tax penalty mechanism & dispute resolution

TRANSCRIPT

TAX PENALTY MECHANISM & DISPUTE

RESOLUTION

ABU TARIQ JAMALUDDIN

INLAND REVENUE BOARD OF MALAYSIA

TAX PENALTY MECHANISM

UNDER THE INCOME TAX ACT 1967 (ITA)

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

PENALTY UNDER ITA 1967

Sect

ion

11

4(1

)

Sect

ion

11

3(2

)

Sect

ion

11

2(3

)

Sect

ion

11

3(1

) Where no prosecution were make, the Director General may require a taxpayer to pay a penalty of up to three time the amount of tax (for the offences under S77(1), S77A & S77(3) ) - (for failure to furnish a tax return under S77(1) & S77A, or failure to give notice of chargebility under S77(3) )

Liable to a fine between RM1,000 to RM10,000 together with a special penalty of up to 200% of the amount of tax which has been understated (for incorrect return by omitting or understating, or incorrect information on the chargebility)

Where no prosecution were make, the Director General may require a taxpayer to pay a penalty equal to the amount of tax which has been understated (for incorrect return by omitting or understating, or incorrect information on the chargebility)

Liable to a fine between RM1,000 to RM20,000 or imprisonment of up to 3 years or both; together with a special penalty of up to 300% of the amount undercharged (for wilful evasion, such as omission from a return; false statement in a return; false reply whether orally or in writing; and false books of account or false records)

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

IMPOSITION OF TAX PENALTY

PENALTY

FRAUD

WILFUL EVASION

NEGLIGENCE SELF ASSESSMENT

AUDIT/ INVESTIGATION

such as omission from a return; false statement in a return; false reply whether orally or in writing; and false books of account or false records

for incorrect return by omitting or understating, or incorrect information on the chargebility, for failure to furnish a tax return

Evade tax to obtain financial benefit by furnishing false and fictitious claim

The finding was from audit/ investigation

Self-assessment regime – for Company since 2001 and for the individual since 2004. As deterrence for fraud, wilful default or negligence

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

TAX PENALTY UNDER THE FRAMEWORK

Tax Audit Framework

Tax

Investigation Framework

• The main objective of tax audit is

to encourage voluntary compliance with the tax laws and regulations and to ensure that a higher tax compliance rate is achieved under the Self Assessment System.

• to ensure that the correct amount

of income has been reported and the right amount of tax has been paid in accordance with the tax laws and regulations.

The main objectives of tax investigation are to:

• Deter tax evasion; • Identify and prosecute tax

evaders; • Enhance voluntary tax

compliance; • To be fair to compliant

taxpayers; and • Collect the correct amount

of tax

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

TAX PENALTY RATE - TAX AUDIT FRAMEWORK

DISCOVERY

Under SS113(2) ITA may impose 100%

Understatement is discovered following an

audit finding

DG exercises discretionary power under SS124(3) ITA, may impose penalty 45%

of tax undercharged

CONCESSIONARY

Voluntary disclosure within 6 month from the due date – submission of

return

Taxpayer makes a voluntary disclosure

concessionary penalty rates for voluntary

disclosure other than above

100% penalty will be imposed to those who has been audited for second time and been issued with letter of Managing Deliberate

Tax Defaulter

Not applicable 35%

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

TAX PENALTY RATE - TAX INVESTIGATION FRAMEWORK

Failure to furnish return or give notice

of chargeability Incorrect returns Wilful evasion

• Section 112 ITA

• On conviction

• be liable to a fine of not

less than RM200 and

not more than RM2,000

or

• to imprisonment for a

term not exceeding six

months or to both

• Section 113 ITA

• on conviction

• fine of not less than

RM1,000 and not more

than RM10,000 and

• shall pay a special

penalty of double

(200%) the amount of

tax which has been

undercharged

• Section 114 ITA

• on conviction

• fine of not less than

RM1,000 and not more

than RM20,000 or

• to imprisonment for a

term not exceeding

three years or to both

and

• shall pay a special

penalty of treble

(300%) the amount of

tax which has been

undercharged

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

PENALTY UNDER SS 113(2) ITA

Whether the penalty imposed

by the DGIR is correct

The Law

Section 113(2) ITA

“Where a person…

makes an incorrect return

gives any incorrect information

DG may require that person to pay penalty equal to the amount of tax charge

The dispute

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

PENALTY UNDER SS 113(2) ITA

Tax payer’s perspective –

If the incorrect return or information was done in good faith the penalty should not be imposed by DGIR.

