swaps finance (derivative securities) 312 tuesday, 5 september 2006 readings: chapter 7

TRANSCRIPT

SwapsSwapsFinance (Derivative Securities) 312

Tuesday, 5 September 2006

Readings: Chapter 7

Nature of SwapsNature of Swaps

Agreement to exchange cash flows at specified future times according to certain rules

Example of a plain vanilla swap• agreement by Microsoft to receive 6-month

LIBOR & pay a fixed rate of 5% per annum every six months for three years on a notional principal of $100 million

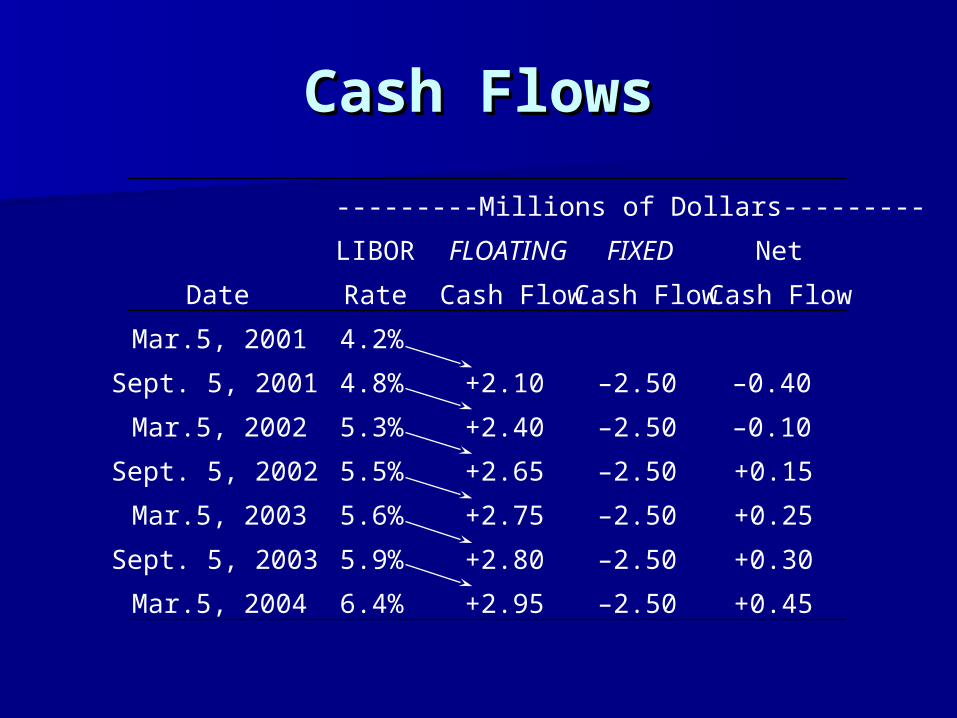

Cash FlowsCash Flows

---------Millions of Dollars---------

LIBOR FLOATING FIXED Net

Date Rate Cash Flow Cash Flow Cash Flow

Mar.5, 2001 4.2%

Sept. 5, 2001 4.8% +2.10 –2.50 –0.40

Mar.5, 2002 5.3% +2.40 –2.50 –0.10

Sept. 5, 2002 5.5% +2.65 –2.50 +0.15

Mar.5, 2003 5.6% +2.75 –2.50 +0.25

Sept. 5, 2003 5.9% +2.80 –2.50 +0.30

Mar.5, 2004 6.4% +2.95 –2.50 +0.45

Use of SwapsUse of Swaps

Converting a liability from• fixed rate to floating rate • floating rate to fixed rate

Converting an investment from • fixed rate to floating rate• floating rate to fixed rate

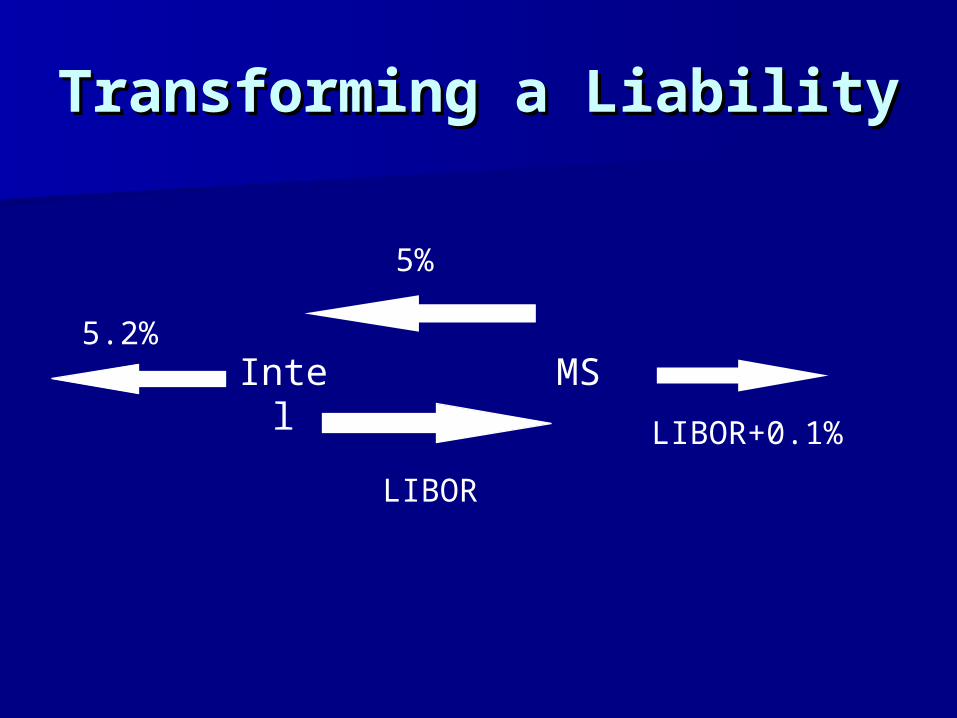

Transforming a LiabilityTransforming a Liability

Intel MS

LIBOR

5%

LIBOR+0.1%

5.2%

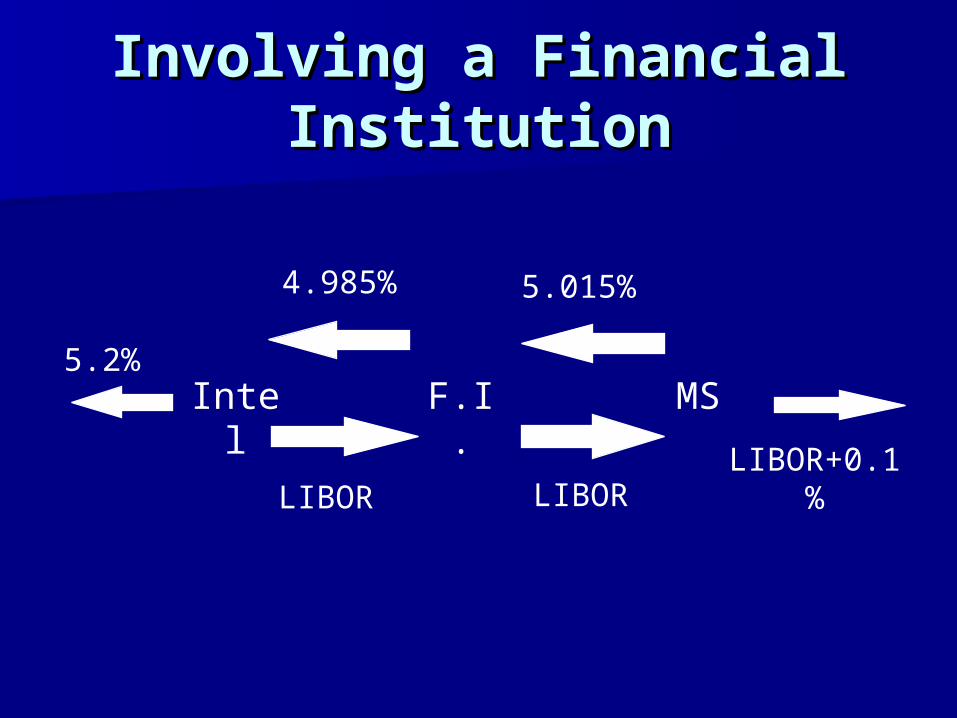

Involving a Financial Involving a Financial InstitutionInstitution

F.I.

