tata group egm proposals for removal of mr. cyrus … · tata group egm proposals for removal of...

TRANSCRIPT

7 DECEMBER 2016

TATA GROUP EGM PROPOSALS 1 | P A G E

INGOVERN VIEWS AND RECOMMENDATIONS

Tata Group EGM Proposals for Removal of Mr. Cyrus Mistry as Director

Six of the seven Tata listed group companies where Mr. Cyrus Mistry serves as a Director,

have called for EGMs between 13th December and 26th December 2016 for removal of Mr.

Mistry as a Director, after having received requisition from the promoter shareholder Tata

Sons Limited. Tata Global Beverages, having already replaced Mr. Mistry as Chairman, is yet

to announce the date and notice of its EGM.

Following are details of EGMs and the proposals as requisitioned by Tata Sons Ltd.

1) Tata Consultancy Services Ltd – 13th December 2016

Removal of CP Mistry as a Director

2) The Indian Hotels Company Ltd – 20th December 2016

Removal of CP Mistry as a Director

3) Tata Steel Ltd – 21st December 2016

Removal of CP Mistry as a Director

Removal of Nusli Wadia as a Director

4) Tata Motors Ltd – 22nd December 2016

Removal of CP Mistry as a Director

Removal of Nusli Wadia as a Director

5) Tata Chemicals Ltd – 23rd December 2016

Removal of CP Mistry as a Director

Removal of Nusli Wadia as a Director

Appointment of Bhaskar Bhat as a Director

Appointment of S. Padmanabhan as a Director

6) Tata Power Ltd – 26th December 2016

Removal of CP Mistry as a Director

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 2 | P A G E

Case of Individual Companies

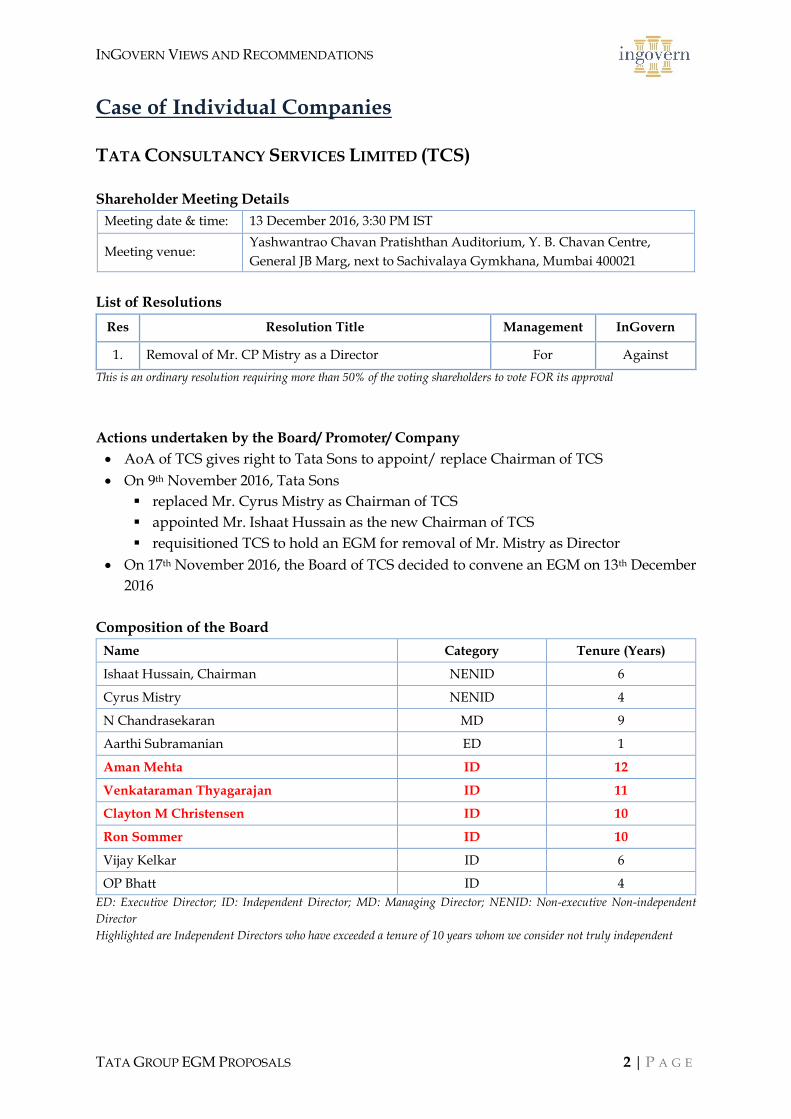

TATA CONSULTANCY SERVICES LIMITED (TCS)

Shareholder Meeting Details

Meeting date & time: 13 December 2016, 3:30 PM IST

Meeting venue: Yashwantrao Chavan Pratishthan Auditorium, Y. B. Chavan Centre,

General JB Marg, next to Sachivalaya Gymkhana, Mumbai 400021

List of Resolutions

Res Resolution Title Management InGovern

1. Removal of Mr. CP Mistry as a Director For Against

This is an ordinary resolution requiring more than 50% of the voting shareholders to vote FOR its approval

Actions undertaken by the Board/ Promoter/ Company

AoA of TCS gives right to Tata Sons to appoint/ replace Chairman of TCS

On 9th November 2016, Tata Sons

replaced Mr. Cyrus Mistry as Chairman of TCS

appointed Mr. Ishaat Hussain as the new Chairman of TCS

requisitioned TCS to hold an EGM for removal of Mr. Mistry as Director

On 17th November 2016, the Board of TCS decided to convene an EGM on 13th December

2016

Composition of the Board

Name Category Tenure (Years)

Ishaat Hussain, Chairman NENID 6

Cyrus Mistry NENID 4

N Chandrasekaran MD 9

Aarthi Subramanian ED 1

Aman Mehta ID 12

Venkataraman Thyagarajan ID 11

Clayton M Christensen ID 10

Ron Sommer ID 10

Vijay Kelkar ID 6

OP Bhatt ID 4

ED: Executive Director; ID: Independent Director; MD: Managing Director; NENID: Non-executive Non-independent

Director

Highlighted are Independent Directors who have exceeded a tenure of 10 years whom we consider not truly independent

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 3 | P A G E

The Articles of Association of TCS gives the authority to Tata Sons to appoint and replace the

Chairman of Board of TCS. On basis of this, on 9th November 2016, Tata Sons replaced Mr.

