taxation of charitable and religious trust of... · 2017-09-08 · trust for charitable purposes...

TRANSCRIPT

TAXATION OF CHARITABLE AND RELIGIOUS TRUST

C.A. P.C. MALOO

Welcome

06th November, 2015 CA P.C. MALOO 2

CHAPTER 1 – PRELIMINARY

Definition of “Total Income” : Section 2(45)

“total income” means the total amount of income referred to in section 5, computed in the manner laid down in this Act;

CHAPTER 2 – BASIS OF CHARGE

Scope of total income : Section 5(1)

Subject to the provisions of this Act the total income of any previous year of a person who is a resident includes all income from whatever source derived which-

(a) is received or is deemed to be received in India in such year by or on behalf of such person; or

(b) accrues or arises or is deemed to accrue or arise to him in India during such year; or

(c) accrues or arises to him outside India during such year.

CHAPTER IV – COMPUTATION OF TOTAL INCOME

Heads of income : Section 14

Save as otherwise provided by this Act, all income shall, for the purposes of charge of income-tax and computation of total income, be classified under the following heads of income :- 06th November, 2015 CA P.C. MALOO 3

CHAPTER – III INCOMES WHICH DO NOT FORM PART OF THE TOTAL INCOME

Income from property held for charitable or religious purposes. SECTION 11 : (1) Subject to the provisions of sections 60 to 63, the following

income shall not be included in the total income of the previous year of the person in receipt of the income –

(a) income derived from property held under trust wholly for charitable or religious purposes, to the extent to which such income is applied to such purposes in India, and, where any such income is accumulated or set apart for application to such purposes in India, to the extent to which the income so accumulated or set apart is not in excess of 15% of the income from such property. (b) ………………………….

06th November, 2015 CA P.C. MALOO 4

SCOPE OF WORD “INCOME”

In case of CIT Vs Rao Bahadur Calavala Cunnan Chetty Charities 135 ITR 485 (Mad) held that taking in to account the purpose for which the conditions of section 11(1)(a) are imposed, it would be clear that one has to consider the income as arrived at in the context of what is available in the hands of the assesse, subject to of course to any adjustment for expenses extraneous to the trust. The expression “income” has to be understood in the popular or general sense and not in the sense in which the income is arrived at for purposes of assessment to tax by the applications of some artificial provisions either giving or denying deductions.

The Court further held that there is no need or scope to arrive at the income of a charitable trust in the manner contemplated by the Income-tax Act, i.e. section 14.

This view has been re-iterated by Madras HC, AP HC, Kerala HC, Gujrat HC and Calcutta HC.

06th November, 2015 CA P.C. MALOO 5

Charitable Trust having agricultural income and non-agricultural income :

• CIT Vs Panchayati Akhara Nirmal 190 ITR 121 (All) : Section 10 exclude agricultural income whereas section 11(1) exclude income derived from property held under trust for charitable or religious purposes to the extent such income is applied or accumulated. Where agricultural and non agricultural properties are held under trust for charitable purposes and no separate accounts are maintained, the A.O. has no option but to allocate the amount spent on charitable religious purposes between agricultural and non agricultural income in an appropriate ratio, before applying the rule laid down in section 11(1)(a) of the said Act.

• However, the Madhya Pradesh High Court, in CIT Vs Nabinanadan Digambar Jain 257 ITR 91 (MP), did not agree with this view, and held that agricultural income, being exempt under section 10, would not form part of the total income of the trust.

06th November, 2015 CA P.C. MALOO 6

• Loss on sale of Investment : Whether allowable

In Hindusthan Welfare Trust Vs Director of Income-tax (Exemption) 201 ITR 564 (Cal), the Calcutta High Court held that the loss on sale of investment was not allowable in computing the real income of a charitable trust in a commercial manner.

• Capital Expenditure : Whether application of income

To avail benefit of exemption from tax u/s 11 of the Act, it is not necessary that the application of income should be revenue in nature. Where the dominant object of the trust was to establish a Dharamshala, the capital expenditure for construction of Dharamshala was an application of income towards the charitable purpose of the trust. (Satya Vijay Patel Hindu Dharamshala Trust Vs CIT 86 ITR 683 (Guj)).

Supreme Court has also held that purchasing of a building to be used as a hospital was nothing but application of income for charitable purpose u/s 11(1)(a) of the Act S.R.M.M. C.T.M. Thiruppani Trust Vs CIT 230 ITR 636 (SC).

