tax reform in singapore2 3 - murdoch university · the main objective of this paper is to analyze...

TRANSCRIPT

Mukul G. Asher1

Tax Reform in Singapore2 3

Working Paper No. 91

March 1999

The views presented in this paper are those of the author(s) and do not necessarily reflect those of the Asia Research Centre or Murdoch University.

© Copyright is held by the author(s) of each working paper: No part of this publication may be republished, reprinted or reproduced in any form without the permission of the paper’s author(s). National Library of Australia.

ISBN: 0-86905-688-3 ISSN: 1037-4612

INTRODUCTION

The main objective of this paper is to analyze Singapore’s tax reform policies since the mid

1980s and their results, and to attempt to highlight possible future challenges and lessons

arising from them.

It may be useful to begin the discussion with a brief overview of Singapore’s

economic and social characteristics. Singapore is an affluent city-state with total population of

3.74 million4, and a per capita income of its resident population of 3.10 million of $US32,940

in 1997 ($US29,000 in PPP terms), the fourth highest in the world (The World Bank, 1998,

Table 1, pp. 190-191). During the 1985-97 period, Singapore’s nominal and real GDP grew at

an average annual rate of 11.46 and 9.69 percent respectively (calculated from the data in

Table A1). It is a highly open economy which has consciously integrated itself into

international division of labour in both manufacturing (particularly electronics) and services,

particularly those relating to trade logistics and finance, primarily foreign exchange trading5.

Its external trade to GDP ratio was 2.68 for 1997 (Republic of Singapore, Department of

Statistics, 1997, Tables 1.4 and 5.4).

Singapore’s economy is dominated by the MNCs6, the statutory boards and the

Government linked companies (GLCs)7. The official policy of the government is to keep the

wage share in national income as low as possible, and correspondingly keep the share of

capital as high as possible8.

The Statutory boards and the GLCs have used their monopoly power and absence of

competition policies to set prices significantly above marginal cost to generate surpluses. As a

result, their prices contain elements of taxation9.

One of the most important features of the Singapore economy is that the government

owns more than 80 percent of total land, up from around 40 percent in 1960 (Phang 1997).

Much of the land was acquired at below market prices under the draconian Land acquisition

act of 1966, which abolished the eminent domain provisions. There is no constitutional right

to land ownership in Singapore. Thus, between 1973 and 1987, the government acquired land

under the Act at 1973 rates rather than the market rates (Phang 1997). The land use rights for

a specified time period are auctioned and these prices then get reflected in residential,

commercial, and industrial developments which tax place. This in turn affects business costs

and cost of living of the households. This makes revenue from lease of land more akin to

taxes than to capital receipts classification used in the Singapore budget documents.

1

Singapore is also expected to experience both individual aging as reflected in higher

life expectancy at birth (it was 75 .0 for males and 79.2 for females in 1997); and in

population aging. Thus, in Singapore the share of population above 60 is expected to increase

from 8.5 percent in 1990 to 29.4 percent in 2030, an increase of 3.5 times (Asher 1998, Table

1, p6). Singapore’s Total Fertility Rate (TFR) is substantially below the replacement rate of

2100 (Table A1). The above demographic trends are expected to have significant implications

for the fiscal system. For the purposes of this paper, tax treatment of financing pensions and

health care is of particular relevance.

Singapore’s social security system almost exclusively consists of state mandated and

managed national provident fund, with tax-financed public pillar conspicuous by its absence

(Asher, 1998). This raises three questions pertinent to this paper. Should compulsory

contributions to the national provident fund (called Central provident fund or CPF in

Singapore) be regarded as taxes or as essentially contributions? Conventional international

practice is to regard them as the later and not include them as taxes. But if the distinguishing

characteristic of a tax is the use of compulsory powers of the state to finance an activity, then

they should appropriately be regarded as taxes. Indeed, Williams (1997) has argued that from

the point of view of an active contributor, there is little difference between the Singapore’s

CPF and the unfunded pay-as –you-go (PAYG) social security system in the United States,

except for the compulsory levels of payments in and the entitlement to payments out (1997,

p.260.).

The second issue is more subtle. In Singapore, the return paid on member’s balances

with the CPF is essentially an administered price rather than the returns actually obtained by

the ultimate investment of these funds. Because of the lack of transparency, the ultimate

investment policies and performance of these funds is not made public. In March 1996, the

minister of finance stated that investment returns on Singapore’s reserves had averaged well

over 5 percent over the past 10 years, though no precise figures were given (The Straits

Times, Singapore, 15 March, 1996.). This is higher than the return actually credited to

member’s balances (Asher,1998). The difference between the two thus represents an implicit

tax which has been estimated for 1995 to be $1,188.6 million or equivalent to 8.8 percent of

the total contributions in that year (Asher,1998,p.21). To the extent this situation persists, the

tax is a recurrent one. But it is not usually included in the conventional definition.

The third issue concerns the use of income tax and estate duties exemptions and

deductions relating to the CPF . Should the estimated value of such tax exemptions be

regarded in the fiscal accounts ? Net value of such exemptions and deductions should be

2

included as a part of Social security expenditure of the government (Adema, 1997). In

addition, the differential benefits of these tax breaks for different income groups should also

be taken into account.

Singapore has been governed by a single party since 1959. The government is

paternalistic which in the Singapore context means that the government decides on the public

policy goals, how to achieve them and whether they have been achieved. Those with differing

views are allowed little room in the society, particularly in the political arena. It has staked its

authority on delivering improved material conditions to its people on a consistent long-term

basis. The government operates on the belief that demands for non-material aspects which

may challenge it can be contained if not marginalised.

The above characteristics of the Singapore economy and society are important in

understanding its tax reform policies. Thus, they help explain the important objective of

maintaining international competitiveness in formulation of tax policies10; general disregard

of the conventional notions of horizontal and vertical equity, strong presence of regulatory

taxes, and the extensive and activist regime of fiscal incentives. Also, as Singapore attempts

to overcome constraints of domestic size by investing abroad, particularly in East Asia,

increasing number of incentives are being directed towards that objective as well.

