taking short-term credit seriously again - c.ymcdn.comc.ymcdn.com/sites/ · taking short-term...

TRANSCRIPT

Taking Short-Term Credit Seriously AgainApril 28, 2015

Brandon T. Swensen, CFACo-Head,

U.S. Fixed Income612-376-7097

John C. DonohueManaging Director,

Head of Liquidity Management617-722-4728

2

3

Types of Money Market Debt

U.S. Treasury Securities

Agency Securities

Repurchase Agreements

Bank Obligations

Commercial Paper

ABCP “Asset-Backed Commercial Paper”

Medium-Term Notes

Floating Rate Notes

4

Repurchase Agreements (“Repo”)

Transactions in which one party sells securities to another while agreeing to repurchase at a specific price and future date

Provider of money “buyer” receives securities as collateral from “seller” to protect it against borrower default

The terms “Repo”, “RP”, and “Reverse Repo” are all used to describe the same transaction

• One firm’s Repo is another’s Reverse Repo• Dealer receiving money is transacting a Repo• Dealer receiving securities is transacting a Reverse Repo• Convention is for both parties to view trade from Dealers Perspective

Underlying securities (a.k.a. “Collateral”) are marked to market daily to maintain margin (excess collateral is typically 102%)

Types of Repo include: Triparty and Delivery vs. Payment

5

Repurchase Agreements (“Repo”)

Types of Collateral(Typical Spread +/- Fed Funds)

Traditional- Treasuries (-1)- Agencies (+1)

Non-Traditional (“NTR”)- Tier-1 CP (+12)- Tier-2 CP (+20)- A or Better Corps (+12)- Munis (+15)- High Yield (+25)- Equities (+20)

News in the “Repo” Market: The Federal Reserve has set up direct

repo lines with money market funds over the past few months. The objective of this action, when executed, will help drain excess reserves from the system.

The New York Federal Reserve has sponsored a task force to reform the repo market. Changes on the horizon include creating standardized margin requirements and reforming the way the market handles intraday credit.

Massive supply of Treasuries are leading to wider spreads on repo backed by traditional collateral