Mistry with Mr. Ishaat Hussain as Chairman of TCS.

Tata Sons holds 73.26% of equity capital of TCS and other promoter entities hold 0.07%,

resulting in total 73.33% equity stake. Since the proposal of removal of Mr. Mistry from the

Board is an ordinary resolution, it is certain that the proposal will pass with requisite majority.

In case of TCS where the Board has not expressed any opinions contrary to that of Tata Sons

and has replaced Mr. Mistry as its Chairman and it is a certainty that the proposal for his

removal will be passed given the promoter’s 73.33% voting power, it is prudent for Mr. Mistry,

to protect further damage to his reputation, to resign from the Board before the EGM.

InGovern Recommendation

The proposal for Mr. Mistry’s removal as a Director is because of his replacement as Chairman

in Tata Sons Limited. As per Tata Sons, one of the primary reasons of his replacement was

non-performance of Tata companies excluding TCS and JLR. Hence, since the promoter itself

accepts that the performance of TCS has been good, we do not see any logic as to why a

shareholder should vote FOR removal of a Director who was the Chairman, for performance

issues.

Secondly, the section on Board Evaluation in the FY16 Annual Report of TCS states:

“The board and the nomination and remuneration committee reviewed the performance of the

individual directors on the basis of the criteria such as the contribution of the individual director to the

board and committee meetings like preparedness on the issues to be discussed, meaningful and

constructive contribution and inputs in meetings, etc. In addition, the chairman was also evaluated on

the key aspects of his role.

In a separate meeting of independent directors, performance of non-independent directors, performance

of the board as a whole and performance of the chairman was evaluated, taking into account the views

of executive directors and non-executive directors.”

Since there is no negative commentary about Mr. Mistry’s evaluation as a Chairman, it is

assumed that he had got a favourable rating from the Board. However, the Board, in the

explanatory statement to the proposal, expresses that it agrees that removal of Mr. Mistry

would be in the best interests of the company.

We seek a logic as to why the Board has recommended removal of a Director who was given

a favourable rating in his evaluation as Chairman a few months back itself. The plausible

reason is that he was a nominee of Tata Sons on Board of TCS and since he was replaced as

Chairman of Tata Sons, it is natural that he is removed from the Board of TCS.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 4 | P A G E

A logical consequence of change in designation at Tata Sons would be replacement as

Chairman of TCS, which has been duly effected with Mr. Ishaat Hussain being appointed as

the new Chairman. However, we believe his removal from the Board altogether is not the best

outcome for the company.

Consider SP Group’s (which is represented by Mr. Mistry) beneficial interest in TCS. SP Group

holds ~18.4% in Tata Sons which holds 73.33% in TCS. This gives SP Group a beneficial

interest of 13.48% in TCS. If this beneficial interest had been a direct stake in the company, it

would have been the largest stake after the promoters and much higher than the largest public

shareholder LIC’s 3.21% stake in TCS. For a director representing a beneficial stake of 13.47%

which ranks second among all shareholders of the company, and having received a favourable

rating in his evaluation, there are no logic for his removal from the Board. On the contrary,

his beneficial stake of 13.47% would reflect his ‘skin-in-the-game’ i.e., alignment of his interests

with that of the company and hence would be in best interests of the company.

Another reason attributed to his removal is the possibility that his presence on the Board may

create an environment of constant conflict and discord on the Board. We do not believe this

hypothesis as it has been historically proved that the effectiveness of the Board increases when

there are directors with an opposing point of view and who are not supposedly ‘Yes-Men’ of

the promoters in the Board.

On basis of these points, we recommend shareholders vote AGAINST Mr. Mistry’s removal

from the Board of TCS.

Although this resolution will ultimately get passed with a certainty due to the promoter

exercising its 73.33% voting power, an AGAINST vote by minority shareholders will serve as

a signal of their opinion to the Board of Directors.

With regards to the articles of association of TCS giving the authority to Tata Sons to appoint

and replace Chairman of Board of TCS without the need to seek prior opinion of the Board,

we believe such a provision greatly restricts the powers of the Board while giving a

shareholder extra rights over that of other shareholders. Not letting the directors –

representative of all shareholders – to appoint their leader is also an abuse of rights of the

minority shareholders of the company. We recommend shareholders raise concern that such

a provision be removed from the articles of association of TCS and the Board is given the right

to appoint its own Chairman.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 5 | P A G E

THE INDIAN HOTELS COMPANY LIMITED

Meeting Details

Meeting date & time: 20 December 2016, 11:00 AM IST

Meeting venue: Indian Merchant Chamber (IMC) Building, IMC Marg, Churchgate, Mumbai – 400020

List of Resolutions

Res Resolution Title Management* InGovern

1. Removal of Mr. CP Mistry as a Director - Against

This is an ordinary resolution requiring more than 50% of the voting shareholders to vote FOR its approval * The Board has not recommended either in favour or against the resolution

Actions undertaken by the Board/ Promoter/ Company

On 4th November 2016, a meeting of Independent Directors was held in which they

unanimously expressed their full confidence in Mr. Cyrus Mistry as their Chairman

On 9th November 2016, Tata Sons requisitioned Indian Hotels to hold an EGM for removal

of Mr. Mistry as Director

On 21st November 2016, the Board decided to convene an EGM on 20th December 2016

Composition of the Board

Name Category Tenure (Years)

Cyrus Mistry NENID 4

Shapoor Mistry NENID 13

Keki B Dadiseth ID 16

Deepak Parekh ID 16

Nadir B Godrej ID 8

Ireena Vittal ID 3

Vibha Paul Rishi ID 2

Gautam Banerjee ID 2

Rakesh Sarna MD 2

Mehernosh S Kapadia ED 5

ED: Executive Director; ID: Independent Director; MD: Managing Director; NENID: Non-executive Non-Independent

Director

Highlighted are Independent Directors who have exceeded a tenure of 10 years whom we consider not truly independent

The Independent Directors, who are in the majority in the Boards, have come out in the public

and expressed their full confidence in Mr. Mistry as Chairman of Indian Hotels. Despite this

public endorsement by the directors, the promoter – Tata Sons has proposed removal of Mr.

