table of contents section f estate, gift & inheritance

TRANSCRIPT

TABLE OF CONTENTS SECTION F

ESTATE, GIFT & INHERITANCE TAXES Alyssa R. Stewart

Anderson, Roberts, Porth, Wallace & Stewart LLP Burlington, IA

Page Estate & Gift Rates/Etc. (2019-2021 Inflation Adjusted) ...................................................... 1 Estate/Gift Tax Rate Schedule ............................................................................................... 1 Special Use Valuation – Interest Rates .................................................................................. 2 Iowa Inheritance Tax. ............................................................................................................ 3-6 Iowa Inheritance Tax Rate Schedule ................................................................ 7 Iowa Administrative Code 701-89.11 Valuation .............................................. 8-14 Iowa Inheritance Tax 2001 CSO Mortality Tables ........................................... 15 Table for Life Estates & Remainders (Iowa) ............................................... 16 Male/Female Life Expectancy (Annuity for Life) ....................................... 17 Iowa Inheritance Tax Application for Extension of Time to File ..................... 18-19 Iowa Inheritance Tax Application for Release of Inheritance Tax Lien .......... 20 Iowa Inheritance Tax Deferral .......................................................................... 21 Iowa Inheritance Tax Election/Application for Deferral of Inheritance Tax ... 22 Portability. .............................................................................................................................. 23-31 Form 706 – Part 6 and Instructions ................................................................... 26-29 Portability Election – Following Death of Spouse ........................................... 30 Declination to File Form 706 ............................................................................ 31 Death of a Farmer – Step Up in Basis.................................................................................... 32 Post-Death Sale of Livestock, Unharvested Crops and Land... ............................................. 33-41 Form 8971 Basis Reporting …………………………………………………………………. 42-50 Form 8971/Instructions .................................................................................................46-50 Recent Developments: Anti Claw-Back Regulations ............................................................................ 51 Proposed 67 (g) Regulations ............................................................................. 51 Small Estate Chapter 635 Change ..................................................................... 54

1

ESTATE AND GIFT TAX RETURN PREPARATION

Unified Transfer Tax System

INFLATION ADJUSTED AMOUNTS 2019 2020 2021 Special Use Valuation –

maximum deduction in value $1,160,000 $1,180,000 $1,190,000**

Annual Gift Tax Exclusion $ 15,000 $ 15,000 $ 15,000* Applicable Exclusion Amount for Estates, Generation- skipping transfers and gifts

$11,400,000 $11,580,000 $11,700,000*

Amount eligible for 2% interest rate under IRC §6166

$1,550,000 $1,570,000 $1,590,000*

* Estimated based on inflation & COLA, Revenue Ruling not yet released

ESTATE/GIFT TAX RATE SCHEDULE 2020

Bracket Tax Is This Amount Plus This Percentage Of the Amount Over

$0 to $2,600 $0 plus 10% $0

$2,600 to $9,450 $260 plus 24% $2,600

$9,450 to $12,950 $1,904 plus 35% $9,450

Above $12,950 $3,129 plus 37% $12,950

2021

(ESTIMATED)

If Taxable Income is Between: Then Tax Due Is:

$0 - $2,650 10% of taxable income $2,651 - $9,550 $265 + 24% of the amount over $2,650 $9,551 - $13,050 $1,921 + 35% of the amount over $9,550

$13,051 $3,146 – 37% of the amount over $13,050

2

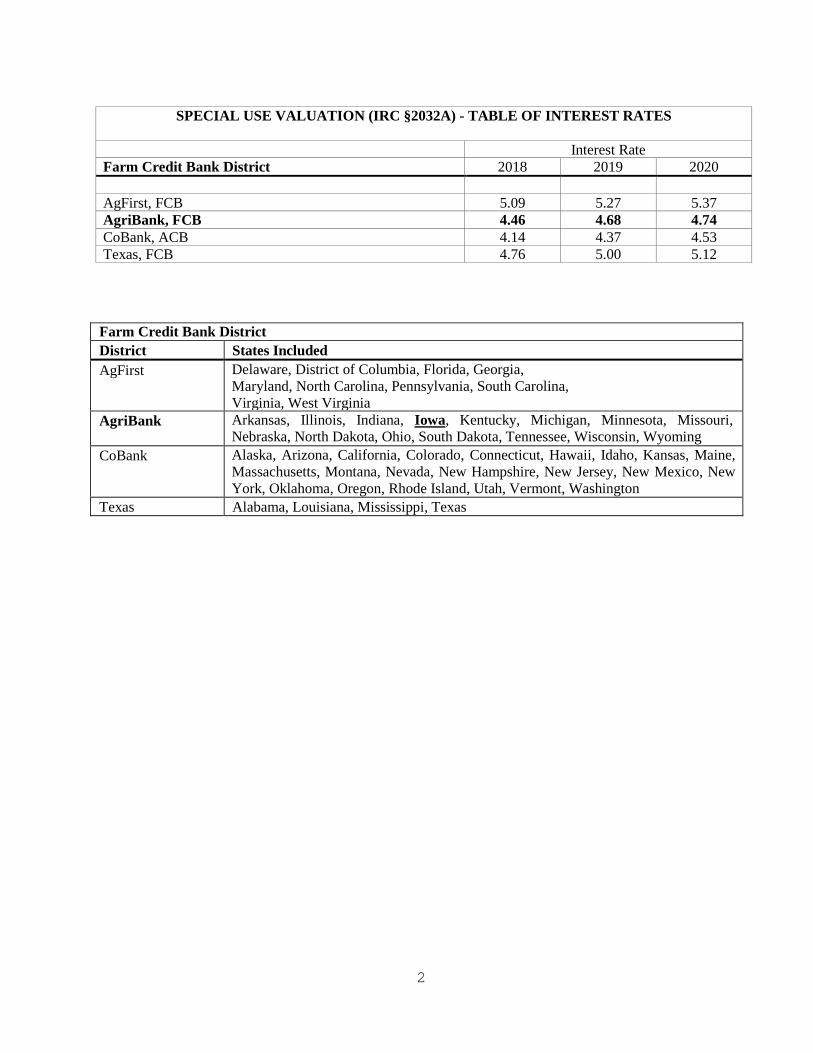

SPECIAL USE VALUATION (IRC §2032A) - TABLE OF INTEREST RATES

Interest Rate Farm Credit Bank District 2018 2019 2020 AgFirst, FCB 5.09 5.27 5.37 AgriBank, FCB 4.46 4.68 4.74 CoBank, ACB 4.14 4.37 4.53 Texas, FCB 4.76 5.00 5.12

Farm Credit Bank District District States Included AgFirst Delaware, District of Columbia, Florida, Georgia,

Maryland, North Carolina, Pennsylvania, South Carolina, Virginia, West Virginia

AgriBank Arkansas, Illinois, Indiana, Iowa, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, Tennessee, Wisconsin, Wyoming

CoBank Alaska, Arizona, California, Colorado, Connecticut, Hawaii, Idaho, Kansas, Maine, Massachusetts, Montana, Nevada, New Hampshire, New Jersey, New Mexico, New York, Oklahoma, Oregon, Rhode Island, Utah, Vermont, Washington

Texas Alabama, Louisiana, Mississippi, Texas

3

IOWA INHERITANCE TAX

Iowa Inheritance Tax is assessed when assets are left to non-lineal descendants, whether through testamentary documents, joint ownership or pay on death designation.