The rest of the paper is organized as follows. A brief discussion of aggregate fiscal

indicators is provided in section II. This is undertaken for the following reasons. First, since

the tax system is a part of the overall fiscal system, it may be useful to have an understanding

of the overall system and its main characteristics. Second, as it is clear from the previous

discussion, traditional definition of taxes is by itself not suitable in the case of Singapore. It is

therefore necessary to at least briefly note the importance of other sources of government

revenue. Section III analyses the revenue structure in greater detail, with particular emphasis

on the nature and structure of various taxes, and how these have been reformed since the

1980s. A brief discussion of tax administration in Singapore is provided in Section IV. Policy

issues and future directions are discussed in Section IV.

MAIN FEATURES OF THE FISCAL SYSTEM

On the basis of Singapore’s aggregate fiscal indicators for the 1991-97 period (Table A2) and

budgetary balance for the 1985-97 period (Table A3), the following observations may be

made.

3

1) While the conventionally measured tax revenue to GDP ratio is rather low (fluctuating

within a narrow range 16 to 18 percent during the 1991-97 period ), its total revenue to

GDP ratio is not only high but has shown a tendency to increase. In 1997, the ratio was as

noted earlier, equivalent to 38.5 percent of GDP11. Since, revenue from the leasing of land

should be regarded as a current rather than a capital receipt, and since there is substantial

tax element in fees and charges, the effective tax burden is substantially higher than the

conventional tax figures suggest. This is the case even if the implicit tax on CPF balances

is ignored. Thus, Singapore cannot be regarded as a low tax country. Anecdotal evidence

suggests that this is indeed how management consultancy and other such firms portray

Singapore. At the same time, Singapore’s wide network of tax treaties is often used in

international tax planning as a shield before money is transferred to tax havens. Those

MNCs with minimal presence in Singapore and whose main motivation is tax planning

may therefore not experience the full impact of a high taxation burden even if they are not

benefiting from an extensive set of fiscal incentives.

2) Extreme conservatism of Singapore’s fiscal stance is indicated by the high budgetary

surpluses and by the substantial share of GNS (Gross national savings) being accounted

for by the government saving, defined as Current account balance (CAB)(Table A3).

Thus, for the 1985-97 period as a whole, government saving averaged 41.2 percent of

GNS. If Statutory board surpluses, profits of the GLCs, and the compulsory CPF savings

are added, it is clear that in Singapore there is extremely high degree of concentration of

the nation’s savings in the hands of the government . This is not an unintentional outcome

but an essential aspect of Singapore’s growth strategy in general and its fiscal strategy in

particular. Whether Singapore government is able to sustain such high concentration over

savings in an era of globalization and as the economy enters the mature phase, and

whether such high concentration is consistent with the greater role for market forces

which the policymakers are professing to foster are issues which would need to be

addressed.

3) The government has been able to keep its total expenditure to GDP ratio fairly low,

though during 1996 and 1997, there is evidence of substantial increases in development

expenditure and in net lending to government enterprises. Since 1995, net lending has

exceeded direct development expenditure by the Ministries. The current expenditure

however has been kept at a very low level. During the 1985-97 period, buoyancy of

current expenditure was only 0.56 as compared to 1.043 for total budgetary revenue and

1.11 for the total tax revenue (Tables A10 to A12).

4

As a result of persistently large surpluses over time combined with substantial internal public

debt, the government's balance sheet exhibited total assets of $285.5 billion as on March 31,

1999 ( Republic of Singapore, 1999 Budget) The Singapore Budget does not provide the

method (eg historical cost, or market value) by which the asset values have been estimated.

Moreover the information contained in the Budget on total assets is not sufficiently detailed to

undertake meaningful analysis. Thus, the 1999 Budget reports that as at March 31, 1999, the

Singapore government held $53.5 billion in cash; $88.5 billion in Government Stocks $106.5

in Quoted other investments; $106.5 billion in Unquoted Other Investments; $3.8 billion in

Deposits with Investment Agents; and the rest of $285.5 billion in other instruments.

The above two characteristics of the balance sheet of the Singapore government has meant

that some very important and significantly large components of its financial transactions have

been non-transparent and have escaped Parliamentary and public scrutiny. This has been

exacerbated by the long-standing practice of the Budget Speech and the consequent Budget

debate in the Parliament focusing only on the artificially delineated budget which departs

significantly from the manner in which the International Monetary Fund (IMF) classifies

budgetary transactions.

REFORMS IN REVENUE STRUCTURE

The period since the early 1980s has witnessed several significant measures in the revenue

structure of Singapore. Three new sources of revenue which have been introduced are the

foreign workers levy (1982), Certificate of Entitlement (COE) which is a right to own a motor

vehicle (May 1990), and the comprehensive Goods and Services Tax (GST), a value added

tax introduced in April 1994. In general there has been rate reductions12 in existing taxes, but

these have not been accompanied by base broadening measures13. Indeed, the social

engineering aspects of tax policies and range and scope of fiscal and non-fiscal incentives for

businesses has grown substantially since the early 1980s. As a result, static resource allocation

effects and equity aspects have been subordinated to achieve paternalistic government’s

socio-economic objectives. Large budgetary surpluses generated by rapid economic growth

and by government’s ability to contain current expenditure have meant that economic

efficiency (as opposed to commercial profitability) considerations have not always received

due recognition.

Income Tax :

5

Income tax was first introduced in Singapore in 1948 when it was still a British

colony. Singapore has a partially integrated source –based income tax. It is achieved through

the dividend –received –credit method . This is designed to tax retained earnings at the

company income tax rate, and tax dividends at the marginal individual tax rate of the dividend

recipients. There is a one year lag in income tax payments, as the tax liability in a given year

is based on the previous years income. This is not conducive to stabilization as illustrated by

the income tax payable in the recession year of 1998 which is based on relatively healthy

incomes and profits earned in 199714. The income tax is based on official rather than self-

assessment.

The source principle provides a built-in tax avoidance mechanism for high income

individuals who can earn non-labor income abroad, often without paying tax in the source

country, and then using the income outside Singapore.

In FY 1992, income tax accounted for half of the tax revenue, and little more than

quarter of the budgetary revenue (Table A4). However, this share has been declining

overtime. Thus, in 1997, 44 percent of tax revenue and only 18 percent of the budgetary

revenue was from the income tax. This decline would have been steep had the Statutory

Boards been not required to pay administratively determined income taxes15.

