tanzania - country strategy paper - african development bank

TRANSCRIPT

AFRICAN DEVELOPMENT BANK

AFRICAN DEVELOPMENT FUND

UNITED REPUBLIC OF TANZANIA

COUNTRY STRATEGY PAPER

2011-2015

REGIONAL DEPARTMENT EAST 1

OREA

JUNE 2011

Task Team: P. Bhakta (TZFO), P. Kariuki (UGFO), B. Hija (TZFO), G. Kaijage (TZFO), L. Kiggundu (TZFO), B.

Kishebuka (TZFO), S. Marandu (TZFO), Rweyamamu (TZFO), D. O. Leo (TZFO), S. Turay (OREA)I. Amadou

(OSAN), C. Ambert (OPSM), S. Chinien (OSGE), P. Dzimiri (OWAS), B. Issahaku (OSHD), F. Mkandawire (ORPF),

E. Muguti (ONEC), M. Muwele (ESTA), E. Negash (ONEC), T. Ngororano (OSGE), B. Purohit (OPSM), T. Temesgen

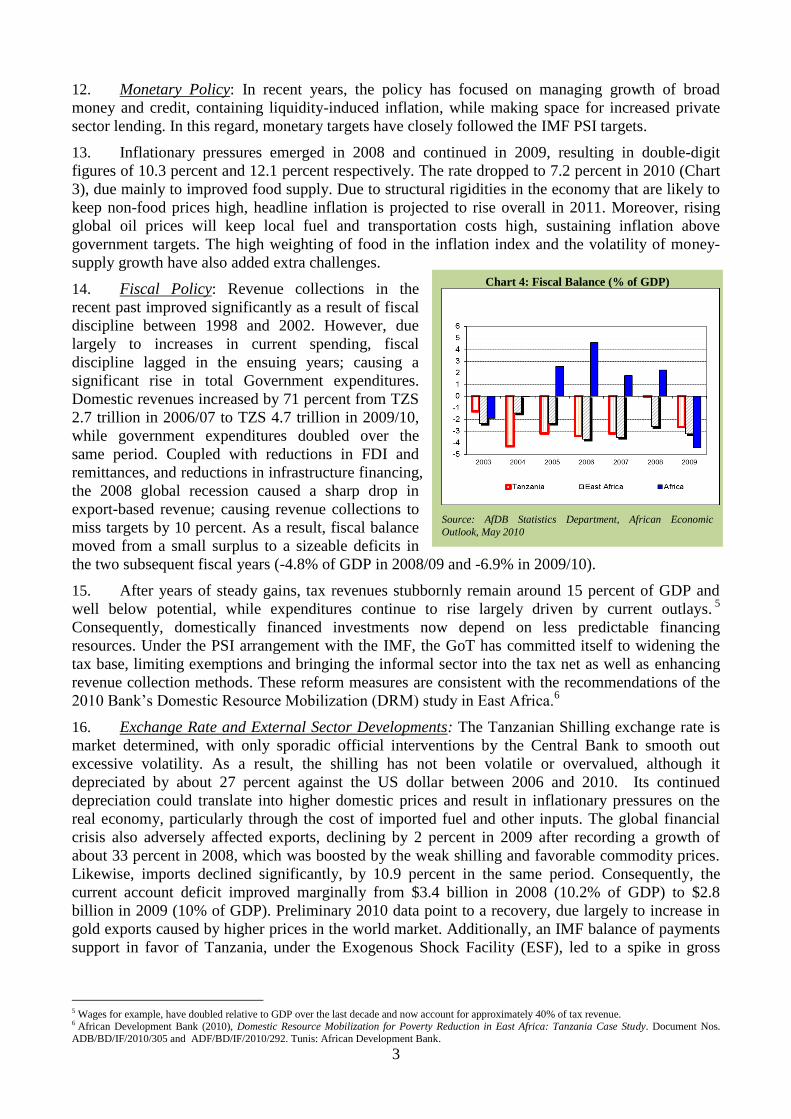

(OSGE),

Peer Reviewers: Ali. A. (OITC), J. Anywanu (EDRE); A. Coulibaly (OSGE), P. Dougna (OSHD), C. Mollinedo

(OSGE), K. Tench (OSGE), R. Walker (KEFO)

Table of Contents

I. INTRODUCTION ......................................................................................................... 1

II. COUNTRY CONTEXT AND PROSPECTS .............................................................. 1

Political Context .................................................................................................................... 1

Economic Context ................................................................................................................. 2

Governance ........................................................................................................................... 4

Business Environment and Competitiveness ........................................................................ 6

Regional Integration and Trade ............................................................................................. 7

Social Inclusion and Equity .................................................................................................. 8

Environment and Climate Change ........................................................................................ 9

III. STRATEGIC OPTIONS ............................................................................................... 9

Country Strategic Framework ............................................................................................... 9

Strengths and Opportunities ................................................................................................ 10

Challenges and Weaknesses ................................................................................................ 10

Aid Coordination/Harmonization ........................................................................................ 12

Bank Group‘s positioning in Tanzania ............................................................................... 13

IV. BANK GROUP STRATEGY ..................................................................................... 15

Rationale for Bank Group Intervention ............................................................................... 15

Pillars for Bank Group Support ........................................................................................... 15

Deliverables and Targets ..................................................................................................... 16

Lending Operations ............................................................................................................... 16

Non-Lending Operations ....................................................................................................... 18

Monitoring and Evaluation ................................................................................................. 18

Country Dialogue Issues ..................................................................................................... 19

Potential Risks and Mitigation Measures ............................................................................ 20

V. CONCLUSION AND RECOMMENDATION ......................................................... 20

ANNEXES

Annex I: Tanzania‘s 2011-2015 CSP Results Monitoring Matrix

Annex II: Summary of Completion Report for the Previous Bank Group Strategy (2006-2010) Annex III: Tanzania Ongoing Portfolio (as of March 2011)

Annex IV: Implementation of Recommendations CPIP 2009 Annex V: Country Portfolio Improvement Plan (CPIP) 2011

Annex VI: Tanzania - Comparative Socio-Economic Indicators

Annex VII: Tanzania: Select Macroeconomic Indicators

Annex VIII: Progress towards the MDGs for Mainland Tanzania

Annex IX: Progress towards the MDGs for Zanzibar

Annex X: Tanzania CPIA Ratings 2005-2010

Annex XI: Major Challenges of the JAST to Development Partners

Annex XII: Tanzania DP Division of Labour: Summary of agreements and Distribution of Roles

Annex XIII: The Transport Sector: Challenges and Priorities

Annex XIV: Tanzania - Administrative Map

Annex XV: References

LIST CHARTS, TABLES AND DESCRIPTIVE BOXES

Charts

Chart 1: Political Context 2009[Score -4.0 (Worst) to 2.5 (Best)]

Chart 2: Real GDP Growth (%)

Chart 3: Consumer Price Index Inflation Average (%)

Chart 4: Fiscal Balance (% of GDP) Chart 5: Rankings - GCI Global Competitiveness Index 2010-2011 (EAC)

Chart 6: Infrastructure Indicators 2009 Chart 7: Composition and Commitment by Sector since 1971 (as at 22 June 2011) Chart 8: Pillars for Bank Support

Tables

Table 1: Ease of Doing Business (Global Rank) 2010-2011 Table 2: Trade Flow – Regional Shares of Exports and Imports Table 3: Indicative Lending Program (National) Table 4: Indicative Lending Program (Multinational) Table 5: Indicative Non- Lending Program

