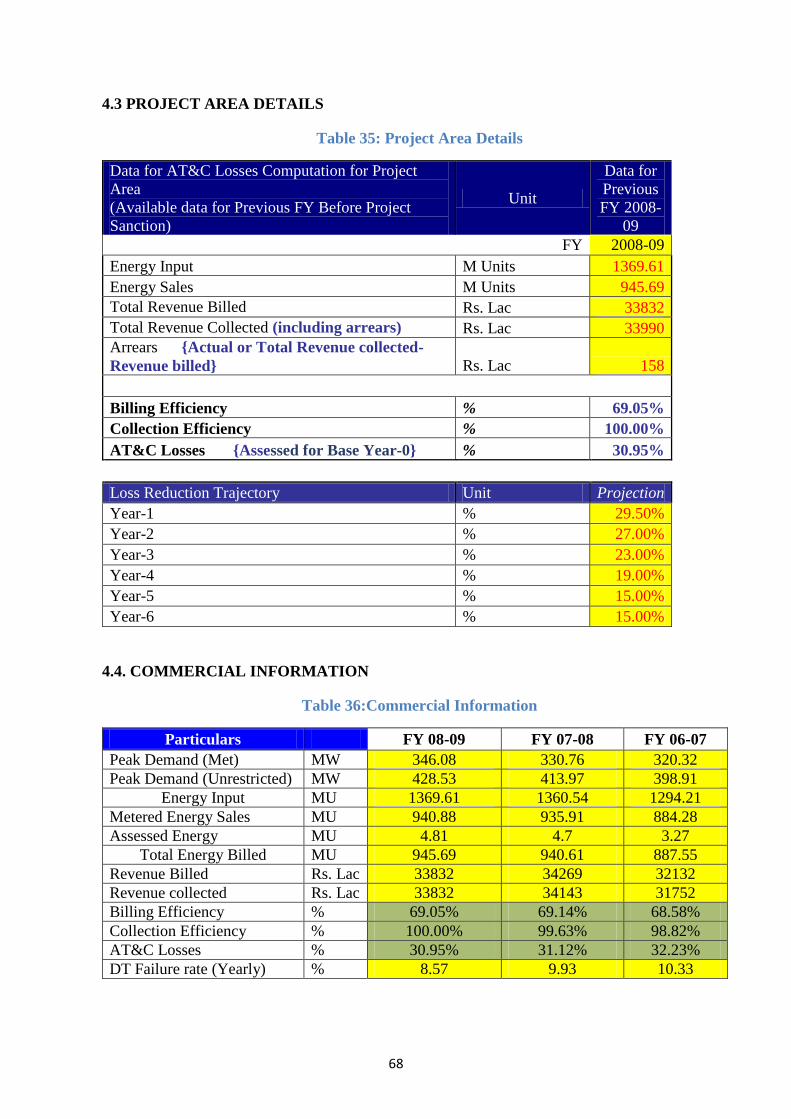

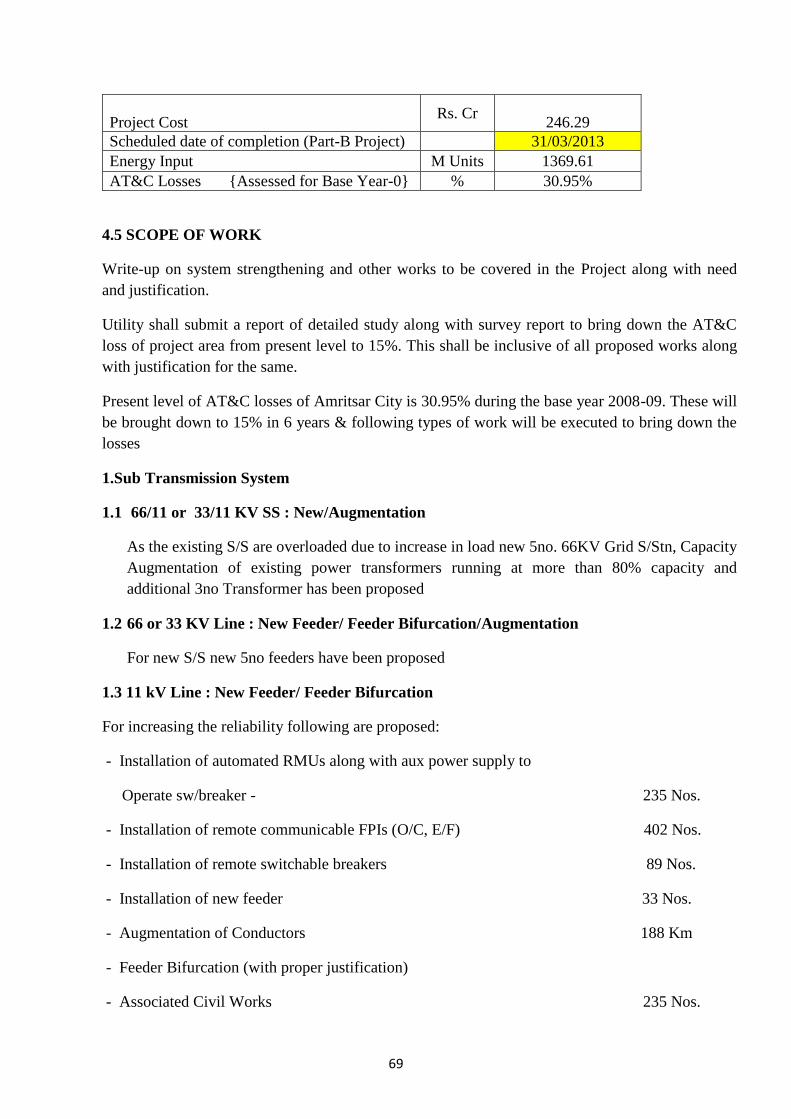

4.3 PROJECT AREA DETAILS.............................................................................................68

4.4 COMMERCIAL INFORMATION....................................................................................68

4.5 SCOPE OF WORK............................................................................................................69

4.6 PROJECT FUNDING........................................................................................................70

4.7 PROJECT BENEFITS.......................................................................................................70

4.8 PROJECT BENEFITS (AT & C LOSSES).......................................................................71

CHAPTER 5

CONLCUSION, LIMITATIONS, RECOMMENDATION AND FUTURE SCOPE

5.1 CONCLUSION..................................................................................................................72

5.2 LIMITATIONS..................................................................................................................73

5.3 RECOMMENDATIONS...................................................................................................74

5.4 FUTURE SCOPE ..............................................................................................................74

6. BIBLIOGRAPHY..............................................................................................................75

x

1

CHAPTER 1

1.1 TRANSMISSION SECTOR IN INDIA Power Sector forms one of the key constituents of Infrastructure essential for the growth of

the Economy. Compared to the other core sectors, the performance of the Power Sector

stands out during the fiscal 2012. A record 20,501 MW was added to the installed capacity in

the year 2011-12 against a capacity addition target of 17,601 MW. In accordance with the

projected estimates of the Planning Commission for XII Five year Plan, 88,425 MW of

capacity addition is required on all India basis. The overall fund requirement for the projected

addition has been estimated at around Rs. 16 lakh crore including commensurate back to back

investment in Transmission and Distribution network.