LIBOR LIBORLIBOR+0.1%

4.985% 5.015%

5.2%Intel MS

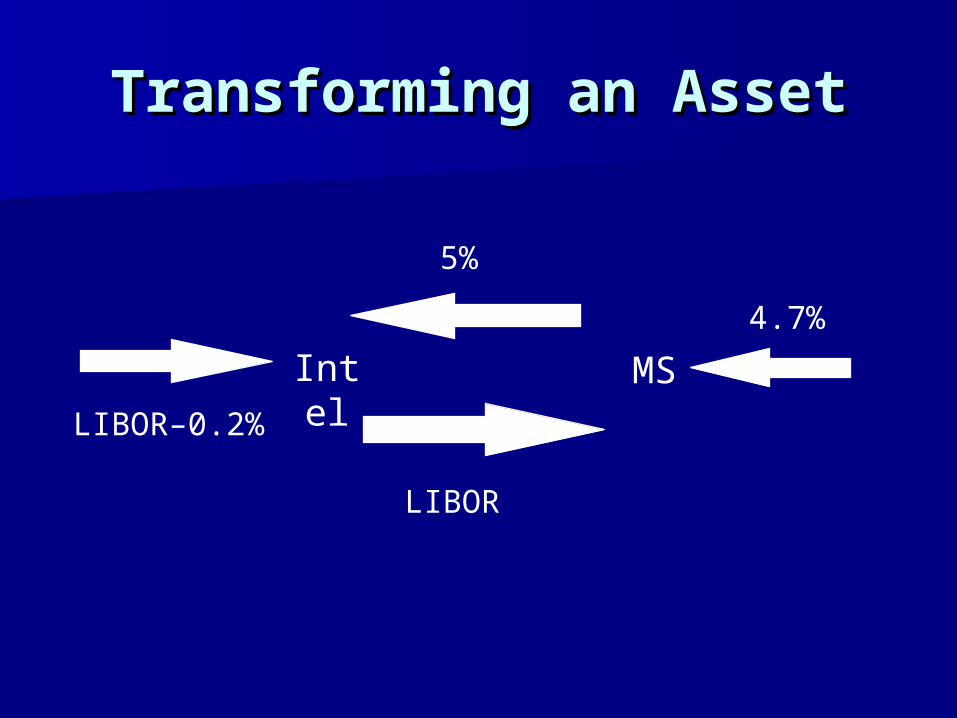

Transforming an AssetTransforming an Asset

Intel MS

LIBOR

5%

LIBOR–0.2%

4.7%

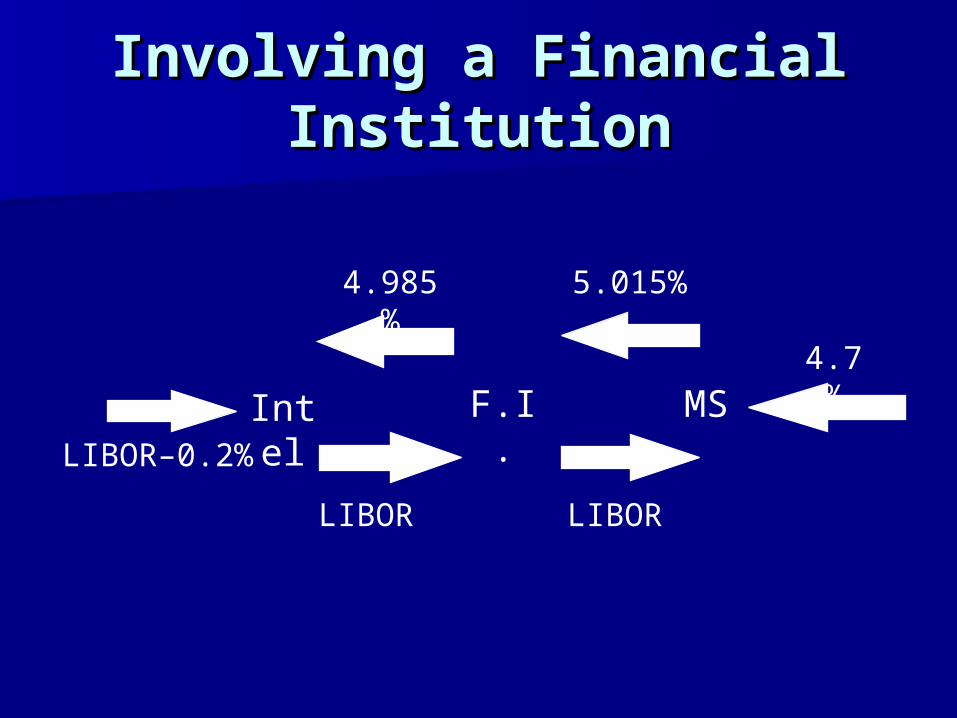

Involving a Financial Involving a Financial InstitutionInstitution

Intel F.I. MS

LIBOR LIBOR

4.7%

5.015%4.985%

LIBOR–0.2%

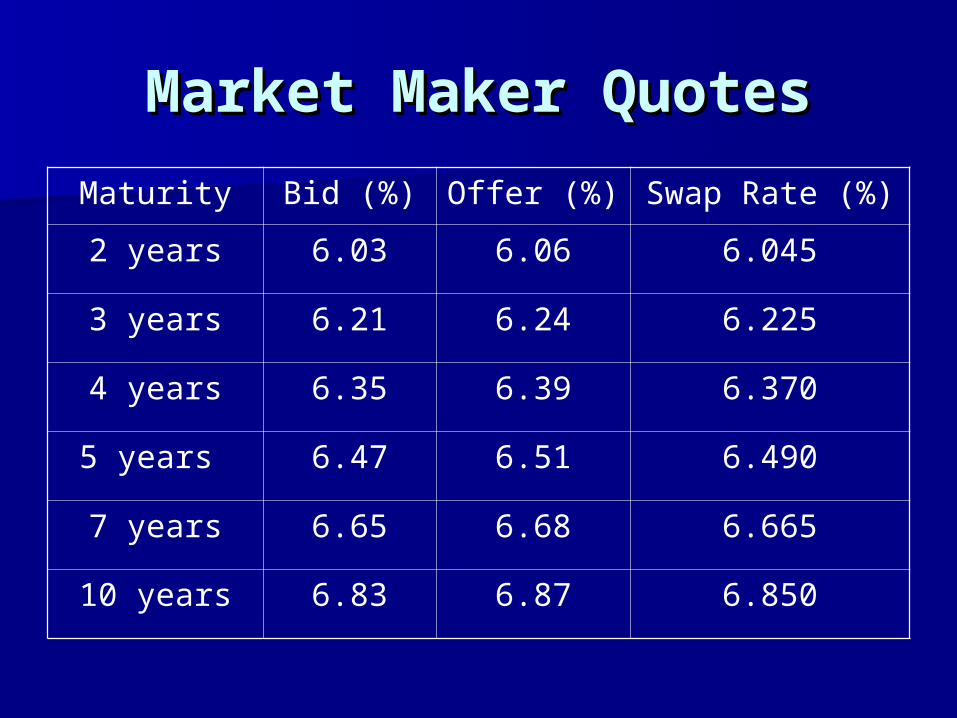

Market Maker QuotesMarket Maker Quotes

Maturity Bid (%) Offer (%) Swap Rate (%)

