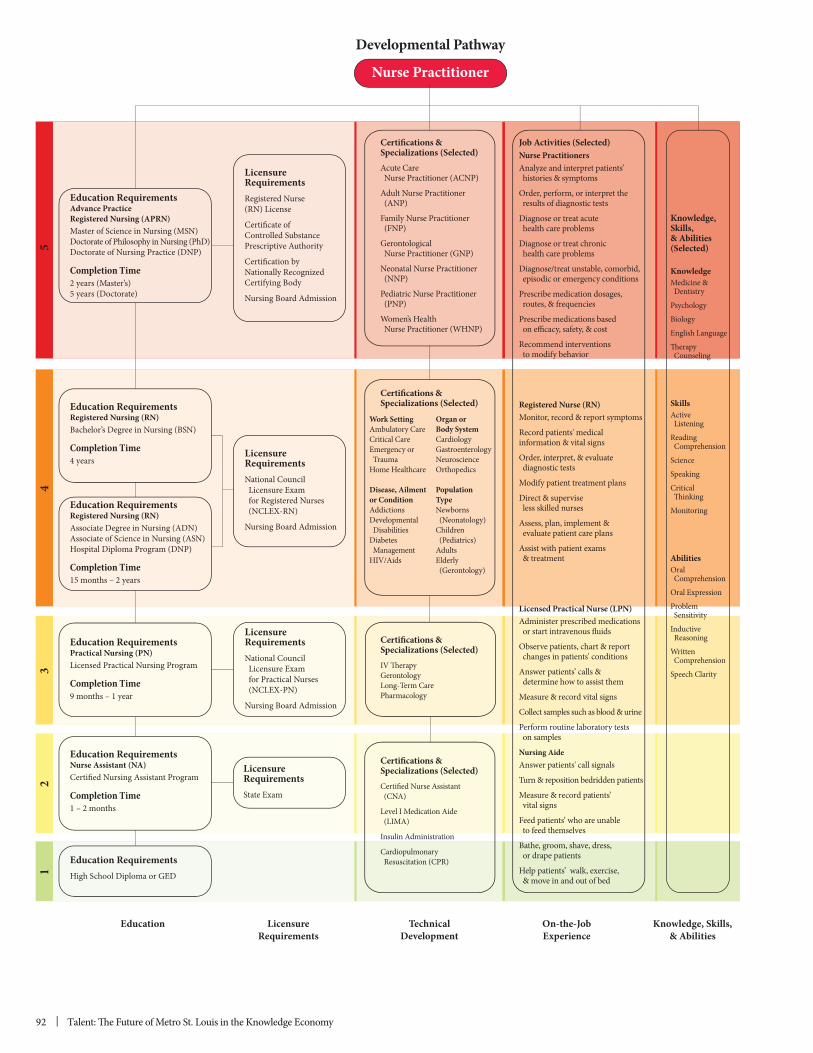

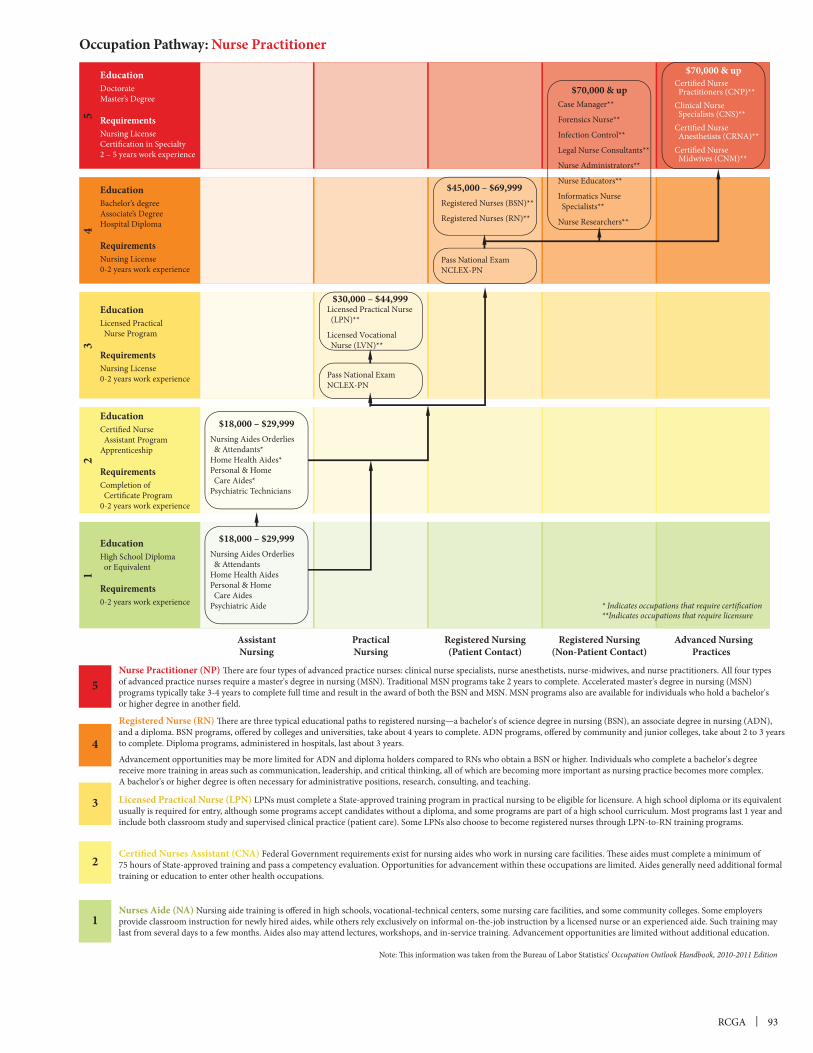

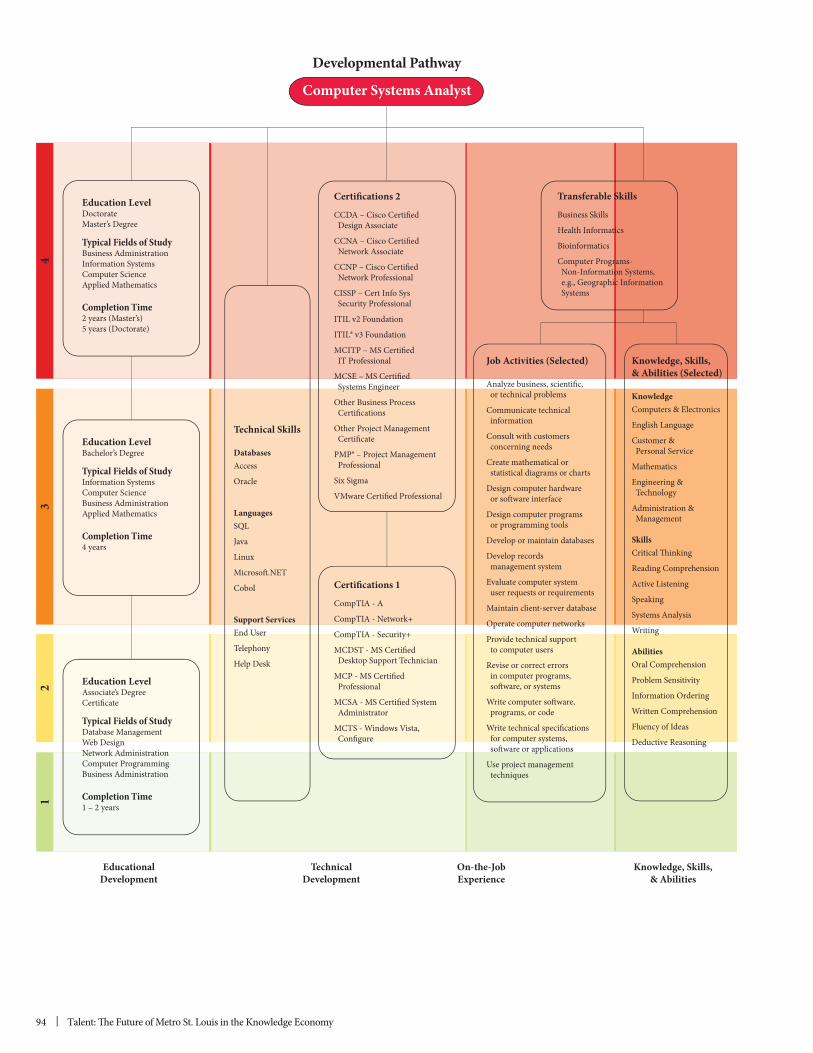

talent: the future of st. louis metro in the knowledge...

TRANSCRIPT

Talent: The Future of

Metro St. Louis in the

Knowledge Economy

2 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Contents

Preface ...................................................................................................................................................................................3

1. Today’s Challenges: St. Louis and the Great Recession ....................................................................................... 4

2. Regional Collaboration: A New Approach for a New Economy .................................................................... 10

3. Talent Development, Job Creation, and Economic Growth: A Virtuous Circle for the Future ................ 12

4. The St. Louis Metro Economy ............................................................................................................................... 18

5. Opportunity: Financial and Information Services ............................................................................................ 28

6. Opportunity: Sustainable Technologies ............................................................................................................... 42

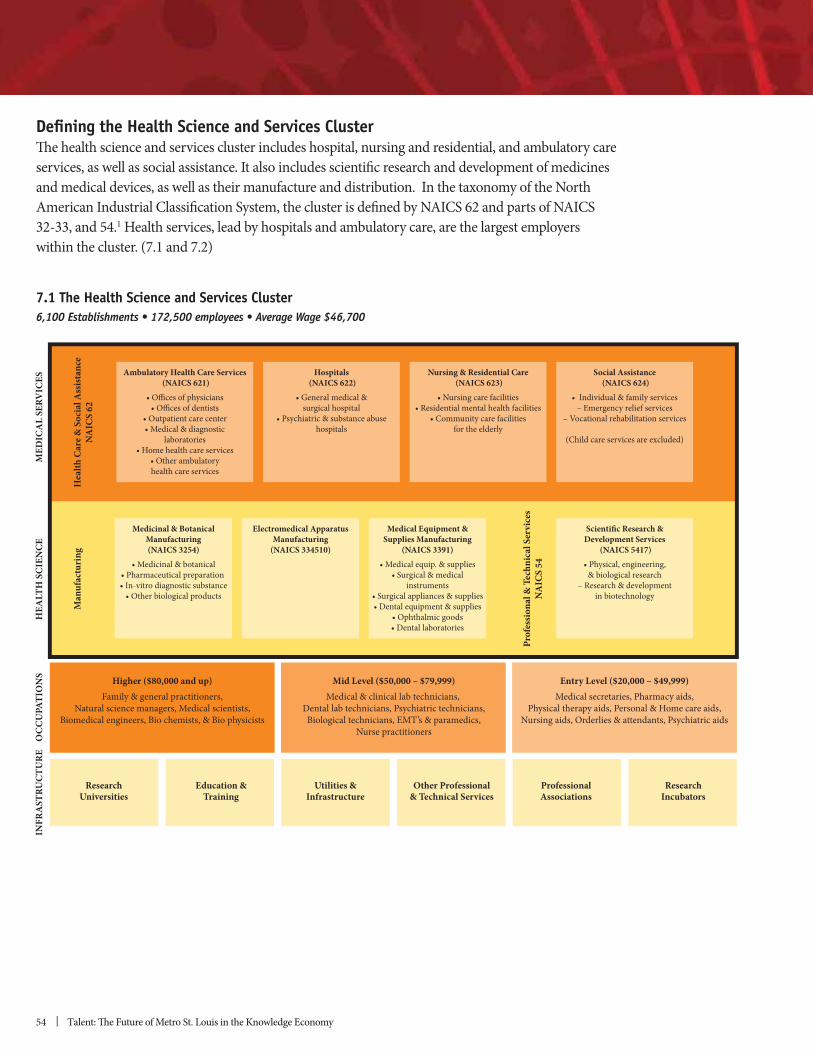

7. Opportunity: Health Science and Services ......................................................................................................... 53

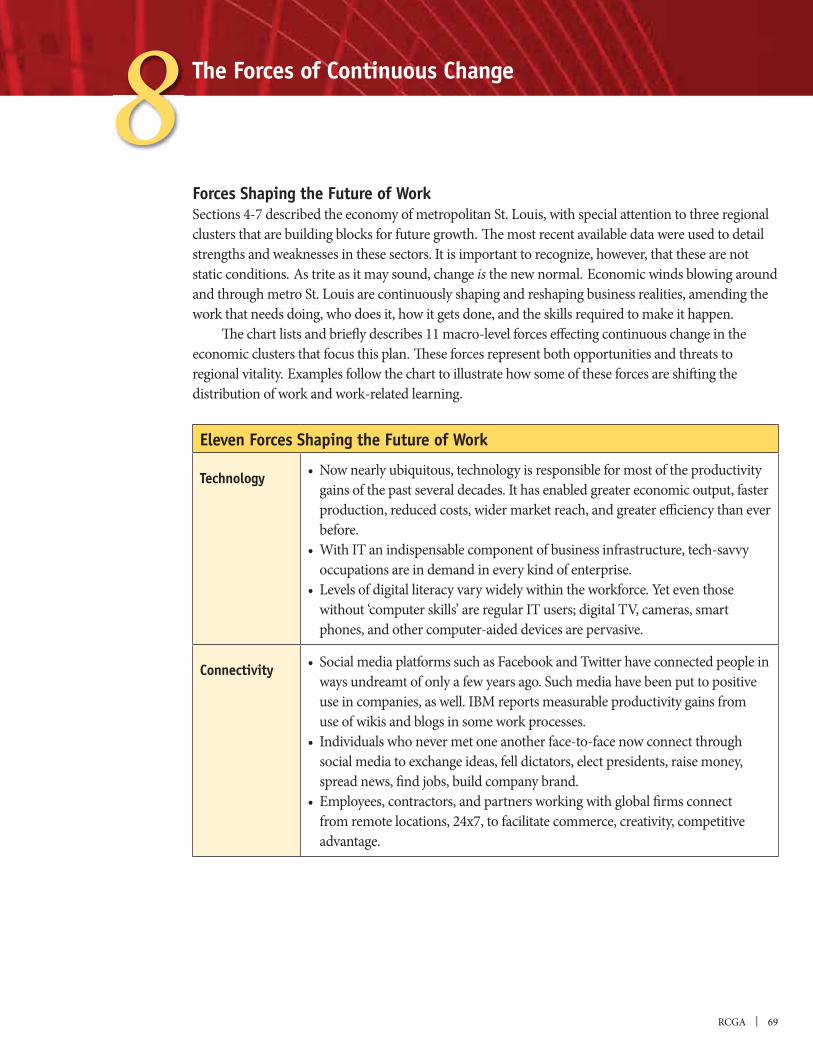

8. The Forces of Continuous Change ....................................................................................................................... 69

9. A New Regional Framework for Talent Development ..................................................................................... 76

10. Leveraging Resources: The Importance of Partnerships ................................................................................100

11. Recommendations .................................................................................................................................................106

Supplemental reports published under separate cover:

St. Louis Regional Chamber & Growth Association

June 2011

The views and opinions expressed in this report are those of the author and do not necessarily represent the views and opinions of the funders or partners.

Talent: The Future of Metro St. Louis in the Knowledge Economy

CHAPTER 1

RCGA | 3

Talented people are capable of many things. They:

Preface

Have developed their “natural ability to do something well” (The Dictionary)

Demonstrate the knowledge, skills, and abilities to perform jobs in demand in today’s economy (O*Net)

Exhibit a “recurring pattern of thought, feeling, or behavior that can be productively applied” in the workplace (Gallup Management Journal)

Are “a good fit” with the culture of the organization or situation in which they work (St. Louis area employers)

Can think creatively (The Economist)

Have a continuing “hunger for learning” (Malcolm Gladwell).

Without talent, the St. Louis metro economy cannot thrive in the competitive global marketplace of which we are a part.

4 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Impacts of the 2007-2009 Recession

reverberated throughout the economy. Many St. Louis area companies quickly evaluated risk and sought to avoid the worst by modifying business plans, changing product lines, reducing labor costs, reorganizing, merging, or—when all else failed—closing their doors. Even the strongest firms battened down the hatches in the face of a global economic storm.

employment peak) and the first quarter of 2010 (its trough), the area lost 78,400 jobs—5.7 percent of its total employment base.1 Although no data base is available to document the origin of all workforce reductions during the Recession, the St. Louis Regional Chamber and Growth Association assembled as much information

layoffs that took place between 2007 and 2009. Five industry sectors accounted for 80 percent of the layoffs: manufacturing (47 percent); financial services (11 percent); pharmaceutical / medical (8 percent); transportation / distribution (7 percent); personal services (7 percent). Among the St. Louis area employers shedding 250 or more workers each were DaimlerChrysler,

job market involuntarily in small groups—two or five or 20 at a time, many without the formalized

The Recession technically at an end, many St. Louis area companies continued to trim employment in response to economic restructuring in 2010 and the first quarter of 2011, although at a slower pace. Government agencies, experiencing the delayed impact of reduced tax revenues, announced significant reductions in force.

The Emerging Recovery

during the Great Recession, recovery has been comparatively sluggish. Among the nation’s 100 largest metro areas, St. Louis ranked 35th in percentage of job loss from peak to low point, but 55th in the rate of recovery between the trough and the fourth quarter of 2010.2

7,000 between April 2010 and April 2011, and the number of unemployed individuals decreased by 15,240. Despite such positive news, the unemployment rate remained high at the end of April 2011: 8.5 percent of the metro labor force, or 122,977 people, were unemployed.3

Today’s Challenges: St. Louis and the Great Recession1

RCGA | 5

CHAPTER 1

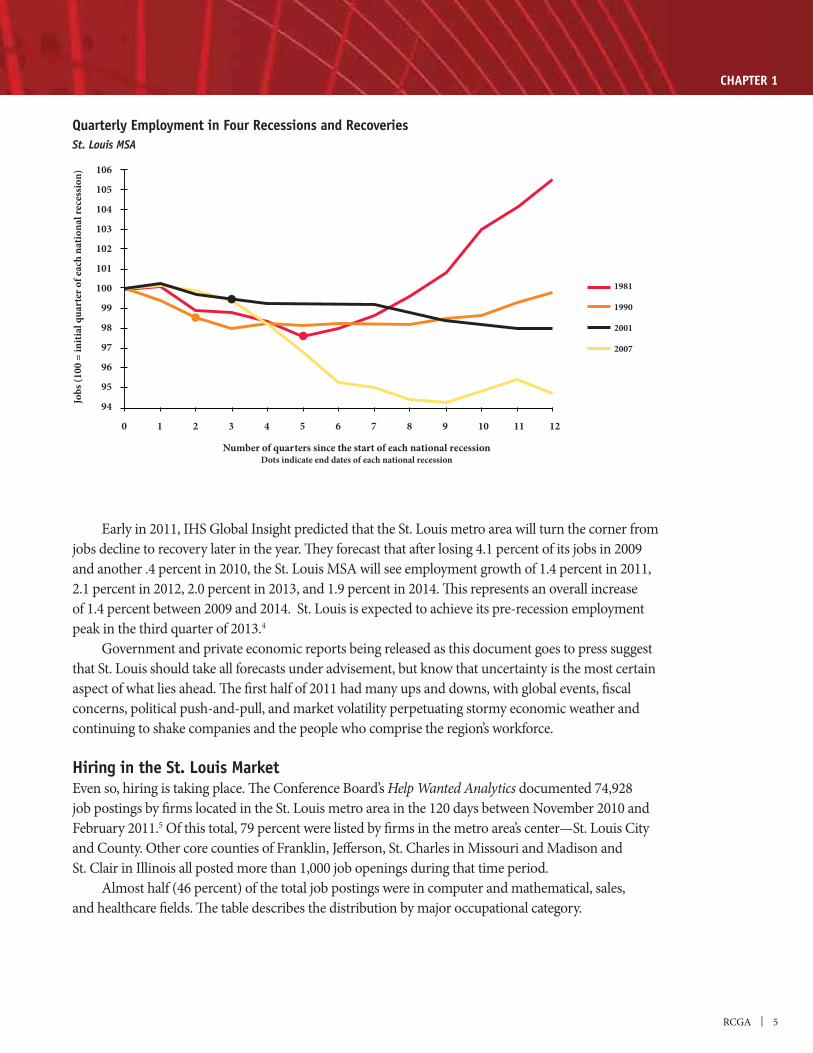

Early in 2011, IHS Global Insight predicted that the St. Louis metro area will turn the corner from jobs decline to recovery later in the year. They forecast that after losing 4.1 percent of its jobs in 2009 and another .4 percent in 2010, the St. Louis MSA will see employment growth of 1.4 percent in 2011, 2.1 percent in 2012, 2.0 percent in 2013, and 1.9 percent in 2014. This represents an overall increase

peak in the third quarter of 2013.4 Government and private economic reports being released as this document goes to press suggest that St. Louis should take all forecasts under advisement, but know that uncertainty is the most certain aspect of what lies ahead. The first half of 2011 had many ups and downs, with global events, fiscal

continuing to shake companies and the people who comprise the region’s workforce.

