tax chp 7 answer key

DESCRIPTION

Tax chapter 7 answer keyTRANSCRIPT

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Chapter 7Corporate Taxation: Nonliquidating Distributions

SOLUTIONS MANUAL

DISCUSSION QUESTIONS

1. [LO1] What is meant by the term double taxation of corporate income?

The term double taxation refers to the fact that under the U.S. system of taxation, corporate earnings are first taxed when earned by a C corporation and then are taxed a second time when the earnings are distributed to the shareholders as a dividend.

2. [LO1] How does the issue of double taxation arise when a corporation decides between making a distribution to a shareholder employee as a dividend or compensation?

A distribution characterized as a dividend is subject to double taxation, first at the corporate level and then a second time at the shareholder level, because a corporation cannot deduct it from taxable income. A distribution characterized as compensation is taxed only once, at the recipient level, because it is deducted by the corporation.

3. [LO1] Why might a shareholder who is also an employee prefer receiving a dividend instead of compensation from a corporation?

An individual might prefer a dividend to compensation because the dividend is eligible for a preferential tax rate if the individual employee/shareholder is below a certain income level, whereas compensation is always taxed at the ordinary tax rates, which could be as high as 39.6 percent.

4. [LO2] What are the three potential tax treatments of a cash distribution to a shareholder? Are these potential tax treatments elective by the shareholder?

A cash distribution to a shareholder can be characterized as 1) dividend to the extent of earnings and profits, 2) tax-free return of capital to the extent of the shareholder’s tax basis in the stock, or 3) gain from sale of the stock (capital gain). The tax law (section 301(c)) prescribes the tax treatment of the distribution; it is not elective by the shareholder.

5. [LO2] In general, what is the concept of earnings and profits designed to represent?

Earnings and profits is intended to represent the corporation’s ability to pay distributions to its shareholders without eroding its invested capital. Earnings and profits is designed to reflect the corporation’s economic income, a broader concept than its taxable income.

6. [LO2] How does current earnings and profits differ from accumulated earnings and profits? Is there any congressional logic for keeping the two accounts separate?

7-1© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Current earnings and profits represents the corporation’s earnings and profits of the current year before reduction (“diminution”) by any distributions made during the year. Accumulated earnings and profits represents undistributed earnings and profits from all years prior to the current year. Congress created this distinction in 1936 when distributed current year earnings were taxed at the corporate level at a lower rate than undistributed earnings. This dual level of taxation was repealed in 1939, but the congressional distinction between current and accumulated earnings and profits remained in the law.

7. [LO2] True or False. A calendar-year corporation has positive current E&P of $100 and accumulated negative E&P of $200. A cash distribution of $100 to the corporation’s sole shareholder at year-end will not be treated as a dividend because total E&P is negative $100. Explain.

False. The $100 distribution will be treated as a dividend because it does not exceed current earnings and profits.

8. [LO2] True or False. A calendar-year corporation has negative current E&P of $100 and accumulated E&P of $100. A cash distribution of $100 to the corporation’s sole shareholder on June 30 will not be treated as a dividend because total E&P at December 31 is $0. Explain.

False. A portion of the distribution could be treated as a dividend based on accumulated earnings and profits on June 30. If the current year deficit is earned ratably over the year, accumulated earnings and profits on June 30 would be $50 [$100 - 181/365 x ($100)]. A deficit in current earnings and profits is allocated on a per day basis unless determined by tracing specific items that caused the deficit.

9. [LO2] List the four basic adjustments that a corporation makes to taxable income or net loss to compute current E&P. What is the rationale for making these adjustments?

A corporation adjusts its taxable income or loss by the following general items to compute current E&P:1. Inclusion of income that is excluded from taxable income2. Disallowance of certain expenses that are deducted in computing taxable income but do not require an economic outflow3. Deduction of certain expenses that are excluded from the computation of taxable income but do require an economic outflow4. Deferral of deductions or acceleration of income due to separate accounting methods required for E&P purposes

10. [LO2] What must a shareholder consider in computing the amount of a noncash distribution to include in her gross income?

7-2© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

A shareholder must determine the fair market value of the distribution and any liability she will assume on receipt of the property. The shareholder’s dividend amount is the fair market value of the property received less any liability assumed on the property.

11. [LO2] What income tax issues must a corporation consider before it makes a noncash distribution to a shareholder?

A corporation must determine if the property’s fair market value exceeds or is less than the property’s tax basis. To the extent the fair market value exceeds the tax basis, the corporation recognizes gain on the distribution. Corporations cannot recognize loss if the property’s fair market value is less than the tax basis.

12. [LO2] Will the shareholder’s tax basis in noncash property received equal the amount she includes in gross income as a dividend? Under what circumstances will the amounts be different, if any?

Not always. Where the shareholder assumes a liability attached to the property, the amount of the dividend income is computed as the property’s fair market value less the liability assumed (section 301(b)). The shareholder takes a tax basis in the property equal to its fair market value, not reduced by the liability assumed (section 301(d)).

13. A shareholder receives appreciated noncash property from his corporation and assumes a liability attached to the property. How does the liability assumption affect the amount of dividend he reports in gross income?

The shareholder’s assumption of a liability attached to noncash property reduces the amount of the dividend income reported.

14. A shareholder receives appreciated noncash property from his corporation and assumes a liability attached to the property. How does this assumption affect the amount of gain the corporation recognizes? From the corporation’s perspective, does it matter if the liability assumed by the shareholder exceeds the property’s gross fair market value?

In general, the shareholder’s assumption of a liability attached to appreciated noncash property distributed as a dividend does not affect the gain recognized by the corporation. Gain recognized is the property’s fair market value less the property’s tax basis. If the liability assumed by the shareholder exceeds the property’s fair market value, the property is deemed to have a fair market value equal to the liability assumed for purposes of determining the gain recognized by the corporation.

15. [LO2] A corporation distributes appreciated noncash property to a shareholder as a dividend. What impact does the distribution have on the corporation’s earnings and profits?

The corporation reduces E&P by the lesser of the property’s fair market value or E&P adjusted basis, reduced by any liability assumed by the shareholder on the distribution.

7-3© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

16. [LO3] Amy is the sole shareholder of her corporation. Rather than have the corporation pay her a dividend, Amy decides to have the corporation declare a “bonus” at year-end and pay her tax-deductible compensation. What potential tax issue may arise in this situation? Which parties, Amy or the corporation or both, are affected by the classification of the payment?

The IRS might argue that a portion of the distribution is really a disguised dividend if the compensation is “unreasonable.” If the IRS prevails, the corporation will be denied a deduction for the portion of the “bonus” determined to be a disguised dividend. Amy will now be eligible for a reduced rate of tax on the dividend portion of her “bonus” and will not be subject to payroll taxes on the recharacterized amount.

17. [LO4] Why might a corporation issue a stock dividend to its shareholders?

Corporations often issue stock dividends as a goodwill gesture to their shareholders when they do not have sufficient cash to make a distribution. Many times, corporations will engage in a stock split to increase the number of shares outstanding and lower the trading price of the stock to make it more accessible to a broader class of investors.

18. [LO4] What tax issue arises when a shareholder receives a nontaxable stock dividend?

The shareholder must allocate some of the tax basis of the existing stock to the new stock received based on the relative fair market values of the existing and newly issued stock.

19. [LO4] In general, what causes a stock dividend to be taxable to the recipient?

Stock dividends generally are taxable when they result in, or have the potential to result in, a change in the proportionate stock ownership of the existing shareholders. For example, where a shareholder can choose between cash or stock, there exists the possibility that some shareholders will choose cash and some will choose stock. Those who choose stock will increase their ownership percentage relative to those who choose cash. In this cash, the stock dividend will be taxable to those who choose to receive stock.

20. [LO5] What are the potential tax consequences to a shareholder who participates in a stock redemption?

A shareholder who participates in a stock redemption potentially could treat the distribution as an exchange (section 302) or as a property distribution (potentially a dividend) under section 301.

21. [LO5] What stock ownership tests must be met before a shareholder receives exchange treatment under the substantially disproportionate change-in-stock-ownership test in a stock redemption? Why is a change in stock ownership test used to determine the tax status of a stock redemption?

7-4© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

A shareholder meets the substantially disproportionate change-in-stock-ownership test by satisfying three mechanical stock ownership tests:1. Immediately after the exchange the shareholder owns less than 50% of the total combined voting power of all classes of stock entitled to vote;2. The shareholder’s percentage ownership of voting stock after the redemption is less than 80% of his or her percentage ownership before the redemption; and3. The shareholder’s percentage ownership of the aggregate fair market value of the corporation’s common stock (voting and nonvoting) after the redemption is less than 80% of his or her percentage ownership before the redemption.

The Code uses a change in stock ownership test to determine the tax status of a stock redemption to distinguish between transactions that resemble sales from transactions that are in substance a dividend distribution (that is, a transaction in which the shareholder does not meaningfully change her stock ownership in the company).

22. [LO5] What are the criteria to meet the “not essentially equivalent to a dividend” change-in-stock-ownership test in a stock redemption?

To satisfy the “not essentially equivalent to a dividend” requirement, the IRS or a court must conclude that there has been a “meaningful” reduction in the shareholder’s ownership interest in the corporation as a result of the redemption. The Code does not provide any mechanical tests to make this determination. At a minimum, the IRS and courts generally require the shareholder to reduce his stock ownership as a result of the transaction and own 50 percent or less of the stock after the transaction.

23. [LO5] When might a shareholder have to rely on the not essentially equivalent to a dividend test in arguing her stock redemption should be treated as an exchange for tax purposes?

A shareholder will have to rely on this test if she cannot meet either the “substantially disproportionate test” or the “complete termination of interest” test, which rely on a mechanical set of criteria.

24. [LO5] Why do you think the tax law imposes constructive stock ownership rules on stock redemptions?

The tax law imposes constructive ownership tests to prevent a shareholder from technically disposing of his stock interest while effectively continuing to own stock through family members or through ownership in an entity that nominally owns the stock.

25. [LO5] Which members of a family are included in the family attribution rules? Is there any rationale for the family members included in the test?

7-5© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Family members include spouse, children, parents, and grandchildren. These are the family members that are the most closely related to the shareholder by blood. Family members excluded are grandparents, brothers and sisters, aunts and uncles, and nieces, nephews, and cousins.

26. [LO5] Ilya and Olga are brother and sister. Ilya owns 200 shares of stock in Parker Corporation. Is Olga deemed to own Ilya’s 200 shares under the family attribution rules that apply to stock redemptions?

No. A brother and sister are not included under the family attribution rules.

27. [LO5] Maria has all of her stock in Mayan Corporation redeemed. Under what conditions will Maria treat the redemption as an exchange and recognize capital gain or loss?