The transmission systems in the country consist of Inter-State and Intra State Transmission

System. Over decades a robust inter-state and inter-regional transmission system has evolved

in the country. Inter State (and Inter-regional) transmission system is mainly owned by

POWERGRID. In future, Inter-State Transmission System (ISTS) schemes would also be

built through competitive bidding by private sector entities. Already, a number of such

schemes by the private sector or joint venture between private sector and POWERGRID are

under construction. Planning and developing inter-state transmission system for IPP projects

is a challenging task because there is greater uncertainty about their actual materialization,

commissioning schedule and their beneficiaries are most often not known at the time of

transmission planning. The process of transmission planning and development has become

very dynamic in the market driven scenario.

At the time of Independence, power systems in the country were essentially isolated

systems developed in and around urban and industrial areas and the highest transmission

voltage was 132 kV. The state-sector network grew at voltage level up to 132 kV during the

50s and 60s and then to 220 kV during 60s and 70s. Subsequently, in many states (U.P.,

Maharashtra, M.P., Gujarat, Orissa, A.P., and Karnataka) substantial 400kV network was also

added as large quantum of power was to be transmitted over long distances.

Considering the operational regime of the various Regional Grids, it was decided

around1990s to establish initially asynchronous connection between the Regional Grids to

enable them to exchange large regulated quantum of power. Accordingly, a 500 MW

asynchronous HVDC back-to-back link between the NR - WR at Vindhyachal was

established. Subsequently, similar links between WR – SR (1000 MW capacity at

Bhadrawati), between ER – SR (1000 MW capacity at Gazuwaka) and between ER – NR

2

(500 MW capacity at Sasaram), were established. In 1992 the Eastern Region and the North-

Eastern Region were synchronously interconnected through a Birpara-Salakati 220kV double

circuit transmission line and subsequently by a 400 kV D/C Bongaigaon -Malda line.

Western Region was interconnected to ER-NER system synchronously through 400kV

Rourkela-Raipur D/C line in 2003 and thus the Central India system consisting of ER-NER-

WR came in to operation. In 2006 with commissioning of Muzaffarpur-Gorakhpur 400kV

D/C line, the Northern region also got interconnected to this system making an upper India

system („NEW‟ grid) having the NR-WR-ER-NER system.

1.2 RAPDRP SCHEME IMPLEMENTATION

Ministry of Power, Government of India, has launched the Restructured Accelerated Power

Development and Reforms Programme (R-APDRP) in July 2008 with focus on establishment

of base line data, fixation of accountability, reduction of AT&C losses upto 15% level

through strengthening & up-gradation of Sub Transmission and Distribution network and

adoption of Information Technology during XI Plan. Projects under the scheme shall be taken

up in two parts. Part-A shall include the projects for establishment of baseline data and IT

applications for energy accounting/auditing & IT based consumer service centres. Part-B

shall include regular distribution strengthening projects and will cover system improvement,

strengthening and augmentation etc.

It is proposed to cover urban areas - towns and cities with population of more than 30,000

(10,000 in case of special category states). In addition, in certain high-load density rural areas

with significant loads, works of separation of agricultural feeders from domestic and

industrial ones, and of High Voltage Distribution System (11kV) will also be taken up.

1.3 PROBLEM STATEMENT

As there is no license required for Generation of power under the Electricity Act, the

generators who construct dedicated transmission lines defined separately in the Electricity

Act are not being governed by the Work of Licensee Rules applicable to Transmission &

Distribution Licensees. As a result, there are disputes between generating companies and

owner/occupier of the land over which such lines are laid, which are essentially on the issue

that dedicated transmission lines were laid without taking prior consent from the owner or

occupier.

3

Each state needed to test the adequacy of transmission with respect to various uncertainties

such as fuel shortage, contingencies, high load growth without commensurate increase in

internal generation etc. Such instances would be frequent and have to be factored for such

uncertainties. Investment in a robust transmission system would also allow greater economy

interchange.

1.4 OBJECIVES

The Company has been funding power generation, transmission and distribution projects

besides funding electrification of villages and Pumpsets energisation. It continued to play an

active role in creating new infrastructure and improving the existing ones under the

transmission and distribution network in the country. In line with the country‟s objective to

provide “power for all” by the year 2012 and also reduce the AT&C losses, the Company

has been laying special thrust in expansion and strengthening of existing transmission

network and more importantly modernising of the distribution system by financing

investment in transformers, meters, capacitors etc. and for conversion of Low Voltage

Distribution to High Voltage Distribution System (HVDS).

In line with the national objective of providing power for all by the year 2012 and also of

reducing the AT&C losses, company has been financing schemes for expansion and

strengthening of the transmission network and more importantly, modernising the distribution

system.

1.5 SCOPE OF WORK

(A) Distribution Category- (13 years tenure except for Bulk loan which is for 7 years) -

Schemes covering voltage up to 11KV on secondary side of sub-station).

(i) System Improvement – To overcome the system deficiencies and to improve the quality

and reliability of power supply, REC finances System Improvement schemes, based on

system studies of an electrical distribution network considering present status of system

capacities, connected demand, voltage profiles and level of losses, together with scope for

future load growths. System deficiencies and weaknesses are identified and suitable solutions

identified.

This broadly includes creation of new sub-stations and feeders, augmentation of existing

Capacities of sub-stations and feeders, installation of capacitors, provision of efficient and

4

tampers proof meters, introduction of innovative equipment and technologies which help in

energy savings and improving the quality of power supply. This results in the supply of better

quality and more reliable power to the consumers and increased revenue to the Power

Utilities. The system improvement programme also includes Bulk loan schemes meant for

procurement and installation of meters, transformers etc, and HVDS schemes meant for

conversion of LVDS to HVDS so as to improve the HT: LT ratio. System Improvement

schemes reduce the AT&C losses to a great extent. Since launch of the programme in 1987-

88, REC has so far sanctioned projects for a loan assistance of Rs 84701 crores till March 12.

(ii) Intensive Electrification – The scheme for intensive electrification of electrified villages

has been termed as Projects Intensive Electrification (P: IE). Schemes under this activity

mainly aim at intensive electrification of already electrified villages. The basic purpose is to

cover intensive load development for providing connections to rural consumers in already

electrified villages. The required infrastructure of DTs, 11 KV lines and 33 KV lines are

provided for in these schemes to extend supply to various types of consumers. Financing of

schemes under the nomenclature of IE started from 1998-99 onwards (similar works were

earlier covered under various categories of schemes for village/dalit basti and hamlet

electrification through REC‟s own sources of financing and under budgetary support). Since

then, till March 12, schemes for a loan assistance of Rs. 6070crores have been sanctioned

under P: IE category.