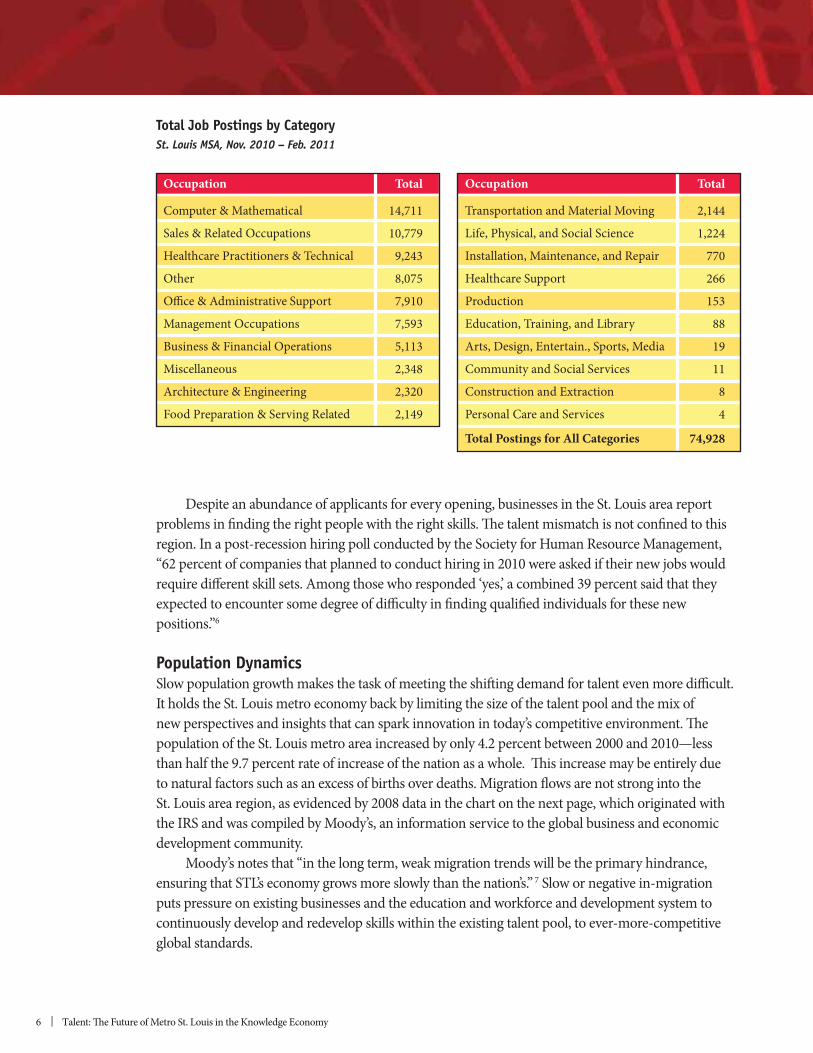

Hiring in the St. Louis MarketHelp Wanted Analytics documented 74,928

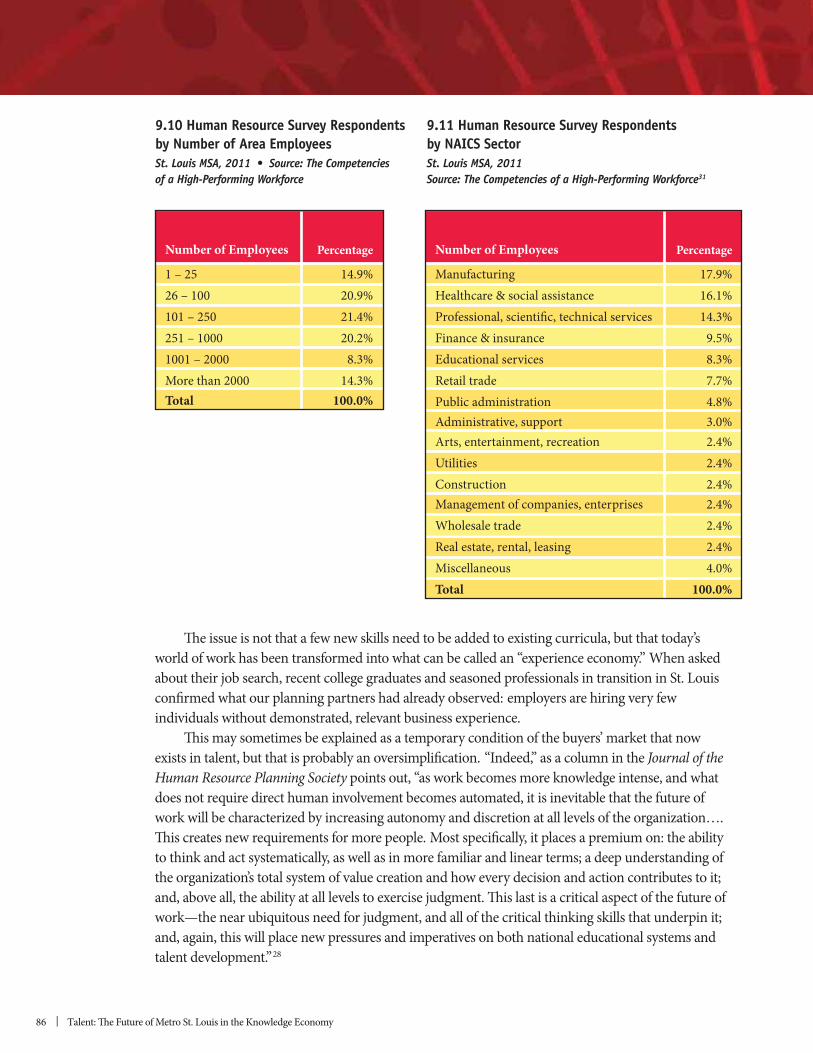

job postings by firms located in the St. Louis metro area in the 120 days between November 2010 and February 2011.5 Of this total, 79 percent were listed by firms in the metro area’s center—St. Louis City and County. Other core counties of Franklin, Jefferson, St. Charles in Missouri and Madison and St. Clair in Illinois all posted more than 1,000 job openings during that time period. Almost half (46 percent) of the total job postings were in computer and mathematical, sales, and healthcare fields. The table describes the distribution by major occupational category.

0 1 2 3 4 5 6 7 8 9 10 11 12

106

105

104

103

102

101

100

99

98

97

96

95

94Jobs

(100

= in

itial

qua

rter

of e

ach

natio

nal r

eces

sion)

Number of quarters since the start of each national recessionDots indicate end dates of each national recession

1981

1990

2001

2007

Quarterly Employment in Four Recessions and RecoveriesSt. Louis MSA

6 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Total

2,144

1,224

770

266

153

88

19

11

8

4

74,928

Occupation

Transportation and Material Moving

Life, Physical, and Social Science

Installation, Maintenance, and Repair

Healthcare Support

Production

Education, Training, and Library

Arts, Design, Entertain., Sports, Media

Community and Social Services

Construction and Extraction

Personal Care and Services

Total Postings for All Categories

Total

14,711

10,779

9,243

8,075

7,910

7,593

5,113

2,348

2,320

2,149

Occupation

Computer & Mathematical

Sales & Related Occupations

Healthcare Practitioners & Technical

Other

Office & Administrative Support

Management Occupations

Business & Financial Operations

Miscellaneous

Architecture & Engineering

Food Preparation & Serving Related

Total Job Postings by CategorySt. Louis MSA, Nov. 2010 – Feb. 2011

Despite an abundance of applicants for every opening, businesses in the St. Louis area report problems in finding the right people with the right skills. The talent mismatch is not confined to this

“62 percent of companies that planned to conduct hiring in 2010 were asked if their new jobs would require different skill sets. Among those who responded ‘yes,’ a combined 39 percent said that they expected to encounter some degree of difficulty in finding qualified individuals for these new positions.”6

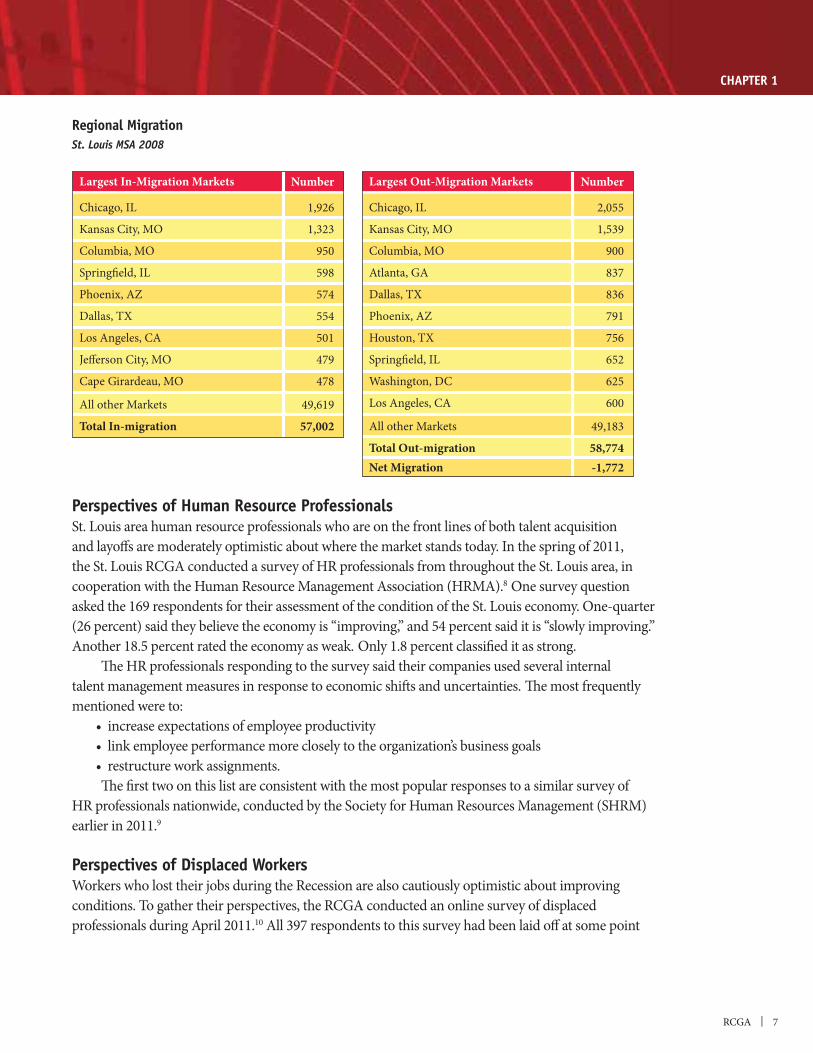

Population DynamicsSlow population growth makes the task of meeting the shifting demand for talent even more difficult. It holds the St. Louis metro economy back by limiting the size of the talent pool and the mix of new perspectives and insights that can spark innovation in today’s competitive environment. The population of the St. Louis metro area increased by only 4.2 percent between 2000 and 2010—less than half the 9.7 percent rate of increase of the nation as a whole. This increase may be entirely due to natural factors such as an excess of births over deaths. Migration flows are not strong into the St. Louis area region, as evidenced by 2008 data in the chart on the next page, which originated with the IRS and was compiled by Moody’s, an information service to the global business and economic development community. Moody’s notes that “in the long term, weak migration trends will be the primary hindrance, ensuring that STL’s economy grows more slowly than the nation’s.” 7

puts pressure on existing businesses and the education and workforce and development system to

global standards.

RCGA | 7

CHAPTER 1

Number

2,055

1,539

900

837

836

791

756

652

625

600

49,183

58,774-1,772

Largest Out-Migration Markets

Chicago, IL

Kansas City, MO

Columbia, MO

Atlanta, GA

Dallas, TX

Phoenix, AZ

Houston, TX

Springfield, IL

Washington, DC

Los Angeles, CA

All other Markets

Total Out-migrationNet Migration

Number

1,926

1,323

950

598

574

554

501

479

478

49,619

57,002

Largest In-Migration Markets

Chicago, IL

Kansas City, MO

Columbia, MO

Springfield, IL

Phoenix, AZ

Dallas, TX

Los Angeles, CA

Jefferson City, MO

Cape Girardeau, MO

All other Markets

Total In-migration

Regional MigrationSt. Louis MSA 2008

Perspectives of Human Resource ProfessionalsSt. Louis area human resource professionals who are on the front lines of both talent acquisition and layoffs are moderately optimistic about where the market stands today. In the spring of 2011, the St. Louis RCGA conducted a survey of HR professionals from throughout the St. Louis area, in cooperation with the Human Resource Management Association (HRMA).8 One survey question

(26 percent) said they believe the economy is “improving,” and 54 percent said it is “slowly improving.” Another 18.5 percent rated the economy as weak. Only 1.8 percent classified it as strong. The HR professionals responding to the survey said their companies used several internal talent management measures in response to economic shifts and uncertainties. The most frequently mentioned were to:

The first two on this list are consistent with the most popular responses to a similar survey of HR professionals nationwide, conducted by the Society for Human Resources Management (SHRM) earlier in 2011.9

Perspectives of Displaced Workers

conditions. To gather their perspectives, the RCGA conducted an online survey of displaced professionals during April 2011.10 All 397 respondents to this survey had been laid off at some point

8 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Less than half (43 percent) of the respondents agreed that the region’s economic outlook is better now than it was one year ago. The percentages varied between those who had gone back to work and

that the economy had improved, compared to 38 percent of those still trying to find new work. The 236 individuals who provided information about the length of time they had been looking for work described a wide range of experiences. Almost 32 percent said that they found work within six months, but another 34 percent looked for more than one year. One of every ten (10.6 percent) indicated that they have been in and out of several jobs during the past three years.

The Future: Strengths, Weaknesses, Opportunities, and Threats

Recession, the sluggish and uncertain recovery, the complex global environment, and slow population growth in St. Louis all represent significant external threats and internal weaknesses for the future.

not been for the region to throw up our collective hands in resignation; rather it has been to chart a new path forward to ensure that the St. Louis metro economy has the talent it needs to fuel a better future—building on the internal strengths and external opportunities we have identified. The rest of this report presents the research, the players, the process, and the learnings that carved that path. Section 2 identifies the business leaders and the many public and private sector partners that formed the core leadership of this planning process. They are among our most important strengths.

talent strategy and how we sought to connect it to the Greater St. Louis Economic Development Plan

the partners, building on key strengths and overcoming the weakness of previously fragmented

Section 3 articulates the vision of a more economically competitive region, names our key competitors in the national marketplace of talent and jobs, and provides baseline numbers for the

of economic vitality’ as a symbol of the inextricable relationship between talent development, job creation, and economic growth and point to the importance of coordinated plans as a foundation for collaboration. Section 4 defines the St. Louis metro economy in terms of population, workforce, employment, and business trends. The three sections that follow provide similar detail about the economic opportunity clusters targeted under this plan: Financial and Information Services (Section 5), Sustainable Technologies (Section 6), and Health Science and Services (Section 7). In these sections,

the fact that our greatest strengths can, in fact, become weaknesses if we do not pay careful attention to the transformation underway inside and external to them.

RCGA | 9

CHAPTER 1

Section 8 identifies 11 macro forces of continuing change that will shape and reshape workforce demand in the near future. These forces are altering the work that we do, who does it, where and how it gets done. They also are driving significant change within the higher education system that prepares

threats to future competitiveness. Section 9 brings together much of what the partners have learned in this planning process and presents an original framework for coordinated talent development. This framework is at the heart of the strategy. It describes the three elements of a great workforce and provides informational tools with which to advance them. It provides a shared reference for business, education, economic development,

Section 10 acknowledges the impact that the economic downturn has had on resources available to support talent development and points to the importance of leveraging existing programs in the

recommendations to advance economic vitality in metro St. Louis’s future. Readers who would like to know more are referred to a series of supplemental reports that have been published as separate documents. They are listed on the Contents page.

______________

1. IHS Global Insight, Inc. Summary of U.S. Metro Unemployment / Employment Forecasts.

Population Survey.” Note that April 2011 rates are preliminary. www.bls.gov/data/#unemployment.

4. IHS Global Insight, Inc. Summary of U.S. Metro Unemployment / Employment Forecasts.

Help Wanted Analytics, accessed by the Missouri Economic Research and Information Center (MERIC), February 24, 2011.

www.shrm.org

Survey of St. Louis Area HR Professionals.” This survey is described in more detail in Section 9, A New Regional Framework for Talent Development, and is available as a supplemental report.

9. Society for Human Resource Management. 2011 Workplace Forecast: The Top Workplace Trends According to HR Professionals. www.shrm.org

10. St. Louis Regional Chamber and Growth Association. “Perspectives of St. Louis Area Professionals Changing Careers in a Turbulent Economy.” May 2011. Available as a supplemental report.

10 | Talent: The Future of Metro St. Louis in the Knowledge Economy

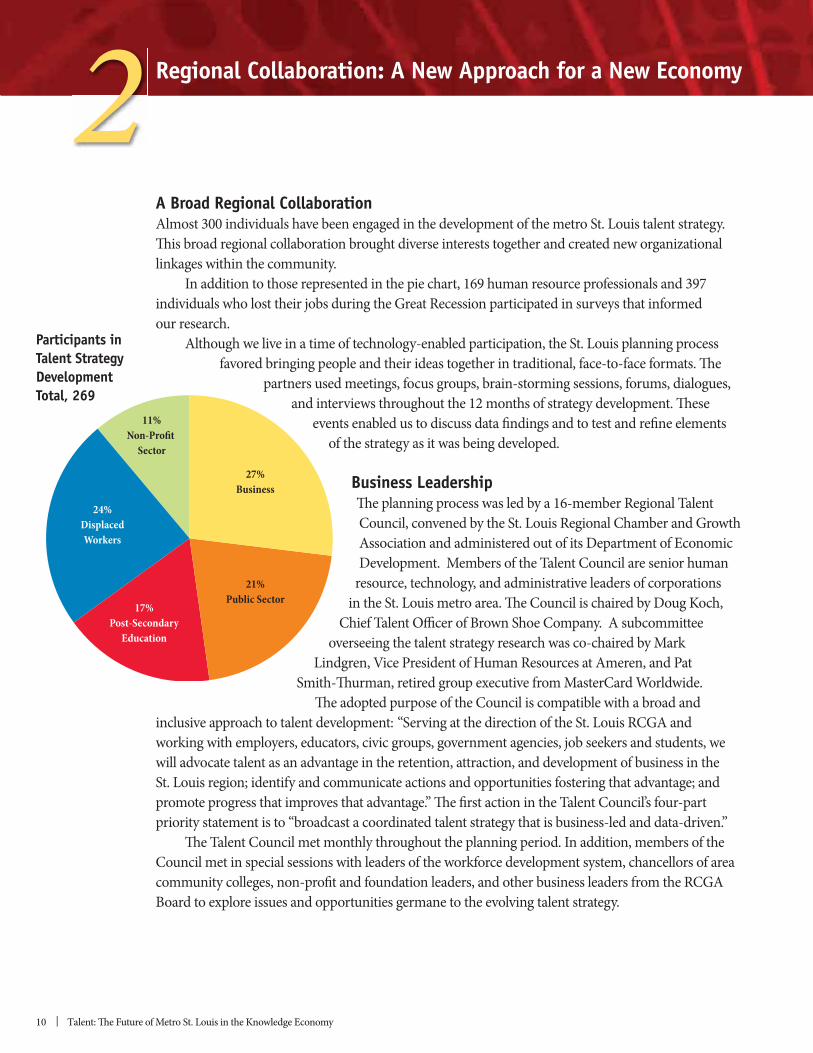

A Broad Regional CollaborationAlmost 300 individuals have been engaged in the development of the metro St. Louis talent strategy. This broad regional collaboration brought diverse interests together and created new organizational linkages within the community.

