supply chains for pharma products. time to penetrate for 3pl-operators? 1.major trends in european...

TRANSCRIPT

Supply Chains for Pharma Products.Time to Penetrate for 3PL-Operators?

1. Major Trends in European and Ukrainian Pharmaceutical Sectors (a 3PL-Operator’s viewpoint)

2. Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

3. What a ‘Classical’ 3PL-Operator Offers to Pharma-Sector? (case study)

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Oleg KalenskyDirector for Strategic Marketing & SalesUVK

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Major Trends in European and Ukrainian Pharmaceutical Sectors (a 3PL-Operator’s Viewpoint)

European Pharma-Market Ukrainian Pharma-Market

Globalization Consolidation (of retail)

Diversification (with value-added services to increase their share)

Coping with risks (currency exchange rate), crisis and state’s improper regulation

Innovations and new products Re-structuring of product portfolios (non-medicine categories to increase their

share)

Development of information-exchange platform to connect manufacturers and

customers

Setting-up of direct relations between manufacturers and retailers

High cost of penetration in pharma retail market (crisis of development)

System marketing to increase its role

Objective: to impact on pharma-manufacturers, timely responding to customers’ changing demand

Objective: to save business

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

FMCG Market Pharmaceutical Market

Turnover = UAH 150 bln (2008) Turnover = UAH 12 bln (2008)

Structure of retail: modern trade (supermarkets), street retail, HoReCa

Structure of retail: drugstore chains, wholesalers, hospitals

# of stores (total) = 75,000 # of stores (total) = 25,000

Consolidation = low level (30 biggest retailers hold 20% of the market)

Consolidation = high level (5 biggest distributors hold over 50% of the market)

Dynamics = +15%-30%, like-to-like (2000-2007)In crisis = -12%-60% (Q4 2008)

Distribution (pref.) = direct(manufacturer -> retail, 60% share)

Distribution (pref.) = indirect(thru distributors, 75% share)

Decrease of customer’s purchasing capabilities, risks (exchange rates, customs duties), ‘manual’ procurement planning, optimization (incl. category management), outsourcing of

non-core activities

Decrease of cap rate of retailers, re-structuring of retail, financing problems, opportunities to acquire competitive advantages (thru M&A)

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

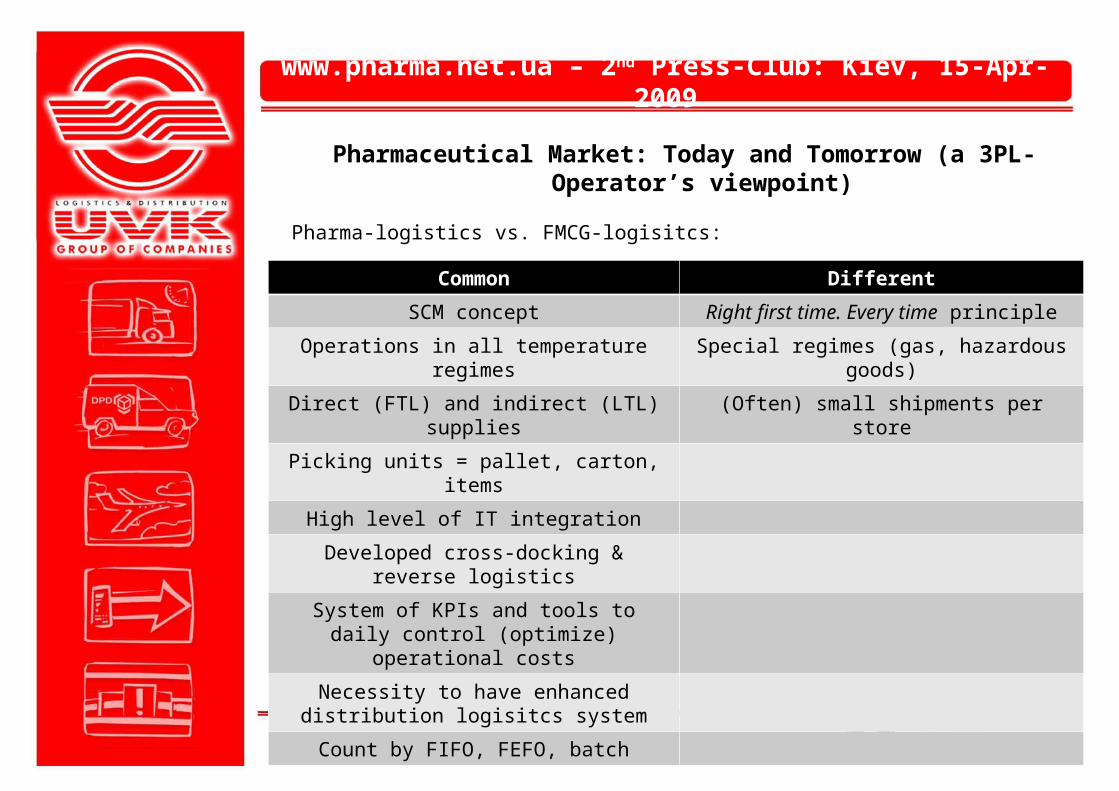

Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

Common Different

SCM concept Right first time. Every time principle

Operations in all temperature regimes Special regimes (gas, hazardous goods)