Effective for deaths on or after July 1, 1997, tax as to certain persons, identified as follows, was eliminated:

ASCENDANTS: Parents, grandparents, great-grandparents and other lineal ascendants.

DESCENDANTS: Children (including legally adopted children), stepchildren, grandchildren, step-grandchildren (after 7/1/2016), great-grandchildren, step-great grandchildren (after 7/1/2016) and other lineal descendants.

All other are subject to Inheritance Tax – see rate schedule on attached pages. I. Practice Pointers 1. Return is due at the end of the ninth month after death.

2. If administering a revocable Trust and not probating an estate and real

estate is involved, it may be beneficial to do an Estate without Present Administration/C.I.T. Proceedings to document in the public record the payment of inheritance taxes. Doing an estate without present administration also gives the added benefit of having the Pour Over Will control after the 5-year period and allowing a formal documenting of the step up in basis.

3. It is no longer a requirement to file Inheritance Tax Returns if all individuals are exempt from inheritance tax. Iowa Code Sections 450.22(4), 450.53(2), 450.58(2) and 450.94. There is, however, a requirement that persons that have an interest in the property must file in the county where the real estate is located a statement to the effect that the property that is described therein is not subject to inheritance tax. This requires a correct legal description so that the matter can be indexed.

4. If entire estate does not exceed $25,000.00, no tax is due, but you still

have to file the return to get the Clearance.

4

II. Valuation

1. Treatment of Annuities (Iowa Administrative Code 701--86.5(12)):

Annuities in general, including the earnings, are considered to be taxable under Iowa Code section 450.3(3) as a transfer made or intended to take effect in possession or enjoyment after the death of the grantor or donor. In re Estate of English, 206 N.W.2d 305 (Iowa 1973); In re Endemann’s Estate, 307 N.Y. 100, 120 N.E.2d 514 (1954); Cochrane v. Commission of Corps & Taxation, 350 Mass. 237, 214 N.E.2d 283 (1966).

2. Employer-provided or employer-sponsored retirement plans and individual retirement (Iowa Administrative Code 701-86.5 (13)) :

Iowa Code section 450.4(5) provides an exemption on that portion of the decedent’s interest in an employer-provided or employer-sponsored retirement plan or on that portion of the decedent’s individual retirement account that will be subject to federal income tax when paid to the beneficiary. This exemption applies regardless of the identity of the beneficiary and regardless of the number of payments to be made after the decedent’s death.

For the purposes of this exemption:

a. An “individual retirement account” includes an individual retirement annuity or any other arrangement as defined in Section 408 of the Internal Revenue Code.

b. An “employer-provided or employer-sponsored retirement plan” includes a qualified retirement plan as defined in Section 401 of the Internal Revenue Code, a governmental or nonprofit employer’s deferred compensation plan as defined in Section 457 of the Internal Revenue Code, and an annuity as defined in Section 403 of the Internal Revenue Code.

EXAMPLE 1. The decedent was a participant in a qualified retirement plan through the decedent’s employer. The beneficiary of the retirement plan is the decedent’s niece. The balance in the retirement plan will be fully subject to federal income tax and included as net income pursuant to Iowa Code section 422.7 when paid to the beneficiary. As a result, Iowa inheritance tax would not be imposed on the value of the retirement plan.

EXAMPLE 2. The decedent was a participant in a qualified retirement plan through the decedent’s employer. The beneficiary of the pension is the decedent’s niece. A portion of the payments received by the niece will be fully subject to federal income tax and included as net income pursuant to Iowa Code section 422.7. As a result, Iowa inheritance tax would not be imposed on the value of the portion of payments included as net income. However, the remaining portion of the payments not reported as net income pursuant to Iowa Code section 422.7 would be subject to Iowa inheritance tax. See Iowa Code section 450.4.

An exemption from Iowa inheritance tax for a qualified plan does not depend on the relationship of the beneficiary to the decedent. Payments under a qualified plan made to the estate of the decedent are exempt from Iowa inheritance tax. See In re Estate of Heuermann, Docket No. 88-70-0388 (September 21, 1989). In addition, for the purpose of determining the taxable or exempt status of payments under a qualified plan, it is not relevant that the decedent rolled over or changed the

5

terms of payment prior to death. Taxation or exemption of payments made under a qualified plan is determined at the date of the decedent’s death.

3. Insurance - Iowa Administrative Code 701-86.5 (6):

Whether the proceeds or value of insurance is includable in the gross estate for inheritance tax purposes depends on the particular facts in each situation. Designated beneficiary and type of insurance (life, accident, health, credit life, etc.) are some of the factors that are considered in determining whether the value or proceeds are subject to tax. In re Estate of Brown, 205 N.W.2d 925 (Iowa 1973).

a. Insurance proceeds subject to tax. The proceeds of insurance on the decedent’s life owned by the decedent and payable to the decedent’s estate or personal representative is includable in the gross estate. Insurance owned by the decedent on the life of another is includable in the gross estate to the extent of the cash surrender value of the policy. The proceeds of all insurance to which the decedent had an interest, at or prior to death, but are payable for reasons other than death, are includable in the gross estate. Bair v. Randall, 258 N.W.2d 333 (Iowa 1977).

b. Insurance proceeds not taxable. Insurance on the decedent’s life payable to a named beneficiary, including a testamentary trust, other than the insured, the estate, or the insured’s personal representative, is not subject to Iowa inheritance tax. In re Estate of Brown, 205 N.W.2d 925 (Iowa 1973).

c. Insurance proceeds includable—depending on circumstances. Credit life insurance and burial insurance are offsets against the obligation. If the obligation is deducted in full or in part in computing the taxable shares of heirs or beneficiaries, the proceeds of the credit life and burial insurance are includable in the gross estate to the extent of the obligation. Insurance on the decedent’s life and owned by the decedent, pledged as security for a debt is an offset against the debt if the insurance is the primary source relied upon by the creditor for the repayment of the obligation and is includable in the gross estate on the same conditions as credit life insurance. See Estate of Carl M. Laartz Probate No. 9641, District Court of Cass County, March 17, 1973; Estate of Roy P. Petersen, Probate No. 14025, District Court of Cerro Gordo County, May 16, 1974.

Insurance on the decedent’s life, payable to a corporation or association in which the decedent had an ownership interest, while not subject to tax as insurance, may increase the value of the decedent’s interest. In re Reed’s Estate, 243 N.Y. 199, 153 N.E.47, 47 A.L.R. 522 (1926).

6

III. Computation of Shares

1. Family settlements - Iowa Administrative Code 701-86.14(2)

Beneficiaries of an estate may contract to divide real or personal property of the estate, or both, in a manner contrary to the will of the decedent. The court of competent jurisdiction may approve the settlement contract of the beneficiaries. However, the department is not a party to the contract and is not bound to compute the shares of the estate based on the settlement contract. Instead, the department must compute the shares of the estate based upon the terms of the decedent’s will, unless a court of competent jurisdiction determines that the will should be set aside. See In re Estate of Bliven, 236 N.W.2d 366 (Iowa 1975).

2. “Stepped-up” basis - Iowa Administrative Code 701-86.14(5).

If a decedent’s will provides that taxes are to be paid from the residue of the estate and not the respective beneficial shares, a “stepped-up” basis will be utilized when computing the shares which will result in the appropriate beneficiaries’ shares to include the tax obligation that was paid as an additional inheritance. A “stepped-up” basis is based on gifts prior to the residual share; shares paid out of the residue are not stepped-up.