Maria will treat the stock redemption as an exchange if she does not own any additional stock through attribution that causes her to fail either of the other two stock ownership tests. If she only owns stock constructively through the family attribution rules, she can waive the family attribution rules by filing a triple i agreement with the IRS and avoid acquiring a prohibited interest in the corporation for 10 years (for example, as an employee or independent contractor).

28. [LO5] What must a shareholder do to waive the family attribution rules in a complete redemption of stock?

A shareholder must file a triple i agreement with the IRS and refrain from having a prohibited interest (shareholder, employee, director, officer, or consultant) for 10 years. The shareholder must agree to notify the IRS district director within 30 days if he or she acquires a prohibited interest within 10 years after the redemption.

29. [LO5] How does a corporation’s computation of earnings and profits differ based on the tax treatment of a stock redemption to the shareholder (that is, as either a dividend or exchange)?

If the redemption is treated as a dividend, the corporation reduces E&P using the dividend reduction rules. If the redemption is treated as an exchange, the corporation reduces E&P at the date of distribution by the percentage of stock redeemed, not to exceed the fair market value of the property distributed. The distributing corporation reduces its E&P by any dividend distributions made during the year before reducing its E&P for redemptions treated as exchanges.

30. [LO6] How does the tax treatment of a partial liquidation differ from a stock redemption?

In a partial liquidation, the shareholders have prescribed tax treatments: individuals receive exchange treatment and corporations treat the distribution as a dividend to the

7-6© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

extent of earnings and profits. In a stock redemption, each shareholder’s tax treatment depends on whether a change in stock ownership requirement is met.

31. [LO6] Bevo Corporation experienced a complete loss of its mill as the result of a fire. The company received $2 million from the insurance company. Rather than rebuild, Bevo decided to distribute the $2 million to its two shareholders. No stock was exchanged in return. Under what conditions will the distribution meet the requirements to be a partial liquidation and not a dividend? Why does it matter to the shareholders?

For a distribution to be in partial liquidation of the corporation, it must either be “not essentially equivalent to a dividend” (as determined at the corporate level) or be the result of the termination of a “qualified trade or business.” In this case, the test likely will be whether the use of the mill constituted a qualified trade or business. The determination matters most to individuals, who will receive exchange treatment if the transaction is a partial liquidation and a potential dividend if not.

Problems

32. [LO1] Gopher Corporation reported taxable income of $500,000 this year. Gopher paid a dividend of $100,000 to its sole shareholder, Sven Anderson. Gopher Corporation is subject to a flat rate tax of 34%. The dividend meets the requirements to be a qualified dividend and Sven is subject to a tax rate of 15% on the dividend. What is the income tax imposed on the corporate income earned by Gopher and the income tax on the dividend distributed to Sven?

Corporate tax: $500,000 34% $170,000Shareholder tax: $100,000 15% 15,000Total income tax $185,000

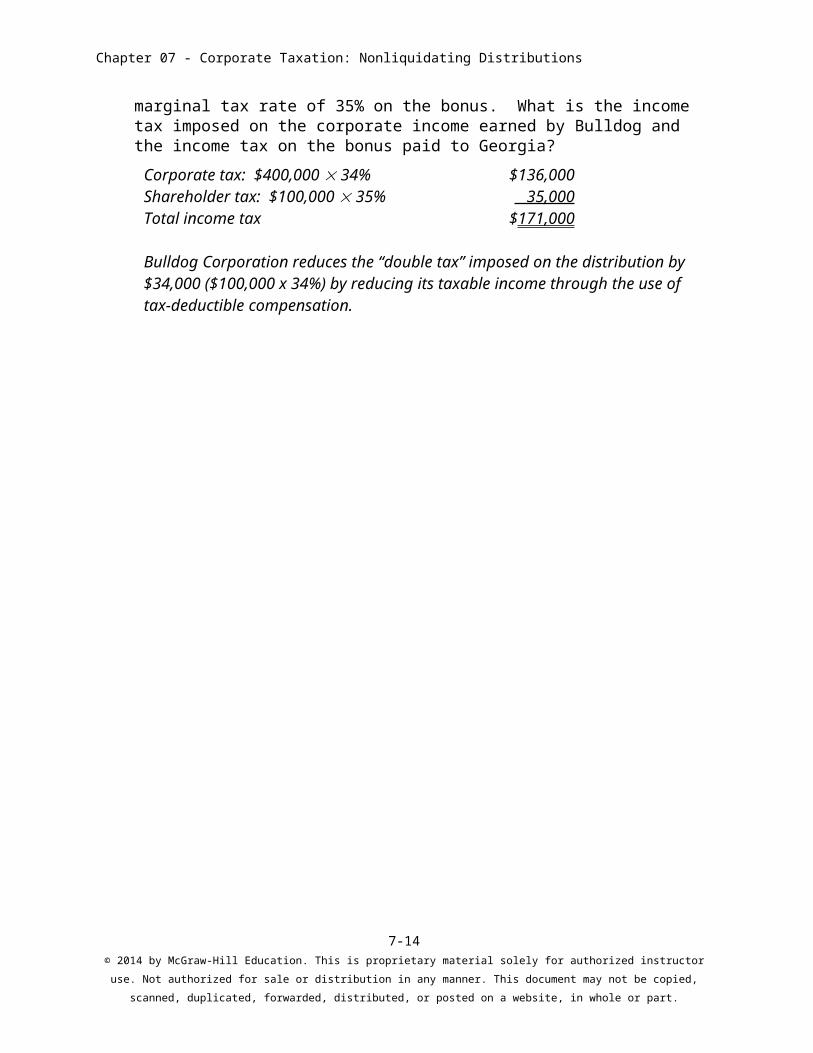

33. [LO1] Bulldog Corporation reported taxable income of $500,000 this year before any deduction for any payment to its sole shareholder and employee, Georgia Brown. Bulldog chose to pay a bonus of $100,000 to Georgia at year-end. Bulldog Corporation is subject to a flat-rate tax of 34%. The bonus meets the requirements to be “reasonable” and is therefore deductible by Bulldog. Georgia is subject to a marginal tax rate of 35% on the bonus. What is the income tax imposed on the corporate income earned by Bulldog and the income tax on the bonus paid to Georgia?

Corporate tax: $400,000 34% $136,000Shareholder tax: $100,000 35% 35,000Total income tax $171,000

Bulldog Corporation reduces the “double tax” imposed on the distribution by $34,000 ($100,000 x 34%) by reducing its taxable income through the use of tax-deductible compensation.

7-7© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

34. [LO2] Hawkeye Company reports current E&P of $300,000 this year and accumulated E&P at the beginning of the year of $200,000. Hawkeye distributed $400,000 to its sole shareholder, Ray Kinsella, on December 31 of this year. Ray’s tax basis in his Hawkeye stock is $75,000.

a. How much of the $400,000 distribution is treated as a dividend to Ray?

All $400,000 is treated as a dividend because the distribution is less than the company’s total earnings and profits of $500,000.

b. What is Ray’s tax basis in his Hawkeye stock after the distribution?

Ray’s tax basis in his Hawkeye stock remains $75,000.

c. What is Hawkeye’s balance in accumulated E&P as of January 1 of next year?

Accumulated E&P as of January 1 is $100,000, computed as $500,000 - $400,000.

35. [LO2] Jayhawk Company reports current E&P of $300,000 and accumulated E&P of negative $200,000. Jayhawk distributed $400,000 to its sole shareholder, Christine Rock, on the last day of the year. Christine’s tax basis in her Jayhawk stock is $75,000.

a. How much of the $400,000 distribution is treated as a dividend to Christine?

Christine has dividend income of $300,000, all of which is from the company’s current E&P.

b. What is Christine’s tax basis in her Jayhawk stock after the distribution?

Christine reduces her tax basis in the Jayhawk stock by $75,000 to $0, which is the lesser of the distribution in excess of current E&P ($100,000) or her basis in the Jayhawk stock ($75,000). The remaining $25,000 is treated as gain from sale of the Jayhawk stock (capital gain).

c. What is Jayhawk’s balance in accumulated E&P on the first day of next year?

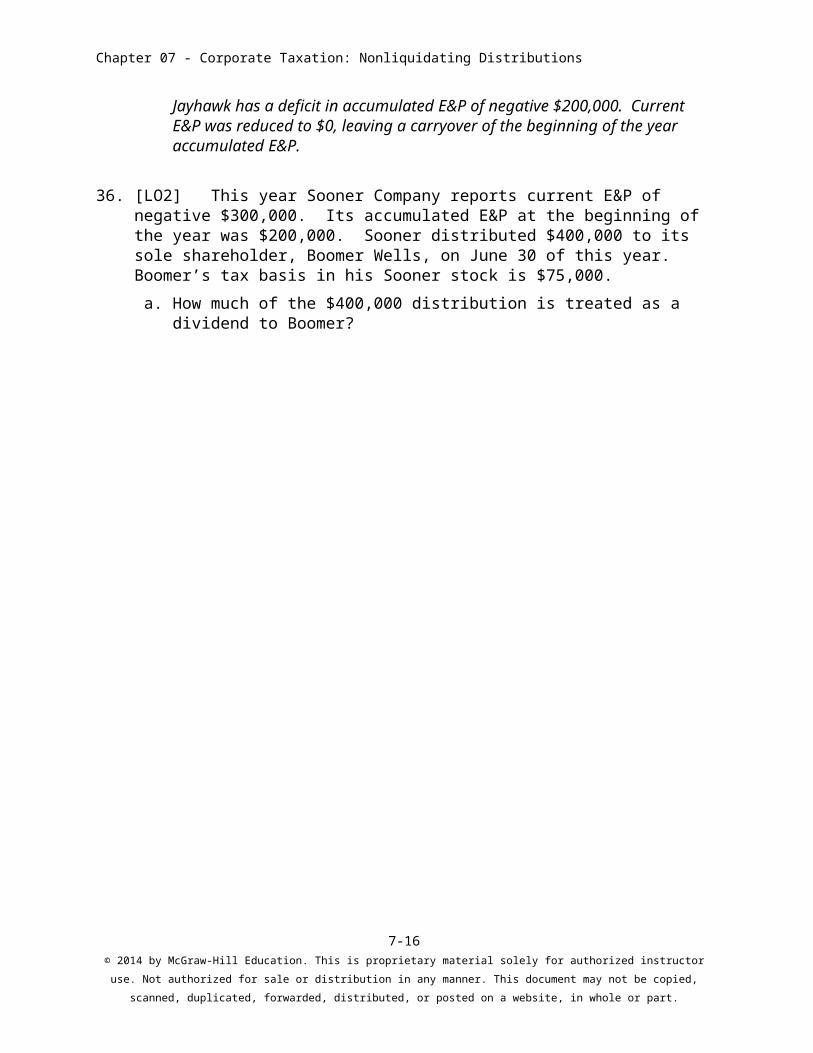

Jayhawk has a deficit in accumulated E&P of negative $200,000. Current E&P was reduced to $0, leaving a carryover of the beginning of the year accumulated E&P.