Revenue’s perspective –

Once proven thru audit finding that the tax payer has given an incorrect return or

information, the DGIR has the discretion to impose penalty. DGIR has no burden to prove that tax payer has acted in bad faith.

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

PENALTY UNDER SS 113(2) ITA

Penalty = Assessment [SS125(2) ITA]

The burden of proof that an assessment is made is excessive or erroneous shall be on the taxpayer

[Paragraph 13, Schedule 5 ITA]

DGIR is given a discretion – DGIR has to ensure that it has not been exercised at whim and fancy [KT Co. v Ketua Pengarah Jabatan Hasil Dalam Negeri (1992) 1 MSTC 3255]

BURDEN OF PROOF

ASSESSMENT

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

CASES ON PENALTY UNDER SS113(2) ITA

For the Revenue

• Syarikat Ibraco Peremba Sdn Bhd v KPHDN [W01-177-04/2013]

• Syarikat Pukin Ladang Kelapa Sawit v KPHDN (2012) 6 MLJ 411

• Dr. Zanariah bt Ramli v KPHDN [R1-14-1-2011]

• Sri Binaraya Sdn Bhd v KPHDN [W-01-448-10/2012]

• Shaklee Product Sdn Bhd v KPHDN [W-01-45-10]

• Datuk Yap Pak Leong v KPHDN (2014) 10 MLJ 255

For the Taxpayer

• Office Park Development Sdn Bhd v KPHDN (2011) 9 MLJ 479

• Success Electronics & Transformer Manufacturer v KPHDN [R1–14–14 of 2009]

• Piramid Intan Sdn Bhd v KPHDN

• KPHDN v Firgos (Malaysia) Sdn Bhd

• Pasdec Corporation Sdn Bhd v KPHDN

• KPHDN v Shell Refining Co (FOM) Berhad

• Kyros International Sdn Bhd v KPHDN

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

DECIDED CASES ON PENALTY UNDER

SS113(2) ITA

FOR THE REVENUE

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Syarikat Ibraco Peremba Sdn Bhd v KPHDN [W-01-177-04/2013]

Court of Appeal affirms the High Court Judge’s decision affirming the SCIT’s decision that section 140(1)(a) of the Act applied to the Appellant

It is without doubt that section 113(2) of the Act gives a discretion to the Respondent to impose a

penalty on a person who has failed to observe the requirements of the law as provided in paragraph

2(a) or (b) of section 113. Hence the use of the phrase “the Director General may require that

person to pay a penalty”. There is a clear distinction between subsection113(1) and subsection 113(2).

Subsection 113(1) provides for an offence being committed in the circumstance provided for in paragraph (a) or (b) unless that person “satisfies the court that the incorrect

return or incorrect information was made or given in food faith”. Whereas subsection 113(2) provides for a situation

where there is no prosecution under subsection 113(1) has been instituted in the circumstances provided for in paragraph 113(2)(a) or (b), the Director General may

require that person to pay a penalty. That being the case, the defence of “good faith”as found in subsection 113(1),

and not found in subsection 113(2), does not apply to the Director General’s discretion under subsection 113(2).

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Syarikat Pukin Ladang Kelapa Sawit v KPHDN [W – 01 – 712 – 12 /2011]

S 33(1)(b) of the ITA 1967 recognize rental payable not as provided under the lease agreement but it must be based on calculation of rental ought to have

been incurred in the basis year based on the principle of expenses wholly and exclusively incurred for the production of gross income in the basis year,

thus in coming to its decision that only annual rental is to be recognized under s 33(1)(b) of the SCIT is therefore right in excluding advanced rental

