surface area grape - international organisation of vine...

TRANSCRIPT

World vitiviniculture situation

Surface area

Grape− Global grape production

Wine− Production− Consumption− Trade

2016 FAO-OIV Focus: Table and Dried Grapes

2

Global area under vines

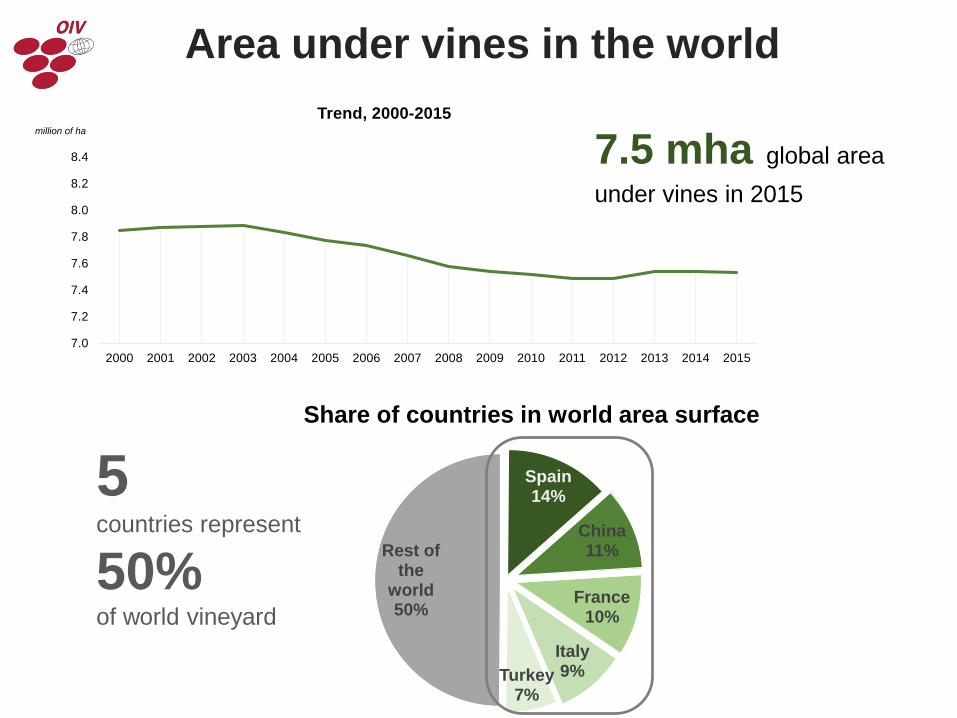

Area under vines in the world

5countries represent

50% of world vineyard

7.0

7.2

7.4

7.6

7.8

8.0

8.2

8.4

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

million of haTrend, 2000-2015

Share of countries in world area surface

7.5 mha global area under vines in 2015

Spain 14%

China11%

France10%

Italy9%Turkey

7%

Rest of the

world50%

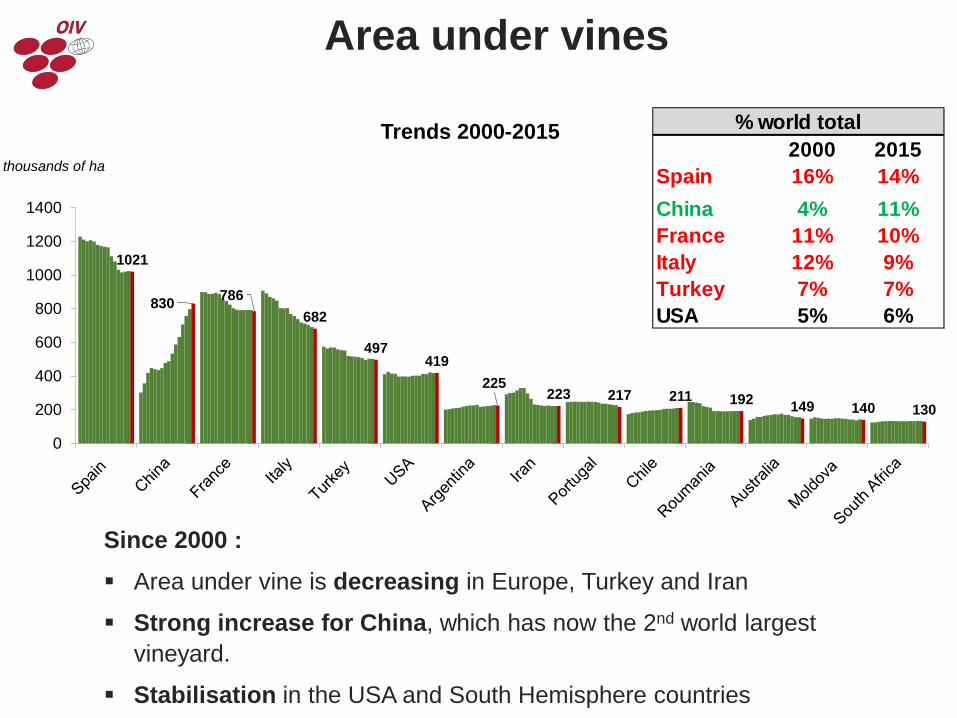

Since 2000 : Area under vine is decreasing in Europe, Turkey and Iran

Strong increase for China, which has now the 2nd world largestvineyard.

Stabilisation in the USA and South Hemisphere countries

Area under vines

2000 2015Spain 16% 14%China 4% 11%France 11% 10%Italy 12% 9%Turkey 7% 7%USA 5% 6%

% world total

1021

830 786682

497419

225223 217 211 192 149 140 130

0

200

400

600

800

1000

1200

1400

thousands of ha

Trends 2000-2015

Grape

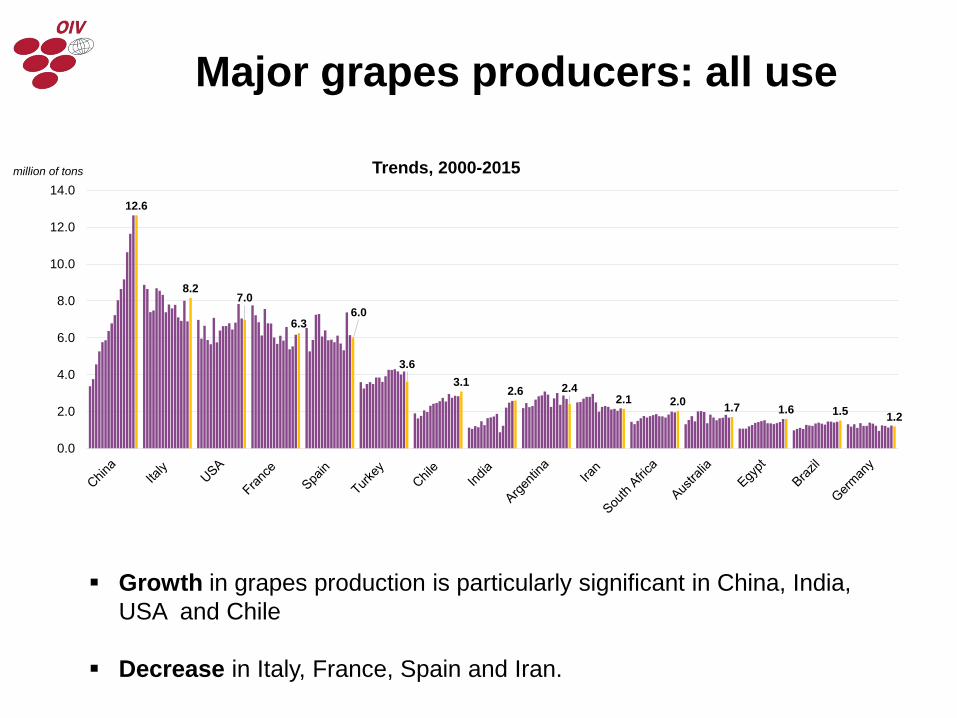

Major grapes producers: all use

Growth in grapes production is particularly significant in China, India, USA and Chile

Decrease in Italy, France, Spain and Iran.