2 years 6.03 6.06 6.045

3 years 6.21 6.24 6.225

4 years 6.35 6.39 6.370

5 years 6.47 6.51 6.490

7 years 6.65 6.68 6.665

10 years 6.83 6.87 6.850

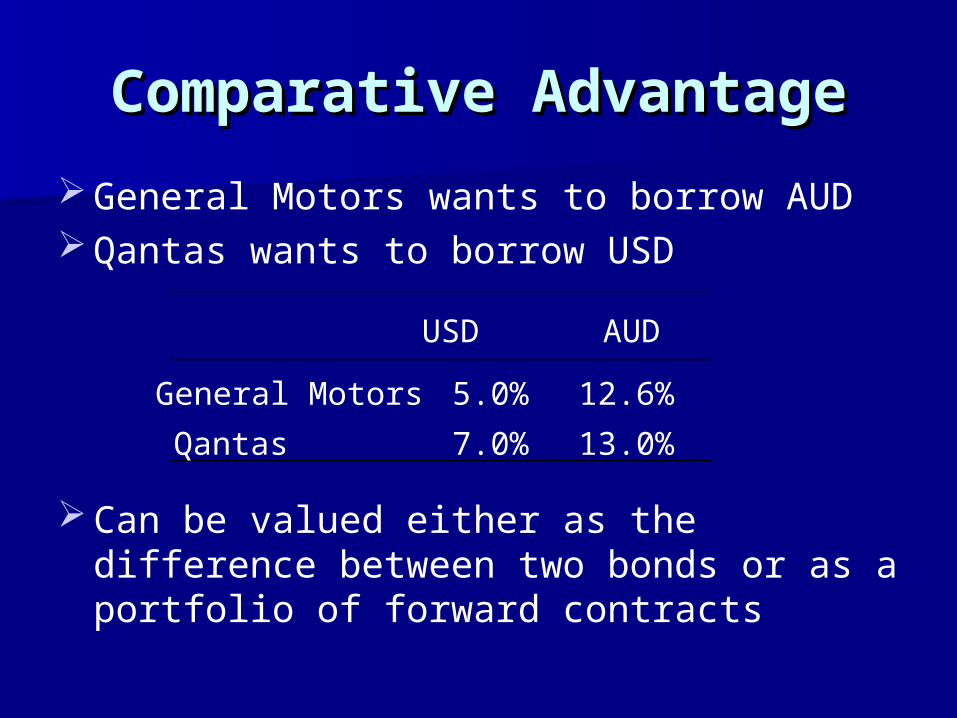

Comparative AdvantageComparative Advantage

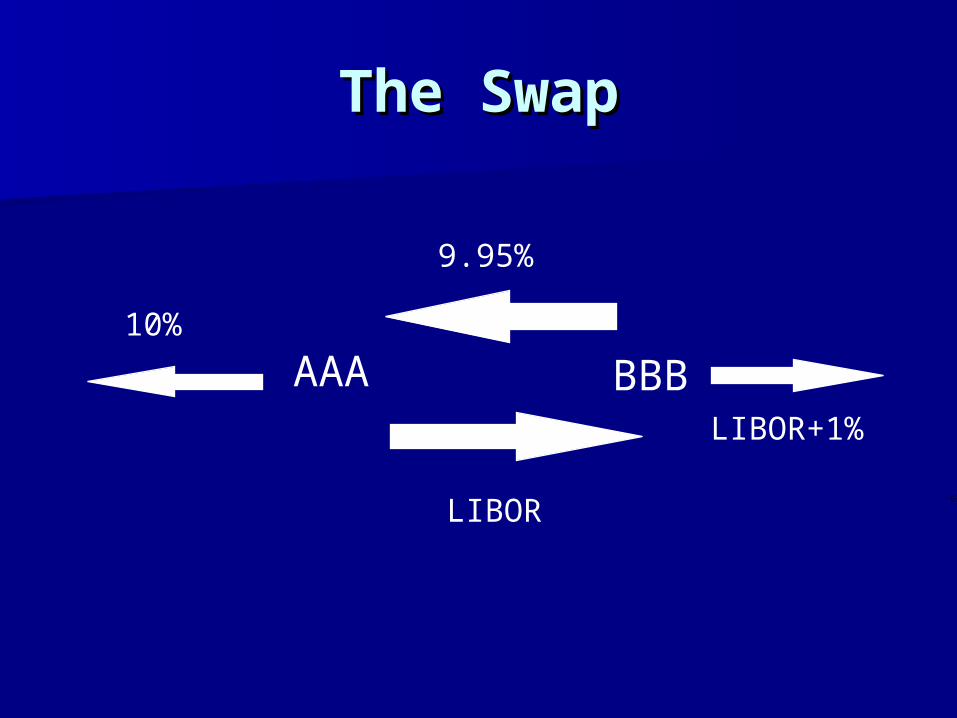

AAACorp wants to borrow floatingBBBCorp wants to borrow fixed

Fixed Floating

AAACorp 10.00% 6-month LIBOR + 0.30%

BBBCorp 11.20% 6-month LIBOR + 1.00%

The SwapThe Swap

P

A

AAA BBB

LIBOR

LIBOR+1%

9.95%

10%

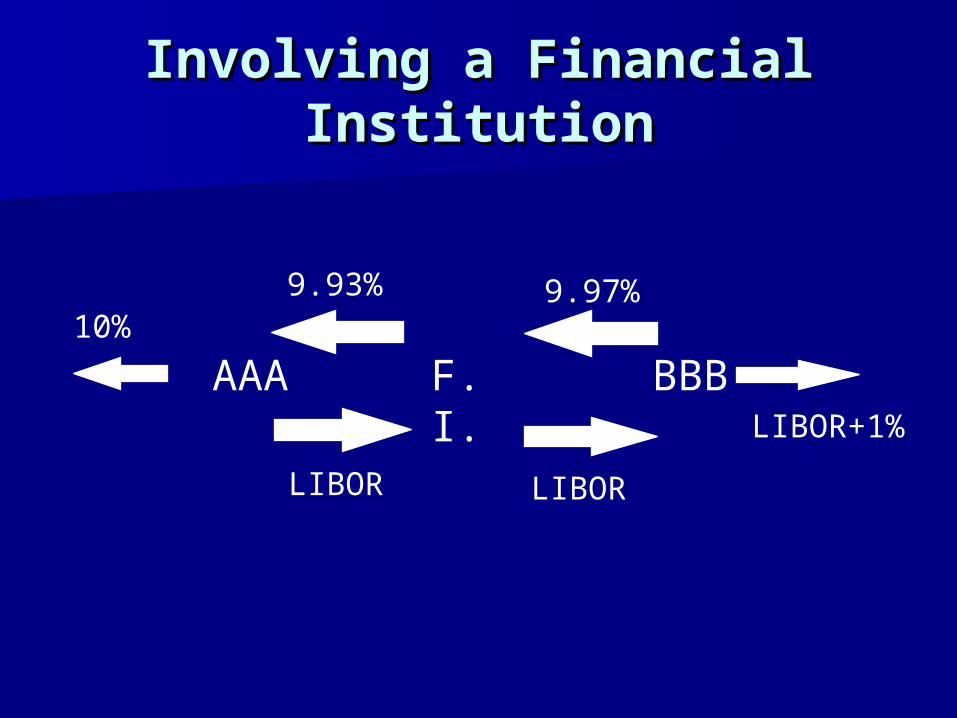

Involving a Financial Involving a Financial InstitutionInstitution

AAA F.I. BBB10%

LIBOR LIBOR

LIBOR+1%

9.93% 9.97%

CritiqueCritique

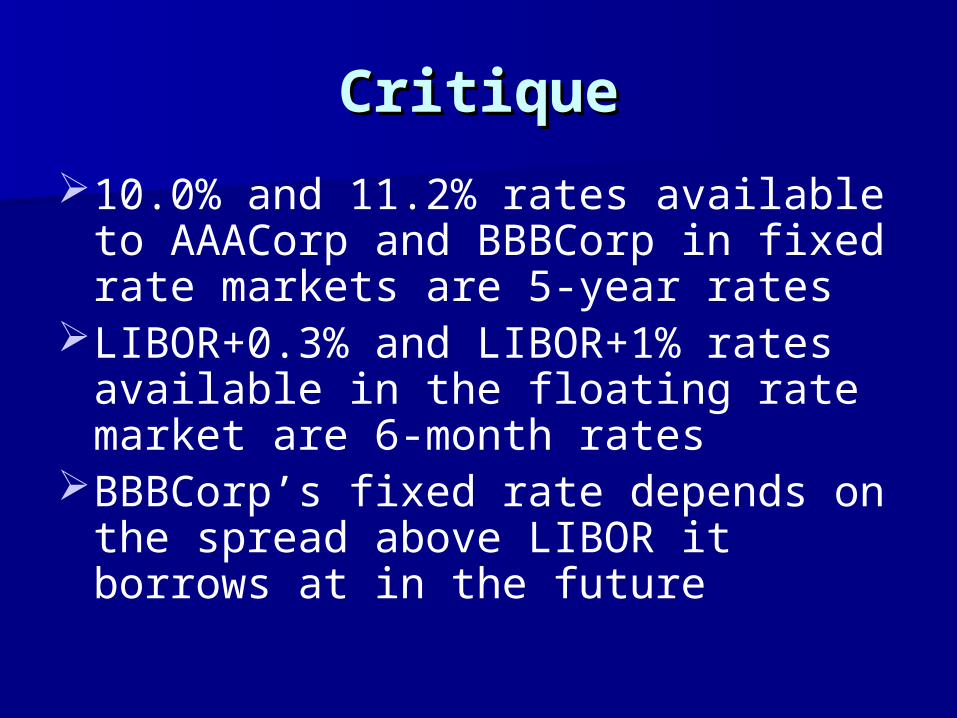

10.0% and 11.2% rates available to AAACorp and BBBCorp in fixed rate markets are 5-year rates