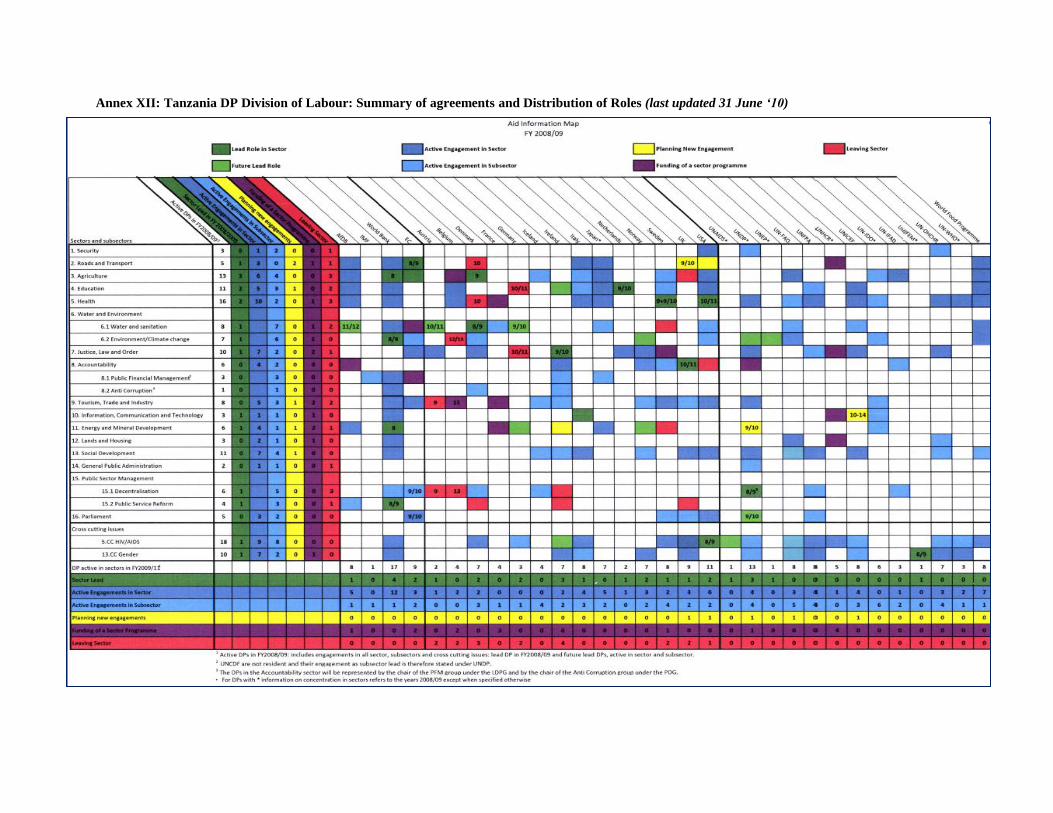

Descriptive Boxes

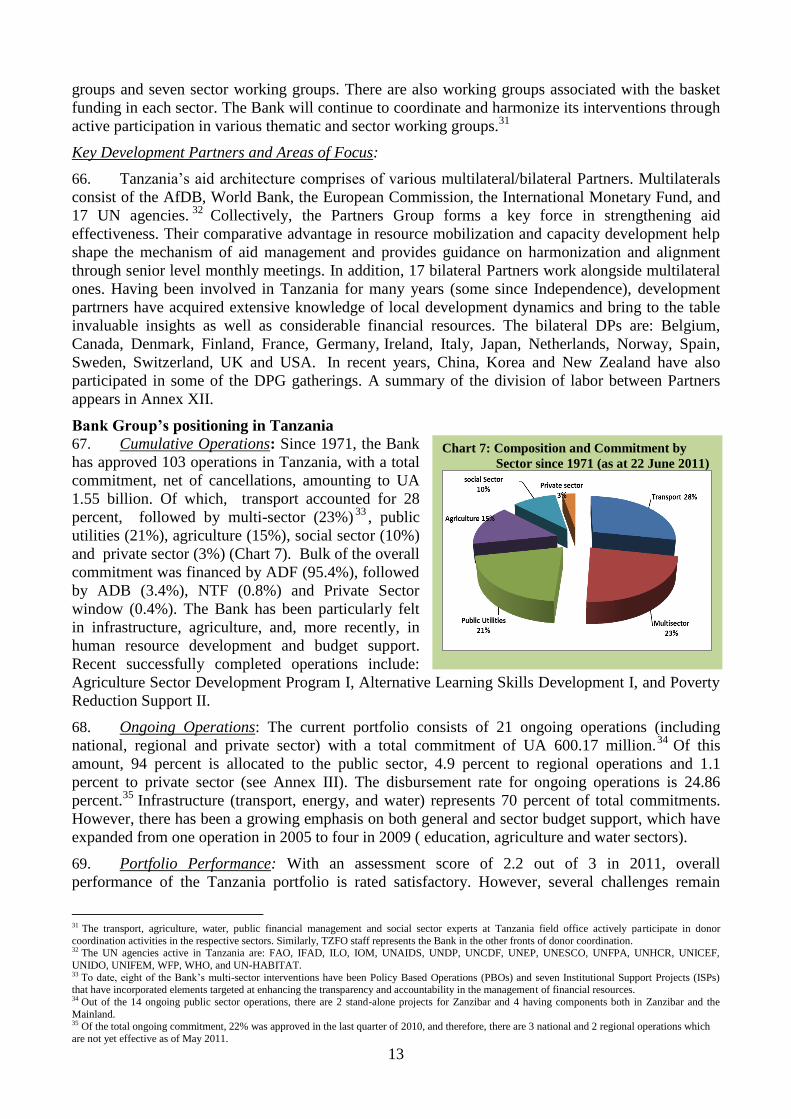

Box 1: Combatting Corruption in Tanzania Box 2: Major Regional Integration and Trade Affiliations

Box 3: Bank Group Consultations on the CSP

CURRENCY EQUIVALENTS

February 2011

UA 1 = US$ 1.453

UA 1 = EUR 1.13117

UA 1 = TZS 2,098.99 (Tanzania Shilling)

US$ 1 = TZS 1,508 (Tanzania Shilling)

GOVERNMENT FISCAL YEAR

July 1st to 30th June

WEIGHTS AND MEASURES

Metric System

ii

ACRONYMS AND ABBREVIATIONS

ADB African Development Bank

ADF African Development Fund

AIDS Acquired Immuno-Deficiency Syndrome

ALC Alternative Learning Center

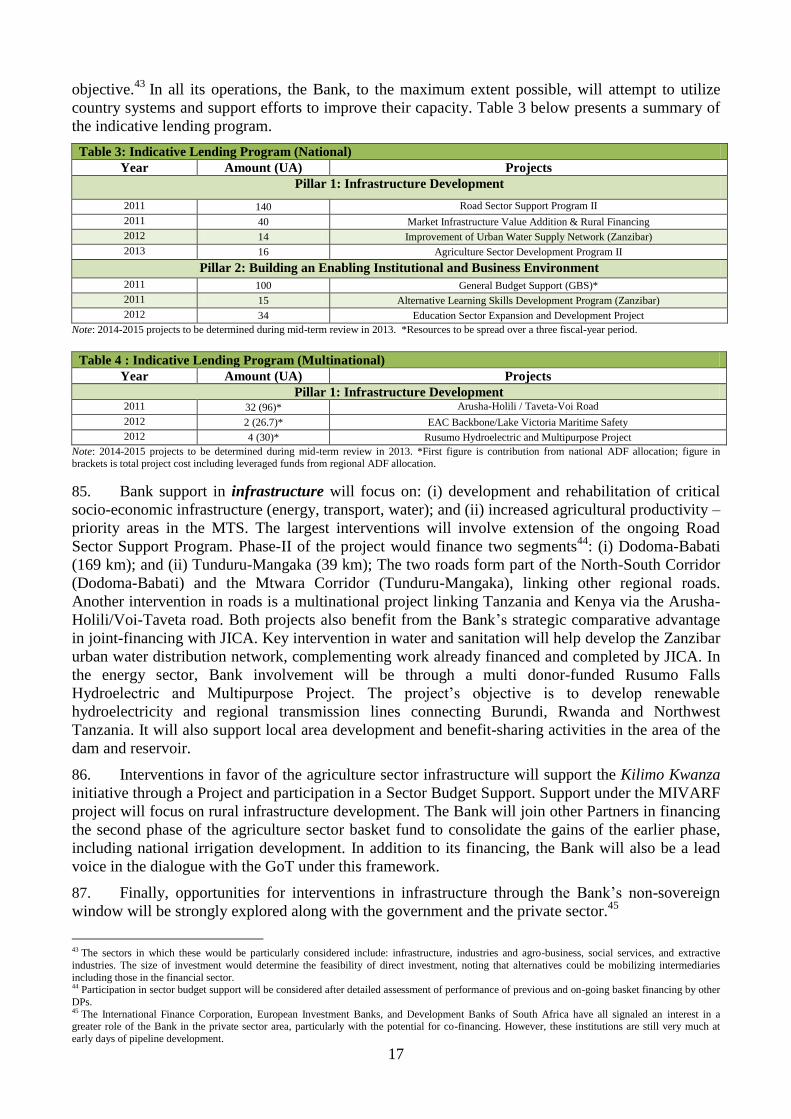

ALSD Alternative Learning and Skills Development Project

ASDP Agriculture Sector Development Program

BOT Bank of Tanzania

CAR Commitment at Risk

CCM Chama Cha Mapinduzi

COMESA Common Market for Eastern and Southern Africa

CPI Consumer Price Index

CPIA Country Policy and Institutional Assessment

CPIP Country Portfolio Improvement Plan

CPPR Country Portfolio Performance Review

CSP Country Strategy Paper

CStP Country Statistical profile

CUF Civic United Front

DP(s) Development Partner(s)