In addition to those represented in the pie chart, 169 human resource professionals and 397 individuals who lost their jobs during the Great Recession participated in surveys that informed our research.

and interviews throughout the 12 months of strategy development. These events enabled us to discuss data findings and to test and refine elements

of the strategy as it was being developed.

Business Leadership

Council, convened by the St. Louis Regional Chamber and Growth Association and administered out of its Department of Economic Development. Members of the Talent Council are senior human

resource, technology, and administrative leaders of corporations

Lindgren, Vice President of Human Resources at Ameren, and Pat

The adopted purpose of the Council is compatible with a broad and inclusive approach to talent development: “Serving at the direction of the St. Louis RCGA and working with employers, educators, civic groups, government agencies, job seekers and students, we will advocate talent as an advantage in the retention, attraction, and development of business in the St. Louis region; identify and communicate actions and opportunities fostering that advantage; and

The Talent Council met monthly throughout the planning period. In addition, members of the Council met in special sessions with leaders of the workforce development system, chancellors of area

Regional Collaboration: A New Approach for a New Economy2

27%Business

21%Public Sector

17%Post-Secondary

Education

24%DisplacedWorkers

11%Non-Profit

Sector

Participants in Talent Strategy DevelopmentTotal, 269

CHAPTER 2

RCGA | 11

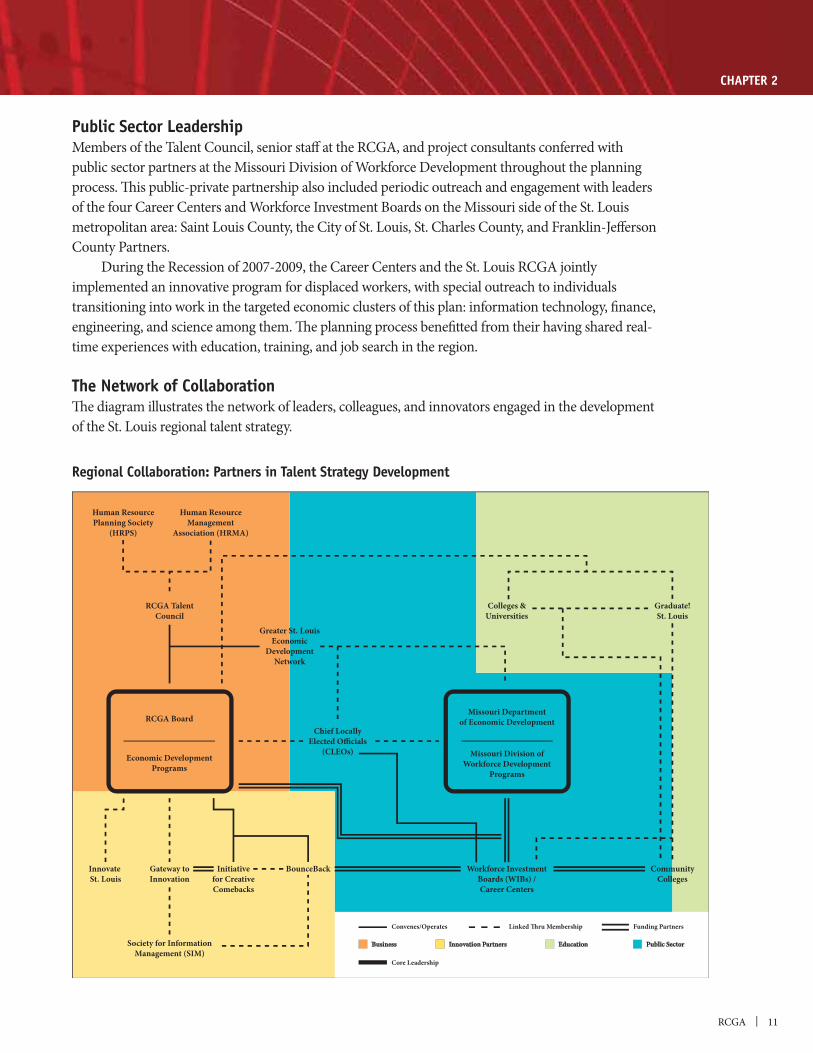

Public Sector LeadershipMembers of the Talent Council, senior staff at the RCGA, and project consultants conferred with

County Partners.

implemented an innovative program for displaced workers, with special outreach to individuals transitioning into work in the targeted economic clusters of this plan: information technology, finance,

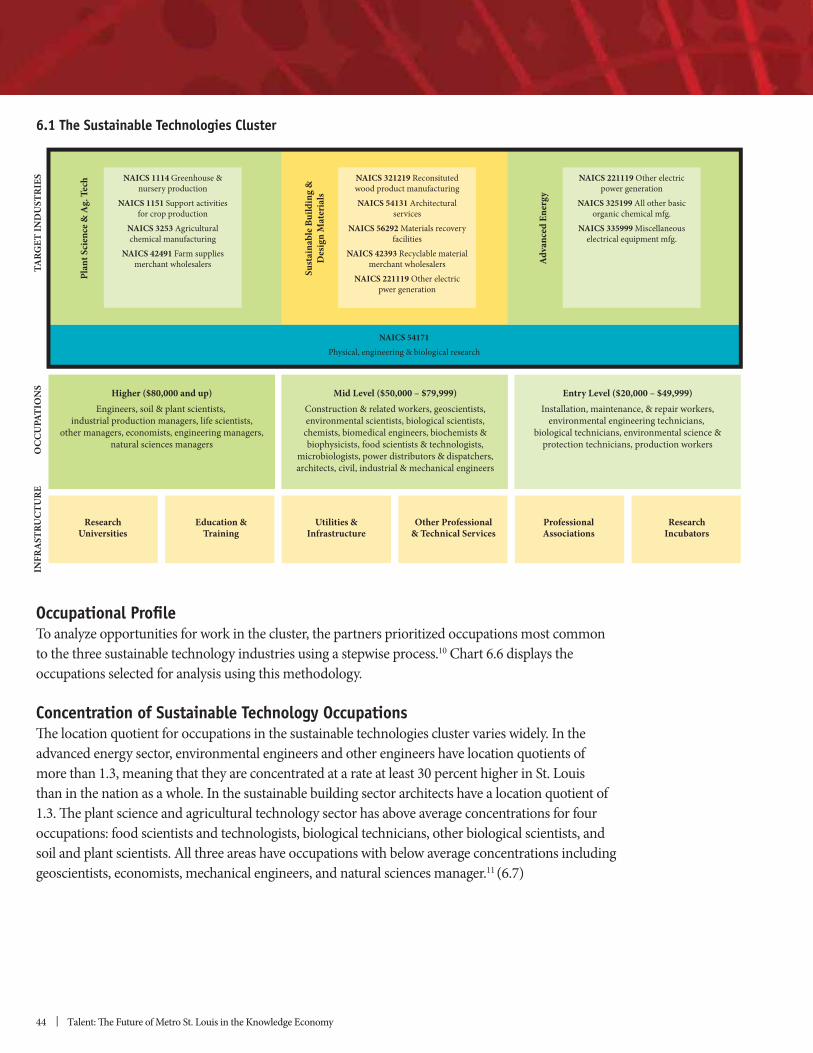

time experiences with education, training, and job search in the region. The Network of CollaborationThe diagram illustrates the network of leaders, colleagues, and innovators engaged in the development of the St. Louis regional talent strategy.

Regional Collaboration: Partners in Talent Strategy Development

Funding PartnersLinked Thru Membership

Core Leadership

Convenes/Operates

Missouri Division ofWorkforce Development

Programs

Missouri Departmentof Economic Development

Economic DevelopmentPrograms

RCGA Board

Colleges &Universities

RCGA TalentCouncil

Human ResourceManagement

Association (HRMA)

Human ResourcePlanning Society

(HRPS)

Greater St. LouisEconomic

DevelopmentNetwork

Initiativefor CreativeComebacks

Innovate St. Louis

Gateway toInnovation

Society for InformationManagement (SIM)

Chief LocallyElected Officials

(CLEOs)

BounceBack CommunityColleges

Workforce InvestmentBoards (WIBs) /Career Centers

Graduate!St. Louis

Public SectorEducationInnovation PartnersBusiness

12 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Talent Development, Job Creation, and Economic Growth:

A Vision and a Virtuous Circle for the Future

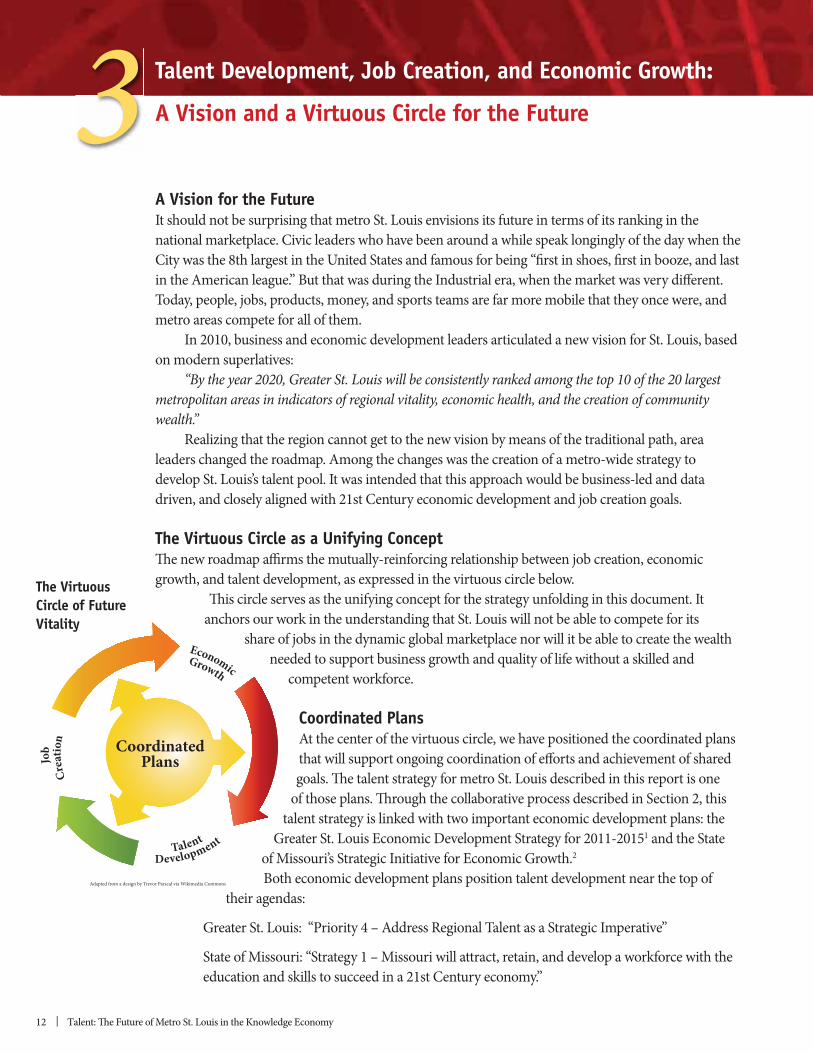

A Vision for the Future It should not be surprising that metro St. Louis envisions its future in terms of its ranking in the national marketplace. Civic leaders who have been around a while speak longingly of the day when the

Today, people, jobs, products, money, and sports teams are far more mobile that they once were, and metro areas compete for all of them. In 2010, business and economic development leaders articulated a new vision for St. Louis, based on modern superlatives: “By the year 2020, Greater St. Louis will be consistently ranked among the top 10 of the 20 largest metropolitan areas in indicators of regional vitality, economic health, and the creation of community wealth.” Realizing that the region cannot get to the new vision by means of the traditional path, area

driven, and closely aligned with 21st Century economic development and job creation goals.

The Virtuous Circle as a Unifying Concept

growth, and talent development, as expressed in the virtuous circle below. This circle serves as the unifying concept for the strategy unfolding in this document. It

anchors our work in the understanding that St. Louis will not be able to compete for its share of jobs in the dynamic global marketplace nor will it be able to create the wealth

needed to support business growth and quality of life without a skilled and competent workforce.

Coordinated PlansAt the center of the virtuous circle, we have positioned the coordinated plans that will support ongoing coordination of efforts and achievement of shared goals. The talent strategy for metro St. Louis described in this report is one

of those plans. Through the collaborative process described in Section 2, this talent strategy is linked with two important economic development plans: the

1 and the State of Missouri’s Strategic Initiative for Economic Growth.2

their agendas:

Greater St. Louis: “Priority 4 – Address Regional Talent as a Strategic Imperative”

State of Missouri: “Strategy 1 – Missouri will attract, retain, and develop a workforce with the education and skills to succeed in a 21st Century economy.”

Adapted from a design by Trevor Parscal via Wikimedia Commons

CoordinatedPlans

DevelopmentTalent

EconomicGrowth

Job

Crea

tion

The Virtuous Circle of Future Vitality

3

RCGA | 13

CHAPTER 3

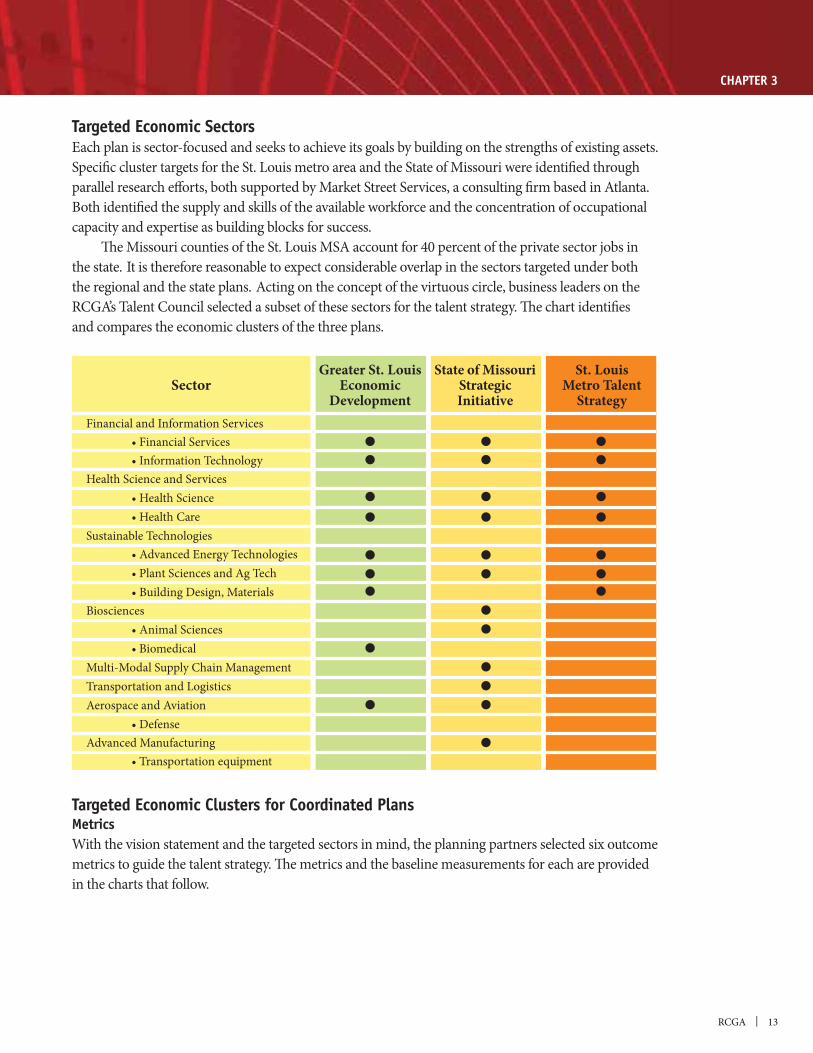

Targeted Economic Sectors

Specific cluster targets for the St. Louis metro area and the State of Missouri were identified through parallel research efforts, both supported by Market Street Services, a consulting firm based in Atlanta.

capacity and expertise as building blocks for success. The Missouri counties of the St. Louis MSA account for 40 percent of the private sector jobs in the state. It is therefore reasonable to expect considerable overlap in the sectors targeted under both the regional and the state plans. Acting on the concept of the virtuous circle, business leaders on the RCGA’s Talent Council selected a subset of these sectors for the talent strategy. The chart identifies and compares the economic clusters of the three plans.

Targeted Economic Clusters for Coordinated PlansMetrics

metrics to guide the talent strategy. The metrics and the baseline measurements for each are provided in the charts that follow.

St. LouisMetro Talent

Strategy

State of MissouriStrategicInitiative

SectorGreater St. Louis

EconomicDevelopment

Financial and Information Services Services Information TechnologyHealth Science and Services Health Science Health CareSustainable Technologies Advanced Energy Technologies t Sciences and Ag Tech Materials

ciences ciences omedicalMulti-Modal Supply Chain ManagementTransportation and LogisticsAerospace and Aviation Advanced Manufacturing Transportation equipment

14 | Talent: The Future of Metro St. Louis in the Knowledge Economy

A growing population ensures an expanding workforce and also serves as an attractor to talented people seeking opportunity in vibrant urban centers. Today, the St. Louis MSA ranks 15th among the nation’s 20 largest metro areas on this measure.

Job creation is key to business growth and the creation of community wealth. Communities where jobs are being created experience greater success in retaining and attracting talented people. Today, the St. Louis MSA ranks 14th among the nation’s 20 largest metro areas on this measure.

35%

30%

25%

20%

15%

10%

5%

0%

-5%

-10%

Rive

rsid

e, C

A

Phoe

nix

Hou

ston

Atla

nta

Dal

las

Was

hing

ton

DC

Tam

pa

Seat

tle

Mia

mi

Min

neap

olis

San

Die

go

Uni

ted

Stat

es

Balti

mor

e

San

Fran

cisc

o

Phila

delp

hia

St. L

ouis

Chi

cago

Los A

ngel

es

Bost

on

New

Yor

k

Det

roit

29.8

%

28.9

%

26.1

%

24.0

%

23.4

%

16.4

%

16.2

%

13.0

%

11.1

%

10.5

%

10.0

%

9.7%

6.2%

5.1%

4.9%

4.2%

4.0%

3.7%

3.7% 3.1%

-3.5

%

Metropolitan Population Growth 3

15%

10%

5%

0%

-5%

-10%

-15%

-20%

-25%

Rive

rsid

e, C

A

Hou

ston

Was

hing

ton

DC

Phoe

nix

Dal

las

San

Die

go

Balti

mor

e

Mia

mi

Seat

tle

New

Yor

k

Atla

nta

Uni

ed S

tate

s

Phila

delp

hia

Min

neap

olis

St. L

ouis

Tam

pa

Bost

on

Los A

ngel

es

Chi

cago

San

Fran

cisc

o

Det

roit

-1.7

%

-1.5

%

-1.3

%

-1.2

%

-0.6

%

1.3%

1.7%

2.2%

3.7%

6.9%

10.7

%12.4

%

12.4

%

-4.4

%

-3.6

%

-3.6

%

-3.3

8%

-21.

4%

-10.