12.6

8.27.0

6.36.0

3.63.1

2.6 2.42.1 2.0 1.7 1.6 1.5 1.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0million of tons Trends, 2000-2015

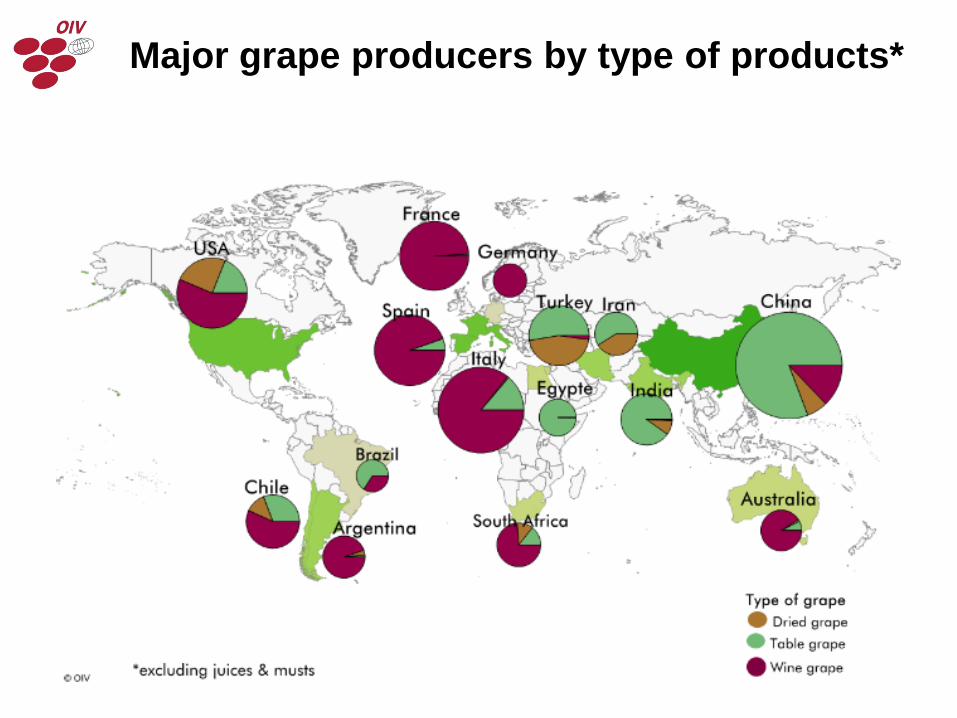

GrapeMajor grape producers by type of products*

Wine production

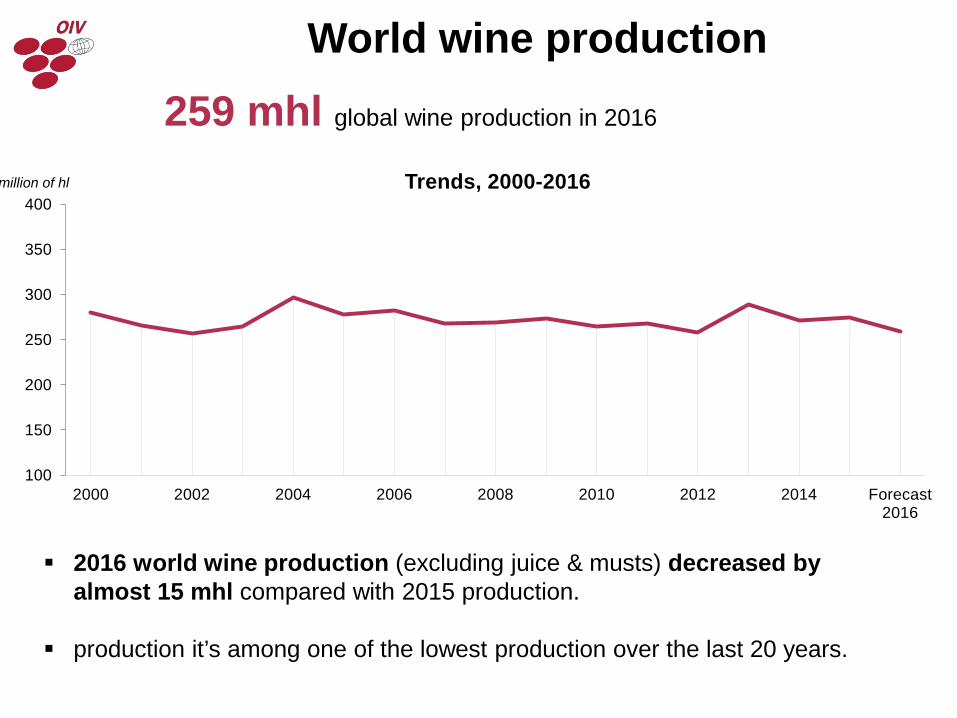

2016 world wine production (excluding juice & musts) decreased by almost 15 mhl compared with 2015 production.

production it’s among one of the lowest production over the last 20 years.

World wine production259 mhl global wine production in 2016

100

150

200

250

300

350

400

2000 2002 2004 2006 2008 2010 2012 2014 Forecast 2016

million of hl Trends, 2000-2016

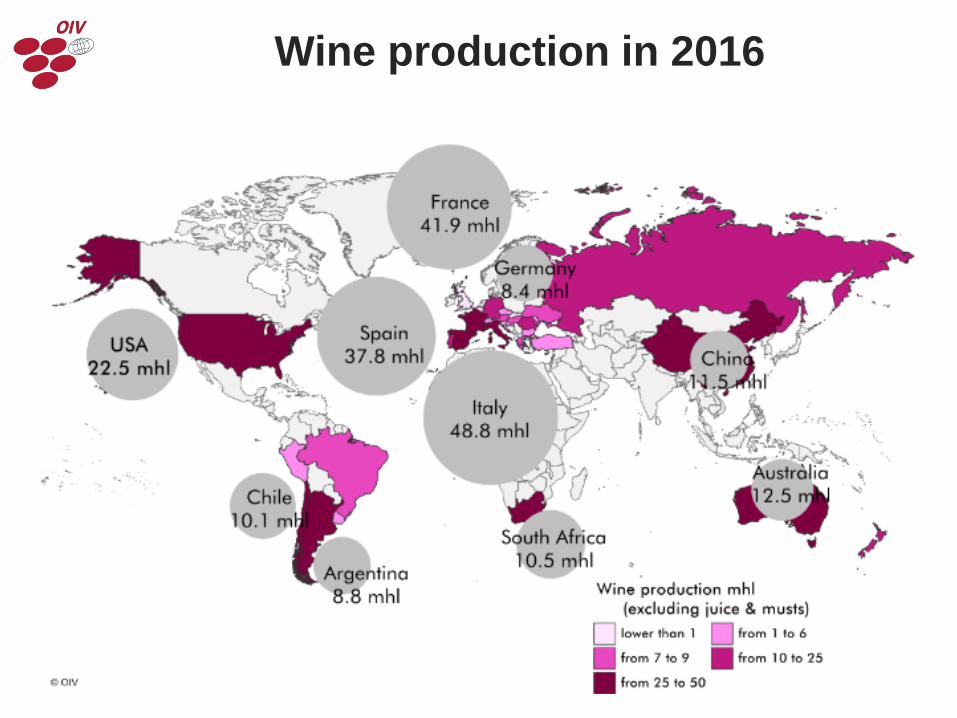

Wine production in 2016

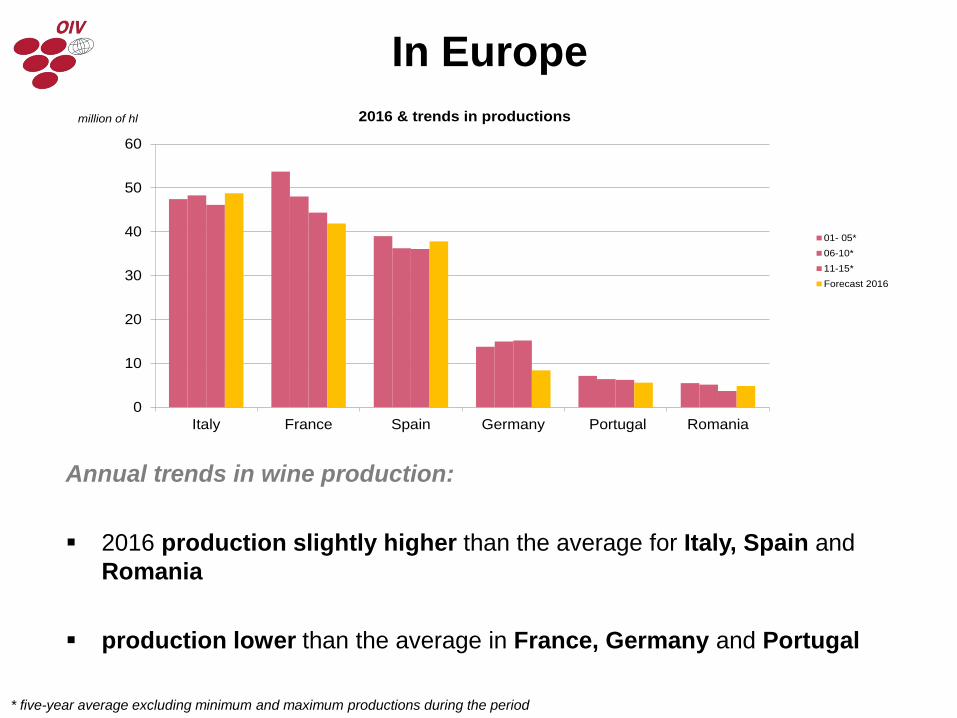

In Europe

* five-year average excluding minimum and maximum productions during the period

0

10

20

30

40

50

60

Italy France Spain Germany Portugal Romania

million of hl 2016 & trends in productions

01- 05*06-10*11-15*Forecast 2016

Annual trends in wine production:

2016 production slightly higher than the average for Italy, Spain and Romania

production lower than the average in France, Germany and Portugal

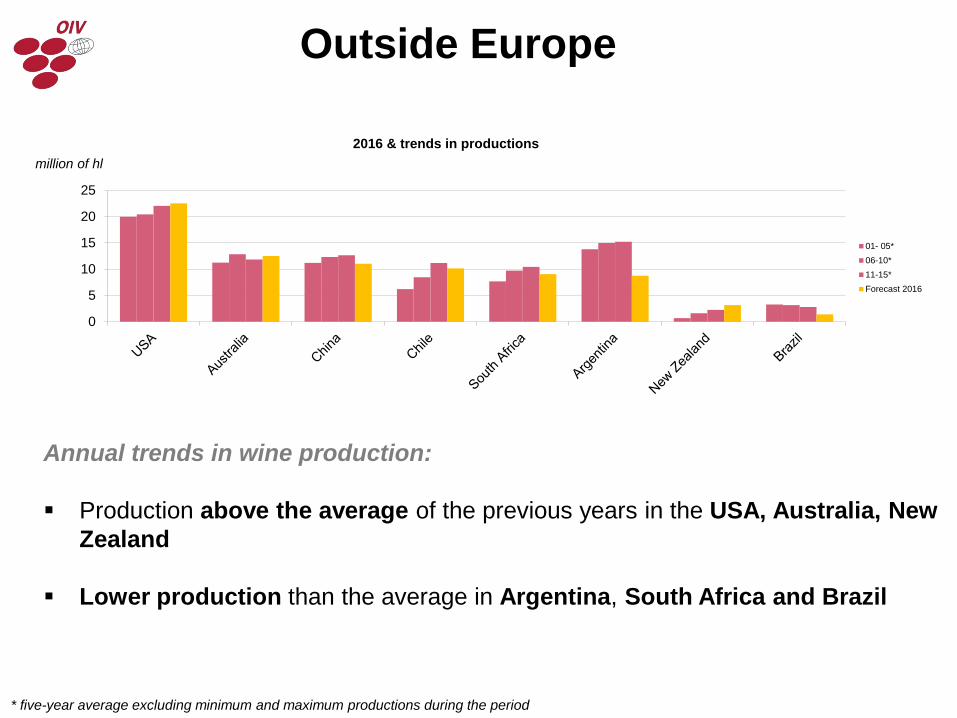

Outside Europe

* five-year average excluding minimum and maximum productions during the period

Annual trends in wine production:

Production above the average of the previous years in the USA, Australia, New Zealand

Lower production than the average in Argentina, South Africa and Brazil

0

5

10

15

20

25

million of hl2016 & trends in productions

01- 05*06-10*11-15*Forecast 2016

Wine productionexcluding juice and musts

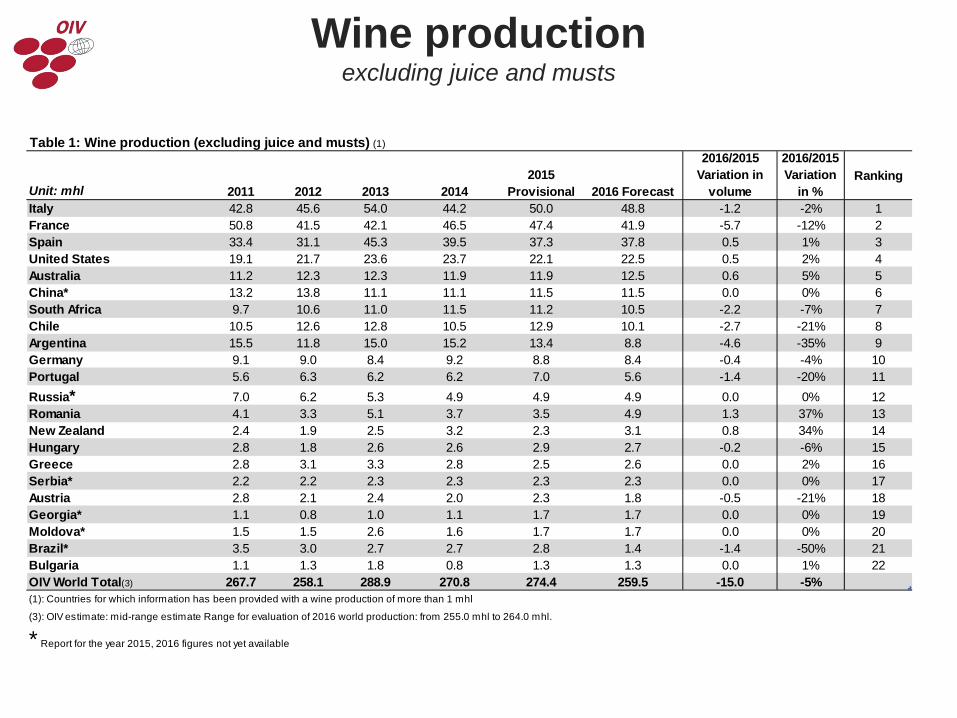

Table 1: Wine production (excluding juice and musts) (1)

Unit: mhl 2011 2012 2013 20142015

Provisional 2016 Forecast

2016/2015 Variation in

volume

2016/2015 Variation

in %Ranking

Italy 42.8 45.6 54.0 44.2 50.0 48.8 -1.2 -2% 1France 50.8 41.5 42.1 46.5 47.4 41.9 -5.7 -12% 2Spain 33.4 31.1 45.3 39.5 37.3 37.8 0.5 1% 3United States 19.1 21.7 23.6 23.7 22.1 22.5 0.5 2% 4Australia 11.2 12.3 12.3 11.9 11.9 12.5 0.6 5% 5China* 13.2 13.8 11.1 11.1 11.5 11.5 0.0 0% 6South Africa 9.7 10.6 11.0 11.5 11.2 10.5 -2.2 -7% 7Chile 10.5 12.6 12.8 10.5 12.9 10.1 -2.7 -21% 8Argentina 15.5 11.8 15.0 15.2 13.4 8.8 -4.6 -35% 9Germany 9.1 9.0 8.4 9.2 8.8 8.4 -0.4 -4% 10Portugal 5.6 6.3 6.2 6.2 7.0 5.6 -1.4 -20% 11Russia* 7.0 6.2 5.3 4.9 4.9 4.9 0.0 0% 12Romania 4.1 3.3 5.1 3.7 3.5 4.9 1.3 37% 13New Zealand 2.4 1.9 2.5 3.2 2.3 3.1 0.8 34% 14Hungary 2.8 1.8 2.6 2.6 2.9 2.7 -0.2 -6% 15Greece 2.8 3.1 3.3 2.8 2.5 2.6 0.0 2% 16Serbia* 2.2 2.2 2.3 2.3 2.3 2.3 0.0 0% 17Austria 2.8 2.1 2.4 2.0 2.3 1.8 -0.5 -21% 18Georgia* 1.1 0.8 1.0 1.1 1.7 1.7 0.0 0% 19Moldova* 1.5 1.5 2.6 1.6 1.7 1.7 0.0 0% 20Brazil* 3.5 3.0 2.7 2.7 2.8 1.4 -1.4 -50% 21Bulgaria 1.1 1.3 1.8 0.8 1.3 1.3 0.0 1% 22OIV World Total(3) 267.7 258.1 288.9 270.8 274.4 259.5 -15.0 -5%(1): Countries for which information has been provided with a wine production of more than 1 mhl

(3): OIV estimate: mid-range estimate Range for evaluation of 2016 world production: from 255.0 mhl to 264.0 mhl.

* Report for the year 2015, 2016 figures not yet available

Wine Consumption

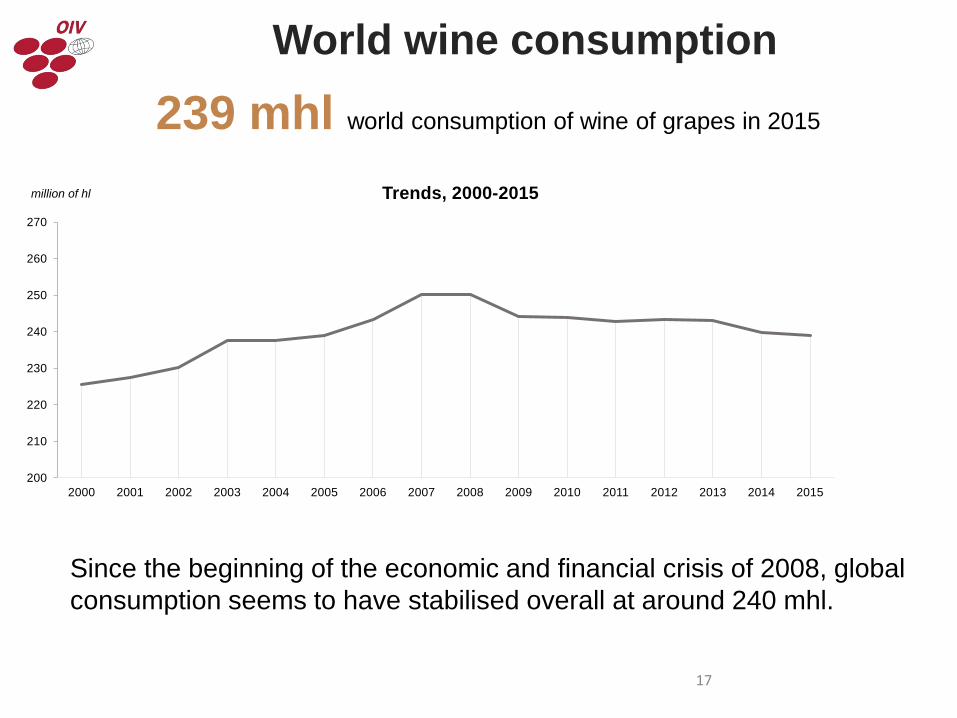

Since the beginning of the economic and financial crisis of 2008, global consumption seems to have stabilised overall at around 240 mhl.