06th November, 2015 CA P.C. MALOO 7

Repayment of Loan or Debt – Treated as Application

CBDT circular no-100 dated 24.01.1973:

Repayment of loan originally taken by a charitable or religious trust to fulfill one of its objects will amount to an application of income.

Where the object of the trust is advancement of education and it grants scholarship loan to students for higher studies in fulfillment of the objectives of the trust, even if interest bearing will amount to application of income for charitable purposes.

Repayment of debt incurred by the trust for construction of the building, which in turn would augment its income, should be treated as application of income of the trust for charitable purposes. CIT Vs Janmbhumi Press Trust 242 ITR 457 (Kar) Similar view was taken by Madras and Kerala HC.

However when the loan is returned to the trust it will be treated as income of the that year . CIT Vs Cutchi Memon Union 155 ITR 51, 54 (Kar).

06th November, 2015 CA P.C. MALOO 8

Payment of Taxes : Whether Application • Payment of Income Tax and Wealth is an incident of the

income or the accumulation of the income of the trust and as such must be deducted from the income of the trust determined on commercial principal. CIT Vs Trustees of HEH The Nijams Supplemental Religious Endoment Trust 127 ITR 378 (AP).

• This view was also confirmed by Gujrat High Court 162 ITR 612.

• TDS out of income received: TDS u/s 194 is not available to the trust for application to charitable purposes and therefore not an income. Though section 198 provides that the amount deducted by way income shall be deemed to be income, it can neither be spent nor accumulated for charitable purposes. CIT Vs Jayashree Charity Trust 159 ITR 280 (Cal)

06th November, 2015 CA P.C. MALOO 9

Refund of Taxes : Whether Income Refund of income tax received by a charitable institution

can not be treated as income derived from property held under trust. CIT Vs Humdard Dawakhana (Wakf) 249 ITR 601 (Del)

Interest Accrued on FDR : whether income The preposition of Calcutta High Court CIT Vs Jayashree

Charity Trust 159 ITR 280 (Cal) may be applied for interest accrued on FDRs where the income has not been actually received and thus not available either for application or for accumulation and therefore such interest accrued on FDRs can not be treated as income.

06th November, 2015 CA P.C. MALOO 10

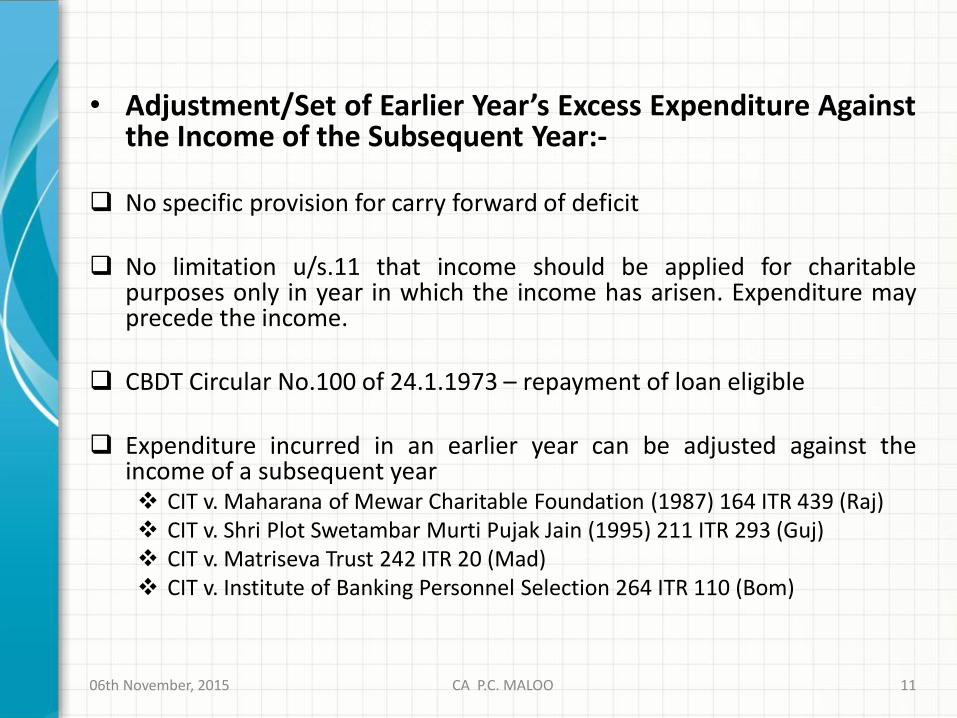

• Adjustment/Set of Earlier Year’s Excess Expenditure Against the Income of the Subsequent Year:-

No specific provision for carry forward of deficit No limitation u/s.11 that income should be applied for charitable

purposes only in year in which the income has arisen. Expenditure may precede the income.