DPG Development Partners‘ Group

DRM Domestic Resource Mobilization

EA Executing Agency

EAC East African Community

EITI Extractive Industries Transparency Initiative

ESW Economic and Sector Work

FAO Food and Agriculture Organization

FDI Foreign Direct Investment

FY Fiscal Year

GBS General Budget Support

GDP Gross Domestic Product

GIZ Gesellschaft für Internationale Zusammenarbeit

GNU Government of National Unity

GoT Government of Tanzania

GSTP Global System of Trade Preferences among Developing Countries

HDI Human Development Index

HIV/AIDS Human Immuno-deficiency Virus/Acquired Immuno-Deficiency Syndrome

IA Implementation Agency

ICP International Comparison Program

IFAD International Fund for Agriculture Development

IFAD International Fund for Agricultural Development

IFMIS Integrated Financial Management Information System

IFLS Integrated Labor Force Survey

ILO International Labor Organization

IMF International Monetary Fund

IOM International Organization for Migration

ISP Institutional Support Project

JAST Joint Assistance Strategy for Tanzania

iii

JICA Japan International Cooperation Agency

JPD Joint Program Document

JSAN (IMF-World Bank) Joint Staff Advisory Note

KOICA Korea International Cooperation Agency

M&E Monitoring and Evaluation

MCC Millennium Challenge Corporation

MDGs Millennium Development Goals

MIVARFP Marketing Infrastructure, Value Addition & Rural Finance Program

MKUKUTA Mkakati wa Kukuza Uchumi na Kupunguza Umasikini Tanzania

MKUZA Mkakati wa Kukuza Uchumi na Kupunguza Umasikini Zanzibar

MTEF Medium Term Expenditure Framework

MIVARF Market Infrastructure, Value Addition and Rural Financing

NSGRP National Strategy for Growth and Reduction of Poverty

PAF Performance Assessment Framework

PCB Prevention of Corruption Bureau

PCCB Prevention and Combating of Corruption Bureau

PCR Project Completion Report

PEDP Primary Education Development Program

PEFAR Public Expenditure Financial Accountability Review

PFM Public Financial Management

PFMRP Public Financial Management Reform Program

PIU Project Implementing Unit

PPP Purchasing Power Parity

PPPs Public Private Partnerships

PRBS Poverty Reduction Budget Support

PRSL Poverty Reduction Support Loan

RIFF Regional Integration Facilitation Forum

RISP Regional Integration Strategy Paper

SADC Southern African Development Community

SAI Supreme Audit Institution

SBS Sector Budget Support

SNA System of National Accounts

SWOT Strengths, Weaknesses, Opportunities and Threats

SEDP Secondary Education Development Program

TANESCO Tanzania Electricity Supply Company

TDHS Tanzania Demographic and Health Survey

TDMS Teacher Development and Management Strategy

THMIS Tanzania HIV and Malaria Indicator Survey

TSMP Tanzania Statistical Master Plan

TZS Tanzanian Shilling

UA Unit of Account

UN United Nations

UNAIDS United Nations Program on HIV/AIDS

UNCDF United Nations Capital Development Fund

UNDP United Nations Development Program

UNEP United Nations Environment Program

UNESCO United Nations Educational, Scientific and Cultural Organization

UNFPA United Nations Population Fund

iv

UN-HABITAT United Nations Human Settlements Program

UNHCR United Nations High Commission for Refugees

UNICEF United Nations Children's Fund

UNIFEM United Nations Entity for Gender Equality and the Empowerment of Women

UNIDO United Nations Industrial Development Organization

USAID United States Agency for International Development

US$ United States of America Dollar

VAT Value Added Tax

WFP World Food Program

WHO World Health Organization

ZSGRP Zanzibar Strategy for Growth and Reduction of Poverty

1

Chart 1: Political Context 2009

[Score -4.0 (Worst) to 2.5 (Best)]

Source: AfDB Statistics Department using data from the WEF,

2011

I. INTRODUCTION

1. The Tanzania1 Country Strategy Paper for 2011-2015 assesses the country‘s development

challenges and prospects, and guides Bank Group‘s support to the priorities expressed in the new

national development strategy 2

. The Country Strategy lays emphasis on selectivity and rests on a

single overarching theme: supporting Tanzania become a more competitive economy and achieve

inclusive growth aimed at reducing poverty. This theme is anchored on two complementary pillars:

(i) infrastructure development; and (ii) building an enabling institutional and business environment.

2. The preceding Bank Group Strategy (2006-2010) was drawn from the Joint Assistance Strategy

for Tanzania (JAST), the Joint Program Document (JPD) and presented in an accompanying Cover

Note.3 The three documents were approved by the Board of Directors in 2007. The Joint Assistance

Strategy expired in 2010. Nonetheless, development partners have principally agreed to continue

working in the spirit of the JAST while deciding on how best to proceed with future collaborations.

Accordingly, the Bank and several other partners are progressing with preparation of their respective

assistance strategies; consistent with the new national development plan.4

3. Preparation of this Strategy benefited from elaborate consultations with Government,

development partners, private sector and civic institutions—including research and academic

concerns. It incorporates lessons from the 2006-2010 JAST and is underpinned by analytic and

diagnostic knowledge products. In addition to optimally utilizing Tanzania‘s performance based

concessionary resources allocation, the Strategy positions the Bank to assume a more catalytic role in

leveraging additional private and non-Bank resources.

II. COUNTRY CONTEXT AND PROSPECTS

Political Context

4. Tanzania continues to be politically stable and

peaceful; free of ethnic cleavages and labor unrest.

These factors partly explain the country‘s continued

attraction as an investment destination despite the

relatively high cost of doing business and other

structural hurdles.

5. The country scores better than other East

African countries in terms of civil liberties and

political rights, although there is room for

improvement (see Chart 1). Strength elements

include liberties such as: freedoms of press, speech

and religion; freedom of assembly and association,

and constitutionally guaranteed Women‘s rights.

Areas needing improvement include: weak transparency and accountability institutions; business

climate bottlenecks; and deteriorating educational quality.

6. In the October 2010 Presidential and Parliamentary elections, the incumbent President and the

ruling Chama Cha Mapinduzi (CCM) party secured re-election; wining 61.2 percent of the votes.

The nearest opposition candidate garnered 26.3 percent. The comfortable victory margin

notwithstanding, these results, compared to the 2005 election results, marked a slump in the CCM‘s

1 Tanzania derives from the names of the two states-- Tanganyika and Zanzibar-- that united in 1964 to form the United Republic of Tanzania. 2 The country‘s new development framework consists of the strategy for the mainland; the National Strategy for Growth and Reduction of Poverty II (or NSGRP II) and the Zanzibar Strategy for Growth and Reduction of Poverty (ZSGRP II). The NSGRP II and ZSGRP II are also popularly referred to

by their Swahili acronyms as MKUKUTA II (Mkakati wa Kukuza Uchumi na Kupunguza Umasikini) and MKUZA II (Mkakati wa Kukuza Uchumi na

Kupunguza Umasikini Zanzibar), respectively. 3 The respective Board documents were ADB/BD/WP/2007/55, and ADF/BD/WP/2007/41. The JAST MOU was signed on 05 December 2006 by the

Government and 19 Development Partners, namely-- African Development Bank, Belgium, Canada, Denmark, European Commission, Finland,

France, Ireland, Japan, Germany, Netherlands, Norway, Spain, Sweden, Switzerland, United Kingdom, World Bank, United Nations Organizations and United States of America. 4 These include: DFID, the UN-system, The World Bank, Denmark and Sweden.

2

Chart 2: Real GDP Growth (%)

Source: AfDB Statistics Department, African Economic Outlook,

May 2010

Chart 3: Consumer Price Index Inflation Average (%)

Source: AfDB Statistics Department

popularity for the first time. The latest result also points to a more spirited and competitive political

environment than before.

7. In a July 2010 referendum that preceded general elections, 66.4 percent of Zanzibari voters

agreed to the formation of a Government of National Unity (GNU). The GNU was, in effect, a

political compromise between the two key political parties; CCM and Civic United Front (CUF). In

the near-term, the key domestic political development to watch is the ongoing national debate about

the Constitution reform process.

Economic Context

8. Economic Structure: The economy is still highly dependent on agriculture, contributing an

estimated 30 percent to GDP and employing nearly 80 percent of the working population. The

service sector—which has been growing rapidly in recent years—accounts for approximately 47

percent (for opportunities and challenges see paragraphs 48-58). The two sectors are expected to

continue their dominance of the economy in the foreseeable future. The industrial sector, dominated

by the construction sub-sector, accounts for 23 percent. Industrial production plummeted in 2008-09

in the aftermath of the global economic slowdown. However, the sector has since rebounded, despite

severe and persistent power outages as well as rising fuel prices, both of which do not bode well in

the short and medium term. Since 2000, the mining sub-sector has attracted the bulk of foreign direct

investment (FDI), contributing to its rapid growth. Nevertheless, its share of GDP remains small (2.3

percent), partly because it is import dependent and not linked to the other sectors of the economy.

The sub-sector still accounts for a quarter of total exports.

9. Economic Growth: The country has achieved

impressive economic growth since the mid-1990s,

with reasonably low inflation. This reflects the

GoT‘s reform agenda, launched in the late 1980s,

ushering in a change in orientation from a state-led

strategy to market liberalization. Real annual GDP

growth increased from 3.3 percent in the early 1990s

to an average of 7 percent in the late 1990s. In 2009,

because of the global financial crisis, GDP growth

stood close to 6 percent, and recovered to 7 percent

in 2010 (Chart 2).

10. Growth Drivers: GDP growth was driven by

private consumption (growing population), exports

(due to favorable gold prices) and gross fixed capital

(mainly public investment). Private investment is

expected to lead growth in the short and medium

term. In terms of dynamic sectors, tourism and

mining continue to experience high growth rate even

if agriculture remains the largest sector.

11. Macroeconomic Management: Since early

2007, macroeconomic managment has been guided

by the IMF‘s Policy Support Instrument (PSI). The

current PSI, approved in June 2010, aims to maintain

macroeconomic stability and support accelerated

growth in line with the national development

strategy. According to the March 2011 IMF review,

the program has been implemented satisfactorily and

remains on track despite short-term challenges. (See para 12 - 14).

3

Chart 4: Fiscal Balance (% of GDP)

Source: AfDB Statistics Department, African Economic

Outlook, May 2010

12. Monetary Policy: In recent years, the policy has focused on managing growth of broad

money and credit, containing liquidity-induced inflation, while making space for increased private

sector lending. In this regard, monetary targets have closely followed the IMF PSI targets.