6

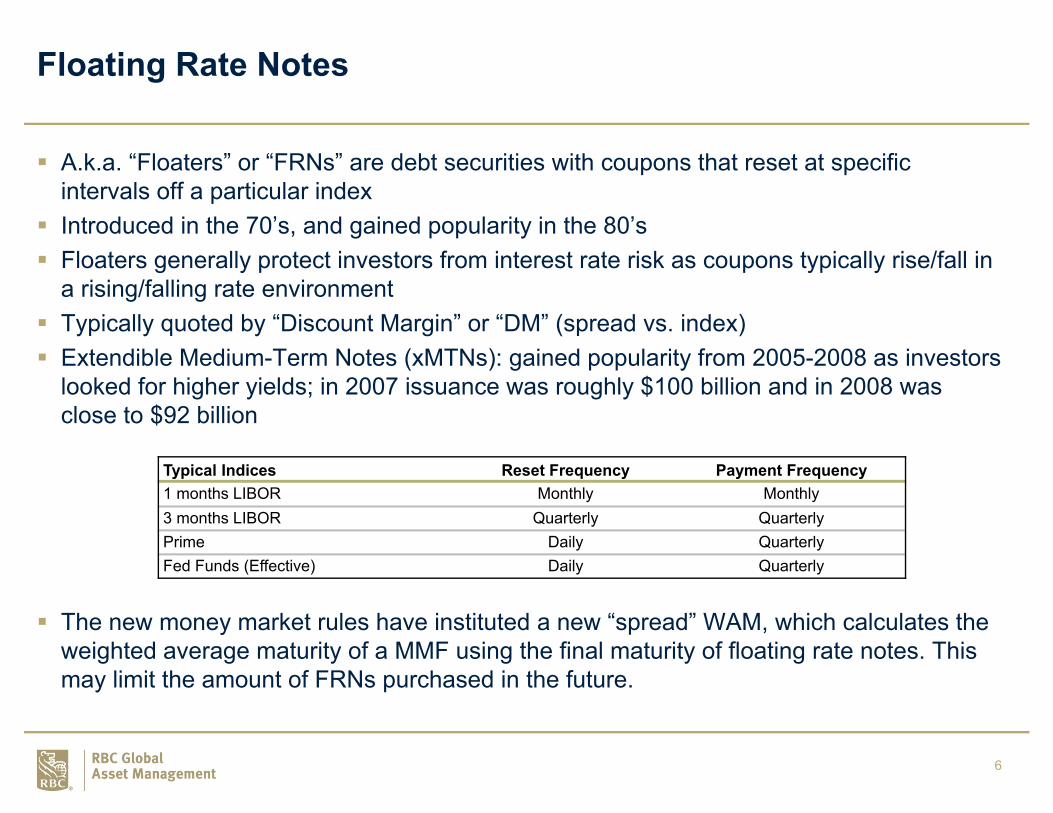

Floating Rate Notes

A.k.a. “Floaters” or “FRNs” are debt securities with coupons that reset at specific intervals off a particular index

Introduced in the 70’s, and gained popularity in the 80’s Floaters generally protect investors from interest rate risk as coupons typically rise/fall in

a rising/falling rate environment Typically quoted by “Discount Margin” or “DM” (spread vs. index) Extendible Medium-Term Notes (xMTNs): gained popularity from 2005-2008 as investors

looked for higher yields; in 2007 issuance was roughly $100 billion and in 2008 was close to $92 billion

The new money market rules have instituted a new “spread” WAM, which calculates the weighted average maturity of a MMF using the final maturity of floating rate notes. This may limit the amount of FRNs purchased in the future.

Typical Indices Reset Frequency Payment Frequency1 months LIBOR Monthly Monthly3 months LIBOR Quarterly QuarterlyPrime Daily QuarterlyFed Funds (Effective) Daily Quarterly

7

Key Takeaways

What is credit risk?

What is the importance of credit analysis?

What is the credit review process?

How do we analyze money market investments?

Causes and effects of the financial crisis

Issues to watch going forward

8

What is Credit Risk?

Credit risk is the likelihood that a debtor will not pay the principal or interest they are contractually obligated to pay.

9

Importance of Credit Risk

Preservation of capital• Spreads can widen dramatically but rarely tighten in the same fashion

Facilitates a buy and hold strategy

Allows for portfolio diversification

Compliance with Rule 2a-7 or client-specific mandate

Provides a competitive advantage among fund managers

10

Credit Review Process

Analyst Team andResearch Process

Credit CommitteeApproval

Approved Issuer

List

Fundamental Analysis

Constant Re-Evaluation• Real-time News and Ratings Feeds• Same-day Financial Modeling• Due Diligence Visits• Proprietary Tools

Asset-Backed• Collateral Performance• Servicing Expertise• Legal Structure

Corporate• Business Risk• Financial Profile• Economic Outlook

Process is shown for illustrative purposes as a general industry practice and is not specific to a firm or group.

11

Analyzing Money Market Investments

Corporate/Financial Credit Risks – rely on the willingness and ability of the corporation to repay its debt originators

Business Risk• Management experience• Competitive position• Industry characteristics

Financial Profile• Profitability• Capital structure• Liquidity

Economic Outlook• Government/regulatory issues• Employment• Inflation

12

Key Financial Ratios

Key Financial Ratios for Financial Companies

Profitability• Return on assets (net income/assets)• Efficiency ratio (non-interest expense/revenues)• Net Interest Margin (net interest income/interest earning assets)

Liquidity• Loans/deposits• Cash and securities/total assets

Capital• Tangible common equity/tangible assets• Tier 1 common equity/risk assets

Asset Quality• Nonperforming assets/loans• Nonperforming assets (tangible common equity + loan loss reserves)• Loan loss reserves/nonperforming assets