36. [LO2] This year Sooner Company reports current E&P of negative $300,000. Its accumulated E&P at the beginning of the year was $200,000. Sooner distributed $400,000 to its sole shareholder, Boomer Wells, on June 30 of this year. Boomer’s tax basis in his Sooner stock is $75,000.

a. How much of the $400,000 distribution is treated as a dividend to Boomer?

7-8© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

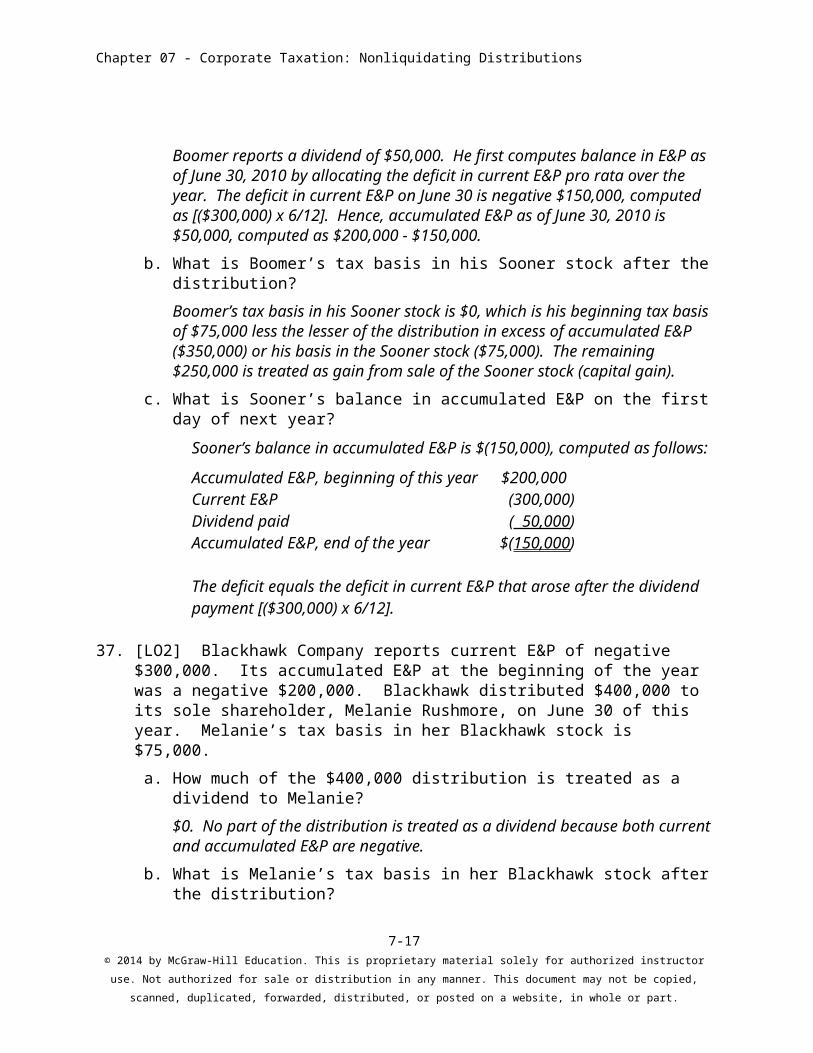

Boomer reports a dividend of $50,000. He first computes balance in E&P as of June 30, 2010 by allocating the deficit in current E&P pro rata over the year. The deficit in current E&P on June 30 is negative $150,000, computed as [($300,000) x 6/12]. Hence, accumulated E&P as of June 30, 2010 is $50,000, computed as $200,000 - $150,000.

b. What is Boomer’s tax basis in his Sooner stock after the distribution?

Boomer’s tax basis in his Sooner stock is $0, which is his beginning tax basis of $75,000 less the lesser of the distribution in excess of accumulated E&P ($350,000) or his basis in the Sooner stock ($75,000). The remaining $250,000 is treated as gain from sale of the Sooner stock (capital gain).

c. What is Sooner’s balance in accumulated E&P on the first day of next year?

Sooner’s balance in accumulated E&P is $(150,000), computed as follows:

Accumulated E&P, beginning of this year $200,000Current E&P (300,000)Dividend paid ( 50,000)Accumulated E&P, end of the year $(150,000)

The deficit equals the deficit in current E&P that arose after the dividend payment [($300,000) x 6/12].

37. [LO2] Blackhawk Company reports current E&P of negative $300,000. Its accumulated E&P at the beginning of the year was a negative $200,000. Blackhawk distributed $400,000 to its sole shareholder, Melanie Rushmore, on June 30 of this year. Melanie’s tax basis in her Blackhawk stock is $75,000.

a. How much of the $400,000 distribution is treated as a dividend to Melanie?

$0. No part of the distribution is treated as a dividend because both current and accumulated E&P are negative.

b. What is Melanie’s tax basis in her Blackhawk stock after the distribution?

Melanie’s tax basis in her Blackhawk stock is $0, which is her beginning tax basis less the lesser of the distribution in excess of accumulated E&P ($400,000) or her basis in the Blackhawk stock ($75,000). The remaining $325,000 is treated as gain from sale of the Blackhawk stock (capital gain).

c. What is Blackhawk’s balance in accumulated E&P on the first day of next year?

Negative $500,000, the combined deficit in the beginning balance in accumulated E&P and the deficit in current E&P.

7-9© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

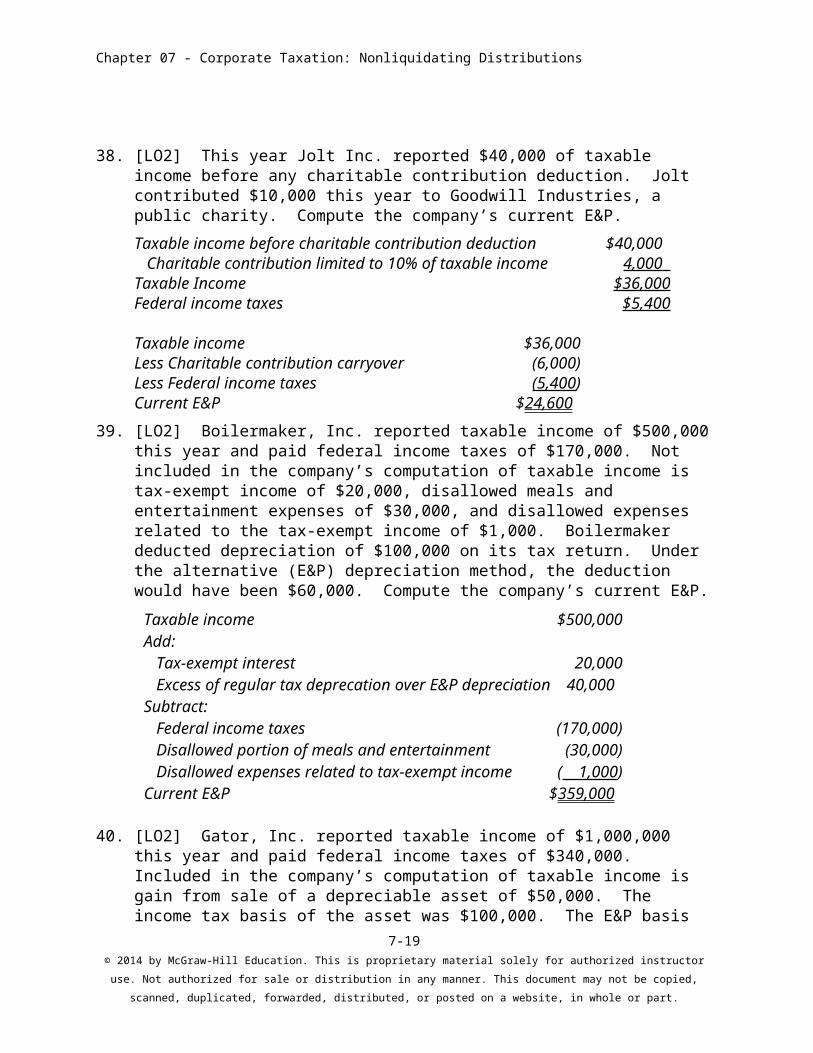

38. [LO2] This year Jolt Inc. reported $40,000 of taxable income before any charitable contribution deduction. Jolt contributed $10,000 this year to Goodwill Industries, a public charity. Compute the company’s current E&P.

Taxable income before charitable contribution deduction $40,000 Charitable contribution limited to 10% of taxable income 4,000 Taxable Income $36,000Federal income taxes $5,400

Taxable income $36,000Less Charitable contribution carryover (6,000)Less Federal income taxes (5,400)Current E&P $24,600

39. [LO2] Boilermaker, Inc. reported taxable income of $500,000 this year and paid federal income taxes of $170,000. Not included in the company’s computation of taxable income is tax-exempt income of $20,000, disallowed meals and entertainment expenses of $30,000, and disallowed expenses related to the tax-exempt income of $1,000. Boilermaker deducted depreciation of $100,000 on its tax return. Under the alternative (E&P) depreciation method, the deduction would have been $60,000. Compute the company’s current E&P.

Taxable income $500,000Add: Tax-exempt interest 20,000 Excess of regular tax deprecation over E&P depreciation 40,000Subtract: Federal income taxes (170,000) Disallowed portion of meals and entertainment (30,000) Disallowed expenses related to tax-exempt income ( 1,000)Current E&P $359,000

40. [LO2] Gator, Inc. reported taxable income of $1,000,000 this year and paid federal income taxes of $340,000. Included in the company’s computation of taxable income is gain from sale of a depreciable asset of $50,000. The income tax basis of the asset was $100,000. The E&P basis of the asset using the alternative depreciation system was $175,000. Compute the company’s current E&P.

7-10© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Taxable income $1,000,000Subtract: Federal income taxes (340,000) Regular tax gain from sale of asset ($150,000 - $100,000) ( 50,000) E&P loss from sale of asset ($150,000 - $175,000) ( 25,000)Current E&P $585,000

41. [LO2] Paladin, Inc. reported taxable income of $1,000,000 this year and paid federal income taxes of $340,000. The company reported a capital gain from sale of investments of $150,000, which was partially offset by a $100,000 net capital loss carryover from last year, resulting in a net capital gain of $50,000 included in taxable income. Compute the company’s current E&P.