13. Inflationary pressures emerged in 2008 and continued in 2009, resulting in double-digit

figures of 10.3 percent and 12.1 percent respectively. The rate dropped to 7.2 percent in 2010 (Chart

3), due mainly to improved food supply. Due to structural rigidities in the economy that are likely to

keep non-food prices high, headline inflation is projected to rise overall in 2011. Moreover, rising

global oil prices will keep local fuel and transportation costs high, sustaining inflation above

government targets. The high weighting of food in the inflation index and the volatility of money-

supply growth have also added extra challenges.

14. Fiscal Policy: Revenue collections in the

recent past improved significantly as a result of fiscal

discipline between 1998 and 2002. However, due

largely to increases in current spending, fiscal

discipline lagged in the ensuing years; causing a

significant rise in total Government expenditures.

Domestic revenues increased by 71 percent from TZS

2.7 trillion in 2006/07 to TZS 4.7 trillion in 2009/10,

while government expenditures doubled over the

same period. Coupled with reductions in FDI and

remittances, and reductions in infrastructure financing,

the 2008 global recession caused a sharp drop in

export-based revenue; causing revenue collections to

miss targets by 10 percent. As a result, fiscal balance

moved from a small surplus to a sizeable deficits in

the two subsequent fiscal years (-4.8% of GDP in 2008/09 and -6.9% in 2009/10).

15. After years of steady gains, tax revenues stubbornly remain around 15 percent of GDP and

well below potential, while expenditures continue to rise largely driven by current outlays.5

Consequently, domestically financed investments now depend on less predictable financing

resources. Under the PSI arrangement with the IMF, the GoT has committed itself to widening the

tax base, limiting exemptions and bringing the informal sector into the tax net as well as enhancing

revenue collection methods. These reform measures are consistent with the recommendations of the

2010 Bank‘s Domestic Resource Mobilization (DRM) study in East Africa.6

16. Exchange Rate and External Sector Developments: The Tanzanian Shilling exchange rate is

market determined, with only sporadic official interventions by the Central Bank to smooth out

excessive volatility. As a result, the shilling has not been volatile or overvalued, although it

depreciated by about 27 percent against the US dollar between 2006 and 2010. Its continued

depreciation could translate into higher domestic prices and result in inflationary pressures on the

real economy, particularly through the cost of imported fuel and other inputs. The global financial

crisis also adversely affected exports, declining by 2 percent in 2009 after recording a growth of

about 33 percent in 2008, which was boosted by the weak shilling and favorable commodity prices.

Likewise, imports declined significantly, by 10.9 percent in the same period. Consequently, the

current account deficit improved marginally from $3.4 billion in 2008 (10.2% of GDP) to $2.8

billion in 2009 (10% of GDP). Preliminary 2010 data point to a recovery, due largely to increase in

gold exports caused by higher prices in the world market. Additionally, an IMF balance of payments

support in favor of Tanzania, under the Exogenous Shock Facility (ESF), led to a spike in gross

5 Wages for example, have doubled relative to GDP over the last decade and now account for approximately 40% of tax revenue. 6 African Development Bank (2010), Domestic Resource Mobilization for Poverty Reduction in East Africa: Tanzania Case Study. Document Nos.

ADB/BD/IF/2010/305 and ADF/BD/IF/2010/292. Tunis: African Development Bank.

4

reserves to about $3.9 billion by January 2011; sufficient to cover six-month import of goods and

services.

17. Medium-term Prospects: The expected continued global recovery and an ambitious green

revolution to revamp agriculture, popularly known as Kilimo Kwanza (agriculture first) initiative,

bode well for Tanzania‘s economy. According to Bank projections, growth is envisaged to revert to

its pre-crisis trajectory, having reached 7 percent in 2010, but expected to slow down slightly to 6.8

percent in 2011; bouncing back to 7.5 percent in 2012 and 7.8 percent by 2013.

18. There are two main challenges to the projected robust growth figures: First, the growing

fiscal deficit (see paragraph 14) resulting from GoT‘s optimistic revenue projections (& expenditure

patterns) implies a potential need to raise bridging funds. In turn, this could lead to an even greater

reliance on foreign grants and investment, or resorting to non-concessional borrowing.7 Public debt

in present value terms stood at 35.8 percent of GDP in 2010, and the ratio of debt service-to-revenue

increased from 7.5 percent in 2008 to 10.9 percent in 2010. However, the May 2010 joint IMF-

World Bank Debt Sustainability Analysis (DSA) concluded that the envisaged additional foreign

financing over the medium term would not necessarily jeopardize long-term debt sustainability, even

though it would increase the Present Value (PV) of debt-to-GDP and other indicators.

19. The second challenge over the medium-term is that growth remains highly heterogeneous;

differentiated geographically and across various segments of society.

20. Tanzania‘s economic challenges are more structural in nature (see paragraphs 53-61). Most

pressing challenges include: acute infrastructural bottlenecks—particularly in transport and energy, a

deficient fiduciary environment impeding private sector development and an under-performing

agricultural sector hindering poverty reduction efforts. A weak human resource base and significant

skills mismatch resulting from a deteriorating higher education system is also part of the structural

constraint. The Bank Group‘s proposed areas of intervention during this Strategy period derive from

these challenges (see paragraphs 76-81).

Governance

21. Tanzania has mixed achieved governance results. The World Bank‘s Governance Indicators

ranks the country between the 25 to 50 percentile amongst the 212 countries surveyed in 2009;

attaining its best score for political stability and lowest for regulatory quality. Furthermore, the Mo

Ibrahim Index of African Governance shows that, between 2008 and 2009, Tanzania maintained its

overall score of 55.0 (out of the highest possible score of 100) and its ranking remained unchanged at

12th place out of the 48 Sub-Saharan African countries. 8

Similarly, Tanzania‘s ranking in the Bank

Group‘s overall Policy and Institutional Assessment (CPIA) rating has remained at 4 for the past five

years, while its governance rating has remained at 3.8.

22. Control of Corruption Various indicators continue to rank Tanzania low in its efforts to

control corruption. For example, although the country‘s score on Transparency International‘s

Corruption Perception Index (CPI) improved between 1998 and 2007, both in absolute and relative

terms9, by 2009 the score was back to its low 2002 levels. In the 2010 CPI Tanzania scored 2.7,

ranking it 116th out of 178 countries. The CPI by definition assesses perceived rather than actual

cases of corruption. It, nonetheless, confirms respondents‘ opinion about rising corruption levels.

23. As highlighted in Box 1, anti-corruption efforts and initiatives go back several decades. Still,

both petty and grand corruption persists in the country. In general, there is inadequate access to

public information on corruption, as well as a lack of systematic surveying/monitoring and reporting.

Recently, the President ordered immediate publication of a long-anticipated National Governance

7 The Government is currently negotiating a non-concessional credit line with of the Commercial Banks. The IMF and other DPs are aware of this

development and are following very closely. 8 The Mo Ibrahim Index assesses the delivery of public goods and services to citizens by government and non-state actors. It uses indicators across four

main categories as proxies for the quality of the processes and outcomes of governance. They are: (i) safety and rule of law; (ii) participation and

human rights; (iii) sustainable economic opportunity; and (iv) human development. 9 Tanzania improved its ranking from 1.9 to 3.2

5

Box 1: Combatting Corruption in Tanzania

Efforts by the GoT to combat corruption go as far back as 1966 with the formation of the Permanent Commission of Inquiry

(Ombudsman) to check on the abuse of powers by government officials and agencies. This was followed by the 1971 Prevention

of Corruption Act, and subsequently, the creation of the Anti-Corruption Squad in 1975, which in 1991 was replaced by Prevention of Corruption Bureau (PCB), and later in 2001 evolved to Prevention and Combating of Corruption Bureau (PCCB).

In 1996, the then president set up the Warioba Commission of Inquiry to undertake a comprehensive study on corruption which

produced a detailed report with various anti-corruption recommendations. Between 2005 and January 2011, PCCB received more

than 35,000 allegations, and completed 7,339 investigations. During the same period, 928 new corruption related cases were taken

to courts, 798 of which were filed since the new Prevention and Combating of Corruption Act (2007) became operational. In total,

between 2005 and January 2011 the courts prosecuted 2,698 corruption related cases, resulting into 208 convictions against

corrupt offenders, and recovery of about US$ 19.5 million. The most recent high profile corruption cases have involved two ex-

Ministers and ex-Permanent Secretary (case still on-going); ex-employees of the Central Bank (one has been convicted – related

to loss of US$ 74 million; one case on-going – related to loss of US$ 70 million); and former Ambassador. Also, between 1995

and 2010, administrative actions were taken against 934 corrupt public servants.

and Corruption Survey report, conducted in 2009. Incidents of grand corruption scandals, weak

sanctions, deficient accounting standards and ineffective internal/external audit; all underscore the

need for greater oversight and accountability in government, strengthening legal and judicial reforms

and revamping the country‘s fiduciary environment.10

24. Public Financial Management: Results in PFM performance have been varied. Government

has enacted various legislations defining roles and responsibilities, accountability of spending

agencies, transparency requirements, and sanctions arrangements. 11

25. The PFM reform agenda is presented in the GoT‘s Public Financial Management Reform

Program (PFMRP III), which expires in June 2011.12

In September 2010, a joint GoT/Partners

mission assessed implementation progress of the action plan and found the overall progress to be

‗moderately satisfactory.‘13

Similarly, the most recent Public Expenditure and Financial

Accountability Assessment Review (PEFAR) results concluded that there are still challenges with

Government ownership of specific reforms. 14

26. The next phase of PFMRP aims to consolidate gains achieved thus far, and address remaining

challenges in the system. Seven key areas have been identified to meet this objective: (i) revenue

collections; (ii) planning and budget management; (iii) public financial accountability and

transparency; (iv) legal regulatory framework; (v) public investments and management; (vi) public

debt management; (vii) change management, program governance and management arrangements;

and (viii) building capacities of the Supreme Audit Institution (SAI), the Accountant General,

internal audit and parliamentary scrutiny.15

27. Along with progress in some areas, reinforcing fiscal discipline on budget formulation and

execution still requires urgent Government action. Improvements are especially needed in cash and

budget management, Integrated Financial Management Information Systems (IFMIS), flow of funds

to Local Government Authorities (LGAs)16

and building local PFM capacity. Annual budget cycles

also need to be carefully integrated into a transparent and realistic medium-term expenditure and

borrowing plans, accompanied by greater oversight. Regular monitoring of the Public Financial

Management Reform Program (PFMRP) is key to improved compliance with procurement

regulations and to achieve better value for money.