CBDT Circular No.100 of 24.1.1973 – repayment of loan eligible Expenditure incurred in an earlier year can be adjusted against the

income of a subsequent year CIT v. Maharana of Mewar Charitable Foundation (1987) 164 ITR 439 (Raj) CIT v. Shri Plot Swetambar Murti Pujak Jain (1995) 211 ITR 293 (Guj) CIT v. Matriseva Trust 242 ITR 20 (Mad) CIT v. Institute of Banking Personnel Selection 264 ITR 110 (Bom)

06th November, 2015 CA P.C. MALOO 11

Capital Asset claimed as application of income :

Whether claim of Depreciation is double deduction

• Claim of Depreciation is not a case of double benefit :

CIT Vs Sheth Manilal Ranchoddas Vishram Bhawan Trust 198 ITR 598 (Guj)

CIT Vs Society of the Sisters of St. Anne 146 ITR 28 (Kar),

CIT Vs Raipur Pallottine Society 180 ITR 579(MP).

CIT Vs Market Committee Pipli 330 ITR 16 (P&H)

Framjee Cawasjee Institute 109 CTR 463 (Bom)

• Above decisions are pre insertion of section 11(6) by Finance Act 2014.

06th November, 2015 CA P.C. MALOO 12

Allowability of depreciation after insertion of section 11(6) by Finance Act 2014. (w.e.f. A.Y. 2015-16)

• Where any asset has been claimed as application of income under this section in same year or in any previous year, depreciation thereon shall not be allowed as deduction.

06th November, 2015 CA P.C. MALOO 13

Voluntary Contributions to Corpus – Whether Income? Section 11(1)(d) : Income in the form of voluntary contribution made with a

specific direction that they shall form part of the corpus of the trust or institution, shall not be included in the total income.

Term “Corpus” not defined in the Act

Corpus in the context of Income Tax Act means intention of the donor to give his money to a trust for carrying on a particular activity. DIT Vs Ramkrishna Sewa Ashram (2012) 205 Taxman 26 (Karnataka)

Donation made by the donor in order to establish an engineering an management college in the name of his grand father, was a corpus donation Addl. CIT Vs Chaudhary Raghuveer Singh Educational and Charitable Trust 55 SOT 211 (Del).

06th November, 2015 CA P.C. MALOO 14

Where amount received by assesse society towards different specific fund i.e. for award, IJA fund, WSJA fund and life membership fees. All these funds were for specific purposes and cannot be treated as voluntary contribution in the nature of income. Indian Society of Anaesthesiologists Vs ITO 32 ITR (Trib) 152 (Chennai).

Can corpus donations be received through offeratory boxes?

o Not a corpus donation

Prabodhan Prakashan v. ADIT 50 ITD 135 (Bom)

Shri Digambar Jain Naya Mandir v. ADIT 70 ITD 121 (Cal)

o Is a corpus donation

Shree Mahadevi Tirath Sharda Ma Seva Sangh v. ITO 133 TTJ (UO) 157 (Chd)

06th November, 2015 CA P.C. MALOO 15

Can amounts received from parents of students at time of/after admission be regarded as voluntary contributions to corpus?

Even if any donation is received in connection with admission of a student, over and above the fee prescribed, the assessee would be eligible for exemption of its income under S.10(23C)/S.11 of the Act.

DCIT V/s. Vellore Institute of Technology(12 Taxman.com.272(Chennai)

ACIT V/s. Balaji Educational & Charitable Public Trust (2011)15 Taxmann.com 53(Mad)

Can corpus donations be applied on objects of the trust? Would it amount to application of income?

If corpus donation are excluded from total income, expenditure out of which would not be application of income.

