tax planning for real estate · pass-thru deduction • deduction equal to 20% of domestic...

TRANSCRIPT

Tax Planning for Real Estate

Robert S. Keebler, CPA/PFS, MST, AEPKeebler & Associates, LLP

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

Pass-thru Deduction

• Deduction equal to 20% of domestic “qualified business income” (QBI) from a pass-

through entity

• Basically, provides an effective top marginal rate of 29.6%

§ 199A, §11011

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

2

Pass-thru Deduction

• For those with taxable income in excess of $415,000 (MFJ) the deduction is limited

to the greater of:

– 50% of W-2 Wages

– 25% of W-2 Wages plus 2.5% of “unadjusted basis”

• Unavailable to Specified Service Business owner’s taxable income in excess of

$415,000 (MFJ)

• Limitations phased-in from $315,000 - $415,000 (MFJ) of taxable income

§ 199A, §11011

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

3

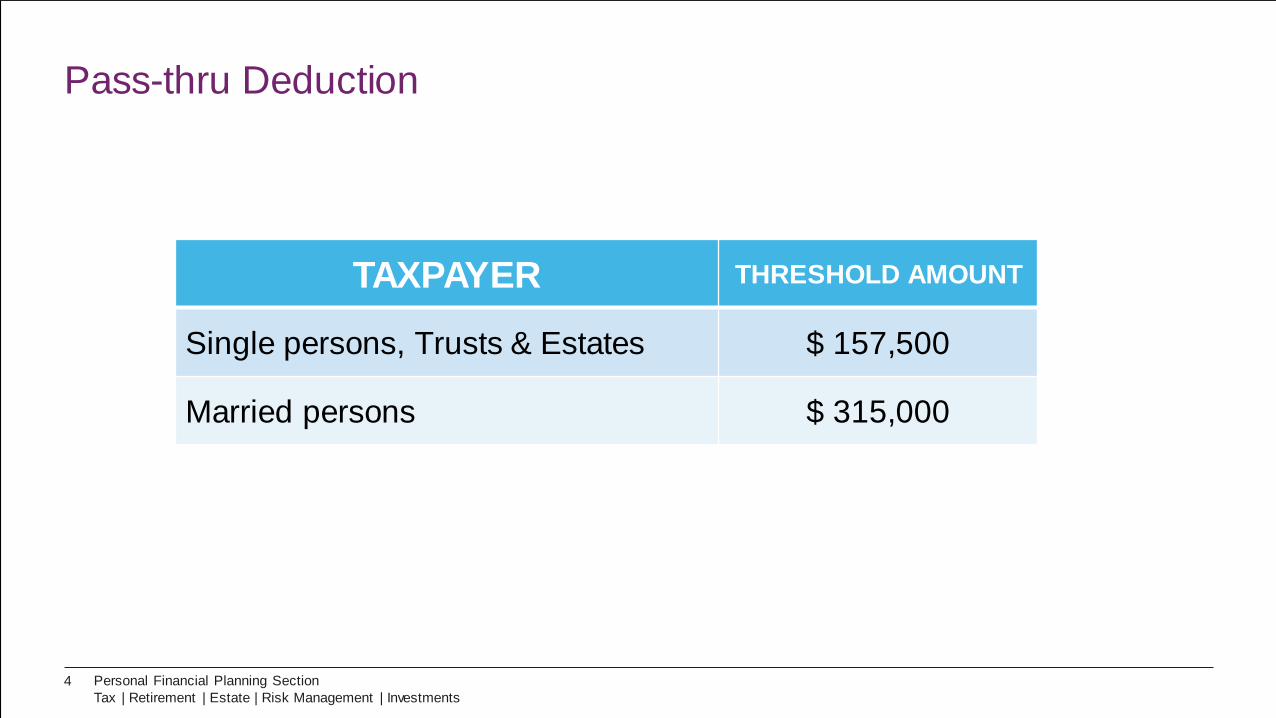

Pass-thru Deduction

TAXPAYER THRESHOLD AMOUNT

Single persons, Trusts & Estates $ 157,500

Married persons $ 315,000

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

4

Is it a Service Business per §§1202(e)(3)(A), 475(c)(2), or 475(e)(2)?

Is taxable income over

the threshold?315/157.5

Is taxable income over the

threshold?315/157.5

Deduction = QBI x 20%

Deduction = QBI x 20%

Over fullPhase – in?415/207.5

Is taxable income over the full phase-in?

415/207.5

Deduction Reduced

Deduction equals

lesser of:

· QBI x 20% or

· The greater of:

- W-2 wages x 50%- W-2 wages x 25% + 2.5% of unadjusted basis

No No

NoNo

No

Yes

Yes Yes

No Deduction

Deduction Reduced

Yes

Yes

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

5

Pass-thru Deduction

• The deduction also cannot exceed the lesser of

– The “Combined QBI Amount,” or

– 20% x (total taxable income – capital gain)

• Combined QBI amount = deduction for each qualified trade or business PLUS 20%

of REIT dividends and PTP income

§ 199A, §11011

20%Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

6

Limitation Formula Definitions

Simplified

• W-2 Wages

– Equal to wage expense [§199A(f)(1)]

– Does not include guaranteed payments or payments to independent contractors

• Qualified Property

– Tangible property being depreciated (e.g. does not include land)

– Depreciation period is the latter of the regular depreciation period or 10-years