10 There are currently several pending legislations designed to address these challenges, including: Right to Information Act; Public Leadership Code of Ethics Act, and; Whistleblowers Act, all of which would help enhance transparency and demonstrate political will to further strengthen Tanzania‘s legal

framework. 11 These include the Constitution (1977); Tanzania Revenue Authority Act (1994); Public Finance Act (2001, revised in 2004); Public Procurement

Act (2004) ; Local Government Finance Act (1982 amended in 2001); Loans, Grants and Guarantees Act, a new Audit Act (2008) and a new Public-

Private Partnership Act (2010). The New PPA being drafted and expected to be presented to parliament by April 2011. 12The Bank‘s intervention in this area is through the Institution Support for Good Governance Project II (ISP II). 13 Out of 24 short-term actions, 15 were assessed as green, 1orange, 5 red, 2 as split and 1 as not applicable – the mission used a ‗traffic light system‘

when assessing implementation (Green indicating successful implementation, orange partially satisfactory and red not implemented). 14 The most recent PEFA was carried out between June 2008 and March 2009, with a further review in May 2010. 15 PFMRP IV and ISP II also address capacity issues at the supreme audit institution; the accountant-general‘s office; internal audit and parliamentary oversight. These interventions, among others, will help the Bank to accelerate Use of Country FM systems in its aid delivery to Tanzania. 16 A KPMG report for the system audit of Epicor IFMS revealed weaknesses both at the Central and Local government.

6

Table 1:

Ease of Doing Business (Global Rank) 2010-

2011

Topic Rankings DB 2011

Rank

DB

2010

Rank

Change

in

Rank

Starting a Business 122 122

No

change

Dealing with

Construction Permits

179 179 No

change

Registering Property 151 148 -3

Getting Credit 89 87 -2

Protecting Investors 93 92 -1

Paying Taxes 120 116 -4

Trading Across

Borders

109 111 2

Enforcing Contracts 32 32

No

change

Closing a Business 113 112 -1

Source: Doing Business, World Bank 2011

Chart 5:

Rankings - GCI Global Competitiveness

Index 2010-2011 (EAC)

Source: The Global Competitiveness Report 2010-

2011, WEF, 2010-11

28. Since 2007, the Bank, through its General Budget Support and Institutional Support

operations,17

and in close coordination with other partners through the General Budget Support

Working Group, has consistently supported Government efforts to implement a robust PFM reform

agenda. These interventions have helped Government to deter and detect corrupt practices by

strengthening accountability and transparency up-stream in the anti-corruption process.

Business Environment and Competitiveness

29. Business Environment: Whereas GoT is

committed to developing the country‘s nascent private

sector, this resolve has yet to be sufficiently translated

into adequate actions. Hence, the slow pace of reforms

continues to dampen overall investor confidence.

30. In recent years, Tanzania has slipped in the

World Bank‘s Doing Business Report 2011. Out of

183 countries, its ranking dropped from 125th to 128th

for 2010 and 2011 respectively. The drop is attributed

to the worsening ranking in five areas (see Table 1).

31. Improving the business environment is

accorded high priority by both the GoT and partners. It

was a key issue in the 2009 and 2010 GBS Annual

Reviews. In response to the deteriorating rankings in

the Ease of Doing Business, the GoT adopted a

Roadmap in 2010 focused on short, medium and long-

term reforms. Its implementation, however, has been

slow, suggesting continued unfavorable legal and

regulatory frameworks plus limited reform capacity in the public sector.

32. Other initiatives under implementation to improve the business environment include the

Business Environment Strengthening for Tanzania

Program (BEST), the Tax Modernization Program,

and an on-going Second Generation Financial Sector

Reform Program. Efforts to simplify business entry,

operation and exit are also underway. A one-stop non-

pre-approved business registration system is scheduled

to come on line in 2011.

33. Competitiveness: Tanzania ranked 113th

in the

2010-11Global Competitiveness Report, having slid by

nine positions from the previous year. Most notably,

the country has dropped from 97th (out of 122

countries) in 2006 to 113th (out of 134) in 2008. Key

challenges underlying this decline include: the

country‘s undeveloped infrastructure, particularly in

energy and transport, low human capital development,

an unsatisfactory regulatory and legal environment,

and poor quality human resource base. The financial sector also remains underdeveloped, resulting in

limited access to financial services. Less than 17 percent of formal businesses reported borrowing from

financial institutions and the stock of private sector credit is only 16-17 percent of GDP.

34. Other challenges contributing to Tanzania‘s poor showing include: failure to implement

pension fund reforms necessary to inject long-term liquidity into the economy, stalled land reform,

17 PRSL I (May-December 2005); PRSL II (June 2006 – December 2007) and PRSL III (November 2008 – August 2009).

7

Box 2: Major Regional Integration and Trade Affiliations

Tanzania is a member of the EAC, SADC, the Regional Integration Facilitation Forum (RIFF), and is granted non-reciprocal trade

preferences by the EC under the Cotonou Agreement and the Everything-but-Arms (EBA) initiative, the United States‘ AGOA, and

the GSP schemes of mainly Australia, Canada, EC, Japan, New Zealand and the United States. It has also participated in the

Agreement on the Global System of Trade Preferences among Developing Countries (GSTP) since 19 April 1989. Under the GSTP,

India and Turkey grant preferential access to Tanzania.

Tanzania is a former member of the Common Market for Eastern and Southern Africa (COMESA), from which it withdrew in 2000.

However, Kenya and Uganda remain members of both the COMESA and EAC, complicating the latter‘s drive towards a unified

market within COMESA. Starting in 2008, there are plans to merge 26 countries in eastern and southern Africa into a single trading

bloc under the COMESA-EAC-SADC tripartite arrangement, which will have a combined gross domestic product (GDP) of $625

billion.

lack of a national identity system18

, and inconsistencies in the application of laws and regulations.

Through selective interventions in infrastructure, governance and human development, the Bank is

well positioned to tackle some of these challenges.

Regional Integration and Trade

35. Tanzania is party to various regional integration and trade affiliations as summarized in Box

2 below. For close to two decades, it has implemented both external and domestic trade liberalization

programs. Measures taken under global trade liberalization include a lowering of applied and bound

tariffs rates, simplification of trade procedures and abolition of licensing as well as administrative

controls. Liberalizations on the domestic front include elimination of state controls, phasing-out

monopoly commodity marketing boards and state companies. Additional measures in this regard

include liberalization of foreign exchange market and attempts to open rural areas to markets through

infrastructure development. A national trade policy was also adopted in 2005, responding to and

building upon the various reforms above.19

36. Since 2006, Tanzania‘s exports of goods and services

have averaged 22 percent of GDP while imports have averaged

35 percent. Exports increased from $1.9 billion in 2006 to $3

billion in 2009, while imports rose from $3.9 billion in 2006 to

$5.9 billion for the same period.

37. The trade flows data in table2 depicts low volume

intra-regional trade within the EAC. These trade flows are

expected to increase following full operationalization of the

EAC Customs Union since January 2010. The Customs Union

has seen the removal of tariffs among member states,

application of a common external tariff and a move to an EAC

Common Market since July 2010. The move to a Common

Market implies freer trade, and freer movement of goods,

services, capital and people within the region. There is also a

substantial amount of informal trade with neighboring EAC

countries, mainly in food items, which is not fully captured by

official statistics

38. Going forward, Tanzania still faces challenges to integration and trade, particularly in the

areas of hard infrastructure (road transport, ports, energy, including the absence of power pools and

interconnections) as well as soft (financial markets, investment and business regulation and

procedures, customs/boarder post arrangements, policy harmonization). 20

All these areas are ripe for

the Bank‘s intervention in regional infrastructure development (transport, energy, ICT and shared

18

Measures are already underway to address this issue, and in April 2011, the Government formally contracted a Malaysian firm to implement the

National Identification Project. Production of national identity cards is expected to start this year. 19 Tanzania (2003), Trade Policy for a Competitive Economy and Export-led Growth. Dar es Salaam: Ministry of Industry and Trade. 20 See African Development Bank (2010), African Development Report: Logistics and Trade in Africa. Tunis: African Development Bank.