The SCIT, however, had wrongly made a finding that the advance rental of RM18,000,000 cannot be recognized under s33 on the ground that it is

capital expenses under s39 of the ITA. From the lease agreement it is clear that the amount of RM18,000,000 is not capital expenses but merely

advance rental

The penalty imposed on the appellant was correctly made, no misapplication of law or facts that merits interference by this

court

The High Court’s

decision upheld by Court of Appeal

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

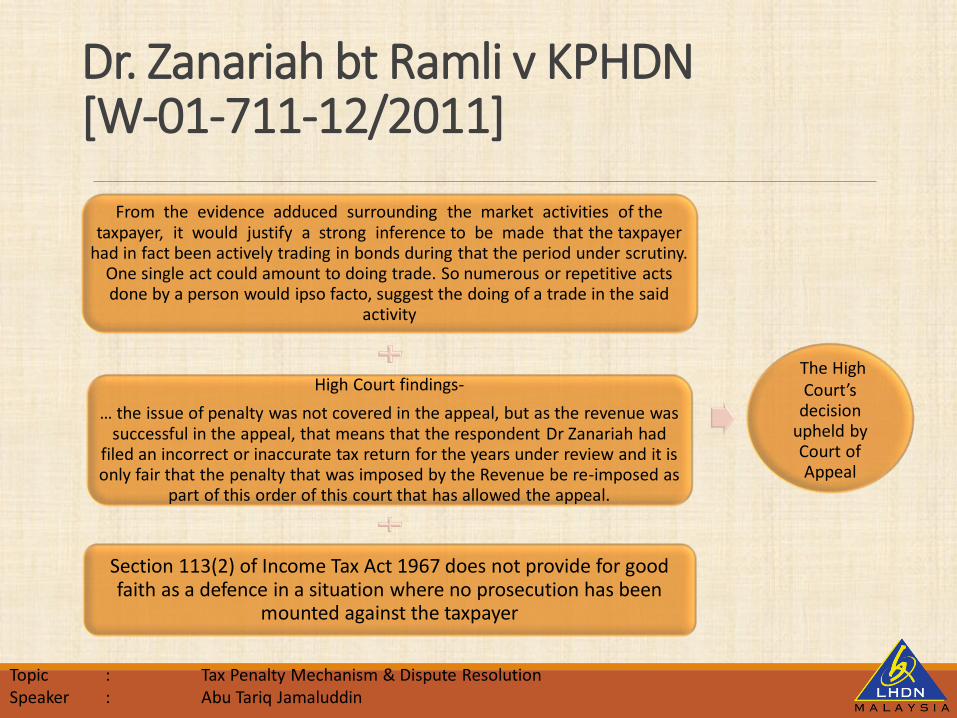

Dr. Zanariah bt Ramli v KPHDN [W-01-711-12/2011]

From the evidence adduced surrounding the market activities of the taxpayer, it would justify a strong inference to be made that the taxpayer

had in fact been actively trading in bonds during that the period under scrutiny. One single act could amount to doing trade. So numerous or repetitive acts done by a person would ipso facto, suggest the doing of a trade in the said

activity

High Court findings-

… the issue of penalty was not covered in the appeal, but as the revenue was successful in the appeal, that means that the respondent Dr Zanariah had

filed an incorrect or inaccurate tax return for the years under review and it is only fair that the penalty that was imposed by the Revenue be re-imposed as

part of this order of this court that has allowed the appeal.

Section 113(2) of Income Tax Act 1967 does not provide for good faith as a defence in a situation where no prosecution has been

mounted against the taxpayer

The High Court’s

decision upheld by Court of Appeal

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

SRI BINARAYA SDN BHD V KPHDN [W-01-448-10/2012]

The Special Commissioners of Income Tax (“SCIT”) findings maintained. The additional assessment raised by the Respondent against the taxpayer was couched upon the wide spirit of section 24 of the Act and there is no issue of

retrospective effect of the Public Ruling 3/2006.

Conditional or sectional certificate of Practical Completion would amount to a Certificate of Practical Completion. The date stated in Certificate of

Practical Completion is the cut-off date for the taxpayer to prepare the final accounts in order to recognize the taxpayer income in the basis year of 2003

Section 113(2) of Income Tax Act 1967 gives a discretion to the Respondent to impose a penalty on a person who has failed to observe the requirements of