Taxable income $1,000,000Add: NCL carryover 100,000Subtract: Federal income taxes (340,000)Current E&P $760,000

42. [LO2] Volunteer Corporation reported taxable income of $500,000 from operations for this year. The company paid federal income taxes of $170,000 on this taxable income. During the year, the company made a distribution of land to its sole shareholder, Rocky Topp. The land’s fair market value was $75,000 and its tax and E&P basis to Volunteer was $25,000. Rocky assumed a mortgage attached to the land of $15,000. Any gain from the distribution will be taxed at 34 percent. The company had accumulated E&P of $750,000 at the beginning of the year.

a. Compute Volunteer’s total taxable income and federal income tax.

Taxable income from operations $500,000Gain on distribution of land ($75,000 - $25,000) 50,000Total taxable income $550,000Federal income tax ($550,000 x 34%) 187,000

b. Compute Volunteer’s current E&P before the distribution.

Taxable income $550,000Subtract: Federal income tax (187,000) Adjustment for E&P gain on distribution of land ( 0)Current E&P $363,000

7-11© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

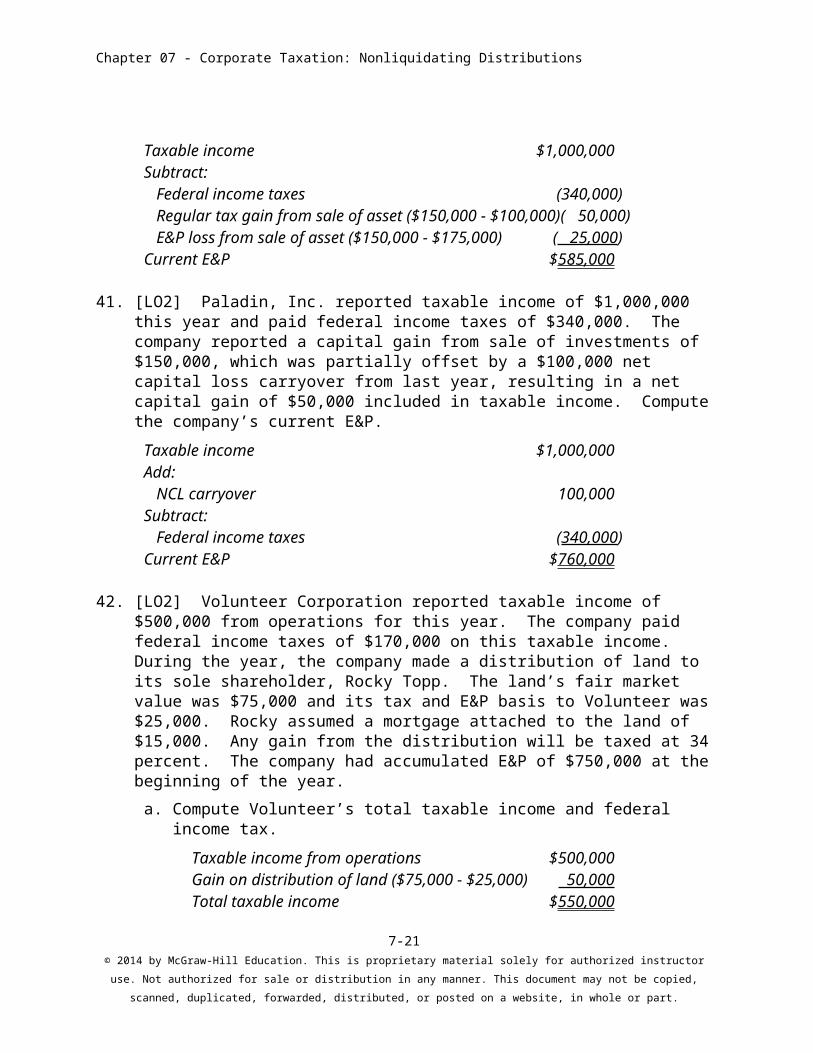

c. Compute Volunteer’s accumulated E&P at the beginning of next year.

Current E&P $363,000Subtract: Fair market value of land distributed this year (75,000)Add: Mortgage assumed by Rocky 15,000CE&P after distribution $303,000Accumulated E&P, beginning of this year 750,000Accumulated E&P, beginning of next year $1,053,000

d. What amount of dividend income does Rocky report as a result of the distribution?

Rocky reports dividend income of $60,000, computed as the fair market value of the land received ($75,000) less the liability he assumes ($15,000).

e. What is Rocky’s income tax basis in the land received from Volunteer?

$75,000. Rocky’s income tax basis in the land equals its fair market value.

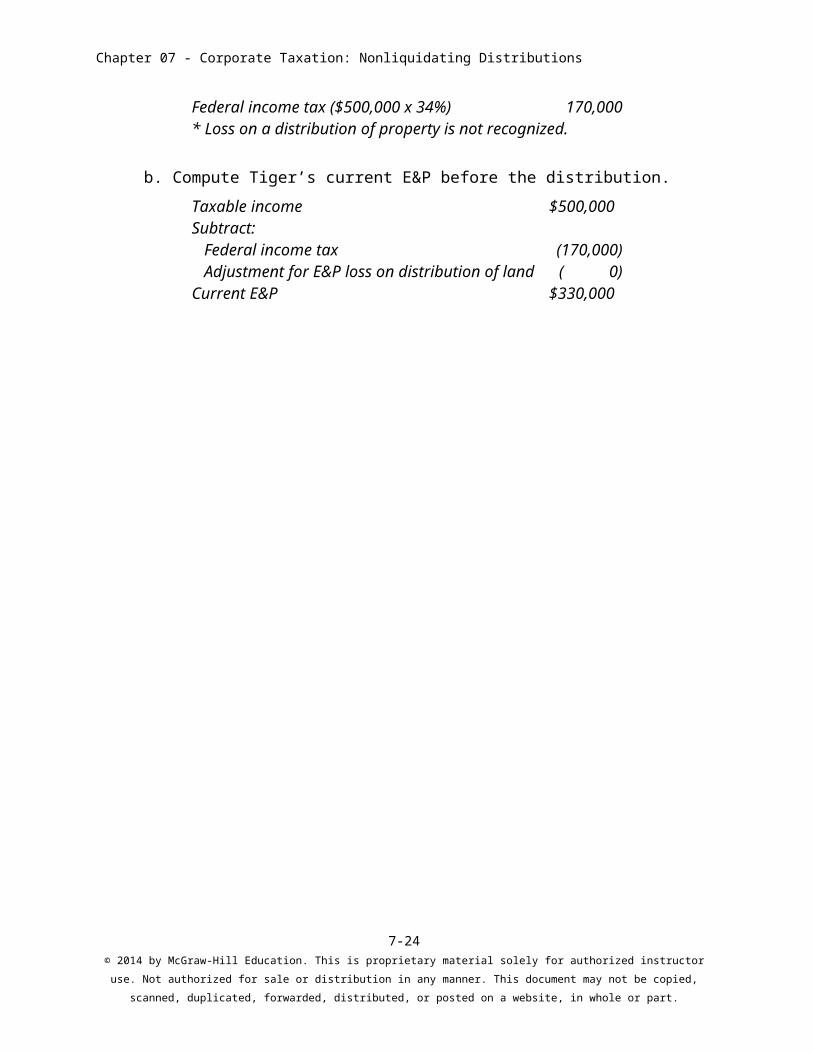

43. [LO2] Tiger Corporation reported taxable income of $500,000 from operations for this year. The company paid federal income taxes of $170,000 on this taxable income. During the year, the company made a distribution of land to its sole shareholder, Mike Woods. The land’s fair market value was $75,000 and its tax and E&P basis to Tiger was $125,000. Mike assumed a mortgage attached to the land of $15,000. Any gain from the distribution will be taxed at 34 percent. The company had accumulated E&P of $750,000 at the beginning of the year.

a. Compute Tiger’s total taxable income and federal income tax.

Taxable income from operations $500,000Loss on distribution of land ($75,000 - $125,000)* 0Total taxable income $500,000Federal income tax ($500,000 x 34%) 170,000* Loss on a distribution of property is not recognized.

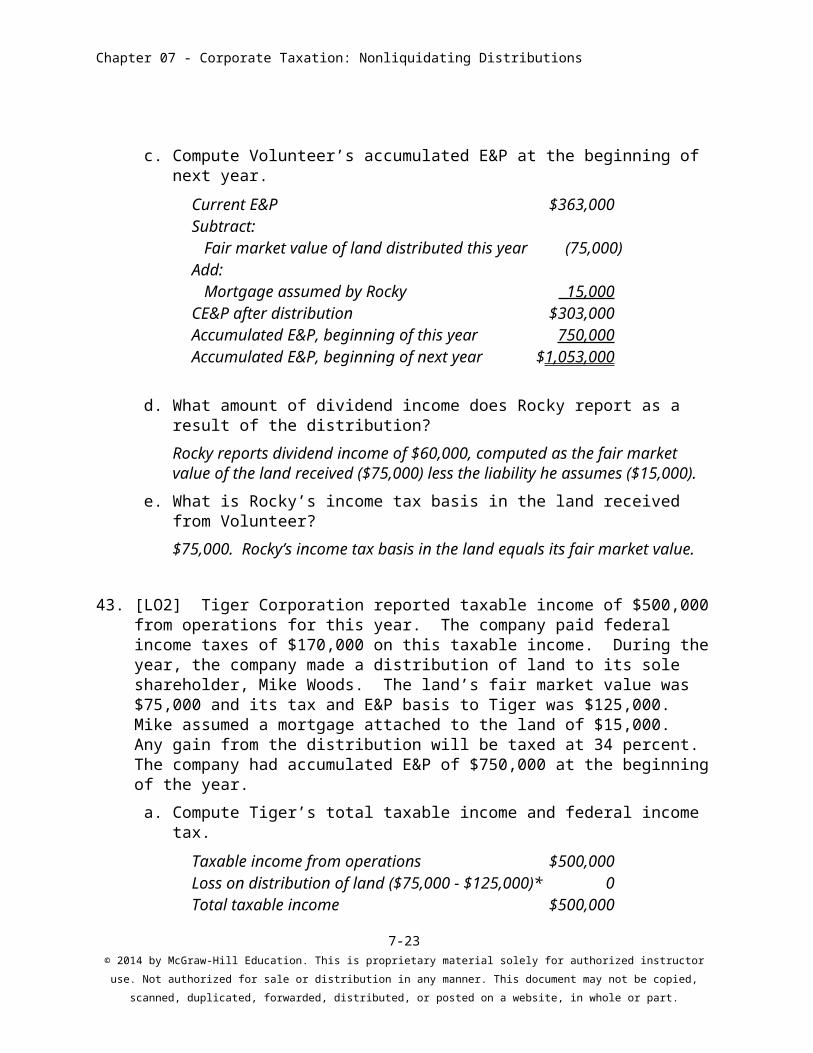

b. Compute Tiger’s current E&P before the distribution.