• Unadjusted Basis

– Equal to basis immediately after acquisition

– Not adjusted for depreciation

§ 199A, §11011Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

7

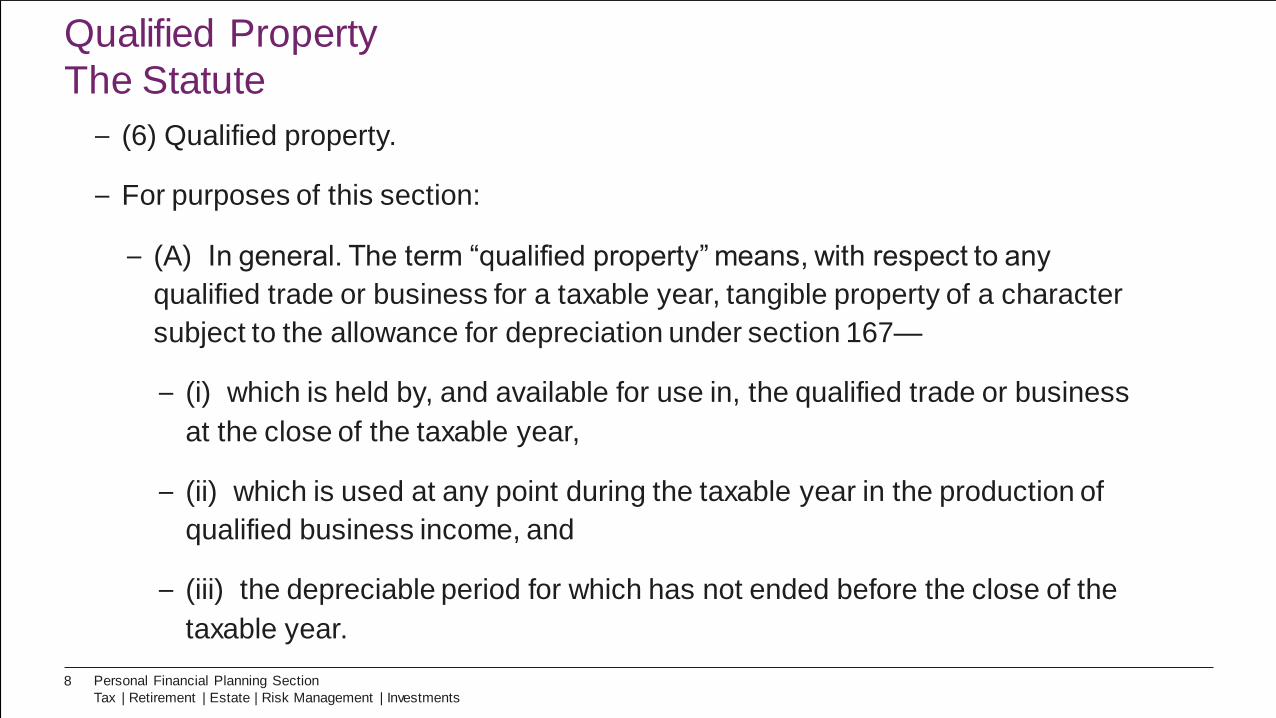

Qualified Property

The Statute

– (6) Qualified property.

– For purposes of this section:

– (A) In general. The term “qualified property” means, with respect to any

qualified trade or business for a taxable year, tangible property of a character

subject to the allowance for depreciation under section 167—

– (i) which is held by, and available for use in, the qualified trade or business

at the close of the taxable year,

– (ii) which is used at any point during the taxable year in the production of

qualified business income, and

– (iii) the depreciable period for which has not ended before the close of the

taxable year.