(iii) Pumpset Energisation – REC started this programme to provide funds for schemes for

energisation of pumpsets, in order to facilitate agriculture. Thus the schemes are termed as

Special Project Agriculture (SPA). Since the start of the programme, till March 12, loan

assistance of Rs. 10582crores has been sanctioned under this programme.

(iv) APDRP Programme: The Accelerated Power Developments and Reforms programme

(APDRP) was launched by the GOI in 2001-02. The MoP sanctions the schemes based on the

recommendations of the concerned Advisor cum Consultants, who formulate the DPRs for

the utilities. The role assigned to REC regarding this programme is extending counterpart

funding to the states (which was 50% of project cost earlier, but now revised to 75%), based

upon the sanction of MOP. Since the launch of the programme, REC has provided a loan

assistance of Rs.5899 crores for year 2011-12

5

1.6 ORGANISATION PROFILE

REC (Rural Electrification Corporation Limited) a NAVRATNA Central Public Sector

Enterprise under Ministry of Power was incorporated on July 25, 1969 under the Companies

Act 1956. REC is a listed Public Sector Enterprise of Government of India with a net worth

of Rs. 14745 Crores as on 31.03.12. REC is a leading public Infrastructure Finance Company

in India‟s power sector. The company finances and promotes rural electrification projects

across India, operating through its Corporate Office located at New Delhi and 17 field units

(Project Offices), which are located in most of the States. The company provides loans to

Central/ State Sector Power Utilities, State Electricity Boards, Rural Electric Cooperatives,

NGOs and Private Power Developers.

The Project Offices in the States coordinate the programmes of REC‟s financing with the

concerned SEBs/State Power Utilities and facilitate in formulation of schemes, loan sanction

and disbursement and implementation of schemes by the concerned SEBs/State Power

Utilities.

MISSION

• To facilitate availability of electricity for accelerated growth and for enrichment of quality

of life of rural and urban population.

• To act as a competitive, client-friendly and development oriented organization for financing

and promoting projects covering power generation, power conservation, power transmission

and power distribution network in the country.

OBJECTIVES

In furtherance of the Mission, the main objectives to be achieved by the Corporation are

listed below:

• To promote and finance projects aimed at integrated system improvement, power

generation, promotion of decentralized and non-conventional energy sources, energy

conservation, renovation and maintenance, power distribution with focus on pumpset

energisation, implementation of Rajiv Gandhi Gramin Vidyutikaran Yojana, a

Government of India scheme for rural electricity infrastructure and household electrification.

• To expand and diversify into other related areas and activities like financing of

decentralized power generation projects, use of new and renewable energy sources,

6

consultancy services, transmission, sub transmission and distribution systems, renovation,

modernization & maintenance, etc. for optimization of reliability of power supply to rural and

urban areas including remote, hill, desert, tribal, riverine and other difficult / remote areas.

• To mobilize funds from various sources including raising of funds from domestic and

international agencies and sanction loans to the State Electricity Boards Power Utilities, State

Government, Rural Electric Cooperatives, Non-Government Organizations (NGOs) and

private power developers.

• To optimize the rate of economic and financial returns for its operations while fulfilling the

corporate goals viz. (i) laying of power infrastructure; (ii) power load development; (iii) rapid

Socio-economic development of rural and urban areas, and (iv) technology up-gradation.

• To ensure client satisfaction and safeguard customers‟ interests through mutual trust and

self-respect within the organization as well as with business partners by effecting continuous

improvement in operations and providing the requisite services.

• To assist State Electricity Boards/Power Utilities/State Governments, Rural Electric

Cooperatives and other loanees by providing technical guidance, consultancy services and

training facilities for formulation of economically and financially viable schemes and for

accelerating the growth of rural and urban India.

1.6.1 PERFORMANCE HIGHLIGHTS:-

7

8

1.7 CATEGORY OF SCHEMES FINANCED UNDER T&D

Table 1: Category of Schemes Financed Under T&D

S.No Category Purpose

1 Distribution scheme

(i) Project system Improvement:

P:SI

To strengthen and improve the sub

transmission and distribution system in the

designated area.

(ii) SI:Meters, Transformers, etc For procurement and installation of meters,

transformers etc.

(iii) P:SI (HVDS) For conversion of LVDS to HVDS

(iv) P:SI (APDRP) For counterpart funding of APDRP schemes

sanctioned by MoP

(v) Project Intensive

Electrification: P:IE

To cover intensive load development for

providing connections to rural consumers in

already electrified Villages.

(vi) Project Pumpsets: SPA:PE For energisation of pump sets.

2. Transmission schemes

Project system Improvement:

P:SI

For evacuation of power from new generating

Stations and to strengthen/improve the

existing transmission System in the designated

areas.

9

CHAPTER 2

2.1 REVIEW OF EXISTING LITERATURE

Brown et al (2006) state that Electric utilities are on a never ending quest to attain higher

levels of performance for increasingly lowers costs. Often times this leads to project requests

that far exceed budget and resource constraints. Many utilities have started to manage this

problem through well-defined project evaluation and selection processes. At a minimum,

these processes are able to rank project proposals within a given category with respect to

expected cost and expected benefit. More mature systems are able to: trade-off capital,

operations, inspection, and maintenance; look at marginal project value; trade-off risk versus

expected performance; and manage performance over multiple years. The most common

project selection approach is to rank all projects based on the ratio of benefit to cost. By

forcing all projects to be assigned a benefit and a cost, projects across departments and

functions can be directly compared. By ranking all projects based on the ratio of benefit to

cost, projects can be selected in order until budgets are exhausted. This presentation suggests

a new approach to project ranking that is designed for multiple performance targets. This

allows a utility to identify a large number of benefit measures and to set performance goals

related to each measure. Once metrics and targets are identified, the methodology identifies a

project portfolio that achieves all performance targets for the least possible cost. This

methodology has been implemented in an easy-to-use tool called AMPS (asset management

project selection), which allows scenarios and sensitivities to be quickly explored

Project Finance: Project financing is an innovative and timely financing technique that has

been used on many high-profile corporate projects, including infrastructural and power.

Employing a carefully engineered financing mix, it has long been used to fund large scale

natural resource projects, from pipelines and refineries to electric-generating facilities and

hydro-electric projects. Increasingly, project financing is emerging as the preferred

alternative to conventional methods of financing infrastructure and other large scale projects

worldwide.

Project finance is different from traditional forms of finance because the credit risk associated

with the borrower is not as important as in an ordinary loan transaction; what are most

10

important are the identification, analysis, allocation and management of every risk associated

with the project.