LIBOR+0.3% and LIBOR+1% rates available in the floating rate market are 6-month rates

BBBCorp’s fixed rate depends on the spread above LIBOR it borrows at in the future

Swap RatesSwap Rates

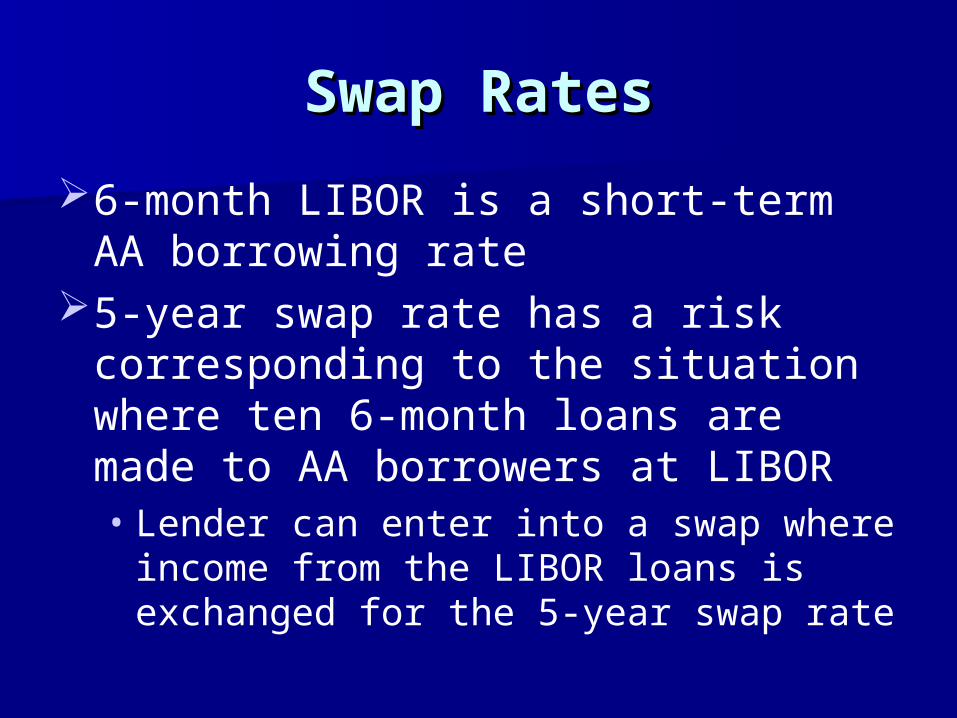

6-month LIBOR is a short-term AA borrowing rate

5-year swap rate has a risk corresponding to the situation where ten 6-month loans are made to AA borrowers at LIBOR• Lender can enter into a swap where income

from the LIBOR loans is exchanged for the 5-year swap rate

Valuation of SwapsValuation of Swaps

Valued as the difference between the value of a fixed-rate bond and the value of a floating-rate bond• Fixed rate bond is valued in the usual way• Floating rate bond is valued by noting that it is

worth par immediately after the next payment date

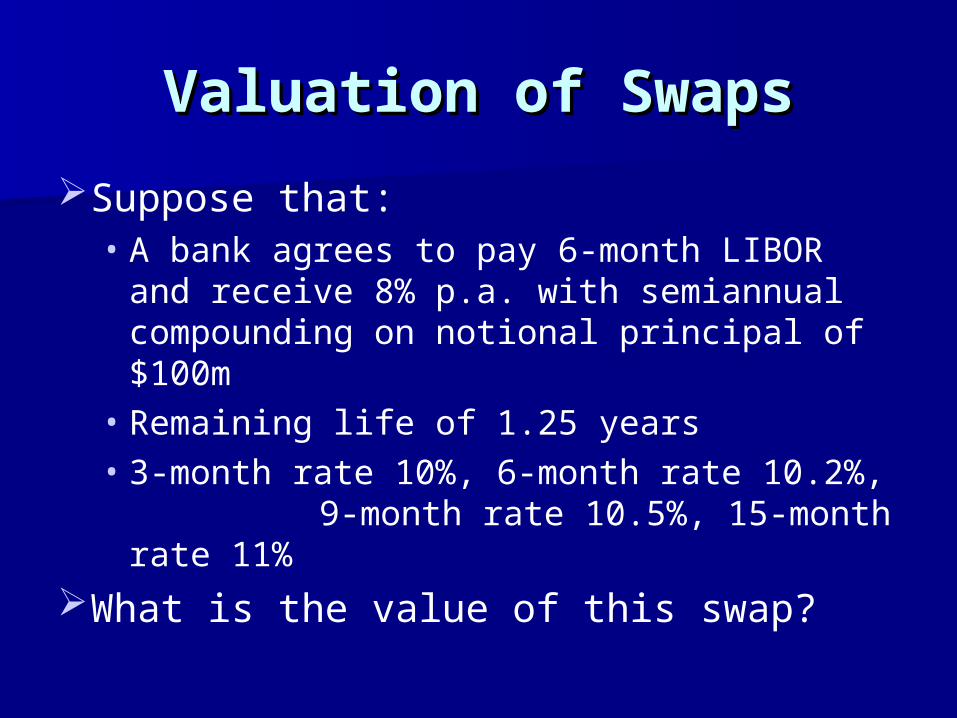

Valuation of SwapsValuation of Swaps

Suppose that:• A bank agrees to pay 6-month LIBOR and

receive 8% p.a. with semiannual compounding on notional principal of $100m

• Remaining life of 1.25 years• 3-month rate 10%, 6-month rate 10.2%, 9-

month rate 10.5%, 15-month rate 11%

What is the value of this swap?