7%

-7.1

%

-6.2

%

Employment Growth 4

RCGA | 15

CHAPTER 3

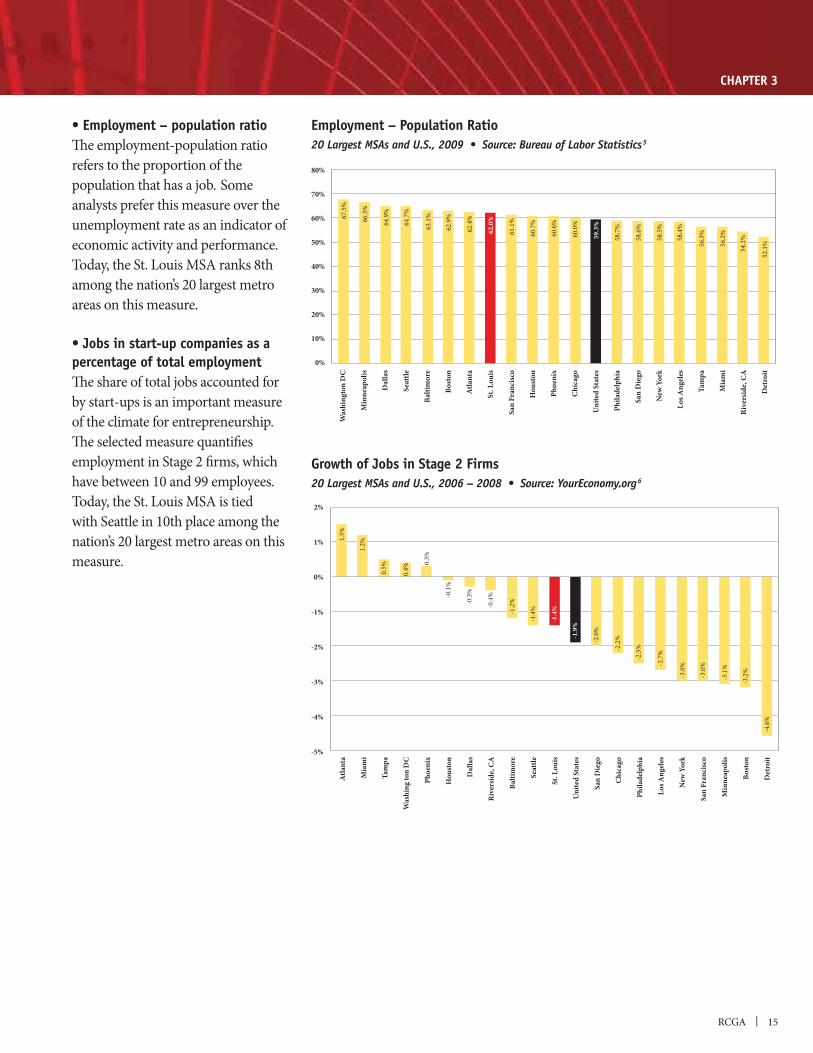

refers to the proportion of the population that has a job. Some analysts prefer this measure over the unemployment rate as an indicator of economic activity and performance. Today, the St. Louis MSA ranks 8th among the nation’s 20 largest metro areas on this measure.

percentage of total employmentThe share of total jobs accounted for

of the climate for entrepreneurship. The selected measure quantifies employment in Stage 2 firms, which have between 10 and 99 employees. Today, the St. Louis MSA is tied with Seattle in 10th place among the nation’s 20 largest metro areas on this measure.

2%

1%

0%

-1%

-2%

-3%

-4%

-5%

Atla

nta

Mia

mi

Tam

pa

Was

hing

ton

DC

Phoe

nix

Hou

ston

Dal

las

Rive

rsid

e, C

A

Balti

mor

e

Seat

tle

St. L

ouis

Uni

ted

Stat

es

San

Die

go

Chi

cago

Phila

delp

hia

Los A

ngel

es

New

Yor

k

San

Fran

cisc

o

Min

neap

olis

Bost

on

Det

roit

1.5%

1.2%

-4.6

%

-3.2

%

-3.1

%

-3.0

%

-3.0

%-2.7

%

-2.5

%-2.2

%-2.0

%

-1.9

%

-1.4

%

-1.4

%-1.2

%-0.4

%

-0.3

%-0.1

%

0.3%

0.4%0.5%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Was

hing

ton

DC

Min

neap

olis

Dal

las

Sea

ttle

Bal

timor

e

Bos

ton

Atla

nta

St.

Loui

s

San

Fra

ncisc

o

Hou

ston

Pho

enix

Chi

cago

Uni

ted

Stat

es

Phi

lade

lphi

a

San

Die

go

New

Yor

k

Los

Ang

eles

Tam

pa

Mia

mi

Riv

ersid

e, C

A

Det

roit

59.3

%

60.0

%

60.6

%

60.7

%

61.1

%

62.0

%

62.4

%

62.9

%

63.1

%

64.7

%

64.9

%

66.3

%

67.5

%

52.1

%

54.2

%

56.2

%

56.3

%

58.4

%

58.5

%

58.6

%

58.7

%

5

Growth of Jobs in Stage 2 Firms 6

16 | Talent: The Future of Metro St. Louis in the Knowledge Economy

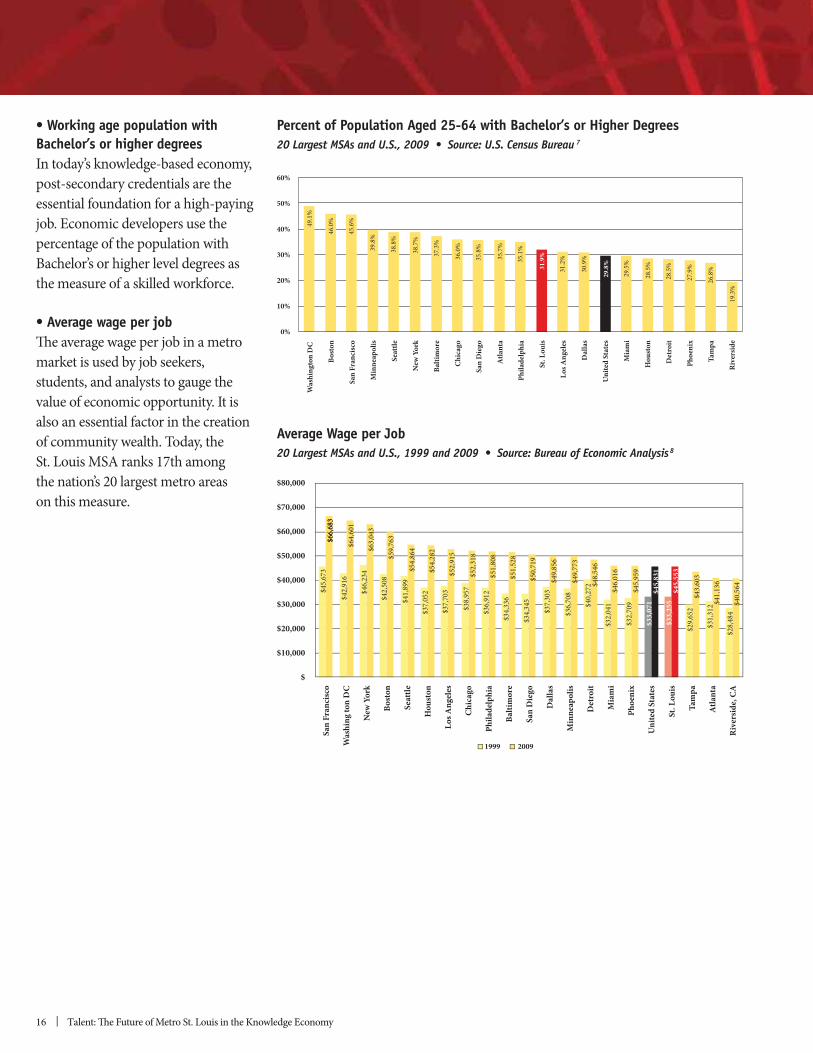

Bachelor’s or higher degrees

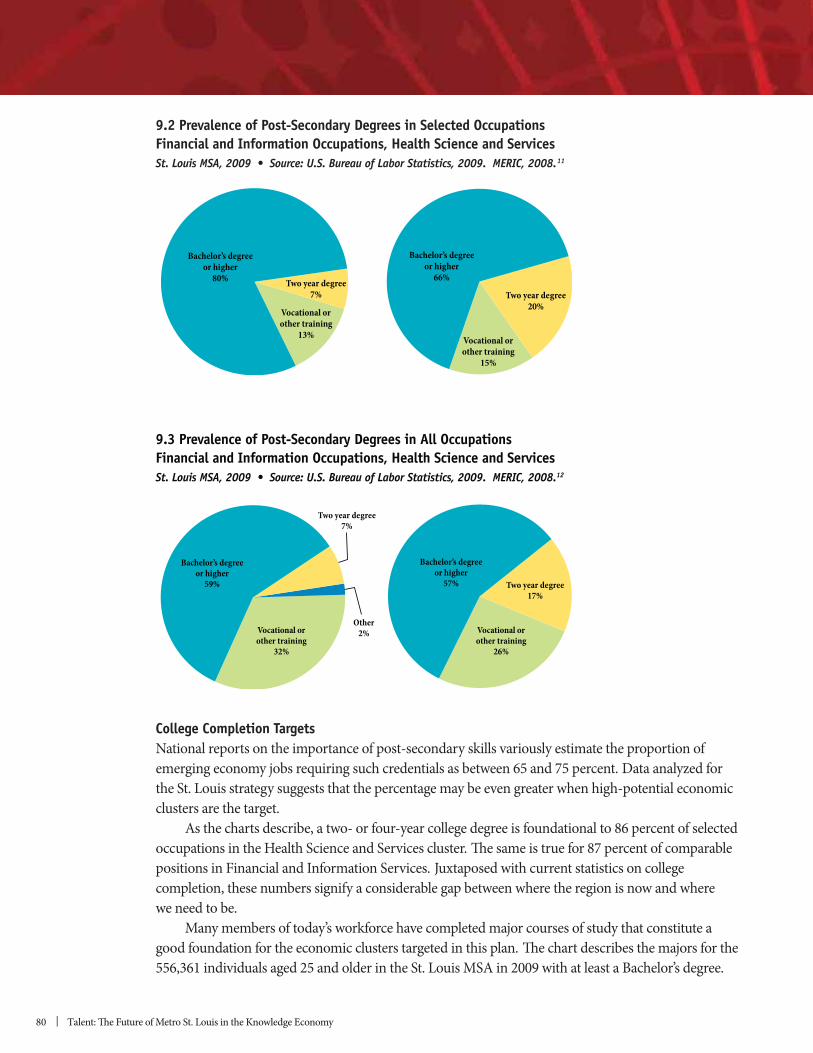

job. Economic developers use the percentage of the population with

the measure of a skilled workforce.

The average wage per job in a metro market is used by job seekers, students, and analysts to gauge the value of economic opportunity. It is also an essential factor in the creation of community wealth. Today, the St. Louis MSA ranks 17th among the nation’s 20 largest metro areas on this measure.

San

Fran

cisc

o

Was

hing

ton

DC

New

Yor

k

Bost

on

Seat

tle

Hou

ston

Los A

ngel

es

Chi

cago

Phila

delp

hia

Balti

mor

e

San

Die

go

Dal

las

Min

neap

olis

Det

roit

Mia

mi

Phoe

nix

Uni

ted

Stat

es

St. L

ouis

Tam

pa

Atla

nta

Rive

rsid

e, C

A

$80,000

$70,000

$60,000

$50,000

$40,000

$30,000

$20,000

$10,000

$

20091999

$45

,673

$66

,683

$42,

916

$46

,234

$42

,508

$41

,899

$37,

052

$37

,703

$38

,957

$36

,912

$34

,336

$34

,345

$37

,303

$36

,708

$40

,272

$32

,041

$32

,709

$33

,071

$33

,255

$29,

652

$31

,312

$28

,484

$64

,601

$63

,043

$59

,763

$54

,864

$54

,282

$52

,915

$52

,318

$66

,683

$51

,808

$51

,528

$50

,719

$49

,856

$49

,773

$48

,546

$46

,016

$45

,959

$45

,831

$45

,553

$43,

603

$41

,136

$40

,564

Was

hing

ton

DC

Bost

on

San

Fran

cisc

o

Min

neap

olis

Seat

tle

New

Yor

k

Balti

mor

e

Chi

cago

San

Die

go

Atla

nta

Phila

delp

hia

St. L

ouis

Los A

ngel

es

Dal

las

Uni

ted

Stat

es

Mia

mi

Hou

ston

Det

roit

Phoe

nix

Tam

pa

Rive

rsid

e

60%

50%

40%

30%

20%

10%

0%

49.1

%

46.0

%

45.6

%

39.8

%

38.8

%

38.7

%

37.3

%

36.0

%

35.8

%

35.7

%

35.1

%

31.9

%

31.2

%

30.9

%

29.8

%

29.5

%

28.5

%

28.5

%

27.9

%

26.8

%

19.3

%

Percent of Population Aged 25-64 with Bachelor’s or Higher Degrees 7

Average Wage per Job 8

RCGA | 17

CHAPTER 3

______________

1. St. Louis RCGA. “Five Core Strategies to Achieve Quality Jobs and Investment.” 2010.

2. Market Street Services, Inc. “Final Report of the Strategic Initiative for Economic Growth: State of Missouri.” 2011.

laugp.htm.

youreconomy.org/pages/ranking/?region=msa, Note: Stage 2 (10-99 employees) — At this phase, a company typically has a proven product, and survival is no longer a daily concern. Companies begin to develop infrastructure and standardize operational systems. Leaders delegate more and wear fewer hats.

acs/www/Products/.

Note: All state and local area dollar estimates are in current dollars (not adjusted for inflation).

18 | Talent: The Future of Metro St. Louis in the Knowledge Economy

The St. Louis Metro Economy

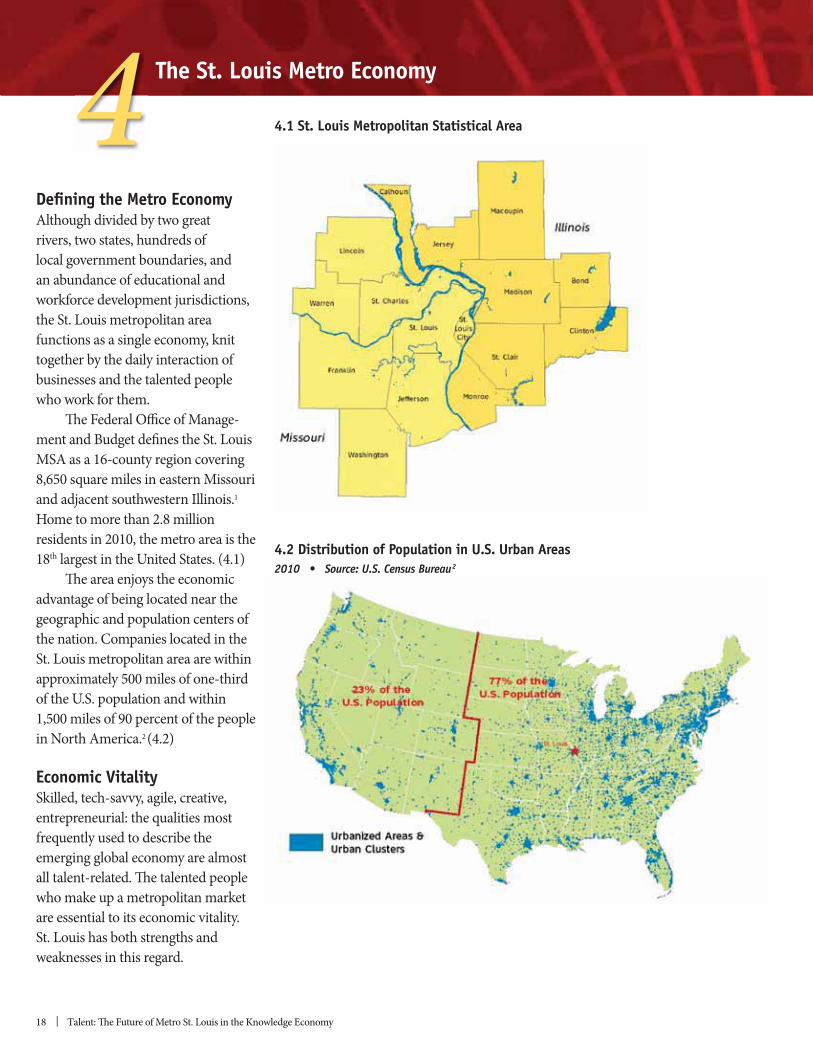

Defining the Metro EconomyAlthough divided by two great rivers, two states, hundreds of local government boundaries, and an abundance of educational and workforce development jurisdictions, the St. Louis metropolitan area functions as a single economy, knit together by the daily interaction of businesses and the talented people who work for them.

8,650 square miles in eastern Missouri and adjacent southwestern Illinois.1 Home to more than 2.8 million residents in 2010, the metro area is the 18th

The area enjoys the economic advantage of being located near the geographic and population centers of the nation. Companies located in the St. Louis metropolitan area are within

1,500 miles of 90 percent of the people in North America.2 (4.2)

Economic Vitality

entrepreneurial: the qualities most frequently used to describe the emerging global economy are almost

who make up a metropolitan market are essential to its economic vitality. St. Louis has both strengths and weaknesses in this regard.

4 4.1 St. Louis Metropolitan Statistical Area

4.2 Distribution of Population in U.S. Urban Areas2

RCGA | 19

CHAPTER 4

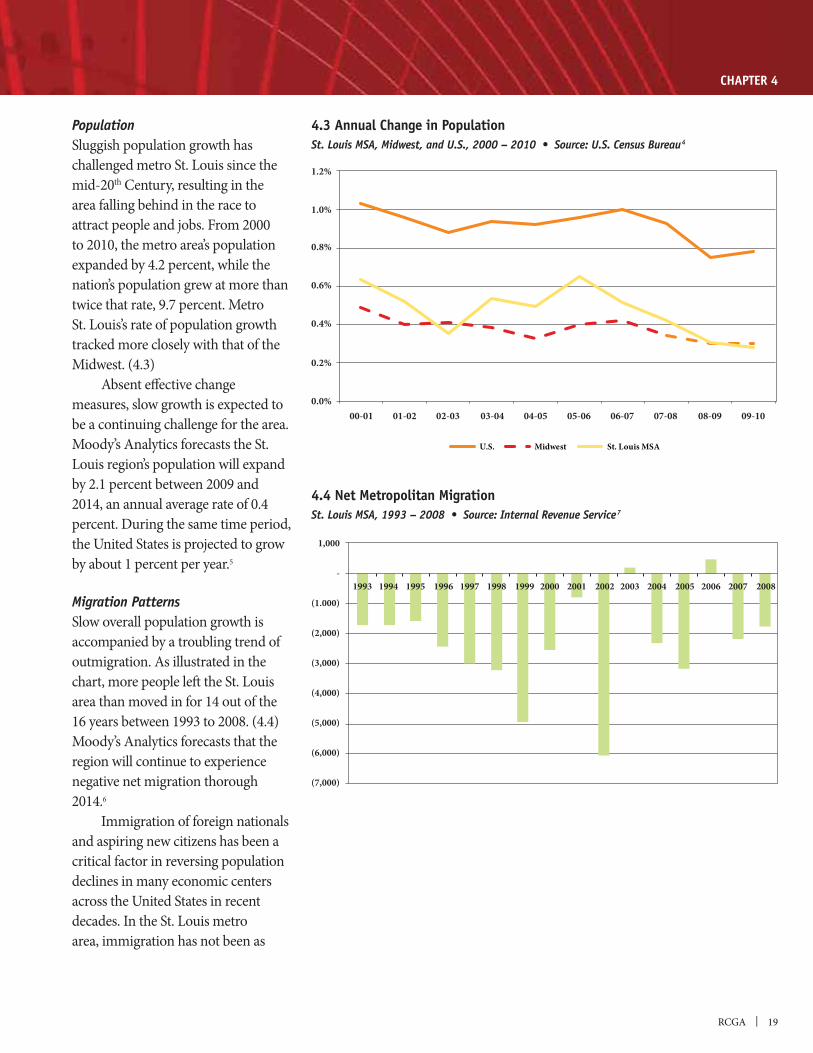

Sluggish population growth has challenged metro St. Louis since the

th Century, resulting in the area falling behind in the race to attract people and jobs. From 2000 to 2010, the metro area’s population expanded by 4.2 percent, while the nation’s population grew at more than twice that rate, 9.7 percent. Metro St. Louis’s rate of population growth tracked more closely with that of the Midwest. (4.3) Absent effective change measures, slow growth is expected to be a continuing challenge for the area. Moody’s Analytics forecasts the St. Louis region’s population will expand by 2.1 percent between 2009 and 2014, an annual average rate of 0.4 percent. During the same time period,

by about 1 percent per year.5

Migration PatternsSlow overall population growth is accompanied by a troubling trend of outmigration. As illustrated in the chart, more people left the St. Louis area than moved in for 14 out of the 16 years between 1993 to 2008. (4.4) Moody’s Analytics forecasts that the region will continue to experience negative net migration thorough 2014.6