EXAMPLE: Decedent’s will gives $1,000 to a nephew and directs that the inheritance tax on this bequest be paid from the residue of the estate. The stepped-up share is computed as follows: Tax: $1,000 × 10% = $100. Divide the tax by the difference between the tax rate and 100 percent (90 percent in this example): $100 divided by 90% = $111.11. Add the stepped-up tax of $111.11 to the original bequest of $1,000. This results in a stepped-up share of $1,111.11, which allows the nephew to keep $1,000 after the tax is paid.

7

Iowa Department of Revenue https://tax.iowa.gov Iowa Inheritance Tax Rates

Pursuant to Iowa Code chapter 450 the tax rates are as follows: • If the net estate of the decedent, found on line 5 of IA 706, is less than $25,000, the tax is zero.

Even if no tax is due, a return may still be required to be filed. See IA 706 instructions. • For deaths on or after January 1, 1988, the surviving spouse’s share is not subject to tax. • For deaths on or after July 1, 1997, no tax is due on the following shares: Parents, grandparents,

great-grandparents, children, stepchildren, grandchildren, great-grandchildren, and other lineal ascendants and lineal descendants.

• Effective July 1, 2003, a stepchild is the child of a person who was married to the decedent at the time of the decedent’s death, or the child of a person to whom the decedent was married, which person died during the marriage to the decedent, as defined in Iowa Code section 450.1(1)(e).

• Effective for decedents dying on or after July 1, 2016, no tax is due on the shares of lineal descendants of a stepchild.

TAX RATE B

Brother, sister (including half-brother, half- sister), son-in-law, and daughter-in-law.

TAX RATE C Uncle, aunt, niece, nephew, foster child, cousin, brother-in-law, sister-in-law, and all other individual persons.

TAX RATE D A firm, corporation, or society organized for profit, including an organization failing to qualify as a charitable, educational, or religious organization, to include social and fraternal organizations that do not qualify under Internal Revenue Code 170(c) or 2055. 15% of the share.

TAX RATE E A charitable, educational, or religious organization, organized under the law of any other state, territory, province, or county, and bequests for religious services in excess of $500.00. 10% of the share.

TAX RATE F

Unknown heirs, as distinguished from beneficiaries who are not presently ascertainable, due to contingent events. 5% of the share.

TAX RATE G

A charitable, religious, educational, or other organization as defined in sections 170(c) and 2055 of the Internal Revenue Code (IRC). All other shares to income tax exempt organizations must provide their IRS letter of determination. Organizations may be required to provide evidence that the bequest has restricted the funds to a conforming activity. Public libraries, public art galleries, hospitals, humane societies, municipal corporations, and bequests for care of cemetery or burial lots of the decedent or the decedent’s family, as well as bequests for religious services not to exceed $500.00 in total. Entirely Exempt: No Tax

Over

But Not Over

Tax is

Of Excess Over

$0 $12,500 5% $0 12,500 25,000 $625 + 6% 12,500 25,000 75,000 1,375 + 7% 25,000 75,000 100,000 4,875 + 8% 75,000

100,000 150,000 6,875 + 9% 100,000 150,000 and up 11,375 + 10% 150,000

Over

But Not Over

Tax is

Of Excess Over

$0 $50,000 10% $0 50,000 100,000 $5,000 + 12% 50,000

100,000 and up 11,000 + 15% 100,000

8

9

10

11

12

13

14

15

16

17

18

19

20

21

DEFERRAL OF INHERITANCE TAX Generally the Inheritance tax return is filed during the estate process, even if the remainder beneficiaries being taxed won’t receive their share until the death of a life estate holder or income beneficiary of a By Pass Trust. The remainder beneficiaries can elect to defer the tax until the death of the life tenant.1 The tax will then be due upon the death of the life tenant, since the tax was in place at the time of deferment. This is a deferral of the tax not avoidance of the tax. The tax is computed based on the fair market value of the assets as of the life tenant’s death.2 The tax is due within nine (9) months from the date of the death of life tenant.3 You can elect to defer by filing the Application for Deferral (on next page). All remainder beneficiaries who are required to pay the tax will have to sign a Deferral Application. The tax due becomes a lien on the property. Never defer without advising the clients of the consequences of the deferral. The potential concern with deferral is that appreciation may result in a higher tax. The fair market value is now based on the life tenant’s date of death and no deduction is given for the life tenant’s life estate. So, if the assets appreciate, the remainder beneficiaries could ultimately pay more in tax due to deferral. Be sure to have all necessary Application/Deferral documents filed of record to show the signature by the remainder beneficiaries and approval by the department. In addition, include specific language in the Final Report that addresses the deferral.

1 IAC §450.46 2 IAC §450.37 3 IAC §450.46

22

23

PORTABILITY

Portability is the right to elect to transfer a deceased spouse’s unused exclusion (DSUE) to a surviving spouse to be added to their own basic exclusion amount.4 This election assures that husband and wife together will have full use of their combined exclusions, no matter the titling of assets.

Electing Portability The Executor of the deceased spouse must timely file (including extensions) a Form 706, US Estate and Generation Skipping Transfer Tax Return, that shows the computation of the DSUE and the portability election. The 706 must be complete and properly prepared.5 Part 6 of Form 706 addresses DSUE and portability. See attached Form 706, Part 6 and instructions. NOTE: Be aware of the rules in Treas. Reg 20.2010-3(a) and (b) relating to what determines the last deceased spouse in the case of re-marriage and which DSUE is used in making gifts during lifetime versus transfers at death. A surviving spouse who makes a taxable gift during life would first use the DSUE amount before the surviving spouse’s own basic exclusion amount. If the surviving spouse remarries, he or she may use the DSUE from the first decedent spouse against taxable gifts made during the year. Upon the death of the current spouse, the surviving spouse loses first decedent spouse’s DSUE and succeeds to the second spouse’s DSUE. This means that a surviving spouse could potentially use two or more successive DSUE’s, but they cannot use the sum of DSUE amounts for multiple pre-deceased spouses. **

** Reproduced from 2015 University of Illinois Federal Tax Workbook – Copyright Board of Trustees of the University of Illinois (October 2015) 4 IRC §2010. 5 IRC § 2010(c)(5)(A).

24

Simply filing the completed form is electing portability unless the executor opts not to elect portability by marking the box on Part 6 of Form 706. Due date of the Form 706 is nine months from the date of death. An automatic 6-month extension can be requested by filing Form 4768.

Once made the election is irrevocable unless an amendment or adjustment is made on an amended Form 706 on or before the due date.

Simplified Reporting Method If an executor is not otherwise required to file Form 706 except for the

purposes of portability, there is a simplified reporting method.6 If the gross estate includes marital deduction property or charitable deduction

property, it is not necessary to report the specific value of that property on the corresponding Form 706 schedule. Instead, the executor only has to report the following information related to those assets:

-Description -Ownership -Beneficiary -Any other information necessary to establish rights to the deduction. The Executor must use due diligence to estimate the fair market value of the

deductible property, rounded up to the nearest $250,000. These amounts are reported on Form 706 Part 5, lines 10 and 23.7 Keep in mind that it is always best to determine date of death value for decedent’s assets so that the step up in basis is documented for future sales. This simplified method of reporting may mean that more expensive appraisals/valuations reports are not necessary in certain situations.