World wine consumption

17

200

210

220

230

240

250

260

270

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

million of hl Trends, 2000-2015

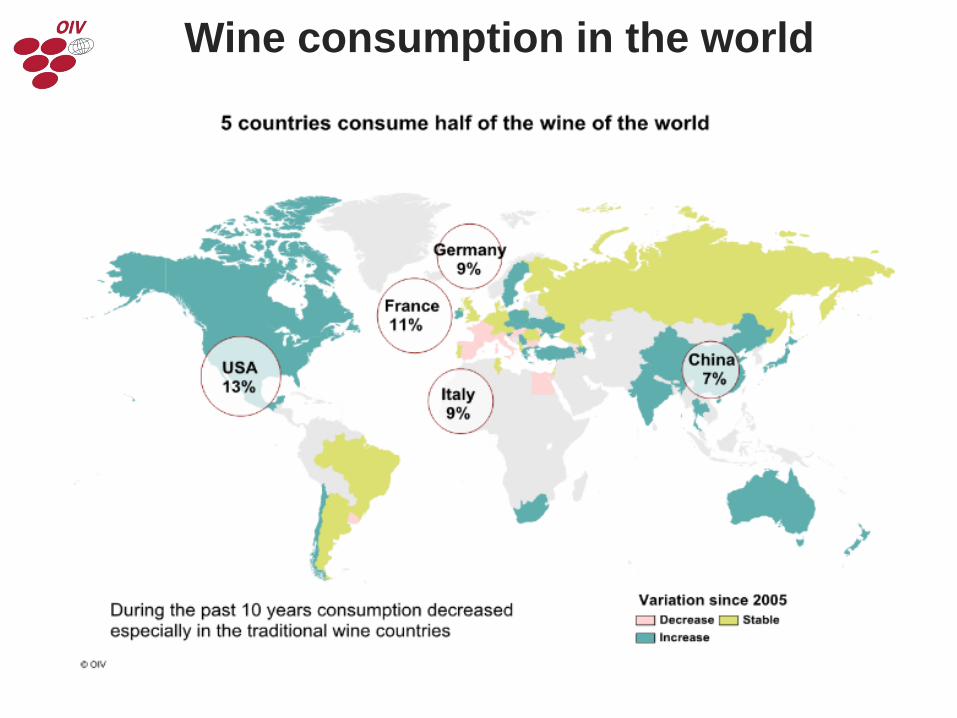

239 mhl world consumption of wine of grapes in 2015

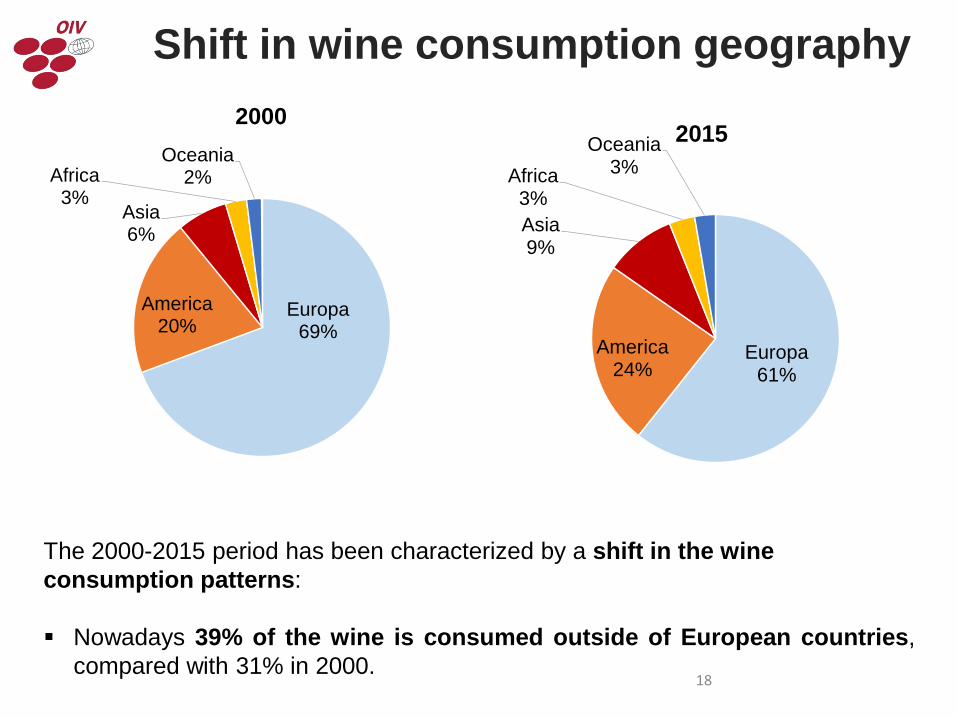

The 2000-2015 period has been characterized by a shift in the wine consumption patterns:

Nowadays 39% of the wine is consumed outside of European countries,compared with 31% in 2000.

Shift in wine consumption geography

18

Europa69%

America20%

Asia6%

Africa3%

Oceania2%

2000

Europa61%

America24%

Asia9%

Africa3%

Oceania3%

2015

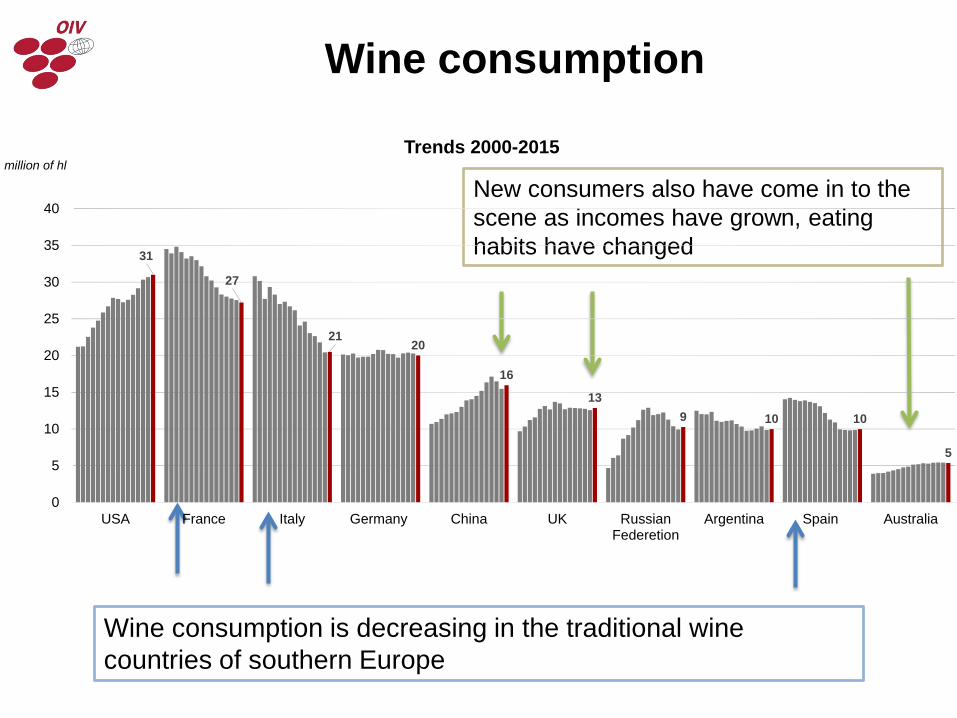

Wine consumption is decreasing in the traditional wine countries of southern Europe

New consumers also have come in to the scene as incomes have grown, eating habits have changed