06th November, 2015 CA P.C. MALOO 16

ACCUMULATION OF INCOME 15% • In order to claim exemption u/s 11(1)(a), the trust has to apply 85% of

such income for the purpose of trust and the balance 15% of income can be accumulated.

• If the trust could not spent 85% of the income for the reason that whole are part of the income has not been received or for any other reason, in such cases explanation (2) of section 11(1) of the Act provides that no tax will be levied on the unspent portion in that year if certain condition for satisfied viz- The trust sends an intimation to the A.O., before the expiry of the time allowed under subsection (1) of section 139, exercising its option:- to apply the unspent portion of the said 85% of the income in the

succeeding accounting year; The short fall to the extent to which it is attributable to the non-receipt of

income is applied to such purposes during the previous year in which the income is actually received or during the previous year immediately following thereafter.

The short fall for any other reasons whatever, is applied to such purposes

during the previous year immediately following the previous year in which income was derived.

06th November, 2015 CA P.C. MALOO 17

ACCUMULATION OF INCOME BEYOND 15% • Section 11(2) : Where 85% of the income derived from

property held under trust could not be applied, the trust has option to accumulate or set apart it for application in future. Such income so accumulated or set apart shall not be included in the total income of the previous year provided following condition are fulfilled:-

A notice in writing in Form no 10 to be given to A.O. before

expiry of time allowed u/s 139(1) for furnishing return of income. In notice, the purpose for which it is accumulated is required to be mentioned which shall in no case exceed five years.

The money so accumulated or set apart is invested in form or mode specified in section 11(5).

Copy of the resolution past by the trustee has to be filed along with the notice.

06th November, 2015 CA P.C. MALOO 18

ACCUMULATION OF INCOME BEYOND 15% • Director of Income Tax Exemption Vs Trustees of Singhania Charitable

Trust 139 ITR 199 (Cal) : where a charitable trust give a notice for accumulation of income u/s 11(2) of the Act the trust must indicate some specific purpose or purposes. It can not list all its object as purposes.

• The Delhi High Court in series of decisions held that section 11(2) does

not prohibit plurality of purposes (Bharat Kalyan Pratisthan Vs DIT(E) 299 ITR 406 (Del).

• As per provision of section 13(9), inserted by Finance Act 2015 w.e.f. 01.04.2016, if the notice as required under section 11(2)(a) is not furnished to A.O. on or before the due date specified u/s 139(1) or the return of income for the previous year is not furnished on or before the due date specified u/s 139(1), section 11(2) shall not operate. CIT Vs Anjuman Moinia Fakharia 208 ITR 568 (Raj) : An application

for accumulation file u/s 11(2) beyond the time limit would not disentitle the assesse to claim exemption from tax. Same view was taken by Punjab & Haryana High Court and Bombay High Court.

06th November, 2015 CA P.C. MALOO 19

TIME LIMIT FOR MAKING INVESTMENT IN MODE PRESCRIBED U/S 11(5) • Not Prescribed the time for making investment in the mode

prescribed u/s 11(5). • However para-2 of Form no- 10 says that such investment are to

be made before the expiry of 6 month from the end of the previous year.

• M.C.T. Muthiah Chettiar Family Trust Vs 4th ITO 86 ITR 282(Mad) :

Declared para-2 of the said form as ultra vires holding that the rule making authority had exceeded its limit in including in the form the time limit for making investment.

• Similar view has been taken by Jammu & Kashmir HC, Kerala HC

and Andhra Pradesh HC.

