surrey learning disabilities costing survey cost … · 3 surrey learning disabilities costing...

TRANSCRIPT

1

SURREY LEARNING DISABILITIES COSTING SURVEY

COST ANALYSIS REPORT

Laing and Buisson

11 January 2013

2

SURREY LEARNING DISABILITIES COSTING SURVEY

COST ANALYSIS REPORT

Contents

Page

EXECUTIVE SUMMARY 5

RESULTS SUMMARY, CONCLUSIONS AND IMPLICATIONS DISCUSSION

INTRODUCTION

Introduction, objectives and confidentiality of data 6

Submissions received 7

Reliability of cost data 8

OVERVIEW OF RESULTS IN MEETING OBJECTIVES 8

CONCLUSIONS 19

SUGGESTIONS FOR THE WAY FORWARD 20

DETAILED RESULTS

OVERALL COSTS AND ADEQUACY OF FEES 25

RELATIVE UNIT COSTS AND FEES IN DIFFERENT HOUSING SETTINGS,

AND IN RELATION TO DIFFERENT LEVELS OF NEED 30

COST ANALYSIS WITHIN COST CATEGORIES 40

SALARIES AND STAFF COSTS 43

EXPENSES AND OVERHEADS

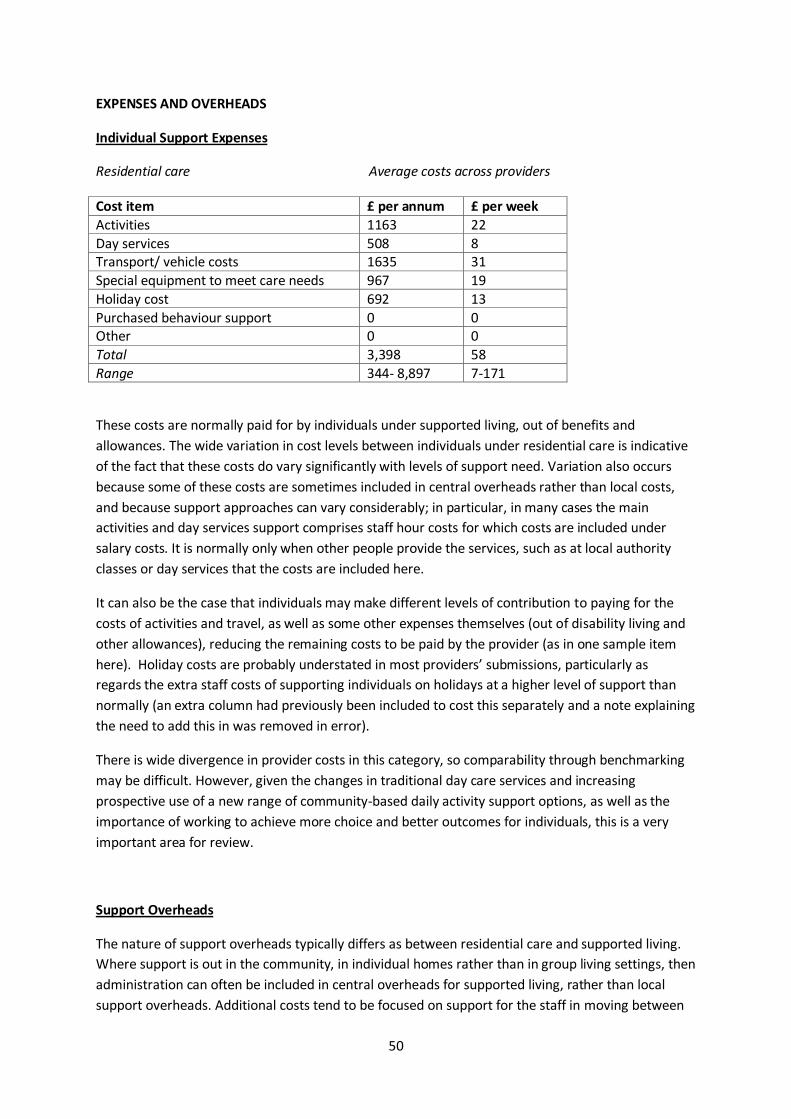

Individual Support Expenses 50

Support Overheads 50

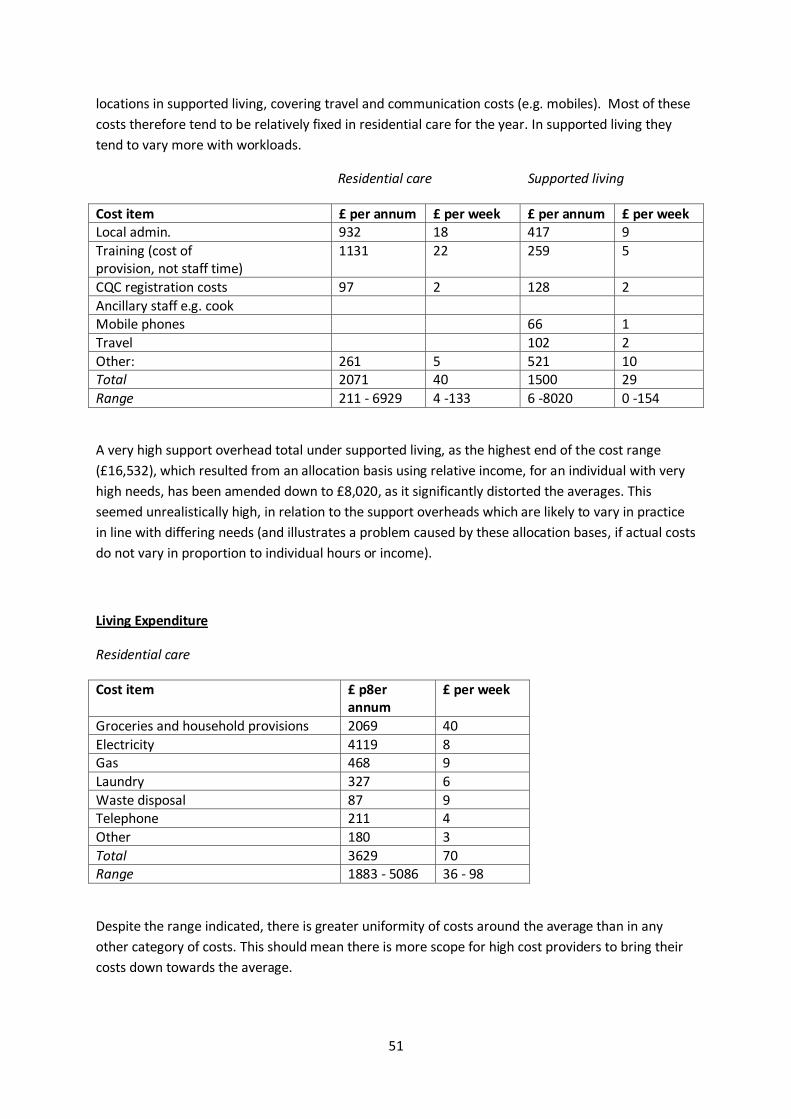

Living Expenditure 51

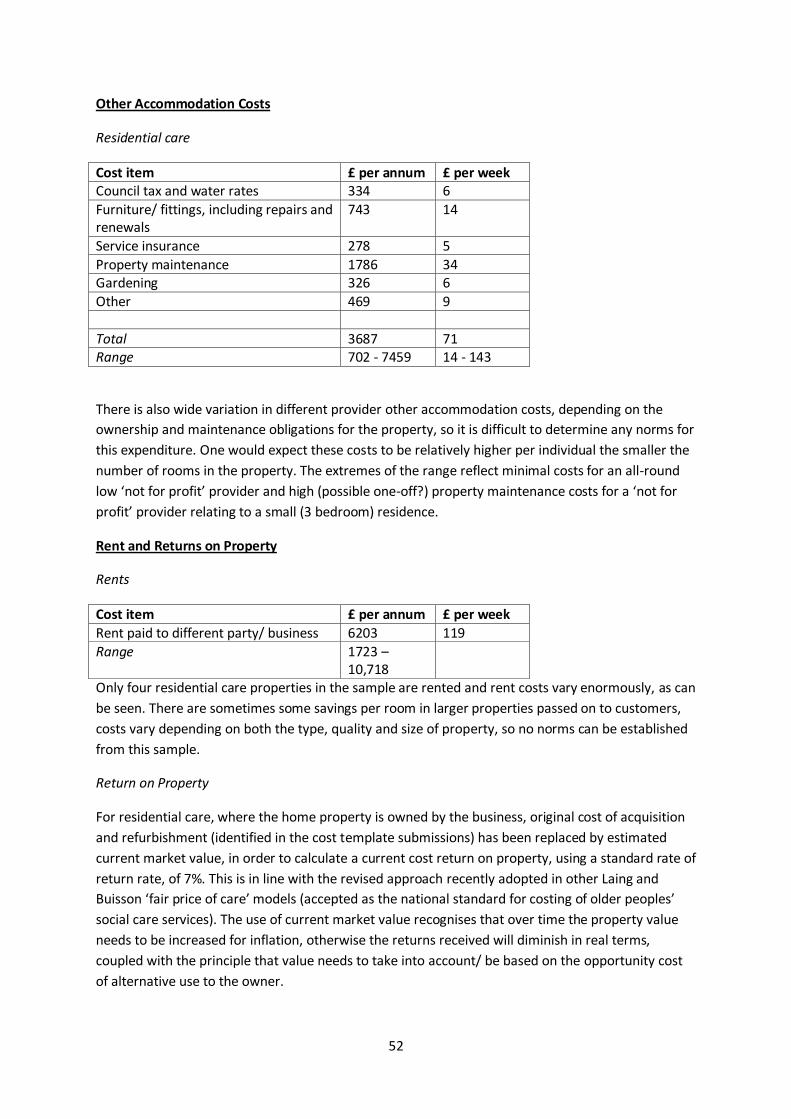

Other Accommodation Costs 52

Rent and Returns on Property 52

Central Overheads 54

3

SURREY LEARNING DISABILITIES COSTING SURVEY

COST ANALYSIS REPORT

EXECUTIVE SUMMARY

Objective

The overall objective of this study has been to establish the actual, true costs of care being incurred

by providers of residential care and supported living services, in relation to individuals with learning

disabilities in Surrey, through a costing survey.

For this purpose, direct costs of support as well as a proportion of all organisational overhead costs

have been allocated within each individual costing, and both a required mark-up on operational

costs and return on property (where owned), added in, to arrive at the true cost of care.

Responses received

20 residential care and 12 supported living examples have been reviewed, validated and included in

the results. This sample is considered sufficient to draw some indicative conclusions on actual/ true

current costs of care, as well as for initial consideration of sustainable cost issues.

Overview of results

For residential care, mark-up percentages on total current operational costs reflected by existing

fees range from -35.5% to +18.5%, with an average of -8.1%, across the sample of 20 analysed. The

median mark-up is -6.9%. There are wide differences between actual current mark-ups, in relation to

individuals, arising for many different reasons, including changes in support needs not reflected in

increased or reduced fees, inflation not matched by equal fee increases etc. It is difficult to draw

firm conclusions about the overall margins across 900 individuals in Surrey from this small sample.

However, the fact that the average level of mark-up is negative when most providers need a

certain minimum mark-up to continue in business is a cause for concern.

In terms of mark-ups required by providers these vary between 7 and 13% for ‘for profit’ providers

and 0 to 5% for ‘not for profit’ providers, within the sample, across residential care and supported

living. Comparing actual current or ‘true’ costs of care with the mark-ups required by providers

indicates a shortfall averaging 9 % across the residential care sample.

For supported living, mark-up percentages on total current support costs reflected by existing fees

range from -16.2% to +15.4%, with an average of +0.4%, for the 12 examples analysed. The median

mark-up is +2.6%. Comparing actual current or ‘true’ costs of care with the mark-ups required by

providers indicates a shortfall averaging 3.4 % across the sample.

There is a wide divergence of unit cost levels between different examples within the sample,

particularly as regards salary costs. Six of the residential care examples relate to individuals

supported in settings where very high cost salaries continue to need to be paid under TUPE transfer

arrangements, where support has been transferred from the NHS or other public sector provision.

There is no evidence that higher or lower positive or negative mark-ups than in the rest of the

4

sample result from TUPE provision, as fees have normally been set to take these higher costs into

account (some show quite large deficits, whilst others show quite large profits/ surpluses).