While the data on income tax revenue collected are not decomposed into personal and

company income tax, the latter has typically accounted for around two-thirds of the income

tax revenue. The gap between assessed tax on individuals and tax payable is particularly

large. Thus, in 1996, the assessed tax on individuals was $2993 million, but the net tax

payable was $2210 million or less than three fourths of the assessed (Inland Revenue

Authority of Singapore, Annual Report 1996, Appendix tables 13 and 15 ).

Individual Income tax :

The nominal rates for individual income tax have been decreasing since the 1980s

(Table A5). At present, the nominal rates range from 2 percent to 28 percent, with 10 income

brackets. In 1987, the rates ranges from 3.5 per cent to 33 per cent with 13 brackets. Thus,

while the government has followed the international trend towards reducing nominal rates, it

has not followed the practice of flattening the rate structure. In addition to rate reduction, the

government has frequently resorted to one-off rebates. So the effective rates have often been

lower (Table A5).

In addition, to compensate for the introduction of the GST in April 1994, the

government had provided additional rebate on a sliding scale. The initial rebate in 1994 of

6

$750 has been reduced by $50 each year until it reaches $500, and thereafter it is to remain at

that level (Table A5).

Moreover, as the unit of tax is the individual, the rebate is provided to each individual

earner, sharply reducing the progressivity of the income tax. As the individual as unit of tax

reduces marginal tax rate on earnings of secondary workers, it is more conducive to their

labor force participation. This constitutes a strong rationale for individual as a unit of taxation

in the labor-scarce Singapore.

As a result of the above rebates, only 27.6 percent of the labor force was paying

individual income tax in 1996 (Table A6) and a significant proportion of them would be

expatriates working in Singapore. This is a sharp reversal from the mid 1980s when between

three-fifths and two thirds of the employees paid taxes (Asher,1989 Table 5.7,pp.155). The

unequal income structure in Singapore is evident from the fact that in 1996, nearly two thirds

of the taxpayers at the bottom contributed just 15.3 per cent of total assessed income tax ;

while at the upper end, 3.8 per cent of the taxpayers contributed 40.4 percent of the assessed

income tax (Table A6).

The Gini coefficient for resident taxpayers increased from 0.41 in 1979 to 0.47 in

1992 and is likely to have increased further since then (Rao, 1996, Table 18.2, p.387). Since

capital gains and income earned abroad but not brought into Singapore are exempt, and since

these accrue disproportionately to higher income individuals, the Gini coefficient for all

income, is likely to be higher than the coefficient for resident taxpayers.

The Singapore government has used deductions, tax credit, and exemptions to promote

a variety of social and other objectives. Capital gains (except for limited types of residential

property transactions ) are exempt in Singapore. A list of a wide range of deductions and tax

credits permitted under the individual income tax is provided in Table A7. As a result, in

1996, the chargeable income was only 75 percent of the assessed income.

As may be expected the largest deduction (about half of the total) is for the CPF

contributions16. But there are also deductions for foreign maid levy, reservists relief, for

children, course fees, life insurance, etc. Each type of deductions has eligibility conditions

attached. These depend on the government’s social engineering goals. A good example is the

provision of progressively generous deductions and tax credit for younger (age specific),

academically qualified women (qualifications specified), who bear children (number

specified). This is to increase the number of children born to women considered socially more

desirable by the government.

7

Company income tax :

The nominal company income tax rate remained unchanged at 40 per cent between

1966 and 1986. Since then, in a series of steps, the nominal rate has been reduced to 26

percent.

In November 1998, the government announced a 10 percent rebate on company

income tax to enable businesses to cope with the current crisis. The Singapore government is

aware that nominal rate of below 25 percent, combined with extensive fiscal incentives, could

be perceived in some cases (e.g. corporate regional headquarters scheme) to be in the nature

of “fiscal dumping” by some countries. This would lead them to regard Singapore as a tax

haven. Australia, for example already has enforced Control led Foreign Corporation (CFC)

legislation in partial response to some of the incentive schemes offered by Singapore. It is for

this reason that the government is reluctant to set the long term company income tax rate

below 25 percent.

The rate reduction has not been accompanied by base broadening . Since the 1960s,

Singapore has actively used fiscal incentives to not only attract desired investments in

manufacturing and services, but also to help facilitate a transition to newer areas of activities.