Immigration of foreign nationals and aspiring new citizens has been a critical factor in reversing population declines in many economic centers

decades. In the St. Louis metro area, immigration has not been as

U.S. Midwest St. Louis MSA

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

09-1008-0907-0806-0705-0604-0503-0402-0301-0200-01

4.3 Annual Change in Population 4

1,000

-

(1.000)

(2,000)

(3,000)

(4,000)

(5,000)

(6,000)

(7,000)

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

4.4 Net Metropolitan Migration 7

20 | Talent: The Future of Metro St. Louis in the Knowledge Economy

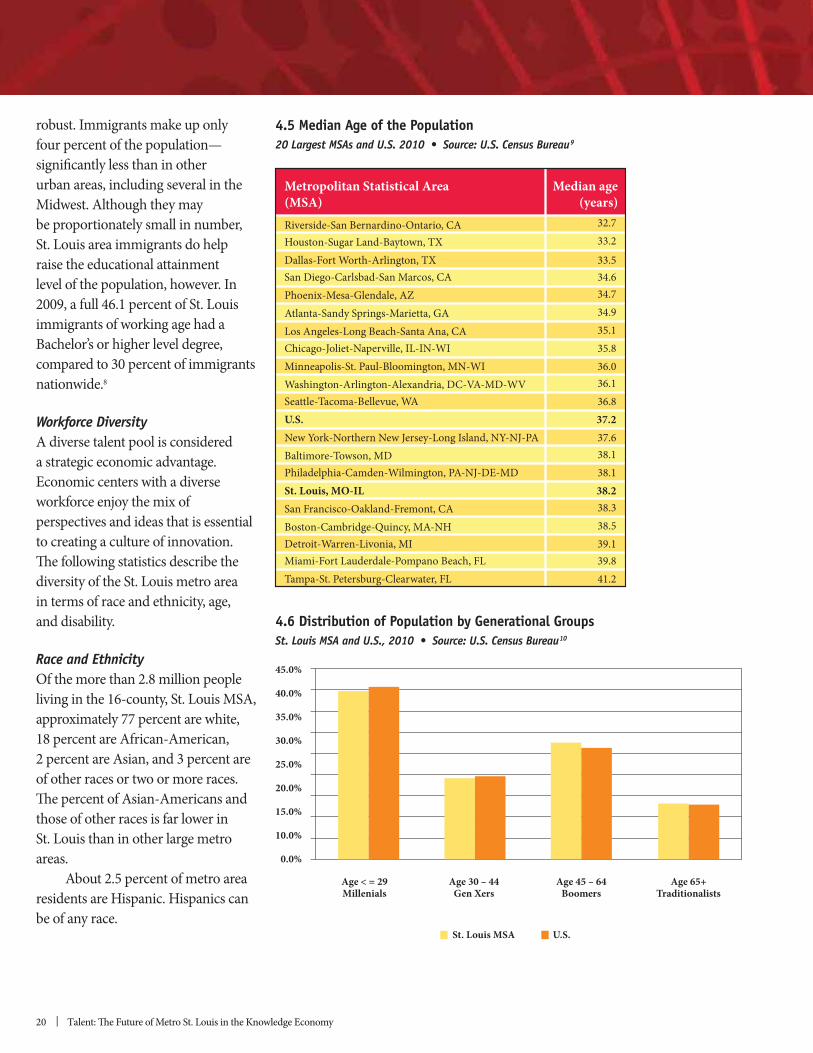

robust. Immigrants make up only four percent of the population—significantly less than in other urban areas, including several in the Midwest. Although they may be proportionately small in number, St. Louis area immigrants do help raise the educational attainment level of the population, however. In 2009, a full 46.1 percent of St. Louis immigrants of working age had a

compared to 30 percent of immigrants nationwide.8

A diverse talent pool is considered a strategic economic advantage. Economic centers with a diverse workforce enjoy the mix of perspectives and ideas that is essential to creating a culture of innovation. The following statistics describe the diversity of the St. Louis metro area in terms of race and ethnicity, age, and disability.

Of the more than 2.8 million people

approximately 77 percent are white,

2 percent are Asian, and 3 percent are of other races or two or more races.

those of other races is far lower in St. Louis than in other large metro areas. About 2.5 percent of metro area residents are Hispanic. Hispanics can be of any race.

Metropolitan Statistical Area(MSA)

Median age(years)

Riverside-San Bernardino-Ontario, CAHouston-Sugar Land-Baytown, TXDallas-Fort Worth-Arlington, TXSan Diego-Carlsbad-San Marcos, CAPhoenix-Mesa-Glendale, AZAtlanta-Sandy Springs-Marietta, GALos Angeles-Long Beach-Santa Ana, CAChicago-Joliet-Naperville, IL-IN-WIMinneapolis-St. Paul-Bloomington, MN-WIWashington-Arlington-Alexandria, DC-VA-MD-WVSeattle-Tacoma-Bellevue, WAU.S.New York-Northern New Jersey-Long Island, NY-NJ-PABaltimore-Towson, MDPhiladelphia-Camden-Wilmington, PA-NJ-DE-MDSt. Louis, MO-ILSan Francisco-Oakland-Fremont, CABoston-Cambridge-Quincy, MA-NHDetroit-Warren-Livonia, MIMiami-Fort Lauderdale-Pompano Beach, FLTampa-St. Petersburg-Clearwater, FL

32.733.2

33.534.634.734.935.135.836.036.136.837.237.638.138.138.238.338.539.139.841.2

4.5 Median Age of the Population 9

Age 65+Traditionalists

45.0%

40.0%

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

0.0%

Age 45 – 64Boomers

Age 30 – 44Gen Xers

Age < = 29Millenials

U.S.St. Louis MSA

4.6 Distribution of Population by Generational Groups 10

RCGA | 21

CHAPTER 4

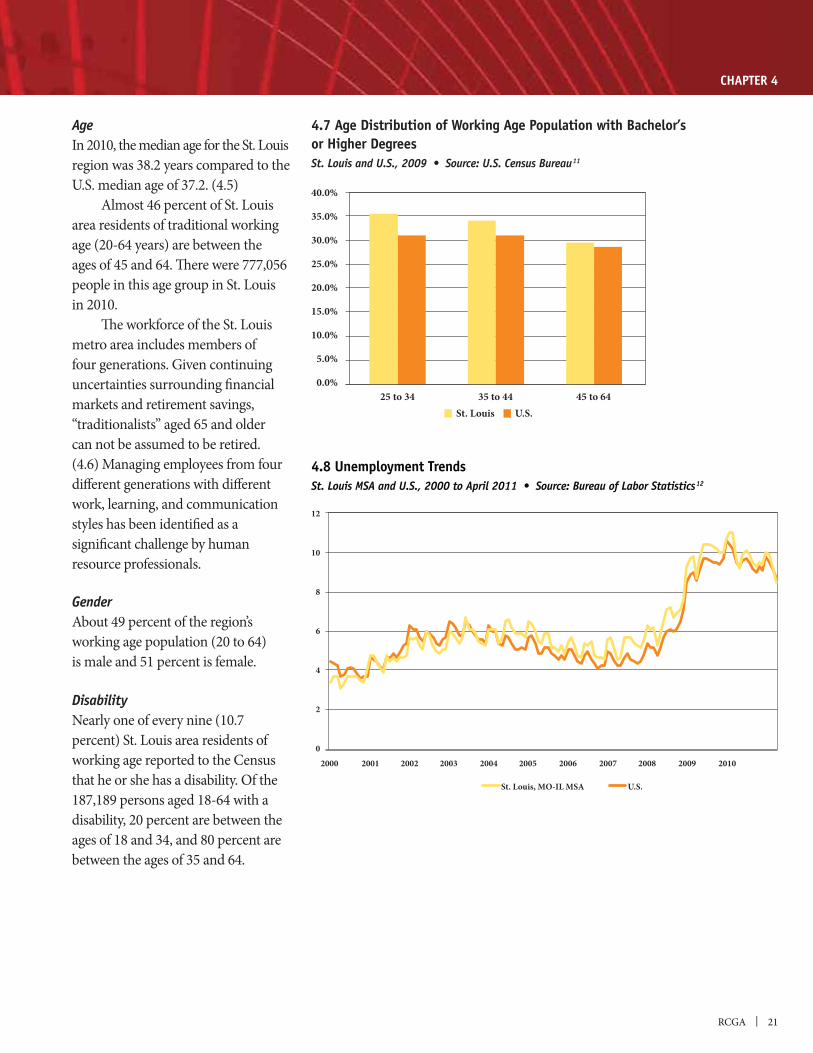

AgeIn 2010, the median age for the St. Louis region was 38.2 years compared to the

Almost 46 percent of St. Louis area residents of traditional working

ages of 45 and 64. There were 777,056 people in this age group in St. Louis in 2010. The workforce of the St. Louis metro area includes members of four generations. Given continuing uncertainties surrounding financial markets and retirement savings, “traditionalists” aged 65 and older can not be assumed to be retired. (4.6) Managing employees from four different generations with different work, learning, and communication styles has been identified as a significant challenge by human resource professionals.

GenderAbout 49 percent of the region’s working age population (20 to 64) is male and 51 percent is female.

Nearly one of every nine (10.7 percent) St. Louis area residents of working age reported to the Census that he or she has a disability. Of the

disability, 20 percent are between the ages of 18 and 34, and 80 percent are between the ages of 35 and 64.

40.0%

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%45 to 6435 to 4425 to 34

U.S.St. Louis

4.7 Age Distribution of Working Age Population with Bachelor’s or Higher Degrees

11

20102009200820072006200520042003200220012000

U.S.St. Louis, MO-IL MSA

12

10

8

6

4

2

0

4.8 Unemployment Trends 12

22 | Talent: The Future of Metro St. Louis in the Knowledge Economy

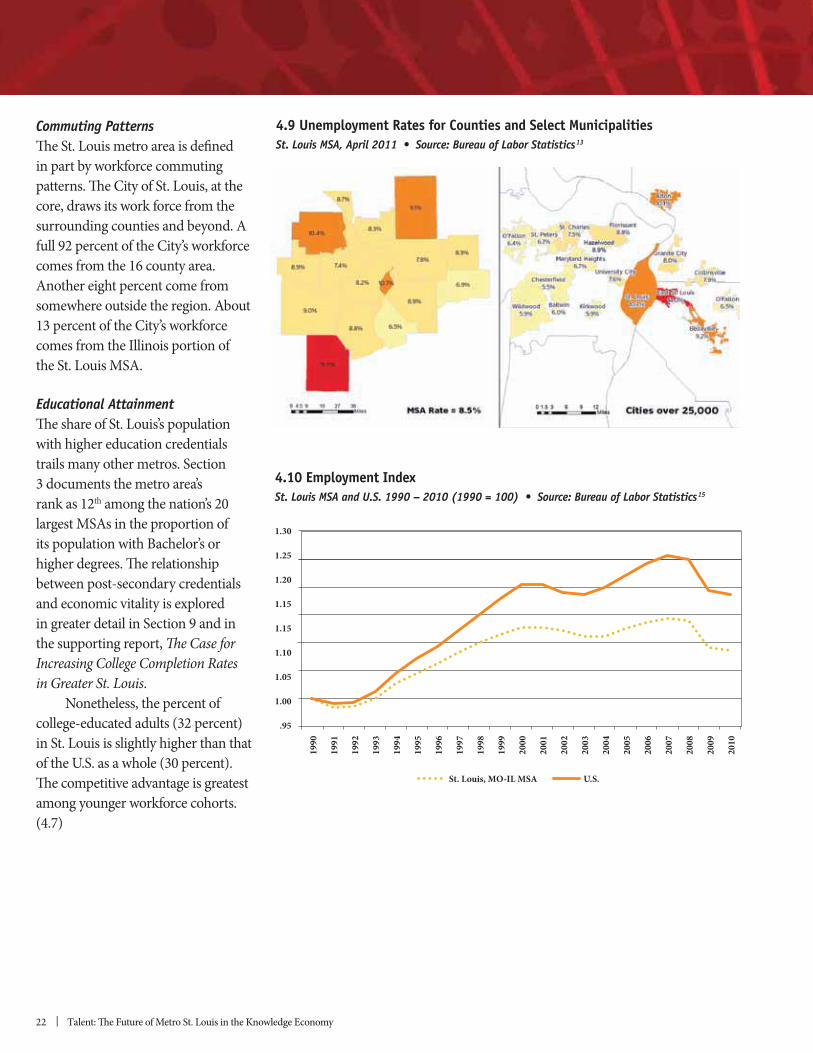

The St. Louis metro area is defined in part by workforce commuting patterns. The City of St. Louis, at the core, draws its work force from the surrounding counties and beyond. A full 92 percent of the City’s workforce comes from the 16 county area. Another eight percent come from somewhere outside the region. About 13 percent of the City’s workforce comes from the Illinois portion of the St. Louis MSA.

The share of St. Louis’s population with higher education credentials trails many other metros. Section 3 documents the metro area’s rank as 12th among the nation’s 20 largest MSAs in the proportion of

higher degrees. The relationship

and economic vitality is explored in greater detail in Section 9 and in the supporting report, The Case for Increasing College Completion Rates in Greater St. Louis. Nonetheless, the percent of

in St. Louis is slightly higher than that

The competitive advantage is greatest among younger workforce cohorts. (4.7)

4.9 Unemployment Rates for Counties and Select Municipalities 13

1.30

1.25

1.20

1.15

1.15

1.10

1.05

1.00

.95

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

U.S.St. Louis, MO-IL MSA

4.10 Employment Index 15

RCGA | 23

CHAPTER 4

Since 2004 the unemployment rate has paralleled but slightly exceeded

area, the highest unemployment rates are found in the urban core and some of the outlying rural counties. (4.9) Labor force participation rates in the region are somewhat higher than the national rates. In 2009, the civilian labor force participation rate was 65.4 percent nationally and 69.3 percent in the St. Louis region.

Economic HealthFollowing population patterns, total employment in metro St. Louis has grown at a considerably slower pace than the nation over the past two decades. The graph shows the area’s employment performance compared to the nation. (4.10) Moody’s Analytics forecasts that jobs will grow at an annual rate of 1.3 percent in St. Louis between 2009 and 2014, compared to an annual rate of 1.6 percent nationally.14

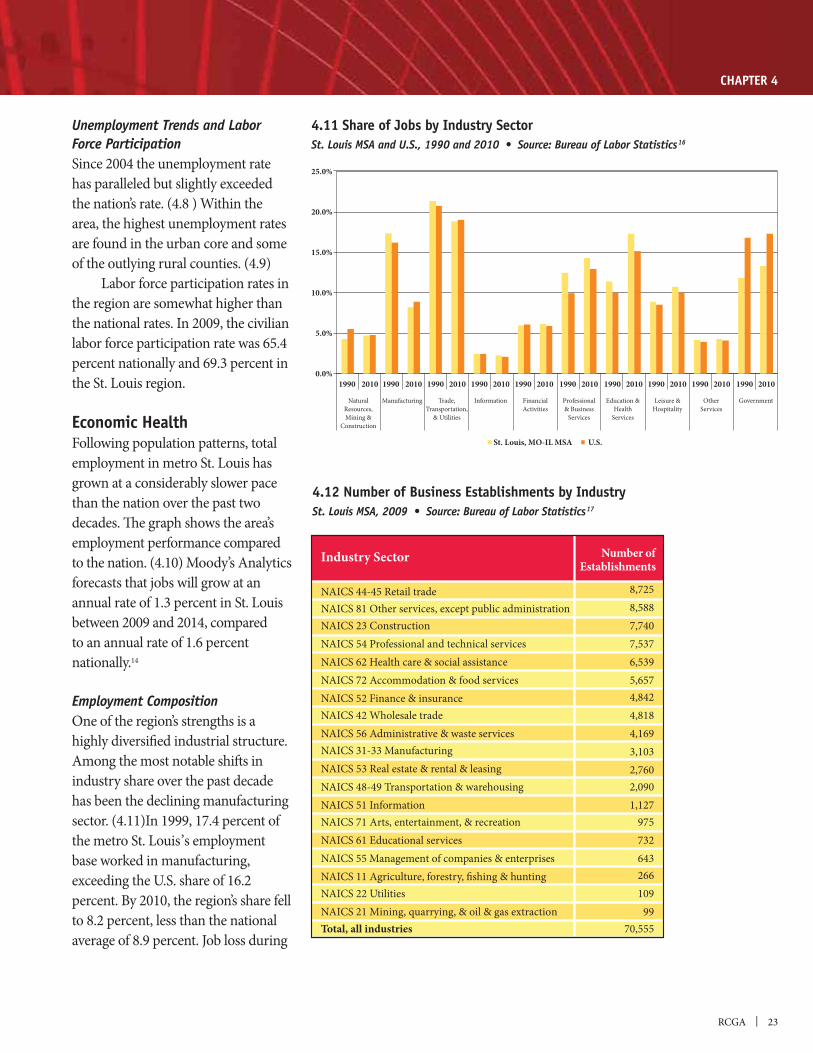

One of the region’s strengths is a highly diversified industrial structure. Among the most notable shifts in industry share over the past decade has been the declining manufacturing sector. (4.11)In 1999, 17.4 percent of the metro St. Louis’s employment base worked in manufacturing,

to 8.2 percent, less than the national average of 8.9 percent. Job loss during

U.S.St. Louis, MO-IL MSA

201019902010199020101990 201019902010199020101990 20101990201019902010199020101990

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

GovernmentOtherServices

Leisure &Hospitality

Education &Health

Services

Professional& Business

Services

FinancialActivities

InformationTrade,Transportation,

& Utilities

ManufacturingNaturalResources,Mining &

Construction

4.11 Share of Jobs by Industry Sector 16

Industry Sector Number ofEstablishments

NAICS 44-45 Retail tradeNAICS 81 Other services, except public administrationNAICS 23 ConstructionNAICS 54 Professional and technical servicesNAICS 62 Health care & social assistanceNAICS 72 Accommodation & food servicesNAICS 52 Finance & insuranceNAICS 42 Wholesale tradeNAICS 56 Administrative & waste servicesNAICS 31-33 ManufacturingNAICS 53 Real estate & rental & leasingNAICS 48-49 Transportation & warehousingNAICS 51 InformationNAICS 71 Arts, entertainment, & recreationNAICS 61 Educational servicesNAICS 55 Management of companies & enterprisesNAICS 11 Agriculture, forestry, fishing & huntingNAICS 22 UtilitiesNAICS 21 Mining, quarrying, & oil & gas extractionTotal, all industries