06th November, 2015 CA P.C. MALOO 20

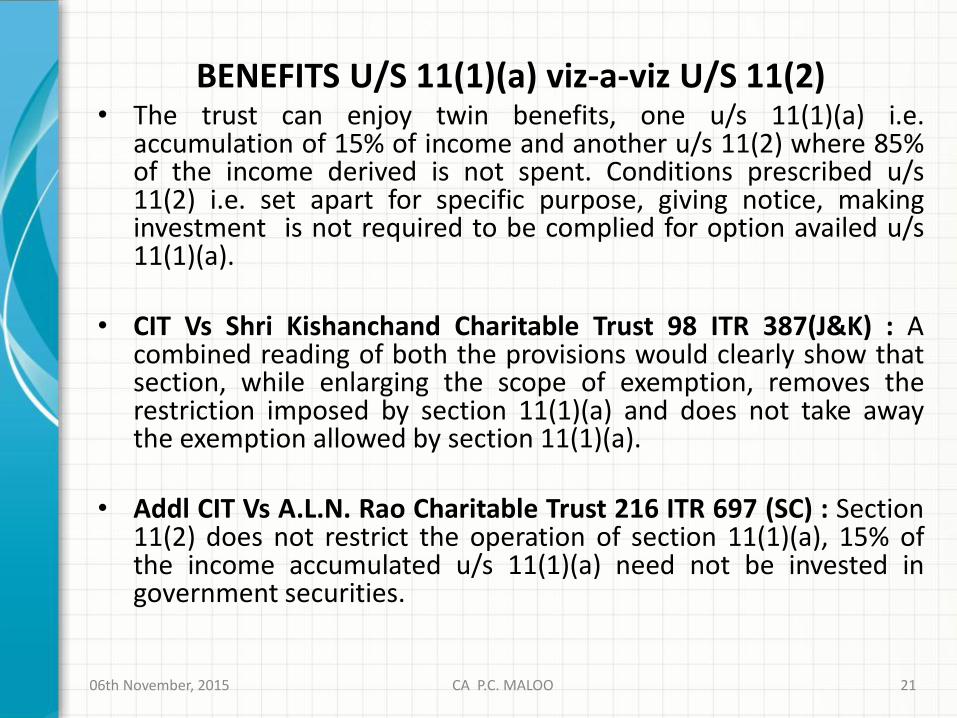

BENEFITS U/S 11(1)(a) viz-a-viz U/S 11(2) • The trust can enjoy twin benefits, one u/s 11(1)(a) i.e.

accumulation of 15% of income and another u/s 11(2) where 85% of the income derived is not spent. Conditions prescribed u/s 11(2) i.e. set apart for specific purpose, giving notice, making investment is not required to be complied for option availed u/s 11(1)(a).

• CIT Vs Shri Kishanchand Charitable Trust 98 ITR 387(J&K) : A

combined reading of both the provisions would clearly show that section, while enlarging the scope of exemption, removes the restriction imposed by section 11(1)(a) and does not take away the exemption allowed by section 11(1)(a).

• Addl CIT Vs A.L.N. Rao Charitable Trust 216 ITR 697 (SC) : Section 11(2) does not restrict the operation of section 11(1)(a), 15% of the income accumulated u/s 11(1)(a) need not be invested in government securities.

06th November, 2015 CA P.C. MALOO 21

Capital Gains SECTION 11(1A) : Net sale consideration is to be utilized for

acquiring another capital asset to be hold then the capital gain arising shall be deemed to be applied.

If fully utilized no income by way of capital gain is chargeable If partly utilized to the extent of amount utilized is not chargeable Capital gain not to be computed as per section 48 There is no requirement to acquire any specific asset No time limit for reinvestment – investment to be seen at end of

year Even 15 day fixed deposit would qualify

CBDT Instruction No.883 dated 25.9.1975 – 6 months FDR Imposition of minimum period of six month by CBDT is not a valid

condition CIT Vs Hindusthan Welfare Trust 206 ITR 138(Cal). 60days FDR was allowed

ADIT(E) v. Murugappa Chettiar Trust 303 ITR 360 (Mad) – even current account is deposit with scheduled bank - qualifies

06th November, 2015 CA P.C. MALOO 22

APPLICABILITY OF SECITON 50C

• Section 50C is applicable to every assesse where the sale consideration is less than the value assessed or assessable by SVA. It recognizes an artificial income.

• This section provides that for the purpose of section 48 the value adopted or assessed by SVA shall be the full value of consideration received or acquiring as a result of transfer.

• After having analyzed the provision section 11, a question arises whether provision of section 50C can be pressed into service in case of trust. Since section 11 do not recognizes any artificial income as income derived from property held under trust, in my opinion provision of section 50C is not applicable.

06th November, 2015 CA P.C. MALOO 23

APPLICABILITY OF SECTION 115JB IN CASE OF A COMPANY REGISTERED U/S 25 OF COMPANIES ACT.

• The provision of section 115JB is applicable to non-profit making companies and the book profit for the purpose of MAT, is to be computed according to the provision of explanation 1 to section 115JB(2).

• The book profit of the company means the net profit as shown in the profit & loss account for relevant previous year as reduced by the amount of income to which any of the provision of section 11 or section 12 apply, if any such amount is credited to the profit & loss account.