Sustainability and implications

The lack of inflationary fee increases together with downward pressures on fees have reduced

provider margins and meant that many providers have not been able to increase salaries over the

last two to three years. However, provider feedback now suggests that current low pay rates

(excluding TUPE situations,) for those providers paying average or below average salaries, are

unsustainably low, and that some increases are required soon if there is not to be a serious problem

with staff retention and a knock-on effect in ensuring that high quality services can continue to be

provided.

Providers are indicating that the mark-ups calculated in the sample are not untypical of those for

other Surrey clients, supported in the same housing and elsewhere in Surrey (i.e. there is a mix of

positive and negative mark-ups). Although the small size of sample used cannot possibly be

concluded to have produced statistically valid results, there is no reason, given the broad mix of

examples in the sample, in our view, to believe that the results in this ‘snapshot’ sample would not

be broadly mirrored if the analysis was extended across the whole population of individuals with

learning disabilities in Surrey. We would expect that mark-ups on average would fall well short of

provider requirements and it seems more likely that there would be a net deficit position overall

than net positive mark-ups.

The additional pressures of the increasing burden of regulatory compliance, the move towards

greater personalisation, the need to make higher employer pension contributions, continuing

inflation in expenses, as well as the pressures to increase salaries for many are likely to exacerbate

this situation. The impact of increasing voids in residential care and higher financing costs are also

putting extra pressure on financial viability.

Justifiability of costs and opportunities for further cost savings

Of course, this is not to say that all provider true cost levels are fully justifiable, or that there may

not be scope for further cost-savings, particularly given the wide diversity in cost levels indicated in

the sample.

This wide divergence in unit costs has also meant that it has proved difficult to ascertain clear

differences in this small sample between the salary costs per hour of supporting individuals with

lower and higher hours of support need, and between unit costs in different housing settings.

However, it has proved possible to compute average costs for each major cost component, and to

estimate these differences, so as to illustrate the likely overall cost ranges for different levels of need

within both residential care and supported living, and for different housing sizes within residential

care. Detailed analysis of the breakdown of average costs within each cost component has also been

produced, to aid cost benchmarking and identification of cost saving opportunities.

Whilst many providers have undertaken significant cost reduction initiatives over recent years and

would claim that there is very limited scope for further savings, the disparity in unit costs,

particularly in relation to the most significant area of salary costs, merits further detailed

5

consideration. It is not just rates of pay which affect these substantial costs, but also the mix of

senior and standard support staff and the levels and cost of supervision.

Previous experience suggests that while pay rates may not be high, in many instances, staffing mix

can become top heavy and overly costly over time, as promoted staff are sometimes not re-

deployed and staffing structures not fully adjusted to achieve the most cost-effective mix of

experience.

The large number of high salary cost ‘TUPE’ constrained salaries also poses a significant cost problem

in Surrey. Although, it is very difficult to change commitments to continue to respect previous salary

terms and conditions, some providers are now successfully arguing the case for harmonisation of

salaries on economic grounds. This would therefore seem to be an important area for further work

in reducing the demands on very limited budgets.

There is also wide variation in central overheads, in particular, which typically constitute 8 or 9% of

total costs, and seem to merit more detailed review.

Suggestions for the way forward

It may be appropriate to extend some aspects of the work to date, to validate initial findings at

individual level, and to consider the extent of financial deficits and related financial risks at overall

home/service levels and across businesses, bearing in mind sustainability, voids etc.

Suggestions have also been made for further work which could now be undertaken, to identify

different staff support unit costs per hour for different levels and types of need, as well as types of

support. This could also embrace better calibration of differences in unit costs for different housing

settings, paving the way for better informed calculation of the levels of unit costs justified.

We believe that serious consideration ought also to be given to the way in which fees are agreed

and, in particular, the way in which hourly fee rates are used in supported living. The mixing of direct

salary costs, which simply increase with extra hours of support, and a variety of variable and fixed

overheads which do not, gives rise to significant distortions in rates and their adequacy, in meeting

lower and higher levels of need. These mask genuine, justifiable differences in costs and can lead to

poor decisions on the cost-effectiveness of relative proposals and fees by the local authority, as well

as poor assessment of financial viability and pricing by providers.

An improved approach to fee setting could also greatly facilitate providers and the local authority

working much more cohesively together, collaborating more effectively in identifying 'efficient/

economic' cost levels, which also take account of economies of scale.

These and other suggestions could also be used to better address the re-assessment of individual,

future, more personalised support needs and related costs, in relation to which a major exercise is

under way. Whilst consideration of the level of support needs of individuals and personal budgets

has been outside our scope, this is clearly a very important, complementary area of study. There is

genuine potential to better respect individual choice in relation to support options, as well as to

identify opportunities to employ a more cost-effective mix of support resources, including greater

levels of community support. Better approaches to investing in developing independent living skills

and reducing dependency levels and support costs over time also need to be addressed.

6

SURREY LEARNING DISABILITIES COSTING SURVEY

COST ANALYSIS REPORT

RESULTS SUMMARY, CONCLUSIONS AND IMPLICATIONS DISCUSSION

INTRODUCTION

This report summarises findings and conclusions arising from the learning disabilities service

provision costing survey conducted by Laing and Buisson, on behalf of Surrey CC during October and

November 2012.

The Results Summary, Conclusions and Implications Discussion section sets out the detailed

objectives and discusses the sample and data received back, before summarising results achieved

against each of these objectives, and then exploring the issues relating to results, drawing

conclusions and setting out how the results might be used , in some possible next steps. For those

wishing to explore and use the results in more detail, the Detailed Results section includes a range

of charts and tables, as well as commentary on average costs under each cost component, which

may be of particular interest as benchmarks and to explore opportunities for improving cost-

effectiveness. The Executive Summary before this current section summarises the overall results

and conclusions in relation to actual/true costs of care in straightforward terms, and highlights a few

suggestions, as a basis for agreeing next steps.

Objectives

The overall objective of this study has been to establish the actual, true costs of care being incurred

by providers of residential care and supported living services, in relation to individuals with learning

disabilities in Surrey, through a costing survey.

More specifically, the subsidiary objectives have been to provide a range of different analyses, for

different purposes, including:

1) Overall costs by individual, to consider both the adequacy of current fees and to provide a

basis for calculating sustainable overall cost and fee levels for the future

2) An indication of the relative unit costs of supporting individuals in different housing settings

(particularly 3, 6, 8 and 10 bedroom homes within residential care), so as to take account of

this in future fee setting

3) An indication of any differences in unit support costs for individuals with different levels of

requirement, so as to help inform thinking around setting overall fee budgets and personal

budgets for those with different levels of need

4) An analysis of costs across providers within different cost categories, to provide benchmark

comparisons for providers, in furthering their (and Surrey CC’s) cost reduction objectives

In finalising the original proposal, a slightly revised definition of terms was agreed which then

described actual/true costs as being ‘current costs’, distinguishing these from ‘sustainable’ costs for

the future.

The idea of establishing sustainable cost levels is to recognise that in some cases current costs might

not be sufficient, for example, to recruit and retain sufficient numbers of good staff to deliver the

7

level of quality service required. On the other hand, particularly where staff have had to be taken on

from the public sector, as a result of service outsourcing, on guaranteed TUPE transfer

arrangements, then current costs might exceed sustainable, economic cost levels.

Sustainable costs need to be paid to ensure that good outcomes can continue to be provided for

individuals, that good quality providers continue to be financially viable and that future market

supply of services is sufficient to meet needs.

Confidentiality of data

In agreeing to provide data on current costs and actual margins, an undertaking was made in the

letter to providers that: “Only Surrey County Council (SCC) will ever know which individuals you have

been asked to provide cost data for, but only Laing and Buisson will ever know the individual cost

data you provide. Costs will never be reported back to SCC or anyone else on an individual or

organisation basis. All reporting will be at aggregate or average level”.

This has obviously meant that we have had to constrain the detailed reporting back on the results of

the exercise, especially in not disclosing individual costs and fees directly, but it has still been

possible to take into account the resultant actual mark-ups and deficits, in calculating averages and

in summarising the range of results obtained, as well as in drawing conclusions, focussing on

highlighting the true costs of care.

Submissions received

Residential Care:

Included in the analysis:

3 bed – 4

5 bed – 1

6 bed –7

7 bed - 1

8 bed –5

9 bed - 1

10 bed – 1

Total – 20 (out of a sample of 40)

Of these, 10 for profit and 10 not-for-profit. These cover only 14 providers, as some providers

submitted extra examples, to make up for shortfalls in other responses.

A further 2 examples were received but have not been included in the analysis, due to corrections

not having been received back, despite repeated requests. A further example has been received

from Surrey CC, but not analysed in detail, as received too late to include in the analysis.

(An additional 10 in the sample were not followed through as these were duplicate costings within the same

homes, and a further 7 examples were provided, beyond the initial sample).

Supported Living:

Total, for range of housing settings: - 12 (out of a sample of 20).

4 for profit and 8 not-for-profit.

A further 2 examples have been received but have not been included in the analysis; one of these

8

was not corrected/completed, due to difficulties in aligning overhead costs in the midst of

restructuring, whilst one was excluded as not representative of typical supported living costs or fees.

Failure to respond can be put down to a combination of reasons, but mainly lack of resources arising

from other work pressures (particularly as many providers are now also finalising budgets for next

year), absence of in-house costing skills or temporary non-availability of key management, rather

than lack of support for the initiative.

Whilst overall numbers of useable responses are somewhat disappointing, there are considered to

be sufficient to draw worthwhile conclusions and to provide a basis to build on for cost estimation

and fee setting.

Reliability of cost data

A lot of time was spent at the outset to produce robust and flexible costing templates, to ensure that

costings can be properly computed, as well as to provide flexible options for providers to be able to

compute costs, and to allocate overhead costs in particular, especially within supported living.

Although the range of options incorporated has meant additional complexity at first sight, and more

time required for providers to understand and get to grips with the templates, this does seem to

have worked well in terms of the results produced. Where input has looked incorrect, or

unexpected results have been produced, these have been questioned rigorously with providers and

amended where necessary. The fact that data for each provider is being treated confidentially and

that all the results have been reviewed for reasonableness means that the results are considered to

be reliable, for purpose, as actual current costs (though this is different from confirming the levels as

necessarily fully justifiable).

Overall margins have first been compared with fees, before the detailed cost analysis has been

reviewed and comments made on cost levels, including consideration of justifiability. All submissions

have been tabled in a range of cost analyses, which have then been used to calculate and compare

key unit costs and ratios.

As well as including an overview of results in meeting objectives, this section of the report includes

consideration of the impact of inadequate mark-ups and deficits, overall fees and the use of

different cost data for different purposes, as well as conclusions and suggestions for further work,

with a range of questions to consider.

OVERVIEW OF RESULTS IN MEETING OBJECTIVES

Results in meeting specific objectives have been summarised below.

OVERALL COSTS AND THE ADEQUACY OF FEES

Objective 1: Analyse overall costs by individual, to consider both the adequacy of current fees and

to provide a basis for calculating sustainable overall cost and fee levels for the future

9

Given the number and mix of submissions received back from providers, and the effective operation

of the tailored costing models developed, it has been possible to fully analyse submissions received,

to calculate current costs and identify mark-ups being achieved in relation to actual fee levels.

This is at an individual level and highlights the extent of any over or under funding, assuming that

levels of need are already correctly assessed i.e. no consideration has been given to whether the

hours of support commissioned and other support arrangements are sufficient or greater than

necessary, as this was outside the scope of the survey. Useful insights have also been gained in

relation to sustainable costs, although more work is needed to consider sustainable fee levels for the

future.