Practice Pointers

1. Under Rev. Proc. 2017-34, if an executor missed the original election date

and was not required to file Form 706 under Sec. 6018(a) without regard to the portability election, for decedents dying after Dec. 31, 2010, the executor may file a complete and properly prepared Form 706, by Jan. 2, 2018, or the second anniversary of the decedent's death, whichever is later, to obtain an extension of time to elect portability. The return must include a note at the top stating that it is "filed pursuant to Rev. Proc. 2017-34 to elect portability under Sec. 2010(c)(5)(a)." No user fee is required.8

2. IRS has the ability to examine a predeceased spouse’s gift tax returns and estate tax returns as part of the review of DSUE amounts being used by a decedent at any time in the future. The statute of limitations does not apply in these situations.

3. You should consider whether it is best practice to always advise executors

6 Treas Reg. §20.2010-2(a)(7)(ii)(A). 7 Instructions for Form 706; Treas. Reg. 20.2010-2(a)(7)(ii)(A), (B) 8 Rev. Proc. 2017-34

25

of estates with surviving spouses, Trustees of trusts, and surviving spouse in the case of no estate administration, to file the Form 706 to elect portability, even if it does not appear that the surviving spouse needs to make the election at that time. Not preserving the DSUE and resulting estate tax at a surviving spouse’s death could lead to a malpractice claim. See attached correspondence to client advising of portability election.

4. If executor elects not to file, best practice would be to obtain a signed statement showing full disclosure by you of the risks of not making the election and the executor’s decision not to elect portability. See attached Declination to File Form 706.

5. In the case of a Trust, in which there is no executor, any individual in actual or constructive possession of any property can make the election. This means the Trustee can do so or the surviving spouse.9

9 Treas. Reg. 20.2010-2(a)(6).

26

27

28

29

30

PORTABILITY ELECTION – FOLLOWING DEATH OF SPOUSE Dear Client: Legislation passed in January, 2013 raised the federal estate tax exemption and continued the portability provision which allows a surviving spouse to utilize the unused federal estate tax exemption of a deceased spouse. Prior to the addition of portability to estate tax law in 2010, when an individual’s estate did not use the individual’s entire exemption amount, the unused amount was effectively wasted. For 2020, a married taxpayer can pass along the unused portion of their $11,580,000 million exemption to their surviving spouse, essentially creating a $23.16 million joint exclusion for married taxpayers. The current portability adjustment is not automatically given to a surviving spouse. In order to take advantage of the provision, the deceased spouse’s estate must file a timely federal Form 706, U.S. Estate Tax Return – even in cases when an Estate Tax Return would not otherwise be required to be filed. Our office routinely charges anywhere from $___________ to $____________ to complete a Form 706. Most taxpayers do not anticipate that they will ever exceed $5.60 million in assets during their lifetime, but there is always the possibility that one spouse could gain an inheritance or win the lottery. Thus, by not making the portability election in a timely manner, the surviving spouse could expose their estate to significant estate tax liability if the value of assets owned at their death exceeds the individual estate tax exemption. The choice of whether to file Form 706 and make the election is your decision. If you choose to file Form 706, my office can assist you in doing so. If you choose not to have our office file this form, we will request that you sign a declination, as outlined below. Please contact my office to discuss this letter and any questions you may have about portability, the filing of the Form 706 or the declination to file.

31

DECLINATION TO FILE FORM 706 FOLLOWING DEATH OF SURVIVING SPOUSE

The undersigned has consulted with the law firm of ______________________________ ________________________________ and has been fully advised of their rights and of the legal and financial significance of this form and of not filing a Form 706 to preserve the portability of any unused federal estate tax exemption following the death of their spouse. They acknowledge full and complete understanding of the legal and financial consequences of their informed decision not to elect portability by filing Form 706 and they have freely and voluntarily chosen not to file said form. Dated this ____ day of ________________________, 202___. ____________________________ Signature of Executor /Surviving Spouse

32

DEATH OF A FARMER – STEP-UP IN BASIS

Upon the death of any individual, various items receive a “step-up” in basis which changes the tax basis for the property. For a farmer who passes away, this may include the following:

(1) The land, tile and fence that are affixed to the land;

(2) All farm machinery and equipment;

(3) All breeding stock, milk cows, all livestock of every kind of the self-employed farmer;

(4) All improvements on the farm to the extent the land is enhanced in value, such as machine shed or grain storage; and

(5) Growing crops.

It is a vital part of the estate administration to document the value of all of the assets. Not only should your appraiser value the land, but they should value the improvements on the land. You should be sure to have a thorough conversation with the client about the type of improvement, fencing, tile maps and the value of the land to be sure the client understands the value of a complete and detailed appraisal.

Tile, in very productive ground, is a very integral part of that land. Upon death, one determines what portion of that value is attributable to that tile in place and one must take into account that the tile has been there for perhaps 20 or 30 or 40 years. It would not be the cost of new tile, but a fraction of that. One comes to that determination and then sets up tile as an asset. It is then put on the depreciation schedule and is depreciated from moment of death on.

Practice Pointers:

1) Be sure that all farming assets are identified in the valuation process; 2) Be sure that a new depreciation schedule related to the assets is

started; and 3) Keep a record of assets that receive a step-up in basis, properly

account for them on the 1041 and then be sure to provide that information to the beneficiary so that they have all the information necessary as the asset transitions to their personal income tax returns.

33

POST-DEATH SALE OF LIVESTOCK, UNHARVESTED CROPS AND LAND10

When a farmer dies during the growing season, the tax treatment of the crop (for both income and estate tax purposes) is tied to the status of the decedent at the time of death. The key question is whether the decedent was a farmer or a landlord. If the decedent was a landlord, the tax treatment is tied to the type of lease involved and whether any crop rent had accrued but had not yet been received as of the date of the decedent's death.

The decedent may have owned livestock in addition to other farm assets at the time of death. Unique tax issues must be addressed in connection with these assets, particularly for livestock.

BASIS ISSUES AND CHARACTER OF INCOME

General Rule

Under the general rule, property interests that the decedent owned at death are valued for estate tax purposes at their FMV as of the date of the decedent's death.11 For income tax purposes, the basis of property in the hands of the decedent's heir or the person otherwise acquiring the property from a decedent is the property's FMV as of the date of the decedent's death.12 This is generally known as the "stepped-up" basis rule. Because of the stepped-up basis rule, the heir is not subject to tax on any appreciation in the property's value that occurred during the decedent's lifetime.

Property values may have declined as of the date of death. In this situation, the property's basis is still its FMV as of the decedent's date of death. This is sometimes referred to as a "stepped-down" basis.

IRD Exception

Income in respect of a decedent (IRD) property does not receive any step-up in basis.13 IRD is taxable income the taxpayer earned before death that is received after a taxpayer dies. IRD is not included on the decedent's final income tax return because the taxpayer was not eligible to collect the income before death.

The focus is on the decedent's right or entitlement to the IRD at the time of death. IRD includes more than just accrued earnings14 of a cash-basis decedent. IRD does not include the income potential in a decedent's appreciated property, even if that appreciation is attributable to the decedent's efforts. This is because further action, such as a sale, is required for the appreciation to be realized as income. Likewise, farm products grown and harvested before death (and livestock that is raised before death) but sold after death is property of the decedent at the time of death. It is not treated as a right to income at the time of death.

10 Reproduced from 2015 University of Illinois Federal Tax Workbook – Copyright Board of Trustees of the University of Illinois (October 2015). 11 IRC § 2031. 12 IRC § 1041(a)(1). 13 IRC §691 14 IRC §691(c). Accrued crop rents are not allocated between the estate and the decedent’s final income tax return.