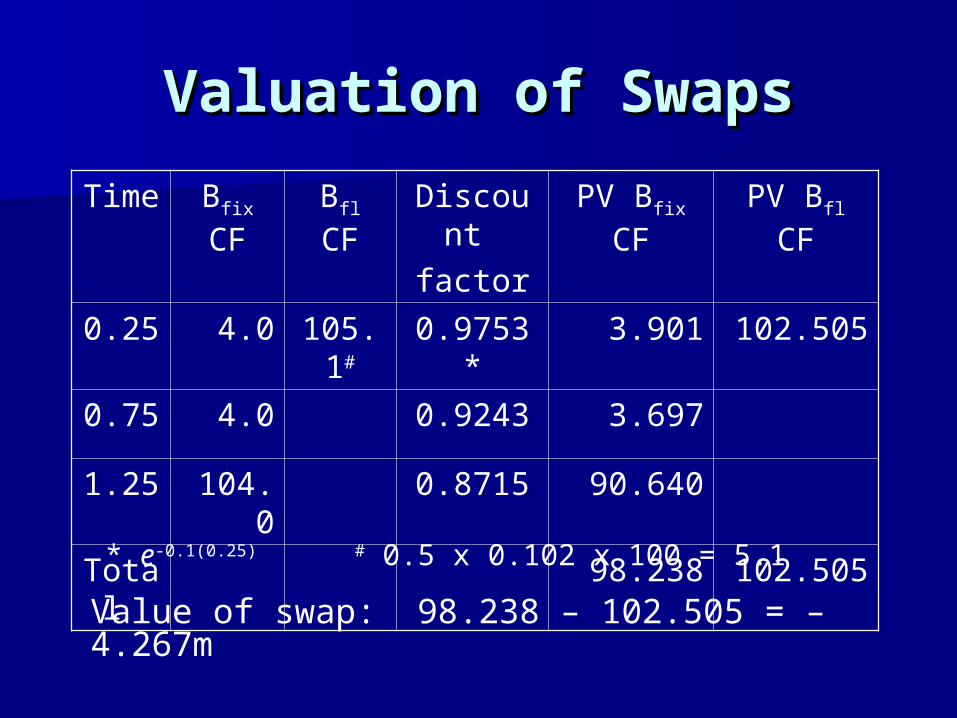

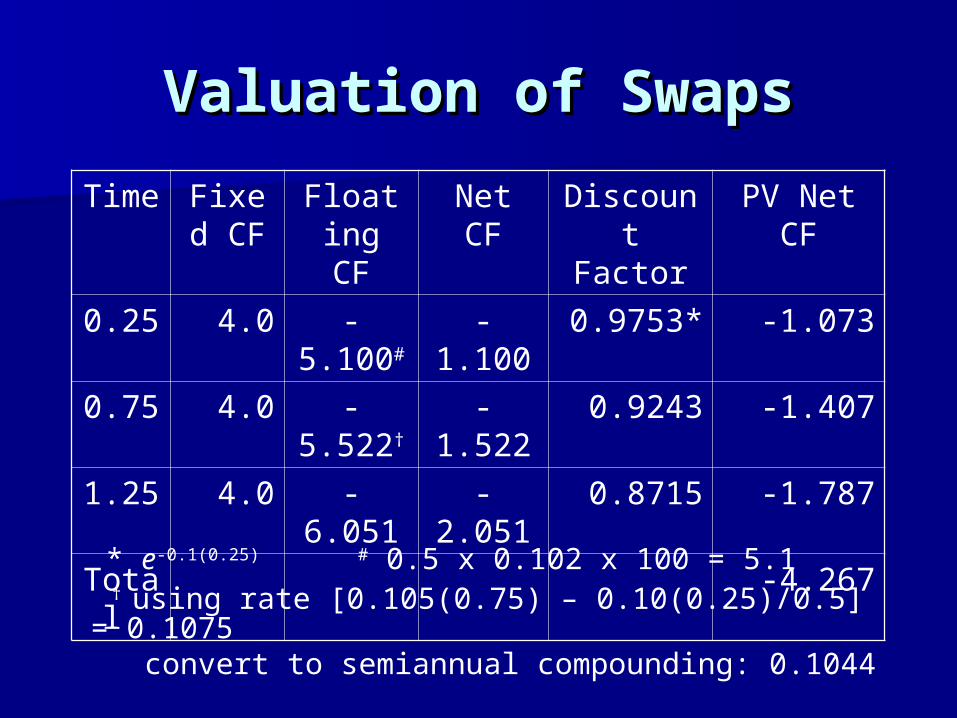

Valuation of SwapsValuation of Swaps

* e-0.1(0.25) # 0.5 x 0.102 x 100 = 5.1

Value of swap: 98.238 – 102.505 = –4.267m

Time Bfix CF Bfl CF Discount

factor

PV Bfix CF PV Bfl CF

0.25 4.0 105.1# 0.9753* 3.901 102.505

0.75 4.0 0.9243 3.697

1.25 104.0 0.8715 90.640

Total 98.238 102.505

Valuation of SwapsValuation of Swaps

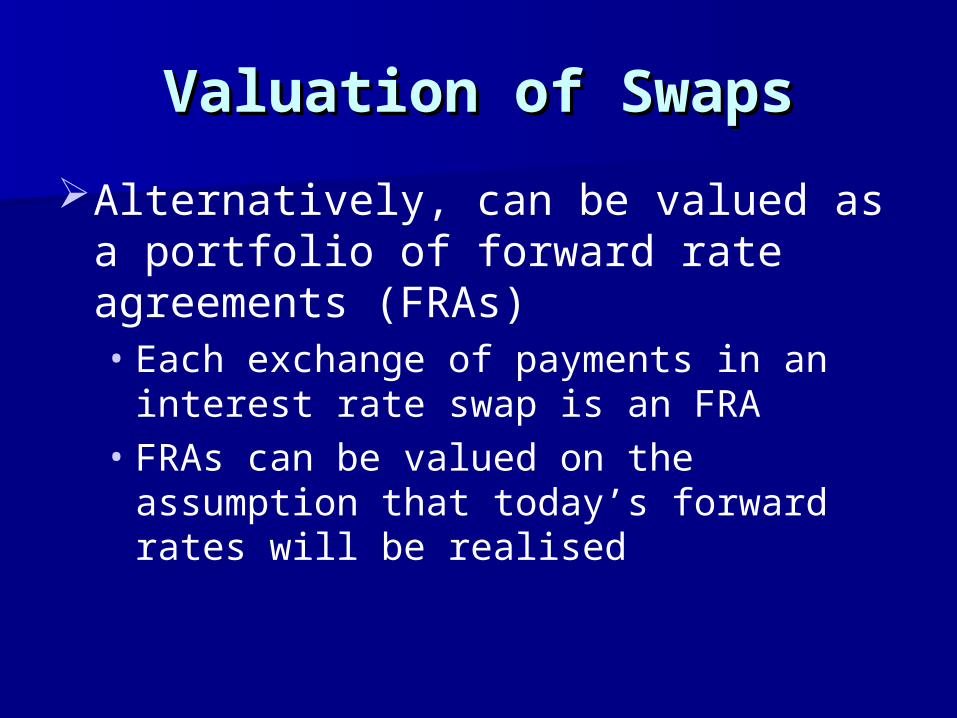

Alternatively, can be valued as a portfolio of forward rate agreements (FRAs)• Each exchange of payments in an interest

rate swap is an FRA• FRAs can be valued on the assumption that

today’s forward rates will be realised

Valuation of SwapsValuation of Swaps

* e-0.1(0.25) # 0.5 x 0.102 x 100 = 5.1 † using rate [0.105(0.75) – 0.10(0.25)/0.5] = 0.1075 convert to semiannual compounding: 0.1044

Time Fixed CF

Floating CF

Net CF Discount Factor

PV Net CF

0.25 4.0 -5.100# -1.100 0.9753* -1.073

0.75 4.0 -5.522† -1.522 0.9243 -1.407

1.25 4.0 -6.051 -2.051 0.8715 -1.787

Total -4.267

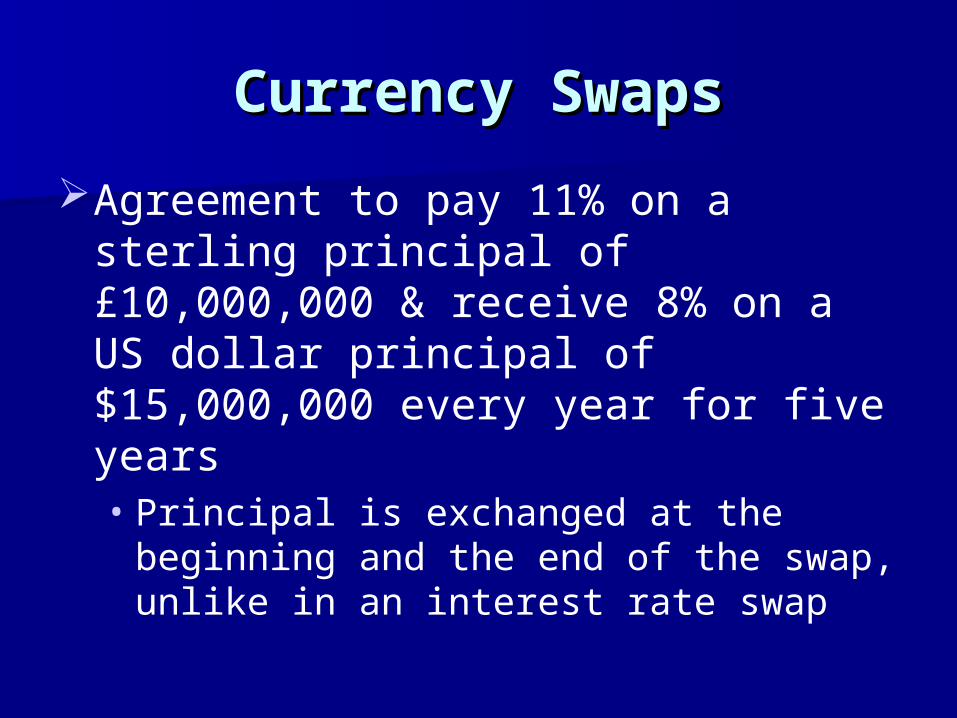

Currency SwapsCurrency Swaps

Agreement to pay 11% on a sterling principal of £10,000,000 & receive 8% on a US dollar principal of $15,000,000 every year for five years• Principal is exchanged at the beginning and