Risk identification and allocation is a key component of project finance. A project may be

subject to a number of technical, environmental, economic and political risks, particularly in

developing countries and emerging markets. Financial institutions and project sponsors may

conclude that the risks inherent in project development and operation are unacceptable

(unfinanced able). To cope with these risks, project sponsors in these industries (such as

power plants or railway lines) are generally completed by a number of specialist companies

operating in a contractual network with each other that allocates risk in a way that allows

financing to take place. The various patterns of implementation are sometimes referred to as

"project delivery methods." The financing of these projects must also be distributed among

multiple parties, so as to distribute the risk associated with the project while simultaneously

ensuring profits for each party involved.

Project Appraisal: It is an assessment of a project in terms of its economic, social

and financial viability. A lending financial institution makes an independent and objective

assessment of various aspects of an investment proposition. It is defined as taking a second

look critically and carefully at a project by a person who is in no way involved or connected

with its preparation. He is able to take independent, dispassionate and objective view of the

project in totality, along with its various components. There are some steps for Project

appraisal.

Management Appraisal: Management appraisal is related to the technical and

managerial competence, integrity, knowledge of the project, managerial competence

of the promoters etc. The promoters should have the knowledge and ability to plan,

implement and operate the entire project effectively. The past record of the promoters is

to be appraised to clarify their ability in handling the projects.

Technical Feasibility: Technical feasibility analysis is the systematic gathering and

analysis of the data pertaining to the technical inputs required and formation of

conclusion there from. The availability of the raw materials, power, sanitary and

sewerage services, transportation facility, skilled man power, engineering facilities,

maintenance, local people etc are coming under technical analysis. This feasibility

analysis is very important since its significance lies in planning the exercises,

11

documentation process, and risk minimization process and to get approval.

Financial feasibility: One of the very important factors that a project team should

meticulously prepare is the financial viability of the entire project. This involves the

preparation of cost estimates, means of financing, financial institutions, financial

projections, break-even point, ratio analysis etc. The cost of project includes the land

and sight development, building, plant and machinery, technical know-how fees, pre-

operative expenses, contingency expenses etc. The means of finance includes the

share capital, term loan, special capital assistance, investment subsidy, margin money

loan etc. The financial projections include the profitability estimates, cash flow and

projected balance sheet. The ratio analysis will be made on debt equity ratio and

current ratio.

Commercial Appraisal: In the commercial appraisal many factors are coming. The

scope of the project in market or the beneficiaries, customer friendly process and

preferences, future demand of the supply, effectiveness of the selling arrangement,

latest information availability an all areas, government control measures, etc. The

appraisal involves the assessment of the current market scenario, which enables the

project to get adequate demand. Estimation, distribution and advertisement scenario

also to be here considered into.

Economic Appraisal: How far the project contributes to the development of the

sector; industrial development, social development, maximizing the growth of

employment, etc. are kept in view while evaluating the economic feasibility of the

project.

Environmental Analysis: Environmental appraisal concerns with the impact of

environment on the project. The factors include the water, air, land, sound,

geographical location etc.

ANALYSIS

Offering credit is an operation fraught with risk. Before offering credit to an organization, its

financial health must be analyzed. Credit should be disbursed only after ascertaining

satisfactory financial performance. Based on the financial health of an organization, REC

assigns credit ratings. These credit ratings are used to fix the interest rate, exposure limit and

security criteria.”

12

2.2 TRANSMISSION POLICIES IN INDIA

GUIDING PRINCIPLES FOR POWER SYSTEM IMPROVEMENT (P: SI)

SCHEMES

2.2.1 THE GUIDELINES

These guidelines are to help in formulation, appraisal, financing and disbursal of loans under

the P: SI category of schemes (of state and central sector borrowers and CPSUs) aimed at

system improvement of transmission, sub transmission and distribution systems, and

supersedes all guidelines issued earlier in this regard.

2.2.2 OBJECTIVES OF THE SCHEMES

The main stress of the schemes should be on:

i) Reduction in technical and commercial losses in the transmission, sub transmission and

distribution systems.

ii) Providing adequate system support for load development in the project area for the next

five years.

(iii) Providing the required infrastructure (lines/sub stations etc.) for power evacuation,

transmission, sub transmission and distribution.

iii) Improving the voltage regulation so as to bring it within the permissible limit.

iv) Improving the quality and reliability of power supply.

v) Improving the power factor in sub-transmission and distribution systems so as to optimize

the utilization of available system capacities.

vi) Introduction of innovative technology such as computerization, IT related projects, load

dispatch, SCADA, communication, GIS, R&D etc.

vii) Energy Audit.

2.2.3 SCHEME AREA

The scheme area shall normally be minimum of a district or tehsil or Electrical Division for

sub transmission and distribution schemes and a circle for transmission schemes. However, in

case it is not possible to follow the aforesaid stipulations, other schemes may be considered

on the specific merits of the case.

13

2.2.4 SCOPE OF WORKS

The project shall cater primarily to the needs of the transmission, sub-transmission and

Distribution systems of the scheme area for the purpose of system improvement as well as for

meeting the needs of system inadequacies covering all or part of the following need-based

works:

i. Construction of new sub-stations at all voltage levels in transmission, sub-transmission

and distribution system along with its associated EHT/HT/LT lines/feeders.

ii. Augmentation of existing sub-stations and lines at all voltage levels in transmission,

subtransmission and distribution system.

iii. Conversion of LVDS to HVDS.

iv. Conversion of three phase system to single phase system.

v. Renovation & Modernisation of the existing HT and LT lines including LVDS.

vi. Regrouping of loads, bifurcation, alignment and augmentation of existing heavily

loaded LT feeders and installation of energy efficient distribution transformers.

vii. Provision of reliable and tamper proof meters at Consumers' premises.

viii. Provision of metering and reliable protection on LT side of distribution transformers.

ix. Provision of inter utility meters.

x. Shunt compensation in LT system.

xi. Bifurcation, alignment and augmentation of existing heavily loaded 11 KV feeders.

xii. Provision of 11 KV automatically Switched capacitors directly on lines.

xiii. Provision of 11 KV voltage boosters, sectionalisers etc.

xiv. Shunt compensation at various substations in sub-transmission system, by installation

of HT capacitor banks.

xv. Provision of metering equipment on all incoming and outgoing feeders in the

existing/ proposed power Sub-stations.

xvi. Provision of service connections (utility share), as also its modernization.

xvii. Provision of controlling equipment, such as, circuit breakers, isolators etc. for the

existing feeders and power transformers wherever necessary.

xviii. Communication and automation equipment which includes computerization, IT

Related projects, load dispatch, SCADA, communication, GIS, R&D etc.

xix. Metering and other Equipment for Energy audit.

xx. Replacement of worn out sub-station equipment.

xxi. Study, evaluation and consultancy relating to aforesaid scope of works at S.No (i) -

14

(xx), if not specifically covered under the concerned project.

xxii. Preparation of DPR (upto 2% of the cost of the scheme).

