tax challenges with u.s.-based private equity fund...

TRANSCRIPT

Tax Challenges With U.S.-Based

Private Equity Fund Formation Maximizing Benefits for Clients Given Diverse Investor Tax Objectives

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information, including

options for phone or Web sound for one or multiple listeners. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, AUGUST 15, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Elizabeth Norman, Attorney, Goulston & Storrs, Boston

Joshua V. Azran, Owner, Azran Financial, Century City, Calif.

David Benz, Principal, Rothstein Kass, Beverly Hills, Calif.

Tips for Optimal Quality

Options

You can listen to the audio for this program both via the phone and the Web.

However, if you listen via the Web, and more than one person is in the room, you

must have a proctor to verify your attendance. Consult your dial-in instructions

for more details.

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Continuing Education Credits

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the ―Official Record of Attendance,‖ please print it now (see

―Handouts‖ tab in ―Conference Materials‖ box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to ―Conference Materials‖ in the middle of the left-

hand column on your screen.

• Click on the tab labeled ―Handouts‖ that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Tax Challenges With U.S.-Based Private Equity Fund Formation

Aug. 15, 2013

Joshua V. Azran, Azran Financial David H. Benz, Rothstein Kass

[email protected] [email protected]

Elizabeth M. Norman, Goulston & Storrs

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

7

Fund Characteristics

• Types of funds

— Private equity

— Venture capital

— Hedge

— Distressed debt

— Real estate

— LBO

— Fund of funds

8

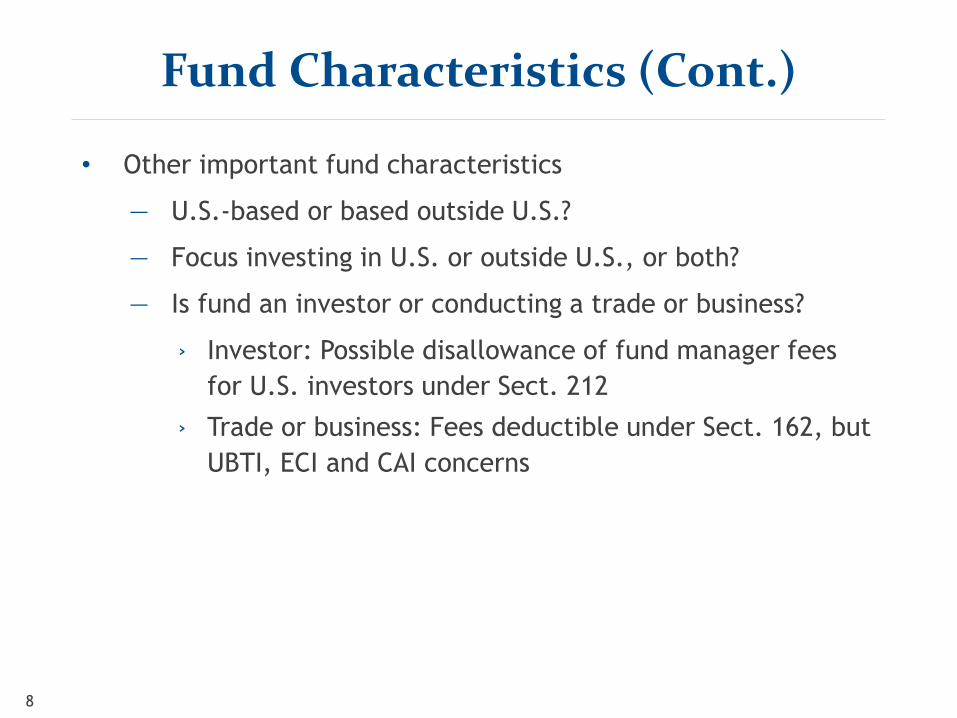

Fund Characteristics (Cont.)

• Other important fund characteristics

— U.S.-based or based outside U.S.?

— Focus investing in U.S. or outside U.S., or both?

— Is fund an investor or conducting a trade or business?

› Investor: Possible disallowance of fund manager fees

for U.S. investors under Sect. 212

› Trade or business: Fees deductible under Sect. 162, but

UBTI, ECI and CAI concerns

9

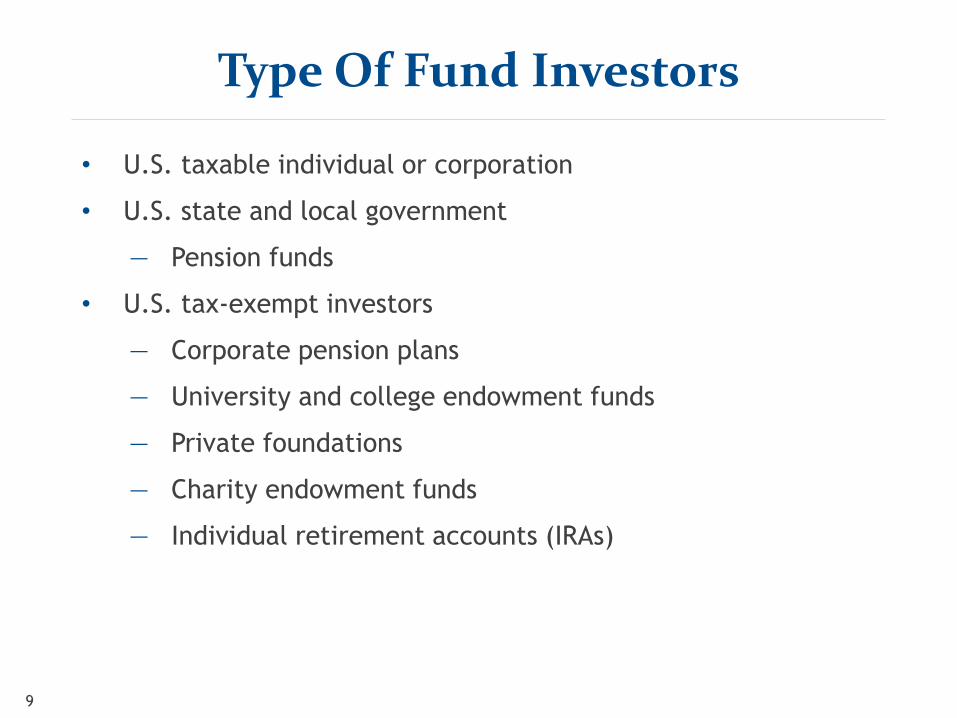

Type Of Fund Investors

• U.S. taxable individual or corporation

• U.S. state and local government

— Pension funds

• U.S. tax-exempt investors

— Corporate pension plans

— University and college endowment funds

— Private foundations

— Charity endowment funds

— Individual retirement accounts (IRAs)

10

Type Of Fund Investors (Cont.)

• Non-U.S. investors

— Individuals

— Non-U.S. entities treated as corporations, for U.S. income

tax purposes

— Pension funds (not taxed in home country)

• Non-U.S. government investors (Sect. 892)

— Sovereign wealth funds

— Pension funds

11

U.S.

taxable

C Corp.

35% c.g. and o.i.

Fund L.P.

Portfolio

Corp.

Portfolio

LLC

- Gain on interest sale

- Gain on asset sale

- Interest

- Gain on debt sale

U.S. taxable

individual

- 20% c.g.

- 39.6% o.i.

- 3.8% nii

- Gain on stock sale

- Dividends

- Interest

- Gain on debt sale

No fund-blocker desired

Unblocked investor can also claim tax credits and treaty benefits.

U. S. Taxable Individuals And Corporations

12

U. S. State and

Local Government

0% U.S. tax rate

Fund L.P.