the end of the swap, unlike in an interest rate swap

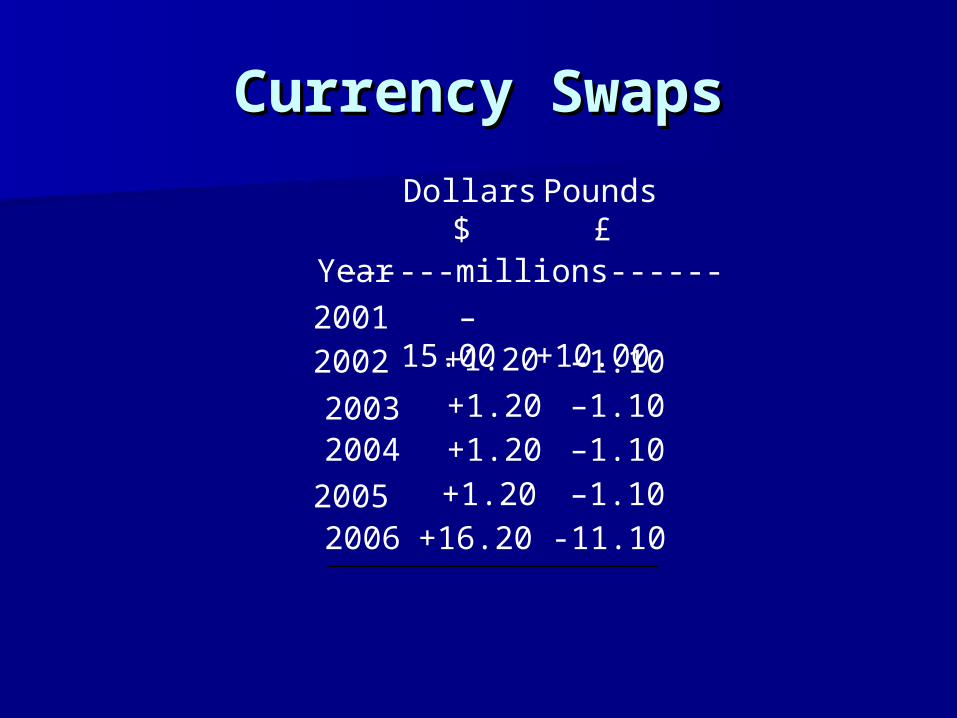

Currency SwapsCurrency Swaps

Year

Dollars Pounds$

------millions------

2001 –15.00 +10.002002 +1.20 –1.10

2003 +1.20 –1.10 2004 +1.20 –1.10

2005 +1.20 –1.10 2006 +16.20 -11.10

£

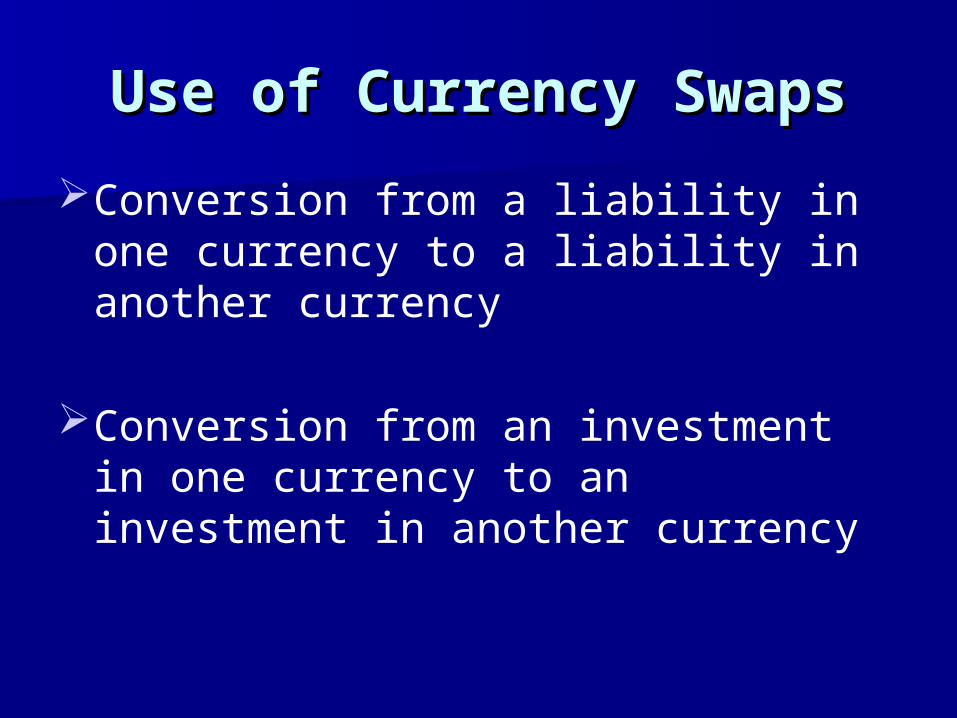

Use of Currency SwapsUse of Currency Swaps

Conversion from a liability in one currency to a liability in another currency

Conversion from an investment in one currency to an investment in another currency

Comparative AdvantageComparative Advantage

General Motors wants to borrow AUD Qantas wants to borrow USD

Can be valued either as the difference between two bonds or as a portfolio of forward contracts