Taxable income $500,000Subtract: Federal income tax (170,000) Adjustment for E&P loss on distribution of land ( 0)Current E&P $330,000

7-12© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

c. Compute Tiger’s accumulated E&P at the beginning of next year.

Current E&P $330,000Subtract: E&P basis of land distributed this year (125,000)Add: Mortgage assumed by Mike 15,000CE&P after distribution $220,000Accumulated E&P, beginning of this year 750,000Accumulated E&P, beginning of next year $970,000

d. What amount of dividend income does Mike report as a result of the distribution?

Mike reports dividend income of $60,000, computed as the fair market value of the land received ($75,000) less the liability he assumes ($15,000).

e. What is Mike’s tax basis in the land he received from Tiger?

$75,000. Mike’s income tax basis in the land equals its fair market value.

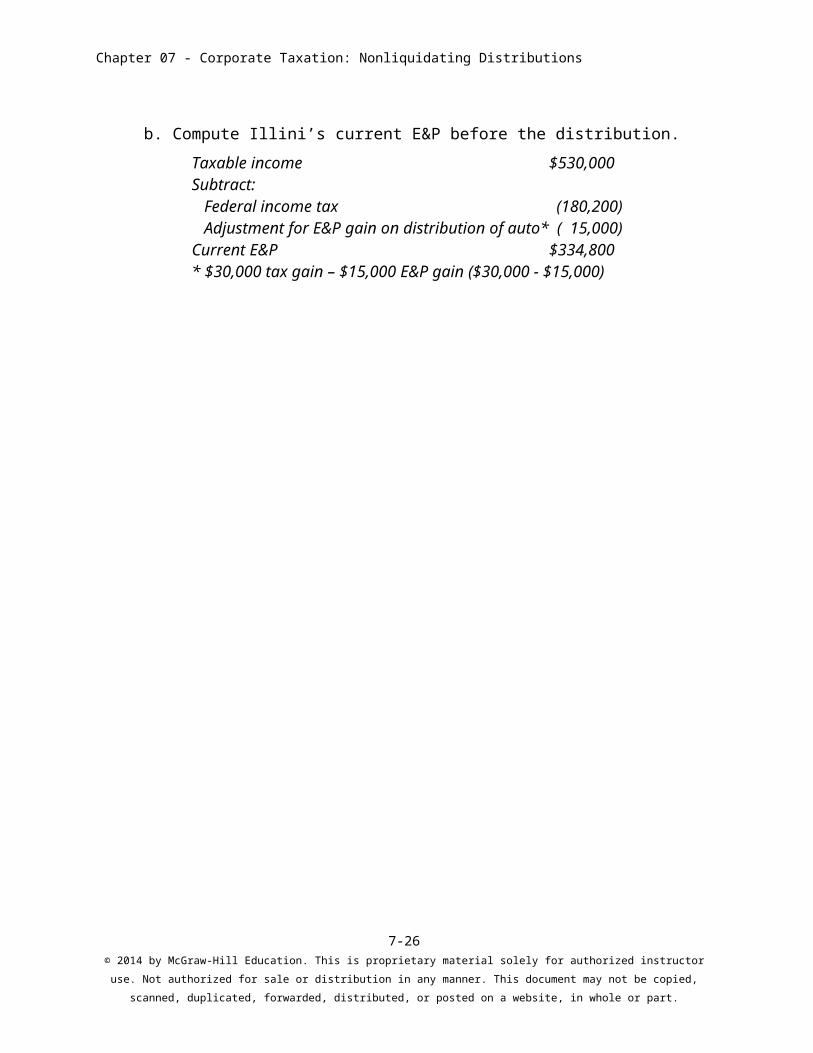

44. [LO2] Illini Corporation reported taxable income of $500,000 from operations for this year. The company paid federal income taxes of $170,000 on this taxable income. During the year, the company made a distribution of an automobile to its sole shareholder, Carly Urbana. The auto’s fair market value was $30,000 and its tax basis to Illini was $0. The auto’s E&P basis was $15,000. Any gain from the distribution will be taxed at 34 percent. Illini had accumulated E&P of $1,500,000.

a. Compute Illini’s total taxable income and federal income tax.

Taxable income from operations $500,000Gain on distribution of auto ($30,000 - $0) 30,000Total taxable income $530,000Federal income tax ($530,000 x 34%) 180,200

b. Compute Illini’s current E&P before the distribution.

Taxable income $530,000Subtract: Federal income tax (180,200) Adjustment for E&P gain on distribution of auto* ( 15,000)Current E&P $334,800* $30,000 tax gain – $15,000 E&P gain ($30,000 - $15,000)

7-13© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

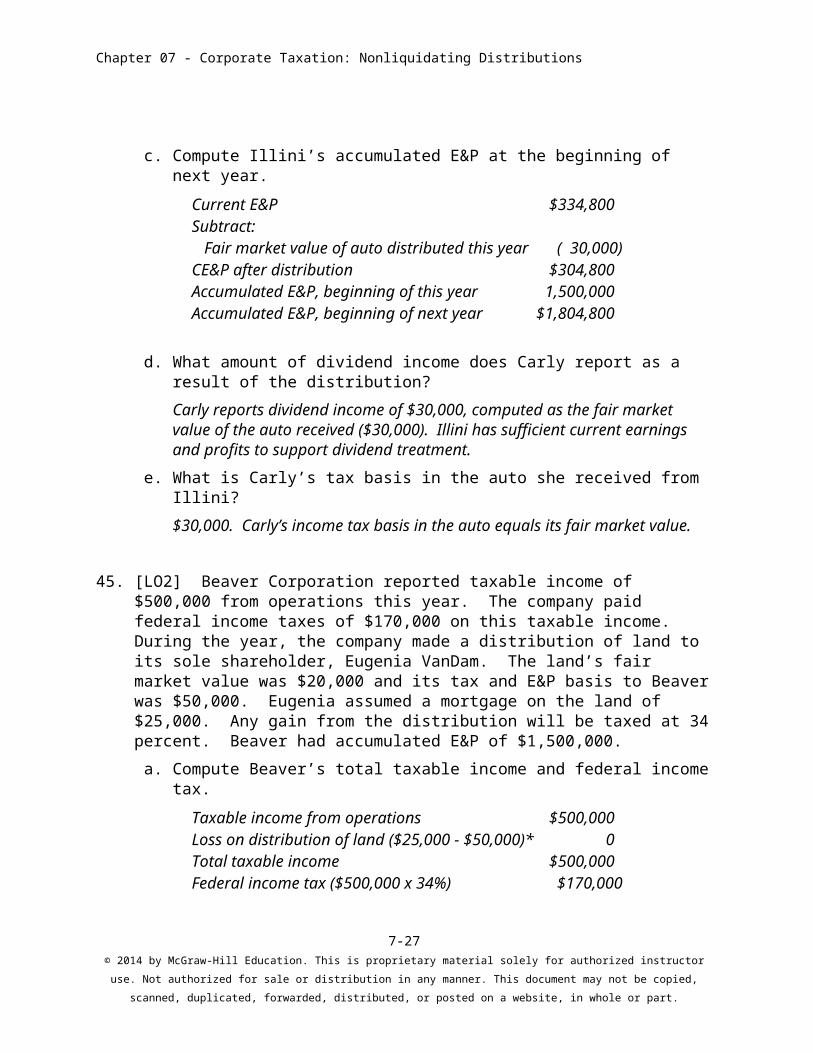

c. Compute Illini’s accumulated E&P at the beginning of next year.

Current E&P $334,800Subtract: Fair market value of auto distributed this year ( 30,000)CE&P after distribution $304,800Accumulated E&P, beginning of this year 1,500,000Accumulated E&P, beginning of next year $1,804,800

d. What amount of dividend income does Carly report as a result of the distribution?

Carly reports dividend income of $30,000, computed as the fair market value of the auto received ($30,000). Illini has sufficient current earnings and profits to support dividend treatment.

e. What is Carly’s tax basis in the auto she received from Illini?

$30,000. Carly’s income tax basis in the auto equals its fair market value.

45. [LO2] Beaver Corporation reported taxable income of $500,000 from operations this year. The company paid federal income taxes of $170,000 on this taxable income. During the year, the company made a distribution of land to its sole shareholder, Eugenia VanDam. The land’s fair market value was $20,000 and its tax and E&P basis to Beaver was $50,000. Eugenia assumed a mortgage on the land of $25,000. Any gain from the distribution will be taxed at 34 percent. Beaver had accumulated E&P of $1,500,000.

a. Compute Beaver’s total taxable income and federal income tax.

Taxable income from operations $500,000Loss on distribution of land ($25,000 - $50,000)* 0Total taxable income $500,000Federal income tax ($500,000 x 34%) $170,000

* Loss on a distribution of property is not recognized. Because the mortgage assumed exceeds the property’s fair market value, the land’s fair market value for purposes of computing gain would equal the mortgage assumed.

7-14© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

b. Compute Beaver’s current E&P before the distribution.

Taxable income $500,000Less: Federal income tax (170,000)Less: Adjustment for E&P loss on distribution of land ( 0)Current E&P $330,000

c. Compute Beaver’s accumulated E&P at the beginning of next year.

Current E&P $330,000Subtract: E&P basis of land distributed (50,000)Add: Mortgage assumed by Eugenia 25,000CE&P after distribution $305,000Accumulated E&P, beginning of this year 1,500,000Accumulated E&P, beginning of next year $1,805,000

d. What amount of dividend income does Eugenia report as a result of the distribution?

Eugenia reports dividend income of $0, computed as the fair market value of the land received ($20,000) less the liability she assumes ($25,000).

e. What is Eugenia’s income tax basis in the land received from Beaver?

$20,000. Eugenia’s income tax basis in the land equals its fair market value.

46. [LO2] {research form} Tiny and Tim each own half of the 100 outstanding shares of Flower Corporation. This year Flower reported taxable income of $6,000 and was subject to a 25 percent tax rate. In addition, Flower received $20,000 of life insurance proceeds due to the death of an employee (Flower paid $500 in life insurance premiums this year). Flower had $5,000 of accumulated E&P at the beginning of the year.

a. What is Flower’s current E&P?

Taxable income $ 6,000Less: Tax at 25% - 1,500Plus: tax exempt income + 20,000Less: expenses associated with exempt income - 500 Current E&P $ 24,000

b. Flower distributed $6,000 on February 15 and $30,000 on August 1. What total amount of dividends will Tiny and Tim report?