34

IRD is subject to both income tax and (for large estates) estate tax. Although IRD does not receive a step-up in basis by virtue of being included in the decedent's estate, the IRD recipient is entitled to a deduction for the federal estate tax that is attributable to the IRD. The deduction occurs in the year the income from the IRD property is recognized.15 The deduction is calculated as the difference between the estate tax with and without the items that generated the IRD.

The deduction is allowed regardless of whether the IRD item is used to fund a marital deduction for the surviving spouse (in the estate of the first spouse to die). Thus, in larger estates, it may be prudent to fund the marital deduction with IRD items (so that the income tax on the IRD further reduces the spouse's taxable estate) or with property items that are intended to be held by the recipient rather than resold or which have relatively low appreciation.

In Estate of Peterson v. Comm’r, the Tax Court set forth four requirements for determining whether post-death sales proceeds are IRD.16

1. The decedent entered into a legal agreement regarding the subject matter of the sale.

2. The decedent performed the substantive acts required as preconditions to the sale (i.e., the subject matter of the sale was in a deliverable state on the date of the decedent's death).

3. No economically material contingencies that might have disrupted the sale existed at the time of death.

4. The decedent would have eventually received (actually or constructively) the sale proceeds if he had lived.

The case involves the sale of calves by a decedent's estate. Two-thirds of the calves were deliverable on the date of the decedent's death. The other third were too young to be weaned as of the decedent's death and the decedent's estate had to feed and raise the calves until they were old enough to be delivered. The court held that the proceeds were not IRD because a significant number of the calves were not in a deliverable state as of the date of the decedent's death. In addition, the estate's activities with respect to the calves were substantial and essential. The Tax Court held that all of the above requirements had to be satisfied for the income to be IRD, and the second requirement was not satisfied.

IRD and Farm Lease Income

Classifying income as IRD depends on the status of the decedent at the time of death. The following two questions are relevant.

1. Was the decedent an operating farmer or a farm landlord at the time of death? If the decedent was a farm landlord, the type of lease matters.

15 IRC § 691(c), 16 Estate of Peterson v Comm’r, 667 F.2d 675 (8th Cir. 1981).

35

2. If the decedent was a farm landlord, was the decedent a materially participating landlord or a non-materially participating landlord?

Note. Materially participating farm landlords report their lease income on Schedule F. Cash-lease income is reported on Schedule E. Nonmaterial participation crop-share or livestock-share lease income is reported on Form 4835, Farm Rental Income and Expenses.

Operating Farmers and Materially Participating Landlords.

For operating fanners (including materially participating farm landlords), unsold livestock, growing crops, and grain inventories are not IRD.17 The rule is the same if the decedent was a landlord under a material-participation lease.18 These assets are included in the decedent's gross estate and receive a new basis equal to their FMV as of the decedent's date of death under IRC §1014.19 No allocation is made between the decedent's estate and the decedent's final income tax return.20 The allocation rules, when applicable, are discussed later.

Note: Crops that a farmer delivers to a cooperative before death, do, however, give rise to IRD.21

For income tax purposes, all of the crop production expenses incurred by the farmer before death are deducted on Schedule F of the decedent's income tax return. At the time of death, the FMV of any growing crop is established in accordance with a formula (as set forth later). That FMV amount is treated as inventory and deducted when the harvested crop is sold. The remaining costs incurred after death are also deducted by the decedent's estate. In many cases, it may be possible to achieve close to a double deduction.

Nonmaterially Participating and Cash-Rent Landlords.

If a cash-basis landlord rents out land under a nonmaterial- participation lease, the landlord normally includes the rent in income when the crop share is reduced to cash or a cash equivalent, not when the crop share is first delivered to the landlord. In this situation, a portion of the growing crops or crop shares or livestock that are sold post-death are IRD and a portion are post-death ordinary income to the landlord's estate. This is the result if the crop share is received by the landlord before death but is not reduced to cash until after death, or if the decedent had the right to receive the crop share and the share is delivered to the landlord's estate and subsequently reduced to cash. In essence, an allocation is made with the portion of the proceeds allocable to the pre- death period (in both situations) being IRD in accordance with a formula described in

17 Rev. Rul. 58-436, 1958-2 CB 366. See also Estate of Burnett v Comm’r, 2 TC 897 (1943) 18 Rev. Rul. 64-289, 1964-2 CB 173. While the Code and the Regulations are unclear on the issue, it appears that the decedent could achieve material participation through an agent. 19 See, e.g., Estate of Tompkins v. Comm 'r, 13 TC 1054 (1949). This is the rule for decedents on the cash method. For those on the accrual method, the items are included in the decedent's closing inventory on the final return. 20 Treas. Reg. §20.2031-l(b). 21 Treas. Reg. §1.691(a)-2(b), Ex. 5. See also Comm 'r v. Linde, 213 F.2d 1 (9th Cir. 1954), cert. den., 348 U.S. 871 (1954).

36

Rev. Rul. 64-289.22 That formula splits out the IRD and estate income based on the number of days in the rental period before and after death.

Example: Bob, a cash-method taxpayer, leased his farm to Sally for one year beginning March 1, 2014. The rental agreement called for Bob to be paid one-third of the crop in cash upon its sale at Bob's direction.

Bob died on July 4, 2014, after too much partying at the Bigfoot Band Festival in a nearby town. Bob was alive 126 days of the rental period.

The executor of Bob's estate ordered the crop sold. The executor was paid $42,000, which was one-third of the crop sale amount, on January 15, 2015. The IRD is $14,499 ((126 +365) x $42,000). The proceeds attributable to the portion of the rent period that runs from the day after death to the end of the rent period is $27,501 ($42,000 -$14,499). This amount is treated as ordinary income earned by Bob's estate after his death.23

Note. The $14,499 was earned before Bob's death, but it is not included on Bob's final income tax return. It is included in Bob's estate for federal estate tax purposes, and the recipient is entitled to a deduction for the federal estate tax (if any) that is attributable to it.

Example: On February 4, 2014, Jerry Mander leased his farm to a tenant on a 60/40 crop-share lease (i.e., Jerry gets 40% of the crop and pays for 40% of the expenses). The lease ran from March 1, 2014, through February 28, 2015, and was for the growing of corn and soybeans on Jerry's farm.

Jerry died on July 4, 2014. The tenant harvested the corn on October 15 and sold it later the same day for $135,000. The soybeans were harvested on October 7 and stored. The soybeans were later sold on January 27, 2015, for $40,000.

The allocation formula operates as follows.

The lease period was for 365 days (March 1, 2014 to February 28, 2015), and Jerry was alive for 126 of those days. Thus, $18,641 ((126 + 365) x $135,000 x 40%) of the amount that the estate received for the com is IRD.

The balance of the amount received by the estate is $35,359 (($135,000 x 40%) -$18,641), which is taxable to the estate as ordinary income.

The entire $16,000 ($40,000 x 40%) that the estate received for the soybeans is taxed to the estate as ordinary income.

Note. If Jerry had died after the crop shares were sold (but before the end of the rental period), the proceeds would have been reported on Jerry's final return. No proration would have been required,

If Jerry had received his crop share in-kind and held it until death, with the heirs selling it after death, the sale proceeds would be allocated

22 Rev. Rul. 64-289, 1964-2 CB 173. The formula is directed to decedents who were on the cash method and specifies that for decedents dying during the rent period, only the crop (or livestock share) rents attributable to the rent period ending with the decedent's death are IRD. 23 See also Estate of Davison v. U.S., 292 F.2d 937 (Fed. Cl. 1961).