USD AUD

General Motors 5.0% 12.6%

Qantas 7.0% 13.0%

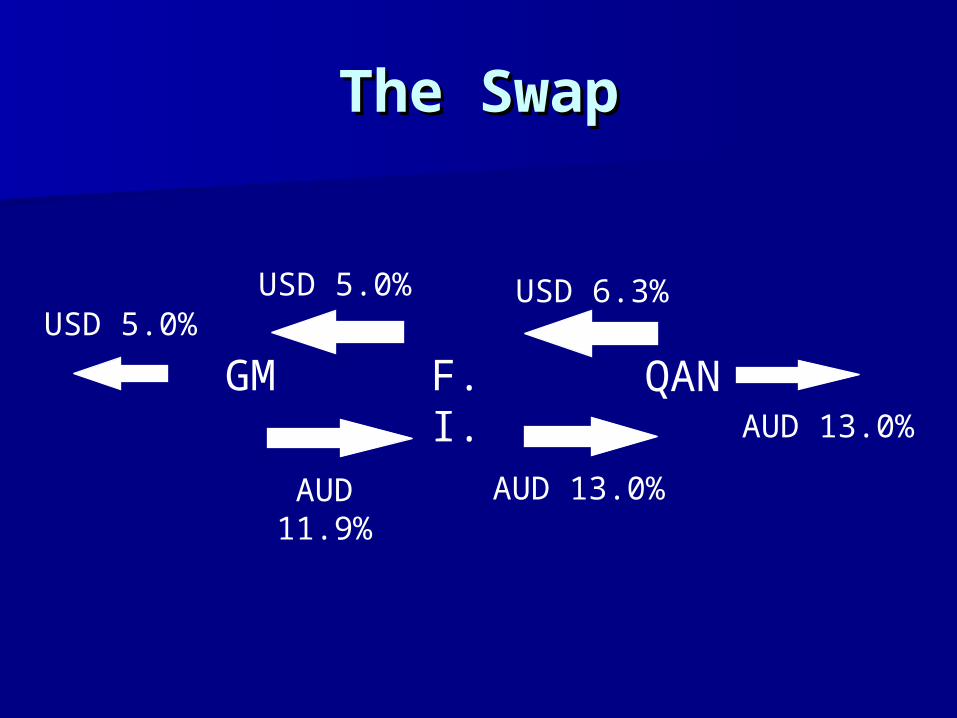

The SwapThe Swap

GM F.I. QANUSD 5.0%

AUD 11.9% AUD 13.0%

AUD 13.0%

USD 5.0% USD 6.3%

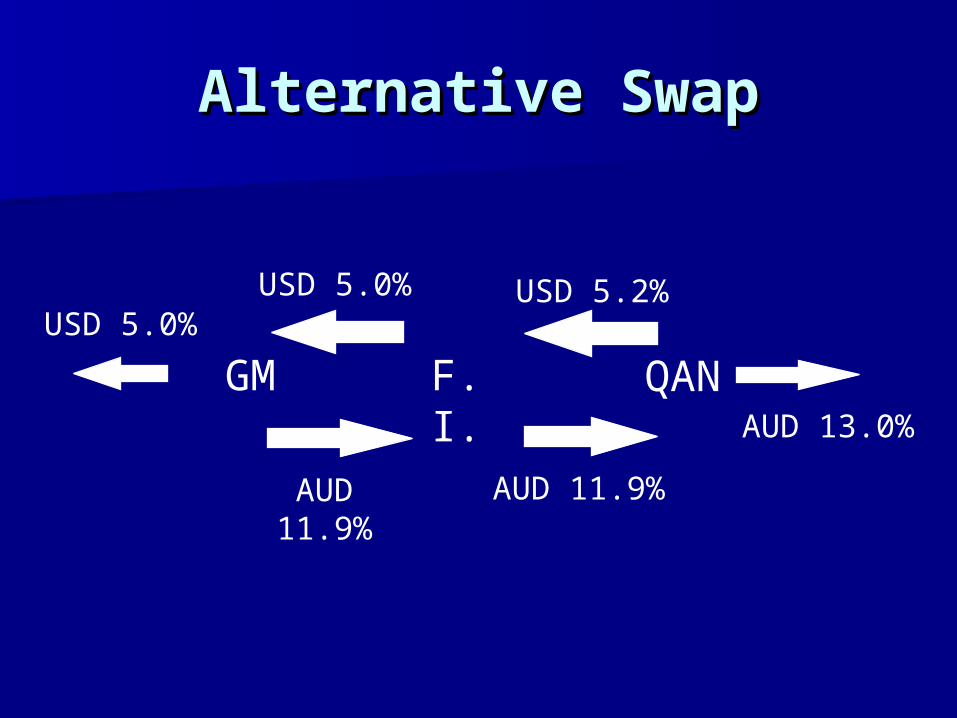

Alternative SwapAlternative Swap

GM F.I. QANUSD 5.0%

AUD 11.9% AUD 11.9%

AUD 13.0%

USD 5.0% USD 5.2%

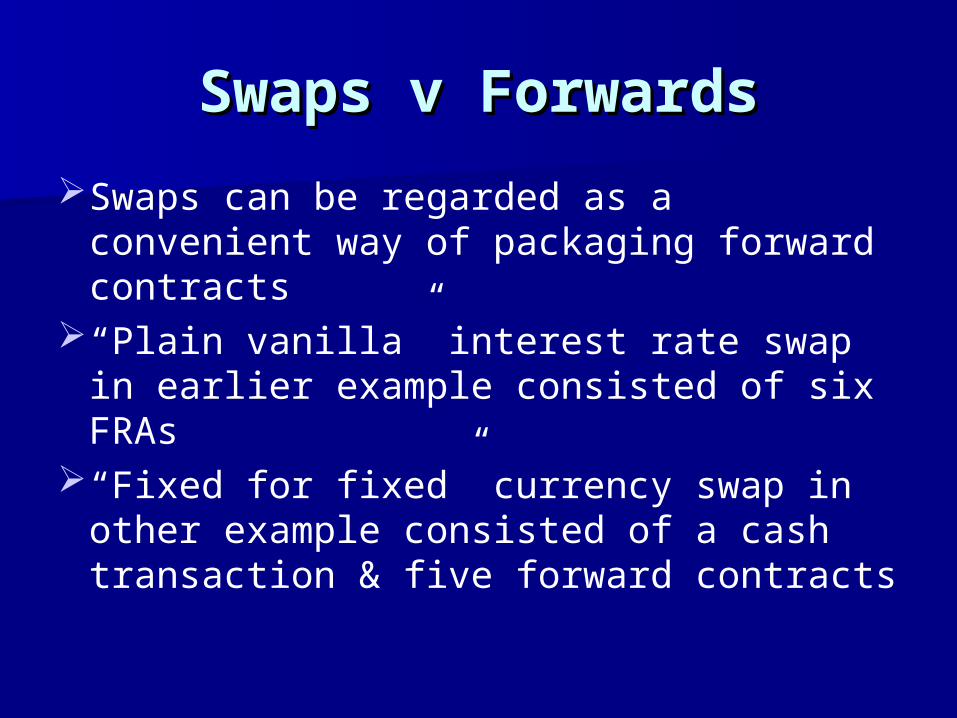

Swaps v ForwardsSwaps v Forwards

Swaps can be regarded as a convenient way of packaging forward contracts

“Plain vanilla” interest rate swap in earlier example consisted of six FRAs

“Fixed for fixed” currency swap in other example consisted of a cash transaction & five forward contracts

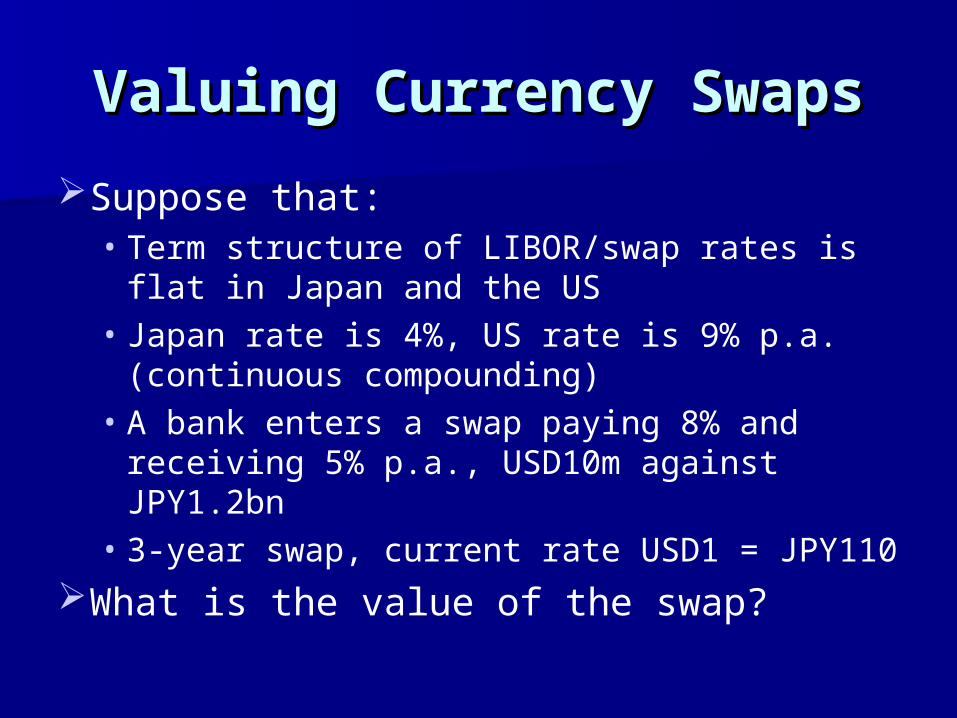

Valuing Currency SwapsValuing Currency Swaps

Suppose that:• Term structure of LIBOR/swap rates is flat in

Japan and the US• Japan rate is 4%, US rate is 9% p.a.

(continuous compounding)• A bank enters a swap paying 8% and

receiving 5% p.a., USD10m against JPY1.2bn• 3-year swap, current rate USD1 = JPY110

What is the value of the swap?

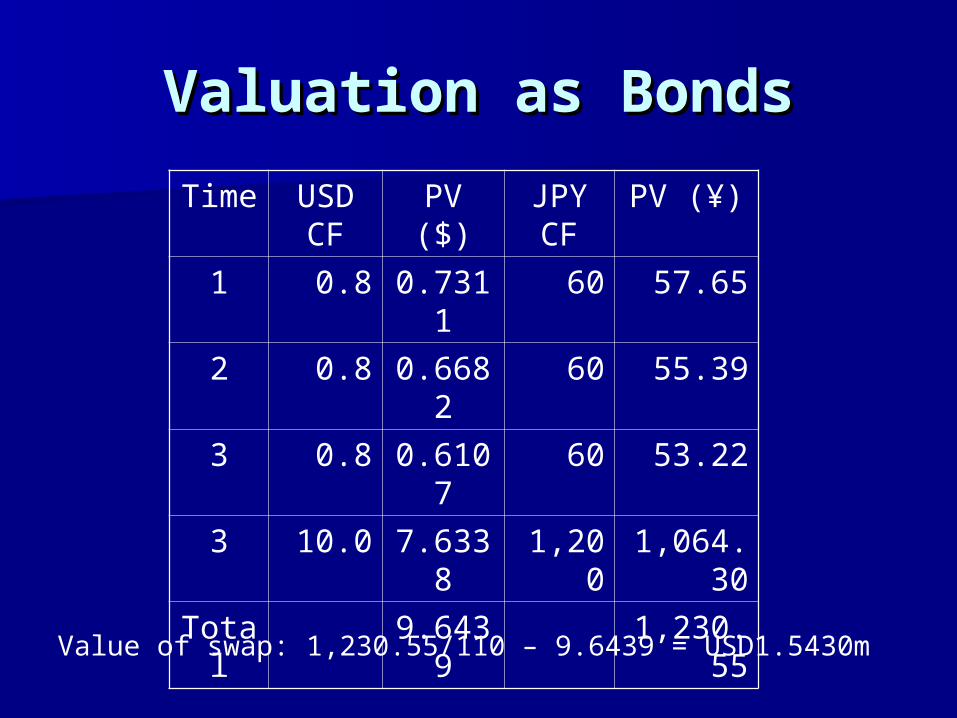

Valuation as BondsValuation as Bonds

Value of swap: 1,230.55/110 – 9.6439 = USD1.5430m

Time USD CF

PV ($) JPY CF

PV (¥)