7-15© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Amount Distributed $6,000 $ 30,000proportion of total distribution 1/6 5/6Current E&P ($24,000 divided 1/6, 5/6) $ 4,000 $ 20,000Accumulated E&P (chronological) 2,000 3,000 Total dividend $ 6,000 $ 23,000

c. What amount of capital gain (if any) would Tiny and Tim report on the distributions in part b if their stock basis is $2,000 and $10,000, respectively?

The $6,000 distribution in February would have no impact on stock basis since this entire amount is treated as a dividend. Only $23,000 of the August distribution was dividend income and so the remaining $7,000 would be treated as a return of capital. Thus, $11,500 of the $15,000 received by each shareholder in August would be treated as dividend and the remaining $3,500 would be a return of capital. The $3,500 return of capital would reduce the basis of Tiny’s stock to zero and generate a $1,500 capital gain ($3,500 - $2,000). The $3,500 return of capital would only reduce Tim’s basis to $6,500 ($10,000 less $3,500).

d. What form would Flower use to report non-dividend distributions?

Form 5452 is used to report non-dividend distributions.

e. On what form (line) would Tiny and Tim report these distributions?

Dividend distributions are reported on line 5 of Part II of Schedule B (or line 9 of form 1040) while non-dividend distributions in excess of basis are reported initially on Form 8949. The totals from Form 8949 are then transferred to either Part I or Part II (depending on holding period) of Schedule D.

47. [LO3] Nittany Company pays its sole shareholder, Joe Papa, a salary of $100,000. At the end of each year, the company pays Joe a “bonus” equal to the difference between the corporation’s taxable income for the year (before the bonus) and $75,000. In this way, the company hopes to keep its taxable income at amounts that are taxed at either 15 percent or 25 percent. This year Nittany reported pre-bonus taxable income of $675,000 and paid Joe a bonus of $600,000. On audit, the IRS determined that individuals working in Joe’s position earned on average $300,000 per year. The company had no formal compensation policy and never paid a dividend.

a. How much of Joe’s bonus might the IRS recharacterize as a dividend?

7-16© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

The IRS could treat Joe as receiving a constructive dividend to the extent the “bonus” is considered unreasonable compensation. The IRS could argue that the total “compensation” in excess of what an individual in Joe’s position typically receives as compensation should be recharacterized as a dividend. Joe’s excess compensation would be $400,000 ($100,000 + $600,000 - $300,000).

b. What arguments might Joe make to counter this assertion?

Joe could argue that his value to the company exceeds what a person in his position receives on average. He would have to convince the IRS or the court that his role in the company has unique features. Factors that would work against Joe are the company’s lack of a formal compensation policy and not paying dividends.

c. Assuming the IRS recharacterizes $200,000 of Joe’s bonus as a dividend, what additional income tax liability does Nittany Company face?

Nittany would be denied a deduction for the $200,000, increasing the company’s taxable income from $75,000 to $275,000. The additional $200,000 increases the company’s tax liability by $76,750.

48. [LO4] Hoosier Corporation declared a 2-for-1 stock split to all shareholders of record on March 25 of this year. Hoosier reported current E&P of $600,000 and accumulated E&P of $3,000,000. The total fair market value of the stock distributed was $1,500,000. Barbara Bloomington owned 1,000 shares of Hoosier stock with a tax basis of $100 per share.

a. What amount of taxable dividend income, if any, does Barbara recognize this year? Assume the fair market value of the stock was $150 per share on March 25 of this year.

The stock dividend is not taxable because it is pro rata to all the shareholders.

b. What is Barbara’s income tax basis in the new and existing stock she owns in Hoosier Corporation, assuming the distribution is tax-free?

The new stock is allocated part of the tax basis of the old stock based on relative fair market value. In a 2 for 1 stock split, Barbara would allocate half of the basis of the old stock ($100) to the new stock, making her tax basis in the old and new stock $50 per share.

c. How does the stock dividend affect Hoosier’s accumulated E&P at the beginning of next year?

Hoosier does not adjust its E&P for the stock dividend because it is not taxable to the shareholders.

7-17© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

49. [LO4] Badger Corporation declared a stock dividend to all shareholders of record on March 25of this year. Shareholders will receive one share of Badger stock for each ten shares of stock they already own. Madison Cheeseman owns 1,000 shares of Badger stock with a tax basis of $100 per share. The fair market value of the Badger stock was $110 per share on March 25 of this year.

a. What amount of taxable dividend income, if any, does Madison recognize this year?

The stock dividend is not taxable because it is pro rata to all the shareholders.

b. What is Madison’s income tax basis in her new and existing stock in Badger Corporation, assuming the distribution is non-taxable?

The new stock is allocated part of the tax basis of the old stock based on relative fair market value. After the stock dividend, Madison will own 1,100 shares of Badger stock (1,000 + 1,000/10), each with the same fair market value. Her basis in each share of stock will be $91, computed as (1,000 shares x $100 basis) / 1,100.

c. How would you answer questions a and b if Madison was offered the choice between 1 share of stock in Badger for each 10 shares she owned or $100 cash for each 10 shares she owned in Badger?

If Madison choose the stock, she would have a taxable dividend equal to $11,000, computed as 1,000/10 x $110, because the distribution has the potential to be non pro rata to the shareholders. Madison’s tax basis in the stock she receives will equal its fair market value of $11,000 (100 x $110). If Madison choose the cash, she would be taxed on the amount of cash received, $1,000.

50. [LO5] Wildcat Company is owned equally by Evan Stone and his sister Sara, each of whom held 1,000 shares in the company. Sara wants to reduce her ownership in the company, and it was decided that the company will redeem 500 of her shares for $25,000 per share on December 31 of this year. Sara’s income tax basis in each share is $5,000. Wildcat has current E&P of $10,000,000 and accumulated E&P of $50,000,000.

a. What is the amount and character (capital gain or dividend) recognized by Sara as a result of the stock redemption?

Sara reduces her ownership in Wildcat Company from 50% to 33.33% (500/1,500). Sara meets the substantially disproportionate test to treat the redemption as an exchange. Under this test, she reduces her ownership below 50%, and her ownership percentage after the redemption is less than 80% of her ownership before the redemption (80% x 50% = 40%). As a result, Sara recognizes a capital gain of $20,000 per share ($25,000 - $5,000).

7-18© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

b. What is Sara’s income tax basis in the remaining 500 shares she owns in the company?

Sara’s income tax basis in the remaining shares remains $5,000 per share.

c. Assuming the company did not make any dividend distributions during this year, by what amount does Wildcat reduce its E&P as a result of the redemption?

$12,500,000. Wildcat reduces its accumulated E&P by the lesser of the cash distributed ($12,500,000 {500 * $25,000}) or the percentage of stock redeemed times accumulated E&P after reduction by any dividends paid during the year (500/2,000 x $60,000,000 = $15,000,000).

51. [LO5] Flintstone Company is owned equally by Fred Stone and his sister Wilma, each of whom hold 1,000 shares in the company. Wilma wants to reduce her ownership in the company, and it was decided that the company will redeem 250 of her shares for $25,000 per share on December 31 of this year. Wilma’s income tax basis in each share is $5,000. Flintstone has current E&P of $10,000,000 and accumulated E&P of $50,000,000.

a. What is the amount and character (capital gain or dividend) recognized by Wilma as a result of the stock redemption, assuming only the “substantially disproportionate with respect to the shareholder” test is applied?

Wilma reduces her ownership in Flintstone Company from 50% to 42.9% (750/1,750). Wilma fails the “substantially disproportionate” test to treat the redemption as an exchange. Although she reduces her ownership below 50%, her ownership percentage after the redemption is not less than 80% of her ownership before the redemption (80% x 50% = 40%). As a result, Wilma recognizes a dividend of $6,250,000 ($25,000 x 250 shares).

b. Given your answer to question a, what is Wilma’s income tax basis in the remaining 750 shares she owns in the company?

Wilma’s income tax basis in the remaining shares of stock is $5,000,000. Wilma adds back the “unused” tax basis of the 250 shares redeemed ($1,250,000) to the basis of her remaining 750 shares ($3,750,000).

c. Assuming the company did not make any dividend distributions this year, by what amount does Flintstone reduce its E&P as a result of the redemption?

Flintstone reduces its E&P by $6,250,000, the amount of dividend income reported by Wilma.

7-19© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

d. What other argument might Wilma make to treat the redemption as an exchange?

Wilma could argue that the distribution is not “essentially equivalent to a dividend” (section 301(b)(1)) because she reduced her ownership below 50 percent. This is a subjective test that requires IRS approval.

52. [LO5] Acme Corporation has 1,000 shares outstanding. Joan and Bill are married, and they each own 20 shares of Acme. Joan’s daughter, Shirley also owns 20 shares of Acme. Joan is an equal partner with Jeri in the J&J partnership, and this partnership owns 60 shares of Acme. Jeri is not related to Joan or Bill. How many shares of Acme is Shirley deemed to own under the stock attribution rules?

Shirley is deemed to own 90 shares of Acme. She owns 20 shares directly and is attributed 20 shares from Bill (family attribution). She is also attributed 50 shares from Joan (family attribution). Joan owns 20 shares directly and another 30 shares is attributed to Joan from J&J (50% of 60 shares through entity attribution). The 30 shares attributed to Joan are reattributed to Shirley through family attribution.

53. [LO5] Bedrock, Inc. is owned equally by Barney Rubble and his wife Betty, each of whom held 1,000 shares in the company. Betty wants to reduce her ownership in the company, and it was decided that the company will redeem 500 of her shares for $25,000 per share on December 31 of this year. Betty’s income tax basis in each share is $5,000. Bedrock has current E&P of $10,000,000 and accumulated E&P of $50,000,000.

a. What is the amount and character (capital gain or dividend) recognized by Betty as a result of the stock redemption, assuming only the “substantially disproportionate with respect to the shareholder” test is applied?

Betty reduces her direct ownership in Bedrock, Inc. from 50% to 33.3% (500/1,500). However, under the family attribution rules, she is deemed to own the 1,000 shares owned by her husband, Barney. Her stock ownership before the exchange is 100%, and her ownership after the exchange is still 100% (1,500/1,500). Betty fails the substantially disproportionate test to treat the redemption as an exchange. As a result, Betty recognizes a dividend of $12,500,000 ($25,000 x 500 shares).

b. Given your answer to question a, what is Betty’s income tax basis in the remaining 500 shares she owns in the company?

Betty’s income tax basis in her remaining shares is $5,000,000. Betty adds back the “unused” tax basis of the 500 shares redeemed ($2,500,000) to the basis of her remaining 500 shares ($2,500,000).