Wine consumption

31

27

2120

16

139 10 10

5

0

5

10

15

20

25

30

35

40

USA France Italy Germany China UK RussianFederetion

Argentina Spain Australia

million of hlTrends 2000-2015

Wine consumption in the world

Wine trade

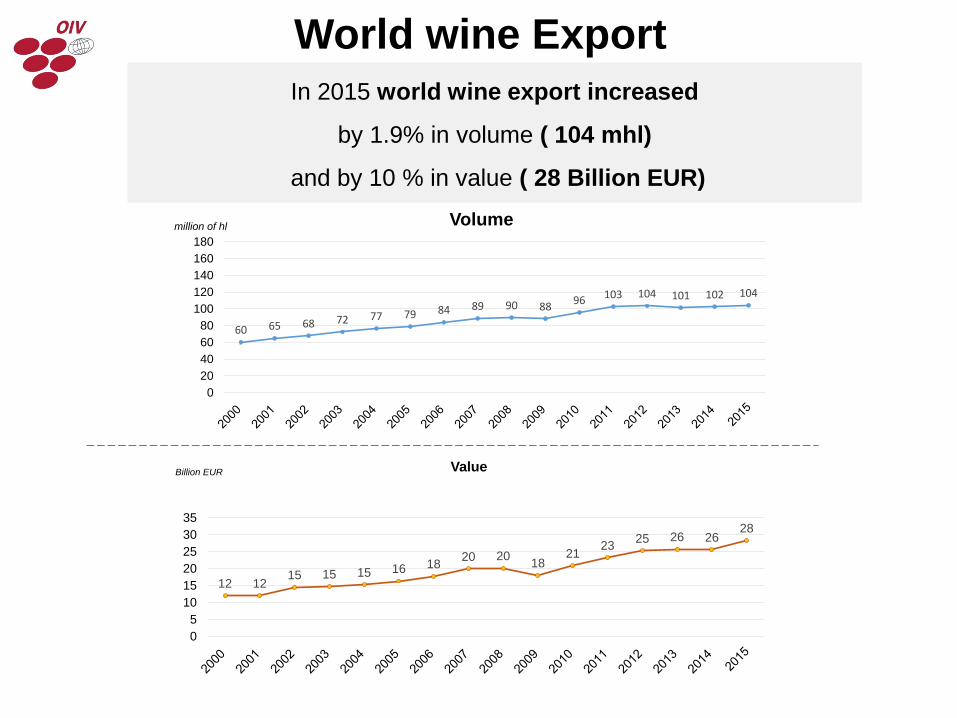

In 2015 world wine export increased

by 1.9% in volume ( 104 mhl)

and by 10 % in value ( 28 Billion EUR)

World wine Export

60 65 68 72 77 79 84 89 90 88 96 103 104 101 102 104

020406080

100120140160180

million of hl Volume

12 1215 15 15 16 18 20 20 18

21 23 25 26 2628

05

101520253035

Billion EUR Value

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

million of hl

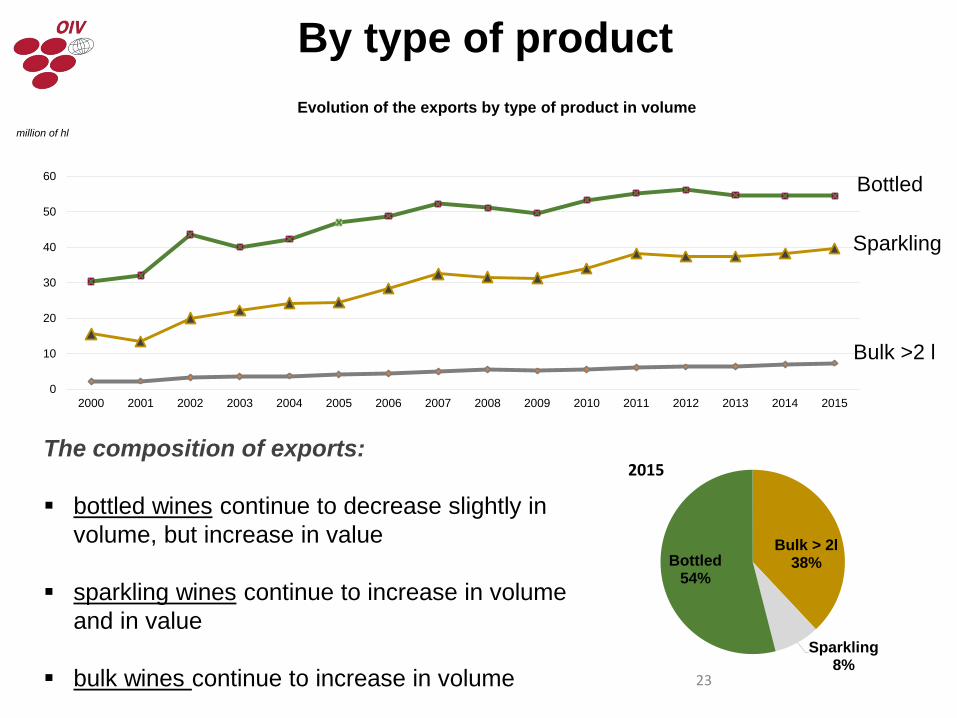

Evolution of the exports by type of product in volume

The composition of exports:

bottled wines continue to decrease slightly in volume, but increase in value

sparkling wines continue to increase in volume and in value

bulk wines continue to increase in volume

By type of product

23

Bulk > 2l38%

Sparkling8%

Bottled 54%

2015

Bottled

Sparkling

Bulk >2 l

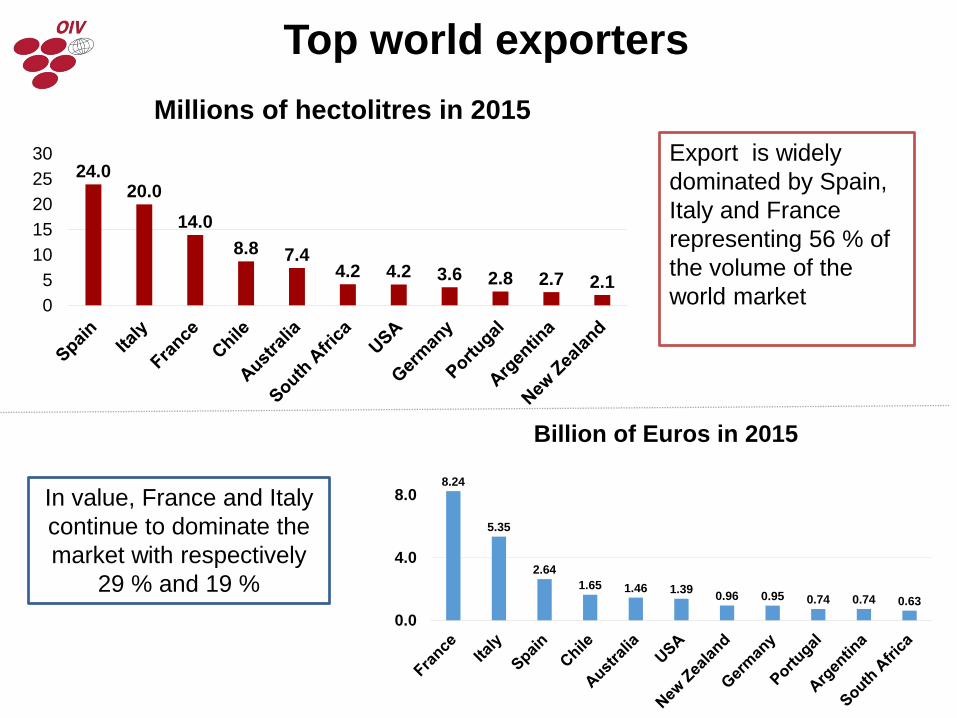

Top world exporters

Export is widely dominated by Spain, Italy and France representing 56 % of the volume of the world market