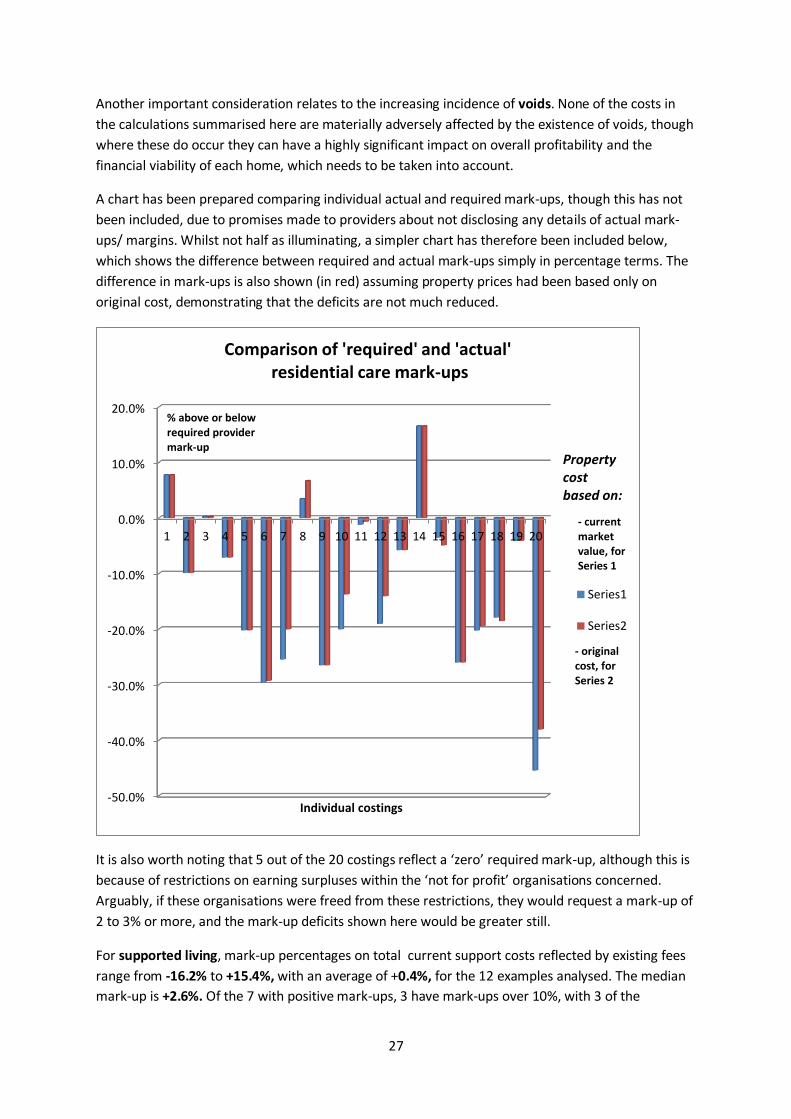

For residential care, mark-up percentages on total current operational costs reflected by existing

fees range from -35.5% to +18.5%, with an average of -8.1%, across the sample of 20 analysed. The

median mark-up is -6.9%. Of 7 with positive mark-ups, only 2 have mark-ups in excess of 15%, while

the remaining 5 show mark-ups of less than 10%. Whereas, of the 13 with deficits, only 4 show

deficits of under 6%, while the remaining 9 all show deficits of over 13%. There are wide differences

between actual current mark-ups, in relation to individuals, arising for many different reasons,

including changes in support needs not reflected in increased or reduced fees, inflation not matched

by equal fee increases etc.

Neither whether the provider is a ‘for profit’ or ‘not for profit’ provider, nor whether the individual is

in a ‘high salary cost’ placement or otherwise seems to have a clear, discernible bearing on surpluses

or deficits arising. 6 out of 20 examples relate to situations where ‘high salary costs’ continue to

need to be paid under TUPE arrangements, for individuals transferred from hospitals and other

public sector provision. Fees have generally been increased to address these higher cost

commitments, but some are now showing surpluses while others are in deficit. It is difficult to draw

firm conclusions about the overall margins across 900 individuals in Surrey from this small sample.

However, the fact that the average level of mark-up is negative when most providers need a

certain minimum mark-up to continue in business is a cause for concern.

In terms of mark-ups required by providers (per their submissions, across both residential care and

supported living examples), these vary between 7 and 13% for ‘for profit’ providers and 0 to 5% for

‘not for profit’ providers, within the sample, taking account of different financing and ownership

arrangements, particularly for ‘for profit’ providers, as well as charity restrictions on a making a

surplus, for ‘not for profits’. Comparing actual current or ‘true’ costs of care with the mark-ups

required by providers indicates a shortfall averaging 9 % across the residential care sample,

reflecting the fact that some of the largest deficits are offset by zero or low mark-up requirements,

in some cases, reducing the average gap.

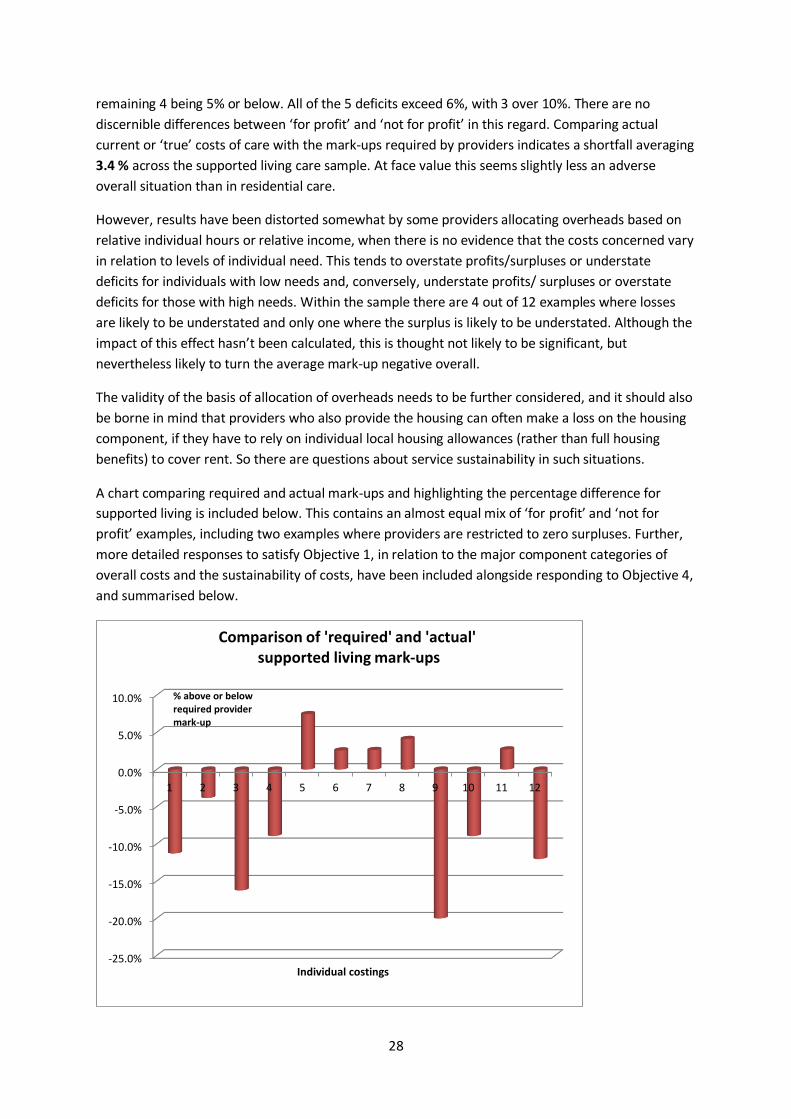

For supported living, mark-up percentages on total current support costs reflected by existing fees

range from -16.2% to +15.4%, with an average of +0.4%, for the 12 examples analysed. The median

mark-up is +2.6%. Of the 7 with positive mark-ups, 3 have mark-ups over 10%, with 3 of the

remaining 4 being 5% or below. All of the 5 deficits exceed 6%, with 3 over 10%. There are no

discernible differences between ‘for profit’ and ‘not for profit’ in this regard. Comparing actual

current or ‘true’ costs of care with the mark-ups required by providers indicates a shortfall averaging

3.4 % across the supported living care sample. At face value this seems slightly less an adverse

overall situation than in residential care.

10

However, results have been distorted somewhat by some providers allocating overheads based on

relative individual hours or relative income, when there is no evidence that the costs concerned vary

in relation to levels of individual need. This tends to overstate profits/surpluses or understate

deficits for individuals with lower needs and, conversely, understate profits/ surpluses or overstate

deficits for those with high needs. Within the sample there are 4 out of 12 examples where losses

are likely to be understated and only one where the surplus is likely to be understated. Although the

impact of this effect hasn’t been calculated, this is thought not likely to be significant, but

nevertheless likely to turn the average mark-up negative overall.