the law as provided in paragraph 2(a) or (b) of section 113

The High Court’s decision upheld

by Court of Appeal

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

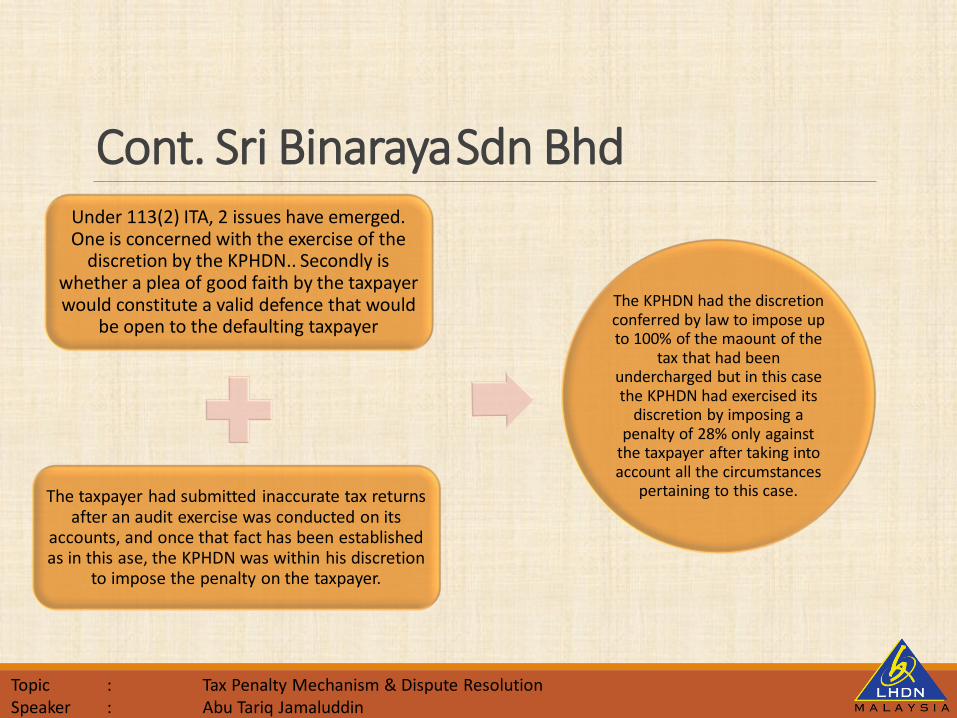

Cont. Sri Binaraya Sdn Bhd Under 113(2) ITA, 2 issues have emerged. One is concerned with the exercise of the

discretion by the KPHDN.. Secondly is whether a plea of good faith by the taxpayer would constitute a valid defence that would

be open to the defaulting taxpayer

The taxpayer had submitted inaccurate tax returns after an audit exercise was conducted on its

accounts, and once that fact has been established as in this ase, the KPHDN was within his discretion

to impose the penalty on the taxpayer.

The KPHDN had the discretion conferred by law to impose up to 100% of the maount of the

tax that had been undercharged but in this case the KPHDN had exercised its

discretion by imposing a penalty of 28% only against

the taxpayer after taking into account all the circumstances

pertaining to this case.

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

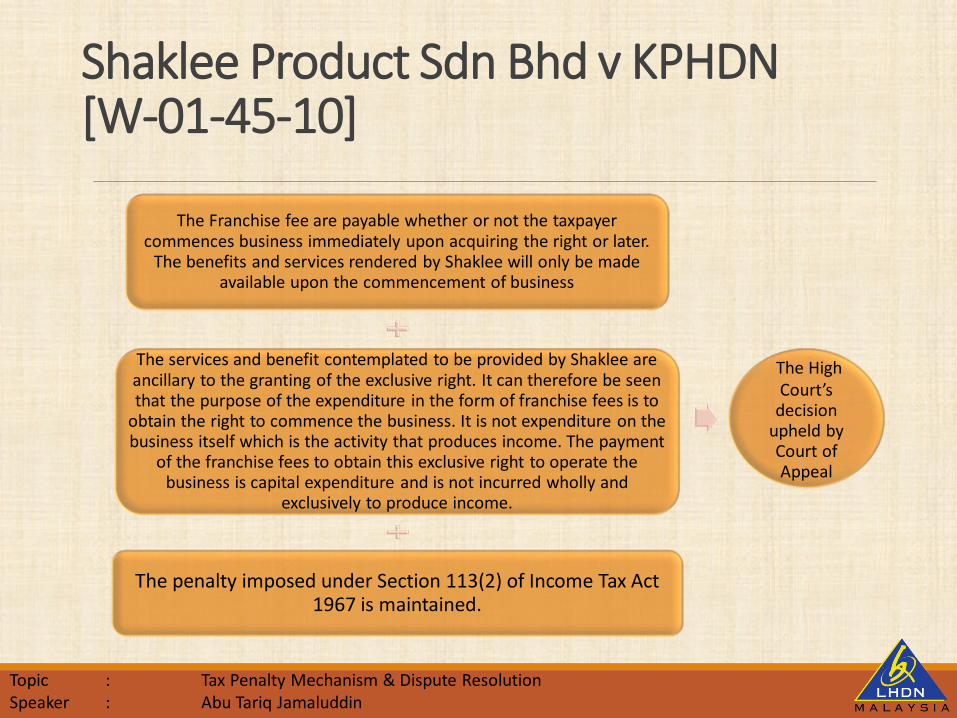

Shaklee Product Sdn Bhd v KPHDN [W-01-45-10]

The Franchise fee are payable whether or not the taxpayer commences business immediately upon acquiring the right or later.