8,7258,5887,7407,5376,5395,6574,8424,8184,1693,1032,7602,0901,127

975732643266109

9970,555

4.12 Number of Business Establishments by Industry 17

24 | Talent: The Future of Metro St. Louis in the Knowledge Economy

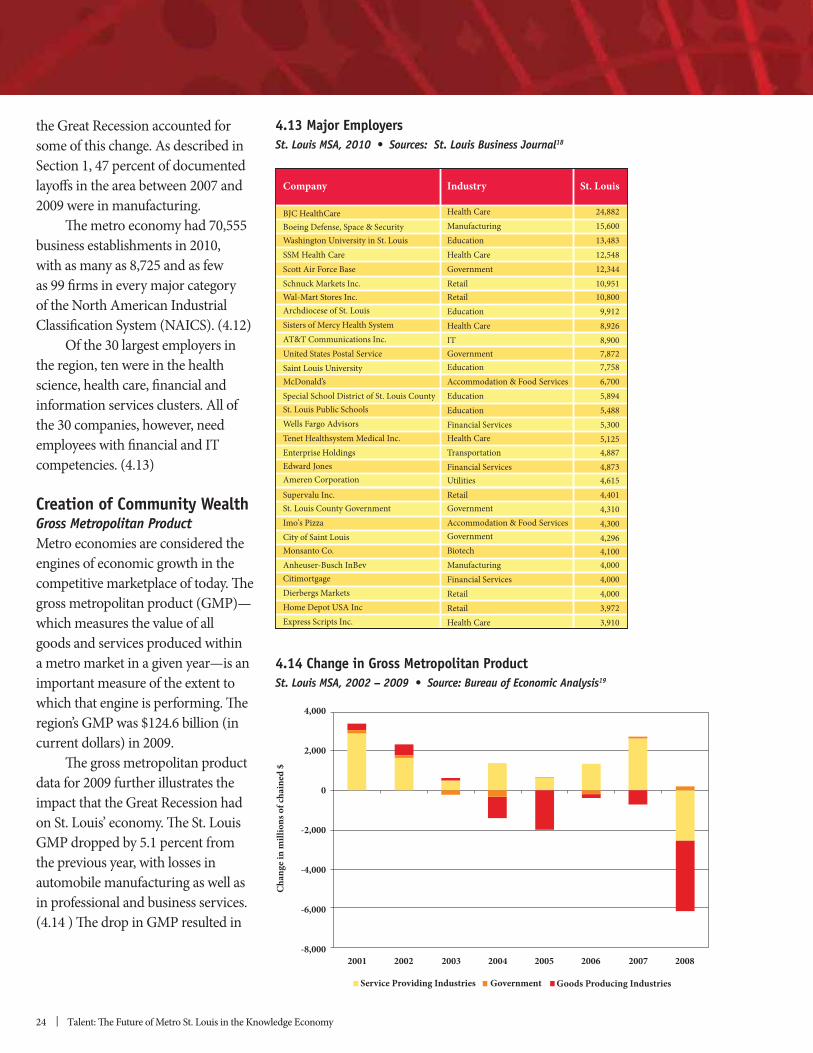

the Great Recession accounted for some of this change. As described in Section 1, 47 percent of documented layoffs in the area between 2007 and 2009 were in manufacturing. The metro economy had 70,555 business establishments in 2010, with as many as 8,725 and as few as 99 firms in every major category of the North American Industrial Classification System (NAICS). (4.12) Of the 30 largest employers in the region, ten were in the health science, health care, financial and information services clusters. All of the 30 companies, however, need employees with financial and IT competencies. (4.13)

Creation of Community Wealth

Metro economies are considered the engines of economic growth in the competitive marketplace of today. The gross metropolitan product (GMP)—which measures the value of all goods and services produced within a metro market in a given year—is an important measure of the extent to which that engine is performing. The region’s GMP was $124.6 billion (in current dollars) in 2009. The gross metropolitan product data for 2009 further illustrates the impact that the Great Recession had on St. Louis’ economy. The St. Louis GMP dropped by 5.1 percent from the previous year, with losses in automobile manufacturing as well as in professional and business services. (4.14 ) The drop in GMP resulted in

4,000

2,000

0

-2,000

-4,000

-6,000

-8,00020082007200620052004200320022001

Goods Producing IndustriesGovernmentService Providing Industries

Chan

ge in

mill

ions

of c

hain

ed $

4.14 Change in Gross Metropolitan Product 19

St. LouisIndustryCompany

BJC HealthCareBoeing Defense, Space & SecurityWashington University in St. LouisSSM Health CareScott Air Force BaseSchnuck Markets Inc.Wal-Mart Stores Inc.Archdiocese of St. LouisSisters of Mercy Health SystemAT&T Communications Inc.United States Postal Service Saint Louis UniversityMcDonald’s Special School District of St. Louis CountySt. Louis Public SchoolsWells Fargo AdvisorsTenet Healthsystem Medical Inc.Enterprise HoldingsEdward Jones Ameren Corporation

Supervalu Inc.St. Louis County GovernmentImo's Pizza City of Saint LouisMonsanto Co. Anheuser-Busch InBev CitimortgageDierbergs MarketsHome Depot USA Inc Express Scripts Inc.

Health CareManufacturingEducationHealth CareGovernmentRetailRetailEducationHealth CareITGovernmentEducationAccommodation & Food ServicesEducationEducationFinancial ServicesHealth CareTransportationFinancial ServicesUtilitiesRetailGovernmentAccommodation & Food ServicesGovernmentBiotechManufacturingFinancial ServicesRetailRetailHealth Care

24,88215,60013,48312,54812,34410,95110,800

9,9128,9268,9007,8727,7586,7005,8945,4885,3005,1254,8874,8734,6154,4014,3104,3004,2964,1004,0004,0004,0003,9723,910

18

RCGA | 25

CHAPTER 4

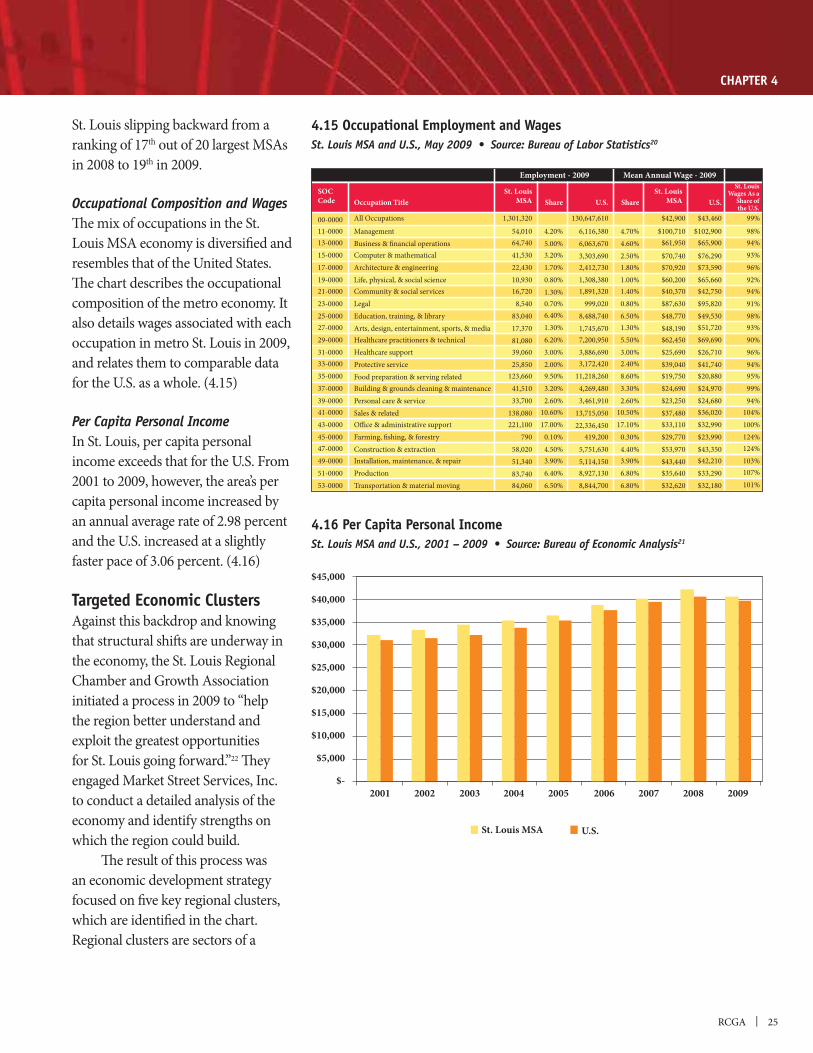

St. Louis slipping backward from a ranking of 17th out of 20 largest MSAs in 2008 to 19th in 2009.

The mix of occupations in the St. Louis MSA economy is diversified and

The chart describes the occupational composition of the metro economy. It also details wages associated with each occupation in metro St. Louis in 2009, and relates them to comparable data

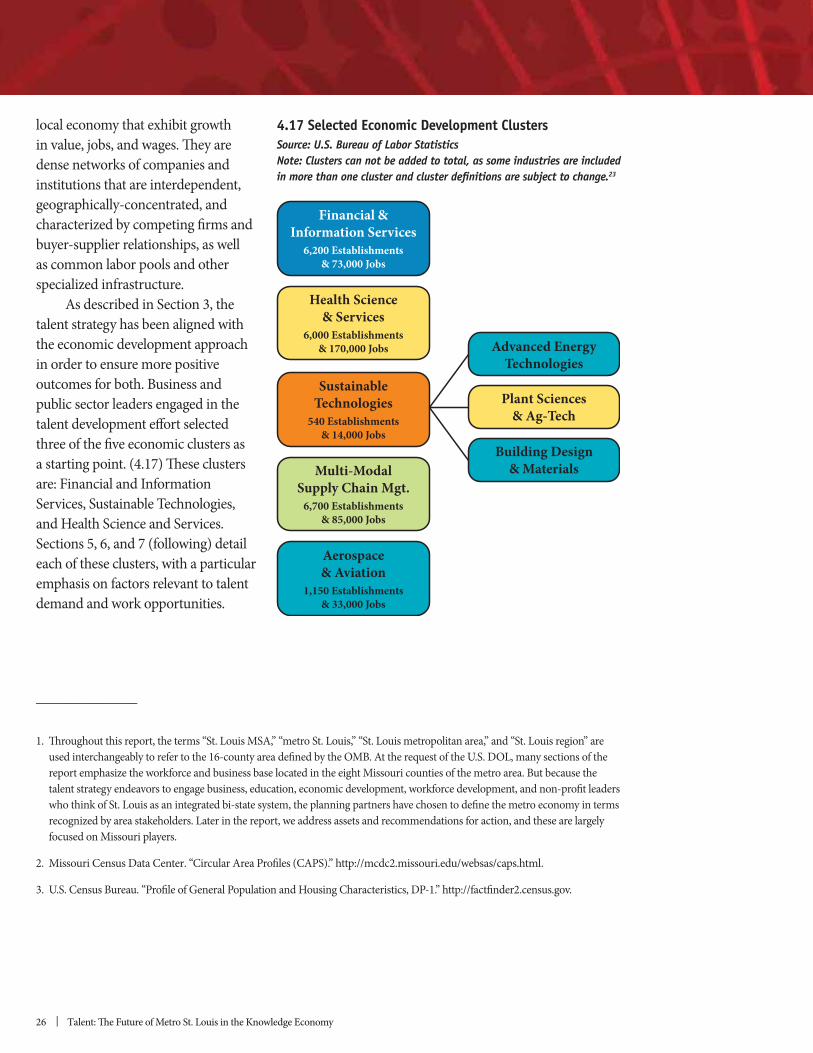

In St. Louis, per capita personal

2001 to 2009, however, the area’s per capita personal income increased by an annual average rate of 2.98 percent

faster pace of 3.06 percent. (4.16)

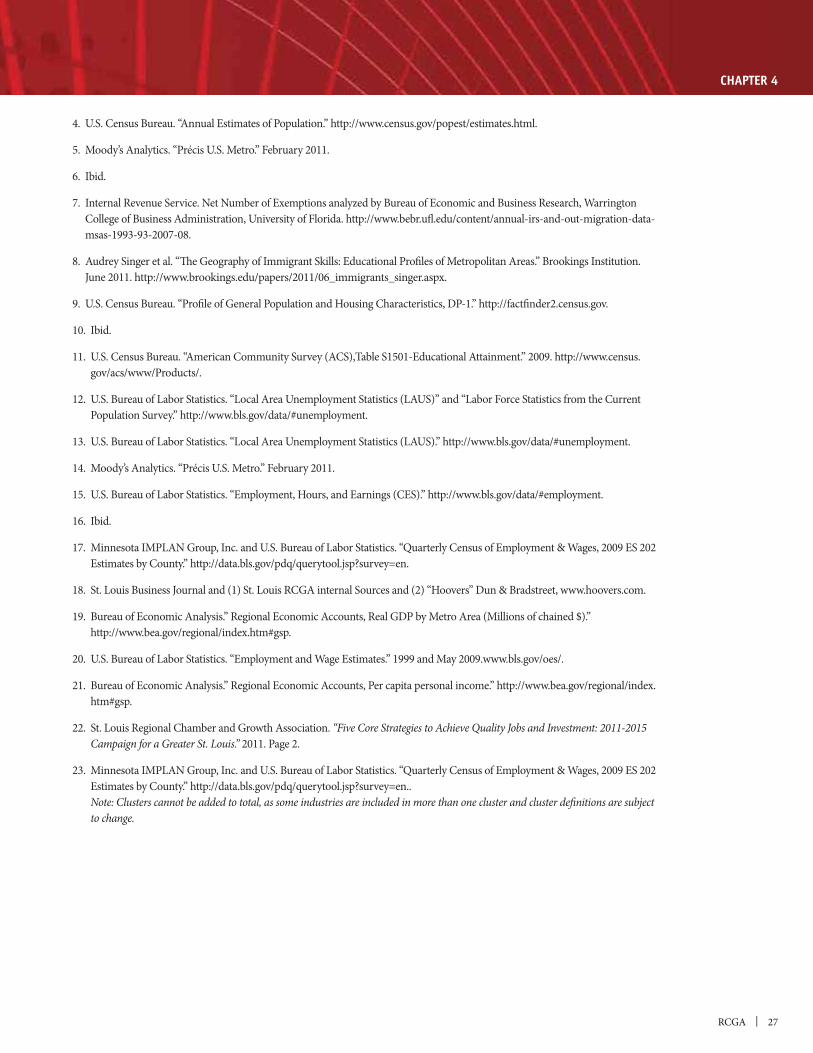

Targeted Economic ClustersAgainst this backdrop and knowing that structural shifts are underway in the economy, the St. Louis Regional Chamber and Growth Association initiated a process in 2009 to “help the region better understand and exploit the greatest opportunities for St. Louis going forward.”22 They engaged Market Street Services, Inc. to conduct a detailed analysis of the economy and identify strengths on which the region could build. The result of this process was an economic development strategy focused on five key regional clusters, which are identified in the chart. Regional clusters are sectors of a

St. LouisWages As a

Share ofthe U.S.

St. LouisMSA

St. LouisMSA U.S.ShareU.S.ShareOccupation Title

SOCCode

00-000011-000013-000015-000017-000019-000021-000023-000025-000027-000029-000031-000033-000035-000037-000039-000041-000043-000045-000047-000049-000051-000053-0000

All Occupations

Management Business & financial operationsComputer & mathematicalArchitecture & engineering Life, physical, & social science Community & social services Legal Education, training, & library Arts, design, entertainment, sports, & media Healthcare practitioners & technical Healthcare support Protective service Food preparation & serving related Building & grounds cleaning & maintenance Personal care & service Sales & related Office & administrative support Farming, fishing, & forestry Construction & extraction Installation, maintenance, & repair Production Transportation & material moving

99%

98%94%93%96%92%94%91%98%93%90%96%94%95%99%94%

104%100%124%124%103%107%101%

$43,460

$102,900$65,900

$76,290$73,590$65,660$42,750$95,820$49,530$51,720$69,690$26,710$41,740$20,880$24,970$24,680$36,020$32,990$23,990$43,350$42,210$33,290$32,180

$42,900

$100,710$61,950

$70,740$70,920$60,200$40,370$87,630$48,770$48,190$62,450$25,690$39,040$19,750$24,690$23,250$37,480$33,110$29,770$53,970$43,440$35,640$32,620

130,647,610

6,116,3806,063,6703,303,6902,412,7301,308,3801,891,320

999,0208,488,7401,745,6707,200,9503,886,6903,172,420

11,218,2604,269,4803,461,910

13,715,05022,336,450

419,2005,751,6305,114,1508,927,1308,844,700

4.70%4.60%2.50%1.80%1.00%1.40%0.80%6.50%1.30%5.50%3.00%2.40%8.60%3.30%2.60%

10.50%17.10%

0.30%4.40%3.90%6.80%6.80%

4.20%5.00%3.20%1.70%0.80%1.30%0.70%6.40%1.30%6.20%3.00%2.00%9.50%3.20%2.60%

10.60%17.00%

0.10%4.50%3.90%6.40%6.50%

1,301,320

54,01064,74041,53022,43010,93016,720

8,54083,04017,37081,08039,06025,850

123,66041,51033,700

138,080221,100

79058,02051,34083,74084,060

Employment - 2009 Mean Annual Wage - 2009

4.15 Occupational Employment and Wages 20

U.S.St. Louis MSA

$45,000

$40,000

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$-200920082007200620052004200320022001

4.16 Per Capita Personal Income 21

26 | Talent: The Future of Metro St. Louis in the Knowledge Economy

local economy that exhibit growth in value, jobs, and wages. They are dense networks of companies and institutions that are interdependent,

characterized by competing firms and

as common labor pools and other specialized infrastructure. As described in Section 3, the talent strategy has been aligned with the economic development approach in order to ensure more positive

public sector leaders engaged in the talent development effort selected three of the five economic clusters as a starting point. (4.17) These clusters are: Financial and Information Services, Sustainable Technologies, and Health Science and Services. Sections 5, 6, and 7 (following) detail each of these clusters, with a particular emphasis on factors relevant to talent demand and work opportunities.

______________

1. Throughout this report, the terms “St. Louis MSA,” “metro St. Louis,” “St. Louis metropolitan area,” and “St. Louis region” are

recognized by area stakeholders. Later in the report, we address assets and recommendations for action, and these are largely focused on Missouri players.

2. Missouri Census Data Center. “Circular Area Profiles (CAPS).” http://mcdc2.missouri.edu/websas/caps.html.

Building Design& Materials

Plant Sciences& Ag-Tech

Advanced EnergyTechnologies

Aerospace& Aviation

1,150 Establishments& 33,000 Jobs

Multi-ModalSupply Chain Mgt.

6,700 Establishments& 85,000 Jobs

SustainableTechnologies

540 Establishments& 14,000 Jobs

Health Science& Services

6,000 Establishments& 170,000 Jobs

Financial &Information Services

6,200 Establishments& 73,000 Jobs

4.17 Selected Economic Development Clusters

23

RCGA | 27

CHAPTER 4

6. Ibid.

June 2011. http://www.brookings.edu/papers/2011/06_immigrants_singer.aspx.

10. Ibid.

gov/acs/www/Products/.

Population Survey.” http://www.bls.gov/data/#unemployment.

16. Ibid.

Estimates by County.” http://data.bls.gov/pdq/querytool.jsp?survey=en.

http://www.bea.gov/regional/index.htm#gsp.

htm#gsp.

22. St. Louis Regional Chamber and Growth Association. “Five Core Strategies to Achieve Quality Jobs and Investment: 2011-2015 Campaign for a Greater St. Louis.” 2011. Page 2.

Estimates by County.” http://data.bls.gov/pdq/querytool.jsp?survey=en.. Note: Clusters cannot be added to total, as some industries are included in more than one cluster and cluster definitions are subject to change.

28 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Opportunity: Financial and Information Services

IntroductionThe financial and information services cluster operates at the core of the 21st Century global economy, where the most competitive firms use the most sophisticated digital technologies to count, manage, secure, move, and account for money and information with amazing speed and accuracy. In the events leading up to the Great Recession, this cluster was not only at the core of the economy, but at the center of the storm.

Today, a number of external trends are influencing both finance and IT, with implications for the talent that is needed now and in the future. A select few of them are listed below.

geopolitical boundaries. Events in one part of the world have ramifications for what happens in others—for better or for worse.

computer security specialists are in high demand.

financial services industry, meaning that there are fewer purely local enterprises and many talent management decisions are made outside the local area.