13

Analyzing Money Market Investments

Asset-Backed Credit Risks – rely on the cash flow from underlying collateral to repay debt obligations

Servicer• Management experience• Systems/technology

Collateral• Quality• Performance• Cash Flow Predictability

Structure• Government/regulatory issues• Liquidity• Credit Protection

14

Credit Rating Agency Process

Ratings request from issuer Initial evaluation

Meeting with issuer

management

AnalysisRating

committee review and vote

Notification to issuer

Publication & dissemination of

public rating opinions

Surveillance of rated issuers and

issues

Source: Standard & Poor’s Rating Services - Guide to Credit Rating Essentials

15

Credit Ratings Scale

Credit ratings are an attempt to qualify the credit risks associated with a particular corporate or asset-backed security and not a recommendation to buy or sell that security

The long-term rating is based on the probability an issuer will default and the expected severity of loss after a default occurs.The short-term rating is based on the probability of default only.

Investment Grade Ratings ST Speculative Grade

Ratings ST

Aaa

P1

Ba1

NP

Aa1 Ba2

Aa2 Ba3

Aa3 B1

A1 B2

A2 B3

A3

P2

Caa1

Baa1 Caa2

Baa2 Caa3

Baa3 P3 Ca

C

Investment Grade Ratings ST Speculative Grade

Ratings ST

AAA

A-1+

BB+

B/C

AA+ BB

AA BB-

AA- B+

A+

A-1

B

A B-

A- CCC+

BBB+ A-2 CCC

BBB CCC-

BBB- A-3 CC

C

D

Moody’s S&P

Source: Moody’s, S&PRatings are relative and subjective and are not absolute standards of quality. A strategy’s credit quality does not remove market risk.

16

Rating Definitions

General summary of the opinions reflected by S&P ratings

Investment Grade

AAA Extremely strong capacity to meet financial commitments. Highest rating

AA Very strong capacity to meet financial commitments

A Strong capacity to meet financial commitments, but somewhat susceptible to adverse economic conditions and changes in circumstances

BBB Adequate capacity to meet financial commitments, but more subject to adverse economic conditions

BBB- Considered lowest investment-grade by market participants

Speculative Grade

BB+ Considered highest speculative-grade by market participants

BB Less vulnerable in the near-term but faces major ongoing uncertainties to adverse business, financial and economic conditions

B More vulnerable to adverse business, financial and economic conditions but currently has the capacity to meet financial commitments

CCC Currently vulnerable and dependent on favorable business, financial and economic conditions to meet financial commitments

CC Highly vulnerable; default has not yet occurred, but is expected to be a virtual certainty

C Currently highly vulnerable to non-payment, and ultimate recovery is expected to be lower than that of higher rated obligations

D Payment default on a financial commitment or breach of an imputed promise; also used when a bankruptcy petition has been filed or similar action taken

Ratings from ‘AA’ to ‘CCC’ may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories.