Mistry as a Director which will automatically remove him as the Chairman.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 6 | P A G E

InGovern Recommendations

Independent Directors should represent the interests of all, including minority shareholders,

and think about the needs of creating a sustainable company. The Companies Act’s code for

independent directors requires them to “safeguard the interests of all stakeholders” and to

“balance the conflicting interest of the stakeholders.” The Independent Directors of Indian

Hotels had expressed their full confidence on Mr. Mistry as their Chairman. The action of Tata

Sons for persisting with the removal of Mr. Mistry as a Director shows the promoter’s

disregard for the opinions of the Independent Directors.

Also, singling out Mr. Mistry for performance issues in these companies doesn’t seem fair. A

Chairman is the leader of the Board which supervises the management and sets the strategy

of the company. However, in a non-executive capacity, the Chairman doesn’t have control on

the day-to-day management of the company and cannot be held solely responsible for poor

performance of the company. Mr. Rakesh Sarna is the Managing Director and Mr. Mehernosh

S Kapadia is the Executive Director of Indian Hotels. Collectively, the Key Management

Personnel and the whole Board of Directors should be held responsible for the poor

performance of the company.

Also, since there is no negative commentary about Mr. Mistry’s evaluation as a Chairman in

these companies, it is assumed that he had got a favourable rating from the respective Boards.

Hence, there is no reason for his removal from the Board after receiving favourable evaluation

from the Boards.

Also, SP Group’s beneficial interest in Indian Hotels is around 5.15%. With no governance

issues regarding Mr. Mistry and considering his significant beneficial interests in these

companies, it is prudent to allow Mr. Mistry to continue in these Boards.

Indian Hotels is an associate company of Tata Sons as it owns less than 50% in Indian Hotels.

Tata Sons directly owns 28.01% and along with other Tata group companies (which include

listed companies as well), own 38.65% in Indian Hotels.

Most importantly, although Tata Sons has proposed removal of Mr. Mistry as Director, it has

not articulated to the public shareholders any specific plans and the way forward for the

company. Unless they explain how their plan is different from what the Board under Mr.

Mistry envisaged for the company, public shareholders will not be able to take an informed

decision.

On basis of these points, we recommend shareholders vote AGAINST Mr. Mistry’s removal

from the Board of Indian Hotels. There is no compelling logic for his removal as Director and

given the support of other Directors on the Board, his continuance would be in best interests

of the company.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 7 | P A G E

TATA STEEL LIMITED

Shareholder Meeting Details

Meeting date & time: 21 December 2016, 3:00 PM IST

Meeting venue: Birla Matushri Sabhagar, 19, Sir Vithaldas Thackersey Marg, Mumbai –

400020

List of Resolutions

Res Resolution Title Management* InGovern

1. Removal of Mr. CP Mistry as a Director - Against

2. Removal of Mr. Nusli Wadia as a Director - Against

These are ordinary resolutions requiring more than 50% of the voting shareholders to vote FOR approval

* The Board has not recommended either in favour or against the resolution

Actions undertaken by the Board/ Promoter/ Company

On 10th November 2016, Tata Sons requisitioned Tata Steel to hold an EGM for removal

of Mr. Mistry and Mr. Wadia as Directors

On 25th November 2016, the Board decided to convene an EGM on 21st December 2016

Also on 25th November 2016, the Board replaced Mr. Cyrus Mistry as its Chairman

through circular resolutions

The Board then appointed Mr. OP Bhatt as its Chairman till the EGM

Composition of the Board

Name Category Tenure (Years)

OP Bhatt, Chairman ID 3

Cyrus Mistry NENID 4

Nusli Wadia ID 37

Ishaat Hussain NENID 17

Subodh Bhargava ID 10

Jacobus Schraven ID 9

Mallika Srinivasan ID 4

DK Mehrotra NENID 4

Andrew Robb ID 2

Koushik Chatterjee ED 4

TV Narendran MD 2

ED: Executive Director; ID: Independent Director; MD: Managing Director; NENID: Non-executive Non-Independent

Director

Highlighted are Independent Directors who have exceeded a tenure of 10 years whom we consider not truly independent

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 8 | P A G E

InGovern Recommendations

The Board of Tata Steel replaced Mr. Mistry as its Chairman by passing circular resolutions

on 25 December 2016. In Tata Steel, we share the same concerns as we have for other Tata

Group companies.

The Board Evaluation section of FY2016 Integrated Report of Tata Steel states:

“The evaluation process endorsed the Board Members’ confidence in the ethical standards of the

Company, the cohesiveness that exists amongst the Board Members, the two-way candid

communication between the Board and the Management and the openness of the Management in

sharing strategic information to enable Board Members to discharge their responsibilities.”

Considering such a positive evaluation of the Board under the leadership of its Chairman, the

logic of removal of Mr. Mistry as Director doesn’t carry weight. If indeed the performance of

the company where to matter, the Key Management Personnel and the whole Board of

Directors should be held responsible for the poor performance of the company. Mr. TV

Narendran is the Managing Director and Mr. Koushik Chatterjee is the Executive Director of

Tata Steel.