Portfolio

Corp.

Portfolio

LLC

Gain/income

No fund-blocker desired

Unblocked can also claim treaty benefits.

Gain/income

U. S. State And Local Government

13

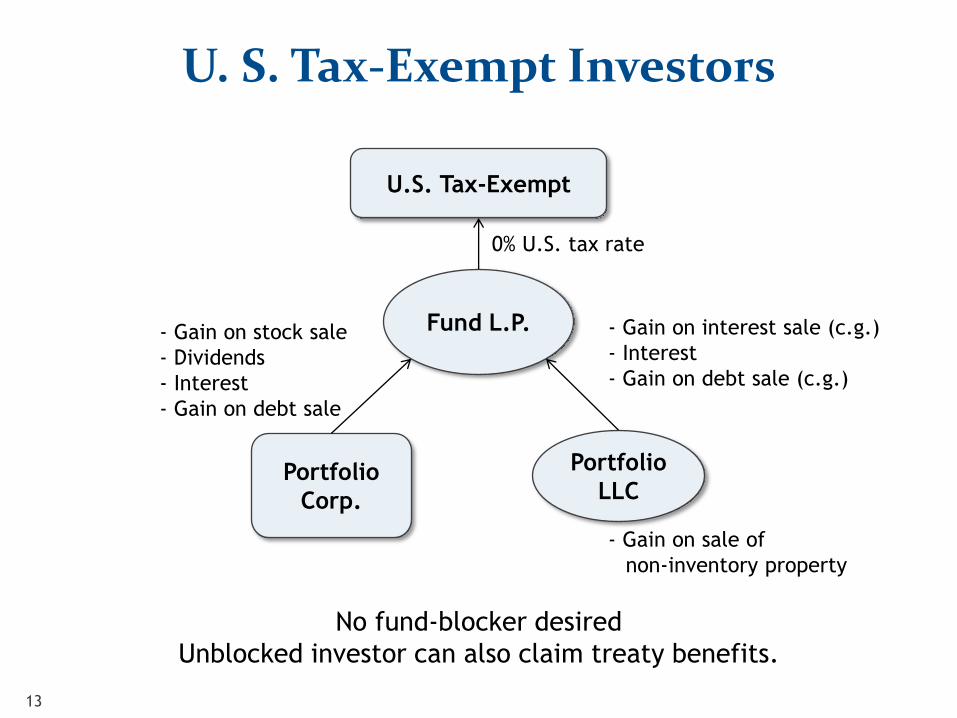

U.S. Tax-Exempt

0% U.S. tax rate

Fund L.P.

Portfolio

Corp.

Portfolio

LLC

- Gain on interest sale (c.g.)

- Interest

- Gain on debt sale (c.g.)

- Gain on stock sale

- Dividends

- Interest

- Gain on debt sale

No fund-blocker desired

Unblocked investor can also claim treaty benefits.

- Gain on sale of

non-inventory property

U. S. Tax-Exempt Investors

14

U.S. Tax-Exempt

35% U.S. tax rate

Fund L.P.

Portfolio

LLC

Fees earned by L.P.

Fund-blocker often desired

Unrelated business taxable income (UBTI)

- Operating income

- Gain on sale of inventory

U. S. Tax-Exempt Investors (Cont.)

15

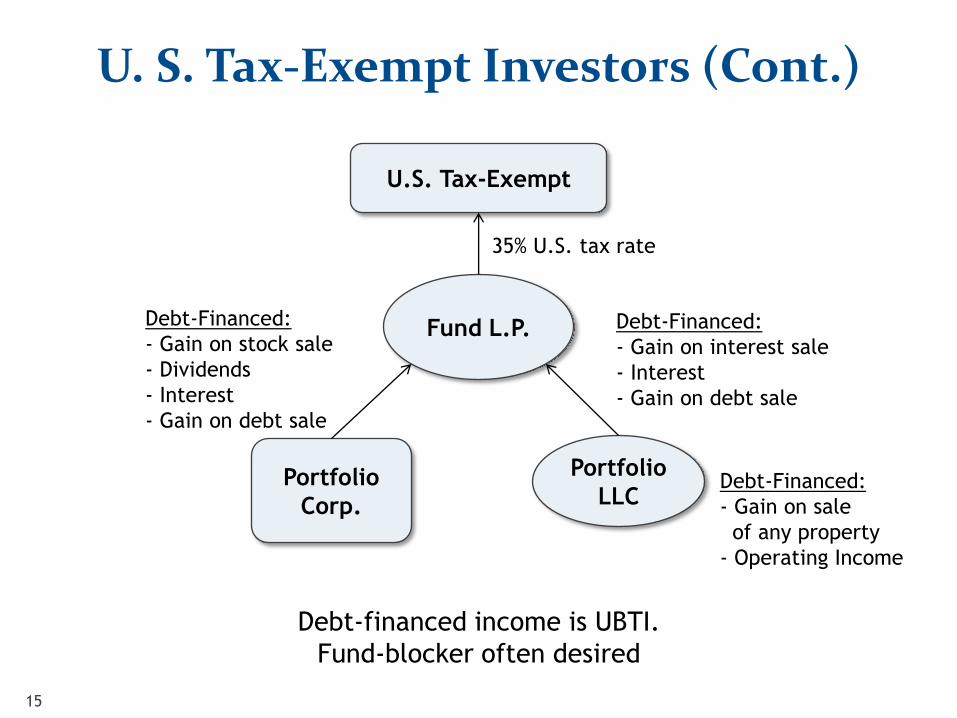

U.S. Tax-Exempt

35% U.S. tax rate

Fund L.P.

Portfolio

Corp.

Portfolio

LLC

Debt-Financed:

- Gain on interest sale

- Interest

- Gain on debt sale

Debt-Financed:

- Gain on stock sale

- Dividends

- Interest

- Gain on debt sale

Debt-financed income is UBTI.

Fund-blocker often desired

Debt-Financed:

- Gain on sale

of any property

- Operating Income

U. S. Tax-Exempt Investors (Cont.)

16

U.S. Tax-Exempt

Non-U.S. or U.S.

Feeder Fund

Non-U.S.

Investments

(No UBTI)

U.S.

Investments

(No UBTI)

U.S.

Corp. Blocker

Investments

(UBTI)

U. S. Tax-Exempt Investors: Parallel Fund Structure

17

Non-U.S. Investors

• U.S. tax goals

— Avoid having to file a U.S. income tax return

— Limit U.S. tax on ―effectively connected income‖ (ECI)

— If ECI:

› Must file U.S. federal, state and local returns

› Must pay income tax at regular, federal, state and

local rates

• Non-U.S. corp. must also pay U.S. 30% ―branch

profits‖ tax.

— Limit U.S. tax on FDAP income

› 30% U.S. withholding tax rate, unless U.S. tax treaty

applies

› Claim U.S. treaty benefits where possible

18

Non-U.S. Investors (Cont.)

• Effectively connected income (ECI) is income recognized by a

non-U.S. person that is effectively connected with a business

carried on in the U.S.

— Does fund have a loan origination business?

— ―Securities trading safe harbor‖ protects offshore funds.

• ECI includes share of operating income from a pass-through

entity conducting business in the U.S.

— Non-U.S. partners are deemed engaged in a U.S. business.

— Sale of partnership interest in partnership that generates

ECI; IRS takes the position that gain is ECI.

• FIRPTA income treated like ECI

19

Non-U.S. Investor

0% U.S. tax rate

Fund L.P.

Portfolio

Corp.