Source: Standard & Poor’s Rating Services - Guide to Credit Rating Essentials

17

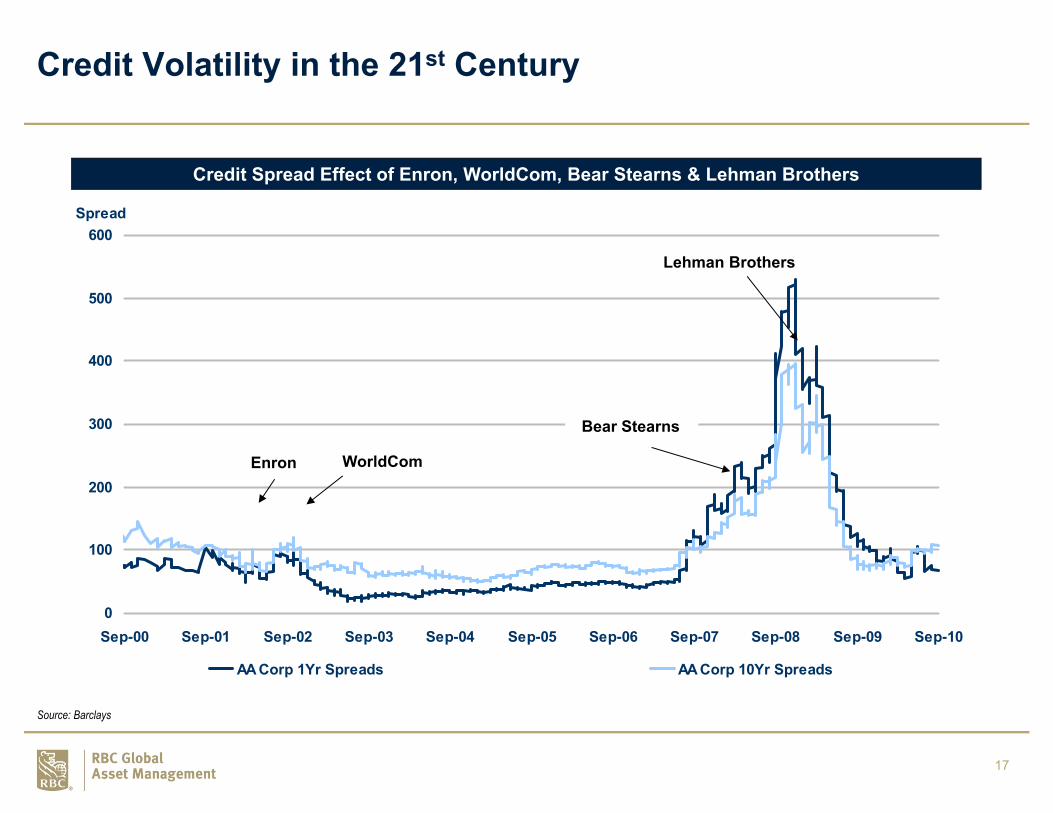

Credit Volatility in the 21st Century

0

100

200

300

400

500

600

Sep-00 Sep-01 Sep-02 Sep-03 Sep-04 Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10

Spread

AA Corp 1Yr Spreads AA Corp 10Yr Spreads

Enron WorldCom

Bear Stearns

Lehman Brothers

Source: Barclays

Credit Spread Effect of Enron, WorldCom, Bear Stearns & Lehman Brothers

18

Asset-Backed Commercial Paper (ABCP) Spread

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

07/16/07 09/14/07 11/13/07 01/12/08 03/12/08 05/11/08 07/10/08 09/08/08 11/07/08

A1+ / P1 Spread A1 / P1 Spread

ABCP Spreads (1 Month ABCP vs 1 Month Libor)

Other factors affecting ABCP spreads:FOMC Cuts rates from 2% to 0% (Sept-Dec), and Central Banks around the world cut rates as well. Oct 7, 2008: CPFFOct 21, 2008: MMIFF

Dec 2007: FOMC cuts 25bps, Fed adopts TAF, Announcements from Citigroup & Rabo to support their SIV Programs

Sept 2008: Lehman Files, andReserve ‘Breaks the Buck’

Aug 6, 2007: Broadhollow and Ottimo ABCP Programs extendAug 9, 2007: Only 13% of maturing ABCP rolls in EuropeAug 15, 2007: KKR and Rams ABCP Extends

Oct - Nov 2007: SIVs hit triggersCheyne, Axon, Orion, Rhinebridge

Sept 18, 2007: Fed cuts 50bps, spreads tighten

Sept 19, 2009: Fed Announces MmktFund Support & AMLF

Source: Bloomberg

19

Casualties of the U.S. Subprime Fallout

Structured Investment Vehicles (SIVs)

Monoline Bond Insurers

Investment Banks

Commercial Banks

Insurance Companies

Government Sponsored Entities

Taxpayers?