SP Group’s beneficial interest in Tata Steel is around 5.47%. With no governance issues

regarding Mr. Mistry and considering his significant beneficial interests, it is prudent to allow

Mr. Mistry to continue in the Board of Tata Steel.

Tata Sons directly owns 29.75% and along with other Tata group companies (which include

listed companies as well), own 31.35% in Tata Steel.

Most importantly, although Tata Sons has proposed removal of Mr. Mistry as Director, Tata

Sons has not articulated to the public shareholders any specific plans and the way forward for

the company. Unless there is a plan different from what the Board under Mr. Mistry envisaged

for the company, public shareholders will not be able to take an informed decision.

On basis of these points, we recommend shareholders vote AGAINST Mr. Mistry’s removal

from the Board of Tata Steel. There is no logic for his removal as Director and his continuance

would be in best interests of the company.

Regarding Mr. Wadia’s removal as a Director, InGovern, in an earlier vote recommendation

report on the company meetings, had recommended shareholders vote AGAINST his re-

appointment to the Board. However, the reason for recommending against was his tenure as

Mr. Wadia has been on Board of Tata Steel since 1979 (i.e., more than 37 years). His tenure is

far greater than the maximum tenure of 10 years for Independent Directors as per Companies

Act, 2013.

However, Tata Sons proposes his removal not because of his long tenure but because he has

expressed an opinion that is contrary to theirs. By stating that he is acting in concert with Mr.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 9 | P A G E

Mistry, Tata Sons has questioned the position of the Independence Directors. Promoters

removing Independent Directors who do not agree with their views also sets a bad precedent

for Indian corporate governance and such efforts should be thwarted by voting against the

promoter proposals.

In case Tata Sons believes that Mr. Wadia’s independence has been affected, it should also

propose removal of other Independent Directors of all its listed group companies with longer

tenures. A list of these directors on Boards of the seven companies is given below.

Independent Directors with tenures longer than 10 years

Tata Consultancy Services Limited

Name Tenure (Years)

Aman Mehta 12+

Venkataraman Thyagarajan 11+

Clayton M Christensen 10+

Ron Sommer 10+

The Indian Hotels Company Limited

Name Tenure (Years)

Deepak S Parekh 16+

Keki B Dadiseth 16+

Tata Steel Limited

Name Tenure (Years)

Nusli Wadia 37+

Subodh Bhargava 10+

Tata Motors Limited

Name Tenure (Years)

Nusli Wadia 18+

Tata Chemicals Limited

Name Tenure (Years)

Nusli Wadia 35+

Nasser Munjee 10+

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 10 | P A G E

Tata Power Limited

Name Tenure (Years)

Homiar Vachha 15+

Nawshir Mirza 10+

We recommend shareholders vote AGAINST Mr. Wadia’s removal from the board because,

the principle against his removal does not set a good precedent for the company or for Indian

corporate governance. However, shareholders should raise concern on the tenure of Mr.

Wadia.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 11 | P A G E

TATA MOTORS LIMITED

Shareholder Meeting Details

Meeting date & time: 22 December 2016, 3:00 PM IST

Meeting venue: Yashwantrao Chavan Pratishthan Auditorium, Y. B. Chavan Centre, General JB Marg, next to Sachivalaya Gymkhana, Mumbai 400021

List of Resolutions

Res Resolution Title Management InGovern

1. Removal of Mr. CP Mistry as a Director … Against

2. Removal of Mr. Nusli Wadia as a Director … Against

These are ordinary resolutions requiring more than 50% of the voting shareholders to vote FOR approval * The Board has not recommended either in favour or against the resolution

Actions undertaken by the Board/ Promoter/ Company

On 10th November 2016, Tata Sons requisitioned Tata Motors to hold an EGM for removal

of Mr. Mistry and Mr. Wadia as Directors

On 14th November 2016, a meeting of Independent Directors was held in which they

stated all decisions taken by the Board with regards to strategy, operations and business

have been unanimous and executed by Chairman and Management accordingly

On 23rd November 2016, the Board decided to convene an EGM on 22nd December 2016

Composition of the Board

Name Category Tenure (Years)

Cyrus Mistry NENID 4

Nusli Wadia ID 18

Raghunath Mashelkar ID 9

Nasser Munjee ID 8

Subodh Bhargava ID 8

Vinesh Jairath ID 7

Ralf Speth NENID 6

Falguni S Nayar ID 3

Guenter Butschek MD 1

Ravindra Pisharody ED 4

Satish Borwankar ED 4

ED: Executive Director; ID: Independent Director; MD: Managing Director; NENID: Non-executive Non-Independent

Director

Highlighted are Independent Directors who have exceeded a tenure of 10 years whom we consider not truly independent

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 12 | P A G E

InGovern Recommendations

Independent Directors represent the interest of all shareholders. The Independent Directors

of Tata Motors, through their meeting on 14 November 2016, emphasised on the collective

responsibility of the Board by stating all decisions taken by the Board with regards to strategy,

operations and business have been unanimous and executed by Chairman and Management

accordingly.

We believe if accountability is indeed put on the Board for non-performance, it should be all

the Directors of the Board as a collective. Mr. Gunter Butschek is the MD and CEO while Mr.

Ravindra Pisharody and Mr. Satish Borwankar are Executive Directors of Tata Motors. Mr.

Butschek was, however, a recent appointment having been appointed as MD and CEO in

February this year.

Also, since there is no negative commentary about Mr. Mistry’s evaluation as Chairman, it is

assumed that he had got a favourable rating from the Board of Tata Motors. Hence, there is

no reason as to his removal from the Board after receiving favourable evaluation from the

Board.

SP Group’s beneficial interest in Tata Motors is around 4.88%. With no governance issues

regarding Mr. Mistry and considering his significant beneficial interests, it is prudent to allow

Mr. Mistry to continue in the Board.

Tata Motors is an associate company of Tata Sons as its stake is less than 50% in Tata Motors.