Portfolio

LLC

U.S. Source:

- Portfolio interest

- Gain on debt sale

No fund-blocker desired

Portfolio

Corp.

Non-U.S.

Source:

- Gain/income

U.S. Source:

- Gain on stock sale

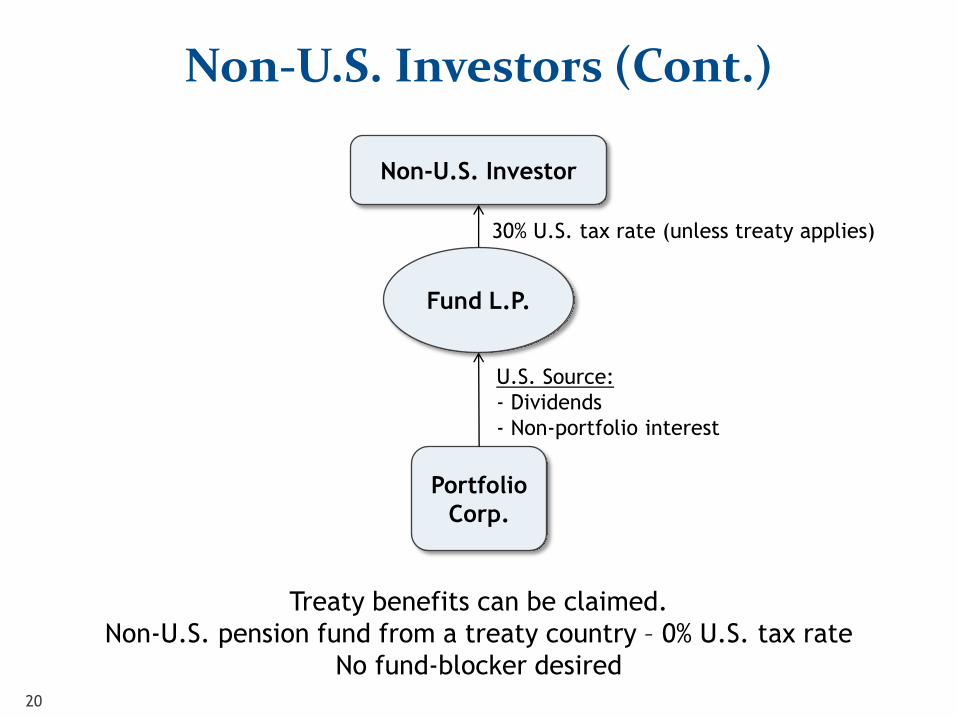

Non-U.S. Investors (Cont.)

20

Non-U.S. Investor

30% U.S. tax rate (unless treaty applies)

Fund L.P.

Treaty benefits can be claimed.

Non-U.S. pension fund from a treaty country – 0% U.S. tax rate

No fund-blocker desired

Portfolio

Corp.

U.S. Source:

- Dividends

- Non-portfolio interest

Non-U.S. Investors (Cont.)

21

Non-U.S. Investor

35%/39.6% U.S. tax rate

Fund L.P.

Fund-blocker usually desired

Gain on interest sale (ECI)

Portfolio

LLC

U.S. Source:

- Gain on sale of operating assets (ECI)

- Operating income (ECI)

Non-U.S. Investors (Cont.)

22

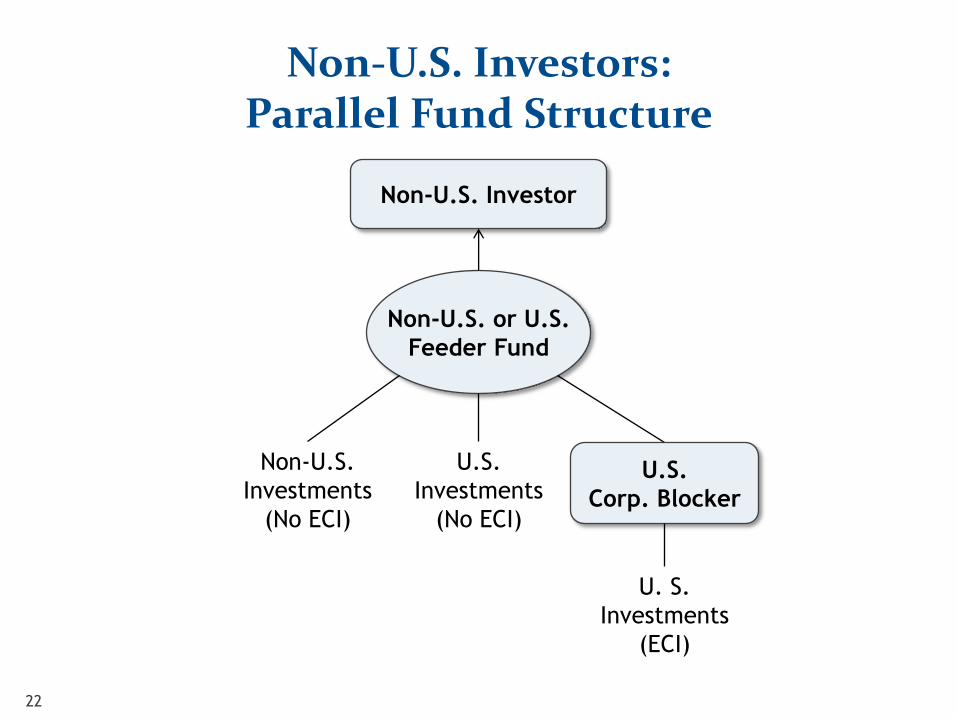

Non-U.S. Investor

Non-U.S. or U.S.

Feeder Fund

Non-U.S.

Investments

(No ECI)

U.S.

Investments

(No ECI)

U.S.

Corp. Blocker

U. S.

Investments

(ECI)

Non-U.S. Investors: Parallel Fund Structure

23

U.S. Tax-Exempt Investor: Parallel Fund Structure (Cont.)

• Why use non-U.S. feeder?

— Not have to report non-U.S. investments

— Can avoid "controlled foreign corporation" (CFC) treatment

in which substantial investors are non-U.S. investors and

fund owns 50% or more of the non-U.S. portfolio company

• Why use U.S. feeder?

— Easier to claim U.S. treaty benefits; only need to issue

W-8BEN to U.S. feeder

— Will relevant non-U.S. tax treaties "flow-through" a non-

U.S. feeder? See also Sect. 894(c)

24

UBTI And ECI: Not Exactly The Same

• Some investments may generate UBTI but not ECI.

— Debt-financed income (including stock sales, dividends,

and interest)

• Some investments may generate ECI but not UBTI.

— Sale of partnership interests when partnership conducts a

U.S. trade or business

— Investments in U.S. real property holding corporations

(holding 50% or more of gross assets in U.S. real property)

— Loan commitment fees are not UBTI but may be ECI.

• Accordingly, a blocker that avoids all ECI may be too broad for

a U.S. tax-exempt investor, and a blocker that avoids all UBTI

may be too broad for a non-U.S. Investor.

Slide Intentionally Left Blank

26

Non-U.S. Governmental Investors

• Non-U.S. governments (including their controlled entities) are

generally exempt from U.S. tax under IRC Sect. 892 on income

from investments from securities, except income from the

conduct of a "commercial activity" (CAI).

• If a controlled entity has CAI (either U.S. or non-U.S.), it could

lose its Sect. 892 exemption (but recent relief in proposed

regulations —―inadvertent‖ and ―de minimis‖ standards;

interest in non-controlled LP)

• Investments in operating partnerships generate CAI/

• Non-U.S. government owning U.S. real property or 50% or

more of the stock of a U.S. real property holding corporation

(USRPHC) can generate CAI.