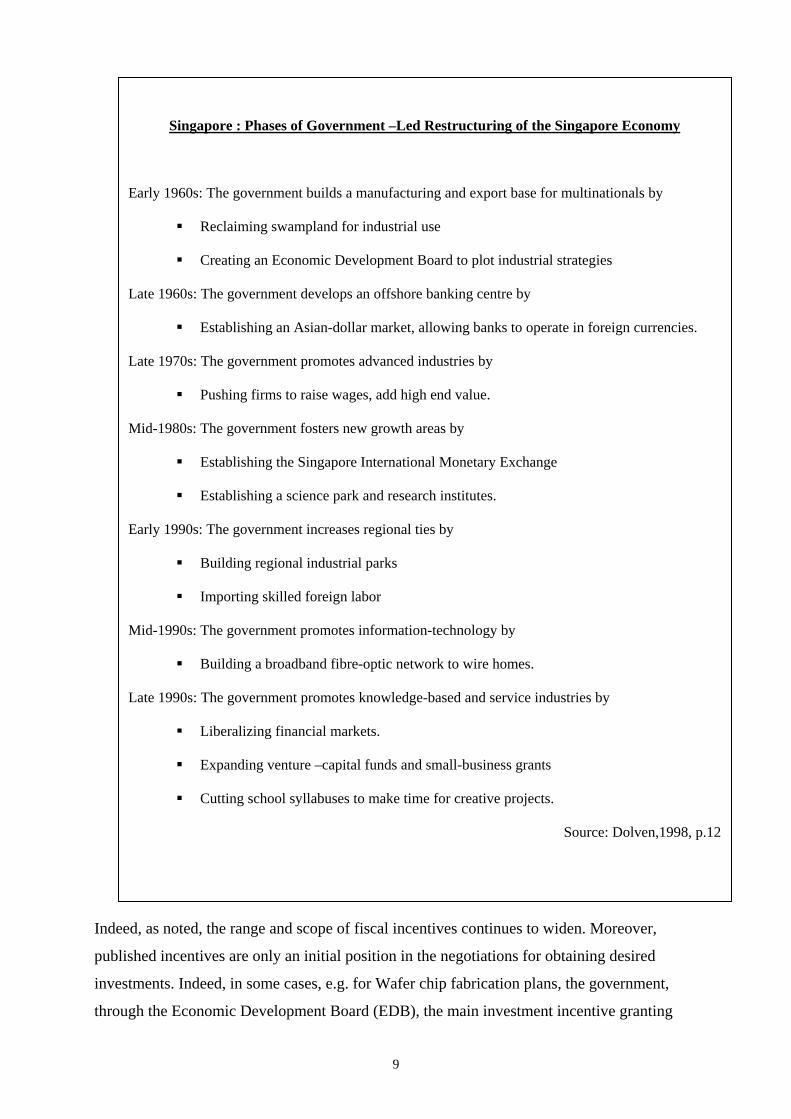

Various phases of government led, top-down restructuring of the Singapore economy are

summarized in the box below :

8

Singapore : Phases of Government –Led

Early 1960s: The government builds a manufactu

Reclaiming swampland for industrial

Creating an Economic Development

Late 1960s: The government develops an offshore

Establishing an Asian-dollar market,

Late 1970s: The government promotes advanced

Pushing firms to raise wages, add hig

Mid-1980s: The government fosters new growth a

Establishing the Singapore Internatio

Establishing a science park and resea

Early 1990s: The government increases regional t

Building regional industrial parks

Importing skilled foreign labor

Mid-1990s: The government promotes informatio

Building a broadband fibre-optic netw

Late 1990s: The government promotes knowledg

Liberalizing financial markets.

Expanding venture –capital funds and

Cutting school syllabuses to make tim

Indeed, as noted, the range and scope of fiscal ince

published incentives are only an initial position in

investments. Indeed, in some cases, e.g. for Wafer

through the Economic Development Board (EDB),

9

Restructuring of the Singapore Economy

ring and export base for multinationals by

use

Board to plot industrial strategies

banking centre by

allowing banks to operate in foreign currencies.

industries by

h end value.

reas by

nal Monetary Exchange

rch institutes.

ies by

n-technology by

ork to wire homes.

e-based and service industries by

small-business grants

e for creative projects.

Source: Dolven,1998, p.12

ntives continues to widen. Moreover,

the negotiations for obtaining desired

chip fabrication plans, the government,

the main investment incentive granting

agency, been willing to offer manpower training at the public expense and to take significant

equity stake in the new ventures17. As each negotiated investment has a unique package of

incentives, and this package is secret, it is not very useful to base studies of incentive effects

on published set of incentives18.

The number of government agencies granting and administering incentives has also been

growing as increasing such incentives are seen as integral part of policy package for attracting

newer activities. Thus, the Trade Development Board (TDB), a statutory board, has a scheme

for cybertraders under which the approved firms receive a concessionary company income tax

rate of 10 percent (instead of 26 percent), full or partial exemption from withholding tax, and

an investment allowance of upto 50 percent.

While the focus has traditionally been on providing incentives for inward investment,

in recent years as a part of its regionalization drive, incentives have been provided for

outward investment as well. This would complicate Singapore’s task of international tax

policy formulation, particularly in the area of tax-sparing.

An important feature of Singapore’s incentive practices which is worth close study is

its method of post-incentive evaluation of investment projects receiving such incentives. This

permits it to monitor and evaluate investment projects receiving incentives much more

carefully after they have gone into operation. In most countries, post investment evaluation of

incentives has not received the attention it deserves.

Property tax :

The announcement for streamlining the property tax structure, essentially uniform 23

% on gross rental value or its equivalent was made in 1979, but implemented over the next

five years. As a part of the package to deal with the 1985-86 recession, property tax rebate (of

initially 30 percent, subsequently 50%) was given until 1990. Since then, the tax rate,

effective from July 1,1996 has been reduced to 12 percent ; for owner occupied residential

properties, a reduced rate of 4% is levied on the current annual value.

In May 1996, Singapore introduced a tax on capital gains and widened the scope of

stamp duties relating to real property. Since then, property investors have been taxed on gains

from real property which is sold within three years of acquisition. Property traders continue to

be taxed on 100% of gains regardless of the time period. Since May 1996, stamp duties apply

to both buyers and sellers of real property. The stamp duties apply on a sliding scale, reaching

a zero rate if property is sold after three years. These measures were designed to reduce

profits arising from the property transactions.

10

To cope with the current East Asian economic crisis, the government has announced a

series of rebates on property taxes, particularly those involving commercial and industrial

properties which provide the bulk of the property tax revenue.

Motor Vehicle taxes:

An important feature of Singapore’s revenue structure is the revenue importance of

motor-vehicle taxes. While the revenue importance has declined since the early 1990s,it

remains substantial (Table A4). Thus in FY 1992, motor vehicle taxes and Vehicle quota

premium, i.e. revenue from COE, accounted for 25 percent of total taxes or 4.4 percent of the

GDP, but the corresponding proportions had declined to 18.7 and 2.9 percent respectively by

FY 97. (Table A4).

In Singapore the motor vehicle taxes have been levied both on ownership and on

usage. Ownership taxes include import duties, registration fees, annual road tax, GST, and the

Certificate of Entitlement (COE); while the usage fees include fuel taxes, parking fees, off

peak car usage, congestion tolls, and Electronic Road Pricing (ERP) scheme (Chia,1998). In

1985-86, the share of ownership taxes in total motor vehicle taxes was 57.2 percent, but it

increased to 83.5 percent by 1995-96 (Chia, 1998,Table 12, p.288).

The COE is needed by a buyer of a new vehicle since the scheme was implemented in

May 199019. It may be obtained in a public tender held by the Registry of Vehicles (ROV)

each month. It is valid for a period of ten years. Owners of cars older than ten years must pay

the prevailing average quota premium. Thus, under the COE, the growth rate of motor

vehicles each year would be determined by the government as it would decide the number of

COEs to be issued each month. While increase in road capacity is perhaps the most important

factor in this decision, there exists room for discretion in deciding on their number.