Many of these will soon be replaced by other technologies, including biometrics.

individuals with credentialed specializations.

demand for talented people who can understand, monitor, and advise on regulatory compliance issues.

partnerships between depository institutions and retail outlets (banks, grocery stores and malls, for

5

RCGA | 29

CHAPTER 5

young people raised with digital tools; older people with paper checkbooks and fixed incomes;

corporations; and everyone in between.

systems toward shared and leased services, such as those provided in “The Cloud.” The Cloud allows businesses and individuals to access applications, content, and computing power remotely through

vendors—locally, nationally, and internationally.

skills, but, as will be discussed more fully in Section 9, having the right technical skills will not be sufficient to launch a successful career in the financial and information services cluster today. Looking

different set of skills, smart deployment of talent and the realignment of compensation structures will be critical to their ability to address the demands of this new world financial order…. Companies are looking to ascertain whether they have enough people with the necessary balance of innovation, risk, compliance, and relationship skills, and gearing their training and recruitment to bridging any gaps.” 1

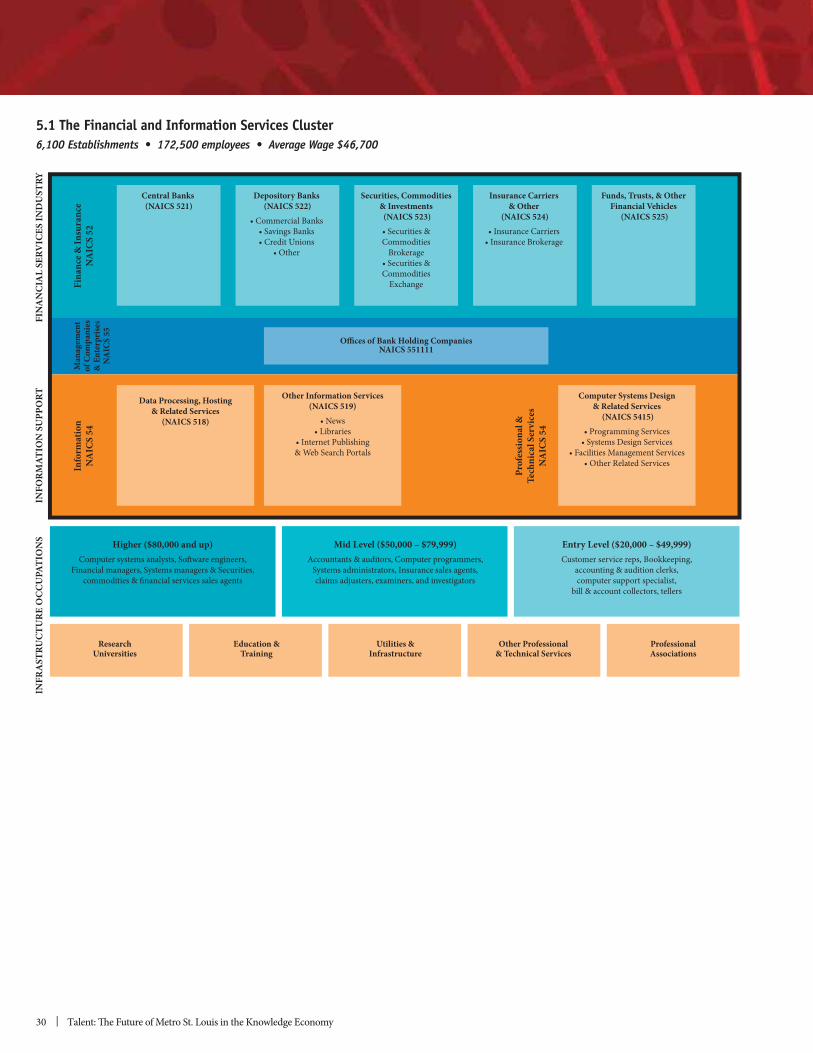

Definition of Financial and Information Services ClusterThe financial services sector is comprised of banks; securities, commodities, and investment firms; insurance carriers; funds, trusts, and other financial vehicles; and bank holding companies. The information services sector includes companies that host and process data and those that design and manage IT systems and services. (5.1) The financial services sector accounted for 5.6 percent of total employment in metro St. Louis

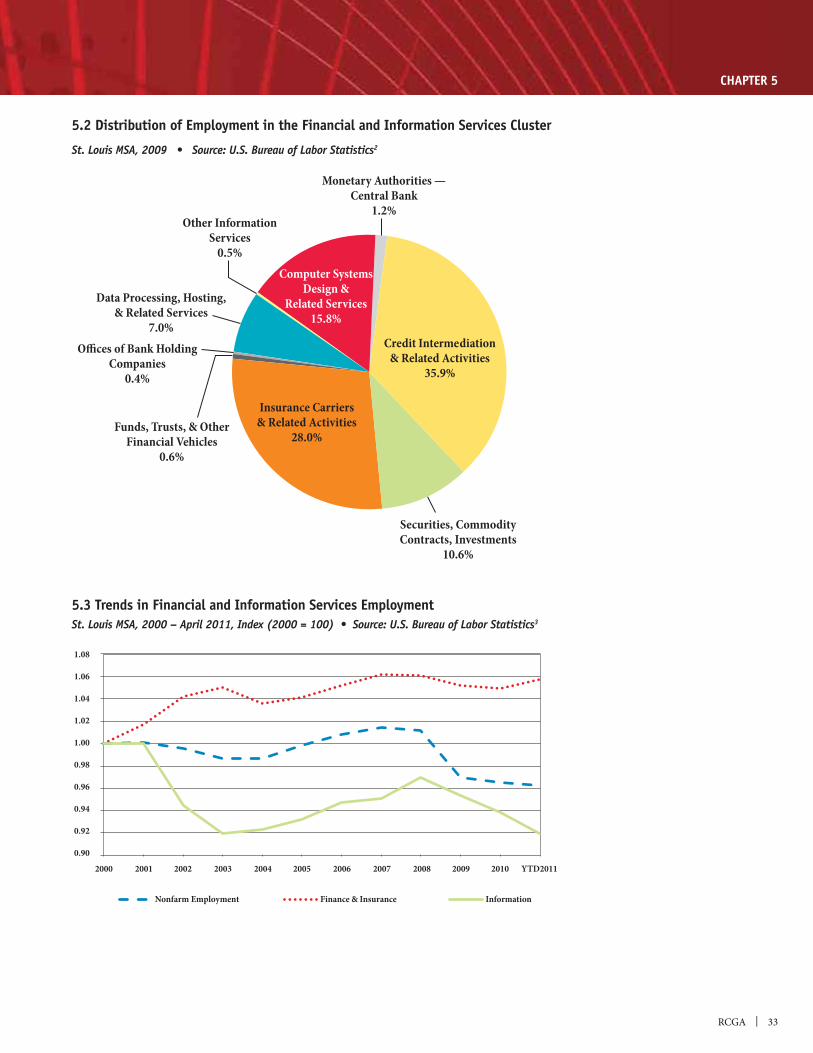

related activities sector demonstrated the strongest performance over this period. This sector includes banking, savings and loan and credit unions, credit card issuing and sales financing, and mortgage brokers. (5.2) These firms operate in a dynamic and interdependent environment. Employment losses in the information industry, driven by contractions in the telecommunications sector, lead the overall information sector to trail the region’s total employment performance. The cluster definition incorporates only a portion of the larger information sector. In the taxonomy of the North American Industrial Classification System, the cluster includes NAICS 52, and parts of NAICS 51, 54, and 55. (5.3)

30 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Computer Systems Design& Related Services

(NAICS 5415)Se

Sy SeSe

Se

Other Information Services(NAICS 519)

Ne

gWe Se

Data Processing, Hosting& Related Services

(NAICS 518)

INFO

RMAT

ION

SU

PPO

RTFI

NA

NCI

AL

SERV

ICES

IND

UST

RY

Prof

essio

nal &

Tech

nica

l Ser

vice

sN

AIC

S 54

Info

rmat

ion

NA

ICS

54M

anag

emen

tof

Com

pani

es&

Ent

erpr

ises

NA

ICS

55

Fina

nce &

Insu

ranc

eN

AIC

S 52

Central Banks (NAICS 521)

Offices of Bank Holding CompaniesNAICS 551111

Funds, Trusts, & OtherFinancial Vehicles

(NAICS 525)

Insurance Carriers& Other

(NAICS 524)

Securities, Commodities& Investments (NAICS 523)

&

&

Ex

Depository Banks (NAICS 522)

ed

INFR

AST

RUCT

URE

ProfessionalAssociations

Other Professional& Technical Services

Utilities &Infrastructure

Education &Training

ResearchUniversities

OCC

UPA

TIO

NS Entry Level ($20,000 – $49,999)

okkeep

ppb

Mid Level ($50,000 – $79,999)A

Sy

Higher ($80,000 and up)Softw

Sy

5.1 The Financial and Information Services Cluster

RCGA | 31

CHAPTER 5

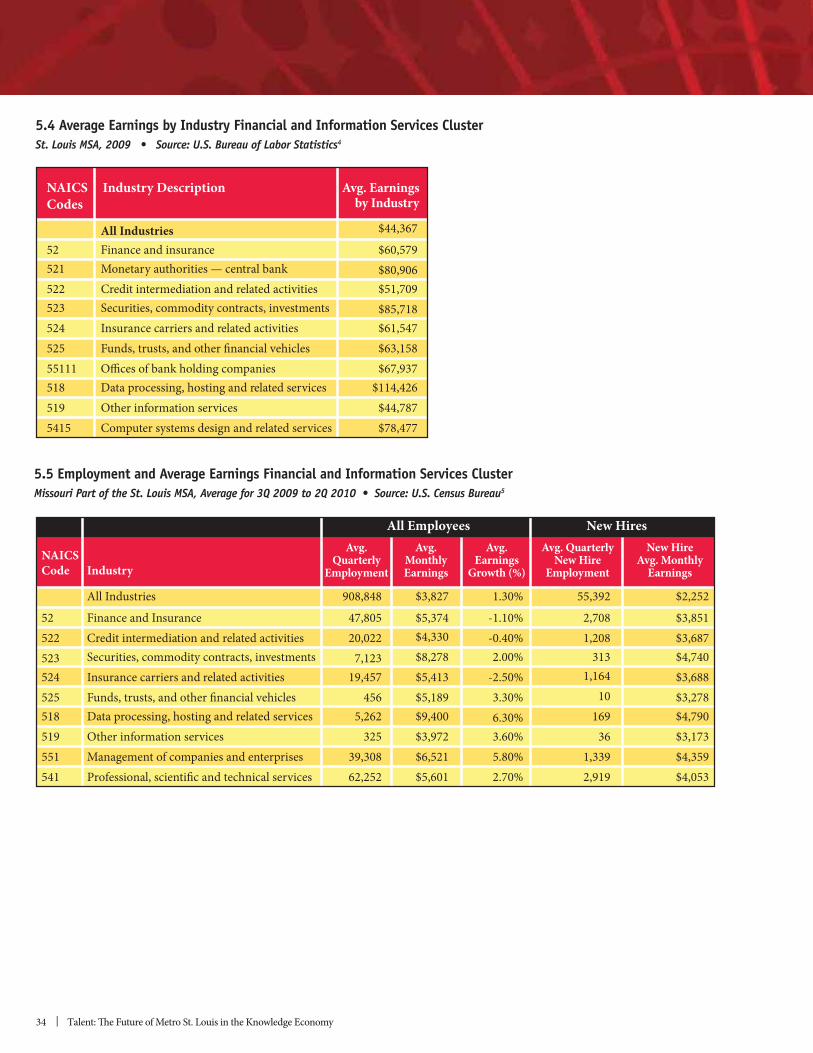

Earnings within the Financial and Information Services ClusterEarnings for employees of the financial and information services cluster are higher than the average for all industries in St. Louis. Average annual earnings of $60,579 in finance and insurance is 37 percent higher than the $44,367 average for all industries, for example. The average earnings for the computer system design and related services industry is $78,477, or 77 percent higher. (5.4) Annual starting wages for new hires in the cluster are also higher than the average for all industries in the St. Louis regional economy. Earnings growth for employees in six cluster subsectors between the third quarter of 2009 and the second quarter of 2010 exceeded the regional average. Earnings growth in data processing and hosting services was particularly strong. (5.5)

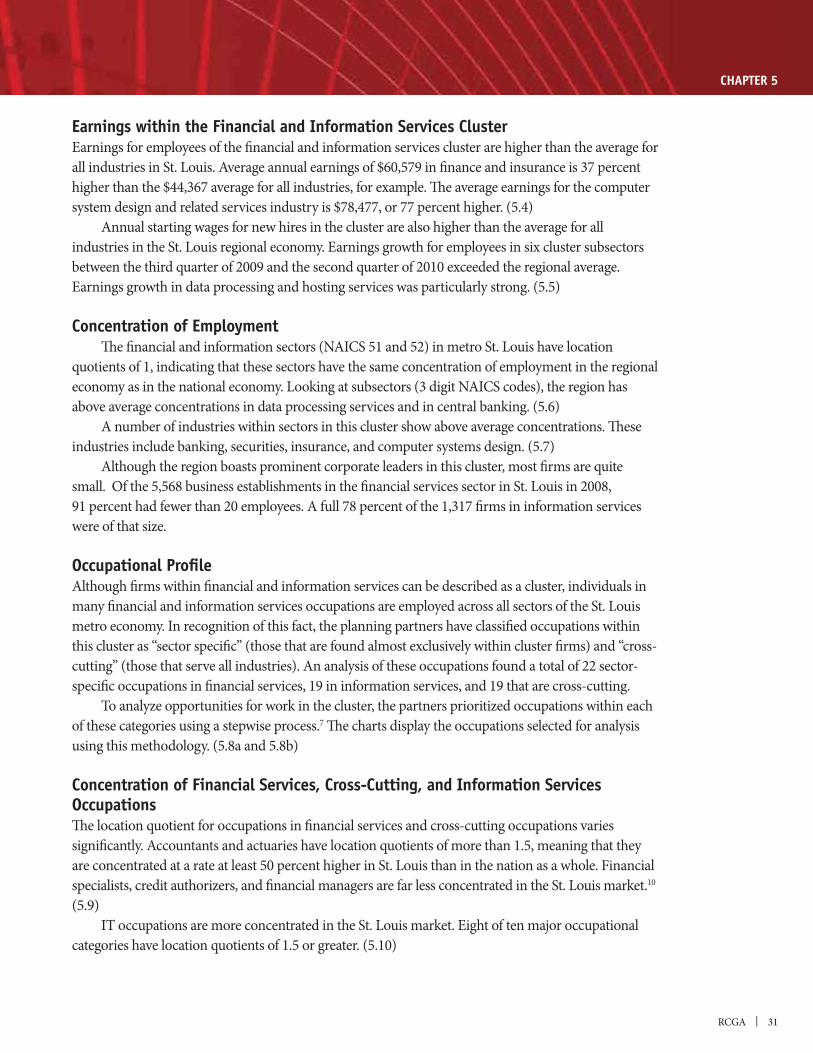

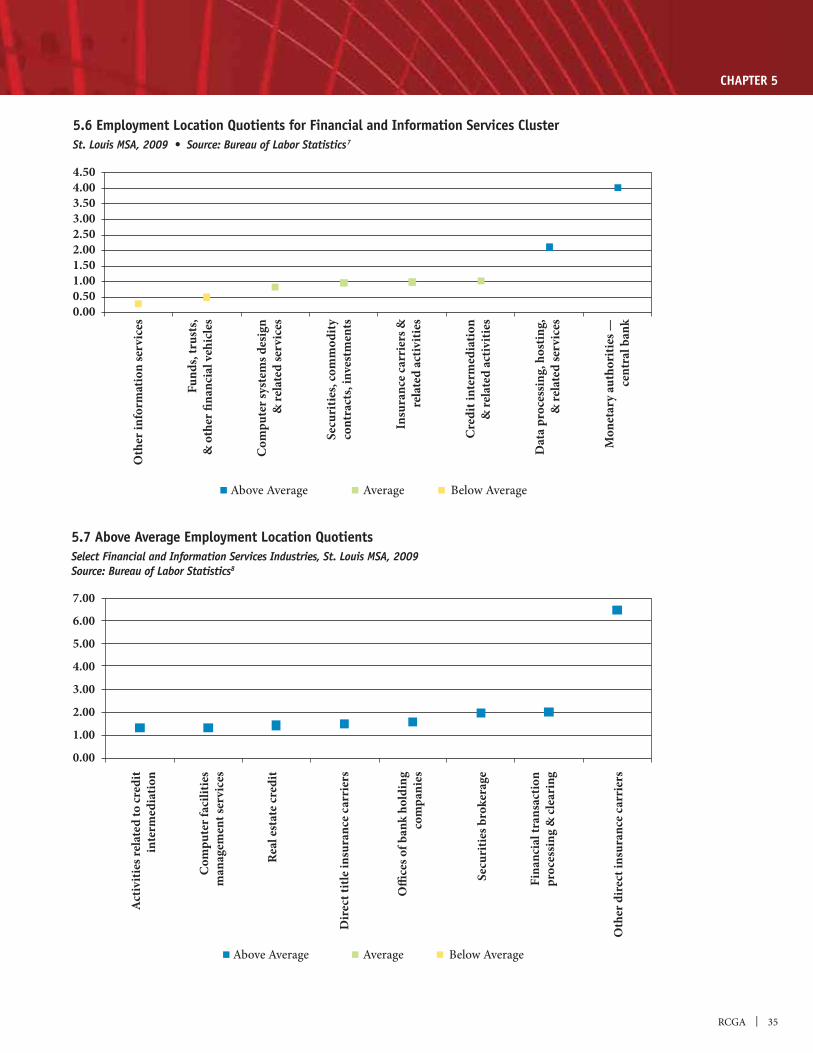

Concentration of Employment The financial and information sectors (NAICS 51 and 52) in metro St. Louis have location quotients of 1, indicating that these sectors have the same concentration of employment in the regional economy as in the national economy. Looking at subsectors (3 digit NAICS codes), the region has above average concentrations in data processing services and in central banking. (5.6) A number of industries within sectors in this cluster show above average concentrations. These industries include banking, securities, insurance, and computer systems design. (5.7) Although the region boasts prominent corporate leaders in this cluster, most firms are quite small. Of the 5,568 business establishments in the financial services sector in St. Louis in 2008, 91 percent had fewer than 20 employees. A full 78 percent of the 1,317 firms in information services were of that size.