27

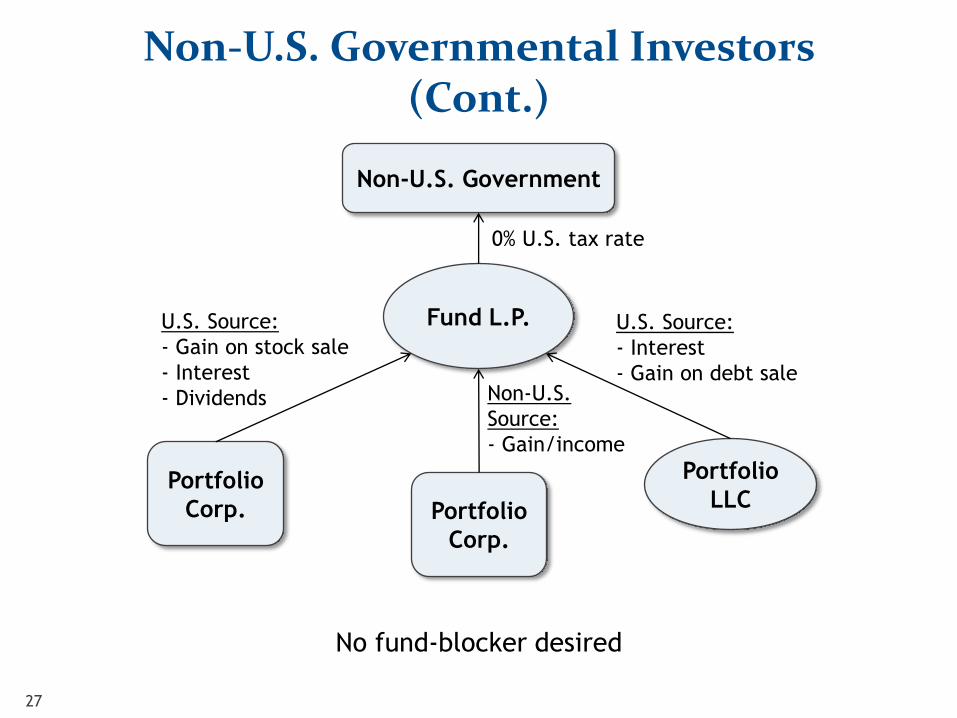

Non-U.S. Government

0% U.S. tax rate

Fund L.P.

Portfolio

Corp.

Portfolio

LLC

U.S. Source:

- Interest

- Gain on debt sale

No fund-blocker desired

Portfolio

Corp.

Non-U.S.

Source:

- Gain/income

U.S. Source:

- Gain on stock sale

- Interest

- Dividends

Non-U.S. Governmental Investors (Cont.)

28

Non-U.S. Government

35% U.S. tax rate

Fund L.P.

Fund-blocker desired

Gain on interest sale (CAI)

Portfolio

LLC

U.S. Source:

- Operating income (CAI)

- Gain on sale of operating assets (CAI)

Non-U.S. Governmental Investors (Cont.)

29

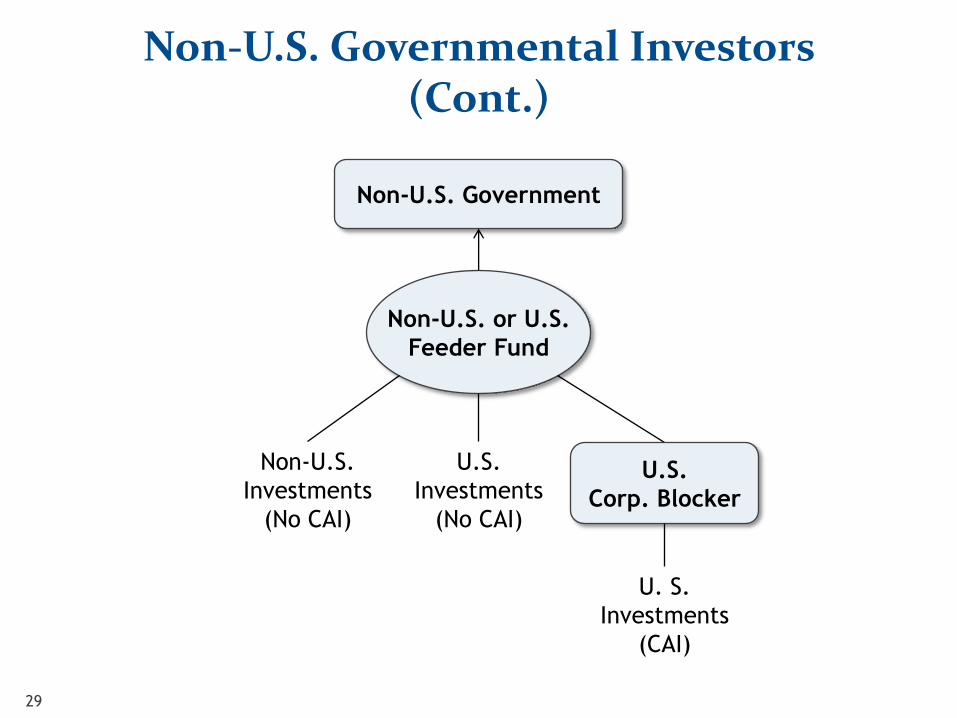

Non-U.S. Government

Non-U.S. or U.S.

Feeder Fund

Non-U.S.

Investments

(No CAI)

U.S.

Investments

(No CAI)

U.S.

Corp. Blocker

U. S.

Investments

(CAI)

Non-U.S. Governmental Investors (Cont.)

30

ECI, FDAP And CAI: Not Exactly The Same

• Some investments may generate ECI but not CAI.

— Investments in U.S. real property holding corporations

(USRPHC) (holding 50% or more of gross assets in U.S.

real property)

› Only CAI if non-U.S. government holds 50% of more

of USRPHC

• Some investments may generate CAI but not ECI.

— Sale at gain of non-U.S. corporate entity controlled by

non-U.S. government, which would be a USRPHC if formed

in the U.S., is taxable CAI but would not be ECI.

• Some investments may generate FDAP withholding

for non-U.S. investors but not for non-U.S. governmental

investors.

31

Parallel Fund Structure

• Most tax-efficient fund structure generally is to use separate

parallel funds for each type of investor.

— Administrative costs

• Should each investment have a newly formed, separate

blocker?

— This can avoid U.S. dividend withholding tax on exit

— But, if a single blocker is used for multiple investments,

then income and gain from one investment can be offset by

losses from another.

• Risk of aggregation of different fund entities used in

parallel/AIV structure, due to applying carried interest across

all funds

32

Main Fund

Other Investors

Parallel Fund

Portfolio

LLC

Intermediate

Partnership

GP

Electing U.S. Tax-Exempt, Non-U.S. and Non-U.S.

Governmental Investors

Blocker Corp.

Portfolio Corp.

Carry Carry

Simplified Parallel Fund

33

AIF “A”

Other Investors

AIF “B”

Portfolio

LLC

Intermediate

Partnership

GP

Main Fund

All Investors

Blocker Corp.

Portfolio Corp.

Carry

Carry

Electing U.S. Tax-Exempt, Non-U.S. and Non-U.S.

Governmental Investors

Alternative Investment Fund

34

Other Investors

Portfolio

LLC

GP

Electing U.S. Tax-Exempt, Non-U.S. and Non-U.S. Governmental Investors

Main Fund L.P.

Feeder Fund

(Offshore)

Portfolio Corp.