2.2.5 FORMAT OF THE SCHEME

The schemes will be submitted by the borrower as per the prescribed structure of the project

report. Also, for transmission schemes, where the utilities are running load flow studies, the

same may be verified and accepted by the CPM, and values as derived from load flow studies

may be indicated in the appraisal note and also used for calculating the required scheme

parameters, without necessarily using the furnished formats. The copies of load flow studies

may be furnished.

2.2.6 ESTIMATION OF LOAD DEMAND

The load growth for the scheme area shall be considered for the next 5 years (referred to as

horizon year) based on either of the following:

(i) Load growth for the utility as per the latest tariff order; or

(ii) Load growth for the state as per the latest available EPS report of CEA.

However, if the projections in the scheme area are substantially higher due to some special

requirements, the same will be clearly spelt out and explained for consideration with proper

justification by the power utility/SEB and recommended by the CPM as a part of the

appraisal report.

The calculation of load growth as above may not be compulsory/applicable in case of certain

transmission schemes where erection of sub stations and lines for power evacuation are

involved and also for certain special types of distribution schemes like HVDS, feeder

separation etc.

2.2.7 ENTITY APPRAISAL

For appraising the capability of the borrower, the latest ratings as specified by the entity

appraisal division of REC may be followed.

2.2.8 EXTENT OF EXPOSURE OF UTILITY

At the time of project appraisal, the CPM shall ensure that the balance credit exposure for the

utility is available.

15

2.2.9 COST DATA

The schemes will be formulated by the utilities based on their latest approved schedule of

rates, and certified by the CPMs that they are as per the latest schedule of rates. If there is a

variation in the cost adopted in the scheme compared to the schedule of rates, the CPM

should give justification for the same. Where the utilities have not formulated the latest

schedule of rates, the cost as per the latest purchase orders can be adopted by the CPMs.

Alternatively, in such cases, the old approved schedule of rates with permitted escalation as

per utility‟s norms may be used. In any case, the PO should invariably give its

recommendations in the processing note regarding the acceptability of the cost estimates

adopted by the power utility.

2.2.10 PROJECT IMPLEMENTATION

a) Project Period

Execution of the scheme shall be completed within the scheduled operating period agreed at

the time of the sanction (normally 2 years for Distribution and 3 years for transmission

schemes), with a grace period of one year (at the discretion of REC). However, the scheme

implementation period may be extended beyond the scheduled operating period agreed at the

time of the sanction, by the competent authority.

b) Execution of the project

The power utility in its project report should clearly indicate whether the scheme would be

executed departmentally or otherwise.

Normally, monitoring and quality assurance of the projects (with loan amount more than

Rs.50 crores) during its implementation should form an integral part of the project and this

shall be got done from a third party/independent agency. The cost of the same shall form part

of the loan assistance from REC.

Evaluation of the project (as applicable) after completion shall be got done by the borrower

from a third party/independent agency, the cost of which may also form part of loan

assistance from REC.

16

2.2.11 DEVIATION PROPOSALS

a) In the event there are some deviations in physical activities (as compared to the sanctioned

project) these will be considered on submission of a deviation proposal by the SEB, during

the project period, subject to the following conditions:

i) The deviations made shall be technically justified.

ii) The Financial commitment of REC is limited to the original loan amount including cost

escalation, if any (except for cases covered under 11b and 12 below).

iii) The scheme continues to meet the viability criteria as per stipulated norms (with the

deviations) despite changes in loss savings, sale of energy and overall cost of works, if any.

iv) The submission of the deviation proposal shall precede the submission of the last

reimbursement claim against the scheme by the SEB and approved by Competent Authority

of REC before release of this amount. This deviation proposal shall be forwarded by the

competent authority of the SEB, justifying the change with details of (i), (ii) and (iii) above.

b) However, enhancement in the loan amount due to change in scope of works may be

considered up to 20% of the original sanctioned loan amount subject to the revised proposal

meeting the prescribed technical and financial viability criteria.

2.2.12 PROJECT FINANCING

a) Provision for cost-escalation up to a maximum of 20% of the project cost (due to

unexpected price rise) will be permitted if desired by the borrower. This will hold good for

projects being executed departmentally or on turnkey or on partial turnkey mode. However,

the viability shall be tested on the capital base including 20% cost escalation.

b) Wherever the borrowers have not sought for such cost escalation towards price rise in the

original sanction, but due to unexpected price rise, the actual cost becomes higher than the

sanctioned amount, the borrower will have the option to revise the project cost on the basis of

actual expenditure incurred, subject to a ceiling of 20% of the original loan amount and seek

the approval of the corporation to the revised project cost, giving proper financial

justification.

c) Notwithstanding the above, in case of schemes to be executed on turnkey basis through

competitive bidding, the overall cost of schemes eligible for financing by REC shall be the

cost approved by the competent authority of the utility/Regulator after award of work. In such

cases, viability as applicable, as per guidelines, would be rechecked.

17

2.2.13 ENHANCEMENT OF LOAN AMOUNT

Enhancement of loan amount on account of both change in scope of works as per para 11 (b)

and price rise as per para 12 (b) shall also be considered, but subject to the total ceiling of

20% of original sanctioned loan amount.

2.2.14 INTEREST DURING CONSTRUCTION (IDC)

The Corporation may also consider financing of interest during construction, for schemes

with loan amount more than Rs. 100 crores, which are sanctioned for an implementation

period of more than 2 years.

2.2.15 DISBURSAL OF LOAN

a) The first installment of the loan amount will be released on execution of the loan

documents and compliance of terms and conditions stipulated in the sanction. The release of

first instalment would be regulated as follows:

i) If the loan amount is more than Rs.100 crore, the scheme may be considered as high value

schemes, and the 1st installment limited to 10% of the loan amount.

ii) In case of schemes where loan amount is more than Rs. 50 crore, but is up to Rs.100 crore,

the 1st installment is limited to 15% of the loan amount.

iii) For schemes having a loan amount of up to Rs. 50 crore, the 1st installment may be

considered up to 20% of the loan amount.

iv) Further in case of turn key projects where generally the power utilities provide advance to

contractors, REC may also consider to provide equivalent advance towards 1st installment to

meet this requirement, if sought by the utility, subject to ceiling of such advance up to 15% of

the loan amount.

v) The advance loan as above would be provided only where the borrower has provided

adequate acceptable upfront security to REC.

b) The 2nd and subsequent installments of loan will be released on pro rata reimbursement

basis depending upon the progress of works indicated in the claims preferred by the borrower

after pro rata adjustment of initial advance. However, release of loan installments beyond

18

50% of loan amount of the scheme shall be preceded by detailed monitoring in accordance

with monitoring guidelines.

c) The final 10% of the loan will be released after final field monitoring, evaluation as

applicable and other terms and conditions of sanction of the scheme.