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

8

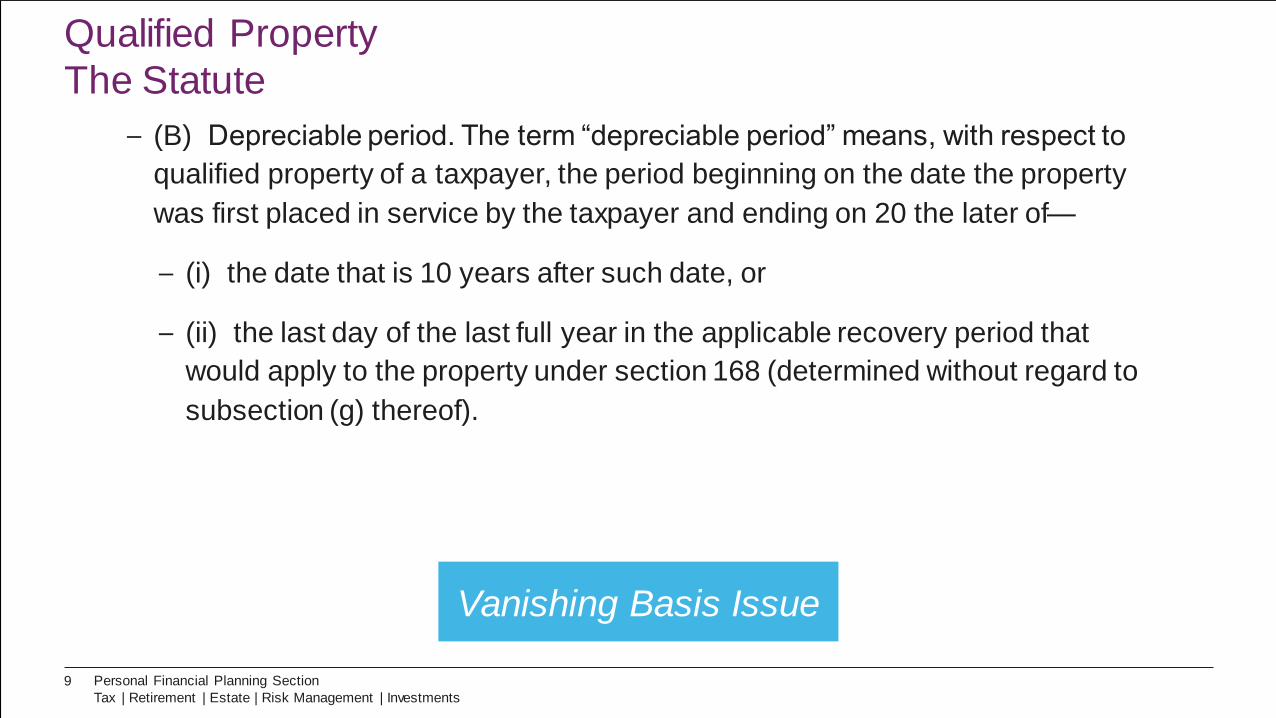

Qualified Property

The Statute

– (B) Depreciable period. The term “depreciable period” means, with respect to

qualified property of a taxpayer, the period beginning on the date the property

was first placed in service by the taxpayer and ending on 20 the later of—

– (i) the date that is 10 years after such date, or

– (ii) the last day of the last full year in the applicable recovery period that

would apply to the property under section 168 (determined without regard to

subsection (g) thereof).

Vanishing Basis Issue

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

9

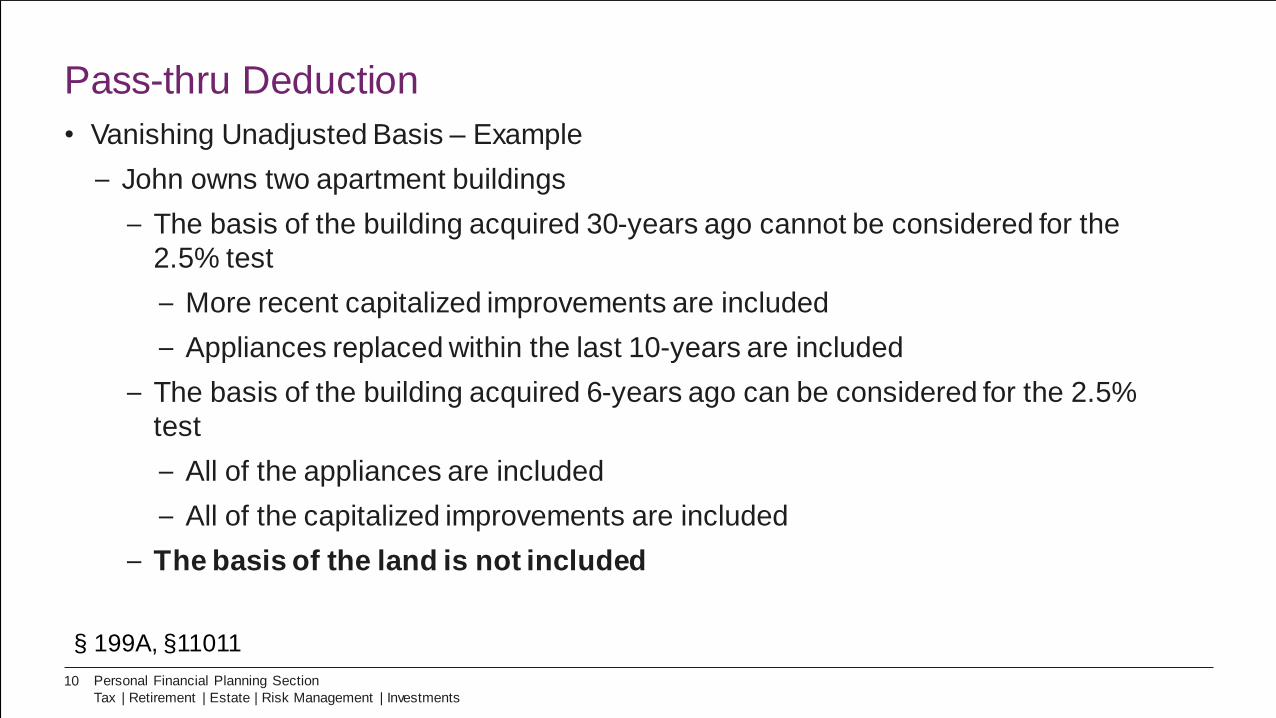

Pass-thru Deduction

• Vanishing Unadjusted Basis – Example

– John owns two apartment buildings

– The basis of the building acquired 30-years ago cannot be considered for the

2.5% test

– More recent capitalized improvements are included

– Appliances replaced within the last 10-years are included

– The basis of the building acquired 6-years ago can be considered for the 2.5%

test

– All of the appliances are included

– All of the capitalized improvements are included

– The basis of the land is not included

§ 199A, §11011

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

10

Partnerships & S-Corps

Allocable Share Simplified

• Partner/shareholder must use their allocable share for all calculations

• Example – 50/50 partners

– Each considers half of QBI, wages, & basis in making all calculations

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

11

Business Interest Deduction

• The bill disallows interest expense in excess of 30% of a business’s “adjusted

taxable income”

– Tested on an entity-by-entity basis

• Businesses with average gross receipts that do no exceed $25,000,000 are exempt