The benefits and services rendered by Shaklee will only be made available upon the commencement of business

The services and benefit contemplated to be provided by Shaklee are ancillary to the granting of the exclusive right. It can therefore be seen that the purpose of the expenditure in the form of franchise fees is to

obtain the right to commence the business. It is not expenditure on the business itself which is the activity that produces income. The payment

of the franchise fees to obtain this exclusive right to operate the business is capital expenditure and is not incurred wholly and

exclusively to produce income.

The penalty imposed under Section 113(2) of Income Tax Act 1967 is maintained.

The High Court’s

decision upheld by Court of Appeal

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Datuk Yap Pak Leong v KPHDN (2014) 10 MLJ 255

The crucial elements in s 33(1) that need to be scrupulously satisfied would necessarily encompass the following: 'outgoings and expenses', 'wholly and

exclusively' and incurred during that period

The grounds for interfering with the decision of the SCIT are limited. In the case of pure findings of fact, the court would not interfere unless it considers that the

only reasonable conclusion on the evidence contradicts the determination of the Special Commissioners

The SCIT is entirely correct in concluding that the respondent has discretion to impose the penalty under s 113(2) and that the defence of good faith is not available - Case of KT Co v Ketua Pengarah Hasil Dalam

Negeri (1996) MSTC 2594

The Decision of SCIT was

upheld by the High Court

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

DECIDED CASES ON PENALTY UNDER

SS113(2) ITA

FOR THE TAXPAYER

Office Park Development Sdn Bhd v KPHDN (2011) 9 MLJ 479

It is not mandatory for the respondent to impose penalty in all tax audits. The respondent has a discretion amplifies the appellant's submission

that a penalty should not be imposed in this case as the appellant had acted in good faith and made full disclosure of information

The special commissioners were correct in their finding that the appellant's incorrect return was made in good faith and that the

penalty imposed by the respondent in respect of the same should be waived. The respondent's contention that s 113(2) of the Act did not

provide the defence of good faith was without basis

The penalty provisions in ss 113(1) and (2) of the Act are to punish taxpayers who deliberately submit incorrect tax returns and

information and it was not the intention of Parliament to punish innocent taxpayers. Further, it was not mandatory for the respondent

to impose a penalty in all tax audits

The Decision of SCIT was

upheld by the High Court

KPHDN v Success Electronics & Transformer Manufacturer [R1–14–14 of 2009]

The High Court had affirmed the SCIT's decision that reinvestment allowance cannot be restricted to 'production area' alone. In this

case, the High Court held that meeting room, office spaces, toilets, staircases, void areas, lift lobby, surau, warehouse, lightning

adjustment and installations of air-conditioning, electrical fitting and partition walls were part of the factory

The functionally of the disputed items in the overall context of the respondent's manufacturing activity ought to be taken as a valid factor

in considering the respondent's reinvestment allowance claim

All the capital expenditures claimed for reinvestment allowance purposes were actually incurred by the respondent. The respondent had made full disclosure in the Form that were submitted and the audit team did not

discover anything contrary to the information disclosed in the Form. The respondent had acted in good faith and made full disclosure

The Decision of SCIT was upheld by the High

Court

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Piramid Intan Sdn Bhd v KPHDN [2015] 10 MLJ 436

The appellant’s upfront payments to STIDC were not wholly and exclusively incurred for the production of gross income for the years of assessment 2003 and 2004. Thus, the appellant failed to justify that the payment or the expenditure incurred by it was

an allowable deduction under s 33(1) of the ITA

The SCIT found as a fact that the appellant did not understate or omit its income but that it was merely a technical adjustment due to a differing interpretation of the tax legislation and as such the penalty under s 113(2) of the ITA should not have been imposed. Surely all documents and

payments made would have been disclosed in the appellant’s annual returns and audited financial statements for 2003 and 2004 and the respondent would have known of the

disclosures.