2.2.16 FINANCIAL VIABILITY

i) The scheme shall be considered viable if it yields Financial Internal Rate of Return (FIRR)

of at least 12% on the investment made under the scheme. The viability calculations shall

normally be based on the benefits at the Horizon year on account of loss savings as well as

additional sale of energy. However, other quantifiable benefits as applicable could also be

considered, with suitable justifications and calculations, wherever applicable/available. The

capital base for calculation is the cost of the scheme including cost escalation charges, if any.

ii) However, for schemes for introduction of innovative technology such as computerization,

IT related projects, load dispatch, SCADA, communication, GIS, R&D, inter utility meters,

DT meters etc. and for schemes relating to energy audit, study, evaluation, consultancy etc.

the IRR is not required to be worked out.

iii) Further, in case of transmission schemes, the IRR is not required to be worked out,

provided the schemes are approved/posed to SERC. In exceptional cases, schemes other than

defined above could be considered on merits of the specific case. In such cases, the Utility

shall undertake that these schemes would be included in the next year‟s approval by SERC.

At the time of sanctioning of a transmission scheme, schemes already sanctioned including

by other FIs/utility‟s own resources would also be taken cognizance of.

19

2.3 STEPS FOR APPROVAL PROCESS OF T&D SCHEME

Receipt of

Scheme at PO

Evaluation and

Processing of

scheme at PO

Receipt of scheme

at CO complete in

all respect

Processing of

scheme at CO for

Approval

If loan amount is

less than 20 Cr

Approval by screening

committee

Financial

concurrence

If loan amount is

less than 100 Cr

If loan amount is

less than 500 Cr

If loan amount is

less than 150 Cr

Approval: By CMD

Recommendation

of CMD

Recommendation

of CMD

Approval: By

BOD

Approval by Loan

Committee

Approval by Executive

Committee

Recommendation

of CMD

Financial

Concurrence

Screening

Committee

YES

NO

YES

NO

YES

NO NO

YES

NO NO

20

STEP 1: Receipt of scheme at PO

STEP 2: Evaluation & Processing of Scheme at PO

STEP 3: Receipt of Scheme at CO complete in all respect

STEP 4: Processing of Scheme at CO for approval

STEP 5: If loan amount is less than 20 Crore, Then Financial Concurrence and approval by

the Screening Committee

STEP 6: If Loan amount is more than 20 Crore, then Screening Committee and Financial

Concurrence

STEP 7: If loan amount is less than 100 Crore then approval by the CMD

STEP 8: If loan amount is less than 150 Crore, then recommendation of CMD and then

Approval by the Executive Committee

STEP 9: If loan amount is less than 500 Crore, then Recommendation of CMD and approval

by loan Committee

STEP 10: If loan amount is greater than 500 Crore, then recommendation of CMD and

approval by BOD.

The PO i.e. Project office plays a very vital role in the working of REC. All the details about

the Schemes are collected by PO. PO people are in direct contact with the Utilities or the

borrowers. The borrower first approaches the PO and then the Scheme is appraised by the PO

people.

PO people are also responsible for collecting the needed data and documents as per the REC

formats and guidelines. After the final appraisal by the PO people the Scheme is send to

corporate office (CO) for final technical and financial appraisal.

21

2.4 RESEARCH METHEDOLOGY

Review of project documents:

Review of the project documents will be helpful for understanding of the process of project

appraisal, risk associated with the financing of projects, economic condition of the concern

utility. This documents includes DPR of the scheme arrived for sanction, Appraisal

guidelines of REC, policy guidelines of CERC and presentations by different utilities, bid and

tender documents of transmission project etc.

Review of past experience:

Risk involved in financing private transmission project is more than the central or the state

utility. Past experiences might be helpful in assessing the risks, calculating the base score for the

utility. The projections of future financial performance are also evaluated with past financial

performance.

Project Appraisal: To evaluate the project rating and conducting the feasibility report of a

project based on the DPR/information memorandum/application form and other related

materials submitted by the borrower.

Assesses the capital needs of the business project and how these needs will be met.

Calculation of DSCR, IRR and sensitivity analysis.

Calculating the cost of generation and relevance.

Entity Appraisal: To assess the financial health of organizations that approach PFC for credit

for power projects. This would entail undertaking of the following procedures:

Analysis of past and present financial statements Examination of Profitability statements

Integrated Rating: Financial feasibility of the project is checked by the calculation of IRR and

DSCR, various cost estimates, tariff calculation, Interest during Construction, working capital

requirement, levellised tariff, etc. On the basis of above data, sensitivity analysis is done at

different input conditions. With the help of these data project is rated and then composite with

entity rating to reach at Integrated project rating.

22

CHAPTER 3

3.1 INTRODUCTION

A) Entity Appraisal Process for Private Transmission Project

The Entity appraisal process for private developers/utilities will be done in two stages,

namely:-

A.1. Preliminary Appraisal

A.2. Detailed Appraisal

A.1. Preliminary Appraisal

The evaluation process should be undertaken immediately on receipt of the loan application

form in the prescribed formats duly filled in with supporting attachments and documentation.

A.1.1 Precondition for Evaluation

a) The promoters prior to approaching REC should have identified 50% of the equity to be

eligible for preliminary evaluation. The name of the equity contributor should be clearly

mentioned and identified in the application. A letter expressing interest in contributing

interest in contributing equity to the project must be obtained from the identified equity

contributors.

b) Basic information on the promoters and their firm should be filled in as per the loan

application format. All the promoters who are eligible (contributing more than 10% of equity)

would undergo preliminary evaluation.

A.1.2 Evaluation Process

The preliminary evaluation involves the Business Analysis, Financial Analysis and the

Management Analysis of the promoters. For each of the parameters and sub-parameters

certain weightage have been assigned. Both quantitative and qualitative parameter has been

identified for assigning a score to each parameter. The project clears the preliminary

evaluation stage only if it scores the cut -off grade

Final score = (Business Analysis score) + (Financial Analysis score) + (Management

Analysis score)

A.1.3 Scoring Process Scoring is being done for promoters both on quantitative factors and qualitative factors. The

relevant score is then considered for the evaluation. The appraising officer needs to assign the

score ranging from 1 to 4.The business analysis score, financial analysis score and

management analysis score of each of the promoters is weighted by their equity contribution

for a combined entity score.

The default by the promoters to any of the financial institutions has been considered as an

overriding criterion for scoring. The default should be analysed in terms of the level of the

default, factors leading to the default and the number of times this has occurred. High

incidence of default or the current default would bring down the score of the promoter to one.