20

History as a Guide

Source: Federal Reserve Board

0

5

10

15

20

01/01/71 06/03/76 11/04/81 04/07/87 09/07/92 02/08/98 07/12/03 12/12/08

(%)

Target Fed Funds Bernanke Greenspan Volcker Miller Burns

Target Federal Funds Rate, January 1971-December 2008

Appendix

22

Terms You Can Use

2a-7 – refers to Investment Company Act of 1940 Rule that governs money market funds

Alt-A – type of mortgage that typically requires less documentation than traditional mortgages

Bullets – a fixed coupon security

Credit Arbitrage – ABCP conduit used to fund acquisitions of investment grade securities

Delivery vs. Payment Repo – repo where security delivery and payment are simultaneous

Discount Margin – spread relative to the base index rate that makes the present value of future cash flows equal to the price plus accrued interest (a.k.a. “DM”)

Duration – weighted average time to receipt of a bonds cash flows; the greater the duration, the greater its percentage price volatility

23

Terms You Can Use (cont.)

ENCs (Extendible Commercial Notes) – short-term notes where issuer has option to extend maturity to 390 days

Federal Funds Rate – interest rate at which banks lend to each other

Federal Open Market Committee – makes key decisions about interest rates and the growth of the U.S. money supply

GDP (Gross Domestic Product) – the market value of all final goods and services made within the borders of a nation in a year

GSEs (Government Sponsored Entities) – including Fannie Mae, Freddie Mac & Federal Home Loan Banks

Hybrid – ABCP conduit that is a mix of multi-seller and credit arbitrage strategies

IMF (International Monetary Fund) – fosters global monetary cooperation

ISM (Institute for Supply Management) – largest supply management association in the world

LIBOR (London Interbank Offered Rate) – rate at which banks lend to each other in the London wholesale market

24

Terms You Can Use (cont.)

Monoline Bond Insurers – insurance providers guaranteeing bond performance

Multi-Seller – ABCP conduit backed by receivables from many asset originators

Nationalization – when a government takes ownership of an institution

NRSRO (Nationally Recognized Statistical Rating Organization) – i.e., Fitch, S&P, Moody’s

Off-Balance Sheet – transactions which have a material affect on a company but are held off its balance sheet

Option-ARM – Adjustable Rate Mortgage with multiple payment options for the borrower

Rally – increase in prices, decrease in yield

SLNs (Secured Liquidity Notes) – short-term notes backed by liquid securities and a total rate of return or market value swap

Spread Product – a non-governmental bond with a premium or spread built in

25

Terms You Can Use (cont.)

Single-Seller – ABCP conduit backed by receivables from a single asset originator

SIV – ABCP conduit with an ABS-type structure used to find acquisitions of securities

Subprime – loan to a borrower with a credit score of <620

TAF (Term Auction Facility) – Fed auction to depository institutions; all primary dealers eligible

TALF (Term Asset Backed Loan Facility) – will purchase up to $200 billion in AAA-rated ABS backed by “newly and recently originated” ABS; the Treasury will finance the first $20 billion in asset purchases from TARP with the Fed providing the remainder of a non-recourse basis

TARP – Troubled Assets Relief Program

Triparty Repo – repo where collateral is held by a third party on the buyer’s behalf

Warehoused Mortgage-Backed Loans – loans that are to be sold into secondary market

26

Royal Bank of CanadaStrength & Stability

*Ratings: S&P: AA-, Moody's: Aa3 (Bloomberg, 12.31.14). Ranked 5th largest bank in North America and 12th globally based on market capitalization (Bloomberg, 12.31.14).All other data in U.S. dollars as of 12.31.14. Refer to disclosure page for more information on RBC GAM and its affiliates.