Tata Sons directly owns 26.51% and along with other Tata group companies (which include

listed companies as well), own 32.43% in Tata Motors.

Most importantly, although Tata Sons has proposed removal of Mr. Mistry as Director, they

have not articulated to the public shareholders their specific plans, the way forward for the

company. Unless they explain how their plan is different from what Mr. Mistry envisaged for

the company, public shareholders will not be able to take an informed decision.

On basis of these points, we recommend shareholders vote AGAINST Mr. Mistry’s removal

from the Board of Tata Motors. There is no compelling logic for his removal as Director and

his continuance would be in best interests of the company.

Regarding Mr. Wadia’s removal as a Director of Tata Motors, InGovern, in its earlier vote

recommendation reports for the company, had recommended shareholders vote AGAINST

his re-appointment to the Board. However, our reason for recommending against was his

tenure on the Board as an Indepdent Director. Mr. Wadia has been on Board of Tata Motors

since 1998, i.e., more than 18 years which is greater than the maximum tenure of 10 years for

Independent Directors as per Companies Act, 2013.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 13 | P A G E

However, Tata Sons proposes his removal not because of his long tenure but because he has

expressed an opinion in Tata Motors that is contrary to theirs. By stating that he is acting in

concert with Mr. Mistry, Tata Sons has challenged the position of the Independence Directors.

Promoters removing Independent Directors who do not agree with their views also sets a bad

precedent for Indian corporate governance.

In case Tata Sons believes that Mr. Wadia’s independence has been affected, it should also

propose removal of all the Independent Directors of these companies with longer tenures.

We recommend shareholders vote AGAINST Mr. Wadia’s removal from the board because,

the principle against his removal does not set a good precedent for Indian corporate

governance. However, shareholders should raise concern on the tenure of Mr. Wadia.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 14 | P A G E

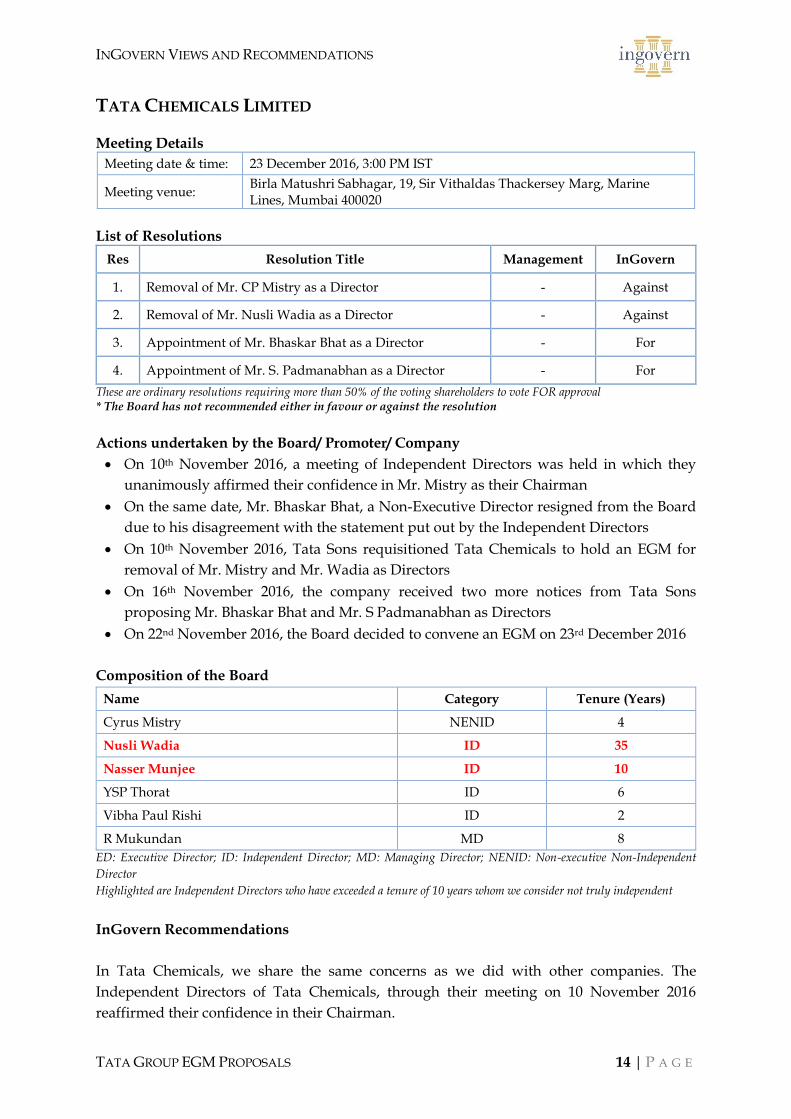

TATA CHEMICALS LIMITED

Meeting Details

Meeting date & time: 23 December 2016, 3:00 PM IST

Meeting venue: Birla Matushri Sabhagar, 19, Sir Vithaldas Thackersey Marg, Marine Lines, Mumbai 400020

List of Resolutions

Res Resolution Title Management InGovern

1. Removal of Mr. CP Mistry as a Director - Against

2. Removal of Mr. Nusli Wadia as a Director - Against

3. Appointment of Mr. Bhaskar Bhat as a Director - For

4. Appointment of Mr. S. Padmanabhan as a Director - For

These are ordinary resolutions requiring more than 50% of the voting shareholders to vote FOR approval * The Board has not recommended either in favour or against the resolution

Actions undertaken by the Board/ Promoter/ Company

On 10th November 2016, a meeting of Independent Directors was held in which they

unanimously affirmed their confidence in Mr. Mistry as their Chairman

On the same date, Mr. Bhaskar Bhat, a Non-Executive Director resigned from the Board

due to his disagreement with the statement put out by the Independent Directors

On 10th November 2016, Tata Sons requisitioned Tata Chemicals to hold an EGM for

removal of Mr. Mistry and Mr. Wadia as Directors

On 16th November 2016, the company received two more notices from Tata Sons

proposing Mr. Bhaskar Bhat and Mr. S Padmanabhan as Directors

On 22nd November 2016, the Board decided to convene an EGM on 23rd December 2016

Composition of the Board

Name Category Tenure (Years)