The COE is premised on the basis that the ownership of a motor vehicle is the main

contributor to negative externalities arising from congestion and pollution. There has,

however been some rethinking as evidenced by the gradual shift at the margin from

ownership taxes to usage taxes (Chia,1998; Phang and Asher,1997).

Both type of taxes are however expected to remain high, and provide substantial

revenue to the government. However, their impact on business costs and on the ability to

attract and retain talent will be of increasing concern to the policy makers.

Goods and Services Tax (GST):

A GST was implemented from April 1, 1994 As a part of the strategy to shift the tax

mix away from taxation of income and profits to that of consumption, the Singapore

11

government introduced Goods and Services Tax (GST) on April, 1, 1994. The government

was quite aware of the need for careful political management leading up to the introduction of

the GST. The campaign slogan for the GST was “ A fairer tax, a brighter future”. Links

between GST and fairness and between GST and brighter future were however not explained.

The paternalistic nature of the Singapore government meant that the different views did not

get aired publicly. There was however an extensive educational campaign. The government

also guided key government-linked companies, including supermarkets, to absorb the GST on

key wage goods during the initial period, thus minimising the impact on the Consumer Price

Index (CPI) used to track inflation.

Along with the introduction of the GST, individual and company income tax rates and

property tax rates were reduced. Also, several rebates on user charges (such as conservancy

fees for public housing) were provided. As noted, provision of individual income tax rebates

to offset the impact of GST reversed a long standing government policy of making as large a

proportion of workforce pay income taxes as possible. In 1996, only 27.6 percent of the labor

force paid income tax as compared to about two thirds in the mid 1980s.

Singapore’s GST is a multi stage tax intended to be on domestic consumption using

the invoice-based input tax credit mechanism. It is levied at a rate of 3 percent. Only exports

and narrowly specified international services are zero rated. However, because of the high

turnover threshold of $ 1 million, specified for businesses to register, only 50,510 businesses

were registered for the GST as on March 31, 1997 (Table A8). This comprises about 25

percent of the total businesses. Exempting such large proportion of business from registering

for the GST could lead to possible cascading effects20, make GST less neutral, and in effect

turn it into a complicated excise tax.

Given Singapore’s dependence on international trade, administering of the GST has

turned out to be a more complex task than originally envisaged. Many ad-hoc schemes have

had to be developed to cope with Singapore’s open economy. These include Major Exporter

scheme designed to relieve the imports of the qualifying exporters from the GST; Bonded

Warehouse scheme ( involving suspension of GST on imported goods that enter Singapore

and are stored in bonded warehouse) ; a limited refund scheme for tourists ( only those

tourists who spend $500 or more in one shop or within the same retail chain ) ; and pre-

determined input tax recovery rates for banks, finance companies, and insurance companies

(Jenkins and Khadka,1998).

Unusually for Singapore, a senior official of a government-linked company has

publicly complained about the need for the GST to be more business friendly, particularly for

12

those in manufacturing and exports ( Chay, 1999). The main contention is that the GST has

become a tax burden to many businesses. The main avenues resulting in such burden are

levying GST on full value of goods sent to neighbouring countries on consignment for simple

processing and then brought back to Singapore for further processing ; Cash-flow impact on

exporting firms who need to initially pay the GST on purchases of local inputs ; and

limitations of Major Exporter scheme which limit relieving of GST on imports only if the

exporter orders directly from overseas rather than through local intermediaries. (Chay,

1999)On the positive side, the GST has helped in administration of the income tax.

A puzzling aspect of the revenue behaviour of the GST is that the effective rate (GST

revenue divided by private consumption expenditures including tourist expenditure in

Singapore, less resident expenditure abroad ) has been over the statutory rate of 3.0 percent

and rising . The effective rate was 3.72 percent in 1995, 3.78 in 1996, and 3.92 in 1997.

There may be three possible reasons for the above. First, government’s non-wage

consumption may be contributing to the GST revenue. If this is the case, private consumption

expenditure may understate the GST base.

However, if the government consumption involves GST, then financing burden will

also increase, and other taxes may have to be raised or service levels and quality reduced.

Thus, the incidence is likely to be still on the taxpayers.

Secondly, cascading effects arising from the large exemption level have increased the GST

tax base beyond just consumption expenditure. Thus, when total GST revenue is divided by

the smaller tax base represented by consumption expenditure, the ratio exceeds the statutory

rate of 3.0 percent .

Third, to the extent the GST incidence is not fully on consumers but is partly on

businesses, it will reduce market value of total consumption expenditure. As the tax base is

reduced, the ratio could once again exceed the statutory rate.

The quantitative importance of the three factors is however not known. What is evident is that

the GST revenue collected exceeds the private consumption expenditure, the presumed tax

base.

The official rationale for the GST is that its implementation permits reduction in

income and property tax rates, thereby maintaining international competitiveness of

Singapore’s tax system. It also permits taxing consumption of increasing number of aged in

the population. The rationale implicitly assumes continuation of the present high structural

budget surpluses. These anticipated benefits need to be counterbalanced against increased

13

inter-generational inequity (those who are presently aged forty years and above would need to

pay higher life-time taxes as a result of the GST); increased regressivity of the fiscal system ;

higher administration and compliance costs (compliance costs as percentage of turnover are

higher for small firms by a significant margin) ; and increased complexity of the fiscal system

(Asher, 1993).

Foreign Workers’ Levy:

This levy, introduced in 1982, is designed to increase the cost of foreign workers, and

thereby reduce their demand. Analytically, it is like a variable payroll tax. In 1994, around

300,000 foreign workers (18 % of the workforce ) were employed in Singapore. The levy is

however only on those earning below $SGD2,000 or less (as of late September 1997). The

rate varies according to the type of worker (e.g. foreign maids levy is different from those in

manufacturing), and by skills levels (levy is higher for unskilled than for skilled workers).

The objectives are to discourage entry of unskilled workers, and to minimize social friction

arising from the presence of a large number of foreign workers.