Direct (FTL) and indirect (LTL) supplies (Often) small shipments per store

Picking units = pallet, carton, items

High level of IT integration

Developed cross-docking & reverse logistics

System of KPIs and tools to daily control (optimize) operational costs

Necessity to have enhanced distribution logisitcs system

Count by FIFO, FEFO, batch

Pharma-logistics vs. FMCG-logisitcs:

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

Flows in Pharmaceutical Market:

Goods (logisitcs)

Distributor

Manufacturer Drugstore

Customer

Cash (finances)

Distributor

Customer

Manufacturer Drugstore

Deals (sales)

Distributor

Manufacturer Drugstore

Customer

Marketing

Distributor

Manufacturer Drugstore

Customer

Agency

3PL-Operator

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

Scopes of Interests of Key Players in Pharmaceutical Market:

Customer: Manufacturer:1) Low price 1) Guaranteed deliveries2) Best quality 2) Guaranteed CF3) Availability4) Consultations

Distributor: Drugstore:1) Maximal margin on trade 1) Delay in payment2) Minimal costs 2) Assortment3) Merchandising 3) Customers’ loyalty

4) Timely supplies

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

Distributor’s Risks:

1) Own costs 2) Credits3) Regional Distribution 4) ‘Landed’ prices5) Innovations 6) Exclusivity7) Product’s Quality 8) Accounts payable9) Merchandizing 10) Currency rate11) Customs duties 12) Logistics

Distributor’s Tasks:

Internal External1) Optimization of sales channels 1) CF effective management2) Revision of development plans 2) Price and market control3) Strategy correction 3) Strengthening of market

advantages4) Crediting solutions 4) Control of primary / secondary5) Risk management distribution

5) Innovative marketing6) Development / extra revenues

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

‘In crisis the one who is not changing is the one who’s going to die’ (Ichak Adizes, public lecture, March 31st, 2009, Kiev)

Analysis and decision-making regarding change – from a Client:

Customer -> AgencyCustomer -> DrugstoreAgency -> ManufacturerManufacturer -> Distributor

Change in demands (Customer)->

Change in the structure of activities by adapting and strengthening competitive advantages (Manufacturer, Distributor, Drugstore)

->Change of the format and essence of relations

(Manufacturer, Distributor, Drugstore, ?)->

Timely satisfaction of demands (Manufacturer, Customer)

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

Pharmaceutical Market: Today and Tomorrow (a 3PL-Operator’s viewpoint)

There are too many open questions, but…

1) Will economy be forecastible on a macro-level?2) To which extent will the state regulate the market?3) How fast will Ukraine integrate in the global economic society?4) …

5) How come will distribution transform? (vertical integration vs. disintegration; consolidation of allied merchandize categories vs. specialization by products, regions, functions, niche)

6) How swiftly will new forces (players) penetrate the market (traders, 3PL-operators, consultants)?

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

What a ‘Classical’ 3PL-Operator Offers to Pharma-Sector? (case study)

To Manufacturer To Distributor To Retailer

Professional stock management

Provision of single information platform

Customization of logisitcs services

Sharing of business risks

Platform for expansion Consolidation of stock

Guaranteed availability in retail

Discounts from manufacturers due to direct

supplies to DC

Centralized quality control

Developed network of regional warehouses

Cutting of logisitcs costs Balanced trade channels for deliveries to FMCG-retail

Increase of turnover

Optimization of stock at stores

Focus on core business

Ops inputs:

1) 1 cont. HC (30 plm), 1 plm = 60 cartons, 1 carton = 40 packages, price (1 package) = $2, gross margin = 50%)

2) Inbound = 50% by mono-plm (15 plm), 50% by cartons (900 cartons)3) Storage & warehousing = turnover 1:1, 50% picking by item + stickering (Ukrainian labels), 50% picking by

cartons4) Outbound = w/h-door delivery system, 50% by mono-plm, 50% by cartons

Pre-quotation:

1) …2) Unloading & acceptance = 15 UAH / 1 plm (mono), 1.5 UAH / carton3) Storage & warehousing:

1) Storage = 2 UAH / 1 plm / day2) Picking by item = 0.25 UAH / 1 package; picking by carton = 1.5 UAH / 1 carton3) Stickering = 0.15 UAH / sticker

4) Loading = 15 UAH / 1 plm (consolidated)5) D2D delivery = 300 UAH / 1 plm, 40 plm / 1 carton (average for Ukraine)6) + extra services (returns, documents return, insurance, FEFO, crediting etc.)

Total (invoice idea) = 56,000 UAH, orInbound-Ukraine logistics costs = 4.04% of on-shelf price

www.pharma.net.ua – 2nd Press-Club: Kiev, 15-Apr-2009

What a ‘Classical’ 3PL-Operator Offers to Pharma-Sector? (case study)