7-20© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

c. Assuming the company did not make any dividend distributions this year, by what amount does Bedrock reduce its E&P as a result of the redemption?

Bedrock reduces its accumulated E&P by the cash distributed ($12,500,000).

d. Can Betty argue that the redemption is “not essentially equivalent to a dividend” and should be treated as an exchange?

No. The attribution rules apply to this test as well as the other stock ownership tests. As a result, Betty is treated as owning 100% of the Bedrock stock before and after the reduction.

54. [LO5] {research} Assume in problem 53 that Betty and Barney are not getting along and have separated due to marital discord (although they are not legally separated). In fact, they cannot even stand to talk to each other anymore and communicate only through their accountant. Betty wants to argue that she should not be treated as owning any of Barney’s stock in Bedrock because of their hostility towards each other. Can family hostility be used as an argument to void the family attribution rules? Consult Rev. Rul. 80-26, 1980-1 C.B. 66, Robin Haft Trust v. Comm., 510 F.2d 43 (CA-1 1975), Metzger Trust v. Comm., 693 F.2d 459 (CA-5 1982, and Cerone v. Comm., 87 TC 1 (1986).

Probably not. The IRS held that family hostility cannot be used to ignore the family attribution rules in Rev. Rul. 80-26, 1980-1 C.B. 66. In Robin Haft Trust v. Comm., 510 F.2d 43 (CA-1 1975), the 1st Circuit reversed the Tax Court (62 T.C. 145 (1974)) and held that family hostility might “negate the presumption” of the family attribution rules. The 5th Circuit (Metzger Trust v. Comm., 693 F.2d 459 (CA-5 1982)) and the Tax Court (Cerone v. Comm., 87 TC 1 (1986)) have held that family hostility should not affect the application of the attribution rules. In Metzger, the 5th Circuit explained its decision as follows:

The courts of appeal have been given the authority to review Tax Court decisions at least in part because it was thought that a generalist’s perspective would be helpful; that we are less likely to succumb to the arcane. Yet the avoidance of the arcane must include recognition of the limits of tax law. It is not a task measured by the chancellor’s foot. As understandable as it may be, yielding to the temptation to “do equity” in a specific tax case by looking past plain language to judicially perceived purpose will not do. We do not.

The Tax Court noted in Cerone that family hostility might have a limited role in testing for dividend equivalence under §302(b)(1).

7-21© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

55. [LO5] Boots, Inc. is owned equally by Frank Albert and his daughter Nancy, each of whom held 1,000 shares in the company. Frank wants to retire from the company, and it was decided that the company will redeem all 1,000 of his shares for $25,000 per share on December 31 of this year. Frank’s income tax basis in each share is $500. Boots, Inc. has current E&P of $1,000,000 and accumulated E&P of $5,000,000.

a. What must Frank do to ensure that the redemption will be treated as an exchange?

Frank must file a triple i agreement with the IRS, in which he agrees he will not acquire a prohibited interest in the next 10 years. By filing such an agreement, Frank can waive the family attribution rules and be treated as having a complete termination of his interest in Boots, Inc.

b. If Frank remained as the Chairman of the Board after the redemption, what is the amount and character (capital gain or dividend) of income that Frank will recognize this year?

Frank will have retained a prohibited interest in the company, which will cause the family attribution rules to apply to the distribution. Frank will be deemed to own 100% of the company before and after the distribution. As a result, the distribution will be treated as a property distribution under section 301. Frank’s distribution totals $25,000,000 ($25,000 x 1,000 shares). The distribution will be a dividend to the extent of the company’s E&P of $6,000,000. The remaining $19,000,000 will be a tax-free return of capital to the extent of Frank’s basis in his shares of stock ($500,000) and a capital gain for the remaining amount ($18,500,000).

c. If Frank treats the redemption as a dividend, what happens to his stock basis in the 1,000 shares redeemed?

Frank will have a basis of $0 in his stock after the transaction. His unused basis otherwise would transfer to Nancy, the person who attributed stock to him that caused him to fail the exchange test.

56. [LO5] {research} In the previous problem, Nancy would like to have Frank stay on as a consultant after all of his shares are redeemed. She would pay him a modest amount of $500 per month. Nancy wants to know if there is any de minimis rule such that Frank would not be treated as having retained a prohibited interest in the company because he is receiving such a small amount of money. Consult Lynch v. Comm., 801 F.2d 1176 (CA-9 1986), reversing 83 T.C. 597 (1984), Seda, 82 T.C. 484 (1984), and Cerone, 87 T.C. 1 (1986).

7-22© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

The courts generally have held that there is no de minimis rule in determining if a shareholder has acquired a prohibited interest in a corporation for purposes of waiving the family attribution rules in a complete termination of the shareholder’s stock interest in a corporation. In Lynch, 83 T.C. 597 (1984), the Tax Court held that a salary of $500 per month was not substantial enough to treat the family member as having a prohibited interest. The 9th Circuit reversed the Tax Court’s decision in Lynch, 801 F.2d 1176 (CA-9 1986), and held that the Tax Court had no authority to read into the legislative history of §302(c) a de minimis rule. In Seda, 82 T.C. 484 (1984), the Tax Court held that a monthly salary of $1,000 was substantial enough to treat the family member as having a prohibited interest. In Cerone, 87 T.C. 1 (1986), the Tax Court ruled that a salary of $14,400 per year was substantial enough to treat the family member as having a prohibited interest (it was in excess of the $12,000 received by the taxpayer in Seda).

57. [LO5] {planning} Limited Brands recently repurchased 68,965,000 of its shares, paying $29 per share. The total number of shares outstanding before the redemption was 473,223,066. The total number of shares outstanding after the redemption was 404,258,066. Assume your client owned 20,000 shares of stock in The Limited. What is the minimum number of shares she must tender to receive exchange treatment under the “substantially disproportionate with respect to the shareholder” change-in-ownership rules?

Before the redemption, your client owned 0.0042263% of the stock (20,000 / 473,223,066). To meet the “substantially disproportionate with respect to the shareholder” change-in-ownership rules, your client must reduce her stock ownership below .0033811% (80%). The algebraic equation to solve for the number of shares to be redeemed is (20,000 – X) / 404,258,066 < .000033811. Solving for X, the number of shares to have redeemed equals 6,332 shares. After the redemption, your client will own 13,668 shares. Her percentage ownership will now be .0033810%, which is below the 80% threshold. With an ownership percentage this small, it is likely that any redemption that reduces the shareholder’s percentage stock ownership will be treated as an exchange under the “not essentially equal to a dividend” test.

58. [LO5] Cougar Company is owned equally by Cat Stevens and a partnership that is owned equally by his father and two unrelated individuals. Cat and the partnership each own 3,000 shares in the company. Cat wants to reduce his ownership in the company, and it is decided that the company will redeem 1,500 of his shares for $25,000 per share. Cat’s income tax basis in each share is $5,000. What are the income tax consequences to Cat as a result of the stock redemption, assuming the company has earnings and profits of $10 million?

7-23© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Cat owns directly 3,000 shares in Cougar Company and owns 1,000 shares indirectly through his father’s ownership in the partnership (1/3 x 3,000). Prior to the redemption, Cat owns 4,000 / 6,000 shares = 66.67%. After the redemption of 1,500 shares, Cat owns 2,500 / 4,500 shares = 55.55%. Because Cat’s stock ownership remains above 50%, he will be treated as having received a dividend to the extent of the corporation’s E&P ($10,000,000). Of the remaining distribution of $27,500,000, $15,000,000 will be treated as a tax-free return of capital (1,500 x $10,000 – the basis in the redeemed stock is allocated to the remaining shares) and $12,500,000 will be treated as gain from sale of stock (capital gain).

59. [LO5] {planning} Oriole Corporation, a privately-held company, has one class of voting common stock, of which 1,000 shares are issued and outstanding. The shares are owned as follows:

Larry Byrd 400Paul Byrd (Larry’s son) 200Lady Byrd (Larry’s daughter) 200Cal Rifkin (unrelated) 200 Total 1,000

Larry is considering retirement and would like to have the corporation redeem all of his shares for $400,000.

a. What must Larry do or consider if he wants to guarantee that the redemption will be treated as an exchange?

Because this is a complete termination of his direct ownership interest in Oriole Corporation, Larry can elect to waive the family attribution rules provided he does not acquire a prohibited interest in Oriole over the next ten years. Larry must file a “triple i agreement” with the IRS to waive the election and agree to alert the IRS if he acquires a prohibited interest within the next 10 years.

b. Could Larry still act as a consultant to the company and still have the redemption treated as an exchange?

No. A consultant is considered a prohibited interest in Oriole Corporation.

7-24© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

60. [LO5] {research} Using the facts from Problem 60, Oriole Corporation proposes to pay Larry $100,000 and give him an installment note that will pay him $30,000 per year for the next 10 years plus a market rate of interest. Will this arrangement allow Larry to treat the redemption as an exchange? Consult §453(k)(2)(A).

Yes. §453(k)(2)(A) allows a corporation to issue an installment note to a shareholder in a redemption if the corporation is privately-held. The installment note would not be considered a prohibited interest (being a creditor of the company is allowed).

61. [LO5] EG Corporation redeemed 200 shares of stock from one of its shareholders in exchange for $200,000. The redemption represented 20% of the corporation’s outstanding stock. The redemption was treated as an exchange by the shareholder. By what amount does EG reduce its total E&P as a result of the redemption under the following E&P assumptions?

a. EG’s total E&P at the time of the distribution was $2,000,000.

In a redemption treated as an exchange, EG reduces its E&P by the lesser of the amount distributed ($200,000) or the percentage of stock redeemed times E&P at the time of the distribution (20% x $2,000,000 = $400,000). In this case, EG reduces its E&P by $200,000.

b. EG’s total E&P at the time of the distribution was $500,000.

In a redemption treated as an exchange, EG reduces its E&P by the lesser of the amount distributed ($200,000) or the percentage of stock redeemed times E&P at the time of the distribution (20% x $500,000 = $100,000). In this case, EG reduces its E&P by $100,000.

62. [LO5] {research} Spartan Corporation redeemed 25% of its shares for $2,000 on July 1 of this year, in a transaction that qualified as an exchange under §302(a). Spartan’s accumulated E&P at the beginning of the year was $2,000. Its current E&P is $12,000. Spartan made dividend distributions of $1,000 on June 1 and $4,000 on August 31. Determine the beginning balance in Spartan’s accumulated E&P at the beginning of the next year. See Rev. Rul. 74-338, 1974-2 C.B. 101 and Rev. Rul. 74-339, 1974-2 C.B. 103 for help in making this calculation.