In FY 1997, revenue from this source was 9.1 % of total taxes or 1.4 % of GDP (Table

A4). While the incidence of the levy is likely to be predominantly on the workers themselves

(indeed in the case of maids, levy of $350 per month is substantially larger than the going

wage of around $250 per month). However, no specific expenditures are allocated for the

benfits of the foreign workers.

It is also pertinent to note that the government not only determine the rate of levy but

also retains control over the overall number and sources of foreign workers allowed into

Singapore on an industry-by-industry basis. Thus, both price and supply of foreign labor are

not left to the market forces. It is therefore not intended to act as a mechanism to determine

the optimum level and allocation of foreign labor, but as a regulatory device which is also

highly revenue productive. Each case of foreign worker has to be applied for, and

discretionary element in the administration is high.

The impact of this levy on the business costs is of increasing concern to the

government during the current East Asian crisis. In November 1998, the government

announced significant cuts in levies for skilled workers, but not for maids or construction

workers. Thus, revenue from this source is expected to decline moderately over the next

several years. There has been a proposal to auction labor beyond a certain pre-determined

level to individual business.

Others:

14

Singapore’s role as an entrepot has meant that it has traditionally levied import duties

on only a limited number of demerit goods such as alcohol and tobacco ; on certain luxury

items such as chocolates, and on motor vehicles. Revenue from this source is therefore quite

small (Table A4). The estate duty structure has been streamlined, with only two rates of 5 %

and 10 % . The excise duties are levied only on petroleum, tobacco and alcohol products, and

these are levied at fairly high levels. The payroll tax has been suspended (but not abolished)

since the 1985 recession. There is also a Skill Development Fund (SDF) levy of 1.0 % of

payroll of those below a certain wage. Betting taxes, and stamp duties are also important

sources of revenue, accounting for 5.6 percent and 7.3 percent of total tax revenue

respectively in 1997 (Table A4).

TAX ADMINISTRATION

The Singapore government has paid considerable attention to the tax administration

issues. Even as it continues to provide extensive and growing set of fiscal incentives, and

continues to exempt transactions which have proved to be administratively complex such as

the capital gains, it has enacted comprehensive anti-avoidance legislation to limit the scope of

aggressive tax planning ; and restructured its tax administration to improve administration and

compliance efficiency.

As a result of the restructuring, the Inland Revenue Department (IRD) was

transformed into a Statutory Board called the Inland Revenue Authority of Singapore on 1

September, 1992.

The main reasons given for the switch were that the official assessment system for

income and other direct taxes, along with increasing number of income taxpayers due to rapid

growth leading to higher wages and profits, had increased the workload significantly while

the staff strength had lagged behind. In 1991, the backlog of assessments was nearly 50

percent ( this meant that at the end of the 1990 cycle, half of tax returns were not assessed )

and the arrears were growing at an annual rate of 7 percent. At the end of 1990, the amount of

accumulated tax unpaid was 20 percent of the annual tax assessment

The turnover rate for professionals was high, and staff morale low. The official

reasoning on much of the information on restructuring of tax administration (Ong,1996) was

that constraints on personnel and financial management imposed by the civil service could be

overcome by adopting the Statutory Board format.

15

IRAS is governed by a Board of Directors, chaired by the Minister of Finance, Chief

Executive Officer of the IRAS, and five other appointed members.

IRAS is paid an agency fee by the Singapore government for its services. The fee is

negotiated and is currently determined by a two –tire formula. The first tier consists of a fixed

percentage (1.65 percent of the projected tax collection) of the tax collection for the year. The

second tier is performance based. An incentive bonus of the 2 percent of the difference

between the actual and projected revenue is paid if the actual collection exceeds projected

collection. Conversely, if actual collection is below projected, a deduction in fee would be

deducted. Details of how the projected revenues are set, and what allowance is made for the

business cycles and other contingencies, as well as the other performance indicators which the

IRAS is to meet, are however not available. In their absence, it is difficult to evaluate the

above arrangement. The accountability of the IRAS is based on the financial statements, and

annual statements on tax assessed and collected provided to the parliament and audited by the

Auditor General.

The shift to the Statutory Board format enabled the IRAS to re-structure work

processes; re-design computer and other system to focus on service rather than tax and task

orientation; and re-organise staff structure and personnel management system (Ong, 1996).

IRAS plans to gradually shift to the self-assessment system of income tax; and to

further streamline, computerise and automate work processes. This will involve extensive use

of information technology (Ong, 1996).

The monocentric power structure in Singapore has resulted in almost no challenges to

the rulings of the IRAS. Its impact on equity is not known, however.

POLICY ISSUES AND FUTURE DIRECTIONS

The analysis in this paper suggests that while Singapore’s revenue system does not

meet the conventional criteria of neutrality, equity, and efficiency, it is highly revenue

productive and is consistent with the countries’ economic strategy and socio-political

characteristics. The tax reform process in Singapore has been continuos one, with emphasis

on professional planning and investing in physical and human capital to increase the

capability of the tax administration. The government has also given sufficient weight to the

need for preparing the political ground for implementing new tax initiatives such as the GST

and the ERP.

16

However, due to a combination of factors, Singapore would need to make major

adjustments to its revenue policy. These factors include globalisation, maturing of the

Singapore economy, rapid aging of the population, its shift to knowledge economy whose

participants increasingly desire greater level of social amenities and personal space, and the

impact of the current economic crisis in East Asia.

Thus, globalisation will make it increasingly difficult to pursue aggressive fiscal

incentive policies. It is also probable that as a result of globalisation, there may be a shift in

taxing corporations from the existing arrangements to the one under which global profits of an

MNC are allocated among different tax jurisdictions according to some agreed upon formula

on a multilateral basis. This would reduce the maneuverability of Singapore’s aggressive

fiscal incentive policies and could reduce its revenue base.

An emerging international issue in taxation concerns how to tax the electronic

commerce (Owens,1997). Singapore has plans to be an important hub for the electronic

commerce. However, such commerce has the potential to erode the tax base, particularly, for

the GST. The E-commerce and the internet could also reduce the need for maintaining

physical presence in different locations. This may impact on Singapore’s attractiveness as a

location for some types of businesses, affecting its tax base. The policymakers in Singapore

however do not appear to be concerned about the implications of E-commerce for the tax

base.