Table 2:

Trade Flow - Regional Shares of Exports

and Imports

2007 2008 2009

Regional Shares of Exports

Europe 36% 33% 30%

SADC 14% 15% 12%

EAC 8% 10% 9%

Africa 22% 29% 22%

America 2% 2% 2%

Asia 17% 20% 28%

Regional Shares of Imports

Europe 29% 27% 23%

SADC 14% 15% 13%

EAC 2% 3% 5%

Africa 17% 19% 19%

America 7% 6% 5%

Asia 40% 44% 43% Source: United Republic of Tanzania, 2010:

Economic Survey

8

water resources) and capacity building; as highlighted in the recent Regional Integration Strategy for

East Africa.

Social Inclusion and Equity

39. Poverty: Tanzania‘s ranking in UNDP‘s Human Development Index improved marginally

from 0.370 in 2005 to 0.398 in 2010. Still, poverty remains high; suggesting that despite impressive

macroeconomic achievements and sustained economic growth over the past decade, there has been

very little impact on the incomes and well-being of the poor. Available evidences point to the weak

redistributive aspect of growth, especially the weak linkages with rural areas where the majority of

the population lives. According to the 2007 Household Budget Survey (HBS), the basic needs

poverty ratio was 33.4 percent, representing only a modest decline from 35.6 percent in the 2000/01

HBS. Income inequality appears to have remained unchanged as reflected in the Gini Coefficients.21

Poverty remains predominantly rural (as high as 37.4% due largely to low agricultural growth caused

by drought, low rainfall and lack of and/or poor agriculture equipment and productivity). There are

also substantial numbers of poor people in urban/peri-urban areas. These developments suggest that

the MDG target of halving abject poverty by 2015 may not be achieved (Annex VIII & Annex IX).

40. Health: Inadequate facilities and acute shortage of skilled personnel pose challenges in the

health sector. Estimates from the 2009 Joint Health Sector Review suggest that only 35 percent of

the required skilled workforce is active in the rural areas. Nonetheless, the sector has recorded some

gains in recent years. The recent Tanzania Demographic and Health Survey (TDHS 2009/2010)

shows infant mortality rate declined from 58 deaths per 1,000 live births in 2007/08 to 51 in 2009/10.

Under-five mortality rate also declined from 91 deaths per 1,000 live births between 2007/8 and

2009/10 to 81 in 2009/10.22

Likewise, between 2007/8 and 2009/10, maternal mortality declined

significantly from 578 to 454 deaths per 100,000 live births. Based on the 2007/08 HIV and Malaria

Indicator Survey, HIV prevalence among the 15-49 age group declined from about 10 percent to 5.7

percent in late 1990s, with a higher incidence among women. Malaria prevalence in Zanzibar has

remained significantly low at 1 percent since 2007, down from over 40 percent before 2005.

41. Education: A quarter of adult Tanzanians have no education and 32.5 percent of women and

16.9 percent of men are illiterate.23

Following implementation of major sector reforms, there have

been significant improvements in the provision of basic education. Net primary school enrollment

increased from 59 percent in 2000 to 95.4 percent in 2010; secondary school net enrolment rate

reached 27.8 percent in 2009, up from 23.5 percent in 2007. However, the quality of education,

particularly in secondary schools, has declined markedly. The pass rate at the Form-IV level dropped

from 26.7 percent in 2008 to 11.5 percent in 2010—a development that points to, among other things,

decreasing performance and the urgency of addressing quality education delivery.24

Key constraints

specific to the sector include: teacher shortages, lack of teaching and learning materials, inadequate

facilities including science and language laboratories.

42. Labor Force and Employment: According to the 2006 Integrated Labor Force Survey (ILFS),

the size of the labor force is estimated to be in excess of 19 million; with an overall participation rate

of 89.6 percent. Unemployment is currently estimated at 4.3 percent and youth unemployment

(people aged 15-24) stood at 14.9 percent in 2006. The rate is estimated to be as high as 24 percent

amongst urban youth. Underemployment, although thought to be high, is not fully captured by

official statistics. Over 76 percent of the labor force is engaged in small-scale, mostly rain-fed,

subsistence agriculture. The lack of requisite skills is a constraint to private sector development. This

was confirmed during several Bank consultations with a cross-section of private sector employers.

21 The Gini coefficient of 0.35 in the 2007 HBS was virtually unchanged from the 2000/01 HBS, and in fact, was essentially the same as the 0.34 figure

in the 1991/92 HBS. 22 Tanzania HIV & Malaria Indicator Survey. 23 2005 Multi-Sector Country Gender Profile for Tanzania. 24 Currently, the main focus in education is to implement the major components of the Education Sector Development Program (ESDP), which are:

Primary Education Development Program Phase II (PEDP II 2007-2011); Secondary Education Development Program (SEDP-2004-2009); Teacher Development and Management Strategy (TDMS)-2007; Technical and Higher Education Sub Master Plan 2003-2018; and Preparation of the second

phase of SEDP.

9

Box 3: Bank Group Consultations on the Country Strategy Paper

In developing this Strategy, the Bank held wide-ranging consultations with the Government, various development partners, as

well as other non-state stakeholders from the private sector, academia and civil society. The discussions focused on the:

(i) country context and prospects; (ii) indicative project pipeline and its consistency with the proposed pillars as well as with

Government priorities; (iii) what other Partners plan to undertake in the period covered by the Strategy; and (iv) formulation of a

Results Framework for the Strategy, focusing on outcome and output indicators.

.

Rising levels of youth unemployment could have adverse implications for national development,

including a loss of their potential contribution to nation building, increased poverty and vulnerability,

and pose a potential threat to the social fabric and national security.

43. Gender: Unemployment is 5.8 percent amongst women compared to 2.8 percent amongst

men (ILFS, 2006); and the former constitute about 89 percent of the labor force. The HBS (2007)

estimates that average earnings for men is 1.7 times higher than women. Though gender parity in

primary school has been consistently good and parity has been attained at the national level, girls in

some regions face difficulties in completing the primary cycle. At the secondary level, proportion of

girls in government schools is still below 45 percent in Form One and below 35 percent in Form Six.

In 2010 Global Gender Gap Report, Tanzania had a Gender Development Index of 0.68 and was

ranked 66 out of 134 countries. This suggests a moderately high male/female gender disparity. To

address this disparity, Tanzania is a signatory to several international treaties including the

Convention on the Elimination of all forms of Discrimination against Women. A dedicated ministry

has also been established to provide leadership on gender equality and formulates gender sensitive

policies/Action Plans to advance women empowerment.

Environment and Climate Change

44. Tanzania faces various environmental challenges, many of which have significant bearing on

government policy choices. Human impacts on deforestation, soil erosion, overgrazing, and abuse of

water resources and loss of biodiversity have all contributed to significant land degradation. Poor

agricultural practices such as shifting cultivation, lack of crop rotation, inadequate agricultural

technology and land husbandry techniques further exacerbate the problem. Pollution is also a major

problem in urban areas, particularly with improper treatment and disposal of solid and liquid waste.

Most recently, there have been challenges in the management of mineral resources, particularly with

prospecting and mining practices and their environmental and social impacts.

45. With regard to climate change and its impact, a 2009 assessment revealed the following

environmental challenges: (a) steady increase in temperature for the past 30 years; (b) severe and

recurrent droughts in the past few years, with over 60 percent of land facing serious desertification;

(c) dramatic drop of water levels in all lakes (e.g., Lake Victoria dropped by 2.57 meters between

1965 and 2006); and (d) loss of about 80 percent of the glacier on Mount Kilimanjaro since 1912,

with projections of total glacier loss by 2025. The GoT, with the support of the Norwegian

government, is developing a national climate change adaptation and mitigation plan. A pilot program

was launched as part of that plan to reduce deforestation, develop methodologies for carbon

accounting, promote research and capacity building, as well as to promote Public Private

Partnerships to enhance investments in sustainable management of forest resources. The GoT also

launched a task force to help develop a National Strategy for Reducing Emissions from Deforestation

and Forest Degradation (REDD) and for enhancement of voluntary carbon market in Tanzania,

which presents an opportunity for Bank intervention in this agenda.

III. STRATEGIC OPTIONS

Country Strategic Framework

46. Tanzania‘s overall development framework and long-term social and economic development

goals are laid out in the National Vision 2025 and Zanzibar Vision 2020. The medium-term

objectives for Mainland Tanzania and Zanzibar are guided by the NSGRP II and ZSGRP II, both of

which make up the national development strategy approved at the end of 2010, and to be

implemented over the period 2010/2011 – 2014/2015.

10

47. The Mainland development strategy focuses on three broad clusters: (i) growth and reduction

of income poverty; (ii) improvement of quality of life and social well-being; and (iii) governance and

accountability. Similarly, Zanzibar‘s development strategy focuses on three clusters: (i) growth and

reduction of income poverty; (ii) improvement of social services and well-being; and (iii) good

governance and national unity. The strategies are fully linked with the MDGs, and encompass key

sectors and cross-cutting issues, including private sector development.

48. According to a Joint Staff Advisory Note (JSAN) published by the IMF and the World Bank

in January 2011, the ambitious projections underlying the new national development strategy (8.5%

growth annually) will require policy interventions on multiple fronts. Furthermore, whereas the

JSAN lauds the strategy‘s focus on agriculture and social sectors, particularly education quality, it

also points out that priority should be accorded to infrastructure projects, especially those most

pivotal for private sector-led growth. The JSAN also points to the need to accelerate implementation

of PFM and anti-corruption reforms.