In value, France and Italy continue to dominate the market with respectively

29 % and 19 %

24.020.0

14.08.8 7.4

4.2 4.2 3.6 2.8 2.7 2.105

1015202530

Millions of hectolitres in 2015

8.24

5.35

2.641.65 1.46 1.39 0.96 0.95 0.74 0.74 0.63

0.0

4.0

8.0

Billion of Euros in 2015

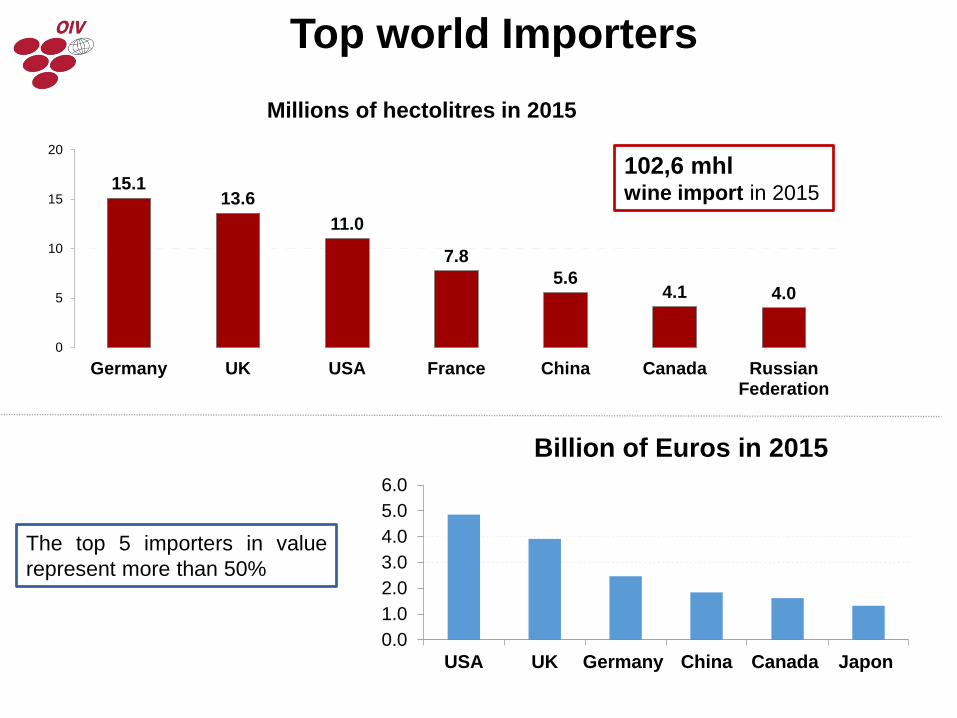

102,6 mhlwine import in 2015

Top world Importers

The top 5 importers in valuerepresent more than 50%

15.113.6

11.0

7.85.6

4.1 4.0

0

5

10

15

20

Germany UK USA France China Canada RussianFederation

Millions of hectolitres in 2015

0.01.02.03.04.05.06.0

USA UK Germany China Canada Japon

Billion of Euros in 2015

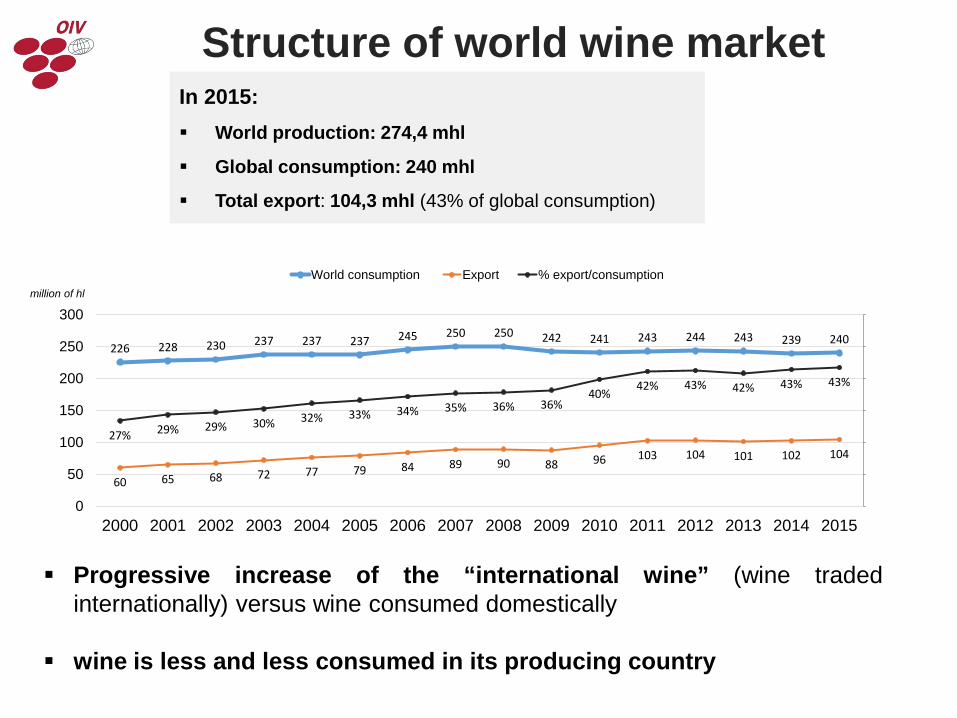

Structure of world wine market

Progressive increase of the “international wine” (wine tradedinternationally) versus wine consumed domestically

wine is less and less consumed in its producing country

In 2015: World production: 274,4 mhl

Global consumption: 240 mhl

Total export: 104,3 mhl (43% of global consumption)

226 228 230 237 237 237 245 250 250 242 241 243 244 243 239 240

60 65 68 72 77 79 84 89 90 88 96 103 104 101 102 10427% 29% 29% 30% 32% 33% 34% 35% 36% 36%

40% 42% 43% 42% 43% 43%

0

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

million of hl

World consumption Export % export/consumption

FAO-OIV Focus 2016:

Table and Dried Grapes

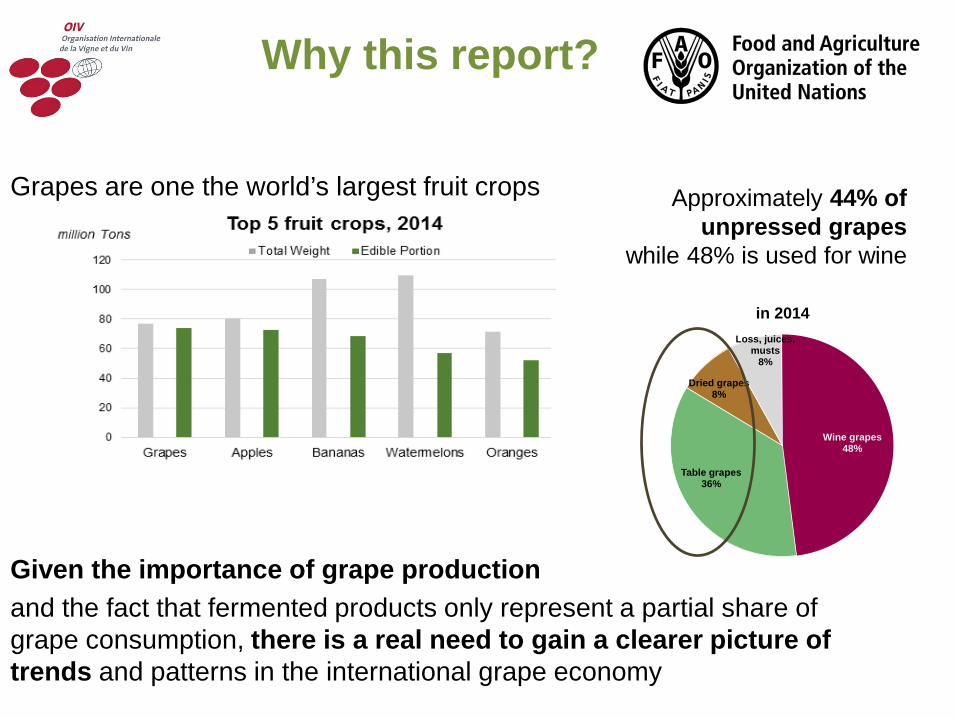

Why this report?

Grapes are one the world’s largest fruit crops

Given the importance of grape production and the fact that fermented products only represent a partial share of grape consumption, there is a real need to gain a clearer picture of trends and patterns in the international grape economy

Wine grapes48%

Table grapes36%

Dried grapes8%

Loss, juices, musts

8%

in 2014

Approximately 44% of unpressed grapes

while 48% is used for wine

FAO with FAOSTAT, the world's largest database of food and agricultural information, with more than a million statistics covering five decades and 245 countries and territories

OIV the reference organization on vines, wine, wine-based beverages, table grapes, raisins and other vine-based products

Content :

Section 1 general considerations of the basics of viticulture, food use of grape crops, and its nutritional aspects.

Section 2 provides an analyses of the table and dried grape market. It presents the latest data on production, consumption and imports.

10

15

20

25

30

2000 2002 2004 2006 2008 2010 2012 2014

million of tons

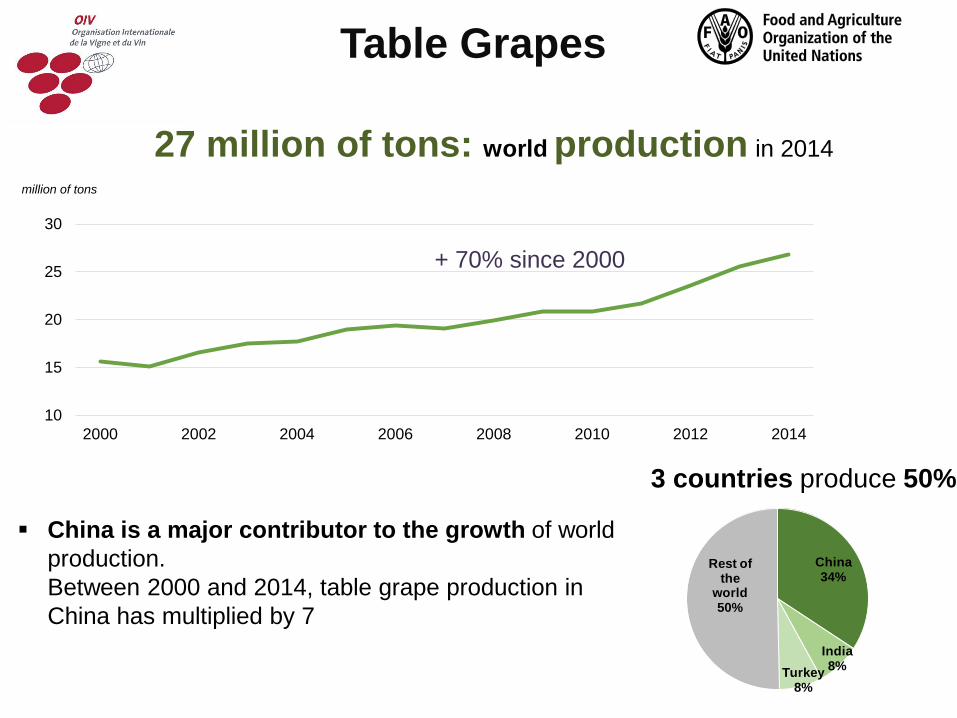

27 million of tons: world production in 2014

Table Grapes

+ 70% since 2000

China is a major contributor to the growth of world production. Between 2000 and 2014, table grape production in China has multiplied by 7