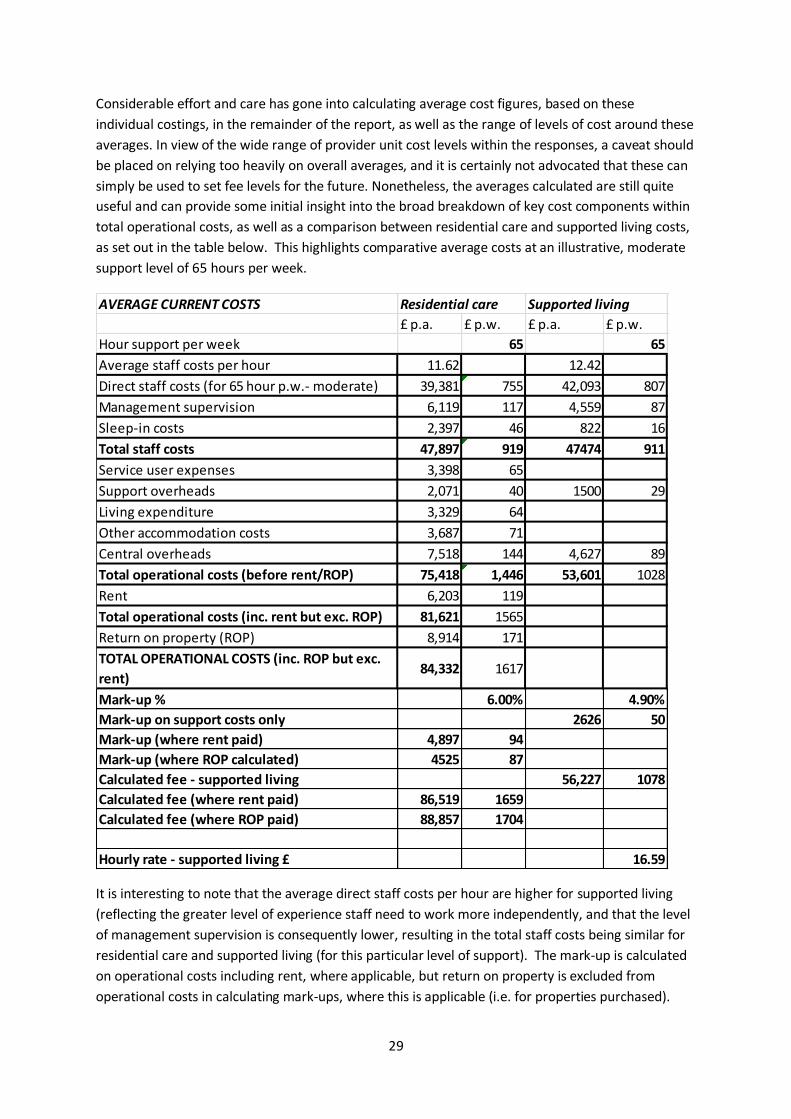

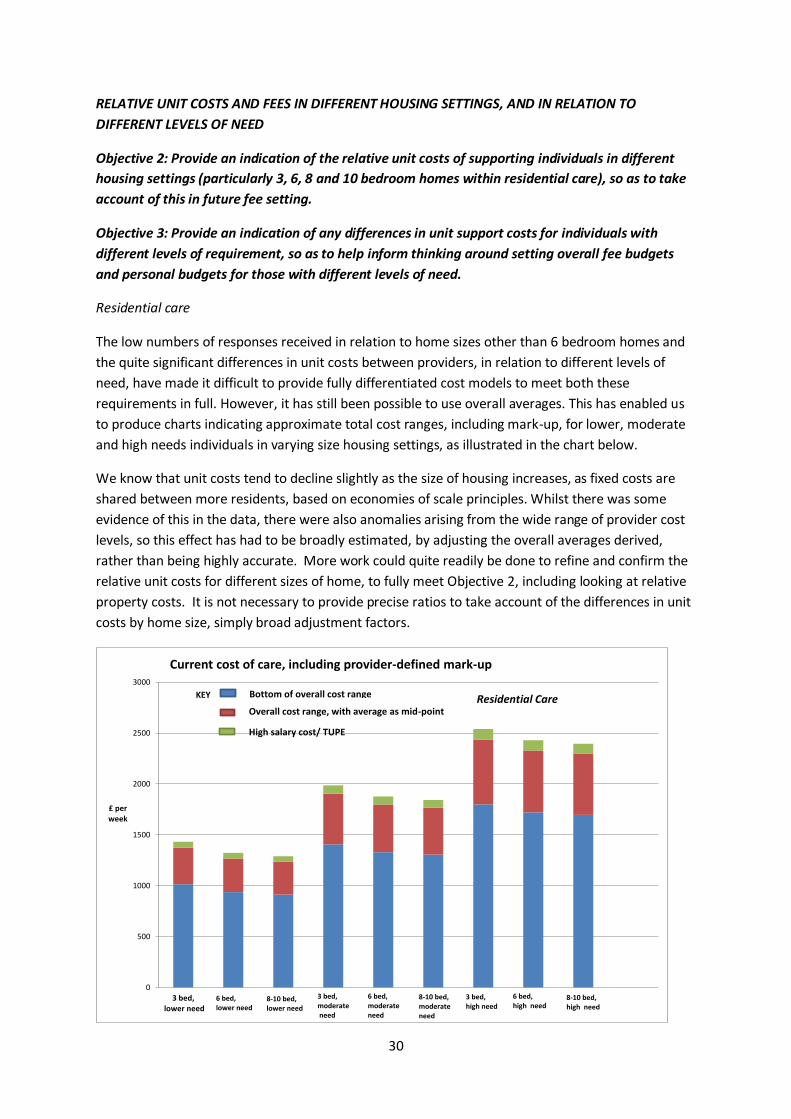

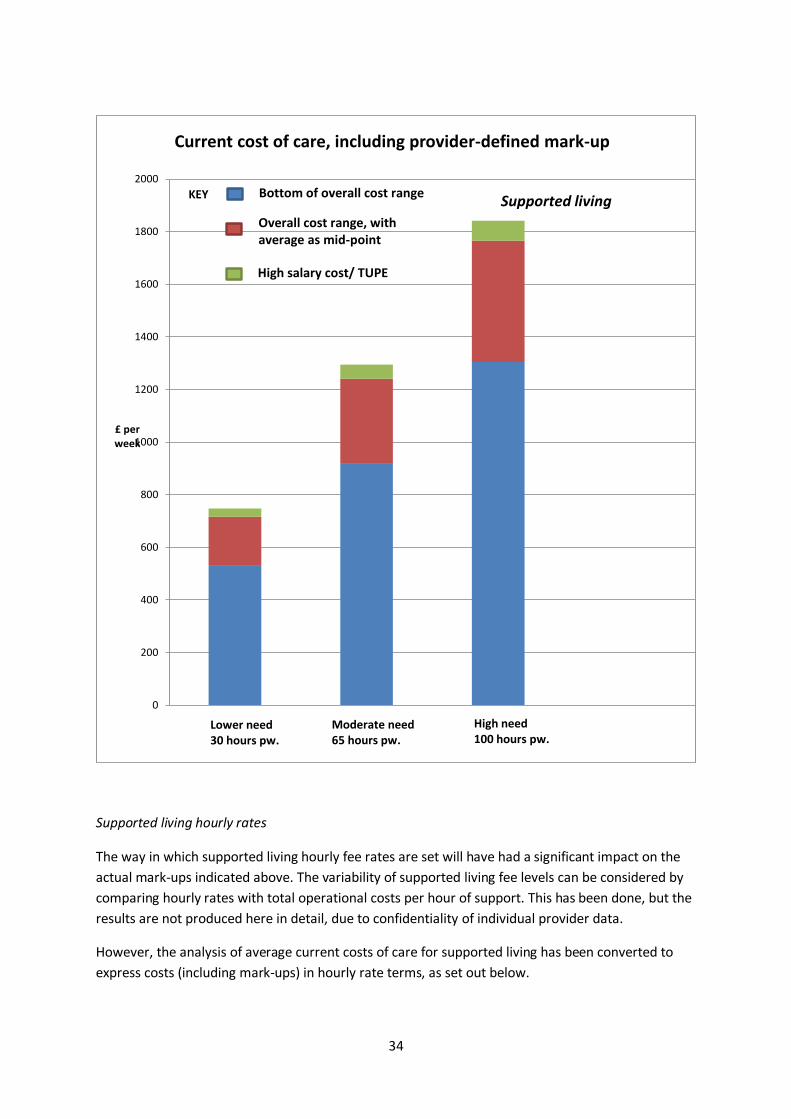

RELATIVE UNIT COSTS AND FEES IN DIFFERENT HOUSING SETTINGS, AND IN RELATION TO DIFFERENT LEVELS

OF NEED

Objective 2: Provide an indication of the relative unit costs of supporting individuals in different

housing settings (particularly 3, 6, 8 and 10 bedroom homes within residential care), so as to take

account of this in future fee setting.

The low numbers of responses received in relation to home sizes other than 6 bedroom homes and

the quite significant differences in unit costs between providers, in relation to different levels of

need, have made it difficult to provide fully differentiated cost models to meet both these

requirements in full. However, it has still been possible to use overall averages.

This has enabled us to produce charts indicating approximate total cost ranges, including mark-up,

for lower, moderate and high needs individuals in varying size housing settings, as illustrated in the

detailed report, for residential care. We know that unit costs tend to decline slightly as the size of

housing increases, as fixed costs are shared between more residents, based on economies of scale

principles. Whilst there was some evidence of this in the data, there were also anomalies arising

from the wide range of provider cost levels, so this effect has had to be broadly estimated, rather

than being highly accurate.

More work could quite readily be done to refine and confirm the relative unit costs for different

sizes of home, to fully meet Objective 2, including looking at relative property costs. It is not

necessary to provide precise ratios to take account of the differences in unit costs by home size,

simply broad adjustment factors.

Objective 3: Provide an indication of any differences in unit support costs for individuals with

different levels of requirement, so as to help inform thinking around setting overall fee budgets

and personal budgets for those with different levels of need.

Nor has it been possible, for the same reasons, to identify differences in staff unit costs per hour, as

between individuals with lower needs and those with higher average needs. We would expect that

staff working with those with higher needs would need to be more experienced and higher paid

individuals, but this cannot be identified from the data, due to differences in levels of cost between

providers, when looking at examples for individuals with different hours of support requirements.

In practice this is likely to have more of an effect in supported living, where there is more dedicated

staffing, as opposed to shared staffing in group living. There will be some difference in residential

11

care, but it should not be so material, in the context of the range of overall average unit costs

produced. An estimated adjustment has, though, been made in charts produced for supported

living. The best way to fully meet objective 3, would be to calibrate this effect first within a single

cost structure (by looking at costs in support of different levels of need for a single provider, where

pay structures are consistent), and then to validate and refine the differentials for staff unit costs, by

repeating the exercise within one or two other providers, for different levels of need.

It would also be expected that levels of management supervision, behaviour management support

and individual expenses would increase for individuals with higher support needs, increasing average

unit costs accordingly. But again this cannot be discerned from the data received given, in addition,

that many submissions were for similar levels of moderate to high needs placements in residential

are. Refinement of unit costs for different levels of need for these factors could also be achieved as

part of the same exercise to understand differences in staff unit costs.

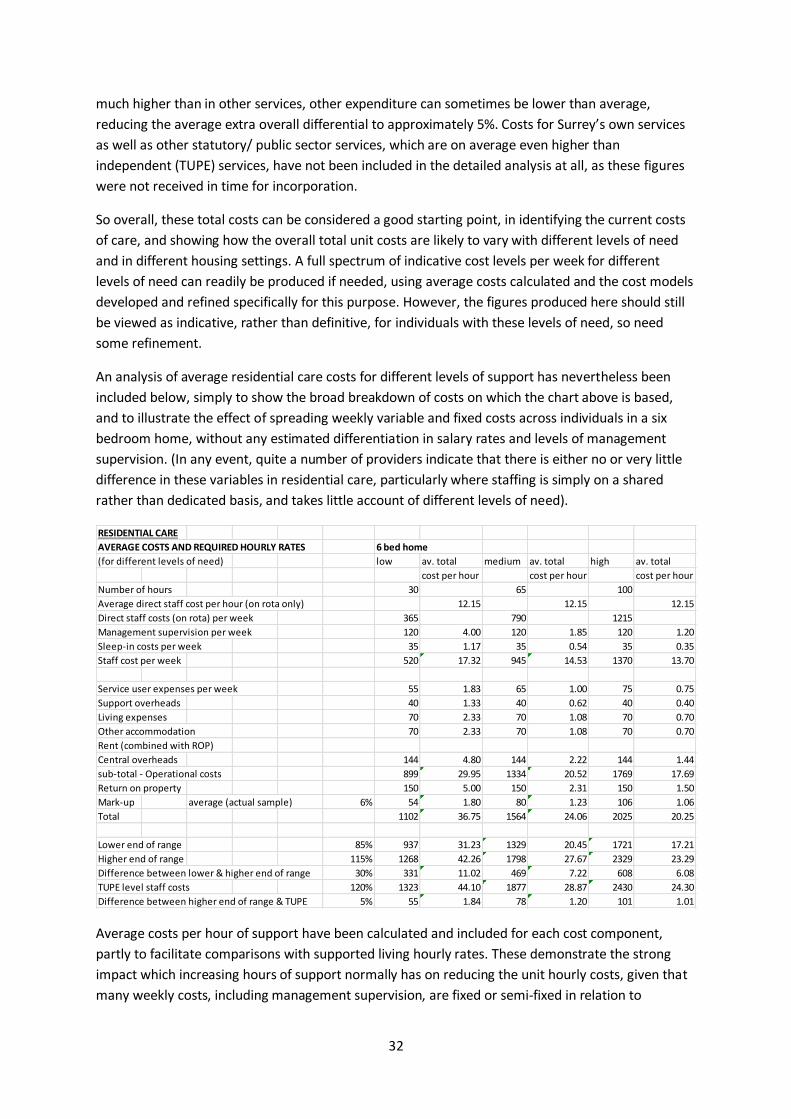

Nonetheless, it has been possible to produce a considerable amount of analysis of average costs

across providers, for both residential care and supported living, and this has proved useful in

identifying the main differences in unit costs for different levels of need, based on a combination of

variable and semi-variable salary related hourly costs and fixed or semi-fixed weekly costs, for all the

other major cost categories. These analyses have been included in the detailed report.

So overall, these total costs can be considered a good starting point, in identifying the current costs

of care, and showing how the overall total unit costs are likely to vary with different levels of need

and in different housing settings. A full spectrum of indicative cost levels per week for different

levels of need can readily be produced if needed, using average costs calculated and the cost models

developed and refined specifically for this purpose. However, the figures produced here should still

be viewed as indicative, rather than definitive, for individuals with these levels of need.

COST ANALYSIS WITHIN COST CATEGORIES

Objective 1: Analyse overall costs by individual, to consider both the adequacy of current fees and

to provide a basis for calculating sustainable overall cost and fee levels for the future

Objective 4: Provide an analysis of costs across providers within different cost categories, to

provide benchmark comparisons for providers, in furthering their (and Surrey CC’s) cost reduction

objectives

Sections have been set out in the main report which consider each major component of costs in

turn, commenting on the level and variability of these costs, as well as considerations relating to

sustainability- in addressing Objective 1. Some useful analysis has also been produced in support of

Objective 4, with average costs being adjusted by line item within each cost category, so that

averages are not distorted by different numbers of times that costs are reported in each line item.

This analysis is also described in detail in the main report. Only a few key points from the three key

cost category sections are summarised here.