Cyrus Mistry NENID 4

Nusli Wadia ID 35

Nasser Munjee ID 10

YSP Thorat ID 6

Vibha Paul Rishi ID 2

R Mukundan MD 8

ED: Executive Director; ID: Independent Director; MD: Managing Director; NENID: Non-executive Non-Independent

Director

Highlighted are Independent Directors who have exceeded a tenure of 10 years whom we consider not truly independent

InGovern Recommendations

In Tata Chemicals, we share the same concerns as we did with other companies. The

Independent Directors of Tata Chemicals, through their meeting on 10 November 2016

reaffirmed their confidence in their Chairman.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 15 | P A G E

Tata Sons directly owns 19.35% and along with other Tata group companies (which include

listed companies as well), own 30.80% in Tata Chemicals. SP Group’s beneficial interest in

Tata Chemicals which is around 3.56%. With no governance issues regarding Mr. Mistry and

considering his significant beneficial interests, it is prudent to allow Mr. Mistry to continue in

the Board.

Also, Tata Sons has not articulated to the public shareholders their specific plans and the way

forward for Tata Chemicals. Unless they explain how their plan is different from what the

Board under Mr. Mistry envisaged for the company, public shareholders will not be able to

take an informed decision.

In line with our recommendations for other companies, we recommend shareholders vote

AGAINST Mr. Mistry’s removal from these Boards. There is no logic for his removal as

Director and his continuance would be in best interests of the company.

Regarding Mr. Wadia’s removal as a Director of Tata Chemicals, InGovern, in our earlier vote

recommendation reports at the AGM of the company, had recommending shareholders vote

against his re-appointment to the Board. Our reason for recommending against was his tenure

on the Board as an Independent Director. Mr. Wadia has been on Board of Tata Chemicals

since 1981, i.e., more than 35 years which is greater than the maximum tenure of 10 years for

Independent Directors as per Companies Act, 2013.

However, Tata Sons proposes his removal not because of his long tenure but because he has

expressed an opinion that is contrary to theirs. By stating that he is acting in concert with Mr.

Mistry, Tata Sons has shown disregard for the position of the Independence Directors.

Promoters removing Independent Directors who do not agree with their views also sets a bad

precedent for Indian corporate governance. In case Tata Sons believes that Mr. Wadia’s

independence has been affected, it should also propose removal of all the Independent

Directors of these companies with longer tenures.

We recommend shareholders vote AGAINST Mr. Wadia’s removal from the board because

while his tenure as an Independent Director is greater than 10 years, the principle against his

removal does not set a good precedent for Indian corporate governance.

Regarding appointment of Mr. Bhaskar Bhat and Mr. S Padmanabhan as Directors, we do not

have any concerns. Mr. Bhat was a Non-executive non-independent Director on the Board and

had resigned recently due to his disagreement with Independent Directors for expressing

their confidence on Mr. Mistry as Chairman. Mr. S Padmanabhan is a new appointment.

We recommend shareholders vote FOR their appointments.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 16 | P A G E

THE TATA POWER COMPANY LIMITED

Meeting Details

Meeting date & time: 26 December 2016, 11:00 AM IST

Meeting venue: Yashwantrao Chavan Prathishthan Auditorium, Y. B. Chavan Center,

Gen. JB Marg, next to Sachivalaya Gymkhana, Mumbai 400021

List of Resolutions

Res Resolution Title Management* InGovern

1. Removal of Mr. CP Mistry as a Director … Against

This is an ordinary resolution requiring more than 50% of the voting shareholders to vote FOR its approval

Actions undertaken by the Board/ Promoter/ Company

Tata Sons requisitioned Tata Power to hold an EGM for removal of Mr. Mistry as Director

On 22nd November 2016, the Board decided to convene an EGM on 26th December 2016

Composition of the Board

Name Category Tenure (Years)

Cyrus Mistry NENID 5

Homiar S Vachha ID 15

Nawshir H Mirza ID 10

Deepak M Satwalekar ID 8

Ashok K Basu ID 7

Pravin H Kutumbe NENID 1

Sandhya S Kudtarkar NENID 0

Anjali Bansal ID 0

Vibha Padalkar ID 0

Sanjay Bhandarkar ID 0

Anil Sardana MD 9

Ashok Sethi ED 2

ED: Executive Director; ID: Independent Director; MD: Managing Director; NENID: Non-executive Non-Independent

Director

Highlighted are Independent Directors who have exceeded a tenure of 10 years whom we consider not truly independent

It is surprising to see that the Board and specifically the Independent Directors of Tata Power

have not made their positions publicly known while those at other six companies have aired

their views.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 17 | P A G E

InGovern Recommendations

In Tata Power, we share the same concerns as we did with other companies.

Along with other points as explained in our vote recommendations in this report, we draw

attention to SP Group’s beneficial interest in Tata Power which is around 5.71%. With no

governance issues regarding Mr. Mistry and considering his significant beneficial interests, it

is prudent to allow Mr. Mistry to continue in the Board.

Also, Tata Sons has not articulated to the public shareholders their specific plans and the way

forward for Tata Power. Unless they explain how their plan is different from what the Board

under Mr. Mistry envisaged for the company, public shareholders will not be able to take an

informed decision.