37

between IRD and ordinary income of the estate under the formula described earlier.

Unpaid (accrued) expenses attributable to IRD items are deducted as an expense on Schedule K of Form 706. They are also deducted on the income tax return of the estate when the expense item is paid.

In a 1997 8th Circuit opinion, a landowner leased his farm to his son in exchange for the right to receive 50% of the proceeds from all crop and livestock sales. In the past, the landowner had always reported the sales proceeds as ordinary income. Upon the landowner's death, his right to receive the rent income was fully vested. If he had lived, he would only have needed to wait to receive his income. Thus, the decedent's right to receive the rent income passed to his estate and the rent the estate received was IRD.24

Note. In these situations, IRD does not exist until the crop share is sold. However, if the landlord received the crop share and sold it before death, the income realized is includable on the landlord's final return and is not IRD.25

IRD results from crop-share rents of a nonmaterially participating landlord that are fed to livestock before the landlord's death if the animals are also owned on shares. If the decedent utilized the livestock as a separate operation from the lease, the in-kind crop-share rents (e.g., hay, grain) are treated as any other asset in the farming operation - included in the decedent's gross estate and entitled to a date-of-death FMV basis.

Crop-share rents fed to livestock after the landlord's death are treated as a sale at the time of feeding26 with an offsetting deduction.

Note. Animals of an active operator or materially participating landlord are entitled to a step-up in basis equal to FMV at the time of the operator's or materially participating landlord's death. However, they do not receive the automatic long-term capital gain treatment if they are sold before the end of the required holding period (24 months for cattle or 12. months for other livestock).27 Livestock that are held for sale generate ordinary income, less the FMV as of the date of the decedent's death. Livestock that are held for replacement purposes have a tax basis and are depreciable when they are placed in service.

CHARACTER OF GAIN ON SALE OF UNHARVESTED CROPS

Sale of Grain

Grain that is raised by a farmer and held for sale or for feeding to livestock is inventory in the hands of the farmer. Upon the subsequent sale of the grain, the proceeds are treated as ordinary income for income tax purposes.28 However, when a farmer dies and the estate sells grain inventory within six months

24 Estate of Gavin v. U.S., ll3 F.3d 802 (&th Cir. 1997). 25 Ibid 26 Rev. Rul. 75-11, 1975-1 CB 27 27 Rev. Rul. 75-361, 1975-2 CB 344. 28 IRC §§61(a)(2) and 63(b).

38

after death, the income from the sale is treated as long-term capital gain if the basis in the crops was determined under the IRC §1014 date-of-death FMV rule.29

Note. Ordinary income treatment occurs if the crop was raised on land that is leased to a tenant.30

If the decedent operated the farming business in a partnership or corporation and the entity is liquidated upon the decedent's death, the grain that is distributed from the entity may be converted from inventory to a capital asset.31 However, to get capital asset status in the hands of a partner or shareholder, the partner or shareholder cannot use the grain as inventory in a trade or business.32 That status is most likely achieved, therefore, when the partner or shareholder does not continue in a farming business after the entity's liquidation.

Sale of Farmland with Unharvested Crop

When farmland with an unharvested crop is sold post-death, the crops are treated as part of the farmland.33 That means that if the selling price of the combined farmland and the unharvested crop exceeds the property's adjusted basis (including the production expenses attributable to the unharvested crop), the gain is treated as long-term capital gain, regardless of how long the property is held after death.

Note. This means that the amount of gain treated as ordinary income (from the sale of crop after harvest) is eliminated and the amount of capital gain is increased.

Additionally, when farmland with an unharvested crop is sold, the gain attributable to the unharvested crop is not subject to SE tax.

Example: Guy Wire planted a soybean crop on April 20, 2015. Guy died on May l, 2015. Guy's estate sold the land with the unharvested soybean crop on it on October 15, 2015, for $1.2 million. The portion of the selling price attributable to the soybean crop was $250,000, and the expenses attributable to the crop were $100,000.

Had the crop been harvested and sold, the net sale price of $150,000 ($250,000 -$100,000) would have been reported on Schedule F, where it would have been subject to SE tax. However, by having Guy's estate sell the farmland with the unharvested crop, the $150,000 of net crop value is treated as part of the IRC §1231 gain and is not subject to SE tax.

29 IRC §1223(9). 30 See, e.g., Bidart Brothers v. U.S., 262 .F.2d 607 (9th Cir. 1959). 31 See, e.g., Greenspan v. Comm 'r,229 F.2d 947 (8th Cir. 1956). The court held that inventory passing to two 50% shareholders upon liquidation of a corporation was a capital asset in the hands of the shareholders. 32 See, e.g., Baker v. Comm’r ,248 F.2d 893 (5th Cir. 1957). Partners who used inventory received upon partnership dissolution in a business similar to the partnership' s business were treated as receiving ordinary income upon the sale of the inventory. 33 IRC §1231

39

Note. Loss is disallowed on a sale or exchange between an executor of an estate and a beneficiary of the estate.34

Summary Points

Although the sale of raised crops or livestock in the estate of an active farmer usually triggers ordinary income, the sale by the estate of land with growing crops results in capital gain treatment for the income that is attributable to the crop.35

The same result is achieved when the crops are harvested during the process of liquidating the farming operation and the land is sold. Part of the basis of the unharvested crop at the date of death is allocated to the crop inventory after harvest. The subsequent sale of the post-harvest crop generates ordinary income, less the cost basis assigned.

VALUATION OF CROPS AT DEATH

For estate tax valuation purposes, the crop is valued as of the date of death or six months after death if the executor makes an alternate-valuation election.36 If an alternate-valuation election is made, any increase in value, attributable to crop growth during the 6-month alternate-valuation period is not directly included in the gross estate.37 Instead, the crop rental value (for both date-of-death and alternate-valuation purposes) is allocated between the pre-death and post-death period in accordance with a formula. The formula multiplies the value by a fraction. The numerator of the fraction is the number of days in the part of the rental period that ends with the decedent's date of death, and the denominator is the total number of days in the rental period.

Note. When the crop is later sold (or fed to livestock), the sale proceeds (or the value of the crop on the date of disposition by feeding to livestock) are used in the formula to determine which portion of the crop rental is IRD and which portion is income to the estate.

Several methods can be used to value an unharvested crop. One approach is to determine a value by discounting the crop by the amount of risk involved between the date of death and harvest. The amount of risk is tied to the type of lease involved.

Alternatively, the crop could be valued by the amount of a loan, secured by the crop, that could have been negotiated as of the date of death.

The simplest (and least beneficial to the decedent's estate) approach is to prorate the allocation of the crop proceeds between the pre-death and post-death periods. It is this pro-rata approach that the IRS utilizes to address both estate tax and income tax issues involving unharvested crops in a decedent's estate.

34 IRC §267(b)(13). An exception exists for a sale or exchange in satisfaction of a pecuniary bequest. 35 IRC §§268 and 1231(b)(4). 36 See, e.g., IRC §2032. 37 Compare Ltr. Rul. 7743007 (Jul. 25, 1977) and Ltr. Rul. 7805008 (Oct.31, 1977).