The slower economic growth as a result of maturing of the economy will impact on

the revenue productivity of company income tax and certain regulatory taxes. It will also

mean much slower increases in personal incomes, thus dampening the buoyancy of the

consumption related taxes. The rapid aging of the population will adversely impact on the tax

base, introduction of the GST notwithstanding. It will also require increases in government

expenditure on social security and health care and possibly reduce the savings rates in the

economy. The knowledge economy will make it increasingly difficult to levy extensive

regulatory taxes and engage in social engineering through the tax system through the same

degree as in the past.

The current economic crisis in East Asia will impact on the revenue system in

a variety of ways :

1) The crisis has substantially reduced the capacity of the statutory boards and the GLCs in

Singapore to use their monopoly power to generate surpluses. This is because there is

extensive over capacity in not only manufacturing but also in services such as Sea ports,

Airports, Telecommunications and others. In November 1998, the Singapore government

announced significant reductions in various user charges, rentals and fees by the public

17

enterprises. As an example, Singapore’s largest industrial landlord, a government agency,

Jurong Town Corporation (JTC) expects 30 to 40 percent decline in its operating revenue

for the year 1998-99 financial year, and has halted all new developments on which

construction has not yet begun (The Straits Times, Singapore, December 18, 1998). It is

unlikely that such reductions will be reversed very quickly.

2) The crisis is likely to hasten the presence of effective domestic and foreign competition.

This will put profit margins of the existing companies under pressure. Combined with the

need for provisions for losses, including those relating to foreign exchange, the above has

the potential to reduce the buoyancy of the most important source of tax revenue, i.e. tax

on company profits.

3) The crisis has exposed oversupply situation in the property and real estate sectors. This is

likely to put pressure on the land values. This, in turn could have an impact on the

revenue from lease of land. The property developers have been lobbying the government

to support the property market .The Singapore government’s decision to suspend any

further lease of land for construction of private property is designed to help stabilize the

property market. As according to the informed estimates, property related loans are

equivalent to about 50 percent of GDP, and as government is the largest landlord in

Singapore, and as most of the population has a significant proportion of the wealth tied in

property, temptation to do so as well as the political costs of not doing so are high.

4) The crisis has underscored the need to expand and institutionalise social safety nets. The

government has recognised this but because of its ideology and its need for the

monocentric power structure, it is unwilling to take measures implying a long term

budgetary commitment let alone institute programs which imply entitlement. Given the

magnitude of the retirement needs of economically mature, affluent economy and rapidly

aging population, such ad-hoc measures will prove to be insufficient (Asher, 1998).

In conclusion, Singapore’s revenue system, while unconventional, has been

continuously adjusted to the requirements of its growth strategy, and social engineering

objectives. In addition, tax administration and compliance issues, and political planning and

management have received considerable attention of the policymakers.

Globalization, maturing of Singapore’s economy, rapid aging of the population, and

the current economic crisis in South east Asia are bringing new challenges requiring

adjustments in Singapore’s revenue system.

While Singapore has so far been quite innovative in generating newer revenue sources

(e.g. foreign workers levy, and the GST), and using existing taxes more intensively (e.g.

leasing of land, motor vehicle taxes, and a variety of user charges and cost recovery fees ), its

18

future options in this regard remain very limited . Its role as a financial centre rules out

recourse to the tax on currency transactions, so called Tobin tax, to general revenue21. As

expenditure needs continue to increase, the government budget constraint is likely to become

more stringent.

Thus, the proposition that tax reform is a process or a journey and not a destination has

been borne out by Singapore’s experience.

19

REFERENCES

Adema, W. 1997. “What Do Countries Really spend on social policies ? : A Comparative note”, OECD Economic Studies, 28, pp. 153-167.

Asher, M.G. 1998. “The future of Retirement Protection in Southeast Asia,” International Social Security Review, 51(1), pp. 3-30.

Asher, M.G. 1993. “The Proposed Goods and Services Tax (GST): Implications for

Singapore’s Fiscal System”, APTIRC Bulletin, 11(6), pp. 212-220. Asher, M.G. 1989. “Fiscal System and Practices” in M.G Asher (ed.), Fiscal Systems and

Practices in ASEAN; Trends,Impact and Evaluation, Singapore : Institute of Southeast Asian Studies, pp. 131-183.

Asher, M.G. and Heij, G.1999. “South East Asia’s Economic crisis : Implications for Tax

systems and Reform Strategies”, Bulletin for International Fiscal Documentation, Forthcoming.

Asher, M.G. and Rajan R. 1998. “Globalisation and Implications for Tax structures with

particular reference to SouthEast Asia,” Unpublished. Bird, G. and Rajan, R. 1998. “Time to reconsider Tobin Tax Proposal?”, unpublished. Chay, Y.M. 1999. “GST Laws need to be more Business friendly”, Business Times,

Singapore, January 5. Chia, N.C. 1998. “The Significance of Motor Vehicle Taxes in the Revenue System”, Asia-

Pacific Tax Bulletin, July, pp. 275-289. Dolven, B. 1998. “Let’s all be creative” Far Eastern Economic Review, December 24, pp. 10-

12. Inland Revenue Authority of Singapore, 1997. Annual Report 1996, Singapore. Jenkins, G.P. and Khadka,R. 1998. “Value Added Tax Policy and implementation in

Singapore”, Harvard Law School International Tax Programme, Working Paper 1001 Ong, K.H. 1996. “Structure and Administration of IRAs”, paper presented for the Tax Policy

and Administration course, organized by the Inland Revenue Authority of Singapore, March 11-26,1996.

Owens, J. 1997. “The Tax Man Cometh to cyberspace”, Tax Notes International, June,

pp.1833-1852. Phang, S.Y. 1997. “Government Intervention and Performance of the Housing sector in

Singapore”, A paper presented at the International Seminar on Housing Policy, organized by the Korean Association for Housing Policy studies, Seoul, November 21.