1 0.8 0.7311 60 57.65

2 0.8 0.6682 60 55.39

3 0.8 0.6107 60 53.22

3 10.0 7.6338 1,200 1,064.30

Total 9.6439 1,230.55

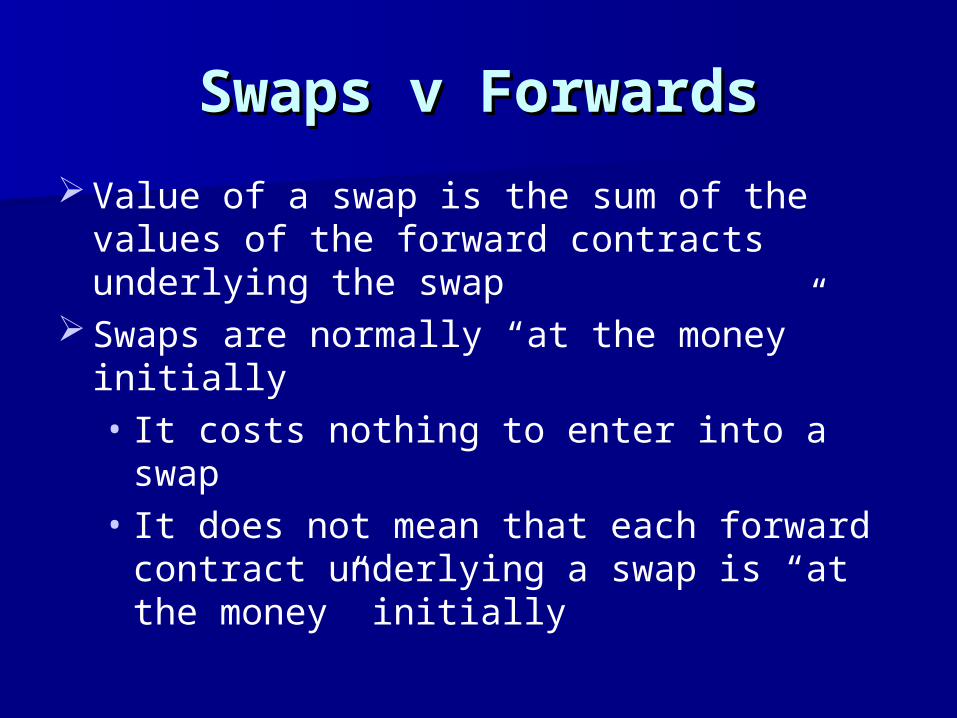

Swaps v ForwardsSwaps v Forwards

Value of a swap is the sum of the values of the forward contracts underlying the swap

Swaps are normally “at the money” initially• It costs nothing to enter into a swap• It does not mean that each forward contract

underlying a swap is “at the money” initially

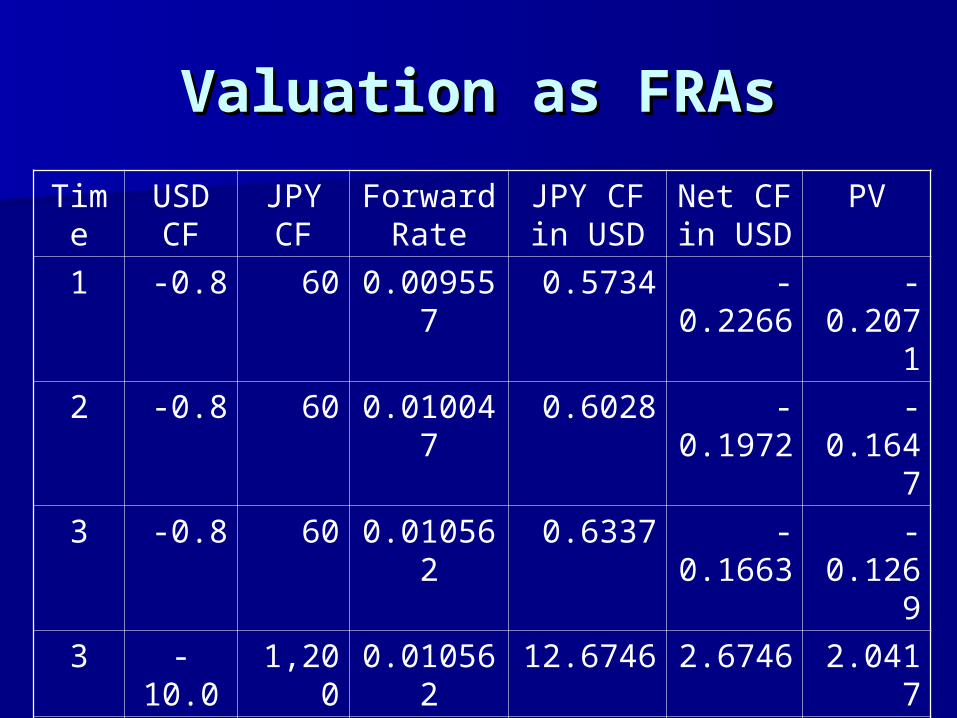

Valuation as FRAsValuation as FRAs

Time USD CF

JPY CF

Forward Rate

JPY CF in USD

Net CF in USD

PV

1 -0.8 60 0.009557 0.5734 -0.2266 -0.2071

2 -0.8 60 0.010047 0.6028 -0.1972 -0.1647

3 -0.8 60 0.010562 0.6337 -0.1663 -0.1269

3 -10.0 1,200 0.010562 12.6746 2.6746 2.0417

Total 1.5430

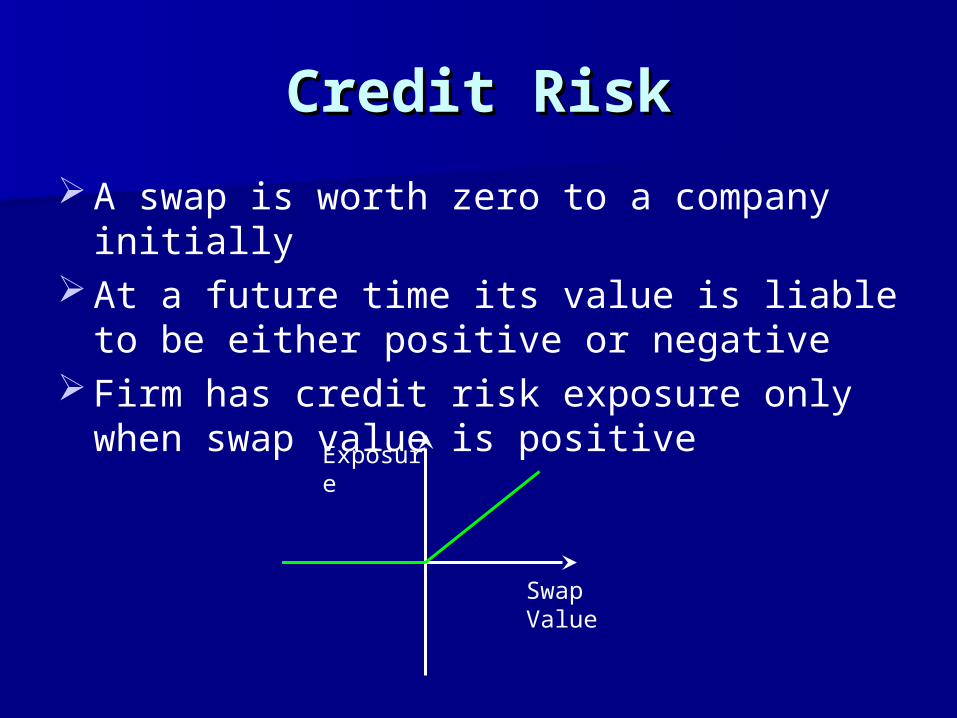

Credit RiskCredit Risk

A swap is worth zero to a company initially At a future time its value is liable to be either

positive or negative Firm has credit risk exposure only when swap

value is positive

Exposure

Swap Value