Feeder Fund: No Flexibility

35

Non-U.S./U.S. Tax-Exempt

Investors

Fund

U.S.

Corp. Blocker

Taxable Investors

Portfolio

LLC

Taxable investor capital

Sensitive investor capital

Subsidiary Blocker Structures

36

Subsidiary Blocker Structures (Cont.)

• Some funds use subsidiary ―blocker‖ corporations for ECI and

UBTI investments.

— Capital of tax-sensitive investors channeled through blockers

› Special allocations at the fund level – substantiality

concerns?

› Risk to non-U.S. investors of U.S. tax return filing

obligation

— GP carry pre- or post-tax? Take out GP carry below the

blocker

• Exit from investment

— Sale of assets and liquidation of blocker

— Sale of blocker shares?

› Allocation of discount?

37

Foreign Investment In Real Property Tax Act (FIRPTA)

• In general, non-U.S. persons generally do not pay U.S. tax on

disposals of stock or securities of U.S. issuers.

• FIRPTA is an exception to this general treatment.

• FIRPTA imposes a tax on gains realized from the disposition of

a U.S. real property interest, which includes direct real estate

holdings and:

— Partnership/flow-throughs that hold U.S. real estate

— Interests in a ―U.S. real property holding corporation‖

(USRPHC)

— Direct or indirect rights to share in proceeds, appreciation

or profit of U.S. real estate

38

FIRPTA (Cont.)

• USRPHCs

— FIRPTA also applies to companies in which at least half of

the fair market value of the company’s trade or business

assets is attributable to U.S. real property assets.

› Five-year lookback

— Carve-out for investments in publicly traded stocks for

which the investor does not hold more than 5% of the class

of stock being traded

— FIRPTA traps

› Distressed companies

› Publicly traded stock de-listed

39

FIRPTA (Cont.)

• Tax imposed at U.S. tax rates

• Collected partially through withholding

• Gains treated as ECI

• Non-U.S. person with FIRPTA gain also incurs a U.S. federal

income tax filing obligation.

• Branch profits tax may also apply.

40

FIRPTA (Cont.)

• U.S. blockers frequently used to hold U.S. real estate assets,

which blocks application of FIRPTA tax and filing obligations

• Note, however, that the U.S. blocker itself may be a

―USRPHC,‖ which would trigger FIRPTA gain if sold (unlikely

exit).

• Trap for unwary: Sect. 1445(e) withholding on non-dividend

distributions from a USRPHC

41

FIRPTA (Cont.)

Non-U.S. Fund

Non-U.S.

Investments

(No FIRPTA)

U.S.

Non-Real

Estate

Investments

(No FIRPTA)

U.S.

Corp. Blocker

U. S. Real

Estate

Investments

42

FIRPTA (Cont.)

Non-U.S. Fund

Non-U.S.

Investments

(No FIRPTA)

U.S.

Non-Real

Estate

Investments

(No FIRPTA)

U.S.

Corp. Blocker

U. S. Real

Estate

Investments

Offshore Blocker

Loan

Financing the U.S. blocker: Potential

complications (withholding tax,

earnings-stripping, AHYDO, Sect. 267)

Interest

Slide Intentionally Left Blank

44

U.S. Tax-Exempt Investors: 514(c)(9)

• Certain tax-exempt investors (―qualified organizations‖ or

QOs) are eligible for an exception to debt-financed UBTI in

certain circumstances.

— Most common QOs are pension funds and educational

organizations

• Provided certain requirements are met, Sect. 514(c)(9)

provides that debt incurred to acquire or improve ―real

property‖ won’t give rise to UBTI for QOs.

— Definition of ―real property‖ unclear

• Compliance with 514(c)(9) poses challenges, particularly for

funds.

45

U.S. Tax-Exempt Investors: 514(c)(9), Cont.

• Sect. 514(c)(9): General requirements for debt-financed

acquisition of real estate

— Purchase agreements

— Borrowing agreements

› General rule

› Eligible lenders

› Multi-property loans

— Leasing agreements

46

U.S. Tax-Exempt Investors: 514(c)(9), Cont.

• Requirements for a 514(c)(9)-compliant fund

— Fund must comply with general requirements,

— AND

› All of the partners must be QOs; or

› Each allocation to a QO partner must be a ―qualified

allocation‖, or

› The partnership’s allocation provisions for tax

purposes:

• Satisfy the ―fractions rule,‖ and

• Have ―substantial economic effect.‖

• Potential legal and economic consequences of complying with

the fractions rule and the substantial economic effect rules

47

Non-U.S. Funds With U.S. Investments

• Same general structural considerations as above

— Non-U.S. Investors will be focused on ECI.

— If fund holds real estate assets, FIRPTA may also apply.

— Special structuring requirements for non-U.S. investors

— Treaty planning and additional documentation

requirements

— Non-U.S. corporation in structure (including offshore

blocker entity)? Potential branch profits tax

• U.S. source income = FATCA implications for fund and

its investors

48

Non-U.S. Funds With U.S. Investors: Investing Overseas

• Some considerations:

— PFIC/CFC issues (want non-U.S. fund to be pass-through)

— Tax filing obligations in non-U.S. jurisdictions

— Non-U.S. withholding tax

— Treaty analysis

— U.S. tax-exempt investors will still be concerned about

UBTI, and may wish to invest through a blocker if there

will be debt-financing or investments in operating

pass-throughs.

— Certain countries (India, China) have begun imposing tax

on indirect gains, which has led to an increase in the use

of ―filing blockers.‖

49

U.S. Funds Investing Overseas

• Same general structural considerations as have been

illustrated, with some additions

— UBTI on debt-financed investments/pass-through income

— Treaty benefits

— PFIC/CFC

— Foreign tax credit flow-through

— Commercial activities income still a concern for controlled

commercial entities (but, 892 benefits generally

irrelevant)

• Some of these are incompatible

— E.g., flow-through structures for taxable investors, but

UBTI issues for tax-exempts

50

U.S. Taxable/U.S.

Government Investors

Fund

(taxed as

partnership)

Non-U.S./U.S.

Tax-Exempt Investors

Non-U.S.

Investments

U.S. Funds Investing Overseas: Parallel Funds

Fund

(taxed as corporation)

51

U.S. Taxable/U.S.

Government Investors

Master Fund

(taxed as

partnership)

Non-U.S./U.S.

Tax-Exempt Investors

Non-U.S.

Investments

U.S. Funds Investing Overseas: Master/Feeder

Feeder Fund

(taxed as corporation)

52

U.S. Funds Investing Overseas (Cont.)

• PFIC/CFC issues for U.S. taxable investors

— Anti-deferral regimes

• PFIC - ≥ 50% passive assets or ≥ 75% passive income

— Look-through 25% owned subsidiaries

• Recharacterization of distributions, gain as ordinary income +

penalty interest charge

— No chance for qualified dividend income

53

U.S. Funds Investing Overseas (Cont.)

• Make ―check the box election‖ to treat as a pass-through

— Can be difficult to persuade local owners to make U.S. tax

election

• QEF election – modified look-through

— Losses and FTCs generally don’t flow through.

— Often, covenants to make election and obtain information

to make U.S. tax filings

— Can be burdensome for funds to gather required

information, including from 25%-owned subsidiaries

54

U.S. Funds Investing Overseas (Cont.)

• CFC – more than 50% of a foreign corporation owned by ―U.S.

shareholders‖

— U.S. persons with 10% or more voting power

› U.S. partnership = 1 U.S. person

— Structure fund and management entities as

Cayman vehicles, to apply 10% voting power test on

look-through basis

— Or, elect to treat foreign portfolio corporation as a pass-

through

55

Luxembourg Investment: Structure Into Europe

• Luxco set up with

minimal capital.