20

Phang, S.Y. and Asher, M.G. 1997. “Recent Developments in Singapore Motor Vehicle Policies”, Journal of Transport Economics and Policy, 31,2, pp. 212-220.

Rao, V.V.B. 1996, “Income Inequality in Singapore : Facts and Policies” in C.Y Lim (ed.)

Economic Policy Management in Singapore, Singapore: Addison Wesley Publishing pp. 383-396.

Republic of Singapore, Department of Statistics, Yearbook of Statistics, Various Years. Republic of Singapore, Ministry of Finance, The Budget, Various Years. Tan, T.Y. 1996. “Corporate Income Tax in Singapore: Issues and Future Directions” in M.G.

Asher and A. Tyabji (eds.), Fiscal System of Singapore: Trends, Issues and Future Directions, Singapore: Centre for Advanced Studies, National University of Singapore, pp. 196-212.

Williams, D. 1997. “Trends in Social Taxation”, Bulletin for International Fiscal

Documentation, June, pp. 254-264. The World Bank. 1998. World Development Report 1998, Washington D.C: The World Bank.

21

ENDNOTES

1 I would like to thank Hiromitsu Ishi,Gitte Heij, Haruhiko Kuroda,Eiji Tajika, and Shinji Asanuma for useful comments on earlier drafts of the paper. I would also like to thank Rahul Sen and Usha Sankari for research assistance. The usual caveat applies. 2 A Revised version of the Paper presented at the International Symposium on Asian Tax Reform: Issues and Results, Organised by the Asian Tax and Public Policy Program of Hitotsubashi Univeristy, Kunitachi, Tokyo, December 4-5,1998. 3 Associate Professor, Department of Economics and Statistics National University of Singapore 10 Kent Ridge Crescent, Singapore 119260 E-mail: [email protected]: (65) 775-2646 4 Its resident population i.e citizens plus Permanent Residents was however 3.10 million or 82.9 percent of the total population (Table A1). Such large foreign population is one of the indicators of the globalised nature of the Singapore’s economy. It also implies that Singapore’s tax base is larger than its resident population alone may suggest. Indeed as discussed elsewhere in the paper, Singapore’s foreign worker levies, whose incidence is likely to be on workers and therefore the levies act as a form of wage income tax, are a lucrative source of tax revenue for the government. If the 7.2 million visitors in 1997 are also considered, then the potential tax base would be even larger. 5 Thus, in April 1998, daily average foreign exchange trading turnover was the fourth highest in the world, at $US139 billion for Singapore, only marginally lower than the turnover of $US148.6 billion in Tokyo (Bird and Rajan, 1998, Table 1). 6 Foreign component of net investment commitments in the manufacturing sector has routinely accounted for around four-fifths of the total. (Republic of Singapore, Department of Statistics, various years). Presence of MNCs in services area, particularly in finance and business services is also quite significant. 7 The number of Statutory Boards exceeds 100, though only about a dozen or so are of major significance. The number of GLCs (including their subsidiaries) exceeds 600. The Statutory Boards and the GLCs account for well over half of Singapore’s stockmarket capitalization. No significant change is envisaged in their denomination of the domestic economy. 8 While Singapore does not publish detailed composition of national income into factor shares, the indications are that the share of wages in national income is only 43 per cent, implying that the share of capital is 57 percent. In contrast, in the U.S, wage share is typically around two-thirds. 9 Greater contestability for markets, mainly due to the technological change in such sectors as telecommunications, is however bringing about price reductions in telecommunications and other affected services in Singapore. 10 The term international competitiveness in the Singapore context implies ability to attract and retain desired level and types of investments. Monitoring cost of doing business is thus an important preoccupation of the policy makers. As Singapore attempts to move up the value chain, this is also being extended to attracting and retaining those with the desired professional, technical, and managerial skills. 11 Even this is understated, as the reported investment income in the budget does not include all budgetary accounts. Thus, if the above adjustment were made, the total revenue for 1997-98, would be 43.4 percent of GDP instead of 38.5 percent. This would also increase the implicit rate of return on total balances from a rather mediocre 1.41 percent to a more respectable 4.9 percent. 12 Often the effective rate reduction, particularly in income and property taxes, has been accomplished by providing one-off rebates rather than formal reductions in rates. 13 The 1986 Economic committee Report, did recommend a more neutral broad-based tax system with fiscal incentives assigned only a minor role, but this has not been followed. This committee was set up to cope with the short-lived 1985 recession.

22

14 Real GDP growth was 7.8 percent in 1997, and 1.5 percent in 1998. The official growth forecast for 1999 is for a range of 1 to-1 percent. For the January to November 1998 period, the overall revenue from taxes collected by the Inland Revenue Authority of Singapore (IRAS) declined by 7.2 percent as compared to the corresponding period for 1997, with only income tax increasing by 2.2 percent (The Straits Times, Singapore, January 14, 1999). 15 This is illustrated by the fact that in FY 1996, Statutory Boards contributed $1,877 million but in FY 1997, this was reduced to only $700 million. Republic of Singapore, The Budget for the FY 1998-99, p.53. 16 The government however has completely removed expatriates from the purview of the CPF from September 1998 . Also, other pension arrangements such as gratuities and annuities are taxed in Singapore, and so are pension arrangements for the exempted expatriates . Thus, the tax exemption is reserved only for the CPF. 17 During 1998 alone, the EDB committed $700 million as co-investment with the MNCs ; while for 1999, it aims to take upto 30 percent equity stake in promising local enterprises to help minimize their debt (The Straits Times, Singapore, January 19, 1999). 18 Nevertheless, it may be useful to examine the extent to which Singapore’s fiscal incentives whose value is based on the amount of fixed capital investment, have impacted the import prices of capital goods . To the extent these prices are increased, the benefits of fiscal incentives accrue to the capital goods producers. As nearly all of the capital goods are imported, this issue is of particular relevance for Singapore. I am indebted to Chang-Tai Hsieh for this point. 19 The details may be found in Chia (1998). 20 Whenever an exempted business sells its products to any taxed business under a GST using the credit –invoice method, which is the method used in Singapore, cascading would result in much the same way a turnover tax does. This in turn increases the GST tax base. 21 For an assessment of the Tobin tax, see Bird and Rajan, 1998.

23