Strengths and Opportunities

49. Geographic Location: Tanzania is the largest country in the EAC and a major import/export

gateway for two members: Burundi and Rwanda. It also has the potential to provide transport and

logistics services for its landlocked neighbors: Eastern Congo, Malawi, Uganda and Zambia. With

800 kilometers of coastline along the Indian Ocean and long historic linkages with the Middle East

and Asia, this vantage location could be better exploited to offer more efficient port services and

related transport logistics crucial for the movement of goods and deepening regional integration.

50. Natural Resources: Tanzania is endowed with rich natural resources, including: land, water

bodies, forest reserves, wildlife, exploitable hydrocarbons and minerals.25

Transforming these

resources through sustainable productive activities into higher value and exportable products could

enable the country to attain the national development strategy‘s vision of a stronger, more balanced,

broad-based and private sector-driven economy. For example, Tanzania controls 55 percent of Lake

Victoria, the largest fresh-water lake in Africa. The yearly fish quota for the Lake is 730,000 tons.

Yet, Tanzania lags behind Kenya in processed fish and fish exports.

51. Tourism: This sector offers various employment opportunities both directly (supporting over

200,000 jobs) and indirectly. In 2009, there were about 700,000 tourist arrivals, and total receipts

from tourism amounted to $1.3 billion in 2009. While tourism is significant in certain parts of the

country, overall there is still more room for growth. Earnings from the sector could be significantly

enhanced by strengthening regulatory and support policy framework, marketing of the sector‘s key

attractions, ensuring sustainable utilization of wildlife and other natural resources, and incentivizing

private investors to undertake infrastructure improvements.

52. Foreign Investment Destination: Tanzania has emerged as an attractive FDI destination partly

due to its political stability, its location with a vast hinterland, and its favorable investment laws—

though saddled with cumbersome implementation challenges. Recent years have seen sharp increases

in FDI, reaching US$ 744 million in 2008 and US$ 650 million in 2009; with most investments

going to the mining sector. FDI is expected to increase if the country enacts more comprehensive

regulatory reforms and addresses infrastructure bottlenecks. Likewise, harmonization of mainland

Tanzania and Zanzibar‘s foreign investment regimes would further boost the prospect.

Challenges and Weaknesses

53. High Level of Poverty and low human development: As discussed earlier (paragraph 39),

despite recent sound macroeconomic achievements, Tanzania remains poor, with growth occurring

in sectors with limited impact on the income levels of most citizens. The 2010 per capita income of

approximately $45326

is low and a large proportion of its 44 million people have limited access to

25 A 2011 Extractive Industries Transparency Initiative report has pointed out that while the country is endowed with rich mineral resources, there are substantial discrepancies between the Government‘s reported revenue from the sector and that reported by mining firms. 26

In U.S. dollars, at 2000 prices, using 2000 exchange rates

11

Chart 6:

Infrastructure Indicators 2009,

(Rank in World Countries)

Source: AfDB Statistics Dept. using data from the WEF,

2010

education, health and other basic services. Translating economic growth into increased poverty

reduction remains the foremost challenge.

54. Substantial Dependence on Aid: Approximately 30 percent of government spending depends

on foreign aid; making Tanzania one of the largest recipients of foreign aid in Sub-Saharan Africa.

This renders the country vulnerable to global economic shocks. Tanzania needs to rectify the

situation by, among other things, strengthening domestic resource mobilization instruments, reining-

in government expenditures and expanding economic activities in the private sector.

55. Infrastructure: The state of transport, energy, water and port facilities is still very poor and in

urgent need of Government action. The power sector is

characterized by exceptionally high demand in the face of

limited supply; even by the standards of other low income

African countries (Chart 6).27

Despite major investments in

the water sector from the 1970s to the 1990s, water supply

and sanitation services remain inadequate. The 2007 HBS

showed that from 2000 to 2007, access to safe water

declined by 10 percent in urban and 6 percent in rural

areas.28

Similarly, the Dar es Salaam port has serious

capacity constraints caused by high traffic growth and poor

backward linkages with inland transport networks, making

the port inefficient and causing a major bottleneck for the

national and regional economies. The poor condition of the

rail sub-sector has caused a shift of freight to road transport

which, in turn, has resulted in the deterioration of the

already crumbling bitumen network due to movement of

heavy goods vehicles. (See Annex XIII)

56. Governance: The public sector is characterized by weak financial controls and accountability,

which translate into significant resource leakages (see paragraphs 21-27). There is an urgent need for

improving internal controls within IFMIS, including better cash management in the control of funds

and rolling out of IFMIS to Local Government Authorities (LGAs). Likewise, budget management

needs to be better integrated in transparent and realistic medium-term expenditure and borrowing

plans and underpinned by vigorous oversight systems and structures. Particular challenges remain

with the public procurement system, especially with regard to the number and quality of procurement

practitioners at LGA level. Lastly, knowledge of the Public Procurement Act and its regulations

requires significant enhancement. This is particularly so, given Tanzania‘s decentralization trends

and Partner‘s growing commitment to use national procurement systems.

57. Agriculture: The agricultural sector presents particular challenges with direct linkages to

growth, poverty, and competitiveness (see paragraphs 8 and 39). In general, yields are low, while

productions costs are high and income remains meager. Various price and export controls in the

sector risk undermining market conditions and jeopardizing long-term sustainability. The new

National Development Strategy emphasizes improvement in technological inputs, rural infrastructure

and small holder financing (including through creation of an Agricultural Bank). There is, however,

a need to fully integrate such interventions into a commercial value chain, which is indispensible for

attracting large investments in the sector and realizing scale economies. This investment is crucial,

especially in transportation, processing and marketing of agricultural produce, a significant

proportion of which is currently wasted through post-harvest losses.

27 These challenges are mostly the result of a lack of investment over time, failure of privatization strategies, lack of diversification in energy sources,

governance issues, difficulties in access financing, and failure in timely implementation of projects. 28 The HBS was based on data from selected samples of the population and a full census will be carried out in 2012. It should be noted that in order to

address sector challenges, the GoT replaced its previous policy of free water provision and adopted instead a new National Water Policy in 2002, which

focused on cost recovery, sustainability, and integrated water resources management. The GoT has also developed a sector strategy and a regulatory framework for sustained delivery of water services. A Water Sector Development Program, which started in 2007 is now in its fourth year of

implementation, involving 280 Implementing Agencies and a funding envelope of $1,200 million over a five-year period.

12

58. Human Capital: At present, much of Tanzania‘s post-primary education system exhibits

severe quality deficiencies, with system expansion in recent years being an aggravating factor. Rapid

and chaotic expansion has left many public sector institutions severely under-funded. Meanwhile,

private for-profit education institutions are focused on short-term, market-driven demands that has

resulted in, among other things, a general lack of skills and marked skills mismatch.29

59. Private Sector Environment: Tanzania‘s private sector is constrained by several factors

including infrastructure bottlenecks, an underdeveloped financial sector and weak human and

institutional (particularly, regulatory) capacity. Further deregulation of the economy and reduction in

the cumbersome bureaucracy will significantly improve the enabling environment. This can be

achieved by creating catalytic and demonstration effects for entrepreneurs as highlighted in the

national development strategy.

60. Other Challenges: High population growth rate of 3 percent will adversely impact on the

country‘s development, especially in the areas of social outcomes, provision of services and sizeable

youth unemployment and underemployment. This rapidly expanding population, majority of which

is still in the informal sector, along with a high prevalence of HIV/AIDS will also negatively impact

the attainment of key MDGs. Unfettered urbanization due to the lack of an appropriate policy and

proliferation of informal settlements and poor housing construction further aggravates the situation.30

61. The Island of Zanzibar also has several unique issues. It has a very small economy ($589

million GDP); high poverty levels (about 40% living below basic needs poverty line) and weak

linkages between tourism (which is the lead sector) and other sectors of its economy. Logistical

difficulties due to distance between its main Islands – Unguja and Pemba and power problems

resulting from its continued dependence on the unreliable supply from the Mainland also pose unique

challenges. These constraints offer possibilities for effective Bank intervention.

Aid Coordination/Harmonization

62. Recent Developments: The Bank has made notable strides towards effectively harmonizing

its operations with the Paris Declaration and the Accra Agenda for Action. The Development

Partners Group (DPG) has been the main conduit through which the Bank and other Partners have

engaged with Government and other stakeholders to strengthen development cooperation.

63. Starting in 2006, aid management has been guided by the Joint Assistance Strategy (JAST),

which sought to operationalize international principles of aid effectiveness. The Bank‘s Cover Note

to the Board described its specific approach and programs, which were aligned to the pillars in the

national development strategy. The new aid strategy, which had its challenges (Annex XI), reflected

a re-orientation from traditional project financing towards basket funding and increased contributions

through GBS. It also required strong contribution by each partner to the policy dialogue on sector-

specific issues.

64. In the years since, there has been a shift towards GBS and more Partners alignment to sector-

funding baskets. A recently finalized new Partnership Framework Memorandum sets out the

partnership terms between GoT and Development Partners in respect to budget support. The

Memorandum outlines the underlying principles for a harmonized approach to aid coordination,

particularly at a time when several Partners, both in Tanzania and elsewhere, are re-evaluating

budget support as the preferred aid instrument.