In line with our recommendations for other companies, we recommend shareholders vote

AGAINST Mr. Mistry’s removal from these Boards. There is no logic for his removal as

Director and his continuance would be in best interests of the company.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 18 | P A G E

TATA GLOBAL BEVERAGES LIMITED

Shareholder Meeting Details

Meeting date & time: No announcement of requisition by Tata Sons

Meeting venue: -

Actions undertaken by the Board/ Promoter/ Company

On 15th November 2016, the Board replaced Mr. Cyrus Mistry as its Chairman

The Board then appointed Mr. Harish Bhat as its Chairman

Company has not notified of any requisition received from Tata Sons

Composition of the Board

Name Category Tenure (Years)

Harish Bhat, Chairman NENID 4

Cyrus Mistry NENID 4

Darius Pandole ID 4

S Santhanakrishnan NENID 3

V Leeladhar ID 7

Mallika Srinivasan ID 8

Analjit Singh ID 8

Ranjana Kumar ID 6

Ajoy K Mishra MD 5

L Krishnakumar ED 3

Ireena Vittal ID 3

ED: Executive Director; ID: Independent Director; MD: Managing Director ; NENID: Non-executive Non-independent Director

The Board of Tata Global Beverages replaced Mr. Mistry as their Chairman by voting in favour

of his replacement in the ratio of 7:3, on 15th November 2016. The Board, then appointed Mr.

Harish Bhat as its new Chairman.

At the time of publishing this report, there is no notification of any requisition by Tata Sons

for holding an EGM. Hence, we haven’t made any recommendations for Tata Global

Beverages.

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 19 | P A G E

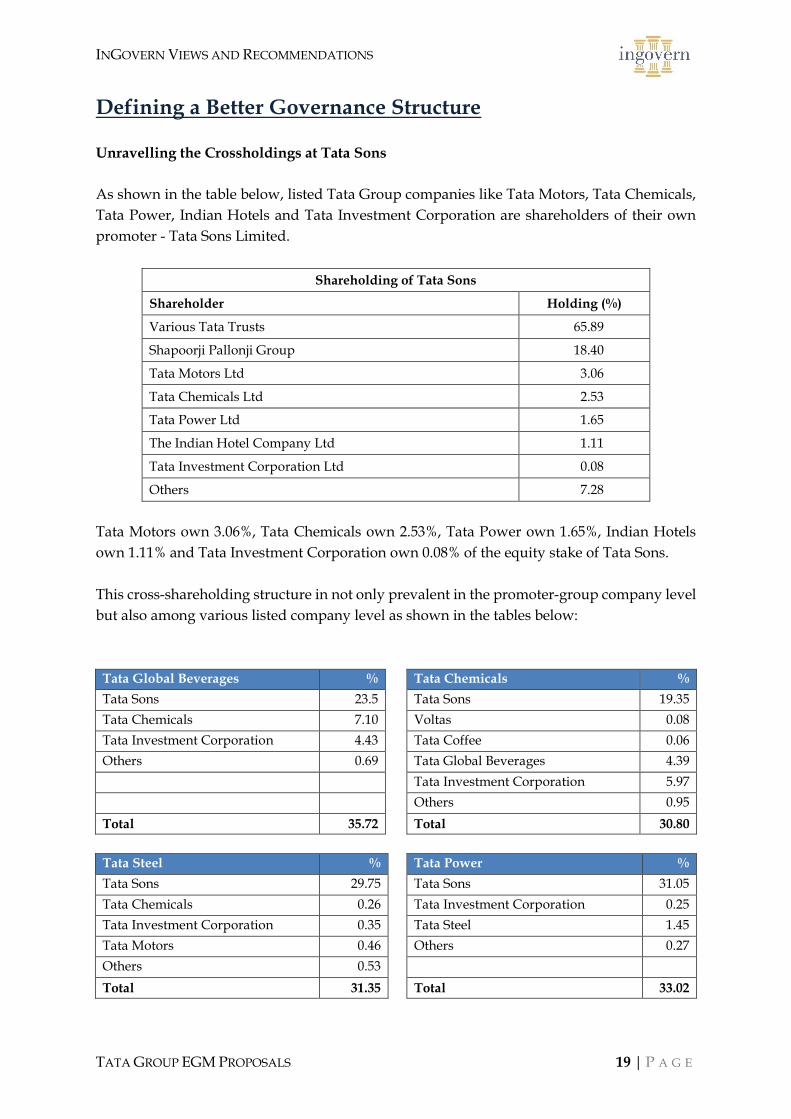

Defining a Better Governance Structure

Unravelling the Crossholdings at Tata Sons

As shown in the table below, listed Tata Group companies like Tata Motors, Tata Chemicals,

Tata Power, Indian Hotels and Tata Investment Corporation are shareholders of their own

promoter - Tata Sons Limited.

Shareholding of Tata Sons

Shareholder Holding (%)

Various Tata Trusts 65.89

Shapoorji Pallonji Group 18.40

Tata Motors Ltd 3.06

Tata Chemicals Ltd 2.53

Tata Power Ltd 1.65

The Indian Hotel Company Ltd 1.11

Tata Investment Corporation Ltd 0.08

Others 7.28

Tata Motors own 3.06%, Tata Chemicals own 2.53%, Tata Power own 1.65%, Indian Hotels

own 1.11% and Tata Investment Corporation own 0.08% of the equity stake of Tata Sons.

This cross-shareholding structure in not only prevalent in the promoter-group company level

but also among various listed company level as shown in the tables below:

Tata Global Beverages % Tata Chemicals %

Tata Sons 23.5 Tata Sons 19.35

Tata Chemicals 7.10 Voltas 0.08

Tata Investment Corporation 4.43 Tata Coffee 0.06

Others 0.69 Tata Global Beverages 4.39

Tata Investment Corporation 5.97

Others 0.95

Total 35.72 Total 30.80

Tata Steel % Tata Power %

Tata Sons 29.75 Tata Sons 31.05

Tata Chemicals 0.26 Tata Investment Corporation 0.25

Tata Investment Corporation 0.35 Tata Steel 1.45

Tata Motors 0.46 Others 0.27

Others 0.53

Total 31.35 Total 33.02

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 20 | P A G E

Tata Motors % Indian Hotels %

Tata Sons 26.51 Tata Sons 28.01

Tata Chemicals 0.07 Tata Investment Corporation 1.35

Tata Investment Corporation 0.36 Tata Chemicals 0.90

Tata Steel 2.85 Others 8.39

Others 2.64

Total 32.43 Total 38.65

Crossholdings between promoter-company or group company levels are not examples of

good corporate governance standards. While crossholdings make the holding structure of the

companies complex, they also benefit the promoters in controlling higher voting powers than

the actual beneficial interest.