12

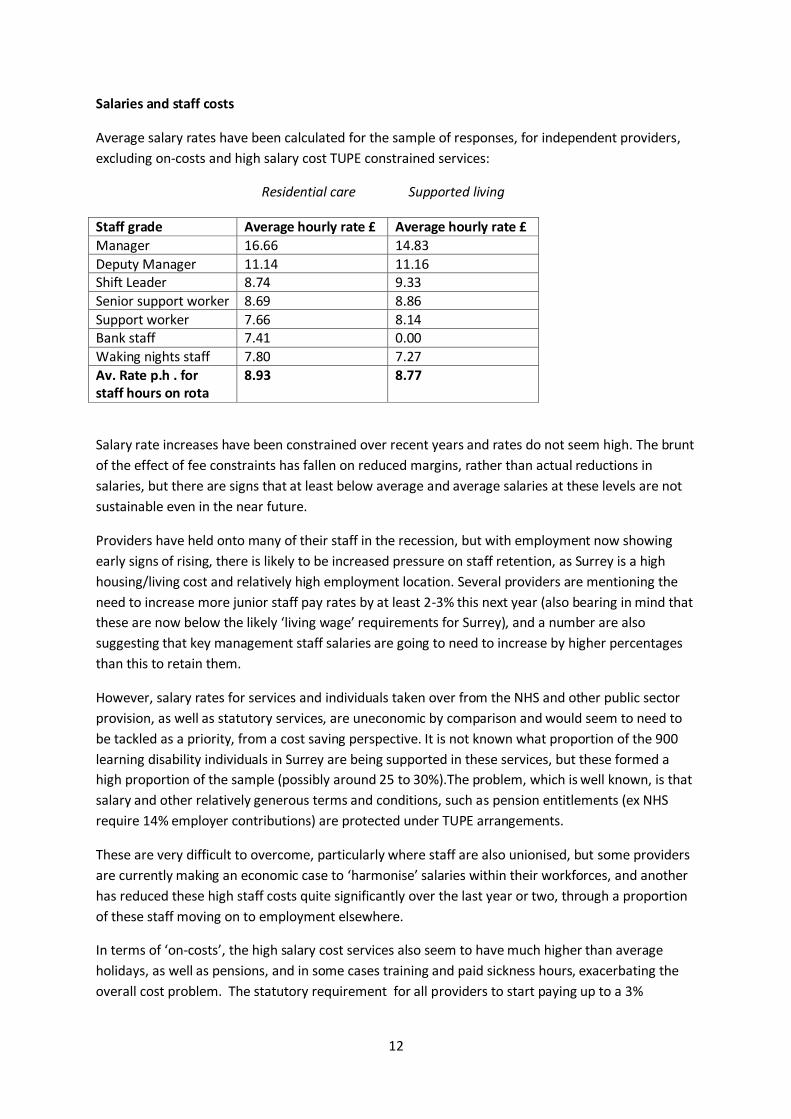

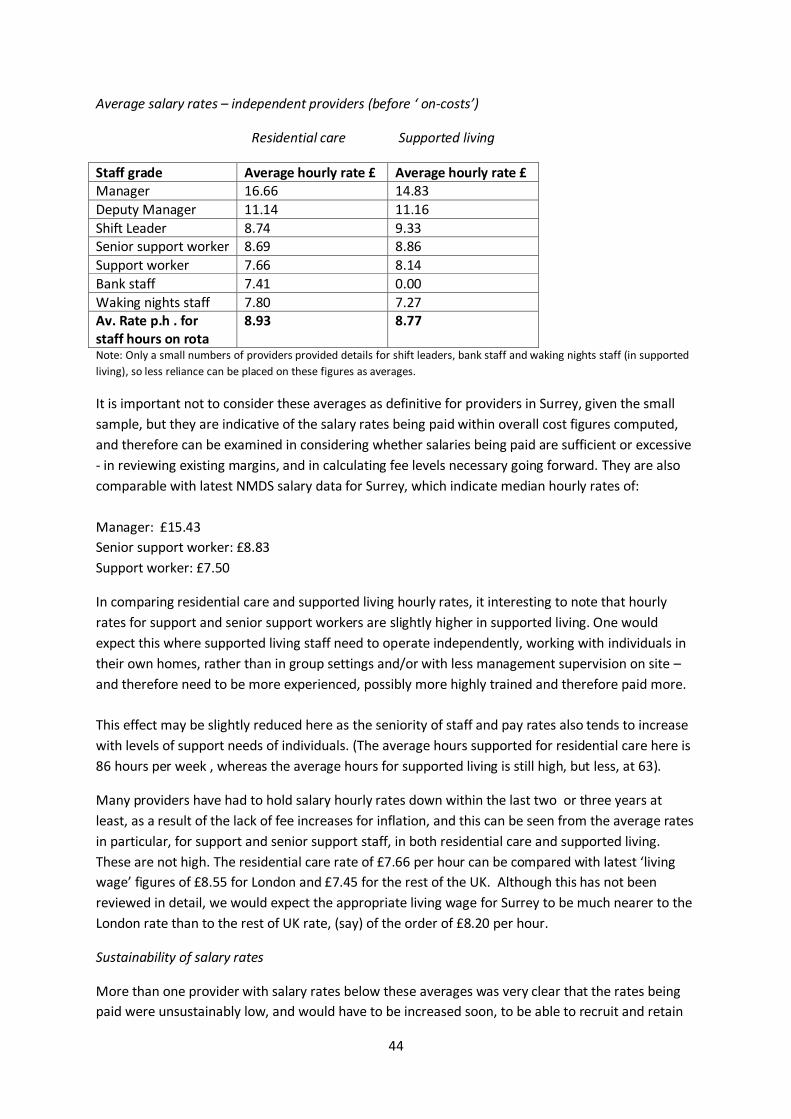

Salaries and staff costs

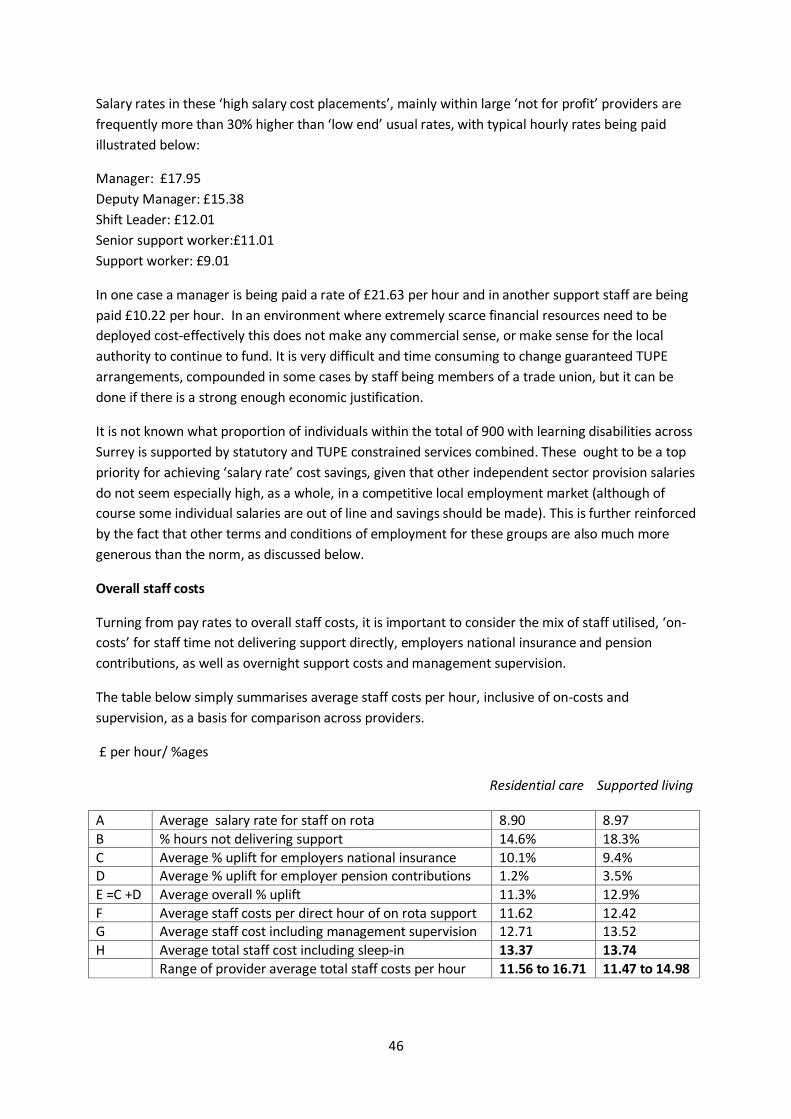

Average salary rates have been calculated for the sample of responses, for independent providers,

excluding on-costs and high salary cost TUPE constrained services:

Residential care Supported living

Staff grade Average hourly rate £ Average hourly rate £

Manager 16.66 14.83

Deputy Manager 11.14 11.16 Shift Leader 8.74 9.33

Senior support worker 8.69 8.86

Support worker 7.66 8.14 Bank staff 7.41 0.00

Waking nights staff 7.80 7.27

Av. Rate p.h . for staff hours on rota

8.93 8.77

Salary rate increases have been constrained over recent years and rates do not seem high. The brunt

of the effect of fee constraints has fallen on reduced margins, rather than actual reductions in

salaries, but there are signs that at least below average and average salaries at these levels are not

sustainable even in the near future.

Providers have held onto many of their staff in the recession, but with employment now showing

early signs of rising, there is likely to be increased pressure on staff retention, as Surrey is a high

housing/living cost and relatively high employment location. Several providers are mentioning the

need to increase more junior staff pay rates by at least 2-3% this next year (also bearing in mind that

these are now below the likely ‘living wage’ requirements for Surrey), and a number are also

suggesting that key management staff salaries are going to need to increase by higher percentages

than this to retain them.

However, salary rates for services and individuals taken over from the NHS and other public sector

provision, as well as statutory services, are uneconomic by comparison and would seem to need to

be tackled as a priority, from a cost saving perspective. It is not known what proportion of the 900

learning disability individuals in Surrey are being supported in these services, but these formed a

high proportion of the sample (possibly around 25 to 30%).The problem, which is well known, is that

salary and other relatively generous terms and conditions, such as pension entitlements (ex NHS

require 14% employer contributions) are protected under TUPE arrangements.

These are very difficult to overcome, particularly where staff are also unionised, but some providers

are currently making an economic case to ‘harmonise’ salaries within their workforces, and another

has reduced these high staff costs quite significantly over the last year or two, through a proportion

of these staff moving on to employment elsewhere.

In terms of ‘on-costs’, the high salary cost services also seem to have much higher than average

holidays, as well as pensions, and in some cases training and paid sickness hours, exacerbating the

overall cost problem. The statutory requirement for all providers to start paying up to a 3%

13

employer pension contribution within the next year or two is also already adding to the burden of

staff costs.

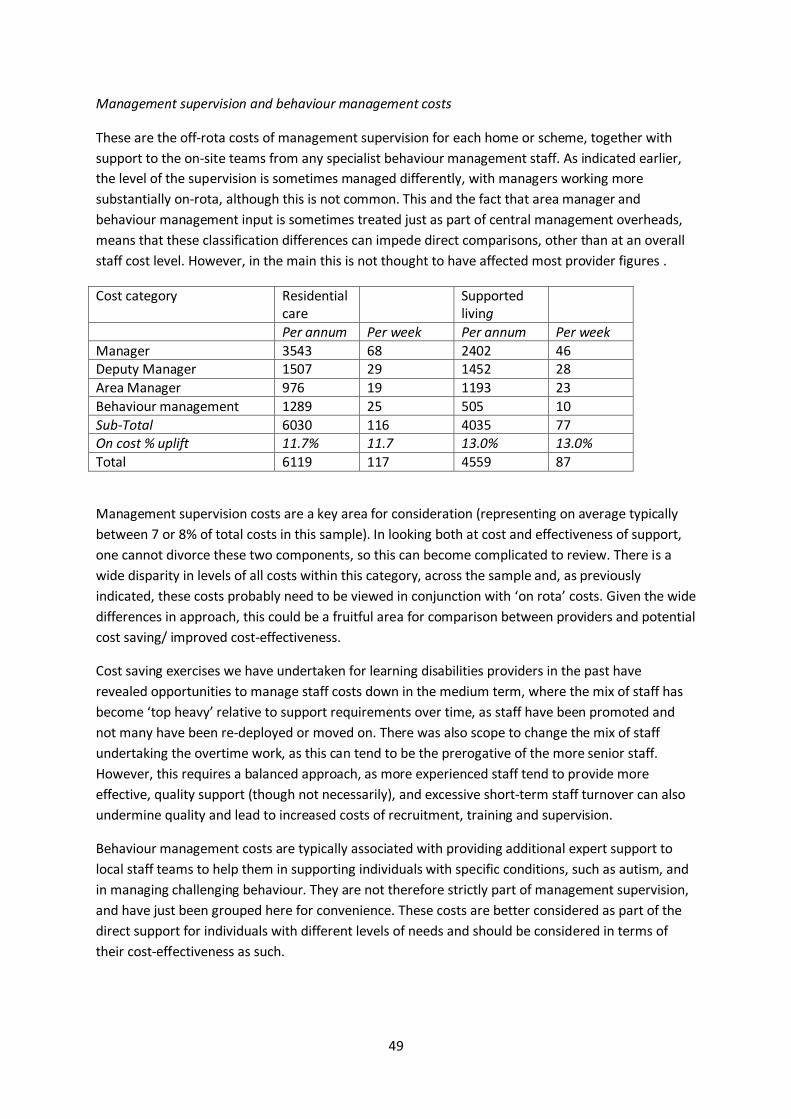

Management supervision costs vary considerably across providers and may still offer some scope for

improving cost-effectiveness. Several large ‘not for profit’, as well as some ’for profit’ providers

have taken layers out of area management supervision, increasing spans of control. In other cases

there are different approaches being followed to use or otherwise of management staff on the rota,

which might be a fruitful area to explore, in terms of relative costs.