– Tested on an affiliated group basis

• Any interest disallowed is carried forward indefinitely

§ 163(j)(1)-(3), § 13301

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

12

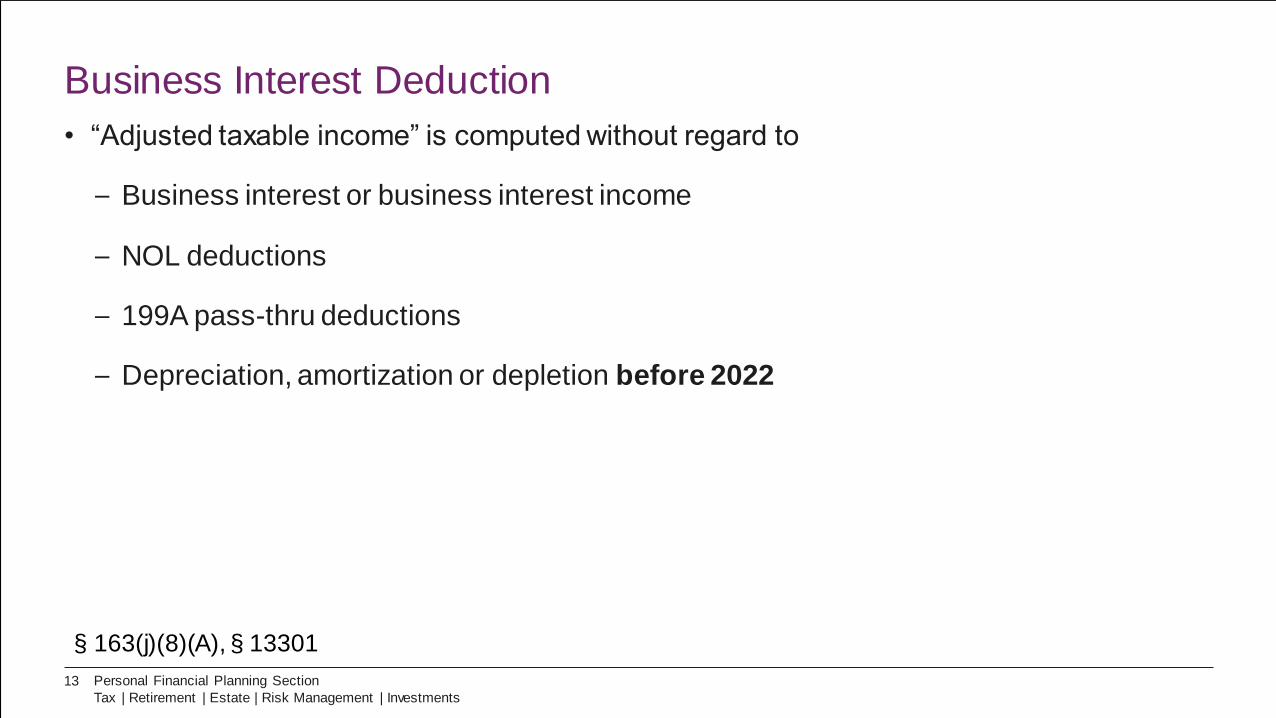

Business Interest Deduction

• “Adjusted taxable income” is computed without regard to

– Business interest or business interest income

– NOL deductions

– 199A pass-thru deductions

– Depreciation, amortization or depletion before 2022

§ 163(j)(8)(A), § 13301

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

13

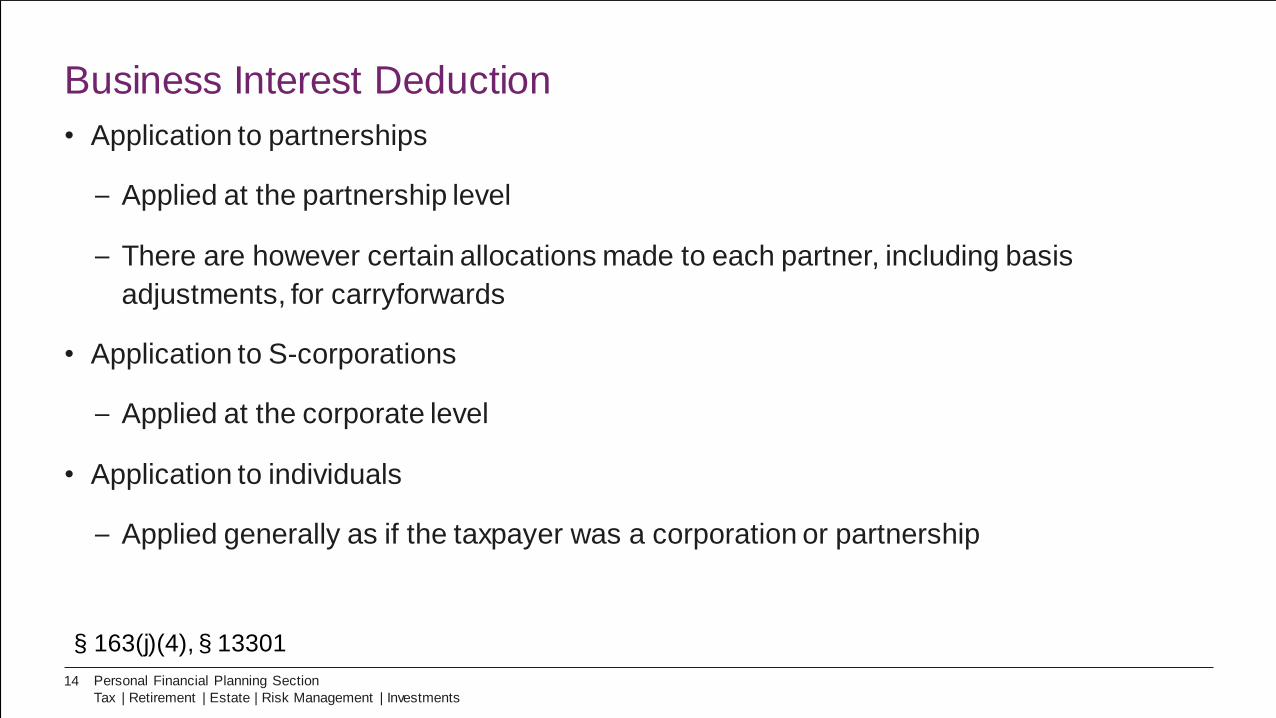

Business Interest Deduction

• Application to partnerships

– Applied at the partnership level

– There are however certain allocations made to each partner, including basis

adjustments, for carryforwards

• Application to S-corporations

– Applied at the corporate level

• Application to individuals

– Applied generally as if the taxpayer was a corporation or partnership

§ 163(j)(4), § 13301

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

14

Business Interest Deduction

• A Real Property Trade or Business or Farming Business can elect for the interest

limitation to not apply