The differing interpretations of whether the payments were capital or revenue expenditure and whether or not they were deductible certainly could not be viewed as

escaping from paying tax.

The SCIT’s decision that the penalty should not have been imposed was correct in law and it rightly concluded that in exercising its discretion to impose a penalty under s 113(2) of the ITA, the respondent failed to give due consideration to all relevant facts and circumstances of the

case

The Decision of

SCIT was upheld by the High

Court

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

KPHDN v Firgos (Malaysia) Sdn Bhd [2014] 1 MLJ 701

Reinvestment allowance would be available where a taxpayer had incurred capital expenditure on a factory, plant or machinery for the

purposes of a qualifying project. The functionally of the disputed items in the overall context of the respondent's manufacturing activity ought to be taken as a valid factor in considering the respondent's reinvestment

allowance claim

The respondent had made full disclosure in the Form that were submitted in the years of assessment 2005–2007 and the audit team did not discover

anything contrary to the information disclosed in the Form. The respondent had acted in good faith and made full disclosure

S 113(2) of the ITA is not a mandatory provision. This section clearly confers discretion on the appellant as to whether penalty should be imposed or not. What more the matter in dispute arose as a result of technical adjustment ie

due to a differing interpretation of the tax legislation by the respondent

The Decision of SCIT was

upheld by the High Court

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Pasdec Corporation Sdn Bhd v KPHDN [2016] 12 MLJ 555

It is obvious that the additional assessment was made because of the difference of opinion on accounting methods. As there was no law to regulate

the computations of income with respect to property and housing development, and the conduct of the respondent to accept and fully endorsed

the DLP method adopted by the appellant for 26 years, the appellant which has adopted consistently a method of accounting which is a generally well accepted method in the industry could not be accused of committing fraud

and or willful default or negligence. In view of the above the additional taxes imposed for YA 1999 was barred by virtue of s 91

The respondent was wrong in imposing the penalties on the appellant under s 113(2) of the Act. Even assuming that the incorrect returns and/or incorrect

information was submitted, the same was made in good faith where full disclosures were made to the respondent

The Decision of SCIT was

overturned by the High Court

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

KPHDN v Shell Refining Co (FOM) Berhad [2014] 9 MLJ 686

It was clear that the payment to SGSI was made based on the service and advice given by the SCIT and this was the income expenses that was entitled to tax rebate. Payment to the SCIT could be tax-rebated

as it fell under 'all outgoings and expenses wholly and exclusively incurred during that period by that person in the production of gross

income from that source'

The SCIT's findings was based on the contention and evidence of witnesses. The SCIT found the appellant's witness had committed many

mistakes in imposing the penalty and in rejecting dismissal

The Decision of SCIT was

upheld by the High Court

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Kyros International Sdn Bhd v KPHDN [2013] 2 MLJ 650

The High Court judge's finding that the franchise fee was not derived from outside Malaysia was an error of law. It is well-settled that the appellate court generally recognised the special position of the SCIT and that the

burden would lie with the respondent DGIR to satisfy the court that appellate interference was necessary. In fact, the appellate court could only

disturb the finding of fact in limited circumstances. Further, in the Malaysian context the SCIT, which was appointed under s 98 of the Act, was

expected to be specialised in the scope of the adjudication process it was entrusted with under the Act. There was much merit in the appellant's

submission that the facts found by the SCIT could not be assailed by the High Court. On the factual matrix of the instant case the finding of facts of

the SCIT did not warrant appellate interference

On the issue of penalty, the High Court judge was right to sustain the decision of the SCIT – there is no specific treatment of franchise fee under the ITA and no guideline / direction pertaining to the same is

available, therefore the benefit should be given to the taxpayer

The High Court’s decision was upheld by

Court of Appeal on imposition of

penalty

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

DISPUTE RESOLUTION

OVERVIEW OF RESOLUTION DEPARTMENT

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Source of Dispute

Right of Appeal

Procedure of Appeal

Dispute Resolution Process

Legal Status

Benefits

Issues Resolved

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Overview

Sources of Dispute

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Sun Mun Tobacco Co. Ltd. v. Government of Malaysia [1972] 2 MLJ 163