40

State-Level Taxation

Some states have specific rules for handling unharvested crops at death for tax purposes. In Iowa, for example, the Iowa Department of Revenue uses the pro-rata approach. Thus, growing crops owned by a decedent at death are valued via a formula.38 Under the formula, the cash value of the crop realized upon sale is prorated by attributing a portion of the value to the period before death and a portion to the period after death. The amount attributed to the pre- death period is the value for Iowa inheritance tax purposes. The numerator of the ratio expresses the number of days the decedent lived during the growing season (com and soybeans), which is considered May 15 through October 15 (153 days). The 153-day period is the denominator. The ratio is multiplied by the number of bushels realized upon harvest with that result multiplied by the local elevator price at the time of maturity. However, if the estate sells the crop within a reasonable time after harvest in an arm's-length transaction, the selling price can be used as the FMV basis. The Iowa regulations provide the following example.39

Example: Pete lived in Iowa and raised corn and beans. He died on August 15. Pete lived 92 days of the 153-day Iowa growing season. In the fall, the estate harvested 2,000 bushels of corn that were sold to a local elevator for $3.10 per bushel. As a result, the value of the crop for Iowa inheritance tax purposes is $3,728 ((92 pre-death days + 153 growing-season days) x 2,000 bushels x $3.l0 price per bushel).40

The Iowa regulations also address the valuation issue if the decedent was a farm landlord with a tenant operating under a cash lease.41 In that situation, the Iowa inheritance tax value of the crop is determined in accordance with a formula in which the cash rent for the entire rental period is prorated over the entire year. The proration period is the number of days the decedent lived during the rental period, divided by 365 days. The resulting percentage is then applied to the total cash rent for the entire year. The regulation allows a deduction for rent payments made before death and specifies that if such a deduction results in a negative amount, no refund or credit is allowed.42

Other states do not have specific procedures for valuing unharvested crops.43 In those states, the value may be determined by discounting the crop by the amount of risk involved between the date of death and harvest, with the amount of risk

38 IAC §701-86.11(7). 39 Ibid. 40 The resulting amount can be reduced by harvesting costs. Such reduction does not appear to be mandatory and, if taken, increases the income tax payable because of the resulting increase of IRD. 41 IAC §701-86.11(7). 42 Ibid. The regulation also states that the valuation formula is utilized whether the decedent is the landlord or tenant of the property 43 Conversely, some states not having established procedures for valuing unharvested crops may have rules for valuing mineral interests at death. In Kansas, for example, interests associated with oil and gas leases are treated as tangible personal property. If the interest is large enough, an appraisal is necessary. However, for smaller interests the state may prescribe the valuation approach to be used. For example, in Kansas, with respect to oil leases and royalties, the average annual income from production for the immediate three years before death is multiplied by 3.5. For a gas well, the average annual production for the five years immediately preceding death is multiplied by 10. If no production occurred in the prior five years, valuation can be based on original cost if the gas well was purchased within a reasonable time before death and there has not been activity in the area to cause an increase in value. ** This outline is from University of Illinois Tax School, 2015.

41

tied to the type of lease involved. Alternatively, the crop's value may be tied to the amount of a loan (secured by the crop) that could have been negotiated as of the date of death. There may also be other acceptable methods of arriving at a reasonable value for unharvested crops.

42

Form 8971 – Basis Reporting

In general, the value of property for estate tax purposes is its fair market value and the tax basis for beneficiaries post death is the fair market value. IRS, in order to try to make sure everyone is using the appropriate basis, now requires that a Form 8971 be filed and pertinent information also be provided to the beneficiary of the asset. The IRS delayed the due date of implementation of this requirement until February 29, 2016 in order to allow time to issue guidance. To date, no further guidance has been issued, so we are relying on the proposed regulations for answers. Form 8971 and the Instructions are attached.

1. Who has to file it?

a. Executor, or person in actual constructive possession of the decedent’s property, required to file a Form 706 must furnish a statement (Form 8971) identifying the value of each interest in property as reported on the estate tax return. I.R.C. §6035 (a)(1).

b. Form 8971 is not required if the estate tax return is not required, even if form 706 is being filed for portability purposes. Treas. Prop. Reg. 1.6035-1(a)(2).

2. When is it due?

a. Form 8971 must be filed and Schedule A’s sent to the beneficiaries by the earlier of 30 days after Form 706 is actually filed or the due date, including extensions. I.R.C. 6035(a)(3).

3. What has to be filed/provided?

a. Form 8971 and accompanying Schedule A has to be provided to the IRS. The Form 8971 and Schedule A identifies the reported value of each asset and who received the property. If it has not been determined which beneficiary will receive which asset, you must report all assets they could possibly receive on their Schedule A. Treas. Prop. Reg. 1.6035-1(c)(3), (e)(3)(i)(B).

b. Only Schedule A is to be provided to the beneficiary who received the property. You do not provide Form 8971 to the beneficiary, just their respective Schedule A.

c. You do not have to report/provide value for the following: 1) Cash; 2) Income in respect of a decedent; 3) Household goods (tangible personal property for which no appraisal is required); and property sold by estate in which gain/loss is recognized and not distributed (sale of stock portfolio, etc).

Practice Pointer – Do not file Form 706 and Form 8971 together; file them separately per the instructions.

43

4. Penalties for Failure to File

a. Zero basis for the asset.

b. Monetary penalties

i. $50 per Form 8971 to the IRS and $50 per Schedule A to each beneficiary if filed within 30 days after the due date.

ii. $260 per Form 8971 to IRS and $260 per Schedule A to the beneficiary if filed more than 30 days after the due date, or if not filed or if filed incomplete. Prop. Treas. Reg. 1.6035-1(h).

iii. Beneficiaries who report a higher basis than Schedule A basis could be subject to a 20% accuracy penalty under Section 6662.

5. Major Concern Area - The Proposed Regulations 1.6035-1(f) require that any property reported to a beneficiary on Form 8971 that is then transferred to a related party (spouse, ancestor, descendant, sibling or spouse of one of those people (Section 2704 (c)(2))) in a carryover basis transaction required the transferor to file a supplement basis information statement to the IRS and the transferee. Related transferees also includes trusts with are grantor trusts and an entity controlled by a transferor and family members.

44

45

46

47

48

49

50

51

RECENT DEVELOPMENTS

1. Anti – Claw Back Regulations In T.D. 9884, the IRS finalized proposed regulations issued in November 2018 (REG-106706-18), amending Regs. Sec. 20.2010-1 to conform with the temporary increase in the basic exclusion amount for estate and gift tax enacted by the legislation known as the Tax Cuts and Jobs Act (TCJA), P.L. 115-97.

For gifts made and estates of decedents dying before Jan. 1, 2018, prior law (Sec. 2010(c)(3)(A)) provided an exclusion from taxable gifts or estates of $5 million, indexed for inflation after 2011. For gifts made or estates of decedents dying after Dec. 31, 2017, and before Jan. 1, 2026, the TCJA increased the amount to $10 million, also indexed for inflation after 2011 (Sec. 2010(c)(3)(C)). Thus, the amount for 2017 was $5.49 million and, for 2018, $11,180,000 (rising to $11.4 million in 2019 and $11.58 million for 2020). The final regulations amend Regs. Sec. 20.2010-1(e)(3) to conform to the TCJA's increase in the exclusion amount and changes regarding the cost-of-living adjustment.