• Real Property Trade or Business is defined in § 469(c)(7)(C)

• Election out is irrevocable

• Election out requires the taxpayer to use ADS

– Longer depreciation periods

– Ineligible for bonus depreciation

§ 163(j)(7), § 13301

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

15

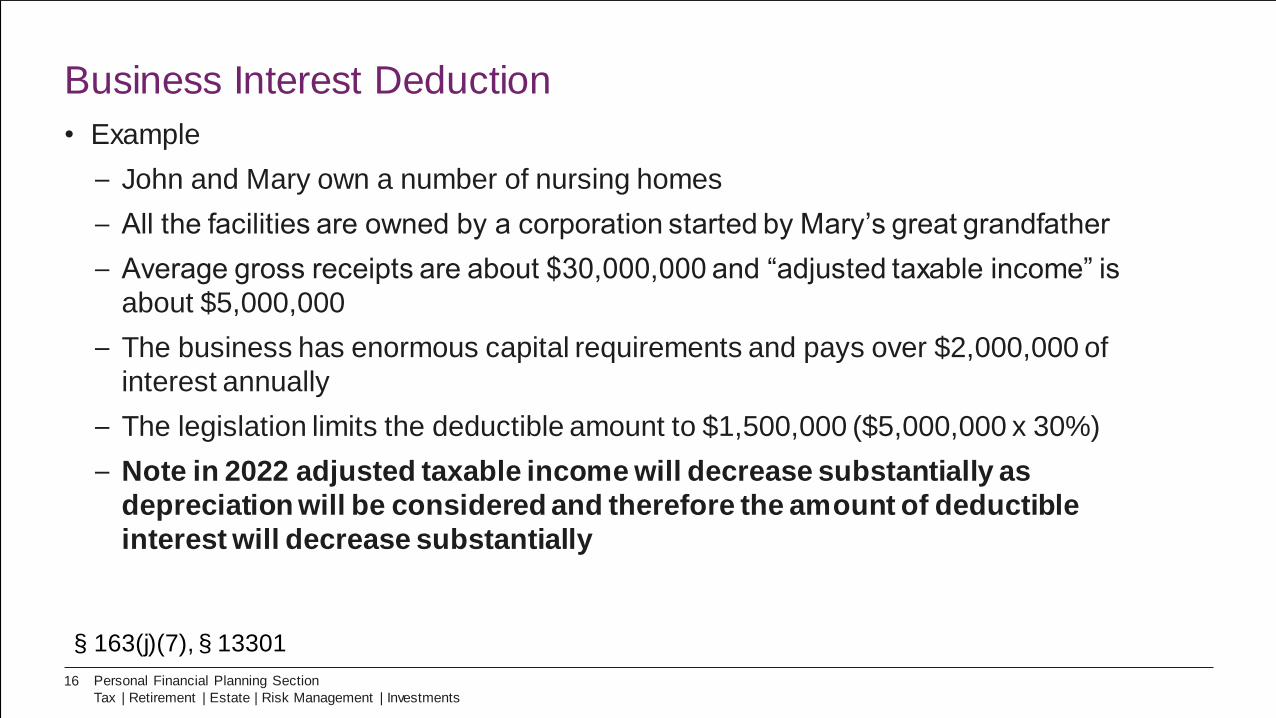

Business Interest Deduction

• Example

– John and Mary own a number of nursing homes

– All the facilities are owned by a corporation started by Mary’s great grandfather

– Average gross receipts are about $30,000,000 and “adjusted taxable income” is

about $5,000,000

– The business has enormous capital requirements and pays over $2,000,000 of

interest annually

– The legislation limits the deductible amount to $1,500,000 ($5,000,000 x 30%)

– Note in 2022 adjusted taxable income will decrease substantially as

depreciation will be considered and therefore the amount of deductible

interest will decrease substantially

§ 163(j)(7), § 13301

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

16

§ 163(j)(7), § 13301

2018-2021 2022+

Average Gross Receipts 30,000,000$ 30,000,000$

Less: Operating Expenses (25,000,000) (25,000,000)

Less: Depreciation (1,750,000)