65. The Bank is a member of the Development Partners Group and chaired the Poverty

Reduction and Budget Support donor group from April 2009 to April 2010. Under this framework,

there is a well-established structure for dialogue which consists of four clusters, 26 thematic working

29 In 2006, the Government introduced a ‗Vocational Education & Training Levy‘ payable at the end of every month, from every employer who has four or more employees. The uses as well as impact of the Levy remain unclear. 30 The urbanization challenge also has potential upsides as it signals an upward trend in urban land prices, construction activity, and greater

concentration of the labor force in urban areas (particularly among the middle class with increasing discretionary income). This could be good for the country‘s construction industry (both material manufacturers and builders, which would include SMEs). From a Bank operations perspective, it would

also open up opportunities in terms of housing and mortgage lending-sector financing.

13

Chart 7: Composition and Commitment by

Sector since 1971 (as at 22 June 2011)

groups and seven sector working groups. There are also working groups associated with the basket

funding in each sector. The Bank will continue to coordinate and harmonize its interventions through

active participation in various thematic and sector working groups.31

Key Development Partners and Areas of Focus:

66. Tanzania‘s aid architecture comprises of various multilateral/bilateral Partners. Multilaterals

consist of the AfDB, World Bank, the European Commission, the International Monetary Fund, and

17 UN agencies.32

Collectively, the Partners Group forms a key force in strengthening aid

effectiveness. Their comparative advantage in resource mobilization and capacity development help

shape the mechanism of aid management and provides guidance on harmonization and alignment

through senior level monthly meetings. In addition, 17 bilateral Partners work alongside multilateral

ones. Having been involved in Tanzania for many years (some since Independence), development

partrners have acquired extensive knowledge of local development dynamics and bring to the table

invaluable insights as well as considerable financial resources. The bilateral DPs are: Belgium,

Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, Norway, Spain,

Sweden, Switzerland, UK and USA. In recent years, China, Korea and New Zealand have also

participated in some of the DPG gatherings. A summary of the division of labor between Partners

appears in Annex XII.

Bank Group’s positioning in Tanzania

67. Cumulative Operations: Since 1971, the Bank

has approved 103 operations in Tanzania, with a total

commitment, net of cancellations, amounting to UA

1.55 billion. Of which, transport accounted for 28

percent, followed by multi-sector (23%)33

, public

utilities (21%), agriculture (15%), social sector (10%)

and private sector (3%) (Chart 7). Bulk of the overall

commitment was financed by ADF (95.4%), followed

by ADB (3.4%), NTF (0.8%) and Private Sector

window (0.4%). The Bank has been particularly felt

in infrastructure, agriculture, and, more recently, in

human resource development and budget support.

Recent successfully completed operations include:

Agriculture Sector Development Program I, Alternative Learning Skills Development I, and Poverty

Reduction Support II.

68. Ongoing Operations: The current portfolio consists of 21 ongoing operations (including

national, regional and private sector) with a total commitment of UA 600.17 million.34

Of this

amount, 94 percent is allocated to the public sector, 4.9 percent to regional operations and 1.1

percent to private sector (see Annex III). The disbursement rate for ongoing operations is 24.86

percent.35

Infrastructure (transport, energy, and water) represents 70 percent of total commitments.

However, there has been a growing emphasis on both general and sector budget support, which have

expanded from one operation in 2005 to four in 2009 ( education, agriculture and water sectors).

69. Portfolio Performance: With an assessment score of 2.2 out of 3 in 2011, overall

performance of the Tanzania portfolio is rated satisfactory. However, several challenges remain

31 The transport, agriculture, water, public financial management and social sector experts at Tanzania field office actively participate in donor

coordination activities in the respective sectors. Similarly, TZFO staff represents the Bank in the other fronts of donor coordination. 32 The UN agencies active in Tanzania are: FAO, IFAD, ILO, IOM, UNAIDS, UNDP, UNCDF, UNEP, UNESCO, UNFPA, UNHCR, UNICEF,

UNIDO, UNIFEM, WFP, WHO, and UN-HABITAT. 33 To date, eight of the Bank‘s multi-sector interventions have been Policy Based Operations (PBOs) and seven Institutional Support Projects (ISPs) that have incorporated elements targeted at enhancing the transparency and accountability in the management of financial resources. 34 Out of the 14 ongoing public sector operations, there are 2 stand-alone projects for Zanzibar and 4 having components both in Zanzibar and the

Mainland. 35 Of the total ongoing commitment, 22% was approved in the last quarter of 2010, and therefore, there are 3 national and 2 regional operations which

are not yet effective as of May 2011.

14

including: (i) limited understanding of Bank rules and procedures; (ii) low financial management

capacity at local government levels; (iii) low and inadequate staffing of implementing agencies; (iv)

delays in fulfillment of loan and grant conditions and project start-up activities; and (v) persistent

procurement problems. Typically, projects experience protracted delays during the bid evaluation

and contract award stages.36

More accurate and elaborate planning of procurement activities, timely

approval of documents by the Ministerial Tender Board and the Bank, and capacity building of

procurement specialists in the implementing agencies should substantially improve procurement

performance.37

70. Projects at Risk (PAR): These decreased from six operations in 2009 to four in 2011 (see

Annex III). This means that the proportion of at risk projects in 2011 fell to 28.6 percent from 35

percent in 2009; ranked well below the Bank‘s average of 45 percent. The at risk projects consist

two Potentially Problematic Projects and two Problem Projects, leading to a Commitment at Risk

(CAR) level of 16.7 percent in 2011 compared to 14.2 percent in 2009.

71. Portfolio Age: The average age of current projects is 2.8 years, compared to 4.5 years in 2009.

There are currently no operations that fall within the category of ageing projects (i.e., 8 years or

above). The time lapse from approval to effectiveness currently stands at 7.7 months, which again is

shorter than the Bank‘s target of 12 months. The average project size increased from UA 33.3

million in 2009 to UA 40.4 million in 2011.

72. Lessons from the Portfolio Improvement Plan38

: A CPPR workshop was held in March to

review implementation status of the 2009 CPIP (see Annex IV) and prepare the 2011 CPIP. A key

lesson from the review is the need for sector specialists in the Field Office to more proactively

engage in the pre-appraisal stage of projects. This should include carrying out fiduciary assessments

to identify weaknesses and incorporate necessary mitigation measures at the design stage. A second

and related lesson is that specialists should actively monitor project activities above and beyond the

standard twice-a-year supervision. This will allow for better tracking of core sector indicators and

improve on performance; including addressing issues before they become a problem (see Annex V

for key actions required as highlighted in the 2011 CPIP). A revamped Country Office and additional

resources through ongoing decentralization efforts are expected to enhance portfolio performance.

73. Lessons from implementation of the 2006-2010 Country Strategy: Key lessons that have

informed the proposed Strategy include: (i) increasing selectivity as per the Medium Term Strategy,

thereby concentrating on sectors where the Bank has comparative advantage; (ii) maintaining candid

and sustained dialogue with Government; (iii) maintaining effective and pro-active communication

and information flow between all parties involved in Bank operations; (iv) close supervision of all

operations, and more regular review of portfolio performance (at least every two years); (v) close

cooperation and coordination with other Partners; and (vi) expanding non-lending activities with

particular focus on more Economic and Sector Work to inform the Bank operations and advisory

services to government based on policy-based knowledge products; and (vii) increasing the size of

operations to benefit from scale economies and increase efficiency in project implementation.

74. The previous CSP/JAST Completion Report further finds that the Bank‘s strategy responded

to Government priorities (See Annex II), and that its operations were aligned with the pillars

articulated in the national development strategy, namely: (i) growth and reduction of income poverty;

(ii) improved quality of life and social well-being; and (iii) good governance and accountability.

36 The slow pace of bids evaluation, contract award and other procurement constraints are mostly the result of missing or insufficient procurement

assessment during project design. Most designs of the past as well as ongoing projects did not carry out proper assessment on public procurement practices as well as on the capacity of implementing agencies in carrying out required procurement activities of respective projects. Only during

projects‘ implementation are these shortcomings observed, introducing poor and/or delayed procurement. 37 Procurement planning, which is very crucial for successful project implementation, should start from the projects‘ preparation stages and procurement training/support should be based on the capacity assessments of implementing agency during the projects‘ designs. 38 Many of these lessons come out of a CPPR questionnaire that was sent to 60 participants (project personnel, Ministry of Finance officials and

Development partners) to provide responses (50% response rate) to issues related to project implementation such as procurement, financial management and monitoring and evaluation. The results were discussed and reviewed at the CPPR workshop (21st March 2011), which led to the

updating of the 2009 Country Portfolio Improvement Plan (CPIP) as well as the development of the 2011 CPIP (see Annex V).

15

Chart 8: Pillars for Bank Support

Bank Group support focused mainly on the first two pillars, but recognizing the importance of

governance and accountability, it remained active in the third pillar through the Institutional Support

for Good Governance project. The Bank‘s multi-sector operations contributed to macroeconomic

stability, while in the agriculture and microfinance sectors, the contribution was mainly through the

development of marketing systems and access to finance, respectively. Tanzania‘s notable progress

in the social sector also benefited from Bank interventions, mainly targeted at improving service

provision through infrastructure development (construction of class rooms and health facilities).

75. Concerning aid modalities, the Bank made significant progress on harmonization as

demonstrated by the increase in GBS and SBS operations. Additional areas of Bank improvement in

donor harmonization include doing away with separate Project Completion Reports (PCRs) from

implementing agencies and the use of parallel monitoring indicators.

IV. BANK GROUP STRATEGY

Rationale for Bank Group Intervention

76. Tanzania has recorded robust macroeconomic performance over the last two decades. To be

translated into tangible and lasting benefits for the majority of Tanzanians, growth must be