• PECs yield 8% per year.

• CPECs can be redeemed for

FMV of shares into which

CPECs are convertible.

• PECs and CPECs

• Debt, for Luxemburg

tax purposes

• Equity for U.S. tax

purposes (99/1 debt

-equity ratio)

German Portfolio Company

U.S. Main Fund LP

Luxco

Cash

CTB to be Taxed as a Disregarded Entity

U.S. Investors

Cash

PECs CPECs

German Portfolio Company

56

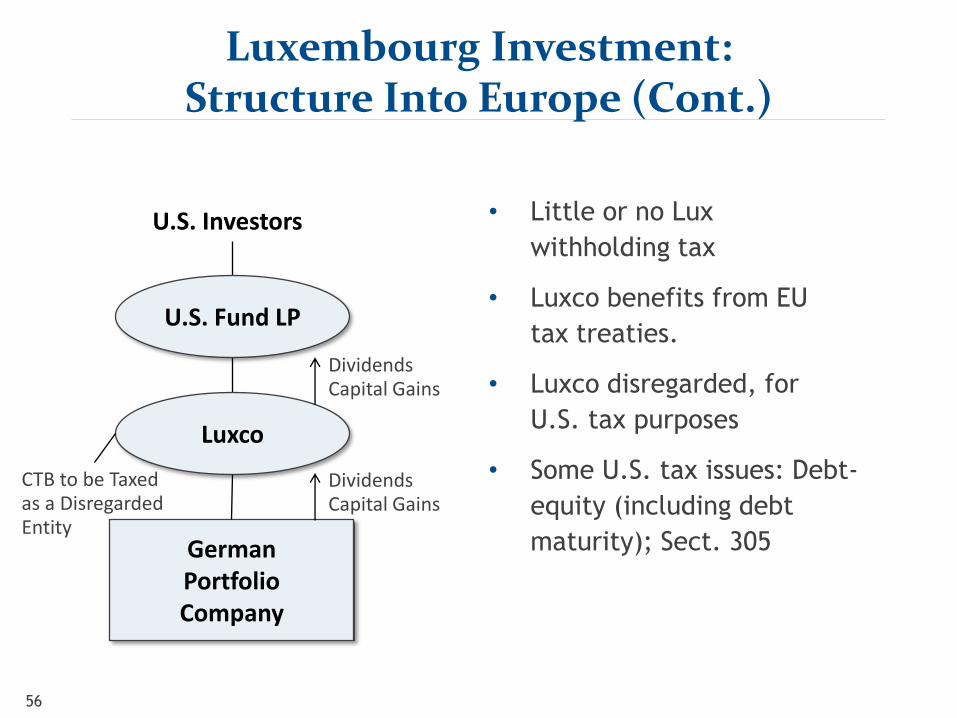

Luxembourg Investment: Structure Into Europe (Cont.)

• Little or no Lux

withholding tax

• Luxco benefits from EU

tax treaties.

• Luxco disregarded, for

U.S. tax purposes

• Some U.S. tax issues: Debt-

equity (including debt

maturity); Sect. 305 German Portfolio Company

U.S. Fund LP

Luxco

Dividends Capital Gains

CTB to be Taxed as a Disregarded Entity

U.S. Investors

Dividends Capital Gains

57

Structuring Fund Manager Entities

• Funds generally have separate general partners and

investment managers

— GP (or special LP owned by principals) receives carried

interest

› Generally special purpose entity for each fund

— Investment manager receives management fees

› Generally single management company across all funds

› Employees, contracts

› Franchise value

58

Structuring Fund Manager Entities (Cont.)

• Reasons for separation?

— Ensure proper tax treatment of separate income streams

› Carried interest – capital gains

› Management fees – ordinary income

— State/local tax reasons

› NYC unincorporated business tax

— Often separate ownership stakes

› Carried interest more widely distributed than

ownership of management company

› Deal-by-deal; fund-by-fund

59

Limited Partners

Fund

General

Partner

Investments

Management

Company

Principals

Carried

interest

Management Fees

Structuring Fund Manager Entities (Cont.)

60

Structuring Fund Manager Entities (Cont.)

• Considerations?

— Management company – choice of entity

› S corp.: Limited flexibility; state tax issues; perhaps

avoid self-employment taxes on dividends

› LLC: Flexibility; self-employment taxes on distributive

share of fee income?

› LP: Flexibility; requires separate GP entity; avoid self-

employment taxes on distributive share of fee income

• Statutory exception from SECA for distributive

share of a limited partner

• Impact of Renkemeyer?

61

Structuring Fund Manager Entities (Cont.)

• Considerations?

— General partner – choice of entity

› Less of an issue than management company as all

distributions should avoid self-employment taxes

› Use of LP arguably avoids new Medicare tax on NII

— General partner – issuances of interests; vesting

› Issuance of profits interest; no interest in current value

› 83(b) election

› Catch-up allocations

› Vesting/forfeiture/allocations to other partners

62

Foreign Account Tax Compliance Act (FATCA)

• Foreign Account Tax Compliance Act, or FATCA, is generally

effective as of Jan. 28, 2013.

• Intended to ensure that U.S. persons holding assets through

offshore entities and accounts pay U.S. taxes on related

income

• Compels non-U.S. financial entities to either (1) document and

report information about their U.S. accountholders/investors

or (2) face a withholding tax of 30% on most U.S. source gross

income or gross proceeds

63

FATCA (Cont.)

• FATCA does not replace the current withholding and reporting

regime for non-U.S. persons.

— FATCA is intended to be coordinated with the current

regime in order to prevent double-withholding,

• While FATCA is generally effective as of Jan. 28, 2013, a

phased implementation timeline applies.

• FATCA has a global reach.

— It imposes new documentation, withholding and reporting

requirements not only on non-U.S. entities, but also on

certain U.S. financial entities.

64

FATCA (Cont.)

• Categories under regulations

• U.S. withholding agents

— U.S. hedge and private equity funds may be required to

act as withholding agents under FATCA.

• Foreign financial institutions (FFIs)

— Non-U.S. funds likely FFIs

— Multiple categories: Participating FFI, deemed compliant

FFI and non-participating FFI

• Non-financial foreign entities (NFFEs)

• Exempt beneficial owners

— Generally not subject to FATCA withholding as long as

necessary documentation is provided to withholding agent

65

FATCA (Cont.)

• Withholding under FATCA

• FFIs: 30% of any ―withholdable payment‖ paid to non-

participating FFIs and recalcitrant account holders

— Tiered implementation of withholdable payments

› 2014: U.S.-source FDAP income

› 2017: U.S.-source gross proceeds on sale of stock or

securities

› 2017: ―Foreign pass-through payments‖

• Other withholding agents: Non-FFI withholding agents must

withhold 30% of any withholdable payment paid to non-

participating FFIs and passive NFFEs that fail to report on their

significant U.S. owners.

• ―Withholding agent‖ broadly construed under FATCA

66

FATCA (Cont.)

• Two-pronged approach to FATCA compliance

— IRS regulations

— Inter-governmental agreements (IGAs)

• Important guidance to come

• FFI model agreement, registration portal, tax certificates,

FATCA reporting form, withholding reports

• Coordinating guidance, plus guidance on ―foreign

pass-through payments‖

• IGAs

67

FATCA (Cont.)

U.S. funds: U.S. withholding agents

• Withholding by U.S. fund: If an investor fails to provide

necessary information to U.S. fund, then 30% FATCA

withholding may be deducted from investor’s share of

withholdable payments.