Adjusted Taxable Income 5,000,000$ 3,250,000$

Interest Limitation 30% 1,500,000$ 975,000$

Business Interest Deduction

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

17

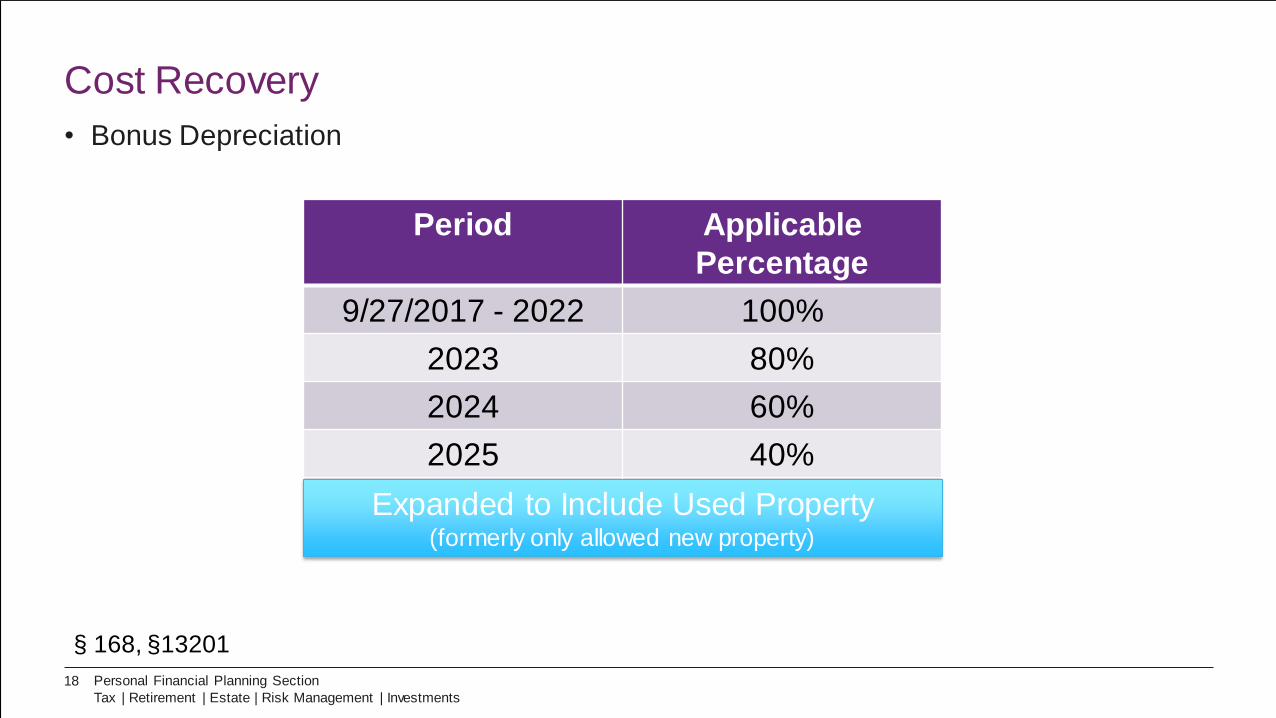

Cost Recovery

• Bonus Depreciation

Period Applicable

Percentage

9/27/2017 - 2022 100%

2023 80%

2024 60%

2025 40%

2026 20%Expanded to Include Used Property(formerly only allowed new property)

§ 168, §13201

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

18

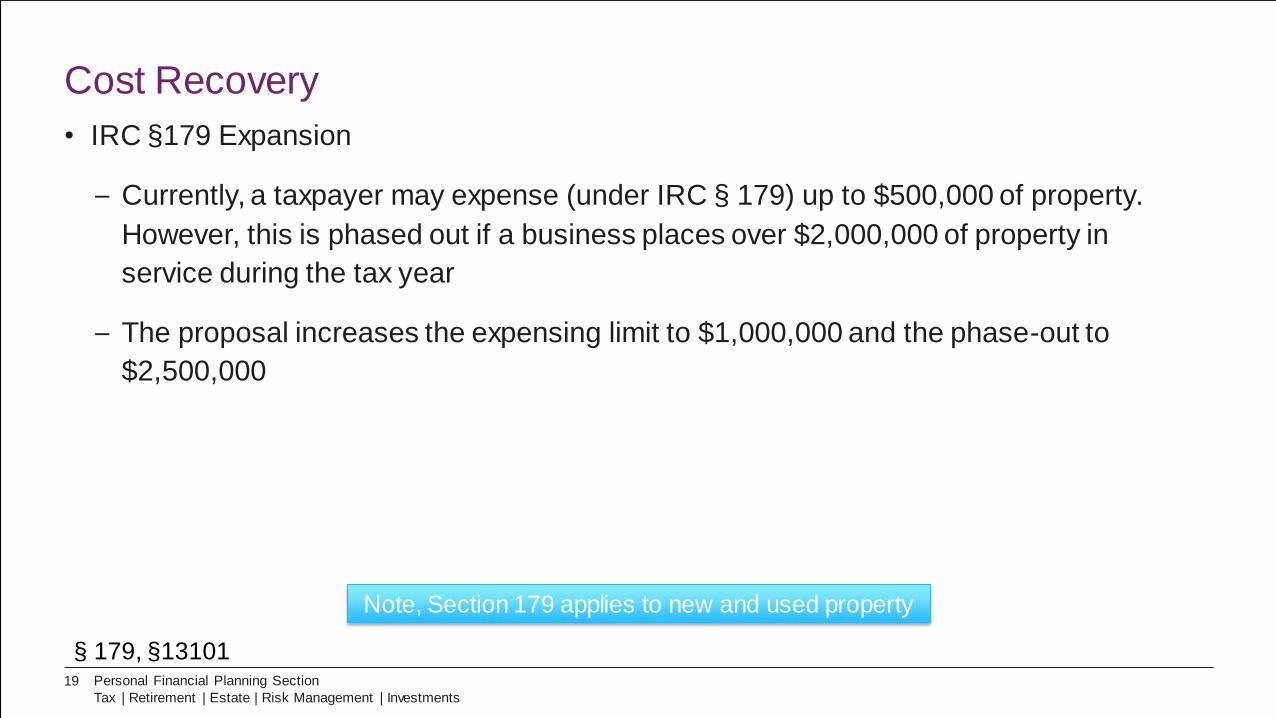

Cost Recovery

• IRC §179 Expansion

– Currently, a taxpayer may expense (under IRC § 179) up to $500,000 of property.