T.D. 9884 confirms that the IRS will not seek to clawback gifts made while the TCJA’s larger exclusion amount is in effect, even if the taxpayer dies after the amount has decreased in 2026. Specifically, the final regulations incorporate a “special rule” in the case of a difference between the exclusion amount applicable to gifts and that applicable at the donor’s date of death. This rule permits the taxpayer’s estate to compute its estate tax credit using the higher of the exclusion amount applicable to gifts made during life or the exclusion amount applicable on the date of death. As a result, a taxpayer can make large gifts now, without a concern of taxpayer’s estate being whipsawed if the gift and estate tax exclusion actually sunsets in 2026.

2. Regulations Clarifying Section 67(g)- Estate & Trust

The Proposed Regulations specify that certain deductions of an estate or trust are allowed in computing adjusted gross income (AGI) and are not miscellaneous itemized deductions and, thus, are not disallowed by I.R.C. §67(g). Instead, they are treated at above-the-line deductions that are allowed in determining AGI. The Proposed Regulations also provide guidance on determining the character, amount and manner for allocating excess deductions that beneficiaries succeeding to the property of a terminated estate or non-grantor trust may claim on their individual income tax returns.

Specifically, the Proposed Regulations amend Treas. Reg. §1.67-4 to clarify that I.R.C. §67(g) doesn’t disallow an estate or non-grantor trust from claiming deductions: (1) for costs which are paid or incurred in connection with the administration of the estate or trust and which would not have been incurred if the property were not held in the trust or estate; and (2) for deductions that are allowed under I.R.C. §§642(b), 651 and 661 (personal exemption for an estate or trust; income distributed currently; and distributions for accumulated income and corpus).

As for excess deductions of an estate or trust, prior Proposed Regulations treated excess deduction upon termination of an estate or non-grantor trust as a single miscellaneous itemized deduction. The new Proposed Regulations,

52

however, segregate excess deductions when determining their character, amount, and how they are to be allocated to beneficiaries. The new Proposed Regulations specified that the excess amount retains its separate character as either an amount that is used to arrive at AGI; a non-miscellaneous itemized deduction; or a miscellaneous deduction. That character doesn’t change in the hands of the beneficiary. The fiduciary is to separately identify deductions that may be limited when the beneficiary claims the deductions.

The Proposed Regulations utilize Treas. Reg. §1.652(b)-3 such that, in the year that a trust or estate terminates, excess deductions that are directly attributable to a particular class of income are allocated to that income. The Preamble to the Proposed Regulations states that excess deductions are allocated to beneficiaries under the rules set forth in Treas. Reg. §1.642(h)-4. After allocation, the amount and character of any remaining deductions are treated as excess deductions in a beneficiary’s hands in accordance with I.R.C. §642(h)(2). This accords with the legislative history of I.R.C. §642(h) in seeking to avoid “wasted” deductions.

The bifurcation of excess deductions into three categories by the Proposed Regulations rather than lumping them altogether miscellaneous itemized deductions disallowed by the TCJA is pro-taxpayer.

The IRS says that the Proposed Regulations can be relied on for tax years beginning after 2017, and on or before the proposed regulations are published as final regulations.

The Final Regulations affirm that deductions for costs which are paid or incurred in connection with the administration of an estate or trust and which would not have been incurred if the property were not held in such trust or estate remain deductible in computing AGI. In other words, I.R.C. §67(e) overrides I.R.C. §67(g). However, the Final Regulations do not provide any guidance on whether these deductions (including those under I.R.C. §§642(b), 651 and 661) are deductible in computing alternative minimum tax for an estate or trust. That point was deemed to be outside the scope of the Final Regulations.

As for excess deductions, the Final Regulations confirm the position of the Proposed Regulations that excess deductions retain their nature in the hands of the beneficiary. Treas. Reg. §1.642(h)-2(a)(2). How is that nature determined? Excess deductions passing from a trust or an estate have their nature pegged by Treas. Reg. §1.652(b)-3. The nature of excess deductions of a trust or an estate is determined by a three-step process: 1) direct expenses are allocated first (e.g., real estate taxes offset real estate rental income); 2) the trustee can exercise discretion when allocating remaining deductions – in essence, offsetting less favored deductions for individuals by using them against remaining trust/estate income (also, if direct expenses exceed the associated income, the excess can be offset at this step); 3) once all of the trust/estate income has been offset any remaining deductions constitute excess deductions when the trust/estate is terminated that are allocated to the beneficiaries in accordance with Treas. Reg. §1.642(h)-4. Treas. Reg. 1.642(h)-2(b)(2).

Example 2 of the Proposed Regulations was modified in the Final Regulations to permit allocation of personal property tax to income, with any I.R.C. §67(e) expenses distributed to the beneficiary. Thus, the fiduciary has discretion to selectively allocate deductions to income or distribute them to

53

a beneficiary. Those excess deductions that are, in a beneficiary’s hands, allowed at arriving at AGI on Form 1040 are to be deducted as a negative item on Schedule 1.

As the Proposed Regulations required and the Preamble to the Final Regulations confirm, the information concerning excess deductions must be reported to the beneficiaries when a trust or an estate terminates. Deduction items must be separately stated when, in the beneficiary’s hands, the deduction would be limited under the Code. The Preamble states that the Treasury Department and the IRS “plan to update the instructions for Form 1041, Schedule K-1 (Form 1041) and Form 1040…for 2020 and subsequent tax years to provide for the reporting of excess deductions that are section 67(e) expenses or non-miscellaneous itemized deductions.”

Because excess deductions retain their nature in a beneficiary’s hands, any individual-level tax limitations still apply. Thus, for example, if an excess deduction results from state and local taxes (SALT) that a non-grantor trust or estate pays, is still limited at the beneficiary’s level to the $10,000 maximum amount under the TCJA. The Final Regulations addressed this issue, but the Treasury determined that it lacked the authority to exempt a beneficiary from the SALT limitation.

The Preamble also notes that beneficiaries subject to tax in states that don’t conform to I.R.C. §67(g) may need access to miscellaneous itemized deduction excess deduction information for state tax purposes. This burden apparently rests with the fiduciary of the estate/trust and the pertinent state taxing authority. The IRS declined to modify federal income tax forms to require or accommodate the collection of this information because it is a state tax issue and not a federal one.

The Final Regulations clarify that a beneficiary cannot carry back a net operating loss carryover that is passed out of a trust/estate in its final year. Treas. Reg. §1.642(h)-5(a), Ex. 1. A net operating loss carryover from an estate/trust can only be carried forward by the beneficiary.

Applicability

The Final Regulations apply to tax years beginning after their publication in the Federal Register. They do not apply to all open tax years. Thus, it is not possible to file an amended return to take advantage of the position of the Final Regulations with respect to excess deductions for a tax year predating the effective date of the Final Regulations.

Conclusion

The Proposed and Final Regulations are, in general, taxpayer friendly. Tax planning will likely focus on the allocation of deductions in accordance with classes of income over which the fiduciary can exercise discretion (amounts allowed in arriving at AGI; non-miscellaneous itemized deductions; and miscellaneous itemized deductions). To the extent that the fiduciary can have excess deductions on termination of an estate or non-grantor trust reduce AGI, that is likely to produce the best tax result for the beneficiary or beneficiaries (with consideration given, of course, to possible TCJA-imposed limitations). Given the compressed tax brackets applicable to trusts and estates, the position taken in the Proposed and Final Regulations on deduction items and the flexibility given to fiduciaries is welcome news.

54

3. Iowa Small Estate – Chapter 635

Effective July 1, 2020, the current value of a Small Estate under Iowa law increased from $100,000.00 to $200,000.00.