• Tax withheld under FATCA is paid by U.S. fund to IRS

68

FATCA (Cont.)

• Non-U.S. funds (and non-US blockers): Are they FFIs?

— Definition of FFI in the final regulations includes (among

others) foreign ―investment entities‖

› Broad definition of ―investment entities‖

— Most non-U.S. funds will be FFIs, with the exception of

certain real estate funds.

— No credit or refund of 30% withholding tax — if fund or

blocker is treated as corporation for U.S. tax purposes and

treaty does not change result

• Does every FFI need to comply with FATCA?

— Material U.S.-source income?

— Legal and practical considerations

— Various classifications for compliant FFIs

69

FATCA (Cont.)

• Special considerations for funds organized as partnerships for

U.S. tax purposes

— FATCA withholding applies not just to withholdable

payments, but also to allocations of income.

— Timing of FATCA withholding on a partnership’s receipt of

gross proceeds is unclear.

— Regulations don’t address how the sale of a partnership

interest will be treated under FATCA.

70

FATCA (Cont.)

• FATCA and fund documentation

— Fund organizational and operational documents

› Operating agreements

› Investor subscription documents and account

applications

› Fund offering documents

› Side letters

— Service provider agreements (transfer agent, custodian,

administrator, withholding agent, adviser, etc.)

— Credit agreements/ISDAs/repo & securities

lending agreements

Slide Intentionally Left Blank

72

New 3.8% Medicare Contribution Tax

• Imposed on U.S. individuals taxpayers, and estates

and trusts

• Not imposed on corporations or pass-through entities — but

―net investment income‖ passes through to U.S. individuals,

and estates and trusts

• Not imposed on non-resident individuals

• Effective date: Jan. 1, 2013

73

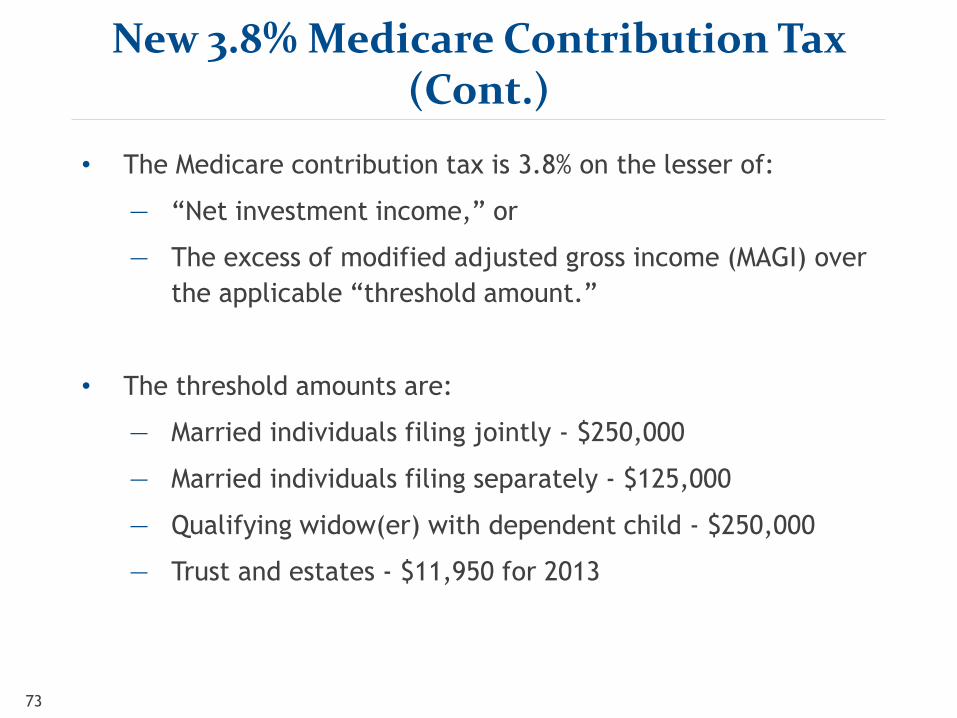

New 3.8% Medicare Contribution Tax (Cont.)

• The Medicare contribution tax is 3.8% on the lesser of:

— ―Net investment income,‖ or

— The excess of modified adjusted gross income (MAGI) over

the applicable ―threshold amount.‖

• The threshold amounts are:

— Married individuals filing jointly - $250,000

— Married individuals filing separately - $125,000

— Qualifying widow(er) with dependent child - $250,000

— Trust and estates - $11,950 for 2013

74

New 3.8% Medicare Contribution Tax (Cont.)

• Three buckets of net investment income:

— Gross income from interest, dividends, annuities, royalties

and rents

— Gross income derived from a business constituting a

passive activity to the taxpayer under IRC Sect. 469 (and

gross income derived from a trade or business comprised

of trading in financial instruments or commodities)

— Net gains from the disposition of property, such as the sale

of stocks, partnership interests, bonds and real estate

• Under proposed regs, the first two buckets can be negative

and offset other buckets, but the third

bucket cannot.

75

New 3.8% Medicare Contribution Tax (Cont.)

Other

Investors

Fund L.P.

Portfolio

Corp.

Portfolio

LLC

- Gain on interest sale

- Gain on asset sale

- Interest

- Gain on debt sale

U.S. Taxable Individual

(and certain Trust and

Estate) Investors

3.8% nii

- Gain on stock sale

- Dividends

- Interest

- Gain on debt sale

76

New 3.8% Medicare Tax

• Impact on fund managers and planning

— Carried interest

› Passive investment income subject to new tax

› Additional 3.8% tax on top of 20% LTCG (or 39.6% for

interest, STCG and nonqualified dividend income)

— Incentive compensation in hedge fund?

› If paid as fee, may be subject to 3.8% self-employment

tax unless qualifying for LP exception or perhaps

flowing through as S Corp. dividends (but, see next

slide)

› If paid as allocation, subject to new Medicare tax

• Even if fund is a ―trader‖ hedge fund

77

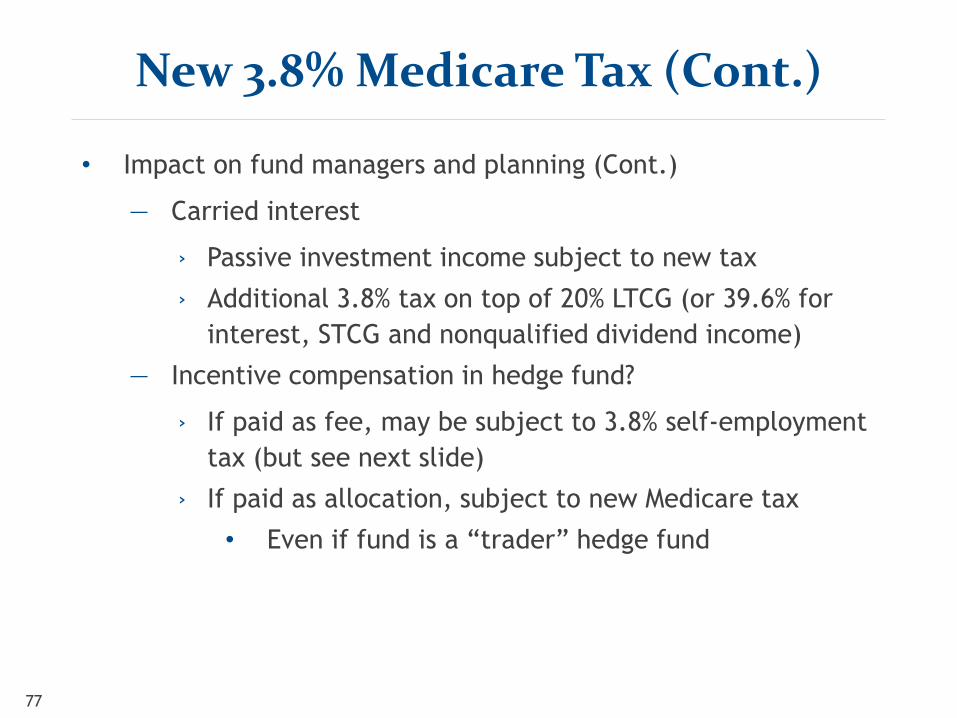

New 3.8% Medicare Tax (Cont.)