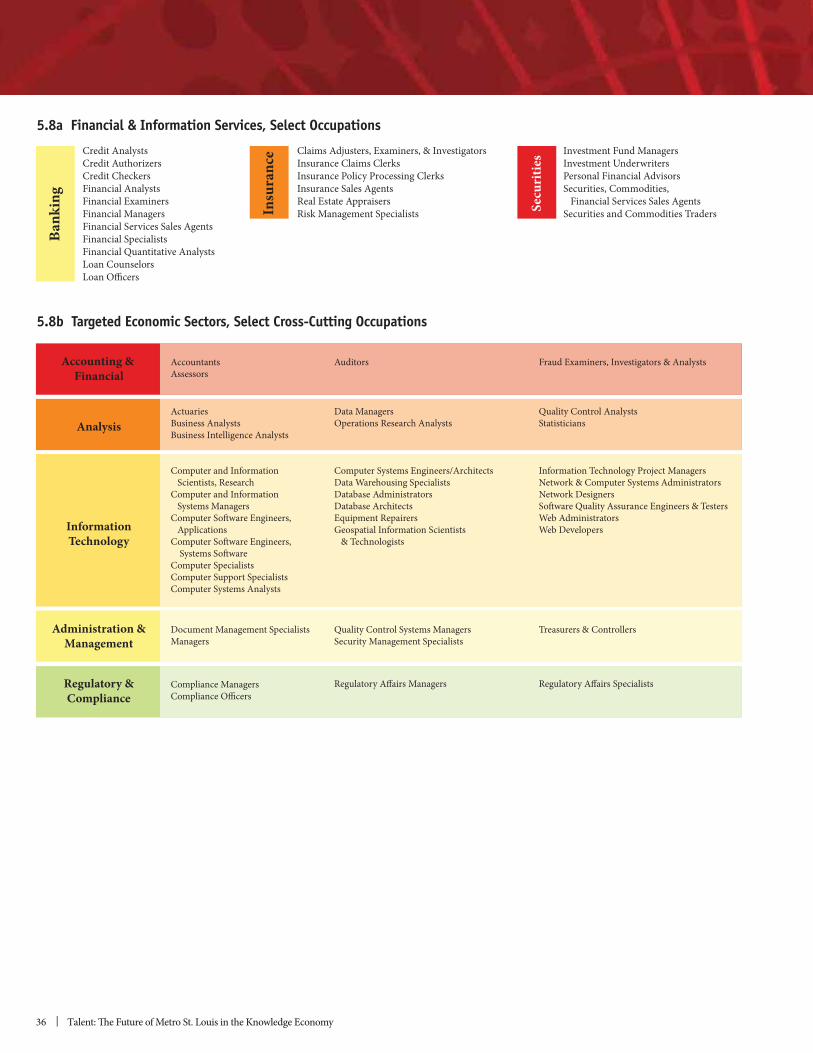

Occupational ProfileAlthough firms within financial and information services can be described as a cluster, individuals in many financial and information services occupations are employed across all sectors of the St. Louis metro economy. In recognition of this fact, the planning partners have classified occupations within

To analyze opportunities for work in the cluster, the partners prioritized occupations within each of these categories using a stepwise process.7 The charts display the occupations selected for analysis using this methodology. (5.8a and 5.8b)

Concentration of Financial Services, Cross-Cutting, and Information Services Occupations

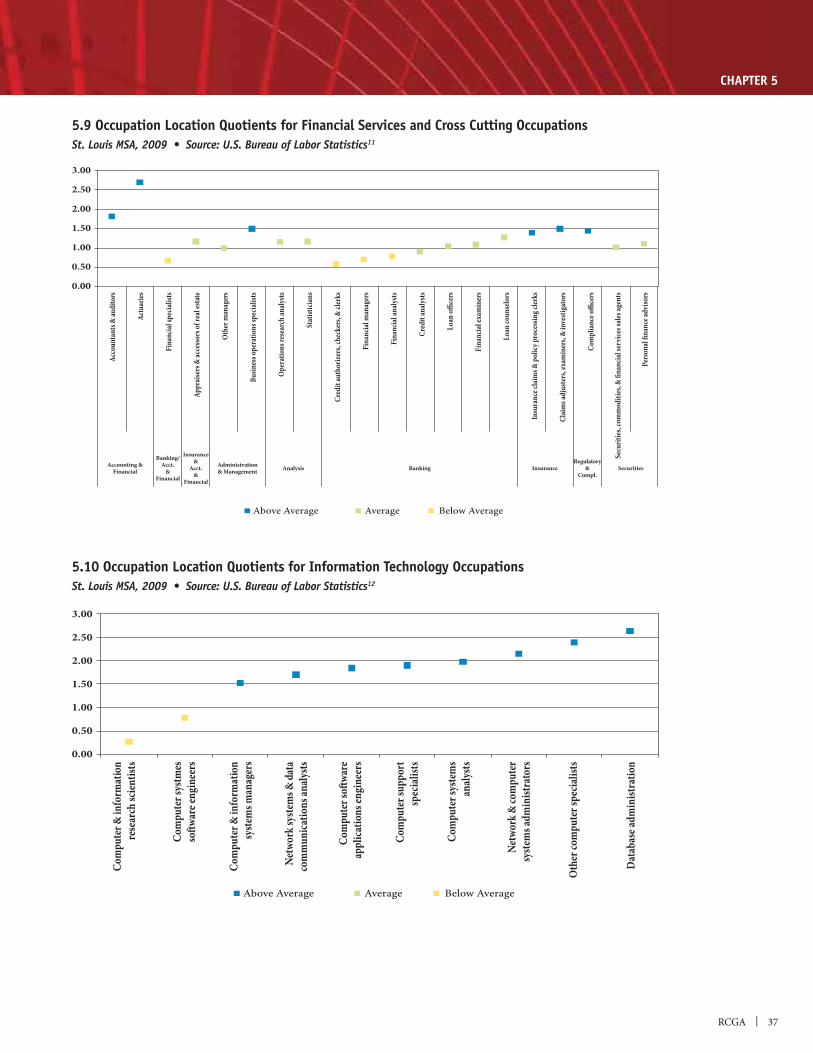

significantly. Accountants and actuaries have location quotients of more than 1.5, meaning that they are concentrated at a rate at least 50 percent higher in St. Louis than in the nation as a whole. Financial specialists, credit authorizers, and financial managers are far less concentrated in the St. Louis market.10

(5.9) IT occupations are more concentrated in the St. Louis market. Eight of ten major occupational categories have location quotients of 1.5 or greater. (5.10)

32 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Wages for Financial Services, Cross-Cutting, and Information Services Occupations

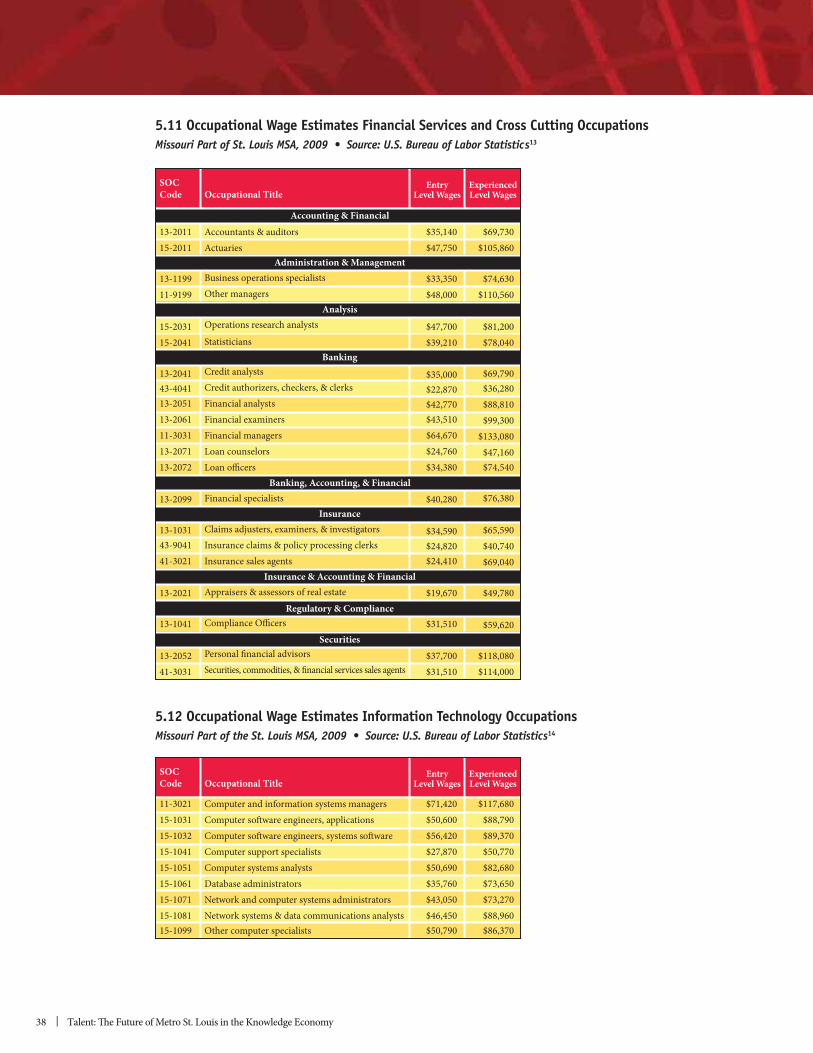

Classification (SOC) system codes and occupational titles. (5.11) Entry level wages in IT occupations are particularly strong. Section 9 provides an example of a career pathway in which motivated and persistent individuals can enter the IT field as computer support specialists and work their way up to computer systems analyst positions with high earning potential. (5.12)

Comparison to U.S. Wages

of wages nationally. At the lower end of this range, wages for credit analysts and insurance sales agents are approximately 89 percent of national wages and, at the higher end, wages for financial examiners and real estate appraisers and assessors are about 105 percent of the national wages. St. Louis area wages for information technology occupations overall are about 91 percent of national wages. The wage differential ranges from a low of 80 percent for computer and information research scientists to 108 percent for network systems and data communication analysts.

College Credentials and Financial and Information Services Occupations

and Information Center (MERIC) have these requirements. In practice at the national level, however, individuals currently working in these occupations have

some college and no degree. Among financial analysts, 31 percent have master’s degrees and 44.6

RCGA | 33

CHAPTER 5

Credit Intermediation& Related Activities

35.9%

Securities, CommodityContracts, Investments

10.6%

Insurance Carriers& Related Activities

28.0%

Computer SystemsDesign &

Related Services15.8%

Monetary Authorities —Central Bank

1.2%Other Information

Services0.5%

Data Processing, Hosting,& Related Services

7.0%Offices of Bank Holding

Companies0.4%

Funds, Trusts, & OtherFinancial Vehicles

0.6%

5.2 Distribution of Employment in the Financial and Information Services Cluster 2

1.08

1.06

1.04

1.02

1.00

0.98

0.96

0.94

0.92

0.90

YTD201120102009200820072006200520042003200220012000

Nonfarm Employment Finance & Insurance Information

5.3 Trends in Financial and Information Services Employment3

34 | Talent: The Future of Metro St. Louis in the Knowledge Economy

NAICS Industry DescriptionCodes

Avg. Earningsby Industry

All Industries 52 Finance and insurance521 Monetary authorities — central bank522 Credit intermediation and related activities523 Securities, commodity contracts, investments524 Insurance carriers and related activities525 Funds, trusts, and other financial vehicles55111 Offices of bank holding companies518 Data processing, hosting and related services519 Other information services5415 Computer systems design and related services

$44,367

$60,579$80,906$51,709$85,718$61,547$63,158$67,937

$114,426$44,787$78,477

5.4 Average Earnings by Industry Financial and Information Services Cluster 4

New HireAvg. Monthly

Earnings

Avg. QuarterlyNew Hire

Employment

Avg.Earnings

Growth (%)

Avg.MonthlyEarnings

Avg.Quarterly

EmploymentNAICS Code Industry

$2,252

$3,851$3,687$4,740$3,688$3,278$4,790$3,173$4,359$4,053

55,392

2,7081,208

3131,164

10169

361,3392,919

1.30%

-1.10%-0.40%2.00%

-2.50%3.30%6.30%3.60%5.80%2.70%

$3,827

$5,374$4,330$8,278$5,413$5,189$9,400$3,972$6,521$5,601

908,848

47,80520,022

7,12319,457

4565,262

32539,30862,252

All Employees New Hires

52522523524525518519551541

All Industries

Finance and InsuranceCredit intermediation and related activitiesSecurities, commodity contracts, investmentsInsurance carriers and related activitiesFunds, trusts, and other financial vehiclesData processing, hosting and related servicesOther information servicesManagement of companies and enterprisesProfessional, scientific and technical services

5.5 Employment and Average Earnings Financial and Information Services Cluster 5

RCGA | 35

CHAPTER 5

4.504.003.503.002.502.001.501.000.500.00

Oth

er in

form

atio

n se

rvic

es

Fund

s, tr

usts

,&

oth

er fi

nanc

ial v

ehic

les

Com

pute

r sys

tem

s des

ign

& re

late

d se

rvic

es

Secu

ritie

s, co

mm

odity

cont

ract

s, in

vest

men

ts

Insu

ranc

e car

rier

s &re

late

d ac

tiviti

es

Cred

it in

term

edia

tion

& re

late

d ac

tiviti

es

Dat

a pro

cess

ing,

hos

ting,

& re

late

d se

rvic

es

Mon

etar

y aut

hori

ties —

cent

ral b

ank

Above Average Average Below Average

5.6 Employment Location Quotients for Financial and Information Services Cluster 7

Act

iviti

es re

late

d to

cred

itin

term

edia

tion

Com

pute

r fac

ilitie

sm

anag

emen

t ser

vice

s

Real

esta

te cr

edit

Dir

ect t

itle i

nsur

ance

carr

iers

Offi

ces o

f ban

k ho

ldin

gco

mpa

nies

Secu

ritie

s bro

kera

ge

Fina

ncia

l tra

nsac

tion

proc

essi

ng &

clea

ring

Oth

er d

irec

t ins

uran

ce ca

rrie

rs7.00

6.00

5.00

4.00

3.00

2.00

1.00

0.00

Above Average Average Below Average

5.7 Above Average Employment Location Quotients

8

36 | Talent: The Future of Metro St. Louis in the Knowledge Economy

Claims Adjusters, Examiners, & InvestigatorsInsurance Claims ClerksInsurance Policy Processing ClerksInsurance Sales AgentsReal Estate Appraisers Risk Management Specialists Se

curi

ties

Insu

ranc

e

Bank

ing

Investment Fund Managers Investment UnderwritersPersonal Financial AdvisorsSecurities, Commodities, Financial Services Sales AgentsSecurities and Commodities Traders

Credit AnalystsCredit AuthorizersCredit CheckersFinancial AnalystsFinancial ExaminersFinancial ManagersFinancial Services Sales AgentsFinancial SpecialistsFinancial Quantitative Analysts Loan CounselorsLoan Officers

Regulatory &Compliance

Administration &Management

InformationTechnology

Analysis

Accounting & Financial

Compliance ManagersCompliance Officers

Regulatory Affairs Managers Regulatory Affairs Specialists

AccountantsAssessors

Auditors Fraud Examiners, Investigators & Analysts

ActuariesBusiness AnalystsBusiness Intelligence Analysts

Data ManagersOperations Research Analysts

Quality Control AnalystsStatisticians

Computer and Information Scientists, ResearchComputer and Information Systems ManagersComputer Software Engineers, ApplicationsComputer Software Engineers, Systems SoftwareComputer SpecialistsComputer Support SpecialistsComputer Systems Analysts

Computer Systems Engineers/ArchitectsData Warehousing SpecialistsDatabase AdministratorsDatabase ArchitectsEquipment RepairersGeospatial Information Scientists & Technologists

Information Technology Project ManagersNetwork & Computer Systems AdministratorsNetwork DesignersSoftware Quality Assurance Engineers & TestersWeb AdministratorsWeb Developers

Document Management SpecialistsManagers

Quality Control Systems Managers Security Management Specialists

Treasurers & Controllers

5.8a Financial & Information Services, Select Occupations

5.8b Targeted Economic Sectors, Select Cross-Cutting Occupations

RCGA | 37

CHAPTER 5

Com

puter

& in

form

atio

nre

sear

ch sc

ientis

ts

Com

puter

systm

esso

ftwar

e eng

inee

rs

Com

puter

& in

form

atio

nsy

stem

s man

ager

s

Netw

ork s

ystem

s & da

taco

mm

unica

tions

analy

sts

Com

puter

softw

are

appl

icatio

ns en

gine

ers

Com

puter

supp

ort

spec

ialist

s

Com

puter

syste

ms

analy

sts

Netw

ork &

com

puter

syste

ms a

dmin

istra

tors

Othe

r com

puter

spec

ialist

s

Data

base

adm

inist

ratio

n3.00

2.50

2.00

1.50

1.00

0.50

0.00

Above Average Average Below Average

5.10 Occupation Location Quotients for Information Technology Occupations 12

5.9 Occupation Location Quotients for Financial Services and Cross Cutting Occupations 11

Acco

unta

nts &

audi

tors

Actu

aries

Fina

ncial

spec

ialist

s

Appr

aiser

s & ac

cesso

rs of

real

estat

e

Othe

r man

ager

s

Busin

ess o

pera

tions

spec

ialist

s

Oper

atio

ns re

sear

ch an

alysts

Stat

istici

ans

Cred

it au

thor

izers

, che

cker

s, &

clerk

s

Fina

ncial

man

ager

s

Fina

ncial

analy

sts

Cred

it an

alysts

Loan

office

rs

Fina

ncial

exam

iner

s

Loan

coun

selo

rs

Insu

ranc

e clai

ms &

polic

y pro

cessi

ng cl

erks

Claim

s adj

uster

s, ex

amin

ers,

& in

vesti

gato

rs

Com

plian

ce offi

cers

Secu

rities

, com

mod

ities

, & fi

nanc

ial se

rvice

s sale

s age

nts

Pers

onal

finan

ce ad

viso

rs

3.00

2.50

2.00

1.50

1.00

0.50

0.00

Insurance&

Acct.&

Financial

Banking/Acct.

&Financial

Accounting &Financial

Regulatory&

Compl.SecuritiesInsuranceBankingAnalysisAdministration

& Management

Above Average Average Below Average

38 | Talent: The Future of Metro St. Louis in the Knowledge Economy

5.12 Occupational Wage Estimates Information Technology Occupations14

ExperiencedLevel Wages

EntryLevel Wages

SOCCode Occupational Title

$117,680 $88,790 $89,370 $50,770 $82,680 $73,650 $73,270 $88,960 $86,370

$71,420 $50,600 $56,420 $27,870 $50,690 $35,760 $43,050 $46,450 $50,790

11-302115-103115-103215-104115-105115-106115-107115-108115-1099

Computer and information systems managersComputer software engineers, applicationsComputer software engineers, systems softwareComputer support specialistsComputer systems analystsDatabase administratorsNetwork and computer systems administratorsNetwork systems & data communications analystsOther computer specialists

5.11 Occupational Wage Estimates Financial Services and Cross Cutting Occupations13

ExperiencedLevel Wages

EntryLevel Wages

SOCCode Occupational Title

13-201115-2011

13-119911-9199

15-203115-2041

13-204143-404113-205113-206111-303113-207113-2072

13-2099

13-103143-904141-3021

13-2021

13-1041

13-205241-3031

$69,730 $105,860

$74,630 $110,560

$81,200 $78,040

$69,790 $36,280 $88,810 $99,300

$133,080 $47,160 $74,540

$76,380

$65,590 $40,740 $69,040

$49,780

$59,620

$118,080 $114,000

$35,140 $47,750

$33,350 $48,000

$47,700 $39,210

$35,000 $22,870 $42,770 $43,510 $64,670 $24,760 $34,380

$40,280

$34,590 $24,820 $24,410

$19,670

$31,510

$37,700 $31,510

Accountants & auditorsActuaries

Business operations specialistsOther managers

Operations research analysts

Statisticians

Credit analystsCredit authorizers, checkers, & clerksFinancial analystsFinancial examinersFinancial managersLoan counselorsLoan officers

Financial specialists

Claims adjusters, examiners, & investigatorsInsurance claims & policy processing clerksInsurance sales agents

Appraisers & assessors of real estate

Compliance Officers

Personal financial advisorsSecurities, commodities, & financial services sales agents

Securities

Regulatory & Compliance

Insurance & Accounting & Financial

Insurance

Banking, Accounting, & Financial

Banking

Analysis

Administration & Management

Accounting & Financial

RCGA | 39

CHAPTER 5

5.13 Distribution of Educational Attainment Levels for Financial Services and Cross Cutting Occupations15

StatisticiansActuaries

Financial analystsSecurities, commodities, & financial services sales agents

Life, physical, & social science techniciansComputer software engineers, systems software

Computer software engineers, applicationsCompliance officers, except agriculture, construction, health & safety, & transportation

Operations research analystsPersonal financial advisors

Other managersOther financial specialists

Financial specialistsBusiness operations specialists

Other computer specialistsComputer systems analysts

Computer and information scientists, researchAccountants & auditors

Database administratorsComputer & information systems managers

Financial managersFinancial examiners

Appraisers & assessors of real estateInsurance sales agents

Network systems & data communications analystsIndustrial production managers

Claims adjusters, examiners, & investigatorsNetwork & computer systems administrators

Credit analystsLoan officers

Loan counselorsComputer support specialists

Insurance claims & policy processing clerksCredit authorizers, checkers, & clerks

100%75%50%25%0%

Less than high school diplomaHigh school diploma or eqivalentSome college, no degreeAssociate’s degreeBachelor’s degreeMaster’s degreeDoctoral or professional degree

40 | Talent: The Future of Metro St. Louis in the Knowledge Economy

______________

Note: Only a portion of the professional, scientific, and technical services sectors is included in the financial and information services cluster

4. The location quotient represents the ratio of an industry’s share of employment in a given area to that industry’s share of

report, employment location quotients of 1.3 or greater is considered above the national average, location quotients from 0.8 to 1.29 are identified as average, and location quotients of 0.79 or lower are considered below average.

Estimates by County” http://data.bls.gov/pdq/querytool.jsp?survey=en

6. Ibid.