However, this is phased out if a business places over $2,000,000 of property in

service during the tax year

– The proposal increases the expensing limit to $1,000,000 and the phase-out to

$2,500,000

Note, Section 179 applies to new and used property

§ 179, §13101Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

19

Cost Recovery

• IRC §179 Expansion (cont.)

– Expands the definition of qualified tangible personal property and qualified real

property eligible to include

– tangible personal property used predominantly to furnish lodging or in

connection with furnishing lodging

– improvements to nonresidential real property placed in service after the date

such property was first placed in service:

– roofs;

– heating, ventilation, and air-conditioning;

– fire protection and alarm systems;

– and security systems.

§ 179, §13101

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

20

Cost Recovery

• A real property trade or business which elects out of the new limit on the deduction

for interest paid must use ADS; which requires the following recover periods:

2017 2018

– Qualified improvement property 39 years 20 years

– Nonresidential real property 40 years 40 years

– Residential real property 40 years 30 years

§ 168, §13204

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

21

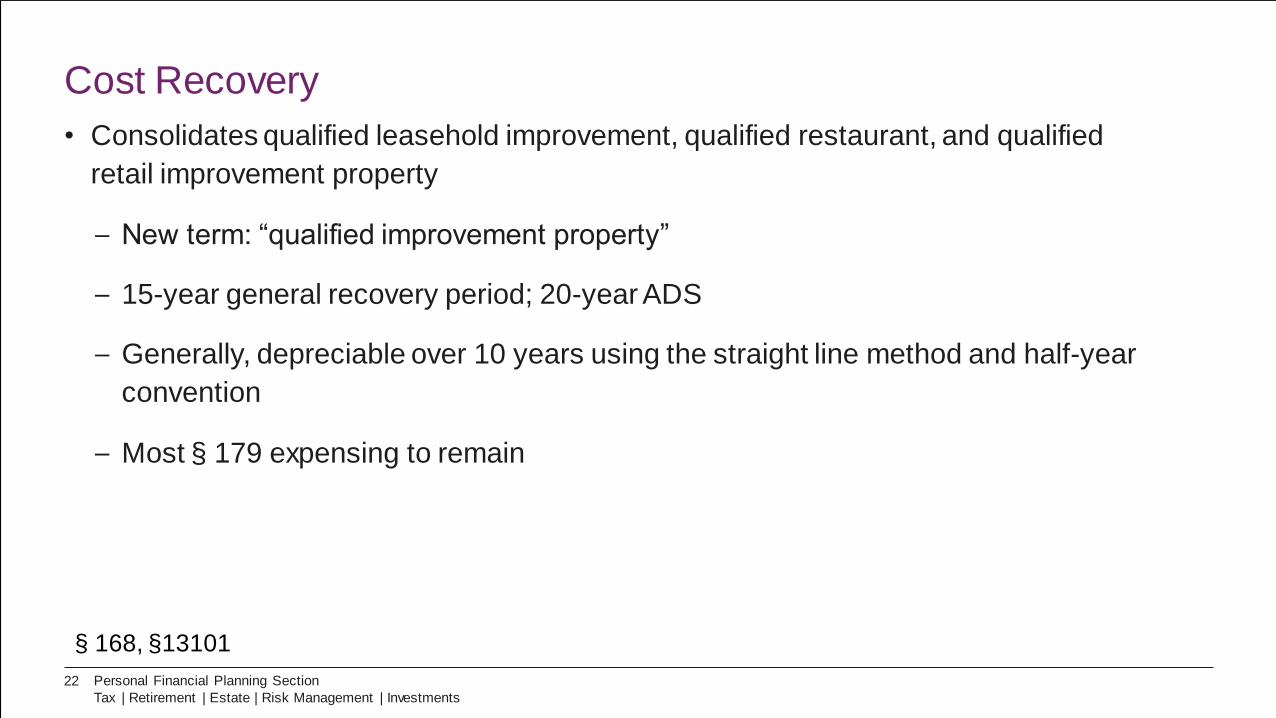

Cost Recovery

• Consolidates qualified leasehold improvement, qualified restaurant, and qualified

retail improvement property

– New term: “qualified improvement property”