China34%

India8%Turkey

8%

Rest of the

world 50%

3 countries produce 50%

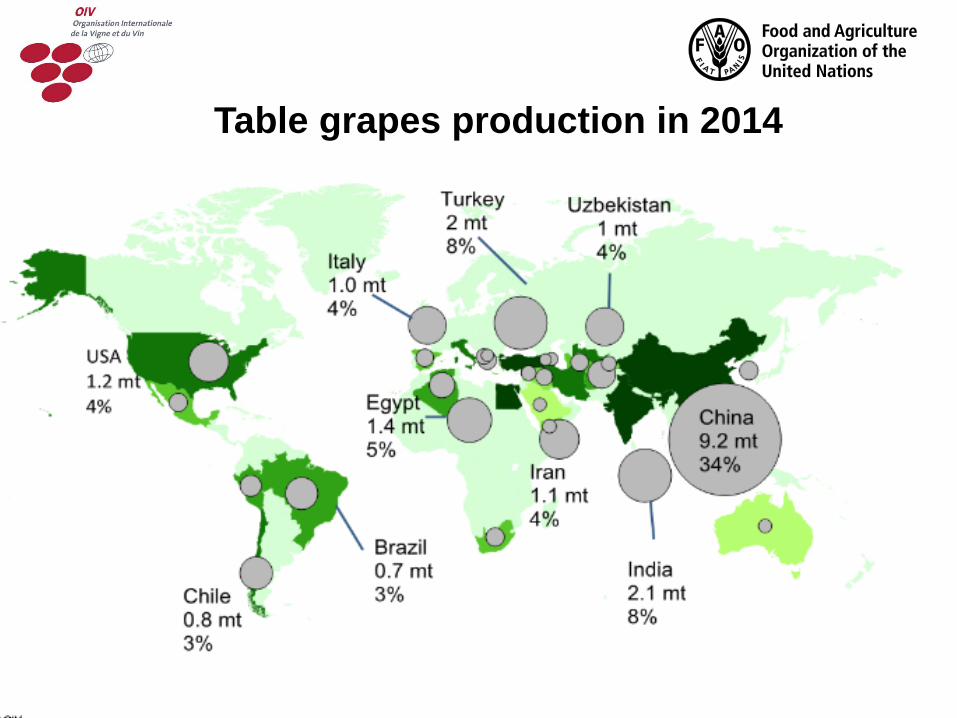

Table grapes production in 2014

10

16

22

28

2000 2002 2004 2006 2008 2010 2012 2014

million of tons

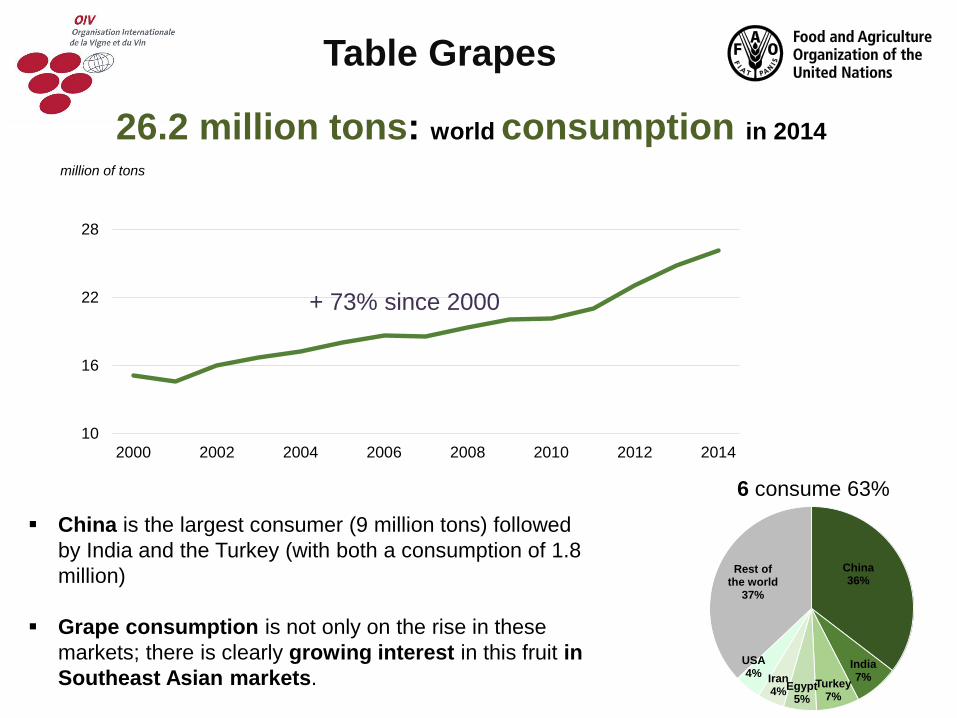

China is the largest consumer (9 million tons) followed by India and the Turkey (with both a consumption of 1.8 million)

Grape consumption is not only on the rise in these markets; there is clearly growing interest in this fruit in Southeast Asian markets.

Table Grapes

+ 73% since 2000

China36%

India7%Turkey

7%Egypt

5%

Iran4%

USA4%

Rest of the world

37%

26.2 million tons: world consumption in 2014

6 consume 63%

2

3

4

5

2000 2002 2004 2006 2008 2010 2012 2014

millions of tons

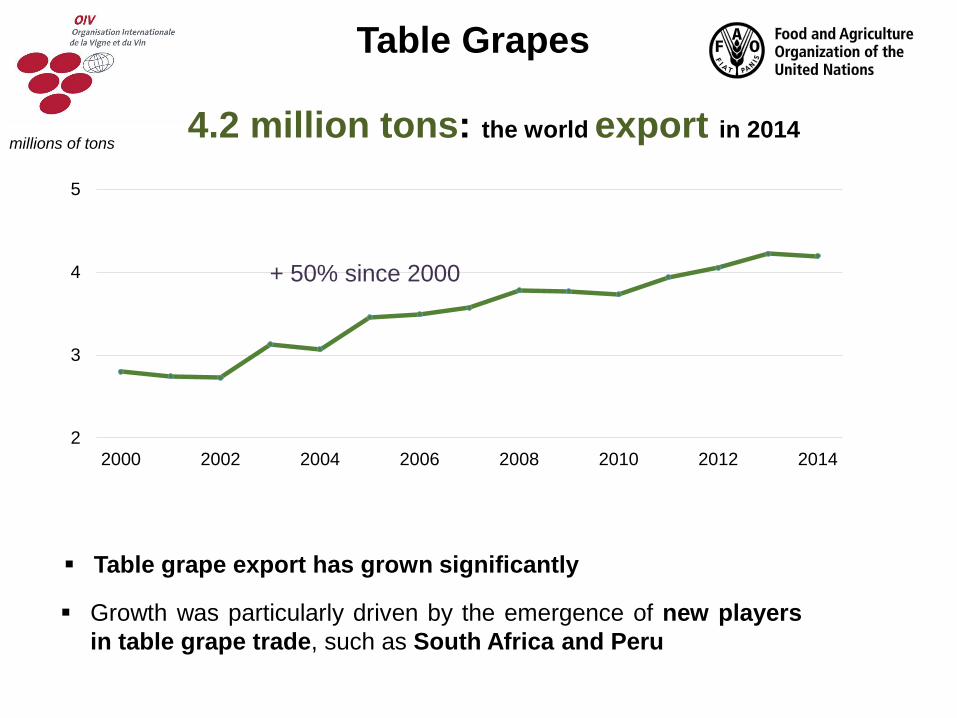

Table grape export has grown significantly

+ 50% since 2000

Growth was particularly driven by the emergence of new playersin table grape trade, such as South Africa and Peru