27

Professionals

John C. DonohueManaging Director, Head of Liquidity ManagementJohn Donohue leads our institutional distribution efforts to position RBC GAM as an industry leader in liquidity management. John has spent the majority of his career in the short duration fixed income space, holding leadership roles within both portfolio management and distribution. John joined RBC GAM-US in January 2015 from Eaton Vance, where he was the Director of Institutional Cash Management Services. Prior to this, he held senior level positions at Dwight Asset Management, where he was Executive Vice President, Head of Liquidity Management and Neuberger Berman (formerly Lehman Brothers Asset Management), where he was Chief Investment Officer, Head of Global Cash Strategies. John is a member of the iMoneyNet Money Market Advisory Board and Conference Faculty. He is also a frequent presenter at industry conferences such as Association of Financial Professionals events, and global forums including the American Chamber of Commerce in Singapore. John earned a BA from Saint Anselm College, an MBA from Assumption College and holds FINRA Series 7 and 63 licenses.

Brandon T. Swensen, CFACo-Head, U.S. Fixed IncomeBrandon Swensen oversees our fixed income research, portfolio management and trading. In addition to shaping our overall fixed incomephilosophy and process, he is a portfolio manager for several of our cash management and core solutions. Brandon joined RBC GAM-US in 2000 and most recently was a portfolio manager on the mortgage and government team before being promoted to Co-Head. He also held research analyst positions covering asset-backed securities and credit and served as a financial analyst for the firm. Brandon earned a BS in finance from St. Cloud State University and an MBA in finance from the University of St. Thomas. He is a CFA charterholder and member of the CFA Society of Minnesota.

28

Disclosures

This document (the “Presentation”) is being provided by RBC Global Asset Management to institutional investors. This Presentation is subject to change without notice and is qualified by these disclosures and the disclosures and definitions contained, may not be reproduced in whole or part, and may not be delivered to any other person without the consent of RBC Global Asset Management. This Presentation is not a solicitation of any offer to buy or sell any security or other financial instrument or to participate in any investment strategy and should not be construed as tax or legal advice.

RBC Global Asset Management is the name used in the United States for certain investment advisory subsidiaries of the Royal Bank of Canada. RBC Global Asset Management (U.S.) Inc. (“RBC Global Asset Management – US” or “RBC GAM-US”) is a federally registered investment adviser founded in 1983.

Past performance is not indicative of future results. There can be no guarantee that any investment strategy discussed in this Presentation will achieve its investment objectives. As with all investment strategies, there is a risk of loss of all or a portion of the amount invested. With respect to goals, targets, objectives, expectations and processes discussed in the presentation, there is no guarantee that such goals, targets, objectives or expectations will be achieved or that the processes will succeed. Any risk management processes discussed refer to efforts to monitor and manage risk but should not be confused with and does not imply no or low risk. The use of diversification within an investment portfolio does not assure a profit or guarantee against loss in a declining market. No chart, graph, or formula can by itself determine which securities an investor should buy or sell or which strategies should be pursued.

This Presentation contains the opinions of RBC Global Asset Management as of the date of publication and is not intended to be, and should not be interpreted as, a recommendation of any particular security, strategy or investment product. Not all products, services or investments described herein are available in all jurisdictions and some are available on a limited basis only, due to local regulatory and legal requirements. Unless otherwise indicated, all information and opinions herein are as of December 31, 2014 and are subject to change without notice.

These materials may contain information collected from independent third party sources. For purposes of providing these materials to you, neither RBC nor any of its affiliates, subsidiaries, directors, officers, or employees, has independently verified the accuracy or completeness of the third-party information contained herein.

Although RBC GAM-US is registered as an investment adviser with the SEC, such registration in no way implies that the SEC has reviewed or approved the investment portfolio and does not imply that RBC GAM-US has achieved a certain level of skill or training.

RBC Global Asset Management (“RBC GAM”) is the asset management division of Royal Bank of Canada (“RBC”) which includes RBC GAM-US, RBC Global Asset Management Inc., RBC Global Asset Management (UK) Limited, RBC Alternative Asset Management Inc., BlueBay Asset Management LLP and BlueBay Asset Management USA LLC, which are separate, but affiliated corporate entities. ®/™ Trademark(s) of Royal Bank of Canada. Used under license. © 2014 RBC Global Asset Management (U.S.) Inc.