7-25© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Spartan first reduces its current E&P for dividend distributions made during the year. Current E&P is $7,000 ($12,000 - $1,000 - $4,000) for purposes of computing the effect of the redemption on accumulated E&P. Accumulated E&P on July 1, 2013, is $5,500 ($2,000 + ($7,000 x 6/12)). Spartan reduces accumulated E&P as a result of the redemption by the lesser of the distribution ($2,000) or (25% x $5,500 = $1,375). Accumulated E&P at January 1, 2014, is $7,625 ($2,000 + $12,000 - $1,000 - $4,000 - $1,375).

63. [LO5] Bonnie and Clyde are the only two shareholders in Getaway Corporation. Bonnie owns 60 shares with a basis of $3,000, and Clyde owns the remaining 40 shares with a basis of $12,000. At year end, Getaway is considering different alternatives for redeeming some shares of stock. Evaluate whether each of these stock redemption transactions qualify for sale or exchange treatment.

a. Getaway redeems 10 of Bonnie’s shares for $2,000. Getaway has $20,000 of E&P at year end and Bonnie is unrelated to Clyde.

Bonnie owns 60% before the redemption and 56% after the redemption (50/90). Thus, the redemption will fail the 50% test in § 302(b)(2). Because Bonnie still has control of the corporation after the redemption (more than 50%) the redemption will likely fail the not essentially equivalent to a dividend test under §302(b)(1).

b. Getaway redeems 25 of Bonnie’s shares for $4,000. Getaway has $20,000 of E&P at year end and Bonnie is unrelated to Clyde.

Bonnie owns 60% before the redemption and 46% after the redemption (35/75). In addition, Bonnie’s share of the outstanding stock after the redemption has dropped by more than 80% (80% x 60%= 48%) of her percentage ownership before the redemption (60% before and 46% afterwards). Thus, the redemption passes both the 50% test and the 80% test in § 302(b)(2). This means that Bonnie will treat her redeemed shares as though she sold them for $4,000 resulting in a capital gain of $2,750 ($4,000 – [(25/60) × $3,000).

c. Getaway redeems 10 of Clyde’s shares for $2,500. Getaway has $20,000 of E&P at year end and Clyde is unrelated to Bonnie.

Clyde owns 40% before the redemption and 33% after the redemption (30/90). However, Clyde’s share of the outstanding stock has not dropped by more than 80%(80% x 40%= 32%) since his ownership percentage would have to be below 32%, and his ownership percentage is 33%. Thus, the redemption passes the 50%

7-26© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

test but fails the 80% test in § 302(b)(2). This redemption might still qualify as a redemption not essentially equivalent to a dividend under § 302(b)(1). Clyde does not have control of the corporation (Bonnie does), and he has suffered a significant reduction in his ownership.

64. [LO6] Spartan Corporation made a distribution of $500,000 to Rusty Cedar in partial liquidation of the company on December 31 of this year. Rusty, an individual, owns 100% of Spartan Corporation. The distribution was in exchange for 50% of Rusty’s stock in the company. At the time of the distribution, the shares had a fair market value of $200 per share. Rusty’s income tax basis in the shares was $50 per share. Spartan had total E&P of $8,000,000 at the time of the distribution.

a. What is the amount and character (capital gain or dividend) of any income or gain recognized per share by Rusty as a result of the partial liquidation?

An individual receives exchange treatment on distributions in partial liquidation of stock. As a result, Rusty reports capital gain of $150 per share of stock exchanged ($200 - $50).

b. Assuming Spartan made no other distributions to Rusty during the year, by what amount does Spartan reduce its total E&P as a result of the partial liquidation?

Because the liquidation is treated as an exchange, Spartan reduces its E&P by the lesser of the amount distributed ($500,000) or (50% x $8,000,000 = $4,000,000). In this case, Spartan reduces its E&P by $500,000.

65. [LO6] Wolverine Corporation made a distribution of $500,000 to Rich Rod, Inc. in partial liquidation of the company on December 31 of this year. Rich Rod, Inc. owns 100% of Wolverine Corporation. The distribution was in exchange for 50% of Rich Rod, Inc.’s stock in the company. At the time of the distribution, the shares had a fair market value of $200 per share. Rich Rod, Inc.’s income tax basis in the shares was $50 per share. Wolverine had total E&P of $8,000,000 at the time of the distribution.

a. What is the total amount and character (capital gain or dividend) of any income or gain recognized by Rich Rod, Inc. as a result of the partial liquidation?

A corporation receives dividend treatment on distributions in partial liquidation of stock. As a result, Rich Rod, Inc. reports a dividend of $500,000, which is eligible for a 100% dividends received deduction.

b. Assuming Wolverine made no other distributions to Rich Rod, Inc. during the year, by what amount does Wolverine reduce its total E&P as a result of the partial liquidation?

$500,000, the amount treated by Rich Rod, Inc. as a dividend.

7-27© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Comprehensive problems

67. Petoskey Stone Quarry, Inc. (PSQ), a calendar year, accrual basis C Corporation, provides landscaping supplies to local builders in northern Michigan. PSQ has always been a family owned business and has a single class of voting common stock outstanding. The 500 outstanding shares are owned as follows:

Number of sharesNick Adams 150Amy Adams (Nick’s wife) 150Abigail Adams (Nick’s daughter) 50Charlie Adams (Nick’s son) 50Sandler Adams (Nick’s father) 100 Total shares 500

7-28© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Nick Adams serves as President of PSQ, and his father Sandler serves as Chairman of the Board. Amy is the company’s CFO, and Abigail and Charlie work as employees of the company. Sandler would like to retire and sell his shares back to the company. The fair market value of the shares is $500,000. Sandler’s tax basis is $10,000.

The redemption is tentatively scheduled to take place on December 31 of this year. At the beginning of the year PSQ had accumulated earnings and profits of $2,500,000. The company projects current E&P of $200,000. The company intends to pay pro rata cash dividends of $300 per share to its shareholders on December 1 of this year.

a. Assume the redemption takes place as planned on December 31 and no elections are made by the shareholders.

1. What amount of dividend or capital gain will Sandler recognize as a result of the stock redemption?

Sandler will have a dividend of $500,000. Under the family attribution rules, Sandler is deemed to own the shares of stock of his son Nick (150) and his grandchildren Abigail (50) and Charlie (50). He is not deemed to own any of Amy’s stock. Prior to the redemption, Sandler owns 350 / 500 shares = 70%. After the redemption, assuming he does not waive the family attribution rules, Sandler is deemed to own 250 / 400 = 62.5% of the company’s stock. The company has ample E&P to absorb the distribution to Sandler on December 31 and the distribution of $150,000 (500 x $300) on December 1.

2. How will the tax basis of Sandler's stock be allocated to the remaining shareholders?

Sandler’s unused tax basis in his stock of $10,000 will be allocated to Nick, Abigail, and Charlie on a pro rata basis because they caused him to fail the exchange test.

b. What must Sandler and the other shareholders do to change the tax results you calculated in question a?

Sandler must file a triple i agreement with the IRS to waive the family attribution rules. He will then have a capital gain of $490,000 ($500,000 - $10,000) because he will be treated as having a complete termination of his interest in PSQ.

c. Compute PSQ’s accumulated earnings and profits on January 1 of next year assuming the redemption is treated as an exchange.

7-29© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Current E&P $200,000Subtract: Cash dividends on December 1 (150,000)Current E&P on December 31 after dividends 50,000Accumulated E&P, beginning of this year 2,500,000Accumulated E&P at December 31 $2,550,000Subtract: Lesser of cash distributed = $500,000 ( 500,000) or 20% x $2,550,000 = $510,000Accumulated E&P at January 1 of next year $2,050,000

68. [comprehensive] Thriller Corporation has one class of voting common stock, of which 1,000 shares are issued and outstanding. The shares are owned as follows:

Joe Jackson 400Mike Jackson (Joe’s son) 200Jane Jackson (Joe’s daughter) 200Vinnie Price (unrelated) 200 Total 1,000

Thriller Corporation has current E&P of $300,000 for this year and accumulated E&P at January 1 of this year of $500,000.

During this year, the corporation made the following distributions to its shareholders:

03/31: Paid a “dividend” of $10/share to each shareholder ($10,000 in total).

06/30: Redeemed 200 shares of Joe’s stock for $200,000. Joe’s basis in the 200 shares redeemed was $100,000.

09/30: Redeemed 60 shares of Vinnie’s stock for $60,000. His basis in the 60 shares was $36,000.

12/31: Paid a dividend of $10/share to each shareholder ($7,400 in total).

a. Determine the tax status of each distribution made this year. (Hint: First, consider if the redemptions are treated as dividend distributions or exchanges.)

The $10,000 distribution on March 31 is a dividend because CE&P of $300,000 exceeds total dividends distributed during the year. The $7,400 distribution on December 31 is a dividend because CE&P of $300,000 exceeds total dividends distributed during the year.

7-30© 2014 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Chapter 07 - Corporate Taxation: Nonliquidating Distributions

Joe is deemed to own 800 of the 1,000 (80%) shares of Thriller Corporation (400 directly and 200 each from Mike and Jane) before the redemption. After the redemption Joe is deemed to own 600 of the 800 (75%) remaining shares of Thriller Corporation (200 directly and 200 each from Mike and Jane). Joe fails the stock ownership tests because he still owns more than 50% of the stock. Therefore, the entire $200,000 received by Joe is treated as a dividend.

Vinnie owns 200 of the remaining 800 (25%) shares of Thriller Corporation stock before the redemption. After the redemption, Vinnie owns 140 of the 740 (18.9%) remaining shares of Thriller Corporation stock. Vinnie meets both the 50% and 80% tests of §302(b)(2) (18.9% is less than 50% and is less than {80% 25%} = 20%). Vinnie treats the redemption as an exchange and reports a capital gain of $24,000 ($60,000 - $36,000).

b. Compute the corporation’s accumulated E&P at January 1 of next year.

Thriller Corporation first reduces its CE&P for the dividends paid during the current year:

Current E&P $300,000- Dividends paid (217,400) Undistributed Current E&P $ 82,600x 9/12 0.75 Undistributed Current E&P at 9/30 $61,950 Current E&P in 4th quarter + 20,650 Accumulated E&P at 1/01 + 500,000 Total Accumulated E&P at 9/30 $582,600

Reduce Accumulated E&P by the lesser of: $60,000, or 60/800 x $582,600 = $43,695 ( 43,695) Accumulated E&P at 01/01 of next year $538,905

c. Joe is considering retirement and would like to have the corporation redeem all of his shares for $100,000 plus a 10-year note with a fair market value of $300,000.

1. What must Joe do or consider if he wants to ensure that the redemption will be treated as an exchange.