“It is open to a taxpayer to go before them (the Special Commissioners) and prove that he is not liable to assessment. The doors of justice are not shut to him merely because the claimant is the Government, but he has to enter the doors of the Special Commissioners first to raise the plea of non observance of the principle of natural justice or to establish that the Director General acted arbitrarily and in a non judicial manner. It is only after he was availed himself of that remedy as laid down by the law that he has right to come to the Court.” Federal Court

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Right of Appeal – Case Law

Section 97A ITA

Section 111 ITA

Section 99 ITA File Form Q at branches

Dispute Resolution

Department

30 days 30 days

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Right of Appeal / Appeal Provisions

Error or mistake in the return or

statement

Application in writing to the

DGIR (Branches)

Decision by the DGIR (Branches)

Request DGIR to forward to SCIT

(Branches)

Dispute Resolution

Department

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Error Or Mistake – Relief Application

Public Ruling No 3/2012

All appeal must be in the prescribed form, letter of objection is no longer accepted:

Aston Villa Sdn Bhd v. Ketua Pengarah Hasil Dalam Negeri Q2-14-19-

10/2011

Medan Prestasi Sdn Bhd v. Ketua Pengarah Hasil Dalam Negeri R1-

14-18/2011

Taxpayer is required to furnish a complete and correct Form Q

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Prescribed Form – Form Q

APPLICATION FOR EXTENSION OF TIME : FORM N

DGIR’s Decision (whether taxpayer is prevented from giving notice within time)

Allowed the extension

Disallowed the Extension

Forward to SCIT

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Extension of Time – Form N

Form Q

(Branches)

Dispute Resolution Department

Appeal Review Panel (ARP)

Dispute Resolution Proceeding (DRP)

Within 30 days

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Process

• Appeal is on the same issue which is still pending in court;

• Appeal is on the same issue that has been decided by court;

• Appeal is solely on question of law;

• Appeal in respect of public ruling.

Appeal suitable for ARP:

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

When Appeal Review (ARP) is Preferred

Appeal Review Panel

Forward appeal to SCIT

Decision

Proposed for DRP Appeal Allowed

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Process – Cont’d

Appeals involving mainly question of facts- transfer pricing

Further clarification is needed on the issues or facts in dispute

Appeal involving wide range of issues

There is misunderstanding or disagreement over how the facts ought to be weighted in coming into decision

Appeal would be of little or limited precedent value

APPEAL SUITABLE FOR DRP:

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

When Dispute Resolution Proceeding (DRP) is Preferred

Dispute Resolution Proceeding

Hearing

Decision

SCIT Agreement

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Process – Cont’d

Ob

jec

tive

s o

f D

RP

Resolve or limit the issues in dispute

Be accessible

Use resources efficiently

Resolves disputes as early as possible

Produce outcomes that are lawful, effective and acceptable to the parties

Enhance the satisfaction of the parties

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Proceeding - Objective

PARTIES

• Taxpayer/tax agent/ lawyer

• DRP Panel –3 persons headed by a legally qualified officer

PLACE OF PROCEEDING

• Branches all over Malaysia which is convenience to the tax payer

CONDUCT

• Informal

DRESS CODE

• Formal attire

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Proceeding - Procedure

RULE ON EVIDENCE

•Not strictly followed

RULE GOVERNING THE PROCEEDING

•Confidential

•Without prejudice basis

COST

•Parties bear their own cost

TIME FRAME

•Decision will be given within one month after the proceeding

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Proceeding - Procedure

Present the issues and facts

Elaborate on the grounds of appeal

Highlight relevant documents

Submit on the relevant laws or cases

Propose any settlement (if any)

Role of taxpayer

Analyze issues and facts presented

Evaluate strength and weaknesses of the case

Explore any settlement on the issue raised

Role of DRP’s Panel

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Proceeding - Procedure

Panel agreed fully with the appeal by the taxpayer (agreement entered by parties pursuant to section 101 ITA)

Taxpayer agreed to withdraw the appeal

Panel/ taxpayer agreed partly on the issue under appeal. The appeal is to

be forwarded to the SCIT (agreement recorded before the

SCIT)

Panel fully disagree with the appeal. The appeal is to be forwarded to the

SCIT

Possible outcome :

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Dispute Resolution Proceeding - Decision

Requires Taxpayer (TP) to furnish particulars

Requires TP to produce books & documents

Examine any person on oath/otherwise

Summons any person to give evidence

DGIR to Review Appeals (12 months)

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Legal Status – Section 101 ITA

Agreement in writing

Confirmed

Assessment

Increased Reduced Discharged

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Legal Status – Section 101 ITA

Deemed Agreement

Failure to reply to DGIR’s Proposal

Oral Agreement

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Legal Status – Section 101 ITA

Where there is no prospect of coming into agreement the DGIR may

within 12 months from the receipt of the notice of appeal (Form Q)

forwarded the same to the SCIT

Minister may extend the 12 months period not exceeding 6 months;

Failure to forward appeal within the 12 months period, the DGIR is

deemed to have accepted the appeal an the assessment will be

discharged.