In case of Tata Group, crossholdings between listed companies benefit Tata Sons as it exerts

control on 35.72% voting rights of Tata Global Beverages and 30.80% of Tata Chemicals while

the beneficial interests are 23.5% and 19.35% respectively.

Also, there is no logic whatsoever on the need for listed Group companies to hold shares of

the promoter company Tata Sons Limited. Efforts should be made by the Tata Group to

unravel these crossholdings and make ownership structure of the Group much cleaner and

simpler.

In addition to the above, there should be greater disclosures and operating guidelines between

the Trusts, Tata Sons Limited and Operating Companies.

Defining a non-conflicted Board and Possible Relationship with listed Group Companies

The following Independent Directors of listed Tata companies are on the Board of Trustees of

various Tata Trusts:

1. Nasser Munjee – Independent Director on Boards of Tata Motors and Tata Chemicals

On the Boards of Trustee of:

Sir Ratan Tata Trust

Bai Hirabai J. N. Tata Navsari Charitable Institution

2. Keko B Dadiseth – Independent Director on Board of Indian Hotels Company

On the Boards of Trustee of:

Sir Ratan Tata Trust

Bai Hirabai J. N. Tata Navsari Charitable Institution

3. Venu Srinivasan – Relative of Mallika Srinivasan, Independent Director on Boards of

Tata Steel and Tata Global Beverages

On the Board of Trustee of:

Sir Dorabji Tata Trust

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 21 | P A G E

The Independent Directors’ and their relatives’ position on the Board of Tata Trusts create a

clear situation of conflict of interests especially in situations like the present one where the

Tata Trusts had given their approval for replacement of Mr. Mistry as Chairman of Tata Sons.

Such conflict of interests should be avoided by replacing these Independent Directors with

new members or asking them to step down from the Board of Trustees of the Tata Trusts.

The Value of “Tata” as a brand

Shareholders should question whether just the “Tata” name is sufficient as a brand. We

believe that such implicit assumptions need to be questioned. There have been successes and

failures associated with the brand, so the inherent business model, customer service and

product quality are also important.

***************

This report has relied on data from:

Press releases by Tata Sons Limited on www.tata.com

Press releases by Mr. Cyrus Mistry and on www.cyrusforgovernance.com

Announcements and EGM notices of each of the operating listed companies to the stock

exchanges

This report has been updated till end of 7th December 2016. There is a possibility that if any

new information is revealed this report will be updated.

****************

INGOVERN VIEWS AND RECOMMENDATIONS

TATA GROUP EGM PROPOSALS 22 | P A G E

About InGovern

InGovern Research Services assists financial institutions and investors that have financial,

investment or reputational exposure to public-listed companies in India by providing our

clients with corporate governance reports and proxy voting solutions. Our clients rely on our

independent analysis and insights.

Our services include:

Corporate Governance Advisory Services

Vote Recommendations

Shareholder Activism

Disclaimer InGovern Research Services Pvt. Ltd. (“InGovern”) is a proxy advisory and corporate governance advisory firm. The range of services provided by InGovern is available at www.ingovern.com. This note is confidential and may not be reproduced in any manner without the written permission of InGovern Research Services Pvt. Ltd. (“InGovern”). This analysis does not constitute investment advice and investors should not rely on it for investment or other purposes. No warranty is made as to the completeness, accuracy or utility of this analysis. Some institutional investor affiliates of issuers may have purchased a subscription to InGovern services, which is disclosed on relevant reports. In addition, advisors to issuers such as law firms, accounting firms, rating agencies or others may subscribe to InGovern services. InGovern does not discuss our analysis or reports with any entity prior to publication. General Disclosures InGovern, its research analyst(s) responsible for the report, and associates or relatives do not have any financial interest in the issuer. InGovern, its research analyst(s) responsible for the report, and associates or relatives do not have actual/beneficial ownership of one per cent or more securities of the issuer at the end of the month immediately preceding the date of publication of the research report. InGovern, its research analyst(s) responsible for the report, and associates or relatives do not have any material conflict of interest at the time of publication of the research report. InGovern provides voting recommendations, corporate governance research and advisory services to investors and companies, which may also include the issuer. Apart from the compensation received for providing such services, InGovern, its research analyst(s) responsible for the report and its associates have not received any compensation from the issuer or any third party for this report. InGovern, its research analyst(s) responsible for the report and its associates have not managed or co‐ managed public offering of securities for the issuer in the past twelve months or mandated by the subject company for any other assignment in the past twelve months. InGovern, its research analyst(s) responsible for the report and its associates have not received any compensation for investment banking or merchant banking or brokerage services from the issuer in the past twelve months. The research analyst(s) responsible for the report has not served as an officer, director or employee of the issuer. Neither InGovern, nor its research analyst(s) responsible for the report have been engaged in market making activity for the issuer. Proxy Adviser Disclosures InGovern gives voting recommendations solely on basis of publicly available information. This may include issuer’s disclosure in its website, through corporate announcement section of the stock exchanges, information available through MCA website, etc. The voting recommendations are guided by InGovern’s Voting Policy Guidelines, which is designed off InGovern’s ‘Governance Radar’ framework consisting of around 400 criteria. After the vote recommendation report is prepared by a research analyst(s), it is reviewed by other research analyst(s) and finally approved by the Managing Director. ‘Against’ vote recommendations are debated in detail by the research analyst(s) and other members.