It is therefore important for providers to look at staff costs overall, rather than simply treating

supervision as totally separate from ‘on rota’ costs. It is also important to look at the mix of staff

used both on and off rota, in exploring whether the overall average staffing cost might be too high,

even if hourly staff pay rates are not in any way excessive, or even perhaps sufficient.

Cost saving exercises we have undertaken for learning disabilities providers in the past have

revealed opportunities to manage staff costs down in the medium term, where the mix of staff has

become ‘top heavy’ relative to support requirements over time, as staff have been promoted and

not many have been re-deployed or moved on. There was also scope to change the mix of staff

undertaking the overtime work, as this can tend to be the prerogative of the more senior staff.

However, this requires a balanced approach, as more experienced staff tend to provide more

effective, quality support (though not necessarily), and excessive short-term staff turnover can also

undermine quality and lead to increased costs of recruitment, training and supervision.

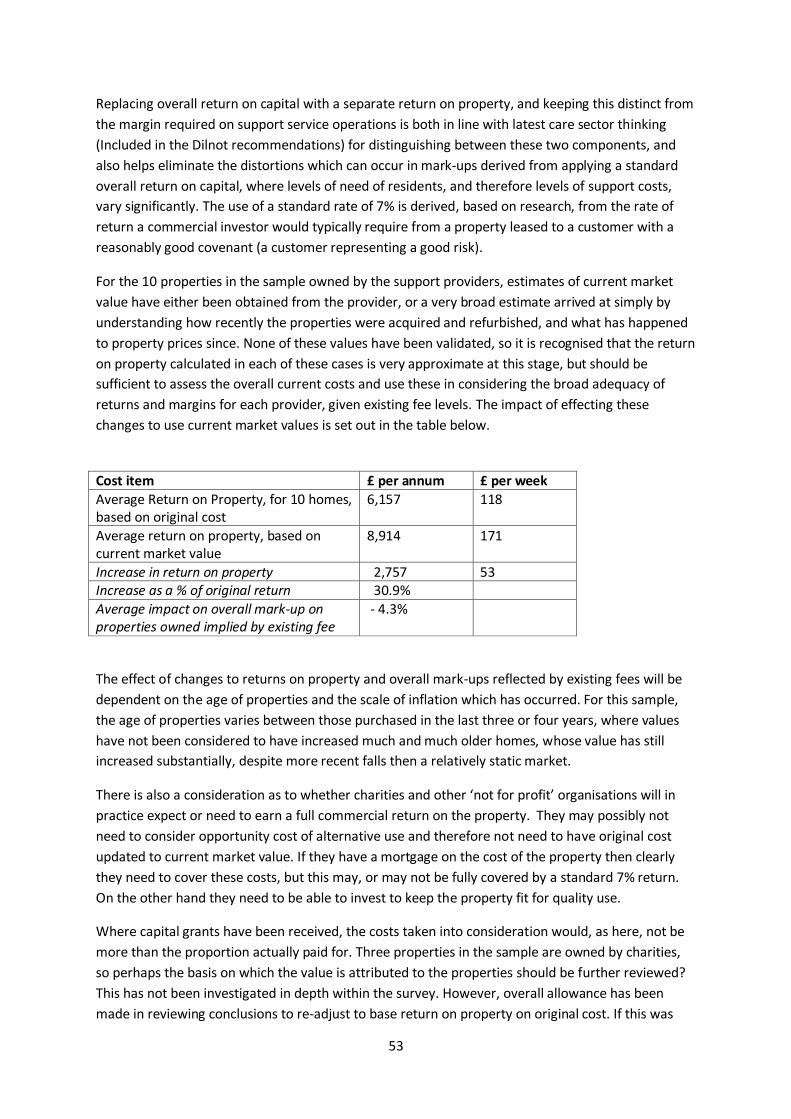

Return on Property

A new approach has been used (for the first time in learning disabilities) to calculate these costs for

residential care, splitting out the return on the property from the mark-up on operational costs

needed, to replace the approach based on calculating an overall return on capital, as used in the

care funding calculator. (This has been shown to give rise to some anomalous results, for smaller

homes and higher needs residents). A 7% return has been used, based on Laing and Buisson

research on the rate of return a commercial investor would typically require from a property leased

to a customer with a reasonably good covenant (i.e. representing a good risk). This is consistent with

the approach which has now been adopted in the Laing & Buisson ‘fair market price’ models for

older peoples’ residential and nursing social care.

Property costs have been updated from original cost to a very broad estimate of current market

value for each property, to allow for the maintenance of returns in real terms, due to the impact of

inflation. Provider estimates of market values have been discounted somewhat to recognise that

conversion of homes for alternative use might reduce values. It is recognised that the figures used

for these returns are only approximate and that more work ought to be done in this area, to assess

market values more rigorously, and to analyse and justify the impact on overall fees, if this approach

is to be taken forward and applied more widely.

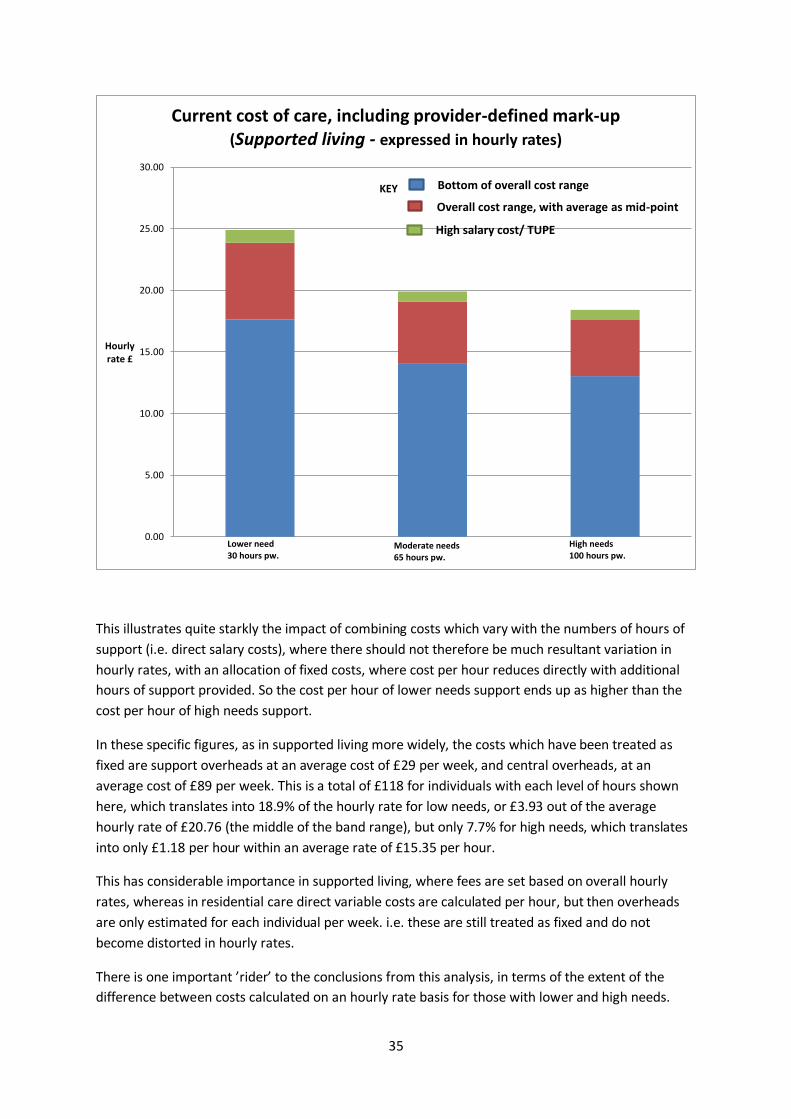

Central Overheads

These represent quite a large proportion of overall operational costs. Within the charts produced

and already discussed, average central overheads derived from the sample and included for

residential care amount to £144 per week (9.2% of average operational costs) and for supported

14

living £89 per week (8.6% of average operational costs) per individual. It is not clear exactly why

there is such a big difference between residential care and supported living and this might usefully

be explored further, along with the differences between organisations of different sizes.

One would expect some central costs not to be applicable to supported living, and in particular

property maintenance costs, as housing-related costs need to be covered by housing benefits, rather

than social care budgets. Other complications relate to the basis of charging for central overheads,

sometimes based on relative income for each scheme, sometimes as a percentage of direct costs,

occasionally including a margin (all of which have hopefully been stripped out in the sample data).

Central overheads are an important area for further exploration from a cost-saving perspective.

IMPACT OF INADEQUATE MARK-UPS AND DEFICITS

Providers have been asked specifically, wherever individual costings show a surplus or a deficit,

whether this result is expected or surprising, what the reasons might be, and whether the result is

typical of the results which might be found for other individuals in the same home or service, or in

other Surrey services. Generally, the feedback has been that these are not untypical results, and that

similar costings and financial outcomes would be likely to be found in looking at other Surrey

individuals for the same provider.

Of course, there are some exceptions to this, where individuals are known to be over or under

funded relative to their needs, but these may tend to balance out across the sample. Although the

small size of sample used cannot possibly be concluded to have produced statistically valid results,

there is therefore no reason to believe that the results in this ‘snapshot’ sample would not be

broadly mirrored if the analysis was extended across the whole population of learning disability

individuals in Surrey. Given the reasonably typical mix of individuals and providers in the sample, as

well as our discussions with providers, we believe that the overall picture should be broadly similar,

although average costs and mark-ups calculated within the sample will be bound to differ to a

degree from those for the whole population of individuals. It should be emphasised that this is a

judgement based on our knowledge and experience, rather than a definitive conclusion.

Given that the sample results indicated that on average providers are experiencing deficits in

residential care and probably also in supported living, or possibly breakeven on average at best,

discussion within the project steering committee considered the question as to whether these net

overall deficit results are being fully evidenced in practice by providers. Various reasons were

suggested as to why the adverse effect of inadequate margins may not be as evident as expected:

1) Where providers are supporting individuals from other local authorities, those fees may not

be as restricted as in Surrey

2) Where residential care providers are long established and have substantially paid off their

mortgages, cash-flow may not be as adverse as deficits indicated; or not-for-profit providers

may not require a full commercial return on property

3) Timing – the adverse effect of fee restrictions/ reductions is only now being felt most

significantly in the current years trading, but will be reflected in the accounts to be

prepared/ published within the next year, so the impact has not yet been publicised

4) Some small private providers are prepared to treat their own time costs for proprietor

supervision and central management as not fully recoverable, and can therefore continue in

15

business despite suffering losses, if accounts and costings for pricing purposes had been

drawn up on a fully costed basis

5) The mix of examples within the sample may not be typical, or costings may be

disproportionately affected by allocation of overheads; in particular, a provider may, in

practice, have a high proportion of supported living clients with high needs, where even low

hourly rates might pay off, if there are plenty of hours of support to provide a high

contribution to overheads

6) The effects of inflation on costs have been minimised by holding down salaries for the last

few years (but are these salary rates sustainable?- increases may need to be conceded soon

or staff retention will become a major problem)

7) Deficits may be offset/ subsidised by surpluses elsewhere in the business, (say) in other

areas of social care or healthcare.