Table Grapes

4.2 million tons: the world export in 2014

Turkey28%

USA21%Iran

13%

China12%

Chile6%

Rest of the world

21%

0.8

1.2

1.6

2.0

2000 2002 2004 2006 2008 2010 2012 2014

million of tons

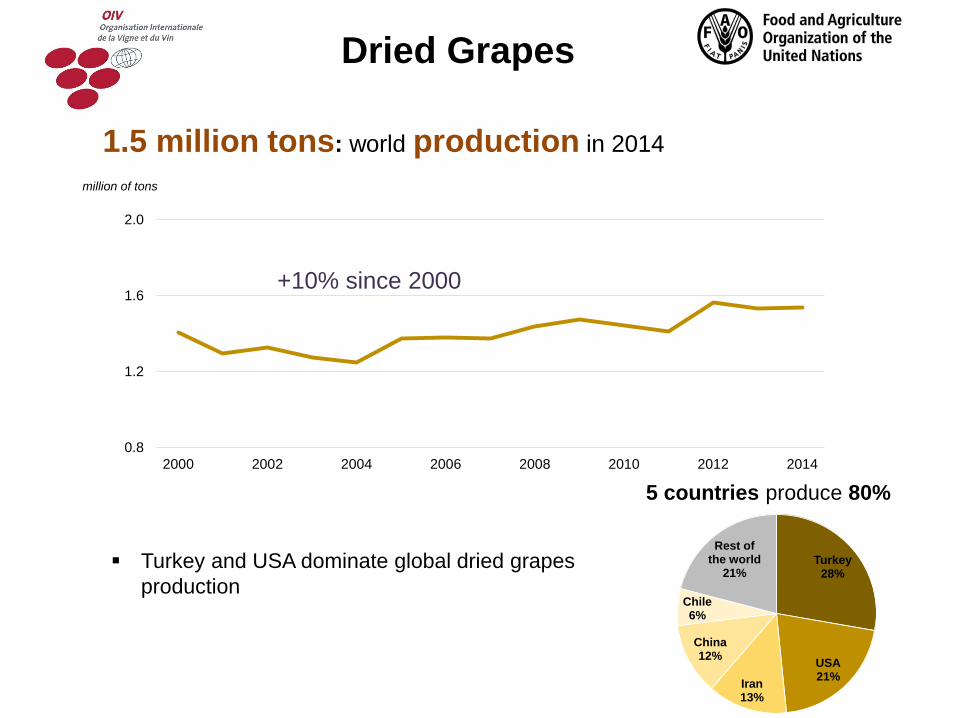

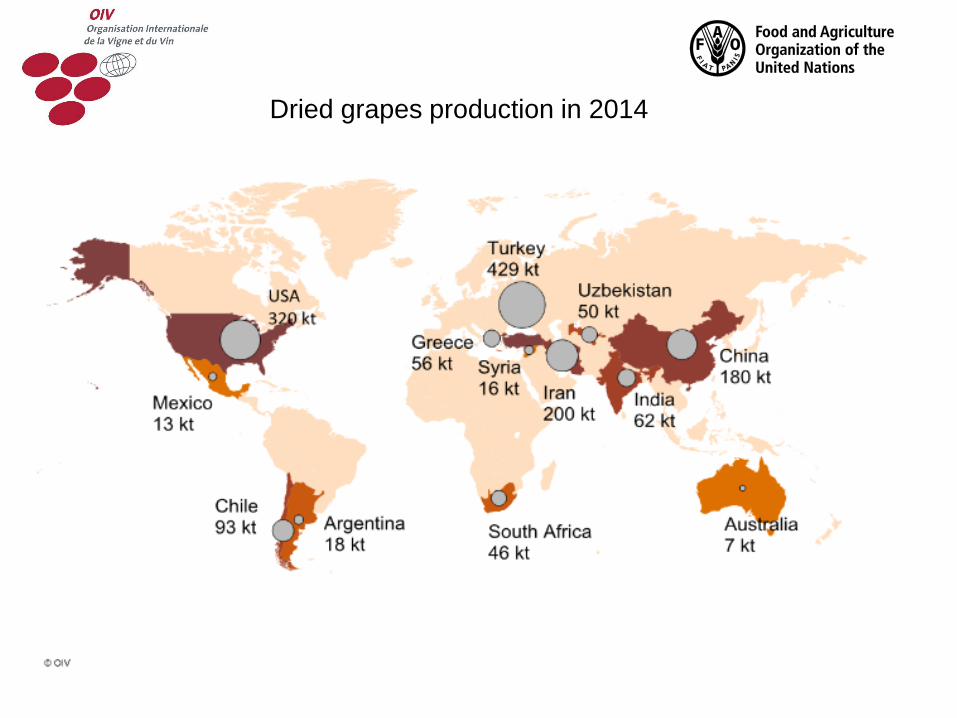

1.5 million tons: world production in 2014

Dried Grapes

Turkey and USA dominate global dried grapes production

+10% since 2000

5 countries produce 80%

Dried grapes production in 2014

1.0

1.4

1.8

2000 2002 2004 2006 2008 2010 2012 2014

million of tons

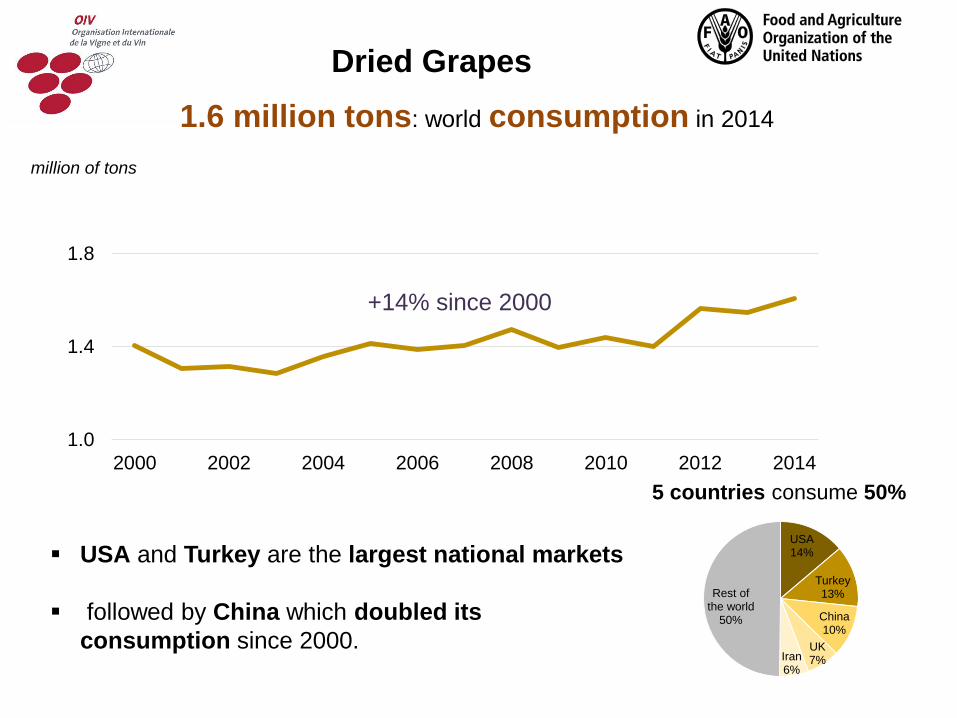

USA and Turkey are the largest national markets

followed by China which doubled its consumption since 2000.

Dried Grapes

+14% since 2000

5 countries consume 50%

1.6 million tons: world consumption in 2014

USA14%

Turkey13%

China10%

UK7%Iran

6%

Rest of the world

50%

400

500

600

700

800

900

1000

2000 2002 2004 2006 2008 2010 2012 2014

thousand of tons

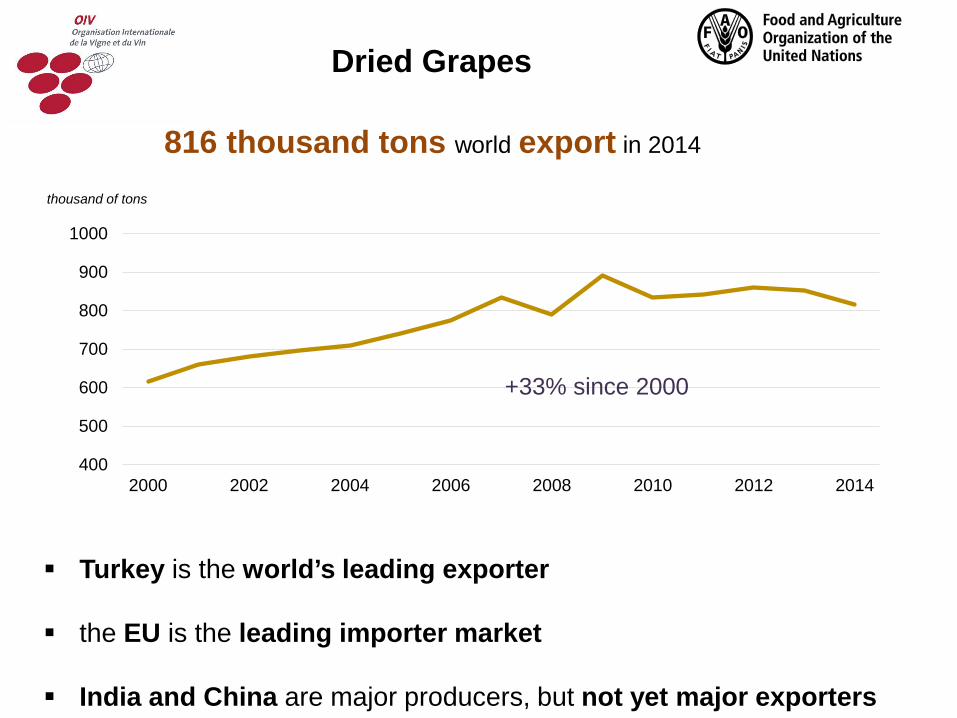

816 thousand tons world export in 2014

Turkey is the world’s leading exporter

the EU is the leading importer market

India and China are major producers, but not yet major exporters

Dried Grapes

+33% since 2000

Future actions:

How to improve the data collection of this segment of the sector?

The statistical data currently available on the quantities of grape juice produced and on intermediate unfermented products do not enable us to analyse these segments of the sector in further details

Thank you for your attention

Vielen Dank für Ihre Aufmerksamkeit

Grazie per la Loro attenzione

Gracias por su atención

Merci de votre attention

Obrigado