23

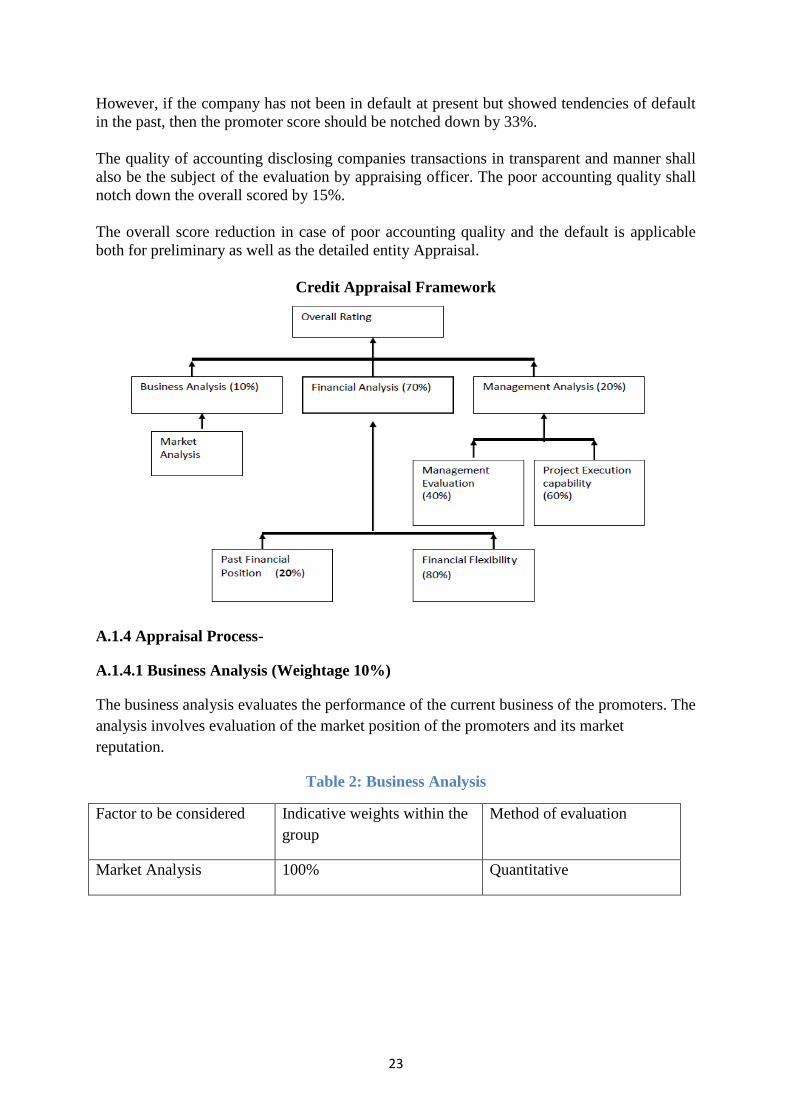

However, if the company has not been in default at present but showed tendencies of default

in the past, then the promoter score should be notched down by 33%.

The quality of accounting disclosing companies transactions in transparent and manner shall

also be the subject of the evaluation by appraising officer. The poor accounting quality shall

notch down the overall scored by 15%.

The overall score reduction in case of poor accounting quality and the default is applicable

both for preliminary as well as the detailed entity Appraisal.

Credit Appraisal Framework

A.1.4 Appraisal Process-

A.1.4.1 Business Analysis (Weightage 10%)

The business analysis evaluates the performance of the current business of the promoters. The

analysis involves evaluation of the market position of the promoters and its market

reputation.

Table 2: Business Analysis

Factor to be considered Indicative weights within the

group

Method of evaluation

Market Analysis 100% Quantitative

24

a) Market Analysis

The market share of the company can be evaluated based on the ratio of the turnover

of the promoting company/divided by the turnover of the market leader in the

business.

Table 3: Market Analysis

Ratio to be considered Method of evaluation

Turnover of the company/turnover of

the industry leader in the business

Quantitative analysis

The ratio so obtained is compared against the score table.

Table 4: Score Table

Market Position Indicative score

>0% but <=10% 1

>10% but <=30% 2

>30% but <=50% 3

Greater than 50% 4

A.1.4.2 Financial Analysis (Weightage 70%)

The analysis of financial capability of the borrower is based on the strength of the

existing business of the borrower. The evaluation further considers the level of

support, which could be available for the project appraisal project. The past five-year

results from the audited annual reports of the company are considered for the purpose

of the analysis under this section.

Table 5: Financial Capability

Factor to be considered Indicative weights Methods of evaluation

a) Review of the past

financial position

20%

Quantitative analysis

b) Financial flexibility 80%

The parameters that profile the strength of the business are detailed below.

25

A.1.4.2.1 Review of past Financial Position

The profitable operation of the business is an important criteria for lenders to draw

comfort that the company would be in a position to fund its equity contribution in the

project.

Table 6: Past Financial Position

Ratio to be considered Indicative Weights Method of Evaluation

Return on capital employed 20%

Quantitative Analysis

Operating margin 20%

Debt service coverage ratio 20%

Total Debt to total Net worth 20%

Cash generation from business 20%

A.1.4.2.2 Basis of the award of the score has the score has been detailed below

a) Return on capital employed (ROCE): the ratio is computed for at least last three

years and average of the same is considered for evaluation. The ratio can be

computed as:

ROCE = profit before interest and tax (PBIT) / capital employed

Where,

Capital employed= (equity capital + Reserves + short term debt + Long term debt-

Revaluation reserves-capital works in progress)

ROCE is to be calculated as average of the last three years figure. In case the ratio

is lower than the one for the preceding year then the latest ROCE should be used

for calculation instead of the average. The ration obtained the score table.

Table 7: ROCE

ROCE range Inductive score

<=5% 0

>5% but <=9% 1.00

>5% but <=9% 1.50

>5% but <=9% 2.50

26

>5% but <=9% 3.00

>5% but <=9% 3.50

Greater than 17% 4.00

b) Operating Margin(OM):

The ratio should be computed for the at least last three years and an average of the

same is considered for evaluation. The ratio can be computed as:

= operating profit before depreciation, interest and taxes (OPBDIT) / operating

income

Income and profit should be considered from the main operation of the company,

income from other sources, extra ordinary income and non-operating income

should be excluded.

In case the ratio is lower than one for the preceding year then the latest operating

margin (OM) should be used for calculation instead of the average .The ratio so

obtained is compared against the score table.

Table 8: Operating Margin

OM range Indicative score

<=0% 0

>0% but <=5% 1.50

>5% but <=10% 2.00

>10% but <=15% 2.50

>15% but <=20% 3.00

>20% but <=25% 3.50

Greater than 25% 4.00

c) Debt Service coverage Ratio (DSCR): The ratio should be computed only for the

latest year. The ratio can be computed as:

=(PBDIT-Tax)/(repayment due to long term loan + interest on long term and short

term loan including interest capitalized)

The DSCR so obtained is compared against the score table.