06th November, 2015 CA P.C. MALOO 24

APPLICABILITY OF SECTION 44AB OF INCOME TAX ACT

• Section 44AB becomes operative where profits and gains of business or profession are computed as a part of total income.

• In other words, it has no applicability where the assesse is not involved in or has no income from profit and gains from business or profession.

• Where the income of the assesse was exempted u/s 10(20) and assesse has no income which would fall under heading profits and gains of business or profession, it could not be said that the provisions of section 44AB were applicable. (CIT Vs Market Committee Sirsa 210 Taxman 20 (Punj. & Har)

06th November, 2015 CA P.C. MALOO 25

Anonymous donations to be taxed in certain cases Section 115BBC

• Not applicable to religious trust • Applicable to educational, hospital or other charitable

institution • Income Tax to be calculated @30% • Exception : 5% of total donation received or 1 lac which

ever is higher will not attract tax. Excess there of is liable for tax.

• Anonymous donations : where identity indicating name & address of person is not maintained. Confirmation letter not required to be filed. Only record of

name & address is to be maintained. Hans Raj Smarak Society Vs Asst. DIT 133 ITD 530 (Del)

06th November, 2015 CA P.C. MALOO 26

REGISTRATION OF TRUST • To make an application in prescribed form 10A to Principal

CIT or CIT (Section 12A(1)(aa)) • Registration is to be granted or refused with in six month

form the month is which application was made (Section 12AA(2))

• If not granted or refused with in six month it will be deemed to be registered. Shri Hari Paramnath Dham Trust Vs CIT 299 ITR (AT) 161 (Del) Promotion of Education Adventure Sports Vs CIT 216 CTR 167

(All)

• Once a trust is registered u/s 12A, it is a fait accompli, and the A.O. can not there after make a further prob in to the object of the trust. ACIT Vs Surat City Gymkhana 300 ITR 214 (SC)

06th November, 2015 CA P.C. MALOO 27

REGISTRATION OF TRUST • On registration exemption under section 11 & 12 will be

effective for the A.Y. following the F.Y. in which application made. CIT has no power to grant registration retrospectively. (Section 12A(2))

• Exemption u/s 11 & 12 shall also be available to preceding assessment years in respect of which assessment preceding are pending before A.O. and objects are same (Effective from 1.10.14 first proviso to section 12A(2))

• No action u/s 147 to be initiated for preceding assessment years, only for non-registration of trust. (Effective from 1.10.14 second proviso to section 12A(2))

• Registration can be canceled if the activities are not genuine or not carried in accordance with object. (Section 12AA(3))

06th November, 2015 CA P.C. MALOO 28

Following trust not to be registered Private Religious Trust : which do no ensure for the

benefit of the public (Section 13 (1)(a))

Communal Trust : Created after 01.04.1962, for the benefit of any particular religious community or caste. (section 13(1)(b))

Trust for the benefit of schedule caste, backward class, schedule tribe or women and children shall not be deemed to communal trust. (Expl 2 to sec 13)

Section 13(1)(b) applies to trust which are purely for charitable purposes. Trust for charitable or religious purposes are not covered by section 13(1)(b) CIT Vs Barkate Saifiyah Society 213 ITR 492 (Guj)

06th November, 2015 CA P.C. MALOO 29

Position on Loss of Exemption

Direct Expenses incurred for Earning Income would be deductible from the Gross Income

Establishment Expenses incurred would also be deductible

Income would be taxable at slab rates of tax (for trusts & societies), but at 30% for companies

06th November, 2015 CA P.C. MALOO 30

CHARITABLE PURPOSE – Sec. 2(15)

• 6 limbs

relief of the poor

Education

Medical relief

Preservation of environment (including watersheds, forests & wildlife)

Preservation of monuments/places/objects of artistic/historic interest

Advancement of any other object of general utility

06th November, 2015 CA P.C. MALOO 31

• Advancement of any other object of general public utility

Amendment w.e.f. AY 2009-10

Not charitable purpose if it involves carrying on of :

Any activity in nature of trade, commerce or business, or

Any activity of rendering any service in relation to trade, commerce or business for a cess/fee/any other consideration, irrespective of nature of use/ application/retention of income from such activity

Exception – if aggregate value of receipts from such activities is Rs.10 lakh (Rs.25 lakh wef AY 2012-13) or less in the previous year

Exception Amended w.e.f. 1.04.2016

Such activity is under taken in course of actual carrying out of such advancement of any other object of general public utility.