The answers to this question may be to some extent a matter of conjecture, in the absence of more

detailed investigation, but a few additional comments may be helpful.

1. Whilst anecdotally, some providers think they are under more fee pressure in Surrey than

elsewhere, they are typically under fee pressure throughout the country, so it is unlikely that

margins are still high enough with other local authorities to materially subsidise shortfalls in Surrey.

From discussions with providers, it is also clear that quite a number are currently involved or have

recently been involved in some major restructuring and other cost saving initiatives. In particular,

several large ‘not for profit’ providers are currently experiencing overall deficits, so the combination

of the high inherited cost levels (where staff have been taken on through TUPE arrangements), as

well as inadequate fee levels in some cases, coupled with voids in particular in residential care,

means that this is certainly not an isolated problem. In fact, the feedback from major local and

national ‘not for profit’ providers in particular, that they are currently, and have in the recent past

been experiencing overall deficits, is evidence contradicting the perception that serious financial

difficulties for providers are not fully apparent.

2. The examples in the sample do not seem to include situations where mortgages have been paid

off and costs are still being recognised, thereby overstating the potential cash-flow implications, if

not the true full costs of care. In the wider local learning disabilities support provision market, there

are known to be many situations where fees have been reduced as a result of reduced property

costs, so presumably there will also be situations where this has not been the case and the cash-flow

implications of deficits on a profit and loss basis are not quite so severe as calculated deficits might

suggest. However, other additional cash-flow demands and the requirement for additional working

capital also need to be taken into account (see comments under ‘overall fee considerations’, below).

3. Anecdotal comments from providers support the contention that results for the current year will

show reduced profitability.

4. Several small private providers selected for the sample were unable to complete the survey due to

lack of time and costing resources, so only one example is actually included in the results. So, it is not

the case that survey results include material elements of full proprietor costs which providers are

prepared to operate without fully recouping in fees. For these small providers as a whole, across

Surrey, full costs are likely to be understated in current fees, thus understating net deficits or

16

shortfalls in meeting mark-ups required (although some of these proprietors may still be able to

continue in business without recouping them in full).

5. Although we are not fully aware of the mix of individuals supported by different providers, we

understand that many of the lower needs clients in supported living are supported by the larger ‘not

for profit ‘ providers. It therefore seems unlikely that the overall financial situation and cover for

fixed overheads will be substantially more favourable, at least for these organisations than the

indicative results within our sample.

6. Sustainable levels of cost are very likely to be higher than most of the costs included within the

results of this survey, both for salary and other costs (with the exception of high salary cost, TUPE

constrained staffing); one provider quoted a committed 3% increase in rents this year, which will

simply further reduce margins by a material amount, in the absence of fee increases.

7. There are unlikely to be many providers who can draw on large surpluses from other areas of

social care business, given the similar fee pressures across the board, unless the bulk of other clients

comprise self-funders, who pay far more than local authorities in fees.

OVERALL FEE CONSIDERATIONS

‘Not for profit’ providers tend to be facing greater problems as a result of high inherited staffing

costs, and consequent difficulties in maintaining price competitiveness for new business.

Positive margins in residential care have often in the past had to be used to supplement supported

living housing deficits, especially by private providers. However, with the continuing move to use

supported living for nearly all new placements resulting in increasing numbers of residential care

voids, coupled with fee restraints, this is increasingly no longer possible. Private providers are also

typically finding it much more difficult than ‘not for profits’ to deregister and restructure residential

care to convert this to supported living, because of inadequate housing allowances and more

stringent bank financing conditions which continue to need to be satisfied.

The cost of any recent restructuring, as well as the recent extra financing costs of having to receive

fees later than previously (as local authority payments in advance are eliminated), are not likely to

be fully covered in individual costings. Equally, the financing costs of establishing and only filling any

new provision over an extended period will not be allowed for. These factors increase overall costs

either directly (for restructuring), or indirectly, via the need for extra working capital financing and

additional interest costs. Once the cost becomes on-going it should be included in central overheads,

but any new costs are unlikely to be budgeted in advance and therefore covered and allocated.

DIFFERENT COSTS FOR DIFFERENT PURPOSES

This costing survey and the costing models used are based on the accounting principle that the full

costs of any organisation, including central overheads in particular, need to be recovered, plus a

margin or surplus on top, if the service and business is going to be viable. So the true costs of care

need to recognise the total actual costs, and this is what needs to be focussed on, amongst other fee

related issues commented on above, in looking at on-going provider financial viability.

However, the related questions regarding how fees are calculated in practice, how overheads are

allocated in pricing, what levels of cost are justified in diverse particular situations, and how prices

17

for services are agreed, involve a range of additional considerations and may require modified

approaches. This is not so straightforward in practice, but merits some clarification here, especially

in view of the different approaches adopted by providers in response to the survey, when allocating

overhead costs.

For one thing, start-up businesses, and small established businesses may not have the economies of

scale to expect to fully recover all their overheads, if these need to be high initially relative to the

scale of the business, whereas the allocated cost of largely fixed central overheads to individuals

supported in a very large business may be low, and therefore fully recoverable in fees.

Fixed and variable costs and the basis of overhead allocation

This also begs the question as to what extent these central costs are actually fixed, and which central

costs will vary, and to what extent, as further individuals need to be supported. For example, any

accounting and payroll work would be expected to increase as more individuals are taken on, as well

as more staff to support them, also increasing the human resources department workload.

Providers and local authorities both really need to understand fixed and variable costs, and the

impact of changes in key variables on unit costs, especially in relation to supported living fees. By

using a standard hourly fee rate, the local authority is enabling the variable direct salary costs to be

calculated and covered in the hourly rate, but has to make an assumption about the allowance in the

rate for fixed costs which do not vary with the level of support provided. This can therefore result in

over or under recovery of a fair proportion of the fixed overheads, in costings relating to individual

individuals.

For an individual with lower needs and low hours of support, the amount of fixed overheads

recovered in the hourly rate available for just a few hours will be very small, whereas for high needs

individuals, a proportion of fixed overheads will be recovered for every hour of support, potentially

leading to over-recovery of fixed overheads. This is assuming that all individuals ought to share these

equally, where these costs tend to increase with extra numbers of individuals, if at all, rather than in

any way being influenced by the different levels of support which individuals need. So high needs

individuals tend to end up subsidising lower needs individuals, in terms of the fees received, based

on standard hourly rates, and lower needs clients can be unprofitable to support.

However, this is only one perspective and does not deal with the whole picture. An established

provider can still afford to take on some new low needs and low fee individuals, if the fee obtained is

sufficient to cover all the variable costs and still make a positive financial contribution to what are

the truly fixed elements of the central costs. But, if most of the individuals supported are already

lower need, then there may still simply be insufficient overall contribution to cover all the fixed costs

and the provider could end up in an overall deficit situation.

So the mix of individuals is important and, if hourly rates are set at low tight levels, it will only

probably be possible for providers to take on a lot of lower needs clients if they also have a

reasonable number of high needs clients providing a much greater financial contribution. The

implications of this standard hourly rate pricing policy can therefore be significant in the market-

place.

18

For the local authority seeking to place quite a number of individuals with lower hours support

requirements , they need to find providers who can utilise economies of scale in relation to central

costs and who also probably have sufficient numbers of high hour needs individuals, so as to still be

receiving enough income overall.

For a new provider entering the market, with(say) a good supported living housing scheme, but no

other existing business across which to absorb relatively fixed costs (until they are able to expand

and spread the overheads around better), low standard hourly rates can be prohibitive. For one

such new scheme advised relatively recently, the proposition from the local authority was that they

were attracted by the service offered and would recommend a compatible mix of some higher needs

and some lower needs individual placements.

However, based on the overall budget and individual costings we prepared, the conclusion and

advice was that the low standard hourly fee rate available would preclude taking on any but

moderately high to high needs clients, if fixed costs were to be fully covered, and the enterprise was

to be financially viable. The practical downside was that to have too many higher needs individuals

together often just does not work, in compatibility and behaviour management terms. As a result,

the prediction has in part come to pass, in that the hourly rate agreed is simply too low to achieve

sufficient profitability with the mix of high and lower needs clients supported.

This demonstrates the complexity and risks associated with using standard, low, hourly fee rates

across the board, without wider consideration of the mix of support needs and the underlying cost

structures, as well as the flexibility to modify rates where necessary and still address the business

proposition cost-effectively. There are no easy answers to this, in an environment where budgets are

so heavily constrained, but there is a need to understand the issues, in formulating future fee

policies and in optimum use of budgets.

These points are made simply to illustrate that determining appropriate levels of fees to pay for the

true costs of care is likely to be more complicated than simply looking at individual costings. There is

a multiplicity of issues around sustainability, financial risks (such as in relation to voids), and the

overall business mix and financial context of providers need to be considered (as already discussed

in the previous section on ‘overall fee considerations’).

Overhead allocation and pricing

Returning to the basis of overhead allocation used by providers, it is useful in conclusion to

comment on this in relation to this survey and the wider pricing issues. Just over half of the

supported living providers in the survey have allocated at least some overheads based on relative

individual hours or relative income, rather than simply individual numbers. In effect this means that

costs are aligned with fees based on the extent to which fees are able to fully pay for a proportion of

the costs, given the problem of using fixed hourly fee rates highlighted above.

If this approach is used by providers in pricing their services for individuals with low hours support

needs, this is similar or equivalent to treating these overheads as fixed, and not needing to be added

in in full, in agreeing fees for new lower hours needs individuals. For high hours needs individuals,

even a relatively low add-on within the hourly rate for central overheads may be sufficient,

particularly if the bulk of these overheads are relatively fixed. So this can represent a practical and

19

pragmatic way of pricing for providers, provided that they also understand the variability of costs

and can manage profitability effectively overall.

For the local authority, it is important to recognise how provider costs vary and to obtain

information from the providers to aid their understanding. There is then the trade off to consider,

as between the simplicity of continuing to wish to use a single range of hourly fee rates, (recognising

that some provision will be underpaid for and some possibly overpaid for), versus the benefits of

being able to tailor these rates better to different real differences in cost levels, in support of making

the most cost-effective commissioning decisions, and possibly being able to support providers more

flexibly and better.

Inflation

Finally, it is also important to stress that this discussion about fixed and variable costs only really

deals with the variability of costs and ‘cost drivers’ i.e. the factors which influence the level of any

activity, and the resultant cost levels. All costs are, in addition, subject to variability year on year,

based on inflationary pressures, so no costs are really fixed in the medium term, from this

perspective.

Inflation affects different cost components in different ways, so both providers and the local

authorities really need to monitor inflation by cost component, bearing in mind the varying

proportion of total costs which each component represents, given different cost structures and

mixes of business between providers. Changes to cost levels need then to be reflected in

modifications to fee rates and levels year on year, to support on-going provider financial viability.

CONCLUSIONS

Establishing reliable data for the current costs of care for the provision of social care support

services for young adults in Surrey has not been a straightforward exercise and one which could ever

have expected to come up with a single set of simple figures.

However, we believe that the costing models developed and deployed have proved to be fit for

purpose, supported by a thorough review process, to ensure as far as possible that not only have

templates been filled in correctly, but that the cost data submitted is as reliable as practicable.

No guarantees can be made about the accuracy of provider figures, or that some figures might not

be overstated, as there must still be some margin of error, but the additional comparative review

process, including asking providers to justify and correct figures which looked out of line, coupled

with the confidentiality of data has, we think, enabled the provision of some very useful cost data

and insights in relation to cost levels and behaviour, as well as how current costs compare with

actual fees. In addition, where figures still looked too unusual, they have been set on one side.

This is not a precise science and a number of assumptions have had to be made in calculating costs,

but there is at least now a stronger basis and set of tools to show what it costs to provide support in

different situations, rather than simply rely on costing data which may not tie back to actual support

levels, staff rotas or the accounting records. Perhaps this can be the start of greater cost

20

transparency and trust on both sides, so that providers feel more willing to ‘open their books’ and

prove the validity of their costs and required fee estimates for the future.

The actual/ current cost figures produced indicate what the costs are, but not what they need to be

in some areas to be sustainable for the future, or on the other hand what they could be reduced to,

to be really efficient, economic and cost-effective. There is a surprisingly wide diversity in some

elements of the costs as between providers, which makes it more difficult to say what cost ‘norms’

might be developed for the future.