– 15-year general recovery period; 20-year ADS

– Generally, depreciable over 10 years using the straight line method and half-year

convention

– Most § 179 expensing to remain

§ 168, §13101

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

22

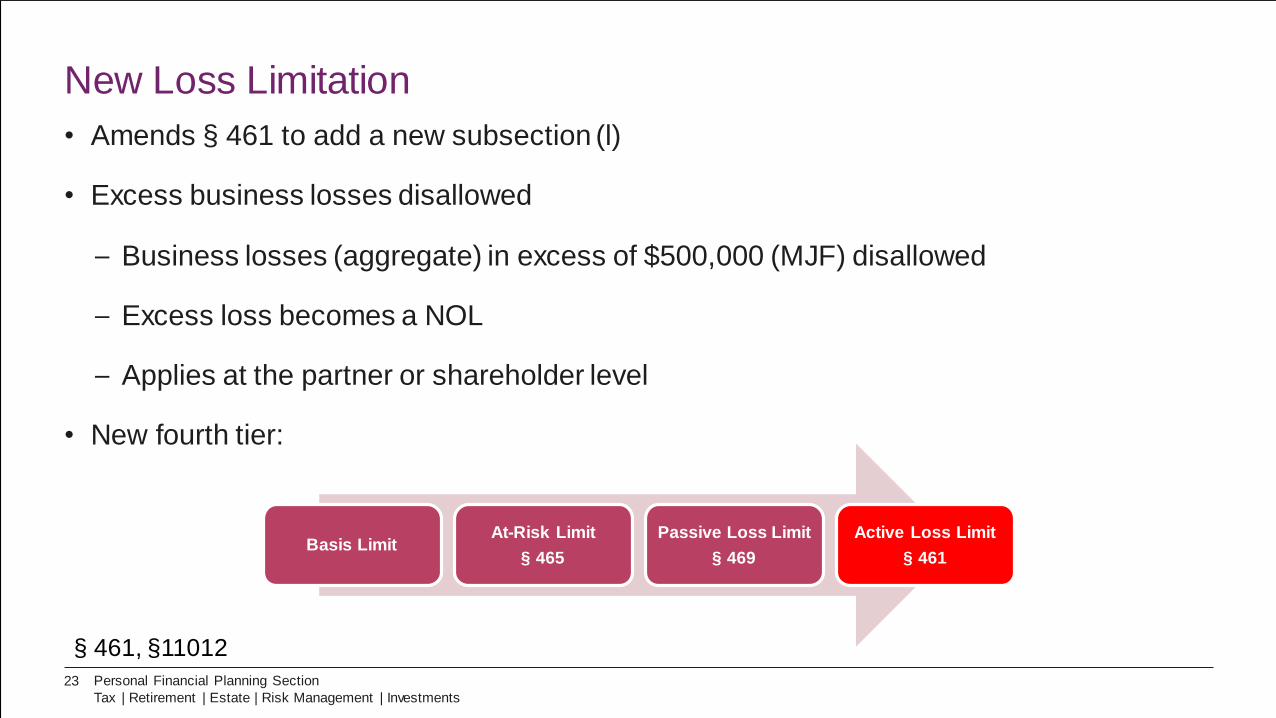

New Loss Limitation

• Amends § 461 to add a new subsection (l)

• Excess business losses disallowed

– Business losses (aggregate) in excess of $500,000 (MJF) disallowed

– Excess loss becomes a NOL

– Applies at the partner or shareholder level

• New fourth tier:

Basis LimitAt-Risk Limit

§ 465

Passive Loss Limit

§ 469

Active Loss Limit

§ 461

§ 461, §11012

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

23

Like-Kind Exchanges

• The bill limits like-kind exchanges to real property

• May complicate some transactions with personal property

• However, the bill allows transactions “open” at the end of 2017 to be completed tax-

free

§ 1031, §13303

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

24

Development Incentives

• Rehabilitation credit

– Tax Reform eliminates the 10% credit for the rehabilitation of certain buildings

constructed before 1936

– Tax Reform retains the 20% credit for the rehabilitation of historic structures, but

now requires it to be claimed over 5-years instead of in the year placed in Service

§ 47

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

25

Development Incentives

• Opportunity Zones

– Allows a taxpayer to defer capital gains that are reinvested in an Opportunity

Zone

– Opportunity Zones are certain low-income census tracts

– Qualified property can include stock, partnership interest, or business property

– If the Opportunity Zone investment is held for at least 10-years, the taxpayer can

elect that basis equals fair market value at sale

§ 1400Z-2, § 13823

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

26

AICPA PFP Section Member Resources

PFP Section members, inclusive of CPA/PFS credential holders, have access to resources on the latest planning strategies and

trends in personal financial planning services so that they can practice competently and profitably. Visit aicpa.org/pfp/resources.

Estate

Investment

Legislative/

Regulatory

Tax

Insurance &

Risk Management

Professional

Responsibilities

Retirement

Practice

Management

Consumer

Content

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

27

About the PFP Section & PFS Credential

• The AICPA Personal Financial Planning (PFP) Section is the premier

provider of information, tools, advocacy and guidance for CPAs who

specialize in providing estate, tax, retirement, risk management and/or

investment planning advice to individuals, families and business owners.

(Learn more

at aicpa.org/PFP.)

• The Personal Financial Specialist (PFS) program allows CPAs to gain and

demonstrate competence and confidence in providing estate, tax, retirement,

risk management and/or investment planning advice to individuals, families

and business owners through experience, education, examination and the

resulting PFS credential. (Learn more at aicpa.org/PFS.)

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

28

Disclaimer

This podcast is designed to provide illustrative information with respect to the subject matter

covered, and does not represent an official opinion or position of the AICPA or AICPA.Org. It

is provided with the understanding that the AICPA and AICPA.Org are not engaged in

offering legal, accounting or other professional service. If such advice or expert assistance

is required, the services of a competent, professional person should be sought. The AICPA

and AICPA.Org make no representations, warranties or guarantees as to, and assume no

responsibility for, the content or application of the material contained herein, and especially

disclaim all liability for any damages arising out of the use of, reference to, or reliance on

such material.

Personal Financial Planning Section

Tax | Retirement | Estate | Risk Management | Investments

29