Aggregate receipt from such activity do not exceed 25% of total receipt.

06th November, 2015 CA P.C. MALOO 32

CHARITABLE PURPOSE – Sec. 2(15)

Gaushalas selling milk and milk products Inmates residing in ashram preaching Gandhian

philosophy, carrying on agriculture, running gaushala, publishing & selling books in Ashram, having conferences and having paid accommodation and boarding for visitors Sevagram Ashram Pratishthan v. CIT 129 TTJ (Nag) 506 - Object

of the amended proviso to s. 2(15) is to create a barrier for those assessees who are engaged in business activities in the garb of charitable purpose and it is not meant for the assessees who are really engaged in charitable purpose

Hiring of auditorium/halls/wadis – mere letting not business DIT(E) v. Sahu Jain Trust 2011-TIOL-204-HC-KOL-IT

06th November, 2015 CA P.C. MALOO 33

Printing & Publication of Books, purchase & sale of cassettes and VCDs Educational activities – Prasanna Trust v. DIT(E) 36 SOT 135 (Bang)

Investment of Surplus funds not business activity ITO v. Jesuit Conference of India 47 SOT 29 (Del)

Running of coaching classes – whether business DIT(E) v. Institute of Chartered Accountants of India 202 Taxman 138

(Del) : it is educational activity not business

Club having sports activities, restaurant and letting grounds/halls? CIT v. Delhi Golf Club Ltd. 2011-TIOL-310-HC-DEL-IT – allowing golf

course to be used by casual members or non-members on higher fee cannot be construed to be carrying on of commercial activities/business

Conduct of Research Projects ICAI Accounting Research Foundation v. DGIT (E) 321 ITR 73 (Del) –

imparting, spreading and promoting knowledge, learning, education, etc. in fields relating to profession of accountancy – services of carrying out research projects provided to various Govt. bodies – not business/commercial activity or in relation to trade, commerce or business

06th November, 2015 CA P.C. MALOO 34

Section 80G Approval

Earlier approval granted for 3 years at a time

Amendment to s.80G(5)(vi) by Finance (No.2) Act 2009 w.e.f.1.10.2009 – the institution or fund is for the time being approved by the Commissioner in accordance with the rules made in this behalf ; and Provided that any approval shall have effect for such assessment year or years, not exceeding five assessment years, as may be specified in the approval.

Explanatory Memorandum to Finance (No.2) Bill 2009 Existing approvals expiring on or after 1st October, 2009 shall be deemed to have been extended in perpetuity unless specifically withdrawn

CBDT Cir No 7 dated 27.10.2010

It appears that some doubts still prevail about the period of validity of approval under section 80G subsequent to October 1, 2009, especially in view of the fact that no corresponding change has been made in rule 11A(4). To remove any doubts in this regard, it is reiterated that any approval under section 80G(5) on or after October 1, 2009 would be a one time approval which would be valid till it is withdrawn.

Babu Hargovind Dayal Trust v. ITAT 199 Taxman 138 (All) 06th November, 2015 CA P.C. MALOO 35

Suggestion Regarding Drafting of Trust Deed

• To provide proper safeguard, it is suggested that the instrument of trust or institution created or established hereafter should contain, inter alia, the following clauses :

Nothing contained in this deed shall be deemed to authorize the trustees to do any act which may in any way be construed as violative or contrary to the provisions of sections 2(15), 10(23B), 10(23C), 11, 12, 12A, 12AA, 13 and/or 80G of the Income Tax Act 1961 and/or any statutory modifications thereof an all activities of the trust shall be carried out with a view to benefit the public at large, without any profit motive and in accordance with the provisions of the Income Tax Act, 1961 or any statutory modification thereof.

The Trust is hereby expressly declared to be a public charitable trust and all the provisions of this deed are to be constituted accordingly

• It is also advisable to have a clause stating that the trust created is irrevocable, so that the provisions of sections 61 or 62 of the Income Tax Act are not attracted

06th November, 2015 CA P.C. MALOO 36

QUESTIONS?

06th November, 2015 CA P.C. MALOO 37

THANKS

06th November, 2015 CA P.C. MALOO 38