Case: KPHDN v. Scania (Malaysia) Sdn Bhd R1-14-4-02/2012

SECTION 102 ITA 1967

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Failure to Forward to SCIT

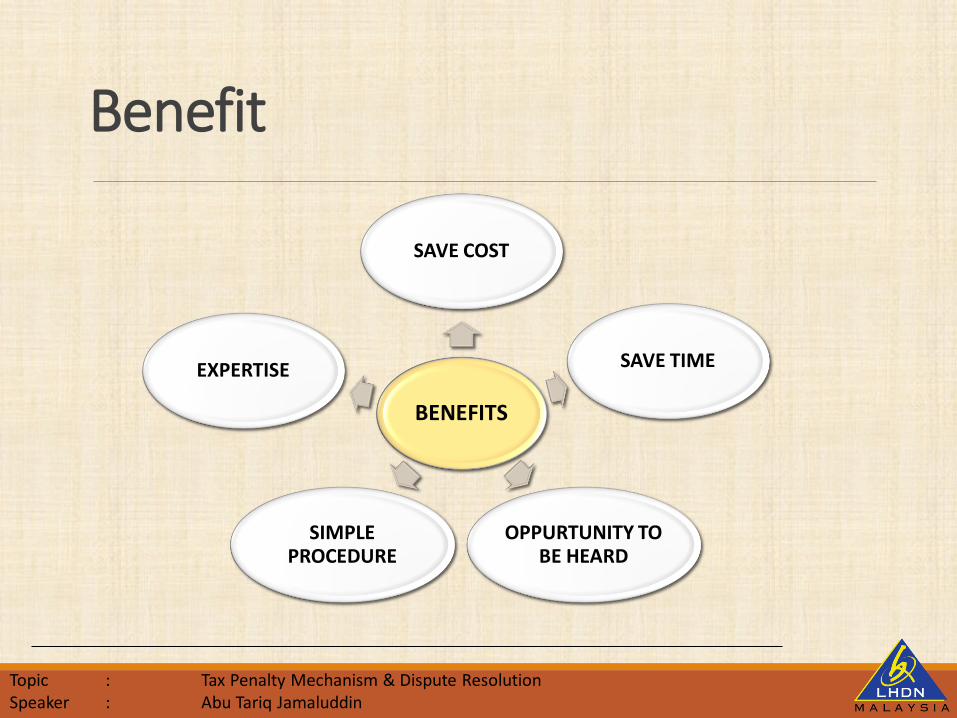

BENEFITS

SAVE COST

SAVE TIME

OPPURTUNITY TO BE HEARD

SIMPLE PROCEDURE

EXPERTISE

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Benefit

Whether profit from disposal of 12 lots of land are

subjected to RPGT or ITA where the consideration for

the disposal is in the nature of shares and 28 units of shop

houses

Whether the taxpayer has complied with all the

conditions to be eligible for OHQ tax incentive.

Whether expenses incurred in respect of insurance payment is deductible under section 33

ITA

Whether penalty is correctly imposed under section 113

ITA

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Issues Resolved

Whether amount of donation received from outside Malaysia is subject to tax under the ITA

Whether income in respect of delivery order fee and bill of lading part of shipping income and exempted under section 54A ITA

Whether research expenditure comprises of cost for producing shoe sampling is deductible under section 33 ITA

Whether a company incorporated outside Malaysia is a tax resident company of Malaysia and thus enjoy 20 per cent special tax rate for the first RM500,000.

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Issues Resolved

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Comparative Study

“……discourage litigation, persuade your neighbors to compromise whenever you can. Point out to them how the normal winners often a loser in fees, expenses, cost and time…. Justice delayed is justice denied

Abraham Lincoln

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

Final Thought

Topic : Tax Penalty Mechanism & Dispute Resolution Speaker : Abu Tariq Jamaluddin

0383138862