• Impact on fund managers and planning (Cont.)

— Carried interest

› Passive investment income subject to new tax

› Additional 3.8% tax on top of 20% LTCG (or 39.6% for

interest, STCG and nonqualified dividend income)

— Incentive compensation in hedge fund?

› If paid as fee, may be subject to 3.8% self-employment

tax (but see next slide)

› If paid as allocation, subject to new Medicare tax

• Even if fund is a ―trader‖ hedge fund

78

New 3.8% Medicare Tax (Cont.)

• Planning opportunities

— More incentive for deferral transactions

— 1031s – gain not picked up under NII rules until recognized

— Restructure carried interests as incentive fees

› If majority of income is already ordinary (STCG,

interest, rent, royalties)

› If carried interest is taxed as OI, further incentive to

convert fees (even if self-employment taxes would

apply as the new Medicare tax is non-deductible

against recipient’s income)

› Potential bad result for taxable investors in fund, due

to 212 limitation on deductibility of incentive fee

79

New 3.8% Medicare Tax (Cont.)

• Planning opportunities

— Convert LLCs to S corps or LPs

› Trade or business income paid as dividends by an S corp

to its shareholders that ―materially participate‖ is not

subject to the tax

› Member in LLC on same facts arguably subject to self-

employment taxes on same income

› Meaning of ―materially participating‖ going to be

very important.

80

New 3.8% Medicare Tax (Cont.)

• Planning opportunities

— Using corporations

› Corporations pay low tax rates on income up to

$50,000.

› Incentive fees up to such amounts could be paid to a

corporation owned by fund manager.

› Dividend out of corporation subject to 20% top federal

tax + 3.8% NII tax

• Effective federal tax rate of 35.8% as compared

with 43.4%

› State and local taxes to be considered

• Potential double-state tax

Slide Intentionally Left Blank

82

What Is A Carried Interest?

• Private equity and hedge fund managers structure funds with a

2 and 20 compensation structure.

— Fixed percentage of gains over losses

› Typically 20%

— Often, most income/gain allocated to the 20% carry is

taxed at favorable capital gain rates.

— New legislation would apply to the 20% carry.

83

Carried Interest Tax Proposals

• In President Obama’s 2014 budget

• Proposed legislation to add new IRC Sect. 710

• Proposal would tax as ordinary income a fund manager’s share

of income from an ―investment services partnership interest‖

in an investment partnership.

• Or a portion, i.e, 50% if the investment is held for five

years or more

• Applies to old and new partnerships (no grandfathering)

84

Carried Interest Tax Proposals (Cont.)

• Applies to persons (or related persons) who:

— Directly or indirectly provide any of the following services

with respect to assets held (directly or indirectly) by the

partnership:

› Advising on investing in, purchasing or selling a

―specified asset‖

› Managing, acquiring or disposing of a specified asset

› Arranging financing with respect to a specified asset, or

› Any activity in support of any of the previously

described activities

85

Definition Of Specified Assets

• The term ―specified asset‖ means:

— Securities (Sect. 475(c)(2))

— Real estate held for rental or investment

— Partnership interests

— Commodities (Sect. 475(e)(2))

— Options or derivative contracts with respect to

these assets

86

Some Partnerships Covered Include:

• Private equity funds

• Hedge funds

• Venture capital funds

• LBO funds

• Real estate funds and partnerships

• Marketable securities funds and partnerships

• Oil and gas funds and partnerships ???

87

Some Partnerships Not Covered

• Partnership operates an active business.

— E.g., profits interests are issued to service providers by an

LLC that operates a manufacturing business.

• Obama budget: Proposal is not intended to affect qualification

of a REIT owning a carried interest in a real estate

partnership.

88

Tax Acceleration

• Tax on carried interest is accelerated if:

— Carried interest holder transfers carried interest (even

transfers to family partnerships or REIT operating

partnerships).

— Carried interest holder receives property distributions

from the partnership.

— Partnership merges into another partnership.

• In limited cases, the carried Interest holder can elect to avoid

the gain if the carried Interest taint is carried over to the new

partnership (e.g., a partnership merger, division or

termination under Sect. 708(b)(1)(B)).

89

Other Consequences

• When an individual is engaged in the trade or business of

providing specified services, income taken into account as

ordinary income would become subject to self-employment

tax .

— This applies regardless of whether the partner is a limited

partner and regardless of whether the underlying

partnership income would be exempt from self-

employment tax (e.g., dividends, interest, capital gain).

• Net income and net loss generally is treated as ordinary.

— The idea is that carried interest is compensation income

and should not receive tax losses like an investment.

90

Qualified Capital Exception

• Carried Interest holder can exclude ―qualified capital‖ that is

acquired for invested capital and is intended to be the ―side-

by-side‖ capital such holder puts in with the investors.

• To apply the rule, there must be an unrelated investor who

contributes cash in exchange for a capital interest on the

same basis as the carried interest holder.

• One exception: Carried interest rule does not apply if all

allocations, distributions and capital contributions have been

pro rata.

91

Qualified Capital Exception: Loans

• Carried interest holder will not be treated as having a

qualified capital interest, to the extent that contributed

capital is attributable to a loan made or guaranteed, directly

or indirectly, by any other partner or the partnership (or a

person related to such partner or the partnership).

• Other loans to carried interest holder are not disqualified.

91

92

Sale Of Interests In Fund Manager Entity

• Obama budget: ―Committed to working with Congress to

develop mechanisms to assure the proper amount of income

recharacterization where the business has goodwill or other

assets unrelated‖ to services

B A

GP

Goodwill

C

LLC

20%

GP 20%

Investors Investors LP LP

A, B and C Sell LLC Interests

XYZ Fund Managers

93

Fund Documents: Key Tax Provisions (Cont.)

• Offering memorandum

• Limited partnership agreement

• Subscription documents

• Side letters

• Tax opinions

94

Fund Documents: Key Tax Provisions (Cont.)

• Private placement memorandum

• Summary of key tax provisions

• General overview of tax treatment

95

Fund Documents: Key Tax Provisions (Cont.)

• Limited partnership agreement (operating agreement)

Examples of key tax-related provisions:

• ECI and UBTI covenants

• GP clawback

• Management fee waivers

• Management fee offsets

• Withholding

• Allocations

• Tax distributions

• Non-U.S. taxes and returns

• Tax information reporting

• Tax matters partner

96

Fund Documents: Key Tax Provisions (Cont.)

• Subscription documents

• Investor tax

representations

• PTP representations

• Transfer restrictions

• Electronic K-1 consent

• Side letters

• PFIC/QEF election and

CFCs

• Foundation issues

• ERISA issues

• Tax reporting, and

much more

• Tax opinions

• Partnership tax opinion

• 514(c)(9) opinion

• Prohibited transactions

• 892 non-U.S.

governmental investors

• Non-U.S. investor-specific

issues