There should still be scope for improving cost-effectiveness and for providers to make further

efficiency savings, rather than simply taking the cost figures provided within this survey as a ‘given’.

The wide disparity in relative cost levels between individual costings and providers across the

sample, set out in the cost analysis which follows, can provide an important starting point, which is

considered, on an initial basis, in the cost analysis which follows.

It is also interesting to note that the resulting surpluses or deficits produced seem quite sensitive to

relatively small adjustments in the individual costs or allocation methods, particularly where these

relate to the key/ material areas of staff costs, central overheads and to a lesser extent the return on

property.

Nevertheless, the results indicate that there is a problem, with many providers in the sample not

receiving an adequate margin on the support they are providing, whilst for others the fees are in

excess of what is required. On balance, in our judgement, the evidence suggests that more fees are

likely to be insufficient than are excessive, and that this situation is likely to deteriorate further, with

inflation and other increasing cost pressures, unless the specific issues can be addressed, with

ramifications for provider on-going financial viability and supply of sufficient good quality services in

the market.

From the local authority’s perspective, there is a need to apply scarce financial budgets in the

optimum way possible, ideally, to provide additional funding where it is most justified, rather than a

‘blanket’ approach, adjusting individual fees in the wrong direction, in relation to surpluses and

deficits.

SUGGESTIONS FOR THE WAY FORWARD

Broader validation of results

A key question is :

1) Whether the evidence in relation to negative (and positive) mark-ups produced in the

examples is really typical of the homes/ services covered, in relation to other individuals

and of the organisations as a whole?

Providers in the survey have already been asked this question informally and the majority have

indicated that results submitted are generally typical (so some have negative mark-ups for many

individuals, but equally some also still have a range of positive mark-ups for individuals). This has

21

already been discussed at some length under ‘the impact of inadequate mark-ups and deficits’,

above.

However, it will be important to substantiate these assertions not only with providers already

covered within the sample, but also to obtain additional insights, from other providers not covered.

Sustainable costs and financial viability

Some comments on the lack of sustainability of salary rates have already been included under the

section above on salaries and staff costs.

The key issues and questions in relation to salary rates have already been raised but require further

consideration:

2) Will these be sufficient at current, or even only marginally increased levels to retain good

quality staff, and to recruit new staff, so as to maintain the provision of high quality

services?

3) In this regard, what might happen to employment locally in Surrey, in terms of the

increase or otherwise in job opportunities in the near future, in potentially increasing

competition for prospective care workers?

4) What is happening to inflation currently and what will be likely to happen in the next year

or so?

The salary sustainability risk will affect providers across the board, but those whose margins are

currently healthier (less restricted or less negative overall) are going to be better placed to respond

in terms of making any increases possible to retain and recruit staff. Arguably many or most (?)

providers will struggle to increase salary levels, in the absence of fee increases to fund these, given

that they have found it difficult to do so in the recent past, and the financial environment has

deteriorated recently, for providers and local authorities alike.

Current and future inflation will also affect other costs, although for most providers salary costs still

represent the bulk of the cost base (between 55 and 80% of overall costs).

There is also the question of the impact of voids, which could be having an even greater impact on

overall financial viability currently than reduced margins. The models already developed, as well as

other (Laing and Buisson) models developed which consider the financial viability of homes and

services overall, and the impact of voids, can be utilised to explore the financial impact of risks. The

specific overall suggestion is therefore:

A. Extend some aspects of the work to date, to validate initial findings at individual level, and to

consider the extent of financial deficits and related financial risks at overall home/service levels

and across businesses, bearing in mind sustainability, voids etc.

The models and data on key cost ratios could be used to estimate the combined effect of changes

required for inflation and to address sustainability issues, and to consider the budget implications,

across the whole learning disability population in Surrey.

22

Establishing ‘normal’ cost allowances and fee levels

Given the above:

5) Should and how can an approach now be developed to take the disparate results obtained

forward to establish new ‘norms’ for cost levels, which can then be used to calibrate how

overall costs need to increase with increasing levels of individual need, in terms of hours

of support?

Broad suggestions have already been made above about how to take forward the work to better

assess the different unit costs associated with providing support in houses of different sizes, as well

as using the cost models developed to calibrate the levels of costs for individuals with different

hours of support.

However, we would counsel against an approach which tries to over-standardise the costs of

support, in terms of ‘norms’, given the very wide range of different support and housing

arrangements possible in the learning disabilities marketplace. This could be counter-productive, in

moving the focus away from working closely with providers in choosing the most cost-effective

solutions offered to meet specific requirements, to ‘one-size fits all’ thinking. Ranges of costs or

hourly rates may be more appropriate, with guidelines as to the factors to be considered, in terms of

where individual fees should fit within the range.

Bearing this in mind, the suggestion is that more specific work might be undertaken as follows:

B. Identify different staff support unit costs per hour for different levels and types of need, as well

as types of support. This could combine consideration of sustainable local salary rates by grade

with study of the mix of staffing, including supervision needed and related costs, to better

calibrate both supported living hourly rate ranges and residential support fees for different levels

of need.

C. Better calibrate differences in unit costs for different housing settings (affecting staffing and

support, as well as housing costs, so at least in part relevant for supported living as well as

residential care); this would be used in conjunction with B to provide guidance re broad

adjustment factors which might be applied.

(It should be recognised that the housing cost part is quite complicated, as a basis for calculating

return on property. This work might therefore be done in conjunction with IESE, who are responsible

for the care funding calculator nationally, to re-visit, revalidate and refine where necessary the ratios

they currently use for adjusting general house prices for different sizes of housing).

This work could then logically be extended to improve the tools used to review provider costs and

agree appropriate fees, both for supported living and residential care.

D. Revise the basis for setting hourly fee rates in supported living, to incorporate results of B and C

re different levels of staff unit cost (on a costs per hour basis), but then use weekly allowances for

all other variable and fixed costs. This would overcome the problems of allocation for lower and

high needs illustrated by the survey and enable SCC to debate with providers/decide what levels of

central overhead allocated cost represent 'efficient/economic' cost levels, bearing in mind

23

economies of scale, and to what extent fixed costs should be included in prices agreed (as well as

whether exceptions should be made for start-up and smaller specialist, high quality operators).

E. Similarly, residential care fees could be established in future based on reviewing costs relating to

each component of overall costs, as these vary in practice i.e. average direct staff costs set per

hour, and all other variable and fixed costs, including return on property, based on costs per week.

This more consistent approach would also have the advantage that supported living and residential

care costings would be compatible and it would be easier to compare relative costs, as well as paving

the way for further deregistration of residential care, where this might be suitable to convert to

supported living.

A further logical extension to this revised approach would be to extend the scope of fee setting to

embrace a full cost and benefits review for each individual, including consideration of housing costs

and all benefits and allowances, whether individuals be in residential care or supported living. This

more holistic approach would have the advantages of enabling overall housing and support

propositions to be formulated which could be tested for financial viability and cost-effectiveness at

the outset, including ensuring that every individual had sufficient benefits and allowances to support

the arrangements proposed, and that individuals contributed an appropriate amount to the overall

costs of their support packages. The specific suggestion is therefore:

E. Consider the benefits (and costs) of moving to an holistic ‘total costs and benefits’ approach to

commissioning, building on suggestions in C and D above.

Budget considerations

These questions also prompt the further key question:

6) Given very limited financial resources for next year, how does Surrey CC, within its social

care budgets, best respond to these shortfalls and surpluses, as well as overall provider

financial risks, and risks to future supply?

For example, will the optimum approach be to try to provide equal extra support to providers,

across the board, or somehow to prioritise support, in relation to relative financial risks and/or

strategic market supply risks?

7) Depending on the answer to this, what should be the focus for further cost analysis, if

further work is needed, and with what relative priority?

Improving cost-effectiveness of support and housing

Given that none of the above is likely to anywhere near fully address the scale of the problem:

8) How can the local authority and providers work more effectively together to identify

genuine ways to improve cost-effectiveness of services?

The fact that provider unit costs vary so much across our sample ought to yield at least some new

opportunities to jointly explore additional cost savings potential.

24

Cost benchmarks for providers can be further developed to aid this task, so:

9) What else needs to be done now, to promote effective use of the benchmarking approach

and data already assembled and analysed?

Cost benchmarking can be fraught with difficulties of consistency of analysis and comparability.

Other sources of reliable comparative data should be considered, as well as how the results of the

current exercise might best be built on.

Re-assessing the support needs of individuals

Surrey CC has embarked on a major exercise to reassess the support needs of individuals. However,

this is time and experience intensive and there is a shortage of suitable expertise and resources.

10) How can the models developed and approach to costing applied be harnessed to expedite

this exercise and best integrate work on re-assessing hours of support required with more

cost-effective support options?

The models developed for the survey, coupled with adoption of the suggestions above, could form

the basis for the costing elements of re-assessing the support needs of individuals more effectively,

as well as supporting benchmarking and cost-effectiveness improvement initiatives and revised fee

setting.

The missing ingredient is the tool or tools to be used to re-assess individual needs and help

formulate improved, personalised approaches to supporting them more cost-effectively. Whilst the

needs matrix within the care funding calculator and resource allocation system points-based

assessment may still have some role to play, both of these are somewhat ‘continuing dependency’

oriented, rather than facilitating ways to increase independence and reduce support needs over

time, or to use and realistically cost a more flexible mix of support resources, in line with personal

choice, harnessing community support and other novel approaches to improve the cost-

effectiveness of support utilised.

We are familiar with new tools, specially designed for learning disabilities support, which might be

used to enhance this re-assessment and which might pave the way for a more dynamic approach to

improving personal outcomes and reducing support budgets over time, coupled with better

calculating the cost of mixed resourcing approaches, to feed in to fee and personal budget setting.

These might be supplemented by our own spreadsheet models. The suggestion therefore is to:

F. Review the overall approach being adopted to re-assessment of individual needs, to consider

whether enhancements might be made to the tools used and approach.

A prioritised plan of action

There is probably a need to consider the efficacy, inter-relationships, timescales and priorities of

these various potential initiatives to come up with a logical and prioritised plan of action. Future

costing work required should also be considered in the context of the limitations of analysis so far,

the funding constraints, relative financial and market risks and cost improvement potential. The

thinking can now be further developed.

25

SURREY LEARNING DISABILITIES COSTING SURVEY

COST ANALYSIS REPORT

DETAILED RESULTS

All submissions have been tabled in a range of cost analyses, which have been used to calculate and

compare key unit costs and ratios, as a basis for addressing each specific objective.

OVERALL COSTS AND THE ADEQUACY OF FEES

Objective 1: Analyse overall costs by individual, to consider both the adequacy of current fees and

to provide a basis for calculating sustainable overall cost and fee levels for the future

Given the number and mix of submissions received back from providers, and the effective operation

of the tailored costing models developed, it has been possible to fully analyse submissions received,

to calculate current costs and identify mark-ups being achieved in relation to actual fee levels.

This is at an individual level and highlights the extent of any over or under funding, assuming that

levels of need are already correctly assessed i.e. no consideration has been given to whether the

hours of support commissioned and other support arrangements are sufficient or greater than

necessary, as this was outside the scope of the survey. Useful insights have also been gained in

relation to sustainable costs, although more work is needed to consider sustainable fee levels for the

future.

For residential care, mark-up percentages on total current operational costs reflected by existing

fees range from -35.5% to +18.5%, with an average of -8.1%, across the sample of 20 analysed. The

median mark-up is -6.9%. Of 7 with positive mark-ups, only 2 have mark-ups in excess of 15%, while

the remaining 5 show mark-ups of less than 10%. Whereas, of the 13 with deficits, only 4 show

deficits of under 6%, while the remaining 9 all show deficits of over 13%. There are wide differences

between actual current mark-ups, in relation to individuals, arising for many different reasons,

including changes in support needs not reflected in increased or reduced fees, inflation not matched

by equal fee increases etc.

Whether the individual is in a ‘high salary cost’ placement or otherwise seems to have no clear,

discernible bearing on surpluses or deficits arising. 6 out of 20 examples relate to situations where

‘high salary costs’ continue to need to be paid under TUPE arrangements, for individuals transferred

from hospitals and other public sector provision. Fees have generally been increased to address

these higher cost commitments, but some are now showing surpluses while others are in deficit. In