27

Table 9: DSCR

DSCR range Indicative score

<=1.0 0

>1.0 but <=1.1 1

>1.1 but <=1.2 1.50

>1.2 but <=1.3 2.00

>1.3 but <=1.4 2.5

>1.4 but <=1.5 3.00

>1.5but<=1.75 3.25

>1.75but<=2.0 3.50

Greater than 25% 4.00

d) Total Debt to Total Net Worth: - The degree of leverage of the current business

would indicate the ability of the borrower in raising funds for the purpose of

equity investment in the proposed project. The above would also influence the

borrower‟s ability to service his current and as well as future debt obligations. The

ratio should be computed only for the latest year. The ratio can be computed as:

= long term loan + other short term loan + WC loan from banks)/ (Equity share

capital+ reserves – Revaluation reserves – intangible assets)

The ratio so obtained is compared against the score table as indicated below.

Table 10: Total Debt to Net Worth

Total Debt to Total Net Worth range Indicative score

0-0.5 4.0

>0.5 but <=1.0 3.0

>1.0but <=1.5 2.5

>1.5 but <=2.0 2.0

>2.0 but <=2.5 1.5

Greater than 2.0 1.0

28

Less than 0 0

`

e) Cash Generation from business:-

In many businesses, profitability may not necessarily indicate a strong cash

position for the business i.e. a profitable company may not necessarily generate

the positive cash flow from the business. This parameter analyses whether the

cash generation in the existing business has been positive or negative in the past

years and thus serves as an indication of the promoter‟s capability in cash flow

management. The ratio should be computed only for the latest year.

= (cash flow from operation) / (long term loans + other short term loans + WC

loans from bankers)

Where,

Cash flow from operation= PAT+ Depreciation + non-cash expenses-increase in

working capital. The ratio so obtained is compared the score table as indicated

below.

Table 11: Cash Flow

CFO/Debt range Indicative score

Less than 0 1.0

>0 but <=0.1 1.5

>0.1 but <=0.2 2.0

>0.2 but <=0.3 2.5

>0.3but <=0.4 3.0

>0.4but <=0.5 3.5

Greater than 0.5 4.0

A.1.4.2.3 Financial flexibility

Financial flexibility evaluates the ability of the promoters to financially manage

the project. The key factors to be evaluated in financial flexibility are:

29

Table 12: Financial Flexibility

Ratio to be considered Indicative

Weights

Method of

evaluation

Equity funding potential 60%

Quantitative

analysis

Bridge finance ability 7.5%

Track records of the funds

raised

15%

Total Debt to Total Networth 10%

Aggregate project cost handled. 7.5%

a) Equity Funding potential: the promoting company can contribute equity to the

project by either raising debt on its books or raising equity or through cash surpluses

in the books. The equity funding potential is the summation of following.

Ability of the company to raise debt upto certain debt/equity ratio of ( 1.5:1.0 ) and

debt service coverage ratio of 1.5.(overall ability is limited by the lower of the two

ratios)

Ability to raise equity from the market by diluting the equity of the promoting

company upto 10% of its average market capitalization. The average market

capitalization is reckoned by the average of the last one year.

Ability to use marketable securities to raise equity for the project.

Any other source of infusing equity into the project.

The summation of the above has to be divided by the equity committed by the particular

promoter. The ratio so obtained is compared against the score table as indicated below.

Table 13: Equity Funding Potential

Equity infusion potential Indicative score

<=0 1

>0.00 but <=0.50 2

>0.50 but <=1.00 3

greater than 1.00 4

30

b) Bridge finance ability:

The borrower / promoters may have to arrange for bridge finance to overcome temporary

shortfall in funding for the project. These shortfalls may arise if disbursements from financial

institutions are not forthcoming as per the expected schedule or in case of the delay in tying

up of the debt funds. To evaluate the bridge finance ability of the promoters, the following

factor is compared with the project cost.

Quarterly cash surpluses= (annual cash flow from operation + Annual marketable

securities)/4

Where,

Annual cash flow from operation=PAT+ depreciation + non-cash expenses-increase in

working capital investments

The marketable securities considered for the equity infusion are not considered here.

Ratio is calculated as follows to judge the bridge finance ability.

Ratio=Quarterly cash surplus / total project cot

This ratio is compared with the indicative ratio in the following table and the corresponding

score is assigned.

c) Track record of the funds raised:

This parameter examines the experience of borrower / promoters in respect of

raising resources from the market. The aggregate funds raised by the promoting

group in the last ten years as a promotion of the project cost is benchmarked

against the scores tabulated below.

Table 14: Raising of Fund

Fund raising track record Indicative score

Less than 0.60 1.0

>0.60 but <=1.1 1.5

>1.1 but <=1.6 2.0

>1.6 but <=2.1 2.5

>2.1 but <=2.6 3.0

> 2.6 but <=3.1 3.5

Greater than 3.1 4.0

31

d) Aggregate project cost:

This parameter evaluates the ability of the project promoter to manage new projects. The

factor is scored by computing the aggregate cost of the project implemented by the promoting

group in the last ten years as a proportion of the cost of present project. The ratio so obtained

is compared against the score table as indicated below.

Table 15: Project Cost & Indicating Score

Aggregate project cost Indicative score

Less than 0.3 1.0

>0.3 but <=0.8 1.5

>0.8 but <=1.3 2.0

>1.3 but <=1.8 2.5

>1.8 but <=2.3 3.0

> 2.3 but <=2.8 3.5

Greater than 2.8 4.0

A.1.4.3 Management Analysis framework (Weightage 20%)

In this section the managerial competence of the promoters of the in managing the company

is being evaluated. Some of the key factors that would be evaluated comprise of:

Table 16: Management Analysis

Factor to be considered Indicative

weights

Methods of

evaluation

Organizational Experience 30%

Qualitative

judgement

Experience of key personnel 20%

Equipment supplier, EPC contractor

and project management Experience

30%

Project preparedness of the

promoters

20%

The score against each of these variables need to be given in a range of 1 to 4.

32

a) Organisational Experience: The experience of the borrower in the power sector needs to

be evaluated in terms of the organisation experience and the experience of the key personnel.

The sector experience of the borrower / promoters in all aspects of the power generation

business have to be analysed to evaluate the quality and relevance of their experience.

b) Experience of key personnel: the power sector experience of the personnel of the

borrower/promoters should be analysed under this section. Further it need to be gauged

whether the borrower is adequately geared up to manage the proposed power project.

c) Equipment Supplier, EPC contractor and project Management Experience:

Equipment Supplier, EPC contractor and project Management Experience of the borrower

/promoter should also be evaluated. Past experience in these aspects in increased comfort